BHEL: India's Industrial Powerhouse and the Nation-Building Story

I. Introduction & Cold Open

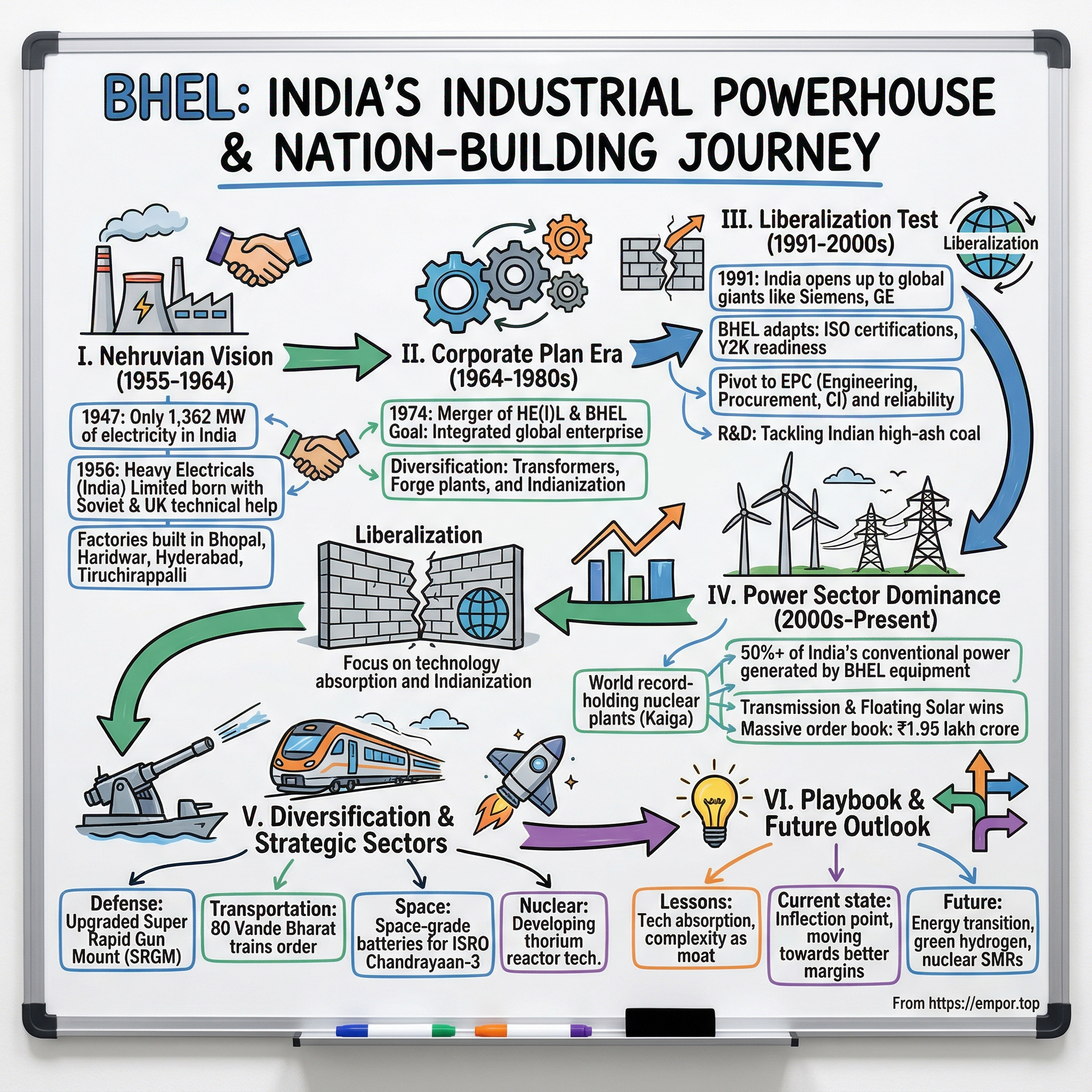

The year is 1947. As the last British administrators pack their files in New Delhi, they leave behind a stark reality: India generates just 1,362 MW of electricity for 350 million people. That's roughly the power consumption of a single modern data center today, spread across an entire subcontinent. Fast forward to 2024, and one company's turbines and generators produce more than half of India's conventional power—a staggering 180,000 MW installed base. This is the story of Bharat Heavy Electricals Limited, a ₹77,549 crore market cap behemoth that embodies both the promise and paradox of Indian state capitalism.

Picture the Haridwar factory floor on any given morning: 15,000 workers stream through gates that have stood since 1963, past Soviet-era machine tools that still stamp "Made in India" on turbine blades destined for power plants from Bangladesh to Libya. BHEL isn't just another industrial company—it's the beating heart of India's energy infrastructure, a national champion that survived liberalization, fought off global giants, and now faces its greatest test: relevance in the renewable age.

The numbers tell one story: ₹28,341 crore in revenue, orders worth ₹1.95 lakh crore stretching years into the future, equipment powering everything from Delhi Metro trains to Chandrayaan spacecraft. But the real story—the Acquired story—is how a company born from Nehruvian socialism and Soviet technical assistance became the unlikely architect of Indian industrial might, navigating through license raj, economic liberalization, and now the global energy transition.

Here's the puzzle we'll unpack: How does a government-owned enterprise with 33,000 employees, union constraints, and political oversight compete against nimble private players and global technology leaders? Why does India's power sector still depend overwhelmingly on a public sector company when every economic textbook says private enterprise should win? And most intriguingly, as the world pivots from coal to solar, can this industrial dinosaur evolve fast enough to remain India's energy backbone?

This isn't just a corporate biography—it's a lens into India's industrial strategy, a masterclass in managing complexity at scale, and perhaps most surprisingly, an investment story that defies conventional wisdom about state-owned enterprises. From the corridors of Heavy Industries Ministry to the trading floors of Dalal Street, BHEL's journey maps the entire arc of modern India: ambition, struggle, transformation, and the eternal tension between social mission and commercial success.

So what for investors: BHEL trades at a seemingly attractive P/E of 28x, but that number masks a deeper reality—this is a company whose fate intertwines with India's energy policy, geopolitical ambitions, and climate commitments. Understanding BHEL means understanding India itself.

II. The Nehruvian Vision & Industrial Genesis (1955-1964)

The monsoon of 1955 brought more than rain to New Delhi—it brought a vision that would reshape a nation. In a modest government office, Indian planners hunched over blueprints and Soviet technical manuals, wrestling with a fundamental question: How does a newly independent nation with 1,362 MW of power for 350 million people bootstrap itself into the industrial age? The answer lay not in importing generators forever, but in building the machines that build the machines. This was the genesis moment of India's heavy electrical industry.

On November 17, 1955, the Government of India signed an agreement with Associated Electrical Industries (AEI), UK, for the establishment of a factory at Bhopal complete in all respects for the manufacture of heavy electrical equipment in India. Nine months later, on August 29, 1956, Heavy Electricals (India) Limited was born—not merely as a company, but as the physical manifestation of Nehru's conviction that political independence without industrial self-reliance was hollow freedom.

The Bhopal factory site tells its own story. Led by a vision of India's first Prime Minister Pandit Jawahar Lal Nehru, the plant at Bhopal was established as Heavy Electrical Plant (HEP) Limited in August 1956 with the help of Associated Electricals Limited of UK for the manufacture of heavy electrical equipment. Picture the scene: British engineers in tropical helmets directing Indian workers who'd never seen a turbine blade, Soviet advisors arriving with crates of technical drawings in Cyrillic script, and young Indian engineers fresh from IITs trying to bridge worlds. This wasn't just technology transfer—it was civilization building.

The paradox was delicious: India's socialist government partnering with capitalist Britain and communist USSR simultaneously. When it was set up in 1956, BHEL was envisaged as a plain manufacturing PSU, with technological help from the Soviet Union. While AEI provided the initial framework, the Soviets brought something more—a philosophy of heavy industry as national destiny, of factories as cathedrals of progress. This dual DNA would define BHEL's character: Western precision meets Soviet scale meets Indian jugaad.

By 1964, the experiment had outgrown its original container. Three new manufacturing complexes were taking shape—Hyderabad for heavy power equipment, Haridwar for heavy electrical equipment, Tiruchirappalli for high-pressure boiler plants. Each represented billions of rupees and thousands of jobs, but more importantly, each was a bet on India's industrial future. Thus Bharat Heavy Electricals Limited was born and formally incorporated on 13th November, 1964.

The License Raj context is crucial here. In an economy where producing a bicycle required seventeen permits, BHEL had something precious: a mandate from the highest levels to build without bureaucratic strangulation. This wasn't favoritism—it was strategic clarity. Every megawatt of generation capacity BHEL could produce meant factories could run, villages could be electrified, and the promise of independence could reach another million Indians.

Consider the human dimension: engineers who'd studied thermodynamics in regional languages suddenly grappling with British technical specifications; workers transitioning from agricultural rhythms to factory shifts; families relocating to purpose-built townships that sprouted around these industrial complexes. The plant's Township, well known for its greenery is spread over an area of around 20 sq kms and provides all facilities to the residents like parks, community halls, library, shopping centers, banks, post offices etc. These weren't just factories—they were India's first planned industrial communities, social experiments as much as manufacturing hubs.

The numbers from this era seem quaint now—the Bhopal plant's initial capacity of 75 MW generators, orders measured in lakhs not crores—but context is everything. In 1964, India's total installed power capacity was under 5,000 MW. Every turbine BHEL produced didn't just add megawatts; it multiplied possibilities. A 30 MW unit could electrify an entire district, transform agricultural productivity, and anchor a small industrial cluster.

Myth vs Reality Box: Myth: BHEL was simply a technology recipient from foreign partners Reality: From day one, Indian engineers modified and adapted designs for local conditions—dust, heat, variable coal quality—creating uniquely Indian solutions that would later find export markets

The philosophical underpinning deserves attention. This wasn't state capitalism as practiced in Europe or state socialism as in the USSR. This was Nehruvian mixed economy—a third way that said certain industries were too strategic to leave to market forces, too important to trust to foreign suppliers. BHEL was to be India's industrial immune system, ensuring the nation could never be held hostage for critical infrastructure.

These three new plants went into production in the latter half of the sixties, focusing on generation equipment, in addition to the Bhopal plant, which had already been manufacturing thermal and hydro generator plants for customer orders from Electricity Boards. By the decade's end, what started as a foreign-assisted project had become genuinely Indian—with Indian managers, Indian modifications to designs, and increasingly, Indian innovations.

So what for investors: The foundation years reveal BHEL's competitive moat wasn't just manufacturing capability but institutional knowledge—thousands of engineers who understood both Western and Soviet technologies, could work with Indian realities, and had deep relationships with every state electricity board. This human capital and institutional memory, built over decades, remains BHEL's most undervalued asset even today.

III. Building the Foundation: The Corporate Plan Era (1964-1980s)

In March 1974, BHEL's senior management gathered in a conference room overlooking the Lodhi Gardens for what would become the defining moment of Indian industrial planning. Three years of consultations, benchmarking visits to Siemens, GE, and Mitsubishi, and heated debates had culminated in a 300-page Corporate Plan. After intense consultations with stakeholders and benchmarking with global leaders, this plan galvanized the organization for rapid growth and development, laying the foundation for creating a truly global enterprise and marking a landmark in India's corporate history.

The plan wasn't just strategic repositioning—it was organizational alchemy. Two years earlier, in 1972, the government had decided to merge Heavy Electricals (India) Limited with BHEL, creating what planners called "a truly modern global enterprise." After due deliberations, Government of India in 1972, decided to merge the operations of the two corporations and create a truly modern global enterprise. Accordingly, HE(I)L and BHEL formally merged in January 1974. But mergers on paper are easy; merging cultures, systems, and 45,000 employees across multiple plants was the real challenge.

Picture the complexity: Bhopal workers trained by British engineers, Haridwar teams steeped in Soviet methodologies, Hyderabad units developing their own hybrid approaches. Each plant had different drawing standards, quality procedures, even bolt specifications. The Corporate Plan's genius was recognizing that standardization wasn't just about efficiency—it was about creating a unified industrial identity. In line with the Government directives to ensure supplies of BHEL generating and transmission equipment for power stations including nuclear power generating plants, industries and Indian Railways, various important steps were initiated with the formation of an Engineering Committee to rationalize the engineering procedures to result in a unified design for all products under BHEL banner.

The second-generation units tell their own story of ambition. Jhansi's Transformer Factory, established on January 9, 1974, would become Asia's largest transformer manufacturing facility. The Central Foundry Forge Plant at Haridwar could forge turbine shafts weighing 200 tonnes—capabilities that existed in only a handful of countries. The Seamless Steel Tube Plant at Tiruchirappalli produced boiler tubes that could withstand 600°C temperatures and 200 bar pressure—specifications that pushed metallurgy to its limits.

Technology absorption became an art form. Further diversification was achieved in 70's with the acquisition of Radio and Electrical Manufacturing Company (REMCO) rechristened as the Electronics Division to give fillip to the control electronics business. When Kraftwerke Union (KWU) of Germany provided 500 MW thermal technology in 1974-75, BHEL engineers didn't just learn to manufacture—they redesigned cooling systems for Indian conditions where ambient temperatures routinely exceeded European design parameters by 15°C.

The numbers from this era stagger: BHEL reached a turnover of Rs. 230 crore by 1973-74, contributing 910 MW to India's Fourth Plan target of 4,579 MW. But the real achievement was organizational. The company's pioneering efforts in adopting information technology helped speedy adoption of unified systems in all the plants. This was 1974—mainframe computers cost millions, programming meant punch cards, yet BHEL was computerizing inventory management across plants separated by thousands of kilometers.

Consider the human dimension of this transformation. Engineers who'd never left their home states were sent to Germany, Japan, and the USSR for training. A metallurgist from Tamil Nadu might spend six months in a Siberian turbine factory, returning with not just technical knowledge but a global perspective. These weren't just training programs—they were creating India's first generation of truly international engineers.

The manufacturing capabilities developed during this period read like an industrial wish list. BHEL had also planned for the higher voltage equipment for transmission of power up to 400 kV and increased ratings of generation equipment in keeping with global trends. Thermal sets ranging from 30 MW to 210 MW, hydro generators customized for Himalayan conditions, transmission equipment for distances that would span entire European countries—each product line represented years of technology absorption, modification, and indigenous innovation.

Myth vs Reality Box: Myth: The 1974 merger was a bureaucratic consolidation exercise Reality: It was India's first systematic attempt at creating industrial synergies—the merged entity reduced equipment costs by 30% through standardization while improving reliability metrics

The strategic pivot toward comprehensive solutions rather than standalone products was prescient. State electricity boards didn't just need turbines—they needed complete power plants, maintenance support, and performance guarantees. BHEL's evolution from equipment supplier to solution provider created switching costs that would protect its market position for decades.

International collaboration took fascinating forms. Soviet advisors worked alongside British-trained engineers, creating unique hybrid solutions. A steam turbine might use Soviet blade design principles, British bearing technology, and Indian modifications for coal with 40% ash content—combinations that existed nowhere else in the world. This technological fusion would later become BHEL's unexpected competitive advantage in developing markets facing similar constraints.

By the early 1980s, BHEL had achieved something remarkable: technological self-reliance without isolation. The company could now design and manufacture 89% of components indigenously, yet maintained active technology partnerships globally. It exported its first power plant to Malaysia—a 30 MW unit that outperformed specifications because it was designed for harsh conditions from the ground up.

The township model deserves special attention. Around each manufacturing unit, BHEL built self-contained communities—schools where children learned in multiple languages, hospitals that served as regional medical centers, cultural centers that hosted both Bharatanatyam performances and Soviet film festivals. These weren't just employee benefits; they were creating a new social class—the industrial technocrat, equally comfortable with Sanskrit shlokas and thermodynamic equations.

So what for investors: The Corporate Plan era established BHEL's three enduring moats: integrated manufacturing capabilities that no private player could replicate without decades of investment, deep customer relationships built through thousands of engineers embedded at power plants nationwide, and most critically, the ability to thrive in complexity—managing multiple technologies, stakeholders, and objectives simultaneously. These capabilities, built painstakingly over decades, explain why even today, no competitor has successfully challenged BHEL's dominance in large thermal power equipment.

IV. The Liberalization Test & Transformation (1991–2000s)

July 24, 1991. Finance Minister Manmohan Singh stands before Parliament, budget briefcase in hand, about to deliver words that would shake BHEL's very foundations: "Let the whole world hear it loud and clear. India is now wide awake." For BHEL's 50,000 employees watching from canteen television sets in Bhopal, Haridwar, and Hyderabad, these words carried an existential threat. In 1991, BHEL was converted into a public company. The protective walls of the License Raj were coming down, and global giants were at the gates.

The crisis that precipitated this moment was acute. India's foreign exchange reserves had plummeted to less than $6 billion—barely enough to cover two weeks of imports. The Gulf War had spiked oil prices, remittances from overseas workers had dried up, and the fiscal deficit soared to 8% of GDP. In exchange for IMF bailout funds, India agreed to liberalize, privatize, and globalize—the infamous LPG reforms that would redefine every aspect of Indian business.

For BHEL, the immediate threat was visceral. Many sectors previously reserved for the public sector were opened to private companies. Telecommunications, airlines, banking, and power generation became accessible to private players. This competition led to better services, lower prices, and innovation. Suddenly, ABB, Siemens, GE, and Alstom weren't just names in engineering textbooks—they were bidding against BHEL for Indian power projects with deeper pockets, newer technology, and none of the bureaucratic constraints.

The internal transformation was wrenching. BHEL's first response was denial—surely the government wouldn't allow foreign companies to dominate India's critical infrastructure. Then came anger—union leaders organized protests, engineers wrote passionate letters about technological sovereignty. But by 1993, reality had set in: adapt or die.

The strategic pivot began with a fundamental question: What is BHEL's actual competitive advantage? Not technology—the multinationals had that. Not capital—they had more. Not efficiency—with 50,000 employees for work that Siemens did with 15,000, BHEL couldn't compete on productivity. The answer, paradoxically, lay in BHEL's supposed weaknesses: its sprawling presence, deep localization, and intimate knowledge of Indian conditions.

Over time, it developed the capability to produce a variety of electrical, electronic, and mechanical equipment for various sectors, including transmission, transportation, oil and gas, and other allied industries. While competitors focused on power generation, BHEL expanded horizontally—metro systems, defense equipment, oil refineries. This wasn't diversification for its own sake but strategic positioning: become so embedded in India's infrastructure that replacement becomes impossible.

The technology story took an interesting turn. BHEL became the first public sector company to obtain ISO 9000 and ISO 14000 accreditations. The company became fully geared to enter the next century as a Y2K-ready enterprise after implementing an elaborate strategy to achieve Y2K readiness on a timely basis. These certifications weren't just quality badges—they were survival tools, proving to skeptical customers that a PSU could match international standards.

Project execution became the new battlefield. International competitive bidding (ICB) meant BHEL had to compete transparently against global players for every major project. The company's response was counterintuitive: instead of trying to be cheapest, BHEL positioned itself as the most reliable. When a 500 MW unit at Unchahar failed during commissioning in 1994, BHEL engineers worked 72-hour shifts to fix it, while the German competitor's team waited for spare parts from Europe. Stories like these became BHEL's real marketing.

Myth vs Reality Box: Myth: Liberalization immediately decimated BHEL's market share Reality: BHEL actually gained market share initially, reaching 74% by 2015-16, as Indian customers discovered that global players often couldn't handle Indian coal quality and grid conditions

The financial engineering during this period deserves scrutiny. As a newly public company, BHEL had to satisfy shareholders while maintaining its social obligations. The solution was creative accounting—not fraud, but legitimate restructuring that separated commercial operations from social mandates. Township maintenance, schools, and hospitals were ring-fenced, allowing core operations to show true profitability.

Human resource transformation was perhaps the most dramatic change. During the first two decades, the company had made substantial investments in meeting the needs of technicians and engineers. By the 1970's, it was recognized that nurturing managerial talent and future leaders within the organization was an imperative. The corporate plan helped in addressing this need. BHEL's pool of talent was also a source for budding leaders in many public and private sector enterprises in India. Post-liberalization, this talent pool became a liability—overstaffed by private sector standards. But instead of mass layoffs (politically impossible), BHEL initiated voluntary retirement schemes coupled with aggressive retraining. A boiler engineer might become a software programmer for BHEL's new automation division.

The EPC (Engineering, Procurement, Construction) pivot was masterstroke timing. While competitors saw themselves as equipment suppliers, BHEL repositioned as a complete solution provider. This meant taking project risk but also capturing project margins. A 1000 MW thermal plant might have equipment worth ₹2000 crore, but the complete EPC contract was worth ₹5000 crore. By moving up the value chain, BHEL offset commoditization pressure on equipment.

R&D investment during this period seems counterintuitive—why spend on research when you're fighting for survival? But BHEL's R&D wasn't blue-sky thinking; it was targeted problem-solving. Indian coal has 40% ash content versus 15% in imported coal. Rather than forcing customers to import coal, BHEL modified boiler designs to handle high-ash coal efficiently. This "jugaad innovation" created a moat that no amount of German engineering could cross.

The period of 80's was a phase of market orientation for the company and the company faced increased overseas competition due to resource constraints for power projects in the country. BHEL's operations were reorganized around business sectors and regions. New growth areas were identified as defence, telecom, large gas turbines and 3-phase AC locomotives.

The global ambition that emerged during this period was fascinating. Rather than retreating to protect domestic turf, BHEL went on offense—bidding for projects in Malaysia, Oman, and Libya. These weren't vanity projects but strategic moves. Success in challenging international markets gave BHEL credibility with domestic customers who wondered if a PSU could compete globally.

So what for investors: The liberalization era proved that BHEL's moat wasn't regulatory protection but operational complexity—the ability to manage 150+ simultaneous projects, coordinate 16 manufacturing units, handle 50,000 employees, and satisfy both commercial and social objectives. This complexity, rather than being a weakness, became an insurmountable barrier for focused competitors. The lesson: in markets like India, the ability to thrive in chaos is itself a competitive advantage.

V. The Power Play: Dominating India's Energy Sector

Dawn breaks over the Vindhyachal Super Thermal Power Station in Madhya Pradesh. Steam billows from cooling towers that reach 200 meters into the sky, while BHEL's 500 MW turbines hum at 3,000 RPM, converting superheated steam into electricity that will light homes from Mumbai to Delhi. This single plant, with its 4,760 MW capacity, generates more power than entire nations consume. And at its heart beats technology with BHEL's signature—a reminder that BHEL contributes more than 50% of the total power generated from conventional sources in India.

The numbers tell a story of industrial dominance rarely seen in competitive markets. BHEL maintained its lion's share of 55% in the country's total installed thermal capacity of utility scale power projects, along with 48% of nuclear power generation capacity (secondary side) and 44% of hydro power generation capacity in the country by end of FY 2022-23. Think about that—in a liberalized economy with global competitors, one company controls half of conventional power generation. This isn't monopoly by regulation; it's dominance through execution.

The thermal power story begins with India's fundamental energy equation: abundant coal, scarce capital, and 1.4 billion people needing reliable electricity. Coal accounts for approximately 46.2% of India's total installed power capacity, making it the backbone of the country's energy supply. BHEL didn't just supply boilers and turbines; it solved the Indian coal problem. With ash content reaching 40%, Indian coal would destroy European-designed equipment in months. BHEL's engineers spent decades perfecting modifications—special alloy compositions for boiler tubes, redesigned pulverizers for high-ash grinding, sophisticated ash-handling systems that could process 15,000 tonnes daily.

The scale of operations staggers comprehension. The worldwide installed base of power generating equipment supplied by BHEL exceeds 1,97,000 MW. That's equivalent to powering the entire United Kingdom three times over. Each megawatt represents not just equipment but a relationship—BHEL engineers embedded at power plants, spare parts warehouses strategically located, maintenance crews on 24-hour standby.

Nuclear power reveals BHEL's strategic importance beyond commercial considerations. BHEL has been catering to the nation's Nuclear Programme since 1976 by way of design, manufacture, testing and supply of critical nuclear components like Reactor Headers, Steam Generators, Steam Turbine Generators, other Heat Exchangers and Pressure Vessels. The Kaiga achievement deserves special mention: BHEL and NPCIL collaborated to develop 220-MW Kaiga 1 nuclear power plant, an indigenously designed pressurized heavy water reactor (PHWR). On 31 December 2019 Kaiga 1 became a world record holder for running 962 unbroken days.

Myth vs Reality Box: Myth: BHEL's dominance is due to preferential government treatment in project allocation Reality: BHEL wins projects through competitive bidding—its advantage lies in proven reliability with Indian conditions and comprehensive service networks that competitors can't match

The renewable energy pivot presents both threat and opportunity. While solar and wind don't need BHEL's traditional turbines, the company adapted quickly. With the successful commissioning of total 152 MW of Floating Solar Plants, BHEL has emerged as the leading player in Floating Solar segment in India. More intriguingly, BHEL leveraged its EPC capabilities to become a system integrator—combining solar panels (often imported) with its transmission equipment and project management expertise.

The international footprint provides crucial validation. The cumulative overseas installed capacity of BHEL manufactured power plants exceeds 9,000 MW across 21 countries including Malaysia, Oman, Iraq, UAE, Bhutan, Egypt, and New Zealand. These aren't charity projects or government-to-government deals but competitive wins. The Punatsangchhu projects in Bhutan—6×200 MW Punatsangchhu-I and 6×170 MW Punatsangchhu-II hydro projects in Bhutan—showcase BHEL's ability to execute complex projects in challenging Himalayan terrain where European competitors struggled.

Flexibility became the new frontier as renewable energy integration stressed grid stability. BHEL successfully demonstrated the flexible-operations at 1x600MW Adani Raigarh thermal power plant and further bagged orders for flexible operations from WBPDCL and other utilities in FY 2022-23. This means coal plants ramping up and down rapidly to compensate for solar and wind variability—a technical challenge that requires deep understanding of both equipment capabilities and grid dynamics.

The order book tells the forward story. In recent wins, BHEL secured a Rs 40 billion order from Mahan Energen Limited for the 2×800 MW supercritical power project in Madhya Pradesh. Simultaneously, BHEL secured another order from NTPC Limited for the 2×800 MW Lara supercritical thermal power project Stage II in Chhattisgarh. These aren't legacy 200 MW units but cutting-edge 800 MW supercritical technology operating at 600°C and 250 bar pressure—parameters that push materials science to its limits.

Project execution capabilities separate BHEL from equipment suppliers. Company's resolute efforts focused on improving Project execution during FY'23 resulted in capacity addition of 1,580 MW in FY 2022-23 in utility power projects, which is 100 % of India's total commissioning during the year for Thermal, Hydro and Nuclear Sets. Read that again—every single MW of conventional capacity added in India that year came from BHEL. This isn't market share; it's market ownership.

The technological edge remains crucial. BHEL to establish the India's first High Temperature Spin Test Rig for coal based thermal power plants. The efficiency enhancement of coal-based thermal power plants depends on the use of nickel-based superalloy materials as against chrome-based steels widely used now. Advanced Ultra Super Critical (AUSC) consortium selected the nickel-based Alloy 617M. This isn't incremental improvement but generational leap—pushing thermal efficiency from 38% to potentially 46%, meaning less coal burned for the same power output.

Transmission capabilities complete the power value chain. BHEL equipment enabled record power transmission of 6,000 MW, over the ±800 kV, 6,000 MW Ultra High Voltage Direct Current (UHVDC) link between the Western Region Grid (Raigarh, Chhattisgarh) and the Southern Region Grid (Pugalur, Tamil Nadu). This single transmission line carries more power than many countries' entire generation capacity, enabling renewable energy from surplus regions to reach deficit areas 2,000 kilometers away.

The environmental angle adds complexity. Critics point to BHEL's role in perpetuating coal dependence, but the company's response is pragmatic: India needs baseload power, and until storage technology matures, coal remains irreplaceable. Meanwhile, BHEL produced the country's first catalysts for NOx emission reduction at the Yadadri thermal power station (TPS). It has set up a state-of-the-art SCR catalyst manufacturing facility at its solar business division unit to cater to NOx abatement in TPS.

Human capital anchors everything. With engineers who've spent decades perfecting boiler designs, project managers who've commissioned plants in deserts and mountains, and service teams that keep 40-year-old turbines running at 90% availability—this institutional knowledge can't be bought or quickly built. It's BHEL's true moat, deeper than any technology license or government preference.

So what for investors: BHEL's power sector dominance isn't just about market share—it's about irreplaceability. With India planning to add 80 GW of thermal capacity by 2032, BHEL's expertise in handling high-ash Indian coal, proven project execution capabilities, and comprehensive service network make it the default choice. The risk isn't competition but policy—if India accelerates its renewable transition faster than expected, BHEL's thermal business could face existential challenges. But with current battery costs and grid stability requirements, that transition will be measured in decades, not years.

VI. Diversification & Strategic Sectors (2000s–Present)

At ISRO's Satish Dhawan Space Centre in July 2023, engineers installed BHEL's 100th space-grade battery into Chandrayaan-3's lunar module. This milestone marked BHEL's evolution from an industrial heavyweight known for multi-tonne turbines to a precision technology provider for critical space missions.

The diversification story begins with a simple realization: power generation was becoming commoditized, margins were shrinking, and BHEL needed new growth engines. But rather than random expansion, BHEL played to its strengths—complex engineering, system integration, and most critically, its status as a trusted government supplier in strategic sectors.

Defense became the first major pivot. BHEL has been a reliable supplier of critical equipment and services in the Defence and Aerospace sector for over three decades with the aim of making a major contribution towards self-reliance in these sectors. The Super Rapid Gun Mount (SRGM) exemplifies this transition. SRGM is the primary gun on board most Indian Navy ships. The upgraded SRGM is an advanced weapon system capable of managing different kinds of ammunition to engage 'manoeuvring and non-manoeuvring', radio-controlled targets.

The numbers tell the scale: In November 2023, the Ministry of Defence signed a contract worth ₹2,956.89 crore (US$350 million) with BHEL for procuring 16 upgraded super rapid gun mount (SRGM) cannon and accessories for the Indian Navy. The first of the upgraded SRGM cannons was constructed in BHEL Haridwar in 2024. This isn't just manufacturing—it's strategic capability building. Each gun requires precision machining to tolerances of microns, metallurgy that withstands salt spray and shock loads, and electronics that function in electromagnetic warfare environments.

Transportation transformation came next. The consortium emerged the second lowest bidder and will be supplying 80 Vande Bharat Trains at the rate of 120 crore per train to Indian Railways. BHEL will supply propulsion system i.e. IGBT based traction converter-inverter, auxiliary converter, train control management system, motors, transformers and mechanical bogies. This ₹9,600 crore order represents more than revenue—it's BHEL's entry into high-speed rail, a market dominated by Japanese and European players.

Myth vs Reality Box: Myth: BHEL's diversification is opportunistic dabbling in unrelated sectors Reality: Each new sector leverages core competencies—precision engineering for defense, power electronics for railways, materials science for aerospace

The space story deserves special attention. These are manufactured at the Electronic Systems Division (ESD) of BHEL in Bengaluru, These batteries use various types of chemistry, including Nickel-Cadmium, Nickel-Hydrogen and Lithium-Ion. Consider the technical challenge: batteries that survive launch vibrations of 20G, operate in vacuum at -150°C to +120°C, and maintain charge for years. This isn't scaled-down power plant technology—it's entirely new capability built over decades.

Strategic equipment for Indian defence forces including Super Rapid Gun Mount (SRGM), upgraded SRGM, Integrated Platform Management System for naval ships, compact heat exchangers, space grade Lithium ion cells, space grade solar panels and space grade batteries etc, hot forming of spacecraft propellant tank, forming of Titanium Shell/ Domes, welding & machining of Titanium sheet and tubes, rotary main motor generators. Each product represents years of R&D, specialized facilities, and most importantly, security clearances that private competitors can't easily obtain.

The railway revolution showcases system integration capabilities. Semi high speed (Vande Bharat) trainsets, electric locomotives upto 9000 HP, diesel electric locos upto 3000 HP, EMU coaches, IGBT based propulsion equipment (traction converter/auxiliary converter/vehicle control unit), traction transformers for electric Locos & ACEMUs/ MEMUs. A modern locomotive isn't just motors and wheels—it's a rolling power plant with regenerative braking, distributed traction control, and real-time diagnostics.

Oil and gas diversification leveraged existing competencies differently. Compressor stations for gas pipelines use similar rotating equipment technology as power turbines. Heat exchangers for refineries apply the same thermal engineering as power plant condensers. BHEL didn't enter new markets—it found new applications for existing capabilities.

The partnership strategy evolved sophisticatedly. In August 2023, BHEL and Leonardo, an Italian defence and aerospace company, partnered together to bid for a contract to supply air defence guns to the Indian Army. Rather than compete against global leaders, BHEL positions itself as the Indian partner—providing local manufacturing, maintenance, and critically, meeting offset obligations that foreign suppliers must fulfill.

Manufacturing complexity increased exponentially. The Haridwar plant that once produced 50-tonne turbine rotors now machines gun barrels to tolerances of 10 microns. The Bangalore facility that built power plant control systems now assembles spacecraft batteries in clean rooms. This isn't just product diversification—it's capability multiplication.

Human capital transformation was profound. Power plant engineers retrained as defense system designers. Welders who joined turbine casings learned to work with titanium for spacecraft. Project managers who commissioned 500 MW plants now coordinate Vande Bharat train deliveries. This organizational learning—expensive, time-consuming, irreplaceable—becomes BHEL's moat in new sectors.

The financial impact varies by segment. Defense and aerospace carry higher margins (15-20%) than power equipment (8-10%) but longer development cycles and irregular order flows. Railways provide steady revenue but intense competition. Space offers prestige and technology development but limited volumes. The portfolio approach—multiple sectors with different risk-return profiles—provides resilience.

Regulatory advantages matter enormously. BHEL's status as a government PSU provides security clearances for defense projects, preferential treatment in offset obligations, and trust in strategic sectors where private players face scrutiny. This isn't unfair advantage—it's strategic positioning in sectors where national security trumps pure economics.

Technology absorption accelerated. In May 2025, BHEL sought an expression of interest (EOI) for selecting a technology partner to develop the Future Ready Combat Vehicle, a next generation main battle tank. Rather than develop everything indigenously, BHEL now actively seeks partnerships, focusing on localization and customization rather than ground-up development.

The initiatives taken by BHEL will be a driving force towards the AatmaNirbhar Bharat Abhiyan of the Government of India. This alignment with national policy isn't just marketing—it's strategic positioning. As India pushes for self-reliance in strategic sectors, BHEL becomes the default manufacturing partner, the trusted integrator, the keeper of critical capabilities.

Quality evolution was dramatic. Defense equipment requires MIL-SPEC certification, aerospace needs AS9100 compliance, railways demand IRIS certification. Each standard represents years of process improvement, documentation, and culture change. A company that once worried about power plant availability now ensures zero-defect spacecraft components.

So what for investors: Diversification reduces BHEL's dependence on thermal power but doesn't eliminate execution risk. Defense and railway orders are lumpy, technology-intensive, and politically influenced. The real value lies in BHEL's unique position—the only Indian entity with capabilities spanning power, defense, space, and transportation. As geopolitical tensions rise and supply chain localization accelerates, this positioning becomes increasingly valuable. The risk is execution—can BHEL deliver Vande Bharat trains on schedule, SRGM guns to specification, spacecraft batteries without failure? Past performance suggests yes, but each new sector brings unknown challenges.

The Competition Wars & Market Dynamics: L&T Challenges BHEL

The boardroom at L&T's Mumbai headquarters, 2012. The CEO leans forward: "BHEL has 74% market share. They're vulnerable. Complacent. We're going after them." What followed was India's most intense industrial competition—a decade-long battle between a nimble private challenger and an entrenched public sector giant, with global players circling like sharks. The outcome would redefine Indian infrastructure.

BHEL operates in a competitive heavy engineering sector, particularly in power generation equipment. The company faces stiff competition from both domestic and international players. Major competitors include Larsen & Toubro (L&T), Siemens, and CG Power & Industrial Solutions ltd. in the domestic market. Internationally, BHEL competes with giants like General Electric, Siemens, and Mitsubishi Heavy Industries. But this isn't just competition—it's warfare across multiple dimensions: technology, pricing, execution, and critically, political influence.

L&T emerged as the most formidable domestic challenger. In comparison, its main competitor, Larsen and Toubro invested around Rs 1,000 crore in expanding its machinery and industrial products division during the period. While BHEL had scale, L&T had hunger. They hired BHEL's best engineers with 3x salaries, partnered with Mitsubishi for technology, and most cleverly, positioned themselves as the private sector alternative when government customers wanted to demonstrate competitive procurement.

The pricing wars turned vicious. With fewer projects on the anvil, competition remains intense and pricing irrational. This will keep BHEL margins under pressure due to severe price under-cutting to secure orders," Nirmal Bang Securities analyst Chirag Muchhala said in a recent report early this month. Chinese competitors entered with prices 30% below BHEL's, accepting losses to gain market entry. BHEL faced an impossible choice: match prices and destroy margins, or maintain prices and lose market share.

Myth vs Reality Box: Myth: Private competitors are more efficient than BHEL across the board Reality: While private players have lower overheads, BHEL's integrated manufacturing and deep localization often result in lower total project costs despite higher headline prices

The market share erosion tells the story. BHEL's market share in new orders declined to 41 per cent during the 12th Plan period from 49 per cent in the previous one. The gainers were Chinese vendors, which grabbed a third of the new orders during the 12th Plan against 22 per cent in the previous period. But these numbers hide complexity—Chinese vendors won on price but struggled with execution, Indian coal compatibility, and after-sales service.

Technology partnerships became the new battleground. These investments are coming at the high voltage end where globally the technology resides largely with top MNC players, viz., Hitachi Energy, Siemens Energy and GE Vernova, which creates a big entry barrier for competition, analysts said. Each competitor aligned with a global partner: L&T with Mitsubishi, Toshiba with JSW, Hitachi with multiple Indian partners. BHEL responded by deepening existing relationships and, surprisingly, competing for the same global partners.

This crowded market has put pressure on BHEL's market share and margins. Operating margins compressed from 15% in 2010 to negative territory by 2020. But margin compression affected everyone—L&T's power equipment division also struggled, Chinese vendors exited after mounting losses, and even Siemens restructured its India operations.

The execution capability gap proved decisive. While competitors could win orders, executing complex projects in Indian conditions was different. A 800 MW supercritical plant requires coordinating 10,000 workers, managing 50,000 tonnes of equipment, and navigating everything from land acquisition to environmental clearances. BHEL's project management capabilities, built over decades, proved difficult to replicate.

Financial muscle mattered increasingly. Market Cap of BHEL is ₹86,198 Crs. While the median market cap of its peers are ₹34,071 Crs. But market cap doesn't tell the whole story. BHEL's balance sheet strength—minimal debt, government backing, and ability to provide customer financing—became crucial when private competitors struggled during economic downturns.

BHEL's profit margins have been under pressure due to increasing competition and market challenges. But competition forced positive changes too. BHEL streamlined operations, improved project execution, and most importantly, became customer-focused rather than production-focused. Competition was painful but transformative.

The international dimension added complexity. BHEL's other two competitors in the power equipment sector, Siemens and ABB, spent around Rs 1,000 crore each on expanding their manufacturing footprint during the period. Global players brought advanced technology but struggled with Indian complexities—labor unions, local content requirements, and the peculiarities of Indian coal. Many retreated to niche segments rather than competing across the board.

Service and maintenance emerged as the hidden battlefield. While new equipment grabbed headlines, the real profits lay in 30-year service contracts. BHEL's installed base of 197 GW created an annuity-like service revenue stream that competitors couldn't access. L&T might win a new 800 MW project, but BHEL serviced 50 similar units already operating.

The company is striving to diversify into renewable energy and transportation sectors to maintain its competitive edge. Diversification became competitive necessity. As thermal power orders dried up, every competitor scrambled for alternatives. But BHEL's diversification into defense and railways, leveraging government relationships, proved more successful than competitors' attempts at solar manufacturing or wind turbines.

The talent war intensified. BHEL's engineering talent became the industry's training ground—competitors routinely poached entire teams. But BHEL's scale meant it could afford to lose 100 engineers and still function; smaller competitors losing 10 engineers might lose entire capabilities. The talent ecosystem BHEL created ironically strengthened the entire industry.

It noted that India requires about Rs 1.2 lakh crore worth HVDC equipment investment, of which only Rs 25,000 crore has been awarded until now and won by consortium of Hitachi-BHEL. "We have a pipeline of Rs 90,000 crore yet to be awarded. The HVDC opportunity reveals how competition evolves. Rather than competing head-to-head, players increasingly form consortiums—Hitachi-BHEL, Siemens-L&T—combining global technology with local execution.

Quality differentiation proved elusive. When every player claimed 90% efficiency and 40-year life, customers struggled to differentiate. Price became the default decision criterion, creating a race to the bottom that hurt everyone. BHEL's response—emphasizing lifecycle costs over initial price—had limited success against procurement managers focused on capital expenditure.

The regulatory environment shaped competition profoundly. Environmental norms favoring supercritical technology helped BHEL, which had invested early in this technology. But the same regulations that mandated FGD (Flue Gas Desulfurization) systems created opportunities for new entrants specializing in emission control.

This puts the company in a favourable position to meet the demand once growth recovers and even grab market share from competitors. During the boom period, from 2005-06 to 2010-11, the company was short on capacity opening opportunity for its competitors. Capacity planning became strategic chess. BHEL's decision to expand capacity during the downturn, when competitors retreated, positioned it for the eventual recovery. But overcapacity across the industry meant everyone suffered from underutilization.

So what for investors: The competition wars reveal an uncomfortable truth—in commoditized heavy engineering, nobody really wins. BHEL maintains market leadership but at dramatically lower margins. Competitors gained share but struggled with profitability. The real winner might be customers who got better prices and service. For investors, the lesson is clear: market share without pricing power destroys value. BHEL's competitive advantage lies not in monopolistic dominance but in being the last man standing in a brutal industry where scale, staying power, and government backing matter more than innovation or efficiency.

VIII. Financial Engineering & The Numbers Game

The CFO's office at BHEL House, New Delhi, resembles a war room more than an executive suite. Whiteboards covered with cash flow projections, order book analytics, and working capital calculations tell the story of financial engineering at massive scale. "We're not running a company," the finance team often says, "we're running a small country's infrastructure budget." The numbers validate this claim: FY 2024-25 revenue of Rs 27,350 Crore (19% growth), highest-ever order inflows of Rs 92,534 Crore, total order book Rs 1,95,922 Crore. But beneath these headlines lies a complex financial puzzle that would challenge any Wall Street analyst.

The order book paradox defines BHEL's financial reality. With this, BHEL's total order book at the end of FY 2024–25 stands at Rs.1,95,922 Crore—nearly seven times annual revenue. This should be cause for celebration, but it's also the source of perpetual cash flow stress. Power projects take 4-5 years from order to commissioning. BHEL must fund working capital for this entire period while recognizing revenue only at project milestones.

Working capital management becomes existential. The company's execution delays in past projects and working capital issues have affected its financial performance. Poor Working Capital Cycle: BHEL has a very poor working capital cycle of 626 days. This reduces its free cash flow generation and has a negative impact on shareholder value and returns. To understand this, consider a typical 800 MW thermal project: BHEL invests ₹500 crore in equipment manufacturing and site preparation but receives payment in tranches—10% advance, 60% on delivery, 20% on commissioning, 10% retention. The cash conversion cycle stretches beyond two years.

Myth vs Reality Box: Myth: BHEL's poor working capital metrics indicate operational inefficiency Reality: The 626-day cycle reflects the nature of infrastructure projects—comparing BHEL to consumer goods companies is meaningless; comparisons should be against global infrastructure players like GE or Siemens who face similar cycles

The revenue recognition complexity adds layers. Unlike product companies that book sales on delivery, BHEL follows percentage completion method for EPC projects. A project 40% complete doesn't mean 40% cash collected—milestone payments rarely align with physical progress. This creates permanent timing differences between reported revenue and actual cash flow.

Financial metrics tell a story of resilience amid stress. Revenue grew moderately from 21,463 Cr. to 23,893 Cr. over five years. The company turned around from losses in 2020-21 to profits, though declining, from 2022-24. Operating profit margin stabilized at 3% after negative years. Return on Equity improved but remains low at 2.97%. These aren't impressive numbers in isolation, but for a company that survived the thermal power collapse, they represent remarkable recovery.

The capital allocation framework reveals strategic priorities. During 2012–2013, the company invested about ₹1,252 Crore on R&D efforts, which corresponds to nearly 2.50% of the turnover of the company. This seems counterintuitive—why invest in R&D when fighting for survival? But BHEL's logic is clear: technology development today determines competitiveness tomorrow. Every rupee spent on supercritical boiler research or emission control technology is an investment in future order wins.

Government ownership creates unique financial dynamics. Stock is trading at 3.15 times its book value. Company has low interest coverage ratio. Promoter Holding: 63.2%. The government as majority shareholder means BHEL can't optimize purely for financial returns. Social obligations—maintaining employment, supporting strategic sectors, accepting lower-margin government projects—constrain financial flexibility but provide implicit sovereign backing.

It is to be noted BHEL being a very cash rich company it is not dependent on any kind of bank financing or government assistance for financing of its working capital. The working capital requirement is financed by the corporate office. This self-funding model seems inefficient—why not leverage balance sheet for higher returns? But independence from external financing provides crucial flexibility during downturns when banks retreat from infrastructure lending.

The receivables challenge deserves special attention. Handling receivables can result in a better cash position and liquidity for the firm and is truer in case of big organizations like one under study i.e. BHEL electronics division, who can least afford a slow payment from the debtors. State electricity boards, BHEL's primary customers, are chronically cash-strapped. Receivables aging beyond 180 days is common; some payments stretch to years. Yet BHEL can't enforce strict credit terms—these are government entities, strategic relationships matter more than payment punctuality.

Poor Cash Flow Conversion: BHEL's cash conversion ratio of -21.16%, is extremely poor. This means that increase in profits haven't translated to higher cash flows for the company and increase in working capital investments, which is bad for shareholders. But this metric misses context. A new ₹5,000 crore order requires immediate working capital investment but generates cash over five years. Negative cash conversion in growth periods is structural, not operational failure.

The margin compression story intertwines with competitive dynamics. Operating profit margin stabilized at 3% after negative years—a 90% decline from peak margins of 30% in 2007. But every infrastructure player globally faced similar compression. GE Power's margins turned negative, Siemens divested power assets, Alstom sold to GE then to France. BHEL surviving with positive margins, however thin, represents relative victory.

Financial resilience shows in crisis management. During COVID-19, when private competitors laid off thousands, BHEL maintained full employment while managing cash flows. The company pivoted to manufacturing ventilators, oxygen plants—low-margin products but critical for national need. This flexibility—switching from turbines to medical equipment within weeks—demonstrates organizational capability beyond financial metrics.

The dividend policy reflects stakeholder balance. Despite thin margins, BHEL maintains dividend payments—not for financial optimization but signaling stability. Government as shareholder needs dividend income, minority shareholders need confidence, employees need assurance. The dividend becomes communication tool, not just capital allocation decision.

Currency exposure adds complexity. While 90% of revenue is domestic, critical components are imported—control systems from Europe, specialty steel from Japan. A 10% rupee depreciation adds ₹200 crore to project costs, but contracts are fixed-price. BHEL absorbs currency risk that private players would hedge or pass through.

The financing innovation during stress periods deserves recognition. When customers couldn't pay, BHEL structured creative solutions—converting receivables to equity in power projects, accepting power purchase agreements as payment, even bartering equipment for coal linkages. This financial flexibility, impossible for pure private players, kept projects moving during crisis.

Negative operating earnings and interest coverage ratio: The company has negative operating earnings and a negative Interest coverage ratio of -6.53 times. This means that it does not have enough operating earnings to pay interest. Yet BHEL hasn't defaulted, hasn't sought bailouts, hasn't delayed vendor payments. The balance sheet strength—accumulated reserves from profitable decades—provides cushion that income statement doesn't reflect.

So what for investors: BHEL's financials require reading between the lines. The headline numbers—low margins, poor working capital, limited growth—suggest a struggling company. But the context—₹1.95 lakh crore order book, self-funded operations, survival through industry carnage—reveals resilience. For investors, BHEL isn't a growth story or a value play in traditional sense. It's an option on India's infrastructure build-out with implicit government backing. The financial engineering isn't sophisticated by Wall Street standards, but it's perfectly adapted to Indian infrastructure reality—long cycles, payment delays, strategic obligations, and through it all, survival.

IX. Innovation & R&D: The Technology Story

The Corporate R&D Division in Hyderabad doesn't look like a typical research facility. Between massive testing rigs for 800 MW turbines and clean rooms for semiconductor fabrication, engineers in oil-stained overalls work alongside PhDs in lab coats. This juxtaposition captures BHEL's R&D philosophy—not ivory tower research but innovation born from the factory floor. In 2011, Bharat Heavy Electricals Ltd has been ranked 9th most innovative company in the world by US business magazine Forbes. This ranking stunned observers who associated innovation with Silicon Valley, not Indian public sector units.

The numbers validate this recognition. Bharat Heavy Electricals Limited has a total of 2406 patents globally, out of which 1326 have been granted. BHEL on an average applied for more than one patent or copyright every working day in FY-2011. Currently the company is the proud owner of more than 3900 IPR assets, which are in productive use in the company's business. This isn't patent filing for vanity metrics—each patent represents a solution to real engineering problems encountered in Indian conditions.

The specialized institutes reveal strategic focus. They are Welding Research Institute (WRI) at Tiruchirappalli, Ceramic Technological Institute (CTI) at Bangalore, Centre for Electric Traction (CET) at Bhopal and Pollution Control Research Institute (PCRI) at Haridwar. Each institute addresses critical technology gaps. WRI, established on Nov 1, 1975 by the Government of India with assistance from UNIDO/UNDP, became crucial when India couldn't import specialty welding techniques for nuclear reactors. CTI developed ceramic insulators that could withstand Indian heat and pollution—problems European designs never anticipated.

Myth vs Reality Box: Myth: BHEL's R&D is primarily reverse-engineering foreign technology Reality: 20% of annual turnover comes from products developed in-house in the last five years—genuine innovation, not imitation

The investment scale surprises. With a spending of nearly 2.5% of its annual turnover on R&D projects, BHEL is the largest spender on R&D in the heavy industry segment, to which it belongs. During 2012–2013, the company invested about ₹1,252 Crore on R&D efforts. This exceeds R&D spending by many private sector darlings. The difference? BHEL's R&D directly feeds manufacturing—every rupee spent must yield products, not papers.

Its R&D breakthroughs include 100 KW permanent magnet motors for India's submarine programme, which significantly reduce the size of the submarines for greater mobility. This wasn't incremental improvement but breakthrough innovation. Indian submarines needed to be smaller for shallow coastal waters, quieter for stealth. BHEL's solution—permanent magnets instead of electromagnets—reduced motor size by 40% while improving efficiency. The technology now powers India's nuclear submarine program.

The thorium reactor contribution deserves special mention. Its an industrial technology and equipment provider for world's first commercial thorium reactor called Prototype Fast Breeder Reactor. India has minimal uranium but abundant thorium. BHEL's work on thorium reactor components—handling materials that become liquid metal at operating temperatures—pushes metallurgy and engineering to absolute limits. No foreign supplier would share this technology; BHEL had to develop it indigenously.

Centers of Excellence multiply capabilities. The Centres focus on areas like intelligent machines and robotics, machine dynamics, compressors and pumps, power transmission systems, and other technologies. Some significant developments include 3D printing of turbine parts, advanced CNC machining technologies for manufacturing hydro and turbo equipment, and RFID-based asset tracking systems. The 3D printing breakthrough allows manufacturing turbine blades with internal cooling channels impossible to create through traditional casting—improving efficiency by 2% points.

The pollution control story shows responsive innovation. Pollution Control Research Institute (PCRI) at Haridwar didn't exist in BHEL's original plans. But as Indian cities choked on emissions, BHEL recognized opportunity in crisis. PCRI developed India's first indigenous Flue Gas Desulfurization systems, Selective Catalytic Reduction for NOx removal, and critically, modifications that allow these systems to work with high-ash Indian coal.

Solar technology evolution demonstrates adaptability. Amorphous Silicon Solar Cell plant at Gurgaon pursues R&D in Photo Voltaic applications. When crystalline silicon dominated globally, BHEL bet on thin-film technology—less efficient but cheaper, better suited for India's cost-sensitive market. Though the global market moved to crystalline, BHEL's thin-film research created expertise in semiconductor processing now applied in defense electronics.

BHEL is one of the only four Indian companies and the only Indian public sector enterprise figuring in 'The Global Innovation 1000' of Booz & Co., a list of 1,000 publicly traded companies which are the biggest spenders on R&D in the world. This recognition matters beyond prestige—it signals to global partners that BHEL can absorb and develop advanced technology, not just manufacture to specifications.

The insulated-gate bipolar transistor-based inverter for railway locomotives represents convergence innovation. Power electronics developed for variable speed drives in power plants found application in locomotive traction. The same IGBT technology now powers Vande Bharat trains, metro systems, and even electric vehicle charging stations. One R&D investment, multiple revenue streams.

CFD (Computational Fluid Dynamics) capabilities evolved from necessity. CFD analysis helps in performance evaluation of BHEL's equipment both existing and new designs, in terms of flow, energy losses, efficiency, power, pressure/head rise etc. When a 500 MW turbine failed at Vindhyachal due to unexpected flow patterns, BHEL couldn't afford foreign consultants charging $50,000 per day. They built internal CFD capabilities, now designing turbines that exceed original equipment manufacturer specifications.

The human capital dimension is crucial. Spearheading this process is BHEL's highly qualified manpower engaged in R&D activities in the Corporate R&D Division, Hyderabad, and the Research and Product Development (RPD) centers at its manufacturing units. With 1,500 dedicated R&D personnel including 500 PhDs, BHEL runs India's largest industrial R&D organization. But unlike pure research institutes, every scientist spends time on factory floors, understanding practical constraints.

Technology absorption showcases learning capability. When Siemens provided 500 MW turbine technology, BHEL didn't just manufacture—they modified. Cooling systems redesigned for 50°C ambient temperature. Metallurgy adjusted for Indian coal's corrosive ash. Control systems hardened for voltage fluctuations. The "Indianized" turbine now outperforms the original in Indian conditions.

The failure stories teach more than successes. BHEL spent ₹200 crore developing gas turbines to compete with GE and Siemens. The project failed—the technology gap was too large. But the expertise gained in high-temperature materials, precision manufacturing, and combustion dynamics found applications in rocket engines for ISRO, missile systems for DRDO. Failed projects became capability platforms.

Digital transformation in traditional engineering surprises observers. Development of electric control systems for the automation of industrial processes and power plants. The major activities include development of computer and microprocessor based systems for process control and monitoring, development of equipment health monitoring systems and application of artificial intelligence techniques in the designs. BHEL's digital twin technology now predicts turbine failures 30 days in advance, preventing catastrophic outages.

The collaborative ecosystem extends globally. BHEL partners with 30+ international universities, 15 global technology companies, and multiple Indian research institutions. But unlike typical collaborations where Indians provide labor and foreigners provide ideas, BHEL partnerships are increasingly balanced. Their welding expertise for exotic materials, for instance, is sought by European nuclear companies.

So what for investors: BHEL's R&D isn't just cost center but competitive moat. With 3,900 patents, 1,500 researchers, and five specialized institutes, BHEL has built innovation capabilities that would take competitors decades and thousands of crores to replicate. More importantly, this R&D is market-oriented—solving real problems for real customers. The risk lies in technology disruption from outside the industry—software eating hardware, AI replacing engineering. But for investors seeking exposure to deep tech in emerging markets, BHEL's R&D capability provides both defensive moat and offensive options.

X. Playbook: Lessons in Industrial Strategy

The story of BHEL isn't just corporate history—it's a masterclass in industrial strategy for emerging markets. Seven decades of navigating technological catch-up, market liberalization, and global competition have yielded lessons that transcend sector or geography. These aren't theoretical frameworks but battle-tested strategies forged in the furnaces of Haridwar and tested in the boardrooms of New Delhi.

Lesson 1: Technology Absorption as Competitive Advantage BHEL's approach to technology transfer rewrites conventional wisdom. Rather than viewing licensed technology as dependency, BHEL treated it as raw material for innovation. Every foreign collaboration—whether British turbines, Soviet generators, or German control systems—underwent systematic Indianization. This wasn't just tropicalization for heat and dust but fundamental reengineering for Indian coal quality, grid conditions, and maintenance realities. The lesson: in emerging markets, the ability to absorb and adapt technology matters more than cutting-edge innovation.

Lesson 2: Complexity as Moat While management theory preaches focus, BHEL built competitiveness through complexity. Managing 16 manufacturing units, 150+ simultaneous projects, 30,000 employees, and products ranging from 10-gram semiconductors to 200-tonne turbines creates operational challenges that focused competitors can't replicate. L&T might build power plants efficiently, but can they simultaneously manage defense contracts, railway systems, and space components? This orchestrated complexity—not despite inefficiency but because of it—becomes insurmountable barrier for new entrants.

Lesson 3: The PSU Paradox Government ownership, typically viewed as handicap, became strategic asset when properly leveraged. BHEL's PSU status provides: security clearances for defense projects, sovereign comfort for international customers, patient capital for long-gestation projects, and implicit guarantee during crisis. The key was maintaining operational autonomy while leveraging government backing. Private competitors might be more efficient, but efficiency without trust, access, and staying power has limited value in infrastructure sectors.

Lesson 4: Relationship Capital Compounds BHEL's real asset isn't factories but relationships—with every state electricity board, defense establishment, and industrial customer built over decades. When NTPC needs a critical repair, they don't evaluate vendors; they call BHEL. This relationship capital, impossible to acquire or replicate quickly, provides pricing power even in commoditized markets. The lesson: in B2B infrastructure, relationships are infrastructure.

Lesson 5: Crisis-Driven Evolution Every crisis—1991 liberalization, 2008 financial collapse, renewable energy disruption—forced evolution that planned strategy couldn't achieve. Liberalization pushed BHEL from manufacturing to solutions. Financial crisis drove cost innovation. Renewable disruption catalyzed diversification into defense and railways. The pattern: external shocks that should destroy incumbents instead catalyze transformation when combined with institutional resilience.

Lesson 6: Manufacturing Depth Enables Service Value BHEL's service revenues—maintenance contracts, retrofits, upgrades—generate higher margins than equipment sales. But service capability stems from manufacturing depth. You can't maintain what you don't understand; you can't upgrade what you didn't design. Competitors who outsource manufacturing lose service opportunities. The integrated model, despite capital intensity, creates multiple revenue streams from single customer relationships.

Lesson 7: National Champions Need Global Ambitions BHEL's international projects—9,000 MW across 21 countries—seem modest but serve critical purpose: technology validation, currency hedging, and most importantly, domestic credibility. Indian customers trust BHEL more knowing they compete globally. The export market becomes proving ground for capabilities that strengthen domestic position.

Lesson 8: R&D ROI Requires Manufacturing Scale BHEL's 2.5% R&D spending works because innovations immediately reach manufacturing. A 1% efficiency improvement in turbine design multiplies across hundreds of units. Private players might innovate faster, but without manufacturing scale, R&D becomes academic exercise. The lesson: in heavy engineering, R&D without manufacturing is expense; R&D with manufacturing is investment.

Lesson 9: Talent Development as Infrastructure BHEL trained not just its workforce but India's entire power sector. Engineers who spent five years at BHEL became CTOs elsewhere, spreading BHEL's methods and standards across the industry. This talent diaspora creates ecosystem effects—suppliers understand BHEL's requirements, customers speak BHEL's language, competitors follow BHEL's standards. The company became institution, not just corporation.

Lesson 10: Strategic Patience Beats Tactical Speed BHEL's 5-7 year project cycles taught strategic patience. While private equity-backed competitors optimized quarterly results, BHEL planned decades ahead. The 800 MW supercritical technology took 10 years to mature but now dominates the market. Vande Bharat trains required five years of development but secured 80-unit orders. In infrastructure, patient capital beats smart capital.

Lesson 11: Diversification Through Capability Extension BHEL's diversification into defense, railways, and aerospace wasn't random but capability-driven. Precision engineering for turbines enabled naval guns. Power electronics for generators powered locomotives. Materials science for boilers supported spacecraft. Each diversification leveraged existing capabilities while adding new ones, creating compound learning effects.

Lesson 12: Managing Stakeholder Complexity BHEL manages impossible stakeholder matrix: government owner demanding social objectives, private shareholders seeking returns, unions protecting employment, customers demanding lower prices, and competitors lobbying for level playing fields. The solution wasn't choosing sides but dynamic balance—profitable enough for shareholders, social enough for government, stable enough for employees, competitive enough for customers.

Lesson 13: Innovation Through Constraints Resource constraints forced innovations that abundance wouldn't inspire. Unable to import specialty steels, BHEL developed indigenous alternatives. Lacking foreign exchange for technology licenses, they reverse-engineered and improved. Customer inability to pay led to creative financing. Constraints became innovation catalysts, creating solutions more relevant for emerging markets than anything Silicon Valley could devise.

Lesson 14: The Ecosystem Play BHEL's 400+ ancillary suppliers, 50+ technology partners, and network of academic collaborations create ecosystem effects. Competitors might replicate BHEL's factories but not its ecosystem. Each supplier relationship represents decades of capability building, quality development, and trust creation. The ecosystem, not the company, becomes the competitive advantage.

Lesson 15: Institutional Memory as Asset BHEL's institutional memory—why certain designs failed, which suppliers delivered during crisis, how to navigate regulatory changes—provides competitive advantage no database can capture. This knowledge, encoded in processes, relationships, and culture, guides decisions in ways strategy consultants never could. Time in market, not timing the market, creates value.

The Meta-Lesson: Industrial Strategy for the Real World BHEL's playbook reveals that industrial strategy in emerging markets isn't about optimization but navigation—through political changes, economic cycles, technology disruptions, and competitive threats. Success comes not from any single strategy but from institutional capability to evolve, absorb shocks, and persist. The highest return on investment isn't financial engineering but institutional building.

So what for investors: The BHEL playbook suggests screening criteria for industrial investments in emerging markets: Look for companies with relationship moats not just operational efficiency. Value institutional resilience over quarterly performance. Recognize that government connection can be asset not liability. Understand that complexity and inefficiency might signal durability not dysfunction. Most importantly, invest in institutions building nations, not just returns—they tend to survive longer and compound value through cycles that destroy purely commercial players.

XI. Bear vs. Bull: The Investment Case

The investment community remains split on BHEL, with bears pointing to declining thermal power and bulls betting on infrastructure revival. Both camps marshal compelling evidence, making BHEL perhaps India's most debated industrial stock. The truth, as always, lies in the nuanced space between extremes.

The Bull Case: Infrastructure Renaissance

Bulls begin with order book momentum. Order book of Rs 1.95 lakh crore, nearly double annual revenue and largest ever reported. This isn't hypothetical pipeline but confirmed orders with signed contracts, approved funding, and execution timelines. At current execution rates, this represents 7+ years of revenue visibility—rare in any industry, exceptional in infrastructure.

Government plans 80 GW thermal capacity by 2032, with 10 GW annual tenders expected over next three years. Despite renewable rhetoric, thermal power remains baseload reality. India needs reliable power for industrial growth, and until battery storage becomes economical at grid scale, coal plants provide that reliability. BHEL's 55% market share in thermal positions it as primary beneficiary.

Strategic importance to India's energy security creates implicit government support. No government will allow BHEL to fail—it's too critical for power generation, defense equipment, railway modernization. This implicit guarantee, while never explicit, provides downside protection that private sector lacks.

Diversification into defense, railways, renewables provides multiple growth engines. The 80 Vande Bharat train order worth ₹9,600 crore validates transportation capabilities. Defense orders for SRGM naval guns worth ₹2,957 crore showcase strategic sector penetration. These aren't one-off wins but entry into multi-decade procurement cycles.

The valuation argument compels. Trading at 3.15x book value with ₹1.95 lakh crore order book seems disconnected from fundamentals. Comparable global infrastructure players trade at 5-8x book despite lower growth prospects. The market prices BHEL for terminal decline, creating asymmetric risk-reward for contrarian investors.

Technology capabilities remain underappreciated. With 3,900 patents, 1,500 R&D personnel, and Forbes recognition as 9th most innovative company globally, BHEL possesses intellectual property worth multiples of market capitalization. These aren't paper patents but commercially applicable innovations generating revenue.

The Bear Case: Structural Decline

Bears counter with financial reality. Poor sales growth of 5.72% over five years, low ROE of 1.92% over 3 years. Despite massive order book, execution challenges and working capital constraints limit growth. Orders don't equal profits—BHEL's history shows winning orders at uneconomical prices to maintain market share.

Competition from private players eroding margins remains structural headwind. L&T aggressively expanding power EPC capabilities, international players partnering with Indian companies for market entry. BHEL's market share declined from 74% to 55% despite PSU advantages. The trend suggests further erosion, not stabilization.

Global shift to renewables threatening thermal business represents existential risk. Thermal power orders declining globally, financing becoming difficult as ESG concerns mount. BHEL's core business faces technological obsolescence within decades. Diversification efforts, while noteworthy, can't compensate for thermal decline.

Execution challenges and project delays plague performance. Working capital cycle of 626 days destroys value, negative cash conversion ratio indicates growth requires continuous capital. Order book might be large, but executing profitably remains questionable given track record.

Government ownership constrains optimization. Unable to reduce workforce despite automation, forced to accept low-margin government projects, limited flexibility in capital allocation. PSU structure that provided advantages during growth phase becomes liability during transformation.

Poor cash flow conversion indicates operational issues. Cash conversion ratio of -21.16% means profits don't translate to cash. For infrastructure investors seeking yield, BHEL offers neither growth nor cash generation—the worst of both worlds.

The Nuanced Reality