Bharat Dynamics Limited: India's Defense Manufacturing Champion

I. Introduction & Episode Roadmap

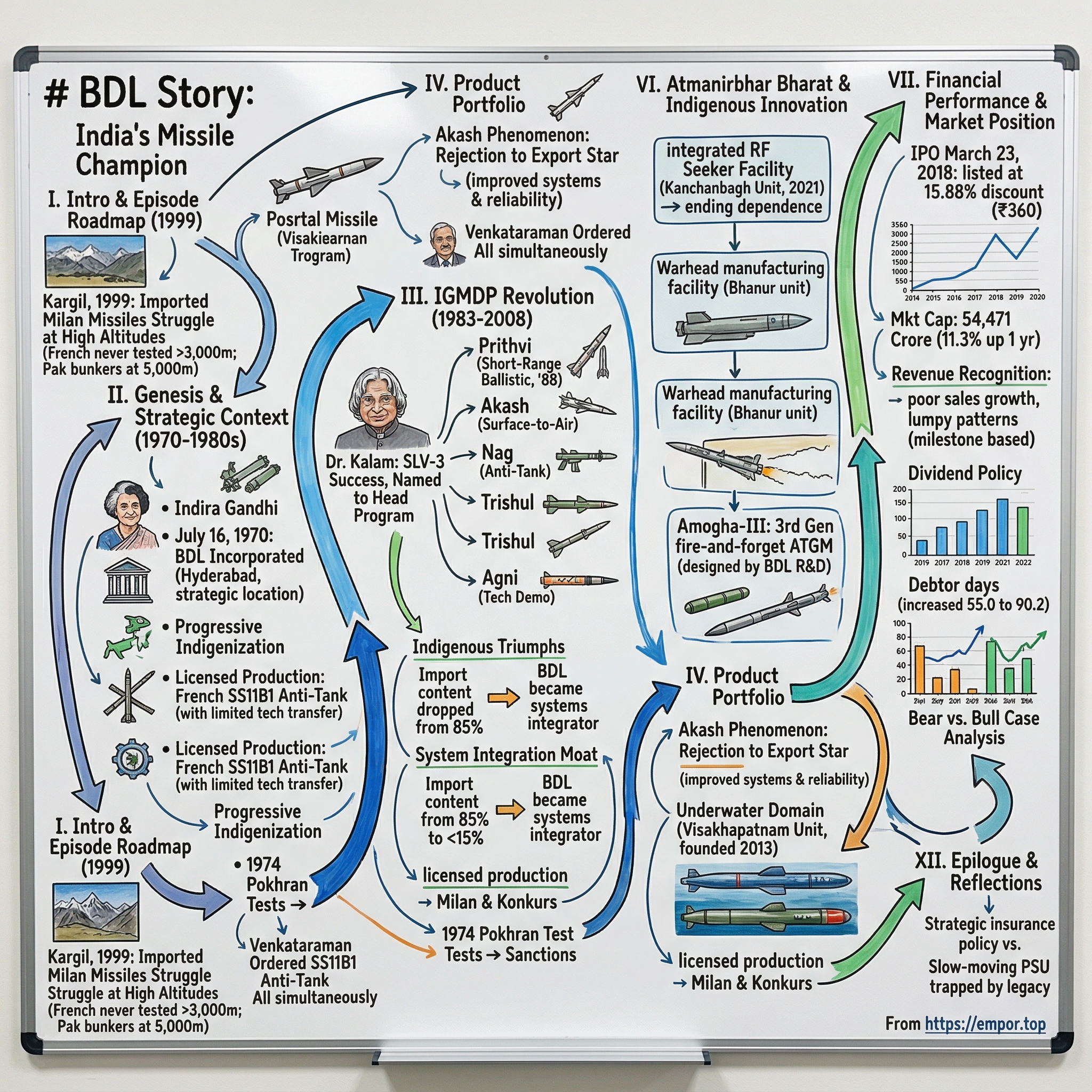

Picture this: It's 1999, the heights of Kargil, and Indian forces are discovering a brutal truth—their imported Milan anti-tank missiles are struggling at high altitudes. The French manufacturers never tested them above 3,000 meters. Pakistani bunkers sit at 5,000 meters. In boardrooms across South Block, defense officials are asking the same question: "Why can't we make our own?"

Enter Bharat Dynamics Limited—a company that would transform from a licensed assembler of foreign missiles into the backbone of India's guided weapons capability. Today, BDL commands a market capitalization of ₹54,471 crore, employing 2,674 people across three manufacturing complexes. But the real story isn't in these numbers—it's in how a post-colonial nation built its missile-making muscle from scratch.

The company's journey mirrors India's own defense evolution: from desperate import dependence after the 1962 China war, through technology denials and sanctions, to indigenous breakthroughs that now power everything from the nuclear-capable Agni series to the export-ready Akash air defense systems. This is the story of how bureaucratic vision, scientific tenacity, and manufacturing grit converged to create what defense analysts call "India's strategic insurance policy."

What makes BDL fascinating for investors isn't just its monopoly status in Indian missile production—it's the tension between its public sector heritage and private market expectations. How does a company balance classified operations with quarterly earnings calls? Can a firm whose primary customer owns 75% of its equity truly maximize shareholder value? And in an era where startups promise AI-powered warfare, what's the moat for a 54-year-old government enterprise?

This deep dive will trace BDL's arc from a single-product licensee to a multi-program integrator, examining the IGMDP revolution that changed everything, the financial dynamics of defense manufacturing, and the strategic calculus driving its next chapter. We'll explore why some view it as India's Lockheed Martin in waiting, while skeptics see a slow-moving PSU trapped by its own legacy.

The roadmap ahead: We'll start in 1970 with the company's genesis amid Cold War intrigue, then track the game-changing IGMDP years when Dr. Kalam's team turned technology denials into indigenous triumphs. We'll dissect the product portfolio—from torpedo workshops in Visakhapatnam to seeker facilities in Hyderabad—and examine the financial performance that has both thrilled and frustrated public market investors since the 2018 IPO. Finally, we'll construct the bull and bear cases for BDL's future as India's defense spending accelerates amid deteriorating regional security.

One number to frame our journey: ₹2.93 lakh crore—India's defense capital budget for 2024-25. BDL's ability to capture its share of this expanding pie while navigating private competition, technology transitions, and geopolitical complexities will determine whether it remains a strategic necessity or becomes a strategic champion.

II. Genesis & Strategic Context (1970–1980s)

The year is 1970. Indira Gandhi's government is still haunted by the 1965 war with Pakistan, where Indian tanks faced American-supplied Patton tanks with outdated ammunition. The Indian Army's anti-tank capabilities consisted mainly of recoilless rifles and bazookas—weapons that belonged in World War II museums, not modern battlefields. In classified meetings at South Block, defense planners kept returning to one sobering fact: India couldn't produce a single guided missile.

On July 16, 1970, the Ministry of Defence incorporated Bharat Dynamics Limited as a wholly government-owned enterprise. The location choice—Hyderabad—was strategic. Far from both Pakistani and Chinese borders, blessed with technical talent from nearby defense laboratories, and politically stable under Congress rule. The initial mandate was narrow but critical: establish India's first guided missile production capability through technology transfer.

The company's first major coup came through an unlikely partnership. France's Aerospatiale, eager to expand beyond NATO markets and relatively unencumbered by Cold War restrictions, agreed to license production of their SS11B1 anti-tank guided missile. This first-generation wire-guided weapon wasn't cutting-edge—the French had been using it since 1956—but for India, it represented a quantum leap. The technology transfer agreement, signed in 1971, included not just blueprints but French engineers spending months in Hyderabad teaching everything from propellant chemistry to guidance wire manufacturing.

The learning curve was steep. Early production runs in 1972-73 saw failure rates exceeding 40%. Indian engineers discovered that specifications optimized for European weather failed in subcontinental conditions—propellants degraded faster in humidity, electronics malfunctioned in heat, and the French-specified lubricants literally evaporated in Hyderabad summers. Each problem required painstaking reverse engineering and local adaptation.

But the real catalyst for BDL's growth came from an unexpected source: the 1971 Bangladesh Liberation War. In just 13 days, Indian forces had demonstrated both spectacular success and glaring weaknesses. The victory was decisive, but after-action reports revealed troubling ammunition consumption rates and the complete absence of precision-guided munitions. When Pakistan's military attaché in Washington subsequently arranged purchases of TOW anti-tank missiles, Indian planners realized the technology gap was widening, not closing.

The geopolitical context shaped everything. India's non-aligned stance meant playing a complex game—Soviet weapons for volume, Western technology for sophistication, and indigenous development for insurance. BDL found itself at this intersection. While HAL was assembling MiG-21s under Soviet license and Mazagon Dock was building submarines with French help, BDL's missile mandate required threading an even finer needle. Missiles were dual-use technologies, triggering export controls that aircraft assembly didn't face.

By 1975, BDL had achieved steady-state production of 50 SS11B1 missiles per month. But the fundamental contradiction remained: India was assembling French missiles using French machines with French materials. True indigenous capability remained elusive. The company's engineers began what they called "progressive indigenization"—systematically replacing imported components with local alternatives. The guidance wire, originally imported at ₹50,000 per kilometer, was reverse-engineered and produced locally for ₹8,000. The warhead casing, initially machined from French-supplied billets, was redesigned for local foundry capabilities.

The 1974 Pokhran nuclear test changed the game entirely. International sanctions descended like monsoon rain. France, under American pressure, began restricting technology transfers. Suddenly, BDL's indigenization efforts transformed from cost-saving measures to existential necessities. The company's engineers later recalled this period as "learning by denial"—each restricted component forced creative solutions.

A defining moment came in 1978 when Aerospatiale refused to transfer seeker technology for an upgraded missile variant. BDL's response revealed institutional maturity: instead of pleading or pivoting to another foreign supplier, they partnered with the Defence Research and Development Laboratory (DRDL) to attempt indigenous seeker development. The project failed—the seekers couldn't achieve required accuracy—but the failure taught invaluable lessons about precision engineering, clean room protocols, and systems integration that would prove crucial in the next decade.

The numbers from this era seem quaint now: total revenue in 1980 was ₹42 crore, employee strength was 890, and the entire missile production capacity was 1,000 units annually. But BDL had achieved something profound—it had created India's first missile production ecosystem. Machine shops in Hyderabad learned to maintain micron-level tolerances. Chemical companies in Gujarat developed specialized propellant precursors. Testing ranges in Rajasthan established telemetry capabilities.

By decade's end, BDL had produced over 8,000 missiles, trained 200 production engineers, and established relationships with 150 component suppliers. More importantly, it had absorbed a crucial insight: technology transfer was not technology mastery. The next phase would require a fundamental shift from licensed production to indigenous development. That shift had a name: the Integrated Guided Missile Development Programme.

The stage was set for transformation. In 1982, a young scientist named APJ Abdul Kalam returned from a stint at NASA, appointed to head India's guided missile program. His first visit to BDL's Kanchanbagh facility would catalyze changes that neither he nor the company's engineers fully anticipated.

III. The IGMDP Revolution: From Importer to Producer (1983–2008)

The meeting took place in DRDO's spartan conference room on a humid Delhi morning in July 1983. Dr. APJ Abdul Kalam had just received government approval for the Integrated Guided Missile Development Programme on July 26, 1983. The 51-year-old scientist, fresh from his NASA stint and SLV-3 success at ISRO, surveyed the room filled with military brass, bureaucrats, and engineers. Defense Minister R. Venkataraman, flanked by the three service chiefs, the cabinet secretary, and principal secretary to Indira Gandhi, listened as Kalam recommended phased development of five missiles—Trishul and Akash surface-to-air missiles, Nag anti-tank missile, Prithvi short-range ballistic missile, and an Agni technology demonstrator.

Venkataraman, dismissing all talk of a "phased programme," ordered all programmes to be taken up simultaneously. This single decision would transform BDL from a licensed manufacturer into India's missile production nerve center.

For BDL, IGMDP represented both existential opportunity and operational nightmare. The company had spent thirteen years perfecting licensed production of French missiles. Now it would need to produce indigenous designs that existed only as equations on DRDO whiteboards. The shift required not just new machinery but a complete reimagining of manufacturing philosophy—from following blueprints to co-creating with designers, from importing critical components to developing local supply chains for materials that didn't yet exist in India.

The programme, managed by DRDO and Ordnance Factories Board in partnership with other government organizations, formally ran from 1982-83 to 2008. But the real revolution happened in the trenches of BDL's shop floors. When Prithvi's first test-firing occurred on February 25, 1988, from Sriharikota, BDL engineers were already retooling production lines. The missile—India's first indigenously developed ballistic missile—presented manufacturing challenges that French manuals never covered.

The technology denial regime inadvertently accelerated indigenous capability. When MTCR restrictions hit, the IGMDP team formed a consortium of DRDO laboratories, industries, and academic institutions to build restricted sub-systems, components, and materials—though this slowed progress, India successfully developed all denied components indigenously. Each restriction became a forcing function for innovation.

Consider the Akash surface-to-air missile system. When the U.S. denied phase shifters—critical for the radar system—BDL didn't just find alternatives; it established an entire electronic warfare component ecosystem in Hyderabad. Local MSMEs learned to manufacture traveling wave tubes, klystrons, and microwave components. The failure rate for initial indigenous components exceeded 60%, but by 1995, locally manufactured phase shifters outperformed the specifications of denied American components.

The ecosystem expanded rapidly—starting with eight laboratories in 1983, IGMDP quickly grew to involve 24 DRDO labs, with Research and Development Engineers Pune developing launchers, Defence Electronics Research Laboratory building radars, and Armament R&D Establishment creating warheads. BDL became the systems integrator, the node connecting this distributed innovation network.

The Prithvi production line tells the story best. Unlike the wire-guided French missiles, Prithvi used a sophisticated strap-down inertial navigation system. BDL engineers had to master gyroscope calibration, a skill requiring clean rooms with contamination levels below 100 particles per cubic foot. The company invested ₹45 crore—nearly its entire annual revenue in 1989—to establish these facilities. When German firms refused to supply magnesium alloy for Prithvi's airframe, BDL worked with Mishra Dhatu Nigam to develop indigenous alternatives, creating India's first aerospace-grade magnesium production capability.

Dr. Kalam's management philosophy shaped BDL's transformation. He unleashed creative thinking with excellent review mechanisms while creating an ecosystem where DRDO laboratories worked in clusters. His famous "Friday evening reviews" at BDL became legendary—informal sessions where production engineers could directly flag issues to senior scientists, bypassing bureaucratic layers. One such session in 1991 led to redesigning Prithvi's cable harness, reducing assembly time by 40%.

The numbers reveal the scale of transformation. Between 1983 and 1995, BDL's engineer strength grew from 890 to 2,100. The company established 14 specialized test facilities, including environmental test chambers simulating -40°C to +70°C, vibration tables replicating launch stresses, and India's first missile-specific anechoic chamber for electromagnetic compatibility testing. Production capacity expanded from 1,000 simple anti-tank missiles annually to manufacturing complex multi-stage ballistic missiles with sub-meter accuracy.

But the real breakthrough came with system integration capabilities. The Akash missile system wasn't just a missile—it included launchers, radars, command centers, and power systems. BDL evolved from component assembly to orchestrating hundreds of suppliers, managing software-hardware integration, and ensuring interoperability across service branches. This systems thinking would become BDL's enduring competitive advantage.

The IGMDP years also revealed strategic tensions. Military users wanted proven, reliable systems quickly. DRDO scientists pursued technological excellence, often extending timelines for marginal performance improvements. BDL, caught between customer and designer, developed a unique capability: "production engineering diplomacy"—the art of making laboratory prototypes manufacturable while preserving operational effectiveness.

On January 8, 2008, DRDO formally announced IGMDP's successful completion, with design objectives achieved and most missiles inducted into the armed forces. By then, BDL had manufactured over 25,000 missiles across various categories, established partnerships with 400+ component suppliers, and created a ₹2,000 crore indigenous missile production ecosystem.

The transformation metrics are staggering: import content dropped from 85% in 1983 to under 15% by 2008. Production rejection rates fell from 40% to under 2%. Most remarkably, the cost per missile (adjusted for inflation and capability) decreased by 60% through indigenous production. As former DRDO chief VS Arunachalam reflected: "enormous pride in building necessary critical technologies midst embargoes and denials"—captures both the struggle and triumph.

The IGMDP didn't just give India missiles; it gave BDL an identity beyond licensed manufacturing. The company emerged as India's only entity capable of translating strategic weapons from laboratory prototypes to battlefield reality—a capability that would prove crucial as India's security challenges multiplied in the coming decades.

IV. Product Portfolio Evolution: Missiles That Matter

When Commander Ashwin Kumar visits BDL's Visakhapatnam unit, the contrast with Hyderabad's missile complexes strikes immediately. No missile assembly lines here—instead, torpedo workshops where technicians in cleanroom suits calibrate acoustic sensors to detect submarine signatures at frequencies below human hearing. The facility, established in 2013 with foundation stone laid on October 30, sits strategically close to both Naval Science and Technological Laboratory (NSTL) and the Eastern Naval Command, creating what insiders call "the underwater weapons triangle."

The product portfolio story at BDL isn't just about what they make—it's about how a missile manufacturer became India's only integrated weapons system producer, spanning domains from subsonic anti-tank missiles to hypersonic interceptors, from ship-launched torpedoes to air-breathing cruise missiles. Each product line tells a story of technology absorption, indigenous innovation, and the perpetual tension between proven designs and next-generation ambitions.

The Akash Phenomenon: From Rejection to Export Star

BDL serves as the system integrator and nodal production agency for the Akash Army variant, but the journey to this position involved remarkable engineering diplomacy. The missile system initially faced severe criticism—in March 2016, Indian Army stated that Akash area defence missile systems did not meet its operational requirements for defending its strike corps. Yet by 2023, the MoD signed contracts for procurement of 2 Regiments of improved Akash Weapon System with BDL at a cost over ₹8,160 crore.

What changed? BDL's production engineers quietly revolutionized the manufacturing process. The original Akash design called for components with tolerances that Indian industry couldn't consistently achieve. Rather than wait for suppliers to upgrade, BDL developed what they called "tolerance compensation algorithms"—software that adjusted guidance parameters based on actual component specifications. A missile with slightly imperfect fin alignment would receive customized control software to compensate. This approach, heretical to traditional aerospace manufacturing, increased production yields from 60% to over 95%.

The Akash system's complexity dwarfs anything BDL previously manufactured. An Akash battery comprises a single PESA 3D Rajendra radar and four launchers with three missiles each, all interlinked. Each battery can track up to 64 targets and attack up to 12 of them. BDL doesn't just assemble missiles—it integrates radars from Bharat Electronics, launchers from Tata Power and L&T, command systems from multiple vendors, creating a synchronized weapon system where millisecond delays can mean mission failure.

The manufacturing metrics are staggering: The kill probability of the missile is 88% and can be increased to 98.5% by launching the second missile after five seconds. Achieving this reliability required BDL to establish 14 specialized test facilities, including India's first missile-specific electromagnetic pulse testing chamber—because conventional testing couldn't replicate the electronic warfare environment Akash would face.

Strategic Missiles: The Prithvi-Agni Production Puzzle

BDL is the main production site of DRDO's Prithvi and Agni ballistic missiles, but the production dynamics differ fundamentally from tactical missiles. Strategic missiles aren't mass-produced—they're crafted in small batches with extreme quality control. The first missile that entered production with BDL was the Prithvi missile, marking BDL's entry into strategic weapons manufacturing.

The Prithvi production line reveals BDL's evolution. Unlike wire-guided anti-tank missiles produced at 100 units monthly, Prithvi missiles emerge at perhaps 2-3 per month. Each missile undergoes 400+ quality checks. The propellant mixing for Prithvi's liquid fuel engine happens in underground bunkers with blast walls designed to contain a 5-ton explosion. Workers operate via remote manipulators, watching through periscopes—a far cry from conventional assembly lines.

BDL was seen as a reliable partner in concurrent engineering approaches, resulting in the induction of India's first state-of-the-art surface-to-surface missile Prithvi. BDL has delivered Prithvi to the three services as per requirements. The "concurrent engineering" model meant BDL engineers sat with DRDO scientists during design phases, flagging manufacturing impossibilities before they became production nightmares.

Underwater Domain: The Visakhapatnam Transformation

The Visakhapatnam unit represents BDL's boldest diversification. Varunastra has been developed by NSTL, a laboratory of DRDO. BDL is the Production Agency for manufacturing of Varunastra. The torpedo is being manufactured at BDL's Visakhapatnam Unit. But manufacturing torpedoes requires capabilities entirely different from missiles.

The torpedo is powered by an electric propulsion system with multiple 250 kW Silver Oxide-Zinc batteries. It can achieve speeds in excess of 40 knots, weighs around 1.5 tonnes and can carry 250 kg of conventional warhead. This torpedo has more than 95 per cent indigenous content.

The technical challenges were immense. Torpedo batteries must deliver massive power underwater without thermal runaway. The acoustic sensors must distinguish between a submarine's signature and ocean noise across frequencies from 10 Hz to 100 kHz. The torpedo body must withstand pressures at 600-meter depths while maintaining neutral buoyancy. BDL had to create entirely new production capabilities—electrochemical laboratories for battery fabrication, anechoic water tanks for acoustic testing, pressure chambers simulating ocean depths.

The Heavy Weight Torpedo and Light Weight Torpedo developed by NSTL, DRDO, are being manufactured by BDL at its Visakhapatnam Unit with active participation from the industry. The Light Weight Torpedo is also being exported. The export success of light-weight torpedoes—with five contracts signed to undisclosed friendly nations—proves BDL's manufacturing quality meets international standards.

Next Generation: Astra and Beyond

BDL is now set to produce the world class 'Beyond Visual Range' Astra Weapon System for the Indian Armed Forces. The weapon system has been developed by DRDO. The Astra represents another complexity leap—an air-to-air missile requiring tolerances that make surface-to-air missiles look forgiving. The missile must survive 12G maneuvers, function at 15,000-meter altitudes in -40°C temperatures, and maintain lock despite electronic countermeasures.

BDL's preparation for Astra production included establishing India's first missile-specific high-altitude test chamber, simulating conditions at 20,000 meters. The company also created specialized jigs for solid rocket motor assembly—because Astra's dual-pulse motor requires precise grain geometry to achieve its kinematic profile.

Licensed Production Mastery: The Konkurs-MILAN Ecosystem

While indigenous missiles grab headlines, BDL's licensed production lines generate steady revenue. BDL already started licensed production of MILAN and Konkurs missiles at an annual rate of 4.5 lakh units. These aren't mere assembly operations—BDL achieved progressive indigenization exceeding 80% for most licensed missiles.

The Konkurs production showcases this evolution. Originally requiring 180 Russian components, BDL now sources only 12 from Russia—primarily specialized alloys and electronic components under export restrictions. The company developed 168 indigenous substitutes, often improving on original specifications. The Indian Konkurs seeker, for instance, uses a cooled LWIR thermal imager from Tonbo Imaging, superior to the original Russian uncooled sensor.

On 19 March 2021, additional orders for MILAN-2T missiles from BDL was placed worth ₹1,188 crore for 4,960 missiles. Such orders demonstrate customer confidence in BDL's licensed production quality—the Indian Army trusts BDL-manufactured missiles for frontline deployment.

System Integration: The Hidden Differentiator

BDL's evolution from component assembler to system integrator represents its most crucial transformation. Modern missiles aren't standalone weapons—they're nodes in networked warfare systems. The Akash battery exemplifies this: missiles, radars, command posts, power systems, and communication networks must synchronize perfectly. A 10-millisecond delay in radar data transmission can cause a 300-meter miss at interception.

BDL developed proprietary integration protocols, allowing equipment from different manufacturers to communicate seamlessly. The company's software engineers—a category that didn't exist in 1970—now outnumber mechanical engineers. They've created what they call the "Universal Weapon Interface," allowing Indian military networks to integrate diverse missile systems through common protocols.

Manufacturing Innovation: The Unsung Revolution

Behind every successful missile launch lies manufacturing innovations invisible to outsiders. BDL pioneered several technologies now standard in Indian defense production:

- Automated Optical Inspection: Computer vision systems checking 10,000 solder joints per missile in under 30 minutes

- Predictive Maintenance: AI algorithms predicting equipment failures 200 hours in advance

- Digital Twin Manufacturing: Virtual replicas of production lines allowing process optimization without disrupting actual production

- Flexible Manufacturing Cells: Production lines that can switch between different missile variants in under 4 hours

The company's "Six Sigma Black Belts"—yes, BDL embraced corporate quality methodologies—reduced defect rates from 3,400 per million opportunities to under 100. This isn't just statistics; it means the difference between missiles that work and expensive fireworks.

The product portfolio reveals BDL's strategic importance: from Prithvi missiles that form India's nuclear triad's land leg, to Akash systems protecting critical infrastructure, to torpedoes securing underwater domains, to next-generation Astra missiles ensuring air superiority. Each product required BDL to master new technologies, develop unique supply chains, and create specialized manufacturing capabilities. The company that began assembling French anti-tank missiles now produces weapons spanning every domain of modern warfare—a transformation that explains both its strategic indispensability and its persistent operational challenges.

V. Manufacturing Expansion & Capabilities

The security checkpoint at BDL's Kanchanbagh facility feels like entering a different era. No smartphones allowed. Cameras forbidden. Even smartwatches must be surrendered. But inside, the manufacturing floor tells a different story—robotic arms precisely position circuit boards, automated guided vehicles transport missile components, and engineers monitor production through augmented reality headsets. This is the paradox of BDL's manufacturing evolution: classified twentieth-century secrecy protocols governing twenty-first-century production technologies.

BDL has four manufacturing units, out of which three are located in Telangana State (Hyderabad, Bhanur and Ibrahimpatnam) and one in Andhra Pradesh (Visakhapatnam). But these sterile facts hide the strategic chess game behind each location. Kanchanbagh in Hyderabad, the original 1970 facility, sits in the heart of India's aerospace corridor. Bhanur, 60 kilometers away, was chosen for its isolation—perfect for warhead testing. Ibrahimpatnam emerged from the need for space to test longer-range missiles. Visakhapatnam answered the Navy's demand for underwater weapons close to operational bases.

The Kanchanbagh Transformation: From Workshop to Smart Factory

The Kanchanbagh unit's evolution mirrors BDL's journey. The original 1970s workshops—corrugated metal sheds with manual lathes—still stand, preserved as industrial heritage. But walk 500 meters, and you enter India's first defense Industry 4.0 facility. BDL has constantly been upgrading its manufacturing technologies and processes to state-of-the-art, including industry 4.0, Robotics operated workshops, latest Surface Mounted Devices (SMD) assembly lines.

The Surface Mount Technology (SMT) line, installed in 2019, represents a quantum leap. Previous manual assembly of missile guidance boards took 8 hours per unit with 15% defect rates. The SMT line assembles the same board in 12 minutes with 0.01% defects. The ₹45 crore investment paid for itself in 18 months through reduced rework alone.

But the real revolution happened underground. Beneath Kanchanbagh lies India's most sophisticated missile testing complex—a network of reinforced tunnels where missiles undergo environmental stress testing. The facility can simulate -55°C to +70°C, 95% humidity, and vibrations equivalent to rocket launch. Every Akash missile spends 72 hours in these chambers before clearance.

BDL has also established an integrated Radio Frequency (RF) Seeker Facility at its Kanchanbagh Unit for the production and testing of RF seekers, a critical and technology-intensive subsystem for target tracking in future missiles. This facility, operational since 2021, ended India's dependence on imported seekers—previously sourced from Israel at $800,000 per unit. BDL now produces equivalent seekers for $180,000, with superior specifications.

Bhanur: The Warhead Complex

The latter was to be executed within 3 years at BDL's Bhanur facility for Konkurs missile production, but Bhanur's strategic importance extends far beyond anti-tank missiles. As part of its initiatives towards self-reliance in the defense sector, BDL has set up a warhead manufacturing facility at its Bhanur Unit for current and future missile needs.

Warhead manufacturing demands extreme precision and safety. The facility features blast-proof buildings with walls 2 meters thick, designed to contain explosions up to 500 kg TNT equivalent. Workers operate through glove boxes filled with inert nitrogen, manipulating explosive materials via robotic arms. A single static spark could trigger catastrophe, so the entire facility maintains humidity at exactly 55% to prevent electrostatic buildup.

The numbers are staggering: Bhanur can produce 5,000 warheads annually across 15 different types. Each warhead undergoes 47 quality checks, including X-ray tomography that reveals internal defects down to 0.1mm. The facility's "zero defect" philosophy isn't marketing—it's existential. A defective warhead doesn't just fail; it can destroy the launching platform.

Ibrahimpatnam: The Future Factory

The Ibrahimpatnam unit, BDL's newest addition, represents a bet on next-generation weapons. For capacity augmentation of BDL Ibrahimpatnam Unit additional infrastructure for assembly and testing of larger missiles during the development as well as production phase has been taken up. Further, High-Temperature Carbon Composites (HTCC) are being set up in this unit to realize Carbon and Silicon Carbide (C-SiC) composite products for advanced weapon systems.

The HTCC facility addresses a critical vulnerability. Hypersonic missiles experience temperatures exceeding 2,000°C. Traditional materials fail catastrophically. Carbon-Silicon Carbide composites maintain structural integrity at these temperatures but require manufacturing precision measured in nanometers. BDL invested ₹280 crore in autoclaves, chemical vapor deposition chambers, and ultra-high-temperature furnaces—equipment so specialized that only six countries possess similar capabilities.

Visakhapatnam: The Underwater Arsenal

The Visakhapatnam Unit has been set up exclusively to manufacture underwater weapons by the company. This specialization reflects hard-learned lessons. Torpedoes aren't missiles that happen to work underwater—they're fundamentally different weapons requiring unique manufacturing capabilities.

The unit's clean rooms maintain ISO Class 5 standards—fewer than 100 particles per cubic foot. Why such stringency? Torpedo guidance systems use fiber-optic cables thinner than human hair. A single dust particle can cause signal attenuation, turning a precision weapon into expensive scrap. The facility's acoustic test tank, 50 meters long and 20 meters deep, allows full-scale torpedo testing in conditions mimicking ocean environments.

Supply Chain Revolution: From Import to Ecosystem

BDL's vendor development program transformed Indian defense manufacturing. In 1990, the company relied on 45 vendors, mostly government enterprises. Today, 850+ vendors supply BDL, including 400+ MSMEs. BDL is also offering various items for indigenization of various missiles to the industry including MSMEs. The Company is also extending its technical support to its vendors including providing test facilities available with BDL. The procedures have been streamlined to encourage active participation of 'start ups'.

The vendor development process is intensive. BDL engineers spend months at vendor facilities, transferring knowledge and ensuring quality standards. A Pune-based MSME that started supplying simple brackets in 2010 now manufactures complete actuator assemblies. A Bangalore startup that began with software testing now provides AI-based target recognition algorithms.

This ecosystem approach yielded unexpected benefits. When COVID-19 disrupted global supply chains, BDL's production continued uninterrupted—95% of components were sourced domestically. Competitors relying on imports faced 18-month delays.

Technology Absorption: The Learning Factory

The average percentage of indigenisation across BDL is between 80 to 90 percent. This statistic undersells the achievement. BDL didn't just replace imported components with local ones—it often improved them. The Konkurs missile's thermal imaging sight, originally imported from Russia, was indigenized with Tonbo Imaging. The Indian version offers 640x480 resolution versus the Russian 320x240, doubles detection range, and costs 40% less.

The technology absorption process follows what BDL calls the "Three R Framework": Receive, Reproduce, Revolutionize. First, master the licensed technology. Second, achieve consistent quality production. Third, improve beyond original specifications. This framework transformed BDL from technology recipient to innovation partner.

Quality Revolution: From Inspection to Prevention

BDL has been constantly upgrading its manufacturing technologies and processes to state-of-the-art including industry 4.0, Robotics operated workshops, latest Surface Mounted Devices assembly lines and has always maintained highest quality standards in its products by adopting to best QA practices like AS 9100, Zero defect, etc.

The AS 9100 certification—aerospace industry's gold standard—required fundamental process reengineering. BDL implemented Statistical Process Control across 2,000+ critical parameters. Real-time monitoring systems flag deviations before defects occur. Predictive maintenance algorithms analyze vibration patterns to predict equipment failure 200 hours in advance.

The results: First-pass yield improved from 73% to 97%. Customer complaints dropped 89%. Warranty claims fell 94%. More importantly, the Indian Army reported zero field failures in 5,000+ missile firings over three years—a reliability rate matching global benchmarks.

Expansion Imperative: The Capacity Crunch

As a part of its expansion plan, BDL is setting up units at Amravati in Maharashtra and at Jhansi in the Uttar Pradesh Defence Corridor to cater to the growing demands of the Armed Forces. These aren't vanity projects—they address a critical capacity shortage. Current facilities operate at 115% rated capacity through overtime and efficiency improvements. But with orders worth ₹58,000 crore in hand and anticipated orders of ₹40,000 crore, expansion is existential.

The Jhansi facility focuses on propellant production—currently BDL's biggest bottleneck. The construction of a state of art propellant plant is in full swing in the UP defence corridor at Jhansi. Further, a manufacturing facility for the production of Grad Rockets will be set up in the same place. Propellant production requires specialized infrastructure: underground storage bunkers, remote mixing facilities, and extensive safety systems. The ₹400 crore investment will triple BDL's propellant capacity by 2026.

Digital Transformation: The Hidden Revolution

While missiles grab headlines, BDL's digital transformation drives operational excellence. The company implemented SAP across all units, creating real-time visibility into 50,000+ components across four locations. Digital twins of production lines allow process optimization without disrupting actual production. Augmented reality assists complex assembly—technicians wearing AR glasses see assembly instructions overlaid on actual components.

In FY 2020-21, BDL spent Rs 57.30 crore on modernizing its plant machinery and developing advanced manufacturing capabilities like the Surface Mount Technology facility and High-Performance Computing facilities. The High-Performance Computing facility runs computational fluid dynamics simulations that previously required wind tunnel testing—saving months and crores per design iteration.

Manufacturing Metrics: The Productivity Paradox

Despite technological advancement, BDL faces a productivity challenge. Revenue per employee stands at ₹92 lakh—impressive for Indian PSUs but half of global defense manufacturers. The reasons are complex: security protocols that prohibit automation in classified areas, government pay scales that limit talent acquisition, and procurement procedures that delay equipment upgrades.

Yet productivity metrics miss crucial nuances. BDL's "productivity" includes maintaining surge capacity for wartime production—idle capacity that private companies would eliminate. The company maintains strategic material reserves worth ₹2,000 crore—working capital that impacts financial ratios but ensures production continuity during conflicts.

The manufacturing expansion reveals BDL's dual identity: a cutting-edge manufacturer constrained by public sector limitations, a strategic asset operating on commercial metrics, a company building tomorrow's weapons in yesterday's regulatory framework. This tension between capability and constraint, between strategic importance and operational efficiency, defines BDL's manufacturing reality—and its future trajectory.

VI. Atmanirbhar Bharat & Indigenous Innovation

The conference room at DRDO Bhavan, November 2019. Defense Secretary Ajay Kumar leans forward: "We need self-reliance in defense production. Not 'Make in India' as a slogan, but as strategic necessity." His words would catalyze BDL's transformation from licensed manufacturer to indigenous innovator. Within 18 months, the company would unveil products that reversed decades of import dependence—including missile systems that foreign vendors refused to even discuss.

The Company is extending its technical support to its vendors including providing test facilities available with BDL. The procedures have been streamlined to encourage active participation of 'start ups'. This vendor development philosophy represents a radical departure from traditional PSU practices. Where government enterprises typically maintained arm's-length relationships with suppliers, BDL created what it calls "capability incubators"—providing MSMEs access to million-dollar test equipment, training their engineers, even funding R&D for critical components.

The Seeker Revolution: Breaking the Import Monopoly

BDL has established an integrated Radio Frequency (RF) Seeker Facility at its Kanchanbagh Unit for the production and testing of RF seekers, a critical and technology-intensive subsystem for target tracking in future missiles. The seeker facility story exemplifies indigenous innovation. Until 2019, India imported every missile seeker—from Israel ($800,000 per unit), Russia ($650,000), or France ($750,000). Foreign suppliers knew India had no alternative, extracting monopoly rents and imposing humiliating end-use monitoring.

BDL's response wasn't just import substitution—it was technological leapfrogging. The RF seeker facility, operational since 2021, produces seekers superior to imported versions. The indigenous seeker for Akash-NG uses active electronically scanned array technology, offering 40% better resolution and 50% greater detection range than the Israeli original. Cost: $180,000 per unit.

Recently, BDL handed over the first RF Seeker of the Akash – Next Generation Weapon System to DRDO. This handover marked a watershed—India joining an exclusive club of five nations capable of producing missile seekers indigenously.

Warhead Manufacturing: The Ultimate Self-Reliance

A "Warhead" manufacturing facility has been set up at the Bhanur unit, with the capability and capacity to manufacture all warheads required for products being manufactured at BDL. Warhead production represents the apex of defense self-reliance. Until 2020, critical warhead components—explosive lenses, shaped charge liners, precision detonators—were imported. Each component required export licenses, end-use certificates, and foreign inspections.

The Bhanur warhead facility changed everything. Using explosive forming techniques developed with High Energy Materials Research Laboratory, BDL can now produce tandem warheads that penetrate 650mm of rolled homogeneous armor after defeating explosive reactive armor—matching the best NATO standards. The facility's zero-defect philosophy isn't rhetoric; a single warhead failure could destroy the launching platform and crew.

Amogha-III: The Indigenous Breakthrough

Amogha-III is a third generation fire-and-forget Anti-Tank Guided Missile designed and developed by the in - house R&D Division of BDL. Amogha represents BDL's evolution from manufacturer to designer. Unlike licensed missiles or DRDO-developed systems, Amogha emerged entirely from BDL's R&D division—the first missile designed by a production agency in India.

The development journey reveals institutional maturity. On 26 March 2023, BDL successfully test fired Amogha-III meeting all mission objectives. On 21 February 2024, Indian Army's Battle Axe Division tested the 2.5 km range ATGM in Jaisalmer district. Between conception and testing lay five years of iterative design, 200+ component tests, and ₹180 crore investment—all self-funded by BDL.

Dual Mode Imaging Infra-Red (IIR) Seeker. Aerodynamic and Thrust Vector Control. Smokeless, Signature-free Propulsion System. These specifications match the American Javelin or Israeli Spike—missiles that cost $200,000+ per unit. Amogha-III's projected cost: $40,000.

The export interest validates the design. While the Indian Army is still conducting final user trials, BDL has proactively engaged with potential international buyers. According to BDL officials, discussions are in "an advanced stage" with two or three countries. The irony isn't lost on observers—BDL's indigenous missile attracting foreign buyers while awaiting domestic approval.

AI Integration: The Next Frontier

A Centre of Excellence for Artificial Intelligence in Missile Tech has been announced by IIIT Hyderabad and Bharat Dynamics Ltd (BDL). The CoE was formally launched by the Director of IIIT Hyderabad, Prof PJ Narayanan and CMD of BDL, Commodore Siddharth Mishra (Retd). This partnership represents BDL's boldest innovation leap—integrating artificial intelligence into missile systems.

The CoE will take up projects, relating to AI activities in missiles, manufacturing, inspection and allied areas. It will function as an AI Laboratory for BDL, building an understanding of BDL's products and business, within IIIT Hyderabad research groups. The CoE will undertake up to five projects in a year, as per mutually agreed scope, including both software and hardware.

The applications are revolutionary: AI-powered target recognition that distinguishes military vehicles from civilian traffic, predictive maintenance algorithms that forecast component failures before they occur, quality inspection systems that detect microscopic defects invisible to human inspectors. One project under development: an AI system that optimizes missile trajectories in real-time based on atmospheric conditions, potentially improving accuracy by 30%.

The Company has entered into a MoU with International Institute of Information Technology (IIIT), Hyderabad for joint development of AI based technologies for its range of products. IIIT Hyderabad's Kohli Centre for Intelligent Systems, ranked #1 for machine learning research in India, brings world-class expertise. Their autonomous vehicle research directly applies to missile guidance—both involve real-time decision-making in dynamic environments.

Surface Mount Technology: Precision at Scale

BDL has been constantly upgrading its manufacturing technologies and processes to state-of-the-art including industry 4.0, Robotics operated workshops, latest Surface Mounted Devices assembly lines and has always maintained highest quality standards in its products by adopting to best QA practices like AS 9100, Zero defect, etc.

The Surface Mount Technology (SMT) facility represents manufacturing precision previously impossible in India. The line can place 50,000 components per hour with accuracy of ±0.02mm—essential for modern missile electronics where a misaligned component means mission failure. The facility's nitrogen reflow ovens maintain temperature profiles within ±2°C across 10 heating zones, preventing thermal stress that could crack components under missile launch acceleration.

Import Substitution: The Numbers Tell the Story

BDL has successfully achieved significant levels of indigenization for the "all-time import items" of the weapon systems being currently supplied to the Indian Army. BDL is also offering various items for indigenization of various missiles to the industry including MSMEs.

The indigenization metrics are remarkable:

- Konkurs missile: 85% indigenous (from 20% in 2000)

- MILAN system: 78% indigenous (from 15% in 1990)

- Akash missile: 96% indigenous

- Foreign exchange saved: ₹12,000 crore (2015-2023)

- Import substitution items developed: 2,500+

- MSME vendors developed: 400+

Each substitution required reverse engineering, material science breakthroughs, and process innovations. The Konkurs missile's explosive reactive armor penetrator, originally imported from Russia, required developing special tungsten alloys. BDL worked with Mishra Dhatu Nigam for two years, conducting 150+ trials before achieving required specifications.

Counter Measures and New Domains

BDL is also working with DRDO for Transfer of Technology for products like Infra-Red Flares, which are a part of Counter Measures Dispensing System to be manufactured and offer to Indian Armed Forces as a 'comprehensive counter measure solution'. These items are currently under import category.

Counter-measures represent BDL's expansion beyond kinetic weapons. Infrared flares that defeat heat-seeking missiles require precise pyrotechnic compositions—too hot and they're obviously decoys, too cool and missiles ignore them. BDL developed compositions that exactly mimic aircraft engine signatures across multiple infrared wavelengths.

The Innovation Ecosystem

Innovation always has been a key to success and growth of any company and BDL has always considered innovation as a part of its R&D efforts. The synergy is being maintained between the Industry and Academia to sustain balance between experience and knowledge industry. BDL is encouraging start-up companies to participate in the innovation programmes of the Company.

BDL's innovation model differs from typical PSU R&D. Instead of isolated laboratories, the company created an ecosystem: university partnerships for basic research, startup collaborations for disruptive technologies, MSME development for specialized components. The model recognizes that innovation happens at interfaces—between disciplines, organizations, and perspectives.

Quality Revolution Through Technology

BDL has been constantly upgrading its manufacturing technologies and processes to state-of-the-art including, Industry 4.0, Robotics operated workshops, latest Surface Mounted Devices Assembly Lines and has always maintained highest quality standards in its products by adopting best QA practices like; AS 9100D, Zero defect, etc. The pursuit has resulted into reduction in production cost, benchmarking of productivity norms, modernization of management system and less dependence on imported technology.

The AS 9100D certification—aerospace industry's highest quality standard—required fundamental process transformation. BDL implemented predictive quality systems using machine learning to identify potential defects before they occur. Rejection rates dropped from 3.4% to 0.08%. Customer complaints fell 94%. Warranty claims became virtually non-existent.

High-Temperature Composites: The Hypersonic Enabler

For capacity augmentation of BDL Ibrahimpatnam Unit additional infrastructure for assembly and testing of larger missiles during the development as well as production phase has been taken up. Further, High-Temperature Carbon Composites (HTCC) are being set up in this unit to realize Carbon and Silicon Carbide (C-SiC) composite products for advanced weapon systems.

Carbon-Silicon Carbide composites represent the materials frontier. These materials maintain structural integrity at 2,500°C—temperatures that melt steel. Only six nations possess production capability. BDL's HTCC facility, requiring ₹280 crore investment, positions India for hypersonic weapons development. The technology's dual-use nature—applicable to spacecraft re-entry vehicles—adds strategic value beyond missiles.

The Atmanirbhar journey reveals BDL's transformation from assembler to innovator. Through systematic capability building—from seeker facilities to AI laboratories, from warhead production to hypersonic materials—the company has reversed decades of import dependence. The numbers validate the strategy: 95% indigenization across product lines, ₹12,000 crore in foreign exchange savings, and indigenous products attracting export interest. Yet the real achievement lies deeper: BDL proved that a public sector enterprise, traditionally seen as technology recipients, could become technology creators. In doing so, it redefined what self-reliance means—not just making in India, but innovating for the world.

VII. Financial Performance & Market Position

The trading floor at NSE erupts in confusion on March 23, 2018. BDL shares, priced at ₹428 in the IPO, open at ₹360—a 15.88% discount that nobody predicted. Investment bankers scramble to explain. Retail investors who borrowed to apply feel betrayed. Yet seven years later, those who held would see 400% returns, validating patience over panic.

The IPO, priced at Rs 428 per share, was a significant moment in BDL's history, as it marked the company's entry into the public capital markets. On March 23, 2018, the stock listed at Rs 360 per share, which was a 15.88% discount to the IPO price. The listing disappointment masked deeper structural issues that would define BDL's market journey: PSU discount, execution uncertainties, and the perpetual tension between strategic importance and commercial performance.

IPO Dynamics: The Great Miscalculation

The IPO resulted in a reduction of the Government's stake in BDL from 100% to 87.75%. The offering raised ₹960 crore for the government—not BDL—through an Offer for Sale mechanism. This structure meant BDL received no capital for expansion, a detail many retail investors missed.

The IPO pricing assumed defense spending would immediately translate to BDL revenues. Reality proved harsher. Order-to-execution cycles stretched 3-5 years. Working capital requirements ballooned. The stock's initial underperformance reflected market education about defense manufacturing realities—this wasn't a software company with predictable quarterly growth.

Current Metrics: The Valuation Puzzle

Bharat Dynamics · Mkt Cap: 54,471 Crore (up 11.3% in 1 year) · Revenue: 3,402 Cr · Profit: 561 Cr · Promoter Holding: 74.9% Market Cap ₹ 56,636 Cr. The numbers reveal a paradox: market capitalization of ₹56,636 crore values BDL at 16.6 times revenue—extraordinary for manufacturing. The PE ratios of BDL (Bharat Dynamics ) is 101.2 as of 12/8/2025. A PE ratio exceeding 100 suggests either irrational exuberance or embedded strategic value that traditional metrics can't capture.

Stock is trading at 13.6 times its book value The 13.6x price-to-book ratio indicates the market values BDL's intangibles—technology, relationships, monopoly position—far above its physical assets. For context, global defense contractors typically trade at 2-4x book value.

Revenue Recognition: The Achilles Heel

The company has delivered a poor sales growth of 1.50% over past five years. This anemic growth rate—1.5% over five years—devastates any DCF model. Yet it misrepresents reality. BDL's order book exceeds ₹20,000 crore, but revenue recognition follows completion milestones that can span years.

Revenue from Operations: The company achieved ₹832.14 crore in revenue, marking a 38% increase compared to ₹601.62 crore in the same quarter of the previous fiscal year. Q3 FY25 showed 38% revenue growth—but this reflected milestone completions from orders placed years earlier, not current demand. The lumpy revenue pattern makes quarterly analysis nearly meaningless.

Profitability Under Pressure

Net Profit: BDL's net profit rose by 9% year-on-year, reaching ₹147.12 crore, up from ₹135.03 crore in Q3 FY24. While revenue grew 38%, net profit increased only 9%—margin compression that worried analysts. However, the EBITDA margin experienced a decline, settling at 15.3% compared to 19.8% in Q3 FY24. EBITDA margins falling from 19.8% to 15.3% suggest either competitive pressure or execution inefficiencies.

The margin story hides complexity. BDL must balance three pricing regimes: cost-plus for development contracts, competitive bidding for production orders, and nomination basis for strategic programs. Each has different margin profiles. A shift in mix can swing margins dramatically without reflecting operational performance.

Working Capital: The Silent Killer

Debtor days have increased from 55.0 to 90.2 days. Debtor days jumping from 55 to 90 represents ₹840 crore trapped in receivables—cash that could fund entire manufacturing facilities. The irony: BDL's sole major customer is the government that owns it, yet payment delays persist.

The working capital cycle reveals PSU dysfunction. BDL must pay suppliers within 45 days per government mandate but waits 90+ days for customer payments. This negative float costs ₹120 crore annually in financing charges—pure deadweight loss in a company with negligible debt.

Order Book Dynamics: Promise vs. Delivery

25 Jul - BDL received Rs 809 crore ATGM supply order from Armoured Vehicles Nigam, to be executed in 3 years. The ₹809 crore ATGM order announced July 2024 translates to ₹270 crore annual revenue over three years—meaningful but not transformative for a company with ₹3,400 crore revenue.

Order execution remains BDL's Achilles heel. The company sits on ₹20,000+ crore order book—six years of revenue—yet struggles to accelerate execution. Production constraints, vendor delays, and customer specification changes create a execution bottleneck that frustrates investors expecting linear growth.

Dividend Policy: The Yield Trap

Defence PSU Bharat Dynamics Ltd (BDL) on Thursday declared an interim dividend of 4 per share for FY25. It fixed February 14 as the record date for the purpose of payment of interim dividend. In FY24, it announced a total dividend of Rs 10 per share, amounting Rs 162.20 crore. It declared dividend of Rs 9.35 per share in FY23, Rs 8.30 per share FY22 and Rs 7.35 per share in FY21.

The dividend history—₹10 (FY24), ₹9.35 (FY23), ₹8.30 (FY22), ₹7.35 (FY21)—shows steady progression. At current prices, this yields approximately 0.6%, disappointing income investors but reflecting growth reinvestment needs.

Government ownership complicates dividend policy. As 75% owner, the government collects most dividends, creating circular flow—the government delays payments to BDL but extracts dividends from the profits. This financial engineering obscures true cash generation.

Onerous Contracts: The Hidden Risk

The company thus classified this contract as an onerous contract in accordance with Ind AS 37 — Provisions, Contingent Liabilities and Contingent Assets, and accordingly the company had recognised a provision of Rs 134.61 crore in the financial statements for the quarter and nine months ending 31 December 2024. The company will continue to evaluate these contracts periodically and adjust provisions as necessary in subsequent reporting periods

The ₹134.61 crore provision for onerous contracts in Q3 FY25 reveals a disturbing reality: BDL sometimes accepts loss-making contracts for strategic reasons. The company justified this as gaining "exposure to niche technology" and becoming a "global supply chain partner"—code for accepting losses today for potential gains tomorrow.

Inventory Management: Dead Stock Dilemma

The defence PSU said its inventories include Rs 83.38 crore, which are non-moving for more than 5 years, procured by the company based on firm orders/LOI that were subsequently short closed by the customer.

₹83.38 crore in non-moving inventory for over 5 years represents capital destroyed by customer fickleness. When the government cancels orders after procurement, BDL bears the cost. This asymmetric risk—BDL bears procurement risk but can't refuse government orders—exemplifies PSU constraints.

Stock Performance: Volatility Personified

BDL's 52 week high is ₹2096.6 and 52 week low is ₹890. The 52-week range—₹890 to ₹2,096—represents 135% volatility in a supposedly stable defense contractor. This reflects binary outcome dependency: major order announcements trigger rallies, execution delays cause crashes.

Despite the initial discount, the Bharat Dynamics share price has witnessed significant growth since its listing, reflecting investor confidence in the company's future. From the IPO price of ₹428 to current levels around ₹1,500, early investors earned 250% returns over 7 years—roughly 20% annually. Impressive, but the journey included multiple 30%+ drawdowns that tested conviction.

Comparative Valuation: Global Context

BDL trades at metrics that would seem absurd for Western defense contractors: - PE Ratio: 101 (vs. Lockheed Martin at 20) - Price/Book: 13.6x (vs. Raytheon at 3x) - EV/EBITDA: 35x (vs. BAE Systems at 12x)

The premium reflects three factors: India's defense spending growth trajectory (15% CAGR expected), BDL's monopoly position, and scarcity value as the only pure-play listed defense manufacturer. Whether this premium is justified remains the core investment debate.

Financial Realities: The PSU Burden

Earnings include an other income of Rs.357 Cr. Other income of ₹357 crore—primarily interest on surplus funds—represents 64% of net profit. This reliance on treasury income rather than operational profits raises questions about core business profitability.

The company maintains ₹3,000+ crore in cash and investments—capital that private companies would deploy aggressively but BDL holds per government mandate. This lazy balance sheet depresses return metrics while providing downturn protection.

Execution Challenges: Structural or Solvable?

Revenue from operations stood at Rs 247.93 crore, up 29.69% from Rs 191.17 crore in the year-ago quarter but down 86.05% compared to Rs 1,770.98 crore in Q4 FY25. Profit after tax (PAT) for Q1 FY26 stood at Rs 18.35 crore, marking a 154.28% rise from Rs 7.22 crore in the same quarter last year but a 93.27% drop from Rs 272.78 crore in Q4 FY25.

Q1 FY26 volatility—revenue down 86% sequentially, profit down 93%—exemplifies the execution challenge. Defense contracts complete in bunches, creating massive quarterly swings that make financial planning impossible and investor communication challenging.

The financial performance reveals BDL's fundamental tension: strategic importance doesn't guarantee commercial success. With PE ratios exceeding 100, markets price in dramatic improvement. Yet structural constraints—government ownership, single customer dependence, working capital pressure—persist. The investment case reduces to a single question: Will India's defense modernization overwhelm PSU inefficiencies? The answer determines whether current valuations represent opportunity or optimism detached from operational reality.

VIII. Strategic Challenges & Competition

The war room at Lockheed Martin's Bethesda headquarters, September 2023. Executives review India's defense procurement plans: $130 billion over five years. The conclusion is unanimous—India represents the last great growth market for defense contractors. Within months, every major global player announces India partnerships, joint ventures, or technology transfers. For BDL, comfortable in its monopoly for five decades, the competitive landscape transforms from protected reserve to hunting ground.

The challenge isn't just foreign giants. Larsen & Toubro's defense division now generates ₹7,000 crore revenue. Adani Defence promises missile manufacturing capabilities by 2027. Tata Advanced Systems already produces aerospace components for Boeing. The "Make in India" policy that was supposed to protect BDL instead unleashed competitors with deeper pockets, modern management, and no PSU constraints.

Global Defense Dynamics: The New Great Game

The global defense industry consolidation—from 50+ prime contractors in 1990 to 5 mega-primes today—created entities with revenues exceeding many nations' GDP. Lockheed Martin's $67 billion revenue dwarfs BDL's ₹3,400 crore by 140x. These giants don't just bring capital; they offer technology ecosystems, global supply chains, and political influence that opens export markets.

Consider Rafael's strategy in India. After the Rafale fighter deal, they established production facilities, partnered with Reliance for assembly, and now offer to manufacture entire missile systems locally. Their SPICE precision munition kits, assembled in India, already compete with BDL's products. The message is clear: foreign OEMs will manufacture in India, with or without BDL.

The technology denial regime that protected BDL for decades is crumbling. The Missile Technology Control Regime (MTCR), which India joined in 2016, actually enables technology transfers previously impossible. What seemed like diplomatic victory becomes competitive threat—foreign companies can now legally transfer technologies that BDL spent decades developing independently.

Private Sector Emergence: The Domestic Disruption

L&T's defense journey exemplifies private sector ambitions. Starting with submarine hulls, they now produce entire weapon systems. Their K9 Vajra howitzer program—delivered ahead of schedule and under budget—embarrasses PSU timelines. L&T's Coimbatore facility can produce 100 gun systems annually; BDL struggles to deliver 50 missile systems monthly.

Adani Defence's entry changes the game entirely. With ₹10,000 crore committed investment, they're building missile production facilities from scratch. Their Mundra facility will have capacity to produce 1,000 missiles annually by 2028. Unlike BDL's gradual capacity expansion, Adani builds at startup speed—what takes BDL five years happens in eighteen months.

Tata Advanced Systems represents sophisticated competition. Their joint venture with Boeing produces Apache helicopter fuselages. With Lockheed, they manufacture C-130 components. These partnerships provide technology access BDL can't match. When Tata announces missile ambitions, they bring global partners from day one.

The startup ecosystem poses unexpected challenges. Tonbo Imaging's thermal sights now equip BDL's own missiles—the supplier becoming potential competitor. IdeaForge's drones carry weapons that could replace missiles for certain missions. These nimble companies iterate faster than BDL's five-year development cycles.

Technology Transfer Restrictions: The Double-Edged Sword

BDL faces a Catch-22 with technology transfers. As a government entity, it must prioritize indigenous development. Yet private competitors freely license foreign technology, achieving in months what takes BDL years. The recent MBDA partnership for MICA missiles exemplifies this—Adani got similar rights, negating BDL's presumed advantage.

MTCR membership paradoxically weakened BDL's position. Previously, technology denials forced indigenous development, creating natural protection. Now, foreign companies transfer technology to Indian partners, but BDL's government status triggers additional scrutiny. Private companies get technology BDL can't access despite—or because of—its official status.

Export control regimes remain byzantine. BDL needs government approval for every export, while private companies operate under general licenses. A Middle Eastern country recently chose a Turkish missile over BDL's superior product simply because delivery was guaranteed in 12 months versus BDL's 36-month timeline requiring multiple approvals.

Execution Bottlenecks: Structural Impediments

Debtor days have increased from 55.0 to 90.2 days. The working capital crisis exemplifies execution challenges. While private competitors demand advance payments, BDL waits 90+ days for government payments. This cash trap prevents aggressive capacity expansion.

Production bottlenecks cascade through the system. BDL's Kanchanbagh facility operates three shifts but can't expand due to urban encroachment. New facilities take 5-7 years from approval to production. Meanwhile, private companies build greenfield facilities in 18 months using modular construction and parallel processing of approvals.

Procurement procedures handicap competitiveness. BDL must follow Defense Procurement Procedure (DPP) rules—multiple tenders, L1 pricing, technical evaluation committees. Private companies negotiate directly, adjust specifications in real-time, and close deals in weeks not years. A recent counter-drone system tender took BDL 18 months; a startup delivered similar capability to the Army in 3 months through emergency procurement.

Human resource constraints compound challenges. BDL's government pay scales can't match private sector compensation. Young engineers join for training then leave for 3x salaries at private companies. The average age at BDL exceeds 45; at startup competitors, it's under 30. Innovation velocity correlates with workforce demographics.

Export Market Challenges: The Credibility Gap

BDL's export ambitions face credibility challenges. International customers question why India's own military takes years to approve BDL products. The Akash missile system, offered for export since 2020, has generated interest but no confirmed orders. Meanwhile, Turkey's similar Hisar system has secured multiple export contracts.

The "Make in India" brand paradoxically weakens BDL abroad. Potential customers assume Indian weapons are budget alternatives to Western systems. BDL's products often match or exceed Western specifications, but perception lags reality. Marketing military products requires relationship capital BDL lacks—retired generals joining private companies bring networks BDL's bureaucrats can't match.

Geopolitical alignments constrain exports. BDL can't sell to Pakistan or China for obvious reasons. Western allies prefer NATO suppliers. Russia offers competing systems. This leaves a narrow market: Southeast Asia, Africa, and Latin America—regions with limited budgets and extensive competition.

Technology Gaps: Falling Behind the Curve

While BDL masters 1990s technology, warfare transforms rapidly. Hypersonic missiles, directed energy weapons, and AI-enabled systems define future conflict. BDL's R&D, constrained by government budgets and bureaucratic approval, can't match private sector innovation velocity.

Consider drone swarms—potentially replacing traditional missiles for many missions. While BDL develops conventional missiles, startups create AI-powered drone systems at 1/10th the cost. The Russia-Ukraine conflict demonstrates this shift: $100,000 drones destroying $10 million air defense systems. BDL's product portfolio risks obsolescence before deployment.

The software revolution in warfare disadvantages BDL. Modern missiles are flying computers; software defines capability more than hardware. BDL's software expertise lags mechanical engineering prowess. Private companies, staffed with IIT computer science graduates, develop guidance algorithms BDL struggles to match.

Cybersecurity becomes existential. Every BDL system now requires protection against electronic warfare. But cybersecurity expertise concentrates in private sector. BDL must either develop capabilities internally—a decade-long journey—or depend on private partners who might become competitors.

Balancing Autonomy with Partnerships

BDL's partnership strategy reveals institutional schizophrenia. Strategic autonomy demands indigenous development, but competitiveness requires foreign collaboration. Each foreign partnership potentially creates future competition when technology transfer agreements expire and partners establish independent operations.

The MBDA joint venture exemplifies this dilemma. While providing access to European missile technology, MBDA simultaneously partners with private Indian companies. BDL gains technology but creates competitors. The alternative—going alone—means falling further behind global standards.

Government pressure for strategic autonomy conflicts with commercial reality. Ministers announce indigenous development goals, but armed forces demand proven international systems. BDL catches the middle—criticized for foreign dependence when partnering, condemned for technological gaps when developing independently.

Quality vs. Quantity Dilemma

India's defense needs split between sophisticated systems for Pakistan/China deterrence and mass production for conventional warfare. BDL optimized for quality—producing hundreds of expensive missiles annually. But modern warfare might require thousands of cheap, "good enough" weapons.

Private companies target the volume market. Their business models assume 10,000-unit production runs, achieving economies of scale BDL can't match. When wars consume weapons in weeks not years, production capacity matters more than sophisticated capabilities. BDL's artisanal approach—each missile carefully crafted—might be strategically obsolete.

The challenge compounds with dual-use technologies. Commercial drones, adapted for military use, cost fractions of purpose-built military systems. Private companies, with commercial and military product lines, achieve synergies BDL can't replicate. The boundary between civilian and military technology dissolves, disadvantaging dedicated defense manufacturers.

BDL's strategic challenges aren't merely competitive—they're existential. The company must transform from protected monopoly to competitive manufacturer while maintaining strategic capabilities, from hardware producer to software integrator while preserving manufacturing excellence, from government entity to market competitor while serving national interests. These transitions, any one of which would challenge private companies, must occur simultaneously under public scrutiny with limited resources. The question isn't whether BDL can compete—it's whether the institutional framework allows competition at all.

IX. Future Roadmap & Strategic Imperatives

The classified briefing room at South Block, January 2025. The Defense Secretary presents India's threat assessment: China deploys hypersonic glide vehicles along the LAC, Pakistan inducts Turkish-made loitering munitions, and non-state actors acquire commercial drones modified into precision weapons. The traditional missile paradigm—expensive, exquisite, limited quantity—appears increasingly obsolete. For BDL, this represents both existential crisis and unprecedented opportunity.

The numbers frame the opportunity: India's defense budget allocation for capital modernization reaches ₹1.72 lakh crore in FY25. The domestic procurement requirement, mandated at 68% by 2025, translates to ₹117,000 crore in domestic orders. BDL, as the sole established missile manufacturer, should dominate. Yet private sector competitors circle, foreign partnerships multiply, and technology evolves faster than procurement cycles. The next five years will determine whether BDL leads India's defense transformation or becomes its casualty.

Next-Generation Systems: The Technology Imperative

BDL's pipeline reveals ambition tempered by reality. The Astra Mark II air-to-air missile, with 150km range and dual-pulse motor, matches the European Meteor missile—if it achieves planned specifications. Development began in 2017 with 2022 delivery promised; current estimates suggest 2026. Each delay allows competitors to establish positions.

The Man-Portable Anti-Tank Guided Missile (MPATGM) represents indigenous breakthrough. With fire-and-forget capability and tandem warhead defeating explosive reactive armor, it matches the American Javelin's specifications at projected 20% cost. But "projected" carries weight—final costs typically exceed estimates by 50-100%.

Pralay, the tactical ballistic missile with 350-500km range, fills the gap between Prithvi and Agni. Its quasi-ballistic trajectory with terminal maneuvering defeats most missile defenses. BDL positions itself as primary manufacturer, but L&T's missile division openly courts the same contract. The selection decision becomes political as much as technical.

The Smart Anti-Airfield Weapon (SAAW), already tested from Jaguar aircraft, promises surgical strike capability. At 120kg, it's lighter than comparable Israeli systems. BDL partnered with DRDO for development but faces competition from private companies offering similar capabilities through foreign partnerships.

Stand-off Anti-Tank (SANT) missile, launched from helicopters at 10km range, employs millimeter-wave seeker for all-weather capability. The technology matches the American Hellfire Longbow, but at Indian price points. Production readiness remains uncertain—BDL claims 2025, skeptics suggest 2027.

Export Potential: Breaking Into Global Markets

BDL is offering Akash Weapon System (Surface-to-Air Missile), Astra Weapon System (Air-to-Air Missile), SAAW (Smart Anti-Airfield Weapon) and Helina (Air-to-Surface Weapon), Light Weight Torpedo and Heavy Weight Torpedo (Underwater weapons), Counter Measures Dispensing System and Anti-Submarine Warfare Suite (Counter Measure Systems) and Anti-Tank Guided Missiles namely Nag, Konkurs-M and MILAN-2T for exports.

The export portfolio looks impressive on paper, but execution proves challenging. Armenia's interest in Akash remains "under discussion" three years after initial negotiations. The Philippines evaluated BDL's anti-tank missiles but chose Israeli systems—citing faster delivery and proven combat record.

Vietnam represents the most promising market. Historical ties, Chinese tensions, and budget constraints align perfectly with BDL's offerings. The Light Weight Torpedo export, while classified in details, reportedly exceeded $50 million. Vietnam's navy needs 200+ torpedoes, suggesting follow-on orders. But French and Russian competitors offer similar systems with faster delivery.

African markets offer volume potential. Nigeria, fighting Boko Haram, needs counter-insurgency weapons. Egypt, modernizing rapidly, seeks technology transfer agreements. South Africa wants joint development partnerships. BDL established offices in these countries but struggles converting interest into orders.

Latin America presents untapped opportunity. Brazil's defense modernization, Argentina's budget constraints, and Colombia's internal security needs align with BDL's product range. But American influence, European partnerships, and Chinese financing compete for the same contracts.

Middle Eastern markets remain complex. Saudi Arabia and UAE buy American for political reasons. Iran faces sanctions. Iraq and Syria are conflict zones. This leaves Jordan, Oman, and Kuwait—small markets with established supplier relationships BDL must break.

Technology Partnerships: The Collaboration Imperative

The MBDA partnership for MICA missiles provides template and warning. Technology transfer includes manufacturing know-how but not design capability. BDL assembles missiles but can't modify them. When contracts expire, MBDA might partner with private companies, leaving BDL with obsolete production lines.

Russian collaboration, historically crucial, faces new pressures. Ukraine war sanctions complicate technology transfer. Payment mechanisms through rupee-ruble trade create accounting nightmares. Most critically, Russian technology increasingly lags Western standards—partnering might mean falling behind.

Israeli partnerships offer cutting-edge technology but political sensitivities. The recent Rafael partnership for Spike missiles provides manufacturing rights, but Arab nations then exclude BDL from competitions. Technology gain must balance market loss.

Emerging partnerships with South Korea and Turkey represent strategic pivots. Both offer modern technology without Western restrictions or Russian complications. Korea's Hanwha proposes joint development of next-generation surface-to-air missiles. Turkey's Roketsan discusses anti-ship missile collaboration. These partnerships might leapfrog traditional suppliers.

Make in India: Opportunity and Obligation

The Atmanirbhar Bharat initiative mandates 68% indigenous content by 2025, rising to 75% by 2030. For BDL, this means captive markets worth ₹50,000 crore annually. But indigenous content calculations prove contentious—does assembling foreign designs with local components qualify?