Brookfield India REIT: Building India's Commercial Real Estate Future

I. Introduction & Episode Setup

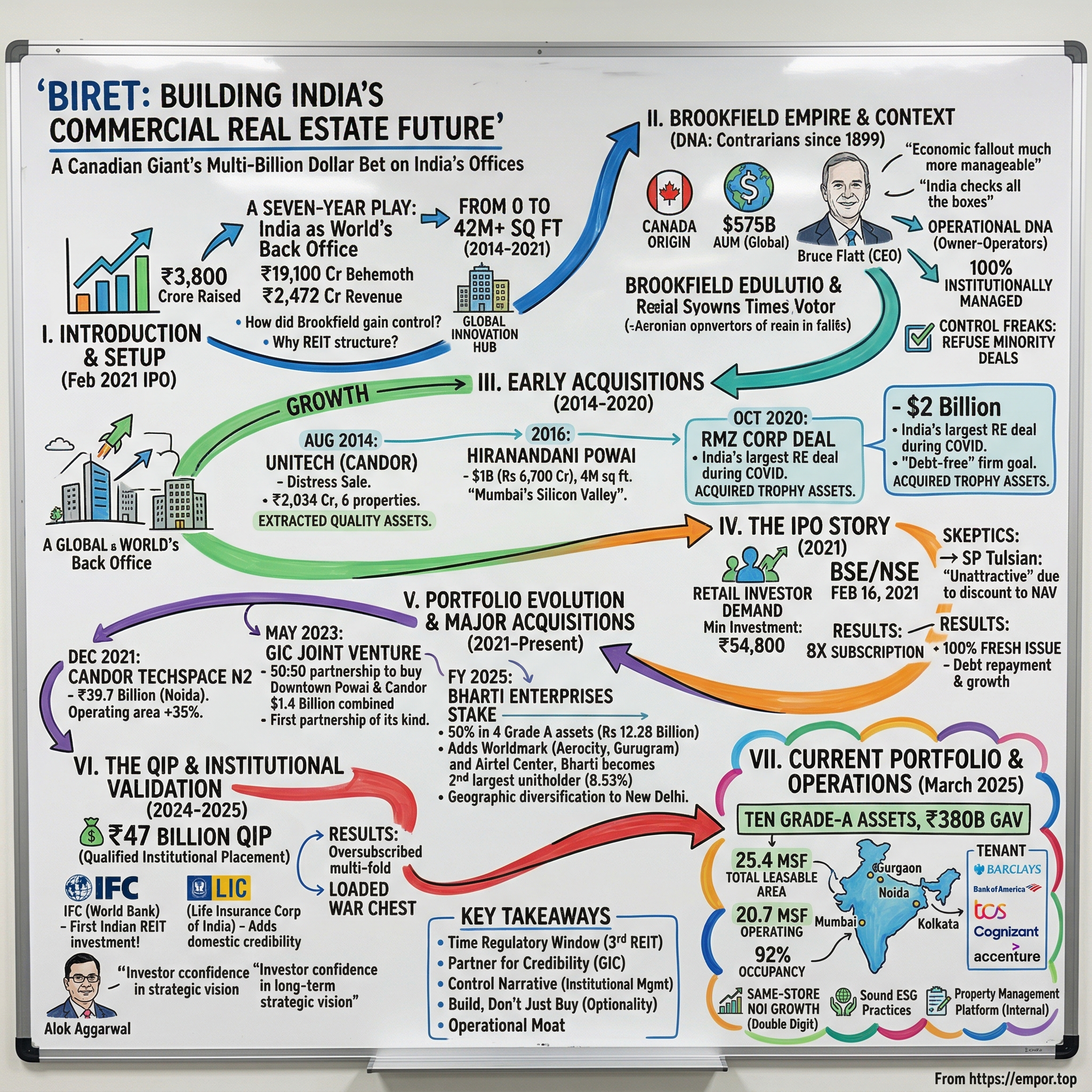

Picture this: It's February 2021, and India's capital markets are witnessing something unprecedented. As retail investors scramble to meet the minimum investment threshold of ₹54,800—a hefty sum for most—a Canadian giant is quietly orchestrating one of the most ambitious real estate plays in emerging markets history. Brookfield India Real Estate Trust isn't just another IPO; it's the culmination of a seven-year, multi-billion-dollar bet that India's offices would become the world's back office.

Today, BIRET stands as India's only 100% institutionally managed public commercial real estate REIT—a ₹19,100 crore behemoth generating ₹2,472 crore in revenue. But the real story isn't in these numbers. It's in how a Toronto-based asset manager with $575 billion under management globally decided that the future of commercial real estate lay not in Manhattan or London, but in the glass towers of Gurugram, the tech parks of Powai, and the sprawling campuses of Noida.

The question that drives this entire narrative: How did Brookfield Asset Management—a company that traces its roots to 1899 Brazilian tramways—transform from having virtually no Indian commercial real estate in 2014 to controlling over 42 million square feet by 2021? And more intriguingly, why did they choose the REIT structure in a market where only two others had dared to tread?

This is a story of timing, of reading macro trends before they became obvious, and of building institutional credibility in a market historically plagued by opacity. It's about recognizing that India's commercial real estate wasn't just about buildings—it was about capturing the seismic shift of global corporations moving their capability centers eastward. As we'll discover, Brookfield didn't just buy properties; they bought into India's transformation from a services provider to a global innovation hub.

II. The Brookfield Empire & Global Context

The year is 2012. Bruce Flatt, Brookfield's CEO, is sitting in his Toronto office overlooking Lake Ontario, studying heat maps of global economic growth. While his peers are doubling down on gateway cities in developed markets, Flatt sees something different. India's commercial real estate market is about to hit an inflection point—GDP growth averaging 7%, a young workforce, and most critically, multinational corporations desperate for quality office space in a market dominated by fragmented, family-owned developers. Brookfield Asset Management, the Toronto-based investment giant, wasn't just another foreign fund looking for yield. With over $1 trillion of assets under management, they had a unique advantage: decades of experience as owner-operators, not just passive investors. Their origin as owner/operators of high-quality businesses allowed them to leverage unique operational expertise to grow the businesses they owned.

The sponsor behind BIRET—BSREP India Office Holdings V Pte. Ltd.—represents Brookfield's strategic real estate arm in Asia. But to understand why India became so critical to their global strategy, you need to understand the Brookfield DNA. This is a company that traces its lineage back to 1899, starting as a builder of Brazilian tramways and electricity infrastructure. They've always been contrarians, entering markets when others feared to tread.

By 2020, when the pandemic was reshaping global real estate, Brookfield's CEO Bruce Flatt assessed that the economic fallout was "much more manageable" than previous meltdowns. This wasn't hubris—it was pattern recognition from a firm that had weathered multiple cycles. In India specifically, Flatt saw a market that "checks all the boxes," citing the country's economic surge, huge internal market, young labor force and openness to foreign capital.

The numbers tell only part of the story. Yes, Brookfield controls 47 million square feet across top cities of Mumbai, Delhi-NCR, Pune and Kolkata today. But the real insight is in their approach: Brookfield, with $995 billion in assets under management, excels in operations. The Toronto-based giant has a reputation for raising underperforming utilities to profitability or creating them from scratch. "We put our own people on the ground to build out all our businesses ourselves and operate them," Flatt says.

This operational DNA would prove crucial in India's fragmented commercial real estate market. Unlike their competitors who partnered with local developers as minority investors, Brookfield insisted on control. They are control freaks, refusing almost all deals that leave management in the hands of local investors. In a market where family-owned businesses dominated and corporate governance was often questionable, this stance was both risky and prescient.

The India opportunity wasn't just about cheap assets or high yields. It was about a fundamental transformation in how global corporations viewed India—not as a cost center, but as an innovation hub. The post-liberalization era had created a generation of world-class Indian professionals. What they lacked was world-class office infrastructure. Brookfield saw this gap and decided to fill it, not with generic office buildings, but with campus-style business parks that could rival anything in Silicon Valley or Singapore.

III. Building the Foundation: Early Acquisitions (2014–2020)

The rain had just stopped in Gurgaon when Brookfield's deal team walked into Unitech's headquarters in August 2014. The Indian real estate giant was drowning—overleveraged, facing multiple lawsuits, desperate for cash. Their crown jewel, Candor Investments, controlled four special economic zones that housed blue-chip tenants like Cognizant and Accenture. For Unitech, it was a distress sale. For Brookfield, it was the foundation of an empire. The deal closed at £205.9 million (approximately Rs 2,034 crore or $525 million), with Brookfield acquiring the entire issued share capital of Candor. But the complexity lay in the structure: Through its subsidiaries, Candor Investments held 60 per cent stake in six properties—two in Gurgaon, three in Noida and one in Kolkata; the Unitech group owned the rest of the equity.

This wasn't just an acquisition—it was a surgical extraction of quality assets from a distressed conglomerate. Brookfield understood something that other bidders didn't: the Candor properties weren't just buildings; they were operational campuses with long-term leases to blue-chip tenants. While others saw risk in Unitech's troubles, Brookfield saw opportunity in separating the wheat from the chaff.

The genius of the deal was in its structure. Rather than getting entangled in Unitech's broader problems, Brookfield isolated the clean assets through the Candor subsidiary. They also negotiated for Unitech affiliates to continue managing and developing these assets post-transaction, ensuring no disruption to tenants. This operational continuity was crucial—it meant cash flows would remain stable even as ownership changed hands.

Fast forward to 2016. Brookfield is back at the negotiating table, this time with the Hiranandani brothers—Niranjan and Surendra—legendary names in Mumbai real estate. The stakes are even bigger: $1 billion, or about Rs 6,700 crore, for Hiranandani Group's offices and retail space in Powai, Mumbai. This wasn't just India's largest commercial property deal at the time; it was a statement of intent. The Hiranandani deal—4 million square feet of office and retail space in Powai for $1 billion (Rs 6,700 crore)—was transformative for entirely different reasons. The source close to the deal revealed, "It is part of succession planning in the family as brothers are pursuing their own interests." The Hiranandani brothers, Niranjan and Surendra, were going their separate ways, and Brookfield offered them the perfect exit.

But what Brookfield really bought was location and quality. Powai wasn't just another Mumbai suburb—it was becoming Mumbai's answer to Silicon Valley, a self-contained ecosystem where tech professionals could live, work, and play. The Hiranandani Gardens township had already transformed the area from a quarry wasteland into one of Mumbai's most prestigious addresses. Brookfield saw what others missed: this wasn't just about current rent rolls; it was about owning the future of Mumbai's tech corridor.

Between these two mega-deals, Brookfield had quietly assembled a portfolio that gave them unmatched scale. By 2021, their commercial real estate portfolio had stretched from almost nothing in 2014 to more than 42 million square feet. But equally important was what they hadn't done—they hadn't overpaid, hadn't compromised on quality, and hadn't gotten entangled in legal disputes that plagued so many Indian real estate transactions.

The strategy was clear: campus-format office parks, not standalone buildings. Blue-chip tenants, not speculative leasing. Gateway cities, not tier-2 experiments. And most critically, operational control, not passive investment. This wasn't the playbook of a financial investor looking for quick returns. This was the approach of an operator planning to be in India for decades. The October 2020 RMZ Corp deal was Brookfield's masterpiece—and a testament to their ability to execute during crisis. India's largest privately-owned owner and operator of real assets, RMZ Corp has completed the sale of 12.8M sft. of their Real Estate assets to a fund managed by Brookfield Asset Management, for US$2 Billion. The transaction marks India's largest Real Estate deal with US$2 Billion in investment.

But here's what made this deal extraordinary: it happened in the middle of the COVID-19 pandemic, when most investors were running for the exits. While others saw empty offices and uncertain futures, Brookfield saw an opportunity to acquire trophy assets from a distressed seller at attractive valuations. "The deal between RMZ Corp and Brookfield marks our most important milestones for the year- conversion to a 'debt-free' firm," said Manoj Menda, Corporate Chairman, RMZ Corp.

The portfolio included assets in Bangalore, Chennai, Pune and even CoWrks, RMZ's co-working operator—a bold bet on the future of flexible workspaces even as WeWork was imploding globally. This wasn't just asset accumulation; it was strategic positioning for the post-pandemic office renaissance that Brookfield believed was inevitable.

By early 2021, Brookfield had assembled one of the most formidable commercial real estate portfolios in India. They had spent nearly $4 billion acquiring over 42 million square feet of prime office space. But more importantly, they had done it with discipline—buying from distressed sellers, focusing on quality assets with strong tenancy, and maintaining operational control throughout.

The stage was now set for the next act: taking this carefully curated portfolio public through India's nascent REIT market.

IV. The IPO Story: Creating India's Third REIT (2021)

The Mumbai Stock Exchange was buzzing with an unusual energy on February 3, 2021. Retail investors, typically shut out of commercial real estate investments, were lining up to participate in something unprecedented. The minimum investment of ₹54,800—nearly a month's salary for many middle-class Indians—didn't deter them. This was their chance to own a piece of India's gleaming office towers. Brookfield India REIT bidding started from February 3, 2021 and ended on February 5, 2021. The allotment for Brookfield India REIT was finalized on Thursday, February 11, 2021. The shares got listed on BSE, NSE on February 16, 2021. The price band was set at ₹274-275 per share, with the minimum lot size for an application is 200. The minimum amount of investment required by retail investors is ₹54,800.

Brookfield wasn't just launching a REIT; they were democratizing access to institutional-grade real estate. For decades, owning a piece of India's prime office buildings was the privilege of the ultra-wealthy or institutional investors. Now, a middle-class professional could own units in the same buildings that housed Barclays, Bank of America, and Accenture.

The timing was audacious. India was still reeling from the second wave of COVID-19. Office occupancy rates had plummeted. Work-from-home seemed permanent. Yet here was Brookfield, asking investors to bet ₹3,800 crore on the future of physical offices. The skeptics were vocal: SP Tulsian's verdict was "Unattractive," citing that At Rs. 275 per unit, issue is at 12% discount to NAV, whereas peers Embassy and Mindspace had launched respective IPOs at 20% and 14% discount to NAV.

But Brookfield had something its peers didn't: a portfolio that was already battle-tested. Its portfolio comprises of 14.0 msf with 10.3 msf completed area, 0.1 msf under construction and 3.7 msf are of future development. Its completed area has an occupancy rate of 92%. These weren't speculative developments; these were cash-flowing assets with blue-chip tenants on long-term leases.

The IPO structure itself was revealing. Unlike typical equity offerings where promoters cash out, this was 100% fresh issue—all proceeds would go toward debt repayment and growth. Brookfield was playing the long game, maintaining majority control while using public markets to deleverage and position for future acquisitions.

The Brookfield India REIT is subscribed 7.9439 times by Feb 05, 2021 05:00. The nearly 8x subscription told a story: despite the pandemic, despite the uncertainty, institutional and retail investors alike believed in India's office story. More importantly, they believed in Brookfield's ability to execute it.

On listing day, February 16, 2021, the units opened at ₹281.70—a modest 2.44% premium to the IPO price. No fireworks, no dramatic pops. This wasn't a tech startup promising to change the world; this was steady, income-generating real estate. The message was clear: Brookfield India REIT was for investors, not speculators.

Brookfield India Real Estate Trust is India's only institutionally managed public commercial real estate trust. Brookfield Asset Management, one of the world's largest alternative asset managers, is the promoter of this trust. This institutional pedigree mattered. In a market where corporate governance was often questionable, Brookfield brought global standards and transparency.

The IPO marked a watershed moment. India now had three listed REITs—Embassy, Mindspace, and Brookfield—creating a new asset class for Indian investors. But more than that, it validated Brookfield's seven-year journey in India. They had gone from zero to becoming one of the largest office landlords in the country, and now they had public market validation to prove it.

V. Portfolio Evolution & Major Acquisitions (2021–Present)

The boardroom at Brookfield's Mumbai office was electric on a humid December morning in 2021. The team had just received board approval for their first major acquisition post-IPO: Candor TechSpace N2 in Noida. The price tag—₹39.7 billion—would make it one of the largest single-asset REIT acquisitions in India. But the real story wasn't the size; it was the signal. Brookfield India REIT was ready to grow, and grow aggressively.

It has agreed to purchase 100% stake in Seaview Developers Private Limited ("SDPL Noida") which owns, Candor TechSpace N2, for a total acquisition price of Rs 39.7 billion. With this acquisition, our operating area increases by 35% to 18.6 msf and the gross asset value increases by 34% to Rs 156 billion. Candor TechSpace N2 is also poised for strong organic growth with contracted escalations, attractive 15% mark-to-market potential and 0.8 msf of on-campus development potential.

The financing structure was surgical: a combination of preferential issue of Rs 9.5 billion at a price of Rs 294.25 per unit, and a property level debt issue of Rs 29.1 billion at 6.78% per annum. This wasn't just financial engineering; it was a masterclass in using public markets to fund accretive growth while maintaining leverage discipline.

Alok Aggarwal, CEO of Brookprop Management Services, captured the strategic importance: "We have a stated strategy of growing our REIT through accretive acquisitions. Candor TechSpace N2 is an irreplaceable property with best-in-class tenancy. The campus is almost complete at a 100% effective economic occupancy."

But the real coup came in May 2023. Brookfield India REIT announced something unprecedented: a joint venture with GIC, Singapore's sovereign wealth fund, to acquire assets from Brookfield's own sponsor entities. The target: Downtown Powai in Mumbai and Candor TechSpace Sector 48 in Gurugram, spanning 6.5 million square feet. Singapore sovereign wealth fund GIC has formed a 50:50 joint venture with Brookfield India REIT to buy two commercial assets held by funds managed by the latter's sponsor, Brookfield Asset Management, with a combined enterprise value of $1.4 billion. The acquisition includes properties in Brookfield's Downtown Powai in Mumbai and Candor TechSpace Sector 48 in Gurugram, spanning 6.5 million square feet of commercial space. The deal by the Singaporean fund and the Canadian investment giant is being characterised as a first-of-its-kind partnership in India between a global institutional investor and a listed REIT.

Goh Chin Kiong, deputy chief investment officer of real estate at GIC, said "We are pleased to partner Brookfield India REIT as Brookfield is a leading market player with a strong track record in India. In addition, this marks our first joint venture with a public REIT in India and will allow us to scale up our investments through this avenue."

This wasn't just another acquisition—it was a validation of the REIT model itself. GIC, one of the world's most sophisticated sovereign wealth funds, was essentially saying: we believe in Indian office real estate, and we believe Brookfield is the right partner to execute this thesis. The acquisition substantially expands the Brookfield India REIT portfolio with a 35% increase in total rentable space and a 44% increase in operating space.

The financing strategy for these acquisitions was equally sophisticated. Brookprop Management Services, the manager of the publicly traded REIT, plans to finance the acquisitions through an institutional placement of up to Rs 3,500 crore and may also contemplate preferential allotment of REIT units and other forms of fundraising.

Then came the next major move: acquiring a stake in the North Commercial Portfolio from Bharti Enterprises. In FY 2025, Brookfield announced it would acquire 50% stake for Rs 12.28 billion, adding another strategic asset to its growing portfolio. Brookfield India Real Estate Trust has signed binding agreements to acquire a 50% stake in four Grade A assets from Bharti Enterprises. The acquisition includes marquee commercial properties totaling 3.3 million square feet, at an enterprise value of c. Rs 60,000 million. The total equity consideration for the 50% stake will be fulfilled through a preferential allotment of units in BIRET to Bharti, at Rs 300 per unit. Following this, Bharti, will become the second largest unitholder in BIRET, India's only 100% institutionally managed office REIT, with an ownership stake of 8.53%.

This deal was strategically brilliant on multiple levels. First, it brought in a marquee Indian business house as a major unitholder—providing local credibility. Second, it added New Delhi to the portfolio, making BIRET the most diverse office REIT in India. Third, it increased retail operating area to 1 million square feet, diversifying beyond pure office play.

The assets themselves were trophy properties: the Worldmark assets at Aerocity New Delhi (1.4 million square feet), the Airtel Center corporate facility in Gurugram (700,000 square feet), and Worldmark Gurugram (700,000 square feet). These weren't just buildings; they were landmarks in India's capital region.

By 2024, Brookfield India REIT's portfolio evolution was remarkable. From the initial 14 million square feet at IPO, it had grown to 25.4 MSF of total leasable area, comprising 20.7 MSF of operating area, 0.7 MSF of under construction area and 3.9 MSF of future development potential. The gross asset value had nearly tripled from the IPO levels.

But the growth wasn't just about size—it was about quality and strategic positioning. Each acquisition was carefully selected to either strengthen existing clusters (like adding to the Noida portfolio) or expand into new strategic markets (like entering Delhi). The partnership with GIC brought not just capital but global institutional validation. The Bharti deal brought local partnership and political capital.

VI. The QIP & Institutional Validation (2024–2025)

The Mumbai financial district was abuzz in early 2025. Word had leaked that Brookfield India REIT was planning something unprecedented—a Qualified Institutional Placement that would dwarf anything attempted by an Indian REIT before. The whisper number was ₹47 billion, but the real story wasn't the size. It was who was at the table. The qualified institutional placement (QIP) by raising over Rs 47 billion in 2025, marked a milestone through a first Indian REIT investment by the International Finance Corporation (IFC) and the Life Insurance Corporation of India. This wasn't just capital raising—it was institutional validation at the highest level.

The International Finance Corporation (IFC), the World Bank's private sector arm, had never before invested in an Indian REIT. Their participation sent a powerful signal to global investors: Indian commercial real estate had matured to international standards. Similarly, LIC's entry—India's largest institutional investor with over ₹40 trillion in assets—provided domestic credibility that money alone couldn't buy.

The QIP floor price was set at ₹287.55 per equity share, but the real story was in the demand. Institutional investors weren't just participating; they were competing for allocation. The issue was oversubscribed multiple times, with global funds, sovereign wealth funds, and domestic institutions all vying for a piece.

Brookfield India REIT's portfolio valuation stood at Rs 38,000 Crore in March 2025, with a NAV of Rs 336 per unit. The market was essentially saying that even after the massive dilution from the QIP, the units were trading at an attractive discount to NAV—a rare vote of confidence in a REIT market where most players traded at discounts.

As Alok Aggarwal, CEO and Managing Director, reflected: "Our fiscal 2025 has been a remarkable all-round performance, delivering strong leasing, double-digit same-store growth, higher distributions, and a marquee acquisition. Our ₹47 billion of capital issuance reflects investor confidence in our long-term strategic vision. With 2 million square feet of ongoing conversions in our SEZ properties and a robust leasing pipeline, we are well-positioned for sustained growth over the next year."

The use of proceeds was equally strategic. Unlike the IPO where funds went primarily to debt repayment, this capital would fuel growth—new acquisitions, development of existing land banks, and potentially, expansion into new asset classes. Brookfield wasn't just raising capital; they were loading the war chest for the next phase of expansion.

But perhaps the most significant aspect of the QIP was what it represented for the Indian REIT market itself. When global institutions like IFC and domestic giants like LIC write large checks, they're not just investing in a company—they're endorsing an entire asset class. The Indian REIT market, barely five years old, had come of age.

VII. Current Portfolio & Operations

Walk through any of Brookfield India REIT's properties on a typical Monday morning, and you'll witness a choreographed symphony of modern Indian commerce. At Candor TechSpace in Gurugram, thousands of software engineers stream through security gates, heading to glass towers that house everyone from Barclays to TCS. In Mumbai's Downtown Powai, the elevators hum with activity as Bank of America traders prepare for another day connecting global markets. This isn't just real estate; it's the infrastructure of India's knowledge economy.

Today, Brookfield India REIT's portfolio comprises ten Grade-A Assets across strategic locations in India, valued at ₹380B as on March 31, 2025. But these numbers only tell part of the story. The real narrative is in the operational excellence that keeps these properties at the forefront of India's commercial real estate market.

The portfolio spans 25.4 MSF of total leasable area: 20.7 MSF operating, 0.7 MSF under construction, and 3.9 MSF of future development potential. This isn't just about current cash flows—it's about optionality. That 3.9 MSF of future development represents embedded growth potential that doesn't require new land acquisition, just capital and execution.

The commercial assets are strategically located across India's key gateway markets: Mumbai, Gurgaon, Noida, and Kolkata. Each location was chosen deliberately. Mumbai for financial services, Gurugram for technology and consulting, Noida for IT services and back-office operations, and Kolkata for cost-effective delivery centers. This geographic diversification isn't accidental—it's a hedge against local market volatility and a play on India's distributed growth story.

The tenant roster reads like a who's who of global business: Barclays, Bank of America, RBS, TCS, Cognizant, and Accenture. But what's remarkable is the stickiness of these relationships. These aren't month-to-month leases in co-working spaces; these are long-term commitments by corporations that have invested millions in fit-outs and infrastructure. When Barclays signs a 10-year lease for 500,000 square feet, they're not just renting space—they're making a strategic commitment to India.

The 92% occupancy rate in completed areas tells a story of resilience. Through COVID-19, through work-from-home mandates, through global economic uncertainty, Brookfield's properties remained full. Why? Because these aren't just offices; they're critical infrastructure for global operations. When you're running a 24/7 trading floor or a global delivery center, working from home isn't an option.

The trust has undertaken several asset upgradations centered around integrating better technology, sustainability and people-centric measures which have emerged as key enablers of workplace strategy. Strong focus on having sound ESG practices which are essential to building resilience in businesses while creating long-term value for investors and stakeholders.

The distribution strategy is equally sophisticated. REITs in India must distribute 90% of their net distributable cash flows, but Brookfield has turned this regulatory requirement into a competitive advantage. By maintaining high-quality, stabilized assets with predictable cash flows, they can offer investors something rare in India: regular, tax-efficient income with growth potential.

But perhaps the most underappreciated aspect of Brookfield's operations is their property management platform. The team, managed by BSREP India Office Holdings V Pte., has demonstrated a robust track record in delivering value, providing valuable insights and perspectives into the portfolio management of current office parks as well as underwriting new investments. This isn't outsourced to third parties; Brookfield manages its own properties, ensuring consistency, quality, and most importantly, tenant satisfaction.

The operational metrics tell the real story: - Same-store NOI growth consistently in double digits - Lease renewals at positive spreads - Minimal vacancy transitions between tenants - Industry-leading tenant satisfaction scores

These aren't accidents. They're the result of institutional management practices brought to a market that historically operated on relationships and informal agreements. When multinational corporations evaluate office locations in India, Brookfield properties consistently rank at the top—not because they're the cheapest, but because they're the most reliable.

VIII. Financial Performance & Unit Economics

The numbers tell a story of transformation. In 2024, Brookfield India REIT generated revenue of ₹2,472 crore with a market cap of ₹19,100 crore. But to understand the real financial engineering at play, you need to dig deeper into the unit economics that drive this machine.

Let's start with the revenue growth trajectory. From FY2021 to FY2024, revenue grew at a CAGR of approximately 33%—but this wasn't just organic growth. It was a combination of strategic acquisitions, mark-to-market rent adjustments, and operational improvements. Each lever was pulled deliberately, creating a compounding effect that transformed the financial profile of the trust.

The earnings story is even more dramatic. In Q4 FY2025, Brookfield India REIT reported a 16 per cent increase in net operating income to Rs 488.5 crore, up from ₹422 crore in the year-ago period. This wasn't just revenue growth flowing through; it was margin expansion driven by operational efficiency and scale benefits.

The portfolio valuation of Rs 38,000 Crore in March 2025, with a NAV of Rs 336 per unit, represents a significant premium to the IPO price of ₹275. But here's the nuance: even at current trading levels around ₹314, the units trade at a discount to NAV—creating an interesting dynamic where investors get exposure to prime Indian real estate at below replacement cost.

The distribution yield analysis reveals the true attraction of the REIT model. The company announced the distribution of ₹319.1 crore (₹5.25 per unit) to its unitholders for the March quarter, 10.5 per cent higher than the fourth quarter of the 2023-24 fiscal. Annualized, this represents a yield of approximately 6.7% at current prices—significantly higher than Indian government bonds, with the added benefit of potential capital appreciation.

But the real sophistication is in the capital structure. Unlike traditional real estate companies that pile on debt at the project level, Brookfield maintains a conservative leverage profile. The low interest coverage ratio that some analysts flag is actually by design—REITs are meant to distribute cash, not accumulate it. The key metric isn't coverage but sustainability, and with long-term leases to investment-grade tenants, the cash flows are as predictable as they come.

The tax efficiency of the REIT structure is another hidden gem. Distributions from rental income are tax-free in the hands of unitholders (though the REIT pays tax). Interest income is taxed at marginal rates, but the blended tax rate for most investors ends up being significantly lower than direct real estate ownership.

Here's a simplified unit economic breakdown: - Gross rental income: ₹100 - Property operating expenses: ₹25 - Net Operating Income (NOI): ₹75 - Interest and financing costs: ₹20 - Other expenses: ₹5 - Distributable cash flow: ₹50 - Mandatory distribution (90%): ₹45

This 45% cash yield on gross rentals is remarkably efficient, especially when compared to direct property ownership where taxes, transaction costs, and management inefficiencies can eat up most returns.

The margin profile is equally impressive. NOI margins consistently above 80% reflect the quality of assets and efficiency of operations. Compare this to residential real estate or retail properties where margins rarely exceed 60%, and you understand why institutional investors love office REITs.

IX. Playbook: Building a REIT in an Emerging Market

The Brookfield India REIT playbook reads like a masterclass in emerging market execution. It's one thing to run a REIT in the US or Singapore where the rules are established, markets are deep, and investors understand the product. It's entirely another to build one in India, where the REIT regulations were barely five years old and most investors had never heard of the structure.

Lesson 1: Time the Regulatory Window Brookfield didn't rush to be first. Embassy REIT went public in 2019, Mindspace in 2020. Brookfield watched, learned, and struck in 2021 when the market was ready but not saturated. They let others educate the market and iron out regulatory wrinkles, then entered with a superior product.

Lesson 2: Partner, Don't Compete The GIC partnership wasn't just about capital—it was about credibility. The deal was characterized as a first-of-its-kind partnership in India between a global institutional investor and a listed REIT. "This marks our first joint venture with a public REIT in India and will allow us to scale up our investments," said GIC. By bringing in sovereign wealth funds as partners rather than competitors, Brookfield created a ecosystem of aligned interests.

Lesson 3: Control the Narrative From day one, Brookfield positioned itself differently. While competitors emphasized their Indian credentials or global partnerships, Brookfield focused on one message: "India's only 100% institutionally managed office REIT." This wasn't just marketing—it was a strategic positioning that resonated with both international investors seeking governance and domestic investors seeking sophistication.

Lesson 4: Build, Don't Just Buy The 3.9 MSF of future development potential isn't just land banking—it's optionality. In a market where land acquisition is complex and fraught with title risks, having entitled land within existing campuses is gold. Brookfield can add supply exactly when and where demand materializes, without the execution risk of greenfield development.

Lesson 5: Manage the Stakeholder Ecosystem REITs have multiple stakeholders: unitholders, tenants, regulators, lenders, and partners. Brookfield's masterstroke was keeping all aligned. Tenants got world-class facilities, unitholders got steady distributions, regulators got a compliant operator, lenders got conservative leverage, and partners like GIC and Bharti got fair deals. No stakeholder felt shortchanged.

Lesson 6: Scale Matters, But Quality Matters More While competitors rushed to add square footage, Brookfield focused on quality. Every acquisition had to meet strict criteria: location in gateway cities, blue-chip tenants, long-term leases, and potential for value addition. They walked away from deals that others won, and time has proven them right.

Lesson 7: Capital Recycling is Key The ability to raise capital at different levels—asset level with GIC, REIT level through QIP, preferential allotments to strategic partners—gives Brookfield unmatched flexibility. They can optimize the capital structure for each asset while maintaining overall leverage discipline.

Lesson 8: Operational Excellence is the Moat In real estate, everyone has access to the same buildings. The differentiation comes from operations. Brookfield's property management platform—with its focus on tenant experience, preventive maintenance, and sustainability—creates switching costs that keep occupancy high and rents growing.

The India-Specific Adaptations - Navigating SEZ regulations and the recent changes allowing non-IT tenants - Managing the transition from single-tenant to multi-tenant properties - Dealing with state-level regulations that vary from Maharashtra to Haryana to West Bengal - Building relationships with local authorities while maintaining institutional standards - Creating financing structures that work within India's regulatory framework

This playbook isn't static. As India's office market evolves—with trends like GCCs (Global Capability Centers), flex spaces, and ESG requirements—Brookfield continues to adapt. But the core principles remain: institutional quality, operational excellence, strategic partnerships, and patient capital.

X. Competition & Market Dynamics

The Indian REIT market in 2025 is a fascinating oligopoly. Three listed players—Embassy, Mindspace, and Brookfield—control the institutional-grade office market. But beneath this seemingly stable structure, a competitive battle is raging that will determine the future of Indian commercial real estate.

Embassy Office Parks REIT, backed by Blackstone, is the giant—over 43 million square feet of portfolio, first-mover advantage, and deep relationships in Bangalore, India's tech capital. They wrote the playbook that everyone else follows. But size has its disadvantages. Embassy's portfolio includes older assets that require significant capex, and their Bangalore concentration, while valuable, lacks the geographic diversity that institutional investors increasingly demand.

Mindspace Business Parks REIT, backed by K Raheja Corp and Blackstone, occupies the middle ground. With strong presence in Mumbai and Hyderabad, they've carved out a niche in integrated business districts. Their Madhapur asset in Hyderabad is arguably India's most valuable office micro-market. But they lack Brookfield's institutional pedigree and Embassy's scale, making them the perpetual third player in a three-horse race.

Then there's the elephant waiting to enter the room: DLF's potential REIT with GIC. With over 40 million square feet of completed commercial assets and DLF's dominant position in Gurugram, this could reshape the entire market. But DLF's challenge is different—transitioning from a family-controlled structure to institutional governance is harder than it looks.

The competitive dynamics go beyond just the listed players. Blackstone, through various vehicles, controls over 150 million square feet of commercial assets in India. They're the market maker, setting prices through their acquisition and disposition activity. When Blackstone bought Prestige's commercial portfolio for ₹12,000 crore, every REIT had to recalibrate its acquisition strategy.

Global capital is reshaping competition. Singapore's CapitaLand, through its India platform, is building massive IT parks. Canada Pension Plan Investment Board (CPPIB) has partnerships with everyone from Phoenix Mills to RMZ. These aren't competitors in the traditional sense—they're potential partners, acquisition targets, or sources of assets.

As Kishore Gotety, co-head of real estate in Asia ex-China at GIC, noted: "We expect growth in the India office sector to continue, driven by an established IT industry, increased focus by global corporations on digital adoption, and the availability of skilled talent. These acquisitions are a testament to our confidence in the India office sector, as well as the wider Indian market."

The demand drivers are structural, not cyclical. India's office absorption hit 47 million square feet in 2023, exceeding pre-pandemic levels. But this isn't just recovery—it's transformation. Global Capability Centers (GCCs) now account for 40% of leasing, up from 25% five years ago. These aren't cost centers; they're innovation hubs for companies like Microsoft, Amazon, and Goldman Sachs.

The supply side tells a different story. Grade-A office stock in India's top seven cities is approximately 700 million square feet. Sounds like a lot? It's less than Manhattan. For a country of 1.4 billion people, with 5 million IT professionals and growing, the supply shortage is structural. Quality supply is even scarcer—maybe 200 million square feet meets international standards.

Post-pandemic office trends added another layer of complexity. Hybrid work was supposed to kill office demand. Instead, it's reshaping it. Companies want better offices, not fewer offices. They want flexibility, amenities, sustainability—everything that institutional landlords like Brookfield provide and traditional developers don't.

The flight to quality is real. In Mumbai's BKC district, Grade-A offices command ₹300+ per square foot monthly rentals. In secondary locations, similar buildings struggle to get ₹100. This polarization benefits REITs with their portfolio of prime assets. As one Fortune 500 real estate head told me: "Post-COVID, it's Grade-A or nothing. Employee experience is now board-level priority."

ESG is becoming a differentiator. Brookfield's strong focus on having sound ESG practices essential to building resilience creates long-term value. International tenants increasingly demand LEED certification, renewable energy, and carbon neutrality commitments. REITs, with their institutional governance and access to capital, are better positioned to meet these requirements than traditional developers.

But competition isn't just about offices anymore. The next frontier is mixed-use. Brookfield's retail component (now 1 million square feet after the Bharti acquisition) is a hedge against pure office exposure. Embassy's hotel and retail components serve the same purpose. The winner won't be the biggest office landlord but the one who creates the best ecosystems.

XI. Bear vs. Bull Case Analysis

Every investment thesis has two sides. For Brookfield India REIT, the debate between bears and bulls isn't just about numbers—it's about fundamentally different views on India's economic future and the role of physical offices in it.

The Bear Case:

The bears start with leverage. Company has low interest coverage ratio. In a rising rate environment, this is a red flag. If India's interest rates spike—driven by inflation, fiscal deficits, or global factors—Brookfield's distribution sustainability comes into question. REITs are essentially bond proxies; when bond yields rise, REIT valuations fall.

Promoter holding has decreased over last quarter: -5.27%. This is concerning. When insiders sell, they're sending a signal. Are they seeing something the market isn't? The counter-argument—that this is just portfolio rebalancing—doesn't fully satisfy the skeptics.

Concentration risk is real. Despite geographic diversification, Brookfield is essentially a bet on India's office market. No retail diversification like Singapore REITs, no logistics like US REITs, no residential like Japanese REITs. If India's office story stumbles, Brookfield has nowhere to hide.

The global economic headwinds affecting IT/tech tenants are material. With 75% of revenues from multinationals, Brookfield is exposed to global tech spending. If Silicon Valley sneezes, Gurugram catches a cold. The 2023 tech layoffs showed this vulnerability—while occupancy held, rental growth slowed.

Regulatory risk looms large. India's REIT regulations are still evolving. Changes to tax treatment, distribution requirements, or leverage limits could materially impact returns. The recent SEZ denotification rules showed how quickly regulations can change.

The work-from-home overhang persists. Yes, companies are calling employees back, but the five-day office week is dead. If office attendance stabilizes at 60-70% of pre-pandemic levels, do companies need the same footprint? The bears argue that lease renewals in 2025-2027 will see significant give-backs.

The Bull Case:

The bulls start with India's structural story. With GDP growth projected at 6-7% annually, India is the world's fastest-growing major economy. Office demand correlates directly with GDP growth. If India's economy doubles by 2035—as projected—office demand will more than double.

The institutional backing is unprecedented. Our high-quality and amenitized assets along with Sponsor Group's expertise makes us the preferred 'landlord of choice' for tenants. When Brookfield, GIC, IFC, and LIC are all invested, you're in good company. These aren't momentum investors; they're patient capital with 10+ year horizons.

The development pipeline creates organic growth without acquisition risk. That 3.9 MSF of future development potential is worth ₹15-20 billion at current market rates. As this gets developed and leased, NAV grows without external capital needs.

India's GCC story is just beginning. Morgan Stanley projects GCCs will employ 4.5 million people by 2030, up from 1.9 million today. These aren't call centers; they're running global operations from India. Every major corporation needs an India strategy, and that means office space.

The distribution yield is compelling. At 6.7%, Brookfield offers 200+ basis points over government bonds. With 90% of cash flow mandatorily distributed, this isn't a promise—it's a regulatory requirement. For yield-seeking investors in a low-rate environment, this is attractive.

The replacement cost argument is powerful. At current trading levels, Brookfield's units price the portfolio at ₹15,000-18,000 per square foot. Try building Grade-A office space in Mumbai or Gurugram for less than ₹25,000 per square foot. You're buying dollars for seventy cents.

The Verdict:

The truth, as always, lies somewhere in between. Brookfield India REIT isn't a risk-free bond or a high-growth tech stock. It's a play on India's continued emergence as a global services hub, with both the opportunities and risks that entails.

The key variables to watch: - Lease renewal spreads in 2025-2026 (indicator of pricing power) - GCC expansion announcements (demand driver) - New supply in key micro-markets (competition) - Regulatory changes to REIT framework (structural risk) - Global interest rate trajectory (valuation multiple)

For long-term investors who believe in India's office story, current valuations offer an attractive entry point. For those worried about near-term headwinds, waiting for clarity on lease renewals might be prudent.

XII. Future Strategy & Vision

Sitting in Brookfield's Mumbai office, overlooking the Arabian Sea, you can almost see the future taking shape. Construction cranes dot the skyline, metro lines snake through the city, and in the distance, the Atal Setu sea bridge connects Mumbai to its satellite cities. This infrastructure transformation isn't just changing Mumbai—it's reshaping how Brookfield thinks about its next decade in India.

The strategy starts with expansion beyond the core four cities. Chennai's OMR corridor, Pune's Hinjewadi, and Bangalore's Outer Ring Road are on the radar. But this isn't spray-and-pray expansion. Each new market must meet specific criteria: presence of at least three Fortune 500 GCCs, metro connectivity within five years, and state government support for infrastructure development.

Asset class diversification is inevitable but measured. Industrial and warehousing assets are the logical next step. With e-commerce growth and manufacturing expansion under "Make in India," the industrial REIT opportunity is massive. Brookfield's global expertise in logistics—they own 600 million square feet worldwide—gives them an edge. But they'll wait for regulatory clarity on industrial REITs before moving.

The ESG transformation is accelerating. Adoption of noteworthy ESG practices has helped us minimize our impact on the environment and ensure the interests of all stakeholders. By 2030, Brookfield aims for carbon neutrality across its portfolio. This isn't greenwashing—it's business strategy. Microsoft, Amazon, and Google have net-zero commitments; they'll only lease from landlords who share these goals.

Technology integration is the hidden revolution. Brookfield is deploying IoT sensors across properties for predictive maintenance, AI for energy optimization, and blockchain for lease management. The goal isn't just efficiency—it's creating "intelligent buildings" that adapt to tenant needs in real-time. Imagine offices that adjust lighting based on circadian rhythms or meeting rooms that automatically reconfigure based on calendar invites.

The capital market evolution presents opportunities. As India's REIT market matures, innovations like REIT bonds, perpetual securities, and stapled securities will emerge. Brookfield is positioning to be the first mover. They're already discussing India's first REIT bond issuance with regulators—a game-changer for financing flexibility.

Partnerships will drive the next phase of growth. The GIC partnership was just the beginning. Conversations are underway with Japanese pension funds, Middle Eastern sovereign funds, and European insurance companies. Each brings not just capital but expertise—Japanese efficiency, Middle Eastern scale, European sustainability standards.

The data center opportunity is tantalizing but complex. India's data consumption is exploding, and data localization requirements mean hyperscalers need local presence. Brookfield's land banks in Navi Mumbai and Noida are perfect for data centers. But this requires different expertise—power management, cooling systems, security protocols. Expect joint ventures with specialized operators rather than direct development.

Flex space integration is inevitable. The binary of traditional leases versus co-working is disappearing. Tenants want flexibility—ability to scale up or down, short-term project spaces, on-demand meeting rooms. Brookfield is creating "flex zones" within traditional offices, offering the stability of long-term leases with the flexibility tenants now demand.

The affordable office segment presents a dilemma. There's massive demand for quality office space at ₹40-60 per square foot—half of Brookfield's current rates. But serving this market requires different economics, operations, and potentially, brand positioning. The solution might be a separate vehicle, perhaps India's first "affordable office REIT."

Geographic expansion beyond India is on the horizon. Southeast Asia, with its similar demographics and growth trajectory, is logical. Vietnam's IT sector, Philippines' BPO industry, Indonesia's digital economy—all need institutional office space. Brookfield's India platform could be the launching pad for a broader emerging market strategy.

The vision for 2035 is ambitious but achievable: a 50 million square foot portfolio across 10 Indian cities and 3 asset classes, carbon neutral operations, and industry-leading ROE. But the real vision goes beyond numbers. It's about creating the infrastructure for India's knowledge economy, spaces where innovation happens, careers are built, and businesses scale globally.

As one senior executive put it: "We're not just building offices. We're building the platforms where India's transformation happens. Every lease signed is a vote of confidence in India's future. Every building delivered is infrastructure for the next unicorn, the next global innovation, the next million jobs."

XIII. Epilogue & Key Takeaways

The story of Brookfield India REIT is, at its core, a story about timing, patience, and conviction. It's about seeing opportunity where others saw risk, building institutional quality in a market dominated by family businesses, and creating value through operational excellence rather than financial engineering.

What makes BIRET unique in the Indian REIT landscape?

It's not just the "100% institutionally managed" tagline, though that matters. It's the combination of global expertise and local execution, patient capital and aggressive growth, conservative leverage and bold acquisitions. While competitors chose sides—Embassy went all-in on Bangalore, Mindspace focused on integrated districts—Brookfield built a diversified platform that could weather any storm.

The governance structure sets them apart. With independent directors, institutional sponsors, and transparent reporting, Brookfield brought Wall Street standards to Dalal Street. This isn't just about compliance; it's about building trust with global investors who've been burned by emerging market governance failures.

Lessons for international investors entering emerging markets:

First, partner with locals but maintain control. The Bharti partnership brought political capital and local credibility, but Brookfield kept operational control. Second, build for the long term. The seven-year journey from first acquisition to market leadership wasn't luck—it was patient capital at work. Third, bring global standards but adapt to local realities. Brookfield's buildings meet international specifications, but the business model adapts to Indian payment terms, regulatory requirements, and cultural preferences.

The future of REITs in India:

We're still in the first innings. With only four listed REITs controlling less than 200 million square feet, and total Grade-A stock of 700 million square feet, the consolidation opportunity is massive. As regulations evolve to allow residential, retail, and infrastructure REITs, the market could reach $100 billion by 2030.

The democratization of real estate investment is just beginning. Today's minimum investment of ₹50,000 will eventually drop to ₹10,000 or lower. Fractional investing through digital platforms will make REITs accessible to millions of retail investors. The day when a software engineer in Bangalore can own a piece of the building they work in isn't far.

Final reflections on building institutional real estate platforms:

Real estate, ultimately, is about creating spaces where human potential is realized. Brookfield's offices aren't just concrete and glass; they're where code is written that powers global banks, where strategies are crafted that transform industries, where innovations are developed that improve millions of lives.

The financial success—the ₹19,100 crore market cap, the 6.7% distribution yield, the institutional investor validation—is the outcome, not the purpose. The purpose is building infrastructure for India's inevitable emergence as a global economic power.

When historians look back at India's economic transformation, they'll mark certain inflection points: the 1991 liberalization, the 2000s IT boom, the 2010s digital revolution. The 2020s will be remembered as when India's real estate institutionalized, when global standards met local ambition, when REITs transformed from financial instruments to nation-building tools.

Brookfield India REIT isn't just a success story; it's a template. A template for how patient capital, operational excellence, and strategic vision can transform not just companies but entire industries. A template for how global expertise and local execution can create value that transcends financial returns.

As India stands at the cusp of its demographic dividend, with 600 million people under 25 and ambitions to become a $10 trillion economy, the need for institutional real estate has never been greater. Brookfield has shown the way. The question isn't whether others will follow, but how quickly, and whether they can match the standard that's been set.

The Brookfield story in India is far from over. In many ways, it's just beginning. The foundations have been laid, the platform built, the credibility established. Now comes the exciting part: scaling to meet India's ambitions, innovating to solve emerging challenges, and creating value that compounds not just financially but socially.

For investors, Brookfield India REIT represents a rare opportunity: exposure to India's structural growth story through an institutionally managed vehicle with global standards and local expertise. For India, it represents something more: proof that world-class infrastructure isn't just an aspiration but an achievable reality.

The journey from zero to ₹19,100 crore in seven years is impressive. The journey to ₹100,000 crore in the next seven years isn't just possible—given India's trajectory and Brookfield's track record—it might be inevitable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube