Castrol India: The Liquid Engineering Empire

I. Introduction & Episode Teaser

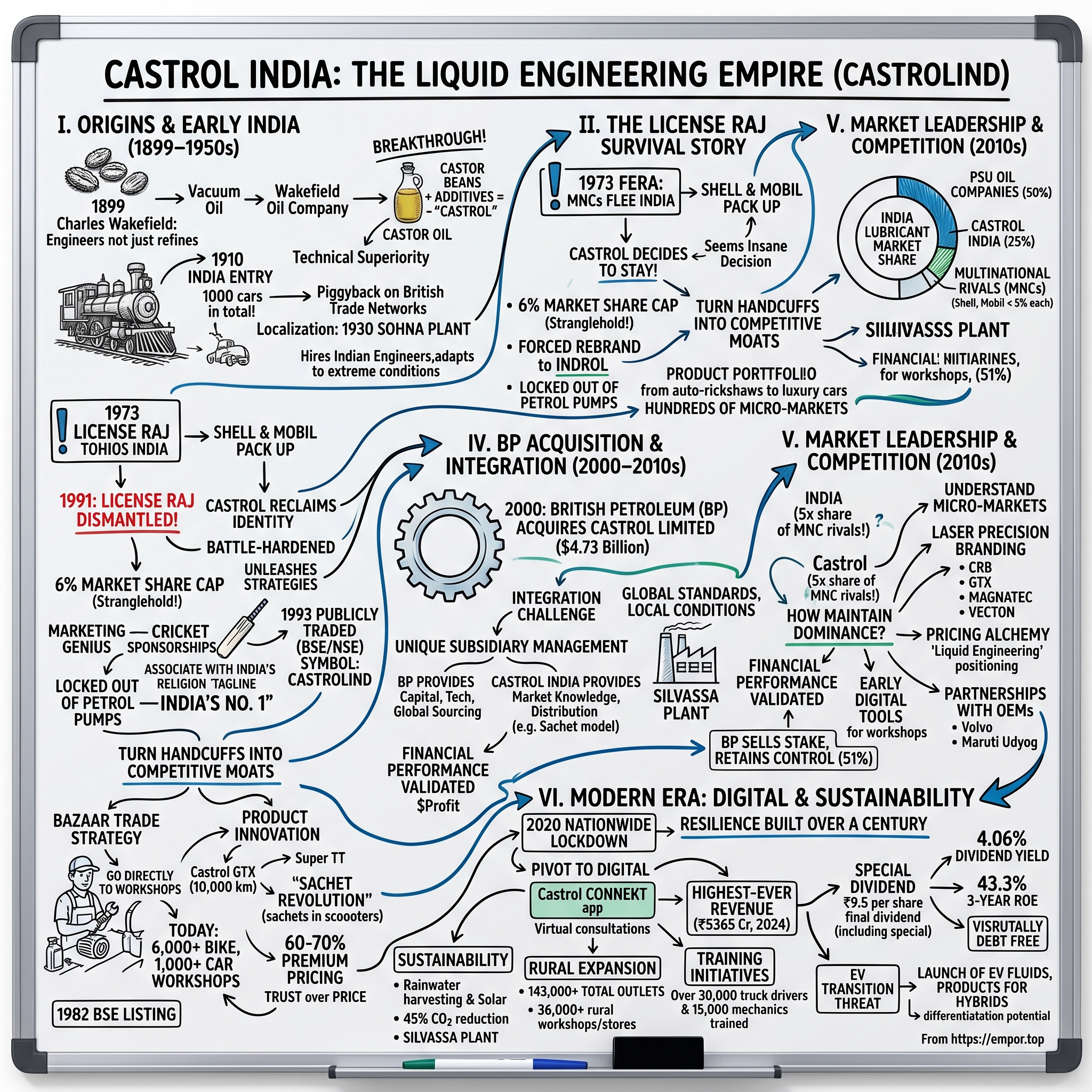

Picture this: It's 1979, and multinational corporations are fleeing India en masse. The License Raj has made it nearly impossible for foreign companies to operate profitably. Shell packs up. Mobil shuts down. But in a cramped office in Mumbai, executives at a British lubricants company make a decision that would seem insane to any rational business strategist—they decide to stay. Not just stay, but rebrand entirely, accept a government-mandated 6% market share cap, and somehow try to build a business in one of the world's most restrictive regulatory environments.

That company was Castrol, and that seemingly irrational decision would eventually create India's most dominant premium lubricants brand, commanding 20% market share and generating ₹5,365 crore in revenue by 2024. Today, Castrol India stands as the second-largest manufacturer of automotive and industrial lubricants in a market where 50% is controlled by state-owned petroleum giants with built-in distribution advantages through their petrol pumps.

The question isn't just how a foreign subsidiary survived when others fled—it's how they turned regulatory handcuffs into competitive moats, transformed vegetable oil experiments into premium pricing power, and built emotional connections with Indian consumers that transcended product categories. This is a story about patience, about the power of staying when everyone else leaves, and about how sometimes the worst business environments create the most durable competitive advantages.

What makes Castrol India particularly fascinating for investors is its financial DNA: virtually debt-free operations, 43% gross margins in a commodity-like business, and a return on equity that has averaged 43.3% over the past three years. Yet the stock trades with a dividend yield of 4.06%, suggesting the market either doesn't fully appreciate the moat or sees storm clouds ahead in the form of electric vehicles.

We're about to trace a century-long journey from London's Cheapside district to India's 143,000 retail outlets, from castor beans to cricket sponsorships, from forced rebranding to market leadership. Along the way, we'll uncover how a company that was literally prohibited from growing beyond 6% market share engineered its way to dominance, and what that means for understanding competitive dynamics in emerging markets.

II. Origins: The Wakefield Legacy & Early India Entry (1899–1950s)

The year was 1899, and Charles Wakefield had just made a decision that would ripple through industrial history. Walking away from a comfortable position at Vacuum Oil, he set up shop in London's Cheapside district with a radical idea: what if lubricants could be engineered, not just refined? His Wakefield Oil Company started by focusing on the unglamorous world of train and heavy machinery lubrication, but Wakefield understood something his competitors didn't—lubricants weren't just about reducing friction; they were about precision engineering.

The breakthrough came from an unexpected source: castor beans. Wakefield's researchers discovered that adding carefully measured amounts of castor oil—a vegetable derivative—to their formulations created lubricants with unprecedented performance characteristics. The viscosity remained stable across temperature ranges that would cause petroleum-based oils to break down. They called it "Castrol," a portmanteau that would become synonymous with premium lubrication worldwide. What seemed like a simple naming convention was actually a declaration of technical superiority—this wasn't just oil; it was engineered liquid.

By 1910, something remarkable was happening 7,000 miles away. India, still under British colonial rule, was experiencing its first automotive revolution. The maharajas were importing Rolls-Royces, the British administrators needed vehicles for the vast subcontinent, and a nascent industrial base was emerging in Bombay and Calcutta. Wakefield saw opportunity where others saw only colonial extraction. In 1910, Castrol India started importing certain automotive lubricants from C C Wakefield & Company made an entry in the Indian market. This wasn't just another colonial commercial venture—it was a bet on an India that didn't yet exist. In those days, all of India had just about 1,000-odd cars. Think about that for a moment: the entire subcontinent had fewer automobiles than a modern Mumbai apartment complex has parking spots.

Yet Wakefield saw something others missed. The British Raj had inadvertently created the infrastructure for automotive growth—roads connecting major cities, railways that would need industrial lubricants, and a nascent class of Indian industrialists who would drive modernization. "About 100 years ago, nobody would have believed that India could become one of the largest automobile markets, but C.C. Wakefield had that foresight," says Ravi Kirpalani, Managing Director, Castrol India.

The early distribution strategy was ingenious in its simplicity. Rather than setting up expensive infrastructure, Castrol piggybacked on existing British trading networks. They partnered with managing agencies—those peculiar colonial institutions that controlled everything from tea plantations to textile mills. These agencies already had relationships with the maharajas, the British administrators, and the emerging Indian business class. Castrol lubricants arrived alongside Scotch whisky and English textiles, but unlike those products, they were essential for the machines that would build modern India.

By the 1920s, something remarkable was happening. Indian entrepreneurs weren't just buying foreign cars—they were setting up transport companies, mechanizing agriculture, and building factories. Each new machine needed lubrication, and Castrol was there. They didn't just sell oil; they sold reliability in a market where a breakdown could mean disaster. The premium pricing that would later become Castrol's hallmark was already emerging—Indian customers were willing to pay more for products that wouldn't fail them.

The real genius was in localization before anyone called it that. By 1930, Castrol had established its first manufacturing plant in India, located in Sohna, Haryana. This wasn't just about reducing import costs—it was about commitment. While other foreign companies treated India as a market to exploit, Castrol was putting down roots. They hired Indian engineers, trained Indian workers, and began adapting their formulations to Indian conditions—the extreme heat, the dust, the monsoons that turned roads into rivers.

World War II changed everything. Suddenly, lubricants weren't just commercial products—they were strategic resources. The British military machine in Asia ran on oil, and Castrol's Indian operations became critical to the war effort. This period saw massive expansion of technical capabilities and distribution networks. By 1947, when India gained independence, Castrol wasn't seen as a foreign interloper but as part of India's industrial fabric.

The partition of India in 1947 could have destroyed the company. Overnight, carefully built distribution networks were severed, key personnel were displaced, and the new governments were suspicious of anything British. But Castrol made a crucial decision: they didn't retreat to the safety of urban markets. Instead, they doubled down on building relationships with the new Indian industrialists who would drive the country's development. They understood that independent India would need lubricants more than colonial India ever did.

III. The License Raj Survival Story (1960s–1980s)

The letter arrived on a humid Bombay morning in 1973. The Foreign Exchange Regulation Act (FERA) had been passed, and foreign companies had two choices: dilute your stake to 40% or leave India. For Castrol's British parent company, it must have seemed like commercial suicide. Castrol had to reduce its stake in its Indian operations to 40 per cent and also re-brand itself under a new name, Indrol. Imagine being forced to abandon the brand name you'd spent six decades building.

"We were not allowed to have more than six per cent market share, and this was the time many MNCs closed shop in India and left, but we decided to stay put. This unbroken run of 100 years has got us the success," says Kirpalani. That 6% market share cap wasn't just a number—it was a stranglehold. The government's logic was perverse but clear: foreign companies shouldn't dominate Indian markets. The fact that Indian consumers wanted their products was irrelevant to the socialist planners in Delhi.

While competitors saw insurmountable obstacles, Castrol's management saw a chess game. If you can't grow market share, you grow market value. If you can't use your global brand, you build local emotional equity. If you can't sell at petrol pumps, you create new distribution channels. In 1979, CIL was incorporated under the name of Indrol Lubricants and Specialities Pvt Ltd. The name change wasn't just cosmetic—it was a complete reimagining of how a lubricants company could operate.

The masterstroke was the bazaar trade strategy. The new guidelines also prevented Castrol lubricants from being sold at traditional retail points - the fuel stations which were owned by the national oil companies. Locked out of petrol pumps, Castrol went directly to where vehicles were actually serviced. Datta is referring to the company's bazaar trade strategy, where it partnered with car and bike workshops across the country to sell its lubricants.

Think about the audacity of this move. Every competitor was fighting for shelf space at petrol pumps, assuming that's where lubricants had to be sold. Castrol said: "What if we're there when the customer actually needs us?" They recruited mechanics as brand ambassadors, turned workshops into retail points, and created a distribution network that no competitor could replicate. Today, there are over 6,000 Castrol-branded bike workshops and 1,000 car workshops in India.

The product innovation during this period was remarkable given the constraints. Identifying new retail windows was accompanied by the launch of new products as well, such as Castrol GTX, which enabled a vehicle to run for 10,000 km without changing the lubricant, and Super TT, a lubricant for two-wheelers. In a market where consumers were price-conscious but quality-obsessed, Castrol positioned itself as the premium choice that actually saved money in the long run.

But the real innovation was the sachet revolution. It launched 40 ml sachets of Super TT. "Consumers would buy sachets in bulk and keep them in their scooters and bikes, and at fuel stations they would use their sachets instead of buying a lubricant available there. This strategy was a huge hit," says Kirpalani. This wasn't just clever packaging—it was guerrilla warfare against the distribution monopoly. Consumers literally carried Castrol in their vehicles, bypassing the PSU-controlled petrol pumps entirely.

"Our products were priced at a 60 to 70 per cent premium compared with the competition, but the demand was tremendous as the brand equity was already built," says Ram Savoor, former MD of Castrol India. A 60-70% premium in a price-sensitive market should have been commercial suicide. Instead, it became Castrol's moat. They weren't selling lubricant; they were selling trust, performance, and status.

It was listed on BSE in 1982 and CIL was converted into a public limited company. Going public during the License Raj was unusual for a foreign subsidiary, but it served multiple purposes: it satisfied government requirements for local ownership, created a class of Indian shareholders who would champion the company, and provided capital for expansion within the regulatory constraints.

The numbers tell a story of patient capital and operational excellence. Despite being restricted to 6% market share, Castrol maintained margins that would make modern software companies envious. They did this through relentless focus on premium segments, operational efficiency that bordered on obsession, and a distribution strategy that turned regulatory constraints into competitive advantages.

IV. Liberalization & Renaissance (1990s–2000)

July 24, 1991. Finance Minister Manmohan Singh stands in Parliament and announces the dismantling of the License Raj. For most companies, this was liberation. For Castrol, it was vindication. On 1 November 1990, the name of the company was changed from Indrol Lubricants & Specialities Ltd. They could finally reclaim their identity, but more importantly, they could unleash strategies they'd been perfecting in the shadows for over a decade.

The company that emerged from the License Raj was battle-hardened in ways its new competitors couldn't understand. While Shell and Mobil scrambled to re-enter India, Castrol had never left. They had relationships with 6,000 workshops, brand equity with millions of consumers, and institutional knowledge that money couldn't buy. "Attempting tasks where the chances of success are improbable, says Kirpalani, was always in the DNA of Castrol India. The first improbable achievement was creating an emotional connect with a lubricant brand, but we managed to do it," he says.

The 1990s saw Castrol's marketing genius fully unleashed. They didn't just advertise; they created cultural moments. Cricket sponsorships weren't just about visibility—they were about associating Castrol with India's religion. When Sachin Tendulkar hit a six, Castrol was there. When India won a match, Castrol celebrated with them. The tagline "Castrol—India's No. 1" wasn't just a claim; it was a declaration of belonging.

In 1993, the company became a publicly-traded entity on the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) under the symbol CASTROLIND. The public listing was strategic—it created liquidity for early investors, provided growth capital, and most importantly, deepened Castrol's roots in India. They weren't just operating in India; they were an Indian company with British DNA.

The product portfolio exploded during this period. From basic engine oils, Castrol expanded into specialized formulations for everything from auto-rickshaws to luxury cars. They understood that India wasn't one market but dozens of micro-markets, each with unique needs. The same company selling premium synthetic oils to BMW owners was creating products for rural transporters who needed their trucks to survive 50,000 kilometers of Indian highways.

Distribution expanded from thousands to tens of thousands of outlets. But this wasn't just about numbers—it was about creating a pull strategy so powerful that retailers demanded Castrol products. The workshop strategy from the License Raj era became the foundation for market dominance. Every mechanic became a Castrol salesman, every service center a Castrol showcase.

The financial performance during this period was staggering. Revenues grew at double-digit rates, margins expanded despite increased competition, and return on capital employed reached levels that attracted global attention. This wasn't supposed to happen—economic theory said that liberalization should compress margins as competition increased. Instead, Castrol proved that brand equity and distribution moats could create pricing power that defied gravity.

Technology transfer accelerated as Castrol could finally leverage its global R&D without regulatory restrictions. Products developed for Formula One found their way into Indian motorcycles. Innovations from British Petroleum's labs were adapted for Indian conditions. This wasn't just importing technology—it was creating a two-way innovation highway where Indian insights influenced global product development.

V. The BP Acquisition & Global Integration (2000–2010)

The fax machine in Castrol's London headquarters churned out the announcement on March 18, 2000: British Petroleum would acquire Castrol Limited for $4.73 billion. For Castrol India, this wasn't just a change in ownership—it was transformation from successful subsidiary to strategic jewel in one of the world's largest energy companies. The price tag—nearly $5 billion—validated what Indian operations had been saying for years: lubricants weren't a commodity business if you did them right.

Around the same time in England, Charles Cheers Wakefield, then an employee of Vacuum Oil (which went on to become Mobil), was planning the launch of his own automotive lubricant company. In 1899, Wakefield called it a day at Vacuum Oil, rented three small rooms on the third floor of 27th Canon Street in Central London and launched C.C. Wakefield & Co. In 1909, Wakefield registered his lubricant under the brand name Castrol - the name derived from its original base component, castor oil. But the company BP was acquiring had traveled far from those three rooms in Canon Street. Castrol had previously been through another major acquisition—In 1966, Castrol was acquired by company Burmah Oil, which was renamed "Burmah-Castrol"—but the BP deal was different in scale and ambition.

For Castrol India, the integration challenge was unique. How do you integrate with a global oil giant while maintaining the local identity that made you successful? The answer became a Harvard Business School case study in subsidiary management. BP provided capital, technology, and global sourcing power. Castrol India provided market knowledge, distribution networks, and most importantly, the template for how to succeed in emerging markets. The manufacturing footprint expansion accelerated dramatically. It has 5 manufacturing plants that are networked with 400+ distributors, serving over 70,000 retail outlets. The Silvassa plant, in particular, became a showpiece of BP's global manufacturing standards adapted for Indian conditions. This wasn't just about capacity—it was about creating a supply chain resilient enough to serve India's fragmented market while maintaining global quality standards.

Since 2000, Castrol Limited has been a subsidiary of BP, which acquired the company for $4.73 billion. The integration strategy was masterful. BP didn't try to impose a global template on India. Instead, they asked: "What can we learn from India?" The sachet strategy, the workshop distribution model, the ability to maintain premium pricing in a price-sensitive market—these became case studies for BP's emerging market strategy globally.

The technology transfer was bidirectional. BP brought advanced formulations, global R&D capabilities, and manufacturing excellence. Castrol India brought market intimacy, distribution innovation, and the ability to create emotional connections with functional products. The synthesis created products that were globally advanced but locally relevant—a sweet spot that competitors struggled to hit.

Financial performance during this decade validated the strategy. During 2015 Castrol India Ltd delivered a record performance with post-tax profit of around Rs 615 crores (US$95 million), 30% up on the previous year. For the full year 2015, net sales from operations were around Rs 3298 crores (USD$507m), profit from operations was up by 25.7% to Rs 856 crores (USD$132m). These weren't just good numbers—they were exceptional for a mature market with intense competition.

The workshop network expanded to unprecedented scale. From the 6,000 bike workshops inherited from the License Raj era, Castrol built a network that touched every corner of India. Urban, rural, tier-1 cities, tier-3 towns—wherever there was a vehicle, there was a Castrol presence. This wasn't achieved through corporate mandate but through patient relationship building, dealer financing, and technical support that made workshops partners rather than just customers.

VI. Market Leadership & Competition Dynamics (2010–2020)

The boardroom in Mumbai was tense. It was 2016, and BP was under pressure globally. Oil prices had crashed, and the parent company needed cash. The decision came down: reduce stake in Castrol India. Castrol Ltd, a wholly owned subsidiary of BP Plc, sold 8.5% equity stake in Castrol India Ltd in a block deal on Tuesday. In May this year Castrol sold 11.5% stake in Castrol India for Rs.2100 crore. As a result of the two sales, BP said, BP through Castrol now holds 51% interest in Castrol India.

For any other subsidiary, this might have been the beginning of the end. But Castrol India turned it into an opportunity. The stake sale brought in institutional investors who provided market discipline while BP retained control. As of 2023, BP plc holds a majority stake in Castrol India Limited, owning approximately 71% of the company. The company now had the best of both worlds: global backing and local market validation.

The competitive landscape during this decade was fascinating. It has a 25 per cent share of the Rs 12,000-crore lubricant industry, and is well ahead of multinational (MNC) rivals such as Mobil and Shell, who have less than five per cent share each. About 50 per cent of the market is with the PSU oil companies. Think about that—Castrol had five times the market share of its multinational competitors despite their global resources and brand recognition.

How did they maintain this dominance? The answer lay in understanding that India wasn't one lubricants market but thousands of micro-markets. The lubricant needs of a Delhi Uber driver were different from a Kerala fishing boat operator, different from a Pune factory owner. Castrol didn't just acknowledge these differences—they built products and distribution strategies around them. The product portfolio evolution was particularly sophisticated. The Company's brands include Castrol CRB, Castrol GTX, Castrol Activ, Castrol MAGNATEC and Castrol VECTON. Each brand targeted a specific segment with laser precision. MAGNATEC for premium car owners who wanted molecular protection, Activ for the vast two-wheeler market, CRB for commercial vehicles that needed durability above all else. This wasn't product proliferation—it was market segmentation executed with surgical precision.

The real genius was in pricing strategy. While PSU competitors had the advantage of selling at their own petrol pumps with minimal distribution costs, Castrol maintained premium pricing through what can only be described as brand alchemy. They turned a functional product into an emotional purchase. "It's not just oil, it's liquid engineering" wasn't just a tagline—it was a positioning that justified paying 60-70% more than alternatives.

Digital transformation began earlier than most realize. While competitors were still thinking of lubricants as a push product sold through traditional channels, Castrol was building digital tools for workshops, creating apps for consumers to track oil changes, and using data analytics to predict demand patterns. This wasn't Silicon Valley disruption—it was thoughtful digitization that enhanced rather than replaced traditional strengths.

The partnership strategy during this period was masterclass in ecosystem building. Castrol India entered a strategic partnership with Volvo Cars India in 2007, an agreement with Maruti Udyog in 1997 and other deals over the years to build customized products and services for the Indian market. These weren't just supply agreements—they were co-creation partnerships where Castrol became integral to the OEM's service strategy.

By the end of the decade, Castrol had created something remarkable: a foreign subsidiary that was more Indian than many Indian companies, a premium brand in a commodity market, a company with distribution reach that matched PSU giants but with margins that resembled software companies. The foundation was set for the next challenge—one that nobody saw coming.

VII. Modern Era: Digital Transformation & Sustainability (2020–Present)

March 23, 2020. India announces a nationwide lockdown. For a company built on physical distribution through 143,000 outlets, this should have been catastrophic. The manufacturing facilities of the company at Patalganga(Maharashtra),Silvassa(UT-DNHDD), and Paharpur(West Bengal) which were closed on 23 March 2020 following countrywide lockdown due to COVID-19,resumed operation in a phased manner from the second week of May 2020. But what happened next revealed the resilience built over a century.

Within weeks, Castrol pivoted to digital engagement at a scale that would have seemed impossible months earlier. The Castrol CONNEKT digital app, which had been a nice-to-have, suddenly became mission-critical. Workshops that had never used smartphones for business were conducting virtual consultations. The company that had built its moat on physical presence proved it could dominate digitally too. The financial resilience was remarkable. For the full year ended 31 December 2024, the Company registered Revenue from Operations of ₹5365 Crore, recording a steady growth of 6% over ₹5075 Crore in the year ended 31 December 2023. Profit Before Tax for 2024 stood at ₹1258 Crore, marking a growth of 6%. In an era of global disruption, Castrol delivered its highest-ever revenue. The company that had survived the License Raj now proved it could thrive in a pandemic.

The sustainability transformation went beyond greenwashing. Commissioned rainwater harvesting and solar power projects at its Silvassa plant, reducing CO2 emissions by 45%. This wasn't just corporate responsibility—it was strategic positioning for a world where ESG credentials would determine access to capital and customers.

Rural expansion accelerated dramatically. We also strengthened our presence in rural India, now reaching over 36,000 workshops and stores, as part of our wider network of over 143,000 outlets across the country. The company that had been forced to innovate distribution during the License Raj was now using those lessons to penetrate markets that digital-only competitors couldn't reach.

The dividend story is particularly telling. To commemorate Castrol's journey of 125 years globally and celebrate Company's strongest year in India, the board has recommended a final dividend of ₹9.5 per share (face value: ₹5 each) including a special dividend of ₹4.5 per share for the financial year ending 31 December 2024. A dividend yield of over 4% in a growth market—this is capital allocation discipline that would make Warren Buffett smile.

The training initiatives reveal long-term thinking. Trained over 30,000 truck drivers and 15,000 mechanics in 2024, empowering ~500,000 individuals since inception of CSR initiative. These aren't just CSR numbers—every trained mechanic becomes a Castrol advocate, every skilled driver a quality-conscious customer.

Product innovation continued despite—or perhaps because of—the EV transition threat. The launch of new variants including products for hybrids showed Castrol wasn't waiting for the transition; they were actively participating in it. The Essential brand targeting the middle market demonstrated that premium positioning didn't mean ignoring volume opportunities.

VIII. Playbook: Business & Investing Lessons

The Castrol India story offers a masterclass in emerging market strategy, but the lessons go far beyond geography. This is about building antifragile businesses—companies that don't just survive volatility but get stronger from it.

The Regulatory Arbitrage Play: When the government capped market share at 6%, Castrol didn't fight the regulation—they transcended it. By focusing on value share rather than volume share, they turned a constraint into a moat. The lesson: regulations that seem restrictive often create pricing power for those willing to play the long game. Today's ESG regulations might be tomorrow's competitive advantages.

Distribution as Destiny: The bazaar trade strategy wasn't just about reaching customers—it was about owning the last mile in a way that couldn't be replicated. Every workshop became a mini-franchise, every mechanic a brand ambassador. In the age of Amazon, this seems antiquated. But Castrol proved that in categories requiring trust and expertise, human distribution networks create switching costs that no algorithm can match.

Premium in Commodity Markets: Maintaining 60-70% price premiums in a market where 50% is controlled by PSUs selling at cost-plus pricing shouldn't be possible. Castrol proved that even in commodity markets, brand equity can create pricing power—but only if you're willing to invest when returns aren't immediately visible. The sachet strategy wasn't about small packaging; it was about making premium accessible without diluting premium perception.

The Subsidiary Sweet Spot: Being 51% owned by BP provided the perfect balance—access to global resources without the suffocation of complete control. Promoter Holding: 51.0% This ownership structure allowed local management to make quick decisions while having the backing of a global giant. For investors, this creates an interesting dynamic: you get the stability of a multinational with the agility of a local player.

Capital Efficiency Excellence: Company is almost debt free. Stock is providing a good dividend yield of 4.06%. Company has a good return on equity (ROE) track record: 3 Years ROE 43.3%. In a capital-intensive industry, Castrol runs an asset-light model. They don't own petrol pumps, they don't need massive working capital, and they generate returns that make software companies envious.

The Power of Staying: When Shell and Mobil left during the License Raj, they thought they were being rational. When they returned post-liberalization, they discovered that Castrol's "irrational" decision to stay had created insurmountable advantages. Sometimes the best investment is the one everyone else abandons.

IX. Analysis & Bear vs. Bull Case

Bull Case:

The India growth story is just beginning. The India Lubricants Market is expected to reach 3.01 billion Liters in 2025 and grow at a CAGR of 4.76% to reach 3.79 billion Liters by 2030. With India's vehicle population expected to double by 2030, even modest market share maintenance means substantial volume growth. Castrol's positioning to grow above market rates could deliver high-single-digit to low-double-digit volume growth.

The distribution moat is nearly impossible to replicate. With 143,000 retail touchpoints and relationships with mechanics built over decades, any competitor would need enormous capital and time to match Castrol's reach. This isn't just about outlets—it's about trust relationships in a market where personal recommendations drive purchase decisions.

Margin resilience despite commodity input costs demonstrates pricing power. We aim to maintain margins within the 22-25% range. The ability to maintain these margins while PSU competitors sell at lower prices proves that brand equity translates directly to the bottom line.

The balance sheet provides enormous flexibility. With virtually no debt and consistent cash generation, Castrol can invest counter-cyclically, acquire selectively, or return capital to shareholders. The special dividend demonstrates management's shareholder-friendly approach.

Bear Case:

The elephant in the room is electrification. EVs need 50-70% less lubricants than ICE vehicles. While the transition will take decades in India, the direction is clear. The company has delivered a poor sales growth of 6.71% over past five years—is this early evidence of structural headwinds?

PSU competition isn't going away. With 50% market share and control of fuel retail, PSU oil companies have structural advantages. As they improve quality and brand perception, Castrol's premium positioning could come under pressure.

Currency and input cost volatility remain significant risks. The company faces challenges with forex fluctuations, which could impact input costs as 50-60% of materials are imported. With limited pricing power in a competitive market, margin compression could accelerate during commodity supercycles.

Growth capital allocation questions persist. With high cash generation but slowing growth, where will incremental capital be deployed? The industrial lubricants market is fragmented and competitive, international expansion faces established players, and the EV transition requires different capabilities.

X. Epilogue & Future Outlook

The chessboard is being reset. Electric vehicles, sustainability mandates, and digital commerce are reshaping the lubricants industry in ways Charles Wakefield couldn't have imagined. Yet Castrol India's history suggests they're uniquely positioned for this transition—not despite their legacy, but because of it.

The EV transition, rather than being an existential threat, might be Castrol's next opportunity for differentiation. EV fluids—coolants, brake fluids, specialized greases—require even more sophisticated formulation than traditional lubricants. The company that turned castor oil into premium products can surely engineer solutions for electric drivetrains. Early partnerships with EV manufacturers could create the same first-mover advantages Castrol enjoyed in the ICE era.

Industrial lubricants represent an underappreciated growth vector. As India's manufacturing scales up—semiconductors, renewable energy, aerospace—specialized lubricants become critical. Castrol's ability to customize products and provide technical support positions them well for this higher-margin segment.

Digital transformation isn't about replacing physical distribution but augmenting it. Imagine IoT sensors that predict when machinery needs lubricant changes, apps that connect vehicle owners directly with Castrol-certified mechanics, or blockchain systems that guarantee product authenticity. The company that innovated with sachets in the 1970s can surely innovate with bytes in the 2020s.

Sustainability is becoming a competitive weapon. As regulations tighten and customers demand greener products, Castrol's investments in renewable energy and sustainable packaging create advantages. The 45% reduction in CO2 emissions isn't just good PR—it's operational efficiency that drops straight to the bottom line.

The broader lesson transcends Castrol or even India. In an era of disruption, the companies that survive aren't necessarily the most innovative or the most efficient. They're the ones that understand their markets deeply, build relationships that transcend transactions, and have the patience to compound advantages over decades. Castrol India didn't just survive the License Raj, the liberalization shock, the global financial crisis, and a pandemic—they used each crisis to strengthen their position.

For investors, Castrol India presents a fascinating study in risk-reward. The bear case is clear and quantifiable—EV transition, PSU competition, commodity volatility. But the bull case rests on something harder to model: the value of deep market knowledge, distribution networks, and brand equity in a market where hundreds of millions of people are entering the middle class.

Perhaps the real insight is this: in markets undergoing structural transformation, the winners aren't always the disruptors. Sometimes they're the incumbents who've learned to transform themselves continuously. Castrol India has been transforming for 115 years—from castor oil experiments to EV fluids, from colonial imports to rural sachets, from Indrol to Castrol and beyond.

The story that began with Charles Wakefield walking away from Vacuum Oil in 1899 continues to unfold. The next chapter will be written by electric vehicles, sustainability mandates, and digital transformation. But if history is any guide, Castrol India won't just adapt to these changes—they'll find ways to turn them into competitive advantages. After all, that's what liquid engineering is really about: finding elegant solutions to complex problems, one drop at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube