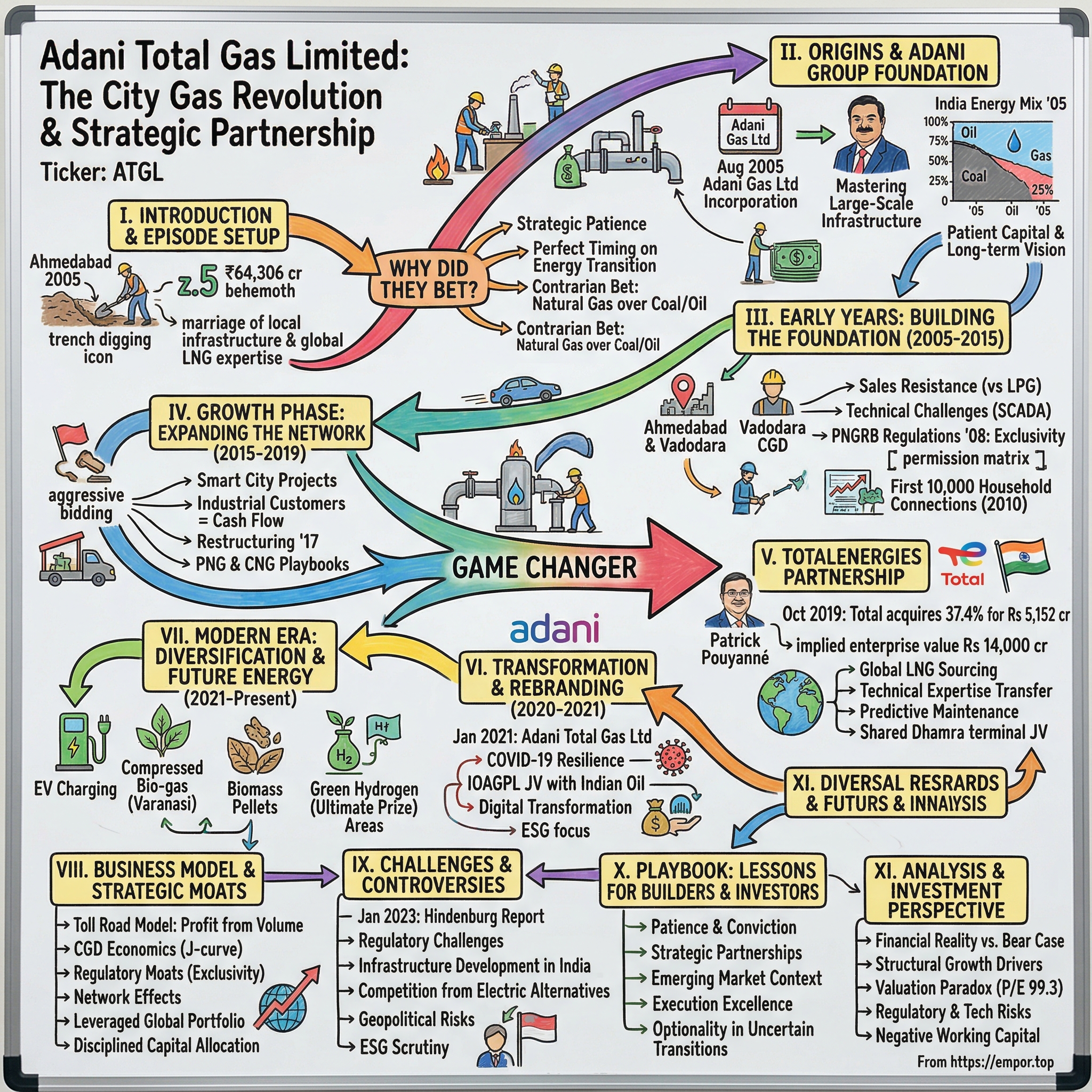

Adani Total Gas Limited: The City Gas Revolution & Strategic Energy Partnership

I. Introduction & Episode Setup

Picture this: It's 2005 in Ahmedabad, and while most of India runs on coal and diesel, a relatively unknown infrastructure company starts laying pipes under the streets of Gujarat's commercial capital. No fanfare, no grand announcements—just workers digging trenches and welding steel pipes that would eventually carry natural gas to millions of homes and businesses. Fast forward to today, and that quiet beginning has transformed into Adani Total Gas Limited (ATGL), a ₹64,306 crore behemoth that's reshaping how India consumes energy.

The company supplies natural gas through an intricate network of pipelines to domestic kitchens, commercial establishments, industrial plants, and CNG stations across 33 geographical areas. With the Adani Group and French energy giant TotalEnergies each holding 37.4% stake, ATGL represents one of India's most significant energy partnerships—a marriage of local infrastructure prowess and global LNG expertise.

But here's the fascinating question: How did a 2005 startup navigate India's complex regulatory landscape, build trust in an unfamiliar fuel source, and convince one of Europe's largest energy companies to bet billions on Indian gas distribution? The answer involves strategic patience, perfect timing on India's energy transition, and a contrarian bet that natural gas—not coal or oil—would power India's urban future.

This is the story of building essential infrastructure in an emerging market, the art of strategic partnerships, and how a company positioned itself at the intersection of India's economic growth and environmental consciousness. It's about recognizing that sometimes the most valuable businesses aren't the flashiest tech unicorns, but the ones laying pipes under your feet.

II. Origins & The Adani Group Foundation

The conference room in Adani House, Ahmedabad, must have been an interesting place on August 5, 2005. While India was celebrating its IT boom and the world was obsessing over crude oil hitting $60 per barrel, Gautam Adani was incorporating a company called Adani Gas Limited in Navrangpura—a business that would sell a fuel most Indians had never used through infrastructure that didn't exist yet.

To understand why this mattered, you need to understand the Adani Group's DNA. By 2005, Gautam Adani had already built one of India's largest commodity trading operations, transformed Mundra from a sleepy coastal town into India's largest private port, and was eyeing the power sector. The group had mastered the art of building large-scale infrastructure where others saw only risk—whether ports, logistics, or power plants. But natural gas distribution? That was different. India's energy landscape in 2005 was stark: coal dominated with over 55% of the energy mix, oil accounted for about 30%, while natural gas represented barely 7% of total energy consumption. The country had minimal gas pipeline infrastructure—most of what existed served fertilizer plants and a handful of power generators. City gas distribution, the business of piping gas to homes and businesses, was virtually non-existent outside of Mumbai and Delhi.

But Gautam Adani saw something others didn't. He understood that India's urbanization wave—with millions moving to cities every year—would create massive energy demand. More importantly, he recognized that environmental pressures would eventually force India to diversify away from coal. Natural gas, cleaner than coal but more reliable than renewables, would be the bridge fuel. The question wasn't if, but when.

The Adani Group's infrastructure DNA made them uniquely positioned for this bet. They had already mastered the art of working with state governments, navigating India's byzantine regulatory landscape, and most critically, they understood patient capital. Port infrastructure taught them that the real money wasn't in quick returns but in building assets that would generate cash flows for decades.

When Adani Gas Limited was incorporated that August day in 2005, it wasn't just starting a company—it was betting on India's energy transition a full decade before the Paris Climate Agreement would make it fashionable. The initial capital was modest, the team small, but the vision was audacious: build the pipes today that would carry the fuel of tomorrow.

III. Early Years: Building the Foundation (2005-2015)

The first CGD license came through for Ahmedabad and Vadodara in Gujarat—home turf for the Adani Group. If you've never tried to convince an Indian household to switch from LPG cylinders to piped gas, you haven't experienced true sales resistance. The LPG cylinder system, despite its inconvenience, was deeply embedded in Indian domestic life. Every household knew their cylinder delivery guy, had perfected the art of gauging when the gas would run out, and most importantly, trusted the system they knew.

Adani Gas faced a chicken-and-egg problem that would define its early years. To make piped natural gas (PNG) economically viable, you needed scale—thousands of connections per area. But to get consumers to sign up, you needed to prove reliability. And to prove reliability, you needed infrastructure that didn't exist yet. The solution? Start with industrial and commercial customers who could anchor the economics, then gradually extend to households.

The Faridabad and Khurja expansions in Haryana and Uttar Pradesh respectively weren't random choices. These were industrial clusters where factories were desperate for cleaner alternatives to coal and diesel. Every textile mill or ceramic factory that switched to natural gas became a proof point, a reference customer that made the next sale easier. The regulatory framework crystallized in 2008 when the Petroleum and Natural Gas Regulatory Board issued regulations on March 19th, 2008, establishing exclusivity periods for CGD operators. This was game-changing—it meant that once you won a license for a geographical area, you had exclusive rights to build and operate the network for a specified period. Suddenly, the economics made sense. The regulatory moat meant you could invest millions in infrastructure knowing competitors couldn't cherry-pick your profitable customers.

But regulations don't lay pipes or connect homes. The real work happened in the trenches—literally. Each kilometer of pipeline required permissions from multiple authorities: municipal corporations for road-cutting, traffic police for diversions, pollution control boards for environmental clearances. Adani Gas developed what internally they called the "permission matrix"—a complex spreadsheet tracking hundreds of approvals across multiple cities.

The CNG station rollout followed a different playbook. While PNG connections grew slowly, CNG for vehicles had immediate demand thanks to Supreme Court mandates for cleaner transportation fuels in major cities. Each CNG station was a ₹2-3 crore investment, but the payback was faster than household connections. Auto-rickshaw drivers, taxi operators, and bus fleets needed CNG to comply with regulations. It wasn't aspirational; it was mandatory.

By 2010, Adani Gas had connected its first 10,000 households—a number that sounds impressive until you realize Mumbai's Mahanagar Gas had already crossed 500,000. But Adani was playing a different game. While established players fought over mature markets, Adani focused on virgin territories where they could shape consumer behavior from scratch.

The technical challenges were immense. Natural gas needs to be odorized for safety (pure methane is odorless), pressure needs constant monitoring, and the entire network needs 24/7 surveillance. One major leak could set back consumer confidence by years. Adani Gas invested heavily in SCADA (Supervisory Control and Data Acquisition) systems, bringing space-age technology to what was essentially a plumbing business.

The slow burn strategy was testing investor patience. Between 2005 and 2015, revenues grew steadily but unspectacularly. The company was burning cash to build infrastructure, with the promise of future returns once the network achieved critical mass. It required a particular kind of investor mindset—one that understood infrastructure cycles and believed in India's long-term energy transition.

IV. The Growth Phase: Expanding the Network (2015-2019)

2015 marked an inflection point, though few recognized it at the time. Modi's government had just launched ambitious smart city projects, global oil prices had collapsed from $100 to $50 per barrel making gas relatively more attractive, and urban air quality was becoming a political issue. Suddenly, Adani Gas's patient infrastructure building looked prescient.

The company's expansion strategy shifted into high gear. Instead of the methodical city-by-city approach of the early years, Adani Gas began bidding aggressively for multiple CGD licenses simultaneously. The PNGRB's authorization rounds became battlegrounds where Adani competed with Indian Oil, GAIL, and other energy giants for the right to serve new geographical areas.

From 2012 to 2014, PNGRB played a key role in authorizing the development of national and regional natural gas pipelines, as well as city gas distribution (CGD) networks, creating opportunities that Adani Gas seized aggressively. Each new license wasn't just about that specific territory—it was about creating network density that would eventually lower operational costs across the entire system.

The 2017 restructuring, when Adani Enterprises Limited transferred 100% equity shares to Adani Gas Holdings Limited, wasn't just corporate housekeeping. It signaled the group's intent to professionalize and potentially bring in strategic partners. The gas business was no longer an experiment within the conglomerate—it was a core vertical deserving focused attention and capital allocation.

Industrial customers became the cash flow engine during this phase. A single textile mill switching to natural gas could generate revenues equivalent to 1,000 household connections. Adani Gas developed specialized teams that could conduct energy audits, demonstrate cost savings, and manage the technical transition from coal or furnace oil to natural gas. These weren't just sales teams; they were energy consultants who understood industrial processes intimately.

The PNG push to households required different tactics. Adani Gas pioneered the "colony approach"—instead of targeting individual homes, they would negotiate with entire residential societies. Get the society's managing committee on board, conduct safety demonstrations, offer attractive connection packages, and you could add 500 connections in one go. It was mass customization—standardized processes with localized execution.

CNG infrastructure expanded from basic dispensing stations to complex mother-daughter configurations. Mother stations compressed gas from pipelines, while daughter stations in areas without pipeline connectivity received gas through cascades (specialized high-pressure cylinder trucks). This hub-and-spoke model allowed Adani Gas to serve customers beyond their pipeline network, capturing revenues while the permanent infrastructure caught up.

Competition intensified as the market's potential became obvious. Indian Oil, Bharat Petroleum, and GAIL all ramped up their CGD investments. But Adani Gas had an advantage—they weren't burdened by legacy thinking from the oil industry. While competitors saw CGD as an extension of their petroleum business, Adani saw it as city infrastructure, more akin to water or electricity distribution.

The regulatory environment evolved favorably. From 2018 to 2020, PNGRB focused on accelerating the expansion of City Gas Distribution (CGD) networks in multiple cities across India. It issued new licenses for CGD networks, helping to increase the reach of piped natural gas (PNG) to households and compressed natural gas (CNG) to vehicles. The government's push wasn't just about energy security anymore—it was about urban air quality, climate commitments, and creating jobs in the gas value chain.

By early 2019, Adani Gas was operating in 11 geographical areas, had crossed 100 CNG stations, and was adding household connections at an accelerating pace. The infrastructure investments of the previous decade were finally yielding returns. EBITDA margins improved as network utilization increased, validating the patient capital approach.

But Gautam Adani knew that to truly scale, Adani Gas needed two things: access to global LNG markets and deep technical expertise in gas distribution. The company had built the pipes, won the licenses, and created the market. Now it needed a partner who could ensure reliable gas supply and bring world-class operational capabilities. The stage was set for one of Indian energy sector's most significant partnerships.

V. The TotalEnergies Partnership: Game Changer (2019)

The boardroom at Total's headquarters in La Défense, Paris, must have been buzzing with anticipation in early 2019. Patrick Pouyanné, Total's CEO, had been eyeing the Indian market for years. Here was a country where natural gas needed to increase to 15% of the energy mix by 2030, but was stuck at around 7%. The math was simple: even modest market share in this growth would create enormous value.

On the other side, Gautam Adani was orchestrating one of his signature moves. He had built valuable infrastructure, secured regulatory licenses, and created market presence. But he understood that global LNG markets were volatile, technical expertise was crucial for safety and efficiency, and international credibility would accelerate growth. He needed a partner, not just an investor.

The October 2019 announcement sent shockwaves through India's energy sector: Total would acquire 37.4% stake in Adani Gas Limited for Rs 5,152 crore, creating one of India's largest downstream energy partnerships. But this wasn't a simple equity sale—it was a strategic architecture designed to align interests perfectly.

The valuation implied an enterprise value of nearly Rs 14,000 crore for Adani Gas, a massive premium to the infrastructure invested. Critics called it expensive; Pouyanné called it "buying tomorrow's infrastructure at today's prices." Total wasn't just buying pipes and licenses—they were buying optionality on India's energy transition.

TotalEnergies (as Total rebranded itself in 2021) brought capabilities that transformed Adani Gas overnight. With operations in 130 countries and decades of LNG expertise, Total could source gas from Qatar, the US, Africa, or Australia depending on market conditions. Their trading desks in London, Singapore, and Houston could optimize procurement in ways a domestic Indian company never could.

The technical expertise transfer was immediate and tangible. Total deployed teams to review Adani Gas's operations, introducing predictive maintenance systems that reduced downtime by 30%, safety protocols that exceeded Indian standards, and digital tools that improved network efficiency. This wasn't passive investment—it was active capability building.

The newly commissioned 5 MTPA Dhamra joint venture terminal between Adani and TotalEnergies on India's east coast exemplified the partnership's strategic value. Adani brought land, permits, and local execution capability. Total brought LNG sourcing, regasification technology, and global financing relationships. Together, they could move faster and more efficiently than either could alone.

The partnership's structure was cleverly designed. Both Adani and Total held 37.4% each, with public shareholders owning the balance. This meant neither partner had absolute control, forcing collaboration on major decisions. It also meant both partners were equally invested in success—no free riding was possible.

For Total, this wasn't just about India. It was about demonstrating their commitment to natural gas as a transition fuel globally. While European peers were divesting fossil fuel assets under ESG pressure, Total argued that natural gas was essential for emerging markets to transition away from coal. The Adani partnership became their proof point.

The market's reaction was initially mixed. Some investors worried about the premium paid, others about governance given the Adani Group's aggressive growth style. But institutional investors who understood infrastructure cycles saw the strategic logic. Here was a partnership combining local execution with global capabilities, focused on essential infrastructure in a growing market.

Internal changes at Adani Gas accelerated post-partnership. The company instituted global best practices in procurement, standardizing specifications across all equipment purchases. Safety training was overhauled with Total's HSE (Health, Safety, Environment) protocols. Financial reporting became more granular, with metrics benchmarked against global CGD operators.

The net acquisition cost of approximately $600 million over 2019-2020 looked like a bargain in retrospect. Total hadn't just bought equity—they had bought a platform to participate in India's energy transformation. As Pouyanné told investors, "In India, we're not just selling molecules, we're building the infrastructure for those molecules to flow through."

By early 2020, the partnership was already yielding results. Gas sourcing costs dropped by 15% through Total's global procurement. New geographical area bids were won partly due to Total's technical credibility. International banks were suddenly willing to finance expansion at lower rates. The transformation from domestic player to global partnership was complete.

VI. Transformation & Rebranding (2020-2021)

January 2021: The company's new logo appeared across thousands of CNG stations, office buildings, and pipeline markers—Adani Total Gas Limited was born. The rebranding wasn't cosmetic; it represented a fundamental transformation in how the company saw itself and how it wanted to be perceived.

COVID-19 had just tested every assumption about energy demand. During the strictest lockdown period in April-May 2020, CNG sales collapsed by 80% as vehicles stayed off roads. Industrial demand plummeted as factories shut. Even household PNG consumption patterns changed as commercial kitchens closed but residential usage spiked. Lesser companies might have retrenched; Adani Total Gas accelerated.

The pandemic response revealed the partnership's strength. While revenues dropped, the company used the period to accelerate infrastructure projects. With minimal traffic, pipeline laying that usually took months was completed in weeks. CNG stations were upgraded with contactless payment systems. Digital customer service platforms, planned for gradual rollout, were launched immediately.

The formation of Indian Oil-Adani Gas Pvt. Ltd. (IOAGPL), the joint venture with Indian Oil Corporation, was masterfully timed. Announced during the pandemic when valuations were depressed, this JV gave Adani Total Gas access to 19 additional geographical areas without the full capital investment. Indian Oil brought their retail network—imagine CNG pumps at every IOCL petrol station—while Adani Total Gas brought execution expertise.

Digital transformation wasn't just about customer apps and online bill payment. The company deployed IoT sensors across their pipeline network, creating a digital twin that could predict failures before they occurred. Leak detection systems using AI could identify potential issues from pressure variations invisible to human operators. The control room in Ahmedabad looked more like a tech company's operations center than a traditional utility.

Supply chain resilience became an obsession. The pandemic had exposed vulnerabilities—imported equipment stuck at ports, specialized technicians unable to travel, critical spares unavailable. Adani Total Gas responded by localizing procurement wherever possible, creating vendor development programs that would build domestic capability while reducing import dependence.

The brand evolution was carefully orchestrated. The company wasn't just distributing gas anymore—it was enabling India's energy transition. Marketing campaigns featured children breathing cleaner air, industries reducing emissions, and vehicles running on indigenous fuel. The narrative shifted from utility service to environmental partnership.

Employee culture transformed as well. The Total influence brought a more structured approach to career development, with global mobility programs allowing Indian engineers to train at Total facilities worldwide. Safety became almost religious—every meeting started with a safety moment, every site visit required HSE briefings, and lost-time injuries became unacceptable rather than unfortunate.

Financial markets began recognizing the transformation. Despite pandemic pressures, the stock price recovered quickly and then surged as investors appreciated the resilience of city gas distribution. Unlike discretionary businesses, CGD was essential infrastructure. People might defer car purchases, but they still needed cooking gas and transportation fuel.

The governance improvements were subtle but significant. Board meetings became more structured with detailed pre-reads and focused agendas. Risk management evolved from reactive to predictive with scenario planning for everything from regulatory changes to climate events. Quarterly earnings calls became mini-tutorials on India's energy transition, educating investors about the long-term opportunity.

By late 2021, Adani Total Gas had emerged from the pandemic stronger than it entered. The company had used the crisis to accelerate digital transformation, strengthen supply chains, and deepen its partnership with Total. Most importantly, it had proven the resilience of its business model. As India recovered, Adani Total Gas was positioned to capture the rebound in energy demand.

VII. Modern Era: Diversification & Future Energy (2021-Present)

The electric vehicle charging station in Mumbai's Bandra-Kurla Complex doesn't look like much—just a few parking spots with charging posts. But for Adani Total Gas, it represents a strategic pivot that would have seemed impossible five years ago. The company that built its fortune on natural gas is now betting on electricity, biomass, and hydrogen. This isn't confusion; it's evolution.

The incorporation of Adani TotalEnergies E-mobility Limited (ATEL) in 2021 signaled the company's recognition that transportation energy was fragmenting. While CNG would remain relevant for commercial vehicles and public transport, private vehicles were going electric. Instead of fighting this transition, Adani Total Gas decided to own it.

The numbers tell the acceleration story: 460+ CNG stations after adding 126 new ones in FY23, over 7 lakh household connections after adding 1.24 lakh in a single year, presence in 33 geographical areas with another 19 through the IOAGPL joint venture. But the real story isn't the quantity—it's the quality of expansion.

The Varanasi compressed bio-gas station, commissioned in 2021, deserves special attention. Using agricultural waste and municipal solid waste, the facility produces bio-CNG that's chemically identical to natural gas but carbon-neutral. It's a template for turning India's agricultural waste problem into an energy solution. Farmers who once burned stubble now sell it for energy production.

Adani TotalEnergies Biomass Limited (ATBL) is pursuing an even more ambitious vision. The company plans to establish biomass pellet production facilities that can replace coal in industrial boilers. It's a bridge technology—cleaner than coal, more reliable than solar, and using India's abundant agricultural residue. The addressable market is enormous: thousands of industrial units still burning coal but unable to switch directly to gas or electricity.

The 104 EV charging stations across 26 locations might seem modest compared to the CNG network, but the strategic placement is brilliant. These aren't random locations—they're at Adani's airports, ports, and commercial complexes where dwell time is high and customers are affluent early adopters. Each charging session is a data point, helping the company understand usage patterns before massive rollout.

The geographical expansion strategy has evolved from opportunistic to scientific. Using heat maps of economic activity, pollution levels, and infrastructure readiness, Adani Total Gas identifies areas where gas penetration can create maximum impact. It's not just about winning licenses—it's about choosing battles where victory creates long-term value.

States like Madhya Pradesh, Tamil Nadu, and Odisha represent different challenges and opportunities. In Madhya Pradesh, industrial clusters need gas for manufacturing. In Tamil Nadu, the focus is on replacing diesel generators in commercial establishments. In Odisha, it's about providing cooking gas to households still using biomass. One size doesn't fit all, and Adani Total Gas has learned to customize.

The technology infrastructure has become a competitive advantage. The company's digital command center can monitor every CNG station's performance in real-time, predict equipment failures, optimize gas procurement based on demand forecasts, and even detect theft or leakage through pattern recognition. It's automated intelligence augmenting human decision-making.

Green hydrogen remains the ultimate prize, though still years from commercial viability. Adani Total Gas is positioning itself as the distribution infrastructure for whatever clean molecule wins—whether compressed natural gas today, bio-CNG tomorrow, or hydrogen eventually. The pipes and stations are fuel-agnostic with modifications. The customer relationships and regulatory licenses are the real moat.

The partnership dynamics with TotalEnergies continue to evolve. Total's own transformation from oil major to multi-energy company aligns perfectly with Adani Total Gas's diversification. Joint R&D projects explore everything from hydrogen blending in natural gas networks to battery storage at CNG stations for grid stabilization.

Recent performance validates the strategy. Despite global energy price volatility, Adani Total Gas has maintained stable margins through dynamic pricing and efficient procurement. Volume growth continues as India's gas consumption rises steadily. The company isn't just riding India's energy transition wave—it's helping create it.

VIII. Business Model & Strategic Moats

Understanding Adani Total Gas's business model requires thinking like a toll road operator, not an energy trader. The company doesn't make money from gas price fluctuations—it profits from volume flowing through its infrastructure. Build the pipes, connect the customers, and collect a margin on every molecule that passes through. It's beautifully simple and devastatingly effective when executed well.

The CGD economics are compelling once you understand the J-curve dynamics. Initial investment is massive—laying pipelines costs ₹30-50 lakhs per kilometer in urban areas, CNG stations require ₹2-3 crores each, and household connections need ₹5,000-10,000 per home including last-mile infrastructure. But once built, the marginal cost of flowing gas is minimal. A pipeline with 30-year life can be depreciated over decades while generating cash from day one.

The regulatory framework creates the first moat. PNGRB authorizes companies to develop and operate CGD networks, supplying piped natural gas (PNG) to households, industries, and commercial establishments, as well as compressed natural gas (CNG) for vehicles. The board conducts periodic bidding rounds to encourage CGD network expansion. Once you win a geographical area, you have exclusive rights for infrastructure development and marketing exclusivity for a defined period. Competitors can't cherry-pick your profitable commercial customers while leaving you with expensive household connections.

Network effects strengthen over time. Each new connection makes the network more valuable for existing users. Industrial customers want reliability that comes from diverse demand. Households want the convenience of widespread CNG stations for their vehicles. CNG vehicle owners want ubiquitous refueling options. It's a virtuous cycle where growth begets growth.

The TotalEnergies partnership provides unique advantages in LNG sourcing. While standalone Indian CGD companies negotiate with suppliers from a position of weakness, Adani Total Gas leverages Total's global portfolio. When spot LNG prices spike, Total's long-term contracts provide stability. When specific sources face disruption, Total's diversified supply ensures continuity.

Capital allocation has been disciplined despite aggressive growth. The company follows an 80-20 rule: 80% of capital goes to proven markets with established demand, 20% to frontier areas with future potential. This balanced approach ensures steady returns while maintaining optionality on emerging opportunities.

ATGL operates in 34 geographical areas directly and another 19 through the IOAGPL joint venture, creating one of India's largest CGD footprints. But coverage isn't just about geography—it's about density within areas. The company focuses on achieving 40-50% penetration in established areas before expanding to new ones, ensuring economies of scale.

The competitive dynamics are fascinating. Against PSU giants like GAIL and Indian Oil, Adani Total Gas competes on execution speed and customer service. Against private players like IGL and MGL, they leverage the Total partnership for technical superiority and financial strength. Against new entrants, they use their established infrastructure and customer relationships as barriers.

Infrastructure sharing agreements multiply capital efficiency. Instead of building parallel networks, CGD operators increasingly share pipeline capacity in non-competing areas. Adani Total Gas has mastered this, using others' infrastructure to serve customers while charging fees for access to their own networks. It's collaborative competition—competing fiercely in the market while cooperating on infrastructure.

The margin structure reveals the model's resilience. Unlike oil marketing companies that suffer when crude prices spike, CGD operators maintain relatively stable margins. Gas purchase costs are passed through to customers with regulatory approval. The company earns from infrastructure usage, not commodity speculation. In FY23, EBITDA margins remained healthy despite global gas price volatility.

Customer stickiness is underappreciated. Once a household converts to PNG, reverting to LPG cylinders is rare. Once an industry invests in gas-based equipment, switching fuels requires capital expenditure. Once a vehicle owner buys a CNG car, they're locked in for the vehicle's life. This isn't subscription software, but customer lifetime value is similarly attractive.

The working capital dynamics are favorable. Customers prepay through deposits, gas suppliers offer credit terms, and regulatory mechanisms ensure timely recovery of costs. Unlike manufacturing businesses that tie up capital in inventory, CGD operations generate negative working capital in growth phases—customers fund expansion.

Risk management has evolved from reactive to predictive. Currency hedging protects against dollar fluctuation in LNG imports. Take-or-pay contracts with industrial customers ensure minimum revenue. Insurance covers everything from pipeline accidents to business interruption. The company has learned to transform uncertainty into manageable risk.

The joint venture strategy deserves special mention. Through IOAGPL with Indian Oil, Adani Total Gas accesses geographical areas without full capital commitment. Similar partnerships are being explored with other oil marketing companies. It's capital-light expansion—gaining market access while sharing investment burden.

Future moats are being constructed today. The EV charging network creates optionality on transportation electrification. Biomass operations hedge against gas price volatility. Digital customer relationships enable new service offerings. The company isn't just protecting today's business—it's building tomorrow's advantages.

IX. Challenges & Controversies

January 24, 2023: Hindenburg Research published its report on the Adani Group, and within hours, Adani Total Gas's stock price began its violent descent. The report alleged accounting fraud, stock manipulation, and money laundering across the Adani empire. Whether true or false, the market's reaction was swift and brutal. ATGL's market cap evaporated by nearly 60% in days.

The Hindenburg impact went beyond stock price. International banks became cautious about financing. Suppliers demanded faster payments. Customers questioned long-term contracts. Employees worried about career prospects. The company that had spent years building credibility watched it evaporate in hours. The Total partnership suddenly became crucial—their continued commitment signaled confidence when others wavered.

But Hindenburg was just the latest chapter in ongoing scrutiny. The Adani Group's meteoric rise had always attracted skeptics. How did a commodity trader become India's largest private port operator, airport operator, and renewable energy producer simultaneously? Critics pointed to political connections, regulatory favors, and aggressive financial engineering. Supporters countered with execution excellence, strategic vision, and risk-taking appetite.

For Adani Total Gas specifically, regulatory challenges persist. Gas allocation policies change with political winds. State governments demand lower prices for consumers while expecting infrastructure investment. Environmental clearances for pipelines face increasing scrutiny. The regulatory framework that creates moats also creates obligations and constraints.

Infrastructure development in India remains challenging despite improvements. Getting permissions for laying pipelines through dense urban areas requires navigating Byzantine bureaucracy. Land acquisition for CNG stations faces resistance from local communities. Right-of-way disputes with other utilities create delays and cost overruns. Every kilometer of pipeline is a negotiation, every station a small victory.

Consumer adoption varies dramatically by geography and demography. While Mumbai and Delhi residents readily adopt PNG, smaller cities remain skeptical. Industrial customers in Gujarat switch enthusiastically, but Tamil Nadu factories resist. The assumption that "if you build it, they will come" doesn't always hold. Market development requires patient education and demonstration.

Competition from electric alternatives is accelerating faster than expected. Electric two-wheelers are already cheaper to operate than CNG vehicles. Electric buses are being deployed in major cities with government subsidies. Industrial heating applications are exploring electric alternatives. The window for gas as a transition fuel might be shorter than anticipated.

Geopolitical risks affect the entire business model. When Russia invaded Ukraine, global LNG prices spiked 400%. When Middle East tensions escalate, supply security becomes questionable. When China locks down for COVID, LNG tankers redirect to Europe. Adani Total Gas operates in a globally connected market where distant events have immediate local impact.

The talent challenge is underappreciated. CGD requires a unique combination of engineering expertise, regulatory navigation, and customer service. Finding professionals who understand both gas technology and Indian market dynamics is difficult. Training takes years, and competitors actively poach experienced staff. The company invests heavily in talent development, but retention remains challenging.

Financial market skepticism persists post-Hindenburg. The stock trades at elevated valuations—P/E of 99.3 versus book value of ₹38.2 suggests markets are pricing in significant growth. But growth requires capital, and capital markets remain cautious about Adani Group companies. The company must balance growth ambitions with financial prudence.

ESG (Environmental, Social, Governance) scrutiny is intensifying. While natural gas is cleaner than coal, it's still a fossil fuel. Methane leakage from pipelines contributes to greenhouse gases. Environmental activists question whether investing in gas infrastructure locks in emissions for decades. The company must navigate the contradiction of being both part of the climate solution and problem.

Technology disruption looms constantly. Hydrogen fuel cells might leapfrog natural gas in transportation. Distributed renewable energy could eliminate industrial gas demand. Synthetic biology might create alternative cooking fuels. The company must invest in current infrastructure while preparing for potential obsolescence.

Safety incidents, though rare, have devastating consequences. A pipeline explosion can destroy years of trust-building. A CNG station accident makes headlines nationally. The company maintains strong safety records, but the risk is ever-present. One major incident could trigger regulatory backlash and consumer exodus.

Political risk remains elevated in India. Change in government could mean policy reversal. State elections affect local permissions and pricing. The company must maintain relationships across the political spectrum while avoiding being seen as too close to any party. It's a delicate balance in India's charged political environment.

X. Playbook: Lessons for Builders & Investors

After studying Adani Total Gas's journey from a 2005 startup to a ₹64,000 crore infrastructure giant, several lessons emerge that transcend the gas distribution business. These insights apply whether you're building infrastructure in emerging markets or evaluating investment opportunities in capital-intensive sectors.

First, timing market transitions requires patience and conviction. Adani started building gas infrastructure when India's energy consumption was dominated by coal and oil. They didn't wait for the market to develop—they built the market. But this required patient capital willing to accept J-curve returns. The lesson: infrastructure investors must think in decades, not quarters.

Strategic partnerships can transform business trajectories. The TotalEnergies partnership wasn't just about capital—it was about capabilities, credibility, and connections. Total brought global LNG sourcing, technical expertise, and international validation. But the partnership structure—equal stakes forcing collaboration—was crucial. Too often, partnerships fail because of misaligned incentives or unequal commitment.

Building infrastructure businesses in emerging markets requires a unique playbook. You can't copy developed market models because the context is different. Indian consumers needed education about natural gas safety. Regulations had to be shaped, not just followed. Government relations became as important as customer relations. The ability to navigate this complexity while maintaining execution excellence separated winners from losers.

The power of regulatory moats is underappreciated. Once Adani Total Gas won exclusive rights to geographical areas, competition was limited. But regulatory moats come with obligations—universal service requirements, price controls, and investment commitments. Understanding this trade-off is crucial. Regulatory advantages aren't free—they're earned through compliance and contribution.

Capital efficiency through joint ventures and partnerships multiplies impact. Adani Total Gas didn't try to own everything. The IOAGPL joint venture with Indian Oil, infrastructure sharing agreements with other operators, and technology partnerships with global vendors allowed capital to go further. In capital-intensive businesses, the temptation is to own everything. The smart strategy is to control what matters and partner for the rest.

Managing stakeholder complexity requires sophisticated orchestration. Adani Total Gas must balance consumer demands for low prices, government expectations for infrastructure investment, partner requirements for returns, and environmental obligations for clean energy. There's no single optimization function—it's multi-variable calculus where satisficing beats optimizing.

Long-term thinking in infrastructure plays out differently than in technology businesses. While tech companies think about network effects and winner-take-all dynamics, infrastructure businesses think about asset utilization and replacement cycles. A pipeline laid today will generate cash flows for 30 years. A CNG station built now will serve vehicles not yet manufactured. This temporal mismatch between investment and return requires different mental models.

The importance of execution excellence in regulated industries cannot be overstated. When prices are regulated and territories are assigned, you can't win through clever pricing or aggressive marketing. You win through operational efficiency, customer service, and stakeholder management. Adani Total Gas's ability to execute complex infrastructure projects on time and budget became their calling card.

Market development is as important as market share in frontier sectors. Adani Total Gas didn't just compete for existing gas consumers—they created new consumers. Industrial customers were taught about gas economics. Households were educated about safety and convenience. Vehicle owners were convinced about running cost savings. Building markets is harder than capturing them, but the rewards are proportionally higher.

The value of optionality in uncertain transitions becomes clear. Adani Total Gas isn't betting everything on natural gas. EV charging, biomass, and hydrogen initiatives create options on different futures. This isn't hedging—it's building capabilities that can be deployed as transitions unfold. In uncertain environments, optionality is more valuable than optimization.

Infrastructure businesses require different metrics than typical companies. ROCE (Return on Capital Employed) matters more than ROE when assets are the business. Asset utilization trumps gross margins. Customer lifetime value exceeds acquisition cost importance. Investors evaluating infrastructure businesses with conventional metrics miss the point.

Governance and credibility become existential in institutional infrastructure. The Hindenburg episode showed how quickly credibility can evaporate. For businesses dependent on long-term contracts, regulatory licenses, and patient capital, reputation isn't just important—it's existential. Building governance systems that ensure transparency and accountability isn't compliance—it's survival.

XI. Analysis & Investment Perspective

The investment case for Adani Total Gas presents a fascinating paradox: a company trading at a P/E of 99.3 with a book value of just ₹38.2 per share, yet generating consistent cash flows from essential infrastructure. At ₹585 per share, the market is pricing in extraordinary growth, but is that justified?

Let's start with the financial reality. The company's return on equity has been consistently above 15%, impressive for a capital-intensive infrastructure business. EBITDA margins have remained resilient despite global gas price volatility. Volume growth continues as new connections are added and utilization increases. The numbers suggest a business performing well operationally.

The growth drivers are structural, not cyclical. A strong emphasis has been laid on expansion of city gas distribution (CGD) networks across the country by covering 407 districts with a potential to make gas accessible to over 70 percent of the population. The distribution networks would enable the supply of cleaner cooking fuel (like, PNG) to households, industrial & commercial units as well as transportation fuel (like, CNG) to vehicles. Urbanization adds 30 million people to cities annually, each a potential gas consumer. Government mandates for cleaner fuels aren't reversing. Industrial energy demand grows with GDP.

But the bear case has merit. Electric vehicles are advancing faster than expected, potentially disrupting CNG demand within this decade. Renewable energy costs are plummeting, making industrial electric heating competitive with gas. The hydrogen economy, while nascent, could leapfrog gas infrastructure entirely. Paying 99 times earnings for a business facing technological disruption seems risky.

The valuation concern is legitimate. At current prices, the market expects Adani Total Gas to grow earnings at 25-30% annually for the next decade. That's aggressive for any business, especially one requiring massive capital investment. Any disappointment—slower connection additions, margin compression from competition, or regulatory changes—could trigger significant correction.

Yet the bull case remains compelling. Essential infrastructure with regulatory moats rarely trades cheap. The company serves basic needs—cooking and transportation—that won't disappear. The TotalEnergies partnership provides stability and capability that standalone players lack. The diversification into EV charging and biomass creates optionality on different futures.

Comparing with global peers provides perspective. Tokyo Gas trades at 15x earnings, Osaka Gas at 12x. But these operate in mature markets with minimal growth. China Gas Holdings trades at 8x but faces regulatory uncertainty. Perhaps the premium for Indian CGD companies reflects the market opportunity—a 1.4 billion population with natural gas at only 6.7% of the energy mix currently.

The competitive analysis reveals strengths and vulnerabilities. Against IGL (Indraprastha Gas Limited), Adani Total Gas has broader geographical reach but lower margins. Versus MGL (Mahanagar Gas Limited), they have stronger partnership backing but less operational history. New entrants face infrastructure barriers, but technology disruption doesn't respect moats.

Cash flow generation capability is underappreciated. Unlike manufacturing businesses requiring constant reinvestment, gas distribution generates substantial free cash flow once infrastructure is built. This cash funds growth, rewards shareholders, and provides resilience during downturns. The business model is more akin to toll roads than factories.

The regulatory risk requires careful consideration. Government intervention in pricing, especially during inflation, could compress margins. Environmental regulations might impose costly upgrades. Policy shifts favoring electricity over gas would undermine the investment thesis. Regulatory giveth, and regulatory taketh away.

Institutional ownership patterns suggest sophisticated investors see value. Despite Hindenburg concerns, FIIs (Foreign Institutional Investors) maintain positions. The Total stake at 37.4% represents significant skin in the game. But retail investors dominate trading, creating volatility that might not reflect fundamental value.

The ESG angle complicates analysis. Natural gas is cleaner than coal but remains a fossil fuel. Some ESG funds exclude gas infrastructure entirely. Others see it as essential transition infrastructure. This schizophrenia affects institutional demand and cost of capital. The company's biomass and EV initiatives might be as much about ESG positioning as business diversification.

Risk-reward calculation depends on time horizon and conviction. For traders, the volatility offers opportunities but requires strong nerves. For long-term investors believing in India's gas economy vision, current valuations might prove reasonable in retrospect. For value investors seeking margin of safety, the premium to book value is concerning.

The key monitorables going forward are clear: volume growth rates to justify valuation, margin stability despite competition, successful diversification into new energy, regulatory stability and support, and technological disruption pace. Missing any of these could impair the investment case significantly.

XII. Epilogue & Future Outlook

Standing at the precipice of 2025, Adani Total Gas embodies India's energy paradox—a nation simultaneously industrializing and decarbonizing, urbanizing and digitizing, growing and greening. The company that started laying pipes in Ahmedabad's streets in 2005 now stands at the intersection of multiple energy transitions, each creating opportunities and existential threats.

India's energy transition trajectory is becoming clearer, though the pace remains debated. Half of India's supply of natural gas comes from domestic production while the other half comes from imported LNG. Industry experts expect that rising demand will prompt a mix of 30% domestic and 70% imported LNG by 2025. This import dependence creates both opportunity for infrastructure players and vulnerability to global price shocks.

The hydrogen economy represents the next frontier. Adani Total Gas's pipeline infrastructure, with modifications, could carry hydrogen blended with natural gas initially, then pure hydrogen eventually. The company's experiments with hydrogen blending at select industrial sites suggest serious commitment beyond mere announcements. But hydrogen remains expensive to produce, challenging to transport, and years from commercial viability.

The mobility transformation will test every assumption. Electric two-wheelers and three-wheelers are already disrupting CNG demand in some markets. But commercial vehicles, long-distance buses, and heavy-duty applications might remain gas-dependent longer. The company's dual strategy—expanding CNG while building EV charging—acknowledges this uncertainty without fully resolving it.

Key milestones to watch include reaching 1,000 CNG stations (doubling current infrastructure), connecting 15 lakh households (doubling current connections), achieving 20% revenue from new energy businesses, maintaining margins despite competition, and successful hydrogen pilot commercialization. Each represents a step toward validating or refuting the growth thesis.

The multi-energy future Adani Total Gas envisions isn't just about different fuels—it's about energy as a service. Imagine integrated energy stations offering CNG, EV charging, battery swapping, and hydrogen. Picture smart homes where the company manages total energy needs—cooking, heating, cooling, and mobility. Think about industrial parks with integrated energy solutions spanning gas, electricity, steam, and cooling.

But execution risks multiply with complexity. Managing gas distribution is challenging enough. Adding electricity, biomass, and hydrogen creates operational complexity that could overwhelm management bandwidth. The company must balance ambition with execution capacity, vision with operational reality.

The infrastructure being built today will shape India's energy landscape for decades. Those pipes under city streets, CNG stations along highways, and digital systems monitoring it all represent enormous sunk costs but also switching barriers. Once built, this infrastructure creates path dependence that influences energy choices for generations.

Regulatory evolution will significantly impact outcomes. If government accelerates electrification through subsidies and mandates, gas infrastructure could become stranded. If hydrogen receives policy support, early movers gain advantages. If carbon pricing becomes reality, gas gains competitiveness versus coal. Policy isn't just context—it's destiny for infrastructure businesses.

The international dimension grows more important. As India's energy demand grows and import dependence increases, global partnerships become crucial. The TotalEnergies relationship provides template, but more partnerships—for technology, capital, and supply—will be needed. Infrastructure at this scale requires global collaboration.

Climate commitments create urgency and opportunity. India's net-zero by 2070 pledge means every energy decision today affects tomorrow's trajectory. Natural gas, while transitional, plays a crucial role in near-term coal displacement. Adani Total Gas positions itself as enabler of this transition, though critics question whether gas infrastructure locks in emissions.

The human element often gets lost in infrastructure discussions, but it's crucial. Millions of Indian households will experience piped gas for the first time. Thousands of entrepreneurs will build businesses around CNG vehicles. Hundreds of communities will breathe cleaner air. Infrastructure isn't just pipes and stations—it's improved lives and opportunities.

Final reflections on building energy infrastructure reveal timeless lessons. First, infrastructure businesses require patient capital and long-term thinking rare in today's quarterly capitalism. Second, successful infrastructure companies don't just build physical assets—they build trust, relationships, and capabilities. Third, timing matters enormously—too early and you burn capital waiting for demand, too late and you miss the opportunity.

Adani Total Gas's journey from startup to infrastructure giant demonstrates what's possible when vision meets execution, when local knowledge partners with global capability, when patient capital funds essential infrastructure. Whether the next chapter brings continued growth or disruption remains uncertain. What's clear is that the company has positioned itself at the center of India's energy transformation, for better or worse.

The story of Adani Total Gas is still being written. Today's infrastructure investments will determine tomorrow's energy options. Today's strategic choices will shape tomorrow's competitive position. Today's partnerships will enable tomorrow's capabilities. In the grand narrative of India's development, Adani Total Gas has earned a significant chapter. Whether it's a success story or cautionary tale will be determined in the decades ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube