Balu Forge Industries: From Single-Cylinder Dreams to Global Crankshaft Empire

I. Introduction & Episode Roadmap

The year is 2017. In a modest conference room in Belgaum, Karnataka, Jaspalsingh Chandock sits across from a delegation of German automotive engineers. They've flown 7,000 kilometers to this industrial town near the Maharashtra border—not to Mumbai, not to Pune, but to Belgaum. They're here because Balu Forge has something even the mighty German auto industry needs: the capability to manufacture crankshafts that meet the world's most stringent emission standards, at scale, with zero-defect quality.

The Germans leave with a contract. Within months, similar delegations arrive from Japan, America, and Brazil. By year's end, Balu Forge is supplying components to 25 OEMs across 80 countries. The company that started with a single forging hammer in 1990 now produces 360,000 crankshafts annually—critical components that convert linear piston motion into rotational force, the beating heart of every internal combustion engine.

Here's the puzzle: How does a company from a tier-2 Indian city become the supplier of choice for Mercedes-Benz trucks, John Deere tractors, and Cummins engines? How do you build a ₹6,428 crore market cap business in one of the most commoditized, capital-intensive, and technically demanding segments of auto manufacturing? The current snapshot tells a remarkable story: Market Cap of ₹6,876 Crore, Revenue of ₹924 crore for FY25, up 65% from ₹560 crore in FY24, with net profit for FY25 at ₹204 crore, up 118% from ₹93 crore in the previous year. The company operates at a nearly debt-free status with debt-to-equity ratio improving to 0.03x from 0.09x a year ago.

This episode unpacks three interlocking mysteries. First, the technical mastery—how a company masters the metallurgical alchemy of converting steel billets into precision crankshafts that must withstand millions of combustion cycles. Second, the strategic chess game—executing a reverse merger that transformed a struggling IT company into a global manufacturing powerhouse. And third, the market positioning—becoming the only Indian company besides Bharat Forge to compete with century-old German and Japanese forging giants.

The themes we'll explore: the democratization of precision engineering, the power of patient capital in manufacturing, the reverse merger as a growth hack, and what happens when emerging market companies stop competing on cost and start competing on capability. This is the story of how Balu Forge went from hammering out simple tractor parts to becoming the beating heart supplier for the world's combustion engines—just as the world began its transition to electric vehicles.

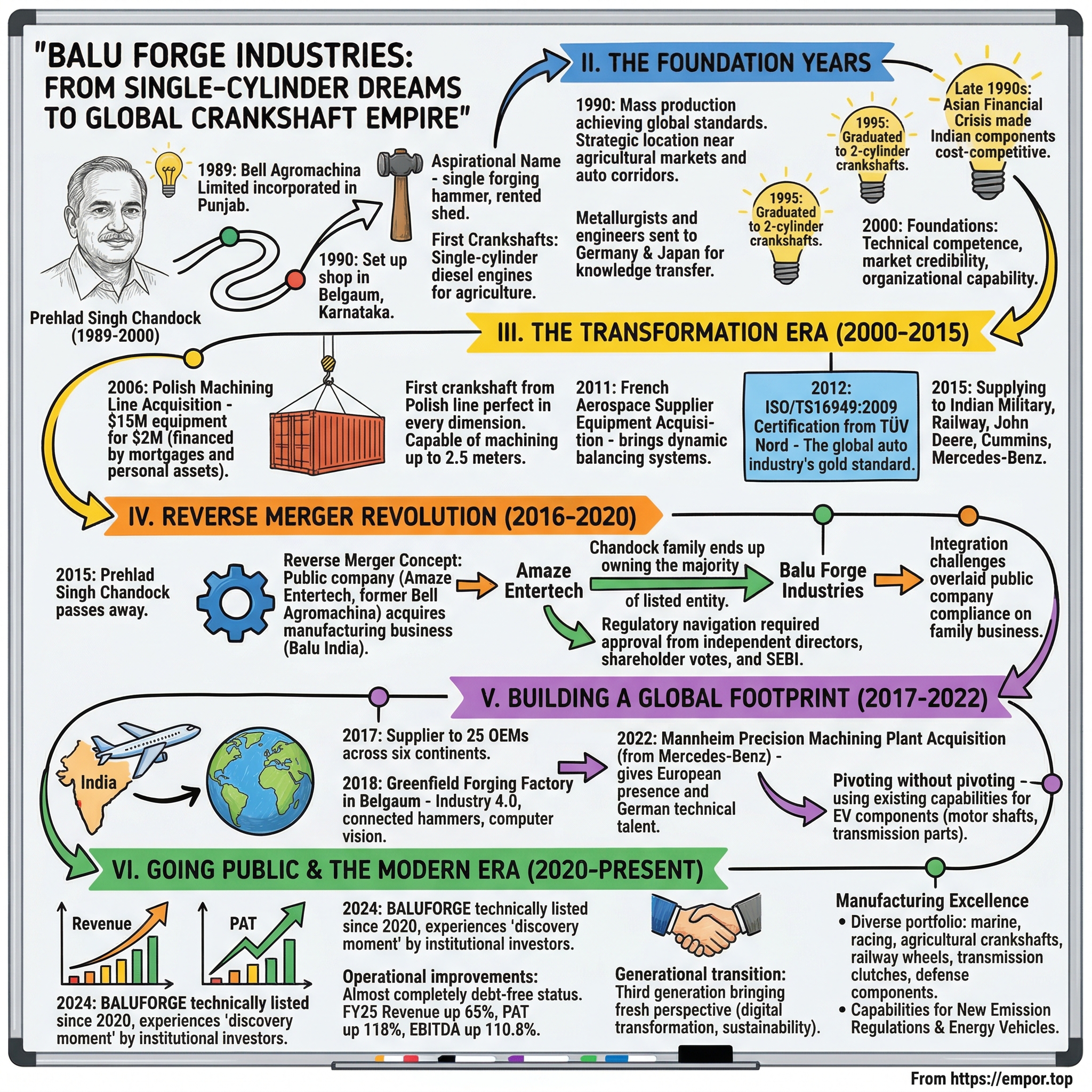

II. The Foundation Years: Prehlad Singh Chandock's Vision (1989–2000)

The story begins not in Belgaum, but in the wheat fields of Punjab in the 1960s. Prehlad Singh Chandock watches tractors transform Indian agriculture during the Green Revolution. He notices something others miss: every time a tractor breaks down, it's usually the crankshaft—the component that converts the explosive force of diesel combustion into the rotational power that drives wheels. Imported replacements take months to arrive and cost more than what most farmers earn in a year.

By 1989, Chandock has saved enough to act on this observation. On March 30, 1989, he incorporates Bell Agromachina Limited. The name is aspirational—'Agromachina' suggesting agricultural machinery, though the company owns nothing but paperwork and ambition. The real work begins a year later when Chandock sets up shop in Belgaum, a dusty industrial town on the Karnataka-Maharashtra border, chosen for its proximity to both agricultural markets and the emerging auto corridor between Pune and Chennai.

The initial setup in 1990 is almost comically modest: a single forging hammer, a handful of workers, and a rented shed that floods during monsoons. Chandock's first crankshafts are for single-cylinder diesel engines—the workhorses of Indian agriculture, powering everything from water pumps to flour mills. The metallurgy is basic, the finishing rough, but they work. More importantly, they're available immediately and cost a fraction of imports.

What makes Chandock's venture remarkable isn't just timing but technical ambition. While competitors are content importing technology, Chandock obsesses over the forging process itself. Forging—the art of shaping metal through controlled deformation—is as old as civilization, but making crankshafts requires a specific mastery. The metal must be heated to exactly 1,200°C, struck with precise force at specific angles, then cooled at controlled rates to achieve the right grain structure. Too hot and the metal becomes brittle; too cool and it won't flow properly. Each crankshaft must withstand millions of combustion cycles, rotating at thousands of RPM, bearing enormous stresses without fatigue or failure.

By 1990, Balu India achieves what no other Indian company has: mass production of crankshafts suitable for tractors, trucks, and passenger cars. The achievement seems modest today, but in the context of India's industrial capabilities in 1990—still emerging from decades of license raj, import substitution, and technological isolation—it's revolutionary. Chandock isn't just making parts; he's proving that Indian manufacturing can meet global engineering standards.

The India of the early 1990s provides both headwinds and tailwinds. The 1991 economic liberalization opens markets but also brings competition. Suddenly, global auto giants are setting up shop in India, demanding components that meet international quality standards. Most Indian suppliers crumble under these requirements. Chandock sees opportunity.

He begins what becomes a Balu Forge tradition: hiring metallurgists and engineers straight from Indian technical institutes, then sending them to learn from German and Japanese forging operations. The knowledge transfer is painstaking. German forging masters are skeptical of Indian capabilities; Japanese engineers guard their processes jealously. But Chandock persists, building relationships one technical discussion at a time.

By 1995, Balu has graduated from single-cylinder to two-cylinder crankshafts—doubling complexity but quadrupling market opportunity. Two-cylinder engines power everything from small tractors to generators, a massive market in power-deficit India. The company's workforce grows to 50, still tiny but now including dedicated quality control and metallurgy teams.

The late 1990s bring the Asian Financial Crisis, which paradoxically helps Balu. As Southeast Asian suppliers struggle with currency collapses, Indian components become cost-competitive globally for the first time. Chandock uses this window to establish relationships with international buyers, initially for simple forgings but laying groundwork for future crankshaft exports.

By 2000, Balu India has achieved three critical foundations. First, technical competence—the ability to consistently produce crankshafts that meet specifications. Second, market credibility—acceptance by domestic OEMs that an Indian company can replace imported components. Third, organizational capability—a team that understands not just how to make crankshafts but why each step matters.

The company's revenue remains modest—under ₹10 crore annually—but Chandock has built something more valuable than sales: a platform for precision engineering in an economy just beginning to embrace manufacturing excellence. As the new millennium dawns, that platform is about to be tested by opportunities and challenges Chandock could never have imagined.

III. The Transformation Era: Building Scale (2000–2015)

The year 2006 marks a turning point that almost destroys Balu before transforming it. Chandock has negotiated to acquire an entire machining line from a bankrupt Polish factory—equipment that cost $15 million new, available for $2 million. The catch: Balu doesn't have $2 million. The company mortgages everything, Chandock pledges personal assets, and they cobble together loans from multiple banks at rates that would make modern CFOs weep.

The Polish equipment arrives in 47 shipping containers during the monsoon of 2006. Half the containers are flooded. The instruction manuals are in Polish. The Polish engineers who were supposed to help with installation have found other jobs. For three months, Balu's engineers sleep in the factory, reverse-engineering the equipment, teaching themselves through trial and catastrophic error. The first crankshaft from the Polish line emerges in December 2006—perfect in every dimension.

This Polish acquisition transforms Balu's capabilities overnight. The company can now machine crankshafts up to 2.5 meters in length—massive components for ship engines, power generators, and heavy trucks. More importantly, the equipment includes computer-controlled machining centers that deliver micron-level precision. Balu jumps from competing with local forgers to competing with global suppliers.

The timing proves perfect. India's automotive industry is exploding—car sales growing 20% annually, commercial vehicles even faster. Every vehicle needs a crankshaft. But the real opportunity comes from an unexpected source: emission regulations. As India adopts Bharat Stage (BS) norms aligned with European standards, engines require more sophisticated crankshafts with tighter tolerances and better surface finishing. Most Indian suppliers can't meet these specifications. Balu can.

In 2011, Chandock repeats the foreign acquisition playbook, this time purchasing equipment from a French aerospace supplier. The French machines bring capabilities even the Polish line lacks: dynamic balancing systems that can detect and correct weight imbalances of less than a gram in a 100-kilogram crankshaft. This precision matters because an unbalanced crankshaft creates vibrations that destroy engines and, at high speeds, can be catastrophic.

The acquisition strategy reveals Chandock's genius for technical arbitrage. European and American forging companies, facing high labor costs and environmental regulations, are consolidating or closing. Their equipment—built to last decades—becomes available at distressed prices. Balu acquires not just machines but embedded knowledge: the peculiar ways German engineers solve thermal expansion problems, the French approach to surface finishing, the Polish methods for handling large forgings.

2012 brings the achievement that changes everything: ISO/TS16949:2009 certification from TÜV Nord. This isn't just another quality certificate—it's the global auto industry's gold standard, a signal that Balu meets the same standards as suppliers to BMW, Toyota, and Ford. The certification process takes 18 months and requires documenting every process, measuring every variance, proving statistical control over thousands of parameters. When the German auditors finally hand over the certificate, Chandock frames it in the boardroom. It's still there today.

The certification opens doors that were previously locked. John Deere, which had been buying Balu crankshafts through intermediaries, signs a direct supply agreement. Cummins, the American engine giant, approves Balu as a global supplier. Mercedes-Benz begins sourcing crankshafts for trucks manufactured in India. Each customer brings not just revenue but knowledge—Deere's agricultural expertise, Cummins's diesel technology, Mercedes's quality obsession.

By 2015, Balu has a surprise customer: the Indian military. The company begins manufacturing components for military vehicles and railway applications—markets where failure isn't just expensive but potentially catastrophic. Military contracts require a different level of documentation, traceability, and testing. Every crankshaft must be traceable to the specific batch of steel, the specific operator, the specific temperature and pressure conditions during forging. This rigor, painful to implement, transforms Balu's quality culture.

The physical expansion matches the capability growth. From the original single shed, Balu now operates across multiple facilities in Belgaum, employing over 500 people. The company installs India's largest crankshaft machining center—a German-made behemoth that can machine six crankshafts simultaneously with tolerances of ±0.01mm. Monthly capacity reaches 30,000 fully finished crankshafts, making Balu one of the largest independent crankshaft manufacturers globally.

2016 brings unexpected recognition: Bharat Forge, India's forging giant and Balu's primary competitor, formally acknowledges Balu as the second source for critical crankshaft supplies. This is like Pepsi acknowledging Coca-Cola—a competitor's recognition of capability. For customers, it means supply security; for Balu, it means arrival at the top tier of global suppliers.

The transformation from 2000 to 2015 isn't just about scale—revenue has grown from ₹10 crore to over ₹200 crore—but about capability. Balu can now make crankshafts that most companies can't: six-meter marine crankshafts for ship engines, micro-finished racing crankshafts for Formula cars, specialized crankshafts for natural gas engines. Each capability required different equipment, different skills, different quality systems.

But perhaps the most important transformation is invisible: the culture of continuous improvement that Chandock has embedded. Every worker understands statistical process control. Quality issues are traced to root causes, not blamed on individuals. Customer complaints—rare but treated as crises—trigger systematic reviews that often lead to process innovations.

As 2015 ends, Balu faces a pleasant problem: demand exceeding capacity despite recent expansions. International customers want more crankshafts than Balu can produce. The company needs capital for expansion, but traditional bank financing is expensive and restrictive. The solution will come from an unexpected direction—a reverse merger that will transform not just Balu's capital structure but its entire strategic trajectory.

IV. The Reverse Merger Revolution (2016–2020)

The story of Balu's reverse merger begins with a funeral. When Prehlad Singh Chandock passes away in 2015, his son Jaspalsingh inherits not just a company but a dilemma. Balu needs ₹500 crore for expansion—new factories, automation, working capital for international orders. The traditional IPO route would take years, dilute the family's control, and subject a manufacturing company to the quarterly earnings pressures that destroy long-term thinking.

Jaspalsingh, trained as an engineer but thinking like a financier, spots an elegant solution hiding in plain sight on the NSE. Bell Agromachina Limited—the very company his father had founded in 1989—had undergone its own transformation. After the agricultural machinery business hadn't scaled, it had pivoted to IT services, renamed itself Amaze Entertech, and somehow gotten listed on the NSE. By 2016, it's a listed shell—minimal operations, clean balance sheet, regulatory compliance intact, trading at a massive discount to book value.

The reverse merger structure Jaspalsingh engineers is brilliantly simple yet complex in execution. Instead of Balu going public, the public company will acquire Balu. But here's the twist: the payment won't be in cash (which Amaze doesn't have) but in shares issued to Balu's owners. Through a series of preferential allotments and business transfer agreements, the Chandock family will end up owning the majority of the listed entity, which will then be renamed Balu Forge Industries.

The first move comes on November 16, 2016, when Bell Agromachina officially becomes Amaze Entertech—clearing the deck of agricultural legacy. The IT operations are gradually wound down, leaving a clean corporate shell. Meanwhile, Jaspalsingh begins the delicate negotiation with minority shareholders, regulators, and stock exchanges. The message is consistent: this isn't financial engineering but industrial transformation.

The key transaction occurs through the Business Succession Agreement dated August 3, 2021 (though negotiations began years earlier). Under this agreement, Jaspalsingh subscribes to 47,840,000 equity shares on September 24, 2020—not for cash but as consideration for transferring Balu India's business to the listed entity. In one stroke, the manufacturing business enters the listed company, and the Chandock family becomes the majority shareholder with 54.8% ownership.

On September 30, 2020, Amaze Entertech officially becomes Balu Forge Industries Limited. The transformation is complete: a struggling IT services company has become a manufacturing powerhouse. The stock market initially doesn't know what to make of it—trading is thin, confusion abounds. But as quarterly results start flowing—real revenues from real customers buying real products—the market begins to understand.

The brilliance of the reverse merger extends beyond speed and cost. By using an already-listed entity, Balu sidesteps the IPO roadshow circus, the investment banker fees, the pressure to price shares attractively for a successful debut. The family maintains control while accessing capital markets. The company can tap institutional investors without the lengthy IPO process.

More subtly, the reverse merger allows Balu to choose its moment. In a traditional IPO, you go public when market conditions permit, often at suboptimal valuations. Through the reverse merger, Balu enters public markets quietly, then reveals its strength through operational performance. It's like entering a poker game with everyone thinking you're a novice, then gradually revealing your hand.

The regulatory navigation deserves its own Harvard case study. Indian securities laws weren't designed for reverse mergers—they're built around traditional IPOs or acquisitions. Jaspalsingh's team has to navigate SEBI regulations on preferential allotments, related party transactions, and change in objects clauses. Each step requires approval from independent directors, shareholder votes, and regulatory no-objections. One misstep could trigger insider trading investigations or minority shareholder lawsuits.

The integration challenges are equally complex. Public company compliance requirements—quarterly results, board composition, audit committees—must be overlaid on a family-run manufacturing business. The Chandock family, accustomed to taking decisions over dinner table discussions, must now document everything, seek independent director approval, and disclose related party transactions.

The cultural transformation is perhaps hardest. Balu's employees, many with the company for decades, suddenly work for a "listed company." Their boss's net worth is now published daily in pink papers. Competitors can download their exact financials. Customers know their profit margins. The transparency that public markets demand conflicts with the secrecy that manufacturing companies traditionally maintain.

But Jaspalsingh turns transparency into competitive advantage. When customers see Balu's strong balance sheet and consistent profitability, they gain confidence in supply security. When employees see the stock price rise, they understand their contribution to value creation. When competitors see Balu's margins, they realize this isn't about undercutting prices but delivering superior value.

The financial engineering continues post-merger. The company systematically retires debt—from ₹50 crore in 2020 to near-zero by 2024. Working capital cycles are optimized—debtor days drop from 169 to 129. The capital structure is cleaned up—no preference shares, no convertible instruments, just straightforward equity with clear ownership.

By the end of 2020, the transformation is complete. Balu Forge Industries Limited trades on the NSE with the symbol BALUFORGE. Market capitalization has grown from ₹100 crore at the time of the reverse merger to over ₹1,000 crore. The Chandock family has achieved the impossible: taking a traditional manufacturing company public while maintaining control, accessing growth capital while avoiding dilution, entering capital markets while preserving operational flexibility.

The reverse merger becomes a template for other family-owned manufacturers considering public markets. It shows that financial innovation isn't just for tech startups—traditional businesses can also hack the system. It proves that Indian capital markets, despite their complexity, can accommodate creative structures that align founder control with public participation.

As 2020 ends, Balu faces a new challenge: delivering on the growth promises implicit in its public market valuation. The company has the capital, the capability, and the credibility. Now it needs to execute on global expansion—a journey that will take it from Belgaum to Mannheim, from supplier to partner, from component manufacturer to solution provider.

V. Building a Global Footprint (2017–2022)

The meeting that changes Balu's global trajectory happens in a Lufthansa lounge at Frankfurt Airport in January 2017. Jaspalsingh is returning from a customer visit when he strikes up a conversation with Klaus Weber, a restructuring consultant specializing in German automotive suppliers. Weber mentions something intriguing: Mercedes-Benz is divesting a precision machining unit at its Mannheim truck plant. The unit is too small for Mercedes's scale but has capabilities most independent suppliers would kill for.

This conversation plants a seed that will bloom five years later. But first, Balu must prove it deserves a seat at the global table. By 2017, the company has become a supplier to 25 OEMs across six continents—an achievement that sounds impressive until you understand what it really means. Each OEM has different specifications, testing requirements, quality systems, and cultural expectations. Americans want detailed documentation; Japanese want continuous improvement; Germans want engineering precision; Indians want cost efficiency. Balu must be all things to all customers.

The complexity is staggering. A crankshaft for a John Deere tractor operating in Iowa cornfields faces different stresses than one for a Ashok Leyland truck navigating Mumbai traffic. A marine crankshaft for a container ship must resist saltwater corrosion while operating continuously for months. A racing crankshaft must be light enough for performance but strong enough to survive 18,000 RPM. Each application requires different alloys, forging techniques, heat treatments, and surface finishes.

2018 marks a pivotal expansion year. Balu acquires and operationalizes a new forging factory in Belgaum—not just any factory but a greenfield facility designed from scratch for Industry 4.0. Every forging hammer is connected to a central control system. Temperature sensors track heat treatment in real-time. Cameras use computer vision to detect surface defects invisible to human inspectors. The facility is less factory, more laboratory—climate-controlled, dust-free, with tolerances measured in microns.

Simultaneously, Balu lays the foundation for a massive 25-acre integrated facility, also in Belgaum. The location choice is strategic: close enough to existing operations for synergy, but independent enough to experiment with new processes. The facility is designed for flexibility—able to handle crankshafts from 50mm to 6,000mm, from 1kg racing components to 500kg marine monsters.

The global expansion strategy reveals sophisticated thinking about comparative advantage. Balu doesn't try to compete with German companies on their home turf for German customers. Instead, it targets German companies manufacturing in Asia, American companies seeking alternative suppliers to China, Japanese companies looking for cost-effective quality. The sweet spot: multinational OEMs that need global supply chains but want regional suppliers who understand local conditions.

The product portfolio expansion during this period is remarkable. Beyond traditional crankshafts, Balu begins manufacturing railway wheels (where failure means derailment), transmission clutches (requiring perfect balance), hydraulic motors (demanding exact tolerances), and even aerospace components (where documentation requirements exceed the weight of the actual parts). Each new product brings new capabilities that enhance existing products—aerospace quality systems improve automotive components, railway safety standards enhance all manufacturing.

Then comes 2022 and the Mannheim acquisition that Jaspalsingh has been orchestrating since that Frankfurt airport conversation. Mercedes-Benz's precision machining unit isn't just equipment—it's a window into German manufacturing excellence. The unit comes with Mercedes-trained operators, Mercedes-approved processes, and most importantly, Mercedes quality DNA. The acquisition cost isn't disclosed, but industry sources suggest Balu paid less for this entire facility than what one new machining center would cost.

The Mannheim acquisition is strategically brilliant for multiple reasons. First, it gives Balu a European presence—critical for serving European customers who want local supply security post-COVID. Second, it provides access to German technical talent—engineers who've spent careers perfecting processes Balu is still learning. Third, it's a signaling device—if Mercedes trusts Balu to take over its precision machining, why shouldn't other OEMs?

The integration of Mannheim reveals Balu's evolved management sophistication. Instead of imposing Indian management on German operations, Jaspalsingh keeps the German team intact, even expanding it. The knowledge transfer goes both ways—Germans learn Indian cost management and flexibility; Indians learn German process discipline and documentation. Video conferences at 2:30 PM IST (11 AM in Mannheim) become daily rituals where best practices are shared across continents.

By 2022, Balu's global footprint extends far beyond customer geography. The company sources steel from Sweden (for quality), Germany (for speciality alloys), and India (for cost). Tooling comes from Japan and Taiwan. Technology partners include Israeli companies (for Industry 4.0), American firms (for simulation software), and German specialists (for heat treatment). This isn't just globalization—it's the careful construction of a best-in-class capability through global knowledge arbitrage.

The customer concentration story during this period is equally impressive. No single customer accounts for more than 15% of revenue—a deliberate strategy to avoid dependence. The customer base spans industries: 30% automotive, 25% industrial, 20% agriculture, 15% marine, 10% others including aerospace and defense. This diversification proves prescient when COVID disrupts automotive but accelerates demand for generators and agricultural equipment.

The technological capabilities Balu builds during this period position it uniquely for the energy transition. The company becomes the only Indian manufacturer capable of producing crankshafts that meet new emission regulations—Euro VI, BS VI, EPA Tier 4. These aren't just tighter versions of old standards; they require fundamental changes in combustion dynamics, which demand different crankshaft geometries, materials, and finishes.

More surprisingly, Balu positions itself for the electric vehicle transition not by abandoning crankshafts but by leveraging precision engineering capabilities for new applications. Electric vehicles still need forged components—motor shafts, transmission parts, suspension components. The same capabilities that make perfect crankshafts can make perfect EV components. It's pivoting without pivoting—using existing capabilities for new markets.

The financial metrics during this global expansion tell their own story. Revenue grows from ₹200 crore in 2017 to ₹560 crore by 2022. But more importantly, margins expand—EBITDA margins improve from 15% to over 20%. This isn't growth through price cutting but through value addition. Average selling prices increase even as volumes grow—a rare combination indicating true competitive advantage.

As 2022 ends, Balu has transformed from an Indian supplier with global customers to a global supplier with Indian roots. The company operates facilities across continents, serves customers in 80 countries, and competes with century-old forging dynasties. But the biggest transformation is yet to come—going fully public and using capital markets not just for funding but for strategic transformation.

VI. Going Public & The Modern Era (2020–Present)

The date is April 29, 2024, and something unusual is happening at the NSE. BALUFORGE, which has been technically listed since 2020 through the reverse merger, is experiencing what traders call a "discovery moment." Institutional investors who dismissed it as another small-cap manufacturing stock are suddenly paying attention. The trigger: Q4 2024 results showing net profit rose 85.56% to ₹28.28 crore compared to previous year, with full-year profit jumping 140.74% to ₹93.67 crore and sales rising 71.40% to ₹559.86 crore.

The transformation from technically-listed to truly-public is a masterclass in capital market communication. Jaspalsingh understands that being listed isn't enough—you need to be discovered, understood, and valued appropriately. The company begins quarterly earnings calls, something unheard of for a ₹1,000 crore market cap company. Jaspalsingh personally presents at investor conferences, explaining not just what Balu makes but why it matters.

The new plant commissioned in Belgaum in FY 2024 represents the physical manifestation of Balu's public market ambitions. This isn't just capacity expansion—it's a statement of intent. The facility incorporates every lesson learned over three decades: German equipment precision, Japanese lean manufacturing, American automation, and Indian jugaad innovation. The plant can switch from producing massive marine crankshafts to precision racing components in hours, not days. The new 52,000 square meter manufacturing facility in Belgaum represents more than expansion—it's an architectural statement of ambition. The facility houses precision machining & forging centers, a defense production unit, dedicated railway wheel & axle production unit, and a unit focused on components for the new energy & mobility sector. In May 2024, Balu acquired three state-of-the-art forging production lines capable of manufacturing 72,000 tons of forged products annually, including a 16-ton closed die forging hammer, a 10-ton closed die forging hammer, and an 8,000-ton capacity mechanical press—all fully automated with the latest technology, including anti-vibration systems and robotic handling, compliant with Industry 4.0 standards.

The operational metrics tell the story of transformation. The company becomes almost completely debt-free—a remarkable achievement for a capital-intensive manufacturing business. Debtor days improve from 169 to 129 days. The debt-to-equity ratio improves significantly to 0.03x from 0.09x a year ago. These aren't just numbers—they represent fundamental operational improvements: better credit terms with customers, improved working capital management, and the financial flexibility to pursue growth without dilution.

The latest quarterly results showcase the momentum. Net profit rose 134.07% to Rs 59.01 crore in Q3 FY25 compared to Rs 25.21 crore in Q3 FY24, with sales rising 73.91% to Rs 255.78 crore from Rs 147.08 crore. For the full financial year FY25, the company posted a 65% rise in revenue to Rs 924 crore, with net profit coming in at Rs 204 crore, up 118% from Rs 93 crore in the previous year. FY25 EBITDA jumped 110.8% to Rs 251 crore.

The capital allocation strategy reveals sophisticated financial thinking. Operating cash flow for FY25 rose 566% to Rs 148 crore, driven by robust EBITDA growth and improved receivables management. The company ended the year with a net cash position of Rs 60 crore—total debt at Rs 36 crore, with cash and equivalents at Rs 96 crore. This cash generation funds organic expansion without dilution, a rare achievement in manufacturing.

The investor communication evolution deserves special mention. Balu begins publishing detailed annual reports that read like business school case studies—explaining not just what happened but why it matters. The company creates an investor relations website with downloadable presentations, something typically seen only in large-cap companies. Quarterly conference calls feature detailed operational metrics, capacity utilization data, and forward-looking commentary that helps investors model the business.

Market recognition follows operational excellence. The stock price rises from ₹200 levels during the reverse merger to over ₹600 by 2024, with market capitalization crossing ₹6,000 crore. Institutional ownership increases from virtually zero to over 15%. Mutual funds that specialize in manufacturing begin taking positions. Foreign portfolio investors discover this hidden gem in India's industrial landscape.

The modern era also brings generational transition. Jaikaran Singh Chandock, Director at Balu Forge and the youngest leader in the company's history, represents the third generation of family leadership. Trained in engineering but with an MBA mindset, Jaikaran brings fresh perspective while respecting institutional knowledge. His focus: digital transformation, sustainability, and preparing for the post-combustion engine world.

The sustainability initiatives reflect evolving stakeholder expectations. Balu implements zero-liquid discharge systems, solar power generation, and heat recovery from forging operations. These aren't just CSR checkboxes—they reduce costs, improve efficiency, and matter to international customers increasingly focused on supply chain sustainability. The company publishes its first ESG report in 2024, quantifying environmental impact and setting reduction targets.

The workforce transformation parallels technological advancement. Employment grows from 375 in FY23 to 525 currently, with expectations to reach 1,000+ employees including contracted workforce. But it's not just about numbers—the skill profile changes dramatically. Balu now employs data scientists who optimize forging parameters using machine learning, metallurgists who develop proprietary alloys, and automation engineers who program collaborative robots.

The customer relationship evolution reflects Balu's transformation from vendor to partner. Major OEMs now involve Balu in design discussions for new engines, seeking input on manufacturability and cost optimization. Some customers share multi-year demand forecasts, enabling better capacity planning. A few strategic customers even co-invest in specialized equipment, deepening partnerships beyond simple purchase orders.

As 2024 progresses, Balu stands at an inflection point. The company has proven it can compete globally, generate cash, and allocate capital efficiently. The question now isn't whether Balu can grow but how fast and in which directions. The electric vehicle transition looms, but so do opportunities in defense, aerospace, and industrial applications. The public market listing provides not just capital but currency for acquisitions. The stage is set for the next phase of growth—one that will test whether Balu can maintain its entrepreneurial edge while operating at institutional scale.

VII. Product Portfolio & Manufacturing Excellence

Walk into Balu's metallurgy lab at 6 AM, and you'll find Dr. Rajesh Kumar, the chief metallurgist, personally examining grain structures under an electron microscope. He's looking at a failed crankshaft—not from Balu but from a competitor—sent by a customer who wants to understand why their previous supplier's component failed after just 50,000 cycles. Kumar's analysis will reveal microscopic inclusions, improper heat treatment, and residual stresses invisible to the naked eye. This obsession with understanding failure modes—even in competitors' products—defines Balu's approach to manufacturing excellence.

The company manufactures fully finished and semi-finished forged crankshafts and forged components including railway wheels, transmission clutches, hydraulic motors, hooks, and brake parts. But this list undersells the complexity. A railway wheel must withstand 500 tons of dynamic loading while maintaining dimensional stability across temperature variations from -40°C to +50°C. A transmission clutch operates in an oil bath at 150°C, engaging and disengaging thousands of times daily without wear. Each product category requires different metallurgy, forging techniques, machining strategies, and quality systems.

The crankshaft portfolio alone spans extraordinary diversity. At one extreme: massive marine crankshafts weighing 500 kilograms, six meters long, forged from specialized steel that resists saltwater corrosion while maintaining strength at the high temperatures of ship engine rooms. At the other extreme: racing crankshafts weighing less than 5 kilograms, machined to tolerances of ±0.005mm, balanced so perfectly that they can spin at 18,000 RPM without vibration. Between these extremes lie hundreds of variants—each optimized for specific applications.

Balu has the capability to manufacture components conforming to the New Emission Regulations & the New Energy Vehicles. This capability isn't just about meeting specifications—it's about understanding the fundamental changes in combustion dynamics required by new emission standards. Euro VI and BS VI engines operate at higher compression ratios, with more precise fuel injection timing, creating different stress patterns in crankshafts. Balu's engineers work backward from these requirements to develop new forging geometries, heat treatment protocols, and surface finishing techniques.

The manufacturing process itself is a symphony of controlled violence and delicate precision. It begins with steel selection—not just any steel but specific grades with controlled chemistry. Too much carbon and the crankshaft becomes brittle; too little and it lacks strength. Trace elements like vanadium, molybdenum, and chromium must be precisely controlled—each affecting different properties like fatigue resistance, hardenability, and corrosion resistance.

The forging process transforms these steel billets through controlled deformation at 1,200°C. The massive hammers—some delivering 16,000 tons of force—must strike with precise timing and pressure. Too fast and the metal tears; too slow and it cools unevenly, creating weak spots. The operator controlling these hammers combines computer assistance with intuitive understanding developed over years—knowing by sound and color when the metal is ready for the next blow.

Heat treatment following forging is equally critical. The crankshafts undergo complex thermal cycles—heating to specific temperatures, holding for precise durations, then cooling at controlled rates. Some components require case hardening, where only the surface is hardened while the core remains ductile. Others need through-hardening for uniform properties. The difference between 850°C and 870°C during austenitization can mean the difference between a crankshaft that lasts 1 million cycles and one that fails at 500,000.

Machining transforms forged blanks into finished components through material removal with cutting tools. But machining a crankshaft isn't like machining a simple shaft—the complex geometry with multiple bearing journals, counterweights, and oil passages requires sophisticated 5-axis CNC machines. The company has incorporated 7-axis precision machining capabilities, allowing even more complex geometries and better surface finishes.

The quality systems supporting this manufacturing excellence go beyond simple measurement. Every crankshaft undergoes non-destructive testing—magnetic particle inspection for surface cracks, ultrasonic testing for internal defects, dimensional verification using coordinate measuring machines accurate to 0.001mm. But Balu goes further: accelerated life testing where sample crankshafts are subjected to millions of cycles under extreme conditions, metallographic analysis of grain structure, residual stress measurement using X-ray diffraction.

Post the acquisition of the Mercedes-Benz precision machining plant in Mannheim, Germany, the company's machining capacity soared to 32,000 MTPA. With further acquisitions and integration of three new forging lines, their forging capacity has reached 72,000 MTPA. This capacity expansion isn't just about volume—it's about capability range. The Mercedes equipment brings German precision to Balu's Indian cost structure, enabling the company to compete for contracts previously monopolized by European suppliers.

The R&D capability deserves special attention. The company's in-house R&D team of 75 engineers works across metallurgy, design, tooling, and testing. This team doesn't just solve today's problems—they anticipate tomorrow's challenges. When a customer mentions plans for a new engine design two years out, Balu's R&D team begins developing the forging and machining processes today. When emission regulations are proposed, they start experimenting with new materials and geometries before the rules are finalized.

The tooling capability—often overlooked but critical—sets Balu apart. Forging dies must withstand thousands of high-pressure cycles at extreme temperatures. Balu designs and manufactures these dies in-house, using specialized tool steels and sophisticated CAD/CAM systems. The ability to rapidly prototype and modify dies means Balu can move from customer drawing to first article in weeks, not months—critical for winning new business in fast-moving markets.

The company has adopted automated robotics, anti-vibration forging systems from GERB Germany, and digital simulation tools to ensure quality, scalability, and efficiency. Advanced machining, additive manufacturing for rapid prototyping, and proprietary material chemistry research form the backbone of Balu's capability. This technology stack enables Balu to compete not on cost but on capability—making components that others simply cannot.

The product portfolio evolution reveals strategic thinking about market positioning. While competitors chase volume in commodity crankshafts, Balu focuses on complex, high-value components where engineering matters more than labor cost. A racing crankshaft might take 10 times longer to manufacture than a standard automotive crankshaft but commands 50 times the price. A marine crankshaft requires specialized equipment and expertise but offers multi-year contracts with predictable demand.

The manufacturing excellence translates into tangible competitive advantages. Balu's first-pass yield—the percentage of components that meet specifications without rework—exceeds 98%, compared to industry averages of 85-90%. Customer PPM (parts per million) defect rates are in single digits, with some customers reporting zero defects across millions of components. These metrics matter because they reduce customer costs for inspection, rework, and warranty claims—making Balu the preferred supplier even at premium prices.

Looking forward, Balu's manufacturing excellence positions it uniquely for emerging opportunities. The defense sector requires components that can withstand battlefield conditions—extreme temperatures, shock loads, contamination. The aerospace sector demands documentation and traceability that would overwhelm most suppliers. The new energy sector needs components optimized for different operating characteristics of electric and hydrogen powertrains. Each represents not just new markets but new capability frontiers that Balu is already exploring.

VIII. Playbook: Business & Investing Lessons

The first lesson from Balu's journey challenges conventional wisdom about emerging market companies: you can build global competitiveness through capability, not just cost. When investors analyze Indian manufacturing companies, they typically focus on labor cost advantages. Balu's labor costs are actually higher than many Indian competitors because it employs skilled engineers and metallurgists. The competitive advantage comes from doing things others cannot—making 6-meter marine crankshafts, achieving single-digit PPM defect rates, meeting emission standards that didn't exist five years ago.

The reverse merger as a growth hack deserves its own business school case study. Most manufacturing companies view going public as an endpoint—the liquidity event that rewards years of building. Jaspalsingh Chandock saw it differently: public listing as a tool for transformation, not just liquidity. By reverse-merging into an already-listed shell, Balu avoided the 18-month IPO process, the 15% discount typically required for successful listing, and the pressure to show quarterly growth from day one. The company entered public markets on its own terms, then proved its worth through operational performance rather than investment banker storytelling.

Building engineering capabilities before brand represents another counterintuitive insight. Consumer companies obsess over brand building—spending fortunes on marketing before they have product-market fit. Balu spent three decades building engineering capabilities before most customers knew its name. When German automotive engineers visited Belgaum in 2017, they didn't come because of Balu's brand—they came because Balu could do something they needed. The brand followed capability, not the other way around.

The importance of certifications in B2B manufacturing cannot be overstated. ISO/TS16949:2009 certification cost Balu millions of rupees and 18 months of effort. The ROI? Infinite. That single certification opened doors to every major automotive OEM globally. In B2B manufacturing, certifications aren't bureaucratic checkboxes—they're binary gates. You either have them and can compete, or you don't and cannot. Balu understood this early, investing in certifications before it had the customers to justify them.

Capital efficiency metrics reveal operational excellence. The company achieves ROCE of 31.3% and ROE of 25.4%—exceptional for capital-intensive manufacturing. How? First, the equipment acquisition strategy—buying distressed assets from European companies at 10-20% of replacement cost. Second, the focus on value-added products—a precision racing crankshaft generates 50x the margin of a commodity tractor crankshaft. Third, operational efficiency—98% first-pass yield means less working capital tied up in rework and scrap.

Managing working capital in manufacturing requires understanding that cash conversion cycles in B2B manufacturing are fundamentally different from B2C businesses. Balu improved debtor days from 169 to 129, but even 129 days would horrify a software company. The key insight: in manufacturing, working capital management isn't about minimizing days but optimizing the entire cash conversion cycle. Balu negotiates longer payment terms with suppliers (using its strong balance sheet as leverage) while offering early payment discounts to customers who pay within 60 days. The result: positive cash flow despite long receivable cycles.

Global expansion from an emerging market base typically follows one of two patterns: either companies try to hide their emerging market origins (adopting Western-sounding names, establishing European headquarters) or they leverage cost advantages until competitors match them. Balu chose a third path: embracing its Indian identity while delivering developed-market quality. The Belgaum facility tours became a selling point—customers saw the combination of Indian ingenuity, German equipment, and Japanese processes as unique rather than contradictory.

Family business professionalization usually involves hiring external CEOs, implementing formal governance, and reducing family involvement. Balu professionalized differently. The family remained central—Jaspalsingh as leader, next generation being groomed—but surrounded themselves with professional managers and independent directors. Board meetings follow formal protocols, but strategic discussions still happen over family dinners. The lesson: professionalization doesn't mean eliminating family influence but channeling it constructively.

The importance of technical depth in leadership emerges clearly from Balu's story. Both Prehlad Singh and Jaspalsingh were engineers who understood metallurgy, forging, and machining at a granular level. They could walk the shop floor and spot problems, discuss alloy chemistry with metallurgists, and debate process improvements with operators. This technical depth enabled better capital allocation decisions—knowing which equipment truly added capability versus just capacity.

Patient capital in manufacturing contradicts the venture capital mentality of rapid scaling. Balu took 30 years to reach ₹1,000 crore market cap—a timeline that would frustrate any VC. But manufacturing doesn't follow software scaling laws. You can't "growth hack" metallurgy or "iterate quickly" on forging processes. Each capability takes years to build, but once built, creates barriers competitors cannot quickly overcome. Investors who understand this patience are rewarded with compounding returns rather than hockey-stick growth.

The diversification paradox shows up clearly in Balu's strategy. Conventional wisdom suggests focus—do one thing exceptionally well. Balu makes crankshafts for tractors, trucks, cars, ships, generators, and racing vehicles, plus railway wheels, transmission parts, and defense components. This seems unfocused until you realize the underlying capability—precision forging and machining—is consistent. The diversification is in application, not capability. This provides resilience (automotive downturns don't affect railway demand) while leveraging core competencies.

Technology adoption in traditional manufacturing often focuses on automation to reduce labor costs. Balu's approach was different: technology to enhance capability. The 7-axis CNC machines don't replace workers—they enable workers to make components that were previously impossible. The Industry 4.0 sensors don't eliminate quality inspectors—they give inspectors data to prevent defects rather than just detect them. Technology amplifies human capability rather than replacing it.

The value of customer intimacy in B2B manufacturing cannot be underestimated. Balu engineers sit in customer design reviews, understanding not just what customers want but why they want it. When a customer specifies a particular surface finish, Balu asks about the application—sometimes suggesting alternatives that perform better at lower cost. This consultative approach transforms vendor relationships into partnerships, creating switching costs that go beyond price.

Financial discipline during growth is perhaps the most important lesson. As revenue grew from ₹200 crore to ₹900 crore, the temptation to lever up, make acquisitions, or diversify into unrelated areas must have been immense. Instead, Balu maintained an almost debt-free balance sheet, acquired only directly synergistic assets, and stayed focused on precision manufacturing. This discipline created the financial flexibility to weather downturns and pursue opportunities without dilution.

For investors, Balu offers a template for evaluating manufacturing companies: Look for technical capability that creates genuine barriers to entry, not just cost advantages that disappear with currency movements. Value certifications and customer relationships that take years to build. Appreciate patient capital allocation that builds long-term competitive advantages. Understand that family ownership can be a strength if properly channeled. Most importantly, recognize that in manufacturing, operational excellence compounds over decades, creating value that financial engineering cannot replicate.

IX. Analysis & Bear vs. Bull Case

The Bull Case: A Precision Engineering Powerhouse

The bull case for Balu Forge starts with valuation reality versus operational momentum. Revenue grew 65% to Rs 924 crore in FY25, with net profit surging 118% to Rs 204 crore. At current valuations around ₹6,800 crore market cap, the company trades at roughly 33x FY25 earnings—seemingly expensive until you consider the growth trajectory and margin expansion story still unfolding.

The financial metrics tell a story of a company hitting its operational sweet spot. FY25 EBITDA jumped 110.8% to Rs 251 crore, while operating cash flow rose 566% to Rs 148 crore. This isn't just revenue growth—it's profitable growth with expanding margins and accelerating cash generation. The company has reached the scale where fixed costs are largely absorbed, and incremental revenue drops disproportionately to the bottom line.

The virtually debt-free balance sheet provides enormous strategic flexibility. The company ended FY25 with a net cash position of Rs 60 crore—total debt at just Rs 36 crore against cash and equivalents of Rs 96 crore, with debt-to-equity improving to 0.03x. In a capital-intensive industry where competitors typically operate at 1-2x debt-to-equity, this balance sheet strength enables Balu to pursue growth opportunities, weather downturns, and negotiate from a position of strength with both customers and suppliers.

The customer diversification achieved presents a formidable moat. Supplying to 25 OEMs across 80 countries, with no single customer exceeding 15% of revenue, Balu has built resilience rare in component manufacturing. The customer base spans industries—automotive, industrial, agricultural, marine, defense—and geographies, providing natural hedging against sector-specific or regional downturns. More importantly, these aren't transactional relationships but multi-year partnerships with significant switching costs.

The unique capability in emission-compliant and EV-ready components positions Balu at the intersection of two massive trends. As the only Indian company with capability to manufacture components conforming to new emission regulations and new energy vehicles, Balu can serve both the last generation of advanced combustion engines and the first generation of electric powertrains. This dual capability extends the runway for growth regardless of how quickly the EV transition occurs.

The promoter holding pattern suggests aligned interests. With the Chandock family maintaining 54.8% ownership, management thinks like owners because they are owners. The recent generational transition bringing in younger family members trained in modern management while respecting manufacturing fundamentals suggests continuity with evolution—perhaps the best combination for long-term value creation.

The capacity expansion trajectory indicates management confidence in demand visibility. Machining capacity at 32,000 MTPA and forging capacity at 72,000 MTPA represent just Phase One of expansion plans. The company wouldn't be investing hundreds of crores in capacity without multi-year visibility from customers. The fact that this expansion is being funded through internal accruals rather than debt or dilution preserves returns for existing shareholders.

The Bear Case: Challenges in a Changing Landscape

The bear case begins with the elephant in the room: the internal combustion engine's eventual obsolescence. While Balu has capabilities for EV components, crankshafts for combustion engines remain the core business. Even if the transition takes 20 years, it represents a melting ice cube that the company must replace with new revenue streams. The question isn't if but how fast and whether Balu can build equally dominant positions in new product categories.

The auto industry's notorious cyclicality poses persistent risks. While Balu has diversified across sectors, automotive and related industries still comprise the majority of revenue. A synchronized global downturn—like 2008 or 2020—would impact demand across customer segments. The operating leverage that drives margin expansion in good times becomes a burden when capacity utilization falls below 70%.

Competition from established giants cannot be ignored. Bharat Forge, with its ₹70,000+ crore market cap and global footprint, has resources Balu cannot match. European forging companies, while struggling with costs, possess centuries of accumulated knowledge and relationships. Chinese manufacturers, backed by state support and massive domestic markets, compete aggressively on price. Balu must constantly run faster just to maintain relative position.

The dependence on global trade brings geopolitical risks. With majority revenue from exports, Balu is exposed to trade wars, tariffs, and protectionist policies. The "friend-shoring" and "near-shoring" trends could disadvantage Indian suppliers to Western markets. Currency fluctuations—particularly rupee appreciation—directly impact competitiveness. A 10% rupee appreciation without corresponding productivity gains could eliminate operating margins.

The limited dividend yield at 0.03% signals that this isn't an income investment. Management reinvests essentially all profits into growth, which is excellent if that growth materializes but provides no cushion if it doesn't. Investors seeking current returns must look elsewhere, making Balu suitable only for those with genuine long-term horizons and tolerance for volatility.

Geographic concentration in manufacturing presents operational risks. Despite global customers, production remains concentrated in Belgaum, with the German facility being relatively small. A natural disaster, labor unrest, or infrastructure failure in Belgaum could disrupt global supply chains. Customers increasingly demand geographic diversification from suppliers, which will require capital investment that might dilute returns.

The valuation multiple at 33x earnings prices in significant growth. Any disappointment—a lost customer, delayed capacity ramp-up, margin compression from raw material costs—could trigger multiple compression. The stock's limited liquidity, with promoters holding 54.8%, means that selling pressure could cause disproportionate price declines. Institutional investors requiring liquidity might avoid the stock despite operational merit.

The Balanced View: Probability-Weighted Outcomes

The reality likely lies between extremes. Balu has built genuine competitive advantages in precision manufacturing that won't disappear overnight. The company's track record of navigating transitions—from agricultural to automotive, from domestic to global, from private to public—suggests adaptability that bears underestimate. The management team's technical depth and capital allocation discipline provide confidence in navigation through challenges.

The EV transition presents both risk and opportunity. While crankshaft demand will eventually decline, the transition period might be longer and more lucrative than expected. Advanced combustion engines for hybrids, range extenders for EVs, and specialized applications (marine, defense, generators) will require crankshafts for decades. Meanwhile, Balu's precision manufacturing capabilities translate to EV components—motor shafts, gear sets, battery housing components—where quality and reliability matter even more than in combustion engines.

The competitive dynamics favor focused specialists over diversified giants. While Bharat Forge has more resources, it also has more complexity. Balu's focus on precision forging and machining allows deeper capability development and faster decision-making. The company's size—large enough for scale but small enough for agility—might be optimal for capturing emerging opportunities that giants overlook and minnows cannot address.

The market structure evolution suggests room for multiple winners. As global OEMs reduce supplier bases but require geographic diversification, being the strong number two or three player might be more profitable than being a subscale number five or six. Balu doesn't need to defeat Bharat Forge—it needs to maintain its position as a credible alternative, which its customer base and capabilities suggest is achievable.

For investors, the key question isn't whether Balu is a good company—operational metrics clearly indicate it is—but whether it's a good investment at current valuations. The answer depends on time horizon and alternatives. For those seeking steady compounders in India's manufacturing renaissance, Balu offers exposure to multiple themes: industrial growth, export competitiveness, and technical capability development. For those worried about near-term volatility or seeking immediate returns, better alternatives exist.

X. Future Outlook & Strategic Priorities

The war room at Balu's Belgaum headquarters has an unusual decoration: a timeline showing every major technology transition in automotive history—from steam to internal combustion, mechanical to electronic control, naturally aspirated to turbocharged. At the end, a question mark labeled "2030-2040?" represents the next transition. Below it, Jaspalsingh has written: "Be ready for all answers."

This preparation for multiple futures defines Balu's strategic thinking. The company isn't betting on a single scenario—rapid EV adoption or extended ICE dominance—but building capabilities that remain valuable across scenarios. The precision forging and machining expertise that makes perfect crankshafts can make perfect motor shafts, transmission gears, or hydrogen fuel cell components. The quality systems that satisfy automotive OEMs work equally well for aerospace or defense customers.

The EV transition strategy deserves careful examination. Rather than abandoning ICE components or pivoting entirely to EV, Balu is playing what chess masters call a "both-and" game. The company continues investing in advanced crankshaft capabilities—particularly for hybrid engines, range extenders, and specialized applications that will persist regardless of passenger car electrification. Simultaneously, it's developing capabilities for EV-specific components where precision and reliability command premiums.

The defense and aerospace opportunities represent natural adjacencies that leverage existing capabilities while diversifying end markets. The defense production unit focuses on production of undercarriage parts & heavy forging components for the global defense industry. These markets value reliability over cost, require extensive documentation that Balu already maintains, and offer multi-year contracts with attractive margins. The company's experience with military vehicle components and railway applications provides credibility in these safety-critical sectors.

The capacity expansion roadmap reveals ambitious but measured growth plans. The current 72,000 MTPA forging capacity represents just Phase One. Phase Two, already in planning, will add specialized capacity for larger components (marine, power generation) and precision components (aerospace, medical). The expansion philosophy: add capacity in modular increments, ensure customer commitments before major investments, and maintain flexibility to adjust product mix as demand evolves.

Technology partnerships are evolving from equipment purchases to capability development. The relationship with GERB Germany for anti-vibration systems extends beyond buying equipment to joint development of solutions for new applications. Israeli Industry 4.0 partners aren't just software vendors but collaborators in developing predictive maintenance algorithms specific to forging operations. These partnerships provide access to global innovation while maintaining control over core manufacturing processes.

The automation strategy focuses on augmentation rather than replacement. While competitors chase lights-out factories, Balu invests in collaborative robots that work alongside skilled operators, AI systems that suggest process improvements for engineers to validate, and sensors that provide data for human decision-making. This human-centric automation preserves the craft knowledge essential in precision manufacturing while enhancing productivity and consistency.

Sustainability initiatives go beyond compliance to competitive advantage. The zero-liquid discharge systems and solar power generation reduce costs while meeting customer sustainability requirements. More strategically, Balu is developing capabilities in lightweight components that improve vehicle efficiency—whether ICE or EV. The company is also exploring green steel sourced from hydrogen-based production, anticipating customer demands for low-carbon supply chains.

The next generation leadership transition unfolds gradually but deliberately. Jaikaran Chandock brings digital native thinking while respecting manufacturing fundamentals. Trimaan Chandock, also part of the next generation, focuses on international market development and customer relationships. This division of responsibilities—technology and operations versus markets and relationships—positions Balu for continuity with renewal.

Geographic expansion considerations reflect lessons from the Mannheim acquisition. Rather than greenfield facilities in new countries, Balu seeks strategic acquisitions that bring local presence, customer relationships, and specialized capabilities. The focus: developed markets where quality commands premiums and emerging markets with growing domestic demand. Each expansion must enhance capability, not just add capacity.

The financial priorities remain consistent: profitable growth, capital efficiency, and balance sheet strength. Management targets 20%+ EBITDA margins, ROCE above 25%, and maintaining near-zero debt. These aren't just financial metrics but strategic choices—high margins indicate differentiated products, strong ROCE suggests capital discipline, and low debt provides flexibility for opportunities or downturns.

The R&D investment trajectory indicates where Balu sees future value creation. Beyond incremental process improvements, the company invests in fundamental research: new alloys for extreme applications, surface treatments that extend component life, manufacturing processes for materials like titanium and composites. This R&D doesn't generate immediate returns but builds options for future growth.

Market communication evolution reflects public company maturation. Quarterly earnings calls become more sophisticated, with detailed operational metrics and strategic updates. The company begins hosting facility visits for institutional investors, showing rather than just telling the Balu story. Management articulates not just current performance but long-term vision, helping markets understand and value the company appropriately.

The strategic priorities crystallize around three themes. First, capability leadership—maintaining technical edge in precision forging and machining regardless of end application. Second, customer centricity—deepening relationships with existing customers while selectively adding new partnerships that enhance capability or market access. Third, operational excellence—continuous improvement in quality, delivery, and cost that makes Balu the supplier of choice even at premium prices.

Looking toward 2030, Balu's ambition extends beyond growth to transformation. The vision: evolving from component supplier to solution provider, from manufacturing partner to innovation collaborator, from Indian company with global customers to global company with Indian roots. This transformation won't happen overnight—in manufacturing, nothing important does—but the foundations laid over three decades and strategic choices being made today position Balu to remain relevant regardless of how technology, markets, and customer needs evolve.

For investors evaluating Balu's future, the key insight is that uncertainty creates opportunity for those with capability to adapt. The company's history of navigating transitions, portfolio of capabilities that transcend specific applications, and financial strength to invest through cycles suggest resilience that static analysis might miss. The future remains unwritten, but Balu appears to hold the right pen.

XI. Recent News### **

Strategic Developments & Major Announcements**

Balu Forge Industries Ltd. announced its unaudited consolidated financial results for the quarter ending 30th June 2025. The Q1 FY26 results showcase continued momentum with revenue from operations rising 33% YoY to Rs. 2,332 Mn, driven by a richer value-added product mix and higher operating leverage as the company scaled capacity and capability. EBITDA grew 67.3% YoY to Rs. 723 Mn, reflecting enhanced manufacturing efficiencies and the benefit of integrated high-margin machining. Profit after tax jumped 66.9% YoY to Rs. 570 Mn, underpinned by margin expansion, stable cost control, and continued gains in global market share despite external uncertainties.

The standout strategic development comes from a Memorandum of Understanding (MoU) signed with Swan Energy Limited to create a Special Purpose Vehicle (SPV) focused on serving global industries, including defence, aerospace, railways, and nuclear. This strategic diversification positions Balu as a prominent player in high-growth, technology-driven sectors. This partnership represents a significant pivot toward higher-margin, more defensible market segments where technical capabilities matter more than cost.

Capacity Expansion & Technology Integration

The integration of 7-axis CNC machining technology strengthens Balu Forge's capability to produce intricate, high-precision components. This expansion, financed through internal accruals, is poised to fuel growth in the aerospace, defence and oil & gas sectors. The technology upgrade isn't just about adding capacity—it's about adding capability that few competitors can match.

The green field manufacturing campus commissioning is in full swing & will house a fully automated plant with modern technology, larger integration of Industry 4.0, installation of a solar farm for energy saving, plant commissioning as per the latest ISO standards, Implementation of 5S & TPM practices & Implementation of OSHA standards. This represents not just expansion but a reimagining of what an Indian manufacturing facility can be—matching global best practices while maintaining cost competitiveness.

Financial Performance Trajectory

The latest quarterly results continue the strong performance trend. For Q4 FY25, Revenue from Operations: Rs 270 crore vs. Rs 161 crore in Q4FY24 — up 67.3%, with EBITDA: Rs 75 crore vs. Rs 34 crore in Q4FY24 — up 118.1%, and PAT: Rs 63 crore vs. Rs 28 crore in Q4FY24 — up 123.1%. The margin expansion is particularly noteworthy, with EBITDA Margin improving to 27.8% vs. 21.3% in Q4FY24 — improvement of 647 bps.

For the full fiscal year FY25, Cash Flow from Operations of Rs 148 crore in FY25, a sharp increase of 566% compared to FY24, underpinned by improved EBITDA and collection of receivables. This cash generation capability funds growth without dilution or debt, a rare achievement in capital-intensive manufacturing.

Market Recognition & Investor Interest

Nuvama has initiated a BUY rating on Balu Forge Industries, projecting a target price of Rs 790, citing strong growth potential in defense and industrial sectors. The institutional recognition reflects growing awareness of Balu's unique positioning at the intersection of traditional manufacturing excellence and emerging market opportunities.

Number of FII/FPI investors increased from 50 to 67 in Mar 2025 qtr. The increasing foreign institutional interest suggests that global investors are beginning to recognize Balu as a play on India's manufacturing capabilities and the global supply chain reorganization away from China.

Strategic Commentary from Management

Management noted: "These results highlight our resilient business model and strong market positioning, setting the stage for continued growth. Our success stems from strategies like portfolio expansion, client diversification, and delivering solutions across key sectors. As the Indian forging industry benefits from China+1 and Europe+1, Balu Forge is investing in innovation and partnerships for sustainable growth and global expansion."

The China+1 and Europe+1 strategies mentioned by management represent massive tailwinds. As global OEMs seek to diversify supply chains away from China and reduce dependence on high-cost European suppliers, Indian precision manufacturers like Balu are perfectly positioned to capture share.

Operational Milestones

Strategic initiatives emphasize expanding defence production, enhancing automation, and strengthening global partnerships. With a strong focus on operational scalability, customer diversification, and ESG commitments, Balu Forge continues to strengthen its global footprint and industry positioning.

The defense focus is particularly strategic given India's push for defense indigenization and the global defense spending cycle. Unlike automotive cycles, defense contracts offer multi-year visibility and are less sensitive to economic cycles.

XII. Links & Resources

Company Resources: - Official Website: www.baluindustries.com - NSE Stock Page: NSE: BALUFORGE - BSE Stock Page: BSE: 531112

Financial Information: - Annual Reports: Available on company website investor relations section - Quarterly Results: Published on NSE/BSE and company website - Conference Call Transcripts: Available post earnings announcements

Research & Analysis: - Screener.in: Comprehensive financial metrics and peer comparison - Trendlyne: Technical analysis and shareholding patterns - ICICI Direct: Research reports and rapid results analysis

Industry Reports: - Auto Component Manufacturers Association (ACMA) India - Society of Indian Automobile Manufacturers (SIAM) - Confederation of Indian Industry (CII) Manufacturing Reports

Relevant Books on Manufacturing & Strategy: - "The Machine That Changed the World" by Womack, Jones, and Roos (on lean manufacturing) - "Good to Great" by Jim Collins (on company transformation) - "The Innovator's Dilemma" by Clayton Christensen (on disruption in traditional industries) - "Zero to One" by Peter Thiel (on building differentiated businesses)

Long-form Articles & Case Studies: - Harvard Business Review: Articles on reverse mergers and manufacturing excellence - McKinsey Insights: India manufacturing and global supply chain reports - BCG Perspectives: Studies on emerging market manufacturing champions

Regulatory Filings: - SEBI EDIFAR: All regulatory filings and disclosures - MCA Portal: Company registration and compliance documents - NSE Corporate Announcements: Real-time updates on material events

Industry Associations: - Forging Industry Association (FIA) - All India Association of Industries (AIAI) - Engineering Export Promotion Council (EEPC) India

Note: This analysis is based on publicly available information and should not be construed as investment advice. Potential investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions. The automotive and manufacturing industries are subject to various risks including technological disruption, regulatory changes, and economic cycles that could materially impact company performance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube