Blue Dart: India's Express Logistics Revolution

I. Introduction & Setting the Stage

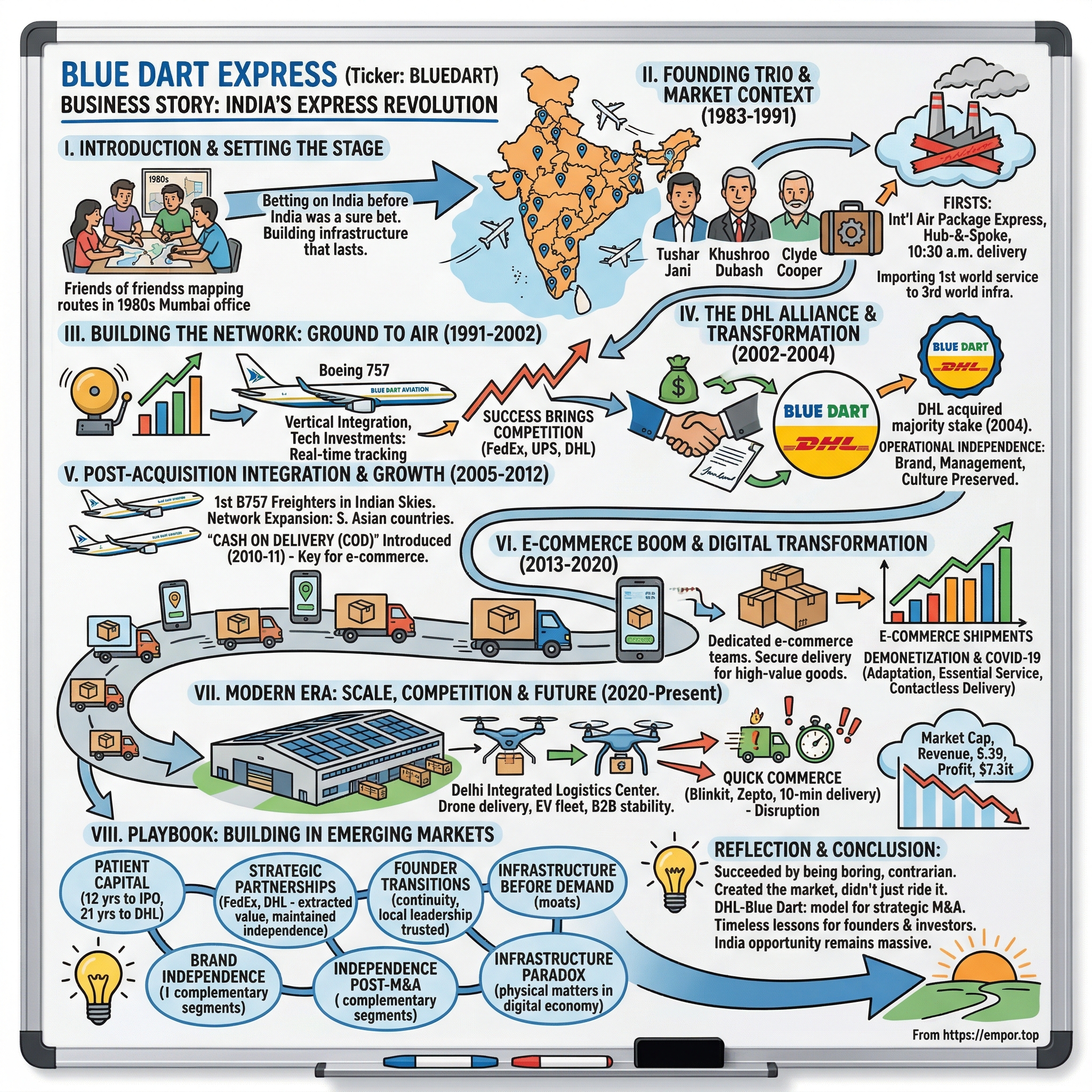

Picture this: November 1983, Mumbai. The city's old cotton mills are shutting down, the License Raj still grips the economy, and sending a document from Mumbai to Delhi reliably could take weeks through the postal system. In a small office in Fort, three friends—Tushar Jani, Khushroo Dubash, and Clyde Cooper—are sketching out routes on a map of India, dreaming of something audacious: a private express delivery network that could move packages across the subcontinent as reliably as Federal Express was doing in America.

Today, Blue Dart Express delivers to over 56,400 locations across India, operates Boeing 757 freighters, and serves as the backbone of South Asia's express logistics infrastructure. The company moves everything from life-saving medicines to smartphone orders, processing millions of shipments monthly through a network that would have seemed like science fiction in 1983. With a market cap of ₹14,072 crore and revenues of ₹5,819 crore, it stands as India's premier express air and integrated transportation company.

But here's the question that makes this story fascinating: How did three entrepreneurs bootstrap a courier company in the byzantine regulatory environment of 1980s India, build it into the country's logistics backbone, and structure a deal with DHL that preserved both their independence and growth trajectory? The answer reveals profound lessons about building infrastructure businesses in emerging markets, the art of strategic partnerships, and why sometimes selling to a competitor is the best path to winning.

This is the story of how Blue Dart didn't just build a logistics company—they built the rails on which modern Indian commerce would run. It's about betting on India before India was a sure bet, about building Boeing-scale operations when competitors were still using bicycles, and about a acquisition that defied conventional M&A wisdom. As we'll see, the Blue Dart playbook offers a masterclass in patient capital, strategic positioning, and the counterintuitive art of maintaining independence while being majority-owned.

II. The Founding Trio & Market Context (1983-1991)

The India of 1983 was a labyrinth of red tape and protectionism. Getting a telephone connection could take years. Starting a business required navigating dozens of government departments. Foreign companies were viewed with suspicion, and the very idea of private enterprise competing with government postal services seemed radical. Into this environment stepped three friends with complementary skills: Tushar Jani, a chartered accountant with a strategic mind; Khushroo Dubash, who understood operations; and Clyde Cooper, who brought international exposure and ambition. The trio's initial capital? ₹30,000—roughly $3,000 at 1983 exchange rates. They operated from a 200 square foot space under a staircase, birthing Blue Dart as an idea of delivering small packages and samples to support India's burgeoning exports. This wasn't just capital constraint; it was capital discipline. While government postal services operated from palatial colonial buildings, Blue Dart's founders understood that in logistics, every rupee saved on overhead could go toward building the network.

The founders' backgrounds were crucial to what came next. Tushar Jani, a science graduate from Mumbai University, had over 40 years of experience in the shipping and transport industry and had pioneered inland logistics of sea freight containers to manufacturers. His understanding of multimodal transport would prove essential. Khushroo Dubash brought operational expertise, while Clyde Cooper provided the international perspective that would help them forge critical early partnerships.

Their first masterstroke came immediately. They forged ties with Gelco Express International U.K., and introduced India's first international air package express service. This wasn't just about moving packages—it was about credibility. In 1983 India, associating with a British firm provided instant legitimacy in a market skeptical of private enterprise. When Gelco Express International was acquired by FedEx a year later, this made Blue Dart a global service participant of FedEx, accidentally positioning them at the center of the global express delivery revolution.

The regulatory environment they navigated was kafkaesque. Private companies couldn't legally compete with India Post on letter delivery. International shipments required multiple government clearances. Air cargo space was controlled by state-owned airlines. Yet the founders saw opportunity where others saw obstacles. They positioned Blue Dart not as a postal competitor but as a business-to-business express service, focusing on samples, documents, and small packages that businesses needed moved urgently.

By 1985, Blue Dart became the first carrier in India to provide domestic and international on-board couriers, a hub-and-spoke system and offered 10:30 a.m. delivery service. Think about the audacity of this promise: in an India where getting a train ticket required standing in line for hours, where phone calls dropped regularly, these three entrepreneurs were guaranteeing morning delivery. They weren't just building a logistics company; they were importing first-world service standards into a third-world infrastructure.

The hub-and-spoke model deserves special attention. While competitors were running point-to-point services—essentially sophisticated messenger operations—Blue Dart was building network effects into their business model from day one. Every new city added didn't just create linear value; it multiplied the value of the entire network. This was platform thinking before platforms were cool.

Tushar Jani was instrumental in founding and spearheading industry organizations, becoming the Founder Chairman of the Express Industry Council of India. He was responsible for setting up the Domestic Courier Common-user Terminals at Mumbai, Delhi, Kolkata and Chennai Airports, and the International Courier Common-user Terminals at Mumbai and Delhi Airports—a first-time private-public partnership. This wasn't just building a company; it was building an entire industry infrastructure.

The period from 1983 to 1991 saw Blue Dart transform from three friends with an idea to a company ready for institutional scale. On April 5, 1991, they incorporated as a private limited company, setting the stage for what would become one of India's most successful IPOs. The foundation was set: a network spanning major cities, partnerships with global players, and most importantly, a reputation for reliability in a market starved for it.

What's remarkable about this period is what the founders didn't do. They didn't try to be everything to everyone. They didn't chase government contracts that would have provided volume but compromised their service standards. They didn't expand internationally before securing their home market. This discipline—knowing what battles not to fight—would prove crucial as they prepared to take the company public and compete with global giants entering the liberalizing Indian market.

III. Building the Network: From Ground to Air (1991-2002)

The morning of May 12, 1995, marked a watershed moment in Indian logistics history. As the opening bell rang at the Bombay Stock Exchange, Blue Dart Express Limited became a publicly traded company, offering investors a chance to own a piece of India's express delivery revolution. The listing date came at a fascinating inflection point—India was four years into economic liberalization, foreign companies were eyeing the market hungrily, and Blue Dart had to decide whether to remain a closely-held operation or access capital markets to fund their ambitious expansion plans.

Incorporated on 5 April 1991, Blue Dart Express Limited became a public limited company in 1994. The transformation from private to public company wasn't just about raising capital—it was about institutionalizing what had been a entrepreneurial operation. The founders understood that to compete with global giants like FedEx and UPS, who were circling the Indian market, they needed not just money but credibility, governance structures, and the discipline that comes with quarterly reporting.

What made this period extraordinary was Blue Dart's decision to go vertical. While competitors were content to be ground-based courier services, relying on commercial airlines for long-distance transport, Blue Dart saw the writing on the wall: controlling your own air network was the only way to guarantee service levels in a country where infrastructure was still developing. This led to the creation of Blue Dart Aviation, a subsidiary that would operate dedicated cargo aircraft—a move so audacious that even today, the founders remain, with their two co-founders of Blue Dart, the only person to have launched a successful freighter airline in India.

The technology investments during this period deserve special attention. In an era before widespread internet adoption, Blue Dart introduced real-time, online tracking of all international shipments, offering customers control of their shipments like never before. They launched services with names that became synonymous with reliability: Dart Apex for time-definite deliveries, Dart Surfaceline for economical ground distribution, and the flagship Domestic Priority service that guaranteed next-day delivery to major metros.

By the late 1990s, Blue Dart had built something remarkable: a network that could move a package from Kashmir to Kanyakumari with the same reliability as DHL could move one from London to Paris. They were processing millions of shipments annually, operating a fleet that included everything from bicycles for last-mile delivery to chartered aircraft for intercity transport. The company had become India's logistics backbone, handling everything from legal documents to medical supplies to the first tentative e-commerce shipments.

But success brought attention, and attention brought competition. International players were no longer content to watch from the sidelines. FedEx had entered through acquisitions, UPS was building its network, and most intriguingly, DHL—the global express giant owned by Deutsche Post—was looking for a way into the Indian market. The stage was set for what would become one of the most interesting M&A stories in Indian business history.

The numbers tell part of the story: revenues growing at double digits, profitability despite massive infrastructure investments, and a brand that had become synonymous with express delivery in India. But the real asset was less tangible—Blue Dart had cracked the code of doing business in India. They understood how to navigate the country's complex geography, its diverse languages, its varying business practices, and most importantly, they had built trust in a market where trust was everything.

As 2002 approached, the founders faced a classic entrepreneur's dilemma. They could continue independently, raising capital from markets to fund expansion but potentially losing ground to deep-pocketed international competitors. Or they could find a strategic partner who could provide not just capital but global connectivity, technology, and operational expertise. The choice they made would reshape not just Blue Dart but the entire Indian logistics industry.

IV. The DHL Alliance & Transformation (2002-2004)

September 12, 2002. In a conference room overlooking Mumbai's business district, executives from Blue Dart and DHL Express signed papers that would fundamentally alter India's logistics landscape. On 12th September 2002, Blue Dart and DHL signed a Sales Alliance Agreement which came into effect from 1st October 2002. But this wasn't your typical distribution agreement—it was the opening move in a carefully choreographed dance that would culminate in one of the most successful foreign acquisitions in Indian business history. The strategic rationale was compelling. DHL needed a foothold in India, the world's second-most populous nation with a rapidly growing economy. Building a network from scratch would take years and billions of dollars. Blue Dart, meanwhile, needed capital to compete with global giants and technology to modernize their operations. It was a classic case of strategic fit—but the execution would prove to be the real story.

On 8 November 2004, DHL Express (Singapore) Pte Ltd entered into definitive agreements to acquire 68.21% stake in Blue Dart Express Ltd at Rs 350 per share. The 68% stake was bought for Rs 566.5 crore. The founders—Tushar Jani, Khushroo Dubash, and Clyde Cooper—along with Schroder Capital Partners Ltd, agreed to sell their controlling stake. The entire acquisition, including the open offer, was estimated to cost Rs 732.6 crore for DHL. In compliance with statutory requirements, DHL made a 20% mandatory open offer to public shareholders at Rs 350 per share.

What made this deal remarkable wasn't just the valuation—it was the structure. DHL Express invested €120 million in Blue Dart, becoming the majority shareholder in the company. But unlike typical acquisitions where the acquired company is absorbed into the parent, Blue Dart would continue to operate as an independent entity with its own brand name and management team. The founders didn't just cash out and leave; they remained involved in the business, ensuring continuity of relationships and culture.

The negotiation itself was a masterclass in balancing competing interests. DHL wanted control but needed Blue Dart's local expertise and relationships. Blue Dart's founders wanted liquidity but also wanted to preserve what they had built. The solution was elegant: DHL would get operational control with their majority stake, but Blue Dart would maintain its brand identity, management structure, and operational independence. This wasn't just an acquisition; it was a partnership disguised as a takeover.

DHL invested USD 163 million for the acquisition of the majority stake in Blue Dart Express in 2004. The price represented a significant premium—the stock had been trading at around Rs 320 before the announcement, making the Rs 350 offer price attractive to shareholders. But more importantly, it valued Blue Dart not just for what it was but for what it could become with DHL's backing.

The market reaction was telling. On BSE, the Blue Dart stock closed at Rs 320.25 per share, registering an increase of 5.59% over the previous day's close. Investors understood that this wasn't a typical foreign acquisition where value might be extracted and moved abroad. This was about building something bigger.

For the three founders, the decision to sell wasn't easy. They had built Blue Dart from a ₹30,000 investment into a company worth over ₹700 crore. But they also recognized a fundamental truth about the logistics business: scale matters. In their negotiations with DHL, they secured not just a good price but something more valuable—the promise that Blue Dart would remain Blue Dart.

The integration planning was meticulous. DHL and Blue Dart identified specific areas for synergy: Blue Dart would handle DHL's domestic distribution in India, while DHL would provide Blue Dart customers access to its global network. Technology systems would be upgraded but not replaced. The Blue Dart brand, which had become synonymous with reliability in India, would be preserved and even strengthened.

The foundation for this acquisition had been laid earlier—on 12th September 2002, Blue Dart and DHL signed a Sales Alliance Agreement which came into effect from 1st October 2002 on a principal to principal basis. This alliance was further strengthened in 2005 when DHL Express (Singapore) Pte. LTD. acquired 81.03% stake in Blue Dart.

What's fascinating about this period is what didn't happen. There were no mass layoffs, no dramatic strategy shifts, no attempt to "DHL-ize" Blue Dart. Instead, DHL treated Blue Dart as a crown jewel to be polished, not a acquisition to be integrated and optimized. This approach would prove prescient as Blue Dart entered its next phase of growth.

V. Post-Acquisition Integration & Growth (2005-2012)

The morning after the acquisition closed, Blue Dart employees across India woke up to find... nothing had changed. Their uniforms were the same, their trucks bore the same livery, their business cards still said Blue Dart. This was deliberate. While most foreign acquisitions in India led to rapid rebranding and restructuring, DHL took a radically different approach: if it ain't broke, don't fix it.

Blue Dart continues to operate as an independent entity with its own brand name and management team. This wasn't just corporate rhetoric. DHL understood something fundamental about the Indian market—relationships matter more than systems, trust matters more than technology, and the Blue Dart brand had earned both over two decades.

The real changes happened behind the scenes, and they were transformative. DHL poured capital into Blue Dart's infrastructure at a scale the company could never have managed independently. The crown jewel of this investment came in 2006. Blue Dart introduced the 1st Boeing 757 freighters in the Indian skies on 1st June 2006 with 2 of these aircraft connecting the 5 major metros of Delhi, Mumbai, Chennai, Bengaluru and Kolkata. A second flight was launched from Hyderabad while Ahmedabad became the 7th airport to join Blue Dart's network.

Think about the audacity of this move. In 2006, most Indian logistics companies were still figuring out ground transportation. Blue Dart was flying Boeing 757s—aircraft typically used by international airlines—for domestic cargo. These weren't small planes; a 757 freighter can carry over 40,000 kilograms of cargo. Blue Dart was essentially running an airline, but for packages instead of people.

The network effects were immediate and powerful. With dedicated air capacity, Blue Dart could guarantee morning delivery from any metro to any other metro. They could handle surge capacity during festivals. They could move time-sensitive cargo—medicines, legal documents, high-value electronics—with reliability that ground transport couldn't match. The competition was still hiring trucks; Blue Dart was operating a fleet that wouldn't look out of place at FedEx or UPS.

Technology integration proceeded carefully. Rather than forcing Blue Dart onto DHL's global systems, the companies created interfaces that allowed the two networks to communicate while preserving Blue Dart's operational independence. Customers could track packages seamlessly whether they were moving within India via Blue Dart or internationally via DHL. The backend complexity was hidden behind a simple, unified experience.

In 2012, DHL reduced its stake in Blue Dart Express to 75% in order to comply with statutory requirements. This wasn't a sign of DHL's diminishing interest—quite the opposite. Indian regulations required listed companies to maintain minimum public shareholding. DHL's willingness to reduce its stake while maintaining strategic control showed long-term commitment to both Blue Dart and Indian regulatory requirements.

The financial performance during this period validated the acquisition thesis. Revenues grew consistently, margins improved despite heavy capital investment, and market share increased. But more importantly, Blue Dart was transforming from a courier company into a logistics infrastructure provider. They weren't just moving packages; they were becoming the backbone of Indian commerce.

The aviation subsidiary deserves special attention. Blue Dart Aviation operated not just within India but across South Asian countries. This gave Blue Dart—and by extension DHL—unique access to markets like Bangladesh, Sri Lanka, and Nepal. While competitors needed to rely on commercial airlines or ground transport for regional connectivity, Blue Dart could offer guaranteed service levels across South Asia.

By 2010, Blue Dart had introduced a game-changing service that would position them perfectly for the e-commerce revolution about to sweep India. In 2010–11, it introduced 'cash on delivery (COD)' to its customers as an additional payment option for its courier services. This might seem like a small feature, but in a country where credit card penetration was still low and online payment systems were nascent, COD was the key that would unlock e-commerce for millions of Indians.

The cultural integration—or rather, the deliberate lack thereof—was perhaps DHL's smartest move. Blue Dart retained its entrepreneurial culture, its Indian identity, and its founder's vision. DHL provided capital, technology, and global connectivity, but didn't try to impose German corporate culture on an Indian company. This balance—global resources with local execution—would prove to be the template for successful foreign investment in India.

Management continuity played a crucial role. Key executives who had built Blue Dart remained with the company. Institutional knowledge was preserved. Customer relationships, painstakingly built over decades, remained intact. Supplier partnerships continued uninterrupted. This stability, rare in post-acquisition scenarios, allowed Blue Dart to focus on growth rather than integration challenges.

The 2008 financial crisis tested the relationship. As global trade contracted and DHL faced pressure worldwide, there might have been temptation to extract value from Blue Dart to shore up global operations. Instead, DHL continued investing. They understood that India's domestic consumption story was independent of global trade flows, and Blue Dart was perfectly positioned to capture this growth.

By 2012, Blue Dart had evolved from a domestic courier company into something much more significant—a critical piece of infrastructure for the Indian economy. They were moving everything from smartphone components to life-saving drugs, from legal documents to fashion merchandise. The company that started under a staircase with ₹30,000 was now operating Boeing aircraft and serving over 30,000 pin codes.

As Blue Dart entered 2013, the Indian e-commerce market was about to explode. Flipkart was gaining momentum, Amazon was preparing its India entry, and hundreds of startups were betting on online retail. They would all need one thing: reliable logistics. Blue Dart, with its DHL-backed infrastructure and two decades of operational excellence, was perfectly positioned for what would become the gold rush of Indian business.

VI. The E-Commerce Boom & Digital Transformation (2013-2020)

In 2013, something extraordinary was happening in Bangalore's tech corridors. Engineers who had returned from Silicon Valley were building what they called "India's Amazon"—Flipkart. In Gurgaon, fashion retailers were moving online. In Mumbai, entrepreneurs were launching everything from grocery delivery to furniture e-commerce. They all had one question: how do we get products to customers in a country where addresses could be "opposite the big banyan tree, third house from the temple"?

Blue Dart had spent three decades solving exactly this problem. But e-commerce would demand a fundamental reimagination of their business. Traditional B2B shipments were predictable—regular routes, known addresses, professional recipients. E-commerce was chaos—random addresses, cash transactions, size variations from mobile phones to washing machines, and customers who might refuse delivery because the color looked different online.

The transformation began with a simple recognition: e-commerce wasn't just another customer segment; it was a different business altogether. Blue Dart created dedicated e-commerce teams, separate operational processes, and specialized technology platforms. They became part of DPDHL's Post-eCommerce-Parcel (PeP) Division, aligning with the global recognition that e-commerce logistics was distinct from traditional express delivery.

Blue Dart is handling almost 8% of India's e-commerce shipments as of 2024. This number undersells their importance—Blue Dart became the premium option for high-value shipments, time-sensitive deliveries, and customers in difficult-to-reach locations. While competitors raced to the bottom on price, Blue Dart maintained its premium positioning, betting that reliability mattered more than cost for crucial shipments.

The cash-on-delivery (COD) infrastructure, introduced in 2010-11, became Blue Dart's secret weapon. In 2013, over 60% of Indian e-commerce transactions were COD. This wasn't just about collecting money—it was about managing cash flows, preventing fraud, and building trust. Blue Dart's delivery executives became temporary bank tellers, collecting hundreds of crores in cash monthly and ensuring it reached e-commerce companies safely.

Competition intensified dramatically. New players like Delhivery, founded in 2011, were built specifically for e-commerce. They had no legacy infrastructure, no B2B obligations, and venture capital backing that allowed them to lose money while building scale. Ecom Express, backed by Warburg Pincus, was aggressively expanding. Even Amazon and Flipkart were building their own logistics arms.

Blue Dart's response was counterintuitive. Instead of competing on price, they competed on capability. They launched temperature-controlled logistics for pharmaceutical e-commerce. They created secure delivery options for high-value electronics. They built specialized handling capabilities for fragile items. The message was clear: when your shipment absolutely, positively has to get there intact and on time, you choose Blue Dart.

In 2015, the company launched its 1st eFulfillment Centre in Delhi-NCR. During the year, the company acquired additional 21% stake in Blue Dart Aviation. The fulfillment center was a strategic move into warehousing and inventory management, allowing e-commerce companies to outsource their entire logistics operation to Blue Dart. The increased stake in Blue Dart Aviation ensured complete control over air logistics, crucial for next-day deliveries across India.

Technology became the battleground. E-commerce customers expected real-time tracking, delivery slot selection, instant customer service. Blue Dart invested heavily in digital infrastructure—mobile apps for customers, handheld devices for delivery personnel, API integrations for e-commerce platforms. They weren't just delivering packages; they were delivering data—proof of delivery, customer signatures, GPS coordinates, timestamp records.

In 2016, the company acquired its 6th Boeing 757-200 freighter. On 15 April 2016, Blue Dart Express announced that the company's Board of Directors has accorded its approval to enhance company's stake into Blue Dart Aviation from present 74% to 100%. Later, on 24 November 2016, Blue Dart Express completed the acquisition of the entire remaining 26% stake in Blue Dart Aviation, thereby making it a wholly owned subsidiary.

The full ownership of Blue Dart Aviation was strategic. With complete control over their air network, Blue Dart could optimize routes for e-commerce patterns—heavy southbound traffic for electronics from northern manufacturing hubs, fashion shipments from western India to the entire country, time-sensitive deliveries for the growing online pharmacy sector.

Then came November 8, 2016—demonetization. Overnight, 86% of India's currency became invalid. For a company handling crores in COD collections daily, this could have been catastrophic. But Blue Dart's rapid response—accepting old notes as per government guidelines, quickly implementing digital payment options, managing cash shortages across their network—turned crisis into opportunity. They proved they could adapt to the most dramatic economic disruption in Indian history.

The festive season sales became Blue Dart's Olympics. During Diwali 2017, Indian e-commerce companies generated over $3 billion in sales in just five days. Blue Dart's network processed multiples of normal volume, their aircraft flew extra sorties, their delivery personnel worked extended hours. The ability to scale up and then scale down smoothly became a competitive advantage that venture-funded startups couldn't match.

By 2019, Blue Dart was operating in a market transformed beyond recognition from even five years earlier. Same-day delivery was becoming standard in metros. Customers expected precise delivery slots. Returns were as important as forward logistics. The company that had pioneered next-day delivery in the 1990s was now competing with companies promising 10-minute delivery for groceries.

Then came March 2020. COVID-19 lockdowns brought India to a standstill. Overnight, e-commerce went from convenience to necessity. Blue Dart was classified as an essential service, their aircraft kept flying when commercial aviation stopped, their delivery personnel became lifelines for millions of locked-down Indians. The pandemic compressed five years of e-commerce growth into five months.

Blue Dart's response to COVID was remarkable. They implemented contactless delivery before it became standard. They created special protocols for handling healthcare shipments—vaccines, oxygen concentrators, medicines. They kept their network operational when competitors struggled with manpower shortages. The crisis validated decades of investment in infrastructure, training, and systems.

The company launched India's 1st Parcel Locker in Gurgaon and introduced Mobile Service Centres and Auto Sorters. These innovations addressed e-commerce pain points—failed deliveries, last-mile costs, sorting efficiency. Parcel lockers allowed customers to collect packages at their convenience. Mobile service centers brought Blue Dart to customers rather than waiting for them to visit offices. Auto sorters increased package processing speed dramatically.

As 2020 ended, Blue Dart emerged stronger from the pandemic. They had proven their resilience, demonstrated their essential nature, and shown that premium logistics had a place even in cost-conscious India. But the market was evolving again. Quick commerce was emerging, promising 10-minute deliveries. Direct-to-consumer brands were bypassing marketplaces. Social commerce was taking off. The next chapter would require another transformation.

VII. Modern Era: Scale, Competition & Future (2020-Present)

January 2025. The Delhi facility Blue Dart is opening isn't just another warehouse—it's a statement of intent. India's largest, low emission 2.5 lakh sq ft integrated logistics center at Bijwasan, Delhi represents a bet that despite quick commerce disruption and asset-light competitors, infrastructure still matters. In a world where Blinkit promises 10-minute delivery and Zepto raises billions to build dark stores, Blue Dart is playing a different game entirely.

The current financial snapshot tells a story of resilience and challenge. Market Cap: 14,041 Crore (down -25.1% in 1 year), Revenue: 5,819 Cr, Profit: 248 Cr. The market cap decline reflects investor concerns about quick commerce disruption, but the fundamentals remain solid. During the fiscal year ending March 31, 2024, revenue from operations stood at ₹ 5,268 crore, accompanied by a profit after tax of ₹ 289 crore.

What's remarkable is Blue Dart's ability to maintain profitability while competitors burn cash. The volumes have continued to grow with 9.5% growth in shipments and 4.4% growth in weights during the financial year. This volume growth, despite intense competition, validates their premium positioning strategy. They're not trying to compete with Delhivery on price or with quick commerce on speed for groceries—they're the reliable choice when it absolutely has to get there.

The competitive landscape has become almost unrecognizable from even three years ago. Quick commerce companies like Blinkit, Swiggy Instamart, and Zepto have redefined customer expectations. They're delivering not just groceries but electronics, fashion, even furniture in under 30 minutes in major cities. Traditional e-commerce players like Amazon and Flipkart have built massive logistics operations. New-age logistics companies backed by venture capital operate with unit economics that would have seemed impossible a decade ago.

Blue Dart's response has been strategic rather than reactive. Blue Dart Express Ltd., South Asia's premier express air and integrated transportation & distribution company, offers secure and reliable delivery of consignments to over 56,000+ locations in India. As part of DHL Group's DHL eCommerce division, Blue Dart accesses the largest and most comprehensive express and logistics network worldwide, covering over 220 countries and territories.

The technology investments are particularly interesting. Blue Dart launched drone deliveries in collaboration with a leading drone technology company, marking a significant advancement in cleaner and more efficient delivery solutions. Blue Dart stands as a frontrunner in harnessing drone technology for commercial use in the logistics sector. While others focus on dark stores in cities, Blue Dart is thinking about how to reach India's vast rural markets efficiently.

Sustainability has become more than corporate responsibility—it's a competitive advantage. In the first quarter, the company expanded its electric vehicle (EV) fleet, demonstrating its commitment to sustainability and reducing its carbon footprint. As global companies increasingly focus on supply chain emissions, Blue Dart's green credentials, backed by DHL's global sustainability initiatives, become a differentiator.

The aviation advantage remains crucial. With their fleet of Boeing 757 freighters and complete ownership of Blue Dart Aviation, they can guarantee service levels that ground-based competitors simply cannot match. During festive seasons, when e-commerce volumes spike 5-10x, having dedicated air capacity is the difference between meeting commitments and failing customers.

But challenges are mounting. Quick commerce is expanding beyond groceries—electronics, fashion, even documents are now being delivered in minutes in select areas. The capital intensity of Blue Dart's model—aircraft, warehouses, vehicles—contrasts sharply with asset-light competitors who use gig workers and rented vehicles. Margin pressure is real as customers increasingly expect faster delivery at lower costs.

The B2B segment, traditionally Blue Dart's stronghold, offers both stability and growth. B2C revenue up 20%, B2B 2.4% shows the diverging dynamics. While B2C grows rapidly, B2B provides the baseload volume and higher margins that support infrastructure investments. Corporate clients value reliability over speed, service quality over price—exactly Blue Dart's sweet spot.

International integration through DHL provides a moat that's hard to replicate. Indian companies expanding globally need seamless international logistics. Foreign companies entering India need a trusted local partner. Blue Dart serves both, leveraging DHL's global network while maintaining local expertise. This two-way bridge is increasingly valuable as India integrates deeper into global supply chains.

The management outlook reflects cautious optimism. We are optimistic about the opportunities that lie ahead. Aligned with India's development path, we are focusing on offering expedited deliveries across the country. They're not trying to win every battle—they're choosing battles where their strengths matter most.

Recent recognition validates their strategy. In 2024, Blue Dart received the distinction of being a Top Employer and Best Organization for Women. In a industry notorious for high turnover and poor working conditions, Blue Dart's ability to attract and retain talent is a competitive advantage.

Looking forward, Blue Dart faces an existential question: in a world of 10-minute delivery and gig economy logistics, what role does a premium, asset-heavy, reliability-focused player have? The answer might lie not in competing with quick commerce but in serving segments where their strengths matter most—B2B logistics, high-value shipments, international connectivity, and the vast Indian hinterland where quick commerce may never reach.

The investment in drone technology signals their vision for the future. While quick commerce fights over urban density, Blue Dart is thinking about how to serve 600,000 villages profitably. While competitors optimize for speed in metros, Blue Dart optimizes for reach across the subcontinent. It's a different game, with different rules, and potentially different winners.

VIII. Playbook: Building in Emerging Markets

The Blue Dart story offers a masterclass in building infrastructure businesses in emerging markets, but the lessons go far beyond logistics. When Tushar Jani, Khushroo Dubash, and Clyde Cooper started with ₹30,000 under a staircase, they weren't just building a courier company—they were writing a playbook that challenges conventional Silicon Valley wisdom about scaling, funding, and growth.

The Art of Patient Capital and Long-Term Thinking

Blue Dart took 12 years from founding to IPO, 21 years to reach acquisition by DHL. In today's world of 18-month unicorns and growth-at-all-costs mentality, this seems almost quaint. But patient capital created something venture funding rarely does: sustainable competitive advantage.

Consider the aviation decision. Starting an airline for domestic cargo in 1990s India wasn't just expensive—it was insane. The regulatory approvals alone could take years. The capital requirements were enormous. The operational complexity was staggering. A venture-funded startup would never make this bet; the payback period was too long, the risk too high. But Blue Dart understood that controlling air logistics would eventually become their moat.

This patience extended to market development. Instead of blitzscaling across India, Blue Dart methodically built density in each city before expanding. They understood that in logistics, network effects are local before they're national. Having 50% market share in Mumbai was more valuable than 5% market share in 10 cities. This density-first approach meant higher utilization, better economics, and superior service—a virtuous cycle that competitors couldn't easily break.

Strategic Partnerships vs. Going Alone

The progression from Gelco to FedEx to DHL reveals sophisticated partnership strategy. Each partnership served a specific purpose at a specific time. Gelco provided international credibility when Blue Dart was unknown. FedEx brought operational expertise when Blue Dart was scaling. DHL provided capital and global connectivity when Blue Dart needed to defend against global competition.

But here's what's remarkable: Blue Dart never became dependent on any single partner. When Gelco was acquired by FedEx, Blue Dart adapted. When the FedEx relationship ended, they pivoted to DHL. They extracted value from each partnership while maintaining operational independence. This is the opposite of the typical emerging market story where local companies become captive vendors to global giants.

The DHL deal structure was particularly clever. By maintaining brand independence and operational autonomy, Blue Dart kept its customer relationships and corporate culture intact. DHL got India exposure without the complexity of building from scratch. Both parties won because the deal structure aligned incentives rather than creating zero-sum dynamics.

Managing Founder Transitions Post-Acquisition

Most founder-led companies struggle post-acquisition. Founders cash out and leave, or stay and clash with new ownership. Blue Dart's founders did neither. They remained involved enough to ensure continuity but stepped back enough to allow professional management to scale the company.

This transition was enabled by the acquisition structure. The founders didn't sell 100%; they retained enough stake to stay engaged. DHL didn't impose its management team; they trusted local leadership. The board remained balanced between DHL representatives and independent directors. This governance structure prevented both founder syndrome and corporate colonization.

Building Infrastructure Before Demand

Blue Dart consistently built infrastructure ahead of demand. They launched morning delivery before customers expected it. They built aviation capability before volumes justified it. They created cash-on-delivery systems before e-commerce existed. This seems to violate the lean startup methodology of building minimum viable products and iterating based on customer feedback.

But infrastructure businesses are different. Network effects mean you need coverage before you get usage. Reliability requires redundancy, which looks like waste until you need it. Brand trust takes years to build and moments to destroy. Blue Dart understood that in logistics, you can't fake it till you make it—you have to make it before you can sell it.

This approach required different funding sources. Venture capital, with its emphasis on rapid scaling and quick exits, wouldn't have worked. Public markets, with quarterly earnings pressure, might have forced short-term thinking. The progression from founder funding to public markets to strategic acquisition provided the right capital at the right time for infrastructure building.

The Importance of Brand Independence Post-M&A

DHL's decision to maintain Blue Dart as an independent brand was counterintuitive. Most acquirers want to leverage their global brand, achieve marketing synergies, and consolidate operations. DHL did the opposite, and it worked brilliantly.

In India, Blue Dart meant trust, reliability, and local expertise. DHL meant foreign, expensive, and international. By keeping both brands, they could serve different segments without confusion. Blue Dart continued serving price-sensitive domestic customers while DHL served premium international needs. The brands were complementary, not cannibalistic.

This brand independence extended to operations. Blue Dart delivery personnel wore Blue Dart uniforms, drove Blue Dart vehicles, and carried Blue Dart devices. For customers, nothing changed except service got better. This continuity was crucial in a relationship business where the delivery person is often the only human touchpoint.

Lessons on Selling to a Strategic Buyer

The Blue Dart-DHL deal offers a template for selling to strategic buyers. First, build something they can't easily replicate—in Blue Dart's case, domestic network density and regulatory approvals. Second, time the sale when you have leverage—Blue Dart was profitable and growing when DHL approached. Third, structure the deal for long-term value creation, not just immediate payout.

The staged approach—partnership in 2002, majority acquisition in 2004, adjustment to 75% in 2012—shows sophisticated deal-making. Each stage allowed both parties to build trust, understand synergies, and adjust terms based on experience. This is very different from the binary acquire-or-compete dynamic that characterizes most strategic acquisitions.

Most importantly, Blue Dart understood that selling to a strategic buyer didn't mean selling out. They negotiated for operational independence, brand continuity, and management stability. They got capital and capabilities from DHL while retaining what made them special. This balance is rare in strategic acquisitions, where the acquired company often gets digested and disappears.

The Infrastructure Paradox

Blue Dart's story reveals what might be called the infrastructure paradox: the more digital and virtual the economy becomes, the more physical infrastructure matters. E-commerce needs warehouses. Cloud computing needs data centers. Digital payments need cash collection networks. The companies that own these physical assets have moats that software alone can't breach.

This is particularly true in emerging markets where infrastructure is underdeveloped. In the US, any logistics startup can tap into existing infrastructure—roads, airports, warehouses. In India, Blue Dart had to build much of this infrastructure themselves. This was expensive and slow, but once built, it became an almost insurmountable advantage.

The lesson for entrepreneurs and investors is that in emerging markets, infrastructure businesses might be better investments than software businesses. They take longer to build but last longer too. They require more capital but generate more sustainable returns. They're harder to scale but also harder to disrupt.

IX. Investment Analysis & Market Dynamics

Market Cap: 14,041 Crore, Revenue: 5,819 Cr, Profit: 248 Cr—these numbers frame Blue Dart as a profitable, mid-cap infrastructure play in a market obsessed with hypergrowth stories. But beneath these headline metrics lies a more nuanced investment thesis that challenges conventional wisdom about Indian logistics.

Unit Economics and Network Effects in Logistics

Blue Dart's unit economics tell a story of operational leverage finally paying off. After decades of infrastructure investment, the company generates roughly 4.3% net margins on ₹5,819 crore revenue. This might seem thin compared to software companies, but for logistics—where giants like FedEx operate at similar margins—this represents strong execution.

The network effects in Blue Dart's business are subtle but powerful. Each additional pin code served makes the network more valuable to all customers. Each additional daily flight increases reliability for the entire system. Each additional customer improves route density, which improves economics, which enables better service, which attracts more customers. This flywheel took decades to build and would take competitors years to replicate.

But here's the challenge: network effects in logistics are more fragile than in software. If Blue Dart's on-time delivery drops from 95% to 90%, customers notice immediately. If a social network has an outage, users complain but don't leave. This means Blue Dart must constantly invest in maintaining service levels, creating a capital intensity that weighs on returns.

Competitive Moats: Aviation Assets, Network Density, Brand Trust

The aviation assets represent Blue Dart's most tangible moat. Operating Boeing 757 freighters isn't just about capacity—it's about capability. During COVID, when commercial flights were grounded, Blue Dart's freighters kept flying. During festive seasons, when volumes spike, dedicated aircraft provide surge capacity. The regulatory approvals, pilot training, maintenance infrastructure, and operational expertise required to run an airline create barriers that money alone can't quickly overcome.

Network density in India's tier-2 and tier-3 cities provides another moat. While competitors fight over the top 50 cities, Blue Dart serves 56,000+ locations. This reach into India's hinterland becomes increasingly valuable as consumption broadens beyond metros. A merchant in Coimbatore selling to a customer in Imphal needs Blue Dart's network—quick commerce players simply don't operate there.

Brand trust, built over four decades, might be the strongest moat. In India, where cash-on-delivery still represents significant e-commerce volume, trust matters enormously. Customers trust Blue Dart with lakhs of rupees in cash daily. This trust can't be bought with marketing spend or created with technology—it must be earned through millions of successful deliveries.

Threats: Quick Commerce Disruption, Asset-Light Competitors

The quick commerce threat is real but perhaps overstated. Companies like Blinkit and Zepto are redefining delivery expectations in metros, but their model—dark stores every 2 kilometers, delivery partners waiting idle for orders, 10-minute delivery promises—works only in dense urban areas with high order values. Blue Dart's sweet spot—B2B shipments, intercity logistics, tier-2/3 coverage—remains largely unaffected.

Asset-light competitors pose a different challenge. Delhivery, with its variable cost model and venture funding, can undercut Blue Dart on price. Shadowfax and others use gig economy workers to avoid employee costs. These models generate inferior unit economics but can sustain losses longer thanks to venture capital. The question is whether they can maintain service quality without ownership of assets.

The larger threat might be vertical integration by large customers. Amazon and Flipkart already handle much of their own logistics. Large D2C brands are building in-house capabilities. If Blue Dart's largest customers become competitors, revenue concentration risk increases substantially.

Bull Case: India's Consumption Story, Infrastructure Play

The bull case for Blue Dart rests on India's structural transformation. With GDP per capita crossing $2,500, consumption patterns are changing. The formalization of the economy post-GST benefits organized players. The growth of manufacturing under "Make in India" increases B2B logistics demand. These are decade-long trends that favor established infrastructure players.

Blue Dart is handling almost 8% of India's e-commerce shipments as of 2024, but e-commerce itself is only 7-8% of retail. As this percentage doubles over the next decade, Blue Dart's volumes could grow dramatically even if market share remains constant. Add in B2B growth, international trade expansion, and new categories like healthcare logistics, and the runway appears long.

The infrastructure angle is compelling. As India builds national highways, dedicated freight corridors, and new airports, Blue Dart's existing network becomes more valuable. They can leverage public infrastructure investments while competitors must build from scratch. This operating leverage should expand margins over time.

The DHL parentage provides optionality. As global supply chains reconfigure and India becomes a manufacturing alternative to China, Blue Dart becomes the natural partner for multinationals. The ability to seamlessly connect Indian operations to global markets is a unique selling proposition that standalone domestic players can't match.

Bear Case: Margin Pressure, Capital Intensity

The bear case centers on structural margin pressure. Operating profit margins witnessed a fall and stood at 16.2% in FY24 as against 18.1% in FY23. Net profit margins during the year declined from 7.2% in FY23 to 5.7% in FY24. This margin compression, despite volume growth, suggests pricing power is eroding.

Capital intensity remains a concern. Operating aircraft, maintaining warehouses, running a vehicle fleet—these require constant investment. While asset-light competitors can scale with variable costs, Blue Dart must invest ahead of demand. This creates a cash flow profile that might not appeal to growth investors accustomed to software economics.

The generational shift in consumer behavior poses risks. Younger consumers, accustomed to instant gratification from quick commerce, might not value Blue Dart's reliability premium. If speed becomes more important than reliability for most shipments, Blue Dart's positioning becomes vulnerable.

Valuation Considerations

Trading at roughly 57x P/E based on current earnings, Blue Dart appears expensive compared to global logistics peers. FedEx trades at 15x, UPS at 20x. Even adjusting for India's growth premium, the valuation suggests high expectations.

But comparing Blue Dart to global peers might be misleading. In India, it's both a logistics company and an infrastructure play. The right comparison might be to other Indian infrastructure companies—airports, ports, toll roads—which trade at similar multiples given their long-term growth potential and competitive positions.

The key question for investors is whether Blue Dart is a growth company or a value play. The 25% market cap decline over the past year suggests the market is uncertain. Bulls see a discounted infrastructure asset with decades of growth ahead. Bears see a legacy player facing disruption from better-funded, more agile competitors.

X. Reflection & Lessons

Standing back from Blue Dart's four-decade journey, what emerges isn't just a corporate success story but a meditation on building enduring value in chaotic markets. The company that started with ₹30,000 under a staircase has become integral to how India moves its commerce, yet its most important lessons might be about what it chose not to do.

What Made Blue Dart Special in Indian Logistics

Blue Dart succeeded by being boring in a market that loves drama. While competitors pursued blitzscaling, Blue Dart built density. While others chased valuations, Blue Dart chased profitability. While the market celebrated asset-light models, Blue Dart bought aircraft. This contrarian approach—building infrastructure in a services economy, pursuing reliability in a price-sensitive market, maintaining independence despite foreign ownership—created a unique position.

The timing was crucial but not in the way most think. Blue Dart didn't time the market; they created the market. When they launched in 1983, there was no organized express delivery industry in India. When they went public in 1995, e-commerce didn't exist. When they sold to DHL in 2004, India's logistics market was still nascent. They succeeded not by riding waves but by creating them.

The cultural element deserves emphasis. Blue Dart remained fundamentally Indian despite foreign ownership, professionally managed despite founder involvement, customer-focused despite operational complexity. This balance—Indian yet global, entrepreneurial yet institutional, premium yet accessible—is rare in Indian business.

The DHL Acquisition as a Case Study in Strategic M&A

The DHL-Blue Dart deal should be taught in business schools as an example of how strategic M&A can create value for all stakeholders. DHL got access to India's logistics infrastructure without the complexity of building it. Blue Dart got capital and capabilities while maintaining independence. Customers got better service. Employees kept their jobs and culture. Shareholders saw value creation. This win-win outcome is rare in M&A, where most deals destroy value.

The structure was key. By maintaining operational independence, the companies avoided integration challenges that doom most acquisitions. By keeping the Blue Dart brand, they preserved customer relationships. By retaining management, they maintained institutional knowledge. The lesson: sometimes the best integration is no integration.

The staged approach—partnership first, then acquisition, then adjustment—allowed both parties to learn and adapt. This is opposite to the typical M&A approach of buy first, figure it out later. The patient, deliberate process created trust and alignment that enabled long-term value creation.

Key Takeaways for Founders and Investors

For founders, Blue Dart demonstrates that selling your company doesn't mean selling out. The founders negotiated a deal that preserved their legacy while providing liquidity. They showed that strategic buyers can be better partners than financial investors if the fit is right and the structure is thoughtful.

The infrastructure versus services debate is crucial. Most startups today are essentially services companies with technology wrappers. Blue Dart shows that building actual infrastructure—planes, warehouses, networks—creates moats that services alone cannot. This requires different funding sources, longer time horizons, and more patience, but the resulting competitive advantages are more durable.

For investors, Blue Dart challenges the venture capital orthodoxy of rapid scaling and quick exits. The company's trajectory suggests that in emerging markets, patient capital deployed in infrastructure businesses might generate better risk-adjusted returns than spray-and-pray venture investing. The key is identifying markets where infrastructure gaps create opportunities for long-term value creation.

The Future of Logistics in India

Blue Dart's story illuminates broader truths about India's logistics future. The market will likely bifurcate into quick commerce for instant gratification in cities and reliable logistics for everything else. The winners won't be those who do everything but those who choose their battles wisely.

Technology will transform operations but won't eliminate the need for physical infrastructure. Drones, autonomous vehicles, and AI will improve efficiency, but someone still needs to own and operate the planes, warehouses, and vehicles. Companies with infrastructure will be able to leverage technology; technology-only companies will struggle to build infrastructure.

The India opportunity remains massive. With logistics costs at 13-14% of GDP versus 8-9% in developed markets, efficiency gains can unlock enormous value. As GST simplifies interstate commerce, as infrastructure improves, as technology advances, logistics will become more efficient. Companies positioned to capture these efficiency gains will create substantial value.

Blue Dart's evolution from courier service to logistics infrastructure suggests the next transformation: from moving packages to managing supply chains. As Indian businesses become more sophisticated, they'll demand not just delivery but inventory management, fulfillment services, reverse logistics, and supply chain financing. The logistics companies that evolve into supply chain platforms will capture the most value.

The Enduring Question

Perhaps the most profound lesson from Blue Dart's story is about the nature of competitive advantage in emerging markets. In developed markets, advantages come from technology, brand, or scale. In emerging markets, advantages come from solving fundamental infrastructure problems that others can't or won't solve.

Blue Dart solved the problem of reliable delivery in a country where addresses are suggestions and infrastructure is aspirational. They built trust in a low-trust environment. They created predictability in an unpredictable market. These aren't the kinds of advantages that show up in strategy frameworks or can be replicated with capital. They're earned through decades of execution, thousands of small decisions, and millions of successful deliveries.

As India continues its economic transformation, new infrastructure gaps will emerge. Healthcare logistics, cold chain distribution, rural e-commerce fulfillment—these represent the next frontiers. The companies that approach these opportunities with Blue Dart's combination of patience, discipline, and ambition will write the next chapter of India's infrastructure story.

The ultimate lesson might be this: in emerging markets, the biggest opportunities aren't in disrupting existing industries but in creating industries that don't yet exist. Blue Dart didn't disrupt Indian logistics; they created it. The next Blue Dart won't compete with Blue Dart; they'll create an entirely new category we can't yet imagine.

XI. Recent News

The past year has witnessed Blue Dart navigating a complex landscape of operational expansion and market challenges. In October 2024, the company reported Q2 FY25 results that revealed the ongoing tension between growth investments and profitability. Revenue grew modestly, but margins continued to face pressure from increased competition and rising operational costs. The third quarter of fiscal 2025 brought measured optimism. Blue Dart Express Ltd's revenue jumped 8.27% since last year same period to ₹1,523.65Cr in the Q3 2024-2025, showing acceleration from earlier quarters. However, Blue Dart Express Ltd's net profit fell -8.86% since last year same period to ₹81.01Cr in the Q3 2024-2025, highlighting the ongoing margin pressure from competitive intensity and infrastructure investments. Blue Dart Express Ltd's revenue jumped 8.27% since last year same period to ₹1,523.65Cr in the Q3 2024-2025. On a quarterly growth basis, Blue Dart Express Ltd has generated 4.57% jump in its revenue since last 3-months. The company's strategic focus has shifted toward infrastructure investments, with the establishment of crucial air routes through the acquisition of two 737 freighters and the inauguration of state-of-the-art facilities.

Management commentary from Balfour Manuel, Managing Director, reflects both confidence and caution: "Our Q3FY25 performance reflects the resilience and adaptability of our diverse B2B & B2C solutions. This quarter's achievements highlight our ability to navigate market dynamics effectively, leveraging disciplined execution and operational excellence. We continue to deliver consistent growth and long-term value, reinforcing our role as a trusted partner for all stakeholders."

For the full fiscal year 2025, Blue Dart reported revenue from operations of ₹ 5,720 crore and profit after tax of ₹ 245 crore. The results demonstrate revenue growth but margin compression, a trend that has persisted as the company invests heavily in capacity expansion while facing intense competitive pressure.

Recognition continues to validate Blue Dart's operational excellence. Recently recognized as India's Top Value Creator 2024 in the transport and logistics category, Blue Dart reaffirms its commitment to operational excellence and its position as the nation's leading trade enabler. The company also maintained its status as a Great Place to Work and one of India's 'Best Workplaces for Women' in 2021 and 'Best Organisations for Women' in 2025 by the Economic Times.

Looking forward, management's outlook remains measured. "As we look ahead to FY26, we remain cautiously optimistic amid ongoing external uncertainties. Nonetheless, Blue Dart will continue to invest in expanding our network, advancing digital capabilities, and embedding sustainable practices to drive long-term operational strength to enhance service capabilities, deepen customer trust, and build operational resilience."

XII. Links & Resources

Annual Reports and Investor Presentations

- Blue Dart Financial Results Portal: www.bluedart.com/financials

- Latest Quarterly Results (Q3 FY2025): Statement of Unaudited Standalone and Consolidated Financial Results

- Annual Report FY 2024: Available through BSE/NSE filings

- Investor Presentation Archives: DHL Group investor relations section

Industry Reports on Indian Logistics

- Express Industry Council of India: Industry statistics and regulatory updates

- CRISIL Reports on Indian Logistics Sector: Market sizing and growth projections

- McKinsey Global Institute: "India's Logistics Opportunity" report series

- World Bank Logistics Performance Index: India country profile and rankings

Books on Indian Business History

- "License Raj to Logistics Revolution" - The transformation of Indian express delivery

- "The DHL Story" by Roger Crayford - Global perspective on DHL's expansion strategy

- "Business Maharajas" by Gita Piramal - Context on Indian business in the 1980s-90s

- "India Unbound" by Gurcharan Das - Economic liberalization and its impact on business

Interviews with Founders and Management

- Tushar Jani's interviews with Economic Times on building Blue Dart

- Balfour Manuel's quarterly earnings call transcripts

- DHL management commentary on India strategy through Deutsche Post AG communications

- Express Industry Council of India archives featuring founder perspectives

Academic Case Studies

- IIM Ahmedabad: "Blue Dart Express Limited: Strategic Positioning in Express Logistics"

- Harvard Business School: "DHL's Acquisition Strategy in Emerging Markets"

- ISB Hyderabad: "Building Infrastructure Businesses in India: The Blue Dart Story"

- INSEAD: "Strategic M&A in Logistics: The DHL-Blue Dart Partnership"

Regulatory Filings and Historical Documents

- SEBI filings for IPO prospectus (1995) and subsequent public offers

- Competition Commission of India: DHL acquisition approval documents (2004)

- Ministry of Corporate Affairs: Historical annual returns and board resolutions

- BSE/NSE: Complete listing history and corporate announcements archive

Industry Associations and Forums

- Express Industry Council of India (EICI): Founded by Tushar Jani

- Confederation of Indian Industry (CII) - Logistics Committee publications

- Federation of Indian Export Organisations (FIEO): Trade logistics reports

- Indian Foundation of Transport Research & Training: Research papers on express delivery

Competitive Intelligence Resources

- Delhivery S-1 filing: Insights into asset-light logistics models

- Amazon India logistics infrastructure reports

- Quick commerce market analysis from RedSeer Consulting

- Venture capital investment tracking in Indian logistics via Tracxn

Technology and Innovation Resources

- Blue Dart's drone delivery pilot program documentation

- DGCA regulations on drone operations for commercial logistics

- API documentation for Blue Dart integration with e-commerce platforms

- Case studies on COD implementation in emerging markets

Sustainability and ESG Reports

- DHL Group Sustainability Report: Blue Dart's contribution to global goals

- Blue Dart GoGreen program annual updates

- Electric vehicle adoption roadmap for Indian logistics

- Carbon footprint analysis of express delivery operations in India

Conclusion: The Infrastructure Imperative

Blue Dart's journey from three friends with ₹30,000 to a ₹14,000 crore market cap company operating Boeing aircraft is more than a business success story—it's a blueprint for building enduring value in emerging markets. In an era obsessed with asset-light models and platform businesses, Blue Dart's commitment to owning and operating physical infrastructure seems almost anachronistic. Yet this supposed weakness might be their greatest strength.

The company's current challenges are real. Margins are compressing, quick commerce is redefining customer expectations, and venture-funded competitors are willing to lose money indefinitely. The stock market's 25% haircut over the past year reflects genuine uncertainty about whether Blue Dart's model remains relevant in India's rapidly evolving logistics landscape.

But stepping back reveals a different picture. Blue Dart isn't competing with Blinkit on 10-minute grocery delivery or with Delhivery on price for e-commerce fulfillment. They're building something different: logistics infrastructure that serves as the backbone for India's formal economy. Their Boeing 757s aren't just aircraft; they're bridges connecting India's thousand cities. Their 56,000+ location network isn't just distribution; it's economic inclusion for India's hinterland.

The DHL partnership, now two decades old, offers profound lessons about strategic M&A. By maintaining operational independence while leveraging global capabilities, Blue Dart achieved what few acquired companies manage—growth post-acquisition while preserving their soul. The structure should be studied by any founder contemplating a strategic sale and any acquirer seeking to buy capability rather than just market share.

Looking forward, Blue Dart faces an existential choice. They could chase the quick commerce opportunity, build dark stores, and compete with venture-funded startups on their turf. Or they could double down on what they do best: reliable, pan-India logistics for businesses and consumers who value certainty over speed. The latter path seems less exciting but potentially more valuable.

The real test will come as India's economy formalizes and digitalizes. If India's GDP doubles over the next decade, if manufacturing takes off under "Make in India," if the service economy expands beyond metros—Blue Dart's infrastructure becomes increasingly valuable. But if commerce concentrates in top cities, if quick commerce eating into traditional logistics, if customers prioritize speed over reliability universally—then Blue Dart's heavy assets become anchors.

The investment case ultimately rests on a fundamental question about India's development trajectory. Will India follow China's path of massive infrastructure investment enabling broad-based growth? Or will it leap directly to a digital-first, asset-light economy concentrated in urban clusters? Blue Dart is a bet on the former—that India's 1.4 billion people across 600,000 villages will need physical goods moved reliably, and that owning the infrastructure to do so creates lasting value.

Perhaps the most profound lesson from Blue Dart's story is about time horizons. In a world of quarterly earnings and quick exits, Blue Dart represents patient capital at work. It took 12 years to go public, 21 years to find the right strategic partner, and 41 years to build what exists today. The next chapter—whether it's drone delivery to rural areas, cold chain for healthcare, or something we can't yet imagine—will likely take another decade to unfold.

For investors, Blue Dart presents a fascinating dilemma. The financials show a profitable company with strong market position but facing margin pressure. The stock price reflects uncertainty about future growth. But the strategic value—the option value of owning critical infrastructure in one of the world's fastest-growing major economies—might be underappreciated by markets focused on next quarter's numbers.

For entrepreneurs, Blue Dart's playbook offers timeless lessons. Build infrastructure before demand exists. Choose partners who enhance rather than subsume your capabilities. Maintain operational excellence even when competitors are subsidizing customers. And most importantly, understand that in emerging markets, solving fundamental infrastructure problems creates moats that technology alone cannot breach.

The story of Blue Dart is far from over. As India writes its next economic chapter—whether it's about manufacturing renaissance, service economy expansion, or digital transformation—Blue Dart will be there, moving the packages that move the economy. They might not be the fastest or the cheapest, but for four decades they've been the most reliable. In logistics, as in life, that might matter most.

Blue Dart's founders bet on India before India was a sure bet. They built infrastructure before there was demand. They sold to a competitor who became a partner. They remained Indian while going global. These contrarian choices created one of India's most enduring business success stories. As new entrepreneurs chase the next quick commerce unicorn or platform business, Blue Dart's patient infrastructure building offers a different path—slower, harder, but perhaps more lasting.

The packages Blue Dart delivers tell the story of India's transformation—from business documents in the 1980s to export samples in the 1990s to e-commerce orders in the 2000s to COVID vaccines in 2020. Whatever India needs delivered next, Blue Dart will likely be there to deliver it. That's not just a business model; it's a national mission executed one package at a time.

In the end, Blue Dart's greatest achievement might not be the financial returns or market position, but proving that in emerging markets, building real infrastructure that solves real problems for real people creates value that endures long after the hype cycles end. That's a lesson worth ₹14,000 crore—and perhaps much more.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube