AWL Agri Business: From Joint Venture to India's Edible Oil Giant

I. Introduction & Episode Roadmap

Picture this: A middle-class Indian household in 2003, the mother carefully measuring out cooking oil from an unmarked tin container bought from the local kirana store. The oil's origin? Unknown. Its quality? A daily gamble. Fast forward to 2024, and that same kitchen likely features a bright yellow Fortune bottle—a brand that reaches 123 million households across India, transforming how the world's most populous nation thinks about edible oil.

This is the story of AWL Agri Business Limited, formerly Adani Wilmar—a company that in just 25 years went from zero to becoming India's second-largest FMCG player with ₹636.72 billion in revenue. It's a tale of how two unlikely partners—an Indian infrastructure conglomerate and a Singapore commodity giant—built an empire that would eventually outgrow its own founding architecture.

The narrative arc is almost Shakespearean: A joint venture born in 1999 between Adani Enterprises and Wilmar International, rising to command 18.9% of India's ₹1.8 lakh crore organized edible oil market, only to see its Indian founder exit stage left in December 2024, selling its 44% stake for $2 billion. The company's February 2025 rebranding to AWL Agri Business marks not an ending, but a metamorphosis.

What makes this story particularly fascinating for students of business strategy is how AWL cracked three seemingly impossible codes simultaneously: building a trusted consumer brand in a commoditized market, creating competitive advantage through vertical integration in a low-margin business, and successfully expanding from edible oils into the broader FMCG universe—all while navigating the peculiar dynamics of being associated with one of India's most scrutinized business groups.

Our journey today takes us from the ports of Mundra where the first refinery was established in 2000, through the aggressive acquisition spree that built India's largest integrated food complex, to the boardrooms where the decision was made to part ways after a quarter-century partnership. Along the way, we'll explore how Fortune became synonymous with quality in Indian kitchens, why the company chose to expand into rice and personal care, and what the post-Adani future holds for this FMCG behemoth.

The themes we'll trace are timeless: How do you build consumer trust in a market scarred by adulteration scandals? Can operational excellence create sustainable moats in commodity businesses? When does vertical integration become a burden rather than a blessing? And perhaps most intriguingly—what happens when a company outgrows its founding narrative?

As we dive into this saga, remember that this isn't just a story about cooking oil. It's about how modern India eats, how global supply chains intersect with local consumption patterns, and how a company can transcend its origins to become something entirely unexpected. The transformation from a port-based refinery operator to a household name is a masterclass in strategic evolution—one that offers lessons far beyond the FMCG sector.

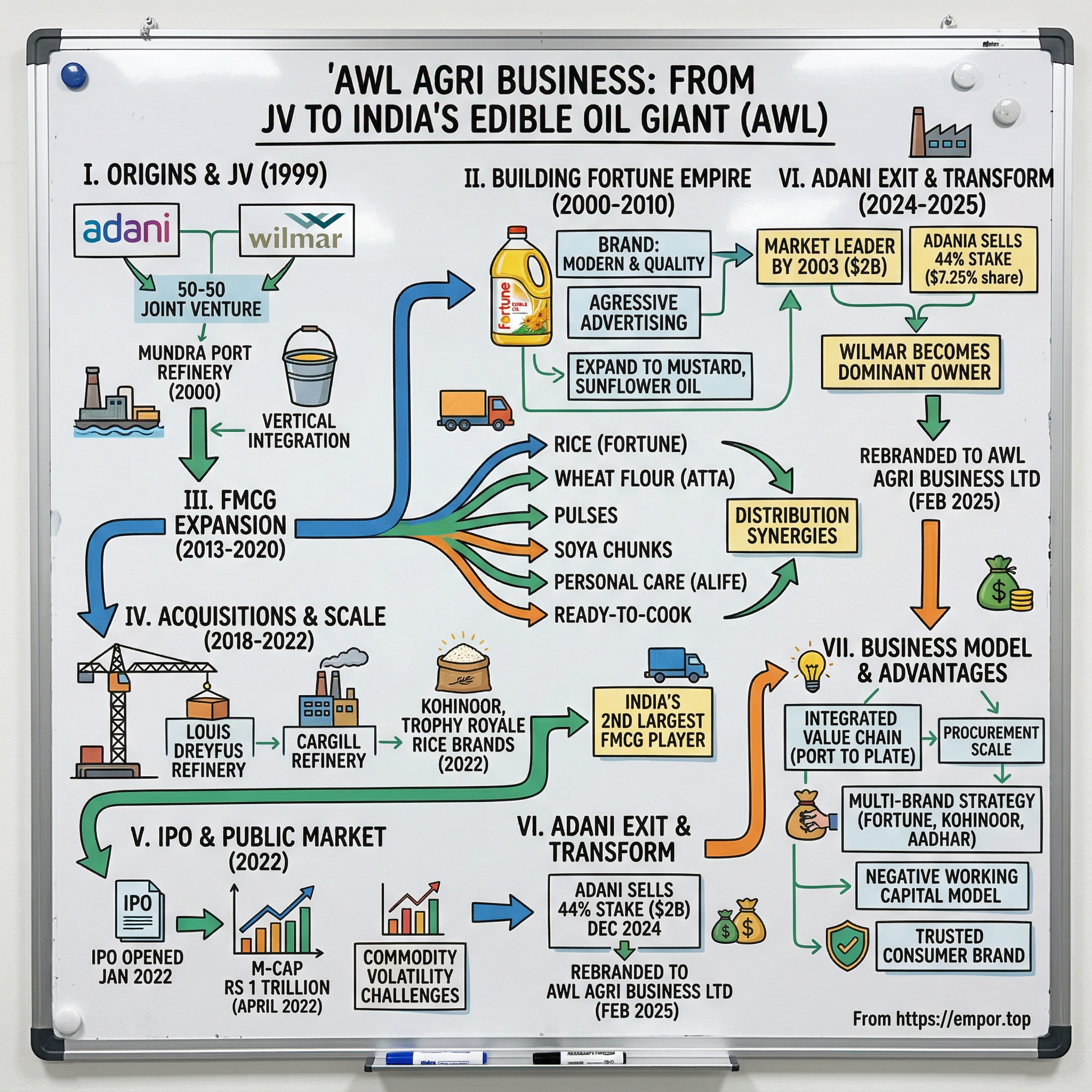

II. Origins & The Joint Venture Formation (1999)

The year was 1999. Y2K fears gripped the technology world, but in the boardrooms of Gujarat, a different kind of transformation was brewing. Gautam Adani, then running a trading and logistics empire built around Mundra port, sat across from representatives of Wilmar International, a Singapore-based agribusiness giant controlled by Malaysian tycoon Robert Kuok. The conversation wasn't about ships or containers—it was about something far more fundamental: how India feeds itself.

To understand why this meeting mattered, you need to grasp the chaos that was India's edible oil market in the late 1990s. The country imported nearly 40% of its edible oil requirements, yet the market was dominated by loose, unbranded oil sold in unmarked tins. Quality was inconsistent, adulteration was rampant, and middle-class consumers had no reliable way to ensure what they were putting in their food. The branded segment represented less than 10% of the market—a shocking statistic for a country where oil forms the foundation of virtually every meal. The genius of the joint venture lay in what each partner brought to the table. Wilmar International, already one of Asia's leading agribusiness groups, commanded the upstream—palm plantations, global commodity trading networks, and deep expertise in tropical oils processing. Adani brought the downstream—port infrastructure, local logistics mastery, and crucially, an understanding of how to navigate India's Byzantine regulatory landscape.

But here's what most analysts missed at the time: this wasn't just about combining assets. It was about timing a massive structural shift in Indian consumption. The liberalization of the 1990s had created a new middle class, but they were still buying loose oil from neighborhood shops. The question wasn't whether India would shift to branded, packaged oil—it was who would capture that transition.

The joint venture was structured as a perfect 50-50 split, unusual in an era when foreign partners typically insisted on majority control. This equality would prove both a strength—forcing consensus and collaboration—and eventually, 25 years later, a catalyst for separation when strategic visions diverged.

The first move was audacious in its simplicity. While competitors built refineries near consumption centers, AWL established its first facility at Mundra port with a capacity of 600 tons per day. The location seemed counterintuitive—Mundra was remote, underdeveloped, and far from major markets. But that was precisely the point. By building at the port, AWL could receive crude palm oil shipments directly from Wilmar's Southeast Asian operations, refine them at the lowest possible cost, and then distribute across India.

The company planned to sell half of the production as bulk oil and the rest as packed oil—a hedge that would prove prescient. The bulk business would provide immediate cash flow and market presence, while the packed segment would be their bet on India's branded future.

What's remarkable about the founding documents is their focus on supply chain from day one. The company viewed supply chain management as one of the important means to get a competitive edge, with approximately 70% of the total logistics cost accounted for by transportation. This obsession with logistics efficiency—unglamorous but fundamental—would become AWL's defining characteristic.

The cultural dynamics of the partnership were equally fascinating. Wilmar brought Southeast Asian efficiency and global commodity market sophistication. Adani brought what one former executive called "jugaad at scale"—the ability to make things work in India's complex environment. The early board meetings, held alternately in Singapore and Ahmedabad, were studies in cultural fusion: PowerPoints filled with global commodity curves meeting hand-drawn maps of Indian distribution routes.

By 2000, as the first oil rolled off the Mundra refinery lines, AWL had positioned itself at the intersection of three massive trends: India's shift to branded products, the globalization of commodity supply chains, and the infrastructure boom that would define the next two decades. The joint venture that seemed like an odd coupling—a Gujarati infrastructure company and a Malaysian-Chinese commodity trader—was actually a perfect marriage for the India that was emerging.

III. Building the Fortune Empire (2000–2010)

The conference room at AWL's Ahmedabad headquarters in early 2000 was tense. The marketing team had just presented their brand name recommendations for the company's flagship edible oil. The list was predictable: names evoking purity, tradition, mother's cooking. Then someone—accounts differ on who—suggested "Fortune." The room went quiet. In a country where cooking oil purchases were driven by trust and tradition, launching a brand that sounded almost Western, certainly modern, was either brilliant or suicidal.

The decision to go with Fortune was AWL's first major bet on aspirational India. While competitors wrapped themselves in tradition, Fortune positioned itself as the choice for the emerging middle class—modern, quality-conscious, but still rooted in Indian cooking. The tagline "Ghar Ka Khana, Ghar Ki Yaadein" (Home Food, Home Memories) perfectly straddled tradition and modernity.

But a brand is nothing without distribution, and here AWL faced a chicken-and-egg problem. Retailers wouldn't stock an unknown brand, and consumers wouldn't trust a brand they couldn't find everywhere. The solution was both expensive and brilliant: flood the market with supply while simultaneously building demand through aggressive advertising.

The early Fortune advertisements weren't about oil at all. They were mini-films about Indian families—the daughter-in-law winning over skeptical in-laws with her cooking, the working mother managing both office and kitchen. The oil was almost incidental. What AWL was selling was validation: you're modern, you're smart, you deserve better than loose oil from a tin drum. The execution was remarkable. By the end of 2003, Fortune had 17.25% share of the Indian packed refined oil market. In just three years, a new brand launched by a new company has become the leader in the Indian edible oils market. This wasn't just market share growth; it was category creation. AWL wasn't competing for a slice of the existing pie—it was baking an entirely new one.

The secret sauce was the company's integrated model combined with aggressive pricing. While competitors outsourced manufacturing or relied on third-party supply chains, AWL controlled everything from port to packet. This vertical integration allowed them to price Fortune 10-15% below premium brands while maintaining superior margins. It was a classic case of having your cake and eating it too.

But the real masterstroke came in 2003 with AWL's expansion beyond soybean oil. The company systematically entered mustard, sunflower, and rice bran segments, each time adapting the Fortune brand to local preferences. In North India, Fortune Mustard Oil emphasized purity and tradition. In South India, Fortune Sunflower Oil highlighted health benefits. Same brand, different stories—a playbook that would later be copied by every FMCG company entering India.

The acquisition strategy during this period was surgical. In 2011, the AWL group acquired the Alwar and Mundra castor units (crushing, refining, and industry essentials) and Gokul Refoils & Solvent (edible oil refining company). These weren't vanity purchases; each acquisition either eliminated a competitor, secured supply chain control, or opened new market segments.

The distribution build-out was equally impressive. AWL didn't just push products into stores; they created an entire ecosystem. Company representatives would visit retailers weekly, not just to take orders but to educate them about oil quality, help with inventory management, and crucially, ensure Fortune always had prime shelf placement. By 2010, Fortune was available in over 500,000 retail outlets—a number that would have seemed impossible a decade earlier.

Perhaps the most underappreciated aspect of Fortune's rise was its timing in riding India's cooking oil transition. As Indian cuisine evolved from deep frying to healthier cooking methods, Fortune positioned itself as the modern choice. The brand's "light" variants, introduced in 2008, weren't just line extensions—they were strategic bets on changing consumer behavior.

The financials tell the real story. From virtually zero in 2000, AWL's revenues crossed ₹10,000 crore by 2010. But more importantly, Fortune had achieved something rare in commodity businesses: brand premium. Consumers were willing to pay 5-7% more for Fortune compared to unbranded alternatives—not because the oil was fundamentally different, but because the brand represented trust, modernity, and aspiration.

By 2010, AWL wasn't just an edible oil company anymore. It was sitting on India's most valuable FMCG asset: consumer trust at scale. The question now was what to do with it.

IV. The FMCG Expansion Playbook (2013–2020)

The boardroom discussion in 2013 was heated. Should AWL remain focused on edible oils where it had clear dominance, or leverage the Fortune brand into adjacent categories? The conservative faction argued for focus—why risk diluting a winning formula? But CEO Angshu Mallick and his team saw a different opportunity: Fortune wasn't just an oil brand anymore; it had become synonymous with the Indian kitchen.

The expansion strategy that emerged was brilliantly simple: follow the cooking oil. Every product AWL would launch had to have a logical connection to oil in the consumer's mind. Rice? You need oil to make biryani. Flour? Oil is essential for making chapatis. Pulses? They're cooked with oil. This wasn't random diversification—it was systematic colonization of the Indian kitchen.

Between 2014 and 2017, the company launched other packaged products, such as rice, soya chunks, and flour, under the same brand name. But the execution was far more nuanced than this simple timeline suggests. Each category entry was preceded by months of consumer research, supply chain preparation, and crucially, retailer education.

Take the rice launch in 2014. AWL didn't just slap the Fortune label on commodity rice. They identified a specific gap: urban consumers wanted premium basmati but didn't trust loose rice sold in traditional stores. Fortune entered with packaged, graded basmati that promised consistent quality. The tagline "Har Dane Mein Khaas Baat" (Something special in every grain) wasn't selling rice—it was selling peace of mind.

The wheat flour entry was even more audacious. In 2015, the atta market was dominated by regional players and the formidable ITC's Aashirvaad. AWL's insight was that Fortune's oil customers were already trusting the brand for one essential ingredient—why not two? The company launched Fortune Chakki Fresh Atta with a unique proposition: flour so fresh it retained the wheat aroma. They even installed mini flour mills in select stores for live demonstrations.

But the real innovation came in distribution synergies. AWL's sales representatives were already visiting retailers weekly for oil orders. Adding flour, rice, and pulses to their portfolio meant marginal additional cost but significant revenue upside. A retailer who might stock two SKUs of Fortune oil would now carry 10-15 Fortune products. The company's share of shelf grew geometrically while distribution costs grew arithmetically.

The 2019-2020 period marked AWL's boldest move yet: Between 2019 and 2020, the company entered the personal care market under the brand Alife. During the same period, AWL also ventured into the ready-to-cook (RTC) products market. The Alife soap launch seemed to violate AWL's own playbook—what did soap have to do with cooking oil? But the logic was consumer-centric rather than product-centric. The same consumer who trusted Fortune for what went into their body could trust Alife for what went onto it.

The ready-to-cook foray was prescient, launching just before COVID-19 would dramatically accelerate adoption of convenience foods. Products like Fortune Khichdi and Ready-to-Cook Biryani weren't targeting traditional home cooks—they were aimed at young professionals and nuclear families seeking convenience without compromising on quality.

What's remarkable about this expansion is what AWL didn't do. They didn't launch carbonated drinks, snacks, or other high-margin impulse products that tempted every FMCG player. They didn't chase trends like organic or gluten-free that commanded premium pricing but had limited scale. Every product launch was disciplined, logical, and leveraged existing capabilities.

The numbers validated the strategy. By 2020, non-oil products contributed nearly 25% of AWL's revenues—from zero just seven years earlier. More importantly, these products enhanced rather than cannibalized oil sales. Retailers reported that consumers who bought Fortune rice were more likely to buy Fortune oil, creating a virtuous cycle of cross-selling.

The cultural impact was equally significant. Fortune had evolved from a product brand to a lifestyle endorsement. The urban Indian household that served Fortune rice cooked in Fortune oil, with rotis made from Fortune flour, was making a statement about their values: modern but rooted, quality-conscious but practical, aspirational but sensible.

Behind the scenes, this expansion required massive operational transformation. AWL built or acquired specialized facilities for each category—rice mills in Punjab, flour mills in Madhya Pradesh, pulse processing units in Maharashtra. The company that started with a single oil refinery now operated dozens of facilities across the country, each optimized for its specific product but integrated into a common supply chain.

The FMCG expansion also transformed AWL's competitive positioning. No longer was it competing just with oil companies like Ruchi Soya or Cargill. It was now in the ring with FMCG giants like ITC, Hindustan Unilever, and Nestle. This elevation in competition would prove crucial for what came next—the acquisition spree that would transform AWL from a large player to an industry giant.

V. The Acquisition Spree & Scale Building (2018–2022)

The acquisition committee meeting in early 2018 had the intensity of a war room. Spread across the conference table were detailed dossiers on a dozen potential targets. AWL's leadership had made a strategic decision: organic growth had taken them far, but to achieve true FMCG leadership, they needed to buy their way to scale. The motto was simple: "Build where we can, buy where we must."

The first major move came swiftly. In 2018, the AWL group acquired a refinery from Louis Dreyfus Commodities, an edible oil refinery from Cargill, and rice plants from Ferozepur Foods. These weren't distressed asset purchases—AWL was buying from global giants who were rationalizing their India operations. The Louis Dreyfus refinery in Kandla port and Cargill's Mangalore facility weren't just capacity additions; they were strategic chess moves that gave AWL unprecedented coastal coverage.

But the real coup came in 2022 with a transaction that shocked the industry. In 2022, Adani Wilmar acquired the Kohinoor, Trophy Royale, and Charminar rice brands from McCormick & Company. McCormick, the American spice giant, had struggled to scale these heritage brands in India's complex market. For AWL, these weren't just brands—they were keys to premium market segments that Fortune rice couldn't access.

Kohinoor, in particular, was a masterstroke. The brand had incredible equity in premium basmati but had been underinvested for years. AWL immediately pumped resources into modernizing Kohinoor's supply chain, upgrading packaging, and most importantly, leveraging Fortune's distribution network. Within months, Kohinoor was available in stores where it hadn't been seen for years.

The integration playbook AWL developed was surgical in its precision. Day one: secure supply chain continuity. Week one: retain key talent and relationships. Month one: integrate back-office functions. Quarter one: launch combined distribution. Year one: full synergy realization. This wasn't the typical Indian conglomerate approach of buying and neglecting—it was systematic value creation.

The manufacturing footprint expansion was equally aggressive. By 2022, AWL operated over 70 manufacturing units, but the crown jewel was the integrated food complex at Gohana, Haryana. This wasn't just a factory—it was a city of food processing. Spread across hundreds of acres, Gohana could process wheat into flour, paddy into rice, oilseeds into oil, and package everything on-site. The scale economies were staggering: transportation costs dropped 20%, processing efficiency improved 15%, and working capital cycles shortened by 10 days.

The Mundra facility evolution tells its own story. What started as a 600 ton-per-day refinery in 2000 had become Gujarat's largest port-based refinery complex by 2022, processing multiple oil types, operating solvent extraction plants, and even producing industrial oleochemicals. The vertical integration was so complete that waste from one process became input for another—palm oil refining waste became soap stock, rice bran became cattle feed, wheat polish became nutritional supplements.

But not all acquisitions were about scale. Some were about capability. The specialty fats business acquired from smaller players gave AWL entry into the high-margin bakery segment. The castor oil facilities provided access to industrial customers. Each acquisition was a calculated bet on adjacencies that leveraged existing strengths while opening new growth vectors.

The cultural integration challenge was immense. AWL was absorbing companies with decades of history, each with its own way of doing business. The company developed what insiders called the "Fortune Way"—a systematic approach to post-merger integration that balanced respect for legacy with urgency for transformation. Town halls, skip-level meetings, and retention bonuses for key talent became standard practice.

The financing of this acquisition spree was equally sophisticated. Rather than diluting equity or taking expensive debt, AWL used its strong operating cash flows and working capital optimization to fund most purchases. The company's negative working capital model—getting paid by customers before paying suppliers—generated hundreds of crores in float that could be deployed for growth.

By late 2021, AWL's board made a momentous decision: it was time to go public. The acquisition spree had built scale, but it had also created complexity. Public market discipline, professional governance, and access to capital markets would be essential for the next phase of growth. The IPO preparation began in earnest, setting the stage for what would become one of India's most watched listings of 2022.

The transformation was complete. In just four years, AWL had gone from a large edible oil player to India's second-largest FMCG company. The acquisition spree hadn't just added capacity or brands—it had fundamentally altered AWL's DNA. The company that once measured itself against other oil refiners now benchmarked against Hindustan Unilever and ITC. The ambition had scaled with the operations.

VI. IPO & Public Market Journey (2022)

January 27, 2022, 10:00 AM. As AWL's IPO opened for subscription, the entire FMCG industry held its breath. This wasn't just another listing—it was the public market debut of a company that had operated in the shadows of its prominent parents for over two decades. The offering was priced at ₹218-230 per share, seeking to raise ₹3,600 crore, but the real story was what this moment represented: AWL's emergence from chrysalis to butterfly.

The roadshow presentations in the weeks prior had been revealing. For the first time, institutional investors got a detailed look under the hood of this FMCG giant. With its Rs 37,090 crore operating revenue in 2020-21, the firm had managed to grow its top-line by an impressive rate (25 per cent year-on-year)—numbers that made even seasoned fund managers sit up. Once listed, AWL will become the third largest listed FMCG company by revenue, only behind ITC and Hindustan Unilever.

The IPO timing seemed perfect. India's consumption story was compelling, the Fortune brand had tremendous recall, and the market was hungry for quality FMCG stocks. But beneath the surface, there were complexities. The Adani Group's reputation, while stellar in infrastructure, carried different connotations in public markets. Environmental concerns around palm oil, questions about related-party transactions, and the inherent volatility of commodity-linked businesses—all needed careful navigation.

February 8, 2022, 9:15 AM. The listing day drama was palpable. The stock opened at ₹218, slightly below the issue price of ₹230, causing momentary panic. But by noon, institutional buying had kicked in, and the stock recovered. The first day's trading volume exceeded ₹1,000 crore—a sign of intense interest and equally intense scrutiny.

The post-IPO disclosures were eye-opening for public market investors. AWL's reach was staggering: products in 2.1 million retail outlets, 98 stock points across India, over 10,000 distributors. The company wasn't just large—it was omnipresent. The B2B business, largely invisible to consumers, contributed nearly 40% of revenues, serving hotels, restaurants, and food manufacturers with bulk oils and specialty fats.

But public market life brought new challenges. Quarterly earnings calls became tribunals where every basis point of margin compression was questioned. The stock price became a daily referendum on everything from palm oil prices in Malaysia to monsoon patterns in India. AWL's management, accustomed to the patient capital of family ownership, had to adapt to the quarter-to-quarter demands of public markets.

The governance transformation was equally dramatic. Independent directors with stellar credentials joined the board. Audit committees, risk committees, and stakeholder relationship committees were formed. Related-party transactions, previously routine, now required elaborate approval processes and disclosures. The company that had operated like a close-knit family business had to embrace the transparency demands of public ownership. The stock market journey reached a crescendo in April 2022 when AWL joined the elite group of companies with market capitalisation (m-cap) of Rs 1 trillion. The stock had rallied 249% since its February debut, a performance that stunned even bullish analysts. For context, it took Hindustan Unilever decades to reach this valuation; AWL did it in less than three months as a public company.

But the trillion-rupee celebration was short-lived. By late 2022, global headwinds hit hard. Palm oil prices swung wildly due to Indonesia's export ban. The Russia-Ukraine conflict disrupted sunflower oil supplies. Suddenly, AWL's commodity exposure, previously seen as a strength, became a liability in analysts' models. The stock gave back most of its gains, a humbling reminder that in public markets, perception can change faster than fundamentals.

The regulatory scrutiny intensified post-IPO. In 2016, the Government of Maharashtra released an official statement indicating that Adani Wilmar had violated regulations set by the Food and Drug Administration (FDA) of Maharashtra while promoting its blended edible vegetable oil, Fortune Vivo. Environmental concerns also emerged, with Adani Wilmar, along with other members of the Roundtable on Sustainable Palm Oil, has been criticized for its role in deforestation and the loss of habitat for orangutans, tigers, and elephants in the Sumatra and Borneo regions of Indonesia and Malaysia. The nonprofit Adani Watch states that "through its joint venture with Wilmar, Adani is a major refiner and trader in palm oil, an industry responsible for devastating large areas of rainforest in Southeast Asia."

Yet the business continued to perform. Quarterly results showed resilient volume growth even as margins compressed. Management's commentary on earnings calls revealed a sophisticated understanding of commodity cycles and hedging strategies. The company wasn't just riding market waves—it was actively managing through them.

The public market experience transformed AWL's strategic thinking. Access to capital markets enabled more aggressive expansion plans. The employee stock options created alignment and retention tools previously unavailable. Most importantly, the public scrutiny forced operational improvements that might have taken years otherwise.

As 2022 ended, AWL stood at a crossroads. It had achieved the scale and recognition of a major FMCG player, but questions lingered about its identity. Was it a commodity company with FMCG aspirations, or an FMCG company with commodity roots? The answer would come sooner than anyone expected, triggered by events that would reshape not just AWL but the entire Adani ecosystem.

VII. Distribution Mastery & Market Dominance

Walk into any kirana store from Kashmir to Kanyakumari, and you'll likely spot the distinctive yellow Fortune bottles gleaming on the shelves. This ubiquity didn't happen by accident—it was engineered through one of India's most sophisticated distribution networks. AWL has emerged as one of the few large FMCG food companies in India to offer most of the essential kitchen commodities for Indian consumers, including edible oil, wheat flour, rice, pulses and sugar, with Fortune as the No. 1 edible oil brand in India.

The numbers are staggering but worth parsing carefully. AWL's products reach 123 million households—that's one in three Indian families. The distribution architecture supporting this includes 98 stock points, over 10,000 distributors, and presence in 2.1 million retail outlets. To put this in perspective, AWL's distribution network touches more points than India's postal system.

But raw reach tells only part of the story. The real innovation lay in how AWL segmented and served different market tiers. In metros, the focus was on modern trade—Big Bazaar, Reliance Fresh, D-Mart. Here, AWL didn't just supply products; they managed entire categories, providing planograms, conducting in-store promotions, and even training store staff on oil quality parameters.

The traditional trade strategy was more nuanced. AWL created a distributor hierarchy that mirrored India's social geography. Super distributors managed districts, regular distributors handled tehsils, and sub-distributors served clusters of villages. Each tier had different margin structures, credit terms, and service levels. This wasn't just distribution—it was a franchise system without the franchise fees.

The rural penetration deserves special mention. While competitors struggled to make rural distribution economics work, AWL cracked the code through what they called "hub and spoke reimagined." Instead of trying to reach every village directly, they identified "golden villages"—rural centers that served 10-15 surrounding villages. These golden villages got direct service, exclusive schemes, and even branded shops. The surrounding villages were served through a network of bicycle vendors and weekly haats (markets), creating a capillary network that reached India's last mile.

The B2B business, often overlooked, became a silent giant. AWL served over 50,000 institutional customers—hotels, restaurants, caterers, food manufacturers. The Taj Hotels group, for instance, standardized on Fortune oils across all properties. McDonald's India used AWL's specialized frying oils. These weren't just bulk sales; AWL provided customized products, technical support, and even helped customers optimize their oil usage, reducing costs and improving quality.

The international expansion followed a different playbook. As of 2022, AWL operates 22 plants across 10 states in India and exports its products to the Middle East, Africa, and Southeast Asia. In Bangladesh, the Rupchanda brand (operated through BEOL - Bangladesh Edible Oil Limited) became market leader by adapting to local preferences—mustard oil for daily cooking, soybean oil for special occasions. In the Middle East, AWL supplied private label products to major chains, leveraging cost advantages while building relationships for future brand entry.

The technology integration in distribution was ahead of its time. By 2020, every distributor had a mobile app that provided real-time inventory, automated ordering, and credit management. Sales representatives carried tablets that could show retailers their purchase history, suggest optimal order quantities, and even provide recipe videos to help them sell to consumers. This wasn't digitization for its own sake—it was about making every interaction more valuable.

The credit management system was particularly sophisticated. AWL extended over ₹2,000 crore in credit to its distribution network at any given time, but bad debts were less than 0.5%. The secret was data-driven credit scoring that considered not just payment history but also local market conditions, seasonal patterns, and even weather forecasts that might affect rural purchasing power.

The logistics optimization was equally impressive. AWL's transportation costs were 20% lower than industry average, achieved through a combination of owned fleet, dedicated contract vehicles, and spot market optimization. The company pioneered the use of GPS-tracked oil tankers that could be rerouted in real-time based on demand, reducing both costs and stockouts.

Perhaps most impressively, AWL had figured out how to make money at every price point. In urban markets, Fortune Premium commanded 15% price premiums. In rural markets, the Aadhar brand sold at prices barely above unbranded oil but still generated positive margins through scale and efficiency. The portfolio approach meant AWL could capture value across the entire market pyramid.

The distribution moat AWL built wasn't just about reach—it was about relationships, data, and trust accumulated over two decades. When competitors tried to replicate this network, they discovered that the physical infrastructure was the easy part. The hard part was the thousands of micro-relationships, the deep understanding of local markets, and the trust that could only be earned through consistent delivery year after year.

VIII. The Adani Exit & Transformation (2024–2025)

December 30, 2024, will be remembered as a watershed moment in Indian FMCG history. Adani Enterprises announced its decision to exit the joint venture by selling its entire 44% stake to Wilmar International for about $2 billion. The announcement, coming after months of speculation, still managed to surprise the market with its timing and structure.

The backstory to this exit was complex. The Hindenburg report of early 2023 had put the entire Adani Group under unprecedented scrutiny. While AWL wasn't directly implicated, the collateral damage was real—institutional investors became wary, ESG funds questioned their holdings, and the stock price remained volatile despite strong operational performance. For Gautam Adani, the decision crystallized around a simple reality: The move is part of Adani's strategy to refocus on core infrastructure businesses, including energy, transport, and logistics.

The exit structure was masterfully orchestrated. To meet India's minimum public shareholding requirements, Adani plans to sell approximately 13% of its stake in the open market, ensuring that at least 25% of AWL's shares are publicly held. Additionally, Wilmar International will acquire Adani Enterprises' remaining 31% stake in the edible oil maker. This wasn't a fire sale—it was a carefully choreographed transition that maximized value while ensuring business continuity.

The immediate market reaction was mixed. Some investors worried about losing the Adani infrastructure advantage—access to ports, logistics networks, and political capital. Others saw liberation from the controversies that had dogged the Adani name. The stock initially dropped 8% but recovered within days as operational metrics remained strong.

The company's consolidated net profit rose 104.55% to Rs 410.93 crore in Q3 FY25, compared to Rs 200.89 crore posted in Q3 FY24—numbers that suggested the business was thriving regardless of ownership changes. Volume growth continued, market share held steady, and new product launches proceeded on schedule.

The rebranding to AWL Agri Business Limited in February 2025 was more than cosmetic. The company's shareholders approved the new name through an online postal ballot dated January 15. It signaled a new identity—no longer defined by its parentage but by its own achievements. The name retained the AWL acronym, maintaining continuity while signaling change.

For Wilmar International, becoming the dominant shareholder was the culmination of a 25-year journey. The Singapore-based giant now had effective control of one of India's largest FMCG companies, providing a massive platform for its global ambitions. Wilmar's CEO, Kuok Khoon Hong, called it "a transformative opportunity to deepen our presence in the world's most populous nation."

The management transition was surprisingly smooth. CEO Angshu Mallick, who had been with the company since 2015, retained his position, providing continuity. The board was reconstituted with more independent directors and Wilmar nominees, but the Indian character of the company was carefully preserved. This wasn't a foreign takeover—it was an evolution.

The strategic implications were profound. Without Adani's infrastructure advantages, AWL would need to compete on pure FMCG fundamentals—brand strength, distribution excellence, and innovation. But it also gained freedom from the controversies and capital allocation constraints that came with being part of a large conglomerate. AWL could now chart its own course, make acquisitions without group-level approvals, and build partnerships that might have been complicated under the previous structure.

The employee impact was carefully managed. Stock options were accelerated, retention bonuses were paid, and communication was transparent. The message was clear: this was not an ending but a new beginning. The company that had been built in the shadow of two giants was finally stepping into its own light.

Operationally, the immediate priority was maintaining business momentum through the transition. Suppliers needed reassurance that payment terms wouldn't change. Distributors needed confidence that support would continue. Customers needed to know that product quality and availability would remain constant. The management team worked overtime to ensure that the ownership change was invisible at the operational level.

The financial engineering of the deal was particularly clever. The $2 billion valuation implied a P/E multiple of about 35x, reasonable for a growing FMCG company but spectacular for what started as a commodity trading operation. Adani Enterprises would use the proceeds to deleverage and fund its infrastructure ambitions. Wilmar would consolidate its position in the world's fastest-growing major consumer market. And AWL would emerge as an independent FMCG powerhouse. Everyone won.

As AWL entered 2025 under its new identity, the challenges were clear but so were the opportunities. The company had the scale, brands, and distribution to compete with anyone. What it needed now was to prove it could thrive without the training wheels of its founding parents. The early signs were encouraging, but the real test would come in the years ahead.

IX. Business Model & Competitive Advantages

Strip away the corporate drama and ownership changes, and what remains is a business model that's both elegantly simple and fiendishly complex. AWL operates what might be the most integrated value chain in Indian FMCG—from port to plate, as insiders like to say.

The foundation is vertical integration, but not the clumsy kind that many conglomerates attempt. AWL's integration is surgical, owning only the links in the value chain where they can create genuine competitive advantage. They don't own palm plantations (too capital intensive, too risky) but they do own port-based refineries (logistics advantage). They don't own farms (too fragmented) but they do own processing facilities (quality control). They don't own trucks (asset-light is better) but they do own the technology platform that orchestrates transportation (data is the real asset).

AWL is India's largest processor of palm oil, a position that provides enormous leverage in global commodity markets. When Indonesian suppliers negotiate with AWL, they're not dealing with just another buyer—they're accessing the gateway to a billion-plus consumers. This scale translates into procurement advantages that smaller competitors simply cannot match.

The multi-brand portfolio strategy is particularly sophisticated. Fortune Foods, Fortune Xpert, Kohinoor Rice, King's Oils, Fryola, Aadhar, Bullet, Raag & Alife aren't random brands—each serves a specific market segment with laser precision. Fortune targets the aspirational middle class. King's serves the premium segment. Aadhar addresses price-conscious rural consumers. Bullet goes after the youth market. This isn't portfolio sprawl—it's market segmentation at its finest.

The manufacturing footprint is a competitive weapon. As of the date, we have 24 owned plants across 11 states in India. In addition, to cater to the excess demand and ensure our presence across different locations in proximity to end consumers, we currently have 47 tolling units across India. This combination of owned and tolling facilities provides flexibility that fixed-asset-heavy competitors lack. When demand spikes in a region, AWL can quickly activate tolling partnerships. When it normalizes, they can scale back without carrying excess capacity.

The cost structure reveals the true genius of the model. AWL operates with negative working capital—they collect from customers before paying suppliers. This generates hundreds of crores in float that funds growth without requiring external capital. The procurement scale provides 3-5% cost advantages. The port-based refineries save another 2-3% in logistics. The integrated supply chain eliminates another 2-3% in middleman margins. Add it up, and AWL has a 10-12% structural cost advantage—massive in a business where net margins are typically 2-3%.

But the real moat isn't physical—it's intangible. Brand equity that took two decades to build. Distribution relationships that cannot be replicated overnight. Consumer trust earned through billions of meals cooked with Fortune oil. Data on consumption patterns, price elasticity, and regional preferences that no amount of money can instantly buy.

The innovation pipeline, often overlooked, is becoming increasingly important. AWL's R&D centers work on everything from oil blending techniques that improve shelf life to fortification methods that address malnutrition. The company holds dozens of patents, unusual for what many consider a commodity business. Recent launches like omega-3 enriched oils and vitamin-fortified variants show that AWL can innovate at the product level, not just in distribution or marketing.

The capital allocation framework is disciplined. Every rupee invested must meet three criteria: does it strengthen the core business, does it leverage existing capabilities, and does it earn returns above the cost of capital? This discipline explains why AWL hasn't chased trendy but unprofitable segments like organic foods or entered unrelated categories like beverages.

The risk management approach is equally sophisticated. Commodity price volatility is managed through a combination of forward contracts, inventory management, and dynamic pricing. Currency fluctuations are hedged systematically. Credit risk is managed through data analytics and portfolio diversification. Even climate risk is addressed through geographic diversification of sourcing and processing facilities.

The competitive advantages compound over time. Scale begets better procurement terms which enable competitive pricing which drives volume growth which increases scale. Distribution reach attracts brand partners which improves retailer economics which increases distribution reach. Brand trust drives trial of new products which strengthens brand trust. These are virtuous cycles that become increasingly difficult for competitors to break.

What's perhaps most impressive is how AWL has managed to be simultaneously a low-cost producer and a premium brand owner. In most industries, companies must choose—be Walmart or be Whole Foods, be Maruti or be Mercedes. AWL has figured out how to be both, using different brands and channels to capture value across the entire market spectrum.

X. Playbook: Business & Investing Lessons

The AWL story offers a masterclass in business strategy that transcends industries. The lessons learned from building a ₹636 billion revenue company from scratch in 25 years deserve careful study.

Lesson 1: Timing Market Transitions AWL didn't create the trend toward branded, packaged foods—they recognized it early and positioned themselves to capture it. The shift from loose to packaged oil was inevitable given India's rising incomes and quality consciousness. AWL's genius was in being ready when the wave arrived. For investors, the lesson is clear: look for structural transitions, not temporary trends.

Lesson 2: The Power of Unglamorous Infrastructure While competitors focused on brand building and marketing, AWL invested in ports, refineries, and logistics networks. These unsexy assets became the foundation for sustainable competitive advantage. The lesson: in commodity businesses, operational excellence beats marketing brilliance every time.

Lesson 3: Brand Building in Commoditized Markets Fortune proved you could build a premium brand in a commodity category. The key was focusing on trust and consistency rather than trying to claim product superiority. AWL never said their oil was fundamentally different—they said it was reliably good. Sometimes, in categories plagued by quality issues, reliability is the ultimate differentiator.

Lesson 4: The Distribution Dividend AWL's investment in distribution paid dividends far beyond oil. Once they had trucks visiting retailers weekly, adding new products had minimal incremental cost. This operating leverage is available in many businesses but few exploit it fully. The lesson: build distribution once, monetize it repeatedly.

Lesson 5: Managing Joint Ventures The 25-year Adani-Wilmar partnership offers a template for successful JVs. Equal ownership forced consensus. Complementary capabilities prevented conflict. Clear governance structures avoided deadlocks. And when strategic interests diverged, the separation was handled professionally. Most JVs fail within five years; this one created billions in value over 25.

Lesson 6: Capital Allocation in Cyclical Businesses AWL's approach to capital allocation during commodity cycles was masterful. They expanded capacity during downturns when assets were cheap. They acquired competitors during distress. They returned cash during good times rather than chasing growth at any cost. This counter-cyclical approach created enormous value over time.

Lesson 7: The FMCG Transformation Blueprint The expansion from oils to foods to personal care followed a clear logic: leverage what you have before building what you don't. Every new category utilized existing distribution, manufacturing expertise, or brand equity. This disciplined expansion contrasts sharply with the random diversification that destroys value at many conglomerates.

Lesson 8: Building Moats in India AWL's moats are particularly suited to the Indian market: relationships matter more than technology, execution beats strategy, and trust trumps innovation. While these moats might not work in developed markets, they're perfectly adapted to India's unique business environment.

Lesson 9: The Exit Premium Adani's $2 billion exit crystallized a crucial insight: sometimes the best time to sell is when things are going well. The 104% profit growth in Q3 FY25 meant Adani could exit at peak valuation rather than being forced to sell during distress. This patience and timing created billions in additional value.

Lesson 10: ESG as Business Strategy While AWL faced criticism on environmental issues, their response was instructive. Rather than just PR management, they invested in sustainable sourcing, reduced packaging waste, and improved energy efficiency. These changes, initially forced by scrutiny, became sources of cost advantage and brand differentiation.

For fundamental investors, AWL presents a fascinating case study. The company has a low return on equity of 7.89% over last 3 years and though the company is reporting repeated profits, it is not paying out dividend. These metrics might seem concerning, but they reflect heavy reinvestment for growth rather than operational weakness.

The key insight for investors is that AWL is really three businesses in one: a commodity trading operation (low margin, high volume), a branded FMCG business (higher margin, strong moats), and an industrial supplies business (stable, cash generative). Valuing it requires understanding each component separately and how they interact.

The governance lessons are equally important. The transition from family-controlled JV to professionally managed public company required systematic changes in decision-making, disclosure, and accountability. The fact that this transition happened smoothly, even during ownership change, suggests institutional strength beyond individual personalities.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Consumption Juggernaut

The optimists see AWL as perfectly positioned for India's consumption boom. Start with market leadership—18.9% share of the ₹1.8 lakh crore organized edible oil market, with the nearest competitor at less than 10%. This isn't a fragile lead; it's dominance built on two decades of investment in brand and distribution.

The integrated supply chain provides structural advantages that only deepen with scale. When palm oil prices spike, AWL's procurement scale and hedging expertise allow them to absorb shocks better than smaller players. When transportation costs rise, their port-based refineries provide buffer. This resilience translates into consistent market share gains during volatility—exactly when competitors stumble.

The FMCG diversification story is still in early innings. Non-oil categories contribute 25% of revenues today but could reach 50% within five years. Each new category leverages existing infrastructure, making expansion capital-efficient. The recent Kohinoor acquisition shows AWL can successfully integrate premium brands, opening new growth vectors beyond the Fortune umbrella.

Distribution reach of 2.1 million outlets provides a platform for infinite adjacencies. Every new product launch has immediate national reach. Compare this to startups spending hundreds of crores to build distribution—AWL has already paid that price and now reaps the benefits with every new SKU.

The under-penetration opportunity is massive. Branded oil is still only 40% of the market; the remaining 60% loose oil market is AWL's to capture. Rural consumption is growing faster than urban. The shift to packaged foods accelerated during COVID and shows no signs of reversing. AWL doesn't need to create demand—they just need to capture the transition already underway.

Post-Adani independence could actually accelerate growth. Free from conglomerate constraints, AWL can make acquisitions, enter partnerships, and access capital markets more flexibly. Wilmar's global expertise in sustainable sourcing and product innovation provides new capabilities. The controversy discount in the stock price should fade, allowing proper FMCG multiples.

Bear Case: The Commodity Trap

The skeptics see fundamental challenges that no amount of branding can overcome. Company has a low return on equity of 7.89% over last 3 years—abysmal for a supposedly high-quality FMCG company. HUL generates 80%+ ROE; Nestle exceeds 100%. AWL's returns suggest this is still fundamentally a commodity business with FMCG aspirations.

The dividend policy—or lack thereof—is telling. Despite repeated profits, no dividends have been paid. This suggests either capital allocation indiscipline or hidden reinvestment needs that management isn't fully disclosing. For a mature business generating hundreds of crores in profit, the absence of dividends is a red flag.

Commodity price volatility remains an existential threat. AWL can hedge short-term fluctuations, but structural changes in palm oil availability due to climate change or regulation could devastate margins. The company's dependence on imported palm oil (60%+ of raw material) creates vulnerability to currency fluctuations, trade policies, and geopolitical risks.

The post-Adani transition risks are real. Loss of infrastructure synergies could increase costs by 2-3%. Key talent might leave during the uncertainty. Suppliers and distributors who had relationships with the Adani Group might reconsider terms. The rebranding to AWL might confuse consumers accustomed to the Adani name.

Environmental and regulatory scrutiny will only intensify. Palm oil's environmental impact and forced labor concerns in the supply chain create reputational risks. Food safety regulations are tightening. GST complications in the food sector remain unresolved. Any major regulatory change could impact profitability significantly.

Competition is intensifying from both ends. At the premium end, multinationals like Cargill and Bunge are expanding in India. At the value end, regional players are consolidating. In the middle, other FMCG giants like ITC and Patanjali are expanding into oils. AWL's market share might have peaked.

The valuation math is challenging. At current valuations, the market is pricing in 15-20% annual growth for the next decade. But oil consumption growth is slowing as health consciousness rises. The non-oil categories face entrenched competition. International expansion requires heavy investment with uncertain returns. The growth required to justify valuations seems optimistic.

The Balanced View

Reality likely lies between these extremes. AWL is neither the next HUL nor a commodity trap—it's a unique hybrid that defies easy categorization. The business has real moats in distribution and brand, but also real vulnerabilities to input costs and regulation.

For investors, the key is understanding what you're buying. This isn't a stable, dividend-paying FMCG blue-chip. It's a growth story with commodity exposure, execution risk, and governance transition challenges. The upside is significant if management executes, but this requires active monitoring rather than passive holding.

The next 18-24 months will be crucial. If AWL can maintain growth momentum post-Adani, successfully integrate recent acquisitions, and improve returns on capital, the bull case strengthens. If growth slows, margins compress, or integration struggles emerge, the bear case gains credibility.

XII. Epilogue & "If We Were CEOs"

Standing at the helm of AWL in 2025, newly independent and rebranded, presents one of the most interesting strategic challenges in Indian business. The company has tremendous assets—brand, distribution, manufacturing scale—but also faces an identity crisis. Is AWL a commodity processor that happens to own brands, or a branded FMCG company that happens to process commodities?

If we were running AWL, the first priority would be doubling down on the FMCG transformation. The commodity business provides cash flow and scale, but the future lies in branded, value-added products. This means accelerating innovation, launching premium variants, and potentially acquiring brands in adjacent categories. The goal: reach 50% revenue from non-oil categories within three years.

The second focus would be technology integration. AWL has been a fast follower in digital, but leadership requires being a first mover. Build India's most sophisticated demand prediction system using AI. Create a direct-to-consumer platform that bypasses traditional retail. Develop blockchain-based traceability that addresses quality concerns. Technology shouldn't just support the business—it should transform it.

International expansion needs rethinking. Rather than just exporting excess capacity, build meaningful positions in select markets. Bangladesh shows what's possible—Rupchanda is market leader because AWL invested in understanding local preferences. Replicate this in 3-4 high-potential markets rather than spreading thin across 50 countries.

The sustainability challenge must become a strategic opportunity. AWL's palm oil dependence is a vulnerability, but also a chance to lead industry transformation. Invest in sustainable sourcing, support small farmers, develop alternative oils. Make Fortune synonymous with responsible consumption. This isn't corporate charity—it's building a moat that regulation-focused competitors cannot cross.

Capital allocation needs dramatic improvement. ROE of 7.89% over last 3 years is unacceptable for a market leader. Either divest low-return assets or improve their profitability. Institute a clear dividend policy that returns excess cash to shareholders. Make acquisitions only when they're accretive to returns, not just revenues.

The organizational culture requires evolution from trader mindset to brand builder mindset. Traders focus on buying low and selling high; brand builders focus on creating consumer value. This shift requires new talent, new incentives, and new metrics. The company that measured success in tons processed must learn to measure it in household penetration and brand equity scores.

Premium segments offer disproportionate profit pools that AWL has barely tapped. Launch ultra-premium oils for health-conscious consumers. Create artisanal brands for urban gourmets. Develop functional foods for specific dietary needs. The mass market provides volume, but premiumization provides margins.

The D2C opportunity is particularly intriguing. AWL has relationships with 123 million households but knows almost nothing about them individually. Build a direct channel that provides consumer data, enables subscription models, and creates community. The company that owns the last mile in physical retail must also own it in digital.

Strategic partnerships could accelerate capability building. Partner with global food tech companies for innovation. Collaborate with agriculture tech startups for sustainable sourcing. Joint venture with specialty food companies for premium categories. AWL doesn't need to build everything itself—it needs to orchestrate an ecosystem.

The governance evolution must continue. The board needs more independent directors with FMCG experience. Management compensation should align with long-term value creation, not short-term profits. Transparency should exceed regulatory requirements, not just meet them. Great companies are built on trust, and trust requires radical transparency.

Most fundamentally, AWL needs a narrative that transcends its origins. It's no longer Adani's FMCG arm or Wilmar's India vehicle—it's AWL, India's kitchen partner. This identity must permeate everything from product development to marketing to investor relations. The company born from a joint venture must find its own voice.

The opportunity ahead is enormous. India's food consumption will double in the next decade. The shift to packaged foods will accelerate. Health consciousness will drive premiumization. AWL is perfectly positioned to capture these trends—if it can execute the transformation from commodity processor to consumer champion.

The journey from zero to ₹636 billion in revenue took 25 years. The next chapter—becoming India's most trusted food company—might take less time but will require even more vision, execution, and courage. The foundation is built; now comes the test of whether AWL can construct something truly extraordinary on top of it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube