Black Box Limited: From Tata Telecom to Global Digital Infrastructure Giant

I. Introduction & The Hook

Picture this: A Bengaluru boardroom in early 2024, where executives of a company most Indians have never heard of are plotting to double their revenue to $2 billion within five years. The company controls critical digital infrastructure for over 100 Fortune 500 companies, manages airport communications systems across continents, and powers the backbone of hyperscaler data centers. Yet walk down Dalal Street and ask about Black Box Limited—you'll likely get blank stares.

This is the paradox of Black Box (NSE: BBOX), a ₹8,450 crore market cap company generating ₹5,967 crore in annual revenue that has somehow remained under the radar despite touching virtually every aspect of modern digital life. When you swipe your card at a retail store, board a plane at a major airport, or stream content from a data center, there's a decent chance Black Box infrastructure made it possible.

The question that drives this story: How did a 1986 Indian telecom equipment manufacturer, born in the license raj era as Tata Telecom, transform through multiple ownership changes—from the Tatas to AT&T to Avaya to Essar—to emerge as a global digital infrastructure powerhouse? It's a journey that mirrors India's own economic evolution, from protected manufacturing to services export to digital transformation leadership.

What makes Black Box particularly fascinating is its contrarian trajectory. While Indian IT giants like TCS, Infosys, and Wipro built their empires on labor arbitrage and software services, Black Box went the opposite direction—acquiring a larger American company, keeping the acquired brand, and using India as a strategic hub for global delivery rather than the primary value proposition. The company's transformation from manufacturing electronic telephone exchanges to orchestrating AI infrastructure represents not just corporate evolution but a complete metamorphosis of identity, capability, and ambition.

This is that story—one of strategic pivots, bold acquisitions, and the relentless pursuit of relevance in an industry where yesterday's innovation becomes tomorrow's commodity. It's about how a company repeatedly reinvented itself, surviving the dot-com bust, the 2008 financial crisis, COVID-19, and multiple ownership transitions to position itself at the center of the AI and digital infrastructure boom.

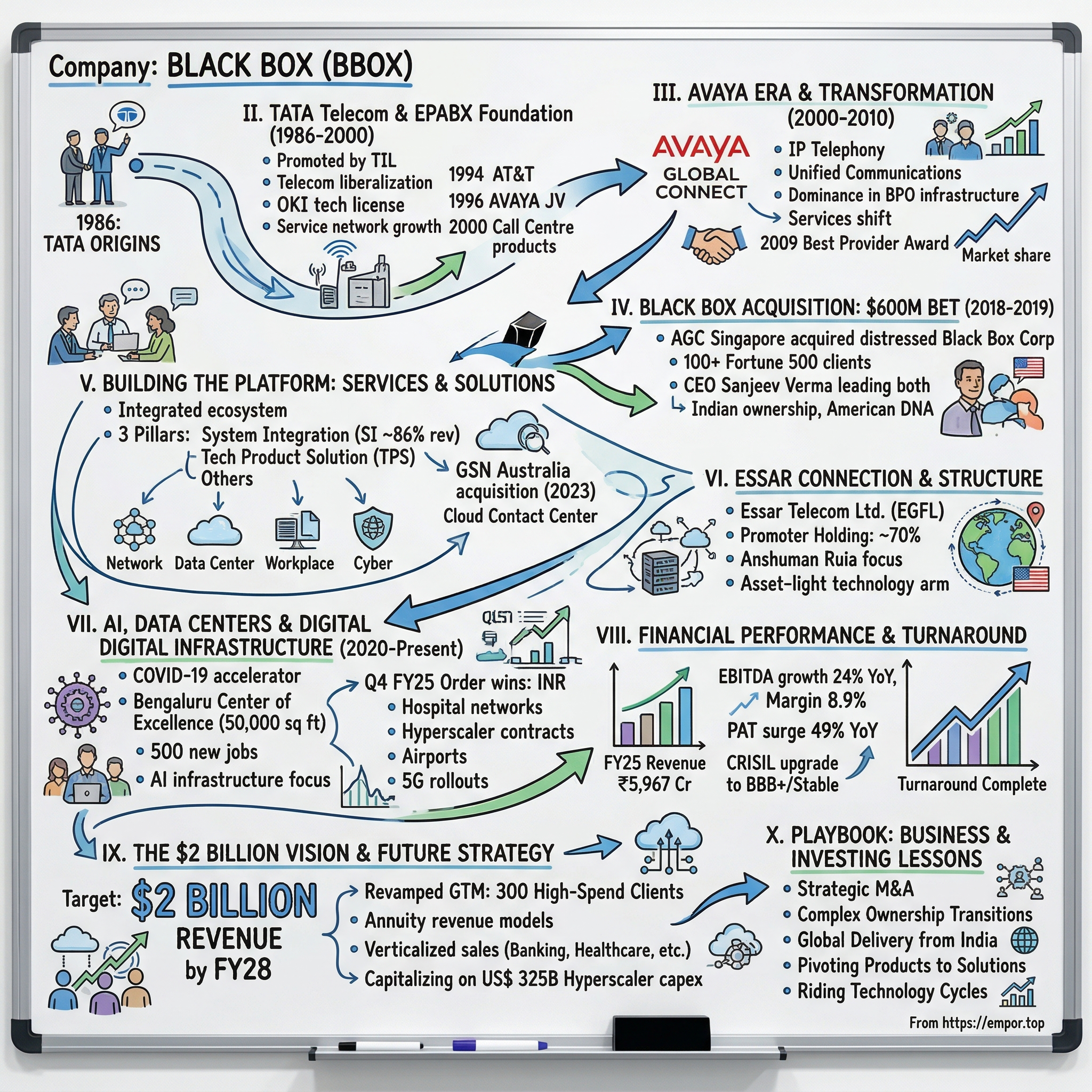

II. The Tata Origins & Foundation (1986-2000)

The monsoon of 1986 brought more than just rain to India's business landscape. In the corridors of Bombay House, the Tata Group's headquarters, executives were sketching out plans for what would become one of the most dramatic transformation stories in Indian corporate history. AGC Networks Limited was established in 1986 under the name Tata Telecom Ltd., promoted by Tata Industries Ltd (TIL), entering a telecom equipment market that was about to explode.

The timing couldn't have been more prescient. India was on the cusp of telecom liberalization, with waiting lists for telephone connections stretching years and businesses desperate for modern communication infrastructure. Manufacturing electronic private automated branch exchanges (EPABX) was one of its main goals, and it also offered services like software integration, installation, commissioning, and service support. These EPABX systems—essentially sophisticated telephone switching systems for offices—were the backbone of corporate communications in an era before mobile phones and internet.

What made Tata Telecom different from the start was its international ambition. With the Japanese company OKI Electric Industrial Co. Ltd. (OKI), Tata Industries Limited signed a technical assistance and license agreement, bringing global technology standards to Indian manufacturing. This wasn't just about making equipment; it was about building capability. The company rapidly expanded its service network, establishing new service facilities in Guwahati, Nagpur, Pune, Jammu, and Baroda—a geographic spread that would prove invaluable decades later.

The 1990s brought a parade of international partnerships that would fundamentally reshape the company's DNA. In 1994, AT&T entered the picture, bringing American telecommunications expertise to Indian shores. But the real transformation came in 1996 when Tata Telecom and Avaya Systems established a joint venture after AT&T's exit. This wasn't just a technology transfer—it was a complete reimagining of what an Indian telecom company could be.

The Avaya partnership marked a critical inflection point. Tata Telecom, the joint venture between Tata and Lucent Technologies, was known as a Tata-Avaya, combining the Tata Group's local market knowledge and distribution strength with Avaya's cutting-edge communication technologies. The partnership brought enterprise-grade communication solutions that were previously unavailable in India, from unified messaging systems to advanced call center technologies.

By 2000, as the dot-com boom was creating unprecedented demand for customer service infrastructure, Tata Telecom introduced a line of call centre products in India that it had purchased from its joint venture partner Avaya Communications. This move positioned the company at the heart of India's emerging BPO revolution. While companies like Infosys and Wipro were writing software, Tata Telecom was building the physical and technological infrastructure that made offshore call centers possible.

The foundation years weren't just about products and partnerships—they were about building a philosophy. The Tata ethos of nation-building through industrialization permeated every decision. Unlike pure traders or importers, the company invested in manufacturing capabilities, service networks, and technical training. They weren't just selling boxes; they were building India's communication backbone.

This period also saw the company navigate the complexities of India's regulatory environment, from import licenses to technology transfer agreements, all while maintaining the Tata Group's reputation for ethical business practices. The relationships built during these years—with government departments, large enterprises, and technology partners—would prove invaluable as the company evolved.

What's remarkable looking back is how these early decisions—the focus on enterprise customers, the emphasis on service and support, the international partnerships, and the geographic spread—created the platform for everything that followed. The EPABX manufacturer of 1986 was unknowingly laying the groundwork for a global digital infrastructure company.

III. The Avaya Era & Transformation (2000-2010)

The turn of the millennium marked a seismic shift in global telecommunications, and for Tata Telecom, it was the beginning of a decade-long metamorphosis that would fundamentally alter its identity. Once the Tata Group sold its 25.1% ownership in Tata Telecom to its joint venture partner, Avaya Inc., the company Avaya Global Connect was created. This wasn't just a change in ownership—it was a complete reimagining of what the company could become.

The newly christened Avaya Global Connect emerged at a fascinating moment in technology history. Avaya Inc. was spun off from Lucent as its own company in 2000, itself a spinoff from AT&T's equipment business. The company that now owned majority stake in the Indian operation was a global communications powerhouse with ambitious plans for emerging markets. For the Indian entity, this meant access to cutting-edge unified communications technology just as Indian businesses were beginning their global ascent.

What made the Avaya era transformative wasn't just the technology transfer—it was the shift in ambition and capability. Avaya GlobalConnect has more than 35 service centers in India that offers facilities to around 6,000 clients with the help of more than 500 ancillaries, producing a yearly profit of USD 87 million. The company wasn't just selling boxes anymore; it was architecting complete communication ecosystems for enterprises navigating the complexities of globalization.

The product portfolio during this period reads like a timeline of enterprise communication evolution. The company introduced IP telephony when most Indian businesses were still getting used to digital phones. They brought unified communications—integrating voice, video, email, and instant messaging—when email itself was still novel in many Indian offices. The firm is a major player in contact center solutions and possesses more than half of the market share in the domain.

This dominance in contact centers wasn't accidental. As India emerged as the world's back office through the BPO boom, Avaya Global Connect found itself at the intersection of two massive trends: India's services export revolution and the global shift to IP-based communications. Every major BPO and call center needed the sophisticated routing, recording, and management capabilities that Avaya's platform provided. The company wasn't just riding the wave; it was providing the surfboards.

The transformation extended beyond products to fundamental business model evolution. Instead of competing on price with local manufacturers, Avaya Global Connect positioned itself as a solutions provider, offering consulting, integration, and managed services. Avaya GlobalConnect offers commercial solutions to the firms that assist them in increasing their returns growth, accelerate market reach, maximize functional values and enhance staff efficiency, by entrenching communication in their operational activities.

Geographic expansion during this period was strategic and deliberate. While maintaining its stronghold in India, the company began exploring opportunities in the Middle East, Southeast Asia, and Africa—markets that shared similar infrastructure challenges and growth trajectories. This wasn't the typical Indian IT company's labor arbitrage play; it was about taking proven solutions from one emerging market to another.

The technical capabilities built during this era would prove invaluable. The company developed deep expertise in mission-critical communications—the kind of systems that absolutely cannot fail. When a bank's call center goes down, millions in transactions hang in the balance. When a hospital's communication system fails, lives are at stake. This wasn't consumer technology where you could push updates and fix bugs later; this was infrastructure that demanded five-nines reliability.

Recognition followed performance. The firm has been identified as the "Best Enterprise Solution Provider Company" in 2009 at INFOCOM CMAI Telecom Awards ceremony. But perhaps more important than awards was the trust built with enterprises during this period—relationships that would endure through multiple ownership changes.

By 2010, as another ownership transition loomed, Avaya Global Connect had evolved far from its EPABX manufacturing roots. It was now a sophisticated technology services company with deep domain expertise, strong customer relationships, and a proven ability to deliver complex solutions. AGC Networks Limited was created in 2010 after Essar Group purchased Avaya Global Connect from Avaya Inc. The Essar acquisition would mark the beginning of yet another transformation, but the foundation laid during the Avaya years—the shift from products to solutions, from local to regional, from vendor to partner—would define the company's trajectory for the decade ahead.

IV. The Black Box Acquisition: A $600M Bet (2018-2019)

November 11, 2018, marked a watershed moment that would define AGC Networks' global ambitions. In a Pittsburgh boardroom, executives of Black Box Corporation—a company that had pioneered data communications since 1976—were about to approve a deal that seemed, on paper, improbable. AGC Singapore would acquire all the outstanding shares of Black Box for $1.08 per share in cash, subject to customary closing conditions and regulatory approvals. The Black Box Board of Directors unanimously approved the merger agreement following a thorough review of the full range of available strategic, financial and capital structure alternatives, which Black Box commenced and announced on February 6, 2018.

The numbers told a story of both opportunity and desperation. A U.S. subsidiary of AGC Singapore will buy Black Box's common stock for $1.08 per share in cash. As a result, Black Box's market capitalization has climbed to about $16.3 million, according to Yahoo Finance. For a company generating $600 million in annual revenue, this valuation was extraordinary—not in a good way. Black Box's business has been under pressure. In a February 2018 SEC filing, the company disclosed that it may not be able to generate sufficient adjusted EBITDA to meet a debt covenant with lenders.

What AGC saw that others didn't was transformational potential. The combination with Black Box will provide a substantial increase in AGC's presence and offerings in North America. In addition, AGC will enhance its footprint in providing technologies and services throughout six continents. The acquisition will be significant for AGC, expected to add over $600 million in annual revenue and approximately 3,000 team members serving enterprise clients globally.

The strategic logic was compelling. Black Box wasn't just any distressed asset—it was a storied American technology company with deep relationships across Fortune 500 enterprises. Founded in 1976, Black Box had built its reputation on the unglamorous but essential business of data communications infrastructure. While Silicon Valley chased consumer apps and social media, Black Box had quietly become indispensable to banks, hospitals, airports, and government facilities that needed their communications to work perfectly, every time.

For Sanjeev Verma, AGC's CEO who would also become President and CEO of Black Box Corporation, this was about more than geographic expansion. AGC Networks CEO Sanjeev Verma said: "We have known Black Box for many years and believe that its skilled teams and strong client relations with world-class enterprises and partners will allow us to better serve our global clients." The acquisition would create a unique entity—an Indian-owned company with American DNA, serving global markets with a combination of cost-effective delivery from India and high-touch presence in developed markets.

The deal structure itself was a masterclass in financial engineering. Under the terms of the merger agreement, an indirect wholly owned U.S. subsidiary of AGC Singapore will commence a tender offer to purchase all of the outstanding shares of Black Box common stock for $1.08 per share in cash. Upon the successful completion of the tender offer, the U.S. subsidiary of AGC Singapore would acquire all remaining shares of common stock not tendered in the offer for $1.08 per share through a second-step merger. The tender offer and the second-step merger are subject to customary conditions, including the tender of a majority of the outstanding shares of Black Box common stock. The U.S. subsidiary of AGC Singapore is financing the merger through a combination of equity and debt.

As December approached and shareholders hesitated, AGC sweetened the deal. AGC Networks' indirect wholly owned subsidiary, Host Merger Sub Inc. ("Purchaser"), has increased its offer price with respect to its tender offer (the "Offer") to purchase all of the issued and outstanding shares of common stock, par value $0.001 per share (the "Shares"), of Black Box Corporation ("Black Box") from $1.08 to $1.10 per Share, representing a 26% premium to Black Box's pre-announcement closing price.

The regulatory hurdles were significant but manageable. Under the merger agreement, the parties have set a goal of filing a Declaration with CFIUS under the new Pilot Program by November 16, 2018. The Committee on Foreign Investment in the United States (CFIUS) review was particularly scrutinized given Black Box's work with critical infrastructure, but The parties agreed to file with CFIUS, but clearance was not a condition to closing.

On January 7, 2019, the deal closed with a whimper that belied its significance. The previously announced tender offer expired at the end of the day on Friday, January 4, at which time 9,126,005 shares of Black Box common stock (excluding shares tendered by guaranteed delivery) had been validly tendered and not withdrawn pursuant to the tender offer, representing approximately 59.89% of the outstanding shares. As a result of the tender offer and the subsequent merger, which were completed today, Black Box Corporation will become a private company and, as of today, its shares of common stock will no longer be publicly traded.

What AGC had accomplished was remarkable: for roughly $16.3 million in equity value (though assuming substantial debt), they had acquired a company with $600 million in revenue, 3,000 employees, and relationships with over 100 Fortune 500 companies. The integration challenges would be substantial—merging an American company with a complex history into an Indian-owned entity with its own cultural DNA. But the potential was even greater.

AGC brings its strong presence in India, the Middle East and Pacific Rim to complement Black Box's services focus in the Americas and Europe, while also enhancing the presence in other global markets. Both companies provide full managed services capabilities in Unified Communications and Collaboration, Cloud, Data Center and Edge Technologies. AGC adds its expertise in digital applications and cybersecurity to Black Box's strong infrastructure and mobility background.

The Black Box acquisition wasn't just about buying revenue or entering new markets. It was about creating something new—a global digital infrastructure company that could compete with anyone, anywhere. In 2021, AGC Networks would complete the transformation by changing its name to Black Box, recognizing that the acquired brand carried more weight in global markets than the acquirer's. It was a bold acknowledgment that in technology services, sometimes the best strategy is to embrace the heritage you acquire rather than impose your own.

V. Building the Platform: Services & Solutions (2010s–Today)

The transformation of Black Box from a distressed American acquisition into a global digital infrastructure powerhouse represents one of the most ambitious platform-building exercises in enterprise technology. Black Box Limited provides information and communications technology solutions in India, the United States, and internationally. It operates through System Integration, Technology Product Solution, and Others segments.

The business architecture that emerged post-acquisition reveals a carefully orchestrated three-pillar strategy. The company's operating segments are System Integration (SI); Technology Product Solution (TPS) and Others comprising of training and consulting services. It generates maximum revenue from the System Integration (SI) segment. This SI dominance—accounting for approximately 86% of revenue—reflects a fundamental shift from product sales to solution delivery, a transformation that began during the Avaya years but accelerated dramatically under Essar ownership.

What makes Black Box's services portfolio distinctive is its breadth and depth across the entire digital infrastructure stack. Black Box has strong service offerings in network integration, digital connectivity infrastructure, data center build-out, modern workplace, and cybersecurity for businesses across various industries including financial services, technology, healthcare, retail, public services like airports; manufacturing, and other sectors. This isn't a collection of point solutions; it's an integrated ecosystem designed to address every layer of enterprise technology needs.

The Technology Products division, while smaller in revenue contribution, serves as a critical differentiator. The Technology Products portfolio transforms operations for businesses with innovative products and solutions across AV, IoT, KVM, Networking, Infrastructure, and Cables. These aren't commodity products but specialized solutions for mission-critical applications—KVM switches that allow operators to control hundreds of servers from a single console, AV-over-IP solutions that power control rooms and broadcast facilities, and specialized cables designed for harsh industrial environments.

Geographic expansion has been methodical and strategic. Black Box (BSE: 500463/NSE: BBOX) is a global digital infrastructure integrator delivering network and system integration services and solutions, support services, and technology products to businesses in the United States, Europe, India, Asia Pacific, the Middle East, and Latin America and has around 4,000 professionals globally. This global footprint isn't just about sales presence; it's about delivery capability—the ability to execute complex, multi-country rollouts for global enterprises.

The 2023 acquisition of GSN Australia exemplifies the platform-building approach. Black Box Limited (formerly AGC Networks Limited) (BSE: BBOX) (NSE: BBOX), a trusted IT solutions provider, announced that it has completed the acquisition of GSN Australia through its indirect wholly-owned subsidiary – Black Box Technologies Australia Pty Ltd. The acquisition of GSN Australia aligns with Black Box's growth strategy and expands its portfolio of products and services. As a result of this acquisition, Black Box will be able to offer its customers an even wider range of Cloud Contact Center and Digital Experience solutions that further strengthens its position in the Trans-Tasman markets and leverage the skills and expertise of our global customers.

This wasn't just about buying revenue or market share. GSN has been helping customers transform their employee and customer experiences by integrating traditional and digital CX solutions. GSN has a strong team in Australia and New Zealand. The New Zealand team is supported by Australia in a matrixed organization. The team comprises a strong Sales, Marketing, and Service team, that work together with their deep domain service delivery expertise to deliver results for Customers. The acquisition brought specialized capabilities in cloud contact centers and digital experience—areas where Black Box saw explosive growth potential.

The client base evolution tells its own story of transformation. From serving primarily Indian enterprises with telecom equipment in the 1980s, Black Box now counts over 8,000 customers globally, including more than 100 Fortune 500 companies. These aren't transactional relationships but deep partnerships where Black Box manages critical infrastructure. When a global bank needs to upgrade its trading floor communications, when an airport needs to modernize its operations center, when a hyperscaler needs to build out a new data center—Black Box gets the call.

The solutions approach has evolved significantly from the traditional systems integration model. The Company has reorganised and renewed its Go-To-Market (GTM) Business Strategy focused on select Industry Verticals for concentrated approach towards these verticals, and simultaneously created a Horizontal Solutions structure around these verticals to be able to offer wide range of solutions for deeper engagement with the customers. This vertical-horizontal matrix allows Black Box to combine deep industry expertise with broad technical capabilities, creating solutions that are both specialized and scalable.

Digital transformation and AI have become central to the platform strategy. The company isn't just implementing others' AI solutions; it's building the infrastructure that makes AI possible. From the high-speed networks that connect GPU clusters to the cooling systems that keep them operational, Black Box touches every aspect of the AI infrastructure stack. This positions the company uniquely as enterprises race to implement AI at scale.

The modern workplace solutions represent another evolution of the platform. Post-COVID, as enterprises grappled with hybrid work models, Black Box emerged as a critical partner in reimagining office communications. This isn't just about video conferencing; it's about creating intelligent workspaces where technology enhances rather than hinders collaboration. Smart meeting rooms that automatically adjust based on participants, unified communications platforms that seamlessly blend office and remote workers, security solutions that protect distributed workforces—these are the building blocks of the future workplace that Black Box is delivering today.

Cybersecurity has evolved from an add-on service to a core capability woven through every solution. In an era where a single breach can cost millions and destroy reputations, Black Box's approach to security—embedding it at every layer rather than bolting it on—has become a key differentiator. The company's CYBER-i framework provides end-to-end security from the network edge to the application layer, addressing the complex security challenges of modern distributed architectures.

The managed services evolution represents perhaps the most significant transformation. Rather than just building and walking away, Black Box increasingly manages the infrastructure it deploys. This creates recurring revenue streams, deeper customer relationships, and valuable operational insights that feed back into solution design. For customers, it means having a single throat to choke for complex, multi-vendor environments.

Looking at the platform today, what emerges is a company that has successfully navigated one of the most difficult transitions in technology—from product company to solutions provider to platform orchestrator. As of 31-Mar-2025, Black Box has a trailing 12-month revenue of $706M. The trailing twelve month revenue for Black Box is $706M. While revenue growth has been modest, the transformation in capability, reach, and strategic positioning has been profound.

VI. The Essar Connection & Corporate Structure

To understand Black Box's trajectory, one must first understand the Essar Group—a conglomerate that has navigated India's economic liberalization with the agility of a speedboat and the ambition of an ocean liner. Essar Group is an Indian multinational conglomerate company, founded by Shashi Ruia and Ravi Ruia in 1969. It is currently held by Essar Telecom Ltd. Over the years, AGC evolved into an information and communication (ICT) solutions provider and integrator with a differentiated vertical approach in business communication systems, applications and services mainly within India.

The Ruia family story reads like a classic Indian business saga—from Shashi Ruia winning a major contract worth Rs. 2.3 crore for the construction of an outer breakwater for Chennai Port in 1969, thus laying the foundation of Essar Group. Five decades later, The company, known as Essar Global Fund Limited (EGFL), owns a variety of assets in the core sectors of energy (oil refining, oil and gas exploration and production, power), infrastructure & logistics (ports, projects), metals & mining, technology, and retail (oilfield services, information technology, and food retail). EGFL holds a nearly 100% stake in all its investments.

The corporate structure of Black Box under Essar ownership reveals a carefully orchestrated architecture. Promoter Holding: 70.4%—a level of control that allows for long-term strategic planning without the quarterly pressures that plague many public companies. This isn't passive ownership; it's active engagement at every level of the business.

Anshuman Ruia is part of the second generation of the Ruia family that founded Essar. Essar was founded in 1969 by his father, Shashi Ruia, and uncle, Ravi Ruia. Anshuman is known for his financial expertise and project execution skills that have been invaluable in Essar's value creation journey. His involvement with Black Box represents a continuation of the family's knack for identifying undervalued assets and transforming them. He was instrumental in overseeing Aegis, Essar's erstwhile BPO business, which expanded more than tenfold within a short span of time. In 2014 and 2017, the Aegis business was monetised in two tranches at a value that was almost 20 times the amount invested in the business.

The Essar philosophy toward Black Box is markedly different from typical private equity ownership. Currently, Anshuman is leading Essar's investment in asset-light, new age businesses in the technology and fintech domains. Black Box fits perfectly into this vision—a technology services company that doesn't require massive capital expenditure but can scale rapidly through expertise and relationships.

What's particularly intriguing is how Essar views Black Box in the context of its broader portfolio. In an exclusive interview with PTI, Prashant Ruia, director of Essar Capital, which manages the group's portfolio of investment, expressed confidence in the sector. "This is a company which can see tremendous growth, because the kind of growth taking place in data centres and managed services globally is exponential," he said.

The geographic and operational reality of Black Box under Essar ownership challenges conventional notions of Indian companies. Black Box, listed on the Indian stock exchanges, has operations spread across 35 countries, but its major business comes from the US. "It's obviously listed in India, but it's primarily headquartered, main operations are in the US. We currently do about USD 800 million of revenue in Black Box… about 75 per cent of the market for us is the US. We have a very large operation headquartered in Dallas, we have close to 3,000 people," he said.

This structure—Indian ownership, American operations, global delivery—creates unique advantages. The company can leverage India's cost advantages for delivery while maintaining high-touch presence in developed markets. It can access Indian capital markets while serving primarily Western clients. It can tap into Essar's relationships in emerging markets while maintaining Black Box's established position in developed economies.

The transformation of Essar itself provides context for Black Box's evolution. In November 2022, the Essar Group has become a debt-free company (cleared $25 billion in liabilities) by selling its power plant and captive ports to ArcelorMittal Nippon Steel at a deal value of $2.05 billion. This deleveraging has freed Essar to focus on growth businesses like Black Box rather than servicing legacy debt.

Essar's telecom heritage adds another dimension to the Black Box story. In 1995, Essar Group entered the telecom sector with a Swiss PTT joint venture partnership branded as the Essar Cellphone. In the same year, Essar Group started GSM operations from Delhi. Essar, independently and in partnership with Hutchison (Hutchison Essar), subsequently acquired more telecom circles in India. By 2006, all the circles were under Hutchison Essar Limited. The eventual exit from telecom—selling to Vodafone for billions—provided both capital and lessons that inform Black Box's strategy today.

Founded by brothers Shashi Ruia and Ravi Ruia in 1969, the Essar group, which once owned Hutchison Essar (now Vodafone-Idea), has no plans to re-enter the telecom market due to a lack of growth potential, said Ruia. The group ventured into the telecom space in 1995, with Essar Cellphone, and started GSM (Global System for Mobile Communications) operations from Delhi in the same year. Through the Hutchison Essar partnership, it started acquiring telecom circles in India, and by 2006, all the circles were under Hutchison Essar Limited. "From 1995-2010, it was an amazing time for being in the telecom sector. And we certainly benefited from that investment, we've benefited from that growth.

The corporate governance evolution under Essar has been notable. Sanjeev Verma is the Executive Director of Black Box Limited (formerly AGC Networks Ltd). He is also the President and CEO of Black Box Corporation (100% subsidiary of Black Box Ltd) since its acquisition by Black Box Ltd in 2019. As Executive Director, he is focused on leading the organization toward its vision to be the leading global IT solutions provider known and trusted for our customer-centric approach, commitment to customer success, and continuous innovation.

The decision to rebrand from AGC Networks to Black Box in 2021 was more than cosmetic—it was a recognition that in global technology markets, heritage and reputation matter. The Black Box brand, built over decades in America, carried more weight with Fortune 500 clients than AGC Networks ever could. It takes confidence and pragmatism for an acquirer to adopt the acquired company's identity.

Looking at the ownership structure today, what emerges is a unique model—concentrated Indian ownership of a fundamentally global business. Mumbai, May 27, 2025: Black Box Limited (BSE: 500463 | NSE: BBOX), Essar's technology arm and a leading provider of digital infrastructure solutions, announced its audited financial results for the quarter and year ended March 31, 2025. The description as "Essar's technology arm" is telling—Black Box isn't just a portfolio company but a strategic asset central to Essar's vision of the future.

The vision for Black Box under Essar extends far beyond its current scale. More than USD 200 billion/year of data centres are getting built in America alone, he said. Ruia, however, noted that the company is not into investing in data centres, but helping build and manage them. This positioning—as the picks-and-shovels provider to the AI gold rush rather than a gold miner—reflects sophisticated strategic thinking about where value accrues in technology cycles.

VII. Modern Era: AI, Data Centers & Digital Infrastructure (2020–Present)

The modern era of Black Box began not with a press release or acquisition announcement, but with a global pandemic that fundamentally altered how businesses think about digital infrastructure. COVID-19 didn't create the digital transformation trend—it put it on steroids, compressing five years of change into five months. For Black Box, positioned at the intersection of physical and digital infrastructure, this was the moment decades of capability building had prepared them for.

September 2023 marked a pivotal moment in Black Box's modern strategy with the inauguration of its new Center of Excellence located in Bengaluru, India. Encompassing an impressive 50,000 square feet, it boasts cutting-edge R&D Labs, Command Centers, client-tailored Offshore Delivery Centers, and dedicated discussion rooms, all designed to foster teamwork across teams and regions. This wasn't just another office opening; it was a statement of intent about where value would be created in the digital economy.

The facility represented more than physical infrastructure. As part of its global expansion plans, the company will be creating 500 additional jobs in India, thus enhancing its services for the growing needs of the customers. The new center is expected to increase the margin of the company by around Rs 50 crore in the near term. These weren't call center jobs or basic IT support roles—these were high-skilled positions in solutions architecture, AI infrastructure design, and hyperscale data center engineering.

The strategic timing of the Bengaluru expansion coincided with the AI revolution that began with ChatGPT's launch in late 2022. Suddenly, every enterprise needed GPU clusters, high-bandwidth networks, specialized cooling systems, and the expertise to orchestrate it all. Black Box found itself perfectly positioned—not as an AI company, but as the company that builds the infrastructure AI runs on.

The numbers from Q4 FY25 tell the story of this positioning paying off. Black Box Limited (BSE: 500463 | NSE: BBOX), a leading global provider of digital infrastructure solutions, today announced its best-ever quarterly performance for the financial year 2024–25, achieving order wins totaling INR 1,550 crore in Q4. This wasn't incremental growth; it was explosive expansion driven by fundamental shifts in technology spending.

The composition of these wins reveals the breadth of digital transformation underway. The quarter was marked by several key victories, including a landmark INR 240 crore order for a large-scale infrastructure modernization initiative with one of the United States' largest hospital networks. Healthcare, once a technology laggard, had become a digital infrastructure leader, driven by telemedicine, AI diagnostics, and electronic health records.

But the real story was in data centers. Additionally, Black Box secured over INR 225 crore in data center service contracts with major global hyperscalers. These weren't traditional data centers but AI-optimized facilities with specialized cooling, power management, and networking requirements. The company also secured two significant data center orders in the United States, one from a global hyperscaler and another from a top-ten global co-location provider. The hyperscalers—Amazon, Microsoft, Google, Meta—were in an arms race to build AI infrastructure, and Black Box was supplying the weapons.

Transportation infrastructure represented another transformation vector. The company also expanded its footprint in the transportation sector, winning over INR 130 crore in new orders for airport modernization projects. Post-COVID, airports weren't just transit points but complex digital ecosystems requiring contactless systems, real-time analytics, and sophisticated security infrastructure. Black Box's ability to integrate physical and digital systems made them ideal partners for these transformations.

The geographic distribution of wins demonstrated the truly global nature of the digital infrastructure boom. Further strengthening its position, Black Box secured significant orders outside of the U.S., with notable wins in the Asia-Pacific and Indian markets. These included a INR 90 crore engagement with a major consumer electronics firm in APAC region, as well as two large deals in India, one in the telecommunications sector for 5G rollout by Indian telcos and another with one of the largest municipal corporations totaling INR 180 crore.

The 5G rollout represented a particularly strategic win. As India deployed 5G infrastructure at unprecedented speed, Black Box's heritage in telecommunications combined with its modern digital capabilities positioned it uniquely. This wasn't just about installing towers; it was about creating the edge computing infrastructure that would enable everything from autonomous vehicles to smart cities.

India's digital public infrastructure initiatives created additional opportunities. As part of its India growth strategy, Black Box has committed ₹100 crore to expand its domestic business and enhance its Bengaluru Center of Excellence. Two major Indian contracts totalling ₹180 crore were secured during the year to support telecom and municipal infrastructure development, in line with the Company's focus on doubling India revenues. The municipal corporation wins were particularly significant, representing the digitization of urban governance—from traffic management to utility monitoring.

The transformation in client engagement models reflected broader industry shifts. Nearly two-thirds of all the deals won in Q1 FY26 were high-value engagements, demonstrating the success of the ongoing transformation and the company's strategic focus on large-scale projects with global marquee clients. The Company also continued to streamline its customer portfolio by reducing the long tail of low-value accounts, bringing the total to below 1,000 from around 1,500 last year. This wasn't just portfolio optimization; it was a fundamental shift from transactional relationships to strategic partnerships.

Financial performance reflected operational transformation. For the year FY25, revenue stood at ₹5,967 crore compared to ₹6,282 crore in FY24, moderated primarily due to delayed customer decision-making and a strategic exit from low-margin accounts. However, these measures contributed to significant margin enhancement, with EBITDA growing 24% YoY to ₹531 crore and EBITDA margin expanding by 210 basis points to 8.9%. PAT surged 49% YoY to ₹205 crore, with PAT margin improving by 120 basis points to 3.4%.

The margin expansion story was particularly compelling. By focusing on high-value solutions rather than commodity services, by leveraging the Bengaluru center for cost-effective delivery, and by embedding AI and automation in their own operations, Black Box was achieving the holy grail of IT services—revenue growth with margin expansion.

Looking at the order backlog provided confidence in future trajectory. The consolidated order backlog stood at $504 million as of March 31, 2025, covering approximately two-thirds of the projected revenue for the upcoming fiscal year. Order momentum remained strong, with the backlog at the end of Q1 FY26 at Rs 4,433 crore ($518 million), up from Rs 4,313 crore ($504 million) at the close of FY25.

The leadership's commentary revealed ambitious plans grounded in current reality. Commenting on the results, Sanjeev Verma, Whole Time Director, said, "Over the past five years, we have transformed Black Box from a loss-making entity into a profitable, cash-generating business with a strong balance sheet. With the turnaround complete, FY26 is about accelerating growth, scaling revenues, and capturing market leadership."

The AI infrastructure opportunity loomed large over everything. More than USD 200 billion/year of data centres are getting built in America alone. This wasn't a bubble but a fundamental rewiring of global computing infrastructure. Every enterprise AI initiative, every large language model deployment, every computer vision application required the kind of infrastructure Black Box specialized in.

The modern era of Black Box represents a convergence of multiple trends—the digitization of physical infrastructure, the physical infrastructure needs of digitization, the globalization of IT delivery, and the localization of global services. The company that started making telephone switches in 1986 was now building the nervous system of the AI age.

VIII. Financial Performance & Turnaround Story

The financial transformation of Black Box from 2019 to 2025 reads like a corporate turnaround masterclass—the kind business schools will study for decades. When AGC Networks completed the Black Box acquisition in January 2019, they inherited a company bleeding cash, struggling with debt covenants, and facing existential questions about its future. Five years later, the numbers tell a radically different story.

The headline achievement speaks volumes: Over the past five years, we have transformed Black Box from a loss-making entity into a profitable, cash-generating business with a strong balance sheet. This wasn't incremental improvement; it was fundamental transformation executed with surgical precision during one of the most volatile periods in modern business history.

The FY25 results crystallize this transformation. For the year FY25, revenue stood at ₹5,967 crore compared to ₹6,282 crore in FY24, moderated primarily due to delayed customer decision-making and a strategic exit from low-margin accounts. However, these measures contributed to significant margin enhancement, with EBITDA growing 24% YoY to ₹531 crore and EBITDA margin expanding by 210 basis points to 8.9%. PAT surged 49% YoY to ₹205 crore, with PAT margin improving by 120 basis points to 3.4%.

The decision to sacrifice revenue for profitability was counterintuitive but brilliant. While competitors chased top-line growth, Black Box methodically pruned its customer base. The Company also continued to streamline its customer portfolio by reducing the long tail of low-value accounts, bringing the total to below 1,000 from around 1,500 last year. This wasn't downsizing; it was focusing firepower where it mattered most.

The margin expansion story deserves particular attention. Moving EBITDA margins from 6.8% to 8.9% in a single year, while the industry struggled with wage inflation and supply chain disruptions, required operational excellence across every dimension. The company achieved this through a combination of automation, offshore leverage through the Bengaluru center, and ruthless focus on high-value solutions over commodity services.

Quarterly progression through FY25 showed accelerating momentum. Profit after tax for Q3FY25 stood at INR 56 crore, highest ever, growing by 37% YoY and 10% QoQ. For 9mFY25, PAT increased to INR 144 crore, reflecting a growth of 49% YoY. PAT margins improved by 120 bps YoY and stood at 3.7% in Q3FY25 whereas for 9mFY25 PAT margins stood at 3.3%, reflecting a growth of 130 bps YoY.

The Q4 FY25 performance represented the culmination of the turnaround. Q4FY25 performance remained strong with revenue rising to ₹1,545 crore, a 4% YoY increase. EBITDA for the quarter stood at ₹147 crore, up 21% YoY, with a margin of 9.5%, an improvement of 130 basis points. PAT in Q4FY25 grew 48% YoY and 8% sequentially to ₹60 crore, with PAT margin increasing by 120 basis points to 3.9%.

What makes these numbers remarkable is the context. The company has delivered a poor sales growth of 3.62% over past five years. Yet profitability exploded. This apparent paradox reveals the depth of transformation—from a volume-focused, low-margin business to a value-focused, high-margin solutions provider.

The credit rating upgrade provided external validation of the turnaround. Further strengthening its financial standing, CRISIL upgraded Black Box's long-term credit rating to BBB+/Stable in March 2025. For a company that couldn't meet debt covenants in 2018, achieving investment-grade rating represented a complete reversal of fortune.

Capital allocation reflected newfound confidence. In recognition of its strong operational and financial performance, the Company has recommended a final dividend of 50% (₹1 per share on a face value of ₹2), subject to shareholder approval. Paying dividends while investing for growth—the hallmark of a mature, cash-generative business.

The order book evolution told its own story of transformation. Order momentum remained robust through Q4FY25, with the Company reporting over Rs 1,550 crore in new deal wins—more than double the average of the previous three quarters. Notable wins included a Rs 240 crore digital modernisation contract with a major US hospital network, over Rs 225 crore in data center services for global hyperscalers, Rs 130+ crore in transportation (airport modernisation), Rs 90 crore in the education sector from a leading U.S. university, and a Rs 90 crore engagement with a major APAC-based consumer electronics firm. The consolidated order backlog stood at $504 million as of March 31, 2025, covering approximately two-thirds of the projected revenue for the upcoming fiscal year.

The shift in deal composition was as important as deal size. Nearly two-thirds of all the deals won in Q1 FY26 were high-value engagements, demonstrating the success of the ongoing transformation and the company's strategic focus on large-scale projects with global marquee clients. These weren't commodity contracts but strategic partnerships requiring deep expertise and long-term commitment.

The India growth strategy added another dimension to the financial story. As part of its India growth strategy, Black Box has committed Rs 100 crore to expand its domestic business and enhance its Bengaluru Centre of Excellence. This investment, while substantial, was expected to pay back quickly through margin improvement and new client wins.

Looking at working capital management, the transformation was equally impressive. From struggling to meet payables in 2018 to maintaining healthy cash reserves while funding growth—the balance sheet had been completely rehabilitated. The company's ability to self-fund expansion while paying dividends demonstrated the sustainability of the turnaround.

The leadership's commentary revealed ambitious yet grounded thinking. Mr. Sanjeev Verma, Whole Time Director, stated: "Our strategic focus on high-value customer segments and operational rigor has led to a meaningful expansion in both order book and profitability. The ongoing digital and AI-driven transformation across industries presents structural growth opportunities, and we are well-positioned to capitalize on them."

The CFO's perspective added financial discipline to strategic ambition. Mr. Deepak Kumar Bansal, Executive Director and Global CFO, noted: "FY25 marked strong progress on profitability and capital efficiency. Our EBITDA margins continue to move toward our double-digit target, supported by quality of revenues and operating discipline."

What emerged from the financial analysis was a company that had successfully navigated one of the most difficult transformations in enterprise technology—from product to solutions, from volume to value, from struggling to thriving. The journey from a distressed American acquisition to a profitable global solutions provider with investment-grade rating and ambitious growth plans represented not just financial engineering but fundamental business transformation.

The company's ability to grow profitability while strategically shrinking revenue, to invest in growth while returning capital to shareholders, to maintain discipline while pursuing ambitious targets—these apparent contradictions revealed sophisticated management thinking rarely seen in turnaround situations.

Looking forward, the financial foundation was now solid enough to support aggressive growth. With the turnaround complete, FY26 is about accelerating growth, scaling revenues, and capturing market leadership. While the year began at a slower pace, we are seeing solid traction in key accounts and are actively engaged in multiple high-value opportunities.

IX. The $2 Billion Vision & Future Strategy

In the boardrooms of Black Box, executives aren't discussing incremental growth or market share gains—they're plotting a complete reimagination of what a digital infrastructure company can become. Digital infrastructure firm Black Box is setting its sights on attaining a $2 billion revenue target by financial year 2028 (FY28) as it capitalises on surging demand for data centres, AI-driven infrastructure, and digital connectivity solutions. For a company generating approximately $700 million today, this isn't evolution—it's revolution.

The audacity of the vision becomes clear when you consider the math. Indian digital network builder Black Box Ltd. is seeking to nearly triple sales to $2 billion over the next four years, betting on growing demand for data centers and cybersecurity services in its largest market of North America. This requires compound annual growth rates that would make even high-flying tech startups envious, but for a company with Black Box's heritage and current positioning, it's not fantasy—it's physics.

The strategy rests on three fundamental transformations, each revolutionary in its own right. First, the shift from transactional to annuity-based revenue models. Second, the concentration on high-value clients with deep, strategic relationships. Third, the positioning at the intersection of physical and digital infrastructure where the AI revolution is creating unprecedented demand.

During an earnings call, Chief Executive Officer (CEO) Sanjeev Verma said that the roadmap to $2 billion revenue is rooted in adapting to the digital infrastructure needs of top global clients. Black Box has recently revamped its go-to-market strategy to concentrate on 300 high-spend clients across sectors like financial services, healthcare, and technology, ensuring deep engagement and tailored services for each. This isn't about finding 300 new clients; it's about becoming indispensable to 300 of the world's most important organizations.

The go-to-market transformation reveals sophisticated strategic thinking. "We realised earlier on that our go-to-market structure wasn't designed to be able to bring in hyper-growth and therefore we invested in high quality talent, reorganising our go-to-market with vertical focus and horizontal focus," said Verma. The vertical focus allows deep industry expertise—understanding the unique needs of healthcare versus financial services versus manufacturing. The horizontal focus ensures comprehensive solution capability across all technology domains.

The numbers behind the strategy are compelling. A healthy pipeline of $2.5 billion signals strong growth visibility amid rising global IT spending, projected at $5.27 trillion in 2024. Black Box's verticalized sales approach targets its top 300 global clients -- including Fortune 500 giants such as Meta, Intel, Disney, and Bank of America -- focusing on expanding wallet share in these strategic accounts. These aren't just customers; they're strategic partnerships where Black Box becomes embedded in the client's digital transformation journey.

The AI infrastructure opportunity alone could justify the ambitious targets. With hyperscalers significantly increasing their capital expenditure—projected at US$ 325 billion in 2025, a 55% year-over-year rise—Black Box is well-positioned to support the next-gen digital infrastructure powering AI and AI-driven models. Every dollar of hyperscaler capex translates into multiple dollars of services opportunity for companies like Black Box that can design, build, and manage the infrastructure.

Geographic strategy adds another growth vector. With India currently contributing 6% to its business, Black Box aims to increase this to 7-8%. Additionally, the firm plans to expand its Indian workforce from around 600 to 1,000 employees in the next few years. Verma emphasized the strategic importance of India from both a local market and global expertise perspective, planning significant investments in Indian capability centers. This isn't just about cost arbitrage; it's about tapping into India's deep pool of engineering talent to serve global markets.

The shift to annuity models represents perhaps the most fundamental transformation. Instead of one-time project revenues, Black Box is building recurring revenue streams through managed services, infrastructure-as-a-service, and long-term support contracts. This shift not only provides revenue predictability but also deepens client relationships and increases lifetime value.

The company's confidence comes from early proof points. This, in turn, will accelerate the need for robust digital infrastructure. As a result, hyperscalers are making significant capital investments in AI infrastructure and data centers, reinforcing our confidence in reaching our growth target of US$2 billion in revenue by FY29. The recent wins with hyperscalers, hospitals, and airports validate both the strategy and execution capability.

Portfolio optimization continues alongside growth initiatives. Focusing on the top 250 clients that generate 90% of its revenues, the company aims to shift from a geography-led go-to-market approach in America to a vertical-led strategy, covering five key sectors: banking, finance, healthcare, technology, and industrial. Black Box also intends to exit non-accretive customers and focus on long-term client relationships to achieve its $2 billion revenue goal by fiscal year 2028.

The leadership team's commitment is evident in their communication. "The rapid advancements in AI and the ongoing developments in this field are expected to drive a global surge in demand for AI tools across businesses," Verma noted, reinforcing the structural tailwinds supporting the growth ambition.

Financial discipline underpins the growth strategy. Mr. Deepak Kumar Bansal, Executive Director and Global Chief Financial Officer of Black Box, commented, "Our relentless focus on improving operating performance allowed us to achieve highest ever quarterly PAT. The company has, over the last few years, consistently generated strong ROE and ROCE, and remains committed to generating positive cash flows and better returns for the shareholders." Growth without profitability is vanity; Black Box is pursuing profitable growth.

The operational levers for achieving the vision are clear. Black Box operates 75 delivery centers worldwide, with 14 in India and 21 in the US, and employs over 4,000 people globally. Scaling to $2 billion will require expanding this footprint, but more importantly, increasing productivity and value creation per employee. The focus on high-value services and AI-augmented delivery can drive this productivity improvement.

Market dynamics support the ambition. The convergence of multiple technology trends—5G rollout, edge computing, AI infrastructure, hybrid cloud, zero-trust security—creates a perfect storm of demand for Black Box's capabilities. Unlike previous technology cycles that were sequential, these trends are simultaneous and synergistic, multiplying the opportunity.

The competitive positioning for this growth is unique. While global system integrators like Accenture and IBM operate at much larger scale, they often lack Black Box's specialized focus on digital infrastructure. While specialized players excel in narrow domains, they lack Black Box's comprehensive capability. Black Box occupies a sweet spot—specialized enough to add unique value, comprehensive enough to be a one-stop shop.

Risk management isn't ignored in the pursuit of growth. The company's strategy of concentrating on fewer, larger clients could increase customer concentration risk, but it also allows deeper relationships and higher switching costs. The focus on annuity revenue reduces project risk and revenue volatility. The geographic diversification across US, Europe, and Asia-Pacific markets provides resilience against regional downturns.

The $2 billion vision isn't just about size—it's about transformation. It's about evolving from a services company to a platform company, from a vendor to a partner, from reactive to proactive. It's about building the digital infrastructure that will power the next decade of technological advancement.

Looking at the trajectory from $700 million to $2 billion, what emerges isn't just a growth story but a reimagination of what Black Box can become. The company that started making telephone switches in 1986, that survived multiple ownership changes and near-death experiences, is positioning itself at the center of the digital economy. The vision is ambitious, but for a company that has already defied odds multiple times, it might just be achievable.

X. Playbook: Business & Investing Lessons

The Black Box story offers a masterclass in corporate transformation, providing lessons that extend far beyond technology services. Each phase of the company's evolution—from Tata Telecom to global digital infrastructure leader—reveals principles that apply to any business navigating technological disruption and market evolution.

Lesson 1: The Power of Strategic M&A in Technology Services

The Black Box acquisition stands as a textbook example of contrarian M&A strategy. AGC Networks paid roughly $16.3 million in equity value for a company generating $600 million in revenue—a Price-to-Sales ratio of 0.027 that would make any value investor salivate. But the real genius wasn't in buying cheap; it was in recognizing that distressed assets in technology services can be transformed through operational excellence rather than financial engineering.

The lesson extends beyond price. Black Box had something money couldn't easily buy: decades-old relationships with Fortune 500 companies, a recognized brand in critical infrastructure, and deep technical expertise. AGC brought what Black Box lacked: financial stability, low-cost delivery capability from India, and patient capital willing to sacrifice short-term revenue for long-term profitability. This complementarity created value that neither company could achieve alone.

Lesson 2: Managing Complex Corporate Ownership Transitions

The company's journey through multiple owners—Tata to Avaya to Essar—demonstrates that ownership changes need not be destructive if managed correctly. Each transition brought new capabilities: Tata provided the foundation and Indian market access, Avaya brought global technology and enterprise relationships, and Essar provided capital and strategic vision for the digital age.

The key was maintaining continuity where it mattered—customer relationships, technical expertise, operational excellence—while embracing change where needed. The decision to keep the Black Box brand after acquisition, rather than imposing AGC Networks' identity, showed remarkable pragmatism. In technology services, reputation and relationships matter more than corporate ego.

Lesson 3: Building a Global Delivery Model from an Indian Base

Black Box inverted the traditional Indian IT services model. Instead of starting in India and trying to go global, it acquired a global company and built Indian delivery capability to support it. This created immediate credibility with Western clients who might have been skeptical of another Indian IT services company.

The Bengaluru Center of Excellence, opened in 2023, exemplifies this strategy. It's not a back-office cost center but a strategic asset that combines Indian engineering talent with global delivery standards. The center enables Black Box to compete on both cost and capability, offering Fortune 500-quality services at competitive prices.

Lesson 4: The Importance of Pivoting from Products to Solutions

Black Box's evolution from manufacturing EPABX systems to delivering comprehensive digital infrastructure solutions illustrates a fundamental truth: in technology, product companies eventually become solution companies or become irrelevant. The margins are in solving problems, not selling boxes.

This transition required fundamental changes in everything from sales approach to delivery model to financial metrics. Instead of measuring success by units sold, Black Box now measures customer lifetime value, solution adoption, and managed services growth. The shift from CapEx to OpEx models aligned with how customers want to consume technology, creating stickier relationships and more predictable revenue.

Lesson 5: Capital Allocation in a Services Business

The financial transformation of Black Box offers crucial lessons in capital allocation. The decision to sacrifice revenue growth for margin expansion—shrinking from 1,500 to under 1,000 customers while improving EBITDA margins from 6.8% to nearly 10%—required courage and conviction.

The company's capital allocation priorities are instructive: First, achieve profitability and cash generation. Second, invest in strategic capabilities (like the Bengaluru center). Third, pursue selective M&A (like GSN Australia). Fourth, return capital to shareholders through dividends. This disciplined approach created a virtuous cycle where profitability funded growth rather than growth consuming capital.

Lesson 6: Navigating the Shift from Public to Private Ownership

Black Box's transition from NASDAQ-listed company to privately held subsidiary of AGC Networks offers lessons in the trade-offs between public and private ownership. As a public company, Black Box faced quarterly earnings pressure that made long-term transformation difficult. Private ownership under Essar allowed patient capital and strategic flexibility.

The current structure—listed in India but operating globally—creates an interesting hybrid. Indian capital markets provide liquidity and transparency, while the concentrated ownership (70.4% promoter holding) enables long-term strategic planning. This structure allows Black Box to access public capital while maintaining strategic flexibility.

Lesson 7: Timing Technology Cycles

Black Box's positioning for the AI infrastructure boom demonstrates the importance of anticipating technology cycles. The company didn't try to become an AI company; instead, it positioned itself as the company that builds the infrastructure AI runs on. This picks-and-shovels strategy often proves more profitable than mining for gold.

The convergence of multiple trends—5G, edge computing, AI, hybrid cloud—created a perfect storm of opportunity. Black Box's broad capabilities across all these domains positioned it uniquely to capture value from the convergence. The lesson: in technology, it's often better to be broadly capable at inflection points than narrowly excellent in stable markets.

Lesson 8: Customer Concentration as Strategy, Not Risk

Conventional wisdom suggests customer concentration is risky. Black Box turned this on its head, deliberately concentrating on 300 high-value clients. This focus allows deep expertise, better resource allocation, and higher margins. When you're embedded in a Fortune 500 company's critical infrastructure, switching costs are high and relationships are sticky.

The key is choosing the right customers. Black Box's focus on Fortune 500 companies and hyperscalers ensures it's serving customers who are themselves growing and have the budget for digital transformation. Serving Meta's data center needs or Bank of America's trading floor infrastructure creates references that open doors globally.

Lesson 9: The Moat in Unglamorous Infrastructure

While Silicon Valley chases the next consumer app or AI model, Black Box built a moat in the unglamorous but essential business of digital infrastructure. The company's expertise in mission-critical systems—where failure isn't an option—creates high barriers to entry and switching costs.

This infrastructure focus provides resilience. Economic cycles affect discretionary technology spending, but critical infrastructure must be maintained. During COVID-19, while many technology companies struggled, demand for Black Box's services accelerated as digital infrastructure became even more critical.

Lesson 10: Culture and Capabilities Through Transformation

Perhaps the most remarkable aspect of Black Box's journey is maintaining organizational capability through multiple transformations. From American public company to Indian private company, from product manufacturer to solutions provider, from North America-focused to globally distributed—each transformation could have destroyed organizational culture and capability.

The key was respecting what worked while changing what didn't. Technical expertise was preserved and enhanced. Customer relationships were maintained and deepened. The Black Box brand, built over decades, was retained rather than discarded. This respect for heritage while embracing change created continuity that customers and employees could trust.

The Meta-Lesson: Transformation as a Continuous Process

The overarching lesson from Black Box is that transformation isn't a destination but a continuous journey. The company that made telephone switches in 1986 bears little resemblance to today's digital infrastructure leader, yet there's a continuous thread of evolution rather than revolution.

Each phase built on the previous one: Manufacturing expertise enabled systems integration. Systems integration enabled managed services. Managed services enabled digital transformation consulting. At each stage, the company retained what worked while adding new capabilities. This evolutionary approach reduced risk while enabling dramatic transformation over time.

For investors, Black Box offers a case study in value creation through operational transformation rather than financial engineering. For operators, it demonstrates that even mature, struggling companies can be transformed with the right vision, capital, and patience. For students of business, it shows that success often comes not from doing one thing brilliantly but from combining multiple capabilities in unique ways.

The playbook isn't complete—Black Box continues to evolve, with its $2 billion vision representing the next chapter rather than the final destination. But the lessons learned so far provide valuable insights for anyone navigating the intersection of technology, globalization, and corporate transformation.

XI. Analysis & Investment Case

Analyzing Black Box as an investment requires viewing it through multiple lenses—as a turnaround story, a play on digital infrastructure, and a bet on AI-driven transformation. The bull and bear cases are both compelling, making this a fascinating study in investment analysis under uncertainty.

Competitive Positioning: David Among Goliaths

Black Box operates in a fiercely competitive landscape, facing giants like Accenture, IBM, and Indian IT majors on one side, and specialized players like Vertiv and CommScope on the other. Yet its positioning is unique—more specialized than the generalists, more comprehensive than the specialists.

Against global system integrators, Black Box's advantage lies in focus. While Accenture might assign junior consultants to a data center project, Black Box deploys specialists who've spent careers in digital infrastructure. This expertise gap becomes critical in mission-critical implementations where failure isn't an option.

Versus Indian IT services companies, Black Box's differentiation is its Western heritage and embedded presence. While TCS or Infosys might struggle to win a US hospital's trust for critical infrastructure, Black Box has been serving these clients for decades. The combination of Western credibility and Indian delivery creates a unique value proposition.

Market Concerns: The Bear's Perspective

The market's skepticism is reflected in the numbers. "Poor sales growth of 3.62% over past five years" isn't a ringing endorsement. Trading at 11.1 times book value suggests the market sees asset value but questions growth potential. The stock down 6.90% over the past year while markets hit records raises red flags.

Customer concentration presents real risks. With 300 clients generating 90% of revenue, losing even a few major accounts could be devastating. The focus on Fortune 500 companies means selling to sophisticated buyers with procurement power, limiting pricing flexibility.

Technology risk looms large. If hyperscalers decide to bring infrastructure services in-house, or if AI advancement reduces the need for human services, Black Box's model could face existential threats. The company's limited R&D spending means it's a consumer, not creator, of technology innovation.

Execution risk on the $2 billion vision is substantial. Tripling revenue in four years requires everything to go right—market growth, competitive wins, operational excellence, and successful M&A. Any stumble could derail the timeline and damage credibility.

The global nature of operations introduces currency risk, regulatory complexity, and geopolitical exposure. With 75% of revenue from the US but significant operations in India, the company faces multiple economic and political variables beyond its control.

Bull Case: Riding Structural Tailwinds

The bull case rests on structural changes in technology spending that favor Black Box's positioning. The AI infrastructure buildout isn't a bubble but a fundamental rewiring of global computing infrastructure. With hyperscalers projecting $325 billion in capex for 2025 alone, even capturing a tiny fraction represents massive growth.

Digital infrastructure has become critical infrastructure. Just as governments invest in roads and airports, enterprises must invest in digital infrastructure to remain competitive. This isn't discretionary spending but existential necessity, providing resilience through economic cycles.

The margin expansion story has legs. Moving from 6.8% to 8.9% EBITDA margins in one year demonstrates operational leverage. With the Bengaluru center ramping up and customer concentration increasing, margins could reach the targeted double digits, dramatically improving profitability even on modest revenue growth.

The annuity revenue shift changes the investment math. Recurring revenue deserves higher multiples than project revenue. As Black Box shifts its mix toward managed services and multi-year contracts, valuation should re-rate higher.

India's emergence as a global technology hub provides sustained advantages. The combination of engineering talent, cost advantages, and government support creates structural advantages that are difficult to replicate. Black Box's ability to leverage India while maintaining Western market presence is increasingly valuable.

Bear Case: Structural Challenges

The bear case extends beyond execution risk to structural challenges. The services business model inherently lacks the scalability of software. Every dollar of revenue requires human delivery, limiting operating leverage and margin potential.

Competition is intensifying, not diminishing. Cloud providers are expanding their professional services arms. Hardware vendors are moving into services. Pure-play specialists are consolidating. Black Box risks being squeezed from all directions.

The technology services industry faces commoditization pressure. What's specialized today becomes standardized tomorrow. Black Box must constantly climb the value chain just to maintain position, requiring continuous investment and transformation.

Customer buying patterns are evolving toward cloud-native, API-first, self-service models that may reduce the need for traditional system integration. If infrastructure becomes code, what role do infrastructure integrators play?

Valuation Analysis: Multiple Perspectives

At ₹8,450 crore market cap on ₹5,967 crore revenue, Black Box trades at 1.4x sales—not expensive for a growing technology services company but not cheap for one with single-digit growth. The 11.1x book value multiple suggests the market values the business well above its tangible assets, implying confidence in intangible value.

Comparing to peers provides context. Indian IT services companies trade at 3-5x sales but grow faster. Global system integrators trade at similar multiples but have more diverse revenue streams. Specialized infrastructure companies command higher multiples but have more focused offerings.

The improving return metrics support higher valuation. With ROE improving and cash generation strengthening, Black Box is creating shareholder value beyond just revenue growth. The dividend payment signals confidence in sustainable cash generation.

Investment Case Synthesis

Black Box represents a complex investment proposition—part value, part growth, part transformation story. For value investors, the operational improvements and margin expansion provide near-term catalysts. For growth investors, the $2 billion vision and AI infrastructure boom offer long-term upside.

The risk-reward appears asymmetric. Downside seems limited given the asset value, customer base, and improving fundamentals. Upside could be substantial if the company executes on its vision and captures even a small share of the infrastructure boom.

Time horizon matters critically. Short-term investors might be frustrated by lumpy revenue and quarterly volatility. Long-term investors could benefit from structural transformation and market growth. The stock appears more suitable for patient capital willing to wait for the story to unfold.

Portfolio context influences attractiveness. As a pure play on digital infrastructure, Black Box offers targeted exposure to a specific theme. Within a diversified portfolio, it could provide differentiated returns uncorrelated with broader technology indices.

Key Metrics to Watch

Several metrics will indicate whether the investment thesis is playing out:

- Order book growth: Sustained growth above 20% would validate demand

- Margin progression: Reaching 10% EBITDA margins would confirm operational leverage

- Customer concentration: Winning new Fortune 500 clients while retaining existing ones

- Annuity revenue mix: Increasing proportion of recurring revenue

- India revenue growth: Successful expansion in home market

- Hyperscaler wins: Continued success with AWS, Azure, Google Cloud projects

- Credit rating: Further upgrades would reduce capital costs

- M&A execution: Successful integration of acquisitions like GSN

The Verdict: Compelling but Complex

Black Box presents a compelling but complex investment case. The company has clearly turned the corner operationally, with improving margins, strengthening cash flow, and ambitious growth plans. The positioning at the intersection of physical and digital infrastructure, just as AI drives unprecedented demand, appears fortuitous.

Yet risks are real and numerous. Execution challenges, competitive threats, and technology disruption could derail the story. The concentrated customer base and services-heavy model limit scalability and increase vulnerability.

For investors willing to do the work—understanding the industry dynamics, tracking execution metrics, and maintaining patience—Black Box offers an interesting opportunity. It's not a simple momentum play or value trap but a transformation story requiring continuous monitoring and assessment.

The investment case ultimately depends on one's view of digital infrastructure's future. If you believe AI and digital transformation will drive sustained infrastructure investment, Black Box is well-positioned to benefit. If you think infrastructure will be commoditized or internalized by cloud providers, the story becomes much more challenging.

XII. Epilogue & Looking Forward

As the sun sets on another trading day in Mumbai, with Black Box shares having traced their familiar pattern on the NSE, it's worth stepping back to contemplate the extraordinary journey this company has traveled—and the road ahead that remains uncharted.

The Digital Infrastructure Supercycle Thesis

We stand at an inflection point in technological history. The AI revolution isn't just another tech trend but a fundamental rewiring of how computation happens, where it happens, and what it enables. Every large language model training run, every computer vision application, every autonomous vehicle deployment requires massive infrastructure investment. The $325 billion in hyperscaler capex projected for 2025 is likely just the beginning.