Bajaj Consumer Care: The "Almond Drops" Hegemony and the Pivot to Professionalism

I. Introduction: The Billion-Dollar Bottle

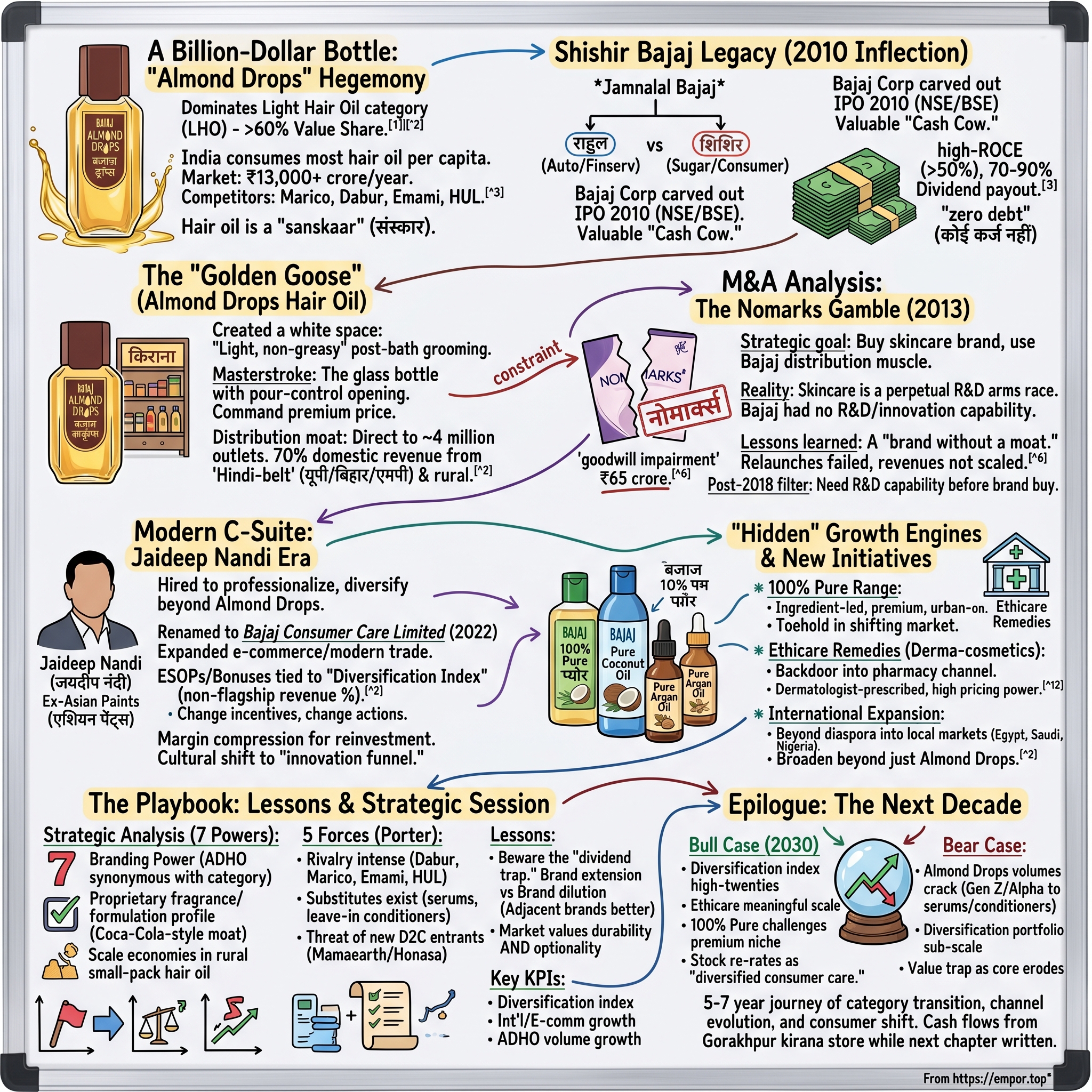

Picture a typical morning scene anywhere across the हिंदी पट्टी Hindi heartland—from a गांव village in eastern Uttar Pradesh to a middle-class flat in Indore. A teenager sits cross-legged on the floor while her grandmother tilts a tall, narrow glass bottle over an open palm. Out comes a thin, golden stream of oil, smelling faintly of almonds and roses. The ritual is so old it predates television, so universal that it has its own catchphrase in Bollywood comedies—"बजाज बादाम तेल लगाओ apply Bajaj almond oil"—deployed whenever a character does something so foolish that, the joke runs, their brain must be running low.

That bottle—बजाज बादाम ड्रॉप्स Bajaj Almond Drops, abbreviated by analysts simply as ADHO—is the entire reason Bajaj Consumer Care Limited exists as a listed company. One product, one fragrance, one glass-bottle silhouette, sitting on shelves in over a hundred million Indian households. Bajaj Consumer Care has held more than half of India's हल्के बालों का तेल light hair oil category by value for the better part of two decades, with the company's own filings repeatedly putting Almond Drops above the 60% mark in its sub-segment.[^1][^2]

To understand why this matters, you have to understand the Indian hair oil category itself. India consumes more hair oil per capita than any other country on earth. The बालों का तेल hair oil market in India is worth somewhere north of ₹13,000 crore annually, dominated by मैरिको Marico, डाबर Dabur, इमामी Emami, हिंदुस्तान यूनिलीवर Hindustan Unilever, and Bajaj Consumer.1 In most countries, hair oil is a niche; in India, it is a संस्कार sanskaar—a sacrament. Mothers oil daughters' hair before exams. Grandmothers oil grandchildren's hair before weddings. It is one of the few FMCG categories on earth that is both a daily-use convenience and a generational tradition.

Within that vast ocean, Bajaj Consumer Care does one thing extraordinarily well, and—as this episode will explore—has spent the last decade trying, with mixed results, to do anything else.

The roadmap from here: we trace how a junior branch of the legendary बजाज Bajaj industrial family ended up with a glass bottle of almond-scented mineral oil; how that single SKU was financially engineered into one of the highest-ROCE FMCG businesses on Indian markets; how a 2013 acquisition called Nomarks taught the entire industry a brutal lesson about brand extension; how a former Asian Paints executive named Jaideep Nandi was brought in to professionalize the place; and finally, the high-stakes diversification chess game playing out across e-commerce, derma-cosmetics, and the Middle East as we record this in mid-2026.

It is, in many ways, the most Indian of business stories—a tale of परिवार family, कैश cash, and the brutal arithmetic of trying to build a second act.

II. The Shishir Bajaj Legacy & The 2010 Inflection

To understand Bajaj Consumer Care, you have to first understand that "Bajaj" in India is less a company name than a clan. The patriarch was जमनालाल बजाज Jamnalal Bajaj, the freedom fighter and confidante of महात्मा गांधी Mahatma Gandhi, who built the original trading and manufacturing house in the 1920s. By the time his grandsons were running things in the 1990s, the empire stretched from two-wheelers (बजाज ऑटो Bajaj Auto) to finance (बजाज फिनसर्व Bajaj Finserv) to sugar to home appliances—a true Indian संगठित घराना industrial house in the classical mould.

What is now Bajaj Consumer Care grew out of a much older sugar-and-trading arm. The hair oil business itself traces its origins to the 1950s, when the family began marketing a light, almond-fragranced mineral-oil-based formulation under the Bajaj brand. For decades it sat as a low-glamour cash generator inside Bajaj Hindusthan Sugar.

The pivotal moment came in 2008 with a formal family settlement. The Bajaj clan, like most large Indian business families, eventually had to split. राहुल बजाज Rahul Bajaj's branch took the iconic two-wheeler and financial services businesses; his cousin शिशिर बजाज Shishir Bajaj, who had run the sugar and consumer side, took those operations. The hair oil business was carved out into a standalone listed entity called Bajaj Corp.

Why does this corporate genealogy matter for an investor? Because it explains the company's defining characteristic: a controlling family that had been separated from the more glamorous parts of the empire, with a strong financial incentive to milk the one crown jewel they had inherited.

That crown jewel listed on the भारतीय राष्ट्रीय शेयर बाज़ार National Stock Exchange of India (NSE) and the BSE in August 2010, with an IPO that priced the shares at ₹660 each in a band that valued the company at roughly ₹1,950 crore.[^4] The issue was subscribed multiple times over. Public markets had never seen anything quite like it: a single-product FMCG company with operating margins north of 30%, virtually zero debt, and a working-capital cycle so tight that suppliers were effectively financing the business.

The early 2010s became the company's "cash cow" phase, a period that institutional investors still reminisce about with a kind of nostalgic awe. Return on Capital Employed regularly exceeded 50%. Dividend payout ratios hovered around 70–90% of net profit.[^5] The reason was almost embarrassingly simple: making hair oil from light liquid paraffin and fragrance compounds in a tax-advantaged factory in Himachal Pradesh required almost no capital. Once the brand had been built, the marginal cost of an extra bottle was a few rupees of input plus distribution. Everything else dropped to the bottom line and most of it went straight back to shareholders.

For long-term investors, that period embedded a kind of dividend-trap thinking inside the company. When you have a business this profitable, this stable, with कोई कर्ज नहीं zero debt and a fanatically loyal customer base, the question becomes not "where should we reinvest?" but "how fast can we send the cash back to promoters?" That bias would, by the late 2010s, become the company's most expensive habit. The seeds of the diversification problem were planted in those very golden years.

III. The Golden Goose: Almond Drops Hair Oil

To appreciate the genius of Almond Drops, you have to mentally walk into a किराना kirana store in, say, Gorakhpur in 1995. The hair oil shelf is dominated by two formats. On one side, the great national giants of coconut oil—पैराशूट Parachute from Marico, डाबर वाटिका Dabur Vatika—heavy, fragrant, leaving hair flat and slightly sticky to the touch. On the other side, the slowly-emerging "value-added" oils—amla, hibiscus, jasmine—usually in plastic bottles, usually positioned as therapeutic.

What was missing was a category that did not yet have a name: a light, non-greasy hair oil for the post-bath grooming moment rather than the pre-bath champi (head massage) ritual. Something a college-going daughter or an office-going son could put on after a shower, before stepping out into the dust of Lucknow or Patna, without looking like they had dunked their head in a ghee bowl.

This is the white space Almond Drops occupied, and the strategic move was almost a sleight of hand. Almond Drops is not, in any meaningful sense, almond oil. The bulk of the formulation is light liquid paraffin—a refined petroleum derivative—plus a small amount of sweet almond oil, vitamin E, and a proprietary fragrance.[^1] But by associating the product with almonds, which in Indian cultural memory are the food you feed children to make them smart and beautiful, Bajaj engineered something extraordinary: a premium-positioned, premium-priced product with the cost structure of a commodity.

Then came the masterstroke—the glass bottle. While every competitor was racing to plastic to cut costs and reduce breakage, Bajaj insisted on the tall, slender glass bottle with the distinctive pour-control opening that lets you dispense just a few drops at a time. The glass communicated luxury, the drop-by-drop pour communicated concentration—you don't need much because each drop is precious—and the overall package commanded a price premium of roughly 50–80% per millilitre over generic almond oils sitting next to it on the same shelf.

The category Bajaj effectively created became known in industry parlance as the Light Hair Oil category, or LHO. By the mid-2010s, Almond Drops had cornered over 60% of LHO by value, and Bajaj's investor presentations regularly carried that number as a kind of moat-trophy.[^1][^2] Competitors tried repeatedly—डाबर Dabur with Dabur Almond Hair Oil, इमामी Emami with 7 Oils in One light variants—and consistently failed to break the 15-20% ceiling in any geography.

But the deeper moat was distribution. Bajaj built a सीधा वितरण direct distribution network that reaches more than four million retail outlets across India, with deep penetration in the geographies where Almond Drops over-indexes: Uttar Pradesh, Bihar, Madhya Pradesh, Jharkhand, Chhattisgarh, and the smaller towns of Maharashtra and Gujarat. Roughly 70% of the company's domestic revenue comes from these Hindi-belt and rural markets—a fact that has been both a source of resilience and a long-term strategic constraint.[^2]

Resilience, because rural distribution moats in India are genuinely hard to replicate. They depend on relationships with sub-stockists and दुकानदार shopkeepers built over decades, credit terms that the giant MNCs are often unwilling to extend, and a willingness to deliver tiny SKUs—the ₹1 sachet, the ₹10 mini-bottle—that the global players consider too uneconomical to bother with.

Constraint, because the same Hindi-belt consumer who is loyal to a ₹50 bottle of Almond Drops is precisely the consumer least likely to trade up to a ₹400 anti-blemish cream or a ₹600 hair serum. The very moat that protects the core business has, over time, become the wall that keeps the company from moving into the higher-margin segments it desperately wants to enter.

Which sets up the most expensive lesson in the company's history.

IV. M&A Analysis: The Nomarks Gamble

By 2013, the cash had been piling up. Three years post-IPO, with operating margins still above 30% and the dividend payout ratio elevated, Bajaj's board faced the same question every single-product FMCG faces eventually: what is Act Two?

The answer, announced in August 2013, was an acquisition that on paper made perfect sense and in execution would haunt the company for the next decade. Bajaj Corp acquired the नोमार्क्स Nomarks brand from Ozone Ayurvedics for roughly ₹140 crore.2 Nomarks was a small but genuinely interesting franchise—an anti-marks, anti-blemish range with herbal positioning, popular among college-going women in tier-2 and tier-3 cities, with a then-decent presence in the modern trade channels of metropolitan India.

The strategic logic was elegant. Bajaj had distribution muscle but no skincare brand. Ozone had a credible skincare brand but limited distribution. Plug Nomarks into the Bajaj sales network and you had—theoretically—an instant Number Three player in the highly fragmented Indian anti-blemish category, behind Hindustan Unilever's Fair & Lovely (now Glow & Lovely) and Emami's Fair and Handsome.

The deal multiple looked reasonable at the time. ₹140 crore for a brand reportedly doing around ₹40-50 crore of revenue worked out to roughly 3x trailing sales—not cheap, not outrageous, certainly cheaper than इमामी Emami's subsequent acquisition of केश किंग Kesh King from एसबीएस बायोटेक SBS Biotech in 2015 for ₹1,651 crore at a substantially richer multiple.3 Industry comparisons suggested Bajaj had not overpaid in nominal terms.

What the deal multiple did not capture was the unforgiving R&D physics of the Indian skincare market. Hair oil is, fundamentally, a low-innovation category—the formulation Bajaj sells in 2026 is barely different from the one it sold in 1996. Skincare is the opposite. Anti-blemish, anti-acne, anti-marks is a perpetual arms race of actives, peptides, and clinical-sounding claims, fought by Hindustan Unilever and Procter & Gamble and L'Oréal and Beiersdorf with R&D budgets that dwarf Bajaj's entire annual profit pool. Plus an entire generation of Korean-influenced niche brands—The Ordinary, Minimalist, Plum, Mamaearth—that emerged from 2018 onwards and ate the entire mass-skincare value chain from above.

By 2016-17, it was clear something was wrong. Nomarks revenues had not scaled in the way the acquisition thesis had assumed. The brand was repeatedly relaunched, reformulated, repackaged. Marketing spends ran higher than the segment could justify. In 2018, the company took a goodwill impairment hit on Nomarks of roughly ₹65 crore, an admission that nearly half the acquisition value had evaporated.[^8]

The post-mortem became required reading for an entire generation of Indian FMCG dealmakers. The diagnosis: Bajaj had bought a brand whose value was deeply tied to ongoing R&D investment in a category Bajaj had no capability or culture to invest in. The selling shareholder had cashed out at the top; the buyer had inherited a brand that needed perpetual feeding it could not provide. It was, in retrospect, a classic "brand without a moat" purchase—the kind of deal a private equity model might have rejected on day one for lack of a defensible competitive position post-acquisition.

For the long-term investor reading the lesson today, the Nomarks chapter rewired how the market values brand acquisitions in Indian FMCG. Post-2018, the analyst community started routinely asking listed FMCG companies a question they had not asked before: do you have the R&D and innovation cadence to defend the brand you are about to buy? It is, in effect, a Bajaj-induced filter.

It also did something subtler. It convinced the controlling shareholder—by then कुशाग्र बजाज Kushagra Bajaj—that family management of a single-product, single-category business was no longer sufficient. The company needed someone who had run a modern, professional, multi-category consumer business. That conviction would, two years later, bring an outsider into the corner office for the first time in the company's history.

V. The Modern C-Suite: The Jaideep Nandi Era

The headhunt itself was telling. In 2019, the search briefs that went out to executive recruiters were unusually specific: the target was someone with consumer-goods experience, a track record of multi-category execution, and crucially, a background in premium rather than mass-market businesses. The brief was essentially looking for an executive who could teach Bajaj how to be premium without losing what made it dominant in the mass.

The name that emerged was जयदीप नंदी Jaideep Nandi, a longtime एशियन पेंट्स Asian Paints veteran who had most recently led the company's PPG-Asian Paints joint venture in India.4 Asian Paints, for context, is one of the most respected operating companies on the Indian stock market—a business celebrated for its supply-chain sophistication, its tinting-system technology that turned paint from a commodity into a customisable product, and its discipline around capital allocation. Bringing in an Asian Paints alumnus was, in itself, a signal to the institutional investor community: this company is serious about becoming a real FMCG operator, not just an Almond Drops cash machine.

Nandi joined as Managing Director in 2020, and the early days were genuinely difficult. The COVID-19 lockdowns devastated FMCG distribution in the geographies Bajaj depended on most—the dense neighbourhood किराना kirana stores of small-town India. Revenue declined and the company had to rebuild much of its primary-distribution muscle even as global supply chains for liquid paraffin and packaging glass were seizing up.

What Nandi did in those years revealed his playbook. First, the company was formally renamed from Bajaj Corp to Bajaj Consumer Care Limited in 2022, an explicit rebranding signal that the company saw itself as a multi-brand "consumer care" platform rather than a single hair-oil franchise.[^2] Second, the supply chain was overhauled with a sharper focus on direct-to-store reach, lower stockist inventory days, and a meaningfully expanded modern-trade and e-commerce coverage. Third—and most strategically important—the management's variable compensation was retooled.

This last piece deserves attention. Under the previous regime, KPIs had been overwhelmingly tied to top-line volume growth and absolute profit, both of which the Almond Drops engine delivered almost automatically. Under Nandi, ESOPs and performance bonuses were tied to what management began internally calling the "diversification index"—the share of revenue coming from products other than the flagship Almond Drops range.[^2] This is a small, technical detail that does enormous strategic work. When you change what executives are paid for, you change what they actually do.

Shareholding is another piece of the puzzle. The promoter family—principally the Kushagra Bajaj branch—has historically held in the 55-60% range, with the rest of the float distributed across mutual funds, foreign portfolio investors, and retail.5 Institutional holders, particularly domestic mutual funds with concentrated positions, have been vocal in pushing for professional oversight and clearer disclosure on the diversification roadmap. Proxy advisors such as IiAS (Institutional Investor Advisory Services) have repeatedly flagged related-party-transactions and royalty structures common to family-controlled Indian businesses, asking for tighter board independence and more granular segment reporting.6

The cultural shift inside the company is harder to capture in numbers but visible to anyone tracking quarterly investor calls. The vocabulary changed. Where management used to talk about "winning the share war in UP and Bihar," it began talking about "channel mix," "premium portfolio," "innovation funnel," and "international synergies." Some of this is, frankly, MBA theatre. But some of it is real. The company began running formal stage-gated innovation processes for new products. It started reporting e-commerce sales separately. It began participating in industry forums on premium personal care—forums where, ten years ago, no one from Bajaj would have shown up.

The transition came at a cost. Operating margins, which used to sit comfortably above 30%, compressed into the high teens and low 20s as marketing investment, digital spends, and new-product launches consumed the cushion that Almond Drops provided.[^2] To some long-time shareholders this looked like value destruction. To others, it looked like a company finally doing what it should have done a decade earlier.

The Nandi era's verdict, ultimately, will not be written in margin lines but in revenue mix. And that brings us to the actual products he has been building.

VI. "Hidden" Growth Engines & New Initiatives

Walk into a ब्लिंकिट Blinkit or ज़ेप्टो Zepto warehouse in suburban Bengaluru and you can see the new Bajaj taking shape on the dark-store shelves. Alongside the familiar Almond Drops bottle, you will find a cluster of products that did not exist in the company's lineup three years ago—stark white-and-pastel bottles under the बजाज 100% प्योर Bajaj 100% Pure sub-brand, including Pure Coconut Oil, Pure Argan Oil, Pure Castor Oil, and a handful of cold-pressed variants positioned for the urban, label-reading, ingredient-conscious consumer.[^2]

The 100% Pure range is interesting precisely because of what it is not. It is not designed to compete with Parachute in the giant coconut-oil market—that battle is unwinnable in the short term. It is designed to ride the "ingredient-led" cosmetics wave that swept urban Indian consumption from roughly 2020 onwards, where consumers actively seek out single-ingredient oils marketed on purity rather than fragrance. The economics are different too: these SKUs are priced at a premium, sold predominantly through modern trade and e-commerce, with negligible exposure to the rural distribution network that defines the legacy business.

This is, in a quiet way, a defensive move. If the Indian consumer's centre of gravity is shifting upward and online, having only an Almond Drops bottle on a shelf in a दुकान dukaan in Mau is not a future-proof position. The 100% Pure range gives the company a credible toehold in the urban-premium-online channel without requiring a wholesale rebrand of the mother franchise.

But the bolder move was Ethicare Remedies. In March 2023, Bajaj Consumer Care announced it would acquire the remaining 75% of Ethicare Remedies that it did not already own, having taken an initial 25% stake earlier.[^12] Ethicare is, in industry terminology, a "derma-cosmetics" company—it sells medicated and dermatologist-recommended skincare products through a pharmacy-led distribution model rather than through general trade.

To understand why this matters, you need to understand the bifurcation that has been quietly transforming Indian skincare. The mass-market end is being commoditised by digital-first D2C brands (mamaearth, Plum, WOW Skin Science) competing on social media. The truly premium end (L'Oréal Paris, Estée Lauder, Lakmé) is dominated by deep-pocketed multinationals. The interesting middle ground is the dermatologist-prescribed, pharmacy-distributed segment—products that doctors actively recommend, that carry a clinical halo, that command both pricing power and lower marketing intensity because the dermatologist's prescription does the selling.

This is where Ethicare plays. Acne treatments, hyperpigmentation creams, sensitive-skin moisturisers, sold through chemists rather than supermarkets. It is the same business model that has made गैल्डर्मा Galderma a global success and that has powered Cipla Health and Eris Lifesciences into pharma-FMCG hybrids. For Bajaj, Ethicare is a backdoor into a category where Nomarks failed—but this time through a fundamentally different distribution channel, with a fundamentally different brand-building logic where prescriptions, not advertising, do the work.

International expansion is the third leg. The company's overseas business has historically been concentrated in the Gulf Cooperation Council countries and parts of Africa, riding largely on the Indian diaspora, with sales clustered around the same Almond Drops product but at significantly higher price points in dollar terms. Under the new strategy, management has signalled an intent to broaden beyond diaspora consumers into local-population marketing in regions like Egypt, Saudi Arabia, and Nigeria, where light hair oils have a genuine cultural fit.[^2] Whether the company can do that without burning enormous amounts of capital on brand-building in unfamiliar markets remains the open question.

Add it all together and you get the revenue-mix arithmetic that defines the bull case. Today, the business is roughly 80-90% Almond Drops, with the remainder split across coconut oils, the 100% Pure premium range, Nomarks, Ethicare, and international. The stated medium-term ambition has been to move that to something closer to 75/25 within three years—getting non-ADHO revenue into the mid-twenties percentage of the total.[^2] That is a meaningful structural shift if achieved. It would be the first time in the company's listed history that anything other than a glass-bottled mineral-oil-and-fragrance compound represented a quarter of its top line.

For the long-term shareholder, the diversification index is now the single number that matters most. Almond Drops itself can be reasonably modelled as a slow-growth, high-margin cash generator. What is unknown—and what determines whether this is a re-rating story or a value-trap story—is the velocity of the non-core portfolio.

VII. Strategy Session: 7 Powers & 5 Forces

If we apply हैमिल्टन हेल्मर Hamilton Helmer's 7 Powers framework to Bajaj Consumer Care, what is immediately striking is how concentrated the company's competitive advantages are around exactly one product.

The first and most obvious power is Branding. Almond Drops occupies what marketing strategists call "category-defining" status in light hair oils—the position where the brand name has become functionally synonymous with the category itself, the way Xerox is to photocopying or Band-Aid is to adhesive bandages. Survey after survey of unaided brand recall in the LHO category puts Almond Drops at the top by enormous margins.[^1] This kind of mental real estate, once captured, is extraordinarily expensive for competitors to dislodge—not because the product is technically superior (it is not particularly differentiated chemically) but because the cognitive cost of switching for a loyal user, especially in rural and small-town India, is high.

The second power is what Helmer calls a Cornered Resource, and in Bajaj's case it is something subtle: the proprietary fragrance and formulation profile of Almond Drops. Consumers who grew up with the product describe a very specific olfactory memory—the slightly sweet, slightly powdery almond-rose-musk scent that no competitor has been able to credibly replicate. It is, in essence, a Coca-Cola-style flavour moat. Marico tried with Parachute Advansed Jasmine. Dabur tried with Almond Hair Oil. Hindustan Unilever has tried versions through Indulekha and Clinic Plus extensions. None of them quite "smell like Bajaj."

A third, lighter-touch power is Scale Economies in the specific distribution micro-segment of small-pack hair oils in rural India. The infrastructure required to economically supply 50-millilitre and 100-millilitre bottles to four-million-plus retail outlets is genuinely hard to build from scratch. New entrants have to either spend years building it or accept distribution-driven shelf inferiority. The downside, of course, is that this scale is category-specific—it does not transfer cleanly to skincare or premium personal care.

Where Bajaj is conspicuously weak in the 7 Powers taxonomy is in Process Power (no proprietary manufacturing or formulation process that is hard to copy), Switching Costs (a hair oil consumer can switch tomorrow at zero financial cost), and Counter-Positioning (the company is not doing anything that competitors structurally cannot do).

Now flip the lens to माइकल पोर्टर Michael Porter's 5 Forces and the picture sharpens further.

Rivalry is intense and is the defining force of the industry. The Indian hair oil market is contested by Marico (massively scaled, vertically integrated into coconut sourcing), Dabur (ayurvedic credibility plus a huge distribution arm), Emami (aggressive marketing, willing to pay for shelf space), and Hindustan Unilever (deep pockets, premium positioning). In any given quarter, all five of these companies are running price promotions, advertising blasts, and channel incentives. Margins for the industry as a whole have been gently compressing for a decade.

Threat of Substitutes is the more existential force. For Bajaj's core consumer of 1995, the only substitute for almond-fragranced light hair oil was a different fragrance of hair oil. For Bajaj's prospective consumer in 2026—a 22-year-old in Pune or Hyderabad—the substitutes are hair serums, leave-in conditioners, hair masks, scalp tonics, argan oil capsules, and the steady global drumbeat that suggests hair oil itself might be an aesthetic of a bygone generation. This is the slow-motion threat that keeps strategists awake.

Bargaining Power of Buyers in FMCG is mediated through retailers and modern-trade chains. As रिलायंस रिटेल Reliance Retail and डीमार्ट DMart have grown, their ability to extract trade margins from suppliers has grown with them. E-commerce platforms like Blinkit and Zepto extract their own toll for shelf placement. The era of suppliers dictating terms to a fragmented retail landscape is ending.

Bargaining Power of Suppliers is, comparatively, low. Light liquid paraffin is a globally traded commodity, glass and packaging are competitive, fragrance houses are numerous. Bajaj has reasonable leverage on input costs—though crude-oil-linked paraffin prices remain a recurring earnings volatility factor.

Threat of New Entrants, finally, is higher than it used to be—but in a curiously asymmetric way. New entrants in legacy hair oil are unlikely to succeed; the moats are too deep. But new entrants from digital-first D2C, who can build a brand through Instagram in 18 months and use third-party manufacturers and Amazon-Flipkart distribution, are suddenly viable. Mamaearth's parent Honasa Consumer is exactly that kind of new entrant, and it now has a market capitalisation in the same order of magnitude as Bajaj Consumer Care itself.

Net-net: the franchise is real, the core moat is real, but the competitive environment around it is structurally tougher than it was a decade ago.

VIII. The Playbook: Lessons for Investors & Founders

There is a particular kind of company that the Indian stock market produces with depressing regularity, and Bajaj Consumer Care for a long time risked becoming the textbook example. The pattern goes like this. A founder family discovers an extraordinarily profitable, low-capital-intensity product. They list the company, the stock re-rates upward as institutional investors fall in love with the metrics. The company generates so much cash that paying it back as dividend feels like the obvious thing to do—and management's incentives are aligned with that, because the family is the largest dividend recipient. R&D budgets stay tiny because innovation does not feel urgent. New product launches are infrequent and tentative. Then the world changes—a new generation of consumers emerges, channel structures shift, competitors industrialise their R&D—and the company finds itself with a fortress balance sheet and no second product.

This is what observers of Indian markets sometimes call the dividend trap, and it explains why companies like कोलगेट पामोलिव Colgate-Palmolive India, नेस्ले इंडिया Nestlé India, and yes, Bajaj Consumer Care, have spent long stretches of the last decade trading sideways or at compressed multiples relative to faster-innovating peers.[^13]

The trap is harder to escape than it looks. Once a company is paying out 80-90% of profits, scaling back the dividend to fund R&D and brand-building feels punitive to the shareholders who priced the stock for that yield. Cutting the payout creates an immediate stock-price reaction even if the long-term value is positive. So companies either (a) keep paying out and gradually erode their competitive position, or (b) cut the payout and absorb a re-rating in the short term to fund the reinvestment.

Bajaj has been doing variant (b) since roughly 2020, which is part of why the stock has traded sluggishly even as the underlying business has been quietly transforming.

A second lesson, even more pointed, is about brand extension versus brand dilution. Can a brand built around "trusted almond hair oil for Indian families" credibly stretch into anti-blemish creams, dermatologist-prescribed acne treatment, and premium argan oil for the urban millennial? The Nomarks experiment suggests that the answer, when done lazily, is no. The Ethicare structure, where the brand is kept entirely separate from the Bajaj parent name and lives in a pharmacy channel, suggests the company has learned the lesson: instead of stretching the master brand, build or buy adjacent brands that share the parent's distribution and procurement scale but carry their own identity.

This is, in fact, the playbook that इमामी Emami, गोदरेज कंज्यूमर Godrej Consumer Products, and ultimately मैरिको Marico have followed—a multi-brand house architecture where the corporate parent does not directly endorse every consumer-facing brand. It is a structurally smarter approach for the kind of categories Bajaj wants to enter.

A third lesson is about the re-rating problem. The Indian market values FMCG companies on a band of price-to-earnings multiples that reflects two things: the durability of their cash flows and the optionality of their growth. A हिंदुस्तान यूनिलीवर Hindustan Unilever trades at a premium because it has both—high durability and high optionality. A pure-play single-product company gets credit only for durability. The way Bajaj re-rates, then, is not by selling more Almond Drops but by demonstrating that the non-ADHO portfolio is real, scaling, and capable of independent growth. Until that re-rating happens, the stock is essentially capped by the multiple investors assign to a single-product FMCG, regardless of how good that single product is.

Myth vs Reality. A few common narratives deserve checking against the actual operational reality. Myth one: Almond Drops is being disrupted by serums. Reality: in volume terms, Almond Drops volumes have been remarkably stable. The disruption is happening at the premium-add-on end of the hair-care basket, not the core daily-oil-routine. Myth two: Bajaj has been a chronic underperformer because management is family-run. Reality: management has been formally professionalised since 2020 and the underperformance reflects deliberate margin investment, not legacy family inertia. Myth three: The company is debt-laden after acquisitions. Reality: the balance sheet remains net-cash positive—Bajaj has been a chronic over-distributor, not an over-leverager.[^5]

Key KPIs to track. For the long-term investor, three numbers matter more than the rest. First, the diversification index—revenue share from non-Almond Drops products. Second, the growth rate of the international and e-commerce channels combined. Third, Almond Drops volume growth in the core Hindi-belt geographies—because that is the canary in the coal mine for the cash engine that funds everything else. Margins are secondary. EPS growth is secondary. These three numbers tell you whether the Act Two thesis is working.

IX. Epilogue: The Next Decade

The story that ends the episode is not really a story about hair oil. It is a story about whether a deeply profitable, deeply defensible single-product business can re-invent itself before the world around it forces a re-invention on terms the company does not control.

The Bull Case. By 2030, the diversification index has moved into the high-twenties. Ethicare has scaled from a small derma-cosmetics player to a meaningful contributor to the topline, riding the broader Indian wave of pharmacist-led skincare. The 100% Pure range has become a genuine challenger in the urban premium-oils niche. International revenue has crossed double-digit percentage of total sales as the Middle East and African expansions mature. Almond Drops itself continues its slow, durable growth—not exciting, but providing the cash engine that funds everything else. The stock re-rates from "single-product FMCG" multiple to "diversified consumer care" multiple, a journey that has historically been worth meaningful upside in Indian markets.

The Bear Case. Almond Drops volumes finally crack as Gen Z and Gen Alpha consumers in tier-2 and tier-3 India migrate decisively to serums, conditioners, and global brands made accessible by e-commerce. Private-label hair oils from Reliance Retail and DMart eat away at the mass-market end. The diversification portfolio remains sub-scale, perpetually burning marketing money to defend tiny market shares against deeper-pocketed rivals. Ethicare struggles to scale beyond the dermatologist relationships it inherited. Operating margins, instead of recovering, settle into a new lower band as the company is forced into a permanent reinvestment posture. The stock continues to underperform broader FMCG indices, becoming a kind of value trap for investors who keep waiting for the turnaround that does not come.

The probability-weighted middle, where reality almost always lands, is some blended outcome. Some of the new initiatives will work; some will not. The diversification index will probably move, but more slowly than management projects. The core franchise will erode at the edges but remain intact through the late 2020s. Whether the resulting trajectory is judged a success will depend less on what Bajaj Consumer Care does and more on what its consumers do.

Second-layer diligence asides worth noting as the next decade unfolds. The promoter holding structure and any related-party-transaction patterns will remain a governance focal point, with proxy advisors like IiAS continuing to scrutinise royalty and trademark arrangements where they exist.6 Capital allocation choices—particularly any large additional skincare acquisitions—deserve a careful look against the cautionary Nomarks template. Climate-linked input cost volatility on liquid paraffin (a petroleum derivative) is a real, if underappreciated, gross-margin sensitivity. The international business carries foreign-exchange and geopolitical exposures that have historically been small but are growing. And the regulatory environment around personal-care labelling and "natural" or "ayurvedic" claims is tightening globally, which will affect both the legacy Almond Drops messaging and the newer brand positioning.

What makes the story genuinely interesting from a दीर्घकालिक निवेशक long-term investor standpoint is that none of these forces will resolve quickly. This is not a single-quarter thesis. It is a five-to-seven-year journey of category transition, channel evolution, generational consumer shift, and management discipline.

For now, the glass bottle still sits on the shelf in the kirana store in Gorakhpur. The grandmother still pours the oil into her grand-daughter's palm before the wedding. The fragrance is still the same. The cash still flows. The cushion is intact while the next chapter is being written.

Whether that next chapter ends up looking more like इमामी Emami's successful multi-brand evolution or more like a slow erosion into irrelevance is the open question of the next decade. It is a fascinating case study in the limits and possibilities of FMCG strategy in the world's most demanding consumer market.

And it all started with the smell of almonds in a glass bottle.

References

References

-

FMCG Sector Analysis: The Light Hair Oil Segment — EquityMaster ↩

-

Bajaj Corp to buy Nomarks brand from Ozone Ayurvedics — Business Standard, 2013-08-22 ↩

-

Analysis of Indian Hair Oil Market Trends — Reuters/Refinitiv ↩

-

Promoter Shareholding and Corporate Governance Review — IiAS (Institutional Investor Advisory Services) ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube