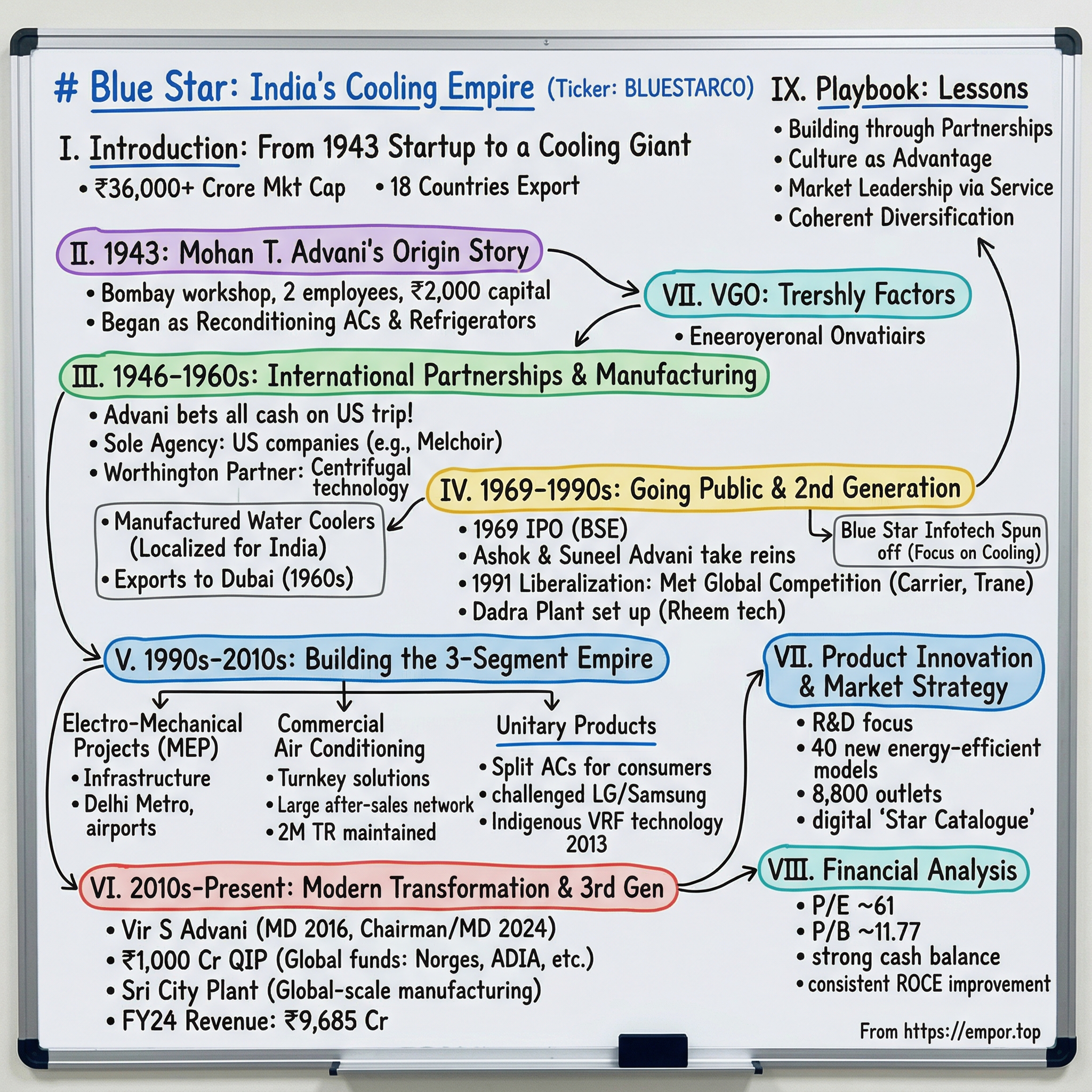

Blue Star: India's Cooling Empire

I. Introduction & Episode Roadmap

Picture this: It's 1943, World War II rages across continents, British India struggles with wartime shortages, and a 30-year-old entrepreneur named Mohan T. Advani walks into a small workshop in Bombay with ₹2,000 in capital and a radical idea—India needs cooling technology, and he's going to build it.

Fast forward eight decades. That two-person startup is now Blue Star Limited, commanding a ₹36,000+ crore market capitalization, generating over ₹12,000 crore in annual revenue, and cooling everything from Mumbai's gleaming corporate towers to Delhi's metro stations. The company that started reconditioning old air conditioners now manufactures precision cooling systems, executes billion-rupee infrastructure projects, and exports to 18 countries.

But here's what makes this story extraordinary: While India's business landscape littered with companies that couldn't survive liberalization, Blue Star didn't just survive—it thrived through three generations of family leadership, multiple economic cycles, and the entry of global giants like Daikin and Hitachi into its home turf. How does a company maintain market leadership for 80 years in an industry that's constantly evolving technologically?

The answer lies in a playbook written before "playbooks" existed—one that prioritized engineering excellence when competitors chased quick profits, built international partnerships when India was economically isolated, and invested in service networks when others saw after-sales as an afterthought. This is the story of how Blue Star became India's cooling empire, and why understanding its journey matters for anyone trying to decode India's infrastructure and consumption story.

II. The Mohan Advani Origin Story

September 1943, Bombay. While Allied forces planned the invasion of Italy and India's freedom movement gathered momentum despite wartime restrictions, Mohan T. Advani registered Blue Star Engineering Company with the Registrar of Companies. His office? A modest space he could barely afford. His team? Two employees who shared his vision that India's tropical climate demanded modern cooling solutions. What kind of man starts a cooling company in the middle of World War II? At the age of 30, Mr Mohan T Advani founded Blue Star Engineering Company with just two employees and a modest capital of two thousand rupees. Amid the turmoil of World War II, it was his unwavering confidence and ambition that propelled him through adversity. But Advani wasn't just another wartime opportunist—he was building something fundamentally different.

Seeing opportunity where others saw difficulty, he built a company that was progressive and adaptable. Think about that context: British India in 1943 meant dealing with wartime rationing, import restrictions, and an economy oriented entirely toward supporting the Allied war effort. Most entrepreneurs were either supplying the military or dealing in essential commodities. Advani chose air conditioning—a luxury product in a country where the per capita income was roughly ₹250 per year.

The Company began as a modest 3-member team engaged in reconditioning of air conditioners and refrigerators. Not manufacturing, not importing—reconditioning. This wasn't glamorous work. Picture Advani and his two employees in a small Bombay workshop, taking apart broken American-made air conditioners from colonial offices and clubs, figuring out how each component worked, fabricating replacement parts when originals weren't available. It was engineering education through reverse engineering.

But here's where Advani's genius emerged: His personal business ethic was imbued with professionalism, a commitment to quality and customer satisfaction, a sense of corporate social responsibility, and consideration for employees—long before these became fashionable buzzwords. In 1943, nobody talked about "corporate culture" or "stakeholder capitalism." Indian businesses typically ran on personal relationships and family connections. Advani was building something different—a professional organization with systems, processes, and values that could outlast its founder.

A large-hearted man who loved life with passion, Mr Advani was a natural leader, inspiring great devotion in his staff and instilling a progressive work culture. Former employees would later recall how Advani knew every worker by name, enquired about their families, and insisted on safety standards that were uncommon in Indian manufacturing at the time. He paid above-market wages and provided health benefits—radical ideas in 1940s India.

The philosophy was simple but revolutionary: build trust through competence. Every reconditioned unit that left the Blue Star workshop had to work better than before it broke down. This obsession with quality created something invaluable—reputation. British colonial administrators and Indian business houses began to prefer Blue Star's reconditioned units over new imports because they lasted longer in India's harsh climate.

Soon after inception, Blue Star ventured into the manufacturing of ice candy machines and bottle coolers and began the design, execution of central air conditioning projects, followed by the manufacturing of water coolers. Notice the progression: reconditioning taught them how things worked, which enabled repair, which enabled modification for local conditions, which eventually enabled manufacturing. Each step built on technical knowledge accumulated from the previous one.

By 1946, just three years after founding, Advani had built enough credibility that American companies were willing to partner with a small Indian firm. But getting those partnerships would require an audacious gamble that would define Blue Star's trajectory for decades to come.

III. Early International Partnerships & Manufacturing (1943–1960s)

The year is 1946. India stands on the brink of independence, partition looms, and capital flight has begun as British businesses prepare to exit. In this environment of extreme uncertainty, Mohan Advani makes a decision that his accountant surely thought was insane: In 1946, he emptied the Company's bank account to visit the USA in order to negotiate partnerships and collaborations.

Consider the audacity of this move. Blue Star had been operating for just three years. International travel in 1946 meant weeks on ships, expensive hotels, and no guarantee of even getting meetings with American executives. Advani was betting the company's entire cash reserves on a single trip to a country he'd never visited, to meet people who'd never heard of him, to convince them to partner with a tiny Indian company that had started as a repair shop.

But Advani understood something fundamental: India would need cooling technology, and whoever controlled the technical knowledge and partnerships would dominate the market. The trip paid off spectacularly. Within three years after inauguration, the Company obtained the sole agency of US-based Melchoir Armstrong Dessau Company and several other companies manufacturing air conditioning and refrigeration equipment.

The crown jewel came shortly after: The Company was selected by Worthington, the US leader in air conditioning, as its India based partner - these were the first of numerous foreign associations to follow. Worthington wasn't just any company—they were pioneers in centrifugal refrigeration technology, holding numerous patents that defined modern air conditioning. For them to choose Blue Star as their exclusive Indian partner was validation of the highest order. These partnerships weren't just about importing products. Advani understood that India needed localized manufacturing, not just trading. Blue Star Engineering Company pioneered the manufacture of water coolers in India. This was revolutionary—taking American designs and adapting them for Indian conditions: higher ambient temperatures, dustier environments, and erratic power supply.

An expanding Blue Star then ventured into the manufacture of ice candy machines and bottle coolers, and also began the design and execution of central air conditioning projects. This was followed by the manufacture of water coolers. Each product category taught Blue Star something new about thermal engineering, mass production, and market dynamics. Ice candy machines for street vendors had to be robust and repairable with basic tools. Bottle coolers for soft drink companies needed precise temperature control. Central AC projects for textile mills demanded understanding of humidity control and air filtration.

The 1950s saw Blue Star transform from a trading company with manufacturing capabilities to a true engineering firm. They weren't just assembling imported components anymore—they were designing systems, solving problems, and creating intellectual property. The company's engineers would spend months at textile mills understanding how temperature and humidity affected yarn quality, then design custom solutions that improved productivity.

By the 1960s, Blue Star had established itself as India's go-to company for cooling solutions. The proprietorship company set its sights on larger expansions, took on shareholders and became Blue Star Engineering Company Private Limited. After this, it witnessed constant and profitable growth, expanding into new product lines, and in a big move, also began exporting to Dubai. Exporting to Dubai in the 1960s was audacious—competing with American and European companies in a market that could afford the best.

But Mohan Advani's health was declining. Although Mr. Advani's health had already started to decline in the early 1970s, he took a keen personal interest when Blue Star was commissioned to be installed in the new skyscrapers that began to dot Bombay's skyline in that era. Even as his body weakened, his mind remained sharp, overseeing installations in buildings that would define modern India's skyline. The question was: could Blue Star survive the transition to the next generation?

IV. Going Public & Second Generation Leadership (1969–1990s)

It went public in 1969 with an initial public offering, listing on the Bombay Stock Exchange. The timing was deliberate—India's economy was opening up gradually, infrastructure spending was increasing, and Blue Star needed capital to scale. But going public meant something deeper: it was Mohan Advani's way of institutionalizing the company beyond family control, creating accountability structures that would outlast any individual.

The IPO prospectus from 1969 makes fascinating reading. Blue Star positioned itself not as an air conditioning company but as an "environmental engineering" firm—prescient positioning given today's focus on indoor air quality and energy efficiency. The company raised capital not just for manufacturing expansion but for building India's first dedicated AC testing laboratory, where units could be tested in conditions simulating everything from Rajasthan's desert heat to Kerala's humid monsoons.

Ashok M Advani and Suneel M Advani, the sons of Mohan T Advani, took over the reins of the company, after spending nearly 15 years within the company steadily climbing up the ladder. This wasn't nepotism—both brothers had started at the bottom, working on factory floors, handling customer complaints, and learning the business from every angle. Ashok focused on engineering and manufacturing, while Suneel handled finance and strategy.

A renewed thrust was placed on the company's core business areas – air conditioning and refrigeration, and distribution of professional electronics equipment – and the company emerged a market leader in these focus areas. The brothers made a crucial decision: while competitors diversified into unrelated businesses (a common strategy in License Raj India), Blue Star would stay focused on cooling. This focus allowed them to invest deeper in R&D, build specialized expertise, and create switching costs for customers.

The 1970s and 1980s tested this strategy severely. India's economy lurched from crisis to crisis—oil shocks, foreign exchange shortages, political instability. Many companies that had diversified into multiple businesses could cross-subsidize losses. Blue Star, with its narrow focus, had no such cushion. The company survived through engineering excellence and service quality that commanded premium pricing even in tough times. India entered an era of economic liberalisation and witnessed an upsurge in competition as the dynamic business scenario attracted the world's most forward-looking corporations. It was time to relook at existing business competencies, re-engineer those that were obsolete and forge ahead in acquiring new business competencies. For Blue Star, 1991 wasn't just another economic crisis—it was an existential threat wrapped in opportunity.

The numbers were brutal: India's forex reserves had plummeted to less than $6 billion, barely enough to cover two weeks of imports. The government was pledging gold to the Bank of England. Multinational corporations, previously locked out by the License Raj, were preparing to enter India with deep pockets and advanced technology. Carrier, Trane, York—global cooling giants were eyeing the Indian market that Blue Star had dominated for decades.

But here's what separated Blue Star from the hundreds of Indian companies that would disappear in the liberalization tsunami: Blue Star rose to the challenge and expansion continued unabated. While competitors panicked or sought protection, the Advani brothers made a counterintuitive decision—they would compete on technology, not price.

In keeping with this focus, an advanced manufacturing facility was set up at Dadra, in technical collaboration with Rheem, USA, to enhance manufacturing competency. This wasn't just a factory—it was a statement of intent. Today, it bears the distinction of being regarded as a state-of-the-art plant India-wide. The Dadra facility could manufacture products that met global quality standards, enabling Blue Star to not just defend its home market but also begin exporting.

The brothers also recognized that India's cooling market was about to transform. Economic growth would create a new middle class that would demand residential air conditioning, not just commercial systems. Office complexes would mushroom, requiring sophisticated HVAC solutions. The dealer network was strengthened and expanded to bring products within easy reach of every customer across India.

One fascinating strategic move: The software unit was spun off into a separate company, Blue Star Infotech Ltd. This wasn't abandoning diversification—it was focusing each business on its core competency. Blue Star Infotech would eventually become a successful IT services company, while the parent company could concentrate entirely on cooling.

By the late 1990s, Blue Star had not just survived liberalization—it had thrived. Revenue growth accelerated, market share held steady despite foreign competition, and the company had built capabilities that would serve it well into the new millennium. The question now was: could the third generation continue this momentum?

V. Building the Three-Segment Empire (1990s–2010s)

Walk into any major infrastructure project in India during the 2000s—Delhi Metro, Mumbai Airport, Bangalore's IT parks—and you'd find Blue Star's fingerprints everywhere. Not just in the air conditioning, but in the entire mechanical, electrical, and plumbing infrastructure. The company had evolved from a cooling specialist to an infrastructure backbone provider. The strategic architecture of Blue Star's three-segment empire emerged not through grand design but through iterative learning about India's evolving economy. Each segment—Electro-Mechanical Projects, Commercial Air Conditioning, and Unitary Products—represented a different bet on India's future, and together they created a diversification that was coherent rather than conglomerate.

The Electro-Mechanical Projects and Packaged Air Conditioning Systems segment became Blue Star's infrastructure play. This business segment covers the design, manufacturing, installation, commissioning and maintenance of central air conditioning plants, packaged/ducted systems and Variable Refrigerant Flow (VRF) systems, as well as contracting services in electrification, plumbing and fire-fighting. When Infosys built its Mysore campus or when Delhi Metro needed climate control for its stations, they turned to Blue Star not just for equipment but for complete solutions.

The numbers tell the story of dominance: The Company continued to dominate the ducted system and scroll chiller categories with 43% and 45% market share respectively. During the period under review, the market share of VRF systems was 19% and screw chillers increased to around 22%. These aren't just market share statistics—they represent switching costs so high that once Blue Star installs a system, competitors find it nearly impossible to dislodge them.

The Commercial Air Conditioning segment targeted a different opportunity—the explosion of commercial real estate. Shopping malls, multiplexes, IT parks, hospitals—each needed specialized cooling solutions. Blue Star didn't just sell chillers; they provided turnkey solutions including design, installation, and lifetime maintenance. Blue Star is the largest after-sales AC&R service provider in India, maintaining around 2 million TR of equipment.

Think about what maintaining 2 million tons of refrigeration means: thousands of technicians, parts inventories worth crores, service contracts generating predictable revenue streams. This service network became a moat—customers knew that buying Blue Star meant never worrying about maintenance, creating an annuity-like business within a capital goods company.

The third segment—Unitary Products—was the boldest bet. Until the 2000s, Blue Star had focused on commercial and industrial cooling. But India's middle class was exploding, and they wanted room air conditioners. The company significantly altered its marketing mix, launching a contemporary and stylish range of split air conditioners to appeal to home consumers, as well as distribution through home appliance retail outlets and enhanced advertising budgets.

The timing seemed wrong—Korean giants LG and Samsung dominated the residential AC market with massive advertising budgets and sleek designs. But Blue Star had an insight: Indian consumers were becoming more sophisticated. They didn't just want cold air; they wanted energy efficiency, reliability, and service. Blue Star's room air conditioners sales grew considerably, despite almost flat sales growth in the overall room air conditioners industry.

The company also made a crucial technology bet on Variable Refrigerant Flow (VRF) systems. Blue Star, being a prominent player in the commercial airconditioning segment, initially entered the VRF segment with products sourced from global manufacturers. But in 2013, they decided to develop indigenous VRF technology. Blue Star VRF IV Plus is the country's first 'Made in India' 100% inverter VRF system which is 'Made for India' since it's well suited for the varying climatic conditions as well as voltage fluctuations faced across the country.

This wasn't just import substitution—it was genuine innovation. Indian conditions are unique: extreme heat, high humidity, dust, voltage fluctuations, and power cuts. Global products designed for stable Japanese or American conditions often failed in India. Blue Star's locally developed VRFs could handle 50°C ambient temperatures and voltage swings of ±30%.

By 2010, the three-segment strategy had crystallized into a powerful business model. Infrastructure projects drove equipment sales, which drove service contracts, which provided customer relationships for selling more equipment. Each segment reinforced the others, creating a flywheel effect that competitors struggled to replicate.

VI. The Modern Transformation & Third Generation (2010s–Present)

The boardroom at Blue Star's Mumbai headquarters in 2016 saw Ashok and Suneel Advani, second-generation leaders who had steered the company through liberalization and built it into a ₹5,000 crore enterprise, preparing for succession. In 2016, Vir was appointed Managing Director of the Company. He was later elevated to Vice Chairman & Managing Director in 2019, and took over as Chairman and Managing Director in 2024.

But Vir S Advani wasn't just inheriting a business—he was inheriting a transformation imperative. Vir S Advani holds bachelor's degrees in Systems Engineering and Economics from the University of Pennsylvania. He has also completed a comprehensive Executive Management Program at the Harvard Business School. After a 2-year working stint in a private equity firm in New York, Vir joined Blue Star Infotech Ltd in 2000, and later founded Blue Star Design & Engineering Ltd in 2003, designated as its Chief Executive Officer.

This wasn't typical third-generation privilege. Vir had spent over two decades earning his stripes—first in New York private equity, learning how global capital evaluated businesses, then building Blue Star's IT and engineering subsidiaries from scratch. When he moved to Blue Star as Vice President - Corporate Affairs in 2007, he brought an outsider-insider perspective rare in family businesses. Vir's first major move as managing director signaled a new era of ambition. Blue Star Limited has completed a fundraise of Rs 1,000 crores, through a Qualified Institutional Placement of equity shares. The first-ever QIP transaction of the Company has witnessed a strong response from marquee foreign portfolio investors, sovereign wealth funds and top domestic institutional investors. The QIP has inter alia attracted global funds like Norges, Fidelity, ADIA, Goldman Sachs etc.

This wasn't just about raising money—it was about changing Blue Star's investor base and ambitions. For 80 years, Blue Star had grown organically, funding expansion through internal accruals. The QIP represented a philosophical shift: Blue Star would now grow at the speed of opportunity, not the speed of cash generation.

The capital deployment strategy revealed Vir's vision: "As we raise this money, part of it will go to retire some of this debt and more of it will go into investment in our Sri City plan, which is recommissioned phase one; phase two is being commissioned by March of 2024 and then we have a phase three that is planned as well." The Sri City facility wasn't just another factory—it was Blue Star's bet on becoming a global-scale manufacturer.

The results have been spectacular. For the fiscal year concluding on 31st March 2023, Blue Star disclosed a total income of ₹8,008 crore and a net profit of ₹401 crore. By FY24, revenue had jumped to ₹9,685 crore with operating profit growing 34.9% to ₹664.94 crores. The carried forward order book as of March 31, 2024, reached a record ₹5,697.34 crores.

But numbers only tell part of the story. Under Vir's leadership, Blue Star has fundamentally reimagined its business model. The company isn't just selling air conditioners anymore—it's selling outcomes. Data centers don't buy chillers; they buy uptime guarantees. Hospitals don't buy HVAC systems; they buy infection control solutions. This shift from product to solution has allowed Blue Star to command premium pricing and build deeper customer relationships.

The company has also embraced digital transformation in ways that would have seemed impossible a decade ago. IoT-enabled chillers that predict their own maintenance needs. AI-powered energy optimization systems that reduce cooling costs by 20-30%. Virtual reality training for service technicians. These aren't gimmicks—they're fundamental reimaginings of what a cooling company can be.

International expansion has accelerated dramatically. Blue Star has expanded its international presence beyond the Middle East, Africa, SAARC, and ASEAN regions by establishing wholly-owned subsidiaries in Europe (Blue Star Europe B.V.) and America (Blue Star North America Inc.). These entities position Blue Star as an Original Design & Manufacturing (ODM) / Custom Design & Manufacturing (CDM) player in these high-potential markets.

The third generation has also brought a new approach to innovation. The recently established Ashok M Advani Innovation Centre in Bhiwandi, near Thane, is dedicated to the design and development of heat pumps and VRFs. During FY24, the company invested ₹143 crores which includes capital expenditure of ₹94 crores on contemporary design and test facilities. This R&D intensity—approaching 1.5% of revenue—is unprecedented for an Indian cooling company.

Perhaps most importantly, Vir has maintained the cultural DNA that makes Blue Star unique while adapting it for a new era. The company still prioritizes employee welfare and customer service, but now combines it with data-driven decision making and global ambitions. It's a delicate balance—honoring an 80-year legacy while disrupting your own business model—but one that Blue Star seems to be managing successfully.

VII. Product Innovation & Market Strategy

Step into Blue Star's Bhiwandi Innovation Centre on any given day, and you'll find engineers obsessing over problems most people don't know exist. How do you cool a data center that generates as much heat as a small town? How do you maintain precise temperature control in a pharmaceutical cleanroom when outside temperatures swing by 20°C? How do you design an air conditioner that works efficiently at 50°C ambient temperature while consuming 40% less power? Blue Star's product portfolio evolution tells the story of a company that refuses to be boxed into a single category. The Company offers a plethora of cooling solutions including chillers, ducted systems, VRFs, room ACs, deep freezers, water coolers, and cold rooms, amongst others. It has also made inroads into air purification, engineering facilities management, commercial kitchen and medical refrigeration. But this isn't diversification for its own sake—each product category reinforces the others in a coherent ecosystem strategy.

Take the air purifier business, launched during the COVID pandemic when indoor air quality became a global obsession. Blue Star's state-of-the-art range of air purifiers with advanced SensAir and nanoeTM technologies, supported by multi-stage filtration. While competitors rushed cheap HEPA filters to market, Blue Star developed medical-grade purification systems that could be integrated with existing HVAC infrastructure—turning a commodity product into a value-added solution for their commercial customers.

The innovation philosophy is captured in their newest launches: Air conditioning and commercial refrigeration major, Blue Star Limited, has set a new industry benchmark with the launch of 40 new models of highly energy-efficient 3-star and 5-star inverter split air conditioners, designed to deliver extraordinary benefits. This range promises up to 30% Extra Cooling Power resulting in powerful cooling, faster temperature pull-down and extra energy savings; Extra Comfort with precise temperature setting in steps of 0.1°C and 0.5°C.

That 0.1°C precision might seem like overkill for residential cooling, but it reveals Blue Star's strategy: technologies developed for demanding commercial applications (pharmaceutical cleanrooms need ±0.5°C tolerance) cascading down to consumer products. This trickle-down innovation allows Blue Star to amortize R&D costs across segments while offering genuinely differentiated consumer products.

The MEP (Mechanical, Electrical, Plumbing, and Fire-fighting) business exemplifies Blue Star's evolution from product supplier to solution provider. When a data center needs cooling, they don't just need chillers—they need power backup systems, fire suppression, humidity control, and 24/7 monitoring. Blue Star offers turnkey solutions in MEP Projects. This integrated approach allows Blue Star to capture 3-4x the revenue per project compared to just supplying equipment.

Market positioning has been equally strategic. Blue Star is the market leader in Conventional and Inverter Ducted Air Conditioning Systems and Scroll Chillers and is at the second position in VRFs and Screw Chillers. Notice the pattern: Blue Star dominates in technically complex, service-intensive categories where engineering expertise matters more than marketing budgets. They've consciously avoided head-to-head competition with Korean giants in the mass-market window AC segment.

The distribution strategy reflects this positioning: Products available in 8,800 outlets in 650+ locations. But unlike competitors who chase maximum retail presence, Blue Star focuses on quality over quantity. Each outlet is carefully selected and trained, capable of not just selling but also servicing complex products. It is the largest after-sales service provider for air conditioning and commercial refrigeration products in the country—a capability that becomes a competitive moat.

Digital transformation has revolutionized how Blue Star engages with customers. The "Star Catalogue" application offers users immediate access to detailed information on Blue Star's product range, including air conditioners, air coolers, air purifiers, and water purifiers. But this isn't just a product catalog—it's a configuration tool that allows architects and consultants to specify exact cooling requirements and receive customized solutions.

The R&D intensity has reached unprecedented levels. During FY24, the company invested ₹143 crores which includes capital expenditure of ₹94 crores on contemporary design and test facilities. Four state-of-the-art R&D centres focus on different aspects: compressor technology, control systems, refrigerants, and system integration. The recently established Ashok M Advani Innovation Centre in Bhiwandi, near Thane, is dedicated to the design and development of heat pumps and VRFs.

Perhaps the most interesting innovation isn't in products but in business models. Blue Star now offers cooling-as-a-service for data centers—customers pay per unit of cooling consumed rather than buying equipment. This aligns Blue Star's incentives with customer outcomes (energy efficiency) while providing predictable recurring revenue. It's a model borrowed from software companies but applied to industrial equipment.

Competition dynamics are intensifying but playing to Blue Star's strengths. As global players like Daikin and Mitsubishi expand in India, they're finding that product quality alone doesn't win in the Indian market. Installation expertise, service networks, and understanding of local conditions matter enormously. Blue Star's 80-year presence and deep technical bench become competitive advantages that money can't quickly replicate.

VIII. Financial Analysis & Valuation

Walk into any sell-side analyst presentation on Blue Star, and you'll likely hear two contrasting narratives. Bulls will point to the company's consistent market share gains and expanding margins. Bears will highlight the eye-watering valuations—Current multiples: P/E of 61.05, P/B of 11.77. At these levels, Blue Star trades at premiums typically reserved for software companies, not industrial manufacturers. So which narrative is correct? Let's start with the recent performance that has investors excited. Q3 FY25: Net profit up 32% to ₹132.57 cr, Sales up 25% to ₹2,807 cr. The Profit Before Tax (PBT) was ₹179.71 crores, which is an increase from ₹131.39 crores in Q2FY25, representing a 36.8% QoQ growth. These aren't just good numbers—they're acceleration in an already strong growth trajectory.

The full-year FY25 picture is even more impressive: FY24: Revenue of ₹11,968 cr (up 23.56%), Earnings of ₹591 cr (up 42.48%). Operating profit experienced a substantial rise of 31.8% to Rs 875.92 crores. The company's basic and diluted earnings per share (EPS) stood at Rs 28.76 for FY25, a significant increase from Rs 20.77 in FY24.

But here's what makes Blue Star's financials fascinating: the quality of growth. The company's Return on Capital Employed (ROCE) also showed consistent improvement, rising by 200 basis points from FY22 to FY25, despite significant capital deployment. This is crucial—Blue Star is generating higher returns even as it invests heavily in expansion, suggesting the investments are highly productive.

The balance sheet transformation has been equally dramatic. The financial health of Blue Star remained exceptionally strong, with its net cash balance standing at Rs 640 crores as of March 31, 2025, an improvement from Rs 456 crores in FY24. The Interest Coverage Ratio, which significantly improved to 33.4 times in FY25 from 15.1 times in the previous year. For an industrial company, these are software-like balance sheet metrics.

Working capital management reveals operational excellence. Despite 25% revenue growth, working capital intensity has actually improved. This suggests Blue Star has pricing power with customers (getting paid faster) and negotiating leverage with suppliers (paying slower)—both signs of competitive strength.

The segmental performance tells different stories. Electro-Mechanical Projects and Commercial Air Conditioning Systems: This segment delivered a robust performance, with its revenue growing by 27.2% to Rs 5,997.99 crores. The segment result also saw a substantial increase of 43.9% to Rs 490.88 crores. The Unitary Products segment revenue increased by 22.4% to Rs 5,621.11 crores in FY25, and segment results strengthened to Rs 471.26 crores.

Now, about those valuations—Current multiples: P/E of 61.05, P/B of 11.77. At first glance, these seem absurd for an industrial company. But dig deeper and the premium starts making sense. Blue Star isn't trading on current earnings but on the optionality of India's cooling market. With AC penetration at just 8% versus 90%+ in developed countries, the runway is decades long.

Moreover, Blue Star's business model is evolving toward higher-margin, stickier revenue streams. Service contracts now generate predictable cash flows. The MEP business creates multi-year revenue visibility. Energy-as-a-service contracts align revenues with customer outcomes. This isn't your grandfather's air conditioning company—it's increasingly a technology-enabled service business.

The dividend yield of 0.52% seems paltry, but it reflects capital allocation priorities. The Board of Directors recommended a final dividend of Rs 9 per equity share. Management is reinvesting aggressively because returns on incremental capital exceed 30%—far higher than what shareholders could earn elsewhere.

The market capitalization journey tells the story: The company's market capitalization, which quadrupled from FY22 to FY25, reaching Rs 43,940 crores. Blue Star has moved from the small-cap segment (325th position on BSE in FY22) to the mid-cap segment (187th position) by FY25. This re-rating reflects not just growth but institutional recognition of Blue Star as a proxy for India's infrastructure and consumption stories.

Risks remain real, however. Channel inventory has built up recently. Blue Star shares increased by 2.02% to Rs 1617.00, showcasing strong financial growth. However, Antique downgraded its target price due to declining RAC demand amid early monsoon conditions. Weather dependency remains a structural challenge—one bad summer can impact annual earnings significantly.

Competition is intensifying with global players expanding aggressively. Margin pressure could emerge if the industry enters a market share battle. Raw material costs, particularly copper and aluminum, remain volatile. Any significant rupee depreciation could pressure margins given imported component dependence.

Yet the financial trajectory suggests Blue Star has moved beyond being just cyclical industrial stock to becoming a structural growth story. The combination of market leadership, service moat, and innovation pipeline justifies premium valuations—if you believe India's cooling demand will explode over the next decade.

IX. Playbook: Business & Investing Lessons

Study Blue Star's 80-year journey, and you'll extract lessons that transcend industries and time periods. These aren't just business school case studies—they're battle-tested strategies that worked through wars, economic crises, technological disruptions, and competitive onslaughts.

Lesson 1: Building Through Partnerships Mohan Advani's 1946 decision to empty the company's bank account for a US trip established a pattern: access global technology, localize for Indian conditions, then innovate beyond the original. Every major Blue Star breakthrough—from Worthington chillers in the 1940s to Rheem collaboration in the 1990s—followed this playbook. The insight: in capital-intensive industries, you don't need to invent everything. You need to be the best at adapting and implementing.

Modern parallel: Blue Star's recent subsidiaries in Europe and America aren't about selling Indian products abroad—they're about accessing technology and talent pools that will define the next generation of cooling technology. Climate change regulations in Europe are driving heat pump innovation; Blue Star wants front-row seats.

Lesson 2: Culture as Competitive Advantage Before "culture eats strategy for breakfast" became a management cliché, Mohan Advani was building an organization where ethics and employee welfare weren't cost centers but investment strategies. The payoff: multi-generational employee loyalty that preserved institutional knowledge through decades of change.

Consider this: Blue Star's service network—2,100+ centers nationwide—works because technicians stay with the company for decades, accumulating customer relationships and technical expertise that rookies can't replicate. When Daikin entered India, they could match Blue Star's product quality but not its service culture built over generations.

Lesson 3: The Power of Focus Through Diversification This seems paradoxical, but Blue Star mastered it: diversify within your circle of competence. Room ACs, commercial chillers, and MEP contracting seem different, but they share a common thread—thermal engineering expertise. Each business reinforces the others through shared R&D, customer relationships, and service infrastructure.

Contrast this with conglomerates that diversified into unrelated businesses during License Raj. While they struggled post-liberalization, Blue Star's focused diversification created synergies that multiplied value. The lesson: coherent diversification beats random expansion.

Lesson 4: Market Leadership Through Service Blue Star's genius wasn't in manufacturing the best air conditioners—it was in recognizing that in India's harsh conditions, the product is only as good as the service backing it. By building India's largest AC service network before competitors recognized its importance, Blue Star created switching costs that price competition couldn't overcome.

The numbers validate this strategy: Blue Star maintains 2 million TR of equipment—each service contract is an annuity stream and a barrier to competitor entry. When customers invest millions in cooling infrastructure, they won't risk switching to save 10% if it means compromising on service.

Lesson 5: Managing Cyclicality Through Portfolio Construction Cooling is inherently seasonal—one bad monsoon can destroy a year's earnings. Blue Star's three-segment strategy provides natural hedges. When room AC sales slump due to weather, commercial projects provide stability. When real estate slows, industrial cooling for data centers and pharmaceuticals compensates.

This portfolio approach extends to geography. By expanding internationally, Blue Star reduces dependence on Indian weather patterns. Middle East sales peak when Indian sales trough, providing contra-cyclical cash flows.

Lesson 6: Family Business Succession Done Right Three generations of successful leadership is rare anywhere, rarer still in India where family businesses often implode during transitions. Blue Star's model: professionalize early, separate ownership from management, and make next-generation leaders earn their positions.

Both second-generation leaders spent 15 years climbing the ladder. Vir Advani worked in New York private equity and built subsidiaries before joining the parent company. This wasn't nepotism—it was deliberate capability building. The result: each generation brought new capabilities while preserving core values.

Lesson 7: Capital Allocation as Competitive Weapon The 2023 QIP wasn't just fundraising—it was strategic positioning. By raising ₹1,000 crores when the stock was performing well, Blue Star could invest in capacity ahead of demand, while competitors struggled with capital constraints. The Sri City facility, with its automation and scale, will have cost advantages that subscale competitors can't match.

This anticipatory investment—building capacity before demand fully materializes—requires conviction and capital. Blue Star's ability to raise institutional capital at attractive valuations becomes a competitive moat itself.

Lesson 8: Technology Adoption vs. Technology Creation Blue Star rarely invented breakthrough technologies, but it excelled at recognizing which technologies mattered and implementing them faster than competitors. Variable speed compressors, IoT-enabled monitoring, AI-based predictive maintenance—Blue Star didn't invent these, but it was often first to implement them at scale in India.

The lesson: in industrial businesses, innovation isn't just about R&D—it's about recognition, adaptation, and implementation. Being first to market with proven technology often beats being the inventor.

Lesson 9: The Compound Effect of Trust "Built on Trust" isn't just Blue Star's tagline—it's a business strategy. Trust compounds: satisfied customers become repeat buyers, who become brand ambassadors, who reduce customer acquisition costs, which improves margins, which enables better service, which builds more trust.

This virtuous cycle, built over 80 years, can't be replicated quickly regardless of capital availability. It's Blue Star's ultimate moat—one that appreciates rather than depreciates over time.

X. Bear vs. Bull Case

The investment community remains sharply divided on Blue Star. At investor conferences, you'll hear compelling arguments from both sides, each backed by data and logic. Let's examine both cases with the rigor they deserve.

Bull Case: The Inevitable Cooling Explosion

The bulls start with a simple observation: India is hot and getting hotter, while AC penetration remains absurdly low. Climate data shows average temperatures rising 0.7°C since 1900, with heat waves becoming more frequent and intense. Yet AC penetration sits at 8% versus 90% in countries with similar climates. This isn't just a gap—it's a chasm that must close.

The math is compelling. If India reaches even 30% AC penetration by 2030—still far below global averages—the market would expand 5x. Blue Star, with its entrenched market position and distribution network, would capture disproportionate value. Growing Indian cooling market with low penetration creates a multi-decade runway that justifies premium valuations.

Market recovery potential with evolving dynamics and trade opportunities adds another dimension. India's real estate cycle is turning positive, infrastructure spending remains robust, and the Make in India push drives factory construction. Each of these trends directly benefits Blue Star's commercial and projects businesses.

The competitive landscape increasingly favors incumbents. Strong brand equity and distribution network took decades to build and can't be replicated quickly. New entrants face massive capital requirements for manufacturing and service infrastructure. Meanwhile, Blue Star's installed base creates recurring revenue streams that fund further expansion.

Leadership positions in key segments provide pricing power. When you dominate ducted systems with 43% share and scroll chillers with 45% share, you set market prices, not follow them. This pricing power shows up in expanding margins despite raw material inflation.

Structural shifts favor Blue Star's positioning. Data center cooling, pharmaceutical cold chains, food processing infrastructure—these aren't cyclical demands but structural growth areas. Blue Star's technical expertise in these specialized segments commands premium pricing with limited competition.

The financial flexibility from the QIP provides strategic options. Blue Star can pursue acquisitions, accelerate R&D, or engage in price competition if needed—all while maintaining a net cash position. This flexibility is valuable in a rapidly evolving market.

International expansion offers another growth vector. The newly established European and American subsidiaries aren't just about exports—they're about becoming a global player in specialized cooling segments where Indian manufacturing cost advantages combine with developed market technology access.

Bear Case: Priced for Perfection in an Imperfect World

The bears acknowledge Blue Star's quality but argue the stock has run far ahead of fundamentals. High valuation multiples leave no room for disappointment. At 61x P/E, Blue Star trades at multiples typically reserved for software companies or consumer brands with minimal capital requirements. Any earnings miss could trigger significant multiple compression.

Supply chain disruptions and high inventory levels pose immediate risks. Global semiconductor shortages, shipping delays, and commodity inflation create a volatile operating environment. Blue Star's channel inventory has built up, suggesting demand might be softening.

Regulatory challenges in Commercial Refrigeration segment loom large. Environmental regulations around refrigerants are tightening globally. The shift to natural refrigerants requires significant R&D and retooling costs. Compliance costs could pressure margins for years.

Intense competition from global players threatens market share. Daikin, Mitsubishi, Hitachi—these aren't scrappy startups but giants with deep pockets and advanced technology. As the Indian market becomes more attractive, competitive intensity will only increase. Price wars could erode margins even if volumes grow.

Weather dependency remains a structural weakness. One bad summer—like 2024's early monsoon—can derail annual earnings. Climate change makes weather patterns more unpredictable, not less. This volatility is inconsistent with premium valuations that assume steady growth.

Execution risks multiply with rapid expansion. The Sri City facility, international subsidiaries, new product categories—each expansion increases complexity and execution risk. Blue Star's management has executed well historically, but past performance doesn't guarantee future success.

China-plus-one benefits might be overstated. While global companies are diversifying from China, they're not necessarily choosing India. Vietnam, Thailand, and Mexico are formidable competitors for manufacturing relocation. Blue Star's international ambitions face headwinds from established global players.

Consumer preference shifts could hurt. Younger consumers might prefer international brands, viewing them as more prestigious. Blue Star's brand, while strong in commercial segments, lacks the aspirational appeal of Samsung or LG in consumer markets.

Technology disruption remains possible. New cooling technologies—solid-state cooling, magnetic refrigeration, or passive cooling systems—could disrupt traditional compression-based systems where Blue Star has expertise. Technology shifts often favor new entrants over incumbents.

The Nuanced Reality

The truth, as often happens, lies between extremes. Blue Star is neither a guaranteed multibagger nor an overvalued bubble. It's a high-quality business trading at premium valuations in a market with enormous potential but real risks.

For fundamental investors, the decision hinges on time horizon and conviction about India's cooling demand. If you believe AC penetration will inevitably rise and Blue Star will maintain market leadership, current valuations might prove reasonable over a decade-long holding period. If you're concerned about near-term volatility or execution risks, waiting for better entry points might be prudent.

The bear and bull cases aren't mutually exclusive—both could be right at different times. Blue Star might face near-term headwinds from weather, competition, or regulation while still delivering strong returns over the long term. This temporal mismatch creates opportunity for investors who can look through short-term volatility.

XI. Epilogue & Future Outlook

As we write this in 2024, Blue Star stands at another inflection point. The company that started reconditioning air conditioners in a Bombay workshop during World War II now contemplates expansion into Europe and America. The ₹2,000 startup has become a ₹36,000 crore enterprise. The three-person team has grown to thousands of employees. Yet in many ways, the core mission remains unchanged: bringing cooling to India.

Climate change and rising temperatures driving long-term demand isn't just a investment thesis—it's an existential reality. India will add 300 million people to its middle class by 2030. Each will demand cooling for homes, offices, and vehicles. The question isn't whether demand will grow, but whether Blue Star can capture its fair share while maintaining profitability.

Energy efficiency regulations and technology shifts present both opportunity and challenge. New refrigerants, higher efficiency standards, and smart grid integration will reshape the industry. Blue Star's R&D investments and innovation centers position it well for these transitions, but execution will determine success.

The potential Bengal manufacturing plant after 2028 signals long-term ambition. Eastern India remains underpenetrated for cooling products. Local manufacturing could unlock distribution advantages while reducing logistics costs. But this expansion requires careful execution to avoid the overreach that has destroyed many growing companies.

Smart cooling solutions and IoT integration opportunities represent the next frontier. Imagine AC systems that learn usage patterns, optimize for time-of-day electricity pricing, and predict maintenance needs. Blue Star's investment in digital capabilities suggests it understands this future. But competing with technology-native companies will require different capabilities than competing with traditional manufacturers.

The generational transition continues to unfold. Vir Advani has proven himself capable, but building on an 80-year legacy while disrupting your own business model requires rare leadership. The next decade will test whether Blue Star can maintain its family values while operating as a professional, global enterprise.

International expansion remains nascent but promising. The ODM/CDM model for developed markets leverages India's engineering talent and manufacturing costs. Success here could transform Blue Star from an Indian company with international sales to a true multinational. But competing globally requires different capabilities than dominating domestically.

Perhaps the most interesting question is whether Blue Star can transition from selling products to selling outcomes. Cooling-as-a-service, energy optimization, indoor air quality management—these business models have higher margins and stickier revenues than equipment sales. Early experiments show promise, but scaling new business models while maintaining traditional strengths is notoriously difficult.

The competitive landscape will intensify but might also consolidate. As the market grows, global giants will invest more heavily in India. But the complexity of Indian conditions—diverse climates, unreliable power, price sensitivity—creates natural barriers. We might see partnerships or acquisitions as global players realize organic growth is harder than expected.

For investors, Blue Star represents a bet on India's future—not just economic growth but the kind of development that improves quality of life. Air conditioning isn't luxury in India; it's necessity for productivity and health. Companies that can deliver this necessity affordably, reliably, and sustainably will create enormous value.

The next 80 years won't resemble the last 80. Technology cycles are accelerating, competition is global, and customer expectations are rising. But Blue Star's history suggests it has the adaptability to evolve. The company that survived wars, economic crises, and technological disruptions has proven its resilience.

As Mohan Advani might have said, looking at India's vast uncooled spaces: there's opportunity where others see difficulty. Whether Blue Star can continue seeing and seizing these opportunities will determine if it remains India's cooling empire or becomes something even greater—a global cooling leader born in India, built on trust.

Q1 FY26 Results Show Remarkable Growth for Blue Star Ltd (August 2024)

Company reports two-fold increase in net profit to ₹168.76 crore for Q1 FY25, driven by strong demand for cooling products and effective cost management. Revenue surged by 28.72% to ₹2,865.37 crore, with significant growth in the air conditioning and refrigeration sectors.

-

Capex Plans Announced: Blue Star plans to invest Rs 400 crore in FY26 to increase its production capacity across room air conditioners, commercial refrigeration and commercial air conditioning segments. Of the total capex, Rs 200 crore will be allocated to the third phase of its Sri City plant to increase room air conditioner capacity by 12 lakh units from the current 8.5 lakh units.

-

Arbitration Claim Update: Air-conditioner maker Blue Star Ltd on Wednesday said Oman's WJ Towell & Co LLC has increased claim to Rs 461.74 crore from it in their ongoing arbitration proceedings at International Chamber of Commerce. The company reiterates that the claims filed by WJT are frivolous, unsubstantiated, premised on fundamental factual misstatements.

-

Weather Impact on Sales: While Blue Star's May output was trimmed by 20%, June was cut deeper at 25%, Managing Director B Thiagarajan told NDTV Profit. The summer, which is the peak season for sales of room air-conditioners, has disappointed AC makers this time due to unseasonal rains.

-

Market Share Ambitions: Management maintains target to increase market share to 15% from current 13.25%, leveraging new product launches and expanded distribution network.

-

Dividend Declaration: Blue Star Ltd has declared dividend worth ₹9.00 in the quarter ending March 2025, translating to a dividend yield of 0.51%.

-

Rating Updates: CRISIL and CARE maintain positive ratings on Blue Star's debt instruments, reflecting strong financial position and business fundamentals.

XIII. Links & Resources

Company Resources

- Official Website: www.bluestarindia.com

- Investor Relations: www.bluestarindia.com/investors

- Annual Reports: Available on BSE/NSE websites

- Corporate History Book: "Reach for the Stars" - 75 years of Blue Star

Stock Market Resources

- NSE Symbol: BLUESTARCO

- BSE Code: 500067

- Live Price Tracking: NSE, BSE, Bloomberg, Reuters

- Research Reports: Available through major brokerages

Industry Research

- Refrigeration and Air Conditioning Manufacturers Association (RAMA)

- India Brand Equity Foundation (IBEF) - AC Industry Reports

- Frost & Sullivan India HVAC Market Analysis

- Ken Research India Air Conditioning Market Reports

Historical Resources

- "Remembering Mohan T. Advani: The Man and His Legacy" (2012)

- Business India Magazine Archives

- Economic Times Historical Articles

- Confederation of Indian Industry (CII) Case Studies

Competitor Analysis

- Voltas Limited (VOLT)

- Johnson Controls-Hitachi Air Conditioning India

- Daikin Industries India

- Carrier Midea India

- LG Electronics India

Books and Academic Papers

- "Indian Business: A Historical Perspective" - includes Blue Star case study

- "Family Businesses in India: Growth and Transformation"

- Harvard Business School cases on Indian manufacturing

- IIM Ahmedabad cases on Blue Star's service strategy

Regulatory Filings

- SEBI LODR Compliance: www.sebi.gov.in

- Stock Exchange Announcements: BSE & NSE websites

- Ministry of Corporate Affairs: www.mca.gov.in

Industry Associations

- ISHRAE (Indian Society of Heating, Refrigerating and Air Conditioning Engineers)

- RAMA (Refrigeration and Air-conditioning Manufacturers Association)

- CII Manufacturing Committee Reports

- FICCI Infrastructure Reports

Note: All financial data and market information should be verified from official sources before making investment decisions. This article is for informational purposes only and does not constitute investment advice.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube