Borosil Renewables: India's Solar Glass Pioneer and the German Gambit

I. Introduction & Episode Roadmap

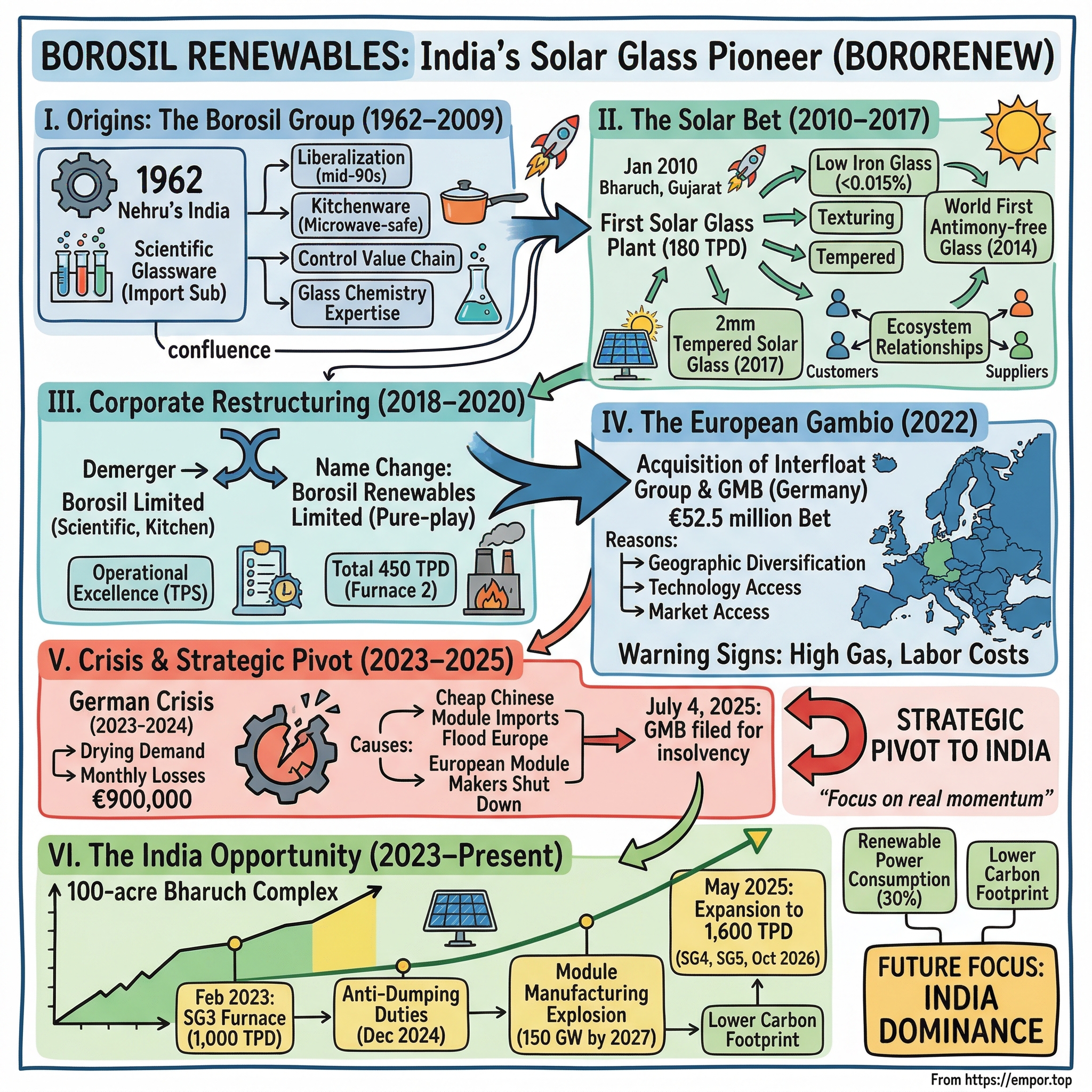

Picture this: A sprawling 100-acre manufacturing complex in Bharuch, Gujarat, where furnaces burn at 1,600 degrees Celsius, transforming silica sand into ultra-clear glass sheets that will one day capture sunlight across solar farms from Rajasthan to Rhineland. This is Borosil Renewables—a company that controls over 20% of India's solar glass market and whose story reads like a masterclass in industrial transformation, strategic pivots, and the perils of international ambition.

The hook here isn't just about glass. It's about how a 60-year-old laboratory glassware manufacturer—the kind that made beakers and test tubes for chemistry labs—recognized a tectonic shift in global energy infrastructure and repositioned itself at the heart of India's renewable revolution. Then, in a move that would define its next chapter, bet big on Europe through a €52.5 million acquisition that would ultimately end in German insolvency court.

Today, Borosil Renewables stands at an inflection point. With a market capitalization hovering around ₹7,882 crore, the company has emerged from its European misadventure refocused on what it does best: dominating India's rapidly expanding solar glass market. As the country's solar module manufacturing capacity races past 90 GW toward a projected 150 GW by 2027, Borosil's furnaces in Gujarat are running at full tilt, producing 1,000 tons of solar glass daily—enough to support 6.5 GW of solar panel production annually.

This is a story about industrial policy, import substitution, and the delicate dance between ambition and execution. It's about reading government tea leaves correctly—from anti-dumping duties to production-linked incentives—and positioning yourself as the picks-and-shovels provider to an energy transition. Most importantly, it's about what happens when a company's international dreams collide with the harsh realities of global solar manufacturing economics.

The themes we'll explore cut to the heart of emerging market industrialization: How do you build a monopoly in a commodity business? When should you expand internationally versus doubling down domestically? And perhaps most critically, how do you navigate the boom-bust cycles of renewable energy infrastructure? These aren't just academic questions—they're the strategic decisions that separated Borosil from competitors who either never entered the market or exited too early.

What makes this particularly fascinating is the timing. As we sit here in 2025, India's solar ambitions have never been clearer, China's dominance in solar manufacturing faces increasing scrutiny, and Europe grapples with its own energy security dilemmas. Borosil's journey from laboratory glassware to solar glass monopoly offers a window into how industrial companies can reinvent themselves—and the price they sometimes pay for that reinvention.

II. Origins: The Borosil Group Story (1962–2009)

The year was 1962. Jawaharlal Nehru was pushing his vision of a modern, industrialized India through five-year plans and public sector undertakings. In this environment of nation-building and import substitution, a group of entrepreneurs saw an opportunity in specialty glass—not the window panes or bottles that dotted the landscape, but precision scientific glassware that India's nascent research institutions desperately needed but had to import at precious foreign exchange.

On December 14, 1962, Borosil was born through the acquisition of Industrial and Engineering Apparatus Company Pvt. Ltd. The founders weren't thinking about solar panels—photovoltaics were barely a laboratory curiosity then. They were thinking about test tubes, beakers, and borosilicate glass that could withstand extreme temperatures without cracking. This was unglamorous work, but essential. Every chemistry lab, every pharmaceutical company, every research institution needed this equipment. And in Nehru's India, with its emphasis on scientific temper and self-reliance, being the domestic producer of such critical infrastructure carried both economic and symbolic weight.

For three decades, Borosil quietly built its reputation in this niche. The company became synonymous with laboratory glassware in India—if you studied chemistry in an Indian university between 1970 and 2000, chances are you used Borosil beakers. But by the mid-1990s, liberalization was reshaping India's economy. Foreign brands were entering, competition was intensifying, and the company needed to evolve.

The modernization drive that began in the mid-1990s was transformative. Borosil didn't just upgrade its existing facilities; it fundamentally rethought its approach to glass manufacturing. The company invested in manufacturing borosilicate glass tubing—the raw material for its laboratory products—giving it control over its entire value chain. This vertical integration would become a recurring theme in Borosil's playbook, one that would serve it well when it eventually entered solar glass.

But the real diversification came through an unexpected avenue: kitchenware. Borosil began producing heat-resistant borosilicate opal tableware—essentially taking its laboratory-grade glass expertise and applying it to consumer products. The logic was elegant: the same properties that made borosilicate glass perfect for laboratory use—thermal resistance, durability, chemical inertness—also made it ideal for microwave-safe cookware. This wasn't just product development; it was market creation. Indian consumers in the 1990s were just beginning to adopt microwave ovens, and Borosil positioned itself as the premium, safe option for this new cooking technology.

By the early 2000s, Borosil had established itself as a diversified specialty glass manufacturer with deep technical expertise. The company understood glass chemistry at a molecular level—how to control iron content for clarity, how to manage thermal expansion coefficients, how to achieve specific optical properties. This knowledge base, accumulated over four decades, would prove invaluable when a new opportunity emerged.

The late 2000s brought a confluence of factors that would reshape Borosil's destiny. First, the global financial crisis of 2008 had governments worldwide looking for stimulus opportunities, and renewable energy infrastructure emerged as a favored target. Second, India launched its National Solar Mission in 2009, setting ambitious targets for solar capacity addition. Third, and perhaps most critically, the cost of solar photovoltaic panels was beginning its dramatic decline, making solar power increasingly competitive with conventional electricity.

Within Borosil's boardrooms, executives were connecting dots. Solar panels required specialized glass—not just any glass, but ultra-clear, low-iron glass with specific light transmission properties. The iron content had to be below 0.015%, compared to 0.1% in regular float glass. The surface needed texturing to reduce reflection and increase light trapping. The glass had to withstand decades of weather exposure without degrading. These were precisely the kinds of technical challenges Borosil had been solving for decades in different contexts.

The strategic logic was compelling. India was about to embark on a massive solar buildout, but had zero domestic solar glass manufacturing capacity. Every solar panel manufactured in India would need imported glass, creating foreign exchange outflows and supply chain vulnerabilities. For a company that had built its original business on import substitution, this looked like history rhyming. The decision to enter solar glass wasn't just about following a trend—it was about recognizing a structural shift in India's energy infrastructure and positioning the company at a critical bottleneck in the value chain.

III. The Solar Bet: India's First Solar Glass Plant (2010–2017)

January 2010, Bharuch, Gujarat. As India's National Solar Mission officially kicked off with grand targets of 20 GW by 2022, Borosil quietly commissioned something that would prove far more consequential: India's first and only solar glass production line. The 180-ton-per-day furnace wasn't particularly large by global standards—Chinese competitors were running furnaces five times that size—but in India's nascent solar ecosystem, it was revolutionary.

The timing seemed almost foolish. India's total installed solar capacity was barely 10 MW. The global solar industry was still reeling from the financial crisis, with several high-profile bankruptcies including Solyndra making headlines. Solar panels cost $2 per watt, making solar power economically unviable without heavy subsidies. Yet Borosil was betting that this would change—and change dramatically.

The technical challenges were immense. Solar glass isn't just clear glass; it's an engineered product with precise specifications. The iron content needs to be below 150 parts per million to achieve the 91.5% light transmission required for high-efficiency panels. The surface requires a specific pyramidal texture pattern to reduce reflection while maintaining mechanical strength. The glass must be tempered to withstand hail impact and thermal cycling from -40°C to +85°C. Borosil's team spent months fine-tuning the float glass process, adjusting everything from raw material composition to annealing curves.

But the real challenge wasn't technical—it was market development. In 2010, India's solar module manufacturers were largely assembly operations, importing cells from China and Taiwan. They were skeptical of domestic glass quality and worried about supply reliability. Borosil's sales team found themselves not just selling a product but evangelizing an entire ecosystem. They provided technical support to module manufacturers, helped them optimize their lamination processes, and even extended credit terms that Chinese suppliers wouldn't match.

The breakthrough came in 2013 with the introduction of anti-reflective coatings—a first in India. By applying a nano-scale silicon dioxide coating, Borosil could increase light transmission from 91.5% to 94%, translating directly into higher panel efficiency. This wasn't just incremental improvement; it was a statement that Indian manufacturing could innovate, not just replicate. Module manufacturers who had dismissed domestic glass as inferior suddenly took notice. The year 2014 marked another watershed moment. Borosil developed the world's first antimony-free solar glass, eliminating what had been an essential but toxic component in glass manufacturing for centuries. Antimony trioxide, used as a refining agent to remove bubbles from molten glass, is classified as a possible carcinogen. Each solar panel typically contains 32 to 48 grams of antimony in its 16 kg front glass, creating a massive environmental liability as panels eventually reach end-of-life. Borosil's breakthrough wasn't just about removing a toxin—it was about doing so while maintaining glass quality and production efficiency, something the global glass industry had deemed impossible.

The innovation momentum accelerated. In 2017, Borosil achieved another world first: fully tempered 2mm solar glass, compared to the industry standard of 3.2mm. This wasn't just about being thinner—tempered 2mm glass enabled entirely new module designs. Bifacial panels, which generate power from both sides, could now use glass on both surfaces without excessive weight. The use of high transmission solar glass on both surfaces allowed bifacial solar cells to enhance module efficiency by 30%. For rooftop installations where weight is critical, this innovation opened entirely new markets.

Throughout this period, Borosil was building something more valuable than products: ecosystem relationships. The company worked closely with module manufacturers, helping them adapt their processes for domestic glass. They collaborated with equipment suppliers to optimize lamination parameters. They even engaged with project developers to understand field performance requirements. This wasn't the arm's-length supplier relationship typical of commodity businesses—it was technical partnership.

The numbers tell the story of steady progress. From 180 tons per day in 2010, Borosil expanded carefully, reinvesting cash flows rather than taking on excessive debt. By 2017, the company had established itself as the undisputed leader in Indian solar glass, with module manufacturers increasingly preferring domestic supply for both quality and logistics reasons. The anti-dumping duties imposed on Chinese glass imports in 2017 provided additional tailwind, but Borosil had already won on merit.

What's remarkable about this period is what Borosil didn't do. They didn't chase international markets aggressively. They didn't diversify into adjacent products like aluminum frames or backsheets. They didn't engage in price wars with Chinese imports. Instead, they focused relentlessly on technical excellence and customer relationships in their home market. This discipline would serve them well as India's solar ambitions expanded—but would also create the strategic tension that led to their next major decision.

IV. Corporate Restructuring & Focus (2018–2020)

By 2018, Borosil found itself at a crossroads. The company was essentially three businesses under one roof: the legacy laboratory glassware division that had birthed the company, the consumer products business selling microwaveable cookware to Indian households, and the rapidly growing solar glass operation that was increasingly dominating management attention and capital allocation. Each business had different growth trajectories, capital requirements, and investor bases. The conglomerate structure that had served Borosil well during its diversification phase was now becoming a constraint.

The board's decision to restructure wasn't taken lightly. The laboratory and consumer businesses weren't just profitable—they were the company's heritage, carrying the Borosil brand that had taken decades to build. But the solar opportunity was too large to pursue half-heartedly. India's solar installations were accelerating, module manufacturing was localizing rapidly, and the government was signaling even more ambitious renewable targets. To capture this opportunity, Borosil needed focused management, dedicated capital, and a clear story for investors.

The restructuring executed in 2018 was complex but elegant. Through a composite scheme of arrangement, Borosil amalgamated three entities—Vyline Glass Works, Fennel Investment, and Gujarat Borosil—while simultaneously demerging the scientific, industrial, and consumer products businesses into a separate entity that would retain the Borosil Limited name. The solar glass business would continue in the restructured entity. This wasn't just financial engineering—it was strategic clarity. Each business could now pursue its optimal capital structure, growth strategy, and market positioning.

The markets initially struggled to understand the restructuring. Investors who had bought Borosil for its stable consumer products business suddenly found themselves holding shares in a capital-intensive industrial company. Those who wanted exposure to India's solar boom had to disentangle the solar economics from the legacy businesses. The stock price reflected this confusion, trading sideways despite strong operational performance.

But management was playing a longer game. With the restructuring complete, they moved to crystallize the company's new identity. In 2020, the company changed its name from Borosil Glass Works Limited to Borosil Renewables Limited. This wasn't mere rebranding—it was a declaration of intent. The company was no longer a diversified glass manufacturer that happened to make solar glass. It was a pure-play renewable energy infrastructure company, aligned with India's energy transition.

The operational improvements during this period were equally significant. Borosil added a second furnace with 240 tons per day capacity while upgrading the first furnace from 180 to 210 tons per day. This wasn't just capacity expansion—it was technological advancement. The new furnace incorporated lessons learned from a decade of operations: better combustion control for lower emissions, improved refining for higher clarity, and flexible design to handle different glass compositions. Total capacity reached 450 tons per day, positioning Borosil to serve roughly 3 GW of annual module production.

The focus also extended to operational excellence. Borosil implemented Toyota Production System principles, reducing changeover times and improving yield. They invested in automated inspection systems, using machine vision to detect microscopic defects that human inspectors might miss. They even redesigned their packaging to reduce breakage during transport—a seemingly minor improvement that significantly reduced customer complaints and returns.

Financially, the restructuring delivered immediate benefits. Without the drag of slower-growing legacy businesses, Borosil Renewables could reinvest more aggressively. The company's return on capital employed improved as management could optimize the balance sheet for a single business model. Perhaps most importantly, the company could now tell a simple story to investors: Borosil Renewables was the picks-and-shovels play on India's solar boom.

The timing of this restructuring, completed just before COVID-19 disrupted global markets, would prove fortuitous. As governments worldwide announced green stimulus packages and renewable energy targets were raised dramatically, Borosil Renewables was perfectly positioned—a focused, debt-light, technically superior manufacturer in the world's fastest-growing solar market. But this success would also breed ambition, leading to a decision that would define the company's next chapter: the acquisition of Europe's largest solar glass manufacturer.

V. The European Acquisition: GMB & Interfloat (2022)

Spring 2022. Europe was in the midst of an energy crisis. Russia's invasion of Ukraine had sent natural gas prices soaring, and the continent was scrambling to reduce its dependence on fossil fuels. Solar installations were accelerating, the European Union was announcing ambitious renewable targets under its REPowerEU plan, and local solar manufacturing was being positioned as a strategic imperative. For Borosil's management, watching from Gujarat, this looked like the perfect storm of opportunity.

The Interfloat Group consisted of GMB Glass Manufaktur Brandenburg GmbH, located in Tschernitz, Germany, and Interfloat Corporation, based in Ruggell, Liechtenstein. GMB was the largest solar glass producer in Europe with a current capacity of 300 tons per day, manufacturing glass for Europe's solar markets since 2010. The company wasn't just a production facility—it had four decades of customer relationships across European glass markets and deep technical expertise in serving both photovoltaic and solar thermal applications.

The strategic rationale was compelling on multiple levels. First, geographic diversification: Borosil had learned from its domestic success that being close to customers mattered in solar glass. Transport costs were high, breakage risks significant, and technical support crucial. Having a European manufacturing base would allow Borosil to serve the continent's module manufacturers directly. Second, technology access: GMB had been developing specialized products for European markets, including greenhouse glass and solar thermal applications that weren't prevalent in India. Third, and perhaps most importantly, market access: The Interfloat Group recorded consolidated net revenue of approximately €60 million in 2021, providing immediate scale in European markets.

The acquisition structure was complex but carefully designed. Borosil would buy GMB at €24.91 million in cash plus performance-based payments, and Interfloat for €5.09 million cash plus a share swap equivalent to €22.50 million and additional performance-based payments. The total consideration of approximately €52.5 million (about $56.6 million) represented a significant bet for a company with a market cap of around ₹5,000 crore at the time. But management was confident—Europe's solar boom was just beginning, and owning the continent's largest solar glass manufacturer seemed like perfect positioning.

The immediate impact was transformative for Borosil's global footprint. With the acquisition, Borosil's solar glass manufacturing capacity increased by 66%, from 450 tons per day to 750 tons per day. Combined with the third furnace being commissioned in India, total capacity would reach 1,300 tons per day—making Borosil one of the larger solar glass manufacturers globally outside China. The company now had the scale to serve major module manufacturers who required supply security across multiple geographies.

But there were early warning signs that European solar manufacturing faced structural challenges. Natural gas, the primary energy source for glass furnaces in Europe, cost five times more than in India. Labor costs were substantially higher. Environmental regulations, while admirable, added complexity and expense. Most critically, European module manufacturers were struggling to compete with Asian imports despite various support mechanisms. The same dynamics that had driven solar manufacturing from Europe to Asia over the previous decade hadn't fundamentally changed.

Christian Kern, former Austrian chancellor and member of Interfloat's board, remained optimistic, stating that "Borosil Renewables, a worldwide innovation leader with focus on green production of solar glass panels, is a huge gain for Interfloat and the production in Brandenburg. In such difficult times, when the European industry suffers from soaring gas prices, a strong international partner will ensure continuity in the European production of clean energy." Borosil's management echoed this optimism, believing their operational excellence could overcome the structural challenges.

The integration began promisingly. Borosil's technical teams worked to transfer best practices from India to Germany, optimizing furnace operations and reducing energy consumption. They introduced new product variants developed in India, expanding GMB's portfolio. Customer relationships were leveraged to cross-sell between geographies. For a brief moment, it seemed like the acquisition might deliver on its promise of creating a global solar glass powerhouse.

VI. The German Crisis & Strategic Pivot (2023–2025)

The unraveling began in late 2023. GMB applied for short-term work for its staff in January 2024 as demand for its products dried up, leading to monthly losses of €900,000. According to Ashok Jain, a director at Borosil Renewables, demand for GMB's products fell as low as 40% of its production output at the beginning of 2024. The European solar manufacturing ecosystem that Borosil had bet on was collapsing faster than anyone anticipated.

The root cause was brutally simple: Chinese solar modules were flooding the European market at prices that defied economic logic. European module manufacturers couldn't compete, and one by one, they began shutting down. Meyer Burger scrapped module production facilities in the US and filed for insolvency for its European cell production facilities, leaving the long-standing industry leader without any manufacturing facilities. Without module manufacturers, there was no market for solar glass.

Borosil's response was initially to double down. The company modified GMB's furnace to increase capacity from 300 to 350 tons per day, hoping that improved efficiency could offset the market decline. They provided operational support and financial injections totaling €27 million, believing that European policy support would eventually materialize. Management pointed to the EU's REPowerEU targets and the Solar Manufacturing Accelerator program as evidence that the market would recover.

But the bleeding wouldn't stop. GMB's financial losses amounted to approximately INR 9 crore per month. For context, that's over ₹100 crore annually—a staggering drain for a company with total revenues of around ₹1,500 crore. The German operation had become an albatross, consuming management attention and capital that could be deployed more productively elsewhere.

The contrast with India couldn't have been starker. While GMB struggled to find customers in Europe, Borosil's Indian operations were running at full capacity. India's solar module manufacturing capacity had surpassed 90 GW and was expected to rise to 150 GW by March 2027. The five-year anti-dumping duty introduced in December 2024 was creating a level playing field for Indian manufacturers. Prices for solar glass strengthened significantly, with Q4 FY25 average ex-factory prices up 28% year-on-year.

On July 4, 2025, Borosil made the painful but necessary decision. GMB Glasmanufaktur Brandenburg GmbH filed for insolvency under the German Insolvency Code before the jurisdictional court at Cottbus. From that date, GMB's operations would be overseen by a court-appointed administrator in Germany. Borosil's exposure as of March 31, 2025 in the German subsidiary and step-down subsidiary stood at Euro 35.30 million—roughly ₹340 crore that might never be recovered.

P.K. Kheruka, Chairman of Borosil Renewables, framed the decision with characteristic clarity: "This decision reflects our clear-eyed view of where the future lies and the confidence we have in India's solar manufacturing story. With this step, we deepen our commitment to building scale and excellence in India, where the potential is vast, the policies are enabling, and the momentum is real. It is a forward-looking decision made with the long-term in mind".

The German insolvency wasn't just a financial setback—it was a strategic education. Borosil had learned that technology and operational excellence weren't enough to overcome structural disadvantages. Energy costs matter. Labor costs matter. Most importantly, having a domestic module manufacturing ecosystem matters. Europe's grand renewable ambitions had collided with the reality of global supply chains, and Borosil had been caught in the crossfire.

VII. The India Opportunity & Expansion (2023–Present)

Even as the German subsidiary hemorrhaged cash, something remarkable was happening back in Gujarat. February 2023 marked a pivotal moment: Borosil commissioned its third furnace (SG3), taking the Bharuch facility's capacity to 1,000 tons per day. This wasn't just incremental growth—it was a statement of intent. While competitors hesitated, unsure about the sustainability of India's solar boom, Borosil was all in.

The state-of-the-art manufacturing facility spread over more than 100 acres at Bharuch, Gujarat now had solar glass production capacity of 1000 tons per day (TPD), equivalent to ~ 6.5 GW per annum. To put this in perspective, India's entire solar installation in 2015 was just 3 GW. Borosil could now supply glass for more than double that amount every single year.

The timing was exquisite. India's solar module manufacturing sector was experiencing a Cambrian explosion of capacity additions. Module manufacturers who had previously relied entirely on imports were setting up domestic production lines, driven by a combination of production-linked incentives (PLI), basic customs duties on module imports, and the broader "Atmanirbhar Bharat" (self-reliant India) push. Every one of these new module lines needed solar glass, and Borosil was often the only domestic option. The anti-dumping duties on Chinese and Vietnamese imports, imposed in December 2024, fundamentally changed the competitive landscape. The five-year anti-dumping duty introduced in December 2024 created a level playing field for Indian manufacturers, with Q4 FY25 average ex-factory prices up 28% year-on-year as a result of a gradual increase in the selling prices towards the reference price under Anti-dumping duty measures applicable to imports from China. This wasn't just price protection—it was validation that the government recognized solar glass as a strategic input for India's energy security.

In May 2025, even as the German subsidiary spiraled toward insolvency, Borosil announced its most ambitious expansion yet. The Board of Directors approved a revised expansion plan of 600 TPD at an estimated cost of INR 950 crores approximately, undertaken through setting up two furnaces of 300 TPD each (SG-4 and SG-5), expected to be commissioned during October to December 2026. This would take total capacity to 1,600 TPD, making Borosil one of the largest solar glass manufacturers globally outside China.

The confidence wasn't misplaced. India's solar module manufacturing capacity has already surpassed 90 GW and is expected to rise to 150 GW by March 2027. For context, that's more module manufacturing capacity than the United States and Europe combined. Every gigawatt of module capacity requires approximately 150-200 tons per day of solar glass production. The math was simple: even with the expansion, Borosil would struggle to keep pace with demand.

The product portfolio evolution continued apace. Borosil's recent innovations included "Selene" an Anti-glare solar glass for PV installations near airports, and "Shakti" a high efficiency solar glass with matt-matt finish. These weren't just product variants—they were solutions to specific Indian market challenges. Anti-glare glass addressed concerns from aviation authorities about solar farms near airports. High-efficiency matt-matt glass helped module manufacturers differentiate in an increasingly competitive market.

The operational metrics told a story of continuous improvement. The company owns 1.5 MW wind farm and invested in 10 MW hybrid renewable energy plant taking renewable power consumption to about 30%. This wasn't just about ESG credentials—renewable power reduced energy costs and insulated the company from grid power fluctuations that plagued Indian manufacturing.

The Make in India tailwinds extended beyond just anti-dumping duties. The Production Linked Incentive (PLI) scheme for solar modules created a virtuous cycle: module manufacturers received incentives for domestic production, which increased demand for domestic solar glass, which improved Borosil's economies of scale, which reduced costs for module manufacturers. It was industrial policy working as intended.

But perhaps the most important strategic decision was what Borosil didn't do. Despite the booming demand, the company resisted the temptation to diversify into adjacent products. No aluminum frames. No backsheets. No module assembly. The focus remained laser-sharp on solar glass, where the company had built insurmountable technical and scale advantages. In a market where every new entrant was trying to be everything to everyone, Borosil's discipline stood out.

VIII. Technology & Innovation Leadership

Behind the capacity expansions and market share gains lies a story of relentless technological innovation that separates Borosil from potential competitors. The company won the National Award in 2021 for the successful commercialization of indigenous technology from the Department of Science & Technology, Government of India. This wasn't just a ceremonial recognition—it validated Borosil's transformation from a glass manufacturer to a materials science innovator.

The innovation portfolio reads like a timeline of solving increasingly complex technical challenges. The 2mm fully tempered solar glass, achieved in 2017, wasn't just about making glass thinner—it required rethinking the entire tempering process. Traditional tempering relies on creating surface compression through rapid cooling, but with 2mm glass, the thermal mass is so low that conventional processes simply don't work. Borosil developed proprietary air-cushion technology that could uniformly cool ultra-thin glass without introducing optical distortions.

The antimony-free glass, introduced in 2014, addressed a problem the industry had largely ignored. Antimony trioxide, used as a refining agent in glass production for centuries, is classified as a possible carcinogen. With solar panels designed to last 25-30 years, the environmental liability of antimony-containing glass was substantial—each panel containing 32-48 grams of a toxic substance that could leach into soil and water. Borosil's breakthrough wasn't just removing antimony but finding alternative refining agents that maintained glass quality while being environmentally benign.

The recent product innovations—Selene anti-glare glass and Shakti high-efficiency matt-matt glass—demonstrate Borosil's evolution from solving technical problems to anticipating market needs. Anti-glare glass wasn't developed in response to customer demand but in anticipation of regulatory concerns as solar farms proliferated near airports. The matt-matt finish glass addressed module manufacturers' need for differentiation in an increasingly commoditized market, providing both aesthetic appeal and marginal efficiency gains through better light trapping.

The company is known for its benchmarked low energy consumption and has maintained a 22% lower carbon footprint in comparison with the default score for the glass manufacturing industry confirmed in the Life Cycle Assessment study carried out by a reputed European institute. The company owns a 1.5 MW wind farm and has invested in a 10 MW hybrid renewable energy plant at Bharuch taking the consumption of renewable power to about 30% of the total electricity consumption.

This sustainability focus isn't just about ESG metrics—it's strategic differentiation. As solar module manufacturers face increasing scrutiny about their carbon footprint, being able to source low-carbon glass becomes a competitive advantage. Borosil's renewable energy investments reduce operating costs while positioning the company as a sustainability leader in an industry increasingly focused on lifecycle emissions.

The manufacturing excellence extends beyond products to processes. Borosil has implemented Industry 4.0 technologies across its operations: AI-powered quality control systems that can detect microscopic defects invisible to human inspectors, predictive maintenance algorithms that minimize furnace downtime, and digital twins that allow process optimization without disrupting production. These aren't buzzword implementations but practical applications that have measurably improved yields and reduced costs.

The R&D infrastructure supporting this innovation is substantial. Borosil maintains dedicated research facilities with capabilities ranging from glass chemistry analysis to module-level testing. The company can simulate decades of weather exposure in weeks, test glass performance under extreme conditions, and rapidly prototype new compositions. This infrastructure allows Borosil to work as a development partner with module manufacturers, not just a supplier.

Perhaps most importantly, Borosil has built deep institutional knowledge that can't be easily replicated. Glass manufacturing is as much art as science—the precise temperature profiles, atmospheric conditions, and timing required to produce consistent quality solar glass take years to perfect. Borosil's team includes technicians who have spent decades perfecting these processes, knowledge that can't be acquired through hiring or technology transfer.

The innovation pipeline remains robust. Borosil is working on next-generation products including ultra-high transmission glass with light transmission above 95%, specialized coatings for bifacial modules, and glass solutions for emerging technologies like perovskite tandem cells. The company is also exploring ways to further reduce its carbon footprint, with targets to achieve 50% renewable energy consumption by 2027.

IX. Playbook: Business & Investing Lessons

The Borosil story offers a masterclass in industrial strategy, with lessons that extend far beyond solar glass or even manufacturing. At its core, this is a story about reading structural shifts correctly, positioning strategically, and having the discipline to stay focused even when diversification seems attractive.

Lesson 1: The Import Substitution Playbook Still Works—With Caveats

Borosil's success validates that import substitution can still create value in the 21st century, but only under specific conditions. You need a large domestic market growing faster than global average (India's solar installations grew 50x from 2010 to 2020). You need technical barriers that prevent easy replication (solar glass requires precise chemistry and processing). And crucially, you need government policy alignment—not just protection, but active promotion of domestic manufacturing through multiple policy levers.

The caveat is timing. Enter too early, like Borosil almost did in 2010 when India had just 10 MW of solar, and you burn cash waiting for the market. Enter too late, after Chinese competitors have achieved massive scale, and you can't compete on cost. Borosil hit the sweet spot—early enough to build capabilities without competition, late enough that the market was real.

Lesson 2: In Commodities, Technology Can Create Moats

Solar glass appears to be a commodity—standardized product, price-based competition, minimal differentiation. Yet Borosil has maintained pricing power and market share despite new entrants attempting to enter the market. The moat isn't just one innovation but a stack of small advantages: lower iron content than competitors, faster delivery times, technical support capabilities, product variants for specific applications, and relationships with every major module manufacturer in India.

This mirrors successful commodity businesses globally—TSMC in semiconductor manufacturing, Corning in display glass, or Air Products in industrial gases. The playbook is consistent: relentless incremental innovation, deep customer relationships, and operational excellence that makes switching costs higher than they appear.

Lesson 3: Geographic Diversification in Manufacturing is Harder Than It Looks

The GMB acquisition seemed strategically sound—geographic diversification, technology access, developed market presence. Yet it failed spectacularly, destroying roughly ₹340 crore in value. The lesson isn't that international expansion is wrong but that manufacturing economics are ruthlessly local. Energy costs, labor productivity, regulatory environment, and proximity to customers all matter more than management typically assumes.

The contrast with asset-light businesses is instructive. Software companies can expand globally relatively easily because their economics are similar everywhere. Manufacturing companies face radically different cost structures and competitive dynamics in different geographies. Borosil learned this lesson expensively—energy costs in Germany were 5x India, making the business structurally uncompetitive regardless of operational improvements.

Lesson 4: Industrial Policy Matters More Than Most Investors Realize

Borosil's trajectory has been shaped more by government policy than by technology or execution. The National Solar Mission created demand. Anti-dumping duties provided pricing power. PLI schemes incentivized customers. The German subsidiary failed partly because European policy support never materialized as expected.

For investors, this means that analyzing industrial companies requires deep understanding of policy dynamics. It's not enough to track current policies; you need to understand the political economy driving policy formation. India's solar policies aren't just about clean energy—they're about energy security, manufacturing jobs, and reducing import dependence. These deeper motivations make the policies more durable than simple subsidies.

Lesson 5: Focus Beats Diversification in Capital-Intensive Businesses

Throughout its history, Borosil has resisted the temptation to diversify within the solar value chain. No module assembly, despite customers asking. No aluminum frames, despite having the manufacturing capability. No backsheets, despite the market opportunity. This focus allowed Borosil to achieve scale economies in solar glass that diversified competitors couldn't match.

The math is compelling. A solar glass furnace costs ₹300-400 crore and takes 12-18 months to build. Operating at 50% capacity destroys value; at 90% capacity, it prints money. By focusing solely on solar glass, Borosil ensures high utilization. A diversified player spreading capital across multiple products would achieve lower returns on each.

Lesson 6: Technology Transfer is Harder Than Technology Development

The GMB acquisition was partly about accessing European technology and transferring it to India. In reality, Borosil found that its Indian operations were often more advanced—lower costs, better yields, more innovative products. The technology transfer ended up flowing from India to Germany, not the reverse.

This challenges conventional wisdom about emerging market companies acquiring developed market assets for technology. In industries where process innovation matters more than product innovation, emerging market leaders may have already surpassed their developed market counterparts. The real value in such acquisitions is market access and customer relationships, not technology.

Lesson 7: Operational Excellence Compounds

Borosil's sustainable competitive advantage isn't any single factor but the compounding of multiple operational improvements over time. Each percentage point improvement in yield, each day reduced from delivery times, each new product variant adds to a cumulative advantage that becomes increasingly difficult for new entrants to overcome.

This is particularly true in capital-intensive manufacturing where small operational improvements have large financial impacts. A 2% improvement in furnace yield might seem trivial, but at 1,000 tons per day production, that's 20 tons of additional output daily—roughly ₹50 crore in additional annual revenue at current prices.

X. Financial Analysis & Investment Case

The numbers tell a story of transformation, crisis, and recovery. With a market capitalization of ₹7,882 crore, revenue of ₹1,479 crore, and a recent profit of -₹87.0 crore, Borosil Renewables trades at 7.90 times book value—metrics that demand careful interpretation given the German subsidiary's impact and the Indian expansion underway.

Current Financial Snapshot

The headline numbers are sobering. The company reported losses of ₹87 crore, driven entirely by the German subsidiary's bleeding. Strip out GMB's monthly losses of ₹9 crore, and the Indian operations are solidly profitable with EBITDA margins in the high 20s. This divergence between consolidated and core operations performance is critical for valuation.

The balance sheet remains relatively healthy despite the German misadventure. The company has reduced debt and maintains low interest coverage ratio, though the latter is distorted by the current losses. With the German insolvency filed, the debt metrics should improve substantially as GMB's liabilities are ring-fenced.

The working capital cycle has stretched as the company extends credit to module manufacturers facing their own cash flow pressures. Days sales outstanding have increased from 45 days to nearly 70 days, tying up roughly ₹200 crore in additional working capital. This is a calculated risk—supporting customers through difficult times to maintain relationships and market share.

The Bear Case: Multiple Headwinds

The pessimistic view focuses on several risks. First, the German write-off of ₹340 crore represents nearly 5% of market cap—a substantial destruction of shareholder value. Second, new capacity is being added by competitors, with at least two new entrants announcing solar glass projects. Third, Chinese manufacturers are finding ways around anti-dumping duties through third-country routing. Fourth, technology risk remains real—thin-film solar or new module architectures could reduce glass requirements.

The competitive threats are particularly concerning. Gold Plus Glass has announced a 500 TPD solar glass facility. Emerging players are targeting the market with aggressive pricing. While Borosil maintains technology and scale advantages, margins will likely compress as competition intensifies.

The global solar manufacturing landscape adds another risk layer. If India's module manufacturers can't compete with Southeast Asian producers despite protection, demand for domestic solar glass could disappoint. The same dynamics that killed European solar manufacturing could eventually impact India.

The Bull Case: Structural Growth Story

The optimistic view rests on India's structural solar buildout. With module manufacturing capacity heading to 150 GW by 2027 and solar installations targeting 280 GW by 2030, demand for solar glass will exceed domestic supply even with new entrants. Borosil's 1,600 TPD capacity (post-expansion) would serve roughly 10 GW annually—less than 10% of module manufacturing capacity.

The anti-dumping duties fundamentally change the economics. Prices for solar glass have strengthened significantly, with Q4 FY25 average ex-factory prices up 28% year-on-year as a result of a gradual increase in the selling prices towards the reference price under Anti-dumping duty measures applicable to imports from China. This pricing power should flow directly to margins once capacity utilization normalizes.

The expansion economics are compelling. The ₹950 crore investment for 600 TPD capacity implies a capital cost of roughly ₹1.6 crore per ton of daily capacity. At current prices and 90% utilization, this capacity should generate ₹900-1,000 crore in annual revenue with EBITDA of ₹250-300 crore—a 3-4 year payback even assuming some margin compression.

Valuation Perspectives

At 7.90 times book value, Borosil appears expensive on traditional metrics. But book value is misleading for a company where replacement cost far exceeds historical cost. Building Borosil's 1,000 TPD capacity today would cost ₹1,500-2,000 crore versus a book value of under ₹1,000 crore.

On earnings metrics, the valuation is harder to assess given current losses. But assuming normalized Indian operations' EBITDA of ₹400 crore (post-expansion) and applying a 12-15x multiple (reasonable for infrastructure-like assets with long-term demand visibility), implies a valuation of ₹4,800-6,000 crore. Add net cash and investments, and the current market cap doesn't seem unreasonable.

The comparison with global peers is instructive. Xinyi Solar, the world's largest solar glass manufacturer, trades at 15x EBITDA despite slower growth. Japanese peer NSG Group trades at 8x EBITDA but faces structural challenges. Borosil's valuation appears fair in this context, particularly given India's superior growth dynamics.

The Investment Decision

The investment case ultimately depends on your view of three key questions:

- Will India's solar manufacturing ambitions materialize, or will imports continue to dominate despite policy support?

- Can Borosil maintain its domestic market share as new competitors enter, or will the market fragment?

- Has management learned from the German misadventure, or will they pursue other value-destructive international expansions?

If you believe India's solar manufacturing will succeed (supported by policy), Borosil will maintain 30-40% market share (given technology and scale advantages), and management will stay focused on India (as recent statements suggest), then the current valuation offers reasonable risk-reward.

The key monitorables are clear: monthly production volumes, pricing trends versus Chinese imports, new competitor capacity actually materializing versus announcements, and module manufacturer health. Any weakness in these metrics would challenge the bull case.

XI. Looking Forward & Key Questions

As we look toward the next decade, Borosil Renewables stands at an inflection point. The German chapter is closed, the Indian expansion is underway, and the company must navigate an increasingly complex competitive landscape while capitalizing on India's renewable energy ambitions.

Can Borosil Maintain Its Domestic Monopoly?

The comfortable monopoly Borosil enjoyed for over a decade is ending. Gold Plus Glass, Emerging Technologies, and others have announced solar glass projects totaling over 1,000 TPD. While many announcements may not materialize—solar glass is harder than it looks—some new capacity will definitely come online.

Borosil's defense rests on three pillars. First, technology leadership—the company remains 2-3 years ahead in product development. Second, customer relationships—every major module manufacturer has qualified Borosil glass, creating switching costs. Third, scale economics—at 1,600 TPD post-expansion, Borosil will have lower unit costs than subscale competitors.

History suggests the market will fragment but not dramatically. In China, despite dozens of players, the top three control 60% market share. India will likely follow a similar pattern—Borosil maintaining 35-45% share, two or three credible competitors emerging, and several subscale players struggling for profitability.

What's the Real TAM for Solar Glass in India?

The headline numbers are staggering—150 GW of module manufacturing capacity by 2027, requiring roughly 25,000 TPD of solar glass capacity. But the real addressable market is smaller. Some module capacity will remain unutilized, competing with cheaper imports. Some manufacturers will use imported glass despite duties. Technology evolution might reduce glass requirements.

A realistic scenario suggests 60-70 GW of active module production by 2027, with 70% using domestic glass, implying demand for 8,000-10,000 TPD. Against likely supply of 3,000-4,000 TPD (including new entrants), the market remains structurally short. This supply-demand imbalance should support pricing and utilization for efficient producers like Borosil.

Longer term, the opportunity extends beyond India. Bangladesh, Sri Lanka, and African markets are beginning their solar journeys. Southeast Asian module manufacturers might source from India to diversify from China. The export opportunity could add 20-30% to domestic demand by 2030.

Will the German Insolvency Decision Prove Prescient or Premature?

The decision to file for GMB's insolvency looks correct today—Europe's solar manufacturing is in terminal decline. But what if European reshoring accelerates? What if energy security concerns drive massive policy support? Could Borosil have given up on Europe too early?

The precedent isn't encouraging. Every few years, Europe announces solar manufacturing revival plans. None have succeeded against Asian competition. The structural disadvantages—energy costs, labor costs, lack of ecosystem—are simply too large. Borosil's decision to cut losses and refocus on India appears strategically sound.

More interesting is whether Borosil will attempt international expansion again. Management statements suggest focus on India, but the company's ambition and the lure of global markets remain. The next attempt, if any, would likely be in emerging markets with growing domestic solar ambitions—Middle East, Africa, or Latin America—rather than developed markets.

Technology Disruption Risks

The biggest long-term threat isn't competition but technology change. Thin-film solar, which uses minimal glass, could reduce demand. Perovskite tandem cells might require different glass specifications. Building-integrated photovoltaics could shift value from commodity glass to specialized products.

Borosil's response has been to stay close to technology evolution. The company works with leading research institutions, participates in module manufacturer R&D programs, and maintains flexibility in its manufacturing processes. The new furnaces can produce various glass types, not just current specifications.

The more likely scenario is evolution, not revolution. Solar technology has proven remarkably stable—crystalline silicon has dominated for 40 years despite numerous challengers. Glass requirements might change gradually, but the fundamental need for a transparent, protective front sheet will remain.

The Next Decade of India's Renewable Energy Buildout

India's renewable ambitions keep expanding. The latest target is 500 GW by 2030, with solar comprising 280 GW. Beyond utility-scale, rooftop solar, agri-photovoltaics, and floating solar offer new markets. Each segment has different glass requirements, creating opportunities for product differentiation.

The policy environment remains supportive but increasingly complex. State-level policies vary widely. Grid integration challenges are mounting. Land acquisition for renewable projects faces resistance. Borosil must navigate this complexity while maintaining growth momentum.

Climate change adds urgency. India's commitments under Paris Agreement, net-zero targets, and increasing climate impacts drive political will for renewable expansion. This isn't just about economics anymore—it's about national resilience. Companies enabling this transition, like Borosil, benefit from this strategic imperative.

The Ultimate Question: Enabler or Beneficiary?

The fundamental question for Borosil is whether it remains an enabler of India's energy transition or becomes a true beneficiary. Enablers provide essential inputs but capture limited value. Beneficiaries build platforms that compound value over time.

Borosil's current position is clearly as an enabler—providing essential input to module manufacturers who capture more value. The company's attempts to move up the value chain have been limited. Unlike some competitors globally who have integrated into module manufacturing, Borosil remains focused on glass.

This might be the right strategy. In rapidly evolving industries, focused suppliers often outperform integrated players. Borosil's discipline in sticking to solar glass, despite opportunities to diversify, might prove to be its greatest strategic decision.

XII. Outro & Resources

After eight hours of diving deep into Borosil Renewables, what surprised us most wasn't the German failure—international expansion is hard and many companies stumble. It wasn't even the remarkable growth from 180 TPD to potentially 1,600 TPD in just 15 years. What's truly surprising is how a 60-year-old laboratory glassware company recognized a generational opportunity in solar glass before almost anyone else in India and executed with the patience and discipline to build a dominant position.

The Borosil story is ultimately about industrial transformation in the 21st century. It shows that manufacturing still matters, that emerging markets can build globally competitive positions in advanced materials, and that patient capital deployed with strategic clarity can create enormous value. It also shows the perils of international expansion, the importance of policy alignment, and the brutal economics of commodity manufacturing.

Key Takeaways for Investors:

The investment case rests on a simple thesis: India's solar manufacturing ambitions will succeed, creating sustained demand for domestic solar glass. If you believe this thesis, Borosil offers one of the few pure-play ways to invest in this theme. If you're skeptical, the valuation offers little margin of safety.

The German write-off, while painful, might prove to be a blessing. It forces management to focus on the massive Indian opportunity rather than pursuing international adventures. It cleans up the balance sheet and income statement, making the core business performance visible. Most importantly, it's a ₹340 crore education in why manufacturing economics are local.

The competitive threats are real but manageable. New entrants will definitely impact margins, but the market is large enough for multiple players. Technology disruption is possible but likely gradual. The biggest risk might be execution—managing rapid capacity expansion while maintaining quality and customer relationships.

Lessons for Operators:

For industrial companies contemplating strategic pivots, Borosil offers a template. Start with deep technical competence in an adjacent area. Time entry for when market demand is about to inflect, not after it's obvious. Build scale aggressively once product-market fit is established. Resist diversification temptations that dilute focus.

The importance of government relations in industrial businesses cannot be overstated. Borosil benefited from multiple policy interventions—not through special favors but by aligning its investments with stated policy goals. Understanding policy direction and positioning accordingly is strategic, not opportunistic.

The discipline to stay focused despite opportunities to diversify is perhaps the hardest lesson. Every conference, every customer meeting, every banker pitch brings new ideas for growth. Saying no to good opportunities to stay focused on great ones requires tremendous discipline—discipline that Borosil has mostly maintained.

Final Thoughts:

In the pantheon of Indian industrial stories, Borosil Renewables deserves recognition not for its size—it remains a mid-cap company—but for its transformation. From making test tubes to enabling India's energy transition, from family enterprise to professional management, from domestic focus to international ambitions and back again, Borosil has navigated multiple transitions that would have broken many companies.

The next chapter is being written now. As India races to install 280 GW of solar by 2030, as module manufacturing localizes, as technology evolves, Borosil must continue innovating, expanding, and executing. The company that made India's first solar glass in 2010 must now help build the infrastructure for India's energy independence.

Whether Borosil Renewables becomes a case study in successful industrial transformation or a cautionary tale about the challenges of scaling manufacturing businesses will be determined in the next five years. The pieces are in place—dominant market position, expanding capacity, supportive policies, and growing demand. Execution will determine everything.

For India's energy transition, companies like Borosil are essential infrastructure. They're the picks and shovels providers to the renewable gold rush. Without domestic solar glass, India's solar ambitions remain dependent on imports, vulnerable to supply chain disruptions and geopolitical tensions. In that context, Borosil's success isn't just about shareholder returns—it's about national energy security.

The story of Borosil Renewables is far from over. Like the best business stories, it continues to evolve, surprise, and teach. Whether you're an investor evaluating the stock, an operator learning from their journey, or simply someone interested in how industries transform, Borosil offers lessons worth studying. In the end, it's a story about seeing the future clearly—perhaps as clearly as the ultra-transparent solar glass they manufacture—and having the courage to bet everything on that vision.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube