Capillary Technologies: The "Salesforce of Loyalty"

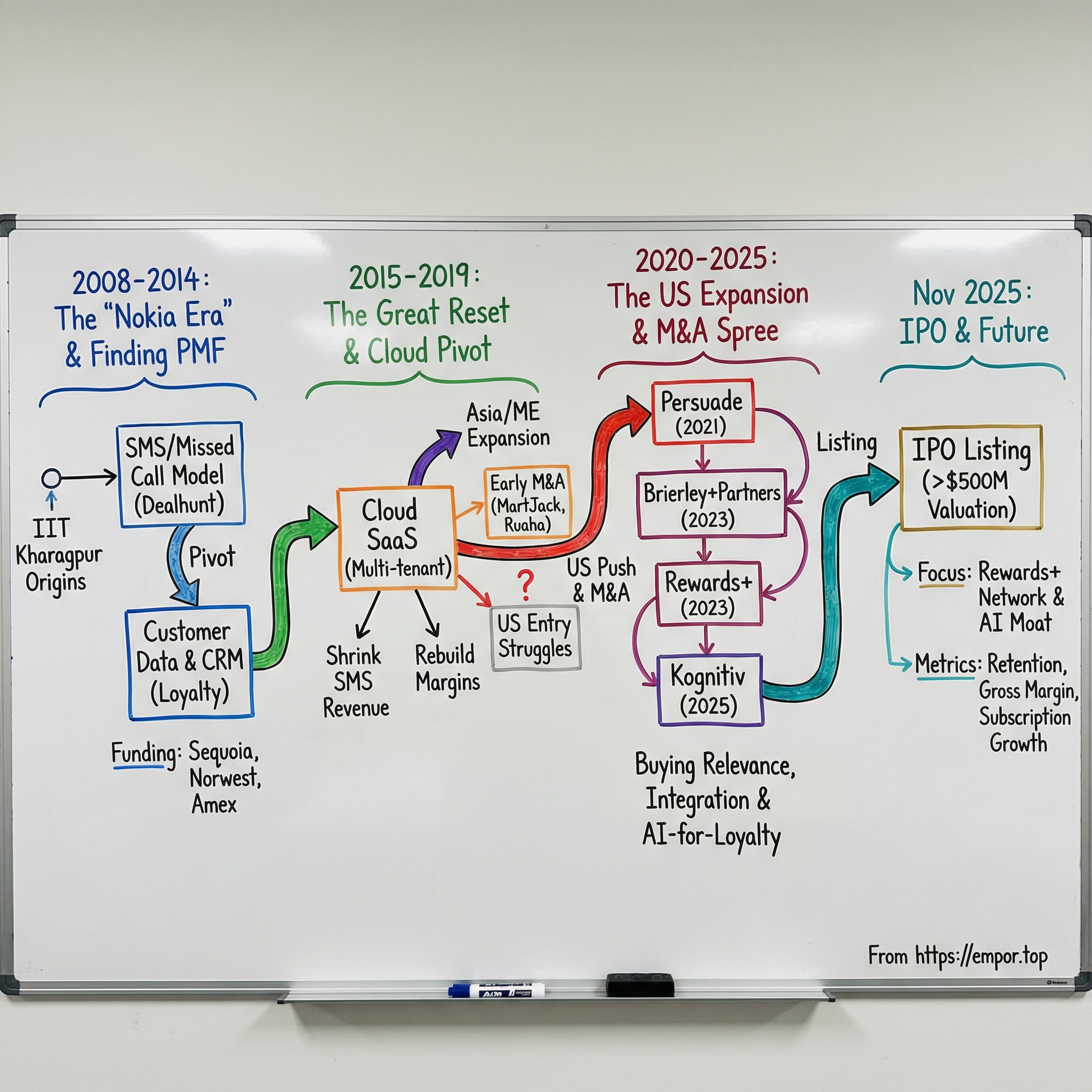

I. Introduction & Episode Roadmap

January 20, 2008. In a dorm-room-adjacent apartment after IIT Kharagpur, three friends, Krishna Mehra, Aneesh Reddy, and Ajay Modani, debated whether to walk away from stable jobs and build a company around one belief: mobile phones were about to reshape retail in India. They had no real product yet, no revenue, and no safety net. And they were starting just as the global financial crisis was unfolding.

Seventeen years later, in November 2025, Capillary Technologies listed in India at a valuation above $500 million. What began in the Nokia-and-SMS era became a global loyalty software platform spanning dozens of countries, with North America emerging as its largest revenue engine. Two founders eventually moved on. Aneesh stayed and evolved from product builder to dealmaker, steering the company through pivots, downturns, and an acquisition-led expansion.

That is the core of this story: not blitzscaling, but endurance. Capillary survived the mobile-marketing graveyard, rebuilt itself more than once, and chose painful trade-offs, including shrinking legacy SMS revenue to protect long-term software margins. This is the long grind: 17 years of resets, near-death transitions, and strategic reinvention.

Why now? Three reasons. First, the 2025 IPO forced the market to price a mature company like a growth asset. Second, the US expansion materially changed Capillary’s profile and investor narrative. Third, the AI-for-loyalty push raises the central question for the next decade: does Capillary’s data moat strengthen with AI, or does AI commoditize the category?

Roadmap for this episode:

From 2008 “missed call” and SMS-led beginnings, to the SaaS pivot, to the cloud reset and survival years, to the M&A spree that cracked North America, and finally to the 2025 IPO and what comes next.

Third, and maybe most consequential for the next chapter, is the acquisition sequence: Persuade (2021), Brierley+Partners (2023), Digital Connect, now branded as Rewards+ (2023), and Kognitiv (May 2025). In four moves, Capillary stitched together software, services, analytics, and a two-sided redemption network. That combination is unusual in loyalty tech. It could become a durable strategic advantage, or a complex integration burden that slows execution. The public-market era will decide which.

That sets up the core theme of this episode: the long grind. Enterprise software is rarely a straight-line story. Sales cycles are long, deployments are messy, and revenue lags effort by quarters, sometimes years. The same switching costs that protect incumbents also make displacement painfully slow. In this category, endurance is often the strategy.

Capillary endured multiple extinction events: the collapse of the SMS-gateway wave, the transition away from on-prem and managed-service economics, and the consolidation of competitors into larger enterprise suites. Through each cycle, the product changed, the go-to-market changed, and eventually the capital-allocation playbook changed. The company kept moving.

So this story runs across four eras. First, the 2008-2014 "Nokia era," when Capillary learned that delivery rails like SMS were commoditizing, but customer data was not. Second, the 2015-2019 reset, when a hard pivot to true cloud SaaS pressured revenue but rebuilt margins and product quality. Third, the 2020-2025 US push, where M&A bought trust and access that organic selling could not. And fourth, the IPO moment, where investors had to value not just a CRM vendor, but a broader loyalty infrastructure platform with hidden optionality.

II. History: The "Nokia Era" & Finding Product-Market Fit (2008-2014)

Capillary’s origin is less Silicon Valley mythology and more IIT Kharagpur pragmatism. In the mid-2000s, startup ambition at IIT was still the exception, not the default path. The safest route was campus placements and multinational jobs; entrepreneurship had more social friction than institutional support.

Aneesh Reddy and Krishna Mehra, hostel wingmates, pushed against that pattern early. Along with peers, they helped start the campus Entrepreneurship Cell in 2005, a small but meaningful signal that building companies could be a first choice, not a fallback. Ajay Modani, from the same network and a year junior, joined that orbit soon after.

Their first instinct was not enterprise loyalty software. It was a simpler consumer concept called Dealhunt, built for a market dominated by Nokia devices, SMS, and missed calls. But that early experiment became the real insight engine: the distribution channel was easy to copy; the underlying customer data layer was not. That realization became Capillary’s first true inflection point.

Timing mattered. In 2008, India’s mobile economy was still the Nokia era: feature phones, prepaid plans, and SMS as the default digital rail. Smartphones existed, but at the margin. For most consumers, “mobile internet” was aspirational; texting was practical. Even missed calls had become a signaling system, a way to communicate without paying for a full call.

Into that market, the founders launched Dealhunt in September 2008, just as the global financial system was seizing up after Lehman’s collapse. The product was simple: consumers would text for nearby offers, and Capillary would route back deal information from local merchants. In hindsight, it was less a scalable consumer app than a live market experiment on how information moved between retailers and shoppers.

The company started with roughly $22,000 in seed capital, structured as a soft loan through IIT Kharagpur’s entrepreneurship ecosystem, with a small equity component. It was symbolic and practical at once: the same campus network they had helped build now became their first institutional backer. But the runway was short, and the margin for error was thinner than the founding story suggests.

Dealhunt’s consumer pull never really broke out. Adoption was modest, retention was weak, and the workflow was too operationally heavy to compound. So the founders did what durable enterprise companies often do early: they sold before they built. Over about six months, they met dozens of branded retailers, from footwear and apparel chains to mall operators, trying to understand what problem had real budget behind it.

That process produced the key insight of Capillary’s first era. Retailers did not primarily need another channel to blast promotions. They needed visibility into their own customers. They could report monthly sales, but not reliably answer basic questions: Who is repeat versus first-time? Which cohorts are churning? Which offers drive return behavior?

In other words, SMS delivery was a commodity; customer data was not. Any aggregator could send messages. Very few could help a retailer create a persistent customer identity layer, connect transactions across stores, and turn that into usable CRM workflows. That was the moat.

The pivot followed quickly. By early 2009, Capillary moved from a consumer-facing deal engine to an enterprise product centered on mobile-number-led CRM. In the Indian context, that design choice was decisive. Email penetration was limited, loyalty cards were fragmented, but mobile numbers were near-universal. At checkout, a phone number became the anchor identity; from there came purchase history, segmentation, and targeted outreach.

That was the real beginning of Capillary: not as an SMS startup, but as a data-software company that happened to use SMS as the first distribution layer. The founders had found their product direction, and more importantly, the economic buyer who would pay for it.

What happened next looked accidental in real time, but became foundational in hindsight. The 2008-2009 downturn hit Indian retail balance sheets hard, and Capillary’s timing collided with a practical constraint: retailers did not want new servers on their books. At the time, enterprise software was still sold as on-prem licenses plus implementation. In a credit-tight market, that model was a non-starter.

So customers pushed Capillary toward a different contract. Instead of paying upfront for hardware and licenses, they asked for hosted software and monthly payments. Aneesh Reddy later summarized it plainly: they arrived at SaaS more by customer pressure than by doctrine. But that pressure created discipline. Recurring revenue meant the product had to keep working every month, not just survive procurement.

That shift mattered more than it seemed. Capillary moved from project-style deployments to a subscription operating model years before “cloud SaaS” was standard language in Indian enterprise conversations. The company was not making a philosophical bet on software architecture; it was adapting to buyer reality. But adaptation became strategy.

Early design partners gave the team the feedback loop it needed. Pizza Hut India became a visible use case for loyalty operations across a large outlet footprint. Shoppers Stop used the platform to analyze behavior across categories and visits. Madura Garments applied it across a multi-brand portfolio, forcing Capillary to think beyond single-store CRM workflows.

With each rollout, the product narrative sharpened. The pitch was no longer “we can send SMS at scale.” It became: “we can identify high-value customers, predict drop-off risk, and improve repeat behavior.” That was a category move, from messaging utility to data system. Even if the tooling was still early, segmentation, campaign triggers, and basic analytics were already delivering measurable retail value.

By 2010-2012, this positioning set Capillary apart in a difficult funding environment. Indian venture capital was still concentrated around consumer internet narratives, and enterprise SaaS from India was viewed as niche and uncertain. The skepticism was simple: could Indian teams build software products, not just services, that sustained enterprise budgets?

Capillary’s first external signal came in 2009 with Qualcomm’s QPrize award and roughly $100,000 in funding. The capital helped, but the deeper benefit was credibility: a technically serious investor had validated the direction.

The stronger institutional endorsement came in September 2012, when Sequoia Capital India and Norwest Venture Partners led a $15.5 million Series A, with Qualcomm participating. For that moment in India’s software market, it was a meaningful vote of confidence, not just in Capillary’s growth curve, but in the broader thesis that Indian-built enterprise software could produce durable, recurring economics.

By 2014, Capillary looked like a category winner in India. It was working with hundreds of retail brands, ingesting millions of transaction records, and building what was arguably one of the most advanced customer data engines in the market. Then came a strong external signal: American Express made a strategic $4 million investment, a sign that global payments players viewed Capillary as a potential infrastructure partner, not just a local vendor. A follow-on $14 million Series B from Sequoia and Norwest reinforced that momentum. From the outside, the scoreboard read exactly how you would want it to read: rising revenue, rising customers, and clear product-market fit.

Inside the company, though, the picture was less clean. The same startup that had survived the zero-to-one years now had to survive itself. As operating complexity grew, founder alignment weakened. Krishna Mehra, the founding CTO and early technical architect, exited after differences with the other founders. Ajay Modani, who had built much of the operating muscle as COO, also moved on and later started new ventures, including Ribbons and Cookifi. What began in hostel corridors at IIT Kharagpur was no longer a three-founder build.

By March 2015, Aneesh Reddy was the last founder standing, 31 years old, leading a company with more than $30 million raised and a rapidly expanding organization. This is a familiar enterprise-software moment: the company has found demand, but the original founding configuration has changed, and the job itself has changed with it. The next chapter was no longer about proving the product worked in India. It was about whether Capillary could be rebuilt for scale: institutionally, technically, and financially.

III. The Great Reset: Cloud, Asia, and Survival (2015–2019)

In September 2015, Warburg Pincus led a $45 million Series C, with Sequoia and Norwest participating. On paper, this was elite validation. In practice, it was the start of a hard reset.

The board’s diagnosis was direct: Capillary had built a successful business model for its first phase, but not one that could compound at global SaaS speed. Much of the revenue still depended on managed-service delivery, deep client-by-client customization, and, in some accounts, lingering on-premise requirements. Implementations were long, services-heavy, and expensive to scale. Each new logo brought meaningful human effort, which capped operating leverage.

That tension defined 2015 to 2019. Capillary had to migrate from a customization-heavy engagement model to a true cloud SaaS platform without breaking customer trust or collapsing growth. It meant painful trade-offs: standardizing product where clients wanted exceptions, retraining go-to-market teams, and accepting short-term revenue pressure to improve long-term gross margins. It also meant abandoning lower-margin messaging rails as a core identity and treating them as plumbing around higher-value software IP.

This was the Great Reset. Not a flashy pivot, but a structural one. And for a period, survival depended on whether the company could execute that transition faster than its legacy model could drag it backward.

To earn the margins and operating leverage of a real SaaS company, Capillary had to move from a single-tenant delivery model to a true multi-tenant cloud platform. That sounds architectural. It was existential. In the old model, large customers effectively ran bespoke versions of the product, with custom code and infrastructure around each account. In the new model, customers would share one core codebase, with differences handled through configuration, not engineering rewrites. One model scales people. The other scales software.

This is one of the hardest transitions in enterprise tech because both systems must run at once. Existing clients cannot be disrupted. New clients will not wait for a multi-year rebuild. So the company has to maintain legacy deployments while funding a next-generation platform, all while sales teams still carry targets and customers still demand exceptions. Revenue quality usually improves before revenue growth does. The income statement often looks worse before the business gets better.

Capillary felt that pain directly. High-paying legacy accounts had been won on deep customization, and those same accounts now had to be migrated toward standardization. Some accepted the trade. Some pushed back. Some churned. Each migration forced a hard choice: preserve near-term revenue by honoring bespoke workflows, or protect long-term economics by enforcing platform discipline.

At the same time, management confronted another drag on quality: the SMS gateway business. It had become large in absolute terms, driven by transactional and promotional messaging across retail clients. From the outside, the topline looked strong. Underneath, the economics were deteriorating. SMS delivery was increasingly commoditized, price competition was intense, and every additional rupee of message revenue carried telecom and operational burden that did not compound like software IP.

So Capillary made the uncomfortable call: shrink the low-margin messaging business and concentrate on higher-margin SaaS. Optically, this looked like deceleration. Strategically, it was the reset. By reducing commodity revenue, the company exposed its real software profile and gave itself a path to stronger gross margins and cleaner unit economics. In the short run, the market did not always reward that choice. In the long run, it likely kept the company from becoming a services-and-plumbing hybrid that could never scale like a global platform.

Geographic expansion in the reset years was a study in contrast, and it shaped Capillary’s strategy for the next decade. Southeast Asia and the Middle East proved to be logical adjacencies: mobile-first consumers, rapidly formalizing retail, and enterprise buyers more open to non-US vendors. Singapore became a regional operating base, and in Saudi Arabia the company set up Capillary Arabia with Veda Holding to gain local distribution, compliance support, and on-the-ground execution in GCC markets.

Even where expansion worked, it was not lightweight. Every country brought different POS stacks, partner ecosystems, data rules, and merchant operating norms. Enterprise sales had to be rebuilt market by market: local teams, local references, local trust. This was not a self-serve SaaS motion. It was services-heavy at the edge, product-led at the core, and operationally demanding. The playbook did not scale elegantly, but it did repeat, and Capillary slowly assembled defensible positions across parts of APAC and the Gulf.

The United States, meanwhile, remained elusive. Capillary’s product could compete, but distribution could not. In 2015–2019, most US enterprise buyers still mapped Indian software companies to IT services, not category-defining product platforms. That perception gap made top-of-funnel access hard: fewer meetings, longer credibility cycles, and limited willingness to run mission-critical loyalty programs on a lesser-known foreign vendor.

The competitive set made that barrier worse. In large accounts, loyalty decisions were often downstream of broader CRM and CX stacks already controlled by Oracle, Salesforce, or SAP. Procurement favored incumbency and integration convenience. Pure-play specialists also had entrenched CMO relationships built over years of conferences, advisory networks, and prior deployments. For Capillary, direct greenfield penetration into Fortune 500 logos was possible in theory, but consistently unproductive in practice.

That mismatch became a strategic lesson: in North America, you could not simply sell your way in; you had to buy relevance. The insight was clear only in hindsight, but the seeds were planted in this period of stalled US traction despite conference spend, local hiring, and outbound effort.

At the same time, Capillary used M&A in Asia to broaden product surface area. In September 2015, soon after the Series C, it acquired MartJack, a multichannel commerce platform serving large enterprises including Walmart India, Unilever, and Future Group. The deal extended Capillary from customer engagement and loyalty into transaction orchestration, linking marketing intelligence to digital commerce execution.

It also absorbed Ruaha Labs, a recommendation and personalization engine for e-commerce use cases. Strategically, this was an early move toward machine-learning-led decisioning inside the core platform: next-best offer, product affinity, and behavior-based targeting. Years before “AI for loyalty” became the headline, Capillary was already assembling the underlying components.

Taken together, 2015–2019 produced a hard but valuable outcome: Asia and the Middle East validated repeatable expansion under constraints; the US exposed the limits of organic entry; and selective acquisitions began shifting the company from a loyalty application to a broader customer-growth stack. The reset was still painful, but the eventual path was starting to come into focus.

In 2016, Capillary added SellerWorx, an e-commerce operations platform, while pushing deeper into China with offices in Guangzhou and Beijing. The logic was obvious: China was the largest and most digitally advanced retail market in the world. The constraints were just as obvious: different platform ecosystems dominated by Alibaba, Tencent, and JD; tighter regulatory complexity; and fierce local incumbents with structural home-field advantage.

By then, management had started to articulate a thesis that would later define the company: Asia could support a multi-product SaaS platform, and acquisitions could accelerate that build faster than organic product roadmaps alone. Instead of waiting years to develop every capability in-house, Capillary could acquire adjacent products and sell them into its existing enterprise base.

That portfolio began to take shape. A retailer already using Capillary for loyalty could layer in MartJack for commerce workflows, Ruaha for recommendations and personalization, and SellerWorx for marketplace operations. The ambition was clear: move from a single loyalty product to a broader retail operating stack tied together by customer identity and transaction data.

Execution, however, lagged strategy. The company was doing three hard things at once: integrating acquisitions, rebuilding its core architecture toward multi-tenant cloud SaaS, and migrating legacy customers without breaking revenue. Organizational bandwidth became the bottleneck.

Financial optics worsened before fundamentals improved. As Capillary intentionally reduced low-margin SMS gateway revenue, headline growth slowed, even while software quality and gross-margin profile improved underneath. This is the classic enterprise-software trough: the old engine is being dismantled before the new engine is fully at scale.

In February 2018, Warburg Pincus and Sequoia reinforced conviction with a $20 million follow-on round. That capital bought time for the reset. By then, Capillary had real enterprise credibility across Asia, a growing data moat, and a defensible regional footprint, even if the US remained stubbornly out of reach.

The lessons from 2015-2019 were hard but clarifying. First, organic US entry was not failing because of feature gaps alone; it was failing on trust, distribution, and incumbency. Second, acquisition integration was the real work, not deal signing. Third, platform transformation took longer than internal plans suggested, and required sustained capital discipline.

Surviving that phase created strategic muscle. Many SMS-led peers disappeared as margins compressed. Several potential regional challengers ran out of funding or shifted focus. Capillary, meanwhile, emerged with stronger SaaS economics, deeper implementation experience across markets, and a repeatable integration playbook.

Those capabilities set up the next era. The company had learned that in North America, credibility would not be won one sales cycle at a time. It would have to be bought, integrated, and operationally improved.

IV. The "American Dream" & The M&A Spree (2020-2025)

By 2020, Aneesh Reddy and his leadership team reached a conclusion that would define the next five years: Capillary could not simply sell its way into US enterprise accounts. It needed to buy relevance, relationships, and trust.

Once management accepted that premise, the logic was hard to unsee. Capillary had already spent years trying to enter the US through direct enterprise sales. The product was credible, but distribution was not. American CMOs were slow to engage a little-known Indian vendor, even one with strong APAC references. In competitive RFPs, incumbents still held the inside track: Oracle, Salesforce, and established loyalty specialists with local teams, local references, and years of procurement trust.

So the objective shifted from feature parity to market legitimacy. Capillary needed US operators who could sell into Fortune 500 accounts without first spending six months explaining the company’s origin story. It needed US logos that procurement teams would recognize. It needed reference customers that could validate mission-critical deployments in the same market. That pointed to one answer: buy credibility, then integrate it into the platform. Expensive, yes, but faster than waiting for organic trust to compound.

The first serious move came in September 2021: Persuade, a Minneapolis-based customer experience firm. Persuade was not a marquee brand, but it delivered exactly what Capillary lacked: US revenue, US talent, and live US customer relationships. It also added useful capabilities around customer journey mapping, satisfaction measurement, and experience optimization, which complemented Capillary’s loyalty core.

Integration was tougher than the initial model implied, and that pattern would repeat in later deals. Bangalore product teams and Minneapolis delivery teams operated with different rhythms, incentives, and communication norms. The technical overlap was manageable; organizational alignment took longer. Still, Persuade did its job. On strategic outcome, this was fair value: not a home run, but a functional beachhead that proved the M&A thesis could work in practice.

More important than near-term synergies, Persuade established process confidence. Capillary had now shown it could source, close, and absorb a US asset without derailing the core business. That capability became the prerequisite for the bigger swing that followed.

That swing arrived in April 2023 with Brierley+Partners. If Persuade was a foothold, Brierley was an unlocking deal. Based in Frisco, Texas, Brierley was a legacy loyalty advisory firm with decades of embedded relationships across major US enterprises. This was the kind of firm CMOs called when they were redesigning tier structures, earn-burn mechanics, and member economics. In trust terms, Brierley had what software vendors spend years trying to build.

But structurally, it was a services business: high-touch consulting, project-led delivery, and margins constrained by utilization. On paper, that looked misaligned with a SaaS company trying to improve operating leverage. In practice, it created the opportunity Capillary wanted: acquire the relationship layer, then inject product and automation to shift the model from people-heavy delivery toward software-led economics.

Capillary’s view was clear, and unusually disciplined: this was a classic private-equity-style operational play, applied inside a SaaS strategy. Acquire a relationship-rich, services-heavy, low-tech loyalty advisor. Layer in Capillary’s product stack. Replace repeatable manual work with software workflows. Expand gross margins over time by shifting delivery from billable hours to platform economics. And use Brierley’s existing CMO access as a distribution engine for Capillary’s technology.

The strategic inversion was the point. Instead of spending years cold-starting trust with US enterprise buyers, Capillary inherited teams already in the room. Instead of entering late-stage RFPs as one more vendor on a feature grid, it could enter earlier as advisor, then steer execution toward its own platform. In practical terms, every Brierley strategy engagement became a potential Capillary software motion.

That is why Brierley became the template for Capillary’s services-to-software conversion thesis. Programs that once required heavy custom buildouts could be delivered on a more standardized technology base. Timelines compressed. Consultants stayed focused on program design, economics, and member strategy, while the platform handled increasing portions of execution. Just as important, Brierley’s legacy brand equity with large US enterprises gave Capillary credibility that would have taken years to build organically. On strategic outcome, this was the unlocking deal.

Then came a very different asset. In June 2023, roughly two months after Brierley closed, Capillary acquired Tenerity’s Digital Connect business and rebranded it as Rewards+. Unlike Persuade or Brierley, this was not primarily about advisory relationships or implementation capacity. It was about network infrastructure.

At a basic level, loyalty programs need meaningful redemption to drive behavior. Earning points is only powerful if customers can spend them on options they actually value. Single-brand discounts are useful but limited. Higher-engagement programs offer broader catalogs: travel, gift cards, merchandise, experiences, and cross-brand value exchange.

Enabling that ecosystem is operationally complex. Someone has to aggregate redemption supply, contract with partners, price and settle transactions, manage fulfillment, and keep the points accounting coherent across participants. Digital Connect already did this. It functioned as a two-sided redemption network connecting earning brands with redemption partners.

That made Rewards+ strategically distinct from pure application software. It carried marketplace properties: more earning brands increase partner demand, and more redemption partners increase brand utility. The result is a reinforcing loop that gets stronger with scale, and harder to dislodge once embedded.

For Capillary, this was a different kind of moat. A competitor can build a loyalty UI or campaign engine. Recreating a contracted, operationally proven redemption network is much slower. Rewards+ therefore expanded Capillary’s position from software vendor toward loyalty infrastructure, with defensibility rooted not only in code, but in network depth.

Then, in May 2025, with the IPO window approaching, Capillary made its most aggressive move yet: acquiring Kognitiv for CAD 23.44 million. Kognitiv added more than 30 enterprise brands, including PetSmart, Hallmark, and Leading Hotels of the World, and materially increased Capillary’s North American footprint in a single step. The timing was deliberate and risky. Closing a complex integration just before public-market scrutiny meant any execution miss would be visible immediately.

The strategic thesis was consolidation at speed. Loyalty software is not a huge enterprise category, but it is fragmented, and scale confers disproportionate advantages in credibility, procurement access, and data depth. Capillary effectively paid a strategic premium to absorb meaningful share before rivals could counter. That premium only made sense if the combined platform could support IPO-level valuation expectations. In plain terms: pay up now, prove operating leverage later.

By FY25, the portfolio effect was visible. North America rose to 57% of revenue, up from 48% a year earlier and from a minimal base five years prior. Management also pointed to roughly 3.5x US growth since Persuade in 2021, reinforcing the core argument of this era: inorganic expansion achieved in four years what organic enterprise selling likely could not have delivered in ten. Just as important, the reference graph changed. Recognizable US logos reduced credibility friction in each subsequent enterprise cycle.

But this is exactly where sophisticated investors pushed hardest. Was Capillary creating value through integration, or simply buying topline at expensive multiples? Could assets acquired across geographies, architectures, and delivery models be unified into one coherent system? Or would the company end up with a stitched-together stack that looked strong in decks but created operational drag in production?

Capillary’s counterargument relied on operating evidence, not narrative alone. Subscription revenue grew 20% year-over-year in FY25, suggesting retention and expansion across acquired cohorts. EBITDA margin reached 13%, indicating that integration costs, while real, were not overwhelming the model. Capital support also mattered: the June 2023 Series D ($45 million, led by Avataar Ventures with Pantheon, 57Stars, Unigestion, and Filter Capital) and the February 2024 extension to $95 million funded the acquisition program and reinforced external conviction in the playbook.

Avataar framed Capillary as “reverse innovation” in practice: a company forged in cost-sensitive, infrastructure-variable markets, then scaled into developed economies. That framing is more than branding. Building for Indian retail forced product discipline, implementation resilience, and ROI clarity. In North America, those capabilities translated into a sharper value proposition, now amplified by acquired distribution. Whether that combination becomes durable category leadership or an integration overhang is the central question the IPO would force the market to answer.

Whether this thesis works will be judged over a multi-year window, not an IPO quarter. The real scorecard is still ahead: retention in acquired cohorts, net revenue expansion inside those logos, cross-sell conversion across the portfolio, and, most critically, technical convergence into a coherent platform instead of a permanent patchwork. But one conclusion was already clear by 2025: Capillary had crossed a strategic line. It was no longer an Indian vendor trying to enter global markets. It was a global loyalty platform headquartered in Bangalore.

V. The IPO & "Hidden" Businesses

On November 21, 2025, Capillary listed on both the National Stock Exchange and the Bombay Stock Exchange, closing a 17-year arc from IIT Kharagpur origins to public markets. The issue was priced at Rs 577 per share, and demand looked euphoric on paper: 52.98x subscription.

Then came the opening print, and the tone shifted. NSE opened at Rs 571.9, below issue price; BSE opened weaker at Rs 560. After all the oversubscription noise, the market’s first message was disciplined rather than celebratory: prove the post-acquisition model in public.

The IPO raised Rs 878 crore (about $105 million), split between fresh issue and offer-for-sale. Early backers including Sequoia, Norwest, and Warburg Pincus took partial liquidity after more than a decade. Proceeds allocation was straightforward and revealing: Rs 143 crore to cloud infrastructure, Rs 71.58 crore to product and R&D, Rs 10.34 crore to systems, and the balance toward inorganic growth plus general corporate use. This was not a “cash out and slow down” listing. It was fuel for the same playbook: platform investment plus selective M&A.

Valuation, however, became the central debate. At listing levels, Capillary traded near 299x earnings, even though FY25 was its first profitable year: Rs 14 crore net income after a Rs 68 crore loss in FY24. The direction was encouraging; the base was still small. Investors were effectively underwriting a future, not paying for present earnings power.

Operationally, the signals were mixed but constructive. EBITDA margin reached 13%, solid but below mature SaaS leaders. Subscription revenue rose 20% year-over-year to Rs 481 crore and crossed 80% of total revenue, reinforcing that the business was increasingly software-led rather than services-led. That mix shift helped explain why the market was willing to assign a growth multiple to a 17-year-old company.

And this is where the story gets more interesting than headline P/E: Capillary is not just a CRM workflow vendor. The underappreciated asset is Rewards+, the redemption network business that behaves less like pure SaaS and more like infrastructure with marketplace dynamics.

Skeptics saw the IPO multiple as aspiration outrunning evidence. At roughly 299x earnings, they argued investors were underwriting a growth curve Capillary still had to prove in public. The bull case flipped that framing: profitability timing was a management choice. Capillary could have optimized near-term earnings by slowing M&A and trimming product spend, but it chose to keep investing while the US window was open. If acquired businesses migrate from people-heavy delivery to software-led execution, margin expansion is plausible.

But the bigger analytical miss is category framing. Most people still model Capillary as a loyalty CRM vendor and benchmark it against Salesforce Loyalty Cloud, Oracle CX, or specialist software players. That lens is incomplete. The most defensible piece of the portfolio may be Rewards+, the business acquired from Tenerity’s Digital Connect and then rebranded.

Rewards+ behaves less like pure SaaS and more like network infrastructure. Loyalty points are only as powerful as redemption utility, and Rewards+ sits in that conversion layer: it connects earning programs to redemption supply across travel, gift cards, merchandise, and experiences. As more brands issue points into the system, redemption partners gain demand. As redemption options deepen, brand programs become more compelling to end customers. That is a two-sided marketplace dynamic, not just a workflow software dynamic.

This is why the moat question changes. A competitor can replicate screens and features faster than it can replicate contracts, settlement rails, partner coverage, and operational trust across a live redemption network. Capillary has said the network now touches more than 300 million consumers across roughly 25,000 connected stores globally. At that scale, each incremental transaction improves pricing, partner utilization, and data exhaust, which in turn strengthens personalization and AI decisioning across the broader platform.

So the hidden optionality is real: part SaaS, part network. If investors value Capillary only as application software, they may miss the infrastructure characteristics inside the model.

The second underappreciated vector is vertical expansion beyond retail, especially healthcare and BFSI. In both sectors, churn is expensive and retention economics are nonlinear. A retail customer may defect for a season; a bank or hospital customer can represent years of high-value cash flows. That changes ROI math. Loyalty in these verticals is less about coupons and more about relationship durability, service engagement, and lifecycle value. If Capillary executes here, the TAM broadens meaningfully without abandoning its core competency in customer data and repeat behavior.

Financial services shows the same retention math, often in sharper form. When a bank loses a customer, it loses more than one account: low-cost deposits that support lending, fee income across payments and service products, and long-tail cross-sell potential across mortgages, investments, and insurance. Acquisition costs are high, payback periods are long, and lifetime value depends on persistence. That is why loyalty in BFSI is becoming strategic infrastructure, not just a marketing program. Capillary has been building quietly in this direction, even if deal disclosure remains limited in a sector where large wins are often kept private.

The IPO prospectus also surfaces a core investor tension: concentration as both risk and signal. In FY25, the top ten customers contributed 58.71% of revenue, and four of those top ten were US-based. The risk is obvious. Losing even one large account could hit quarterly growth and annual guidance, and large enterprises usually have enough buying power to pressure pricing and contract terms.

But concentration here also reflects depth. Capillary is not a lightweight campaign tool sitting at the edge of the stack. Its platform sits in workflows that cut across business units, touches sensitive customer data, and integrates with POS systems, marketing automation layers, customer data stores, and analytics pipelines. Replacing it is not a routine software switch; it is a multi-year transformation with budget, executive sponsorship, and operational risk. Most CIOs avoid that disruption unless outcomes have clearly deteriorated. That is the practical expression of switching costs in this category.

VI. Management & Governance

In enterprise software, many founding teams turn over long before year ten. Capillary’s path is different. Seventeen years after founding, Aneesh Reddy is still the operating CEO. Of the three IIT Kharagpur founders who started the company in 2008, only Reddy remains in day-to-day leadership. Krishna Mehra and Ajay Modani had exited by 2015. Reddy stayed and changed with the job: first product builder, then turnaround operator through the cloud reset, and eventually capital allocator through the acquisition cycle.

That transition is harder than it sounds. The skills that win in year one, product intuition, founder-led selling, and early-team recruiting, are not the skills that win in year fifteen, portfolio construction, integration governance, public-market communication, and capital discipline. Many founders who excel at zero-to-one struggle at one-to-hundred and either step aside or are replaced. Capillary tested that boundary, and Reddy adapted through it, including periods when succession or role redefinition appeared plausible.

His pre-Capillary operating exposure helps explain some of that adaptability. Before founding the company, Reddy worked at ITC, one of India’s most established conglomerates, spanning FMCG, hotels, packaging, paperboards, and agriculture. He was involved in setting up a greenfield FMCG factory, which gave him early exposure to execution under constraints: process rigor, cross-functional coordination, and the discipline of scaling complex operations rather than just launching ideas. Those instincts became useful later, when Capillary’s challenge shifted from invention to institution-building.

His IIT Kharagpur degree in Manufacturing Science and Engineering also shaped how he led. Most software founders are trained to build products; Reddy was trained to design and optimize systems. That shows up in Capillary’s history: he repeatedly re-architected the company when economics changed, from SMS-led workflows to cloud SaaS to an acquisition-integrated platform, instead of defending the original model on sentiment.

Recognition came in phases, usually after the operating work was already done. Fortune India named him in its 40 Under 40 list in 2014, as Capillary was consolidating leadership in India. The Economic Times followed with ET 40 Under Forty in 2017, during the hardest stretch of the cloud transition. IIT Kharagpur also honored him in 2017, closing a loop with the campus entrepreneurship ecosystem he helped build in the mid-2000s.

The more revealing governance test came in 2022-2024. Reddy moved out of the CEO seat and brought in Sameer Garde, former President of Cisco India, signaling a willingness to separate founder identity from operating control as the company prepared for a public-market future. It was a rational move: Capillary was entering a phase where process rigor, reporting discipline, and integration governance mattered as much as product instinct.

That transition was short. Garde resigned in March 2024, and Reddy returned as CEO ahead of the IPO run-up. Whatever the internal reasons, the practical outcome was continuity at a critical moment. For investors, the signal was clear: the founder who had navigated prior resets was back in command for the listing and post-listing integration phase.

Around Reddy, the key operator is Anant Choubey, who holds the combined COO/CFO mandate. That structure is unusual, but in Capillary’s case it fits the strategy: M&A-heavy expansion requires tight coupling between integration execution and capital discipline. Choubey joined in 2010, long before Capillary had category clarity, and built deep context across finance, operations, and transformation programs over fifteen years.

His role became especially important in the 2021-2025 acquisition cycle, where the central challenge was not signing deals but converting them into software-led economics. Internally, this is where the Rule of 40 lens matters: maintain growth while protecting margin trajectory as services-heavy assets are operationally reworked. Choubey’s 2023 elevation to co-founder status formalized what had already become true in practice, that Capillary’s second act was being run by a founder-operator pair, not by founder heroics alone.

Choubey’s most consequential contribution was less visible than deal announcements: he built the integration operating system. Capillary completed a rapid acquisition sequence without losing the core business, which is rare in enterprise software. Most failures happen after close, not at signing, when cultures collide, product roadmaps fragment, and sales teams stop trusting what they are selling. Capillary’s ability to keep growth moving while improving profitability suggests the playbook was functional, at least on public metrics. Through the spree, management kept a clear Rule of 40 orientation: defend margin trajectory while preserving expansion. The open question is depth, not optics. The real test is still unfolding in retention, cross-sell conversion, and expansion across acquired cohorts.

Sridhar Bollam, elevated alongside Choubey to co-founder status in August 2023, anchors the customer side of that thesis in North America. As Chief Customer Officer for the region, he sits at the fault line between strategy and execution: whether acquired credibility converts into durable enterprise relationships. Bollam was an early builder of Capillary’s analytics capabilities, which later became foundational to its AI positioning. His elevation carried a clear signal. North America is now mission-critical, and leadership continuity there is being reinforced with long-term ownership incentives.

Board composition also reflects a company that has crossed from startup governance to public-company governance. Neelam Dhawan, Chairperson and Independent Director, brings heavyweight enterprise credentials from leadership roles at HP India and Microsoft India, along with earlier roles at IBM and HCL. She also serves on multiple public and technology boards, including ICICI Bank, Yatra, Fractal Analytics, and UK-listed Capita. For institutional investors, especially outside India, that profile matters: it signals board maturity, external credibility, and oversight beyond founder centrality.

This does not eliminate governance risk, but it does improve the balance. Capillary appears to retain meaningful insider ownership relative to many late-stage venture-backed peers of similar age. That can align management with long-term shareholder outcomes, especially during integration-heavy years when near-term earnings can be noisy. The counter-risk is familiar: concentrated insider influence can weaken accountability if performance slips. So far, the setup looks reasonable for this stage, experienced independent oversight paired with high-management alignment, but its quality will be judged over time by board independence in hard decisions, not by structure alone.

VII. Analysis: The 7 Powers & 5 Forces

Hamilton Helmer’s 7 Powers is a useful stress test here, because it forces a simple question: what protects this business when competitors have similar feature lists? For Capillary, the strongest answer is Switching Costs, with Scale Economies as a secondary power. The rest of the powers are either emerging or situational, not foundational.

Start with switching costs, because this is where loyalty infrastructure gets mispriced. Replacing Capillary is not a clean vendor swap; it is a multi-system migration touching POS rails, customer identity stores, campaign engines, mobile apps, analytics layers, and finance workflows that track points liability. The real asset is not just software logic, but years of accumulated behavioral history: transaction trails, segment definitions, earn-burn rules, and program mechanics tuned through trial and error. In large programs, that can mean tens of millions of active profiles and complex balances that must transfer without customer-facing errors.

That is why procurement math and operating math diverge. On paper, another vendor may offer a lower contract. In practice, the migration risk is enormous: broken point balances, downtime in redemption flows, retraining across store and support teams, and months of parallel testing before cutover. Most CIOs will not sponsor that disruption unless outcomes have materially deteriorated. This is the core of Capillary’s retention durability: once embedded, the platform is hard to rip out.

The second power is scale economies, increasingly tied to Capillary’s AI layer. The company’s “Generative Loyalty” push and aiRA tooling benefit from breadth of signal that single-brand systems do not have. A single-tenant competitor sees one dataset. Capillary sees patterns across hundreds of brands and roughly 300 million consumers, which improves prediction quality in churn risk, offer optimization, and audience design. Better models improve campaign outcomes; better outcomes increase adoption; adoption generates more data. That loop compounds.

Importantly, this is not a claim that Capillary owns a monopoly on AI. It does not. The claim is narrower and more defensible: in loyalty workflows, scaled cross-client signal plus deep workflow integration creates a practical edge that is hard for new entrants to match quickly. In Helmer terms, switching costs keep customers in, and scale economies improve the product while they stay. Together, those two powers explain most of Capillary’s strategic resilience today.

The one place Capillary does show a form of network effect is Rewards+. It is weaker than consumer platforms like Uber or Airbnb, but strategically meaningful. Add more earning brands, and you increase the pool of points-holding consumers that redemption partners want to access. Add more redemption partners, and each brand’s loyalty program becomes more valuable to end customers. Better redemption utility drives program engagement, which attracts more brands, which deepens partner demand.

That flywheel is hard for pure-play SaaS competitors to copy. They can match workflows and UI, but not quickly replicate a contracted redemption network built over years. Rebuilding that from scratch means negotiating large partner rosters, implementing settlement and fulfillment rails, and reaching enough transaction scale for economics to compound.

Porter’s Five Forces, though, gives a more grounded view than 7 Powers alone.

Supplier power is low. Capillary runs on commoditized cloud infrastructure, where AWS, Azure, and Google Cloud are viable alternatives. There is no single irreplaceable supplier with structural pricing control, which is a favorable position for software margins.

Buyer power is medium-high. Large enterprises such as Tata, Domino’s, or Walmart have real procurement leverage, and Capillary’s concentration profile amplifies that: the top ten customers account for 58.71% of revenue. In contract cycles, those buyers can push hard on price, terms, and bundled services.

But switching costs blunt that leverage at the point of decision. Buyers can threaten to run a process; actually migrating loyalty infrastructure is costly, risky, and slow. So renewals often become a negotiated equilibrium: customers extract concessions, while Capillary retains the account because replacement risk is high.

Threat of new entrants is moderate, and AI has lowered the barrier to building features. A startup can now assemble recommendation logic, campaign content generation, and program-rule tooling faster than before. So yes, parts of the product surface are becoming easier to reproduce.

What remains difficult is not feature construction, but enterprise trust. Mission-critical loyalty systems sit on sensitive customer data, integrate across core stacks, and require auditability, uptime, and compliance discipline (SOC 2, GDPR, PCI-related controls). Fortune 500 buyers do not hand that layer to unproven vendors quickly. Capillary’s implementation record, governance maturity, and reference base still matter more than demo velocity.

The threat of substitutes is the sharpest force in this market. Capillary’s most dangerous competitor is often not another software company, but the customer’s own IT organization.

For large enterprises, “build versus buy” is always live. The in-house case looks compelling in board slides: no vendor margin, full roadmap control, tighter integration with core systems, and stricter data custody. Some companies can pull it off. Amazon built Prime internally. Starbucks built its own rewards stack.

The problem is what happens after launch. Internal platforms rarely benefit from cross-client learning, while vendors improve from hundreds of implementations. Maintenance burden grows as teams turn over and tribal knowledge fades. Feature velocity slows when the same engineering org is reprioritized toward payments, mobile, security, or AI mandates. Over a multi-year horizon, total cost of ownership often rises above the original model. But this substitute threat never disappears; every enterprise RFP still includes “do nothing” and “build internally,” and Capillary has to re-earn the buy decision each cycle.

Among external vendors, rivalry is structurally uneven. Oracle, Salesforce, and SAP can bundle loyalty modules into broader CRM and CX contracts, making standalone pricing comparisons difficult. If a CIO is already committed to a suite, loyalty can look nearly “free” at the margin.

Then there are focused loyalty specialists, including Epsilon, Comarch, and Annex Cloud, competing on depth, domain execution, and implementation track record. In those deals, the contest is more direct: capability breadth, deployment risk, and measurable retention outcomes.

Capillary’s position is unusual because of the acquisition-built stack. It can combine software platform, advisory layer (Brierley), analytics, execution tooling, and the Rewards+ redemption network inside one commercial relationship. That is differentiated, but it carries a trade-off: buyers must believe one integrated vendor is better than a best-of-breed architecture assembled across multiple partners. For organizations prioritizing speed, accountability, and fewer integration seams, Capillary’s model is attractive. For organizations optimizing for modular control, it is a harder sell.

VIII. Bull vs. Bear

The bull case is that Capillary becomes the “Shopify of Loyalty”: invisible infrastructure behind how points are earned, valued, and redeemed across industries. In that scenario, the US acquisitions are not just additive revenue. They become a compounding system where distribution, software, and network effects reinforce each other, and margins expand as services work is progressively absorbed into platform workflows.

In the bull case, the acquisitions do more than add revenue; they reinforce each other. Brierley’s advisory access converts into software bookings as consultants increasingly design programs around Capillary’s stack. Persuade strengthens the customer-experience layer, improving measurable outcomes and supporting premium enterprise pricing. Kognitiv widens the account base in North America, and those logos become expansion vectors across business units and geographies.

That cross-pollination changes the income statement. Services-heavy engagements are progressively productized, and revenue mix shifts toward recurring software. If that conversion holds, gross margins can move materially higher from current levels and begin to resemble scaled SaaS benchmarks. Operating leverage follows: growth outpaces cost growth, and a larger share of incremental revenue flows through to EBITDA and net income.

Rewards+ is the second leg of the bull thesis. As more brands issue points into the network and more partners accept redemption, utility increases for both sides. This is the flywheel pure workflow software cannot easily replicate: contracts, settlement rails, and partner depth compound with scale. Over time, that infrastructure can support better pricing power than application features alone.

The AI layer is the third leg. If Generative Loyalty tools continue to produce visible ROI, better retention, stronger personalization, and improved program economics, Capillary can defend value even as generic AI tooling gets cheaper. The scale of behavioral data across roughly 300 million consumers becomes an advantage in model quality and workflow relevance, reinforcing switching costs already embedded in enterprise deployments.

A fourth upside vector is vertical diversification. If healthcare and BFSI scale into meaningful contributors, Capillary reduces retail concentration while proving that its loyalty infrastructure transfers to sectors where churn economics are even more severe. That would expand addressable market and support the argument that current valuation framing is still too retail-centric.

In that full bull path, the roughly 299x IPO P/E looks less like excess and more like a forward contract on execution. Not because the assumptions were safe, but because management delivers enough growth, margin expansion, and integration quality to validate them.

The bear case is the mirror image, and it is credible. The acquisition program could harden into a Frankenstein stack: multiple architectures, data models, and product philosophies stitched together with persistent integration drag. Engineering bandwidth then gets consumed by harmonization instead of innovation, and promised synergies arrive slower than underwriting models assumed.

If that happens, margin expansion stalls. Services revenue proves harder to convert, integration costs remain elevated, and platform unification slips. Technical debt accumulates, customer experience degrades at handoff points between acquired systems, and the “single platform” narrative looks cleaner in investor decks than in production. At that point, retention risk rises, growth slows, and valuation compression does the rest.

In that bear path, multiple compression comes first. Growth slows, integration benefits arrive late, and the market stops underwriting Capillary as a transformation story. The stock gets rerated from “future platform optionality” to “current earnings durability.” Once that narrative flips, a premium IPO multiple can unwind quickly.

The deeper risk is product-level commoditization. If AI makes core loyalty logic cheap and ubiquitous, offer generation, churn prediction, and program design stop being differentiators and become baseline features. Capillary’s long-built intelligence layer would still matter, but less than investors assumed if rivals can ship “good enough” alternatives in quarters, not years.

That pressure compounds if AI also reduces migration friction. Tools for data mapping, rule conversion, and integration could shrink switching timelines from years to months. The practical moat is still real, but thinner. Renewal conversations then shift: fewer customers need to leave for pricing pressure to intensify. Gross margin can compress even with retention intact.

Concentration risk is the next fault line. With revenue still weighted toward large accounts, losing even one or two top-ten customers would create a meaningful hole that is slow to refill through new logos. In this version, the US thesis underdelivers: acquired relationships remain relationship-deep but software-shallow, cross-sell lags, and organic North America growth cools once post-deal momentum fades.

If that happens, geographic mix can drift back toward Asia, where Capillary remains strong but is valued more as a regional leader than a global consolidator. The company could still be profitable and growing, but the market would price it as a steadier, lower-multiple business. Not a collapse, just a very different outcome from what IPO-era expectations implied.

The three KPIs that matter most from here are net revenue retention, subscription growth, and gross margin trajectory.

Net revenue retention is the cleanest read on product strength because it combines churn, downgrades, and expansion in one number. Above 110% supports the land-and-expand thesis. 100%-110% implies stability without real expansion. Below 100% signals contraction and weakens the long-term compounding case.

Subscription revenue growth isolates the health of the core software engine from services and transaction noise. FY25 delivered about 20% growth. Sustained double-digit performance would validate the platform strategy; sharp deceleration would point to saturation, competitive pressure, or integration drag. The quality of growth matters as much as the headline: expansion inside existing accounts is generally more durable than logo-driven bursts.

Gross margin trend is the execution truth serum for the services-to-software conversion. The thesis only works if margin structurally improves as low-margin work is reduced and software mix rises. Progress toward SaaS-like levels north of 70% would confirm conversion is real. Flat or declining gross margin would suggest the portfolio is remaining more services-heavy than the strategy assumes.

IX. Grading the Story

So how do we grade it?

Start with the US pivot. On execution, this is an A-. In roughly five years, Capillary moved from marginal US relevance to North America contributing 57% of revenue. That is not a branding change; it is a business-model change. Persuade opened the door, Brierley unlocked C-suite access, Rewards+ added infrastructure depth, and Kognitiv accelerated scale right before listing. The sequence was fast, high-risk, and operationally coherent enough to avoid visible customer disruption.

On capital efficiency, the grade is lower: B. The strategy worked, but it was expensive. Capillary funded the push with large private rounds and paid strategic premiums, especially late in the cycle. Those prices can be justified only if integration keeps converting services-heavy revenue into software-led economics, and if acquired cohorts continue to expand rather than just renew. That evidence is improving, but not complete.

So the final verdict: great survivor, with a credible path to becoming generational.

The survival record is already exceptional. Seventeen years, multiple resets, founder turnover, architecture rewrites, and category consolidation, yet the company kept compounding. But generational status requires more than resilience. It requires durable, deepening power. For Capillary, that means proving three things over the next few years: that switching costs stay high, that Rewards+ compounds as a real network, and that integration complexity declines rather than accumulates.

If those hold, this story may be remembered as more than endurance. It may be remembered as one of the few Indian enterprise companies that used the long grind to build global category relevance.

Whether loyalty is entering a structural AI-led transition, and whether Capillary can own that transition, is still unproven. The AI push is a real strategic wager: that model-driven personalization, decisioning, and program design become a durable advantage, not a temporary feature race. Rewards+ is a second wager: that loyalty infrastructure behaves like a network, with compounding value as brands and redemption partners scale. The healthcare and BFSI expansion is a third: that Capillary’s retention playbook travels beyond retail and materially expands the TAM.

All three bets are coherent. None are guaranteed. Their outcomes will be shaped by competitive response, customer adoption curves, and integration quality over multiple years, not quarters.

What is clear is that the easy part is over. The IPO delivered capital, visibility, and liquidity. Now Capillary has to prove that its assembled portfolio is a true system, not a collection of assets. North America must shift from acquisition-led entry to organic compounding. AI must show measurable ROI that supports pricing power. Rewards+ must demonstrate real flywheel behavior, not just strategic narrative.

So the scoreboard is straightforward. Net revenue retention above 110% would validate stickiness and expansion. Subscription growth above 15% would support growth-stock framing. Gross margin progression toward 75% would confirm the services-to-software conversion is structurally working. If those metrics hold over the next three to five years, the IPO valuation will look early, not excessive. If they stall, rerating is the rational outcome.

That leaves the final verdict unchanged: great survivor, credible path to generational. Capillary has already proven endurance. The next chapter is about power. Can it turn switching costs into long-duration expansion, turn Rewards+ into infrastructure advantage, and turn AI from promise into moat? The grind that started in Kharagpur in 2008 is now under public-market scrutiny, quarter by quarter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube