BSE Limited: Asia's Oldest Stock Exchange Reinvents Itself

I. Cold Open & Episode Setup

The morning of February 3, 2017, marked one of the most surreal moments in the history of global capital markets. At 9:15 AM, as trading bells rang across Mumbai's financial district, BSE Limited—Asia's oldest stock exchange, guardian of India's financial heritage for 142 years—began trading on the National Stock Exchange. The irony was inescapable: the grand old institution that had birthed Indian capitalism was now just another ticker symbol on its younger rival's screens.

This wasn't merely a listing. It was a capitulation wrapped in a triumph, a surrender disguised as strategy. How does an institution that predates the telephone, survived two world wars, weathered independence, and outlasted the British Empire find itself seeking validation from a competitor barely two decades old?

The answer lies not in BSE's failures but in one of the most dramatic transformations in financial history. From traders gathering under banyan trees in colonial Bombay to executing trades in six microseconds—faster than any other exchange on Earth—BSE's journey mirrors India's own evolution from colony to economic powerhouse. This is a story about what happens when tradition collides with technology, when monopolies meet markets, and when the very definition of a stock exchange gets rewritten by algorithms and regulations.

Today, BSE processes millions of transactions daily across equities, derivatives, commodities, and mutual funds. Its market capitalization exceeds $5 trillion, making it the sixth-largest exchange globally. Yet for all its modern prowess, BSE carries the weight of history—sometimes as armor, often as anchor. Understanding how this institution navigated from exclusive brokers' club to public corporation, from outcry pits to co-location servers, from domestic monopoly to global competitor, offers profound lessons about institutional reinvention.

The paradox deepens when you consider that BSE achieved something seemingly impossible: it became the fastest stock exchange in the world while being the oldest in Asia. It's as if the Vatican had somehow won the space race. This transformation didn't happen through disruption or revolution—it happened through a painful, decade-long metamorphosis that forced BSE to shed its very identity to survive.

What follows is the complete story of how native Indian traders created their own Wall Street under colonial rule, built a financial system from scratch, lost their monopoly to a government-backed startup, and then clawed their way back to relevance through sheer technological audacity. It's about power, politics, and the price of progress. Most importantly, it's about what happens when an institution must choose between its legacy and its future—and somehow manages to preserve both.

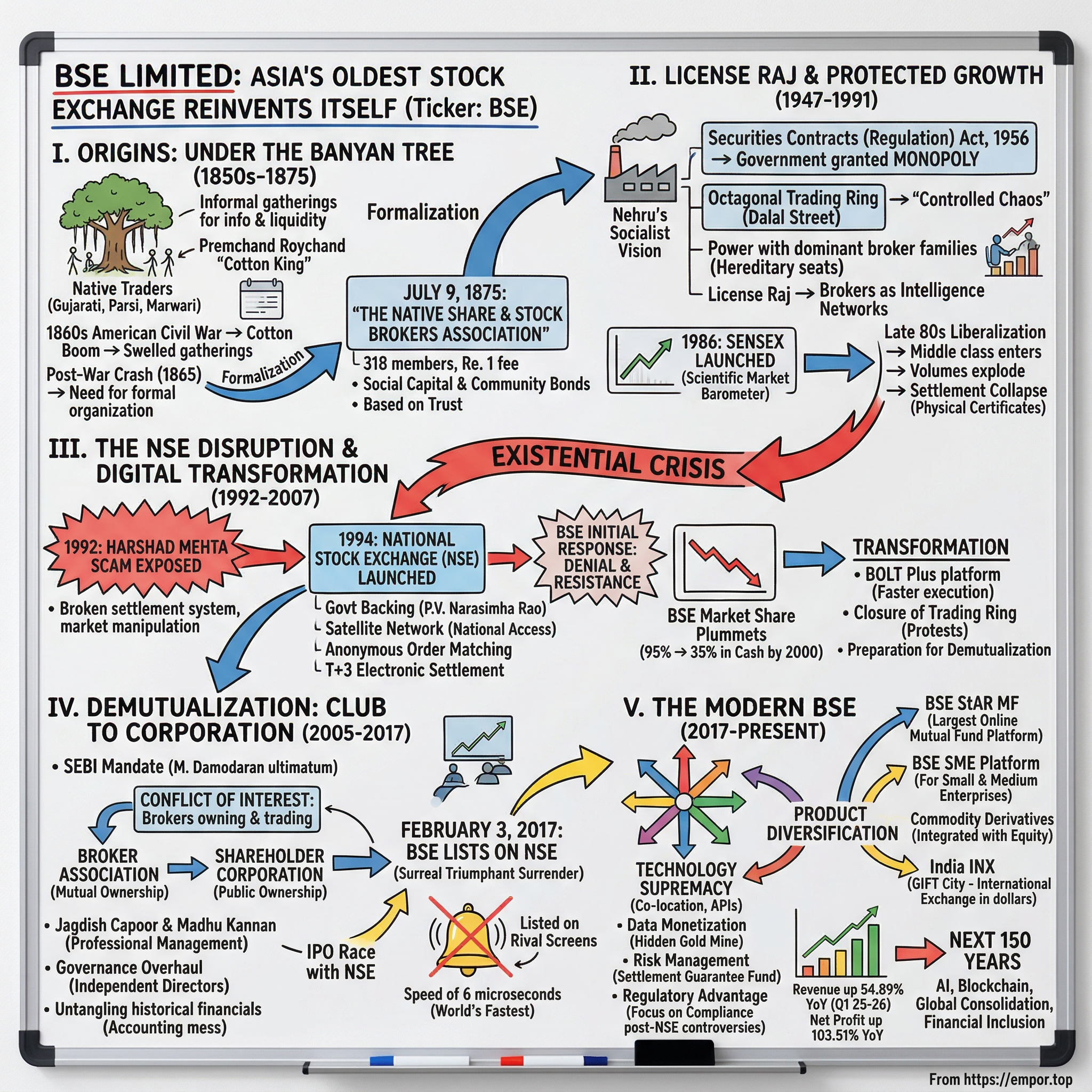

II. Origins: Under the Banyan Tree (1850s-1875)

Picture Bombay in 1850: a humid, chaotic port city where cotton bales competed with spice sacks for dock space, where British merchants in tropical whites brushed past Parsi traders in traditional garb, where fortunes changed hands based on ships appearing on the horizon. The city's commercial heart beat strongest at the intersection of Meadows Street and what locals would later call Dalal Street—literally, "Broker Street." Here, under the spreading canopy of an ancient banyan tree, a peculiar ritual played out each afternoon.

As the sun reached its zenith, driving British administrators to their clubs for gin and tonic, a different sort of gathering materialized. Gujarati merchants, Parsi industrialists, Marwari traders—men whose combined net worth could buy small kingdoms—assembled in the tree's shade. They came not for the relief from heat but for something more valuable: information. In an era before telegraphs reached every corner of India, before standardized pricing, before regulated markets, these men were creating liquidity where none existed.

Premchand Roychand understood this better than most. Born into a prominent Jain family, Roychand possessed that rare combination of mathematical brilliance and social magnetism that marks great market makers. While his British counterparts traded in the comfort of colonial clubs, Roychand recognized that real price discovery happened in the streets, in the casual conversations between men who actually moved goods across oceans. By 1855, he had become the unofficial coordinator of these banyan tree gatherings, keeping mental ledgers of who owned what, who needed capital, who had ships arriving next month.

The American Civil War changed everything. When Confederate ports closed in 1861, Manchester's cotton mills—the beating heart of the Industrial Revolution—suddenly faced starvation. India's cotton, previously considered inferior, became liquid gold overnight. Prices quadrupled, then quintupled. Ships that once carried 100 bales now carried 1,000. The banyan tree gatherings swelled from dozens to hundreds. Roychand, who had positioned himself perfectly, became arguably the richest Indian of his generation, earning the title "Cotton King" and "Bullion King" simultaneously.

But Roychand saw beyond the cotton boom. He recognized that these informal gatherings had created something unprecedented: a native Indian capital market operating parallel to, but independent from, British financial control. The colonial government, focused on resource extraction, had never bothered creating sophisticated financial infrastructure for Indians. This oversight became Roychand's opportunity. In 1868, he began formalizing what had been informal, documenting what had been verbal, standardizing what had been chaotic.

The transformation accelerated after the cotton crash of 1865. When the American Civil War ended, cotton prices collapsed as dramatically as they had risen. Fortunes evaporated. Roychand himself lost everything, dying bankrupt in 1866. Yet the infrastructure he'd begun creating survived. The remaining brokers, having learned the harsh lessons of unregulated speculation, recognized the need for formal organization. They moved from the banyan tree to a building at Dalal Street, establishing membership criteria, trading hours, and settlement procedures.

On July 9, 1875, this evolution culminated in the formation of "The Native Share & Stock Brokers Association." The word "native" wasn't accidental—it was defiant. In colonial India, "native" typically carried condescension, implying inferior or primitive. These brokers reclaimed it, wearing it as a badge of pride. This was their exchange, built by Indians, for Indians, operating under Indian social norms of trust and reciprocity that British observers never quite understood.

The original association consisted of 318 members, each paying a then-princely sum of Re. 1 as entrance fee. They created their own admissions process, their own code of conduct, their own dispute resolution mechanisms. The British colonial government, initially suspicious, gradually realized that this native institution actually served their interests by channeling Indian capital into productive enterprises rather than hoarding or land speculation.

What made BSE unique wasn't just its indigenous origins but its social architecture. Unlike Western exchanges built on legal contracts and formal enforcement, BSE operated on community bonds. Gujarati merchants trusted each other because their families had intermarried for generations. Parsi industrialists honored agreements because reputation in their tight-knit community mattered more than legal documents. This social capital became BSE's greatest asset, enabling trades worth millions of rupees to execute on verbal commitments alone.

The exchange's early years established patterns that would persist for a century. Power concentrated among a few dominant broker families who controlled both access and information. Trading remained as much about relationships as economics. The physical proximity of traders—literally standing shoulder-to-shoulder in the ring—created an intimacy that electronic trading would later destroy. These weren't just market participants; they were a community with shared festivals, shared losses, shared destinies.

The building at Dalal Street became more than a trading venue—it evolved into the nerve center of Indian capitalism. Every major business house, from the Tatas to the Birlas, would eventually need to court these brokers. Every government policy affecting commerce would be debated here first. Every economic tremor, from monsoon failures to global wars, would register first in the frantic hand signals and shouted prices of the trading ring.

Yet for all its early sophistication, BSE remained fundamentally a 19th-century institution. Trades were recorded in handwritten ledgers. Price discovery happened through open outcry. Settlement took days or weeks. Information traveled at the speed of human runners. The exchange that would one day execute trades in microseconds was born in an era when the fastest communication technology was the telegraph, and even that was a luxury reserved for the colonial government.

The banyan tree still stands on Dalal Street, now dwarfed by glass towers housing algorithmic trading firms. It's been designated a heritage structure, a reminder of when finance was personal, when markets were physical, when trust came from knowing your counterparty's grandfather. The transition from that tree to today's BSE—processing millions of electronic trades daily—represents not just technological evolution but a fundamental reimagining of what a stock exchange could be. That transformation would take another century to unfold, through independence, scandal, competition, and ultimately, a complete reinvention of BSE's very identity.

III. The License Raj Era & Protected Growth (1947-1991)

The stroke of midnight on August 15, 1947, brought freedom to India and unexpected power to BSE. As British administrators sailed home and princely states dissolved into the new republic, the Bombay Stock Exchange found itself in an extraordinary position: it was the only sophisticated financial institution that was entirely Indian, entirely private, and entirely operational. While the government scrambled to create everything from a central bank to a planning commission, BSE simply continued what it had done for 72 years—only now, without colonial oversight.

Jawaharlal Nehru's socialist vision for India created an unexpected gift for BSE: a monopoly wrapped in regulation. The Prime Minister, deeply suspicious of private capital yet pragmatic about its necessity, chose to control rather than compete. The Securities Contracts (Regulation) Act of 1956 embodied this philosophy perfectly. Rather than creating new exchanges or nationalizing existing ones, the government simply licensed BSE as the sole recognized exchange. It was easier to monitor one devil you knew than unleash several you didn't.

This regulatory embrace transformed BSE from a regional institution into a national monopoly. Every company seeking public capital had to list in Bombay. Every serious investor had to work through BSE's brokers. Every price that mattered was discovered in the octagonal trading ring at Dalal Street, where 1,800 brokers jostled, shouted, and signaled their way through each trading session. The ring itself became theater—visitors would crowd the viewing gallery to watch the controlled chaos, the elaborate hand signals indicating buy or sell, quantity, price, all executed in a standardized sign language that took years to master.

The power dynamics within the ring reflected India's evolving social hierarchies. The old Gujarati and Parsi families still dominated, but new players emerged—Marwaris who had made fortunes in independence-era trade, South Indians who brought technical expertise from nascent engineering firms, even a few Muslims who had chosen India over Pakistan and needed to quickly establish new business networks. Each community brought its own style: Gujaratis preferred steady accumulation, Parsis favored industrial stocks, Marwaris excelled at arbitrage, South Indians introduced analytical rigor.

K.R.P. Shroff embodied this era's contradictions perfectly. A second-generation broker who had inherited his father's seat, Shroff understood that BSE's monopoly was both blessing and curse. As BSE's president through multiple terms in the 1960s and 70s, he modernized operations while fiercely protecting broker privileges. Under his leadership, BSE introduced its first calculating machines, standardized contract notes, even experimented with early computers. Yet he also ensured that membership remained hereditary, that trading stayed physical, that power remained concentrated among a few dozen families.

The License Raj—India's byzantine system of permits and quotas—paradoxically strengthened BSE's position. Since private companies needed government permission for everything from importing machinery to expanding capacity, their valuations became puzzles that only insiders could solve. Which firm had secured a coveted license? Whose application was stuck in bureaucratic limbo? This information asymmetry made BSE's brokers invaluable. They didn't just execute trades; they were intelligence networks, using family connections, club memberships, and carefully cultivated sources to divine which stocks would move.

Then came 1986, and with it, BSE's most enduring creation: the SENSEX. The Sensitive Index, developed with S&P, gave India its first scientific market barometer. Thirty stocks, weighted by market capitalization, selected to represent the economy's commanding heights. The number would become as important to Indian households as monsoon predictions. "SENSEX ne kya kiya?"—What did the SENSEX do?—entered everyday vocabulary. The index gave BSE something invaluable: a brand that transcended the institution itself.

The SENSEX launch coincided with Rajiv Gandhi's tentative liberalization efforts. The young Prime Minister, enamored with technology and impatient with socialist orthodoxy, began dismantling some License Raj restrictions. Foreign institutional investors received limited entry. Private mutual funds gained approval. The equity cult, dormant since independence, suddenly revived. Middle-class Indians, who had traditionally parked savings in gold or fixed deposits, discovered the stock market. BSE's daily turnover jumped from a few crores to hundreds of crores.

This boom created BSE's first existential crisis: the settlement system collapsed under volume. The exchange still operated on a 14-day settlement cycle, with physical share certificates shuttling between buyers and sellers. As volumes exploded, the back office couldn't cope. Trades failed. Disputes multiplied. Bad delivery—shares that couldn't be transferred due to signature mismatches or fake certificates—became epidemic. The exchange that had operated on trust for a century suddenly faced a trust deficit.

Regional stock exchanges, previously content as BSE satellites, began asserting independence. Calcutta, Madras, Delhi—each developed its own trading ecosystem, its own listed companies, its own broker networks. While none could challenge BSE's dominance in blue-chip stocks, they eroded its monopoly at the margins. The government, recognizing the danger of single-point failure, encouraged this fragmentation. By 1990, India had 19 recognized exchanges, though BSE still commanded 70% of total turnover.

The protected environment bred complacency. BSE's governing board, dominated by broker-members, prioritized their interests over market development. Technology adoption lagged global standards by decades. While exchanges in New York, London, and Tokyo experimented with electronic systems, BSE's brokers insisted that physical trading's "price discovery through human interaction" couldn't be replicated by machines. They weren't entirely wrong—the ring's information density, with hundreds of simultaneous negotiations visible to all participants, did enable remarkable price efficiency. But they missed how technology could democratize access, reduce costs, and eliminate human error.

By 1991, contradictions accumulated to a breaking point. The exchange processing India's capitalist aspirations operated like a medieval guild. The institution meant to allocate capital efficiently was itself inefficiently managed. The market that should have been transparent was opaque to all but insiders. BSE had become simultaneously indispensable and inadequate, powerful yet vulnerable. The protected monopoly that had seemed like permanent privilege was about to face its greatest challenge.

The stage was set for disruption. It would arrive not through gradual reform or internal revolution but through scandal, crisis, and a government-backed competitor designed explicitly to destroy BSE's comfortable oligopoly. The Harshad Mehta securities scam of 1992 would provide the crisis. The National Stock Exchange would become the competitor. Together, they would force BSE to confront a brutal question: evolve or die.

IV. The NSE Disruption & Digital Transformation (1992-2007)

Harshad Mehta drove a Lexus—an almost mythical vehicle in 1991 India, where imported cars required permits that cost more than the cars themselves. The "Big Bull," as media christened him, had discovered something that BSE's old guard desperately wanted hidden: the settlement system was so broken that anyone clever enough could manufacture money from thin air. Using a financial instrument called the "Ready Forward" deal, Mehta borrowed money from banks, leveraged BSE's 14-day settlement cycle, pumped stocks to astronomical levels, sold at peaks, and repeated the cycle. When Associated Cement Company jumped from ₹200 to ₹9,000 in three months, even naive investors knew something was wrong.

The scam's unraveling in April 1992 exposed more than Mehta's fraud—it revealed BSE's structural rot. The exchange's response was telling: instead of comprehensive reform, the broker-dominated board proposed cosmetic changes. They would reduce the settlement cycle from 14 to 7 days. They would increase margin requirements slightly. They would create a "surveillance committee." What they wouldn't do was embrace electronic trading, eliminate physical certificates, or break the broker cartel's stranglehold on governance. This intransigence would cost them everything.

R.H. Patil saw opportunity in this chaos. A career bureaucrat with an economics PhD, Patil had spent years studying global exchanges. He understood that technology wasn't just about efficiency—it was about trust. Electronic systems created audit trails. Automated matching eliminated manipulation. Depositories removed fake certificates. When the government asked him to design a new exchange that would break BSE's monopoly, Patil didn't just propose competition; he proposed revolution.

The National Stock Exchange launched on November 3, 1994, with a weapon BSE couldn't match: political backing. Prime Minister P.V. Narasimha Rao, architect of India's economic liberalization, personally championed NSE. The Finance Ministry provided initial capital. Public sector financial institutions became anchor investors. SEBI, the newly empowered regulator, fast-tracked every approval. This wasn't David versus Goliath—this was Goliath's own father sending a younger, stronger son to destroy him.

NSE's first innovation seemed simple: a satellite-based trading network connecting cities across India. Suddenly, an investor in Chennai could trade as easily as one in Bombay. The second innovation was devastating: anonymous order matching. On BSE, every trade revealed counterparties, enabling manipulation and front-running. NSE's system showed only prices and quantities. The third innovation was existential: T+3 rolling settlement with electronic confirmation. What took BSE weeks now took NSE days.

BSE's initial response was denial. Chairman Mahendra Kampani dismissed NSE as a "government experiment that will fail like all government experiments." The old guard believed their relationships, accumulated expertise, and institutional memory were irreplaceable. They were wrong. By 1995, NSE's daily volumes exceeded BSE's. By 1996, NSE dominated the derivatives market BSE hadn't even entered. By 1997, foreign institutional investors traded almost exclusively on NSE.

The exodus began slowly, then accelerated. Junior brokers, frustrated by BSE's hereditary hierarchy, defected to NSE where merit mattered more than lineage. Technology companies, seeing BSE's reluctance to modernize, partnered exclusively with NSE. Most damaging, corporations began dual-listing, then primarily listing on NSE. When Infosys—poster child of India's IT revolution—chose NSE for its IPO, the symbolism was unmistakable: BSE represented the past, NSE the future.

Panic finally pierced BSE's complacency. In March 1995, the exchange grudgingly accepted CMC Ltd's offer to digitize operations. The Bombay Online Trading System (BOLT) launched with great fanfare but little conviction. Brokers sabotaged implementation, claiming technical glitches when they simply preferred the old system. The trading ring remained active alongside BOLT, creating two parallel markets with different prices for the same securities. International investors, confused by this duality, simply avoided BSE altogether.

The numbers told a brutal story. BSE's market share in cash equities plummeted from 95% in 1994 to 35% by 2000. In derivatives—the future of global markets—BSE barely registered while NSE captured 99%. Daily turnover, once BSE's monopoly, shifted decisively to NSE. The financial press, once reverential toward Asia's oldest exchange, now portrayed it as a dinosaur awaiting extinction.

Jagdish Capoor's appointment as BSE chairman in 2001 marked the beginning of serious transformation. A banker rather than broker, Capoor understood that BSE needed cultural revolution, not just technological evolution. He forced the closure of the trading ring despite violent protests. He mandated BOLT for all trades. He recruited technology professionals from India's booming IT sector. Most importantly, he began preparing BSE for demutualization—the separation of ownership from trading rights that would break the broker cartel's control.

The technology transformation was staggering in scope. BSE didn't just need to match NSE's capabilities; it needed to leapfrog them. The exchange invested hundreds of crores in new systems: BOLT Plus for faster execution, BEST for real-time risk management, WebEx for internet trading. Response times dropped from seconds to milliseconds. System capacity increased from thousands to millions of orders daily. The exchange that had resisted computers now ran entirely on them.

Yet technology alone couldn't restore BSE's position. The network effects that once worked in BSE's favor now worked against it. Liquidity attracts liquidity. Once NSE became the primary market for most stocks, buyers and sellers naturally gravitated there. BSE found itself in a vicious cycle: lower volumes meant wider spreads, wider spreads deterred traders, fewer traders meant lower volumes. Breaking this cycle would require more than better technology—it would require reimagining BSE's very purpose.

The derivatives debacle illustrated this perfectly. When SEBI finally allowed BSE to launch derivatives in 2000—six years after NSE—the exchange discovered that being second in a winner-take-all market meant being irrelevant. Despite offering identical products with lower fees, BSE couldn't attract traders. NSE's first-mover advantage had crystallized into permanent dominance. BSE's derivatives segment, launched with great hope, languished with less than 1% market share.

Regional stock exchanges, watching this battle of titans, quietly died. Exchanges in Pune, Kanpur, and Mangalore—once vital to local capital formation—couldn't compete with electronic networks. By 2005, India effectively had just two exchanges: NSE dominating with 70% market share, BSE surviving with 30%. The fragmented landscape of 19 exchanges had consolidated into a duopoly, with one player clearly winning.

The humiliation reached its nadir in 2004 when BSE had to adopt NSE's technology standards for straight-through processing. The exchange that had created India's capital markets was now following its junior competitor's technical specifications. Industry conferences that once featured BSE executives explaining Indian markets to global audiences now showcased NSE leaders while BSE representatives sat in the audience.

Yet beneath this surface defeat, transformation was occurring. A new generation of BSE employees—engineers rather than clerks, MBAs rather than hereditary appointees—was rebuilding the exchange's technical foundation. The broker stranglehold was weakening as demutualization approached. International partnerships with Deutsche Börse and Singapore Exchange brought global expertise. The exchange that had resisted change for decades was finally changing at breakneck speed.

By 2007, BSE had achieved technical parity with NSE. Both exchanges offered electronic trading, T+2 settlement, derivatives products, and internet access. But parity wasn't enough. BSE needed differentiation, new revenue streams, and most importantly, governance reform that would convince investors it had truly transformed. That would require the most radical change in its 132-year history: converting from a broker-owned association to a shareholder-owned corporation, listing its own shares for public trading, and submitting to the market discipline it had administered to others for over a century.

V. Demutualization: From Club to Corporation (2005-2017)

The annual general meeting of 2005 felt like a funeral. BSE's trading floor, once alive with the chaos of open outcry, sat silent as 200 broker-members gathered to vote on their own dispossession. The resolution was simple in language, revolutionary in implication: convert BSE from a broker-owned association to a shareholder-owned corporation. After four hours of acrimonious debate, where old-timers invoked everything from tradition to treason, the vote passed by the narrowest margin. The brokers had chosen survival over sovereignty.

SEBI's demutualization mandate wasn't a suggestion—it was an ultimatum delivered with surgical precision by Chairman M. Damodaran. A former bureaucrat who understood power better than most, Damodaran recognized that BSE's broker-ownership model created intractable conflicts of interest. Brokers who owned the exchange also traded on it, regulated themselves, and set rules that advantaged insiders over investors. The same person could be defendant, prosecutor, judge, and jury. This incestuous arrangement, tolerable in protected markets, became untenable in competitive, globalized ones.

The international context made resistance futile. Every major exchange—NYSE, London, Deutsche Börse, Tokyo—had demutualized. The model was proven: separation of ownership from trading rights increased valuations, improved governance, and attracted capital. Stockholm's exchange saw its value triple post-demutualization. Australia's ASX became a billion-dollar company. These weren't abstract case studies but concrete examples that SEBI cited repeatedly, bludgeoning BSE's old guard with evidence of their own obsolescence.

The actual transformation required unwinding 130 years of embedded privilege. Each broker-member owned one share in BSE Ltd, carrying equal voting rights regardless of trading volume or contribution. Under the new structure, these shares would be converted to equity with economic value but limited voting power. Trading rights would be separated from ownership. Anyone could own BSE shares, but only qualified entities could trade. The democratization was radical: the same brokers who had inherited seats from their grandfathers would now compete with algorithm-armed institutions for trading access.

Madhu Kannan's appointment as CEO in 2009 accelerated the corporate transformation. Unlike previous administrators who emerged from BSE's internal ranks, Kannan came from Bank of America, bringing Wall Street sensibilities to Dalal Street. He understood that demutualization without professionalization was meaningless. Under his leadership, BSE recruited from IITs and IIMs rather than broker families. Performance metrics replaced patronage. Revenue targets superseded relationship management.

The governance overhaul was systematic. Independent directors—former regulators, technology experts, distinguished academics—joined the board, outnumbering broker representatives. Audit committees gained real power. Risk management moved from afterthought to obsession. Compliance, previously managed by a single officer, expanded into a department larger than entire regional exchanges. The transformation wasn't just structural but cultural: BSE was learning to think like a corporation rather than a club.

The IPO preparation revealed just how difficult this metamorphosis was. Investment bankers from Kotak and Axis, conducting due diligence, discovered accounting practices that belonged in museums. Revenue recognition was inconsistent. Related-party transactions were labyrinthine. Historical financials needed complete restatement. The process that typically took months stretched to years as BSE untangled decades of informal arrangements, gentleman's agreements, and off-book understandings.

The regulatory approval process became Kafkaesque. SEBI, having mandated demutualization, now scrutinized every detail with paranoid intensity. The prospectus went through 17 drafts. Every broker settlement from the past decade was audited. The exchange's technology infrastructure underwent stress tests that simulated nuclear war. The irony wasn't lost on observers: BSE, which had operated for a century on trust, now needed thousands of pages of documentation to prove its trustworthiness.

Meanwhile, NSE faced its own demutualization drama, but with a crucial difference: as a corporation from inception, its transformation was simpler. This asymmetry added urgency to BSE's efforts. If NSE listed first, it would capture the "exchange stock" premium, leaving BSE to follow as a lesser alternative. The race to IPO became existential. Internal presentations showed stark projections: list first and achieve a $2 billion valuation, list second and accept $500 million.

The breakthrough came through financial engineering rather than operational improvement. BSE's real estate—prime property in Mumbai's most expensive district—was worth more than its exchange operations. The company owned not just the iconic building at Dalal Street but surrounding properties accumulated over decades. Revaluation at market prices added hundreds of crores to the balance sheet. Suddenly, BSE wasn't just a struggling exchange but a valuable real estate company that happened to run a stock market.

By 2016, the pieces finally aligned. The broker shareholding had been diluted to 43.56% through strategic stake sales to foreign investors (20.72%), domestic institutions (9.05% to LIC alone), and public shareholders (21.99%). The ownership structure that had concentrated power among a few dozen families now distributed it across thousands of shareholders. The exchange that had resisted transparency now published quarterly results with the detail of a Fortune 500 company.

The IPO process itself became theater. BSE couldn't list on itself—SEBI regulations prohibited such circular arrangements. The only option was listing on NSE, its bitter rival. The symbolism was devastating: Asia's oldest exchange would make its public debut on the platform that had nearly destroyed it. NSE, sensing the historic moment, extracted maximum advantage. They demanded full compliance with their listing requirements, charged standard listing fees without discount, and scheduled the listing ceremony for maximum visibility.

January 23, 2017, marked the IPO launch—an offer for sale of 1.54 crore shares, priced at ₹805-806 per share. The response was tepid: barely 2x subscription compared to the 10x+ oversubscription typical for hot IPOs. Institutional investors remained skeptical about BSE's ability to compete with NSE. Retail investors, BSE's traditional base, largely ignored their own exchange's offering. The muted response was its own verdict on BSE's diminished status.

The listing ceremony on February 3, 2017, was surreal. BSE executives, dressed in their finest, stood in NSE's modern building as their company's ticker appeared on their rival's screens. Ashishkumar Chauhan, BSE's CEO since 2012 (and ironically, NSE's former deputy CEO), rang NSE's opening bell with a frozen smile. The media coverage focused entirely on the irony rather than the achievement. Headlines read "David Lists on Goliath" and "The Ultimate Surrender."

Yet beneath the humiliation lay transformation. The listed BSE was fundamentally different from the association it had been. Market discipline replaced broker politics. Quarterly earnings calls forced transparency. Shareholder activism demanded performance. The stock price—publicly visible, constantly judged—became the ultimate accountability mechanism. BSE's shares, opening at ₹999, would become a report card updated every second of every trading day.

The demutualization journey had taken 12 years from conception to completion, far longer than any global precedent. But the delay reflected the complexity of unwinding not just legal structures but social ones. BSE hadn't simply changed its ownership—it had changed its very identity. The broker's club had become a public corporation. The guardian of tradition had embraced disruption. The monopolist had accepted competition.

The transformation's success would be measured not by the IPO's reception but by BSE's ability to leverage its new structure for growth. Corporate status enabled international partnerships impossible under the association model. Listed shares became currency for acquisitions. Professional management could make decisions without broker approval. The exchange that had spent a decade preparing to list now had to prove it deserved its listing.

VI. The Modern BSE: Products, Technology & Strategy (2017-Present)

The co-location servers hummed at exactly 18.5 degrees Celsius in BSE's data center, their temperature controlled to the decimal because microseconds matter when you're the world's fastest exchange. Six microseconds—that's BSE's response time, a number that Ashishkumar Chauhan repeats with the pride of a parent announcing their child's academic achievements. To put this in perspective: light itself, traveling at 300,000 kilometers per second, moves just 1.8 kilometers in six microseconds. BSE processes trades faster than a beam of light can travel from Marine Drive to Dalal Street.

This technological supremacy didn't emerge from Silicon Valley consultants or foreign partnerships but from a deliberate decision to make speed BSE's differentiator. When competing on liquidity seemed impossible—NSE controlled 90% of derivatives volume—BSE chose to compete on latency. The strategy was counterintuitive: become the Formula 1 car of exchanges in a market where most traders still drove Ambassador cars. Build it, the thinking went, and the algorithms will come.

The BOLT Plus platform, BSE's technological backbone, processes 200,000 messages per second per partition, with capacity to scale to 1.5 million. These aren't just numbers but weapons in the high-frequency trading wars where fortunes are made in microseconds. The architecture is deliberately over-engineered: if BSE's current volume requires a pipeline, they've built an ocean. This excess capacity sends a message to algorithmic traders: bring your most demanding strategies, and our systems won't blink. Looking at the current landscape, BSE's market capitalization stands at ₹97,183 crore, a testament to its remarkable transformation. The revenue jumped 54.89% year-over-year to ₹1,072.69 crore in Q1 2025-2026, while net profit jumped 103.51% to ₹539.41 crore in the same period. These aren't just numbers—they represent the culmination of a decade-long technological revolution that transformed BSE from a laggard to a leader in execution speed.

The product diversification strategy reflects sophisticated portfolio thinking. BSE StAR MF has emerged as India's largest online mutual fund platform, processing over 27 lakh transactions monthly. This isn't competing with NSE on their turf—it's creating entirely new battlegrounds. The platform aggregates mutual fund transactions from across the industry, earning fees not from trading but from processing and settlement. It's the plumbing of India's mutual fund industry, unglamorous but essential.

The SME platform tells another story of finding niches within niches. BSE SME, India's largest platform for small and medium enterprises, has listed over 500 companies that would never qualify for main board listing. These aren't tech unicorns or industrial giants but family businesses from tier-2 cities seeking growth capital. A textile manufacturer from Surat, a spice exporter from Guntur, a auto-parts supplier from Ludhiana—BSE provides them access to public markets that NSE, focused on blue-chips and derivatives, largely ignores.

The commodity derivatives launch in October 2018 seemed late—MCX had dominated this space for years. But BSE's entry coincided with SEBI's universal exchange framework, allowing integrated trading across asset classes. Traders could now hedge equity positions with commodity futures on the same platform, using the same margins, with unified settlement. The integration advantage compensated for the late start.

India International Exchange (India INX), launched December 30, 2016, at GIFT City, represents BSE's most ambitious bet. As India's first international exchange, it operates in dollars, trades 22 hours daily, and offers tax advantages that make Mumbai competitive with Singapore or Dubai. The timing was perfect: just as Indian companies began raising global capital and foreign investors sought Indian exposure without currency risk, BSE created the infrastructure to facilitate both.

The partnerships reveal strategic sophistication. Deutsche Börse brought European market structure expertise. Singapore Exchange provided derivatives know-how. These weren't vanity associations but technology transfers. BSE learned how Germans achieve sub-microsecond latency, how Singaporeans manage multi-currency settlement, how global exchanges monetize data. The student was studying to become the teacher.

But the real transformation happened in the derivatives segment. BSE's derivatives segment achieved a daily premium turnover of Rs 8,758 crore in Q3 FY25, compared to Rs 2,550 crore in the year-ago period. This wasn't organic growth—it was the result of regulatory intervention. When SEBI introduced interoperability, allowing trades executed on one exchange to be settled through another's clearing corporation, it broke NSE's monopolistic advantage. Suddenly, BSE could compete on execution while leveraging others' settlement infrastructure.

The single stock derivatives relaunch in July 2024 showcased this new competitive dynamic. Rather than challenging NSE's weekly expiries head-on, BSE chose mid-month expiries—the second Thursday. It's a classic flanking maneuver: don't fight where the enemy is strongest, create a new battlefield. Early results proved promising, with 174 members participating and turnover exceeding ₹1,000 crore across futures and options.

The technology infrastructure supporting this product explosion is staggering. BSE operates primary data centers in Mumbai with disaster recovery sites in Chennai. The architecture is built for "five nines" reliability—99.999% uptime, meaning less than 5 minutes of downtime annually. Co-location services, where trading firms place their servers physically next to BSE's matching engines, generate recurring revenue with software-like margins. Every microsecond of reduced latency commands premium pricing.

Market data has become BSE's hidden gold mine. Real-time feeds, historical databases, analytics packages—information that was once given away now generates hundreds of crores annually. The exchange that once survived on transaction fees now monetizes every aspect of the trading lifecycle: pre-trade analytics, execution, post-trade processing, and data services. It's the transformation from product company to platform ecosystem.

The algo trading revolution changed BSE's customer base entirely. Where once relationship managers courted traditional brokers, now quantitative analysts design products for algorithmic funds. The exchange publishes APIs, maintains GitHub repositories, and runs hackathons. The cultural shift is profound: BSE employees now speak Python as fluently as they once spoke Gujarati.

Risk management evolved from afterthought to obsession. BSE's clearing corporation maintains a Settlement Guarantee Fund exceeding ₹4,000 crore. Margin requirements are calculated in real-time using SPAN and VAR methodologies. Position limits are enforced algorithmically. The exchange that once operated on trust now trusts nothing, monitoring everything. This paranoia is feature, not bug—in modern markets, one failed settlement can trigger systemic collapse.

The cybersecurity infrastructure reflects post-digital anxieties. BSE faces thousands of attacks daily—from script kiddies to state actors. The security operations center, staffed 24/7, uses artificial intelligence to detect anomalies. Regular "red team" exercises simulate attacks. The nightmare scenario isn't just system breach but data manipulation—imagine if someone could alter the SENSEX calculation even briefly. The reputational damage would dwarf any financial loss.

Yet for all this technological sophistication, BSE's greatest innovation might be its simplicity initiatives. The exchange that serves algorithmic traders also enables ₹500 systematic investment plans for first-time investors. Mobile apps bring market access to tier-3 cities. Regional language support makes trading accessible to non-English speakers. BSE is simultaneously racing toward the future and bringing India along.

The revenue model has transformed completely. Transaction fees, once 100% of revenue, now represent less than 40%. Data services, technology solutions, and listing fees provide diversified income streams. The company that was once hostage to daily volumes now enjoys predictable, recurring revenues. This isn't just financial engineering—it's existential insurance against the next NSE or the next disruption.

The international ambitions extend beyond GIFT City. BSE is exploring partnerships in Africa, where capital markets remain nascent. The technology and expertise developed competing with NSE could help build exchanges in Kenya, Nigeria, or Egypt. The colonized has become potential colonizer, exporting financial infrastructure to emerging markets. It's a delicious historical irony.

The numbers tell the transformation story: from struggling to match NSE's capabilities to becoming the fastest stock exchange in the world with a speed of 6 microseconds. From broker-controlled club to professionally managed corporation with almost debt-free status. From domestic focus to international ambitions. From single product to multi-asset platform. The BSE of 2024 would be unrecognizable to the brokers who voted for demutualization in 2005.

But questions remain. Can technology differentiation sustain competitive advantage when technology commoditizes rapidly? Can product diversification overcome network effects in the core derivatives market? Can BSE remain relevant if global exchanges consolidate and enter India? The answers will determine whether BSE's transformation was resurrection or merely postponement of the inevitable.

VII. The Competitive Battlefield: BSE vs NSE

The derivatives trading floor at NSE's headquarters in Bandra-Kurla Complex processes more orders in a minute than BSE handles in an hour. This stark reality—NSE commanding over 90% of India's derivatives market—defines the David-versus-Goliath dynamic that has persisted for three decades. Yet the battlefield keeps shifting, and BSE has learned that survival doesn't always mean winning; sometimes it means redefining what victory looks like.

The numbers are brutal in their clarity. NSE's average daily turnover in equity derivatives exceeds ₹80 lakh crore. BSE struggles to reach ₹10,000 crore on good days. In the cash equity segment, NSE maintains a 70% share despite BSE's 150-year head start. The options market—where retail traders now generate most exchange revenues—is virtually an NSE monopoly. These aren't competitive disadvantages; they're structural realities that no amount of technology investment or product innovation can easily overcome.

Network effects in financial markets are particularly vicious. Liquidity attracts liquidity in a self-reinforcing cycle. A trader seeking to buy Reliance Industries options goes to NSE because that's where sellers congregate. Sellers go there because buyers are there. This circular logic, once established, becomes nearly impossible to break. BSE learned this lesson painfully when it launched identical products with lower fees yet couldn't attract volumes. In markets, being cheaper means nothing if you're illiquid.

The regulatory interventions meant to level the playing field often backfired. When SEBI mandated interoperability in 2018, allowing trades on one exchange to settle through another's clearing corporation, the expectation was that BSE could compete on execution while leveraging NSE's settlement infrastructure. Instead, traders simply continued using NSE for both. Habits, once formed in financial markets, calcify into infrastructure.

Yet BSE discovered competitive advantages in unexpected places. The exchange recorded its highest-ever quarterly revenue of Rs 835.4 crore in Q3 FY25, not by beating NSE at derivatives but by dominating niches NSE ignored. The SME segment, physically settled commodity derivatives, and mutual fund processing became BSE's guerrilla warfare against NSE's conventional army.

The technology arms race reveals fascinating strategic choices. NSE invested heavily in matching engine capacity, handling millions of orders per second. BSE chose latency, achieving the six-microsecond response time that attracts high-frequency traders. NSE built for volume; BSE built for speed. Both strategies are valid, but they attract different customer segments with different economics.

The most interesting competition happens in the shadows—the battle for index supremacy. SENSEX versus NIFTY isn't just about branding; it's about derivatives contracts, ETF licenses, and global recognition. SENSEX, despite being older and more recognized domestically, has lost ground to NIFTY in the derivatives space. NSE's NIFTY options are among the world's most traded contracts. BSE's SENSEX options barely register. The index that defined Indian markets for decades now plays second fiddle to its younger rival.

Corporate listings reveal another dimension of competition. Companies once considered BSE listing prestigious—it meant joining the ranks of Tatas and Birlas. Now, NSE listing signals modernity and liquidity. When startups like Zomato or Paytm go public, they list on NSE first, treating BSE as an afterthought. This isn't just about trading volumes; it's about cultural relevance. BSE represents establishment; NSE represents disruption.

The talent war mirrors the market share battle. NSE attracts IIT graduates with promises of cutting-edge technology and market leadership. BSE recruits from the same pool but must offer higher salaries to compensate for lower prestige. The best quantitative analysts join NSE to work on India's most liquid markets. BSE gets second picks, though sometimes second picks with chips on their shoulders outperform first choices who grow complacent.

Regulatory arbitrage becomes a weapon. When NSE faced co-location controversy—allegations that some traders received preferential access to its systems—BSE positioned itself as the "clean" alternative. When NSE's former CEO faced investigation, BSE emphasized governance. These moments of competitor weakness provide rare opportunities to gain ground, though gains often prove temporary once controversies fade.

The international expansion strategies diverge tellingly. NSE pursues global investors, seeking to become the gateway for foreign capital entering India. BSE targets emerging markets, offering technology and expertise to countries building their own exchanges. NSE wants to be India's NYSE; BSE aims to be India's exchange technology exporter. Both strategies make sense given their respective positions.

Price competition proves futile in winner-take-all markets. BSE's transaction fees are often 50% lower than NSE's, yet traders gladly pay NSE's premium for liquidity. This pricing power differential—NSE can raise fees without losing customers while BSE must discount to retain them—creates a profitability gap that compounds over time. NSE's margins approach software companies'; BSE's resemble traditional services businesses.

The mutual fund platform success offers lessons in asymmetric competition. BSE didn't try to out-trade NSE; it created infrastructure for an entirely different market. The StAR MF platform processes mutual fund transactions, not stock trades. It's the difference between competing for the same pie versus baking a new one. This strategic pivot—from head-to-head competition to lateral expansion—may be BSE's template for survival.

Technology partnerships reveal contrasting philosophies. NSE builds internally, maintaining control over its technology stack. BSE partners aggressively, leveraging external expertise. NSE's approach ensures seamless integration but moves slowly. BSE's strategy enables rapid capability acquisition but creates dependency. Neither is definitively superior; both reflect organizational cultures shaped by different histories.

The commodity derivatives battle showcases how late entrants can sometimes leverage regulatory changes. BSE launched commodities just as SEBI unified regulation across asset classes. While MCX dominated commodity-only trading, BSE offered integrated equity-commodity strategies. For treasurers hedging both input costs and currency exposure, single-platform convenience outweighed MCX's liquidity advantage in pure commodity trades.

Customer segmentation strategies diverge markedly. NSE focuses on institutional clients—mutual funds, foreign investors, proprietary trading firms. These customers generate enormous volumes with relatively low service costs. BSE increasingly targets retail investors, providing education, simplified products, and regional language support. It's the classic choice between whale hunting and fishing with nets.

The derivatives innovation reveals fundamental differences in risk appetite. NSE launches products cautiously, ensuring liquidity before expansion. BSE throws everything at the wall, hoping something sticks. NSE's approach minimizes failures but misses opportunities. BSE's strategy generates numerous failures but occasionally strikes gold. The single-stock futures relaunch exemplifies this: modest success after multiple previous failures.

Market surveillance and integrity become competitive differentiators. Both exchanges invest heavily in monitoring systems, but their approaches differ. NSE emphasizes automated surveillance, using algorithms to detect manipulation. BSE combines technology with human expertise, leveraging its institutional memory of past scams. When SEBI investigates market manipulation, BSE's historical perspective sometimes provides insights NSE's pure data approach misses.

The real competition might not be with each other but with global exchanges eyeing India's growth. If regulatory barriers fall, CME or ICE could enter India directly or through acquisition. In that scenario, BSE and NSE might need to cooperate for survival. The bitter rivals of today could become strategic allies tomorrow, united against foreign competition.

BSE's derivatives segment sustained its growth trajectory with a daily premium turnover of Rs 8,758 crore, showing momentum despite NSE's dominance. This growth, while impressive in isolation, still represents less than 1% of NSE's derivatives volume. It's the paradox of BSE's competitive position: growing rapidly yet falling further behind in relative terms.

The infrastructure investments reveal long-term thinking despite short-term pressures. BSE spending on technology infrastructure exceeds its profits some quarters, betting that superior execution will eventually attract volumes. NSE, with established dominance, invests more selectively. It's the difference between playing catch-up and playing defense.

Looking ahead, the competitive dynamics seem set in stone yet surprisingly fluid. NSE's dominance appears unassailable, yet BSE continues finding profitable niches. The war is lost, but battles remain winnable. Perhaps that's the ultimate lesson: in markets, as in life, survival itself is a form of victory.

VIII. Power Dynamics & Governance Evolution

The boardroom at BSE's headquarters tells its own story of power transition. Where once sat hereditary broker-kings who inherited their seats like feudal titles, now sit former RBI governors, technology entrepreneurs, and independent directors with Harvard MBAs. The portraits on the walls—generations of broker-chairmen in traditional attire—look down at board meetings now conducted in English rather than Gujarati, reviewing PowerPoints instead of handwritten ledgers, discussing algorithms instead of relationships.

The transformation from broker-controlled association to professionally managed corporation wasn't just structural—it was a revolution in power dynamics that played out over two decades. The old guard didn't surrender willingly. They fought every change, every regulation, every dilution of their control with the tenacity of an entrenched aristocracy sensing its own obsolescence.

Consider the pre-demutualization power structure: 200 broker-members, each owning one share, each carrying equal voting rights regardless of their contribution to revenues or trading volumes. The Jhunjhunwala family, trading millions daily, had the same vote as a dormant member who hadn't executed a trade in years. This wasn't democracy; it was oligarchy masquerading as equality. Real power concentrated among two dozen families who controlled key committees, decided market rules, and essentially regulated themselves.

The first crack in this edifice came through generational change. The sons and daughters of traditional brokers, educated at IIMs and Whartons, returned with different ideas. They had seen electronic trading at NYSE, studied market microstructure at university, understood that BSE's clubby atmosphere was anachronistic. Yet they faced the impossible position of reformers within a system that rewarded conformity. Many chose to leave, joining foreign banks or starting their own funds, creating a brain drain that weakened BSE from within.

SEBI's regulatory assertiveness under Chairman M. Damodaran fundamentally altered power equations. Damodaran, a former insurance regulator who understood institutional capture, systematically dismantled broker privileges. Trading rights were separated from ownership. Broker representation on boards was capped. Independent directors were mandated. Each reform faced legal challenges, with brokers arguing that SEBI was exceeding its mandate, violating property rights, destroying tradition. The courts consistently sided with SEBI, recognizing that public interest outweighed private privilege.

The appointment of professional CEOs marked another power shift. Unlike broker-chairmen who emerged from within, CEOs like Madhu Kannan and Ashishkumar Chauhan came from investment banks and rival exchanges. They brought different networks, different skills, different loyalties. Kannan's first act was replacing the all-broker management committee with professionally qualified executives. Chauhan, ironically NSE's former deputy CEO, understood BSE's competitive disadvantages better than anyone—he had helped create them.

The ownership transformation through strategic stake sales diluted broker control decisively. When BSE was demutualized and corporatized on 19 May 2007, brokers owned 100%. Today, they control just 43.56%, with foreign investors holding 20.72%, domestic institutions 13.73%, and public shareholders 21.99%. This wasn't just financial engineering but political restructuring. Foreign investors demanded governance standards. Institutional shareholders insisted on performance metrics. Public shareholders, through small individual holdings, created pressure for transparency.

The international investors brought more than capital—they brought expectations. Deutsche Börse's strategic investment came with board representation and governance demands. Singapore Exchange's partnership included technology transfer but also compliance requirements. These foreign stakeholders had no patience for the old ways of doing business, no respect for hereditary privileges, no interest in preserving tradition at the expense of profits.

The role of Life Insurance Corporation deserves special attention. LIC's 9.05% stake makes it BSE's largest institutional shareholder, but its influence extends beyond shareholding. As India's largest domestic institutional investor, LIC's endorsement legitimized BSE's transformation. When LIC backed management over dissident brokers, it signaled that the old power structure was truly dead.

Independent directors brought radical transparency to an institution built on opacity. Former regulators like C.B. Bhave (ex-SEBI chairman) and Usha Thorat (former RBI deputy governor) understood markets from the oversight perspective. Technology experts questioned why BSE needed hundreds of employees for processes that could be automated. Academic directors introduced concepts like cost of capital and economic value added that were alien to traditional broker thinking.

The cultural clash was sometimes comedic, often tragic. Board meetings that once began with prayers and proceeded through consensus now featured heated debates and formal votes. Compensation committees tried to implement performance-based pay in an organization where salaries had been determined by seniority and connections. Audit committees discovered practices that weren't illegal but were certainly irregular. The sanitization was necessary but painful.

The staff transformation paralleled board changes. BSE's employee profile shifted from clerks processing paper to engineers writing code. The average age dropped from 45 to 35. The gender ratio improved from 95% male to 70%. Educational qualifications jumped from undergraduate degrees to post-graduate specializations. This wasn't just modernization but cultural revolution. The organization that had operated like an extended family became a corporation with HR policies and performance reviews.

Yet pockets of the old culture persist. Senior employees who remember the trading ring maintain informal networks. Broker families, while diminished in formal power, retain influence through relationships and institutional knowledge. The Gujarati business community, BSE's historical backbone, still matters for crucial decisions. Power has shifted but not disappeared; it has transformed from explicit to implicit, from formal to informal.

The governance structures now resemble global best practices. Board committees for audit, risk, nomination, and compensation operate with independent majorities. Related-party transactions require special approval. Whistleblower mechanisms protect employees reporting irregularities. Quarterly earnings calls subject management to analyst scrutiny. The governance that was once internal and opaque is now external and transparent.

The regulatory relationship with SEBI evolved from adversarial to collaborative. Where once BSE fought every SEBI directive, it now often exceeds regulatory requirements. This isn't just compliance but competitive strategy—positioning BSE as the governance leader compared to NSE's recent controversies. When NSE faced co-location investigations, BSE's clean record became a marketing advantage.

Executive compensation reveals changed priorities. Broker-chairmen had drawn modest salaries, their real wealth coming from trading profits. Professional CEOs demand competitive packages benchmarked to global standards. Ashishkumar Chauhan's compensation exceeds ₹10 crore annually—shocking to old-timers who remember when the entire board's compensation was less. Yet shareholders approve, recognizing that attracting talent requires paying market rates.

The decision-making process transformed from intuition to analytics. Where broker-leaders made decisions based on market feel and personal relationships, professional management relies on data and analysis. Product launches require business cases. Technology investments need ROI calculations. Strategic initiatives undergo scenario planning. The judgment-based management style gave way to evidence-based decision-making.

Power now flows from performance rather than patrimony. A successful product launch creates more influence than inherited membership. Technical expertise matters more than community connections. The ability to generate revenues trumps family reputation. This meritocratic shift, while improving organizational performance, destroyed the social fabric that had sustained BSE for a century.

The shareholder activism emerging post-listing introduces another power center. Institutional investors question strategies at annual meetings. Proxy advisory firms recommend voting against resolutions. Activist investors propose board changes. The management that once answered only to itself now faces constant scrutiny. Every decision is evaluated not just for its business merit but for its impact on stock price.

Looking forward, the power dynamics will continue evolving. As algorithms replace human traders, technology leaders gain influence over market experts. As global exchanges consolidate, international partnerships become more critical than domestic relationships. As regulation converges globally, compliance expertise matters more than local knowledge. The BSE that was once controlled by a few dozen Mumbai families is becoming a node in global financial networks, its power structures determined by forces far beyond Dalal Street.

The irony is striking: BSE had to destroy its traditional power structure to preserve its institutional existence. The brokers who fought demutualization, who resisted professional management, who opposed foreign investment, ultimately benefited most—their BSE shares, once worthless paper certificates of membership, became liquid securities worth crores. They lost control but gained wealth. They surrendered power but secured prosperity. In the end, perhaps that was the best trade they ever made.

IX. The Tech Stack & Infrastructure Play

At 3:47 AM on a humid Mumbai morning, BSE's disaster recovery site in Chennai automatically takes over from the primary data center. The failover happens in 37 seconds—no human intervention, no service disruption, no data loss. By the time the first engineer arrives at 6 AM to investigate the Mumbai power fluctuation that triggered the switch, seventeen thousand orders have already been processed through Chennai. This isn't disaster recovery; it's disaster invisibility.

The technology infrastructure supporting BSE represents one of India's most complex civilian computing operations. The primary data center in Mumbai's suburbs houses over 2,000 servers in a 100,000-square-foot facility that consumes as much electricity as a small town. The backup site in Chennai mirrors every component, every configuration, every byte of data. A third facility in Gujarat provides additional redundancy. Together, they ensure that BSE never stops trading—not for earthquakes, not for floods, not for cyberattacks.

The numbers defining this infrastructure boggle the mind. Network capacity exceeds 100 gigabits per second. Storage systems hold 15 petabytes of data—every trade, every quote, every order from the past decade instantly accessible. The matching engine processes 200,000 messages per second per partition, with theoretical capacity reaching 1.5 million. Response times are measured in microseconds, jitter in nanoseconds. This isn't just fast; it's faster than human perception, faster than most physics experiments, faster than light traveling across a cricket pitch.

The co-location facility represents infrastructure as a competitive weapon. Trading firms pay millions annually to place their servers in BSE's data center, reducing the distance between their algorithms and BSE's matching engine to mere meters. Every meter of cable adds three nanoseconds of latency. In high-frequency trading, three nanoseconds can mean the difference between profit and loss. BSE ensures fairness through equal-length cables—if your server is closer to the matching engine, your cable is longer, ensuring everyone faces identical latency.

Building this infrastructure required expertise BSE didn't possess internally. Partnerships with technology giants became essential. IBM provided hardware architecture. Oracle delivered database systems. Cisco designed networking infrastructure. But BSE learned from its NSE experience—never become dependent on single vendors. Every critical system has alternatives. Every vendor relationship includes knowledge transfer. BSE engineers shadow vendor specialists, learning not just how to operate systems but how to design them.

The software stack reveals architectural sophistication. The BOLT Plus trading platform runs on distributed computing architecture, spreading load across multiple servers. If one server fails, others instantly absorb its workload. The risk management system operates in parallel, checking every order against multiple parameters in real-time. The surveillance system monitors patterns across millions of transactions, flagging anomalies for human review. These aren't separate systems but an integrated technology ecosystem where each component strengthens others.

Cybersecurity infrastructure operates like a digital fortress with multiple defensive layers. Perimeter firewalls block obvious attacks. Intrusion detection systems identify subtle penetration attempts. Behavioral analytics spot insider threats. Encryption protects data in transit and at rest. Regular penetration testing—hiring hackers to attack your own systems—reveals vulnerabilities before criminals find them. The security operations center operates 24/7, staffed by specialists who think like attackers to defend like guardians.

The API ecosystem democratizes access while maintaining control. BSE publishes hundreds of APIs allowing third-party developers to build trading applications. Want real-time quotes? There's an API. Need historical data? Another API. Want to submit orders? API again. This openness enables innovation—thousands of applications built on BSE's infrastructure—while generating revenue through API calls. Every request costs fractions of a paisa, but millions of requests daily generate crores annually.

Data monetization emerged as infrastructure's unexpected dividend. BSE sells real-time feeds to Bloomberg and Reuters. Historical data goes to quantitative funds training machine learning models. Analytics packages help brokers understand customer behavior. The same infrastructure that processes trades becomes a data factory, generating information products with software-like margins. The exchange that once gave away data now treats it as a core product.

The clearing and settlement infrastructure prevents financial catastrophe. Every trade creates obligations—buyers must pay, sellers must deliver. BSE's clearing corporation stands between parties, guaranteeing both sides. This requires sophisticated risk management: calculating margins in real-time, monitoring positions continuously, managing collateral dynamically. The technology must be perfect—a single failed settlement could trigger cascading defaults destroying market confidence.

Network architecture prioritizes reliability over efficiency. Multiple internet service providers ensure connectivity. Dedicated leased lines connect major brokers. Satellite backup links activate if terrestrial networks fail. The philosophy is redundancy everywhere—if something can fail, assume it will fail, and have alternatives ready. This paranoia costs millions annually but prevents billions in potential losses.

The testing infrastructure rivals production systems. A complete duplicate environment allows BSE to test every change before deployment. Load testing simulates 10x normal volumes. Stress testing pushes systems to failure points. Chaos engineering deliberately breaks components to ensure graceful degradation. The investment in testing exceeds many companies' entire IT budgets, but BSE can't afford production failures.

Technology vendor relationships evolved from transactional to strategic. Microsoft doesn't just sell licenses; it helps optimize code. Intel doesn't just provide processors; it assists in architecture design. These partnerships go beyond commercial contracts to knowledge exchange. BSE engineers attend vendor training globally. Vendor specialists embed in BSE teams for critical projects. The exchange that once outsourced everything now collaborates as a peer.

The database architecture handles staggering scale. Every quote, trade, order modification, and cancellation creates database records. Millions of records accumulate daily, billions annually. Traditional databases would collapse under this load. BSE uses distributed databases, spreading data across multiple servers. Time-series databases optimize for temporal queries. In-memory databases provide microsecond response times. Different databases for different purposes, all synchronized in real-time.

Infrastructure monitoring resembles mission control at NASA. Giant screens display system metrics: CPU utilization, network traffic, disk I/O, application response times. Anomalies trigger alerts—SMS to engineers, automated phone calls to managers, escalation protocols if responses delay. The monitoring system itself is monitored, creating recursive loops of oversight. Nothing happens in BSE's infrastructure without being observed, measured, recorded.

The capacity planning challenge never ends. Today's peak load becomes tomorrow's average. Systems designed for millions of messages now handle billions. Infrastructure sufficient for domestic markets must scale for international expansion. The planning horizon extends years—ordering equipment today for volumes expected in 2027. Over-provisioning wastes money; under-provisioning risks failure. The balance requires predictive analytics and intuitive judgment.

Power and cooling infrastructure consumes enormous capital. Data centers require uninterrupted power—diesel generators backing up battery arrays backing up dual power grids. Cooling systems maintain precise temperatures—too hot and servers fail, too cold and condensation forms. The physical infrastructure supporting digital infrastructure costs as much as the computers themselves. It's the hidden foundation of electronic trading.

The technology refresh cycle never stops. Servers replaced every three years. Network equipment upgraded every five. Software versions updated quarterly. Security patches applied weekly. The infrastructure that seems permanent is actually in constant flux. BSE spends hundreds of crores annually just maintaining current capabilities, separate from new investments. It's the price of staying current in a world where yesterday's innovation becomes today's obsolescence.

Edge computing brings infrastructure closer to users. Instead of routing all traffic through Mumbai, BSE deploys edge servers in major cities. Local servers handle non-critical tasks—quote distribution, static data serving—reducing latency and load on core systems. It's distributed computing meeting financial markets, creating infrastructure that's simultaneously centralized and decentralized.

The cost structure of infrastructure reveals financial markets' technology intensity. BSE spends more on technology than many software companies. The infrastructure supporting a few thousand active traders costs more than systems serving millions of retail customers in other industries. But the value processed justifies the investment—BSE's infrastructure handles transactions worth trillions annually. A single minute of downtime could cost crores in lost revenue and destroyed confidence.

Looking ahead, infrastructure requirements will only intensify. Quantum computing threatens current encryption. Artificial intelligence demands new processing architectures. Blockchain might revolutionize settlement. 5G networks enable microsecond mobile trading. BSE must invest in technologies that don't yet exist for markets that haven't been invented. The infrastructure play never ends; it only accelerates.

X. Playbook: Lessons from BSE's Journey

The transformation of BSE from colonial-era brokers' club to high-frequency trading platform offers a masterclass in institutional reinvention. Not the clean, strategic pivots celebrated in business schools, but the messy, political, often painful evolution that real organizations endure when survival is at stake. The lessons aren't always inspiring—sometimes they're cautionary tales—but they're always instructive.

Lesson One: Incumbency is simultaneously asset and liability. BSE's 150-year history provided unmatched brand recognition, deep relationships, and institutional knowledge. The SENSEX became synonymous with Indian markets. Generations of businesses had relationships with BSE brokers. This heritage created trust that no startup could replicate. Yet the same history created inertia. Every change faced resistance from stakeholders who benefited from status quo. Traditional practices calcified into sacred rituals. The organization that should have been most capable of change became least willing to change. The playbook insight: heritage must be selectively preserved and strategically abandoned.

Lesson Two: Disruption often comes with government backing. NSE wasn't a scrappy startup disrupting from the garage—it was a government-sponsored initiative designed to break BSE's monopoly. This pattern repeats globally: governments create competition when private monopolies become problematic. The Chicago Mercantile Exchange faced government-backed electronic platforms. London Stock Exchange confronted EU-mandated competition. The lesson isn't that government always wins, but that regulatory power can instantly create formidable competitors. Incumbents must maintain regulatory relationships not just for compliance but for competitive intelligence.

Lesson Three: Technology transitions create winner-take-all dynamics. The shift from physical to electronic trading wasn't gradual—it was catastrophic for laggards. BSE's five-year delay in embracing electronic trading cost decades of market share. In platform businesses, network effects amplify first-mover advantages. Once NSE became the liquid market for derivatives, BSE couldn't compete even with superior technology and lower prices. The playbook teaching: when technology shifts occur, moving second means losing permanently.

Lesson Four: Demutualization is about power, not structure. Converting from broker association to public corporation wasn't primarily about governance—it was about breaking entrenched power structures that prevented adaptation. The same brokers who controlled BSE also benefited from its inefficiencies. They had no incentive to improve systems that gave them advantages. Demutualization forcibly aligned interests by making brokers shareholders rather than owners. The broader lesson: when stakeholder interests conflict with organizational needs, structure must change to change incentives.

Lesson Five: Network effects can be broken through regulatory intervention. BSE couldn't overcome NSE's liquidity advantage through competition alone. It required SEBI's interoperability mandate, allowing trades on one exchange to settle on another. This regulatory intervention weakened NSE's network effect moat. The pattern holds across industries: antitrust actions against Microsoft, interoperability requirements for telecom, data portability for social media. Incumbents facing network effect disadvantages should pursue regulatory strategies alongside competitive ones.

Lesson Six: Niche dominance beats broad mediocrity. BSE couldn't compete with NSE across all products, so it dominated specific segments. The SME platform became India's largest. The mutual fund platform processed most transactions. Commodity derivatives found unique positioning. Instead of trying to reclaim overall market leadership, BSE built multiple monopolies in smaller markets. The strategic insight: when you can't win the war, win enough battles to remain relevant.

Lesson Seven: Professional management requires cultural revolution. Bringing external CEOs and independent directors wasn't enough—BSE needed complete cultural transformation. This meant replacing nepotism with meritocracy, relationships with processes, intuition with analytics. The organization's DNA had to change. Many employees couldn't adapt and left. Others adapted but remained skeptical. The successful transformed themselves completely. The lesson: governance changes without cultural changes are cosmetic.

Lesson Eight: International partnerships provide capability leapfrogging. BSE's partnerships with Deutsche Börse and Singapore Exchange weren't just strategic alliances—they were knowledge transfer mechanisms. BSE learned in months what would have taken years to develop internally. These partnerships provided technology, expertise, and credibility. The playbook principle: when behind, don't build—partner, learn, then build.

Lesson Nine: Data becomes more valuable than transactions. BSE discovered that selling market data generated higher margins than processing trades. Real-time feeds, historical databases, analytics packages—information products scaled without marginal costs. The exchange that once gave away data now monetizes every byte. The broader principle: in digital businesses, the exhaust from core operations often becomes more valuable than the operations themselves.