Bajaj Housing Finance: The 100-Year Startup

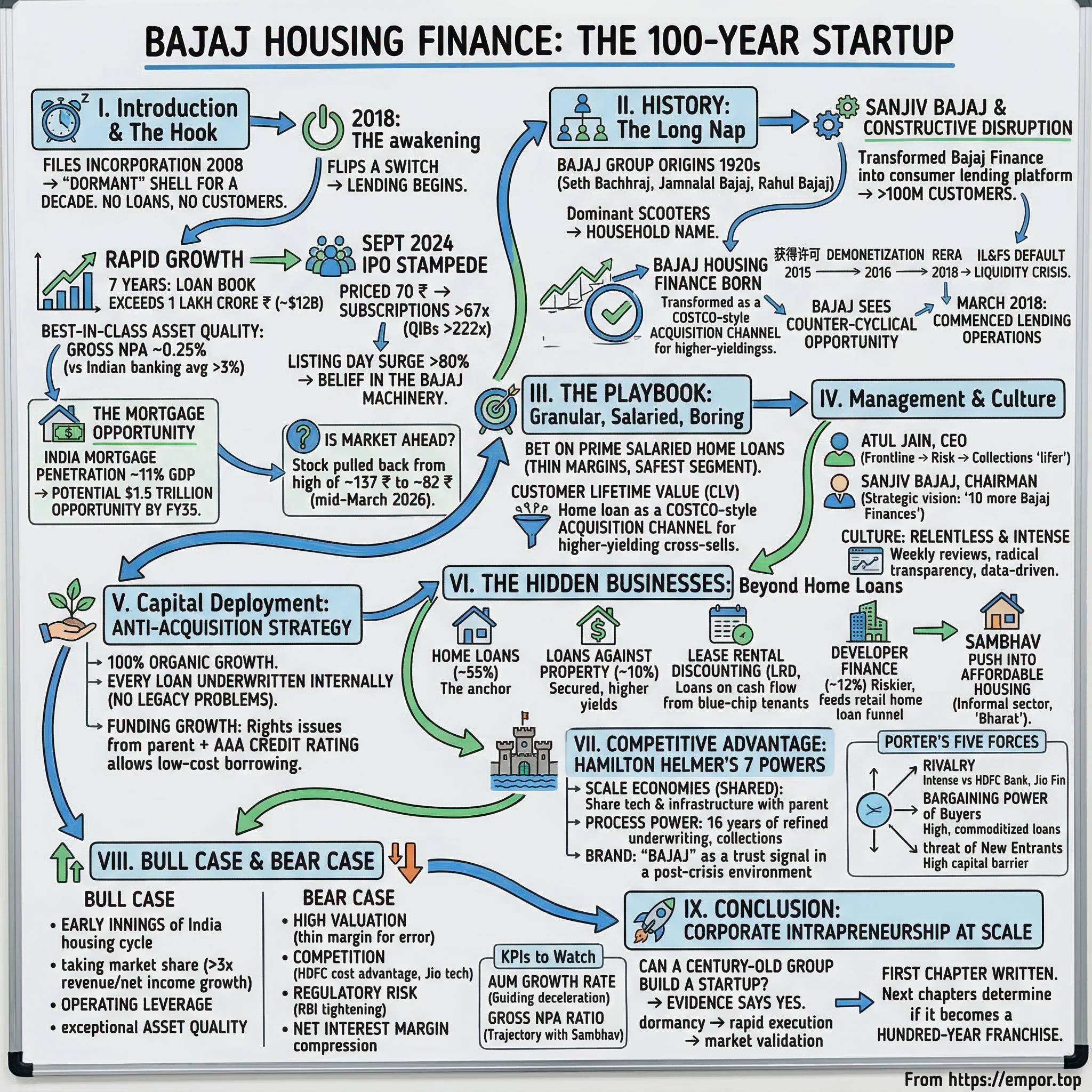

I. Introduction and The Hook

Picture this: a company files its incorporation papers in 2008, gets a nondescript name — Bajaj Financial Solutions — and then proceeds to do absolutely nothing for nearly a decade. No loans disbursed, no customers acquired, no revenue generated. It sits on the corporate registry like a placeholder, a ticket stub for a movie that has not yet been made. Then, in 2018, someone flips a switch. The company wakes up, changes its name, and begins lending. Seven years later, it has amassed a loan book exceeding one lakh crore rupees — roughly twelve billion US dollars — with asset quality metrics that would make the most conservative Japanese banker blush. Its gross non-performing asset ratio hovers around a quarter of a percent. For context, India's banking system average sits somewhere north of three percent. Even the best private banks in the country run gross NPAs of one percent or higher.

This is the story of Bajaj Housing Finance Limited, ticker BAJAJHFL on the National Stock Exchange of India. And it is not merely a story about a company that gives people mortgages. It is a story about corporate intrapreneurship at its most disciplined, about a century-old conglomerate proving that big, established groups can still launch ventures with the urgency and precision of a Silicon Valley startup — provided they marry that urgency with something Silicon Valley often lacks: an almost obsessive credit culture.

The premise is deceptively simple. India, despite being the fifth-largest economy on the planet, has mortgage penetration of roughly eleven percent of GDP. China sits at thirty percent. The United States and most of Europe exceed fifty percent. The gap represents what analysts estimate could be a 1.5-trillion-dollar mortgage opportunity by fiscal year 2035. Everyone in Indian financial services knows this. State Bank of India knows it. HDFC Bank — fresh off its landmark forty-billion-dollar merger with Housing Development Finance Corporation in July 2023 — certainly knows it. LIC Housing Finance, PNB Housing, Can Fin Homes — they all know it. The question has never been whether India's housing finance market will grow. The question has always been: who will capture that growth with the best risk-adjusted returns?

Bajaj Housing Finance's answer to that question was so convincing that when it finally came to the public markets in September 2024, investors stampeded. The initial public offering, priced at seventy rupees per share, attracted subscriptions worth over sixty-seven times the shares on offer. Qualified institutional buyers — the smart money — oversubscribed their portion by a staggering two hundred and twenty-two times. On listing day, September 16, 2024, the stock surged over eighty percent from its issue price. The market was not just pricing in a mortgage lender. It was pricing in a belief system — the conviction that the Bajaj machinery, once pointed at a market, would execute with a ruthlessness and precision that competitors simply could not match.

But has the market gotten ahead of itself? The stock, which touched a high of nearly one hundred and thirty-seven rupees in its early exuberance, has since pulled back sharply, trading around eighty-two rupees as of mid-March 2026 — actually below its listing day close. The honeymoon, as they say, is over. What remains is the fundamental question: is this business as good as the brand suggests, or is it a well-packaged commodity in a brutally competitive market?

To answer that, one has to go back much further than 2018. One has to go back to the 1920s.

II. History: The Long Nap and The Awakening

The Bajaj Group traces its origins to a trading family in central India. Seth Bachhraj built a successful merchant operation in the late nineteenth century. When he died in 1906, his seventeen-year-old adopted grandson, Jamnalal Bajaj, took control. Jamnalal was an unusual figure — a businessman who was also a close associate of Mahatma Gandhi, a freedom fighter who believed deeply in the trusteeship concept that wealth should serve the common good. He built a cotton trading empire and diversified into sugar refining in 1931 and steel rolling in 1937, long before Indian industrialization became fashionable.

But the Bajaj name became a household word for an entirely different reason: scooters. Bajaj Auto, established in 1959, went on to become the dominant two-wheeler manufacturer in India. For decades, owning a Bajaj Chetak scooter was a rite of passage for the Indian middle class. The brand became synonymous with practical, reliable, no-nonsense engineering for the masses.

Under Rahul Bajaj, who took the helm in 1965 and ran the group for over five decades, Bajaj Auto grew from a seventy-five-million-rupee turnover company to a twelve-thousand-crore-rupee giant. Rahul Bajaj was famously blunt, a Padma Bhushan awardee who sparred with governments and refused to accept mediocrity. His leadership style — direct, confrontational, deeply principled — became the cultural DNA of the entire group. When the Bajaj family eventually split the empire between his two sons, Rajiv Bajaj took the auto business, and Sanjiv Bajaj took the financial services arm.

This is where the housing finance story really begins. Sanjiv Bajaj, a Harvard Business School MBA and a mechanical engineer from Pune, inherited what was then a relatively modest financial services operation. Bajaj Finance Limited existed, but in the early 2000s, it was primarily a vehicle financing company. It was Sanjiv who envisioned transforming it into a diversified financial services juggernaut. He has spoken openly about his philosophy of "constructive disruption" — the idea that large corporations must constantly cannibalize their own businesses before competitors do it for them. Under his stewardship, Bajaj Finance evolved from an auto-loan NBFC into India's premier consumer lending platform, with a customer base exceeding one hundred million and assets under management of over four lakh crore rupees.

It was within this context that Bajaj Housing Finance was born — first as a corporate shell in 2008, registered under the name Bajaj Financial Solutions. For years, it existed on paper only. Why the dormancy? Because the parent, Bajaj Finance, was in the middle of its own extraordinary growth trajectory. Between 2008 and 2017, Bajaj Finance was busy revolutionizing consumer lending in India — two-wheeler loans, consumer durables financing, personal loans, the entire cross-sell ecosystem that would later become the envy of every bank in the country. Housing finance was on the strategic roadmap, but the timing was not right.

Two things changed the calculus. First, in September 2015, the company obtained its certificate of registration from the National Housing Bank, the industry regulator, as a non-deposit-taking housing finance company. This was the license — the permission slip to play in the mortgage market. But having a license and deploying capital are two very different things. Bajaj waited.

The second inflection point came in 2017 and 2018, when a confluence of events reshaped the Indian real estate and financial landscape. Demonetization in November 2016 had flushed black money out of real estate transactions, making the market more transparent. The Real Estate Regulation and Development Act, known as RERA, came into effect in 2017, bringing accountability to developers for the first time. And then, in September 2018, came the earthquake: Infrastructure Leasing and Financial Services — IL&FS — defaulted on its obligations, triggering a cascading liquidity crisis across India's non-banking financial sector.

The IL&FS collapse was a watershed moment. Suddenly, the NBFC sector that had been growing at breakneck speed found itself starved of funding. Dewan Housing Finance Corporation, better known as DHFL, would eventually collapse into bankruptcy. Indiabulls Housing Finance came under severe pressure. Even well-run housing finance companies found themselves battling perception and liquidity challenges. The market was terrified.

Bajaj saw something different. Where others saw carnage, Bajaj Finance's leadership saw a counter-cyclical opportunity of generational proportions. The weakest players were being eliminated. The regulatory environment, post-RERA and post-demonetization, was cleaner than it had ever been. And the competitors who survived would be so focused on shoring up their own balance sheets that they would cede market share to anyone bold enough to enter aggressively.

In March 2018, Bajaj Housing Finance commenced lending operations. The timing was deliberate, almost surgical. They entered a market precisely when others were retreating. They had a pristine balance sheet with zero legacy problems, a technology stack borrowed from one of India's most sophisticated lenders, and a brand name that, in a trust-deficit environment, was worth more than any amount of advertising could buy. The long nap was over. The sprint had begun.

By the end of fiscal year 2019, just twelve months after starting, the company had built an assets-under-management base of fifteen thousand crore rupees. By fiscal 2020, it doubled to thirty thousand crore. The pace was unlike anything the Indian housing finance industry had seen from a standing start.

III. The Playbook: Granular, Salaried, Boring

Walk into the credit committee of most housing finance companies in India, and the conversation inevitably gravitates toward yield. How do we earn more? Where is the high-margin business? Should we do more developer loans at fourteen percent, or push into small-ticket unsecured lending? The instinct to chase yield is almost primal in Indian financial services, where the cost of funds is high, competition is fierce, and the pressure to deliver return on equity in the high teens is relentless.

Bajaj Housing Finance made a fundamentally different bet. They chose the most boring, most competitive, and — crucially — the safest segment of the mortgage market: prime salaried home loans. These are loans to people with steady jobs at established companies, buying homes for personal use, with pristine credit scores and verifiable income. The yields on these loans are thin — around eight to nine percent in an environment where the cost of funds for a well-rated housing finance company sits around seven to seven and a half percent. The spread is a razor-thin one hundred to one hundred and fifty basis points. Critics asked the obvious question: why fight banks for scraps?

The answer lies in a concept that Bajaj Finance has perfected across its consumer lending business — customer lifetime value. A prime salaried borrower who takes a home loan is not just a mortgage customer. That borrower has a stable income, a demonstrated willingness to take on and service debt, and a long financial life ahead. Once inside the Bajaj ecosystem, that customer becomes a candidate for insurance products, personal loans, credit cards, wealth management services, and more. The home loan is not the product. The home loan is the acquisition channel.

Think of it as the Costco model applied to financial services. Costco sells rotisserie chickens at a loss — roughly five dollars each — because the chicken gets people into the store, and once they are inside, they buy everything else at healthy margins. Bajaj Housing Finance's prime home loan is the rotisserie chicken. The margins on the mortgage itself may be modest, but the customer acquisition cost is subsidized by the lifetime value of keeping that customer in the Bajaj financial ecosystem. Bajaj Finance, the parent, cross-sells multiple products to housing finance customers, creating a compounding revenue stream that more than compensates for the thin mortgage spread.

This strategy also has a profound risk management benefit. Prime salaried borrowers, almost by definition, represent the lowest credit risk in the lending pyramid. Their incomes are predictable, their employment is stable, and their repayment behavior is excellent. This is why Bajaj Housing Finance's gross NPA ratio has hovered in the range of 0.25 to 0.30 percent — a figure so low that it borders on the implausible for a fast-growing lender. For comparison, even HDFC Limited, the gold standard of Indian housing finance before its merger with HDFC Bank, typically ran gross NPAs of around one to one and a half percent. LIC Housing Finance sits north of three percent. The gap is not marginal. It is structural.

The technology underpinning this strategy deserves its own discussion. India's digital public infrastructure — what the industry calls the "India Stack" — has transformed how financial products are underwritten and delivered. Aadhaar-based biometric verification, electronic KYC, the Account Aggregator framework that allows lenders to pull a borrower's bank statements digitally with their consent, e-signatures, e-stamping, digital property record verification — all of these components existed by the time Bajaj Housing Finance launched. Unlike legacy lenders who had to retrofit their processes for the digital age, Bajaj built its entire operation on top of this stack from day one.

The result is the "E-Home Loan" — a process that delivers a digital sanction letter within ten minutes of a customer submitting their application. Not ten business days. Not ten hours. Ten minutes. The customer applies online, the system pulls their credit bureau data, verifies their income through the Account Aggregator, assesses the property through digital valuation models, and produces a conditional sanction. Full disbursal can happen within forty-eight hours of document verification. For a customer used to the traditional mortgage experience — multiple branch visits, photocopying stacks of documents, waiting weeks for approval — this is a revelation.

Behind the customer-facing simplicity lies a sophisticated hub-and-spoke credit model. Local branch teams handle customer relationships and property verification, but credit decisions are centralized and algorithmic. This separation of origination from underwriting is a hallmark of the Bajaj Finance operating model — it prevents the conflicts of interest that arise when the person approving the loan is also the person compensated for originating it.

The home loan book, as of September 2025, constituted approximately fifty-five percent of total assets under management. It is the anchor — the foundation of stability around which higher-yielding products are layered.

IV. Management and Culture

In March 2002, a young man with an MBA in finance from Punjabi University walked into the Bajaj Finance branch in Lucknow, Uttar Pradesh, and started work as a branch manager. His name was Atul Jain. He was thirty-one years old. He had previously worked brief stints in investment banking at PNB Capital Services and Prudential Capital Markets — roles that, by any measure, did not telegraph the career trajectory that would follow.

For four years, Jain managed branches in Lucknow and Delhi — the frontline of consumer lending, where you learn the business not from spreadsheets but from sitting across the table from borrowers, understanding why people pay and why they default. In 2006, he was moved to a role that would prove far more formative: National Collections Manager. If lending is the art of saying yes, collections is the art of dealing with the consequences when things go wrong. For three years, Jain's world was delinquent accounts, recovery strategies, and the granular mechanics of credit loss. He learned, at the most visceral level, what happens when underwriting fails.

From 2009 onward, his career at Bajaj Finance became a progression through risk management — Chief Collections Officer, President of Rural Lending and Collections, and finally Enterprise Risk Officer. Over eleven years, he sat at the intersection of credit and operations, developing an intimate understanding of how consumer credit portfolios behave through economic cycles, regulatory changes, and market disruptions. By the time Bajaj Finance's leadership tapped him to build the housing finance subsidiary in March 2018, Jain had spent sixteen years inside the organization. He was not a founder in the entrepreneurial sense. He was a "lifer" — a professional manager who had been forged in the Bajaj system and who embodied its credit-first culture.

This distinction matters enormously for understanding how Bajaj Housing Finance operates. Atul Jain's compensation, as disclosed in regulatory filings, was approximately sixteen crore rupees annually — roughly 1.9 million US dollars. This is substantial by Indian corporate standards but modest for the CEO of a company with a market capitalization that briefly exceeded one lakh crore rupees. More significantly, he held zero direct equity in Bajaj Housing Finance at the time of the IPO. His compensation was almost entirely salary and cash-based, with no stock options or equity grants of the kind that are standard at comparable financial services companies globally.

What does this tell us? It suggests a culture of professional stewardship rather than founder-style wealth creation. Jain is executing a mandate defined by the parent company's vision, not gambling for a personal fortune tied to the stock price. The incentive is to build sustainably, to protect the balance sheet, to never make a decision that trades long-term asset quality for short-term growth. In an industry where several housing finance companies blew up precisely because their promoters prioritized growth and personal enrichment over prudent lending, this alignment — or more precisely, this absence of misalignment — is quietly powerful.

Above Jain in the organizational hierarchy sits Sanjiv Bajaj as Chairman. Sanjiv does not run the day-to-day operations of the housing finance company, but his strategic imprint is unmistakable. He has publicly stated that "for India to realise its full potential, the country will need another ten Bajaj Finances and ten HDFC Banks." This is not modesty masquerading as ambition. It is a genuine belief that India's financial services market is so vast that success is not zero-sum. The strategic DNA he has instilled across Bajaj Finserv — consumer-first digital approach, relentless focus on data, cultural emphasis on innovation within disciplined frameworks — permeates every level of the housing finance subsidiary.

The operating culture at Bajaj Finance, and by extension at Bajaj Housing Finance, is legendarily intense. Weekly business reviews are exhaustive affairs where every metric is scrutinized — disbursement volumes, portfolio quality, customer complaints, process turnaround times, cost ratios. The operative philosophy can be summarized simply: if it is not in the dashboard, it did not happen. Anecdotes from former employees describe a culture where the rigor of the review process forces radical transparency. Problems cannot be hidden, and excuses are not tolerated. It is not a comfortable culture. It is, however, an effective one. The results — industry-leading asset quality, rapid scaling without deteriorating credit standards, operational efficiency ratios that improve even as the business grows — speak for themselves.

The leadership bench beyond the top is worth noting. The Chief Financial Officer, Gaurav Kalani, oversees a balance sheet that has grown from effectively zero to over one lakh crore rupees in seven years. The Chief Risk Officer, Niraj Adiani, manages the underwriting and risk framework. Vipin Arora, as Senior Executive Vice President of CRE (Commercial Real Estate), oversees the critical lease rental discounting business. The entire leadership team is drawn from within the Bajaj ecosystem, reinforcing a cultural continuity that is rare in fast-growing organizations.

V. Capital Deployment: The Anti-Acquisition Strategy

In the annals of Indian financial services, growth by acquisition is practically a default playbook. Kotak Mahindra Bank bought ING Vysya Bank. ICICI Bank absorbed Bank of Rajasthan. IndusInd Bank purchased Bharat Financial Inclusion. The logic is straightforward: buying an existing institution gives you branches, customers, a loan book, and market share in a single transaction. The downside, of course, is that you also buy the acquired company's culture, its legacy systems, its hidden skeletons, and its problem loans — often at a premium of three to four times book value.

Bajaj Housing Finance has taken the diametrically opposite approach. As of this writing, the company has made zero major acquisitions. Not one portfolio purchase, not one entity absorption, not one bolt-on deal. Every rupee of its one-lakh-plus-crore loan book has been originated organically — loan by loan, customer by customer, property by property.

The economics of this choice are worth examining. When you acquire a housing finance company or portfolio at, say, three times book value, you are paying three rupees for every rupee of net assets. You then need the acquired book to deliver outsized returns to justify that premium, which often means you are inheriting risk you did not underwrite. When you build organically, you are deploying capital at roughly one times book value, plus operating expenses. Every loan on your books was underwritten by your team, using your algorithms, applying your credit standards. The quality assurance is built in from origination, not bolted on after the fact through integration.

To fund this organic growth, Bajaj Housing Finance has relied on a combination of parent company capital infusions and market borrowings. In 2019, the company raised two thousand crore rupees through rights issues subscribed by Bajaj Finance. In 2020, another fifteen hundred crore followed. These were not public fundraising events — they were capital injections from the parent, essentially Bajaj Finance writing checks to fuel its subsidiary's growth engine.

The September 2024 IPO represented a new chapter in the capital story. The offering included a fresh issue component of approximately thirty-five hundred and sixty crore rupees — new capital flowing into the company, not exits for existing shareholders. This was growth fuel, not a liquidity event for insiders. The IPO also included an offer-for-sale component, primarily by Bajaj Finance, reducing its holding from a hundred percent to about roughly eighty-eight and a half percent. Even after the partial sale, Bajaj Finance retained overwhelming control. The message to the market was clear: we are not selling the company. We are bringing in public shareholders as partners for the next leg of growth, and we are raising capital to deploy into a market we believe is just getting started.

The total assets of the company stood at approximately one lakh three thousand crore rupees as of the end of fiscal 2025, funded by a combination of equity — roughly twenty thousand crore rupees — and debt of approximately eighty-two thousand crore rupees. The debt is overwhelmingly in the form of term loans and non-convertible debentures from banks and institutional investors. The company's AAA credit rating from CRISIL and ICRA — the highest possible — ensures that it can borrow at rates close to the sovereign benchmark, a critical competitive advantage in a spread-based business where even twenty-five basis points on the cost of funds translates directly to the bottom line.

VI. The Hidden Businesses: Beyond Home Loans

Investors who look at Bajaj Housing Finance and see only a mortgage lender are missing at least half the story. While home loans to individual borrowers constitute the majority of the book — approximately fifty-five percent as of September 2025 — the remaining forty-five percent is allocated across three distinct businesses, each with very different risk-return characteristics and strategic rationale.

Loans Against Property make up roughly ten percent of the portfolio. This product involves lending against existing real estate — a borrower owns a property, pledges it as collateral, and receives a loan for business or personal purposes. The yields here are meaningfully higher than on home loans, typically one hundred to two hundred basis points above the home loan rate, because the end-use is not standardized housing purchase but rather business expansion, working capital, or personal needs. The risk is modestly higher, but the loan is fully secured by tangible real estate. For investors, this segment is the "juice" — it is where the return on equity comes from, providing higher margins on a secured asset base.

Lease Rental Discounting, or LRD, represents approximately twenty-two percent of the book and is perhaps the most intellectually interesting part of the business. LRD is a product designed for owners of commercial real estate — think office buildings leased to blue-chip tenants like Google, Amazon, Infosys, or TCS. The owner of such a property approaches Bajaj Housing Finance and says: I have a lease agreement with a multinational corporation that guarantees rental income of, say, five crore rupees per year for the next ten years. I want to borrow against that predictable future cash flow. Bajaj Housing Finance evaluates the lease, assesses the creditworthiness of the tenant (not just the property owner), and extends a loan that is essentially collateralized by both the physical property and the contracted rental stream.

The beauty of LRD lies in its risk profile. When the tenant paying the rent is a Fortune 500 company or a large Indian IT services firm, the probability of rental default is extremely low. The property itself provides additional security. And the ticket sizes are large — often hundreds of crore rupees per transaction — which means Bajaj Housing Finance can deploy significant capital with relatively low origination costs per rupee lent. This is a high-ticket, low-risk corporate game that sits quietly in the portfolio, generating stable returns without the volatility associated with retail lending. Most retail investors have never heard of LRD, and very few analysts discuss it in detail, but it is arguably the segment that gives Bajaj Housing Finance its distinctive character among peers.

Developer Finance makes up around twelve percent of the book. This is the segment where risk is highest and where the company treads most carefully. Developer finance involves lending to real estate developers for construction — effectively financing the building of residential and commercial projects before the units are sold to end buyers. In the Indian context, this segment carries memories of spectacular failures. DHFL, IL&FS, and several other institutions blew up partly because their developer finance books turned toxic when the real estate cycle turned.

Bajaj Housing Finance has been deliberate about keeping this segment contained — never exceeding roughly twelve to thirteen percent of the total book. The strategic rationale, however, goes beyond the interest income. When you finance a developer's project, you gain first access to the home buyers in that project. Every apartment that a Bajaj-financed developer sells represents a potential home loan customer for Bajaj Housing Finance. The developer loan is, in a sense, a customer acquisition investment — it feeds the retail home loan funnel. This vertical integration of the construction lending and retail mortgage pipeline is a subtle but powerful competitive advantage that most pure-play home loan providers cannot replicate.

The newest initiative — branded "Sambhav," which translates to "possible" — represents Bajaj Housing Finance's push into affordable housing. Launched with the tagline "Karein Har Ghar Mumkin" (Making Every Home Possible), Sambhav targets a dramatically different customer segment: micro-entrepreneurs, informal sector workers, economically weaker sections, and lower-income households. These are borrowers who may not have formal salary slips or tax returns, whose income documentation is limited or non-existent, and who have traditionally been shut out of the formal mortgage market.

The Sambhav business unit was established roughly eighteen months ago and has already scaled to monthly disbursements of three hundred and twenty-five to three hundred and fifty crore rupees. The minimum income requirement starts at just ten thousand rupees per month. Borrowers can access loans with or without formal income proof, and the product integrates with the Pradhan Mantri Awas Yojana Urban 2.0 — the government's flagship affordable housing subsidy scheme.

This is Bajaj Housing Finance's bet on moving beyond "India" — the urban, salaried, digitally savvy demographic — to "Bharat" — the vast, semi-urban, informal-economy population that represents the majority of the country. The risk profile is different, the economics are different, and the operational challenges are entirely different. Whether Bajaj can apply its data-driven credit culture to a segment where traditional underwriting signals barely exist will be one of the most important questions for the company over the next five to ten years.

VII. Competitive Advantage Through the Lens of Strategy

To understand whether Bajaj Housing Finance's advantages are durable, it helps to analyze them through Hamilton Helmer's Seven Powers framework — the strategic moats that create persistent differential returns.

Scale Economies (Shared) represent perhaps the most obvious structural advantage. Bajaj Housing Finance does not operate as a standalone entity in any meaningful sense. It shares the cost infrastructure — human resources, information technology, legal, compliance, office space — with its parent, Bajaj Finance, which is one of India's largest NBFCs with over a hundred million customers. The IT platform, the data analytics engine, the credit bureau integrations, the customer relationship management systems — all of these were built and paid for by Bajaj Finance. The housing finance subsidiary gets to ride on this infrastructure at marginal cost. A standalone housing finance company with a one-lakh-crore book would need to build all of this from scratch, spreading the cost over a much smaller revenue base. This shared cost structure gives Bajaj Housing Finance an operating expense ratio that standalone competitors simply cannot match.

Process Power is the second major advantage. Over sixteen years, Bajaj Finance has refined its underwriting algorithms, its collections processes, its fraud detection systems, and its customer onboarding workflows through millions of lending transactions. Bajaj Housing Finance inherited these processes and adapted them for mortgage lending. The hub-and-spoke credit model, the separation of origination from underwriting, the digital-first customer journey, the ten-minute sanction process — these are not features that can be replicated by hiring a few technology consultants. They represent years of iterative refinement embedded in organizational systems and culture.

Brand is the third power, and in the Indian context, it carries unusual weight. The financial services landscape in India was scarred by the NBFC crisis of 2018-2019. Customers lost money in DHFL. Investors were burned by IL&FS. The trust deficit in the financial sector was palpable. In this environment, the "Bajaj" brand — backed by a century-old industrial group, a publicly listed parent with a strong regulatory track record, and AAA credit ratings — functions as a trust signal that smaller or newer competitors cannot replicate. When a salaried professional in Mumbai or Bangalore is choosing between a Bajaj home loan and an offer from a lesser-known housing finance company, the brand provides comfort that has real economic value in the form of lower customer acquisition costs and higher conversion rates.

Looking at the competitive landscape through Michael Porter's Five Forces provides additional perspective. The threat of new entrants is high in Indian housing finance — the licensing barrier is relatively low, and the government actively encourages more players to expand housing credit. However, the capital requirements are enormous, and building the credit culture and technology infrastructure takes years. The bargaining power of buyers (borrowers) is significant because home loans are largely commoditized — a home loan from Bajaj is functionally identical to one from SBI or HDFC Bank, and borrowers are increasingly price-sensitive thanks to aggregator platforms. The bargaining power of suppliers (providers of capital) favors well-rated players — Bajaj's AAA rating gives it access to the cheapest debt in the market. Rivalry among existing competitors is intense, with public sector banks holding nearly forty-seven percent of the housing loan market and private banks and HFCs fighting for the rest. Finally, the threat of substitutes — in this case, alternative sources of home financing like self-funding, family borrowing, or government schemes — is moderate and declining as India's housing market formalizes.

The counter-positioning argument is particularly compelling. Against banks, Bajaj Housing Finance positions itself as faster, more digital, and more service-oriented. Against other housing finance companies, it positions itself on cost of funds — its AAA rating allows it to borrow at rates that mid-tier HFCs simply cannot access. Against both, it offers the Bajaj ecosystem as a differentiator — the promise of a broader financial relationship, not just a mortgage.

The most important competitive question, however, concerns the two elephants in the room. HDFC Bank, post-merger, is the undisputed behemoth of Indian housing finance. It has the largest branch network, the deepest customer base, and the legacy of HDFC Limited's decades of mortgage expertise. It can price loans at rates that are difficult for any NBFC to match because its cost of funds — largely sourced from low-cost current and savings account deposits — is structurally lower than what any housing finance company pays in the bond market. Jio Financial Services, backed by Mukesh Ambani's Reliance empire, represents the other threat — a tech-first financial services platform with potentially transformative distribution capabilities through Jio's four-hundred-million-plus telecom subscriber base. Neither of these competitors has fully deployed their strategies in housing finance, but their mere presence on the horizon keeps the competitive pressure elevated.

VIII. Bull Case and Bear Case

The case for optimism rests on several reinforcing pillars. India's housing cycle is arguably in its early innings. After a decade-long correction that began in 2013, residential real estate prices across most Indian cities started recovering in 2021 and 2022, supported by low interest rates, government incentives, regulatory reform through RERA, and pent-up demand from a population where seventy percent of people are under the age of forty. Mortgage penetration at eleven percent of GDP is less than half of China's level and a quarter of the developed-market average. Even conservative estimates project the mortgage market growing at twelve to fifteen percent annually for the next decade.

Within this growing market, Bajaj Housing Finance is demonstrably taking share. Its assets under management grew twenty-six percent year-over-year in fiscal 2025, outpacing the overall market growth rate by a wide margin. The company's revenue has grown from approximately thirty-two hundred crore rupees in fiscal 2021 to over nine thousand crore in fiscal 2025 — a nearly three-fold increase in four years. Net income has followed a similar trajectory, rising from roughly four hundred and fifty crore to over two thousand one hundred and sixty crore over the same period. These are not incremental gains. This is market share conquest at scale.

Operating leverage is beginning to materialize. As the loan book grows, certain costs — technology infrastructure, compliance frameworks, brand building — are relatively fixed. The cost-to-income ratio has improved, and the company's medium-term target of an operating expenses to net income ratio of fourteen to fifteen percent suggests confidence that efficiency gains will continue as the book scales further.

The asset quality story is the crown jewel of the bull case. A gross NPA of approximately 0.28 percent and a net NPA of around 0.12 percent are not just good — they are exceptional by any global standard for a mortgage lender growing at this pace. The company's medium-term GNPA target of 40 to 60 basis points provides a buffer, implicitly acknowledging that asset quality may normalize somewhat as the book seasons and as the Sambhav affordable housing portfolio scales. But even at the upper end of that target range, the credit costs would be well below industry averages.

The case for caution is equally substantive. Valuation is the most obvious concern. Despite the recent correction from its post-listing highs, Bajaj Housing Finance still trades at a price-to-book ratio that embeds significant growth expectations. This is a company where the stock has retraced below its listing day levels — the year high of nearly one hundred and thirty-seven rupees versus the current price around eighty-two — suggesting that the market is recalibrating its willingness to pay for future growth. At these multiples, the margin for error is thin. If growth slows, if asset quality deteriorates, or if competitive pressure compresses margins, the stock has limited downside support from valuation floors.

Competition is the second risk. HDFC Bank, with its structural cost-of-funds advantage from deposit-based funding, can always undercut any NBFC on pricing. The question is whether it will choose to compete aggressively on price or maintain its margins — but the optionality sits with HDFC Bank, not with Bajaj Housing Finance. Jio Financial Services remains a wildcard. While it has not yet made a significant move into housing finance, its technology platform and distribution reach through Reliance's digital ecosystem could disrupt customer acquisition economics for the entire industry.

Regulatory risk is real, though indirect. The Reserve Bank of India has been progressively tightening prudential norms for NBFCs, including enhanced capital requirements, more stringent provisioning standards, and increased compliance obligations under the Scale-Based Regulation framework. Bajaj Housing Finance is classified as an "Upper Layer" NBFC, subjecting it to the most demanding regulatory requirements. While the company is well-capitalized and compliant, any future regulatory changes — such as risk-weight adjustments, restrictions on lending to certain segments, or changes to the definition of NPAs — could affect growth trajectory or profitability.

Net interest margin compression is the final bear case factor. As Bajaj Housing Finance grows, it will increasingly compete for the same prime salaried borrowers that every bank in India wants. The competitive pressure on home loan rates has been relentless — several banks and HFCs have cut rates to attract market share, and the spread between the best available rate and the average rate has narrowed considerably. If the cost of borrowing does not decline proportionally — and with the RBI maintaining a cautious monetary policy stance, it may not — margins will come under pressure.

Key Performance Indicators to Watch: For investors tracking this company going forward, three metrics matter above all others. First, AUM growth rate — the company has guided for 21-23 percent growth in fiscal 2026, down from 26 percent in fiscal 2025; any further deceleration would signal competitive headwinds or a strategic shift toward quality over growth. Second, Gross NPA ratio — currently at 0.26-0.29 percent with a medium-term target of 0.40-0.60 percent; the trajectory of this number, particularly as the Sambhav affordable book seasons, will reveal whether the credit culture holds as the customer mix changes.

IX. Conclusion: Corporate Intrapreneurship at Scale

Bajaj Housing Finance is, at its essence, a test case for a question that every large corporation in the world grapples with: can a century-old conglomerate build a new business from scratch with the speed and intensity of a startup, while maintaining the discipline and risk management of an established institution?

The evidence, seven years into the experiment, is remarkably positive. A loan book built from zero to over one lakh crore rupees. Asset quality that is the best in the industry by a wide margin. Technology infrastructure that enables ten-minute loan sanctions. A brand that generates trust in a market scarred by institutional failures. A management team that has been forged inside the system, incentivized to build sustainably rather than to gamble for a windfall. And a parent company that provides shared infrastructure, capital support, and customer cross-sell opportunities that no standalone housing finance company can replicate.

The September 2024 IPO was a powerful validation of this model. The sixty-seven-times oversubscription and the listing-day surge reflected the market's belief that Bajaj Housing Finance is not just another mortgage lender — it is a platform being built to capture a structural, multi-decade opportunity in Indian housing.

But validation and valuation are different things. The stock's decline from its post-listing peak to levels below its listing-day close is a reminder that even the best businesses can be poor investments if purchased at the wrong price. The competitive landscape — HDFC Bank's scale, Jio Financial's ambitions, the relentless pricing pressure from public sector banks — ensures that nothing about this market will be easy.

India's mortgage market is on the cusp of an expansion unlike anything the country has ever seen. The demographic tailwinds — a young population, rapid urbanization, rising incomes, formalization of the economy — are powerful and durable. The question is not whether the market will grow. It is whether Bajaj Housing Finance can maintain its execution edge as it scales into this growth, whether the credit culture that has produced 0.28 percent gross NPAs can survive the push into affordable housing and the pressures of competitive pricing, and whether the Bajaj Finserv flywheel will keep spinning fast enough to justify the market's expectations.

What is clear is this: Bajaj Housing Finance has done something that very few corporate subsidiaries anywhere in the world have done. It has taken a dormant shell company, infused it with an established credit culture and a world-class technology platform, launched it into a fiercely competitive market at exactly the right cyclical moment, and built a franchise that the market values at tens of billions of dollars — all without a single acquisition, all within the span of one economic cycle. Whether you call that intrapreneurship, corporate strategy, or simply excellent execution, it is a story worth studying. The first chapter is written. The next several will determine whether this hundred-year startup becomes a hundred-year franchise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube