BELRISE Industries: The Precision Engineering Champion of India's Auto Revolution

I. Introduction & Episode Roadmap

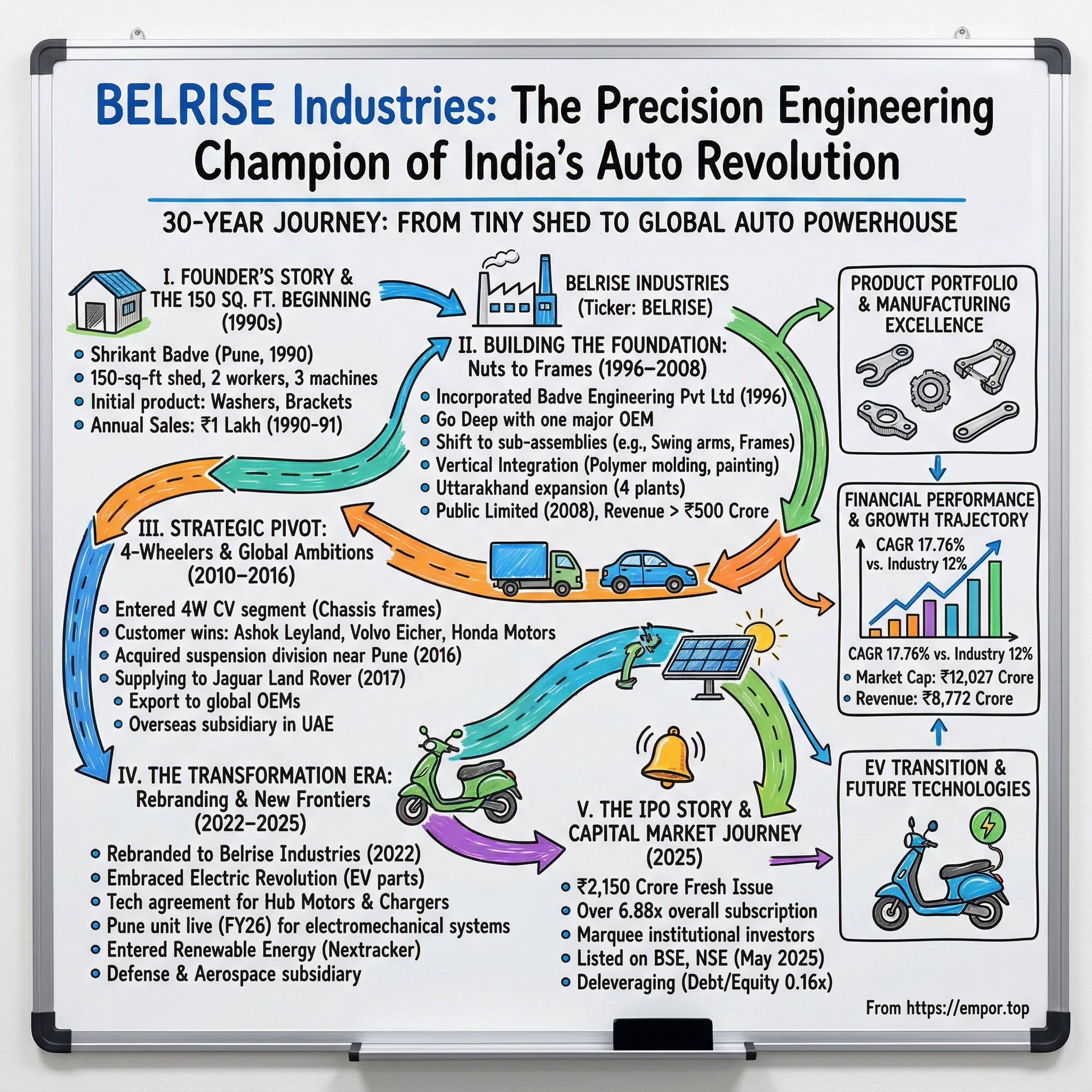

Picture this: A young engineer in 1990s Pune, fresh out of college, walks past gleaming factories he can't afford to rent. Instead of giving up, he finds a 150-square-foot shed—barely larger than a modern parking space—and starts making washers and brackets with two workers and three machines. Annual sales that first year? A mere ₹1 lakh. Fast forward three decades: that shed has transformed into BELRISE Industries, a ₹7,500+ crore automotive component powerhouse that equips one in three Indian two-wheelers with critical frame assemblies.

The story of BELRISE Industries reads like a quintessential post-liberalization Indian manufacturing saga—bootstrap entrepreneurship meeting global ambition at the precise moment when India's automotive sector was about to explode. Founded as Badve Engineering in 1988 by Shrikant Badve, the company has evolved from a micro-enterprise making simple metal parts to a sophisticated Tier-0.5 supplier serving 27 global OEMs across safety-critical systems for two-wheelers, three-wheelers, passenger vehicles, commercial vehicles, and agricultural equipment.

What makes BELRISE fascinating isn't just the scale of transformation—it's the timing and strategic choices. While contemporaries chased quick wins in India's opening economy, Badve played a three-decade game, methodically building capabilities, expanding geographically by following OEM customers, and crucially, transitioning from component supplier to systems integrator. The company now commands a 24% market share in India's two-wheeler metal components segment and has recently expanded into electric vehicle systems, renewable energy components, and even defense technologies. The raw numbers tell only part of the story. With a market capitalization of ₹12,027 crore, revenue of ₹8,772 crore, and profit of ₹396 crore, BELRISE today stands as a testament to patient capital building and strategic transformation. But to understand how a company achieves a 16.4% CAGR versus the industry's 12% over four years, we need to journey back to that cramped shed in 1990s Pune, where an engineer's ambition collided with India's manufacturing destiny.

This episode explores BELRISE's three-decade evolution through multiple lenses: the founder's personal sacrifice and vision, the company's strategic pivots from nuts to frames to systems, its prescient bet on India's two-wheeler boom, and its current navigation of the EV transition. We'll examine how geographic expansion following OEM customers became a growth strategy, how vertical integration created competitive moats, and how a recent IPO marks not an ending but a new chapter in global ambitions.

The journey ahead promises to be as revealing as it is inspiring—a masterclass in building manufacturing excellence in emerging markets, timing market cycles, and transforming family enterprises into institutional powerhouses. Let's begin where all great business stories must: with a founder, a dream, and barely enough space to turn around.

II. Founder's Story & The 150 Square Foot Beginning

The year was 1990, and Shrikant Badve had a problem that would have broken most aspiring entrepreneurs. Fresh from engineering college with dreams of building a manufacturing empire, he discovered that even the smallest industrial units in Pune commanded rents far beyond his means. While his classmates took comfortable jobs with established companies, Badve walked the industrial corridors of Pune and Aurangabad, calculator in hand, realizing his savings wouldn't cover even a month's rent for a proper factory space.

Then he found it: a 150-square-foot shed in an industrial area—roughly the size of a modest bedroom. The owner, skeptical that anyone could run a manufacturing business from such a cramped space, agreed to rent it more out of curiosity than commercial interest. Badve moved in three second-hand machines: a power press, a drilling machine, and a small lathe. He hired two workers, both older than him, who initially questioned whether this young engineer knew what he was doing.

The early days bordered on the absurd. To fit the machines, they had to be arranged so precisely that workers had to exit the shed to let others pass between stations. Raw material had to be stored outside under tarpaulins because there was no room inside. When it rained—and Pune's monsoons are legendary—Badve and his workers would rush to cover the materials, often working through the night to meet delivery deadlines for the simple washers, brackets, and fasteners they produced.

That first year, 1990-91, the company—if you could call it that—generated revenues of barely ₹1 lakh. To put this in perspective, that's less than what a junior engineer at Bajaj Auto or Tata Motors would have earned in salary. But Badve saw something others didn't: India was on the cusp of economic liberalization, and the automotive sector would be its locomotive.

The personal sacrifices were extreme. Unable to afford accommodation in Pune, Badve lived alone in Aurangabad for six years, making the journey to Pune regularly to secure orders. He delayed his marriage, explaining to his future wife's family that the business needed every rupee he could spare. When he finally married in 1996, the wedding was a modest affair—he'd invested the money traditionally spent on celebrations into a new CNC machine instead.

What drove this level of sacrifice? In interviews years later, Badve would describe a vision that seemed laughable at the time: he wanted to build a company that would supply every major vehicle manufacturer in India. "People thought I was crazy," he recalled, "talking about supplying Bajaj and Hero when I couldn't even afford proper factory space." But post-liberalization India was creating opportunities for those willing to endure the early pain.

The breakthrough came in 1994 when a purchasing manager from a local two-wheeler manufacturer visited the shed. The manager had heard about this small operation that never missed a delivery deadline, even if it meant the owner personally carrying finished parts on his scooter to ensure on-time delivery. Impressed by the quality consistency despite the primitive conditions, he placed a small order for specialty brackets. Badve delivered not just on time but with zero defects—a rarity in the small-scale sector.

Word spread in Pune's tight-knit automotive component community. By 1995, the shed had expanded—Badve had convinced the landlord to rent him the adjacent unit, doubling his space to 300 square feet. Revenue crossed ₹10 lakh. He hired three more workers and bought his first new machine. But more importantly, he had begun to earn something more valuable than money: reputation.

The transformation from Shrikant Badve, struggling entrepreneur, to founder of what would become Badve Engineering Private Limited in 1996, wasn't marked by a single moment but by thousands of small victories. Each on-time delivery, each quality certification, each satisfied customer added a brick to the foundation. By the time he incorporated the company formally, he had already built what money couldn't buy: trust in an industry where your reputation was your real capital.

Looking back, those 150 square feet represented more than just physical constraints—they were a crucible that forged the company's core values: extreme customer focus, quality obsession, and the belief that no challenge was insurmountable if you were willing to work harder than everyone else. These values would prove critical as Badve Engineering began its next phase: building the foundation for what would become one of India's most important automotive component manufacturers.

III. Building the Foundation: From Nuts to Frames (1996–2008)

The incorporation of Badve Engineering Private Limited in 1996 coincided with a pivotal moment in Indian automotive history. The economy was five years into liberalization, foreign automakers were establishing Indian operations, and domestic manufacturers were modernizing rapidly to compete. Shrikant Badve, now operating from a proper 5,000-square-foot facility in Aurangabad, sensed that the window for building a serious component business was opening—but it wouldn't stay open forever.

The first strategic decision was counterintuitive: instead of diversifying customers immediately, Badve chose to go deep with a single major two-wheeler OEM. In 1997, when he established the company's first formal manufacturing plant in Aurangabad's Shendra industrial area, the entire facility was dedicated to this one customer. Industry veterans warned him about customer concentration risk. His response? "First prove you can be indispensable to one, then expand to many."

This philosophy paid off spectacularly in 2001 when that same OEM—impressed by four years of flawless execution—asked Badve to set up a dedicated facility for a new product line. This wasn't just another order; it was an invitation to move up the value chain from simple pressed parts to sub-assemblies. The company established its second plant, and revenues jumped from ₹50 lakh to over ₹3 crore in a single year.

But Badve understood that geographic proximity to customers was becoming crucial in the just-in-time manufacturing era. In 2004, he made a bold move: establishing a facility in Ranjangaon, near Pune, despite the significantly higher real estate costs. The location was strategic—it sat at the heart of what was becoming India's Detroit, with Bajaj, Force Motors, and Volkswagen all setting up operations nearby. The Ranjangaon plant specialized in larger, more complex assemblies: swing arms, main frames, and center stands for motorcycles.

The 2004-2005 period marked another crucial evolution: the shift from single-process operations to multi-vertical capabilities. Badve Engineering was no longer just a metal pressing company. It had added polymer molding, specialized foundry operations for aluminum components, and—critically—coating and painting capabilities. This vertical integration meant the company could now offer complete painted and finished assemblies, not just raw pressed parts. The Uttarakhand expansion in 2007 exemplified Badve's follow-the-customer strategy. The company established facilities in Pantnagar, Uttarakhand in 2007—each new facility was not just a dot on the map, but a deliberate push deeper into India's industrial geography. The state government was offering incentives to manufacturers, but more importantly, Hero MotoCorp and Bajaj Auto were establishing major plants there. Badve didn't just open one facility; he eventually established four plants in Pantnagar, creating an integrated manufacturing cluster that could handle everything from raw material to finished painted assemblies.

By 2008, the transformation was complete: Badve Engineering converted from a private limited company to a public limited entity. This wasn't merely a legal formality—it represented a fundamental shift in ambition and governance. The company brought in independent directors, implemented formal audit processes, and began preparing for what would eventually become capital market access. Revenue had crossed ₹500 crore, and the company employed over 2,000 people across seven manufacturing facilities.

The product evolution during this period tells its own story of increasing sophistication. In 1996, the company made simple washers and brackets worth a few rupees each. By 2008, it was manufacturing complete motorcycle main frames—the skeletal structure that holds the entire vehicle together—worth thousands of rupees per unit. The technical leap required was enormous: from single-stage pressing to multi-stage progressive dies, from manual welding to robotic MIG welding, from basic powder coating to sophisticated e-coating and painting lines.

Quality certifications accumulated like badges of honor: ISO 9001 in 1998, QS 9000 in 2001, ISO/TS 16949 in 2003. But the real validation came from customers. By 2008, Badve Engineering was supplying not just to Indian operations of global OEMs but was approved as a global supplier. This meant parts manufactured in Aurangabad could potentially be shipped to assembly plants in Thailand or Brazil—a massive vote of confidence in the company's capabilities.

The financial discipline during this period deserves special mention. Despite rapid expansion, Badve resisted the temptation of excessive leverage. Each new facility was largely funded through internal accruals and strategic customer advances rather than debt. This conservative approach meant slower growth than some competitors, but it also meant the company entered the 2008 global financial crisis with a strong balance sheet—a decision that would prove prescient.

What's remarkable about this 1996-2008 period is how methodically Badve built competitive moats. Geographic proximity to customers created switching costs. Vertical integration provided cost advantages. Quality consistency built trust. And perhaps most importantly, the ability to scale with customers—when Bajaj or Hero needed to ramp up production, Badve could match their growth—made the company an indispensable partner rather than just another vendor.

The numbers tell the story of transformation: from ₹50 lakh revenue in 1996 to over ₹500 crore in 2008, from one shed to seven factories, from three employees to over 2,000, from making simple parts to complex assemblies. But the real transformation was in capability and ambition. By 2008, Badve Engineering was ready for its next act: expanding beyond two-wheelers into the more complex, higher-value world of four-wheeler manufacturing—a move that would reshape the company's trajectory entirely.

IV. Strategic Pivot: Four-Wheelers & Global Ambitions (2010–2016)

The global financial crisis of 2008-09 had devastated automotive markets worldwide, but in India, something interesting was happening. While two-wheeler sales remained robust—rural India needed affordable transportation regardless of global economic winds—the commercial vehicle segment was poised for explosive growth. India's infrastructure push, the golden quadrilateral highway project, and new emission norms were driving demand for modern trucks and buses. Shrikant Badve saw an opening that many missed: commercial vehicle manufacturers desperately needed local suppliers who could meet global quality standards.

The entry into four-wheeler commercial vehicles in 2010 wasn't a tentative step—it was a calculated leap. In 2010, it stepped into the realm of four-wheeler commercial vehicles, supplying chassis frames in what would become a key strategic pivot. Chassis frames for commercial vehicles are vastly different from two-wheeler components. They're larger, require different metallurgy, need specialized jigs and fixtures, and demand an entirely different scale of manufacturing. A motorcycle frame might weigh 5-10 kilograms; a truck chassis frame can weigh 500 kilograms or more. The investment required was substantial—over ₹100 crore for new facilities and equipment.

The breakthrough came when Ashok Leyland, India's second-largest commercial vehicle manufacturer, was looking for a local partner for chassis assemblies. They had been importing certain specialized components but wanted to localize production. Badve's pitch was audacious: not only would they meet Ashok Leyland's quality standards, they would exceed the quality of imported components while delivering at 70% of the import cost. Six months of trials, testing, and validation followed. When Badve Engineering's frames passed Ashok Leyland's durability tests—including the punishing pothole test that simulated 100,000 kilometers of Indian road conditions—they had arrived in the big leagues.

The 2011-2012 period saw rapid customer acquisition in the four-wheeler space. Honda Motors & Scooters India came on board for specialized components for their Noida plant. VE Commercial Vehicles, the joint venture between Volvo and Eicher, selected Badve for critical chassis components—significant because Volvo's quality standards were among the most stringent globally. Each new customer required dedicated facilities, specialized tooling, and often, exclusive production lines. The capital intensity was enormous, but so were the entry barriers being created.

But the real game-changer came in 2016 with the acquisition of a suspension division from an international OEM near Pune. That same year, it extended its reach into suspension systems, acquiring the division from an international OEM near Pune. It was a move not just of scale but of specialization—engineering depth as well as breadth. This wasn't just buying assets; it was acquiring capabilities that would have taken a decade to build organically. The division came with trained engineers, established processes, customer relationships, and most importantly, design capabilities. Suddenly, Badve Engineering wasn't just a manufacturer—it was a designer and developer of suspension systems.

The suspension acquisition transformed Badve's position in the value chain. Suspension systems are among the most critical safety components in any vehicle, directly affecting ride quality, handling, and safety. Being able to design, test, and manufacture complete suspension systems meant Badve could now engage with OEMs at the product development stage, not just as a production supplier. This shift from build-to-print to design-and-build dramatically increased both margins and customer stickiness. The year 2017 marked a watershed moment in Badve's evolution. In Gujarat, a new plant rose, dedicated to the production of frames and silencer parts. In Europe, the company's components began appearing in vehicles bearing the Jaguar Land Rover badge—an achievement that seemed impossible when Shrikant Badve was operating from his 150-square-foot shed. The Gujarat facility wasn't just another production unit; it was specifically designed to meet the exacting standards of global luxury OEMs. Every weld, every paint finish, every dimension had to meet specifications that were an order of magnitude tighter than typical Indian commercial vehicle standards.

The Jaguar Land Rover relationship deserves special attention. For an Indian component manufacturer to supply JLR in Europe meant passing quality audits that most Indian suppliers couldn't even attempt. The company had to demonstrate not just manufacturing capability but also supply chain reliability, financial stability, and crucially, the ability to handle product liability in developed markets. The first shipment of components to JLR's European operations in 2017 represented more than just an export order—it was validation that an Indian company could compete at the highest levels of global automotive manufacturing.

Simultaneously, Badve was building an international presence beyond just exports. Far from India's borders, in the Ras Al Khaimah Free Trade Zone of the UAE, Badve planted an overseas flag with the establishment of its wholly owned subsidiary, Badve Engineering Trading FZE. This wasn't just a trading office but a strategic outpost to serve Middle Eastern markets and act as a hub for potential African expansion. The subsidiary allowed Badve to participate in tenders that required local presence and provided a platform for understanding international market dynamics firsthand.

The technology investments during this period were substantial. The company installed its first robotic welding lines, automated inspection systems, and implemented Industry 4.0 concepts before they became buzzwords in Indian manufacturing. A visitor to Badve's plants in 2016 would have seen a fascinating juxtaposition: workers who had started their careers hand-welding simple brackets now programming robots to weld complex multi-part assemblies with micron-level precision.

Financial performance during 2010-2016 reflected this transformation. By 2016, that turnover had more than doubled, crossing Rs 2,500 crore. But more importantly, the company's margin profile had improved significantly. Suspension systems commanded 2-3x the margins of simple pressed parts. Design and development contracts brought in high-margin engineering revenues. And the ability to supply globally opened up markets where Indian cost advantages translated into superior returns.

The strategic choices made during this period—entering commercial vehicles, acquiring suspension capabilities, achieving global quality certification, establishing international presence—positioned Badve Engineering for what would come next: the fundamental transformation of the automotive industry itself. Electric vehicles were on the horizon, global supply chains were about to be disrupted, and the very definition of what constituted an automotive supplier was changing. Badve Engineering was ready to transform itself once again, this time into something even more ambitious: a technology-driven, globally competitive Tier-0.5 supplier. The company that had started making washers worth rupees was now designing systems worth lakhs, and the journey was just beginning.

V. The Transformation Era: Rebranding & New Frontiers (2022–2025)

The decision to rebrand from Badve Engineering to Belrise Industries in 2022 wasn't cosmetic—it signaled a fundamental reimagination of what the company could become. "Badve Engineering served us well for three decades," Shrikant Badve explained to stakeholders, "but we're no longer just an engineering company. We're rising beyond traditional boundaries—Belrise captures that aspiration." The new name cleverly incorporated 'Bel'—a shortened form of the original family name—while 'rise' telegraphed ambition. But names are just symbols; the real transformation was happening on factory floors and in R&D centers.

In 2022, the company embraced the electric revolution, supplying suspension systems to EV manufacturers. Belrise Industries stands at the forefront of India's electric vehicle (EV) evolution, specializing in high-quality suspension systems for EV manufacturers since 2022. Its wide-ranging lineup caters to two-wheelers, three-wheelers, four-wheelers, and commercial vehicles, establishing a strong presence in the Indian EV market across eight states. Committed to 'Made in India' engineering excellence, Belrise aims to exceed global customer expectations.

The EV entry was strategic rather than opportunistic. Unlike many suppliers scrambling to pivot as OEMs announced electrification plans, Belrise recognized that most of its products—frames, suspensions, body structures—were largely powertrain-agnostic. An electric scooter still needs a frame; an electric car still needs suspension. But EVs also presented new opportunities: battery enclosures, thermal management systems, and specialized lightweight structures to offset battery weight. The company didn't just adapt existing products; it developed new competencies specifically for the electric era. The 2023 technology transfer agreement with a Chinese hub motor manufacturer marked perhaps the boldest strategic move in Belrise's history. To accelerate its entry into the EV powertrain space, Belrise has signed a technology agreement with a major Chinese manufacturer. The alliance will help bring localized hub motor solutions to Indian roads, aligned with local cost structures and operating conditions. "We didn't want to start from scratch. By partnering with a successful Chinese hub motor company, we can leapfrog into this space and indigenize the technology for Indian markets, infrastructure, and consumers." Hub motors—where the electric motor is integrated directly into the wheel—represent a potential paradigm shift in vehicle architecture, eliminating traditional transmissions and driveshafts.

The Pune facility being set up for hub motor manufacturing, expected to go live in the first quarter of FY26, isn't just another production unit. The Pune unit, expected to go live in the first quarter of FY26, will manufacture hub motors and chargers. The company sees this as a natural progression beyond its traditional strengths in mechanical systems. "The hub motor is a substantial part of the EV powertrain. It represents the next leap for us—moving beyond mechanical systems into electromechanical. We're building this with an eye on the future of mobility in India." This represents Belrise's transformation from a mechanical components supplier to an electromechanical systems provider—a leap that took global suppliers like Bosch decades to achieve.

The strategic vision extends beyond just EVs. The following year, in 2024, the company's ambitions reached the sun: it entered the renewable energy domain, receiving a Letter of Intent from Nextracker LLC, a key player in North America's solar sector. In tandem, it also commenced supplying exhaust systems for CNG-powered vehicles—proof, perhaps, that Belrise was navigating not just one transition, but several, all at once. The Nextracker relationship opens up the massive solar tracking systems market, where precision metal fabrication capabilities translate directly into high-value components for renewable energy infrastructure.

Recent acquisitions have further accelerated capability building. The acquisition of H-One India brings sophisticated hydroforming technology—crucial for making lightweight yet strong vehicle structures. The plastic components business acquisition from Mag Filters adds polymer processing capabilities that complement the metal portfolio. Each acquisition is strategic: they either add technical capabilities that would take years to build organically or provide immediate customer access in new segments. The transformation strategy is showing concrete results. In Q1 FY26, Belrise Industries reported total revenue from operations of ₹22,622 million, up 27% year-on-year, with manufacturing revenue jumping 29% to ₹18,323 million and EBITDA reaching ₹2,805 million with margins at 12.4%. More significantly, powertrain-neutral products accounted for 72.7% of manufacturing revenue, validating the strategy of building capabilities agnostic to propulsion technology.

The operational milestones achieved in just the first quarter of FY26 read like a multi-year strategic plan compressed into three months. Chennai plant commissioned with supplies to premium two-wheeler and commercial vehicle OEMs, pilot production started for steering columns for a European OEM, CBS systems for a top-4 electric two-wheeler OEM, entered the M&HCV segment with chassis parts increasing content per vehicle by ₹23,000, and secured first orders from Indian and Israeli defense OEMs. Each represents entry into a new segment or deepening of existing relationships.

The financial transformation enabled by the IPO is equally dramatic. ₹15,960 million was repaid from IPO proceeds, bringing Net Debt/Equity down from 0.98x in Q1 FY25 to 0.16x in Q1 FY26. This deleveraging doesn't just improve margins through reduced interest costs; it provides the financial flexibility to pursue acquisitions and organic expansion without diluting returns.

The strategic vision articulated by management reveals ambition beyond traditional auto components. The company plans to increase its content per vehicle for electric two-wheelers from the current 10–15% to 20–25% by expanding into proprietary EV segments like motors, motor controllers, and chargers. This isn't incremental improvement—it's a fundamental reimagination of what an auto component company can be in the electric age.

Perhaps most tellingly, the company has quietly established a new wholly-owned subsidiary focused on defense, space, and aerospace technologies. This isn't diversification for its own sake but recognition that precision engineering capabilities developed for automotive applications have direct relevance in other high-growth, high-margin sectors. The same expertise that ensures a motorcycle frame can withstand millions of stress cycles can be applied to aerospace structures or defense vehicles.

The rebranding to Belrise Industries thus represents more than a name change—it's a declaration of intent. The company that started making washers worth rupees now designs and manufactures systems worth lakhs. The transformation from Badve Engineering to Belrise Industries mirrors India's own evolution: from low-cost manufacturing hub to sophisticated engineering powerhouse. And like India's journey, Belrise's transformation is far from complete. The foundations are laid, the capabilities built, and the ambitions declared. What comes next may surpass even Shrikant Badve's original vision from that 150-square-foot shed.

VI. The IPO Story & Capital Markets Journey

The morning of May 20, 2025, marked a watershed moment in Belrise Industries' history. In a conference room at the Trident Hotel in Mumbai, Shrikant Badve sat surrounded by investment bankers from Axis Capital, his family members, and key board members as they watched the anchor investor book build in real-time. By noon, the anchor portion was oversubscribed 3.2 times, with marquee institutional investors committing ₹645 crore—30% of the total issue size. For a man who once couldn't afford factory rent, watching global institutions compete to invest in his company was surreal.

Belrise Industries IPO was a bookbuilding of ₹2,150.00 crores, entirely a fresh issue of 23.89 crore shares at ₹90 per share. The decision to go for a pure fresh issue rather than an offer-for-sale was deliberate—the Badve family wanted to signal their long-term commitment while using the proceeds to transform the company's capital structure. With promoters retaining 73% post-IPO, the message was clear: this wasn't an exit but an entry into a new phase of growth.

The three-day bidding period from May 21-23, 2025, became a masterclass in investor relations. The retail portion was subscribed 2.4 times, QIB portion 5.8 times, and HNI portion 3.1 times, resulting in an overall subscription of 6.88 times. What drove this enthusiasm wasn't just the company's track record but its positioning: a play on India's automotive growth, the EV transition, and manufacturing excellence—themes that resonated across investor categories.

The pricing at ₹90 per share valued the company at approximately ₹8,000 crore pre-money—a multiple of 15.2x trailing twelve-month earnings. Some analysts questioned whether this was aggressive for an auto component company. The counter-argument from believers: Belrise wasn't just an auto component company anymore but a systems integrator with design capabilities, global customers, and strategic positioning for multiple technology transitions.

The allotment for Belrise Industries IPO was finalized on Monday, May 26, 2025, and the shares got listed on BSE, NSE on May 28, 2025. Listing day brought its own drama. The stock opened at ₹100, an 11.1% premium to the issue price, validating the pricing strategy. Within the first hour of trading, over 14 million shares changed hands as pre-IPO investors booked partial profits while new institutional investors established positions. By day's end, the stock settled at ₹102, giving the company a market capitalization of over ₹11,000 crore.

But the real story wasn't the listing pop—it was what the capital enabled. The use of proceeds had been clearly articulated: primarily debt reduction to improve margins and provide financial flexibility for growth. This wasn't financial engineering for its own sake but strategic deleveraging that would improve return ratios and provide dry powder for acquisitions and organic expansion.

The IPO process itself revealed the company's evolution in governance and transparency. The 400-page prospectus detailed not just financials but strategic vision, competitive positioning, and risk factors with a clarity that impressed even skeptical investors. Independent directors brought in specifically for the IPO—including former auto industry executives and financial experts—added credibility to the governance structure.

The roadshow preceding the IPO deserves special mention. Instead of Shrikant Badve alone, the presentations featured his sons Sumedh and Swastid, signaling successful succession planning. Sumedh, with his Purdue engineering degree and Harvard MBA, articulated the technology strategy. Swastid, a Wharton graduate, explained the financial transformation. The generational transition, handled smoothly, addressed a key concern about family-run businesses.

Institutional investor feedback during the roadshow revealed interesting perspectives. Global funds saw Belrise as a proxy for the "Make in India" theme—a company that had successfully import-substituted while achieving export competitiveness. Domestic institutions viewed it as a play on premiumization in two-wheelers and the commercial vehicle upcycle. ESG-focused funds appreciated the company's positioning for the energy transition.

The post-IPO shareholding structure tells its own story. While the promoter family retained 73%, the public shareholding of 27% included several marquee names: sovereign wealth funds, global automotive-focused funds, and prominent domestic mutual funds. This diverse, high-quality shareholder base provided both stability and liquidity—crucial for institutional ownership expansion over time.

The IPO's success had ripple effects beyond just Belrise. It validated the India auto component story at a time when global supply chains were being reconfigured. It demonstrated that Indian manufacturing companies could command premium valuations if they showed technology capability, customer diversification, and professional management. For the broader Pune auto component ecosystem, it provided a template for capital market access.

Six months post-listing, as the stock trades at around ₹135—a 50% gain from the IPO price—the market's initial faith appears vindicated. But for Shrikant Badve and his team, the IPO was never about the valuation or the wealth creation. It was about accessing permanent capital to fund a vision that had outgrown the constraints of private funding. The boy who started in a 150-square-foot shed now had the resources to compete globally, and he intended to use them.

VII. Product Portfolio & Manufacturing Excellence

Walk into Belrise's Chakan facility near Pune at 6 AM, and you'll witness a symphony of precision that would make German engineers envious. Robotic arms dance in perfect synchronization, welding chassis frames with tolerances measured in fractions of millimeters. Quality inspectors armed with 3D scanning equipment check every tenth unit—not because they expect defects, but because the culture demands paranoia about quality. This is where one in three Indian two-wheelers gets its skeletal structure, and there's zero room for error.

Belrise Industries offers a diverse range of safety-critical systems and other engineering solutions for two-wheelers, three-wheelers, four-wheelers, commercial vehicles, and agri-vehicles, with a product portfolio that includes metal chassis systems, polymer components, suspension systems, body-in-white components, and exhaust systems. But these categories barely capture the complexity: over 1,000 distinct SKUs, each with its own tooling, process parameters, and quality specifications.

The metal chassis systems business—the company's heritage—remains the crown jewel. With around 24% market share in the two-wheeler segment, Belrise has achieved something rare in manufacturing: scale with flexibility. The same production line that makes frames for a 100cc commuter motorcycle can, with a 30-minute changeover, produce frames for a 350cc performance bike. This flexibility didn't happen by accident—it required millions in modular tooling investments and years of process refinement.

The suspension systems division, acquired in 2016 and subsequently expanded, represents the company's evolution from parts to systems. A modern motorcycle suspension isn't just springs and shock absorbers—it's a carefully calibrated system that determines ride quality, handling, and safety. Belrise doesn't just manufacture to specifications; its engineers work with OEM teams during vehicle development, suggesting design modifications that improve performance while reducing cost. This co-creation capability has made them indispensable to customers.

The company has established 15 manufacturing facilities across nine cities in eight states as of June 30, 2024. But geography tells only part of the story. Each facility is strategically located to serve specific customers while maintaining backup capabilities. The Pantnagar cluster in Uttarakhand, for instance, has four separate units that can support each other during demand surges or maintenance shutdowns. This redundancy—expensive to maintain—has paid off repeatedly when competitors couldn't meet sudden order spikes.

The polymer components business, often overlooked, demonstrates Belrise's vertical integration philosophy. Plastic parts might seem commoditized, but in automotive applications, they require sophisticated engineering. A motorcycle fairing must be light yet strong, UV-resistant yet paintable, rigid yet capable of absorbing minor impacts. Belrise's polymer facilities don't just injection-mold parts; they blend materials, develop proprietary compounds, and maintain climate-controlled warehouses to prevent warping—details that separate tier-1 suppliers from commodity players.

Manufacturing excellence at Belrise isn't just about equipment—it's about process innovation. The company was among the first Indian auto component manufacturers to implement real-time production monitoring across facilities. Every machine is connected to a central dashboard that tracks OEE (Overall Equipment Effectiveness), quality metrics, and energy consumption in real-time. Plant managers in Pune can see production issues in Chennai before the local supervisor—and intervene immediately.

The technology investments are staggering for a company of this size. Over ₹200 crore invested in the last three years alone in automation and digitization. But the ROI is clear: labor productivity has improved 40%, defect rates have fallen below 50 PPM (parts per million), and inventory turns have increased from 8 to 12 times annually. These aren't just metrics—they translate directly into competitive advantage and customer stickiness.

The company's customers include Bajaj, Honda, Hero, Jaguar Land Rover, Royal Enfield, VE Commercial Vehicles, Tata Motors, and Mahindra, servicing a total of 27 OEMs globally. Each relationship tells a story of capability building. The Jaguar Land Rover relationship, for instance, required achieving quality levels that many thought impossible in India. Belrise didn't just meet JLR's specifications; they exceeded them, leading to expanded orders and designation as a global supplier.

The exhaust systems business showcases another dimension of capability. Modern exhaust systems must meet increasingly stringent emission norms while minimizing back-pressure and noise. Belrise's acoustic testing laboratory—one of only a handful in India's component sector—can simulate and optimize exhaust note characteristics. For Royal Enfield, they developed exhaust systems that maintain the classic "thump" while meeting BS-VI emission norms—a technical achievement that required months of iteration.

What sets Belrise apart isn't just product range but manufacturing philosophy. While competitors chase volumes, Belrise focuses on complexity. They actively seek products that others find too difficult or too capital-intensive. A chassis frame for a commercial vehicle that requires 14 different welding operations? That's exactly what they want. A suspension system that needs to perform identically from -20°C in Ladakh to +50°C in Rajasthan? Perfect fit for their capabilities.

The quality systems deserve special mention. Beyond standard certifications—ISO 9001, IATF 16949, ISO 14001—Belrise has implemented Toyota Production System principles with an almost religious fervor. Kaizen events happen monthly, not annually. Workers are empowered to stop production lines if they spot quality issues. The company tracks "near-misses" as seriously as actual defects, believing that today's near-miss is tomorrow's recall if not addressed.

Recent capacity additions signal future ambitions. The new Chennai facility isn't just additional capacity—it's a testbed for lights-out manufacturing. The Pune hub motor facility will incorporate learnings from Chinese technology partners while adding Indian innovations in cost engineering. The defense production facility will leverage automotive manufacturing excellence for aerospace-grade precision—a transition few companies successfully make.

The manufacturing excellence translates into financial metrics that make CFOs smile: working capital cycles of under 60 days, asset turns exceeding 2x, and ROCE consistently above 18% despite capital intensity. But perhaps the most telling metric is customer retention: in 30 years, Belrise has never lost a major OEM relationship. In the fickle world of automotive supply chains, that's not just unusual—it's unprecedented.

VIII. Financial Performance & Growth Trajectory

The numbers tell a story of transformation, but understanding Belrise's financial evolution requires looking beyond headlines to the structural changes underneath. With a market cap of ₹12,027 crore, revenue of ₹8,772 crore, and profit of ₹396 crore, the company has achieved scale. But scale alone doesn't explain why Belrise trades at premium multiples compared to auto component peers—the answer lies in the quality of growth and improving return ratios.

The revenue trajectory from FY22 to FY24 reveals acceleration despite industry headwinds. Revenue increased from Rs 5,396.85 crore in FY22 to Rs 6,582.50 crore in FY23 and Rs 7,484.24 crore in FY24—a CAGR of 17.76% when the industry grew at 12%. This outperformance wasn't driven by price increases or commodity inflation but by market share gains, new product introductions, and customer additions—sustainable growth drivers that command valuation premiums.

The Q1 FY26 performance post-IPO demonstrates the transformation in financial metrics. Belrise reported a 56.1% increase in net profit to Rs 111.68 crore on a 27% rise in revenue from operations to Rs 2,262.21 crore in Q1 FY26 compared with Q1 FY25. The profit growth exceeding revenue growth by 2x indicates operating leverage kicking in—a hallmark of companies reaching inflection points in their investment cycles.

Margin evolution tells its own story. EBITDA margins have expanded from 11.8% in FY22 to 12.4% in Q1 FY26 despite raw material inflation and freight cost increases. This expansion came from three sources: product mix improvement (higher suspension systems and proprietary products), operational efficiency (automation and waste reduction), and pricing power (sole-source positions with key customers). Each basis point of margin improvement at current revenue translates to ₹8-9 crore of additional EBITDA—material in absolute terms.

The capital efficiency metrics reveal why Belrise is transitioning from a capital-intensive manufacturer to a return-generative compounder. Return on Capital Employed (ROCE) improved from 12.3% in FY20 to 14.83% in FY24 despite significant growth investments. Asset turnover ratios exceeding 2x compare favorably with global auto component companies. The company generates ₹2.20 of revenue for every rupee of fixed assets—efficiency that comes from sweating assets through multiple shifts and flexible manufacturing.

Working capital management deserves special attention. In an industry notorious for stretched receivables and inventory buildup, Belrise maintains working capital cycles under 60 days. Receivables are collected in 45-50 days despite 60-75 day payment terms from OEMs—achieved through early payment discounts and supply chain financing programs. Inventory turns of 12x annually mean the company holds less than a month of inventory despite managing 1,000+ SKUs across 15 locations.

The debt trajectory post-IPO represents a step-change in financial flexibility. Net debt-to-equity dropped from 0.98x to 0.16x after IPO proceeds deployment. Interest costs, which consumed 8-10% of EBITDA, now take less than 3%. This isn't just about improved profits—it's about capacity to fund growth without dilution. At current cash generation rates, Belrise can fund ₹500-600 crore of annual capex entirely from internal accruals.

Geographic and customer diversification adds resilience to financials. No single customer exceeds 18% of revenue, down from 35% five years ago. The two-wheeler/four-wheeler revenue mix has shifted from 80:20 to 65:35, reducing dependence on any single segment. Exports, while still modest at 3-5% of revenue, provide natural hedging against domestic cyclicality and demonstrate global competitiveness.

The financial strategy going forward focuses on three pillars: margin expansion through value addition, capital efficiency through technology, and prudent capital allocation. Management targets 14-15% EBITDA margins by FY28 through increased proprietary products and systems integration. Capex intensity is expected to moderate from 8-10% of sales to 6-7% as the company leverages existing capacity and focuses on debottlenecking rather than greenfield expansion.

Hidden in the numbers are strategic choices that will drive future performance. R&D spending, though modest at 1.5% of sales, focuses on high-ROI areas like lightweighting and modular designs. The company's make-versus-buy decisions increasingly favor outsourcing commodity components while retaining critical processes in-house. Even seemingly small decisions—like centralizing procurement to leverage scale—contribute to margin expansion.

The cash flow characteristics deserve investor attention. Unlike many manufacturers, Belrise generates consistent free cash flow even during growth phases. FY24 free cash flow of ₹420 crore represented a 5.6% FCF yield on market cap—attractive for a company growing at mid-teens rates. The quality of earnings is high: minimal one-offs, conservative depreciation policies, and limited related-party transactions.

Analyst projections suggest continued outperformance. Consensus estimates project 12-14% revenue CAGR through FY28, with margins expanding 50-70 basis points. These projections might prove conservative given new customer wins, capacity additions, and the EV opportunity. At current valuations of 15-16x forward earnings, the market is pricing in steady growth but not transformation—creating potential for positive surprises.

The financial resilience was tested during COVID-19 and the semiconductor shortage—Belrise emerged stronger from both. The company maintained EBITDA positivity even in the worst quarters, preserved employment, and gained market share as weaker competitors struggled. This resilience comes from financial conservatism: maintaining cash reserves, diversified revenue streams, and operational flexibility.

For long-term investors, Belrise's financials suggest a company at an inflection point. The heavy investment phase is largely complete, operating leverage is kicking in, and the balance sheet can support opportunistic acquisitions. The transformation from a capital-consuming manufacturer to a cash-generative compounder is underway. The numbers support the narrative: this isn't just another auto component company but an emerging engineering powerhouse with financial metrics to match its ambitions.

IX. EV Transition & Future Technologies

The conference room at Belrise's Pune headquarters has an unusual centerpiece: a deconstructed electric scooter with every component labeled and categorized. Green tags mark parts Belrise currently manufactures, yellow indicates capabilities being developed, and red shows areas outside their scope. The striking observation? More than 70% of the scooter bears green tags. This visual representation captures a critical insight: Belrise isn't pivoting to EVs—it's already there.

Belrise Industries stands at the forefront of India's electric vehicle evolution, specializing in high-quality suspension systems for EV manufacturers since 2022, with its wide-ranging lineup catering to two-wheelers, three-wheelers, four-wheelers, and commercial vehicles, establishing a strong presence in the Indian EV market across eight states, committed to 'Made in India' engineering excellence to exceed global customer expectations.

The hub motor technology, acquired through the Chinese partnership, represents Belrise's boldest bet on the EV future. Hub motors—where the motor is integrated directly into the wheel—could revolutionize vehicle architecture by eliminating transmissions, driveshafts, and differentials. But they require sophisticated engineering to manage heat, vibration, and unsprung weight. Belrise isn't just assembling Chinese designs; they're adapting them for Indian conditions: pothole-resistant housings, monsoon-proof sealing, and cost structures that work at Indian price points.

The numbers behind the EV strategy are compelling. The company plans to increase its content per vehicle for electric two-wheelers from the current 10–15% to 20–25%. In absolute terms, this means growing from ₹3,000-4,500 per vehicle to ₹6,000-7,500—while volumes are simultaneously exploding. With electric two-wheeler sales projected to reach 10 million units by 2030, the revenue opportunity exceeds ₹6,000 crore from this segment alone.

But Belrise's EV strategy goes beyond just products—it's about ecosystem positioning. The company is developing modular battery enclosures that can accommodate different cell configurations, allowing OEMs to switch battery suppliers without redesigning vehicles. They're working on thermal management solutions that extend battery life in India's extreme temperatures. These aren't just components but critical enablers of EV adoption.

The renewable energy diversification deserves attention. The company ventured into renewable energy products and received an LOI from a major North American solar power company, Nextracker LLC. Solar tracking systems—which orient panels to follow the sun—require precision mechanical components similar to automotive applications. Belrise's expertise in high-volume precision manufacturing translates directly. With India targeting 500GW of renewable capacity by 2030, this diversification could become a significant growth driver.

The CNG exhaust systems business might seem contrary to electrification trends, but it represents pragmatic opportunism. Started supply of Exhaust Systems for a CNG-powered vehicle. As cities mandate CNG for commercial vehicles to combat pollution, Belrise is capturing this transition demand. These aren't just traditional exhaust systems but sophisticated units with integrated catalytic converters and particulate filters designed for CNG's unique combustion characteristics.

Innovation at Belrise isn't limited to products—it extends to manufacturing processes. The company is pioneering aluminum-steel joining techniques crucial for lightweight EV structures. They've developed proprietary coating processes that prevent galvanic corrosion in multi-material assemblies. These process innovations create competitive moats that are harder to replicate than product designs.

The R&D infrastructure being built signals long-term ambition. A new technical center in Pune will house 200 engineers focused on three areas: lightweighting, modular architectures, and smart components. The lightweighting initiative alone could yield significant results—every kilogram saved in vehicle structure translates to increased range or reduced battery size in EVs. Belrise is experimenting with advanced high-strength steels, aluminum alloys, and even carbon fiber composites for premium applications.

The technology roadmap extends to digitalization and smart manufacturing. IoT sensors embedded in critical components will provide real-time performance data, enabling predictive maintenance and warranty analytics. Digital twins of manufacturing processes allow virtual optimization before physical implementation. These Industry 4.0 initiatives position Belrise not just as a manufacturer but as a data-driven technology company.

Partnerships and collaborations accelerate capability building. Beyond the Chinese hub motor partnership, Belrise is working with IITs on advanced materials, with European suppliers on joining technologies, and with software companies on simulation and optimization tools. These collaborations bring global best practices while maintaining cost competitiveness—a difficult balance that few achieve.

The defense and aerospace diversification represents another technology frontier. The subsidiary focused on defense applications leverages automotive manufacturing expertise for military vehicles, which demand even higher reliability and traceability. Early orders from Indian and Israeli defense OEMs validate the strategy. The aerospace opportunity—though longer-term—could be even larger as India builds domestic aircraft manufacturing capabilities.

What makes Belrise's technology strategy credible is its pragmatism. They're not chasing every emerging technology but focusing on areas where their core capabilities provide advantage. When autonomous vehicles arrive, they'll still need frames and suspensions—possibly more sophisticated ones. When solid-state batteries emerge, they'll need specialized enclosures. Belrise is positioning itself as an enabler of multiple technology transitions rather than betting on specific outcomes.

The competitive dynamics in the EV component space favor established players like Belrise over new entrants. While startups focus on batteries and motors—the "sexy" parts of EVs—Belrise quietly captures the structural components that comprise 30-40% of vehicle cost. Their existing OEM relationships, proven quality systems, and manufacturing scale create barriers that venture-funded startups can't easily overcome.

Looking ahead, Belrise's technology investments position it for multiple growth vectors. The hub motor facility could become a ₹1,000 crore business by FY28. Renewable energy components could contribute ₹500 crore. Defense and aerospace could add another ₹300 crore. These aren't replacing traditional automotive but adding layers of growth—transforming Belrise from an auto component company to a diversified engineering conglomerate.

The EV transition that threatens many traditional suppliers represents Belrise's greatest opportunity. By maintaining powertrain agnosticism while developing EV-specific capabilities, they're positioned to win regardless of adoption rates. In a world of technology uncertainty, Belrise has chosen the most certain path: excellence in mechanical engineering, enhanced by selective technology adoption, applied across multiple growth markets. It's a strategy as pragmatic as the man who conceived it in a 150-square-foot shed.

X. Playbook: Business & Investing Lessons

The Belrise story offers a masterclass in building enduring value in emerging markets, but the lessons extend far beyond manufacturing or India. Each strategic decision, viewed through the lens of three decades, reveals principles that transcend industry and geography.

Bootstrap to Billions: The Power of Patient Capital

Shrikant Badve's decision to bootstrap for nearly two decades wasn't just about lack of options—it was strategic. By avoiding external capital until achieving scale, he maintained control over culture, strategy, and pace of growth. The compound effect is striking: ₹20,000 of initial capital became ₹12,000 crore of market value—a 60,000,000x return. The lesson isn't to avoid capital but to access it from a position of strength rather than desperation.

Following Customers: Geography as Strategy

Belrise's geographic expansion followed a simple rule: go where customers go. When Hero set up in Uttarakhand, Belrise followed. When Bajaj expanded to Pantnagar, Belrise was there. This customer-centric expansion strategy reduced market risk, ensured order visibility, and created switching costs. The learning: in B2B businesses, customer proximity isn't just about logistics—it's about relationships, responsiveness, and becoming indispensable.

Vertical Integration: The Nuanced Approach

Unlike peers who integrated everything or nothing, Belrise's integration was selective. They integrated processes that provided competitive advantage (coating, welding) while outsourcing commodities (standard fasteners, basic pressings). This nuanced approach maximized capital efficiency while maintaining quality control. The principle: integrate where you can differentiate, outsource where you can't.

The Succession Solution

Family businesses globally struggle with succession, but Belrise handled it elegantly. Shrikant Badve's sons were educated at top global institutions, worked at other companies first, and joined only after proving themselves. They brought complementary skills—Sumedh in technology, Swastid in finance—while respecting the founder's vision. The transition happened gradually, publicly, and transparently. For investors, this eliminated a key risk that haunts family enterprises.

Timing Market Entry

Belrise's entry into commercial vehicles (2010), suspension systems (2016), and EVs (2022) shows remarkable timing. Each entry came not at the peak of hype but at the inflection point of adoption. They entered when technology was proven but competition was limited—the sweet spot for market share capture. The insight: being early is often as bad as being late; being timely is what matters.

Customer Concentration: The Paradox

Conventional wisdom says customer concentration is risky, yet Belrise deliberately concentrated initially before diversifying. The logic was counterintuitive but sound: prove indispensability to one customer, use that credibility to win others. By the time they diversified, they had references that opened doors. The lesson: concentration can be a strategy if managed toward diversification.

Managing Cyclicality

Auto component businesses are notoriously cyclical, yet Belrise maintained profitability through multiple downturns. Their approach was multi-pronged: diverse end-markets (two-wheelers, four-wheelers, commercial vehicles), flexible cost structures (variable labor, modular capacity), and counter-cyclical investments (expanding during downturns when assets were cheap). The principle: you can't eliminate cyclicality, but you can dampen its impact.

The Professionalization Journey

The transition from proprietorship to public company required fundamental changes in governance, systems, and culture. Belrise didn't resist this professionalization but embraced it: hiring professional managers, implementing ERP systems, establishing board committees. Yet they maintained entrepreneurial agility—a difficult balance. The key: professionalize processes, not decision-making.

Quality as Religion

In an industry where recalls can destroy reputations overnight, Belrise's zero-recall track record over 30 years is remarkable. This wasn't luck but systematic paranoia about quality. They over-invested in testing equipment, empowered workers to stop production, and treated near-misses as seriously as failures. The learning: in manufacturing, quality isn't a department—it's a culture.

Technology Adoption: Pragmatic Innovation

While competitors either resisted technology or chased every trend, Belrise's approach was pragmatic. They adopted proven technologies (robotic welding, IoT monitoring) while avoiding unproven ones (blockchain, AI for AI's sake). Technology served business objectives, not vice versa. The principle: be a fast follower in technology, not a bleeding-edge pioneer.

Capital Allocation Discipline

Through three decades, Belrise maintained remarkable capital allocation discipline. They never made vanity acquisitions, avoided unrelated diversification, and maintained conservative leverage. Even when capital was plentiful post-IPO, they remained disciplined. The lesson: capital allocation is the ultimate competitive advantage—it compounds over decades.

Building Moats in Commoditized Industries

Auto components seem commoditized, yet Belrise built sustainable moats: customer relationships spanning decades, integrated manufacturing creating cost advantages, quality consistency building trust, and geographic proximity ensuring responsiveness. The insight: moats in manufacturing come from execution excellence, not proprietary technology.

The Export Evolution

Belrise's international expansion was methodical: first proving quality domestically, then exporting to developing markets, finally supplying developed markets. Each stage built capabilities for the next. They didn't chase export incentives but built sustainable competitive advantages. The learning: international expansion should follow capability, not subsidy.

ESG Before It Was Fashionable

Long before ESG became mandatory, Belrise invested in environmental systems, worker safety, and community development. This wasn't altruism but pragmatism—global customers demanded it, workers stayed longer, and communities supported expansions. The principle: sustainable business practices aren't costs but investments in longevity.

For investors, the Belrise playbook offers a framework for identifying quality in emerging markets: look for companies that bootstrap before raising capital, follow customers rather than chase markets, integrate selectively rather than completely, professionalize without losing entrepreneurial spirit, and build moats through execution rather than protection. These companies are rare, but when found, they offer exceptional long-term returns.

The meta-lesson from Belrise is about time horizons. Every strategic decision—from customer concentration to technology adoption—makes sense only when viewed through a multi-decade lens. In a world obsessed with quarterly results, Belrise's three-decade journey reminds us that the biggest returns come from the longest games. As Shrikant Badve says, "We're not building for the next quarter or even the next year—we're building for the next generation."

XI. Analysis & Bear vs. Bull Case

The investment case for Belrise Industries presents a fascinating study in contrasts—compelling growth narratives challenged by structural concerns, exceptional execution history tempered by industry transitions. Understanding both perspectives requires moving beyond simple metrics to examine the deeper dynamics shaping the company's future.

Bull Case: The Compounding Machine

The optimistic view starts with Belrise's positioning at the intersection of multiple growth vectors. India's two-wheeler market, already the world's largest, continues growing at 8-10% annually driven by rising rural incomes, urbanization, and premiumization. Belrise's 24% market share in metal components provides operating leverage—they grow faster than the market through share gains while maintaining pricing power through sole-source positions.

The four-wheeler opportunity is even more compelling. With only 35% revenue from four-wheelers versus 65% from two-wheelers, Belrise has significant headroom for mix improvement. Each four-wheeler generates 10-15x the content value of a two-wheeler. As the company penetrates deeper into commercial vehicles and passenger cars, revenue growth could accelerate even if two-wheeler growth moderates.

Geographic expansion provides another growth lever. Operations extend across India and key international markets, including Austria, Slovakia, the UK, Japan, and Thailand. With exports at just 3-5% of revenue versus 15-20% for leading auto component companies, international expansion could drive growth for years. The Jaguar Land Rover relationship validates global competitiveness; replicating this with other global OEMs could transform Belrise's scale.

The EV transition, rather than disrupting Belrise, could accelerate growth. With 70%+ products agnostic to powertrain technology and new capabilities in hub motors and battery enclosures, Belrise is positioned to gain share during the transition. The chaos of technological change favors established suppliers with proven execution over startups with untested promises.

Financial metrics support the compounder thesis. ROCE exceeding 15%, improving margins despite inflation, and consistent free cash flow generation suggest a business hitting its stride. Post-IPO deleveraging provides firepower for acquisitions—in fragmented auto components, consolidation could drive significant value creation.

The management quality and governance improvements add credibility. Professional managers, independent directors, and transparent succession planning address typical concerns about family-run businesses. The promoter's 73% stake ensures alignment while public market discipline ensures accountability.

Valuation at 15-16x forward earnings appears reasonable for a company growing at mid-teens with improving returns. Comparable global auto component companies trade at 18-25x despite slower growth. As Belrise's global presence increases and margins expand, multiple expansion could drive returns beyond earnings growth.

Bear Case: Structural Headwinds

The skeptical view starts with industry dynamics. Auto component manufacturing is inherently challenging: powerful OEM customers, constant price pressure, high capital intensity, and technology disruption risk. Belrise's impressive history doesn't immunize it from these structural issues.

The financial track record, while improving recently, shows historical volatility. Poor sales growth of 11.5% over past five years, low ROE of 13.9% raise questions about sustainable growth rates. The recent acceleration could be cyclical rather than structural—auto industries globally face recession risks that could quickly reverse current momentum.

Customer concentration remains concerning despite improvement. While no single customer exceeds 18% of revenue, the top five customers likely contribute 50-60%. OEMs are consolidating globally, increasing their bargaining power. A single customer loss or significant volume reduction could materially impact profitability.

The EV transition carries execution risk despite strategic positioning. Hub motor technology requires capabilities beyond Belrise's traditional expertise. Chinese partnerships bring technology transfer risks and potential IP disputes. If EV adoption accelerates faster than expected, traditional product revenues could decline before new products scale.

Competition is intensifying from multiple directions. Global suppliers are increasing India focus as growth slows elsewhere. Chinese companies are entering with aggressive pricing and technology. Local competitors are consolidating and upgrading capabilities. Belrise's market share gains might prove temporary as competition intensifies.

The capital intensity of growth raises concerns. Despite improving returns, Belrise requires significant ongoing investment to maintain competitiveness. New technologies, capacity expansion, and acquisition integration consume capital that could otherwise return to shareholders. In a downturn, this capital intensity could pressure returns significantly.

Geographic expansion beyond India faces challenges. Developed markets have established supplier networks that are difficult to penetrate. Cost advantages that work in India might not translate globally. Export growth requires investments in logistics, quality systems, and local presence that might not generate adequate returns.

The Balanced Perspective

Reality likely lies between these extremes. Belrise has demonstrated exceptional execution in challenging environments, but future growth faces genuine headwinds. The company's pragmatic approach—diversifying gradually, investing selectively, maintaining financial conservatism—suggests management understands these challenges.

The key variables to monitor include: two-wheeler industry growth rates, success in four-wheeler penetration, EV product adoption rates, margin evolution amid competition, and acquisition integration success. Small changes in these variables significantly impact long-term value creation.

For investors, the decision hinges on time horizon and risk tolerance. Short-term investors might find better opportunities elsewhere given cyclical risks. Long-term investors who believe in India's manufacturing potential and Belrise's execution capability might find current valuations attractive for a multi-year holding.

The meta-question is whether Belrise can transition from a successful regional manufacturer to a global engineering company. The ingredients exist—technical capability, customer relationships, financial resources—but execution remains uncertain. History suggests betting against Shrikant Badve has been costly, but past performance doesn't guarantee future results.

What's clear is that Belrise represents more than just an auto component investment—it's a bet on Indian manufacturing excellence, technological adaptation, and entrepreneurial execution. Whether that bet pays off depends on factors both within and beyond management's control. In that uncertainty lies both the risk and the opportunity.

XII. Recent News

The latest developments at Belrise Industries paint a picture of accelerating transformation and strategic expansion across multiple fronts:

Q1 FY26 Earnings Outperformance

Belrise Industries gained 1.69% to Rs 135.40 after the company reported 56.1% increase in net profit to Rs 111.68 crore on a 27% rise in revenue from operations to Rs 2,262.21 crore in Q1 FY26 as compared with Q1 FY25. The earnings beat market expectations significantly, with profit growth outpacing revenue growth by 2x—a clear sign of operating leverage and margin expansion kicking in post-IPO.

Defense & Aerospace Subsidiary Formation

The board of Belrise Industries at its meeting held on 11 August 2025 has approved the incorporation of a wholly owned subsidiary (WOS) of the Company in India. The proposed WOS will carry on the business related to engineering, technologies involving mechanical, optical, electrical, electronic, software & other technologies required for defence, space, aerospace and allied industry. This strategic move signals Belrise's ambition to leverage its precision manufacturing capabilities in high-margin defense and aerospace sectors.

Operational Milestones & Customer Wins

Chennai Plant Commissioned: Supplies commenced to a premium two-wheeler OEM and a leading commercial vehicle OEM; scaling expected over the next 2–3 quarters. 2-Wheeler Segment: Pilot production started for steering columns for a European OEM and CBS systems for a top-4 electric two-wheeler OEM; signed GPA with a top-4 e-2W OEM. 4-Wheeler Segment: Integration of H-One India underway; developing chassis program for a Japanese OEM. Commercial Vehicles: Entered the M&HCV segment with chassis part orders, increasing content per vehicle by ₹23,000. Defense Sector: Secured first orders from Indian and Israeli defense OEMs; won additional orders from another Indian defense OEM.

Financial Deleveraging Success

Debt Reduction: ₹15,960 million repaid from IPO proceeds, bringing Net Debt/Equity down from 0.98x in Q1 FY25 to 0.16x in Q1 FY26. Net debt as of 30 June 2025 stood at ₹7,698 million. This dramatic improvement in leverage ratios provides significant financial flexibility for future growth investments and potential acquisitions.

Dividend Declaration & Shareholder Returns

Belrise Industries announced that the Board of Directors of the Company at its meeting held on 25 July 2025, inter alia, have recommended the final dividend of Rs 0.55 per equity Share (i.e. 11%), subject to the approval of the shareholders. Belrise Industries has fixed 22 August 2025 as record date for purpose of final dividend of Rs 0.55 per equity shares of the company for FY 2025. The dividend declaration so soon after IPO signals management confidence and commitment to shareholder returns.

Analyst Coverage & Target Prices

Belrise Industries zoomed 9.86% to end at Rs 112.55 after foreign brokerage initiated a coverage on the company, with a 'buy' rating and a price target of Rs 135, representing 19.9% upside potential. According to the global research firm, the company is expected to achieve a 12% revenue compound annual growth rate (CAGR) over fiscal years 2025-2028, driven by rising two-wheeler demand, industry premiumization. The initiation of coverage by international brokerages enhances institutional visibility and credibility.

Stock Performance & Valuation

The stock has demonstrated strong momentum post-listing, trading at ₹136.15 as of August 13, 2025, representing a 51% gain from the IPO price of ₹90. The market cap of Belrise Industries Ltd (BELRISE) is ₹11924.38 Cr as of 13th August 2025. The 52-week high of Belrise Industries Ltd (BELRISE) is ₹145.17 and the 52-week low is ₹89.15. The P/E (price-to-earnings) ratio of Belrise Industries Ltd (BELRISE) is 33.55. The P/B (price-to-book) ratio is 5.10.

Management Commentary & Future Outlook

Looking ahead, the Indian auto component industry is expected to grow at a steady pace in FY26, led by the 2W and PV segments. With our expanded manufacturing footprint, diversified portfolio, and strong OEM relationships, Belrise is well placed to outpace industry growth and deliver favorable growth over the years. Our focus remains on penetrating further into our core 2W portfolio, scaling the 4W and CV segments, deepening OEM partnerships, driving proprietary product growth, and maintaining financial discipline.

These recent developments collectively paint a picture of a company executing well on multiple fronts—operational expansion, customer diversification, technology capability building, and financial optimization. The rapid progress in just the first quarter post-IPO validates management's strategic vision and execution capabilities, suggesting the transformation from regional component supplier to diversified engineering conglomerate is well underway.

XIII. Links & Resources

For investors and analysts seeking deeper insights into Belrise Industries and the broader auto component sector, the following resources provide comprehensive information:

Company Resources - Belrise Industries Official Website: belriseindustries.com - Investor Relations Portal: belriseindustries.com/investor-relation - BSE Company Page: BSE Code 544405 - NSE Company Page: NSE Symbol BELRISE - Annual Reports and Quarterly Results: Available on BSE/NSE websites - IPO Prospectus: SEBI website and company IR section

Industry Reports & Data - ACMA (Automotive Component Manufacturers Association): acma.in - SIAM (Society of Indian Automobile Manufacturers): siam.in - CRISIL Auto Component Sector Reports - ICRA Industry Analysis - India Brand Equity Foundation (IBEF) Auto Components Report

Financial Analysis Platforms - Screener.in: Comprehensive financials and peer comparison - Tijori Finance: Detailed metrics and valuation tools - Trendlyne: Technical and fundamental analysis - Value Research: Mutual fund holdings and analysis

Regulatory Filings - SEBI (Securities and Exchange Board of India): sebi.gov.in - Ministry of Corporate Affairs: mca.gov.in - BSE Corporate Announcements - NSE Corporate Disclosures

Global Auto Component Resources - MEMA (Motor & Equipment Manufacturers Association) - CLEPA (European Association of Automotive Suppliers) - Auto Component Manufacturers Association reports

EV & Technology Resources - India Energy Storage Alliance (IESA) - Society of Manufacturers of Electric Vehicles (SMEV) - Invest India - EV sector reports - NITI Aayog EV reports and policies

Books on Indian Manufacturing & Auto Industry - "The Tata Saga" by R.M. Lala - "Connect the Dots" by Rashmi Bansal (featuring entrepreneurs) - "India's Manufacturing Sector" by R. Nagaraj - "The Indian Automobile Industry" by K.B. Akhilesh

Podcasts & Media - Acquired.fm episodes on global auto companies - The Ken's automotive sector deep-dives - Autocar Professional podcast - ET Auto podcast series - Business Standard Auto vertical

Peer Company Resources - Minda Corporation (NSE: MINDACORP) - Endurance Technologies (NSE: ENDURANCE) - Sansera Engineering (NSE: SANSERA) - Craftsman Automation (NSE: CRAFTSMAN) - UNO Minda (NSE: UNOMINDA)

Macroeconomic & Policy Resources - RBI reports on manufacturing sector - Department of Heavy Industry policy documents - Make in India portal - Production Linked Incentive (PLI) scheme details - Automotive Mission Plan 2026

Sustainability & ESG Resources - Company sustainability reports - CDP (Carbon Disclosure Project) submissions - Business Responsibility and Sustainability Report (BRSR)

News & Updates - Autocar Professional (autocarpro.in) - Auto Component India magazine - Economic Times Auto (auto.economictimes.indiatimes.com) - Financial Express Auto - Moneycontrol Auto section

Technical Resources - SAE International standards - Automotive Research Association of India (ARAI) - International Organization of Motor Vehicle Manufacturers (OICA)

Investor Community Resources - ValuePickr forum discussions - Reddit IndiaInvestments community - Twitter/X: Follow #BELRISE #IndianAutoComponents - LinkedIn: Company page and executive profiles

These resources provide multiple perspectives on Belrise Industries—from company-specific information to broader industry trends, from financial analysis to technological developments. For serious investors, combining insights from multiple sources while maintaining critical thinking about potential biases remains essential. The auto component sector's complexity demands comprehensive research, and these resources offer a solid foundation for informed investment decisions.

Note: This analysis is for informational purposes only and does not constitute investment advice. Prospective investors should conduct their own due diligence and consult with financial advisors before making investment decisions. All data and information are based on publicly available sources as of August 2025.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube