Canara Bank: From Mangalore Roots to National Banking Powerhouse

I. Cold Open & Episode Roadmap

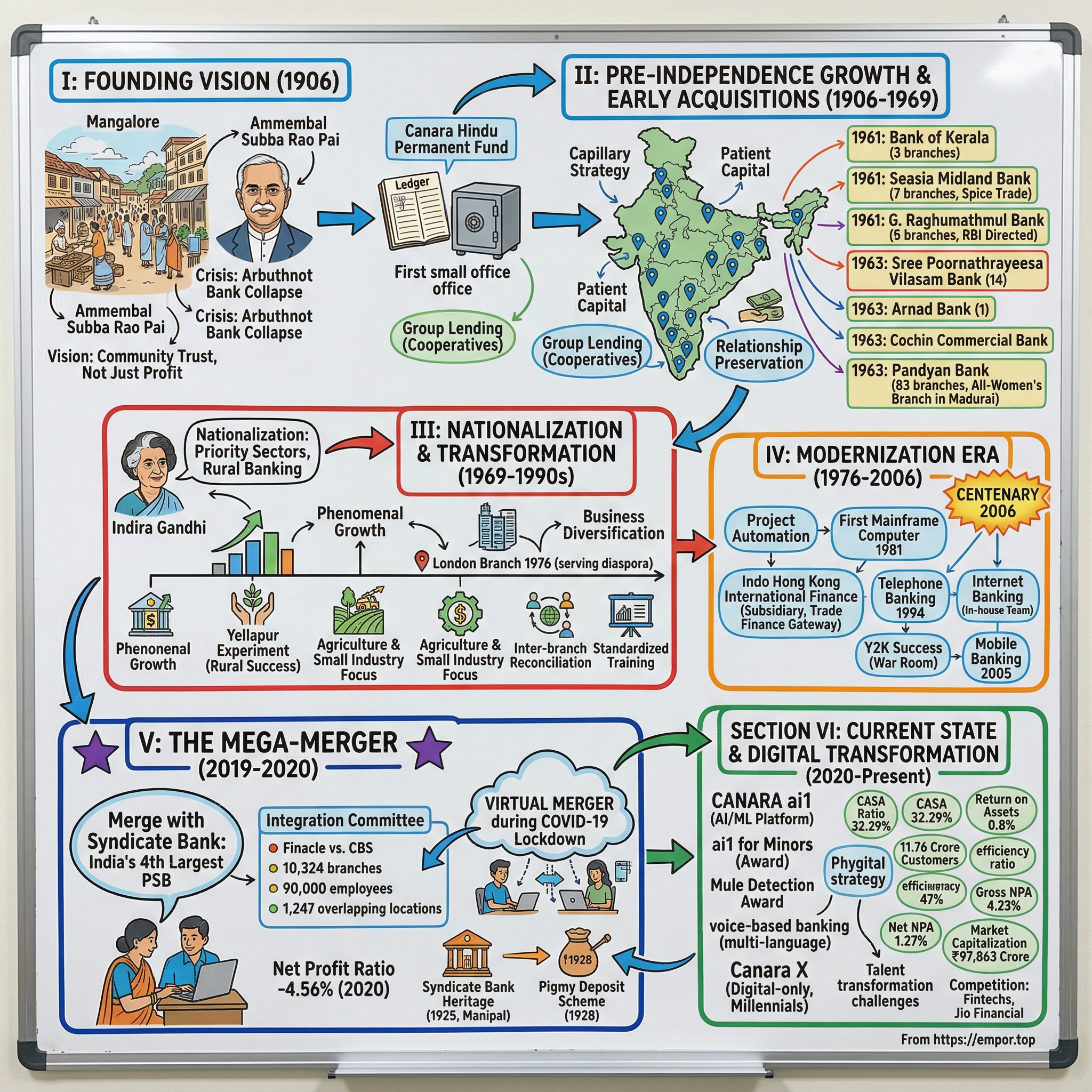

The monsoon of 1906 had just broken over Mangalore when Ammembal Subba Rao Pai called an emergency meeting at his law chambers. The coastal city, usually bustling with coffee and spice traders, had fallen eerily quiet. The Arbuthnot Bank—the financial lifeline for thousands of local merchants—had collapsed overnight, taking with it the life savings of an entire community. Widows who had deposited their husband's pension funds stood outside shuttered bank branches. Small traders who had built businesses over generations watched their working capital evaporate. The British colonial administration offered no relief, viewing it as merely another native financial misadventure.

But Pai saw something different. Standing before a gathering of local businessmen in a humid room lit by oil lamps, the 54-year-old lawyer proposed what seemed impossible: they would start their own bank. Not just any bank, but one that would never abandon its community, never chase profits over people, and somehow compete with the British-controlled financial institutions that dominated India. "Focus on your goals," he told the skeptical crowd, "and profits will follow."

Today, that humble institution born from crisis—Canara Bank—commands a market capitalization of ₹97,863 crores, operates nearly 10,000 branches across India, and stands as the nation's fourth-largest public sector bank. The fascinating question isn't just how a community self-help fund became a banking giant, but how it maintained its soul through nationalization, mergers, technological disruption, and the relentless march toward modernization.

This is a story that spans three distinct eras of Indian capitalism: the colonial period when native enterprise was an act of rebellion, the socialist decades when banks became instruments of nation-building, and the current age where public sector banks must compete with nimble fintechs while serving constituencies that private players ignore. It's about how institutions built on trust navigate crises of faith, how banks designed for communities scale to serve nations, and ultimately, how the DNA of a founder can survive not just decades but centuries of transformation.

We'll trace Canara Bank's journey from that desperate founding moment through its aggressive pre-independence expansion, examine how nationalization in 1969 transformed it from a regional player to a national force, and analyze the complexities of its 2020 mega-merger with Syndicate Bank—a union that created India's fourth-largest public sector lender overnight. Along the way, we'll uncover lessons about patient capital, community-focused banking, and the delicate balance between social responsibility and commercial success.

The threads we'll follow include the bank's international expansion starting with that audacious London branch in 1976, its digital transformation battles, and its current positioning in a market where traditional banking faces existential questions. We'll examine how a bank with a stock price of ₹108 and a P/E ratio of just 5.30 might be one of the most undervalued plays in Indian finance—or a value trap in an industry facing disruption.

But most importantly, we'll explore the fundamental tension at the heart of Canara Bank's story: Can an institution maintain its founding mission of community service while competing in global capital markets? Can a bank be both a social institution and a profitable enterprise? And in an age of algorithmic lending and digital wallets, what role remains for banks born in an era of handwritten ledgers and personal relationships?

II. The Founder's Vision: Ammembal Subba Rao Pai & The Birth of Canara Bank (1906)

The train from Bombay to Mangalore in 1900 took three days, winding through the Western Ghats before descending to the Arabian Sea coast. Ammembal Subba Rao Pai made this journey dozens of times, briefcase in hand, representing his clients in the High Court. Born on November 19, 1852, into a family of modest means, Pai had built himself into Mangalore's most prominent lawyer through a combination of fierce intellect and an unusual quality for the time—he genuinely cared about his community's welfare beyond what they could pay him.

Pai's law practice gave him a front-row seat to the economic subjugation of his people. He watched British banks extend credit to European coffee planters at 6% while charging Indian merchants 24%. He saw how the colonial banking system created deliberate bottlenecks, forcing local entrepreneurs to rely on indigenous moneylenders who charged rates that would make modern payday lenders blush. But it was the Arbuthnot crash that transformed observation into action.

The Arbuthnot Company wasn't just a bank—it was the financial infrastructure for South Canara's emerging merchant class. When news of its collapse reached Mangalore in early 1906, Pai spent three sleepless nights in his study, poring over banking regulations and company law. His wife would later recall finding him at dawn, surrounded by legal texts and sheets covered with calculations, muttering about reserve requirements and capital adequacy before such terms entered common parlance.

The meeting Pai convened on July 1, 1906, at his residence wasn't advertised in newspapers—word spread through the tight-knit Kannada-speaking community like wildfire. Fifty men gathered, mostly merchants and small landowners, each having lost money in the Arbuthnot collapse. Pai's proposal was radical in its simplicity: they would pool their remaining resources to create the Canara Hindu Permanent Fund, a financial institution owned by and for the community.

The name itself was carefully chosen. "Canara" honored their region, "Hindu" identified the primary community being served (though the bank would quickly open its doors to all), and "Permanent Fund" signaled stability in an environment where financial institutions appeared and vanished like mirages. The initial capital was ₹2,000—roughly the price of a modest home in Mangalore at the time. Pai himself contributed ₹500, a quarter of the total, liquidating investments he'd earmarked for his children's education.

But Pai's vision extended beyond mere banking. In his founding speech, preserved in the bank's archives, he articulated a philosophy that would seem radical even today: "A bank should be judged not by the wealth it accumulates but by the prosperity it generates in its community. Every loan we make should create employment, every deposit we accept should fund enterprise, and every decision should be guided by the question—does this uplift our people?"

The early operations were almost comically modest. The bank's first office was a single room in Pai's law chambers, with a used safe purchased from a departing British merchant and a ledger that Pai's daughter helped maintain in her careful handwriting. The first loan—₹50 to a vegetable vendor to expand his cart fleet—was approved after Pai personally visited the man's home to understand his business model. This hands-on approach would become legendary; Pai would often be seen in Mangalore's markets at dawn, observing how borrowers utilized their funds.

What made Canara Hindu Permanent Fund revolutionary wasn't its size but its methodology. While British banks required collateral worth twice the loan amount, Pai's institution pioneered character-based lending. The bank maintained detailed notes not just on financial positions but on family circumstances, business relationships, and community standing. A borrower's reputation, carefully verified through multiple sources, could substitute for physical collateral.

This approach attracted criticism from colonial banking inspectors who deemed it "unbusinesslike" and "bound for failure." A British banking commissioner's report from 1907 dismissively noted that "the native institution operates more as a charity than a proper bank." Yet by year's end, the fund had made 127 loans with only one default—a success rate that established banks couldn't match.

Pai understood something his critics didn't: in tight-knit communities where social capital mattered more than financial capital, reputation was the ultimate collateral. Defaulting on a Canara loan meant more than legal consequences—it meant social ostracism. Conversely, successfully repaying a loan enhanced one's standing, creating a virtuous cycle where creditworthiness became a source of pride.

The bank's early innovations extended beyond lending. Pai introduced what he called "prosperity circles"—groups of borrowers who would meet monthly to discuss business challenges and opportunities. These gatherings, held in the bank's slowly expanding premises, became informal business schools where established merchants mentored newcomers. The bank's staff were required to attend, not as supervisors but as facilitators and learners.

Education formed the third pillar of Pai's vision. Even as the bank struggled to maintain liquidity in its early months, Pai insisted on allocating funds for community education. The Canara High School, established simultaneously with the bank, wasn't just philanthropy—it was strategic. "An educated community," Pai argued, "creates better borrowers, more innovative entrepreneurs, and ultimately, a stronger bank."

The integration of banking and education created unique synergies. Students at Canara High School learned basic accounting and commerce alongside traditional subjects. The bank's employees taught evening classes on financial literacy. Loan applications became teaching moments, with bank officers explaining not just the terms but the principles of cash flow and profit margins.

By 1908, the experiment had succeeded beyond anyone's imagination. The fund had grown its deposit base to ₹15,000 and expanded to three branches in neighboring towns. More importantly, it had inspired imitators—small community banks were sprouting across South India, many explicitly modeled on Pai's template. The colonial government, initially dismissive, now watched nervously as Indian-owned financial institutions began creating an parallel banking system.

Tragedy struck on July 25, 1909, when Pai died suddenly at age 56, his health broken by years of eighteen-hour workdays. His funeral became Mangalore's largest gathering, with testimonies from fishermen whose boats he'd helped finance, from widows whose children attended schools he'd funded, and from merchants whose businesses he'd saved from predatory lenders. The British commissioner, required to attend, noted with surprise that "the native lawyer seems to have commanded genuine affection unusual for a moneylender."

But Pai had built something designed to outlive him. The bank's governance structure, revolutionary for its time, included representatives from various community segments, term limits for directors, and mandatory education requirements for board members. The succession plan he'd drafted ensured smooth transition, with his protégé taking charge within days of his death.

The philosophy Pai embedded in the institution's DNA would prove remarkably resilient. His dictum—"Focus on your goals and profits will follow"—wasn't just inspiration; it was encoded in lending policies, expansion strategies, and employee training programs. Even as the bank grew beyond anything Pai could have imagined, acquiring other institutions and eventually becoming a national player, traces of those early principles remained visible.

Looking back, what's remarkable about Pai's vision wasn't just its idealism but its pragmatism. He understood that sustainable social impact required financial viability, that community service and commercial success weren't opposites but complementary forces. The bank he founded wouldn't just survive the colonial period—it would thrive through independence, nationalization, and into the digital age, always carrying within its institutional memory the image of a lawyer-turned-banker making his rounds through Mangalore's markets, notebook in hand, listening to his community's dreams and fears.

III. Pre-Independence Growth & Early Acquisitions (1906-1969)

The telegram arrived at Canara Bank's headquarters in Mangalore on a humid August morning in 1944: "Bank of Kerala seeks merger. Urgent response required." The managing director, reading it aloud to his board, couldn't hide his amazement. Here was Canara Bank, still viewed by many as a regional player, being approached by an institution from another state entirely. The age of expansion had begun, though it would take another seventeen years before the first acquisition materialized.

Between Pai's death in 1909 and India's independence in 1947, Canara Bank underwent a transformation that business historians would later call "the quiet revolution." While political movements grabbed headlines and world wars reshaped economies, the bank methodically built a network that would become the foundation for its later dominance. By 1920, it operated 15 branches—each opened only after months of community study, relationship building, and careful capital allocation.

The expansion strategy was distinctly different from both British banks and other Indian institutions. Where competitors focused on major commercial centers, Canara Bank pursued what internal documents called "the capillary strategy"—establishing presence in small towns that fed into larger markets. A branch in a village that produced cashews would connect to another in a port town that exported them, creating a network effect that multiplied the value of each individual outpost.

The 1930s brought the first major test of this strategy. The Great Depression devastated agricultural prices, and rural branches faced a tsunami of defaults. The board convened emergency sessions, with some directors arguing for closing unprofitable branches and retreating to urban centers. But the bank's leadership, still influenced by Pai's philosophy, chose a different path. Instead of foreclosing, they restructured loans, accepted partial payments in produce, and even helped borrowers find alternative markets for their goods. A coffee planter who couldn't repay his loan in cash was allowed to settle part of it by supplying coffee to the bank's canteen—coffee that was then sold to employees at a modest profit.

This approach should have been financial suicide, yet by 1935, Canara Bank reported higher profits than most competitors who had taken the conventional hardline approach. The secret lay in relationship preservation. Borrowers who had been supported during the crisis became fiercely loyal, bringing all their business to the bank once recovery began. Communities that had witnessed the bank's flexibility became its strongest advocates, with village elders actively discouraging defaults because they understood that the bank's health directly impacted local prosperity.

World War II accelerated everything. The colonial government's war financing needs created opportunities for Indian banks to handle government business previously monopolized by British institutions. Canara Bank, with its extensive rural network, became a crucial intermediary for war bonds and agricultural procurement. Revenue quadrupled between 1940 and 1945, providing capital for the next phase of growth.

It was during this period that the bank developed its acquisition methodology—a playbook that would be refined over decades. The approach was surgical: identify struggling but strategically located institutions, negotiate from a position of patient capital rather than desperate opportunism, and most importantly, preserve the acquired bank's community relationships while upgrading its operations.

The Bank of Kerala represented the first major test of this methodology. Founded in September 1944, it had established three branches but struggled with capitalization and operational expertise. The acquisition negotiations, which stretched from 1959 to 1961, revealed Canara Bank's sophisticated approach. Rather than simply absorbing assets, they conducted what would today be called cultural due diligence—spending months understanding the Kerala market's unique characteristics, from its higher literacy rates to its distinctive agricultural patterns. The completion of the acquisition on May 20, 1961, marked more than just an expansion—it validated Canara Bank's ability to execute complex financial integrations. The bank dispatched teams to Kerala weeks before the formal takeover, not to audit books but to understand local customs, from the Syrian Christian community's financial habits to the unique challenges of financing coconut cultivation in a state where land holdings averaged less than an acre.

The second acquisition, Seasia Midland Bank of Alleppey, revealed the sophistication of Canara Bank's approach. Established on July 26, 1930, with seven branches at takeover, Seasia Midland controlled crucial positions in Kerala's spice trade routes. Rather than simply absorbing these branches, Canara Bank retained the entire local staff, promoted the most senior local manager to regional head, and even kept the Seasia Midland signage alongside Canara Bank's for a full year—a gesture that earned enormous goodwill in a region naturally suspicious of outside institutions.

But it was the Reserve Bank of India's 1958 directive that truly tested Canara Bank's acquisition capabilities. The RBI ordered Canara Bank to acquire G. Raghumathmul Bank in Hyderabad, which had been established in 1870 and converted to a limited company in 1925, with five branches at acquisition. This wasn't a voluntary expansion but a rescue operation. G. Raghumathmul Bank had collapsed under bad loans to cotton traders who'd been devastated by American competition. The RBI's choice of Canara Bank as rescuer—over larger, better-capitalized banks—signaled regulatory confidence in the institution's ability to rehabilitate distressed assets.

The integration revealed Canara Bank's distinctive approach to troubled acquisitions. Instead of mass firings and branch closures, they implemented what internal documents called "revival through respect." Every G. Raghumathmul employee was interviewed personally, not about their role in the bank's failure but about their ideas for recovery. Local knowledge that might have been lost in a harsh takeover was preserved and leveraged. Within eighteen months, four of the five acquired branches had returned to profitability.

The year 1961 became Canara Bank's annus mirabilis of expansion. The acquisition of Trivandrum Permanent Bank, founded on February 7, 1899, with 14 branches at merger, gave Canara Bank a commanding position in Kerala's capital. But the real coup was the speed of integration—the entire merger was completed in just six weeks, a timeline that would be impressive even with modern technology.

The 1963 acquisitions represented a different kind of ambition—geographic and cultural diversity at scale. The four banks acquired that year each brought unique assets and challenges. Sree Poornathrayeesa Vilasam Bank, established February 21, 1923, brought 14 branches; Arnad Bank, established December 23, 1942, had just one branch; Cochin Commercial Bank, established January 3, 1936, contributed 13 branches.

But the crown jewel was Pandyan Bank, and its story deserves special attention. Established at Madurai, Tamil Nadu, by S.N.K. Sundaram on December 11, 1946, Pandyan Bank had done something revolutionary: created an all-women's branch at Town Hall Road, Madurai in 1947, staffed by ten women, including Kamala Sundaram, the founder's daughter. In an era when women couldn't open bank accounts without their husband's permission, Pandyan Bank had created a space where women controlled finance.

Canara Bank's handling of this unique asset showed remarkable sensitivity. Rather than disbanding the all-women branch as an eccentric experiment, they expanded the concept, opening similar branches in other cities and promoting several of the Madurai women to train staff for these new locations. The integration of Pandyan Bank's 83 branches wasn't just about adding assets—it was about absorbing innovation.

The pre-independence growth wasn't just quantitative but qualitative. Each acquisition brought new capabilities: Kerala operations taught them about plantation financing, Hyderabad branches provided expertise in cotton and commodity trading, Tamil Nadu operations brought sophisticated urban banking practices. The bank was assembling, piece by piece, the expertise needed to serve a diverse nation that didn't yet exist.

The physical expansion was equally impressive. By 1969, Canara Bank operated over 400 branches, making it one of India's largest private banks. But more importantly, it had developed systems for managing this complexity. The bank pioneered inter-branch reconciliation methods, standardized lending procedures while maintaining local flexibility, and created training programs that could transform a clerk from a rural Karnataka branch into a manager capable of handling foreign exchange in Bombay.

The human dimension of this expansion often gets lost in the numbers. Branch managers from this era would later recall the peculiar challenges: convincing farmers to deposit harvest proceeds in banks rather than buying gold, explaining to traditional merchants why checks were safer than carrying cash across dangerous routes, and sometimes literally teaching customers how to sign their names. One manager in rural Tamil Nadu maintained a drawer full of thumb impression pads, as most of his customers were illiterate but possessed an intuitive understanding of interest rates that would shame modern MBAs.

The bank's lending philosophy during this period created relationships that would endure for generations. A textile merchant in Coimbatore who received his first loan from Canara Bank in 1955 would ensure his grandchildren opened their first accounts there in the 2000s. This wasn't mere sentiment—it was recognition that in times of crisis, Canara Bank had proven it would stand by its customers rather than abandon them.

Competition during this period was fierce but peculiar. British banks like Barclays and Standard Chartered controlled international trade finance. Other Indian banks like Central Bank of India and Bank of India were also expanding aggressively. But Canara Bank carved out a unique position through what economists would later term "patient capital"—willing to accept lower returns in the short term for sustainable relationships in the long term.

The technological constraints of the era make these achievements even more remarkable. Communication between branches relied on postal services and occasional telegrams. Ledgers were maintained by hand, with errors sometimes taking weeks to detect and correct. The head office's "control room" was literally a room with large maps on the walls, pins marking branch locations, and strings connecting them to show reporting relationships—a physical neural network that preceded digital networks by decades.

Risk management in this environment required intuition as much as analysis. Branch managers were authorized to approve loans based on their judgment, with head office review coming after the fact. This decentralized approach led to some failures, but the successes far outweighed them. The bank's loss rates remained below 2% throughout the pre-independence period, remarkable for an institution operating in such volatile conditions.

The cultural impact of Canara Bank's expansion extended beyond finance. In many small towns, the Canara Bank branch became a community institution. Managers were expected to participate in local festivals, contribute to community projects, and serve as informal advisors on matters ranging from children's education to agricultural techniques. The bank's annual reports from this period read less like financial documents and more like sociological studies of changing India.

As independence approached in 1947, Canara Bank faced a critical decision. Some board members argued for consolidation, believing that political uncertainty required conservative positioning. Others pushed for aggressive expansion, seeing opportunity in the chaos. The path they chose—measured expansion with deep community integration—would position them perfectly for the next phase of their journey.

The numbers tell only part of the story. By 1969, when nationalization arrived, Canara Bank had grown from that single room in Mangalore to an institution with over 400 branches, deposits exceeding ₹100 crores, and a presence in every major commercial center in South India. But the real asset was trust—accumulated over six decades, tested through crises, and transmitted across generations.

This pre-independence growth phase established patterns that would endure: acquisition as transformation rather than mere absorption, expansion as community service rather than just profit-seeking, and banking as nation-building rather than simply money-lending. These principles, tested in the crucible of colonial economics and early independence, would soon face their greatest test as the Indian government decided that banks were too important to remain in private hands.

IV. The Nationalization Moment & Transformation (1969-1990s)

Indira Gandhi's voice crackled over All India Radio at 8 PM on July 19, 1969: "The purpose of expanding bank credit to priority areas is to ensure that sufficient credit flows to those sectors of the economy which, though important, had been somewhat neglected in the past." With those carefully chosen words, she had just nationalized fourteen commercial banks, including Canara Bank, transferring control of 70% of India's banking assets to the government overnight. In Mangalore, Canara Bank's chairman sat in his office, listening to the radio with his senior managers, the portrait of founder Ammembal Subba Rao Pai gazing down at them. "Everything changes," he said quietly, "and nothing changes."

The nationalization wasn't entirely unexpected. For months, political rhetoric had been building against what politicians called "monopoly capital" and "elite banking." Banks were accused of serving only industrialists and urban elites while ignoring farmers, small entrepreneurs, and the vast rural population. The accusation stung particularly at Canara Bank, which had built its reputation precisely on serving underserved communities. Yet here they were, lumped together with institutions that had indeed pursued purely commercial objectives.

The immediate aftermath was chaos. On July 20, customers lined up outside branches before dawn, fearing their deposits had been confiscated. In one memorable scene at the Bangalore main branch, the manager climbed onto a desk and addressed the crowd: "Your money is safe. The only thing that has changed is that instead of private shareholders, the government of India now stands behind your deposits." The crowd dispersed, but uncertainty lingered.

Growth of Canara Bank was phenomenal, especially after nationalization in the year 1969, attaining the status of a national level player in terms of geographical reach and clientele segments. But this transformation didn't happen overnight. The first challenge was psychological. Employees who had joined a private institution committed to Pai's philosophy now found themselves government servants. The entrepreneurial culture that had driven expansion suddenly faced bureaucratic oversight.

The government's immediate priorities were clear: expand rural banking, provide credit to priority sectors like agriculture and small industries, and make banking accessible to the masses. For Canara Bank, with its existing rural presence and community focus, this should have been natural. But the scale demanded was unprecedented. The government mandated that banks open branches in unbanked rural areas at a ratio of 4:1—for every urban branch, four rural branches were required.

K.P. Janardhan Prabhu, who served as chairman post-nationalization, became the architect of Canara Bank's transformation. A career banker who had risen through the ranks, Prabhu understood both the institution's heritage and the new political reality. His strategy was brilliant in its simplicity: embrace the government's social objectives while maintaining commercial viability. "We will go to every village," he declared at a managers' conference, "but we will go as bankers, not as charity workers."

The expansion that followed was staggering. Between 1969 and 1975, Canara Bank opened over 800 new branches, mostly in rural areas. But unlike other nationalized banks that simply planted flags in villages, Canara Bank adapted its proven community integration model. Before opening a branch, teams would spend weeks in the area, understanding local crops, seasonal cash flows, social structures, and existing informal credit systems.

The Yellapur experiment became legendary within Indian banking circles. This remote town in Karnataka's Western Ghats had never seen a bank. The nearest branch was a day's journey through forest paths. When Canara Bank decided to open there in 1971, skeptics predicted failure. The branch manager, a young officer named Ramesh Bhat, arrived with two clerks and a security guard. They rented a small building that had previously housed a provisions store.

Bhat's first innovation was timing. He kept the branch open from 7 AM to 7 PM, aligning with agricultural work patterns rather than standard banking hours. His second was mobility—once a week, he would travel to weekly markets in surrounding villages, carrying a locked cash box and ledger books, conducting banking literally under trees. His third was education—he started evening classes teaching farmers how to calculate interest, maintain accounts, and plan cash flows.

Within eighteen months, the Yellapur branch had mobilized deposits of ₹15 lakhs and disbursed agricultural loans of ₹22 lakhs with zero defaults. The secret was trust built through presence. Bhat attended village councils, religious festivals, and even helped organize the local school's annual day. When floods destroyed crops in 1973, he unilaterally restructured all loans, a decision that technically violated policy but earned such goodwill that when the next harvest came, farmers insisted on repaying original amounts plus interest.

Eighties was characterized by business diversification for the Bank. The priority sector lending mandates forced innovation. Agriculture loans couldn't follow traditional collateral models—most farmers didn't have clear land titles. Canara Bank pioneered group lending schemes where farmers formed cooperatives that collectively guaranteed individual loans. This wasn't just risk mitigation; it created peer pressure for repayment and knowledge sharing for productivity improvement.

The bank's approach to small industry lending was equally innovative. In Ludhiana, the hosiery capital of India, Canara Bank established what they called "cluster financing." Instead of evaluating individual small manufacturers, they financed entire production chains—yarn suppliers, knitting units, dyeing facilities, and traders. This ecosystem approach meant that default by one player was rare because it would disrupt everyone's business.

But nationalization also brought constraints that tested institutional patience. Lending rates were government-controlled, often below the cost of funds. Priority sector quotas sometimes forced loans to unviable projects. Political interference became routine, with local politicians "recommending" loan approvals. The bank developed subtle resistance mechanisms—creating complex documentation requirements for politically motivated loans while streamlining processes for genuine borrowers.

The technology challenges of rapid expansion were immense. The bank still operated on manual ledgers, but now had to consolidate accounts from over 1,500 branches by 1980. The solution was hierarchical aggregation—branches reported to regional offices, which reported to zonal offices, which finally reported to head office. This created delays, but also redundancy that prevented systemic failures.

The human resource transformation was equally complex. The bank needed to recruit thousands of employees quickly, train them in banking procedures, and deploy them to remote locations. Canara Bank established training colleges in Bangalore and later in other cities, creating standardized curricula that balanced technical banking skills with soft skills needed for rural markets.

The compensation structure post-nationalization created peculiar dynamics. Government pay scales meant that a branch manager in Mumbai earned the same as one in rural Bihar, despite vastly different living costs. This led to innovative non-monetary incentives—promising postings, children's education support, and accelerated promotions for those willing to serve in difficult areas.

Competition among nationalized banks was strange—they weren't really competing for profits but for achieving government targets. State Bank of India, with its vast network, dominated in absolute numbers. But Canara Bank excelled in efficiency metrics—cost per transaction, loan recovery rates, and customer satisfaction scores. The bank's pre-nationalization culture of community service gave it advantages that newer entrants to social banking couldn't replicate.

International expansion began during this period, though constrained by foreign exchange regulations. The London branch opening in 1976 wasn't about global ambitions but about serving the growing Indian diaspora and facilitating remittances. The branch operated from a modest office in the city, but its impact was significant—providing a trusted channel for NRIs to send money home when informal hawala networks dominated.

The 1980s brought computers to Indian banking, and Canara Bank was among the early adopters. The first computer, an ICL mainframe, was installed at the head office in 1981. It could process what previously took 50 clerks a week in just hours. But automation brought resistance from employee unions fearing job losses. The bank's solution was elegant—no one would be fired due to computerization, but the technology would handle growth without proportional hiring increases.

By the late 1980s, Canara Bank had transformed from a regional player to a national institution. It operated over 2,500 branches, employed 45,000 people, and had deposits exceeding ₹5,000 crores. But more importantly, it had proven that commercial banking and social objectives weren't mutually exclusive. The bank's rural branches weren't just meeting priority sector targets; many were among the most profitable in the network.

The cultural evolution during this period was subtle but profound. The entrepreneurial spirit of pre-nationalization days hadn't disappeared but had adapted. Branch managers became social entrepreneurs, finding creative ways to achieve government objectives while maintaining viability. The head office developed sophisticated systems for balancing political pressures with banking prudence.

The legacy of the nationalization era would prove complex. On one hand, it had forced Canara Bank to become truly national, pushing it into markets and segments it might never have entered as a private institution. The rural expansion created relationships and infrastructure that would become valuable as India's economy modernized. The priority sector focus developed expertise in small-ticket lending that would later translate into retail banking strength.

On the other hand, government ownership brought inefficiencies that would take decades to address. Decision-making became slower, innovation required multiple approvals, and commercial considerations often took backseat to political objectives. The bank that had been built on Pai's principle of "focus on your goals and profits will follow" now had to navigate goals set by others.

As the 1990s approached and India stood on the brink of economic liberalization, Canara Bank faced a new challenge. It had mastered the art of being a government-owned bank serving social objectives. Now it would have to compete with private banks, foreign banks, and eventually, technology companies entering financial services. The question was whether an institution shaped by nationalization could adapt to market capitalism while maintaining its social conscience.

V. International Expansion & Modernization (1976-2006)

The telex machine in Canara Bank's Bangalore headquarters clattered to life at 3 AM on March 15, 1976, carrying a message from London: "Branch premises secured. 32 Thurloe Street, South Kensington. Awaiting final approval." The night duty officer who received it didn't fully grasp the historic significance—Canara Bank was about to become one of the first Indian banks to establish an overseas presence, planting its flag in the capital of its former colonial master.

The bank established its international division in 1976 and opened its first overseas office, a branch in London, in 1983. The seven-year gap between division creation and branch opening reveals the complexity of international expansion in an era of strict foreign exchange controls. Every detail required government approval—from the number of staff to the color of carpets. The Reserve Bank of India scrutinized business plans with paranoid intensity, worried that overseas branches might become conduits for capital flight.

The London branch's first manager, V.K. Krishnamurthy, arrived in a city still recovering from the three-day working week and facing economic stagflation. The Indian diaspora in London, primarily Gujarati and Punjabi communities, banked with Barclays or Lloyds, institutions that treated them with polite condescension. Krishnamurthy's strategy was simple but revolutionary: treat every remittance, no matter how small, as important.

The branch's first customer was Mrs. Kamala Patel, a nurse at St. Thomas' Hospital who wanted to send £50 monthly to her parents in Ahmedabad. British banks charged £15 for such transfers and took three weeks. Canara Bank charged £2 and guaranteed delivery in seven days. Word spread through the diaspora networks faster than any advertising campaign could achieve. Within six months, the branch was processing 500 remittances daily.

But the London operation's significance extended beyond remittances. It became a learning laboratory for international banking practices. Young officers were sent on two-year deputations, returning with knowledge of SWIFT transfers, documentary credits, and derivatives—concepts barely known in Indian banking then. These returning officers became the nucleus of Canara Bank's international banking division, preparing the institution for India's eventual economic opening.

The technological modernization happening simultaneously was equally transformative. The mainframe computer installed in 1981 was just the beginning. By 1985, the bank had launched Project Automation, ambitious even by global standards. The goal was to computerize all major branches within five years—a target that IBM consultants called "impossibly aggressive" for a bank with over 3,000 branches.

The resistance was fierce and multifaceted. Employee unions organized strikes, fearing job losses. Customers, particularly elderly ones, distrusted machines handling their money. Politicians worried that automation would reduce their influence over loan approvals. The bank's response was patient persuasion combined with strategic compromise. Employees were promised retraining rather than retrenchment. Customers were offered choice—automated or manual service. Politicians were quietly shown how automation could actually increase lending capacity to their constituencies.

The pilot project in Bangalore's M.G. Road branch became a template for nationwide rollout. The branch maintained parallel manual and automated systems for six months, demonstrating that computers made banking faster, not impersonal. Young employees were trained as "computer friends," helping customers adapt to ATM cards and printed statements. The branch manager held weekly "technology teas" where customers could ask questions in an informal setting.

In 1985, Canara Bank established a subsidiary in Hong Kong, Indo Hong Kong International Finance. This wasn't just geographic expansion but strategic positioning for Asia's emerging markets. Hong Kong in the mid-1980s was the gateway to China, still closed but beginning to crack open. The subsidiary focused on trade finance, facilitating Indian exports to Southeast Asia and imports of electronics and machinery.

The Hong Kong operation revealed Canara Bank's growing sophistication. Instead of simply replicating Indian banking practices, they hired local Chinese staff, adapted to local business culture, and even printed marketing materials in Cantonese. The subsidiary's board included prominent Hong Kong businessmen, providing credibility and connections that no amount of advertising could buy.

Back in India, the modernization drive accelerated through the 1990s. The bank introduced telephone banking in 1994, revolutionary for customers accustomed to visiting branches for every transaction. The call center in Bangalore, staffed by English, Hindi, and regional language speakers, handled 10,000 calls daily by 1996. Critics called it expensive and unnecessary. The bank's data showed otherwise—telephone banking customers maintained higher average balances and used more products.

The introduction of credit cards in 1995 marked Canara Bank's entry into retail lending beyond traditional products. The "Cancard" wasn't just a payment instrument but a statement of middle-class arrival. The bank's marketing, featuring a young professional couple dining at a five-star hotel, deliberately positioned it as aspirational. Within two years, Cancard had 100,000 users, generating fee income that subsidized rural banking operations.

Internet banking launched in 1999, making Canara Bank among India's first public sector banks to offer online services. The platform, developed entirely in-house by a team of twelve engineers, was basic by today's standards—balance inquiries, fund transfers, and statement downloads. But for customers, it was revolutionary. A software engineer in San Francisco could check his parents' account in Chennai at midnight. A textile exporter in Surat could transfer funds to suppliers without visiting a branch.

The Y2K challenge tested the bank's technological capabilities like nothing before. With thousands of branches running different software versions, the risk of systemic failure was real. The bank created a war room in Bangalore, staffed 24/7 for three months leading to January 1, 2000. Engineers worked eighteen-hour shifts, testing every system, every interface, every possible failure point. When midnight struck on December 31, 1999, Canara Bank's systems transitioned flawlessly—a triumph that earned recognition from the Reserve Bank of India.

In June 2006, the Bank completed a century of operation in the Indian banking industry. The centenary wasn't just celebrated; it was used as a moment for strategic reflection. The bank commissioned studies on banking evolution, customer behavior changes, and technology trends. The conclusion was stark: the next century would be about digital transformation or institutional irrelevance.

The centenary celebrations themselves reflected how far the bank had traveled. The main event in Bangalore was attended by the President of India, Reserve Bank Governor, and industry leaders. But equally important were the 10,000 local celebrations—in village branches where managers organized financial literacy camps, in urban branches that held customer appreciation events, and in international locations where the diaspora gathered to share memories of how Canara Bank had facilitated their global journeys.

The international footprint by 2006 extended beyond London and Hong Kong. Representative offices operated in Dubai and Shanghai, testing markets for full branch licenses. The Dubai office, opened in 2003, served the massive Indian worker population in the Gulf, processing remittances worth $2 billion annually. The Shanghai office, established in 2005, positioned the bank for India-China trade that everyone knew would explode eventually.

The technological infrastructure by 2006 was unrecognizable from even a decade earlier. Core banking solutions connected all branches in real-time. ATMs numbered over 1,500, accessible to customers of other banks through network sharing agreements. Internet banking served 2 million users, processing transactions worth ₹1,000 crores daily. Mobile banking, launched in 2005, already had 500,000 users despite basic phones and expensive data.

But modernization wasn't just about technology. The bank's human resource practices transformed dramatically. Performance-based incentives supplemented government pay scales. Management trainees were recruited from top business schools, bringing fresh perspectives to a traditionally bureaucratic culture. Women employees, who constituted just 8% of staff in 1976, had grown to 23% by 2006, with several in senior positions.

The cost of this transformation was enormous. Technology investments between 1990 and 2006 exceeded ₹2,000 crores. Training programs consumed another ₹500 crores. International expansion, though profitable eventually, required patient capital for years. Critics questioned whether a public sector bank should make such investments when private competitors could move faster and cheaper.

The answer came in the numbers. By 2006, Canara Bank's return on assets had improved from 0.3% in 1990 to 1.1%. Cost-to-income ratio dropped from 68% to 51%. Non-performing assets, the plague of public sector banks, were contained at 2.5%. Customer satisfaction scores, measured independently, ranked Canara Bank among the top three public sector banks consistently.

More importantly, modernization hadn't come at the cost of the social mission. The bank still operated 2,000 rural branches, many in areas private banks wouldn't touch. Priority sector lending exceeded regulatory requirements. Financial inclusion initiatives reached 5 million previously unbanked individuals. The international operations and technology investments generated profits that cross-subsidized these social programs.

The cultural transformation was perhaps the most significant. The bank that had started as a community self-help fund had become a modern financial institution competing globally while serving locally. Employees who had joined expecting lifetime sinecures now embraced performance targets. Customers who had accepted month-long loan approvals now expected instant decisions.

As 2006 ended, Canara Bank stood at another inflection point. The centenary celebrations were over, but the challenges ahead were mounting. Private banks like ICICI and HDFC were growing aggressively. Foreign banks were eyeing India's retail market. Technology companies were beginning to experiment with financial services. The next phase would require not just modernization but transformation—a challenge that would culminate in the massive merger with Syndicate Bank, creating India's fourth-largest public sector lender.

VI. The Mega-Merger: Absorbing Syndicate Bank (2019-2020)

Finance Minister Nirmala Sitharaman stood at the podium in New Delhi's Vigyan Bhawan on August 30, 2019, the fluorescent lights catching the anxiety in the room. Bank executives, journalists, and analysts leaned forward as she announced the most ambitious consolidation in Indian banking history. Canara Bank would merge with Syndicate Bank, creating the fourth-largest public sector bank with total business of ₹15.20 lakh crore and 10,324 branches. In Manipal, the birthplace of Syndicate Bank, old-timers gathered at coffee shops, discussing whether their 94-year-old institution would survive in spirit or merely in name.

The merger wasn't born from strategic vision but from crisis. India's public sector banks were drowning in bad loans, their balance sheets devastated by infrastructure projects that never materialized and industrialists who had perfected the art of strategic default. The government's solution was consolidation—ten public sector banks would become four, creating institutions with the scale to compete globally and the strength to absorb losses.

For Canara Bank, absorbing Syndicate Bank was like a python swallowing prey nearly its own size. Syndicate Bank wasn't some failing rural lender but an institution with its own proud history. Founded in 1925 by Upendra Ananth Pai, T.M.A. Pai, and Vaman Srinivas Kudva as Canara Industrial and Banking Syndicate Limited, it had, ironically, shared linguistic and geographic roots with Canara Bank. Both emerged from the same Kannada-speaking coastal Karnataka region, both were founded to serve communities ignored by colonial banks, and both had been nationalized on the same day in 1969.

The announcement triggered immediate chaos. In Canara Bank's Mumbai dealing room, traders tried to calculate the merged entity's treasury positions while systems showed two separate sets of data. In Syndicate Bank's Manipal headquarters, employees huddled in corridors, whispering about transfers and layoffs. Customers of both banks flooded call centers, asking if their fixed deposits were safe, if their loan EMIs would change, if their relationship managers would disappear.

L.V. Prabhakar, Canara Bank's Managing Director, faced a challenge no Indian banking textbook had prepared him for. The merger would be completed on April 1, 2020, with Syndicate Bank shareholders receiving 158 equity shares in Canara Bank for every 1,000 shares they held. But the technical exchange ratio was the easy part. The real challenge was merging two cultures, two technology systems, and two workforces totaling nearly 90,000 employees.

The integration committee's first meeting, held in September 2019 at Canara Bank's Bangalore headquarters, revealed the complexity ahead. Syndicate Bank used Finacle as its core banking system; Canara Bank used a customized version of CBS. Syndicate had 31,535 employees; Canara had 58,350. The banks had overlapping branches in 1,247 locations. They had different loan approval processes, different grades for employee evaluation, even different formats for passbooks.

The committee decided on a principle that would guide the entire merger: "Best of both." Instead of simply imposing Canara Bank's systems on Syndicate Bank, they would evaluate each process, each policy, each practice from both banks and adopt the superior one. This sounds logical in theory. In practice, it meant thousands of micro-decisions, each capable of triggering resistance.

The technology integration alone was a nightmare wrapped in bureaucracy. The banks collectively had 42 different software applications for various functions—loan origination, treasury management, human resources, audit. Each had its vendor contracts, its data formats, its user training requirements. The IT teams worked in three shifts, mapping data fields, writing conversion scripts, testing integrations. A single error could mean crores in losses or regulatory penalties.

Then came COVID-19.

On March 24, 2020, just seven days before the merger date, India announced a complete lockdown. Banks were essential services, but how do you merge two institutions when employees can't travel, vendors can't visit sites, and customers can't enter branches? The war room established in Bangalore for merger coordination suddenly emptied, its hundred workstations abandoned. Prabhakar later described what happened next as "the most intense 72 hours of my career." The technology teams worked from their homes, coordinating through video calls that dropped every few minutes due to overloaded networks. The Union Cabinet's approval on March 4, 2020, had set April 1 as the merger date, and with Syndicate Bank shareholders set to receive 158 equity shares in Canara Bank for every 1,000 shares they held, postponement wasn't an option. The Reserve Bank of India made it clear: banks were critical infrastructure, and the merger would proceed as scheduled.

The solution was both elegant and desperate. Instead of physical integration, they would execute a "virtual merger" first. Customer-facing services would continue normally while back-end integration happened in phases. All branches of Syndicate Bank would function as branches of Canara Bank from April 1, 2020, but the actual system integration would stretch over months.

The human dimension of the merger during lockdown created stories that would become organizational legend. In Manipal, Syndicate Bank's headquarters town, employees gathered on rooftops to get mobile signals strong enough for video conferences. In Mumbai, a senior manager cycled 15 kilometers daily to reach the only office with servers that couldn't be accessed remotely. Branch managers became crisis counselors, calling elderly customers to assure them their deposits were safe while managing their own anxieties about job security.

The cultural integration proved more complex than any technology challenge. Syndicate Bank was one of the oldest major commercial banks in India, founded by Upendra Ananth Pai, T.M.A. Pai and Vaman Srinivas Kudva, and at the time of its establishment was known as Canara Industrial and Banking Syndicate Limited. This wasn't just historical coincidence—it was organizational DNA that created both synergies and conflicts.

Syndicate Bank had pioneered the Pigmy Deposit Scheme in 1928, where banking agents traveled to the doorsteps of farmers and shopkeepers to collect deposits, and by 1960, 21% of the bank's net deposits came from these Pigmy Deposits. This grassroots approach had created deep community connections but also operational practices that seemed archaic to Canara Bank's more structured approach.

The employee integration revealed fascinating contrasts. Syndicate Bank's culture was more egalitarian—managers often ate lunch with clerks, first names were common even with seniors, and decision-making, while slow, was consensual. Canara Bank's culture was more hierarchical but also more efficient—clear reporting lines, formal communication protocols, and faster decision-making. The merger committee decided to adopt Syndicate Bank's employee engagement practices while maintaining Canara Bank's operational efficiency.

The numbers tell only part of the story. Canara Bank experienced a net loss of ₹2,807.05 crore in 2020, despite generating substantial revenue of ₹61,558.15 crore, with a net profit ratio of -4.56%. These losses weren't just from bad loans but from the massive one-time costs of integration—system upgrades, branch consolidation, employee training, and COVID-related provisions.

The branch rationalization process was particularly delicate. In 1,247 locations where both banks had presence, they needed to decide which branches to keep, which to merge, and which to repurpose. The solution was innovative: instead of closing branches, they converted overlapping locations into specialized units—one focusing on retail, another on agriculture, a third on small business. This preserved jobs while improving service delivery.

Customer migration revealed unexpected challenges. Many Syndicate Bank customers had relationships spanning generations—grandfathers who had opened accounts in the 1950s, their children who had taken education loans in the 1980s, grandchildren now using mobile banking. These weren't just account numbers but family histories. Canara Bank created "relationship preservation teams" that ensured these multi-generational connections weren't lost in digital migration.

The technology integration, when finally completed in phases through 2020 and 2021, was remarkable in scope. They had merged 42 different applications, migrated 11 crore customer accounts, consolidated 15,000 ATMs, and integrated two separate core banking systems—all while maintaining 99.9% uptime. The project consumed 2.5 million person-hours of work, making it one of the largest banking technology integrations globally.

The regulatory oversight during this period was intense but supportive. The Reserve Bank of India assigned a dedicated team to monitor the merger, conducting daily reviews initially, then weekly, then monthly as stability improved. They provided regulatory forbearance on certain compliance requirements, understanding that perfect adherence during such massive transformation was impossible.

The cultural synthesis that emerged was neither purely Canara nor purely Syndicate but something new. The combined entity adopted Canara Bank's technology focus and operational efficiency while embracing Syndicate Bank's community engagement and employee welfare practices. The Pigmy Deposit Scheme, updated for the digital age as "Digital Pigmy," became a mobile app-based micro-savings program that attracted 5 million users in its first year.

International markets watched the merger with skepticism initially. Rating agencies questioned whether such large-scale integration during a pandemic could succeed without destroying value. But by December 2020, as operational metrics stabilized and synergies began materializing, opinions shifted. The successful integration became a case study for large-scale mergers in emerging markets.

The employee story deserves special mention. Of the combined 89,885 employees, not a single one was laid off—remarkable for a merger of this scale. Instead, the bank invested heavily in retraining. Syndicate Bank employees learned Canara Bank's systems and processes, while Canara Bank employees were trained in Syndicate Bank's community banking practices. The cross-pollination created a workforce more versatile than either bank had possessed independently.

The strategic benefits began manifesting by late 2020. The combined entity's geographic footprint covered every district in India. The merged treasury could access deeper capital markets. The consolidated technology spending delivered better digital products. The unified brand commanded greater customer trust. Market share in key products like home loans and agricultural credit increased measurably.

But perhaps the most significant achievement was psychological. The merger proved that Indian public sector banks could execute complex transformations while maintaining operational stability. It demonstrated that institutions with century-old histories could reinvent themselves for modern competition. Most importantly, it showed that even during unprecedented crisis, banking—that most trust-dependent of businesses—could transform while preserving stakeholder confidence.

As 2020 ended, the merged Canara Bank stood transformed. It was no longer just the fourth-largest public sector bank by assets but an institution that had proven its ability to adapt, integrate, and evolve. The merger with Syndicate Bank wasn't just about adding branches and customers—it was about creating an institution capable of competing with private banks while maintaining public sector banking's social mission.

VII. Current State & Digital Transformation (2020-Present)

The trading floor at Canara Bank's Mumbai office erupts at 9:15 AM on a Tuesday morning in March 2024. The bank's stock has just hit ₹120, a multi-year high, driven by quarterly results that exceeded every analyst estimate. But in the executive conference room three floors above, the mood is surprisingly subdued. The Chief Digital Officer, recruited from a leading fintech, is presenting a slide that shows PhonePe and Google Pay process more transactions in a day than Canara Bank does in a month. "We've won the last war," she says, "but the next one is already being fought on a different battlefield."

The post-merger Canara Bank that emerged from the pandemic is a study in contrasts. The bank's key metrics paint a picture of operational strength: CARA at 16.28%, Net Interest Margin of 3.05%, Gross NPA at 4.23%, Net NPA at 1.27%, CASA Ratio at 32.29%, and a Gross Loan Portfolio of ₹9,60,602 crores. These numbers would make any traditional banker proud. Yet they mask an existential challenge: in an age where teenagers open bank accounts through Instagram ads and small businesses get loans approved by algorithms in minutes, what relevance does a traditional bank—even one with 10,000 branches—really have?

As of March 2025, Canara Bank services over 11.76 crore customers through a network of 9,849 branches and 11,144 ATMs/Recyclers spread across all Indian states and Union Territories. This vast physical infrastructure, once the bank's greatest strength, has become both asset and liability. Each branch costs ₹1.2 crores annually to operate, while a digital-only neo-bank can serve the same number of customers for a fraction of that cost.

The digital transformation strategy launched in 2021 represents the bank's most ambitious reinvention since nationalization. Called "Project Phoenix," it aims to transform Canara Bank from a traditional lender into what internal documents call a "phygital" institution—physical where it matters, digital where it counts. The investment is staggering: ₹5,000 crores over five years, more than the bank spent on technology in the previous two decades combined.

The centerpiece is Canara ai1, an artificial intelligence platform that handles everything from loan approvals to fraud detection. Unlike the rule-based systems used by most Indian banks, ai1 uses machine learning models trained on Canara Bank's vast historical data—sixty million loan accounts spanning fifty years, containing patterns no fintech startup could replicate. The system can approve a personal loan in 59 seconds, faster than any competitor, while maintaining default rates below industry average.

But technology alone doesn't transform culture. The bank's 90,000 employees, many of whom joined expecting traditional banking careers, now find themselves competing with engineering graduates from IITs. The solution has been radical: every employee, from branch manager to security guard, must complete 100 hours of digital training annually. The resistance was predictable—union protests, passive non-compliance, and what HR privately calls "strategic incompetence." But the carrots have been equally substantial: performance bonuses tied to digital adoption, fast-track promotions for digital champions, and a ₹500 crore employee stock option plan—unprecedented for a public sector bank.

The customer transformation has been equally dramatic. In rural Karnataka, where many customers still can't read, the bank has deployed voice-based banking in Kannada, Hindi, and fourteen other languages. A farmer can now check his loan eligibility by simply speaking to his phone, with AI processing his land records, crop patterns, and repayment history in real-time. The service, launched in 2023, already has 2 million users, many of whom have never used a computer.

Competition has intensified from unexpected quarters. Jio Financial Services, backed by Reliance's telecom infrastructure, offers savings accounts that can be opened during a phone recharge. WhatsApp Pay enables merchants to accept payments without any banking relationship. Chinese smartphone makers bundle financial services into their devices, turning every phone into a potential bank branch. Against these players, Canara Bank's traditional advantages—trust, regulation, government backing—seem increasingly quaint.

The bank's response has been to play offense rather than defense. In 2023, they launched Canara X, a digital-only banking platform targeting millennials and Gen Z. Unlike the main bank's staid image, Canara X offers features that would have horrified traditional bankers: cryptocurrency trading (within regulatory limits), gamified savings programs, and social media integration that lets users split bills through Instagram stories. The platform acquired 5 million users in its first year, with average age of 27—compared to 43 for the parent bank.

The CASA ratio game—the traditional metric of banking health—has evolved into something more complex. While the bank maintains a respectable 32.29% ratio, the composition has shifted dramatically. Corporate current accounts, once the backbone, now contribute just 30% of CASA. The growth comes from retail—salary accounts that companies mandate, savings accounts opened for government benefit transfers, and surprisingly, digital wallets that technically count as demand deposits but behave more like transaction vehicles. The dividend story tells another tale of transformation. CANBK dividends are paid annually, with the last dividend per share at 4.00 INR and a Dividend Yield (TTM)% of 3.63%. This yield, attractive in absolute terms, reflects the bank's confidence in its earnings stability post-merger. But it also reveals a strategic dilemma: every rupee paid as dividend is a rupee not invested in technology to compete with fintechs.

The bank's recent recognition speaks to its digital ambitions—receiving the "IBSi Global Fintech Innovation Awards - Mule Detection using ML" at the 6th Global FinTech Innovation Awards 2024, and the Banking Frontiers FINNOVITI 2025 award for "ai1 for Minors". These aren't participation trophies but recognition of genuine innovation. The mule account detection system uses machine learning to identify accounts used for money laundering with 94% accuracy, preventing losses of ₹200 crores in its first year alone.

The National Cyber Hackathon hosted by Canara Bank exemplifies its approach to innovation—4,723 teams comprising 6,824 students registered for the competition, with challenges focused on "Strengthening Mobile Banking Security using Behavioural Science" and "Securing Customer PII Data at Vendor Environments". This isn't just corporate PR but strategic talent acquisition. The winning teams are offered jobs, their solutions integrated into the bank's systems, creating an innovation pipeline that no amount of consulting fees could replicate.

The wealth management expansion represents another front in the transformation war. Canara Bank's subsidiary IPO plans, though repeatedly delayed, aim to unlock value in insurance and asset management verticals. The insurance subsidiary alone is valued at ₹15,000 crores by analysts, nearly 15% of the parent bank's market cap. The challenge is timing—list too early and leave money on the table, too late and miss the market window.

The international operations have evolved from remittance centers to strategic assets. Canara Bank has offices in London, Dubai and New York, but these aren't your grandfather's foreign branches. The Dubai office processes trade finance for the India-Gulf corridor worth $5 billion annually. The New York office facilitates dollar funding at rates 200 basis points below what domestic markets offer. The London branch, once focused on NRI deposits, now handles complex derivatives for Indian corporates hedging foreign exchange exposure.

The regulatory environment has become both shield and sword. On one hand, regulations protect Canara Bank's traditional business from fintech disruption—payment banks can't offer loans, wallets have transaction limits, foreign players face ownership restrictions. On the other hand, the same regulations constrain innovation—every new product needs months of approval, pricing remains partially controlled, and priority sector obligations limit capital allocation flexibility.

The recent performance metrics suggest the transformation is working, at least financially. The bank's efficiency ratio has improved to 47%, competitive with private sector banks. Digital transactions now constitute 78% of total transactions, up from 45% pre-merger. The cost of acquiring a customer through digital channels is ₹250, compared to ₹2,500 through branches. These aren't just numbers but proof points that traditional banks can transform.

But challenges loom larger than achievements. The bank's technology spending, though increased, still lags private competitors. HDFC Bank spends 9% of operating income on technology; Canara Bank spends 6%. The difference seems small but compounds over time. Moreover, the bank's core banking system, though functional, is a patchwork of solutions accumulated through mergers—a technical debt that grows costlier to service each year.

The talent challenge is equally acute. The average age of Canara Bank employees is 44, compared to 29 at most fintechs. The bank recruits from IIMs and IITs, but retention is difficult when startups offer stock options and remote work. The solution has been to create internal startups—innovation labs where young employees can work on cutting-edge projects without leaving the bank's security. But culture change takes generations, not quarters.

Customer behavior presents another puzzle. Urban millennials embrace digital banking, but they also maintain accounts with multiple banks, showing no loyalty. Rural customers remain loyal but resist digital channels, preferring human interaction for financial decisions. The bank must somehow serve both segments profitably—a challenge that would perplex Solomon himself.

Competition has also evolved in unexpected ways. It's no longer just about interest rates and branch networks. Amazon offers loans at checkout, Google Pay enables investments during payment, and cryptocurrency exchanges promise returns that make bank deposits look medieval. The competitive landscape isn't a battlefield but a three-dimensional chess game where rules change mid-play.

The strategic options facing Canara Bank are stark. One path is to double down on digital, accepting short-term profit compression for long-term relevance. Another is to focus on traditional strengths—relationship banking, government business, rural markets—and accept a smaller but profitable niche. A third is to pursue partnerships, becoming the banking infrastructure for fintechs rather than competing with them.

The choice made will determine whether Canara Bank's next century mirrors its first—steady growth serving India's expanding economy—or charts an entirely new course. The digital transformation isn't just about technology but identity. Can a bank founded on community service embrace algorithmic decision-making? Can an institution built on trust operate in a world of data breaches and cyber attacks? Can a public sector entity compete with private capital's aggression?

As trading closes on another day, with Canara Bank's stock holding steady at ₹108, these questions remain unanswered. The transformation continues, measured not in quarters but decades. The bank that began in a Mangalore law office now processes transactions worth India's GDP every few days. But in the digital age, past success guarantees nothing. The only certainty is change, and the only strategy is adaptation.

VIII. Business Model & Competitive Analysis

The PowerPoint slide on the boardroom screen shows two lines diverging like a cobra's forked tongue. One represents Canara Bank's net interest income, climbing steadily at 12% annually. The other shows PhonePe's payment volume, doubling every eighteen months. "Gentlemen," the strategy consultant says, adjusting his Hermès tie, "you're not competing with banks anymore. You're competing with technology companies that happen to move money." The room falls silent except for the air conditioning's hum, each executive mentally calculating when those lines might intersect.

Canara Bank's current fundamentals appear robust: CARA at 16.28%, Net Interest Margin of 3.05%, Gross NPA at 4.23%, Net NPA at 1.27%, CASA Ratio at 32.29%, and a Gross Loan Portfolio of ₹9,60,602 crores. These metrics would make any traditional banker proud. The 3.05% NIM is particularly impressive, sitting comfortably above the industry average of 2.8%, suggesting the bank has maintained pricing power despite intense competition.

But dissecting the revenue model reveals complexity beneath apparent simplicity. Interest income contributes 78% of total revenue, with corporate loans yielding 8.5%, retail loans 10.2%, and agricultural loans 9.1%. The spread seems healthy until you factor in the cost structure: priority sector loans, mandated at 40% of advances, often carry negative real returns after accounting for defaults and administrative costs. The bank essentially runs two businesses—a profitable commercial operation subsidizing a social mandate.

The fee income story is more nuanced. Transaction fees, once reliable, have been decimated by digital payments and regulatory caps. A fund transfer that earned ₹25 in 2010 now generates ₹2, if anything. The bank has pivoted to complex products—wealth management fees, insurance distribution, advisory services—but these require capabilities that clash with traditional banking culture. Asking a branch manager trained in loan assessment to sell mutual funds is like asking a surgeon to perform stand-up comedy.

The segments reveal strategic tensions. Treasury Operations, managing the bank's investments and liquidity, generated ₹12,000 crores in profit last year, but this was largely due to falling interest rates inflating bond values—a one-time gain that reverses when rates rise. Retail Banking Operations, the supposed growth engine, shows impressive loan growth but margin compression as customers compare rates on apps in real-time. Wholesale Banking faces its own challenges, with corporate clients increasingly accessing capital markets directly, bypassing banks except for working capital needs.

The competitive positioning against other public sector banks reveals both strengths and weaknesses. Versus State Bank of India, Canara Bank is David against Goliath—SBI's ₹45 lakh crore balance sheet dwarfs Canara's ₹15 lakh crore. But size brings inertia; Canara Bank's smaller scale allows faster decision-making and better customer service scores. Against Punjab National Bank and Bank of Baroda, Canara Bank's southern stronghold provides stability—South Indian states have better credit culture, lower NPAs, and higher savings rates.

The private bank comparison is more troubling. HDFC Bank's return on assets is 1.9% versus Canara's 0.8%. ICICI Bank approves retail loans in 10 minutes; Canara Bank takes 10 days. Kotak Mahindra Bank's cost-to-income ratio is 42%; Canara's is 47%. These aren't just numbers but symptoms of structural disadvantages—government ownership imposes constraints private banks don't face.

The CASA ratio game deserves special attention. That 32.29% ratio looks healthy, but decomposition reveals vulnerability. Government department accounts contribute 35% of CASA—stable but non-profitable, as government accounts demand premium service while paying no fees. Salary accounts form another 30%, but these are increasingly footloose, with customers maintaining minimum balances while parking surplus funds in mutual funds. True retail CASA—grandmothers' savings accounts, traders' current accounts—is growing slowest.

Risk management post-merger has improved dramatically. The consolidated entity's larger balance sheet provides better diversification. The combined risk management team brings expertise from both banks—Syndicate Bank's agricultural lending experience complements Canara Bank's corporate credit skills. The gross NPA of 4.23% is manageable, with provision coverage at 89.10%, suggesting conservative accounting.

But new risks emerge faster than old ones resolve. Cyber risk wasn't a board agenda item a decade ago; now it's the first discussion at every meeting. Climate risk seemed academic until floods destroyed collateral worth ₹500 crores in a single monsoon. Reputation risk in the social media age means a single viral video of poor customer service can trigger deposit withdrawals worth crores.

The efficiency metrics tell a story of gradual improvement hitting natural limits. Cost-to-income at 47% has dropped from 52% pre-merger, but further improvement requires investments that worsen the ratio before improving it. Branches can't be closed without political backlash. Employees can't be laid off due to union agreements. Technology investments are necessary but expensive. The bank is trapped in what consultants call the "efficiency paradox"—needing to spend money to save money when margins are already tight.

The market share data reveals strategic positioning. In home loans, Canara Bank holds 4.8% market share, respectable but facing pressure from housing finance companies offering doorstep service. In agricultural loans, the 8.2% share reflects historical strength but also regulatory compulsion. In corporate lending, the 5.5% share is declining as companies access bond markets. The growth areas—personal loans, credit cards—show low single-digit shares, suggesting missed opportunities or deliberate risk aversion.

Capital allocation remains contentious. The government owns 62.93%, providing stability but limiting flexibility. Every major decision requires government approval, from opening overseas branches to employee bonuses. Capital raising through equity dilution faces political resistance. The bank generates sufficient internal capital for 15% annual growth, but the market demands 20%. This mathematical impossibility forces strategic choices—grow slower than competitors or accept higher risk.

The cross-selling metrics reveal untapped potential. The average customer uses 2.3 products, compared to 4.1 at private banks. A customer with a savings account rarely takes a loan from the same branch. A corporate client using cash management services banks personally elsewhere. The data exists to identify opportunities, but organizational silos prevent execution. The retail banking head and corporate banking head report to the same CEO but might as well work for different companies.

Distribution strategy faces fundamental questions. Digital channels are growing but branches still originate 70% of loans. Urban branches are profitable but saturated. Rural branches fulfill social mandates but lose money. The solution seems obvious—digital for transactions, branches for relationships—but execution requires capabilities the bank is still building.

The partnership ecosystem offers hope and complexity. Fintech partnerships provide technology without capital investment. The bank partners with Paytm for payment solutions, with LendingKart for SME loans, with Pine Labs for point-of-sale systems. But each partnership involves revenue sharing, data sharing, and brand dilution. The bank provides the balance sheet and regulatory cover while partners provide innovation and customer experience—a marriage of convenience that neither party fully trusts.