Aditya Birla Money: The Transformation of India's Capital Markets Pioneer

I. Introduction & Episode Preview

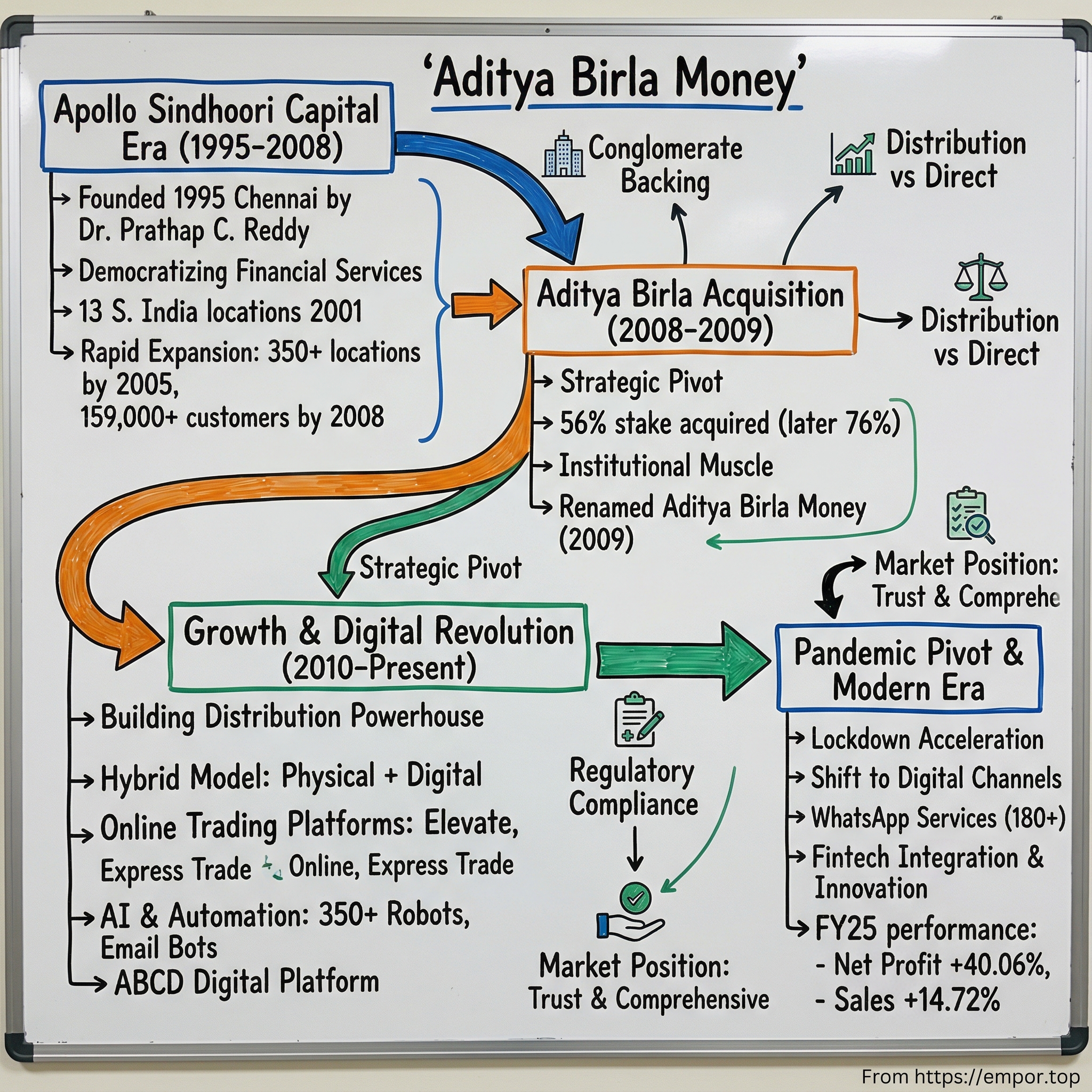

Picture this: A sweltering Chennai morning in 1995. Dr. Prathap C. Reddy, the legendary founder of Apollo Hospitals, sits across from his advisors discussing an audacious new venture. India's capital markets had just begun their liberalization journey four years prior, and the doctor who revolutionized Indian healthcare saw another opportunity—democratizing financial services for the emerging middle class. What started in that boardroom as Apollo Sindhoori Capital would, through a series of strategic pivots and one transformative acquisition, become Aditya Birla Money—a digital powerhouse managing over ₹1,000 crore in market capitalization today.

The central question that drives this narrative isn't just how a regional Chennai broker expanded nationally. It's how a company born in the pre-internet era of physical share certificates managed to reinvent itself—not once, but multiple times—to survive the rise of discount brokers, navigate a global financial crisis that became its greatest opportunity, and emerge as a digital-first platform in an industry where Zerodha and Groww seem to dominate headlines.

This is a story of three distinct eras: the Apollo years of geographic conquest, the Aditya Birla transformation that brought institutional muscle, and the digital revolution that forced a traditional broker to compete with venture-backed fintechs. Along the way, we'll explore how conglomerate backing can be both shield and sword, why distribution still matters in a direct-to-consumer world, and what happens when a 30-year-old financial services firm decides to act like a startup.

The numbers tell part of the story—from 13 South Indian locations in 2001 to over 350 nationally by 2005, from serving 185,000 customers post-acquisition to processing nearly double their digital volumes during the pandemic. But the real narrative lies in the decisions made in conference rooms and crisis meetings, the bets on technology when peers hesitated, and the delicate balance between leveraging group synergies and maintaining entrepreneurial agility.

What makes Aditya Birla Money particularly fascinating is its position at the intersection of old and new India. Unlike pure-play digital brokers that started with a blank canvas, this company carries the weight and wisdom of three decades while attempting to sprint alongside nimble competitors. It's a high-wire act that many legacy players have failed—yet somehow, as we'll see, this particular transformation story offers unexpected lessons about resilience, timing, and the enduring value of patient capital.

II. Origins & Apollo Sindhoori Era (1995–2008)

The monsoon had just broken over Chennai when Apollo Sindhoori Capital Investment Limited filed its incorporation papers on July 4, 1995. Dr. Prathap C. Reddy, fresh from building Apollo Hospitals into India's first corporate healthcare chain, saw parallels between healthcare and financial services—both were essential services dominated by government institutions, both were ripe for private sector disruption, and both required trust above all else.

The timing was prescient. India's capital markets were experiencing their first real boom post-liberalization. The Harshad Mehta scam of 1992 had paradoxically increased retail awareness about stock markets, even as it exposed regulatory gaps. SEBI had just gotten statutory powers in 1992. The National Stock Exchange, barely a year old, was beginning to challenge the century-old Bombay Stock Exchange with electronic trading. Into this chaos stepped Apollo Sindhoori, armed with the credibility of the Apollo brand and ambitious expansion plans. Operations commenced in 1996, with the company methodically establishing its presence throughout South India. The company was promoted by Prathap C Reddy, Chairman of Apollo Hospitals Group, who brought not just capital but a systematic approach to expansion learned from scaling healthcare operations. By 2001, Apollo Sindhoori had established 13 locations across Tamil Nadu, Karnataka, and Andhra Pradesh—a modest footprint that would explode exponentially over the next four years.

The period from 2001 to 2005 marked Apollo Sindhoori's great geographic leap. The company added locations at a breathtaking pace—from 13 in 2001 to over 350 by 2005. During 2005-06, the company added 120 new offices and the client base rose to 77,000 from around 45,000. This wasn't organic growth; it was systematic conquest. The strategy was deceptively simple: establish a presence in tier-2 and tier-3 cities before competitors arrived, leverage the Apollo brand's trust factor, and build relationships with local sub-brokers who brought their own client networks. During the year 2004-05, the company added 106 new offices all over the country. The expansion wasn't just about numbers—it was about timing. The Indian economy was growing at 7-8% annually, the middle class was expanding, and retail participation in equity markets was surging post the tech boom and bust cycle. Apollo Sindhoori's subsidiary, Apollo Sindhoori Commodities Trading Ltd, was simultaneously expanding to 100 locations, capitalizing on the commodities trading boom that followed the introduction of futures trading in gold and silver on MCX in 2003.

During 2005-06, the company added 120 new offices and the client base rose to 77,000 from around 45,000. By 2006-07, they added 71 sub-broker offices and 51 branches, with the customer count increasing by 22,780. The 2007-08 period saw the most aggressive expansion yet—237 offices added, with the client base reaching over 159,000, a 49% growth from 107,000 the previous year. The total office count rose from 561 to 798, with own branches growing from 168 to 197.

This breakneck expansion had a method to its madness. Unlike pure online brokers that would emerge later, Apollo Sindhoori understood that Indian retail investors in the mid-2000s needed hand-holding. They wanted to see a physical office, meet a relationship manager face-to-face, and have someone explain complex financial products in their local language. The company's systematic gold saving scheme, launched through its commodities subsidiary, exemplified this approach—making gold investment accessible through systematic investment plans, initially in Tamil Nadu before expanding nationally.

The technology backbone supporting this expansion was crucial but unglamorous. While the front-end remained relationship-driven, the back-end was being systematically digitized. Trading terminals, risk management systems, and settlement processes were being automated even as the company maintained its high-touch service model. This dual approach—digital infrastructure with human interface—would prove prescient when the financial crisis hit and the company needed both operational efficiency and customer trust to navigate the storm ahead.

III. The Aditya Birla Acquisition: A Pivotal Inflection Point (2008–2009)

August 28, 2008. Lehman Brothers was two weeks away from collapse. Global credit markets were freezing. In Mumbai, executives at Aditya Birla Nuvo Limited were signing papers to acquire 56% of Apollo Sindhoori Capital Investments for an undisclosed sum. The timing seemed either incredibly brave or foolishly reckless. As it turned out, it was a masterclass in contrarian investing.

The context matters enormously here. The Indian financial services sector was experiencing tectonic shifts. Consolidation was inevitable—standalone brokers were struggling with rising compliance costs, technology investments, and margin pressure from discount brokers. The global financial crisis, rather than being purely destructive, was creating once-in-a-decade acquisition opportunities for well-capitalized players. Kumar Mangalam Birla, chairman of the Aditya Birla Group, saw financial services as the next frontier for the conglomerate that had built its fortune in commodities, textiles, and telecom. The acquisition valued Apollo Sindhoori at Rs 355 crore, with Aditya Birla Nuvo paying Rs 198.81 crore for the 56% stake. Apollo Sindhoori had reported a topline of Rs 120 crore and a net profit of Rs 22 crore in 2007-08. For a company with over 190 own and 570 franchisee branches and 150,000 customers, this represented a reasonable valuation multiple—approximately 16x earnings—especially considering the market turmoil.

The mechanics of the acquisition were textbook Indian M&A. On August 28, 2008, the company entered into a Share Purchase Agreement with Aditya Birla Nuvo Ltd for sale of 56% equity shares. Pursuant to this agreement, Aditya Birla Nuvo Ltd made an open offer for purchase of 20% equity shares of the company, which was completed on February 24, 2009. By March 2009, the group had acquired 76% of the company. The company officially became a subsidiary of Aditya Birla Nuvo Limited on March 6, 2009.

Ajay Srinivasan, then chief executive of financial services at Aditya Birla Group, articulated the strategic rationale: "The strategic intent of this agreement is to position Aditya Birla Financial Services Group as a broad based and integrated player in the financial services business. We already have a strong presence across financial services verticals, including life insurance, fund management, distribution and wealth management, security-based lending, insurance broking and private equity."

The integration began immediately. During 2008-09, the company added 43 new branches including 18 offices placed in the premises of Birla Sun Life Distribution Ltd. This wasn't just co-location—it was the beginning of a cross-selling strategy that would define the next decade. Customers walking into a Birla Sun Life office for insurance could now open trading accounts. Apollo Sindhoori's broking customers could be introduced to mutual funds and insurance products.

The name change came swiftly. The company changed its name from Apollo Sindhoori Capital Investments Ltd to Aditya Birla Money Ltd with effect from August 3, 2009. This wasn't mere rebranding—it signaled complete integration into the Aditya Birla Financial Services ecosystem. The Apollo Hospitals Group retained a 10% stake, with Suneeta Reddy explaining they believed in the value creation potential under Aditya Birla's stewardship.

Post-acquisition, the focus shifted immediately to three areas: process improvement, new product introduction, and cost rationalization. The company was serving 1,85,000 customers through over 800 own and sub-broker branches, but efficiency metrics lagged industry leaders. Technology systems needed upgrading, compliance processes required standardization, and the product suite needed expansion beyond vanilla broking.

The financial crisis, rather than hampering integration, actually accelerated it. Competitors were retrenching, talent was available, and customers were seeking stability—exactly what the Aditya Birla brand provided. The acquisition transformed a regional broker with national presence into a diversified financial services platform with institutional backing, setting the stage for the next phase of growth.

IV. Building the Distribution Powerhouse (2010–2015)

February 23, 2010 marked a subtle but significant shift in Aditya Birla Money's corporate structure. Aditya Birla Nuvo Limited transferred its shareholding in the Company to Aditya Birla Financial Services Private Limited (ABFSPL) by way of 'inter-se' promoter transfer. This wasn't just paperwork—it was strategic positioning. The company was being moved under the dedicated financial services umbrella, signaling the group's intent to build a comprehensive financial services powerhouse.

The 2010-2015 period was characterized by relentless distribution expansion and product diversification. While pure-play online brokers like Zerodha (founded in 2010) were betting on technology and low costs, Aditya Birla Money doubled down on its hybrid model—physical presence backed by digital capabilities. The logic was compelling: India's financial services penetration remained abysmal, with less than 2% of the population investing in equities. The opportunity wasn't just in serving existing investors better but in creating new investors. The expansion strategy focused on building complementary capabilities. Equity and derivative trading through NSE and BSE formed the core, but the company systematically added currency derivatives on MCX-SX, commodities trading through MCX and NCDEX, and depository participant services for both NSDL and CDSL. Each addition wasn't just about revenue diversification—it was about becoming the one-stop shop for retail investors' entire portfolio needs.

The sub-broker model proved particularly effective. Rather than competing with local brokers, Aditya Birla Money partnered with them, providing technology, training, and brand support while they brought local relationships and trust. This franchisee model allowed rapid expansion without proportional capital investment. By 2012, the company was operating through a combination of own branches and a vast network of sub-brokers, creating a distribution footprint that pure online players couldn't match.

Recognition came in the form of awards—notably the Best Performing National Financial Advisors award at CNBC TV 18 Financial Advisor Awards. But more importantly, the company was building synergies within the Aditya Birla ecosystem. Birla Sun Life Insurance customers were being cross-sold broking accounts. Mutual fund investors were being introduced to direct equity. The holy grail of financial services—the integrated customer relationship—was beginning to take shape.

The period also saw important corporate restructuring. The Aditya Birla Group was consolidating its financial services businesses, creating clearer reporting lines and operational synergies. The message to the market was clear: financial services wasn't a side bet for the conglomerate but a core growth pillar alongside cement, metals, and textiles.

What's remarkable about this period is what didn't happen. While competitors were slashing brokerage rates in a race to the bottom, Aditya Birla Money maintained its focus on service quality and relationship management. The company understood that in a market where financial literacy remained low, the value wasn't just in execution but in advice, hand-holding, and trust. This positioning would prove prescient as the market evolved toward fee-based advisory models.

V. Digital Revolution & Platform Transformation (2015–2020)

The year 2017 brought another corporate restructuring that signaled the growing importance of financial services within the Aditya Birla empire. Aditya Birla Nuvo Limited (ABNL) was amalgamated with Grasim Industries Limited through a Composite Scheme of Arrangement, and consequently, the Company's ultimate holding company changed from ABNL to Grasim Industries Limited effective July 1, 2017. This wasn't mere corporate shuffling—it placed financial services at the heart of one of India's most valuable companies.

But the real transformation was happening at the operational level. The Aditya Birla Group had initiated a comprehensive digitization strategy in 2017, integrating data analytics, AI, and robotics across businesses. For Aditya Birla Money, this meant a fundamental reimagining of the customer experience. The traditional broker-client relationship, built on phone calls and branch visits, needed to evolve into an omnichannel experience that could compete with digital-first players.2018 marked two significant milestones. First, the company launched its Wholesale Debt business, targeting institutional clients and high-net-worth individuals. This wasn't just product expansion—it was a strategic move up the value chain, from pure execution to advisory. Second, and more transformatively, Aditya Birla Commodities Broking Limited, a wholly owned subsidiary, was amalgamated with the company effective December 14, 2018. This consolidation streamlined operations and created a unified platform for all trading products.

The digital transformation accelerated dramatically. The company developed multiple platforms—the Elevate app for premium customers, Elevate web for desktop traders, Express Trade for quick transactions, and a comprehensive Mutual Funds Platform. Each platform targeted specific customer segments with tailored interfaces and features. The underlying architecture, however, was unified, allowing seamless data flow and cross-selling opportunities.

What set Aditya Birla Money's digital strategy apart was its focus on the ecosystem play. Rather than viewing itself as a standalone broker, the company positioned itself as the trading and investment arm of Aditya Birla Capital's comprehensive financial services platform. On-boarded 90% of the customers digitally across all the businesses and implemented digital service journeys on multiple digital platforms, including the Web, WhatsApp, chatbots and voice bots.

The integration of AI and machine learning wasn't just buzzword compliance—it had real operational impact. Over 350 robots perform live activities across Aditya Birla Capital's businesses in multiple functions, including operations, customer service, finance and human resources. Email bots have been handling over 200,000 emails every quarter, driving high operational efficiencies across businesses. Turnaround time cut down by 80% due to the implementation of an OCR (online character recognition) mechanism for auto-extraction of data from various sources.

By 2019, the company was operating in a fundamentally different way than it had just five years earlier. Physical branches remained important, but they had transformed from transaction centers to advisory hubs. The heavy lifting of order execution, settlement, and basic customer service had moved online. The human element focused on complex queries, relationship management, and financial planning—activities where personal touch still mattered.

The stage was set for what no one could have predicted—a global pandemic that would accelerate digital adoption by a decade in just a few months.

VI. Pandemic Pivot & Digital Acceleration (2020–2022)

March 24, 2020. India announced one of the world's strictest lockdowns. Markets crashed, branches shuttered, and suddenly a business model built on physical presence seemed obsolete. For Aditya Birla Money, this could have been catastrophic. Instead, it became their finest hour.

The company's digital investments of the previous three years suddenly paid dividends in ways no one had imagined. While competitors scrambled to enable work-from-home capabilities, Aditya Birla Money's cloud-based infrastructure allowed seamless transition to remote operations. Over 87% customer applications are on public and private cloud, enabling a better up-time—a prescient move that proved invaluable when physical infrastructure became inaccessible.

The numbers tell a remarkable story. Between April and June 2020, the company processed nearly twice the volume through digital channels compared to the same period in 2019. This wasn't just existing customers moving online—new customer acquisition shifted almost entirely digital. The onboarding process, which traditionally required branch visits and physical documentation, was reimagined as a completely digital journey using video KYC and e-signatures. But the real innovation came through WhatsApp. The company built comprehensive WhatsApp channels with over 180 services across products. Customers could check their portfolio, place orders, get research reports, and even complete mutual fund transactions—all through WhatsApp. With over 4 million customer interactions on digital and social media platforms, including WhatsApp, own websites, apps and chatbots, ABCL companies recorded nearly twice as much volume through digital channels between April and June 2020 as compared to the same period last year.

The WhatsApp strategy was particularly brilliant because it met customers where they already were. Rather than forcing app downloads or website visits, Aditya Birla Money brought financial services to the messaging platform Indians used dozens of times daily. ABCL even launched several industry-first initiatives like change of address requests in the stockbroking business on its web portal through video-based interaction, renewal of health insurance policies through WhatsApp and registering mutual fund SIPs on WhatsApp.

The pandemic also accelerated the shift in customer demographics. Younger investors, many experiencing their first market correction, flocked to equity markets attracted by the sharp recovery from March 2020 lows. These digital natives had different expectations—they wanted instant account opening, real-time analytics, educational content, and social features. The company's platforms evolved rapidly to meet these needs.

Employee transformation was equally dramatic. 100% of the learning interventions at Aditya Birla Capital have been delivered virtually over the past few years. Over 90% of the workforce is undergoing learning through digital mediums. A consistent focus on enabling the workforce to become future-ready through exposure to AI, ML, cloud computing and robotic process automation learning.

The operational metrics from this period are staggering. Self-service actions by customers shot up 65 per cent in April 2020 against the FY20 average, while digital reach increased over four times in April 2020 as compared to the FY20 average. A staggering 92 per cent of policy renewals in the health insurance business were achieved through digital channels during April 2020, compared to a 58 per cent average during FY20.

What's remarkable is how the company maintained service quality despite the operational upheaval. Claims processing continued uninterrupted, settlements happened on schedule, and customer complaints actually decreased—a testament to the robustness of the digital infrastructure. The crisis had forced a decade of digital transformation into a few months, and somehow, it had worked.

By the end of 2021, as India emerged from successive COVID waves, Aditya Birla Money was a fundamentally different company. The branch network remained, but its role had evolved from transaction processing to advisory and complex problem-solving. Digital wasn't an add-on channel—it was the primary interface for most customers. The pandemic, rather than being a setback, had accelerated the company's evolution into a digital-first financial services platform.

VII. Modern Era: Fintech Integration & Innovation (2023–Present)

The post-pandemic world presented a new challenge: how to compete when every broker had gone digital. The moats that once protected traditional brokers—branch networks, brand trust, regulatory compliance—had been eroded by venture-funded fintechs offering zero brokerage and slick mobile apps. Aditya Birla Money's response was to stop trying to beat fintechs at their own game and instead become the platform that integrated them.

2023 marked a strategic pivot with the launch of the Financial Product Distribution Channel. Rather than viewing fintechs as competitors, the company began partnering with them, offering their innovative solutions through Aditya Birla Money's distribution network. This wasn't capitulation—it was recognition that the future of financial services would be ecosystem-based rather than product-based. By 2024, the company had launched access to advisory services from multiple Fintechs, creating a curated marketplace of financial solutions. This was a fundamental shift in business model—from being a product manufacturer to becoming a distribution platform that happened to manufacture some products. The distinction is crucial: it acknowledged that customers didn't want a broking relationship or a mutual fund relationship—they wanted their financial lives simplified.

The numbers from FY25 tell a story of successful transformation. The Profit after Tax stood at Rs 74.19 Crore for the year ended 31st March 2025, as compared to Rs 52.97 Crore in Previous Financial Year, an increase of 40%. The company opened 66 new branches in FY25, driving customer growth—but these weren't the transaction-processing centers of old. They were advisory hubs, relationship centers, and onboarding points for complex products that still required human explanation.

The full year FY25 performance was impressive: Net profit rose 40.06%, sales rose 14.72% to Rs 447.61 crore. With a market cap of Rs 1005.98 Crore as of September 2025, the company had not just survived the fintech onslaught—it had found its niche in the new ecosystem.

The integration with Aditya Birla Capital's broader ecosystem reached new levels of sophistication. The ABCD (Aditya Birla Capital Digital) platform, launched in 2024, offers a comprehensive portfolio of more than 25 products and services such as payments, loans, insurance, and investments. It helps customers to fulfil their financial needs and serves as an acquisition engine for the Company. The platform has witnessed a strong response with about 5.5 million customer acquisitions till date.

The modern Aditya Birla Money operates on three levels. At the base, it provides commoditized services—trading, demat accounts, mutual fund transactions—at competitive prices through digital channels. The middle layer offers curated solutions and advisory services, leveraging both proprietary products and third-party fintech partnerships. At the top, it provides comprehensive wealth management for high-net-worth individuals, where relationships and trust still command premium pricing.

Competition remains intense. Zerodha, with its zero-brokerage model and minimalist approach, dominates retail trading volumes. Groww has captured the millennial mutual fund investor. PayTm Money and other super-apps are bundling financial services with payments and commerce. Yet Aditya Birla Money has found its positioning—not as the cheapest or the most innovative, but as the most comprehensive and trustworthy platform for serious long-term wealth creation.

The company's approach to AI and automation in this period has been pragmatic rather than revolutionary. SimpliFi, their AI-powered financial assistant embedded in the ABCD app, provides personalized recommendations based on customer behavior and market conditions. The company can now dynamically scale to handle heavy workloads and further increase concurrency with Azure Kubernetes Service (AKS), significantly reducing development cycles.

What's particularly interesting about the modern era is the company's approach to regulation. While fintechs often operate in regulatory grey areas, pushing boundaries until regulators catch up, Aditya Birla Money has positioned itself as the compliant alternative. In an environment where SEBI has been increasingly aggressive about protecting retail investors, this conservative approach has become a competitive advantage.

VIII. Playbook: Strategic Lessons & Business Model Evolution

The transformation from Apollo Sindhoori to modern Aditya Birla Money offers a masterclass in corporate evolution. The playbook that emerges isn't about any single brilliant strategy but rather a series of pragmatic adaptations to changing market realities.

From Regional Broker to National Platform

The geographic expansion strategy of the early 2000s seems quaint in today's digital world, yet it laid crucial foundations. By establishing physical presence in 350+ locations before competitors arrived, Apollo Sindhoori built relationships and trust that couldn't be easily replicated by online-only players. These weren't just branches—they were beachheads in local markets, each bringing its own network of sub-brokers, high-net-worth families, and corporate relationships.

The brilliance was in the sequencing. Start in South India where the Apollo brand had maximum resonance. Build density in each state before moving to the next. Partner with local sub-brokers rather than competing with them. By the time of the Aditya Birla acquisition, the company had a distribution network that would have taken a new entrant decades to build organically.

The Power of Conglomerate Backing

The Aditya Birla acquisition could have been a disaster—many such deals are. Large conglomerates often smother entrepreneurial companies with bureaucracy and corporate politics. Instead, the acquisition became a catalyst for transformation. The key was in how the integration was managed.

Rather than imposing a top-down restructuring, Aditya Birla Group provided three things: capital for technology investment, brand credibility for customer acquisition, and most importantly, access to a captive customer base across insurance, mutual funds, and banking relationships. The cross-selling opportunity wasn't forced—it evolved naturally as systems integrated and teams collaborated.

The financial backing also provided staying power during the brokerage price war of the 2010s. While standalone brokers had to choose between profitability and growth, Aditya Birla Money could afford to maintain service quality while competitors slashed costs. This patient capital approach—accepting lower returns today for strategic positioning tomorrow—is a luxury few companies enjoy.

Digital Transformation as Survival Mechanism

The digital transformation story is often told as visionary leadership embracing technology. The reality was more pragmatic—it was embrace digital or die. What distinguished Aditya Birla Money was the execution. While competitors either went fully digital (abandoning existing customers) or remained stubbornly physical (losing new customers), the company managed a delicate balance.

The key insight was that different customer segments needed different service models. Young traders wanted mobile apps and zero-touch experiences. Wealthy retirees wanted relationship managers and branch visits. SME owners wanted a combination—digital for routine transactions, human for complex decisions. Building this multi-channel architecture was expensive and complex, but it prevented customer churn during the transition.

Distribution vs. Direct Model Balance

The evolution from manufacturer to platform represents perhaps the most important strategic shift. Traditional brokers saw fintechs as existential threats. Aditya Birla Money saw them as potential partners. By 2024, the company was distributing products from multiple fintechs through its channels while also offering its own products through fintech platforms.

This required significant humility—acknowledging that the company couldn't be best at everything. It also required sophisticated technology to integrate multiple providers seamlessly. But the payoff was significant: customers got best-in-class products regardless of manufacturer, and Aditya Birla Money captured value through distribution fees, advisory charges, and platform revenues.

Managing Regulatory Changes

Indian financial services regulation has been in constant flux—from the introduction of GST to changes in margin requirements to restrictions on F&O trading. Each change created winners and losers. Aditya Birla Money's approach was to over-invest in compliance infrastructure, maintaining dedicated teams to interpret and implement regulatory changes quickly.

This conservative approach had costs—some profitable but questionable practices had to be abandoned, some innovative products couldn't be launched. But it also had benefits. Regulators began to see the company as a responsible player, often consulting them on proposed changes. Customers, particularly institutional ones, valued the certainty that their broker wouldn't be suspended for regulatory violations.

Capital Allocation and Profitability Focus

The historical ROE performance tells its own story: highest 125.09%, lowest 10%, median 40.25% over 13 years. This volatility reflects the challenges of the broking business—highly cyclical, capital intensive during growth phases, and vulnerable to market downturns. The current ROE of 26.05% as of September 2025 represents a more sustainable equilibrium.

The capital allocation strategy evolved significantly post-2015. Rather than pursuing growth at any cost, the focus shifted to profitable growth. Unprofitable branches were closed or converted to franchisees. Technology investments were evaluated on ROI rather than novelty. Customer acquisition costs were carefully monitored against lifetime value.

The result is a more resilient business model. Revenue streams are diversified across broking, distribution, advisory, and platform fees. The cost base is more variable, with technology handling routine tasks and humans focusing on high-value activities. The balance sheet is stronger, providing cushion for market downturns and capital for opportunistic investments.

IX. Analysis & Investment Thesis

The investment case for Aditya Birla Money requires nuance. This isn't a high-growth fintech story that will capture venture capital imagination. Nor is it a deep-value play trading at distressed multiples. It's something more complex—a transformation story where the future trajectory depends on execution of a delicate strategic balance.

The Bull Case

The optimistic view starts with India's dramatic under-penetration in financial services. With less than 3% of the population investing in equities and mutual fund penetration below 15%, the runway for growth appears endless. As India's per capita income crosses $3,000 and moves toward $5,000 over the next decade, financial services adoption typically accelerates exponentially.

Aditya Birla Money is uniquely positioned to capture this growth. Unlike pure-play digital brokers that struggle with customer trust, the company combines digital convenience with institutional credibility. Unlike traditional brokers burdened by legacy infrastructure, it has successfully transformed its technology stack. The sweet spot positioning—not the cheapest but not the most expensive, not the most innovative but not outdated—appeals to the mass affluent segment that drives industry profitability.

The integration within Aditya Birla Capital's ecosystem provides sustainable competitive advantages. With 5.5 million customers acquired through the ABCD platform and access to millions more through insurance and mutual fund relationships, customer acquisition costs are structurally lower than standalone competitors. The ability to cross-sell multiple products increases lifetime value while reducing churn.

Digital transformation initiatives are beginning to show results. The 40% growth in PAT for FY25 wasn't just market beta—it reflected operational improvements, cost rationalization, and improved product mix. As AI and automation initiatives mature, operating leverage should improve further. The company's technology infrastructure, built over the past five years, can handle multiple times current volumes without proportional cost increases.

Regulatory tailwinds could provide additional support. SEBI's increasing focus on investor protection and market integrity favors established players with strong compliance infrastructure. Recent restrictions on F&O trading for retail investors might reduce volumes but improve quality of revenue. The push toward formalization of the economy benefits organized players at the expense of informal operators.

The Bear Case

The pessimistic view starts with brutal industry economics. Broking is increasingly commoditized, with prices racing toward zero. Zerodha has proven that a lean operation with minimal overhead can capture massive market share while charging almost nothing. In this environment, Aditya Birla Money's multi-channel model with physical branches and relationship managers looks anachronistic and expensive.

The company's market cap of Rs 1,006 crore seems modest, but in context of industry dynamics, it might be generous. Pure-play digital brokers are valued on growth and potential; traditional brokers on assets and earnings. Aditya Birla Money sits uncomfortably between these paradigms, making valuation challenging.

Competition is intensifying from unexpected directions. Banks are becoming more aggressive in capital markets, leveraging their deposit relationships. Payment companies are adding investment features, bundling them with their super-apps. Global giants like Interactive Brokers are entering India with sophisticated platforms and competitive pricing. Each new entrant further fragments an already competitive market.

Technology disruption remains a constant threat. The company's digital transformation, while impressive, is essentially catching up to where pure-digital players started. As artificial intelligence and blockchain reshape financial services, legacy players might struggle to adapt quickly enough. The next disruption might not be about digitizing existing processes but reimagining financial services entirely.

Margin pressure appears structural rather than cyclical. Brokerage rates have fallen 90% over the past decade and show no signs of stabilizing. Advisory fees are under pressure as robo-advisors and passive investing gain acceptance. Even distribution fees are being squeezed as manufacturers go direct to consumers. Finding new revenue streams while existing ones shrink is a challenging equation.

Comparison with Peers

Against pure-play digital brokers like Zerodha, Aditya Birla Money looks expensive and slow. Zerodha's operating margins above 50% make Aditya Birla Money's profitability seem pedestrian. The customer acquisition metrics are even more stark—Zerodha adds more customers in a quarter than Aditya Birla Money's entire base.

However, this comparison misses important nuances. Zerodha's customers are predominantly traders, generating volatile transaction-based revenues. Aditya Birla Money's customers include long-term investors, corporate clients, and high-net-worth individuals who provide more stable, fee-based revenues. The quality of revenue matters as much as quantity.

Against traditional brokers like ICICI Direct or HDFC Securities, Aditya Birla Money holds up better. It has successfully digitized while maintaining relationship-based services. The technology infrastructure is modern and scalable. The cost structure, while not as lean as pure-digital players, is more flexible than traditional full-service brokers.

The more relevant comparison might be with wealth management platforms like 360 One (formerly IIFL Wealth) or Nuvama (formerly Edelweiss). These companies are also navigating the transition from transaction-based to fee-based models, from product push to advisory pull. In this context, Aditya Birla Money's transformation looks more credible, though execution remains key.

Valuation Considerations

At current valuations, the market seems to be pricing Aditya Birla Money as a mature, slow-growth financial services company rather than a digital transformation story. The P/E multiple of approximately 15x (based on FY25 earnings) is below the industry average for both traditional brokers and fintech players.

This might represent opportunity or value trap depending on execution. If the company successfully transforms into a platform-based model with recurring fee revenues, multiple expansion is possible. If it remains stuck between digital and traditional, fighting on price while maintaining high costs, multiple compression is likely.

The ROE of 26% is respectable but not exceptional. For a capital-light platform business, this should be higher. For a capital-intensive traditional broker, it's quite good. Again, the trajectory matters more than the current position. If ROE trends toward 30%+ through operational leverage, the equity story improves significantly.

X. Future Outlook & Strategic Priorities

The next five years will determine whether Aditya Birla Money emerges as a winner in India's financial services transformation or becomes another casualty of digital disruption. The strategic priorities are clear, but execution will be challenging.

AI and Automation Initiatives

The company's AI journey has moved beyond experimentation to implementation. SimpliFi, the AI assistant, is evolving from a chatbot to a genuine financial advisor, capable of analyzing portfolios, suggesting rebalancing, and even predicting customer needs. The technology exists—the challenge is integration and adoption.

The next phase involves predictive analytics for customer behavior. Which customers are likely to churn? Who might be interested in margin trading? When should a relationship manager reach out versus letting digital channels handle the interaction? These micro-decisions, made millions of times daily, determine profitability in a low-margin business.

Automation of back-office processes continues to offer efficiency gains. The company has reduced turnaround time by 80% through OCR and workflow automation, but there's room for improvement. The goal is straight-through processing for 95% of transactions, with human intervention only for exceptions. This would dramatically reduce operational costs while improving customer experience.

Expanding into Wealth Management

The wealth management opportunity in India is enormous. The number of ultra-high-net-worth individuals is growing at 11% annually. The mass affluent segment—households with $50,000 to $500,000 in investable assets—is expanding even faster. This segment needs sophisticated advice but can't access traditional private banking.

Aditya Birla Money's strategy is to build a technology-enabled wealth management platform that can serve this segment profitably. This means robo-advisory for basic portfolio management, human advisors for complex planning, and access to exclusive products like alternative investments and structured products.

The challenge is talent acquisition and retention. Experienced wealth managers command high compensation and have portable client relationships. Building a sustainable wealth management business requires creating systematic processes and technology platforms that reduce dependence on star performers while maintaining service quality.

Cross-selling Within Ecosystem

The Aditya Birla Capital ecosystem includes insurance, mutual funds, housing finance, and SME lending. Each business has millions of customers who could benefit from other products. The theoretical cross-sell opportunity is enormous—the practical execution is complex.

The ABCD platform is the technical solution, providing single sign-on across products and unified customer view for relationship managers. But technology is only part of the answer. The bigger challenges are organizational—aligning incentives across businesses, sharing customer data while respecting privacy, and coordinating marketing without overwhelming customers.

Early results are promising. Customers acquired through the ABCD platform have 2.3x higher lifetime value than single-product customers. The key is patient execution—building trust before pushing products, understanding needs before offering solutions.

Regulatory Landscape

The regulatory environment will continue evolving, generally in directions that favor established players. SEBI's focus on investor protection means higher compliance costs but also barriers to entry for new players. The emphasis on transparency and disclosure plays to Aditya Birla Money's strengths in process and compliance.

Potential regulatory changes could be transformative. If India introduces tax-advantaged retirement accounts similar to America's 401(k), it could drive massive flows into capital markets. If cryptocurrency regulations provide clarity, it could open new business opportunities. If F&O restrictions reduce retail speculation, it could shift focus to long-term investing.

The company's strategy is to stay ahead of regulatory curves—implementing changes before they become mandatory, engaging with regulators on policy formation, and building flexibility into systems to adapt quickly. This proactive approach has costs but prevents the disruption and penalties that come from reactive compliance.

The Next Decade: Predictions and Scenarios

Scenario 1: The Platform Winner In the optimistic scenario, Aditya Birla Money successfully transforms into India's leading financial services platform. The ABCD ecosystem becomes the default choice for mass affluent Indians, offering everything from trading to insurance to loans through a unified interface. Revenue shifts from transaction-based to subscription and fee-based, providing predictable growth and higher multiples. The company becomes an acquisition target for global financial services giants looking for Indian exposure.

Scenario 2: The Steady Performer In the base case, the company continues its current trajectory—growing with the market, maintaining profitability, but never quite breaking out. It remains a solid tier-2 player, benefiting from India's financial services growth but not capturing disproportionate share. The stock delivers returns in line with the broader market, providing decent dividends but limited capital appreciation.

Scenario 3: The Digital Casualty In the pessimistic scenario, digital disruption accelerates beyond the company's ability to adapt. A new generation of AI-powered platforms makes traditional broking and advisory obsolete. Customers migrate to lower-cost alternatives for basic services and specialized boutiques for complex needs, leaving Aditya Birla Money stuck in an unprofitable middle. The company becomes a value trap, generating enough cash to survive but not enough to thrive.

The most likely outcome sits between scenarios one and two. The company has demonstrated ability to adapt and transform, but the pace of change in financial services is accelerating. Success will require not just good strategy but excellent execution, some luck with regulatory changes, and continued support from the parent group.

For investors, Aditya Birla Money represents a derivative play on India's financial services growth with the safety net of conglomerate backing. It won't deliver venture-style returns, but it also won't go to zero. In a portfolio context, it offers exposure to India's capital markets expansion with less volatility than pure-play brokers and more upside than traditional banks.

The journey from Apollo Sindhoori to Aditya Birla Money has been remarkable—from 13 branches in South India to a national platform serving millions. The next chapter of this story is being written now, in code and algorithms, in regulatory filings and customer interactions, in the daily decisions of thousands of employees working to build India's financial future. Whether it becomes a case study in successful transformation or another example of disruption's casualties remains to be seen. What's certain is that the outcome will be determined not by market forces alone but by the choices made in conference rooms and coding sessions, by the ability to balance tradition with innovation, and by the courage to change while maintaining what matters most—trust.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube