CDSL: The Democratization of India's Capital Markets

I. Introduction & Episode Roadmap

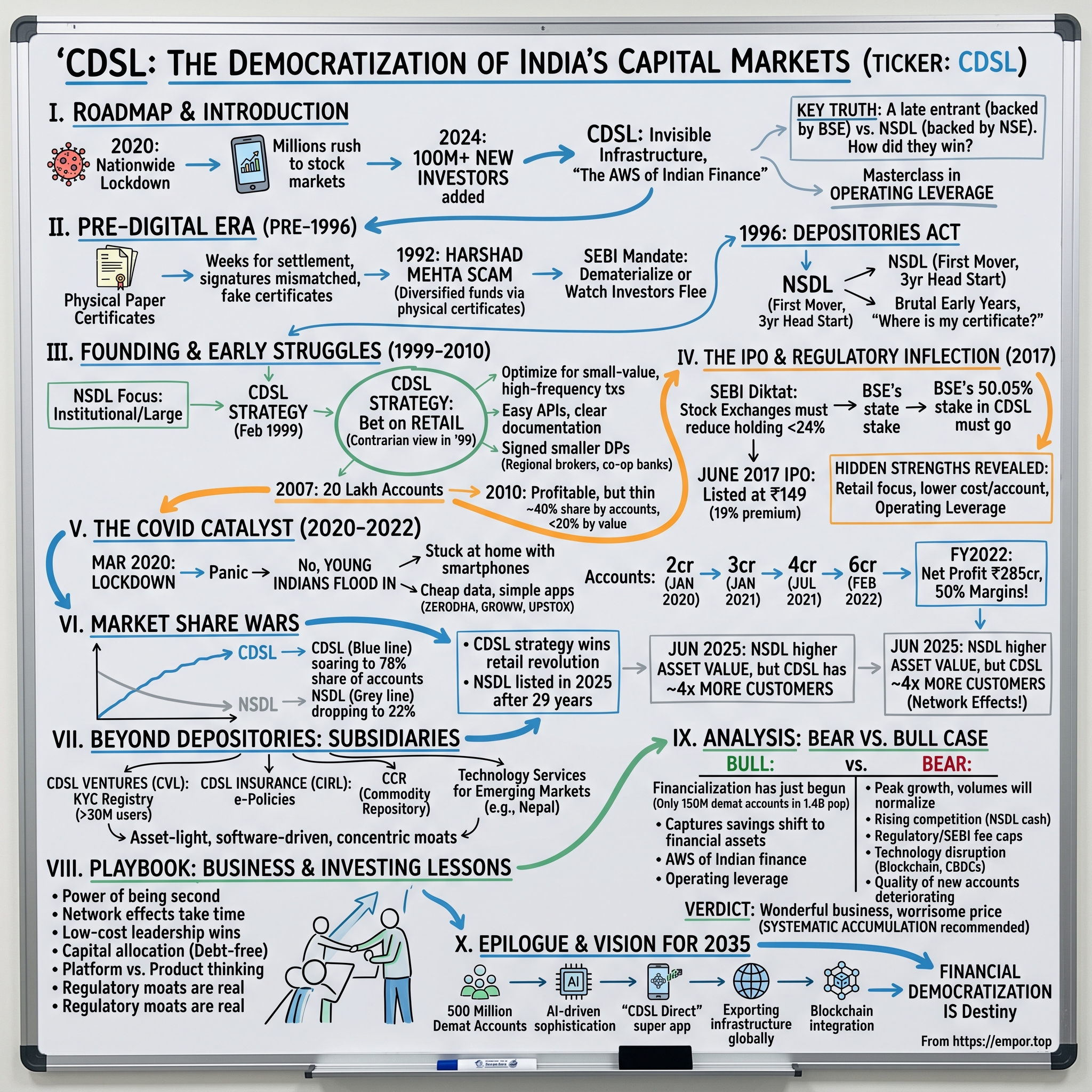

Picture this: It's March 2020. India enters its first nationwide lockdown. The BSE Sensex crashes 40% from its peak. Panic selling grips the markets. Yet something extraordinary happens in the months that follow—millions of Indians, stuck at home with smartphones and savings, don't flee the markets. They flood in.

Between March 2020 and March 2024, India adds over 100 million new stock market investors. To put that in perspective, that's more than the entire population of Germany becoming first-time investors in just four years. At the center of this revolution sits a company most people have never heard of: Central Depository Services Limited, or CDSL.

Today, CDSL commands a staggering 78% market share of all demat accounts in India. If you're one of India's 150 million retail investors, there's a three-in-four chance CDSL holds your securities in electronic form. They're the invisible infrastructure that makes India's capital markets tick—the AWS of Indian finance, if you will.

But here's what makes this story fascinating: CDSL wasn't the first mover. They entered a market three years after their rival NSDL had already established dominance. They were promoted by the smaller exchange, BSE, while NSDL had the backing of the mighty NSE. For their first decade, they barely registered as competition.

So how did a late entrant, backed by the weaker exchange, operating in a heavily regulated duopoly, become the chosen depository for India's retail revolution? How did they flip from 20% market share to 78% in less than a decade? And what happens when you suddenly democratize access to capital markets for 1.4 billion people?

This is a story about timing, technology, and transformation. It's about how regulatory quirks can create opportunities, how COVID accelerated a decade of change into two years, and how sometimes being second means you get to learn from everyone else's mistakes. It's also a masterclass in operating leverage—how a business with essentially fixed costs can see profits explode when volumes go parabolic.

Over the next several hours, we'll trace CDSL's journey from a paper-pushing back office operation to a high-margin technology platform. We'll explore the Harshad Mehta scam that created the need for depositories, the regulatory twist that forced their IPO, and the perfect storm of factors that turned them into one of India's best-performing stocks. We'll dive deep into their competitive dynamics with NSDL, their expansion beyond depositories, and what their dominance means for India's financial future.

But most importantly, we'll unpack the playbook—the strategic decisions, market dynamics, and execution excellence that turned a boring piece of market infrastructure into a compounding machine. Because in the end, CDSL's story isn't just about one company. It's about what happens when you give a billion people access to wealth creation for the first time in history.

II. The Pre-Digital Era: Paper Certificates & Market Infrastructure

The year is 1992. India has just begun liberalizing its economy. Foreign institutional investors are arriving. The Bombay Stock Exchange hums with activity. But beneath this modernizing facade lurks an antiquated system that's about to spectacularly implode.

Every stock trade in India involves physical paper certificates. When you buy shares, you wait weeks for the actual certificates to arrive by post. Settlement takes T+14 days. Signature mismatches void transactions. Fake certificates circulate freely. Lost certificates mean lost wealth—no recourse, no recovery. The back offices of brokerages overflow with paper, stamps, and frustrated clerks manually matching trades.

Into this chaos steps Harshad Mehta, a broker who discovers he can exploit the settlement system's gaps. Using a practice called "ready forward deals," Mehta diverts funds from banks to pump up stock prices, creating artificial demand. He physically intercepts share certificates, pledges the same shares to multiple banks, and builds a ₹4,000 crore scam—roughly $1.3 billion in 1992 dollars.

When the scam unravels in April 1992, it doesn't just crash the markets—it exposes the terrifying fragility of India's entire financial infrastructure. The BSE index falls 72% from its peak. Investors lose fortunes not to bad trades but to lost certificates, forged signatures, and settlement failures. The message becomes crystal clear: India cannot build a modern capital market on Victorian-era infrastructure.

SEBI, India's market regulator established just months before the scam, suddenly finds itself with an urgent mandate: revolutionize market infrastructure or watch foreign investors flee. The solution they prescribe seems radical for paper-obsessed India: dematerialization. Convert all physical shares into electronic entries. Create depositories—the financial equivalent of email servers for securities.

The Depositories Act gets passed in 1996, creating the legal framework for electronic shareholding. But legislation is one thing; execution is another. Who will build this infrastructure? Who will convince millions of Indians to give up their physical share certificates—often kept in bank lockers as family heirlooms—for invisible electronic entries?

Enter NSDL—National Securities Depository Limited—in November 1996. Promoted by the National Stock Exchange (NSE), State Bank of India, and IDBI, NSDL becomes India's first depository. They face a herculean task: not just building technology infrastructure in a country where computers remain luxury items, but fundamentally changing investor behavior.

The early years are brutal. Investors don't trust electronic holdings. "Where's my certificate?" becomes the constant refrain. Registrars resist change—their entire business model depends on processing physical transfers. Even brokers hesitate, worried about losing control. NSDL spends three years essentially missionary selling, educating one investor at a time.

By 1999, NSDL has made modest progress but the market remains fragmented. Physical certificates still dominate. Settlement risks persist. Foreign investors demand better infrastructure. The market needs competition, innovation, and most importantly, choice.

This is the world CDSL enters in February 1999. Promoted by the Bombay Stock Exchange—NSE's older but now smaller rival—CDSL faces an uphill battle. NSDL has a three-year head start, relationships with major institutions, and the backing of the dominant exchange. But CDSL's founders see opportunity where others see obstacles. They believe India's capital markets will eventually democratize, that retail investors will embrace equities, and that being second means you can learn from the pioneer's mistakes.

The vision CDSL articulates is deceptively simple: "Convenient, dependable and secure depository services at affordable cost to all market participants." That phrase "all market participants" becomes crucial. While NSDL focuses on institutions and large investors, CDSL quietly positions itself for a retail revolution that won't arrive for another two decades.

When CDSL commences operations in March 2000, few notice. The dot-com bubble is bursting globally. Indian markets remain subdued. The company starts with just a handful of depository participants and a few thousand accounts. But they're building for a future where every Indian might own stocks—a future that seems impossibly distant in 2000 but will arrive with stunning speed twenty years later.

III. Founding Story & Early Struggles (1999–2010)

The boardroom at BSE's historic Phiroze Jeejeebhoy Towers buzzes with tension in early 1999. The exchange's leadership faces a strategic dilemma: their rival NSE has leapfrogged them in trading volumes, partly due to superior technology and their captive depository NSDL. BSE needs its own depository to remain relevant, but they're three years behind.

The man tasked with this seemingly impossible catch-up is the BSE's leadership team, who approach it with a contrarian insight: don't compete where NSDL is strong. Instead, build for the market segment everyone ignores—retail investors. In 1999, this seems almost absurd. Retail participation in Indian equities is minimal. The middle class keeps savings in gold, real estate, and fixed deposits. Stocks are for the wealthy or the reckless.

But BSE has history on its side. As Asia's oldest exchange, established in 1875, they understand market cycles. They've seen retail investors flood in during the Harshad Mehta boom. They believe—no, they know—retail will return. The question is when, not if.

CDSL incorporates with authorized capital of ₹25 crores, with BSE holding 50.05% stake. The remaining equity gets distributed among leading banks—Bank of India, Bank of Baroda, HDFC Bank, and State Bank of India among others. This ownership structure proves crucial: while NSDL has institutional DNA, CDSL gets retail banking DNA from day one.

The early technology choices reveal their strategy. While NSDL builds for large batch processing—massive institutional trades—CDSL optimizes for high-frequency, small-value transactions. They invest in user interface simplicity when everyone else focuses on backend robustness. They make their APIs easier to integrate, documentation clearer to understand. Small decisions that seem insignificant in 2000 but prove prescient by 2020.

The first five years are agonizing. By 2005, CDSL has barely 10% market share. Board meetings feature heated debates about strategy. Should they pivot to compete directly with NSDL for institutional business? Should they seek additional capital? Some directors push for aggressive pricing to gain share. Others worry about sustainability.

The company makes a crucial decision: stay the course. They continue investing in retail infrastructure even as losses mount. They sign up smaller depository participants—regional brokers, cooperative banks, small financial advisors—entities NSDL considers uneconomical to service. Each DP gets personal attention, training, hand-holding. CDSL employees joke they're running a consulting firm, not a depository.

Then comes an unexpected break. In 2003, SEBI mandates that all IPOs must issue shares only in demat form. Suddenly, every retail investor wanting to participate in the IPO boom needs a demat account. CDSL's retail-friendly infrastructure perfectly positions them to capture this demand. Their smaller DP partners, spread across Tier 2 and Tier 3 cities, become crucial distribution channels.

The numbers start improving marginally. By 2007, CDSL crosses 20 lakh demat accounts. Still far behind NSDL's institutional dominance by value, but gaining ground in sheer account numbers. The company remains unprofitable, burning through capital to build infrastructure for a retail boom that hasn't materialized.

The 2008 financial crisis nearly breaks them. Retail investors flee equities. Account openings plummet. The board faces pressure to cut costs, reduce headcount, scale back ambitions. BSE itself struggles with declining volumes. There's talk of merging CDSL with NSDL to create a monopoly depository.

But CDSL's management makes a counterintuitive observation: the investors who remain after 2008 are different. They're younger, more educated, comfortable with technology. They trade online through discount brokers starting to emerge. They don't need hand-holding; they need efficiency and low costs. This isn't the retail boom CDSL expected, but it's the beginning of something.

By 2010, CDSL has survived its first decade—barely. They have about 75 lakh demat accounts, roughly 40% market share by account numbers but less than 20% by value. They're finally profitable, but margins remain thin. The company looks like a modest success at best, a survivor in a duopoly where the winner (NSDL) has already been decided.

Nobody—not the board, not management, not investors—imagines that within a decade, CDSL will completely flip this market share, or that their patient investment in retail infrastructure is about to pay off in ways that seem impossible in 2010. The stage is set, the infrastructure is built, the partnerships are in place. All CDSL needs now is a catalyst—or three.

IV. The IPO & Regulatory Inflection Point (2017)

The letter from SEBI arrives at BSE headquarters in 2016 like a lightning bolt. The regulator's message is clear and non-negotiable: stock exchanges must reduce their shareholding in market infrastructure institutions to below 24%. BSE's 50.05% stake in CDSL must go. The deadline is tight. The implications are massive.

For CDSL's management, this regulatory diktat transforms from crisis to opportunity. An IPO isn't just compliance—it's a chance to rewrite their story. They're no longer BSE's subsidiary but an independent market infrastructure company. The timing couldn't be better: India's markets are booming, retail participation is growing, and fintech disruption is beginning.

The preparation for the IPO reveals CDSL's hidden strengths. As bankers pore through financials, a compelling narrative emerges. Yes, NSDL dominates by value of assets held. But CDSL owns the future—younger accounts, retail relationships, lower costs per account. The numbers tell a story of operating leverage waiting to explode: 90% gross margins, minimal capital requirements, regulatory moat.

The IPO prospectus, filed in May 2017, makes fascinating reading in hindsight. CDSL positions itself not as a depository but as a "financial market infrastructure company." They highlight their 1.6 crore demat accounts, their profitable subsidiaries, their technology platform. But buried in risk factors is a telling admission: "Our business depends significantly on retail investor participation in the securities market."

The roadshow generates unexpected enthusiasm. Institutional investors who've ignored CDSL for years suddenly see the potential. The retail story resonates. The operating leverage excites. The valuation seems reasonable—₹524 crore for a monopoly-like business with 40% market share and expanding margins.

On June 30, 2017, CDSL lists on the exchanges at ₹149 per share, a 19% premium to the issue price of ₹125. It's a respectable debut, not spectacular. BSE successfully reduces its stake to 24%, raising about ₹330 crores. The financial media covers it as a routine infrastructure IPO. Nobody calls it transformational.

But something subtle and powerful happens post-IPO. CDSL is now Asia-Pacific's first listed depository, only the second globally after Russia's National Settlement Depository. This unique position attracts attention. International investors start analyzing India's market structure. The transparency of quarterly results forces management to articulate strategy clearly, execute precisely.

The new shareholding structure energizes management. With BSE no longer majority owner, CDSL can partner with NSE-affiliated brokers without political complications. They can invest in technology without bureaucratic approval. They can pursue acquisitions, enter new businesses, think bigger.

The first post-IPO quarters show steady but unspectacular growth. Revenues grow 15% annually. Profits expand slightly faster due to operating leverage. The stock price meanders, trading between ₹130-180. Sell-side analysts remain lukewarm—it's a decent business but hardly exciting.

Inside CDSL, however, a transformation is underway. The IPO proceeds fund technology upgrades. They rebuild their core platform for cloud-scale. They develop APIs for the emerging fintech ecosystem. They hire engineers from India's top technology companies. None of this shows up immediately in financials, but they're building infrastructure for exponential growth.

The company also uses its listed status strategically. They become thought leaders on market structure, regularly engaging with regulators, publishing research, hosting conferences. The message is consistent: India's retail investor base will explode, and CDSL is the infrastructure play on this theme.

By 2019, subtle signs of acceleration appear. Account additions increase from 2-3 lakhs monthly to 4-5 lakhs. Young Indians, comfortable with smartphones and attracted by the bull market, start opening demat accounts. Discount brokers like Zerodha, Upstox, and Groww report user growth. CDSL's market share in new accounts quietly crosses 60%.

The board and management sense something building but can't quite quantify it. The infrastructure investments seem prescient. The retail focus feels validated. But nobody—absolutely nobody—predicts what's about to happen. In their wildest projections for 2020, CDSL's management forecasts maybe 2.5 crore accounts by year-end.

Reality will exceed their wildest dreams by multiples. The company that listed at a ₹1,500 crore market cap will soon be worth ₹15,000 crores. The "boring" depository will become one of India's best-performing stocks. And it all starts with a black swan that nobody sees coming.

V. The COVID Catalyst: Retail Revolution (2020–2022)

March 24, 2020, 8 PM. Prime Minister Modi announces India's first nationwide lockdown. Within hours, 1.4 billion people are confined to their homes. The BSE Sensex, which had already fallen 30% from its peak, will drop another 10% the next day. Traditional wisdom suggests retail investors should panic, sell everything, hide in fixed deposits.

Traditional wisdom is spectacularly wrong.

What happens next defies every historical pattern of retail investor behavior during crises. Instead of fleeing, young Indians flood into the markets. They're stuck at home with smartphones, savings from cancelled vacations, and YouTube videos explaining options trading. The market crash isn't a disaster—it's a discount sale.

At CDSL's Mumbai headquarters, now operating with skeleton staff, the operations team watches their dashboards with disbelief. Daily account openings, which averaged 15,000 in January 2020, hit 50,000 by May. Then 75,000 by July. Then 100,000 by September. Their servers, built for gradual growth, strain under exponential demand.

The numbers become surreal. CDSL adds more accounts in April 2020 than they did in all of 2015. Their two-crore account milestone, reached in January 2020 after 20 years of operations, becomes three crores by January 2021. Just six months more to hit four crores. The hockey stick isn't just vertical—it's practically perpendicular.

Behind this surge lies a perfect storm of factors. Discount brokers like Zerodha and Groww make account opening completely digital—Aadhaar-based KYC, video verification, zero paperwork. These brokers specifically choose CDSL over NSDL for a simple reason: better APIs, faster integration, lower costs. Every Zerodha account, every Groww user, every Upstox customer becomes a CDSL account by default.

The operational challenge is staggering. CDSL's technology team works round-the-clock, scaling infrastructure in real-time. They move from on-premise servers to cloud computing. They implement auto-scaling. They optimize databases that were designed for thousands of daily transactions but now handle millions. It's like rebuilding an airplane engine mid-flight.

The financial impact is immediate and dramatic. CDSL's revenue model—transaction fees, account maintenance charges, settlement fees—benefits from perfect operating leverage. Their costs are largely fixed: the same technology platform handles 2 crore or 10 crore accounts. But revenues scale linearly with accounts and transactions.

The FY2021 results shock everyone. Net profit explodes to ₹201 crores from ₹106 crores—a 90% jump. But that's just the beginning. FY2022 sees profit hit ₹285 crores. Margins expand from 35% to 50%. Return on equity exceeds 30%. The stock price, which bottomed at ₹275 in March 2020, crosses ₹1,400 by December 2021—a 400% gain.

But the real transformation isn't financial—it's structural. CDSL's market share in new account openings reaches an astounding 88%. They're adding 30-40 lakh accounts monthly while NSDL adds 5-10 lakhs. The David and Goliath dynamic has completely reversed. NSDL still holds larger institutional accounts by value, but CDSL owns retail, and retail is the future.

The demographic shift is equally remarkable. The average age of new account holders drops from 35 to 27. Small towns contribute 60% of new accounts. First-time investors comprise 70% of additions. This isn't just market participation—it's democratization. The rickshaw driver in Ranchi, the teacher in Tiruchirappalli, the shop owner in Surat—they're all becoming investors.

CDSL's management, to their credit, doesn't rest on laurels. They use windfall profits to invest aggressively in technology. They launch CDSL Ventures, expanding into KYC services. They develop new products—e-voting platforms, consolidated account statements, insurance repositories. They sign partnerships with payment apps, mutual fund platforms, cryptocurrency exchanges. Every Indian financial service wants to integrate with CDSL's massive user base.

By February 2022, CDSL becomes the first Indian depository to cross 6 crore active demat accounts. The press release is triumphant but understated. What it doesn't say is more interesting: at current run rates, they'll hit 10 crores within two years. India is adding more stock market investors monthly than most countries have in total.

The COVID catalyst reveals a fundamental truth about India's economic transformation. Given the tools—smartphones, cheap data, simple apps—Indians don't just participate in capitalism; they embrace it with extraordinary enthusiasm. CDSL isn't just benefiting from this trend; they're enabling it. Every account they open is a vote for India's economic future.

As 2022 ends, CDSL's transformation is complete. The "boring" back-office utility is now a high-growth technology platform. The perpetual second-place player has become the dominant market leader. The BSE subsidiary is now worth more than many banks. And we're still in the early innings of India's financialization story.

VI. Market Share Wars & Competitive Dynamics (2022–Present)

The boardroom at NSDL headquarters erupts in celebration on August 6, 2025. After nearly three decades as a private entity, India's pioneering depository finally lists on the exchanges at ₹800 per share. The irony isn't lost on anyone—NSDL, which enabled thousands of companies to go public, has taken 29 years for its own IPO. Meanwhile, their younger rival CDSL has been public for eight years and commands a market cap nearly double NSDL's debut valuation.

CDSL's market share in demat accounts increased to 78% from 74% in September 2023, a dominance that seemed impossible just five years ago. The numbers tell a David-and-Goliath story with a stunning reversal. NSDL's market share fell to 22% in September from 26% in the previous year. But this isn't just about percentages—it's about fundamentally different strategies colliding in India's fastest-growing financial market.

The competitive dynamics between CDSL and NSDL reveal a masterclass in market positioning. While NSDL focused on institutional clients and high-value accounts—a sensible strategy given their NSE parentage—CDSL quietly built the rails for retail revolution. In FY2024, India saw a significant increase in demat accounts with an average of 30 lakh additions monthly, and CDSL captured the lion's share of this growth.

The technology stack differences prove decisive. CDSL's APIs, designed for high-frequency, small-value transactions, perfectly match the needs of discount brokers. When Zerodha needs to onboard 100,000 accounts in a day, CDSL's infrastructure handles it seamlessly. When Groww wants real-time account opening with video KYC, CDSL's systems deliver. This isn't accidental—it's the payoff from two decades of betting on retail when retail didn't exist.

The broker dynamics tell the real story. Groww posted a 3.8 percent MoM increase in its client count to 95 lakh with a 50 basis points rise in market share to 23.4 percent. These new-age brokers overwhelmingly choose CDSL. Why? Lower costs, better APIs, faster integration, superior support. NSDL's institutional focus, once an advantage, becomes a liability in the age of retail democratization.

With a 77% market share of demat accounts as of June 2024, CDSL enjoys a dominant position in this space. But market share alone doesn't capture the strategic moat CDSL has built. As of June 2025, CDSL manages 15.9 crore demat accounts, with around 80% market share. Simply, 8 out of every 10 investors have their demat accounts with CDSL.

The financial implications are staggering. Every new demat account generates recurring revenue—account maintenance charges, transaction fees, corporate action charges. With 88% market share in new account additions, CDSL essentially owns the future revenue stream of India's capital markets. It's like owning 88% of new mobile connections in a country transitioning from landlines to cell phones.

NSDL's upcoming IPO in 2025 adds another layer of complexity. NSDL IPO bidding started from Jul 30, 2025 and ended on Aug 1, 2025. The shares got listed on BSE on Aug 6, 2025. The IPO valued NSDL at ₹16,000 crores, substantial but still below CDSL's market cap which has soared past ₹30,000 crores.

The contrast in valuations reflects market perception of future growth. NSDL is bigger by value in demat accounts, as of June 2025, it holds ₹511 lakh crore worth of demat assets, compared to CDSL's ₹79 lakh crore. But CDSL has a wider investor base with over 15.9 crore demat accounts, almost 4 times more than NSDL. NSDL holds more value, but CDSL holds more customers—and in a network effects business, customers eventually drive value.

The operational metrics reveal CDSL's efficiency advantage. In terms of revenue, NSDL generated 31% higher revenue than CDSL; however, when it comes to profits, CDSL is more efficient. CDSL made ₹48.6 from every ₹100 rupee of revenue while NSDL made just ₹22.4 in FY25. This isn't just about cost control—it's about operating leverage at scale. CDSL's infrastructure, built for millions of small accounts, generates higher margins as volumes explode.

The accessibility factor cannot be ignored. CDSL has cultivated relationships with 581 depository participants compared to NSDL's 296. These DPs—brokers, banks, financial advisors—are the distribution network. More DPs mean more touchpoints, more account openings, deeper penetration into India's vast geography. It's the difference between having stores in metro cities versus having kiosks in every small town.

The strategic implications extend beyond market share. CDSL's dominance in retail gives them unprecedented data on investor behavior. They know what stocks retail investors buy, when they panic sell, how they respond to IPOs. This data, properly anonymized and analyzed, becomes invaluable for regulators, researchers, and market participants. CDSL isn't just infrastructure; they're becoming the Bloomberg of retail investor intelligence.

Looking forward, the competitive dynamics seem set but not settled. The new accounts opened reached 44 lakh in September 2024, suggesting the retail boom continues unabated. NSDL's IPO provides capital for innovation and expansion, but changing market share in a network effects business proves extraordinarily difficult. Once brokers integrate with CDSL, once investors get comfortable with CDSL's interface, switching costs become prohibitive.

The international comparison provides context. In most developed markets, securities depositories are monopolies or quasi-monopolies. The U.S. has DTC, Europe has Euroclear and Clearstream. India's duopoly structure creates competition but also complexity. The market has essentially voted—CDSL for retail, NSDL for institutional. Whether this segmentation remains stable or one player eventually dominates completely remains the billion-dollar question.

As we transition to examining CDSL's expansion beyond core depository services, remember this: market share in infrastructure businesses is destiny. CDSL's 78% share of demat accounts isn't just a number—it's a generational moat that compounds daily.

VII. Beyond Depositories: Subsidiaries & New Ventures

The conference room at CDSL Ventures Limited buzzes with energy unusual for a subsidiary of a financial infrastructure company. The team isn't discussing settlement cycles or corporate actions—they're architecting India's digital identity layer. What started as a small KYC subsidiary has quietly become one of India's largest identity verification platforms, processing millions of checks daily for everyone from cryptocurrency exchanges to dating apps.

CDSL's expansion beyond depositories began with a simple observation: if you're already verifying identities for stock market investors, why not verify them for everyone else? In 2018, CDSL Ventures Limited (CVL) launched as India's first SEBI-registered KYC Registration Agency. The timing proved perfect—just as India's digital economy exploded, every fintech startup needed KYC services.

The numbers reveal stunning growth. CVL's KYC database now exceeds 30 million investors, making it one of India's largest repositories of verified financial identities. But the real innovation isn't size—it's interoperability. Complete KYC once with any SEBI-registered intermediary, and CVL ensures you never need to do it again. It's the "login with Google" of Indian finance.

The business model brilliance becomes apparent when you examine the unit economics. KYC verification costs CVL roughly ₹10-15 per user for initial verification. They charge intermediaries ₹50-150 depending on volume and service level. But here's the kicker: once verified, that identity generates recurring revenue through repeated checks, updates, and cross-selling opportunities. A one-time cost becomes a lifetime revenue stream.

The subsidiary strategy extends beyond KYC. In 2017, CDSL Insurance Repository Limited (CIRL) began operations, bringing the dematerialization playbook to insurance. Just as CDSL eliminated physical share certificates, CIRL eliminates physical insurance policies. Your life insurance, health coverage, motor policy—all stored electronically, accessible instantly, claims processed digitally.

The insurance repository might seem like a minor business, but consider the TAM (Total Addressable Market). India has over 50 crore insurance policies. Less than 5% are currently in electronic form. As insurance penetration grows and digitization accelerates, CIRL stands to capture value from one of India's largest financial markets. It's CDSL's demat story, just 20 years later and in a different asset class.

The technology services division represents CDSL's transformation from infrastructure provider to platform company. They now offer white-label solutions for depositories in emerging markets. Nepal Stock Exchange signed an agreement for CDSL to establish their national depository. Bangladesh, Sri Lanka, and several African nations are in discussions. CDSL isn't just running India's market infrastructure—they're exporting it.

The API ecosystem deserves special attention. CDSL has opened up its infrastructure through carefully designed APIs that third parties can integrate. Want to verify if someone owns shares? There's an API for that. Need to check insurance holdings? API. Verify KYC status? API. Each API call generates microtransactions—tiny fees that aggregate into substantial revenue.

The venture into commodity repositories through CCRL (CDSL Commodity Repository Limited) targets another massive market. As India's commodity derivatives market matures, electronic warehouse receipts become critical. Farmers storing grain, traders holding metals, importers managing inventory—all need digital proof of ownership. CCRL provides the infrastructure, leveraging CDSL's two-decade expertise in dematerialization.

But the most intriguing expansion might be CDSL's quiet move into government securities and bonds. As retail participation in government bonds increases—driven by apps like RBI's Retail Direct—CDSL positions itself as the infrastructure layer. Every retail investor buying government securities needs depository services. CDSL already has the accounts, the relationships, the trust.

The platform strategy reveals itself through these expansions. CDSL isn't just diversifying revenue—they're creating an ecosystem where each service reinforces others. Your demat account becomes your KYC source. Your KYC enables insurance purchases. Your insurance holdings integrate with wealth management platforms. It's the "super app" approach applied to financial infrastructure.

The margin profile of these subsidiaries is even more attractive than the core business. KYC services operate at 60%+ EBITDA margins. Insurance repository enjoys similar economics. Technology services are essentially pure margin after initial development. These aren't capital-intensive manufacturing subsidiaries—they're asset-light, software-driven, network effects businesses.

The competitive moat deepens with each subsidiary. A new entrant can't just compete with CDSL's depository services—they'd need to replicate the entire ecosystem. The KYC database, insurance repository, commodity platform, API infrastructure—each element protects and enhances the others. It's not a moat; it's a series of concentric moats.

Risk management across subsidiaries shows sophisticated thinking. No single subsidiary contributes more than 15% of consolidated revenue. If insurance digitization slows, KYC continues growing. If commodity markets struggle, government securities compensate. The portfolio approach provides resilience while maintaining growth optionality.

Looking ahead, CDSL's subsidiary strategy positions them for India's next phase of financialization. As cryptocurrencies get regulated, CDSL's KYC infrastructure becomes essential. As carbon credits trade, CDSL can provide registry services. As intellectual property gets tokenized, CDSL offers the platform. They're building infrastructure for financial assets that don't yet exist.

The international expansion through technology services could become a significant growth driver. Emerging markets worldwide need depository infrastructure. CDSL's proven technology, operational expertise, and cost-effective solutions position them as the default choice. Imagine CDSL powering depositories across South Asia, Africa, and Latin America—a ₹1,000 crore opportunity conservatively.

VIII. Playbook: Business & Investing Lessons

Step back from the numbers and the narrative, and CDSL's journey reveals timeless principles about building enduring businesses in regulated markets. This isn't just a story about one company riding India's retail boom—it's a masterclass in strategic patience, operating leverage, and the power of being perfectly positioned when lightning strikes.

Lesson 1: Network Effects in Financial Infrastructure Are Different

Traditional network effects—like social media or marketplaces—are immediate and visible. Financial infrastructure network effects are slow, subtle, but ultimately more powerful. Every demat account CDSL opens makes their platform more valuable to brokers. Every broker integration makes them more attractive to investors. Every investor makes them more important to issuers. It's a flywheel that took 20 years to start spinning but now seems unstoppable.

The key insight: financial infrastructure network effects are regulatory-enhanced. SEBI rules require interoperability, but they also create switching costs. Once a broker integrates with CDSL's systems, trains staff on their platforms, and builds processes around their APIs, switching to NSDL requires enormous effort for marginal benefit. The network effect isn't just economic—it's operational inertia at scale.

Lesson 2: The Power of Being Second

CDSL's late entry, initially seen as a disadvantage, became their greatest strategic asset. They watched NSDL struggle with technology choices, learned from their regulatory battles, understood their pricing mistakes. Being second meant CDSL could optimize where NSDL pioneered.

But the real advantage was positioning. NSDL, as first mover, naturally focused on the obvious market—large institutions with immediate needs. CDSL was forced to find a different angle, betting on retail when retail barely existed. Sometimes the best strategy isn't being first to market but being first to the right market.

Lesson 3: Timing the Market vs. Time in the Market

CDSL spent two decades building infrastructure for a boom that hadn't arrived. They were "too early" by any reasonable measure. But when COVID catalyzed retail participation, CDSL wasn't scrambling to build capacity—they had it ready. The lesson isn't about predicting timing but about being prepared whenever the timing arrives.

This patience required extraordinary discipline. Through the 2008 crisis, the 2013 taper tantrum, multiple market crashes—CDSL kept investing in retail infrastructure. Most companies would have pivoted, but CDSL understood a fundamental truth: in infrastructure businesses, you build for the inevitable, not the immediate.

Lesson 4: Low-Cost Leadership in Regulated Markets

CDSL's pricing strategy deserves its own business school case. In a regulated duopoly, you can't compete on product features—both depositories offer essentially identical services mandated by SEBI. CDSL chose to compete on price, but not through unsustainable price wars. Instead, they built a structurally lower cost base through technology choices and operational efficiency.

The master stroke was partnering with discount brokers early. Zerodha, Groww, Upstox—these platforms needed rock-bottom costs to offer free equity delivery trades. CDSL provided those costs, betting that volume would compensate for lower unit economics. When volumes exploded 10x, the bet paid off spectacularly.

Lesson 5: Capital Allocation Excellence

CDSL remains virtually debt-free despite massive growth. They've funded expansion entirely through internal accruals. No dilutive equity raises, no expensive debt, no complex financial engineering. This isn't financial conservatism—it's recognition that infrastructure businesses with regulatory moats don't need financial leverage.

The capital allocation priorities reveal strategic clarity: technology first, geographic expansion second, acquisitions rarely. They've returned excess capital to shareholders through dividends while maintaining growth investments. It's the Buffett playbook applied to Indian market infrastructure.

Lesson 6: Platform vs. Product Thinking

CDSL evolved from product company (depository services) to platform company (financial infrastructure ecosystem). The transition wasn't planned—it emerged from recognizing that their core asset wasn't technology or operations but trust and relationships.

Once millions trust you with their wealth, extending that trust to adjacent services becomes natural. KYC, insurance, commodities—all leverage the same trust infrastructure. It's why Amazon could move from books to everything, why Google could move from search to workspace. Trust, once earned at scale, becomes a platform for expansion.

Lesson 7: The Operating Leverage Miracle

CDSL's financial statements from 2020-2024 should be required reading for anyone studying operating leverage. Revenue grew 3x, but profits grew 5x. Margins expanded from 30% to 50%+. ROE exceeded 30%. This isn't financial engineering—it's the natural mathematics of high fixed-cost businesses hitting scale.

The lesson extends beyond finance. Every business has potential operating leverage hiding somewhere. The question is whether you can survive long enough and grow fast enough to realize it. CDSL survived two decades of suboptimal scale to hit the inflection point. Most businesses give up far earlier.

Lesson 8: Regulatory Moats Are Real Moats

In technology businesses, moats are fragile—subject to disruption, innovation, paradigm shifts. Regulatory moats are different. They're not impervious, but they're incredibly durable. New entrants can't simply raise venture capital and blitzscale. They need regulatory approval, years of compliance history, and stakeholder trust.

CDSL's duopoly with NSDL might seem vulnerable to disruption, but consider the requirements for a third depository: SEBI approval, technology infrastructure, integration with every broker and exchange, trust from millions of investors. The barriers aren't just high—they're multiplicative. Each barrier reinforces others.

Lesson 9: The Democratization Dividend

CDSL's biggest insight was recognizing that democratization of financial services wasn't just morally important but economically massive. They bet that millions of small accounts would ultimately prove more valuable than thousands of large accounts. This wasn't obvious—institutional finance has traditionally been more profitable than retail.

But democratization changes unit economics. When account opening drops from ₹500 to ₹50, when transactions cost paisa not rupees, when services are automated not manual—suddenly serving millions becomes not just possible but profitable. CDSL built for this future before the technology fully enabled it.

Lesson 10: Compound Effects in Subscription Businesses

Each demat account CDSL opens is essentially a subscription—generating annual maintenance fees, transaction charges, and corporate action fees for potentially decades. A 25-year-old opening an account today might remain a customer for 50+ years. The lifetime value is enormous.

This subscription dynamic creates compound effects. Not only does CDSL add 30-40 lakh new "subscriptions" monthly, but existing subscriptions appreciate in value as customers trade more, accumulate more wealth, and use more services. It's SaaS economics applied to financial infrastructure—predictable, scalable, compounding.

These lessons converge into a simple but powerful framework: identify inevitable trends, build infrastructure ahead of demand, maintain cost leadership, expand thoughtfully into adjacencies, and let operating leverage work its magic. CDSL didn't invent any of these principles, but their execution demonstrates mastery.

IX. Analysis & Bear vs. Bull Case

The investment committee room fills with tension as analysts debate CDSL's valuation. At 60x P/E, the stock prices in perfection. Bulls see a generational compounding story just beginning. Bears see unsustainable growth rates and increasing competition. Both sides marshal compelling evidence. Let's examine their arguments with the rigor this decision deserves.

The Bull Case: The Financialization of India Has Just Begun

Bulls start with a simple observation: India has 150 million demat accounts for a population of 1.4 billion. The U.S. has 100 million brokerage accounts for 330 million people. Adjusting for demographics and income, India should have 400-500 million demat accounts at maturity. CDSL, with 78% market share, will capture most of this growth.

The math is seductive. The new accounts opened reached 44 lakh in September 2024, suggesting an annual run rate of 5 crores new accounts. At this pace, India reaches 300 million accounts by 2030. If CDSL maintains even 70% share and generates ₹100 per account annually, that's ₹2,100 crores in revenue from demat alone—triple current levels.

But bulls don't stop at demat accounts. They see CDSL as the AWS of Indian finance—invisible infrastructure that becomes more essential as the economy digitizes. Every mutual fund purchase, every bond trade, every insurance policy—all flow through CDSL's platforms. As India's household savings shift from physical to financial assets, CDSL captures value from trillions in wealth migration.

The operating leverage story remains compelling. CDSL's marginal cost of adding an account approaches zero. Their technology platform, built for 50 crore accounts, currently serves 16 crores. Every additional account is nearly pure profit. If margins are 50% at 16 crore accounts, what happens at 32 crores? Bulls project 70%+ EBITDA margins—software-like economics in a regulated utility.

The competitive dynamics favor continued dominance. Network effects strengthen daily. Broker relationships deepen. Retail investors have no reason to switch depositories. NSDL seems content with institutional focus. New entrants face impossible barriers. It's not quite a monopoly, but it's the next best thing—a dominant player in a regulated duopoly with switching costs approaching infinity.

International expansion offers optionality worth billions. If CDSL can replicate even 20% of their Indian success across South Asia and Africa, it doubles their addressable market. The technology is proven, the expertise unmatched, the brand increasingly recognized. Bulls see CDSL as India's first global financial infrastructure export.

The subsidiary businesses provide multiple expansion drivers. KYC services could become a ₹500 crore business as every Indian eventually needs identity verification. Insurance repository captures value from a ₹50 trillion market. Government securities democratization is beginning. Cryptocurrency regulation will require KYC infrastructure. Each opportunity is a call option on India's digital future.

Valuation, bulls argue, should reflect quality and growth duration. Yes, 60x P/E seems expensive, but Amazon traded at 100x for years. Quality compounds deserve premium multiples. With 30%+ ROE, negligible capital requirements, and decades of growth ahead, CDSL could be cheap at current prices. The terminal value when India's financialization matures justifies almost any entry multiple.

The Bear Case: Peak Growth, Rising Competition, Regulatory Risks

Bears begin with mean reversion—the most powerful force in finance. CDSL's recent growth is unprecedented and therefore unsustainable. Account additions will slow. Trading volumes will normalize. Margins will compress. The COVID boom was a one-time accelerant, not a new normal. Extrapolating recent growth rates is the classic investor mistake.

The competition is intensifying, not diminishing. NSDL's IPO war chest enables aggressive expansion into retail. New-age brokers might vertically integrate, building their own depository infrastructure. Blockchain technology could eventually disintermediate traditional depositories entirely. CDSL's moat is regulatory, and regulations change.

Regulatory risk looms large. SEBI could cap fees, mandate fee reductions, or require infrastructure sharing. The government might view depositories as too profitable, too concentrated, requiring intervention. With low promoter holding at 15%, CDSL lacks a powerful defender against regulatory overreach. One adverse ruling could permanently impair economics.

The retail dependency is concerning. CDSL generates most revenue from retail trading activity—inherently volatile and cyclical. When markets correct, retail investors flee. Trading volumes collapse. Account additions slow. Revenue falls faster than costs. The 2008 experience could repeat, just from a much higher base. Operating leverage works both ways.

Technology disruption is inevitable. Central Bank Digital Currencies (CBDCs) might eliminate the need for traditional depositories. Blockchain-based securities could trade peer-to-peer. Young Indians comfortable with cryptocurrency might skip traditional equity entirely. CDSL's infrastructure, built for a paper-to-digital transition, might miss the digital-to-crypto evolution.

Valuation leaves no room for error. At ₹30,000 crore market cap, CDSL is priced for perfection. Any disappointment—slower account growth, margin compression, regulatory changes—will trigger savage derating. The risk-reward is asymmetric: 50% downside if anything goes wrong, maybe 20% upside if everything goes right.

The quality of new accounts is deteriorating. Early adopters were serious investors with substantial capital. Recent accounts are younger, poorer, more speculative. They trade more but invest less. They generate transaction fees but limited custody revenue. The unit economics of serving small-town, small-ticket retail might prove challenging.

International expansion is harder than it appears. Each country has unique regulations, entrenched incumbents, and political considerations. CDSL's India playbook might not translate. The Nepal project remains small after years of effort. Technology export is a nice narrative but unlikely to move the needle financially.

The Verdict: A Wonderful Business at a Worrisome Price

Both bulls and bears are right—CDSL is a phenomenal business trading at a precarious valuation. The company enjoys competitive advantages that would make Buffett salivate: regulatory moats, network effects, capital-light growth, recurring revenues. But the stock price assumes these advantages persist forever and growth barely decelerates.

The resolution might be time arbitrage. Short-term investors should probably avoid CDSL—too much execution risk, valuation risk, and market risk. But long-term investors thinking in decades, not quarters, might find CDSL attractive even at current prices. If India's financialization story plays out over 20 years, today's valuation becomes a rounding error.

The smart approach might be systematic accumulation during corrections. CDSL's stock is volatile—it fell 40% in 2022 before rallying 100%. Patient investors who buy during pessimism and hold through optimism will likely compound wealth significantly. The business quality justifies owning it; the valuation suggests waiting for better entry points.

Ultimately, CDSL represents a bet on India's economic transformation. If India becomes a $10 trillion economy with developed capital markets, CDSL will be worth multiples of current valuation. If India's growth disappoints or financialization stalls, CDSL will struggle. It's not just an investment in a depository—it's an investment in India's capitalist future.

X. Epilogue & "If We Were CEOs"

Picture India in 2035. The country has just become the world's third-largest economy. The Sensex trades at 200,000. India has 500 million demat accounts—more than America and Europe combined. At the center of this transformed landscape sits CDSL, now processing a billion transactions daily, holding ₹500 trillion in assets, powering not just India's markets but emerging economies worldwide.

This isn't fantasy—it's trajectory. The question isn't whether India's capital markets will grow but how fast and who captures the value. If we were running CDSL, here's how we'd position for this future while managing present risks.

First Priority: Technology Infrastructure for the Next Billion

The current platform, impressive as it is, won't scale to 50 crore accounts. We'd invest aggressively in cloud-native architecture, artificial intelligence, and quantum-resistant security. Not incremental improvements but fundamental reimagination. Think AWS-level infrastructure—infinitely scalable, globally distributed, practically indestructible.

We'd build AI systems that predict and prevent settlement failures, detect fraud before it happens, and personalize services for each investor. Imagine an AI assistant that helps rural investors understand corporate actions, alerts them to better investment options, and educates them about risk—all in their local language. Technology shouldn't just process transactions; it should democratize sophistication.

Second Priority: The Super App Strategy

CDSL touches every Indian investor but remains invisible. We'd change that. Launch a direct-to-consumer platform—"CDSL Direct"—offering consolidated views of all holdings, intelligent analytics, and value-added services. Not competing with brokers but complementing them.

The platform would aggregate everything: stocks, mutual funds, bonds, insurance, pension, gold, and eventually crypto. One dashboard showing complete net worth. One login for all financial services. One source of truth for India's wealth. The data insights alone would be worth billions.

Third Priority: International Expansion at Scale

Forget one-off deals with Nepal. We'd create "CDSL Global"—a standardized, cloud-based depository solution for emerging markets. Package two decades of expertise into software that deploys in weeks, not years. Target the next 20 countries beginning their financialization journey.

The model would be SaaS, not consulting. Annual contracts, not one-time implementations. We'd price aggressively to capture market share, knowing that switching costs make customers sticky for decades. Imagine CDSL powering depositories across Africa, Southeast Asia, and Latin America—a ₹10,000 crore opportunity conservatively.

Fourth Priority: Vertical Integration into Wealth Management

CDSL knows more about Indian wealth than anyone except maybe the tax department. We'd leverage this intelligence responsibly to build wealth management services. Not competing with mutual funds but providing infrastructure for robo-advisors, portfolio analytics, and automated investing.

Partner with fintechs to offer "Investing as a Service"—APIs that enable any app to offer investment products. Your payment app, shopping app, even gaming app could integrate investment options powered by CDSL infrastructure. Make investing as ubiquitous as payments have become.

Fifth Priority: Blockchain Integration, Not Disruption

Rather than fear blockchain, embrace it. Build hybrid infrastructure supporting both traditional securities and tokenized assets. Create bridges between old and new systems. When security tokens eventually trade on blockchains, CDSL should provide custody, settlement, and registry services.

Launch pilot programs for tokenized real estate, art, and commodities. Build expertise before markets mature. Position CDSL as the trusted intermediary between traditional finance and crypto innovation. The future isn't blockchain or depositories—it's blockchain and depositories.

Sixth Priority: The Sustainability Play

As ESG investing explodes, CDSL could become the source of truth for sustainability metrics. Track carbon credits, verify green bonds, and authenticate sustainability claims. Build infrastructure for the coming wave of climate finance.

Create India's first comprehensive ESG database. Every listed company's environmental impact, social metrics, and governance scores—verified, standardized, accessible. Charge premium fees for ESG analytics. Capture value from the intersection of capitalism and consciousness.

Risk Management: The Shadows in Paradise

Of course, execution is everything. The biggest risk isn't competition or regulation but complacency. Market leaders often become lazy monopolists. We'd maintain startup urgency despite market dominance. Quarterly hackathons. Innovation labs. Partnerships with IITs. Keep the organization young, hungry, and paranoid.

Regulatory relationships need careful cultivation. Regular dialogue with SEBI, RBI, and the government. Proactive compliance beyond requirements. Share data insights that help regulators make better policy. Position CDSL as a partner in India's development, not just a profit-seeking corporation.

Succession planning is critical. CDSL's current leadership has delivered extraordinary results, but institutions must outlive individuals. Build deep bench strength. Rotate high-performers through subsidiaries. Create a culture where the mission matters more than any individual, including the CEO.

The Next Frontier: 50 Crore Indians as Capitalists

The ultimate vision isn't just processing transactions but transforming India into a nation of owners. Every Indian with a stake in India's growth. Every worker a shareholder. Every saver an investor. CDSL as the infrastructure enabling this ownership revolution.

Imagine auto-enrollment in equity markets, like 401(k)s in America. Every formal sector employee automatically gets a demat account, and contributes to index funds. CDSL processes everything seamlessly. Twenty years later, India has created the world's largest pool of domestic capital.

Or consider financial inclusion through innovation. Partner with India Post to open demat accounts in 150,000 post offices. Enable ₹10 investments through UPI. Create Bengali, Tamil, and Telugu interfaces. Make the stock market as accessible as a savings account.

The Surprises from Our Research

Diving deep into CDSL revealed unexpected insights. First, the company's culture is remarkably engineering-driven for a financial services firm. They think like technologists, not bankers. This explains their API-first approach and platform thinking.

Second, CDSL's data assets are vastly undermonetized. They're sitting on one of India's richest datasets—every trade, every holding, every pattern—but barely scratch the surface of potential insights. Privacy-preserving analytics could unlock enormous value.

Third, the international opportunity is larger than anyone realizes. Emerging markets collectively need depository infrastructure for $100 trillion in assets over the next decade. CDSL's proven low-cost model positions them perfectly. They could become the MongoDB of market infrastructure—ubiquitous, essential, incredibly valuable.

Final Reflections: Infrastructure for a New India

CDSL's story transcends finance. It's about building the pipes and plumbing for India's economic transformation. Every demat account opened is a vote for capitalism, a bet on India's future, a step toward prosperity. CDSL doesn't just facilitate transactions—they enable dreams.

The next decade will test whether CDSL can evolve from national champion to global platform. Whether they can maintain growth while managing complexity. Whether they can innovate while preserving stability. The challenges are immense, but so are the opportunities.

Standing at this inflection point, CDSL reminds us why infrastructure investments endure: they're boring until they're not. For twenty years, CDSL built boring infrastructure. Then COVID arrived, and boring became beautiful. The next twenty years promise even more dramatic transformation.

The depositary that democratized India's capital markets now aims to democratize ownership itself. From 2 crore accounts to 20 crores to perhaps 50 crores—each milestone marking not just business growth but national development. In enabling millions to participate in India's growth story, CDSL has become inseparable from that story itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube