CARE Ratings: The Arbiters of Indian Credit

I. Introduction & The "License to Hunt"

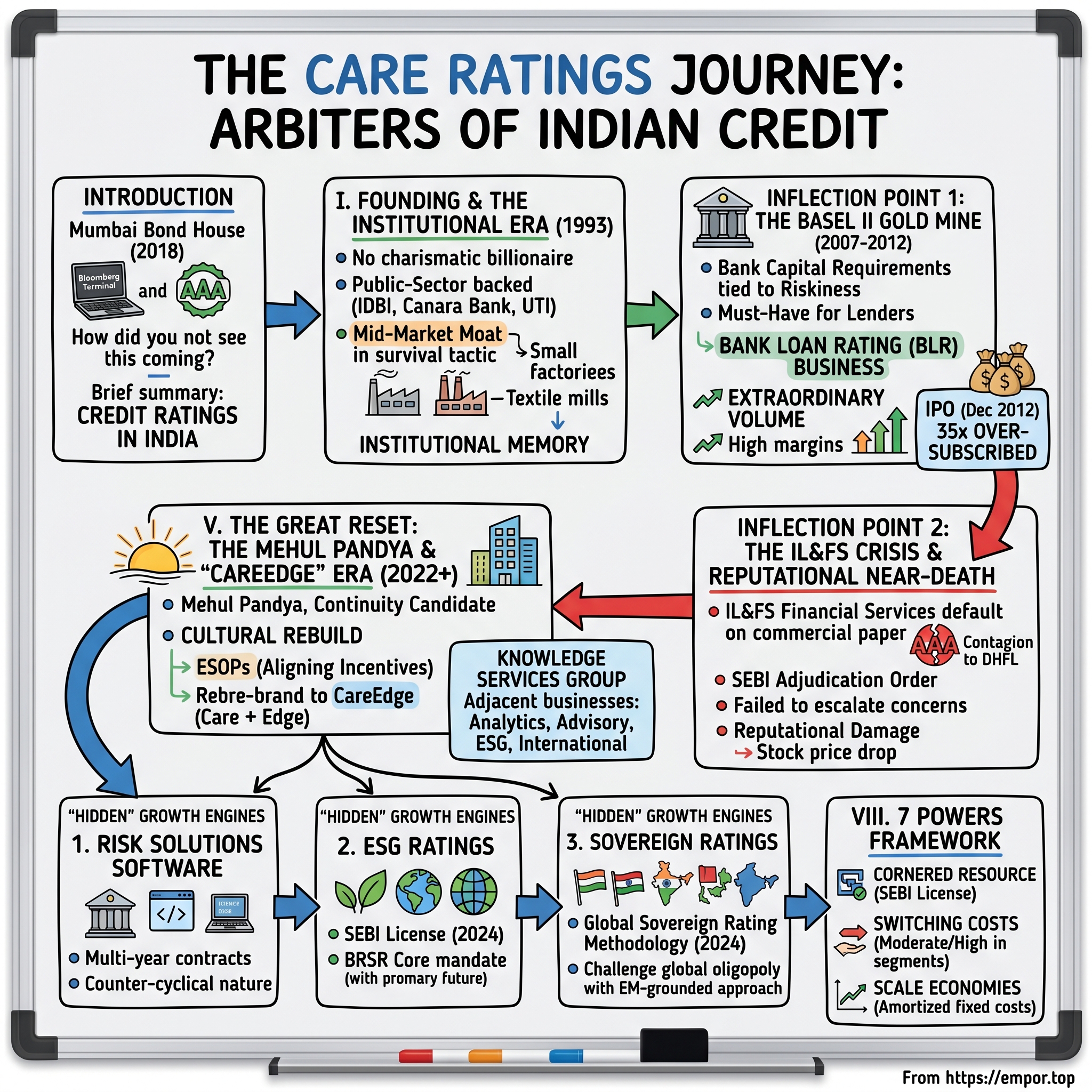

Picture the trading floor of a Mumbai bond house on a Wednesday morning in 2018. A treasury executive at a mid-sized non-banking finance company is staring at a Bloomberg terminal that has just lit up red. A AAA-rated infrastructure giant — one of the largest borrowers in the country — has missed an interest payment on a commercial paper. The phone is already ringing. The compliance team needs a statement. Mutual funds are about to mark down their schemes. Somewhere in a glass-walled office across the Bandra-Kurla Complex, a credit analyst at a rating agency is being asked the question that defines the entire industry: how did you not see this coming?

That single question — and the answer to it — is the entire business of credit ratings in India.

Welcome to the story of केयर रेटिंग्स लिमिटेड CARE Ratings Limited, now operating under the global brand CareEdge, the country's second-largest credit rating agency by both revenue and number of outstanding ratings.[^1] In an industry where you don't sell a product — you sell an opinion stamped with a letter grade — CARE has spent more than three decades grading the trustworthiness of Indian borrowers, from village-level cooperative banks to sovereign issuers in sub-Saharan Africa.

The genius of this business model is something the great fundamental investors have always loved: it is a regulatory toll booth on the highway of capital. In India, if a corporate wants to issue a bond, a commercial paper, or — after 2007 — even take a large bank loan, somebody with a license has to slap a rating on it. There are only seven such licenses in the country, granted by the भारतीय प्रतिभूति और विनिमय बोर्ड Securities and Exchange Board of India (SEBI), and reinforced by the भारतीय रिज़र्व बैंक Reserve Bank of India (RBI) for bank capital purposes.[^7] Three names dominate the league tables: CRISIL (majority-owned by S&P), ICRA (majority-owned by Moody's), and CARE Ratings (institutionally founded, with no foreign parent). Behind them sit smaller players like India Ratings (Fitch), Brickwork, Acuité, and Infomerics — but the top three together command roughly 85% of the market.

That structure — a near-statutory oligopoly with negligible marginal cost — is the kind of "cornered resource" that Hamilton Helmer dreams about. It explains why a CARE rating, once awarded, generates 60–70% gross margins on the surveillance fee that comes year after year, decade after decade. It also explains why this is one of the most regulator-watched, scandal-prone industries in Indian finance.

The arc this episode will trace is dramatic. It begins in 1993 with an institutional founding — no charismatic billionaire, no garage-startup story — backed by some of the largest public-sector financial institutions in the country. It runs through the Basel II revolution of the late 2000s, when an obscure central bank circular turned every Indian corporate loan into a mandatory rating event. It hits a near-fatal stumble in September 2018, when the collapse of इंफ्रास्ट्रक्चर लीज़िंग एंड फाइनेंशियल सर्विसेज Infrastructure Leasing & Financial Services (IL&FS) brought the entire Indian credit market to its knees and put CARE's AAA stamp under SEBI scrutiny.[^4] And it lands in 2026 with a freshly rebranded, ESOP-aligned, sovereign-rating-ambitious knowledge group trying to convince investors that the worst is behind it and the next decade of Indian debt-market deepening is a tailwind in its favor.

In other words: it is a story about trust, regulation, and the strange economics of selling an opinion that nobody wants to need — but everyone is legally required to buy.

II. The Founding & The Institutional Era

The year 1993 in India had the energy of a country that had just been let out of a locked room. Two years earlier, in the foreign-exchange crisis of 1991, the country had nearly defaulted on its sovereign obligations. The then-Finance Minister, डॉ. मनमोहन सिंह Dr. Manmohan Singh, had dismantled the License Raj. Foreign capital was beginning to trickle in. The Bombay Stock Exchange had just been shaken by the Harshad Mehta securities scam, and the brand-new National Stock Exchange was being built to bring electronic, screen-based trading to a market that still settled trades on physical paper. Capital, after four decades of being rationed by central planners, was suddenly looking for a price.

But how do you price risk when nobody has a track record of independently measuring it?

This was the gap that CRISIL — founded in 1987 by ICICI and other institutions — had first tried to fill, followed by ICRA, founded in 1991 with IFCI as a sponsor. By 1993, the architects of India's financial system decided the country needed a third house, one that would not be captive to a single development financial institution. And so CARE Ratings was born — a creature of consensus rather than vision, founded by a consortium of state-owned giants: the Industrial Development Bank of India (IDBI), Canara Bank, and a clutch of other public-sector banks and financial institutions, with the Unit Trust of India (UTI) soon joining the cap table.[^1]

The very name was telling. CARE was an acronym — Credit Analysis and Research — chosen by a committee, not a founder. Unlike Moody's, named for John Moody who literally invented the bond rating in 1909, or Standard & Poor's, which traces its lineage back to Henry Varnum Poor's railroad guides, CARE had no romantic origin story. There was no equivalent of John Moody walking the floor of the New York Stock Exchange in a top hat. The company was, in the most literal sense of the term, promoter-less — owned by an institutional syndicate that had been instructed by the regulators to create another voice in a market that needed competition.

This institutional ownership had two profound consequences that would echo for decades. The first was distributional discipline. Because no single shareholder controlled the company, no single shareholder could pressure analysts to upgrade a friendly borrower or downgrade an enemy. The second consequence was strategic. With CRISIL fixated on the S&P-branded blue-chips and ICRA tracking Moody's playbook of large industrials, CARE found itself elbowed into the mid-market — the second-tier corporates, the public-sector enterprises, the regional NBFCs that the bigger agencies treated as a courtesy. For a young agency in the mid-1990s, this was less a strategy than a survival tactic. In hindsight, it became the moat.

The mid-market was where the volume was. The blue-chip universe in India had perhaps 200 names; the mid-market universe had thousands, and would eventually number in the tens of thousands. By understanding promoter behavior in mid-sized family businesses — the cross-holdings, the related-party transactions, the unique stresses of a textile mill in Surat or a sugar cooperative in Maharashtra — CARE built up an institutional memory that the offshore-influenced agencies couldn't easily replicate.

Then came the moment that turned the entire industry from a polite intellectual exercise into a regulated necessity. In July 1999, SEBI introduced the SEBI (Credit Rating Agencies) Regulations, 1999, which made it mandatory for any debt instrument offered to the public to be rated by a SEBI-registered rating agency. Suddenly, the question was no longer "is a rating useful?" but "do you have one?" The "nice-to-have" became a "must-have." Issuers without ratings were locked out of the bond market. Investors couldn't park money in unrated paper. Pension funds and insurance companies, governed by their own conservative mandates, gravitated toward higher-rated instruments.

This was the alchemy that turned CARE — and its two larger peers — from research boutiques into licensed gatekeepers. Once the regulator said you needed a rating, the rating agencies had effectively been handed a perpetual annuity. The marginal cost of producing one more rating opinion, once the methodology and analyst bench were built, was close to zero. Yet the marginal price — set by the regulator's effective monopoly — was healthy and growing.

What changed even more fundamentally was who paid for the rating. In the academic world of capital markets, the cleanest model would be investor-pays — bondholders paying for an independent opinion that protects them. But globally, and in India, the dominant model became issuer-pays — the borrower itself paying the agency to be rated. This created the original sin of the credit rating industry: the entity being judged is also the entity writing the check. CARE inherited this model whole, along with all its embedded conflicts. It was a structure that would not be tested seriously until 2008 globally, and not until 2018 in India.

By the end of the 1990s, with the regulatory tailwind at its back and a mid-market franchise quietly compounding, CARE was no longer a curiosity. It was an institution. But the real prize — a structural acceleration in volume that would catapult margins toward those of a software business — was still seven years away.

III. Inflection Point 1: The Basel II Gold Mine

To understand what happened to the Indian credit rating industry between 2007 and 2012, you have to first understand what was happening inside a small set of conference rooms in Basel, Switzerland. The Basel Committee on Banking Supervision had spent years drafting what would become known as Basel II — a global framework that, in essence, said this: a bank's regulatory capital requirement should be tied to the riskiness of its loan book, not just its size. Lend to a AAA-rated infrastructure company, and you set aside less capital. Lend to a BB-rated textile mill, and you set aside more. Lend to an unrated borrower, and you set aside the highest amount of all.

Look at that last clause again — and you set aside the highest amount of all. For the credit rating industry, that was the only sentence that mattered.

When the RBI began phasing in Basel II for Indian scheduled commercial banks from March 2008, it triggered a stampede.3 Every corporate borrower in India who had a bank loan suddenly had an incentive — channeled through their lender — to get a rating. Not because the borrower wanted one. Because the bank, in order to keep its capital adequacy ratio healthy and not have to raise expensive new equity, needed the borrower to be rated. An unrated loan got a 100% risk weight. A AA-rated loan got a 30% risk weight. The math was so good that banks essentially insisted on it.

This was the birth of what the industry came to call the Bank Loan Rating (BLR) business. Within a few years, the number of outstanding rating actions in the country exploded from the low thousands into the tens of thousands. CARE Ratings, with its dense mid-market relationships and a sales force that already spoke the language of regional manufacturing clusters, was perfectly positioned. The pricing per rating was modest — sometimes a few lakh rupees per assignment — but the volume was extraordinary, and once a borrower was on your books, you collected a surveillance fee every single year to keep the rating live.

If you ran the unit economics on this, you understood why people who study moats started talking about CARE in the same breath as companies like Moody's. A single senior analyst could oversee dozens of ratings. A team of associate analysts did the spreadsheet work. The IT infrastructure was modest. There was no factory to maintain, no inventory to write down, no working capital to fund. Every additional rupee of revenue, once the fixed cost of an analyst team was paid, dropped to operating profit at a rate that resembled software economics. By the early 2010s, the rating agencies were posting EBITDA margins in the high 40s and occasionally above 50% — numbers that companies in metals, chemicals, or consumer staples could only fantasize about.3

It was against this backdrop of structurally accelerating volumes and software-like margins that CARE went public. On December 26, 2012, the company listed on the National Stock Exchange and BSE through an offer for sale of equity shares by its institutional shareholders. The offer was priced at ₹750 per share. The IPO was 35 times oversubscribed. Listing-day gains were modest but the trajectory over the next eighteen months was steep — the stock more than doubled by 2014, as institutional and retail investors began to grasp the toll-booth nature of the business.

What made the listing strategically clever was its structure. There was no fresh issue of capital. The company didn't need it — it generated more cash than it knew what to do with. Instead, the institutional founders — IDBI, Canara Bank, IFCI, and others — used the listing as an exit vehicle to monetize their stakes. Over the subsequent decade, those founders would steadily trim down to small positions or exit entirely, and the shareholder register would migrate toward foreign portfolio investors, domestic mutual funds, and an increasingly diffuse retail base. By 2024, the largest single shareholder was a foreign asset manager holding a single-digit stake, with no entity above 10%.4 CARE became one of the rare large Indian listed companies that was truly promoter-free — a feature that would prove to be both a governance virtue and a vulnerability.

For investors in 2012 looking at the listing prospectus, the math was almost embarrassing. Here was a regulated oligopolist, with negligible capex requirements, a near-pure annuity revenue stream tied to the most strategic input in modern finance (capital), and a balance sheet that was net cash. The bond market in India was, by global standards, embryonic — corporate bonds outstanding were perhaps 15% of GDP, compared to over 100% in the United States. Every bond that didn't exist yet was a future rating fee waiting to happen.

And then, of course, the cracks started to show. Because in a business where you are paid to be skeptical of the people writing your checks, sooner or later the system finds its way to test exactly how skeptical you are willing to be.

IV. Inflection Point 2: The IL&FS Crisis & Reputational Near-Death

September 14, 2018, was a Friday. By the time markets opened the following Monday, the Indian financial system would never quite look the same again.

That weekend, IL&FS Financial Services Limited, a subsidiary of the IL&FS group — one of the largest infrastructure financing platforms in the country, with hundreds of subsidiaries and over ₹91,000 crore in consolidated debt — defaulted on a commercial paper repayment. Days earlier, the group had defaulted on a separate short-term loan. The parent was rated AAA. Not AA. Not A+. AAA — the highest possible mark, an assertion that the borrower was virtually risk-free. CARE Ratings, along with ICRA and India Ratings, had each affirmed that AAA opinion within months, in some cases weeks, of the default.[^4]

What followed was the closest thing the Indian credit market has had to a Lehman moment. Money market mutual funds that had loaded up on IL&FS paper — perceived as gold-standard infrastructure debt — had to mark down their NAVs overnight. Pension funds and insurance companies faced losses on instruments their mandates said they shouldn't have been able to lose money on. The contagion spread to other non-banking financial companies, most notably Dewan Housing Finance Limited (DHFL), which would later default itself, taking down another set of AAA assumptions.

The government's response was unprecedented. The board of IL&FS was superseded — a move usually reserved for failed banks — and Uday Kotak was brought in to chair a new board to manage the unwind. A forensic audit by Grant Thornton was commissioned and would later document a chain of related-party transactions, hidden leverage, and what could politely be described as creative accounting going back years.

For CARE Ratings, the question was brutally simple: how could a team of analysts paid to evaluate IL&FS's group-wide leverage, dependency on rollovers, and operating cash conversion have rated it AAA up to the eve of default?

The SEBI investigation that followed produced a paper trail that was uncomfortable for the entire industry, but particularly so for CARE. On December 26, 2019, SEBI issued an adjudication order against CARE Ratings in the matter of IL&FS, imposing a monetary penalty and detailing what the regulator described as failures in the rating process — including inadequate consideration of group structure, failure to escalate concerns in a timely manner, and lapses in surveillance.[^4] Other agencies faced similar orders. The penalties themselves were modest. The reputational damage was not.

In a business where the product is trust, a series of headlines reading "CARE rated AAA until weeks before default" is the equivalent of a bank robbery for a security company. Issuers began questioning whether to engage CARE for fresh mandates. Bond fund managers began discounting CARE-only ratings versus those with multiple agencies. Internally, the company entered a period of intense pressure. Senior analysts left. Mid-level managers second-guessed every committee decision. And the board — institutional, conservative, deeply uncomfortable with public scandal — concluded that the issue went beyond a single rating error.

The fallout reached the top. In July 2019, the company's then-Managing Director and CEO, Rajesh Mokashi, was sent on leave following a whistleblower complaint that alleged interference in rating decisions. He would eventually exit. The CFO and several senior analysts followed in subsequent months. For an institution that had spent twenty-five years building a reputation for stolid mid-market expertise, the executive turnover was the deepest cultural rupture in its history.

In hindsight, the IL&FS episode was less a unique failure of CARE Ratings than a system-wide indictment of the issuer-pays model in a market where opacity in group structures was the norm rather than the exception. But the system-wide indictment did not particularly comfort CARE shareholders. The stock, which had peaked above ₹1,800 in 2017, halved over the next two years. Revenue growth flatlined. The Bank Loan Rating volumes, the engine of the prior decade, began to decline as corporate credit growth itself slumped and competition from smaller agencies — Acuité, Brickwork, Infomerics — intensified on the margins.

There is an old saying in the rating world: you can fail one rating, you cannot fail your franchise. For roughly eighteen months between mid-2018 and the end of 2019, it was a genuine open question whether CARE Ratings had failed its franchise. The answer, it turned out, would depend on whether the institution could find leadership willing to do something rare for an Indian financial firm: rebuild the culture from the inside out, while the building was still smoldering.

V. The Great Reset: The Mehul Pandya & "CareEdge" Era

When Mehul Pandya was formally appointed Managing Director and CEO on June 1, 2022 — initially for a five-year term — he was, in one sense, the obvious choice.[^3] A chartered accountant by training, he had been with CARE Ratings for nearly two decades, rising from a sector analyst in the late 1990s, through senior leadership of the ratings business, and into the role of Executive Director. He had been the interim CEO since 2020, holding the franchise together through the post-Mokashi cleanup, the pandemic, and the ratings-revenue slump.

But he was also, in a deeper sense, the riskier choice. The IL&FS episode had created a constituency — particularly among foreign investors and some board members — that wanted a clean break: a CEO parachuted in from outside, someone with no fingerprints on any of the prior decisions. Pandya was a continuity candidate in an organization that, on paper, looked like it needed a discontinuity. The board's bet was that an insider who genuinely understood the cultural dysfunction would heal it more durably than an outsider who would have spent the first two years just learning what the acronyms meant.

Pandya's leadership style is something corporate India has not seen much of among CEOs of regulated financial-services firms. He is not a TV-circuit personality. He rarely gives sound-bite interviews. His public appearances tend to be technical conferences, where he comes across less as a chief executive and more as a senior analyst who happens to run the company. Internally, the management overhaul under his watch focused on three things: rebuilding the analyst bench after a wave of post-2019 attrition that the company itself later acknowledged had touched 52% in certain analyst cohorts; restructuring rating committees to insulate analysts from commercial pressure; and aligning compensation through equity rather than annual cash bonuses.

That last point matters more than it sounds. In June 2020, the company introduced an ESOP scheme — the CARE Ratings Employees Stock Option Scheme 2020 — that significantly expanded the pool of employees eligible to receive equity compensation, including mid-level analysts and managers below the executive committee.[^10] For an Indian listed company, where ESOPs have historically been concentrated at the very top of the org chart, this was unusual. The logic was straightforward: an analyst whose three-year compensation depends meaningfully on the long-term reputation of the firm is less likely to compromise a rating to win a one-off mandate. It was an admission that the prior incentive structure had been, in subtle ways, miscalibrated.

In the same period, Pandya's own equity stake in the company — built up through years of grants and vesting — settled in the range of roughly 0.15% of shares outstanding. Modest by global CEO standards, but a meaningful skin-in-the-game position by Indian financial-services norms where many CEOs of professionally-managed firms own essentially nothing.4

The most visible move of the Pandya era, however, was the rebrand. In 2022, the company began transitioning its consumer-facing identity from "CARE Ratings" to CareEdge — short for Care + Edge, signaling the ambition to expand from a pure ratings franchise into a knowledge-services group. The rebrand was not merely cosmetic. It corresponded to a structural reorganization, with the ratings business sitting as one operating segment under the CareEdge umbrella, alongside a separately housed advisory and analytics business (CARE Analytics & Advisory, formerly CARE Risk Solutions), an ESG ratings subsidiary, and an international ratings business operating out of Mauritius and serving African markets.

The strategic shift implied by the rebrand was the most important architectural change in the company's history. The bet was that the pure ratings business — while still highly profitable — was effectively GDP-plus growth, capped by the size of the Indian debt market and the competitive intensity in the BLR segment. To grow at the rates that listed equity markets reward, CARE needed adjacent revenue lines: software for banks (which, once installed, is sticky for years), ESG ratings (a new mandatory market created by SEBI's BRSR Core disclosure framework), economic and industry research, and over the longer arc, sovereign ratings for emerging markets.

What investors began to appreciate, watching this from the outside in 2023 and 2024, was that the rebrand was not a vanity project. It was a hedge. If something like IL&FS happened again — and in a country with ₹200 lakh crore in outstanding debt, something will happen again — the new CareEdge wanted to be earning a growing portion of its revenue from businesses where reputation damage in core ratings would not be existential.

By early 2026, with margins recovering, the Risk Solutions business growing at double digits, the ESG license freshly in hand, and the global sovereign methodology published, the Pandya-era reset looked considerably more durable than the skeptics of 2020 had expected. The franchise, in short, had not failed. But that was a baseline, not a victory. The harder questions about whether CareEdge could become something more than a recovered ratings agency turned on the capital deployment choices the company had been quietly making for over a decade.

VI. M&A & Capital Deployment: The Kalypto Bet

For a company sitting on net cash, with almost no organic capex requirement, and a regulator-protected core business that generates more free cash flow than it can reinvest, the most consequential decisions a management team makes are about M&A. CARE Ratings, for most of its history, has been an extraordinarily disciplined — some would say too disciplined — capital allocator. The company has not done a single transformative acquisition. It has paid out, year after year, dividends that would make a utility blush. And in 2011, it did one small acquisition that, more than a decade later, may turn out to be the single most important capital-allocation decision in its history.

The target was Kalypto Risk Technologies, a small Mumbai-based software company building risk-management products for banks — credit risk, operational risk, asset-liability management, the unglamorous plumbing that every bank balance sheet runs on. The deal was announced in November 2011, with CARE taking a controlling stake; the consideration, while modest in absolute terms, was material relative to Kalypto's revenue at the time.2 By any conventional metric — discounted cash flow, comparable trading multiples, revenue-based — the price looked rich on the day of announcement. Kalypto was a niche player with a handful of customers, in a B2B enterprise software niche dominated globally by companies many times its size.

So why do it?

The strategic logic, in retrospect, was elegant. Credit ratings and bank-risk software live in the same building. The agency that rates a bank's borrowers already knows the bank's risk officers, already understands the regulatory framework the bank operates under, already has data on the bank's loan book. Selling a risk-management platform into the same set of customers is a natural extension. Moreover, ratings revenue is cyclical — it follows credit cycles. Software revenue, particularly enterprise software with multi-year contracts, is countercyclical or at least non-cyclical. For a CRA looking to smooth its earnings, owning a risk-software subsidiary was strategic insurance.

The execution, however, was painfully slow. For the better part of a decade, Kalypto — eventually renamed CARE Risk Solutions — was a drag on the parent's consolidated margins. It bled cash. Its competitive position against giants like SAS, Oracle, and a clutch of well-funded fintech challengers was unclear. Multiple analyst notes in the mid-2010s urged management to either divest it or write it down. The official line was patience: enterprise software in India was a long-cycle business, and the right customer relationships would compound.

That patience began to pay off after 2020. The combination of pandemic-era digital acceleration, RBI's progressively tighter expectations around model-based risk management for Indian banks, and an Indian-banking-system upgrade cycle for ALM and ERM software finally translated into Kalypto-now-CRS winning a string of large bank deals. By the time the company rebranded the unit to CARE Analytics & Advisory as part of the CareEdge transition, the subsidiary was growing in the high-teens to mid-20s annually, was profitable, and was contributing materially to consolidated revenue.

What this looked like, from the outside, was a textbook example of why a public-market investor evaluating asset-light financial firms should pay close attention to small acquisitions in adjacent verticals. The Kalypto deal did not move the stock when it was announced. It did not move the stock for nine years after. And then, sometime between 2021 and 2024, the market quietly woke up to the fact that CareEdge owned not just a ratings franchise but a risk-software franchise — one that, were it spun out as a standalone software company at typical Indian software multiples, might trade at a meaningful fraction of the parent's market capitalization.

The lesson management drew from Kalypto became visible in subsequent M&A. The company has not done large transformative deals — that is not its style and, frankly, in a regulated industry, large M&A creates antitrust and concentration concerns. Instead, it has built out adjacent capabilities through a series of incremental moves: a wholly-owned subsidiary in Mauritius (CARE Ratings (Africa) Private Limited) serving African sovereigns and corporates; a presence in Nepal through CARE Ratings Nepal Limited; a research subsidiary that produces industry and economic outlooks under the CareEdge Research brand; and a separately licensed ESG ratings subsidiary.

Capital not deployed into M&A has historically been returned to shareholders through dividends. The payout ratio has run, in normal years, between 60% and 80% — extraordinarily high by Indian standards, where most listed companies hoard cash for vague future strategic purposes. The implicit message from management has been: we do not pretend to have a long pipeline of compelling acquisitions; we will return the cash and let you reallocate it. For long-term fundamental investors, this is exactly the kind of discipline you want to see at a regulator-protected oligopolist with structurally high margins. The temptation to "diworsify" — Peter Lynch's coinage for empire-building acquisitions that destroy shareholder value — is constant in a cash-rich franchise. CARE has, broadly, resisted it.

The combination — disciplined dividend policy, one well-timed strategic acquisition that took a decade to mature, and a series of smaller bolt-ons to build geographic and product reach — is the platform on which the next phase of growth rests. And that growth, increasingly, comes from segments that did not exist on the income statement five years ago.

VII. The "Hidden" Growth Engines

Walk into the New Delhi office of a senior risk officer at a top-five Indian private-sector bank and ask her how she runs her bank's expected-credit-loss model under the Ind AS 109 framework — the Indian equivalent of IFRS 9. There is a non-trivial probability that the software running her bank's loan-loss provisioning is licensed from CARE Analytics & Advisory — formerly Kalypto, then CARE Risk Solutions, now operating as the technology arm of CareEdge. She likely doesn't think of it as a "CARE product." It is just the system. Her predecessor implemented it. The integration with the core banking system took eighteen months. Switching it out would be a nightmare. So it stays, year after year, generating a license fee and an annual maintenance contract.

That mundane reality is the entire investment thesis for the first of CareEdge's "hidden" growth engines. The risk-software business, while still a relatively small line on the consolidated P&L, has the structural characteristics of an enterprise-software franchise: high gross margins, very high customer retention, multi-year contract visibility, and a cost of customer acquisition that has already been paid in the form of the existing CARE Ratings relationship with the bank. The company has not disclosed precise unit economics for the segment, but management commentary in recent earnings calls has consistently pointed to revenue growth in the 20%+ range, with operating leverage as more customers are onboarded onto a relatively fixed engineering cost base.

The second hidden engine is ESG ratings. On May 2, 2024, SEBI granted a Category-I ESG Rating Provider license to a CareEdge subsidiary, CareEdge ESG Ratings Limited, making it among the first set of Indian agencies to receive the dedicated ESG license under the regulatory framework introduced earlier that year.[^6] The market this license unlocks is structurally created by regulation. SEBI's Business Responsibility and Sustainability Report (BRSR) Core framework, introduced in phases starting with the top 1,000 listed companies by market capitalization, requires audited disclosure on a defined set of nine environmental, social, and governance attributes. ESG-rated debt instruments are increasingly being designed by issuers seeking access to a growing pool of sustainability-aligned investor capital. As BRSR Core expands in coverage and ESG-labeled bonds become more common, the need for credentialed third-party ESG opinions multiplies.

It is worth pausing on what makes ESG ratings a genuinely interesting business as opposed to a buzzword. Unlike credit ratings, which compress decades of methodology into a single letter grade and a single dimension (probability of default), ESG ratings are multi-dimensional, methodology-divergent across providers, and far less standardized globally. This is, paradoxically, an opportunity for a regional player. CareEdge can build a methodology calibrated to the Indian regulatory and disclosure environment — one that does not, for instance, penalize Indian power utilities for coal exposure in a way that purely global ESG raters might. For investors who want India-specific signal, a locally-calibrated ESG rating is more useful than an MSCI ESG score that treats every emerging market the same way.

The third — and most ambitious — hidden engine is the sovereign ratings business. On January 29, 2024, CareEdge announced the launch of a Global Sovereign Rating Methodology through CARE Ratings (Africa) Private Limited, its Mauritius-domiciled subsidiary, becoming the first Indian-headquartered rating group to publish sovereign opinions on countries.1 The early rated universe focused on African and emerging-market sovereigns, with initial publications covering several African nations alongside India's own sovereign rating.

This is, by any conventional measure, a bold move. The global sovereign rating space is dominated by an entrenched triumvirate — S&P, Moody's, and Fitch — known collectively as the Big Three, with a smaller but credible fourth player in DBRS Morningstar (Canadian-origin). Multiple emerging-market governments, particularly across Africa, have long argued that the Big Three apply a "Western bias" — overweighting institutional and political-stability factors in ways that systematically penalize lower-income, faster-growing economies. The premise of CareEdge's sovereign business is that an emerging-market-grounded methodology, applied by an emerging-market-domiciled agency, will produce ratings that more accurately reflect the actual credit profile of emerging-market sovereigns — and that issuers and investors will, over time, pay attention.

Whether this works as a business is a different question. Sovereign ratings, in and of themselves, generate relatively modest fees. The strategic value lies in what they enable: a halo of legitimacy that supports the agency's corporate ratings in those geographies, a research footprint that translates into advisory and analytics revenue, and — if the methodology gains genuine traction — a seat at the table in global discussions about how emerging-market credit should be priced. It is, in essence, a soft-power play disguised as a product launch.

Add it all together and the operating model of CareEdge in 2026 looks notably different from the BLR-dominated company of 2014. Pure ratings revenue still anchors the P&L. But the share of revenue coming from Risk Solutions software, ESG ratings, sovereign and international ratings, and research and advisory has been climbing year after year. The pivot from "a ratings company" to "a knowledge-services group" is real, even if it is still incomplete. And whether or not the sovereign and ESG bets compound into something larger over the next decade, they have already done one important thing: they have reduced the gravitational pull of a single segment — and therefore a single segment's reputational exposure — on the franchise as a whole.

VIII. Playbook: The 7 Powers of CareEdge

To understand the durability of any business, the Hamilton Helmer 7 Powers framework is a useful chess-board, and CareEdge is one of the cleanest case studies of how a few of those powers, stacked together, produce a moat that is wider than it looks. Let's walk through the relevant powers in order.

Cornered Resource. This is the most important — and most underappreciated — power in the franchise. The SEBI Credit Rating Agency license is, in the strictest Helmer sense, a cornered resource. SEBI has, since 1999, issued exactly seven such licenses. The regulator has been transparent that it does not currently view the market as undersupplied; new licenses are theoretically possible but, in practice, exceedingly rare. To compete in this market without a license is not unprofitable — it is illegal. That is the highest form of cornered resource: not a contractual advantage that competitors can match by being smarter, but a statutory advantage they cannot replicate at all without an act of the regulator. Add to that the RBI's External Credit Assessment Institution (ECAI) designation, which is what allows a CRA's ratings to be used by banks for Basel III capital calculations, and the regulatory barrier deepens.

Switching Costs. These vary dramatically by segment. In core ratings, switching costs are moderate — an issuer can theoretically drop CareEdge in favor of CRISIL when the next surveillance review comes up. In practice, however, several frictions make this rare: bond covenants often require a rating from a specific named agency or set of agencies; multi-agency ratings are common, and dropping one without dropping all is unusual; and changing a rating agency mid-cycle invites uncomfortable questions from investors about why. In the Risk Solutions software segment, switching costs are far higher — replacing a deeply-integrated bank risk-management platform is an 18-to-24-month migration project that requires re-validation by the bank's regulators. Once installed, the software is, for all practical purposes, sticky.

Scale Economies. The economics of rating production are quintessentially fixed-cost. CareEdge employs hundreds of analysts across sectoral coverage groups — banking, manufacturing, infrastructure, financial services, structured finance — whose work product can be amortized across thousands of rating mandates. The marginal cost of producing one more rating, once the methodology is established and the analyst team is funded, is meaningfully below the marginal price. Smaller competitors — Acuité, Brickwork, Infomerics — struggle to match the depth of sectoral coverage because their lower revenue base cannot support the same fixed analyst spend.

Branding. In credit ratings, "brand" is functionally a synonym for "trust." The franchise value of the three largest Indian CRAs is not really about marketing — it is about decades of cumulative methodology, surveillance history, and investor familiarity. A CRISIL or CareEdge rating, by virtue of having been around since the 1990s and having been used in millions of investment decisions, carries an institutional weight that newer entrants cannot fast-forward to. This is also why reputational events — like IL&FS — are so damaging: they erode the only power that ratings agencies actually have over their customers.

Counter-Positioning, Process Power, and Network Economies. These are weaker for CareEdge. There is no obvious incumbent-disrupting business model the company is exploiting (counter-positioning); rating production, while sophisticated, is not so process-driven that it cannot be replicated by a peer (process power); and ratings are not network-effect products in the way that exchanges or marketplaces are (network economies).

Layered on top of the 7 Powers, the Porter's Five Forces read of the industry is even more favorable.

Bargaining Power of Buyers is structurally low. Issuers of bonds, commercial paper, or large bank loans do not have the option to skip getting a rating; regulation mandates it. They can choose among the licensed agencies, but they cannot opt out. This is the rare market where the buyers of the service are obligated to be in the market at all.

Threat of New Entrants is near zero. The SEBI registration process for a new CRA is multi-year, capital-intensive, and discretionary on the regulator's part. International CRAs that want to enter the Indian market typically do so by acquiring an existing licensed player, as Moody's did with ICRA and S&P with CRISIL.

Threat of Substitutes is the most interesting force. Could institutional investors bypass ratings entirely and do their own credit research? In theory yes; in practice, regulatory frameworks for mutual funds, insurance companies, and pension funds require ratings for many investment decisions. Private credit funds and certain alternative investment vehicles do bypass ratings — and this is the segment where the threat is real. As private credit grows in India, it eats some of the addressable market for public bond ratings.

Bargaining Power of Suppliers is essentially the bargaining power of the analyst labor pool, which is real but manageable. The analyst job market in Mumbai is competitive — analysts move among CRISIL, ICRA, CareEdge, the Big Three sell-side research desks, and increasingly private credit funds. The ESOP-heavy compensation restructuring at CareEdge is a direct response to this supplier-side dynamic.

Industry Rivalry is concentrated but real. CRISIL, with the deepest S&P-backed methodology and the broadest analyst bench, is the market leader and the most credible competitor for premium mandates. ICRA, with Moody's behind it, is a close second on certain large-cap and financial-sector mandates. CareEdge is structurally the largest of the non-foreign-owned licensed agencies and competes most directly across the mid-market and BLR segments where its sector coverage is densest.

Net of all this, the playbook is consistent with what an investor would expect: regulator-protected moat, asset-light unit economics, modest top-line growth tied to debt-market expansion, lumpy reputational risk, and meaningful capital return through dividends. The wild card is whether the adjacent segments — risk software, ESG, sovereign — can compound into a genuine second leg of growth before the core ratings business hits its long-term ceiling.

IX. Bear vs. Bull Case & The Future

Every credit rating agency, anywhere in the world, lives one rating away from a headline that could rewrite its franchise. That is the central tension of the investment case here, and it deserves a sober airing of both sides.

The bear case starts with reputational risk and does not really need to go anywhere else. The IL&FS episode demonstrated that a single AAA default — particularly one involving a large, systemically important issuer — can compress multiples, accelerate analyst attrition, and trigger regulatory orders that take years to fully digest. The Indian credit cycle in 2026 is not benign; corporate debt levels in certain sectors, especially renewable energy financing structures and certain NBFC sub-segments, contain pockets of stress. A second IL&FS-scale event is not a base case, but it is not a tail risk that can be assumed away either. The bear would also point to the structural pressures from passive investing and direct private lending: as a growing share of institutional flows goes into index-tracking debt funds (which rely on aggregate index inclusion rules rather than incremental rating-by-rating diligence) and into private credit funds (which do their own underwriting and do not require a public rating), the structural addressable market for issuer-pays public ratings could grow more slowly than the underlying debt market.

The bear case extends to competition. The smaller licensed agencies — Acuité, Brickwork, Infomerics — have been winning share at the lower end of the BLR market, pricing aggressively in segments where issuers are price-sensitive. This compresses the pricing-power assumption that underpins the high-margin annuity model. The bear would also argue that the rebrand to CareEdge, while strategically sensible, has not yet translated into a step-change in either growth rate or margin trajectory — and that the sovereign and ESG businesses, while interesting optionality, are unlikely to be material to consolidated revenue for several more years.

The bull case is, in a sense, the inverse of all of the above. Start with the structural backdrop. India's corporate bond market, expressed as a share of GDP, is still in the mid-teens, compared to roughly 100%+ in the United States and Europe.[^11] Every percentage point of that gap that closes over the next decade represents a multi-trillion-rupee expansion of the ratable debt universe. Government policy — through measures like the Insolvency and Bankruptcy Code, the Bharat Bond ETF, and progressive easing of FPI access to Indian debt — is consistently designed to deepen the bond market relative to bank lending. CareEdge, as one of three franchises with the scale and brand to handle that expansion, is mechanically a toll collector on that transition.

Add to this the structural demand from infrastructure financing: India's announced multi-year infrastructure capex pipeline — running into the tens of lakh crores across roads, power, renewables, ports, and rail — is increasingly being funded through bond-market structures rather than pure bank lending, because the duration and scale exceed what bank balance sheets can comfortably hold. Every infrastructure trust (InvIT), every renewable bond, every road-project securitization needs ratings. Each is multi-year, often multi-agency, surveillance-fee-generating business.

The bull then layers in the optionality from adjacent segments. The Risk Solutions software franchise, growing structurally as Indian banks upgrade their risk infrastructure under tighter RBI expectations, could plausibly become a meaningful share of consolidated revenue by the late 2020s — at software-like margins. The ESG ratings business, riding the BRSR Core mandate, is a regulator-created new market that did not exist as a discrete line of business five years ago. And the sovereign ratings push, while a long-cycle bet, is asymmetric — if it works at all, it changes the global perception of the agency and creates marketing power that money cannot buy directly.

The sovereign dream is worth dwelling on for a moment because it captures something larger about Indian financial-services ambition in 2026. For the better part of a century, the global credit rating cartel has been dominated by three American firms whose collective opinions effectively set the price of sovereign borrowing for every country on the planet. Multiple emerging-market governments — most vocally African finance ministries, but also voices from Indian policy circles — have argued that this cartel embeds biases that systematically over-penalize the global South. CareEdge's bet is that an Indian-headquartered agency, with a methodology calibrated to emerging-market realities, can carve out a place at this table. It is not yet at a place where it can tell a G7 sovereign what its rating should be. But the very fact that an Indian agency now publishes its own opinion on Indian, African, and selected emerging-market sovereigns is, in soft-power terms, not nothing.

The myth vs. reality lens is useful here. The dominant narrative around CareEdge in financial media has often been "the second-best CRA, scarred by IL&FS, trying to claw back relevance." That framing captures a piece of the truth but misses three structural realities. First, the IL&FS scar, while reputational, did not destroy the underlying client franchise — issuers who needed multi-agency ratings continued to engage CARE, because the alternative was not a fourth agency of equivalent scale but a smaller, less-credible one. Second, the rebrand and the management overhaul have actually been more substantive than rebrands at most listed Indian firms; ESOP-driven compensation realignment is a deeper cultural change than a new logo. Third, the cyclical headwinds of 2018-2020 — sluggish corporate credit, fee pressure, and the loss of confidence — have largely reversed by 2026 as credit growth has reaccelerated and infrastructure-related debt issuance has surged.

What should an investor watch as the KPIs that actually matter? Three stand out, and only three. First, the share of consolidated revenue from non-domestic-ratings segments — Risk Solutions, ESG, international, research — because that is the leading indicator of whether the CareEdge knowledge-services pivot is real or rhetorical. Second, the year-over-year growth in the number of outstanding rated entities and ratings issued, particularly in the BLR segment, because that is the volume signal that drives the core franchise. And third, the EBITDA margin trajectory of the ratings segment alone, because that is the cleanest readout of whether competitive pressure from smaller agencies and the rising fixed cost of analyst quality (ESOPs, compliance, surveillance) is eroding the historical software-like profitability. A reader who tracks these three metrics annually will understand more about the business than one who reads every quarterly press release.

There are also genuine second-layer overhangs worth flagging. Regulatory tightening — SEBI's increasingly prescriptive guidance on rating committee composition, disclosure standards, and surveillance protocols — raises the fixed cost of operating a CRA and disproportionately benefits scale players, but it also constrains pricing flexibility. Climate and ESG-related disclosure requirements are evolving rapidly and could either be a tailwind (more required ratings) or a competitive disadvantage (if methodology proves vulnerable). The promoter-less shareholding structure remains a governance feature and a vulnerability: with no single anchor shareholder above 10%, the company is, in principle, more vulnerable to an opportunistic takeover attempt than a typical Indian listed firm — though regulatory consent from SEBI would make any change-of-control highly procedural. And finally, the personnel risk in the analyst bench: if Pandya's ESOP-driven retention strategy fails to hold the next generation of senior analysts, the cultural reset could prove fragile.

The franchise that emerges from all of this, in May 2026, is one that has been through its near-death experience, has rebuilt with a more institutionally sound governance and incentive structure, and is now standing at the foot of what could plausibly be a decade-long deepening of the Indian debt market. Whether it makes the climb depends less on the regulator-protected core — which is, by design, hard to disrupt — and more on whether the adjacent bets compound, the next IL&FS doesn't show up in a portfolio of AAA ratings, and a culture that was bruised in 2018 has truly healed by the time the next stress event arrives.

That is the entire story of CareEdge: a business that prints money quietly when no one is watching, and finds itself on the front page exactly when something has gone wrong. The opportunity, and the burden, of being an arbiter of credit in a market that is just now learning how much credit it actually has.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube