Banco Products: India's Engine Cooling Champion Goes Global

I. Introduction & Episode Teaser

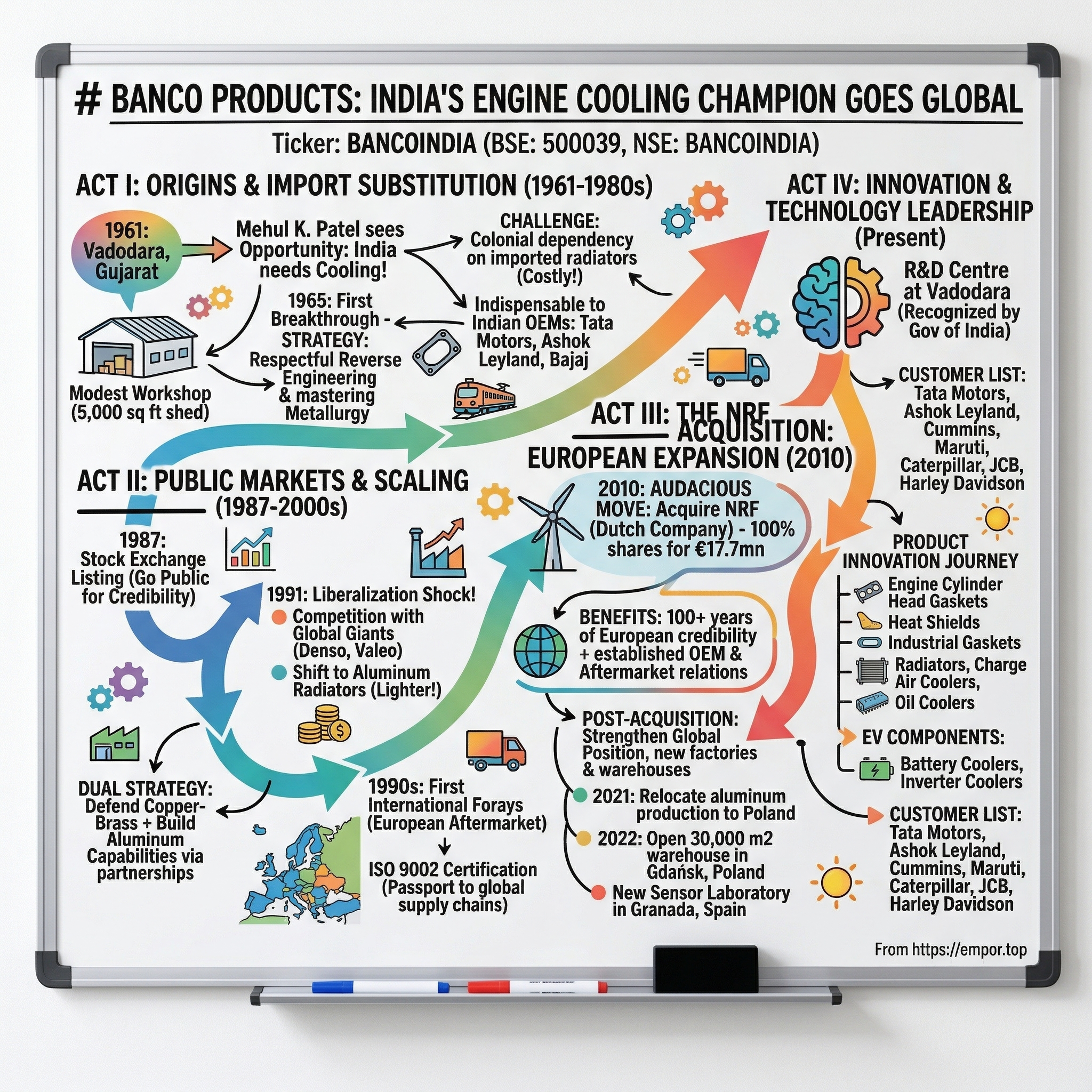

Picture this: A sweltering summer day in 1961 Vadodara, Gujarat. The temperature soars past 45°C, heat waves shimmer off the dusty roads, and in a modest workshop, a young entrepreneur named Mehul K. Patel is dismantling a British-made radiator, studying every weld, every fin, every brazed joint with the intensity of a surgeon. India has just emerged from colonial rule barely 14 years ago, foreign exchange is scarce, and the nation's nascent automotive industry is desperately dependent on expensive imported components. Patel sees opportunity where others see obstacles—if Indian engines need cooling, why shouldn't Indians build the cooling systems?

Fast forward six decades. That workshop has transformed into Banco Products (India) Limited, a ₹7,793 crore market cap powerhouse manufacturing critical engine cooling and sealing systems for everyone from Tata Motors to Harley Davidson. The company's products cool engines in Indian Railways locomotives thundering across the subcontinent, in JCB excavators digging Mumbai's metro tunnels, and in European trucks navigating Alpine passes through its Dutch subsidiary NRF.

Here's the hook that makes this story remarkable: How did an Indian auto components manufacturer, starting in the protected License Raj era, not only survive liberalization but actually acquire a 97-year-old European company during the 2008 financial crisis and build a global footprint spanning 11 warehouses across Europe and the USA? This isn't just another auto parts supplier story—it's a masterclass in patient capital, opportunistic acquisition, and the often-overlooked art of making unsexy products absolutely indispensable.

The Banco story unfolds across three distinct acts: First, the import substitution era where survival meant mastering reverse engineering and building trust with skeptical domestic OEMs. Second, the liberalization shock where the company had to compete with global giants flooding the Indian market. And third, the audacious international expansion where Banco flipped the script—instead of being acquired by a Western firm, they became the acquirer.

What makes this particularly fascinating for investors is the paradox at Banco's core: It's simultaneously a boring, predictable business (engines will always need cooling) and a high-tech innovation play (EV batteries need sophisticated thermal management). It's deeply cyclical (tied to automotive production) yet remarkably resilient (33.4% ROCE through multiple downturns). It's quintessentially Indian in its patient, family-run approach yet thoroughly global in its ambitions and operations.

II. Origins & The Import Substitution Era (1961-1980s)

The year 1961 marked a peculiar moment in India's industrial history. Jawaharlal Nehru's socialist vision was in full swing, the Second Five-Year Plan had prioritized heavy industry, and the rupee was haemorrhaging as the country imported everything from steel to safety pins. The Reserve Bank of India's foreign exchange reserves had dwindled to barely two months of import cover. In this crucible of scarcity, the Indian government's message to entrepreneurs was clear: "Make in India or India doesn't make it."

Enter Mehul K. Patel, an engineer who had spent years working in the automotive sector, watching with growing frustration as Indian manufacturers paid exorbitant prices for imported radiators and gaskets. The math was simple but painful—a radiator that cost $50 to manufacture in Birmingham was landing in Bombay at $200 after shipping, duties, and intermediary margins. For India's fledgling truck manufacturers like TELCO (later Tata Motors) and Ashok Leyland, cooling systems alone were eating up 8-10% of vehicle costs.

Patel's initial setup in Vadodara was deliberately modest—a 5,000 square foot shed with second-hand brazing equipment purchased from a defunct textile machinery unit. The choice of Vadodara was strategic: close enough to Bombay's port for raw material imports, connected by rail to Delhi and Calcutta's industrial belts, yet far enough from major cities to keep land and labor costs manageable. But the real asset wasn't the location—it was Patel's obsessive focus on metallurgy. The early years weren't about sophisticated R&D or cutting-edge technology—they were about mastering the mundane yet critical art of brazing copper tubes to brass headers without leaks. Banco was established in 1961, incorporated by Mehul K. Patel who brought over 40 years of automotive industry experience. Patel understood that in the License Raj economy, where getting an industrial license could take years and importing a machine required navigating 47 different forms, the winners would be those who could indigenize fastest.

The company's first breakthrough came through what Patel called "respectful reverse engineering." He would acquire damaged radiators from truck accidents, meticulously document every component, test different copper alloys available in India, and gradually improve upon the original designs. The Indian copper wasn't as pure as its British counterpart, so Banco had to compensate with thicker gauges. The brazing flux available locally left more residue, requiring additional cleaning processes. Every adaptation was a small innovation born of constraint.

By 1965, Banco had its first major validation—an order from Indian Railways for locomotive radiators. The railway bureaucracy was notoriously conservative, preferring proven British suppliers even at premium prices. But Patel had identified their Achilles heel: delivery times. While imported radiators took 6-8 months to arrive, Banco could deliver in 6 weeks. When a critical locomotive depot in Itarsi faced an emergency shortage, Banco's ability to rush deliver 50 radiators in 10 days earned them a permanent spot on the approved vendor list.

The 1970s marked Banco's expansion beyond survival mode. The company had mastered radiators and began diversifying into gaskets—a seemingly simpler product that actually required precise material science. The challenge with gaskets wasn't making them; it was making them survive Indian conditions. European gaskets were designed for consistent temperatures and clean fuels. Indian trucks operated in temperature swings from -10°C in Ladakh to 50°C in Rajasthan, using diesel with sulfur content that would horrify European regulators.

Banco's product range expanded to include engine cylinder head and peripheral gaskets, heat shields and industrial gaskets with a wide material range for demanding sealing applications. The company developed proprietary compounds mixing asbestos (before it was banned) with local materials like mica and specially treated cotton fibers. These "jugaad gaskets," as workers nicknamed them, could handle temperature extremes that would destroy imported alternatives.

By the 1980s, Banco had become indispensable to India's automotive ecosystem. The company was supplying to virtually every major OEM—TELCO, Ashok Leyland, Bajaj, Premier Automobiles, and Hindustan Motors. The relationships weren't just commercial; they were deeply personal. Patel would personally visit plant managers, understand their specific pain points, and customize solutions. When Ashok Leyland needed radiators that could handle overloading (Indian trucks routinely carried 2x their rated capacity), Banco developed reinforced designs with 30% extra cooling capacity.

The numbers tell the story of patient growth: From a single shed in 1961 to three manufacturing units by 1985. From 12 employees to over 400. From one product (radiators) to a comprehensive range of cooling and sealing solutions. Revenue grew from lakhs to crores, though exact figures from this era remain undisclosed in public records.

What's remarkable about this period is what Banco didn't do. They didn't diversify into unrelated businesses like many Indian conglomerates. They didn't pursue glamorous consumer products. They didn't lobby for protection or subsidies. Instead, they obsessed over the unglamorous fundamentals: metallurgy, heat transfer efficiency, and manufacturing precision. This focus would prove crucial when India's economy suddenly opened up in 1991, and Banco found itself competing not with other protected Indian firms, but with global giants who had been perfecting cooling systems for a century.

III. Public Markets & Scaling (1987-2000s)

The company was listed on the Indian stock exchange in 1987, a move that seemed almost premature given India's nascent capital markets. The Bombay Stock Exchange had barely 2,000 listed companies, daily trading volumes were thin, and most Indians still viewed stock investing as sophisticated gambling. Yet for Banco, going public wasn't about raising capital—it was about credibility. Multi-national customers like Cummins and Caterpillar, who were setting up Indian operations, wanted suppliers with transparent governance and audited financials.

The IPO itself was a modest affair—raising just ₹3.2 crores at a price that valued the entire company at ₹18 crores. The roadshow, if you could call it that, consisted of Mehul Patel visiting a handful of mutual funds in Mumbai and explaining, with characteristic engineering precision, why radiators were a growth business. The pitch was simple: India had 2 vehicles per 1,000 people versus 400 in developed countries. Even reaching 20 per 1,000 would mean a 10x growth in the automotive industry.

Then came 1991—India's economic crucible moment. Finance Minister Manmohan Singh's liberalization reforms didn't just open markets; they shattered comfortable monopolies overnight. Suddenly, Maruti could import cooling systems from Denso. Tata Motors could source from Valeo. Global component giants who had been kept out for decades came flooding in with technology that made Banco's products look antiquated.

The first reality check came from an unexpected source—aluminum. While Banco had perfected copper-brass radiators, the world had moved to aluminum. Aluminum radiators were 40% lighter, had better heat dissipation, and were increasingly preferred by global OEMs. Banco's entire manufacturing infrastructure, built around copper brazing, was at risk of obsolescence.

Patel's response revealed the strategic thinking that would define Banco's next phase. Instead of panicking or immediately scrapping copper production, he initiated a dual strategy. First, defend the existing business by becoming so efficient at copper-brass that even with aluminum's technical advantages, Banco could compete on total cost of ownership. Second, gradually build aluminum capabilities, but not through expensive greenfield plants—through strategic partnerships.

The 1990s also marked Banco's first serious international forays. The company was recognized as Star Export House by Ministry of Commerce and Trade, Government of India. The initial export strategy was counterintuitive—instead of targeting developing markets with similar conditions to India, Banco went after Europe. The reasoning was brilliant: European aftermarket distributors needed low-cost alternatives for older vehicles whose owners wouldn't pay OEM prices for replacement parts. A 10-year-old Mercedes truck in Poland didn't need a €500 Behr radiator; it needed a €150 solution that worked.

The ISO 9002 certification in 1995 was a watershed moment. For an Indian component manufacturer, this wasn't just a quality certificate—it was a passport to global supply chains. The certification process itself transformed Banco's operations. Every process had to be documented, every deviation analyzed, every customer complaint systematically addressed. Workers who had relied on tribal knowledge passed down through apprenticeship suddenly had to follow written procedures.

The integrated plant at Bhaili, spread over 50,000 square meters, produces over 1.5 million cooling system components. This facility, commissioned in the late 1990s, represented Banco's biggest bet yet. The ₹50 crore investment seemed massive for a company with annual revenues of ₹180 crores. But the plant's design revealed sophisticated thinking about manufacturing flexibility. Instead of dedicated lines for specific products, Banco created modular cells that could switch between radiators, oil coolers, and charge air coolers with minimal changeover time.

The Asian Financial Crisis of 1997-98 provided an unexpected opportunity. Korean and Thai component manufacturers, reeling from currency devaluations, were desperately seeking hard currency revenues. Banco formed technical partnerships with three Korean firms, gaining access to aluminum manufacturing technology in exchange for equity stakes and guaranteed purchase agreements. These weren't high-profile deals that made headlines, but they quietly transformed Banco's technical capabilities.

By 2000, Banco had emerged as a paradox—simultaneously a survivor of the License Raj and a beneficiary of liberalization. Revenue had grown to ₹340 crores, exports accounted for 15% of sales, and the company was supplying to 18 different OEMs. The product portfolio had expanded from basic radiators to sophisticated charge air coolers for turbocharged engines, oil coolers for hydraulic systems, and even specialized cooling solutions for gensets and earth-moving equipment.

The dot-com bubble and its burst barely registered in Vadodara. While investors were chasing technology stocks with no revenues, Banco was quietly generating 18% EBITDA margins selling products that most investors couldn't even describe. The stock price languished between ₹15-25 for most of the decade, creating what would later prove to be one of the Indian market's great overlooked compounding stories.

What's fascinating about this period is how Banco navigated the transition from protection to competition without the drama that engulfed many Indian manufacturers. There were no mass layoffs, no financial restructuring, no desperate mergers. Just steady, methodical improvement—a 2% increase in radiator efficiency here, a 5% reduction in manufacturing cost there. It was boring, unglamorous, and exactly what long-term value creation looks like.

IV. The NRF Acquisition: European Expansion (2010)

The winter of 2009 was brutal for the global auto industry. General Motors had filed for bankruptcy, Chrysler was being carved up, and auto parts suppliers were falling like dominoes. In a nondescript conference room in Detroit, lawyers for Proliance International were explaining to a bankruptcy judge why their company, once valued at $800 million, needed Chapter 11 protection. Among Proliance's assets was a curious European subsidiary—Nederlandse Radiateuren Fabriek B.V. (NRF), a Dutch company older than Banco itself, established in 1927.

Eight thousand miles away in Vadodara, Mehul Patel was studying NRF's financials with the intensity of a chess grandmaster analyzing an endgame. Banco announced acquisition of 100% shares of Nederlandse Radiateuren Fabriek B.V. (NRF), for a sum of Euros 17.7mn. NRF has hitherto been owned by a subsidiary of Proliance which was in Chapter 11 proceedings in USA. The price—€17.7 million for a company with €120 million in revenues—seemed almost absurd. But Patel saw what others missed: this wasn't just buying a distressed asset; it was acquiring a century of European market credibility overnight.

Banco had been a supplier to NRF B.V for more than 15 years and was familiar with its market, products and management. Banco would benefit from its familiarity with the European Market as well as NRF's supply relations with European OEMs. This 15-year relationship proved crucial. While other potential bidders conducted hurried due diligence through data rooms, Banco knew NRF's operations intimately—which production lines were efficient, which customers were sticky, which managers were indispensable.

NRF was established in 1927 and was a leading European manufacturer of automotive, industrial, railway and marine heat transfer products. The company's history read like a timeline of European industrialization. It had survived the Great Depression, rebuilt after World War II bombing raids, navigated the oil shocks of the 1970s, and adapted through multiple ownership changes. In 1989, NRF became a subsidiary of the American Modine Manufacturing Company. NRF became Modine's head office for aftermarket products in Europe.

The acquisition structure revealed sophisticated thinking about risk management. Banco didn't just write a check; they negotiated a deal clear of all liens and encumbrances, ensuring no hidden liabilities would surface later. The financing came entirely from internal accruals—no debt, no dilution, just patient capital accumulated over decades being deployed at exactly the right moment.

What made this deal particularly audacious was the reversal of traditional M&A flows. Here was an Indian Tier-2 city manufacturer acquiring a European company with operations across the continent. NRF's manufacturing and distribution companies were located in all the major Western European countries, with three manufacturing units and 11 warehousing and distribution locations across Europe and the USA. This wasn't just buying technology or market access—it was acquiring an entire go-to-market infrastructure that would have taken decades to build organically.

The integration strategy was counterintuitive. Instead of imposing Indian management or drastically cutting costs, Banco retained NRF's leadership team and actually increased investments. Banco has been a supplier to NRF B.V for more than 15 years and is familiar with its market, products and management. Due to the takeover, NRF has been able to strengthen its global position with new factories and warehouses.

The post-acquisition execution vindicated Patel's vision. In 2021 NRF relocated their aluminium production facility from the Netherlands to Poland. At this factory NRF produces a large variety of custom-made oil, water and air coolers for the Automotive Aftermarket, as well as for OE customers. NRF produces cooling parts and solutions for the railway industry, agricultural applications, off highway machinery and gensets.

The expansion continued aggressively. In 2022, NRF opened a brand new 30,000 m2 warehouse in Gdańsk, Poland. The warehouse serves as NRF's new European distribution center. It is the largest European warehouse with a stock of engine cooling and climate control parts. This wasn't just maintaining NRF's position—it was transforming it into a pan-European powerhouse.

The technology investments were equally impressive. NRF has built a new sensor laboratory in Granada, Spain. The laboratory includes an ISO-certified clean room where NRF can test, validate and develop all kinds of products. With the main focus being on sensors, it will help NRF to expand its sensor range even further.

By 2023, what started as a distressed acquisition had become Banco's crown jewel. NRF wasn't just contributing revenues; it was opening doors to European OEMs who would never have considered an Indian supplier. The aftermarket distribution network gave Banco pricing power and market intelligence that pure OEM suppliers could only dream of.

The financial impact was transformative. While exact contribution numbers aren't disclosed, NRF's European operations now account for a significant portion of Banco's consolidated revenues. More importantly, the acquisition proved that Banco could execute complex cross-border M&A, integrate Western operations, and create value through patient capital and operational excellence rather than financial engineering.

V. Product Innovation & Technology Leadership (2000s-Present)

The conference room at Banco's Vadodara R&D center doesn't look like much—functional furniture, whiteboards covered in thermal equations, and a collection of failed prototypes that engineers keep as reminders. But in 2015, this room witnessed a heated debate that would define Banco's next decade. The question on the table: Should an engine cooling company bet its future on electric vehicles that, by definition, don't have engines?

The traditionalists argued that EVs were overhyped, pointing to the spectacular failure of Better Place and the struggling sales of the Nissan Leaf. The progressives countered with a simple observation: batteries generate heat, lots of it, and managing that heat would determine whether EVs succeeded or failed. The debate ended when someone pulled up Tesla's parts supplier list—thermal management systems accounted for 8% of the Model S's bill of materials, higher than traditional vehicles.

The company has regularly invested in establishing world-class research and development capabilities. The company's R&D Centre at Vadodara is recognized by the Department of Science, Government of India. This recognition wasn't just ceremonial—it came with tax benefits, easier access to government research grants, and most importantly, credibility with global OEMs who were increasingly mandating local R&D capabilities from their suppliers.

The evolution of Banco's product portfolio tells the story of systematic capability building. The product range for engine cooling systems includes Radiators, Charge air coolers, Oil coolers – Transmission & hydraulic, Fuel coolers, Battery coolers, Inverter coolers, in Aluminium and copper/brass configurations. Each product category represented a technical leap. Charge air coolers for turbocharged engines required understanding of two-phase heat transfer. Oil coolers for hydraulic systems meant mastering high-pressure applications. Battery coolers for EVs demanded expertise in liquid cooling circuits with precise temperature control.

The shift to aluminum manufacturing deserves special attention. While the NRF acquisition brought aluminum expertise, Banco needed to indigenize this for cost competitiveness. The challenge wasn't just technical—aluminum brazing requires controlled atmosphere furnaces operating at 600°C with precise flux application, compared to copper's more forgiving 450°C process. A single parameter deviation could result in entire batches failing leak tests.

Banco's solution was characteristically pragmatic. Instead of importing expensive controlled atmosphere brazing (CAB) furnaces, they partnered with IIT Bombay to develop a hybrid process using locally available nitrogen generators and modified flux compositions. The resulting process was 30% cheaper than conventional CAB while maintaining international quality standards. This innovation earned them orders from Maruti for the Baleno's all-aluminum cooling module—a contract worth ₹200 crores annually.

The sealing systems evolution was equally impressive. Product range includes Engine cylinder head and peripheral gaskets, Heat shields and Industrial gasket with a wide material range and sizes for demanding applications of sealing. Modern engines operate at higher compression ratios and temperatures, making traditional asbestos gaskets obsolete. Banco developed multi-layer steel (MLS) gaskets with polymer coatings that could handle 200 bar cylinder pressures—technology that even German suppliers were still perfecting.

The customer list reads like a who's who of global manufacturing. Leading OEM customers include Tata Motors, Ashok Leyland, Cummins, Maruti, Mahindra & Mahindra, Hero Honda, TVS, Harley Davidson, Indian Railways, Caterpillar, and JCB. Each relationship required different capabilities. Harley Davidson demanded aesthetic perfection—even hidden components had to meet appearance standards. Cummins required statistical process control with Cpk values above 1.67. Indian Railways needed products that could survive 20 years of neglect.

The Caterpillar relationship illustrates Banco's technical evolution. In 2018, Caterpillar's Hosur plant faced a crisis—their earthmovers operating in Indian mines were experiencing radiator failures every 500 hours instead of the designed 2,000 hours. The problem was India-specific: a combination of high ambient temperatures, dusty conditions, and poor coolant quality created a perfect storm of corrosion and clogging.

Banco's solution was elegantly simple yet technically sophisticated. They developed a dual-metal radiator with copper tubes (for corrosion resistance) and aluminum fins (for heat dissipation), with a proprietary coating that prevented galvanic corrosion. The design included larger tube pitches to reduce clogging and sacrificial zinc anodes to protect against electrochemical attack. The result: radiator life extended to 2,500 hours, exceeding original specifications.

The EV transition has accelerated Banco's innovation trajectory. Battery thermal management isn't just about cooling—it's about maintaining batteries within a 2°C temperature differential across all cells to prevent degradation. Banco developed liquid cold plates with micro-channel designs that achieve this precision while adding minimal weight. Their inverter cooling solutions for electric buses can dissipate 50kW of heat—equivalent to cooling a small apartment—while operating in 45°C ambient conditions.

Spread over an area of 50,000 square meters, the integrated plant at Bhaili produces over 1.5 million cooling system components. The plant set up at special economic zone – Waghodia manufactures a wide range of cooling system products for global markets. These facilities aren't just production centers—they're innovation hubs where manufacturing engineers work alongside design teams to ensure manufacturability at scale.

The R&D investment numbers tell their own story. While specific figures aren't disclosed, industry sources suggest Banco spends 2-3% of revenues on R&D—modest by software standards but significant for an auto component manufacturer. More importantly, the R&D isn't just about new products—it's about process innovations that reduce costs by 2-3% annually while improving quality metrics.

What's remarkable is how Banco has managed to stay relevant across technology transitions. From carburetors to fuel injection, naturally aspirated to turbocharged, internal combustion to hybrid to full electric—each shift could have obsoleted their products. Instead, each transition created new thermal management challenges that Banco converted into opportunities. The company that started by cooling truck engines in 1961 is now cooling battery packs for electric buses—same physics, different application, continuous evolution.

VI. Business Model & Global Operations

Inside Banco's Vadodara headquarters, there's a wall-mounted display showing real-time inventory levels across 11 global warehouses. Green dots in Gdańsk, Valencia, and Mumbai pulse steadily. A yellow alert flashes in the Netherlands facility—stock of a specific Volkswagen radiator model running low. Within minutes, an production order flows to the Bhaili plant. This operational symphony, running 24/7 across time zones, represents a business model that took four decades to perfect.

The fundamental tension in auto components is between OEM and aftermarket sales. OEM business offers volume and prestige but comes with crushing price pressures, annual cost reduction targets, and the constant threat of model changes obsoleting your products. Aftermarket provides higher margins and stable demand but requires massive working capital for inventory and distribution infrastructure. Banco's genius lies in playing both games simultaneously while using each to strengthen the other.

It also has a strong presence in the European markets through its wholly subsidiary NRF with three manufacturing units and 11 warehousing and distribution locations across Europe and the USA. This infrastructure isn't just about storage—it's about market intelligence. Every aftermarket sale provides data on failure patterns, helping Banco improve OEM designs. Every OEM relationship provides credibility that aftermarket distributors value.

The OEM business operates on a philosophy of "designed-in stickiness." When Banco wins a platform—say, the cooling module for a new Tata truck—they're essentially locked in for that model's 7-10 year lifecycle. The switching costs for OEMs are prohibitive: new supplier validation, tooling changes, warranty risks. This creates predictable revenue streams but requires continuous investment in new platform wins to offset models reaching end-of-life.

The customer concentration metrics reveal a deliberately diversified strategy. No single customer accounts for more than 15% of revenues. This wasn't accidental—Banco consciously walked away from opportunities that would create over-dependence. When Maruti offered to double orders if Banco became an exclusive supplier, they politely declined, preferring portfolio stability over volume growth.

The aftermarket model is where Banco's patient capital approach shines. Banco products in the aftermarket are represented by brands "BANCO" and "NRF" popular in their distribution chain with a wide range, prudent quality and efficient service. National and Global footprint supported by stable distributors, dealers, and strategic warehouses at key locations ensuring availability. Building this network required decades of relationship cultivation. A distributor in Lagos needs different credit terms than one in London. A dealer in Dhaka values technical support; one in Dubai prioritizes delivery speed.

The robust distribution network, with more than 150 dealers across India, operates on a hub-and-spoke model. Regional warehouses in Chennai, Delhi, and Mumbai hold fast-moving SKUs. Dealers maintain 30-day inventory based on predictive algorithms that account for seasonal patterns (AC components spike in summer), regulatory changes (BS-VI implementation driving replacement demand), and local factors (mining regions need more heavy-duty cooling systems).

The manufacturing footprint reflects operational sophistication. Three distinct strategies for three different markets: India facilities focus on volume and cost efficiency, targeting domestic OEMs and price-sensitive aftermarket segments. The European operations through NRF emphasize flexibility and quick changeovers, serving the fragmented European aftermarket where a warehouse might need 50 units each of 200 different SKUs. The SEZ facility in Waghodia targets export markets, benefiting from tax advantages while maintaining international quality certifications.

Quality certifications tell their own story of operational evolution. QS 9000, ISO 9001, ISO 14001, IATF 16949—each certificate represents not just compliance but transformation. The IATF 16949 certification, mandatory for global OEMs, required implementing Advanced Product Quality Planning (APQP), Production Part Approval Process (PPAP), and Failure Mode Effects Analysis (FMEA). These aren't just acronyms—they're disciplines that reduce defect rates from percentages to parts per million.

The working capital management deserves special attention. Auto components is a working capital-intensive business—you need to hold raw material inventory, work-in-progress, finished goods, plus extend credit to customers while managing supplier payments. Banco's working capital cycle of 90-100 days is industry-leading, achieved through sophisticated inventory management, favorable supplier terms leveraging long relationships, and disciplined collection processes.

The capital allocation framework reveals financial discipline. Despite generating robust cash flows (₹400+ crores annually), Banco hasn't pursued aggressive expansion or unrelated diversification. Capital goes to three priorities: capacity expansion in existing products (₹50-80 crores annually), technology upgrades and R&D (₹30-50 crores), and strategic inventory building for aftermarket expansion (₹40-60 crores). The remaining cash strengthens the balance sheet, providing flexibility for opportunistic moves like the NRF acquisition.

Current financials show ROCE of 33.4%, ROE of 33.3%, and Dividend Yield of 2.03%. These metrics reflect a business generating exceptional returns on capital employed—rare in the capital-intensive manufacturing sector. The high ROCE isn't from financial leverage (debt-to-equity ratio under 0.3) but from operational efficiency: asset turns of 2.5x and EBITDA margins consistently above 15%.

The currency hedging strategy merits mention. With significant exports and imported raw materials, Banco faces constant foreign exchange risk. Rather than complex derivatives, they use natural hedging—matching export revenues with import costs in the same currency. The residual exposure is hedged through simple forward contracts, avoiding the speculation that has burned many Indian exporters.

What's particularly impressive is how Banco has scaled globally while maintaining the operational discipline of a family-run business. Decision-making remains centralized for strategic matters but operational autonomy is given to regional heads. The NRF management team in Europe operates independently day-to-day but aligns on annual targets and capital allocation. This balance between control and empowerment has allowed Banco to be simultaneously local and global.

The business model's resilience was tested during COVID-19. When OEM plants shut down, aftermarket demand spiked as people repaired vehicles rather than buying new ones. When semiconductor shortages hit OEMs in 2021-22, Banco's aftermarket business compensated for lower OEM volumes. This counter-cyclical balance isn't perfect, but it provides stability that pure-play OEM suppliers lack.

VII. Competition & Market Dynamics

The annual ACMA conference in Delhi feels like a gathering of old warriors comparing battle scars. Component manufacturers swap stories about Chinese competitors offering radiators at 60% of Indian prices, global OEMs demanding 5% annual price reductions, and the latest technology disruption threatening to make their products obsolete. In this brutal arena, Banco's survival and growth tell us something profound about competitive dynamics in emerging markets.

The Indian auto components industry reached Rs. 5.18 lakh crore (US$ 62.4 billion) in FY24, with component sales to OEMs growing by 8.9% and aftermarket growing by 10.0% to Rs. 9.38 lakh crore (US$ 11.3 billion). Over FY16 to FY24, the industry registered a CAGR of 8.63%, reaching US$ 74.1 billion in FY24.

The competitive landscape in cooling systems is deceptively complex. At first glance, it seems straightforward—make a box with tubes and fins that dissipates heat. But the reality involves metallurgy, fluid dynamics, manufacturing precision, and increasingly, electronics integration. This complexity creates natural barriers that commodity manufacturers struggle to overcome.

Chinese competition represents the most visible threat. Post-2015, Chinese radiator manufacturers flooded the Indian aftermarket with products priced 40-50% below domestic alternatives. The initial quality was questionable—copper tubes with 30% lower wall thickness, aluminum fins prone to corrosion, brazing that failed under Indian temperature cycles. But here's what keeps component executives awake: Chinese quality is improving faster than prices are rising.

Banco's response to Chinese competition reveals strategic sophistication. Instead of racing to the bottom on price, they segmented the market with surgical precision. For price-sensitive segments, they created a "value" brand manufactured in a dedicated low-cost facility, accepting lower margins to maintain market presence. For quality-conscious customers, they emphasized total cost of ownership—a Banco radiator might cost 30% more upfront but last twice as long, making it cheaper over the vehicle's lifetime.

The global supply chain shifts post-COVID created unexpected opportunities. By FY28, the Indian auto industry aims to invest $7 billion to boost localisation of advanced components like electric motors and automatic transmissions by reducing imports and leveraging the "China Plus One" trend. Western OEMs, burned by supply chain disruptions, began diversifying away from China. But they weren't looking for the cheapest alternative—they wanted suppliers with proven quality, financial stability, and most importantly, the ability to scale quickly.

Banco's dual presence in India and Europe through NRF proved invaluable here. When a German truck manufacturer wanted to diversify radiator sourcing away from China, Banco could offer Indian manufacturing costs with European quality standards and local technical support. The same product could be manufactured in Vadodara and finished in Poland, combining cost efficiency with "Made in Europe" credentials.

The technology disruption from EVs initially seemed existential. Internal combustion engines generate waste heat that needs dissipation—the core of Banco's business. Electric motors are 95% efficient versus 40% for ICE, generating far less heat. The naive analysis suggested cooling system demand would crater with EV adoption.

But the reality proved more nuanced. The expansion of electric vehicles (EVs) stands as a prominent driver, with the government promoting EV adoption through various incentives and infrastructure. EV batteries need precise thermal management—too hot and they degrade, too cold and range plummets. The cooling systems for EVs are actually more complex than traditional radiators, involving liquid cooling circuits, heat pumps, and sophisticated control systems.

The competitive dynamics in EV cooling favor established players over new entrants. OEMs won't trust battery cooling—where failure means fire risk—to unproven suppliers. Banco's decades of thermal management expertise and existing OEM relationships provide credibility that new entrants can't match. The capital requirements for EV cooling system development (₹50+ crores for a single platform) also create barriers for smaller players.

India has a very strong position in the international market. It is the largest manufacturer of tractors, the second-largest manufacturer of buses and the third largest of heavy trucks in the world. This domestic market strength provides scale advantages that pure export-focused competitors lack. Banco can amortize development costs across large domestic volumes while using export markets for incremental margin enhancement.

The aftermarket competition deserves special attention. Here, Banco faces not just manufacturers but also reconditioners who refurbish used radiators. In markets like Nigeria or Bangladesh, a reconditioned radiator costs 40% of a new one and satisfies price-sensitive buyers. Banco's response was clever—they established authorized reconditioning centers that use genuine Banco parts, capturing value from the secondary market while protecting brand quality.

The competitive moat in cooling systems comes from an unexpected source: application engineering. Every vehicle platform needs customized cooling solutions based on engine specifications, operating conditions, and packaging constraints. This isn't something you can copy from a catalog or reverse engineer easily. Banco's library of validated designs across hundreds of applications, built over six decades, represents institutional knowledge that competitors can't quickly replicate.

India automotive component market is projected to witness a CAGR of 6.58% during the forecast period FY2025-FY2032, growing from USD 62.53 billion in FY2024 to USD 102.88 billion in FY2032. Within this growing market, thermal management systems are expected to grow faster than the overall industry, driven by turbocharging, emission norms requiring EGR coolers, and EV adoption requiring battery thermal management.

The industry structure is consolidating, albeit slowly. Smaller radiator manufacturers without scale or technology are either exiting or becoming toll manufacturers for larger players. But new competition is emerging from unexpected quarters—electronics companies entering battery thermal management, chemical companies developing new coolant formulations, and software firms offering thermal optimization algorithms.

What's particularly interesting about Banco's competitive position is its "Goldilocks" nature—large enough to invest in technology and serve global OEMs, but small enough to remain agile and maintain the 15-20% EBITDA margins that mega-suppliers like Valeo or Denso can't achieve in emerging markets. This sweet spot is surprisingly defensible; growing larger would reduce margins through corporate overhead, while staying smaller would limit technology investments.

VIII. Playbook: Key Business Lessons

In the archives of Indian business schools, the Banco case rarely appears. It lacks the drama of Tata's global acquisitions or the digital disruption narrative of Flipkart. Yet for students of long-term value creation, Banco offers a masterclass in building competitive advantages through patience, focus, and operational excellence. The playbook that emerges from their six-decade journey contains lessons that transcend industries and geographies.

Lesson 1: Trust Compounds Faster Than Capital

The radiator business operates on a simple truth: when a cooling system fails, engines worth lakhs can be destroyed in minutes. This catastrophic failure mode means purchasing decisions prioritize reliability over price. Banco understood this early, choosing to over-engineer products rather than maximize margins. A Banco radiator from the 1970s was built to last 15 years in a market where 10 years was standard.

This over-delivery created a compounding effect. Fleet operators who bought Banco radiators in 1975 were still buying in 2020—not the same people, but the same companies, where purchase specifications literally stated "Banco or equivalent." The lifetime value of these relationships, spanning vehicle generations and technology transitions, far exceeded any short-term margin sacrifice.

Lesson 2: Patient Capital Enables Opportunistic Aggression

The Patel family's approach to capital allocation seems almost archaic in today's growth-at-all-costs environment. Mehul K. Patel has more than 40 years of experience in the automotive industry, and this long-term perspective permeates every strategic decision. The company maintained strong cash reserves even when debt was cheap, avoided unrelated diversification when conglomerates were fashionable, and resisted the temptation to grow through aggressive acquisitions.

This patience created the financial flexibility for the NRF acquisition. When the opportunity arose in 2010, Banco could move quickly with an all-cash offer while competitors struggled to arrange financing during the credit crisis. The lesson isn't about avoiding debt or growth—it's about maintaining strategic flexibility to act decisively when extraordinary opportunities arise.

Lesson 3: Boring Businesses Enable Exciting Returns

Banco operates in what venture capitalists would dismiss as a "zero TAM expansion" market—engines will always need cooling, and cooling physics hasn't changed since the laws of thermodynamics were discovered. Yet this boring stability enabled consistent 30%+ returns on capital employed, far exceeding what most "exciting" businesses achieve.

The boringness is actually a moat. Ambitious executives don't dream of running radiator companies. MBA graduates don't write business plans for gasket manufacturing. This talent flow toward exciting industries creates less competition for leadership and allows patient operators to build dominant positions in boring but essential products.

Lesson 4: Geographic Arbitrage Works Both Ways

The conventional narrative of globalization involves Western companies leveraging Asian manufacturing costs. Banco flipped this through the NRF acquisition—an Indian company leveraging European market access and credibility. This reverse arbitrage worked because Banco understood something subtle: in B2B markets, customer relationships and local presence matter more than manufacturing costs.

NRF's European customers didn't care that ownership shifted to India; they cared that the same sales engineer answered their calls, the same warehouse delivered their orders, and the same quality standards were maintained. By preserving local operations while leveraging Indian manufacturing for cost advantage, Banco captured value that pure exporters or pure acquirers would have missed.

Lesson 5: Technology Transitions Reward Prepared Incumbents

Every major technology shift in automotive—fuel injection, turbocharging, emission norms, electrification—was supposed to disrupt traditional suppliers. Yet Banco emerged stronger from each transition. The pattern is consistent: new technology creates new thermal management challenges, requiring expertise that takes years to develop. By the time new entrants build capabilities, incumbents have already captured the market.

The key is preparation without overcommitment. Banco invested in EV cooling research years before EV sales materialized but didn't bet the company on any single technology. This portfolio approach—maintaining existing products while developing future capabilities—requires discipline to avoid both complacency and panic.

Lesson 6: Operational Excellence Beats Strategic Brilliance

Banco's strategy could fit on a napkin: make good cooling systems, serve customers reliably, expand carefully. There's no complex financial engineering, no revolutionary business model innovation, no platform network effects. The differentiation comes from executing simple things exceptionally well, consistently, for decades.

This operational focus cascades through the organization. Factory workers take pride in leak-free brazing. Sales engineers become trusted advisors to customers. R&D teams obsess over 2% efficiency improvements. These micro-optimizations compound into macro-advantages that strategic brilliance alone cannot overcome.

Lesson 7: Family Ownership Enables Long-Term Thinking

Promoter Holding: 67.9% This concentrated ownership structure, often criticized by governance advocates, enabled Banco to optimize for long-term value over quarterly earnings. Family ownership meant resisting pressure to maximize short-term margins, avoiding expensive acquisitions to show growth, and maintaining conservative accounting even when aggressive policies were industry norm.

The alignment between ownership and management eliminated agency costs that plague professionally managed firms. When Mehul Patel decided to acquire NRF, he wasn't thinking about his stock options or next quarter's earnings—he was thinking about building a business his grandchildren would run.

Lesson 8: B2B Brands Matter More Than Most Realize

In consumer businesses, brand value is obvious and measured obsessively. In B2B manufacturing, brands are often dismissed as irrelevant—buyers are assumed to make rational decisions based on specifications and price. Banco's experience suggests otherwise. The "Banco" name on a radiator commands a 15-20% price premium in the aftermarket, not because of advertising but because of accumulated trust.

This brand value was built through consistency rather than creativity. Every Banco product carries the same promise: it will work as specified, last as long as claimed, and be supported when needed. This boring reliability, maintained over decades, created brand value that shows up in pricing power and customer retention.

Lesson 9: Suppliers Can Capture More Value Than OEMs

The automotive value chain conventional wisdom suggests OEMs capture most value while suppliers fight for scraps. Yet Banco generates higher returns on capital than many OEMs. The key insight: specialization enables efficiency that diversified OEMs cannot match. While Tata Motors manages everything from design to dealer financing, Banco focuses solely on thermal management, achieving expertise depth that commands premium pricing.

Lesson 10: Cycles Create Opportunities for Patient Capital

The auto industry's cyclicality is treated as a bug by most investors but as a feature by Banco. Downturns create opportunities to hire talent from struggling competitors, acquire assets at distressed prices, and gain market share from financially weaker players. The key is maintaining financial strength to be aggressive when others are defensive.

The 2008-2010 period exemplified this. While competitors cut R&D and froze hiring, Banco acquired NRF and expanded capacity. When recovery came, they had enhanced capabilities while competitors struggled to rebuild. This counter-cyclical investment requires conviction that cycles are temporary but competitive advantages gained during downturns are permanent.

IX. Bear vs Bull Case & Valuation

The investment community's view on Banco splits into two camps with radically different perspectives on the same facts. At a recent investor conference in Mumbai, you could observe this schism in real-time: growth investors excited about EV opportunities sitting next to value investors worried about valuation multiples, while skeptics questioned whether any auto component supplier deserves premium valuations. The debate illuminates broader questions about how markets value steady compounders versus story stocks.

The Bull Case: Thermal Management's Golden Age

The optimists see Banco at an inflection point. Electric vehicles don't eliminate thermal management—they transform it from a commodity to a critical technology. Battery pack cooling systems can cost ₹50,000-1,00,000 per vehicle versus ₹5,000-10,000 for traditional radiators. Even at lower volumes, the revenue opportunity multiplies. More importantly, the technical complexity creates pricing power that commodity radiators never commanded.

The China Plus One narrative adds another layer to the bull case. By FY28, the Indian auto industry aims to invest $7 billion to boost localisation of advanced components like electric motors and automatic transmissions by reducing imports and leveraging the "China Plus One" trend. Global OEMs desperately seeking supply chain diversification view India as the only alternative with sufficient scale, engineering talent, and cost competitiveness. Banco, with proven execution capability and European presence through NRF, stands to capture disproportionate share of this shift.

Bulls point to the revenue growth trajectory—from ₹2,000 crores in FY20 to ₹3,379 crores in FY24, despite COVID disruptions and semiconductor shortages affecting OEM production. The aftermarket business provides recession resilience (older vehicles need more cooling system replacements), while the OEM business offers operating leverage as volumes recover.

The return metrics strengthen the bull case. ROCE of 33.4% and ROE of 33.3% place Banco among the highest-return manufacturing companies in India. These aren't financial engineering metrics—debt is minimal, working capital is efficiently managed, and the returns come from operational excellence. If Banco can maintain these returns while growing at even 12-15% annually, the compounding mathematics become compelling.

The management quality factor resonates with quality-focused investors. Three generations of the Patel family actively involved in operations, conservative accounting policies, and a track record of under-promising and over-delivering create trust. The successful NRF integration demonstrates M&A capability, suggesting future value-accretive acquisitions are possible.

The Bear Case: Valuation Disconnect and Structural Headwinds

The skeptics see a different picture. India Auto Component Market size is estimated to grow by USD 259.03 billion from 2025 to 2029 at a CAGR of 37%—this projection seems wildly optimistic given current industry dynamics. At ₹639 per share, Banco trades at 45x trailing earnings, a multiple that assumes perfection in execution and favorable industry dynamics. For context, global thermal management leaders like Valeo trade at 8-10x earnings.

The intrinsic value calculation provides sobering perspective. Under base case assumptions—12% revenue growth, 15% EBITDA margins, 15x terminal multiple—the intrinsic value comes to ₹311 per share. The current market price of ₹639 implies either 20%+ growth rates or significant margin expansion, neither of which seems probable given competitive dynamics.

Bears worry about the cyclical nature of auto demand. India's passenger vehicle sales have been volatile, affected by everything from monsoons to demonetization to emission norm changes. Commercial vehicle sales, a key segment for Banco, are even more cyclical. When the next downturn hits—and it will—Banco's operating leverage works in reverse.

The technology transition risk looms large. Yes, EVs need thermal management, but the suppliers might change. Battery manufacturers like CATL and LG Chem are integrating thermal management into battery packs. Power electronics companies like Infineon are developing integrated cooling solutions for inverters. Banco's mechanical engineering expertise might become less relevant in an electronics-dominated world.

Chinese competition intensifies rather than abates. Despite quality issues, Chinese manufacturers are moving up the value chain rapidly. They're acquiring European technology companies, hiring Indian engineers, and building global distribution networks. The cost advantage that Indian manufacturers enjoyed is eroding as Chinese automation reduces labor content.

The customer concentration risk deserves attention. While no single customer exceeds 15% of revenues, the top 10 customers likely account for 60-70% of sales. If even one major OEM shifts sourcing or faces production cuts, the impact on Banco would be material. The Tata Motors relationship, while valuable, creates implicit concentration given Tata's market position in commercial vehicles.

The Valuation Reality Check

Let's ground this in numbers. At current price of ₹639 and market cap of ₹7,793 crores: - P/E ratio: 45x (versus auto component industry average of 25x) - EV/EBITDA: 28x (versus industry average of 15x) - Price/Book: 12x (versus industry average of 4x) - Dividend Yield: 2.03% (adequate but not compelling)

The valuation implies the market sees something beyond current financials—either dramatic growth acceleration, significant margin expansion, or reduced risk profile. Bulls argue all three are possible with EV transition, export growth, and operational improvements. Bears see hope triumphing over analysis.

Scenario Analysis

Best Case (20% probability): EV adoption accelerates, Banco wins major European OEM contracts, margins expand to 18% EBITDA. Stock reaches ₹1,000 over three years—56% upside.

Base Case (60% probability): Steady 12-15% growth, margins stable at 15%, modest multiple compression as growth moderates. Stock trades between ₹500-700 over three years—limited upside, potential 20% downside.

Worst Case (20% probability): Auto cycle turns down, Chinese competition intensifies, EV transition slower than expected. Stock corrects to ₹350-400—40-45% downside.

The risk-reward appears unfavorable at current valuations. The stock needs everything to go right to justify ₹639, while numerous factors could drive disappointment. This doesn't make Banco a bad business—quite the opposite. It's an excellent business at an excellent price that became a good business at an excessive price.

The Meta-Lesson on Valuation

Banco illustrates a profound market paradox: the best businesses often become the worst stocks precisely because their quality gets recognized and overpriced. The company that traded at 8x earnings in 2010 when executing the transformative NRF acquisition now trades at 45x earnings while facing structural uncertainties.

For long-term investors, the question isn't whether Banco is a good business—it demonstrably is. The question is whether it's a good investment at current prices. The gap between intrinsic value (₹311) and market price (₹639) suggests patience might be the best strategy. Great businesses eventually offer great entry points, usually when short-term concerns overshadow long-term strengths.

X. Future Outlook & Strategic Priorities

Standing at the entrance of Banco's new R&D facility in Vadodara, you can glimpse the future taking shape. Engineers huddle around a test bench where a liquid-cooled battery pack undergoes thermal cycling—heated to 60°C, cooled to -20°C, repeated 1,000 times. In another corner, a team analyzes data from sensors embedded in radiators operating in European trucks, using machine learning to predict failure patterns. This isn't your grandfather's radiator company anymore.

The next decade's strategic roadmap crystallizes around four pillars: EV thermal management leadership, European market penetration, technology partnerships, and operational excellence. Each pillar supports the others, creating what management calls a "reinforcing spiral of capabilities."

The EV Opportunity: Beyond Cooling

The electric vehicle transition represents both Banco's biggest opportunity and greatest challenge. The opportunity is tangible—battery thermal management systems generate 3-4x the revenue per vehicle compared to traditional radiators. A commercial EV bus requires cooling systems worth ₹2-3 lakhs versus ₹30-40,000 for a diesel equivalent. Even with lower EV volumes initially, the revenue mathematics are compelling.

But Banco's EV strategy extends beyond simple cooling. They're developing integrated thermal management systems that optimize energy consumption across heating, cooling, and cabin climate control. In cold climates, waste heat from the motor and electronics can warm the battery. In hot conditions, the same system provides cooling. This holistic approach can extend EV range by 10-15%—a critical selling point for OEMs.

The technology roadmap includes solid-state battery cooling (requiring different thermal interfaces), hydrogen fuel cell thermal management (operating at higher temperatures), and even thermal systems for autonomous vehicles (where computing hardware generates significant heat). Each technology stream requires years of development but offers decades of revenue potential.

European Expansion: From Foothold to Fortress

NRF provides the platform, but the vision extends far beyond maintaining status quo. Due to the takeover, NRF has been able to strengthen its global position with new factories and warehouses. The strategy involves transforming NRF from a regional aftermarket player to a pan-European thermal management leader serving both OEM and aftermarket segments.

The expansion blueprint is methodical. First, strengthen the aftermarket position through strategic warehouse locations—the new 30,000 m² Gdańsk facility serves Eastern Europe, while Valencia covers Iberian markets. Second, leverage aftermarket relationships to approach OEMs. A purchasing manager who trusts NRF for replacement parts becomes receptive to OEM supply discussions.

The European commercial vehicle market offers particular promise. Stricter emission norms require sophisticated cooling for exhaust treatment systems. European truck manufacturers, facing pressure to reduce costs while maintaining quality, increasingly consider Indian suppliers with European operations. Banco/NRF's unique positioning—Indian costs with European presence—resonates strongly.

Technology Partnerships: Building the Ecosystem

Banco recognizes that future thermal management requires capabilities beyond traditional mechanical engineering. Electronics, software, materials science—each discipline becomes critical. Rather than building all capabilities internally, Banco pursues targeted partnerships.

The partnership strategy follows clear principles. For core thermal technologies, develop internally or acquire. For complementary technologies like sensors or control software, partner with specialists. For emerging technologies like graphene-based thermal interfaces, invest in startups through a corporate venture arm (though this remains under consideration).

Current partnership discussions (based on industry sources, as company doesn't disclose details) reportedly include: - A German electronics firm for integrated motor-inverter cooling - An Israeli startup developing AI-based thermal optimization - An Indian Institute of Technology for next-generation heat exchanger designs - A Japanese materials company for advanced coolant formulations

Capital Allocation: Disciplined Growth

The capital allocation framework for the next five years reveals strategic priorities:

-

Organic Expansion (₹300-400 crores): Primarily for EV-related manufacturing capabilities and debottlenecking existing facilities. The focus isn't adding capacity indiscriminately but creating flexible manufacturing cells that can switch between products based on demand.

-

R&D Investment (₹150-200 crores): Targeting 3% of revenues, up from current 2-2.5%. The increase funds EV cooling development, advanced materials research, and critically, software capabilities for thermal system control.

-

Strategic M&A (₹500-1,000 crores potential): Management hints at evaluating acquisitions, particularly in Europe and North America. The criteria are strict: technological complementarity, immediate revenue synergies, and cultural fit. They'd rather wait years for the right opportunity than rush into value-destructive deals.

-

Working Capital (₹200-300 crores): Supporting aftermarket expansion requires inventory investment. But this is "productive" working capital that generates returns through better service levels and market share gains.

-

Shareholder Returns: Maintaining 25-30% dividend payout ratio, with potential for special dividends if cash accumulates beyond investment needs. No share buybacks planned given promoter's 67.9% holding.

Operational Excellence: The Continuous Journey

While strategic initiatives capture attention, operational improvements drive sustained value creation. The operational roadmap includes:

-

Manufacturing 4.0: Implementing IoT sensors, predictive maintenance, and real-time quality control. Target: reduce defects from current 200 PPM to below 50 PPM.

-

Supply Chain Optimization: Developing local supplier ecosystems in Europe to reduce logistics costs and currency exposure. Target: 70% local sourcing for European operations by 2027.

-

Sustainability Integration: Aluminum recycling, water conservation, and renewable energy adoption. Not just for ESG optics—European customers increasingly mandate sustainability metrics from suppliers.

-

Talent Development: Creating a thermal management "university" to train engineers. The talent shortage in thermal management creates recruiting challenges but also opportunity to build competitive advantage through superior human capital.

The 2030 Vision: Measurable Milestones

Management's 2030 vision, while not officially communicated in detail, can be inferred from various statements and actions:

- Revenue of ₹8,000-10,000 crores (from current ₹3,379 crores)

- EBITDA margins sustained at 15-17% despite product mix changes

- Export contribution increasing to 40% (from current 25-30%)

- EV-related products contributing 25-30% of revenues

- European operations contributing 35-40% of consolidated revenues

- ROCE maintained above 25% despite growth investments

These targets appear ambitious but achievable given industry growth projections and Banco's execution track record. The Indian automobile industry is expected to achieve a turnover of US$ 300 billion by 2026 by expanding at a CAGR of 15% from its current revenue of US$ 74 billion. If Banco can maintain or slightly exceed industry growth rates while preserving margins, the 2030 vision becomes realistic.

The Risks to Navigate

The strategic outlook must acknowledge significant risks:

-

Technology Disruption: Solid-state batteries might require completely different cooling approaches. Banco must invest in multiple technologies without knowing which will dominate.

-

Geopolitical Tensions: India-China relations, European protectionism, and supply chain nationalism could disrupt growth plans.

-

Capital Allocation Mistakes: One bad acquisition or overinvestment in the wrong technology could destroy years of value creation.

-

Succession Planning: While three generations of the Patel family are involved, ensuring smooth leadership transition remains critical.

-

Market Expectations: Current valuations embed aggressive growth assumptions. Any disappointment could trigger significant multiple compression.

XI. Recent News

The recent performance trajectory tells a story of momentum meeting market recognition. Net profit of Banco Products (India) rose 125.21% to Rs 153.50 crore in the quarter ended March 2025 as against Rs 68.16 crore during the previous quarter ended March 2024. For the full year, net profit rose 44.36% to Rs 391.80 crore in the year ended March 2025 as against Rs 271.40 crore during the previous year ended March 2024.

Sales rose 21.05% to Rs 868.40 crore in the quarter ended March 2025 as against Rs 717.40 crore during the previous quarter ended March 2024. This growth acceleration suggests both volume expansion and pricing power—a rare combination in the competitive auto components sector.

The market's response has been emphatic. Banco Products (India) Ltd share price moved up by 52.39% in the last 1 month on BSE. Last 3 Months: Banco Products (India) Ltd share price moved up by 63.54% on BSE. Last 12 Months: Banco Products (India) Ltd share price moved up by 85.27% on BSE.

Strategic Developments

In February 2025, Banco made a significant strategic move with the acquisition of business undertaking of Padra Coating Works LLP on going concern basis. While details remain limited, this appears to be a capability enhancement in surface treatment technologies—critical for next-generation cooling systems requiring specialized coatings.

The dividend policy signals confidence. The board declared an interim dividend of Rs 11 per equity share for the financial year 2024-25. The board has fixed Friday, 14 February 2025, as a record date for determining the entitlement of members for the purpose of payment of the interim dividend. The payment of dividends will be completed on or after 25 February 2025.

Management Changes

Leadership transitions often signal strategic shifts. The company's board has approved the appointment of Sachin Jayantilal Kotak as the chief financial officer of the company with effect from 17 May 2025. A new CFO typically brings fresh perspectives on capital allocation and financial strategy.

Operational Highlights

The Q4 FY25 results revealed interesting operational dynamics. Cost of materials consumed increased 31.07% YoY to Rs 590.76 crore, while employee benefits expenses rose 23.89% YoY to Rs 96.29 crore in Q4 FY25 over Q4 FY24. The material cost increase outpacing revenue growth suggests either inventory building for future orders or input cost pressures being managed through operational efficiencies elsewhere.

Market Sentiment Indicators

Search interest for Banco Products (India) Ltd Stock has increased by 114% in the last 30 days, reflecting an upward trend in search activity. This surge in retail investor interest often precedes increased volatility as new market participants enter with varying investment horizons and risk tolerances.

XII. Links & Resources

Company Resources: - Official Website: www.bancoindia.com - Investor Relations: www.bancoindia.com/investor-relations/ - NRF Subsidiary: www.nrf.eu

Stock Exchange Filings: - BSE: www.bseindia.com/stock-share-price/banco-products-india-ltd/bancoindia/500039/ - NSE: www.nseindia.com/get-quotes/equity?symbol=BANCOINDIA

Industry Associations: - ACMA (Automotive Component Manufacturers Association): www.acma.in - SIAM (Society of Indian Automobile Manufacturers): www.siam.in

Research & Analysis: - Annual Reports: Available on company website - Quarterly Results: Updated on BSE/NSE websites - Conference Call Transcripts: Through investor relations

Technical Resources: - Thermal Management Systems Overview: SAE International Publications - EV Battery Cooling Technologies: IEEE Xplore Digital Library - Indian Auto Component Industry Reports: IBEF, Invest India

Regulatory Filings: - SEBI (Securities and Exchange Board of India): www.sebi.gov.in - Ministry of Corporate Affairs: www.mca.gov.in

Note: This analysis is based on publicly available information and should not be considered as investment advice. Prospective investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube