Avalon Technologies: The "Full-Stack" Architect of Modern Electronics

I. Introduction & Episode Roadmap

Somewhere over the Bay of Bengal, a remote-sensing satellite drifts through low-earth orbit. Inside its main avionics bay, tucked behind layers of thermal blanketing, sits a printed circuit board assembly no larger than a paperback novel. It will not be repaired. It will not be replaced. For the next decade, this board has exactly one job — to switch power without flinching, in a temperature range that swings from minus 40 to plus 85 degrees Celsius, while being bombarded by enough cosmic radiation to scramble a consumer-grade chip in under an hour.

Three thousand kilometres away, in a glass-walled shop floor in चेन्नई Chennai, the engineers who designed and built that board are leaning over the next one. There is no fanfare. No "as featured in" sticker. The customer logo has been deliberately scrubbed from every press release and investor deck. And yet, if you trace the supply chain of a surprising slice of the world's mission-critical electronics — the boxes inside locomotive traction controls, the inverters inside green-hydrogen electrolyzers, the avionics inside satellite payloads, the medical pumps inside operating theatres — you find a quiet, persistent name showing up on the bill of materials: एवलॉन टेक्नोलॉजीज लिमिटेड Avalon Technologies Limited, ticker AVALON on the National Stock Exchange of India.1

This is the story of how a tiny cross-border experiment, founded in 1999 by two engineers shuttling between Fremont and Chennai, evolved into one of India's most unusual contract manufacturers. Unusual, because Avalon does not look like the names that dominate Indian electronics headlines. It is not a Foxconn-style assembler racing to slap together millions of iPhones. It is not a डिक्सन Dixon Technologies-style scale player printing television sets and washing machine PCBs at razor-thin margins. The right mental model is closer to a Benchmark Electronics or a Plexus — a high-mix, low-volume, high-complexity Electronics Manufacturing Services (EMS) house, where every project is a small puzzle and the customer "marries" you for a decade.2

Three threads run through the next ninety minutes. The first is the "Dual-Shore" advantage — a phrase Avalon's own filings use to describe the rare trick of being legally and operationally rooted on both sides of the Pacific, designing in Silicon Valley and manufacturing in Tamil Nadu.3 The second is the strategic trade-off between high-complexity and high-volume — why Avalon chose, repeatedly, to walk away from the latter. And the third is the journey from a founder-led American startup to a listed Indian powerhouse, with all of the governance, capital allocation, and identity questions that transition forces.

This is not a viral story. There is no consumer brand to fall in love with. But for fundamental investors trying to understand what India's electronics manufacturing renaissance actually looks like beneath the smartphone-assembly headlines, Avalon is one of the most instructive case studies on the exchange. The bridge to its origin runs through a Bay Area office park, in the last year of the twentieth century.

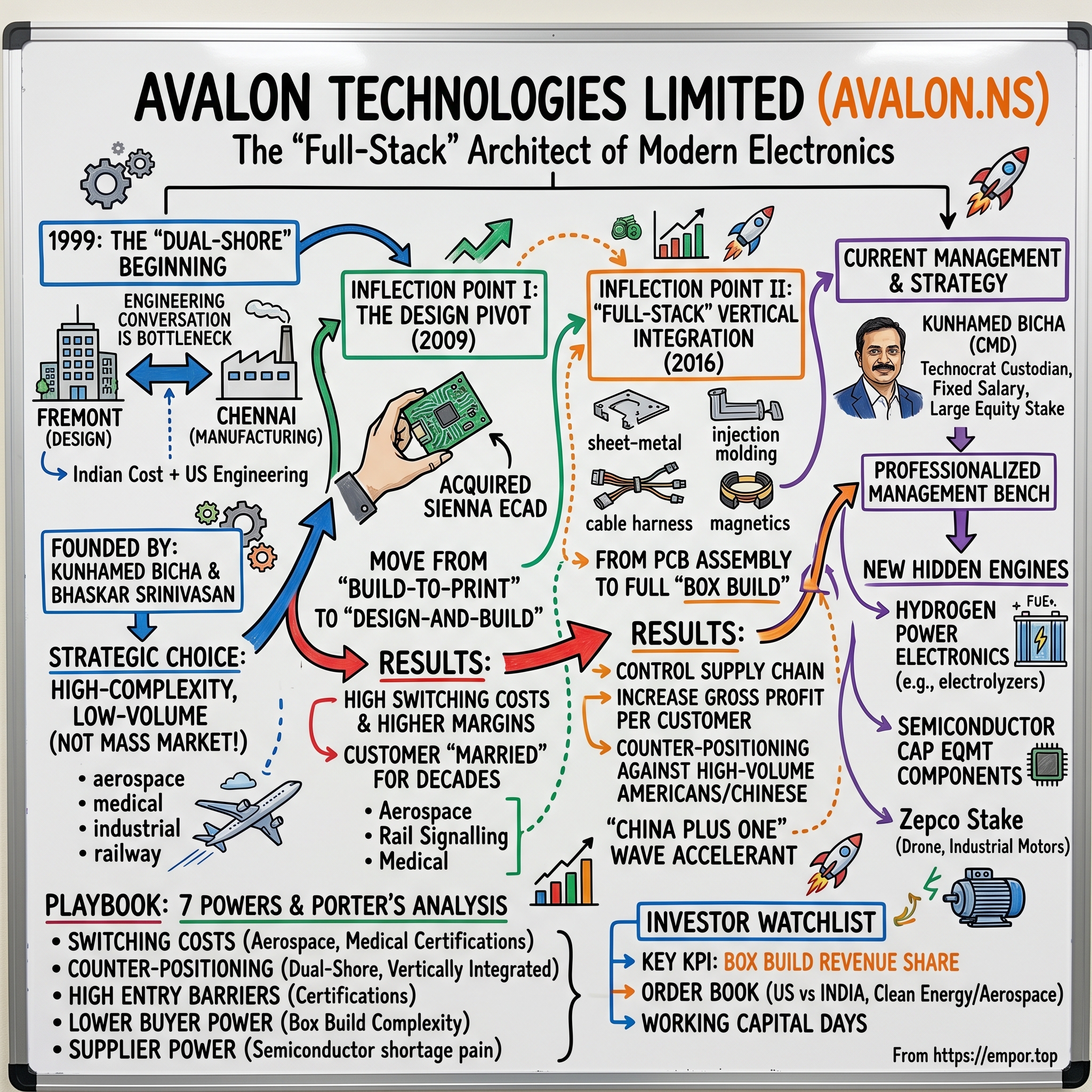

II. The Dual-Shore Origin: From Fremont to Chennai

It is the autumn of 1999 in फ्रेमोंट Fremont, California. The dot-com bubble has not yet popped. Cisco is briefly the world's most valuable company. Across the South Bay, every available square foot of industrial space is being colonised by hardware startups trying to ride the networking boom. In a modest office, two engineers — कुनहम्मद बिचा Kunhamed Bicha and भास्कर श्रीनिवासन Bhaskar Srinivasan — incorporate a company called Sienna Corporation.4 They are not, strictly speaking, trying to compete with the giants around them. They are trying to solve a specific, unglamorous problem.

The problem is this. In the late 1990s, every hardware startup in Silicon Valley faced the same painful trade-off when it came to manufacturing its prototype boards. You could go to a domestic US contract manufacturer, who would treat your two-hundred-unit pilot run as an annoying distraction from their automotive customer, charge you a small fortune, and still take eight weeks. Or you could go to China, where your design files might end up — euphemistically speaking — "shared" with a competitor, and where engineering changes had to travel across a twelve-hour time zone gap before anyone touched a soldering iron. India, in 1999, was not yet on anyone's map for serious electronics manufacturing. Liberalisation was less than a decade old, the केंद्रीय बजट Union Budget was still wrestling with current-account anxieties, and the country was best known for software services, not hardware.

Bicha and Srinivasan saw the gap. Both had spent the previous decade in US semiconductor and systems companies. They understood that the engineering conversation — the back-and-forth between a customer's design team and the factory — was the bottleneck that mattered. If you could pair a small US-based design and front-office shop with a sister manufacturing operation in India, run by people who could pick up the phone and speak Silicon Valley's language, you could collapse the lead time and the trust gap simultaneously. The Indian side was incorporated as Avalon Technologies, headquartered in Chennai. The US side, Sienna Corporation, would handle customer relationships, design support, and the all-important warm handshake.4

The first few years were brutal. The Nasdaq crashed in March 2000, taking with it roughly half of Avalon's prospective customer pipeline. Hardware orders evaporated overnight as venture-funded networking startups ran out of runway. The temptation, for any rational management team, would have been to chase volume — to pivot toward consumer electronics, to bid for handset assembly contracts, to fight on price. Bicha and Srinivasan did the opposite. They went up the complexity curve. They started taking on the boards that other contract manufacturers refused to quote — six-layer, eight-layer, and eventually twelve-layer PCBs, with fine-pitch ball-grid arrays and exotic substrates. They began chasing customers in industries where the regulatory bar was so high that a low-cost Chinese competitor literally could not enter without years of audit cycles: medical devices, aerospace, industrial automation, and railway signalling.

By the mid-2000s, the dual-shore identity had become the company's most defensible asset. To a procurement officer at a US OEM, Avalon looked and sounded American — same time zone for design reviews, same legal jurisdiction for IP protection, same English-language engineering vocabulary — while quietly delivering Indian cost economics on the back end.3 To an Indian customer, by contrast, Avalon brought the discipline and quality systems of a Silicon Valley supplier. The arbitrage was not just labour cost. It was credibility cost. In an industry where a single field failure on a medical pump can end a supplier relationship overnight, the ability to underwrite trust with a Fremont letterhead was worth more than any per-board price difference.

The seed of everything that followed — the eventual IPO, the box-build empire, the satellite payloads — was planted in those dot-com-bust years, in the deliberate decision to be a small, weird, expensive, certifications-heavy shop that solved problems other people could not. Which is exactly the kind of strategic moat that, ten years later, would let Avalon do something almost no Indian EMS peer attempted: buy its own design house.

III. Inflection Point I: The Design Pivot (2009)

If you walk into a typical Electronics Manufacturing Services factory anywhere in the world, you will hear a phrase repeated like a mantra: "build to print." It means exactly what it sounds like. The customer hands over a finished design — schematics, gerber files, bill of materials, test instructions — and the EMS firm builds to that print, no questions asked. It is a low-margin, low-risk, low-defensibility business. The customer owns the intellectual property. The customer can move the work to another shop with sixty days' notice. The customer captures essentially all of the value created by the design itself, and pays the manufacturer a thin spread on the bill of materials.

For its first decade, Avalon was a build-to-print shop. A very good one — winning customers in aerospace and medical, with quality systems that survived audits from Boeing-tier OEMs — but still, fundamentally, executing on somebody else's blueprint. In 2009, with the global financial crisis still rippling through the supply chain and most contract manufacturers retrenching, Bicha and Srinivasan made the move that quietly defined the next fifteen years of the business. They acquired Sienna ECAD, the Electronic Computer-Aided Design house that had been operating as a sister entity within their broader corporate family.[^5]

To appreciate why this mattered, you have to understand what an ECAD team actually does. When a fabless customer — say, a sensor startup or a defence prime — has an idea for a new product, they typically know the system architecture: what the box must do, what inputs it must accept, what outputs it must drive, what environment it must survive. What they often do not have is the painstaking work of electrical layout: choosing exactly which components to source, drawing the multilayer copper traces that route signal between them at the speeds required, modelling the thermal and electromagnetic behaviour of the assembled board, and producing the manufacturing files that the factory then builds against. That work is part art, part physics, and it is where the bulk of a product's eventual cost — and reliability — is locked in. By owning an ECAD team, Avalon could now walk into a customer conversation not with "send us your files and we'll build them," but with "send us your concept and we'll design and build it."

In the language of Hamilton Helmer's 7 Powers, this is the moment Avalon installed its first real moat: switching costs. Once a customer's product is designed by Avalon's engineers, the design data, the supplier qualifications, the test fixtures, and the institutional memory of why a particular capacitor was chosen over its near-twin all live inside Avalon's walls. Moving to another EMS firm no longer means handing over a clean file package. It means paying for a full re-design, re-qualification, and re-certification — which in aerospace or medical can take eighteen to thirty-six months and cost millions of dollars. The customer is, in the industry's blunt phrase, "married."

The margin profile shifted accordingly. Build-to-print EMS work globally tends to deliver gross margins in the low double digits and EBITDA margins in the mid-to-high single digits. A design-and-build (or "build-to-spec") engagement, particularly in regulated end markets, can sustain meaningfully higher gross margins because the design IP and qualification effort earn a separate economic rent on top of the bill of materials.5 Avalon never broke out its design business as a standalone line — the value showed up indirectly, in the mix of customers and projects it was able to win.

That mix tilted sharply, post-2009, into two industries that would later become structurally important: aerospace (both civil and defence) and railway signalling, including a growing footprint of business with Indian and global rolling-stock OEMs. Both end markets share the same brutal logic. Certification is multi-year. Design cycles are long. Volumes are modest. But once you are in, you are in for the life of the platform — often ten to twenty years of recurring spare-and-support revenue from a single design win. The 2009 ECAD acquisition is what made those wins technically and commercially possible. And it set up the next, even more capital-intensive move that would arrive seven years later.

IV. Inflection Point II: The "Full Stack" Vertical Integration (2016)

There is a particular kind of conversation that EMS executives dread. It usually happens on a Friday afternoon, when a global customer's supply-chain head calls to say that the cable harness vendor in टियरुपुर Tiruppur has had a fire, or that the sheet-metal enclosure shop in Shenzhen has been shut down by a local power restriction, or that the injection-moulded plastic bezel from a tier-three supplier has failed an incoming inspection for the third lot running. The PCB is ready. The customer is waiting. The product cannot ship without the cable, the enclosure, the bezel. The EMS firm gets to explain, again, why a thirty-rupee component has held up a thirty-thousand-rupee assembly.

Around 2016, Avalon's leadership stopped trying to manage that problem and started trying to absorb it. The strategic insight was deceptively simple. If you have already invested in the most expensive, most specialised, most heavily certified part of the build — the PCB assembly — the marginal capital cost of bringing in the surrounding mechanical and electromechanical capabilities is small compared to the strategic prize. So Avalon went on a vertical-integration spree. It built and acquired capabilities in sheet-metal fabrication, injection moulding, cable and wire harness assembly, magnetics (transformers and inductors), and mechanical box build.6 The Chennai campus expanded. Capex climbed. Working capital ballooned. And the company's conversation with customers changed.

The new pitch was the "Box Build." Instead of shipping a finished PCB into the customer's own final assembly line, Avalon would ship the entire finished product — the populated board, inside the metal enclosure, with the harness pre-installed, the plastic facia attached, the firmware loaded, the unit functionally tested, the serial number etched, and the whole thing palletised for the customer's end customer. In many cases, Avalon's name never appeared on the product. The customer's brand was on the front. But economically, Avalon had moved from selling a component priced at, say, two hundred dollars to selling a complete unit priced at a thousand. The bill-of-materials revenue scaled up roughly five-fold. The margin per project scaled up proportionally less — but the gross profit per customer relationship and the switching cost per relationship both jumped meaningfully.6

This is what strategists call counter-positioning. Pure-play PCB assemblers, especially in mainland China and Vietnam, could not credibly follow Avalon up the box-build curve without abandoning their high-volume, high-throughput business model. The two operating systems are fundamentally incompatible. A Chinese mega-factory optimised for one million units a month of a single SKU is structurally hostile to a customer who wants two hundred units a quarter of a configurable industrial controller. Conversely, a small Indian or US engineering shop without the capital base to build sheet-metal and injection-moulding capacity in-house could not match Avalon's lead-time promise. By spending the capital to vertically integrate, Avalon parked itself in a competitive sweet spot where the giants could not reach down and the small shops could not reach up.

There was a second-order benefit that proved important during the COVID era and the subsequent "China Plus One" wave. When global OEMs began frantically diversifying their supply chains away from single-country dependence in 2020 and 2021, the firms that could quote a complete assembly — not just a board, not just a harness, but the whole product on a single purchase order — won an outsized share of the redirected work.7 Avalon's customer concentration in the United States, which had been a structural feature of the dual-shore model since inception, suddenly became a strategic accelerant. The phone started ringing with enquiries from companies that had spent twenty years assuming China would always be the answer, and now needed an alternative that could speak English, hold an AS9100 certificate, and ship a finished box.

That tailwind, paired with the capacity that had been quietly building since 2016, set up the capital-markets event that would finally take Avalon from a privately held curiosity to a publicly listed institution. Which brings us to the people who had to navigate that transition, and the particular philosophy of stewardship they brought to it.

V. Current Management: The Technocrat Custodians

If you spend any time with founder-led Indian industrial companies, you start to develop a sixth sense for the moments when a promoter is genuinely thinking like an owner versus moments when they are extracting cash. The tells are small and consistent. Salary structures. Bonus disclosures. Related-party transactions. The pattern of dividend distributions in the years immediately before an IPO. Avalon, on almost every one of these dimensions, screens unusually conservatively for an Indian listed industrial.

Start with कुनहम्मद बिचा Kunhamed Bicha, Chairman and Managing Director. Bicha co-founded the business in 1999 and, at the time of writing, has been at the helm for over twenty-five years.4 That longevity itself is unusual; the modal Indian listed company has cycled through at least two CEOs in the same window. More striking is the composition of his pay. Avalon's annual disclosures show Bicha's remuneration structured almost entirely as fixed salary, with no performance-linked bonus component and no stock-based compensation grants to himself.8 In a country where promoter-CEO pay packages are often the single largest item on an annual report's related-party note, this is a deliberate signal: Bicha makes his money from the equity, not from the payroll.

The equity story reinforces the salary story. Bicha personally holds a direct stake of roughly twenty-two per cent in the listed company, and the broader promoter group — which includes family trusts and Bhaskar Srinivasan's holdings — controls approximately forty-four per cent.9 That is a level of insider ownership which materially aligns long-term decision-making with public shareholders. It also means that Avalon's capital-allocation choices — whether to push capex into a new clean-energy facility, whether to take on a large lumpy aerospace contract that will tie up working capital for eighteen months, whether to refuse a high-volume consumer programme that would dilute margins — are being made by a team whose own wealth is overwhelmingly tied to the long-run compounding of book value per share rather than the next four quarters of reported EPS.

Bicha's personal story is itself worth pausing on, because it shapes the culture. He is, by training and temperament, an engineer first and a CEO second. Colleagues describe his shop-floor visits as the kind of slow, line-by-line walks where he stops at a single workstation for ten minutes to understand why a particular operator has chosen a particular soldering tip. He sits on technical review panels for new programmes. He has resisted, repeatedly, the temptation to take Avalon into businesses he does not personally understand — most notably, smartphone and white-goods assembly, where peers like Dixon and Foxconn-India have built much larger top lines on much thinner margins. The phrase one hears inside the company is that Bicha would rather grow at fifteen per cent at thirty per cent gross margin than at forty per cent at fifteen.

The institutional layer beneath the founders has been deliberately professionalised over the last several years. The most visible signal was the lateral hire of Shriram Vijayaraghavan as Chief Operating Officer, brought in from outside the founding family to handle the kind of plant-level execution discipline that a listed-company-scale operation demands.10 Around the IPO and in the period afterward, the board was expanded with independent directors carrying capital-markets, audit, and global manufacturing backgrounds — the kind of composition a SEBI-regulated company has to maintain, but in Avalon's case, also one that signalled a genuine willingness to dilute family control of governance.

The most poignant management event of the recent past has been the retirement of co-founder भास्कर श्रीनिवासन Bhaskar Srinivasan from executive responsibilities. After two and a half decades of partnership, the operating company has transitioned to a model where Bicha remains the strategic and capital-allocation anchor, while day-to-day operations sit with the professional management bench. For an Indian promoter-led business, succession from a founding duo to a single-CMD-plus-professional-team structure is a non-trivial cultural moment. It is the kind of transition that, done badly, breaks companies; done well, it is what allows them to outlive their founders.

Bicha has signalled, in earnings calls and at investor meetings, that this professionalisation is itself in service of the next decade of growth — a decade which will see Avalon deliberately expand into a set of end markets that, even a few years ago, would have looked like distractions from the core EMS business. Those new engines deserve their own examination.

VI. The "Hidden" Engines: Hydrogen & Semiconductors

In a non-descript corner of the Chennai campus, a relatively new production cell hums with a slightly different rhythm than the rest of the building. The boards being assembled here are larger and heavier than typical EMS work. The copper traces are thicker, the heat-sinks bulkier, the power semiconductors mounted on the boards are rated for hundreds of amps. These are power conversion sub-assemblies — the unglamorous, business-end electronics that take raw electricity from a renewable source and turn it into the precisely controlled DC current required to crack water molecules apart. They are bound, in many cases, for green-hydrogen electrolyzer manufacturers, both in India and overseas.

This is one of the quietest strategic bets on the Indian listed market. The world's emerging green-hydrogen economy — the double-carbon transition that virtually every major industrial economy has now committed to, in various forms — requires a vast build-out of electrolyzer capacity over the next two decades. Each electrolyzer stack needs sophisticated power electronics: rectifiers, controllers, monitoring boards, communication modules. Avalon's clean-energy roadmap, published in March 2025, laid out the company's intent to position itself as a tier-one supplier of these sub-assemblies to electrolyzer OEMs, particularly those building hydrogen capacity in India under the राष्ट्रीय हरित हाइड्रोजन मिशन National Green Hydrogen Mission.[^12] The bet is not that hydrogen will dominate the energy mix tomorrow. The bet is that somebody has to build the power electronics for the electrolyzers, and Avalon would prefer that to be Avalon.

Adjacent to that bet sits an even more recent one. In early 2025, Avalon announced its intent to manufacture high-precision components for semiconductor capital equipment — the machines that themselves make chips.11 To appreciate the strategic elegance of this move, consider where the actual money in the semiconductor value chain accumulates. Fab construction is enormously capex-heavy, but a meaningful slice of that capex flows to a small group of equipment makers — Applied Materials, Lam Research, KLA, Tokyo Electron, ASML and their tier-one suppliers — who in turn need extremely high-tolerance machined parts, sub-assemblies, and electromechanical modules. Avalon does not have to build a fab. It does not have to design a chip. It just has to supply the boring, precision-engineered pieces that go inside the tools. The market is smaller than chip-making itself, but the margins are healthier, the supplier list is shorter, and the qualification barrier — once crossed — is brutal for incoming competition. India's broader semiconductor mission has, as a structural by-product, created a domestic anchor demand for exactly these kinds of components.

A third, smaller move worth flagging is Avalon's minority stake — approximately four per cent — in Zepco Electricals, a domestic electric-motor manufacturer.12 On its own, a four per cent stake is not a strategic centrepiece. But read alongside the hydrogen and semiconductor moves, the pattern is unmistakable: Avalon is methodically positioning around the electrified, decarbonised, locally-manufactured industrial economy that India is now politically committed to building. Electric motors are an input into drones, e-mobility, industrial automation, and a long list of adjacent applications. A small equity stake gives Avalon visibility into the technology and the customer base without committing the capital to build a motor plant of its own.

Step back and look at the segment composition reported in Avalon's investor materials. The business now operates across four broad end-market verticals: Mobility (automotive, aerospace, rail), Industrial (factory automation, instrumentation), Communication (RF, networking, infrastructure), and Clean Energy and Medical (renewables, hydrogen, medical devices).13 Each behaves differently across the cycle. Mobility carries the lumpiness of aerospace contracts and the long platform tails of rail. Industrial is a closer proxy for the broader capex cycle. Communication has been the segment most exposed to the post-COVID inventory-destocking wave that gutted the US distribution channel through 2023 and into 2024. Clean Energy is the segment most likely, in management's own framing, to be the "coiled spring" of the next two to three years, as both hydrogen capex and India's domestic renewable build-out translate from announcement into actual purchase orders.

The investor question is whether the mix of these segments, weighted by the order book, can deliver the kind of operating leverage and margin expansion that turns Avalon from a respected mid-cap EMS player into something materially larger. That question is really a question about competitive structure, which is the right lens for the next section.

VII. The Playbook: 7 Powers & Porter's Analysis

When Hamilton Helmer wrote 7 Powers, he was attempting something deceptively ambitious — to compress every durable source of competitive advantage into a single, mutually exclusive framework. Run Avalon through that framework and a clear primary power emerges, with a recognisable secondary power layered on top.

The primary power is Switching Costs. Once Avalon's engineering team has designed and qualified a board — and especially a complete box build — for an aerospace, medical, or industrial customer, the cost of moving that programme to another EMS firm is enormous and the timeline is brutal. Aerospace programmes typically require a full re-qualification cycle of eighteen to thirty-six months at the new supplier, often with the original equipment manufacturer paying for parallel production runs at both sites until the new supplier is proven. Medical devices subject to ISO 13485 quality systems face similar friction. The result is a customer base that, once won, tends to deepen rather than churn — a structural feature that shows up in Avalon's disclosures as long-running relationships with marquee global OEMs that have lasted over a decade.13

The secondary power is Counter-Positioning. The dual-shore design-plus-manufacture model — Silicon Valley-facing front office, Chennai-based execution, vertically integrated mechanical and electromechanical capability — is structurally difficult for incumbents to copy without sacrificing the very thing that makes them competitive in their own segment. A pure-play domestic US EMS shop cannot compete on labour cost. A pure-play Chinese assembler cannot offer the IP-protection comfort that a US defence prime needs. A purely "build-to-print" Indian peer cannot match the engineering depth. Avalon's geography and capability stack are the answer to a question that none of the established competitors are organised to ask.3

Run the same business through Michael Porter's Five Forces and the picture remains favourable, with some genuine vulnerabilities worth naming out loud.

Threat of new entrants is structurally low. The certifications that gate the most attractive end markets — AS9100 for aerospace, ISO 13485 for medical devices, IATF 16949 for automotive, and a long tail of programme-specific approvals — typically take three to seven years to earn from a standing start, and require continuous re-audits to maintain. A would-be entrant cannot simply build a factory and start quoting on aerospace work next quarter. This is the moat that makes high-mix, low-volume EMS structurally more defensible than its high-volume cousin.

Bargaining power of buyers is moderate. Avalon's customer base is concentrated enough that the loss of any one large account would be material — a fact the company's own risk factors disclose plainly. But that bargaining power is materially blunted by the switching costs described above, and further blunted by the box-build complexity. A customer who buys a fully integrated unit from Avalon cannot, in practice, take the work to a competitor who only does PCB assembly without first finding a sheet-metal vendor, a harness vendor, a moulding vendor, and an integrator — at which point the cost and lead-time advantage of the move has usually evaporated.

Bargaining power of suppliers has been the area of most acute pain in the recent past. The 2021 and 2022 global semiconductor shortage exposed every EMS firm globally to component-level price spikes and allocation gymnastics, and Avalon was not exempt. Vertical integration on the mechanical side of the bill of materials helps, but the firm is still exposed to the global merchant market for active electronic components, which is dominated by a small number of distributors and original component manufacturers.

Threat of substitutes is industry-specific. For the mission-critical end markets Avalon serves, there is no real substitute for high-mix, design-led EMS — the alternative is for the customer to do it themselves, which most large OEMs have spent two decades unwinding precisely because of the operational drag.

Industry rivalry is intense in aggregate but fragmented in the high-complexity niche. Avalon competes with global names like Benchmark Electronics, Plexus, Sanmina, and on certain programmes with regional Indian players like Kaynes Technology and Syrma SGS, each of whom occupies its own corner of the mix-versus-volume map.2 The most relevant comparison is probably to Kaynes — a Mysuru-based peer that has aggressively pursued its own version of high-mix, high-complexity EMS with a meaningfully larger top line but a different segment mix. The two are best understood as adjacent rather than head-to-head, and India's overall EMS market is large enough that both can grow without directly cannibalising each other for the foreseeable future.

Which is the right framing for honestly considering the optimistic and pessimistic cases for the next phase of the business.

VIII. Analysis: Bull vs Bear, and a Myth-vs-Reality Check

Every listed EMS company in India is, at the moment, the recipient of a particular kind of narrative tailwind. The headlines write themselves: "Make in India," Production-Linked Incentive (PLI) schemes, China Plus One, electronics import substitution, the renewables build-out. Investors who have lived through enough cycles know that these macro narratives can mask large differences in execution, segment mix, and balance-sheet quality between superficially similar companies. So before walking through the bull and bear cases, it is worth pressure-testing the consensus narrative with a brief myth-versus-reality pass specific to Avalon.

Myth: Avalon is a beneficiary of smartphone and white-goods PLI tailwinds. Reality: Avalon has deliberately stayed out of those high-volume consumer segments. The PLI flows most relevant to Avalon are the ones around industrial electronics, defence offsets, and aerospace localisation — important, but smaller and less visible in mainstream financial press than the smartphone PLI numbers.

Myth: Avalon's US revenue concentration is just a function of its founders' geography. Reality: it is also a function of where the high-mix, low-volume customer base structurally lives. Roughly sixty per cent of revenue has historically been generated from US customers,13 which is both an asset (access to the deepest and most demanding industrial electronics market in the world) and a liability (a single-country macro shock can ripple through the order book, as the 2023 destocking cycle demonstrated).

Myth: Box-build is just a higher-priced version of PCB assembly. Reality: the working-capital intensity is significantly higher. A larger bill of materials means more inventory days, more debtor days, and more capital tied up per rupee of revenue. Margin expansion is real, but it has to be earned against a working-capital headwind.

With those clarifications, the bull case writes itself. The structural China-Plus-One tailwind is real and multi-year. The 2023-2024 US destocking cycle — in which Avalon's US-facing distribution customers worked down inventory built up during the post-COVID component shortage — appears, on the latest available commentary, to have substantially normalised, setting up the comparative base for re-stocking in the period ahead.14 The box-build mix is climbing from a meaningful share of revenue toward, in management's stated ambition, a strategically dominant share over the medium term, with attendant margin and switching-cost benefits. The clean-energy and semiconductor adjacencies offer optionality that does not yet show up in the visible order book but could become material within the next three to five years. And the management team is owner-operated, conservatively paid, and increasingly institutionalised — a combination that screens better than the median Indian mid-cap industrial.

The bear case is equally honest and equally important. Working-capital intensity has been the most consistent operational drag, and is structurally embedded in the business model rather than being a transient problem. Aerospace contracts are lumpy by nature; a single large platform win can flatter one year's growth and a single delay can do the opposite. The roughly sixty per cent US revenue concentration is a real risk, particularly in a world where US industrial demand is itself cyclically sensitive and where geopolitical tariff regimes between the US and China can change without notice. The Indian EMS sector has, in aggregate, traded at valuation multiples that price in a significant amount of secular optimism — and Avalon's specific multiple has not been immune to that.14

This is where Helmer and Porter circle back into the investment conversation. The most defensible reading of Avalon is that it is a "cyclical compounder" rather than either a pure compounder or a pure cyclical. The end markets are cyclical and the working capital cycle amplifies that. But the design-led, switching-cost-protected, vertically integrated business model creates a base of recurring programme revenue that grows on top of the cyclicality rather than washing in and out with it.

For investors trying to monitor the business in real time, the three KPIs that matter most can be stated simply, without doing the arithmetic for the reader.

The first is the share of revenue from Box Build (versus standalone PCB assembly). This is the single most informative number in the deck, because it captures the strategic migration up the value chain, the switching-cost deepening, and the margin-mix expansion in one metric. The second is the order book composition and book-to-bill ratio, particularly the split between US and India and the share contributed by Clean Energy and Aerospace — these tell the investor where future revenue will come from and how lumpy it will be. The third is working-capital days (the combined inventory and receivables cycle), because this is where the business model's biggest structural friction lives, and where any genuine operational improvement will show up first.

Track those three honestly, and most of the noise in any given quarter becomes interpretable.

IX. Epilogue & Conclusion

Twenty-five years on from that Fremont office where Bicha and Srinivasan first drew the dual-shore map on a whiteboard, the business they built has become almost the platonic example of what India's industrial renaissance was supposed to produce — and what, in the smartphone-assembly headlines, often gets missed. It does not stamp out millions of identical units. It does not chase the lowest-cost contract. It does not put its name on a consumer product. It does something quieter and, on a long enough timeline, possibly more durable: it sits between the world's most demanding industrial OEMs and the soldering iron, taking on the engineering risk, the certification burden, the working-capital intensity, and the lead-time anxiety, and turning all of it into the boring physical objects that make satellites work, locomotives move, electrolyzers crack water, and medical pumps deliver exact micro-doses.

The journey from a small cross-border shop to a listed institution on the भारतीय राष्ट्रीय शेयर बाजार National Stock Exchange of India has involved, among other things: two major strategic inflections — the 2009 design pivot and the 2016 vertical integration push — both of which were under-appreciated at the time and look, in retrospect, like the moves that determined everything else. It has involved a management team that has resisted the usual Indian-promoter temptations around pay, related-party transactions, and unrelated diversification. It has involved an unfashionable commitment to high-mix, low-volume work in an investor market that has periodically been more excited about the volume side of the equation. And it has involved a willingness to plant seeds in adjacencies — hydrogen power electronics, semiconductor equipment components, a small electric-motor stake — that may or may not bear fruit on any given quarterly call, but together describe a coherent bet on the electrified, decarbonised industrial economy of the next decade.

Whether that bet earns superior compounding returns from any particular entry point is a question for individual investors, their time horizons, and their own assessment of valuation against the cyclical realities of the EMS industry. What is harder to dispute is that Avalon Technologies has built something genuinely unusual: a vertically integrated, design-led, dual-shore manufacturing house, owner-operated by a founder who still walks the shop floor a quarter-century after he first switched on the lights, and that quietly serves as the architectural backbone for a surprising slice of the world's mission-critical electronics. In an industry where the most valuable companies are often the ones you have never heard of, that is exactly the kind of story that rewards a careful, second-look investor — and exactly the kind of story this series exists to surface.

References

References

-

NSE India Company Profile: AVALON — National Stock Exchange of India ↩

-

EMS Sector Report: The High-Mix Low-Volume Opportunity — Nuvama Institutional Equities, 2024 ↩↩

-

Red Herring Prospectus (RHP) — SEBI / Avalon Technologies, 2023-03-23 ↩↩↩

-

Sienna-Avalon Group Corporate History — AvalonSienna.com ↩↩↩

-

Avalon Technologies: A Bet on High-Complexity EMS — Moneycontrol, 2023-04-03 ↩

-

Investor Presentation Q4 FY24 — Avalon Technologies, 2024-05 ↩↩

-

Analysis of Promoter Compensation and Alignment — Simply Wall St ↩

-

Avalon Technologies expands into Semiconductor Components — Business Standard, 2025-01-10 ↩

-

Earnings Call Transcript Q4 FY24 — Avalon Technologies, 2024-05-17 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube