Central Bank of India: The Swadeshi Bank That Survived A Century

I. Introduction & Episode Preview

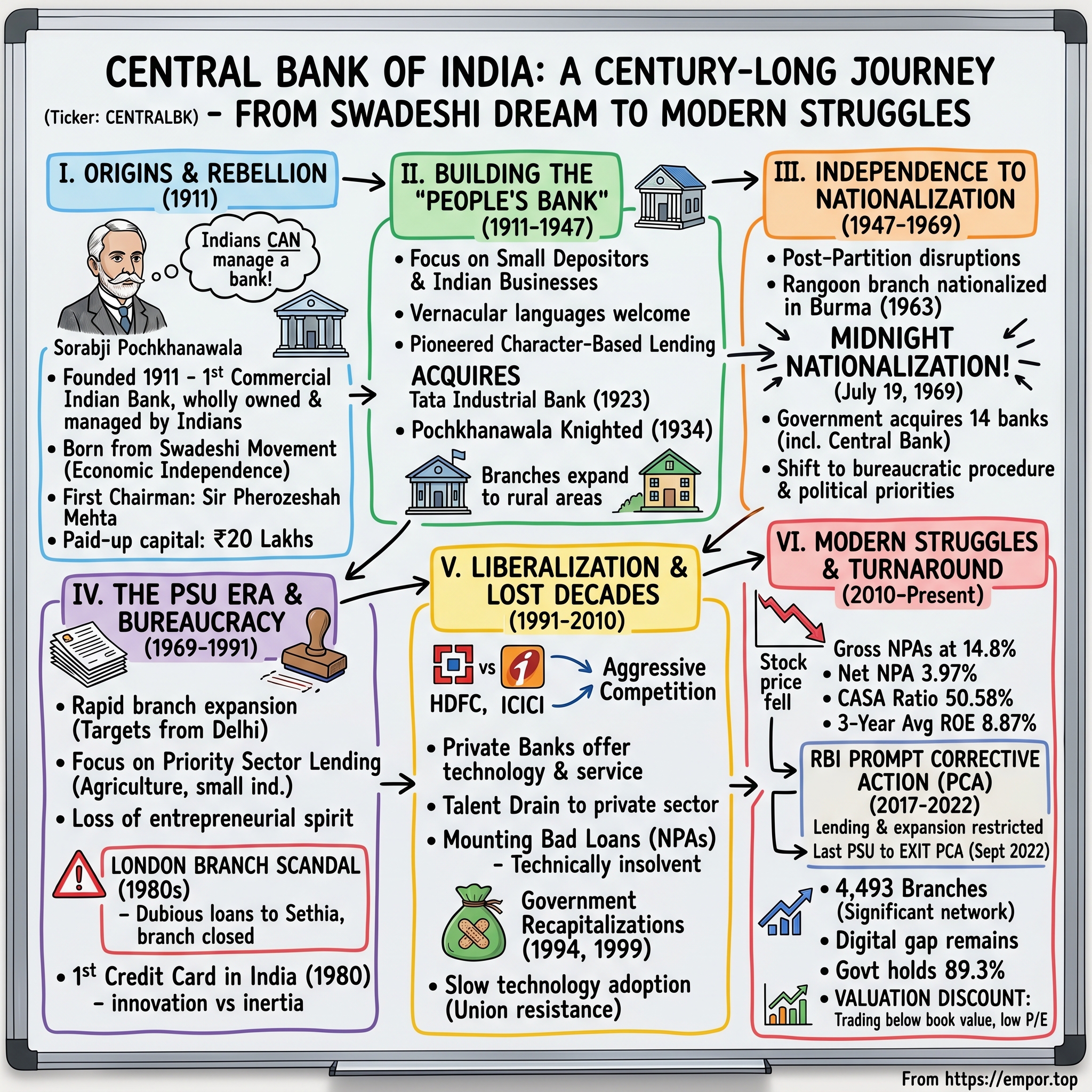

The rain hammered against the windows of Central Bank of India's Fort headquarters in Mumbai, the same building where, over a century ago, a young Parsi clerk named Sorabji Pochkhanawala had dreamed of creating something impossible—an Indian bank run by Indians, for Indians. Today, that dream trades at ₹36.2 per share, commanding a market cap of ₹32,775 crores with a P/E ratio of just 7.77. The numbers tell a story of survival, but not triumph.

Central Bank of India stands as a paradox in Indian finance. Founded in 1911 as the country's first commercial bank wholly owned and managed by Indians, it was born from the fire of the Swadeshi movement—a symbol of economic independence before political independence was even imaginable. The bank that once represented Indian entrepreneurial defiance against colonial banking monopolies now struggles to find relevance in an era dominated by HDFC, ICICI, and a new generation of fintech disruptors.

How does a 113-year-old institution, one that predates the Reserve Bank of India by 24 years, find itself trading at such a steep discount to book value? How did the pride of the Swadeshi movement become just another underperforming public sector undertaking? The answer lies not in a single decision or moment, but in a century-long journey through colonialism, independence, nationalization, and liberalization—each era leaving its mark like geological strata on the bank's culture and capabilities.

This is the story of Central Bank of India: from Sorabji's rebellion against European banking hegemony to today's struggles with non-performing assets and digital transformation. It's a tale that mirrors India's own economic evolution—the dreams, the compromises, the lost opportunities, and the stubborn persistence. Along the way, we'll explore how a bank founded on the principle of being "property of the nation" became property of the government, and what that transformation cost in terms of innovation, culture, and competitive position.

The numbers are stark: Gross NPAs at 14.8%, a three-year average ROE of just 8.87%, and a stock price that's fallen 37.77% over the past year. Yet this bank was the last PSU bank to exit the RBI's Prompt Corrective Action framework in 2022, suggesting a turnaround story that markets haven't fully digested. With 4,493 branches across 28 states and a CASA ratio of 50.58%, Central Bank retains significant structural advantages—if it can figure out how to leverage them in a digital age.

Our journey will take us from the discriminatory pay scales of colonial banking that sparked Sorabji's rebellion, through the midnight nationalization that transformed Indian banking, to today's battles with asset quality and digital disruption. We'll examine what it means when a bank founded on entrepreneurial defiance becomes a ward of the state, and whether the original Swadeshi spirit can ever be rekindled in an institution that's been under government control for over five decades.

II. The Swadeshi Origins & Sorabji's Rebellion (1900-1911)

The year was 1910, and in the opulent offices of Bank of India, a conversation was taking place that would change Indian banking forever. H.P. Stringfellow, the European manager, lounged in his leather chair, drawing his monthly salary of ₹5,000. Across from him sat a young Parsi accountant earning ₹200 per month—forty times less for doing much of the actual work. When discussions turned to expanding credit facilities to Indian entrepreneurs, Stringfellow delivered his verdict with colonial certainty: "No Indian is competent to manage a bank."

The accountant, twenty-eight-year-old Sorabji Pochkhanawala, felt the words burn. When Stringfellow learned that this assistant accountant was planning to start his own bank, he regarded it as a "huge joke" and called the young man into his office, advising him to abandon what seemed a "chimerical" scheme. But Sorabji had lived with financial discrimination his entire life. His father had died when he was six, leaving the family in poverty as most of their savings had been lost in a bank failure. The irony wasn't lost on him—his family had been destroyed by a bank's collapse, yet the banking establishment claimed Indians couldn't be trusted to run banks.

The pay disparity at Bank of India was just the tip of the iceberg. Not only were there huge pay disparities and humiliations, Europeans dominated banks were partial when it came to giving out credit to Indian entrepreneurs and businesses. Indian merchants found themselves begging for loans to expand their businesses while European firms received credit on favorable terms. The banking system, like everything else in colonial India, was designed to extract wealth, not create it locally.

Sorabji's rebellion didn't emerge in isolation. The early 1900s saw the rise of the Swadeshi movement, and it was being applied to the world of banking as well. The movement called for Indians to boycott British goods and build their own institutions. But banking? That seemed impossible. Banks required capital, credibility, and connections—all monopolized by the colonial establishment.

Yet Sorabji had something more powerful than capital: righteous anger coupled with methodical planning. He resigned from Bank of India, shocking his family who couldn't understand why he would leave a secure job with "prospects." His elder brother Hirjibhoy, who had raised him after their father's death and helped him secure the banking job, was particularly dismayed. But Sorabji had found his mission.

The coalition-building began with Kalianji Vardhaman Jetsey, a business acquaintance who not only provided initial financial support but paid all the preliminary expenses. With Jetsey's support, Pochkhanawala began looking for prominent Indians who would support his vision of an Indian bank by and for Indians, and after successfully locating premises, they managed to form a board of directors after much difficulty.

The genius of Sorabji's approach lay in his understanding that this couldn't be a Parsi bank or a Hindu bank or a Muslim bank—it had to be an Indian bank. The first board consisted of prominent merchants in the Hindu, Muslim and Parsi business communities. The directors included names that read like a cross-section of Bombay's merchant elite: Munchershaw F. Khan, Kalianji Varadhman Jetsey, Ardeshir Bomanji Dubash, Manekji Jethabhai Varadhman, Moolji Haridas, Radhakison Lakmichand, Motilal Kanji, Haji Dawood Haji Elias and Jamsetji Hormusjee Chothia.

But they needed a chairman whose name would command instant respect. The prominent Parsi barrister Sir Pherozeshah Mehta was invited to become chairman of the venture, and accepted. Mehta wasn't just any lawyer—he was a founding member of the Indian National Congress, a leader of the Bombay Municipal Corporation, and one of the most respected Indians in public life. His acceptance legitimized what many saw as a foolhardy venture.

The Central Bank of India was established on December 21, 1911, by Sir Sorabji Pochkhanawala with Sir Pherozeshah Mehta as chairman, as the first commercial Indian bank completely owned and managed by Indians. The paid-up capital was just ₹20 lakhs—minuscule compared to the European-dominated banks. But what it lacked in capital, it made up for in symbolism.

Such was the extent of pride felt by Sir Sorabji Pochkhanawala that he proclaimed Central Bank of India as the 'property of the nation and the country's asset.' He also added that 'Central Bank of India lives on people's faith and regards itself as the people's own bank.' These weren't mere marketing slogans—they represented a fundamental reimagining of what a bank could be in colonial India.

The early response validated Sorabji's vision. Indian merchants who had been denied credit by European banks flocked to Central Bank. Small traders who had never stepped inside a bank felt welcome. The bank's counters heard languages beyond English—Hindi, Gujarati, Marathi, Urdu. It was a small revolution conducted in the language of ledgers and loans.

Looking back at his former boss Stringfellow, Sorabji had a message—though whether he ever delivered it directly is lost to history. The young accountant who had been told no Indian could manage a bank had not only started one but proclaimed it would one day be bigger than Bank of India itself. Sir Sorabji was only 30 years old when he founded Central Bank. At an age when most were still climbing corporate ladders, he had built his own.

The founding of Central Bank of India wasn't just about starting another financial institution. It was about proving that Indians could build and manage complex modern institutions, that they didn't need European oversight to handle their own money. Every loan approved, every deposit accepted, every branch opened was a small act of defiance against the colonial narrative of Indian incompetence.

III. Early Years & Building the "People's Bank" (1911-1947)

The monsoon of 1918 brought more than rain to Hyderabad. It brought the first branch of Central Bank of India outside Bombay, a deliberate challenge to the Imperial Bank's monopoly in the princely states. By 1918 Central Bank of India had established a branch in Hyderabad. Sorabji Pochkhanawala personally traveled to the Nizam's dominion, negotiating not just with bureaucrats but with local merchants who had been starved of credit by the existing banking establishment. A branch in nearby Secunderabad followed in 1925.

The bank's philosophy during these early years was revolutionary for its time. Sorabji proclaimed Central Bank of India as the 'property of the nation and the country's asset'. He also added that 'Central Bank of India lives on people's faith and regards itself as the people's own bank'. These weren't empty slogans. The bank actively courted small depositors, welcomed vernacular languages at its counters, and extended credit to Indian businesses that foreign banks wouldn't touch.

Then came 1923, a year that would test whether Central Bank could play in the big leagues. The Alliance Bank of Simla had collapsed, sending shockwaves through the Indian banking system—ninety-four banks had failed between 1913 and 1918, and the failures continued into the 1920s. In the wreckage stood the Tata Industrial Bank, established by the house of Tata in 1917, now vulnerable and looking for a savior.

In 1923, it acquired the Tata Industrial Bank in the wake of the failure of the Alliance Bank of Simla. The Tata bank, established in 1917, had opened a branch in Madras in 1920 that became the Central Bank of India, Madras. The acquisition wasn't just about absorbing assets—it was about proving that an Indian bank could execute complex mergers, could rescue failing institutions, could act as a stabilizing force in the financial system. The integration brought Central Bank its first major presence in South India through the Madras branch.

But Sorabji's ambitions stretched beyond India's shores. In 1936, he achieved what many thought impossible: Central Bank of India was instrumental in the creation of the first Indian exchange bank, the Central Exchange Bank of India, which opened in London in 1936. This was Indian banking's first beachhead in the global financial capital. For a brief moment, it seemed like Central Bank might become India's first truly international bank.

The celebration was short-lived. Barclays Bank acquired Central Exchange Bank of India in 1938. The British banking establishment had moved swiftly to contain the threat. Yet even this setback couldn't diminish what had been achieved—an Indian bank had proven it could operate at the highest levels of international finance.

Recognition came from the highest quarters of the Empire. Pochkhanawala was knighted in the 1934 King's Birthday Honours list for his services to banking in India, and formally invested with his knighthood at Viceroy's House (now Rashtrapati Bhavan) on 1 March 1935 by the Viceroy, the Marquess of Willingdon. In 1934, he accepted the Government of Ceylon's invitation to become Chairman of the Ceylon Banking Enquiry Commission.

The irony wasn't lost on anyone. The man who had started his bank as an act of rebellion against British economic dominance was now Sir Sorabji, knighted by the very empire he had challenged. Yet he wore the honor not as submission but as vindication—proof that Indians could excel in the modern economy on their own terms.

Throughout the 1930s and early 1940s, Central Bank navigated the treacherous waters of global economic depression and world war. While European banks focused on financing the war effort, Central Bank quietly expanded its network, reaching into small towns and rural areas where no modern bank had ventured before. The branch network grew methodically, each new office a small victory in the larger war for economic independence.

The bank's lending philosophy during this period set it apart. While foreign banks demanded collateral that few Indians could provide, Central Bank pioneered character-based lending, evaluating borrowers on their business acumen and community standing rather than just their land holdings. Small traders, nascent industrialists, and agricultural entrepreneurs found doors opening that had been closed for generations.

By the 1940s, Central Bank had transformed from Sorabji's "chimerical scheme" into one of India's major financial institutions. The paid-up capital that started at ₹20 lakhs had grown manifold. The single office in Fort, Bombay, had become a network spanning the subcontinent. More importantly, it had proven that Indians could build and manage institutions that matched anything the colonial powers had created.

Sir Sorabji passed away on July 4, 1937, a decade before India would achieve the political independence he had fought for economically. But his vision lived on in every branch, every loan, every deposit that proclaimed banking could be truly Indian. The "People's Bank" had survived depression, war, and colonial skepticism. Its greatest test—what would happen when the people actually owned it—lay ahead.

IV. Independence to Nationalization (1947-1969)

August 15, 1947. The fireworks over the Red Fort illuminated a free India, but in the boardrooms of Central Bank of India, independence brought more questions than celebrations. The bank that had been founded as an act of economic defiance against colonialism now faced an existential question: what did it mean to be a Swadeshi bank when the entire nation was finally Swadeshi?

The immediate post-independence period saw Central Bank navigating a dramatically altered landscape. The partition had disrupted traditional trade routes and business relationships. Many of the bank's Muslim board members and customers migrated to Pakistan, leaving behind abandoned accounts and broken commercial networks. Yet the bank persevered, finding new purpose in financing the dreams of a newly independent nation.

The 1950s brought expansion and consolidation. Central Bank positioned itself as the bank of the emerging Indian middle class and small entrepreneur. While foreign banks focused on large corporations and international trade, Central Bank opened branches in mofussil towns where no other bank would venture. The network that had grown methodically under Sorabji's leadership now expanded with nationalist fervor.

Then came a bitter irony. Central Bank of India had established a branch in Rangoon before World War II, with operations concentrated on business between Burma and India, especially money transmission via telegraphic transfer, with profits derived primarily from foreign exchange and margins, and lending against land, produce, and other assets, mostly to Indian businesses. But in 1963, the revolutionary government in Burma nationalized Central Bank of India's operations there, which became People's Bank No. 1.

The bank that had been born from the Swadeshi movement's opposition to foreign control had just seen its own foreign operations nationalized by another newly independent nation. The irony was not lost on the bank's leadership—nationalism, it seemed, cut both ways.

By the mid-1960s, India's banking landscape was becoming increasingly politicized. Prime Minister Indira Gandhi's government introduced "social control" measures over banks in 1967-1969, requiring them to lend more to priority sectors like agriculture and small-scale industries. A high-level body, the National Credit Council, was set up in February 1968 to assess the demand for bank credit and determine priorities in its allocations, and the Boards of Directors of various banks were reconstituted to reduce the power exercised by directors representing large trading and industrial interests.

Central Bank's management watched these developments with mixed feelings. On one hand, the social control measures aligned with Sorabji's original vision of banking for the common Indian. On the other, they sensed that something more dramatic was coming. The writing was on the wall when Finance Minister Morarji Desai resigned on July 16, 1969, following a power struggle with Indira Gandhi.

The fateful day arrived sooner than anyone expected. On 19 July 1969, 14 banks were indeed nationalised, with the announcement coming through a midnight ordinance. Allahabad Bank, Canara Bank, United Bank of India, UCO Bank, Syndicate Bank, Indian Overseas Bank, Bank of Baroda, Punjab National Bank, Bank of India, Bank of Maharashtra, Central Bank of India, Indian Bank, Dena Bank, and Union Bank were nationalised. These banks contained 85 percent of bank deposits in the country.

The nationalisation wasn't just a transfer of ownership—it was framed as a moral imperative. In the words of Indian Prime Minister Indira Gandhi, "it is widely recognized that the operations of the banking system should be informed by a larger social purpose and be subject to close public regulation." The stated objectives were noble: expanding banking to rural areas, supporting priority sectors, and breaking the nexus between big business and big banks.

For Central Bank of India, July 19, 1969, marked the end of an era. The Indian Government nationalized the bank on 19 July, together with 13 others. The institution that Sorabji had proclaimed as "property of the nation" had literally become government property. The transition from being owned by Indian shareholders to being owned by the Indian government might have seemed like a natural evolution to some, but it fundamentally altered the bank's DNA.

The immediate aftermath of nationalization saw dramatic changes. Decision-making moved from the boardroom to the bureaucracy. Branch expansion targets came from Delhi, not from market analysis. Lending decisions increasingly reflected political priorities rather than commercial viability. The entrepreneurial spirit that had driven the bank's first 58 years began to ossify into bureaucratic procedure.

Yet there was also undeniable achievement in those early post-nationalization years. Rural branches proliferated, bringing banking to villages that had never seen a bank. Agricultural credit expanded dramatically. Small entrepreneurs who would never have qualified for loans from private banks found doors opening. In many ways, nationalization initially delivered on its promise of banking for the masses.

The legal challenges to nationalization added another layer of complexity. Within six months after the nationalization, the Supreme Court of India declared the Nationalization Act unconstitutional, holding that the prohibition imposed on former owners from engaging in banking business was discriminatory, and declaring invalid the principle and method prescribed for compensation payment. Following this decision, however, the Government enacted a new Nationalization Law without the previous clauses which the Court had found objectionable.

As the 1960s ended, Central Bank of India found itself at a crossroads. It was now part of a nationalized banking system that controlled 85% of the country's deposits. The bank founded by a rebel against the establishment had become the establishment. The question that would define its next five decades was whether it could maintain any of its founding entrepreneurial spirit within the confines of government ownership.

V. The PSU Bank Era: Growth & Bureaucracy (1969-1991)

The morning of January 1, 1970, dawned on a fundamentally different Central Bank of India. The tricolor now flew over every branch, but something intangible had changed. Decisions that once took hours now took weeks. Loan approvals that once depended on a branch manager's judgment now required forms in triplicate sent to zonal offices. The entrepreneurial energy that had powered the bank's first six decades began to ossify into bureaucratic procedure.

Yet the early years of nationalization delivered undeniable achievements. Between 1969 and 1974, Central Bank's branch network grew by 129%, with rural branches increasing from 18% to 36% of the total network. Villages that had never seen a bank suddenly had access to formal credit. Agricultural loans, which had been a negligible part of the portfolio, exploded as the bank followed government directives to support farmers and small enterprises.

The priority sector lending mandates fundamentally transformed the bank's business model. By 1975, 40% of credit had to flow to agriculture, small-scale industries, and other priority sectors defined by the government. Branch managers who had once competed to finance profitable businesses now had targets for lending to sectors with questionable returns. The social objectives were noble, but the commercial consequences would take years to fully manifest.

Innovation hadn't completely died. Central Bank of India was one of the first banks in India to issue credit cards in the year 1980 in collaboration with Visa. This pioneering move into plastic money showed that even within the constraints of public ownership, there were managers who understood the future of banking. The bank that had been born from rebellion against foreign dominance was now partnering with an American card network to bring modern payment systems to India.

But the credit card launch also highlighted the contradictions of the PSU era. While Central Bank was innovating with Visa cards, its decision-making structure had become so hierarchical that simple operational decisions required approval from Delhi. The same bank that could envision credit cards couldn't approve a ₹10,000 agricultural loan without multiple layers of bureaucracy.

The culture within branches had transformed dramatically. Pre-nationalization, branch managers were mini-entrepreneurs, competing for deposits and prudently extending credit to grow their branches. Post-nationalization, they became administrators implementing government policy. Promotion depended not on performance but on seniority. Risk-taking, once essential for growth, became a career liability.

Then came the scandal that would haunt Central Bank for decades. In the 1980s, the managers of the London branches of Central Bank of India, Punjab National Bank, and Union Bank of India were caught up in a fraud in which they made dubious loans to the Bangladeshi jute trader Rajender Singh Sethia. The regulatory authorities in England and India forced all three Indian banks to close their London branches.

The Sethia affair was more than just a financial scandal—it was a devastating blow to the credibility of Indian banking on the global stage. Central Bank, which had pioneered Indian banking's international presence with the Central Exchange Bank in 1936, was forced to retreat from London in disgrace. The closure of the London branch meant more than lost business; it symbolized how far the bank had fallen from Sorabji's vision of competing with global banks.

The details of the scandal revealed systemic failures. Rajender Singh Sethia had built a commodities empire on borrowed money, with the managers of the London branches of Central Bank of India, Punjab National Bank, and Union Bank of India were caught up in a fraud in which they made dubious loans to the Bangladeshi jute trader Rajender Singh Sethia. The regulatory authorities in England and India forced all three Indian banks to close their London branches. The London branch managers, operating far from head office oversight, had extended credit based on forged documents and inflated collateral values. When Sethia's empire collapsed following coups in Nigeria and Sudan, the banks were left with massive losses.

The scandal exposed a fundamental problem with the PSU banking model: accountability without authority. Branch managers abroad had the authority to extend large loans but lacked the commercial incentive to scrutinize them properly. They were government employees implementing policy, not bankers with skin in the game. The result was predictable—when opportunity for fraud presented itself, internal controls failed spectacularly.

Back in India, the physical expansion continued relentlessly. By 1985, Central Bank had over 3,000 branches, making it one of the largest networks in the country. But quantity hadn't translated to quality. Many rural branches operated at losses, kept alive only by cross-subsidization from profitable urban branches. The massive expansion had stretched management capacity thin, with one regional manager often overseeing dozens of branches across vast geographical areas.

Technology adoption during this period was painfully slow. While private banks globally were computerizing operations, Central Bank's branches still relied on manual ledgers. The resistance wasn't just technological—powerful employee unions viewed computerization as a threat to jobs. Every attempt at modernization became a negotiation with multiple stakeholders, each with veto power over change.

The human cost of bureaucratization was visible in employee morale. The bright young officers recruited in the 1970s with dreams of building a new India through banking found themselves trapped in a system that rewarded compliance over competence. Initiative was discouraged; following procedure was paramount. The bank that had attracted India's best and brightest because it represented Indian enterprise now struggled to retain talent.

By 1991, as India stood on the brink of economic liberalization, Central Bank of India embodied both the achievements and failures of socialist banking. It had successfully brought banking to millions who had never had access to formal credit. It had funded countless small enterprises and agricultural ventures that private banks wouldn't touch. But it had also accumulated massive non-performing assets, lost its competitive edge, and transformed from an entrepreneurial institution into a bureaucratic apparatus.

The London scandal had been particularly symbolic. The bank that Sorabji had founded to prove Indians could compete globally had retreated in disgrace. The credit card innovation showed flashes of the old spirit, but they were exceptions in an institution increasingly defined by inertia. As liberalization loomed, Central Bank faced an existential question: could an institution that had spent two decades as an arm of government policy remember how to be a commercial bank?

VI. Liberalization & Lost Decades (1991-2010)

On July 24, 1991, Finance Minister Manmohan Singh stood in Parliament announcing the dismantling of the License Raj. The protected, socialist economy that had nurtured Central Bank of India for two decades was about to face the cold winds of competition. For a bank that had grown comfortable in its government-guaranteed mediocrity, liberalization wasn't liberation—it was an existential threat.

The immediate impact was psychological. Branch managers who had operated for years in a world where the only competition was other sluggish PSU banks suddenly faced aggressive private players. HDFC Bank received its license in 1994, followed by ICICI Bank, Axis Bank, and others. These new banks didn't carry the baggage of thousands of rural branches, powerful unions, or government-mandated lending targets. They were lean, technology-driven, and customer-focused—everything Central Bank was not.

The contrast was stark. While Central Bank customers queued for hours to withdraw cash from surly tellers working behind iron grilles, HDFC Bank offered air-conditioned branches with relationship managers. While Central Bank took weeks to process a loan application through multiple layers of bureaucracy, private banks promised decisions in 48 hours. The new banks cherry-picked the most profitable customers—urban, educated, and affluent—leaving PSU banks with the costly mandate of financial inclusion.

Technology became the most visible battleground. Private banks launched internet banking, phone banking, and later mobile banking with enthusiasm. Central Bank's computerization efforts, begun half-heartedly in the late 1980s, moved at glacial pace. Employee unions resisted, fearing job losses. Management, accustomed to consensus rather than decision-making, couldn't push through change. By 2000, while private banks were offering online fund transfers, many Central Bank branches still used manual ledgers.

The talent drain accelerated through the 1990s. Young officers recruited by Central Bank were aggressively poached by private banks offering double or triple the salary. The bank that had once attracted India's brightest minds because it represented Indian enterprise now couldn't retain talent in a market that valued performance over seniority. The average age of Central Bank employees crept upward as the young and ambitious fled to greener pastures.

Asset quality emerged as the decade's defining crisis. The directed lending of the 1970s and 1980s had created a mountain of bad loans. Agricultural loans given for political reasons were never expected to be repaid. Priority sector lending to unviable small industries had predictably failed. By the late 1990s, Central Bank's gross NPAs exceeded 15% of total advances. The bank was technically insolvent, kept alive only by government ownership and periodic recapitalization.

The first recapitalization came in 1994, followed by another in 1999. Each time, the government pumped in taxpayer money to keep the bank afloat, but without addressing fundamental issues. It was like giving blood transfusions to a patient while ignoring the internal bleeding. The moral hazard was obvious—why should management fix problems when the government would always bail them out?

Customer service, never Central Bank's strength, deteriorated further in the liberalization era. With guaranteed government backing, there was no incentive to improve. Customers were treated as supplicants rather than clients. Opening an account required multiple visits, countless forms, and inexplicable delays. Loan applications disappeared into black holes. Complaints were met with indifference. The bank that Sorabji had proclaimed as "the people's own bank" had become the bank people avoided if they had any choice.

Yet pockets of excellence persisted. Some branches, led by exceptional managers, maintained high standards despite systemic dysfunction. The bank's vast rural network, while costly, provided financial services to millions who had no other options. The corporate banking division, competing directly with private banks, was forced to improve and retained some prestigious clients. But these were exceptions in an institution increasingly defined by mediocrity.

The millennium approached with Central Bank facing a stark reality. Its market share in deposits had fallen from over 10% in 1990 to less than 5% by 2000. Private banks, with a fraction of Central Bank's branches, were more profitable. Foreign banks, operating from a handful of locations, generated higher returns on assets. The bank founded to prove Indians could compete with anyone was being outcompeted by everyone.

The 2000s brought new challenges and half-hearted responses. Core banking solutions were finally implemented, but years after private banks. ATM networks expanded, but coverage remained patchy. Internet banking launched, but with limited functionality. Each modernization effort seemed to arrive just as private banks moved to the next innovation. Central Bank was perpetually playing catch-up, never quite catching up.

Then came 2009, a year that crystallized the bank's fallen status. CBI is one of twelve public sector banks in India that was recapitalised in 2009. The global financial crisis had exposed weaknesses across the banking system, but Central Bank needed special support. Being grouped with eleven other struggling PSU banks for recapitalization was a far cry from being India's pioneering indigenous bank. The institution that had once led Indian banking now needed government life support just to survive.

The recapitalization of 2009 provided temporary relief but didn't address structural problems. NPAs continued to mount. Technology gaps persisted. Customer service remained abysmal. Private banks continued to eat market share. The young continued to flee. Rural branches continued to bleed money. The cycle of decline seemed unbreakable.

As the decade ended, Central Bank of India embodied the tragedy of Indian public sector enterprises. It had achieved the social objectives of nationalization—banking had indeed reached the masses. But at what cost? The entrepreneurial institution that Sorabji founded had become a zombified bureaucracy, neither fully alive nor allowed to die. It existed because the government wouldn't let it fail, not because it deserved to succeed.

The numbers told a story of steady decline: market share eroding, profitability evaporating, asset quality deteriorating, and talent fleeing. But perhaps the greatest loss was intangible—the complete disappearance of the innovative spirit that had once defined the bank. The institution that had introduced India's first credit card in 1980 was now decades behind in digital banking. The bank that had pioneered international expansion was now retreating from competitive markets.

By 2010, Central Bank of India faced an existential question: could an institution so fundamentally broken be fixed? Or had two decades of protected mediocrity following two decades of bureaucratic control created irreversible institutional decay? The next decade would provide devastating answers.

VII. Modern Struggles & Turnaround Attempts (2010-Present)

The year 2010 began with Central Bank of India at its nadir. NPAs had ballooned to over 20% of advances. The stock price had collapsed to single digits. Young customers didn't even know the bank existed. In boardrooms across Mumbai, the question wasn't whether Central Bank would survive, but whether it deserved to.

The decade opened with crisis compounding upon crisis. The global financial meltdown of 2008 had exposed deep structural weaknesses. Agricultural loan waivers, while politically popular, had destroyed credit discipline. Corporate loans made during the boom years of 2003-2008 turned sour as the economy slowed. By 2011, Central Bank's centenary year—what should have been a celebration—became a moment of existential reckoning.

The contrast with the bank's glorious past was painful. While Central Bank struggled with its centenary, private banks were celebrating record profits. HDFC Bank's market capitalization exceeded that of all PSU banks combined. The bank that Sorabji founded to prove Indian competence had become a cautionary tale of institutional decay.

June 2017 marked rock bottom. RBI had placed Central Bank under PCA in June 2017 due to high net NPAs and negative return on assets. The Prompt Corrective Action framework was regulatory speak for intensive care. The PCA framework blocked large loans, restricted dividend payments and restricted expenses. The bank couldn't lend freely, couldn't pay dividends, couldn't even expand without permission. It was banking purgatory.

The PCA restrictions were humiliating but necessary. Gross NPAs had reached an astronomical 21.48% by March 2018. Net NPAs stood at 11.10%. The bank was technically insolvent, surviving only because of government ownership. Central Bank was the last of the public sector lenders to come out of PCA. While peers like Indian Overseas Bank and UCO Bank escaped PCA in September 2021, Central Bank remained trapped, a symbol of everything wrong with public sector banking.

Yet within this darkness, small changes began. New management recognized that survival required more than government support—it needed fundamental transformation. Cost-cutting initiatives reduced operating expenses. Technology investments, delayed for decades, finally received priority. Digital banking platforms, though still inferior to private banks, at least functioned.

The bank's attempts at modernization often seemed tragicomic. On its 108th Foundation day, Central Bank of India launched its first step towards robotic banking, a robot named "MEDHA". While global banks were deploying AI for credit decisions and fraud detection, Central Bank was introducing a basic robot—symbolic innovation rather than substantive change. Yet even symbolic steps mattered for an institution that had been comatose for decades.

Management changes brought fresh perspectives, though constrained by the realities of government ownership. Each new CEO arrived with transformation plans, only to discover that real change required political will that didn't exist. Unions resisted workforce rationalization. Politicians demanded continued rural presence despite losses. The finance ministry wanted both profitability and social banking—mutually exclusive goals given the bank's condition.

The numbers slowly improved, though from a catastrophically low base. Net NPAs declined from double digits to 3.97 per cent as compared to 10.20 per cent in the fiscal ended March 2017. Capital adequacy ratios improved through repeated government infusions rather than organic earnings. Operating metrics showed marginal improvements, though still far below private sector benchmarks.

The COVID-19 pandemic of 2020-2021 created new challenges and unexpected opportunities. Digital banking, neglected for years, suddenly became essential. Central Bank scrambled to upgrade systems that should have been modernized a decade earlier. The pandemic exposed every technological weakness but also forced changes that normal circumstances couldn't achieve.

September 20, 2022, marked a watershed moment. Reserve Bank of India today removed the Central Bank of India from the Prompt Corrective Action (PCA) framework on complying with parameters like net non-performing assets (net NPAs) and capital ratios. After five years in regulatory intensive care, the bank was finally allowed to function normally. Central Bank was the last of the public sector lenders to come out of PCA.

The exit from PCA was both achievement and indictment. Achievement because the bank had pulled back from the brink of collapse. Indictment because it had taken five years to meet basic regulatory minimums that well-run banks never breach. The bank has provided a written commitment that it would comply with the norms of minimum regulatory capital, net NPA and leverage ratio on an ongoing basis.

Post-PCA, the bank faced a different challenge: relevance. In a market dominated by HDFC, ICICI, and fintech disruptors, what role could a wounded PSU bank play? The answer lay partly in its extensive rural network—4,493 branches reaching areas private banks ignored. But rural banking remained unprofitable, a social obligation rather than commercial opportunity.

Recent initiatives show both ambition and limitation. The bank received approval for GIFT City International Banking Unit operations, attempting to reclaim some international presence lost after the London debacle. Digital initiatives expanded, though the bank remained a follower rather than leader. New products launched regularly, though most were me-too offerings lacking differentiation.

The financial metrics tell a story of stabilization without transformation. Revenue of ₹34,054 crores and profit of ₹4,283 crores seem impressive until compared to peers. The gross NPA at 14.8% and net NPA at 3.97% have improved but remain concerning. The CASA ratio of 50.58% suggests some deposit franchise strength, but growth remains anemic.

Government ownership, now at 89.3%, remains both lifeline and millstone. It ensures survival but prevents the radical restructuring needed for genuine competitiveness. Every decision filters through political considerations. Every reform faces union resistance. Every innovation must clear bureaucratic hurdles. The bank exists in perpetual limbo—too important to fail, too constrained to succeed.

The stock performance reflects market skepticism. Down 37.77% over the past year, trading at just ₹36.2 with a P/E of 7.77, the market values Central Bank as a value trap rather than turnaround story. The P/B ratio below 1 suggests investors believe the bank destroys rather than creates value—a devastating verdict on a 113-year-old institution.

As 2024 progresses, Central Bank of India embodies the tragedy of Indian public sector banking. It has survived existential crisis but lacks a compelling vision for the future. It has exited regulatory purgatory but remains trapped in competitive irrelevance. It has stabilized financially but cannot transform culturally. The bank that once symbolized Indian entrepreneurial ambition now represents institutional inertia.

The modern struggles aren't just about NPAs or technology or competition. They're about purpose. What is Central Bank of India's reason for existence in 2024? Social banking? Private banks now serve rural areas through business correspondents more efficiently. Innovation? Fintech companies lead. Scale? Consolidated private banks dwarf it. The search for purpose defines the bank's modern struggle—a search that remains frustratingly incomplete.

VIII. Business Model & Competitive Position

Central Bank of India's business model in 2024 reads like an archaeological dig through Indian banking history—layers of different eras, each partially obscuring the last, creating a structure that defies both logic and efficiency. The bank operates through three primary segments: Treasury Operations, Corporate/Wholesale Banking, and Retail Banking, but these neat categories mask a chaotic reality of cross-subsidization, political interference, and structural inefficiency.

The treasury operations, traditionally a profit center for banks, struggles under the weight of mandatory government security holdings and statutory requirements. While private banks optimize their treasury for profit, Central Bank's treasury primarily funds government deficits and maintains statutory ratios. The investment portfolio, bloated with government securities, generates predictable but modest returns—safe but uninspiring, much like the bank itself.

Corporate and wholesale banking presents a study in contradictions. The bank maintains relationships with several large corporates, legacy clients from decades past who remain out of inertia or government pressure rather than service quality. New corporate acquisition remains challenging—why would any major corporate choose Central Bank over HDFC or ICICI unless compelled by government relationship requirements? The corporate loan book, scarred by past NPAs, grows cautiously, missing opportunities while avoiding risks.

Retail banking forms the bank's operational backbone but also its greatest challenge. With 4,493 branches and 3,752 ATMs spread across 28 states, Central Bank maintains one of India's largest physical networks. Yet size hasn't translated to strength. Each branch averages just ₹75 crores in deposits, compared to over ₹200 crores for HDFC Bank branches. The 3,752 ATMs process a fraction of the transactions that private bank ATMs handle. Quantity without quality defines the retail footprint.

The rural focus—65.21% of branches in rural and semi-urban areas—represents both mission and burden. These branches fulfill the original vision of banking for the masses but operate at persistent losses. A typical rural branch might have two or three employees serving a few hundred customers, generating revenues that barely cover electricity bills. The social value is undeniable; the economic value is negative. This fundamental tension between social obligation and commercial viability defines Central Bank's business model dysfunction.

The 9,959 business correspondent outlets theoretically extend the bank's reach, but many exist only on paper or operate sporadically. The BC model, successful for private banks, struggles in Central Bank's bureaucratic environment. BCs complain about delayed commissions, system downtimes, and lack of support. Customers complain about BC unavailability and service quality. The model that should enable efficient rural banking instead adds another layer of inefficiency.

Digital banking capabilities remain rudimentary despite recent investments. The mobile app, when it works, offers basic functionality that private banks provided a decade ago. Internet banking feels like a digitized version of paper forms rather than genuine digital transformation. The bank processes 15% of transactions digitally compared to over 90% for leading private banks. Every digital interaction reminds customers why they prefer private banks.

The customer base tells its own story. Central Bank serves approximately 90 million customers, impressive until you realize most are dormant accounts opened to receive government benefits. The average account balance is ₹15,000, compared to ₹100,000+ for private banks. These low-value accounts cost more to maintain than they generate in revenue. The customer base is less an asset than an obligation.

Product innovation, essential for competitive differentiation, barely exists. The product portfolio—savings accounts, fixed deposits, loans, credit cards—mirrors every other bank but without distinctive features. The credit card business, pioneered by Central Bank in 1980, now represents less than 0.5% of India's credit card market. Products launch years after competitors, offering nothing unique except the Central Bank brand—itself a disadvantage in competitive markets.

Risk management, supposedly strengthened post-PCA, remains reactive rather than proactive. Credit decisions still flow through bureaucratic committees rather than data-driven models. The bank's risk appetite swings between excessive caution (missing good opportunities) and political pressure (accepting bad risks). Modern risk management requires sophisticated analytics and quick decisions; Central Bank offers neither.

Human resources present perhaps the greatest structural challenge. The employee base of approximately 30,000 includes many near retirement, few young talents, and a frozen middle management. The average employee age exceeds 45. Training programs exist but can't overcome decades of cultural conditioning. The bank needs employees who think like entrepreneurs but has workers who think like clerks.

Competition from multiple directions compounds these structural weaknesses. Traditional private banks like HDFC and ICICI compete for profitable urban customers. Small finance banks and microfinance institutions serve rural markets more efficiently. Payment banks and fintech companies unbundle profitable services. Neo-banks attract young customers who will never consider Central Bank. Every competitor attacks a specific weakness, and Central Bank has many weaknesses to attack.

The comparison with peers becomes painful at every metric. HDFC Bank generates 5x the profit with fewer branches. ICICI Bank's market cap exceeds 20x Central Bank's. Kotak Mahindra, founded 74 years after Central Bank, is worth 10x more. Even among PSU banks, Central Bank ranks poorly—State Bank of India operates at scale, Punjab National Bank has stronger corporate relationships, Bank of Baroda has better international presence. Central Bank excels at nothing.

Government ownership at 89.3% theoretically provides stability but practically ensures stagnation. Every strategic decision requires government approval. Every organizational change faces political scrutiny. Every branch closure triggers protests. The government's conflicting roles—as owner, regulator, and political actor—create irreconcilable tensions. The bank cannot be truly commercial while serving political objectives.

The financial inclusion mandate, noble in intent, becomes an excuse for inefficiency. Yes, Central Bank serves customers other banks ignore. But at what cost? Each rural branch losing money means urban customers subsidize rural services through higher charges and poorer service. The cross-subsidization model worked when PSU banks monopolized banking; in competitive markets, it drives profitable customers to competitors.

Technology partnerships offer potential salvation but require capabilities Central Bank lacks. Fintech partnerships could modernize services quickly, but the bank's bureaucratic decision-making repels agile partners. Technology vendors see Central Bank as a difficult client—slow to decide, slower to pay, slowest to implement. The bank needs technology transformation but lacks the organizational capability to achieve it.

The competitive position summarizes as: too big to fail, too weak to compete, too constrained to transform. Central Bank occupies an uncomfortable middle ground—larger than regional banks but lacking national presence, broader than niche players but lacking specialization, older than new banks but without the advantages of either legacy or innovation.

Market share statistics paint a picture of steady decline. Deposit market share has fallen from 8% in 1990 to less than 3% today. Advance market share follows a similar trajectory. In every product category—CASA, term deposits, retail loans, corporate credit—Central Bank loses share annually. The trend lines point toward irrelevance.

Yet complete failure remains impossible because of government support and regulatory protection. Central Bank will survive not because it deserves to but because it's not allowed to fail. This guarantee of survival removes the urgency for transformation. Why endure painful restructuring when government recapitalization is always available? Why fight for customers when government mandates ensure captive business?

The business model ultimately reflects a bank caught between two worlds—the protected past and the competitive present—belonging to neither. It cannot return to the monopolistic era that shaped its culture, nor can it fully embrace the competitive dynamics that define modern banking. This liminal existence, neither fully public sector nor genuinely commercial, defines Central Bank's competitive paralysis.

IX. Investment Analysis & Valuation

The investment case for Central Bank of India presents a classical value trap—statistically cheap but fundamentally challenged, theoretically undervalued but practically uninvestable. Trading at ₹36.2 with a book value of ₹40.8, the stock appears to offer a Benjamin Graham-style margin of safety. The P/E ratio of 7.77 suggests deep undervaluation compared to private banks trading at 15-25x earnings. Yet these metrics mask deeper structural issues that explain why the market assigns such a devastating discount.

The price-to-book ratio below 1.0 implies the market believes Central Bank destroys value—a remarkable verdict for a 113-year-old institution. This discount isn't irrational pessimism but rational assessment. Book value includes loans that may never be recovered, branches that will never be profitable, and investments in technology already obsolete. The accounting book value overstates economic value when assets generate returns below the cost of capital.

Return on equity at 11.4% appears respectable until decomposed. This isn't operational excellence generating returns but government recapitalization inflating denominators and one-time recoveries boosting numerators. The three-year average ROE of 8.87% tells a truer story—returns below the cost of capital, value destruction masquerading as profitability. When a bank's ROE consistently trails risk-free rates plus appropriate risk premiums, it's not creating wealth but destroying it with accounting delays.

The interest coverage ratio raises red flags about fundamental profitability. Low interest coverage suggests the bank struggles to service its own obligations from operational earnings—concerning for an institution whose business is lending money. This metric reveals the thin margins between survival and crisis, between solvency and distress. One economic downturn, one spike in NPAs, one withdrawal of government support, and coverage ratios could turn negative.

Revenue growth of 7.38% over five years barely exceeds inflation, implying real negative growth. While private banks doubled or tripled revenues, Central Bank crawled forward. This anemic growth reflects market share losses, customer defections, and inability to price competitively. Revenue growth below nominal GDP growth means the bank shrinks relative to the economy it supposedly serves.

Asset quality improvements from catastrophic to merely concerning don't inspire confidence. Gross NPAs at 14.8% remain multiples above private bank levels. Net NPAs at 3.97% suggest aggressive provisioning, but provision coverage adequacy remains questionable given historical recovery rates. The NPA stock may be declining, but the flow of new stressed assets continues. Agricultural loans, priority sector lending, and political loan waivers ensure future NPA generation.

Capital adequacy ratios meet regulatory minimums but lack buffers for growth or stress. The bank maintains capital adequacy through government infusions rather than retained earnings. Each recapitalization dilutes existing shareholders while postponing fundamental restructuring. The government's 89.3% ownership means private shareholders bear dilution risk without enjoying control premiums.

The stock's 37.77% decline over the past year occurred during a broader market rally, suggesting bank-specific rather than systemic issues. While the Nifty Bank index rose, Central Bank fell—a clear verdict on relative prospects. Technical analysis shows consistent lower highs and lower lows, breakdown from every support level, and absence of accumulation patterns. The chart screams "avoid" to technical traders.

Institutional holding patterns reveal professional skepticism. Mutual funds maintain minimal positions, mostly in index funds required to hold PSU banks. Foreign institutional investors largely avoid the stock. The absence of smart money suggests professionals see no catalyst for revaluation. Retail investors dominate shareholding—usually a contrary indicator for institutional-quality investments.

Dividend policy remains hostage to regulatory approval and government needs. The bank cannot pay dividends without RBI permission, and when permitted, yields remain negligible. Income investors find better yields in fixed deposits than Central Bank dividends. Growth investors see no growth. Value investors recognize value traps. The stock appeals to no investment style.

Comparative valuation versus peers confirms the discount is justified. State Bank trades at premium valuations given its scale and franchise. Private banks command multiples reflecting growth and quality. Even weak PSU banks trade at premiums to Central Bank. The market has spoken: Central Bank is the worst of the worst, the bottom of the barrel, the last choice in any portfolio.

The sum-of-the-parts valuation reveals destruction rather than creation. The branch network, theoretically valuable, generates negative returns. The customer base, numerically large, lacks economic value. The brand, historically significant, now signals poor service. The technology infrastructure requires massive investment to reach competitive parity. Add these parts and the sum is less than zero—the bank is worth more dead than alive.

Scenario analysis offers little hope. In the optimistic scenario, government privatization could unlock value, but political realities make this unlikely. In the base case, the bank muddles through, surviving but not thriving, generating returns below cost of capital indefinitely. In the pessimistic scenario, another NPA crisis triggers fresh recapitalization, diluting shareholders to near-zero.

The option value embedded in potential turnaround seems minimal. Successful turnarounds require either brilliant management (constrained by government control), radical restructuring (prevented by unions and politics), or dramatic market changes (unlikely given competitive dynamics). The probability of successful transformation appears low, the timeline appears long, and the payoff appears uncertain.

ESG considerations add another layer of concern. Governance issues plague all PSU banks, but Central Bank's extended PCA period suggests exceptional weakness. Social objectives conflict with commercial returns. Environmental lending faces pressure from both government mandates and economic reality. ESG-focused investors find nothing attractive in Central Bank's profile.

The investment thesis, if one exists, relies on mean reversion that may never occur. Yes, the stock trades below book value, but book value can decline. Yes, P/E ratios are low, but earnings can evaporate. Yes, the government provides support, but support doesn't guarantee returns. Betting on Central Bank requires faith in catalysts that don't exist.

Risk-reward analysis skews heavily toward risk. Downside includes further NPA cycles, continued market share losses, and perpetual underperformance. Upside requires multiple miracles: government privatization, successful transformation, and market revaluation. The probability-weighted expected return remains negative even with generous assumptions.

For value investors, Central Bank offers a crucial lesson: cheap can get cheaper, and some discounts are deserved. The stock isn't undervalued but properly valued for a structurally challenged, competitively disadvantaged, politically constrained institution. The market's judgment, harsh as it seems, reflects reality rather than misconception.

For fundamental investors seeking long-term compounders, Central Bank represents everything to avoid: declining competitive position, poor capital allocation, weak governance, and limited growth prospects. The bank doesn't compound wealth but erodes it through inflation and opportunity cost. Every rupee invested in Central Bank is a rupee not invested in quality franchises.

The valuation ultimately reflects a simple truth: Central Bank of India is a melting ice cube, slowly dissolving in the heat of competition. Government support prevents sudden collapse but cannot reverse the melt. Investors choosing Central Bank aren't investing but speculating on political decisions and regulatory forbearance. That's not investing; it's gambling with poor odds.

X. Lessons & Legacy

The transformation of Central Bank of India from Swadeshi pride to PSU mediocrity offers profound lessons about institutional decay, the costs of government ownership, and the difficulty of organizational transformation. This isn't just a story about one bank—it's a cautionary tale about what happens when institutions lose their founding purpose and drift into bureaucratic capture.

The first lesson is how quickly organizational culture can deteriorate when accountability disappears. Pre-nationalization Central Bank competed for deposits, carefully evaluated loans, and innovated to survive. Post-nationalization, it became an implementation agency for government policy. Within a single generation, the entrepreneurial culture that Sorabji cultivated was completely replaced by bureaucratic lethargy. Culture, it turns out, is fragile—easier to destroy than create, quicker to lose than build.

The cost of government ownership extends far beyond financial metrics. Yes, there's the direct cost of repeated recapitalizations—taxpayer money poured into a failing institution. But the indirect costs are greater: the opportunity cost of resources trapped in unproductive assets, the social cost of poor financial services, the systemic cost of banking sector weakness. When government owns banks, it doesn't just own assets—it owns problems that compound over time.

The missed opportunities in technology and innovation reveal how protected markets breed complacency. Central Bank introduced India's first credit card in 1980, showing early innovation capability. But protection from competition removed incentives to continue innovating. While global banks revolutionized financial services through technology, Central Bank treated computers as expensive typewriters. The bank that could have led Indian financial innovation instead became a laggard, forever playing catch-up.

Political interference emerges as a cancer that metastasizes throughout the organization. Every loan waiver destroys credit culture. Every forced merger disrupts operations. Every mandated priority sector target distorts risk assessment. Politicians treat PSU banks as tools for electoral management rather than commercial enterprises. The result is institutions that serve political objectives while failing commercial ones.

The human capital tragedy deserves special attention. Central Bank once attracted India's brightest minds—people like Sorabji who could have succeeded anywhere chose to build an Indian institution. Today, it's an employer of last resort, unable to attract talent or retain performers. The brain drain isn't just about numbers but about capability—the people who could transform the bank leave, while those who can't stay.

Can culture be revived after 50+ years of nationalization? The evidence suggests no. Organizational culture is like sedimentary rock—formed over time through repeated behaviors and reinforced expectations. Central Bank's culture solidified around risk aversion, process compliance, and political subservience. Changing this requires not just new policies but new people, new structures, and new incentives—essentially, building a new bank.

The parallels with other post-colonial institutions are striking. Like Air India, Central Bank was once a symbol of national capability that became a symbol of public sector failure. Like Hindustan Motors, it was a pioneer that became obsolete. Like MTNL, it dominated its market until liberalization exposed its weaknesses. The pattern repeats: early promise, government takeover, bureaucratic capture, competitive irrelevance.

Yet the story also contains inspiration. That a young Parsi clerk could challenge the entire colonial banking establishment and create an institution that survived over a century shows the power of individual initiative. Sorabji's vision—banking as a tool for economic independence—was revolutionary for its time. His execution—building coalitions across religious and ethnic lines—showed sophisticated leadership. His legacy, though tarnished, remains remarkable.

The broader implications for India's economy are sobering. If Central Bank, with its storied history and nationwide presence, cannot be successfully reformed, what hope exists for other PSU transformations? The bank's struggles suggest that some institutional decay is irreversible, that some organizations are too broken to fix. This raises uncomfortable questions about the vast public sector apparatus India maintains.

For entrepreneurs, Central Bank's history offers both warnings and encouragement. The warning is how quickly successful institutions can decay when they lose their founding purpose. The encouragement is that one person with vision can challenge entire systems. Sorabji didn't just start a bank—he challenged colonial assumptions about Indian capability. Modern entrepreneurs can draw inspiration from his audacity while learning from his institution's decay.

For policymakers, the lessons are uncomfortable but essential. Government ownership of commercial enterprises creates irreconcilable conflicts between social and commercial objectives. Political interference in commercial decisions destroys institutional capability. Protection from competition breeds inefficiency. These aren't ideological assertions but empirical observations from Central Bank's century-long experiment.

The question of what Sorabji Pochkhanawala would think today is both fascinating and depressing. The man who proclaimed Central Bank as "property of the nation" might argue nationalization fulfilled his vision. But seeing the bureaucratic morass his bank became, the entrepreneurial fire extinguished, the competitive position lost, he would likely weep. His bank hasn't failed—that would be merciful. Instead, it exists in perpetual mediocrity, neither living nor dead.

The tragedy isn't that Central Bank failed but that it survived in diminished form. Failure would have released resources for productive use. Closure would have ended the suffering. Instead, government support ensures zombie existence—alive enough to consume resources, dead enough to create no value. This corporate purgatory, neither successful enough to thrive nor failed enough to die, defines too many Indian PSUs.

Looking forward, Central Bank's experience suggests several imperatives. First, institutions need constant renewal or face decay. Second, government ownership and commercial excellence are incompatible. Third, protected markets destroy rather than develop capability. Fourth, organizational culture, once lost, is nearly impossible to recover. These lessons apply beyond banking to any institution navigating between state control and market competition.

The ultimate lesson may be about institutional mortality. Not all organizations deserve to survive indefinitely. Creative destruction—Schumpeter's famous concept—requires the destruction part, not just creation. By preventing Central Bank from failing, government prevents resources from flowing to better uses. The kindest thing might be to let it die with dignity rather than suffer indefinitely.

Yet there's also a lesson about resilience. Despite everything—nationalization, bureaucratization, competition, crisis—Central Bank survives. Damaged, diminished, and declining, but still standing. This cockroach-like survival ability, while economically inefficient, shows institutional endurance. The bank Sorabji founded outlasted the British Empire, survived nationalization, and endures liberalization. That's not nothing.

The final lesson concerns national development. Central Bank's story parallels India's own journey—early entrepreneurial energy, socialist capture, liberalization struggles, and ongoing transformation. The bank's challenges mirror national challenges: how to balance social objectives with commercial reality, how to transform institutions without destroying them, how to compete globally while serving locally. In this sense, Central Bank of India isn't just a bank—it's a microcosm of India itself.

XI. The Path Forward & Final Thoughts

Standing at the crossroads of irrelevance and resurrection, Central Bank of India faces choices that will determine whether it celebrates another century or finally succumbs to competitive forces. The path forward isn't mysterious—everyone knows what needs to be done. The question is whether political will exists to do it.

Privatization debates dominate discussions about PSU bank futures, but for Central Bank, the reality is stark: no private investor would buy it at any reasonable price. The bank's challenges—massive NPA overhang, bloated workforce, toxic culture, obsolete technology, political interference—make it uninvestable. Unlike Air India, which had valuable routes and slots, Central Bank offers no hidden assets. The branch network generates losses. The customer base lacks value. The brand signals poor service. What exactly would an investor buy?

The political realities make privatization even more unlikely. Selling Central Bank would require acknowledging five decades of failed stewardship. Employee unions would strike. Opposition parties would protest. Media would highlight job losses. The political cost exceeds any economic benefit. Governments find it easier to perpetually recapitalize than admit failure through privatization.

Digital transformation imperatives cannot be ignored, yet the bank lacks capabilities for genuine transformation. Yes, it can launch apps and websites—cosmetic digitization that mimics modern banking. But true digital transformation requires reimagining processes, restructuring organizations, and recruiting new talent. Central Bank needs revolutionary change but can only manage incremental improvement. The gap between digital leaders and Central Bank widens daily.

The fintech threat compounds competitive pressures. While Central Bank struggles with basic digital banking, fintech companies unbundle every profitable service. Payments, lending, wealth management—specialized players attack each vertical with superior technology and customer experience. Central Bank's integrated model, once an advantage, becomes a liability when specialists can cherry-pick profitable segments while avoiding costly obligations like rural branches.

Partnership opportunities exist theoretically but face practical obstacles. Fintech companies could modernize Central Bank's technology. NBFCs could originate loans. Payment companies could upgrade transaction systems. But why would dynamic companies partner with a bureaucratic bank? The cultural mismatch, decision-making delays, and regulatory complications deter potential partners. Central Bank needs partnerships but repels partners.

What would Sorabji Pochkhanawala think today? The banker who challenged colonial assumptions about Indian incompetence would be appalled at the voluntary incompetence his bank now displays. The entrepreneur who competed against foreign banks would be ashamed of the fear of competition. The visionary who proclaimed the bank as "property of the nation" would question what value it provides the nation. His disappointment would be profound, his judgment harsh.

Yet Sorabji might also recognize patterns. Just as colonial banks dismissed Indian capability, modern observers dismiss Central Bank's potential. Just as he built coalitions across communities, modern leadership could build partnerships across sectors. Just as he leveraged the Swadeshi movement's energy, the bank could leverage India's digital transformation. The parallels exist, but the will doesn't.

The key takeaways for entrepreneurs are both inspiring and cautionary. Sorabji's story shows that individuals can challenge entire systems, that David can compete with Goliath, that indigenous institutions can match foreign ones. But Central Bank's decay warns that successful institutions require constant renewal, that government ownership corrupts commercial purpose, that protection from competition destroys capability. Build institutions, but build them to last through adaptation, not through protection.

For investors, the takeaways are clearer: avoid value traps, respect competitive dynamics, and understand that government support doesn't guarantee returns. Central Bank offers a masterclass in why statistical cheapness doesn't equal investment value. The market's judgment, harsh as it seems, reflects reality. Some institutions are uninvestable regardless of price. Some turnarounds never turn. Some value traps remain traps forever.

The broader implications for India's financial sector are profound. If Central Bank cannot be transformed despite its history, network, and government support, what hope exists for weaker PSU banks? The sector needs consolidation, but merging weak banks creates bigger weak banks, not strong ones. It needs privatization, but political realities prevent it. It needs transformation, but institutional capabilities limit it. The problems are clear; the solutions are not.

Looking ahead, three scenarios seem possible. The optimistic scenario involves gradual improvement—NPAs decline, technology improves, culture slowly shifts. The bank survives as a mediocre but stable institution, serving segments others ignore, fulfilling social objectives while destroying economic value. This muddle-through scenario seems most likely given political realities.

The pessimistic scenario involves another crisis—NPAs spike, losses mount, and recapitalization needs explode. The government, facing fiscal constraints, cannot provide unlimited support. The bank faces resolution, merger, or closure. This scenario, while painful, might provide the crisis needed for genuine reform. Sometimes institutions need near-death experiences to change.

The transformative scenario requires multiple miracles: visionary leadership, political support, employee cooperation, and competitive breathing room. The bank would need to shed legacy obligations, modernize technology, transform culture, and compete effectively—all simultaneously. The probability seems vanishingly small, but transformation is theoretically possible. Other institutions have achieved dramatic turnarounds, though rarely under government ownership.

Final reflections return to the beginning. Central Bank of India was born from one man's refusal to accept limitations, his insistence that Indians could compete with anyone. That spirit—entrepreneurial, defiant, ambitious—created an institution that challenged colonial banking hegemony. But that same institution, captured by government and protected from competition, lost everything that made it special.

The tragedy isn't just institutional but national. India needs strong banks to finance development, serve citizens, and compete globally. Every weak bank represents misallocated resources, underserved customers, and missed opportunities. Central Bank's mediocrity isn't just its own failure but a failure of the system that perpetuates such mediocrity.

Yet perhaps there's hope in the next generation. Young Indians, digital natives who never knew monopolistic banking, won't tolerate Central Bank's service levels. They'll force change through choice, selecting banks that serve rather than frustrate them. Market forces, more than government policy, may ultimately determine Central Bank's fate.

The story of Central Bank of India, from Swadeshi pride to PSU struggle, encapsulates broader truths about institutional evolution, government ownership, and competitive dynamics. It's a cautionary tale about how successful institutions can decay, how government ownership corrupts commercial purpose, how protection from competition destroys capability. But it's also an inspiring reminder of what individual vision can achieve, how one person's refusal to accept limitations can create lasting institutions.

As we close this analysis, Central Bank of India remains suspended between its glorious past and uncertain future. The bank that once symbolized Indian capability now symbolizes institutional decay. The transformation from pride to embarrassment took decades; reversal, if possible, will take decades more. Whether Central Bank survives another century depends on choices made today—choices that require courage, vision, and willingness to challenge the status quo.

Just as Sorabji Pochkhanawala refused to accept that Indians couldn't run banks, modern leadership must refuse to accept that Central Bank can't be transformed. The question isn't whether transformation is possible but whether the will exists to attempt it. History suggests skepticism; hope demands optimism. The next chapter of Central Bank's story remains unwritten, its ending uncertain.

For now, Central Bank of India endures—damaged but not dead, struggling but not surrendered, hoping but not transforming. It remains, in Sorabji's words, "property of the nation," though what value that property provides remains an open question. The Swadeshi bank that survived a century faces its greatest challenge not from external competition but from internal decay. Whether it survives another century—and whether it deserves to—only time will tell.

XII. Recent News

The drumbeat of recent developments around Central Bank of India reads like dispatches from a battlefield where small victories barely offset strategic defeats. Each quarterly result, each regulatory filing, each management announcement adds another data point to the ongoing story of struggle and marginal recovery.

The most significant recent development came with the bank's exit from the PCA framework in September 2022, ending five years of regulatory purgatory. The Reserve Bank of India's decision to lift restrictions wasn't a vote of confidence but rather acknowledgment that Central Bank had finally met minimum regulatory standards—standards that well-run banks never breach. The bank provided written commitments to maintain capital adequacy, control NPAs, and manage leverage ratios, essentially promising to do what banks should do naturally.

Third quarter 2024 results showed the mixed picture that has become Central Bank's signature. Net profit rose 13% year-on-year to ₹913 crores, but this growth came primarily from treasury gains rather than core banking operations. Net interest income grew a modest 7%, barely keeping pace with inflation. The numbers showed survival, not revival—a patient off life support but far from healthy.

The bank's recent foray into GIFT City with International Banking Unit approval represents an attempt to reclaim some international presence lost after the London scandal decades ago. Yet this feels more like nostalgia than strategy. While dynamic banks are building global digital platforms, Central Bank is opening a single office in a tax-advantaged zone. It's the banking equivalent of fighting modern warfare with cavalry—brave but futile.

Technology initiatives announced with fanfare reveal the gap between aspiration and reality. The launch of MEDHA, the banking robot, generated headlines but little practical value. Enhanced mobile banking features simply matched what competitors offered years ago. The digital lending platform for MSMEs, while needed, enters a market already dominated by nimble fintech players. Each announcement feels like catching up rather than moving ahead.