Aditya Vision: The Kings of the Hindi Heartland

I. Introduction & The "Bihar" Opportunity

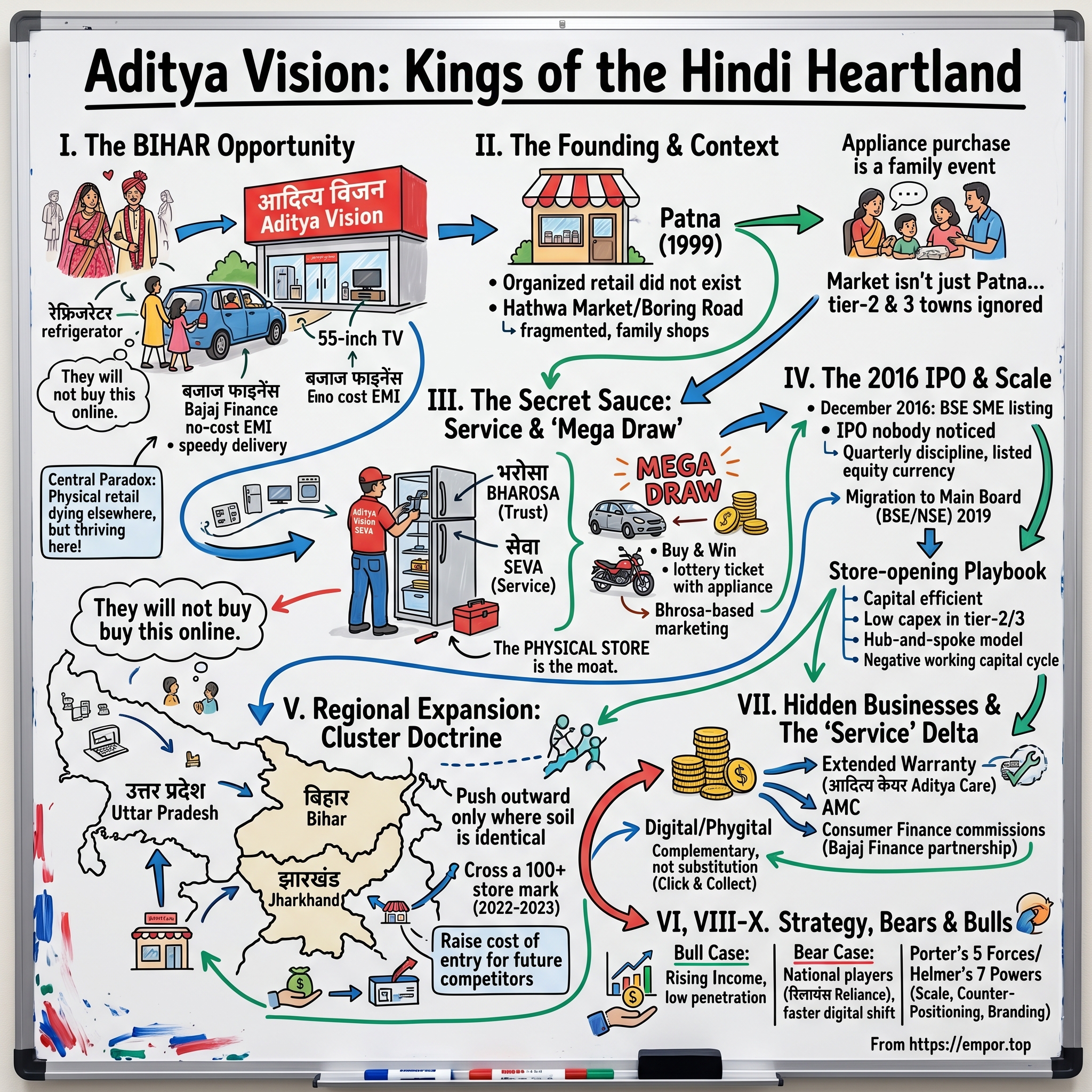

Picture a wedding in Muzaffarpur, Bihar, in the winter of 2024. The bride's family has been saving for two years. The dowry conversation has shifted in the last decade — gold and cash are still expected, but the modern bride and groom want a रेफ्रिजरेटर refrigerator, a 55-inch Smart TV, a front-load washing machine, and ideally an inverter air conditioner, because Bihar summers now routinely cross 44 degrees Celsius. The family piles into a hatchback and drives past three small unbranded electronics stores in the market, past a Reliance Digital that opened recently in the new mall, and pulls up at a brightly lit store with red-and-white signage that reads आदित्य विजन. They will spend the next three hours here. The store manager will personally walk them through floor models, the in-house finance desk will activate a बजाज फाइनेंस Bajaj Finance no-cost EMI within twenty minutes, and a delivery truck will install everything at their home within forty-eight hours. They will not consider buying this online. They never even checked Amazon.

This scene — multiplied across hundreds of small towns from Patna to Lucknow to Ranchi — is the story of Aditya Vision Ltd. (आदित्य विजन लिमिटेड), a regional electronics retail chain that has done something nearly nobody in modern Indian retail has managed: it has grown revenues and store count at a blistering pace while compounding shareholder capital at a rate that puts most of the Nifty 50 to shame. Since the company's 2016 BSE SME listing at a modest valuation, the stock has delivered returns measured not in percentages but in multiples — what investors politely call a "multi-bagger," and what early holders just call life-changing.[^1]

Here is the central paradox the company forces you to confront. The conventional wisdom of the last decade has been that physical electronics retail is dying. Best Buy survived only by reinventing itself as a services company. Circuit City vanished. In India, even well-capitalized players like रिलायंस डिजिटल Reliance Digital and Tata-owned Croma have struggled to extract real economics from the consumer durables business, sandwiched between Amazon, Flipkart, and the manufacturer-owned exclusive stores. And yet, in बिहार Bihar — a state that consistently ranks at the bottom of India's per-capita GDP league tables — a homegrown chain headquartered in Patna has been opening stores at a clip of roughly two to three per month, and earning genuinely attractive returns on each one.[^2]

The thesis of this episode is simple but counterintuitive. Aditya Vision is not really an electronics retailer. It is a भरोसा bharosa (trust) and सेवा seva (service) franchise that happens to sell electronics. In a geography where the post-sale service ecosystem of global brands is patchy at best, where customers want to physically touch a ₹80,000 refrigerator before buying it, and where a major appliance purchase is treated as a multi-generational family event, the physical store is not a liability. It is the moat.

Over the next three hours of narrative, we will trace how a single 1999 storefront in Patna grew into a regional powerhouse straddling Bihar, Jharkhand (झारखंड), Uttar Pradesh (उत्तर प्रदेश), and beyond; we will dissect the "Mega Draw" marketing engine that turns a transactional commodity purchase into something closer to a Diwali lottery; we will examine the 2016 IPO that nobody noticed; we will inspect the genuinely unusual capital efficiency of their store-opening playbook; and we will war-game the bull and bear scenarios against the looming spectre of Mukesh Ambani's रिलायंस Reliance Industries and Tata's deep pockets. Along the way we will pay particular attention to founder-managing director Yashovardhan Sinha (popularly referred to in earlier media coverage as part of the founding Prabhakar family, though the executive chairman and managing director on record is Yashovardhan Sinha), whose hands-on, store-walking style sets the cultural tone for the whole operation.[^3]

II. The Founding & The Bihar Context

To understand why Aditya Vision could exist at all, you have to first understand Bihar in the late 1990s. The state had just emerged from one of the most politically chaotic decades in modern Indian history. Organized retail, as the rest of India was beginning to know it through Pantaloons and Shoppers Stop, simply did not exist here. The electronics market in Patna's main commercial district of Hathwa Market and Boring Road was dominated by hundreds of small, family-run shops, each carrying a narrow slice of inventory — one shop sold only TVs and VCRs, another only refrigerators, another stabilizers and batteries (because the state's notoriously erratic power supply made voltage stabilizers a non-negotiable companion purchase for any major appliance).

Into this fragmented landscape stepped a young entrepreneur with a deceptively simple insight: what if all of this could happen under one roof, with one bill, one warranty contact, and one delivery truck? In 1999, the first Aditya Vision showroom opened on Boring Road, Patna — a multi-brand electronics store at a time when "multi-brand" was itself a novelty in the city.[^4] The store carried televisions, refrigerators, washing machines, and the smaller white goods that were just beginning to penetrate middle-class Bihari households as economic liberalization's second wave finally lapped against the eastern states.

The early years were not glamorous. There was no venture capital. There was no private equity. The business was financed the way nearly all Indian family businesses of the era were financed — promoter capital, supplier credit, and rolling working capital from local relationship-based banks. The first hire was probably a relative. The second was probably a salesperson poached from a competitor on Hathwa Market. Inventory was managed on paper for years. The store opened at 10 a.m. and closed when the last customer left, which during Diwali could mean midnight.

What turned out to be the foundational strategic insight — and you will hear the founders repeat it in interviews to this day — is that in Bihar, a major appliance purchase is not a transaction. It is a family event. The husband, the wife, the wife's mother, and at least one uncle who "knows about machines" will all show up at the store. The decision can take three visits. Demonstrations matter. The salesperson must be able to explain in Bhojpuri or Maithili why the inverter compressor in the refrigerator will save electricity. The customer needs to see the product turn on, hear it run, and ideally have someone vouch for it. None of this translates to an Amazon product page.

The second insight — equally foundational — was about geography. The young Aditya Vision team realized that Bihar's market wasn't really Patna. Patna was perhaps 15-20% of the state's spending power on durables. The rest was distributed across district headquarters like Muzaffarpur, Gaya, Bhagalpur, Darbhanga, Purnia, towns of two hundred thousand to a million people where nobody — not LG, not Samsung, not Sony, and certainly not any organized retailer — was paying serious attention. The brands sold through local distributors who were themselves stretched thin. After-sales service in these towns was, charitably, an afterthought. A washing machine breaking down in Purnia in 2005 could mean a three-week wait for a brand technician to make it out, if at all.

This is the soil in which the Aditya Vision model germinated. By the mid-2000s, the company had taken what was learned in Patna and begun pushing into these tier-2 and tier-3 towns with a deliberate value proposition: same brands you'd find in a metro store, same prices (or close to it), but with a service network that was actually local, actually responsive, and actually accountable. The chain that emerged was unmistakably Bihari in flavour — the showrooms were brightly lit, the staff spoke the customer's dialect, the financing was on-the-spot, and the delivery vehicles bore the company's red-and-white logo, gradually becoming part of the visual furniture of every small Bihari town.

By the early 2010s, the question facing the company was no longer whether the model worked. It was how to scale it without losing what made it work. That question would shape every decision over the next decade, and it would lead, in 2016, to a capital markets debut that almost nobody outside Patna noticed.[^1]

III. The Secret Sauce: Service & The "Mega Draw"

There is a story that circulates among Aditya Vision's longtime customers about a man in a small town in north Bihar whose refrigerator stopped cooling on a Friday afternoon in mid-May. He called the store. By Saturday morning a technician had arrived. The compressor was the issue. The technician did not have the part with him, but rather than tell the customer to wait a week, he loaded the entire refrigerator onto a small truck, took it back to the town's service center, fixed it, and returned it on Sunday — with the family's food still in the freezer transferred to a loaner unit in the meantime. The customer told this story to his entire extended family. Three of them subsequently bought air conditioners from Aditya Vision the following summer.

Whether this exact incident happened is almost beside the point. The Aditya Vision brand in the Hindi heartland is built on hundreds of stories like this — incidents that get told and retold at chai stalls, in WhatsApp groups, at weddings. The company internalized very early that in deep भारत Bharat, word-of-mouth is not a marketing channel. It is the marketing channel. Everything else is supporting fire.

The core operational architecture behind this reputation is what the company internally calls its service wing — sometimes branded as Aditya Vision Seva or Aditya Care, depending on which product or warranty layer you're touching. Most regional electronics retailers in India outsource the entire after-sales service problem to the brand. If your LG refrigerator breaks down, you call LG's service hotline, not the retailer. The retailer's job ends at the cash register. Aditya Vision early on decided this was unacceptable for their geography because in tier-3 Bihar, the brand's service network often simply wasn't there. So they built their own.1

In practice this means a layered model. For products under brand warranty, the company facilitates the brand-technician visit but takes ownership of the customer experience — escalating with the OEM, providing temporary replacements where feasible, and making sure the customer's complaint is closed. For products outside brand warranty, or for the company's own extended-warranty plans, the in-house service team handles the work directly. This requires investment that most retailers refuse to make — service centers in each cluster, a fleet of vehicles, parts inventory, trained technicians on payroll — and the operating cost looks ugly on a P&L line item. But it generates the one thing that compounds: trust.

The second pillar of the marketing edifice is even more genius, and it is something a Western retailer would struggle to imagine. Every year, typically during the festive season around Dussehra and Diwali, Aditya Vision runs what it calls the "Mega Draw" or "Buy & Win" scheme. Every customer who buys above a certain ticket size during the campaign window becomes eligible for a lottery. The prizes are not subtle: cars, motorcycles, scooters, gold coins, and in past iterations, even residential apartments. The grand prize draw is conducted publicly, often with a celebrity or local dignitary present, and the winners' photos plastered across local newspapers and the company's stores for the entire following year.[^6]

To understand why this works, you have to understand what it does culturally. In the Bihari middle-class household, buying a refrigerator is already an aspirational event. Now layer onto it the possibility — however statistically remote — that you might also win a Maruti Suzuki. The purchase is no longer a transaction. It is a लॉटरी टिकट lottery ticket with a refrigerator attached for free, psychologically speaking. The customer leaves the store telling everyone they know that they have just bought a car-lottery ticket. The store traffic during festive months becomes self-reinforcing in a way no online platform can replicate. Amazon can give you a 10% discount; it cannot give you the chance to drive home in a मारुति Maruti Suzuki Alto.

This is what Indian marketing scholars sometimes refer to as भरोसा-आधारित विपणन bharosa-based marketing — the conversion of trust, hope, and aspiration into commerce. It is not unique to Aditya Vision (पतंजलि Patanjali famously exploited similar emotional vectors in FMCG), but Aditya Vision has industrialized it in consumer electronics with a discipline that no national player has matched. The marketing budget is not small, but every rupee is spent on activities that reinforce the physical store as the gravitational center of the purchase experience.

The investor implication is sobering for anyone betting on e-commerce inevitability in this geography. The company's core market is not a market that is going online any time soon for large-format appliances. The combination of the financial complexity (most customers need credit), the logistical reality (installation, demonstration, after-sales), and the cultural texture (family event, lottery hope, trusted local face) creates a structural moat that pure e-commerce cannot easily breach.

IV. The 2016 IPO & The Pivot to Scale

By the middle of the 2010s, Aditya Vision had quietly built a chain of around two dozen stores, mostly across Bihar, with a clean balance sheet and a track record of consistent same-store sales growth. The next decision — and it was a non-obvious one — was to go public. Not on the National Stock Exchange's main board, where the institutional money and the media attention lived, but on the BSE's SME platform, a venue designed for small and medium enterprises, with lower listing thresholds and proportionately less analyst coverage.

The IPO, completed in December 2016, was a modest affair by Mumbai standards. The issue size was small, the offer document detailed a company most metropolitan investors had never heard of, and the listing day did not generate magazine covers.[^7] But the choice of going public early — at a stage when most regional Indian retailers would have continued to bootstrap or taken private equity — turned out to be one of the most strategically clarifying decisions the company ever made. It forced quarterly discipline. It created acquisition currency in the form of listed equity. It established a transparent governance baseline. And it created a window through which long-duration, fundamentally-oriented public investors could eventually find the story.

Three years later, in 2019, the company migrated from the BSE SME platform to the main board of both BSE and NSE, a graduation that opened the door to institutional ownership and analyst coverage.2 By the early 2020s, the stock was on the watchlists of nearly every India-focused small-cap fund manager, and the story had become a case study in the regional Indian consumer durables thesis.

What did the company actually do with the capital? The honest answer is: relatively little, by the standards of growth-stage retailers. Aditya Vision has consistently operated with one of the most capital-efficient store-opening models in Indian organized retail. A typical new store reportedly requires capital expenditure that is a fraction of what a Reliance Digital or a Croma store of comparable square footage requires in a metro location. The reasons are structural: Aditya Vision's stores are in tier-2 and tier-3 cities where real estate is dramatically cheaper, leases are negotiated through local relationships rather than national brokerage firms, fitouts are simpler and use regional contractors, and the brand does not need to spend on glossy interior design to attract its core customer.[^9]

The store-economics math, in rough strokes, looks like this. A new store pays back its initial capex over a period that is materially shorter than the industry norm. Once payback is achieved, the contribution margin compounds. Working capital is managed tightly through what the company has described as a regional hub-and-spoke model, with a central warehouse and just-in-time replenishment to individual stores. Inventory turns are higher than they would be for a chain attempting national reach with a fragmented logistics footprint, and supplier credit terms with the major OEMs are favorable enough that the negative working capital cycle — buy now, pay supplier in 30-60 days, collect from customer (or financier) the same day — funds a meaningful portion of growth without dipping into the equity pool.

This is the part of the story that doesn't make for great podcast theatre but is absolutely central to understanding why the stock has compounded the way it has. The combination of low new-store capex, fast payback, negative working capital, and a non-promotional balance sheet means that the company has been able to grow store count at a torrid pace without diluting equity, without taking on dangerous leverage, and without sacrificing return on invested capital at the store level. In an industry where most growth is financed at the cost of returns, Aditya Vision has been a notable exception.

The investor lens here is the one that long-term fundamental compounders inevitably gravitate toward. A business that can reinvest at high incremental returns on capital, in a market that is still under-penetrated, run by an owner-operator with significant skin in the game, is the platonic ideal of the compounding investment. The 2016 listing decision, however small it looked at the time, was the gate through which that compounder could be observed.

V. The Regional Expansion Strategy

There is a temptation, when a regional Indian retailer hits the size where it can be publicly listed and analyst-covered, to make the leap to national presence. This is the canonical playbook of Indian retail: build in one geography, raise growth capital, hire metro-bred executives, open flagship stores in Mumbai and Bangalore, and brand yourself as the next national consumer story. Most companies that have tried this have failed. The graveyard of Indian retail is littered with regional chains that overextended, broke their unit economics, and were either acquired at distressed valuations or quietly liquidated.

Aditya Vision has, refreshingly, refused this path. The expansion philosophy that has guided the company since the early 2020s is best described as the "cluster doctrine" — push outward only where the soil is identical to the home market. From its Bihar base, the company has methodically extended into झारखंड Jharkhand, the carved-out state directly to the south whose language, culture, and consumer behavior are essentially indistinguishable from rural Bihar. From Jharkhand, the next vector has been into eastern उत्तर प्रदेश Uttar Pradesh, the Bhojpuri belt around Varanasi, Gorakhpur, and Allahabad, where again the cultural code is the same as Patna.3

Notice what is not on this list. Mumbai. Bangalore. Hyderabad. Chennai. Delhi NCR. These are markets where the existing customer culture, the real estate cost structure, the labour market, and the competitive intensity (Reliance Digital, Croma, Vijay Sales) bear no resemblance to the Aditya Vision native environment. Pushing into them would mean rebuilding the entire playbook — new vendor relationships, new store managers, new marketing language, new service network — at vastly higher cost and against entrenched competition. The company has, to its credit, recognized that its competitive advantage is not transferable in the way a software company's product can be exported to a new geography. The advantage is the geography.

The most consequential phase of expansion came in the 2022-2023 window, when the company pushed past the 100-store mark and continued an aggressive opening cadence. By the financial year 2023-24 disclosures, the store count had climbed into the higher reaches of the cluster footprint, with the strategic target of crossing further milestones as the eastern UP and Jharkhand penetration deepens.[^11] The pace was aggressive enough to raise the obvious analyst question: are they over-extending?

The honest second-layer diligence answer requires watching two things. First, same-store sales growth (SSSG) — the closest proxy for whether the underlying box economics are holding up as the chain scales. If SSSG deteriorates materially as new stores cannibalize existing trade areas or as the freshly opened stores in unfamiliar micro-markets underperform, that would be the first crack. Second, store-level return on invested capital — whether the new boxes are paying back as fast as the legacy Bihar boxes did. Both metrics have, through the most recent reporting cycles, held up well enough to justify the expansion pace, though investors with long memories know that retail rollouts can go from triumph to catastrophe within four quarters if discipline lapses.

There is a subtle strategic chess move embedded in the cluster expansion that deserves explicit credit. By going dense in eastern UP and Jharkhand before any national player has built equivalent density, Aditya Vision is essentially raising the cost of entry for any future competitor. By the time रिलायंस डिजिटल Reliance Digital decides that small-town eastern UP is a market worth attacking with its full balance sheet, Aditya Vision will already have the prime high-street real estate, the local brand recall, the customer database for repeat servicing, and the trained workforce. A competitor would have to build all of that from scratch while fighting an incumbent on its home turf — exactly the kind of asymmetric battle that produces the bloodied late entrant in industry after industry.

The transition into the next phase of growth, however, will not be about geography alone. It will be about whether the cultural and operational DNA forged in 1999 Patna can survive the institutional weight that comes with scale. That question lands squarely in the lap of management.

VI. Management, Incentives & Governance

If you ask longtime Aditya Vision employees what differentiates the company from its peers, you will eventually arrive at a recurring theme: the founders show up. Unannounced. At stores you would not expect them at, on days they have no reason to visit, asking questions that betray a level of operational granularity that has no business surviving past the first hundred stores. This is the operator-founder culture that Aditya Vision has, so far, managed to preserve as it has scaled.

The face of the company in regulatory filings is Yashovardhan Sinha, who serves as the Executive Chairman and Managing Director and is the dominant promoter shareholder. Alongside him, the next generation has been integrated into the operating structure — his son Nishant Prabhakar Sinha and other family members hold key executive roles, which is increasingly visible in the company's annual reports and investor communications.[^12] The transition from the first generation's storefront-and-handshake era to a second generation that is more comfortable with capital markets, investor presentations, and digital initiatives is the kind of generational handoff that makes or breaks Indian family businesses. So far the evidence suggests this one is being handled with unusual deliberateness.

Promoter shareholding sits in the range that would make a governance-focused public market investor relax. The founding family collectively holds a clear majority of the equity, with the precise percentage hovering in the band that is meaningfully above the threshold at which incentive alignment becomes a question — meaning that for every rupee the public shareholder loses, the promoters lose multiple rupees, and for every rupee of value created, the promoters capture the lion's share alongside minority holders.[^13] This is the textbook owner-operator setup, and it is the structural condition that makes most great long-duration compounding stories possible.

The institutional ownership story has evolved interestingly over the past several years. As the company graduated from BSE SME to the main board, then as it crossed key revenue milestones, then as the multi-bagger price action attracted attention, mutual funds, foreign portfolio investors, and small-cap-focused PMS managers progressively built positions. This is visible in the shareholding pattern disclosures published quarterly and tracked by aggregators such as Trendlyne, which show institutional ownership rising from negligible levels in the late 2010s to a meaningful, though still minority, position by the mid-2020s.[^14] The implication is that the float available to incoming investors has been thinning, which has its own consequences for liquidity and volatility.

The incentive architecture at the store-manager level is one of the under-discussed pieces of the puzzle. The company has historically operated with a model that gives store managers meaningful local ownership of the P&L — not literal equity, but compensation structures linked to store-level performance metrics, with enough variability that a great store manager in a great year earns dramatically more than a mediocre one. This is the operating-leverage analog of the promoter-skin-in-the-game story at the top of the org chart. It is what allows a 150-plus-store chain to behave, at the customer-experience layer, more like a network of owner-operated small businesses than a corporate retailer.

The corporate governance overlay deserves a sober second look. The company is family-controlled, operates in a state with a history of opaque business practices, and has not yet been subjected to the kind of stress-test (a major fraud allegation, an accounting restatement, a regulatory action) that would definitively reveal the strength of its internal controls. Investors should monitor the standard checkpoints — auditor changes, related-party transactions disclosed in the annual report, board composition and independent director quality, and any qualifications in audit opinions. To date, the public record shows a clean operating history, but the absence of past trouble is never quite the same as proof of future resilience. The next decade of growth, particularly across state boundaries, will test the governance architecture in ways the Bihar-only phase did not.

Which brings us to the businesses that are quietly making more money than anyone notices.

VII. Hidden Businesses & The "Service" Delta

Walk into an Aditya Vision store on any given Tuesday afternoon and watch what happens after a customer says yes to a refrigerator. The transaction does not end with the appliance sale. In rapid succession, the salesperson will offer three things: an extended warranty plan, an annual maintenance contract for after the base warranty expires, and an in-store financing arrangement that turns the upfront ₹45,000 ticket into an equated monthly installment of around ₹3,800 for twelve months. By the time the customer leaves the store, the company has potentially booked three revenue streams — the appliance margin, the warranty fee, and a financing referral commission — and has bound the customer into a multi-year service relationship that dramatically raises the cost of going elsewhere for the next purchase.

This is the part of the Aditya Vision business model that does not show up neatly in a "revenue from operations" line. It is the margin layer that sits behind the storefront, and it is where a meaningful chunk of the company's economic profit is generated. Extended warranties and annual maintenance contracts (AMCs) are a high-margin business globally — Best Buy's Geek Squad in the United States is a useful analog, generating disproportionate profit relative to its revenue contribution because the underlying cost of service is amortized across a portfolio of customers, most of whom never invoke it. Aditya Vision has built a similar structure in its आदित्य केयर Aditya Care warranty program and ancillary service offerings.

The consumer finance partnership is the other quiet engine. In a market where the typical customer ticket is multiple times monthly household income, on-the-spot financing is not a nice-to-have. It is the price of entry. The company's deep operational relationship with Bajaj Finance — which has built its own enormous Indian consumer durables financing book by partnering with retailers exactly like Aditya Vision — turns each Aditya Vision store into a lead-generation node for a financial services giant.[^15] The retailer earns a commission on each financed sale; the financier earns the interest spread on the loan; the customer takes home the refrigerator without writing a check that would empty their savings account. Everybody is happy, and the structure has made a substantial portion of Aditya Vision's growth possible. Without it, the addressable market would shrink dramatically.

There is a third layer that is even less visible. Vendor financing, OEM-funded promotional schemes, in-store advertising and visual merchandising income from the brands themselves — these are the small streams that, at scale, add up to a non-trivial cushion to the gross margin. The company's stores are, from the perspective of LG, Samsung, Whirlpool, Daikin, and the rest, prime billboards in markets where the brands themselves have limited direct retail presence. The brands are willing to pay, in cash or in promotional support, for that real estate. A well-managed chain captures this; a poorly-managed one leaves it on the table.

The digital and फिजिटल phygital initiative is the most interesting strategic question facing management today. The company has rolled out a customer-facing mobile application, has begun building a direct e-commerce capability, and has tied these into the physical store network for click-and-collect, home delivery, and post-sale service requests. The temptation, given the multi-bagger stock and the consultant-class enthusiasm for "omnichannel," would be to invest enormous capital in building a digital channel that competes with the physical stores. The smarter and more disciplined path — which leadership has so far publicly committed to — is to use digital as a complement: a way to extend reach into neighbouring micro-markets where opening a full store is not yet justified, a way to capture browsing intent before the customer arrives in-store, and a way to operationalize the after-sales service relationship at lower friction.

Whether the digital build-out enhances or cannibalizes the franchise will be one of the more important things to monitor over the next several years. The base case, given the cultural dynamics described earlier, is that for the foreseeable future the physical store remains the dominant transaction venue for the company's core SKUs, and digital plays a supporting role rather than a substitutional one. But this is a question worth watching, because if customer behavior in the heartland evolves faster than expected, the moat could look different in five years than it does today.

VIII. Porter's 5 Forces & Hamilton's 7 Powers

It is one thing to tell a charming story about a regional retailer with a service-led moat. It is another to subject the moat to the cold analytical frameworks that long-term equity investors apply to any business they intend to hold for a decade or more. So let us run Aditya Vision through both Michael Porter's classic Five Forces and Hamilton Helmer's more recent Seven Powers framework, with as much intellectual honesty as the evidence permits.

Start with Helmer's seven powers, which is the more useful lens for a consumer franchise of this kind. The first power, Scale Economies, applies in a regional rather than national sense. Aditya Vision does not have the absolute scale of a Reliance Digital, but within its cluster geography it has a density of stores, a vendor relationship base, and a logistics footprint that lets it operate at a cost per unit sold that a sub-scale entrant cannot match. Density compounds within a cluster — the marginal store added in Bihar costs less to support than the first store in a new state would cost.

The second power, Network Economies, applies weakly to Aditya Vision in the strict sense — there are no two-sided network effects in appliance retailing — but the customer-referral-and-trust dynamic functions as a sort of pseudo-network effect. Each satisfied customer generates word-of-mouth that lowers the customer acquisition cost for the next sale in the same town. This is not Metcalfe's Law, but it is meaningful for the unit economics.

Counter-Positioning is interesting and somewhat applicable. National players cannot easily replicate the Aditya Vision model because doing so would require them to abandon the metro-focused, premium-brand-experience playbook that anchors their economics. Reliance Digital optimizing for tier-3 Bihar would mean lower ticket sizes, lower per-store revenues, and a different operating model that would conflict with the existing chain. The same is true for Croma. This is the textbook setup for counter-positioning: the incumbent's strengths in another segment become a structural disincentive to attacking the new segment.

Switching Costs are real, though not contractual. They flow from the service relationship — once a customer has bought multiple appliances from Aditya Vision and registered them under the company's care plan, switching to a different retailer for the next purchase means losing the relationship, the service history, and the credibility built up with the in-store team. These are soft switching costs, but in a market where trust is the currency, they are not trivial.

Branding is the most underrated of the Aditya Vision powers. The brand carries genuine emotional weight in its geography — the kind of weight that LG and Samsung have at the manufacturer level but no retailer in India has at the channel level. This is unusual and durable.

Cornered Resource applies in the form of the company's local real estate footprint, its trained workforce that speaks the customer's language and understands the cultural texture, and the relationships with thousands of local landlords, distributors, and service vendors that would take any new entrant years to replicate. Real estate in particular is a slow-moving constraint — the prime high-street locations in district headquarters are finite, and once Aditya Vision has them locked in, the next entrant must accept inferior locations at higher rents.

Process Power — the seventh power, the hardest to build — is the open question. Has Aditya Vision codified its operating model with enough institutional rigor that it can be transferred across geographies without quality degradation? The early evidence from the Jharkhand and UP expansion suggests yes, but this remains the area where the company has the most to prove over the next several years.

On Porter's Five Forces, the most important is the threat of substitution from online retail. The honest read is that for small electronics — smartphones, smaller appliances, accessories — e-commerce has already substituted away a meaningful share of the market in even tier-3 cities. But for the company's core categories of large appliances (refrigerators, washing machines, air conditioners, large TVs), where the installation requirement, the financing complexity, and the demonstration need all favour the physical store, the substitution risk is materially lower. The market continues to grow fast enough that even the online-share gain in some sub-categories is dwarfed by the underlying category expansion.

Rivalry among existing competitors is moderate but rising. National chains have not aggressively attacked Aditya Vision's home geography yet, but the strategic logic for them to do so will only strengthen as tier-2/3 consumer durables markets grow. Buyer power is low at the individual customer level (no single customer is a meaningful share of revenue) but moderately high through price-sensitivity. Supplier power is moderate — the major OEMs need the regional channel as much as the channel needs them, creating a relatively balanced negotiation. Threat of new entrants is meaningful but not imminent, because the capital and time required to replicate the Aditya Vision footprint is significant.

The synthesis: a strong but not impregnable competitive position, with the most durable advantages flowing from regional density, branding, and the service-led switching costs.

IX. Bear vs. Bull Case

The bull case for Aditya Vision rests on a single demographic and economic megatrend that nobody seriously disputes: per-capita income in the Hindi heartland is rising, and as it rises, the share of household income spent on consumer durables explodes nonlinearly. The pattern has played out in every emerging market that has crossed the per-capita GDP threshold of roughly $2,500 to $3,500 — the household goes from owning a fan to owning an air conditioner, from a single TV to multiple screens, from a washing machine to a washer-dryer combination, from no dishwasher to a dishwasher. Bihar and eastern UP are at the very early stages of this curve. The penetration of refrigerators, washing machines, and air conditioners in these states remains a fraction of all-India averages, which themselves are a fraction of developed-market levels.[^16]

If the per-capita income story plays out as expected over the next decade, the addressable market for an Aditya Vision in its existing geographies could multiply several times over without any geographic expansion. Layer on the cluster-densification opportunity (more stores within existing states), the ancillary income from warranties and financing, and the very real possibility of selective expansion into adjacent geographies (Odisha, West Bengal, Madhya Pradesh — all states with cultural and economic similarities to the existing footprint), and the bull case is not exactly modest.

The bull case also rests on the operational metrics continuing to behave. Same-store sales growth, the single most important leading indicator of franchise health, has held up through multiple cycles. Store-level returns on capital remain strong. Working capital management continues to be tight. Promoter incentives remain aligned. Each of these is a fragile assumption that requires ongoing verification, but each has, to date, delivered.

The bear case is more interesting precisely because it is structural rather than tactical. The single largest threat is a deliberate, well-capitalized assault on the Aditya Vision geography by a national player. If Mukesh Ambani decides that small-town consumer durables retail is a strategic priority, and instructs Reliance Retail to open 500 stores across Bihar, Jharkhand, and eastern UP over a three-year window with the explicit instruction to win at any cost, the competitive landscape would look very different. Reliance has the balance sheet to absorb sustained losses, the vendor relationships to match or beat Aditya Vision on pricing, and the brand recognition to draw foot traffic from day one. The same logic applies to Tata's Croma at slightly lower intensity, or to a अमेज़न Amazon-फ्लिपकार्ट Flipkart push into installation-heavy categories with a hyperlocal physical fulfillment network.

The counter-argument to the bear case is that even if these national players attack, they would face the same unit-economics challenges that have hobbled them in the cities. Lower ticket sizes in tier-3, harder logistics, more demanding service requirements, lower brand premium — all of these would compress the national player's margins below corporate hurdle rates, leading either to a strategic retreat or to a price war that bleeds both sides without producing a clear winner. The history of Indian organized retail's attempts to crack the deep heartland is not encouraging for the attackers, which is part of why the moat has held.

A second bear case worth contemplating is what happens if the digital transition accelerates faster than expected. The current generation of small-town consumers may be loyal to the physical store, but the next generation — digital natives growing up with smartphones and ubiquitous payments — may not feel the same cultural pull toward the showroom experience. If twenty years from now, refrigerators and washing machines are bought as routinely on a mobile app as smartphones are today, the moat erodes regardless of who attempts the attack.

A third, more prosaic bear case is execution risk. Family-run businesses in their growth phase can stumble on succession, on internal controls as scale exceeds the founders' direct supervisory bandwidth, on the temptation to diversify into adjacent categories that compromise the core focus. The history of Indian retail is full of regional champions that broke themselves through over-ambition more than they were broken by competitors.

For investors, the single most important key performance indicator is same-store sales growth (SSSG). It is the unfiltered signal on franchise health. A close second is new-store productivity — whether stores opened in the last 12-24 months are ramping to mature run-rates on the expected curve, or are underperforming, which would be the early warning that the cluster expansion thesis is breaking. A useful third indicator, harder to measure from outside, is the share of revenue from extended warranties and financing — the higher this trends, the more entrenched the customer relationship is becoming.

X. Playbook: Lessons for Founders & Investors

There is a tendency, when summarizing the success of a regional champion, to extract universal lessons that apply to all businesses everywhere. This is usually intellectually lazy and almost always wrong. Aditya Vision's success is deeply contingent on a specific geography, a specific cultural moment, a specific category of products, and a specific operator-founder culture. The right way to extract lessons from it is to be deliberate about which lessons are transferable and which are not.

The first lesson is that going deep beats going wide in a market like India. The conventional wisdom of the 2010s — that scale requires national presence, and that a regional player will be eventually steamrolled by a national one — has been falsified repeatedly in Indian retail and Indian consumer businesses. Companies that have stayed disciplined about their core geography and built true density within it have, in category after category, outperformed companies that diluted focus by sprinting for national flag-planting. Aditya Vision is the consumer electronics expression of this pattern. Page Industries in innerwear, Symphony in air coolers in earlier eras, several QSR chains, multiple regional pharmacy chains — the pattern recurs.

The second lesson is that service is the product in markets where the formal infrastructure for post-sale service is patchy. In the developed-world model, a retailer sells you something and the manufacturer's warranty handles everything after. In tier-3 India, the manufacturer's warranty exists on paper but the physical execution is unreliable. The retailer that solves this — by building its own service capability, by owning the customer relationship after the sale, by treating service as a moat-building activity rather than a cost center — captures economic value that the manufacturer-only model leaves on the floor. This is not a uniquely Indian observation; it is the central insight of Best Buy's late-stage Geek Squad reinvention. But the magnitude of the opportunity is uniquely large in India.

The third lesson — and the most culturally specific — is that marketing to the soul beats marketing to the algorithm. The Mega Draw is not a sophisticated marketing innovation by Madison Avenue standards. It is a lottery, dressed up as a sales promotion, delivered through the kind of in-store, locally-rooted theatrics that have animated Indian commerce for centuries. But it works in its market in a way no algorithmic targeting, no programmatic advertising, no influencer campaign could match. The lesson for any business operating in emotionally-textured markets is that local cultural resonance is its own form of competitive advantage, and one that is curiously underweighted by both Western-style management consultants and by the playbook-driven private equity industry.

The fourth lesson is about founder-led capital efficiency. The Aditya Vision model is one where the founders have, year after year, refused to take the easy money — refused to over-raise equity, refused to over-leverage, refused to dilute focus for the sake of headline growth. The compounding is the reward for that discipline. For founders building businesses today, the lesson is that capital is not the constraint they may think it is. Discipline is.

For investors, the meta-lesson is more sobering. Multi-bagger compounders of the Aditya Vision type look obvious in retrospect but were extraordinarily difficult to identify in advance. The 2016 IPO offer document, read with a sceptic's eye, would have surfaced multiple reasons to pass — small company, unfamiliar geography, unproven beyond Bihar, family-controlled, modest size. The investors who held through the journey did so because they recognized, somewhere along the way, that the underlying business quality and operator discipline were exceptional. The lesson is not to chase the next Aditya Vision; it is to develop the analytical framework that lets you recognize an exceptional small business when you encounter one, and the temperamental discipline to hold it through the long flat stretches when nothing in the chart looks exciting.

The story is not finished. The next decade will test whether the cluster doctrine survives geographic expansion, whether the second generation can carry the operator-founder culture forward, whether the national players finally decide to make the heartland a strategic priority, and whether the digital transition unfolds at a pace that honors or threatens the physical-store moat. None of these questions has a knowable answer today. What is knowable is that the company has, against the dominant narrative of Indian retail, built something rare — a regional franchise with genuine durability, deep customer trust, and the financial structure to keep compounding.

In the meantime, somewhere in a small town in eastern Uttar Pradesh, a family is walking into a brightly lit store with red-and-white signage to buy their first air conditioner. Their kids are excited. Their parents are sceptical. The salesperson knows their name. The Bajaj Finance form is already half-filled out. The installer will be at their home tomorrow. The Mega Draw entry has been printed. The cycle continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube