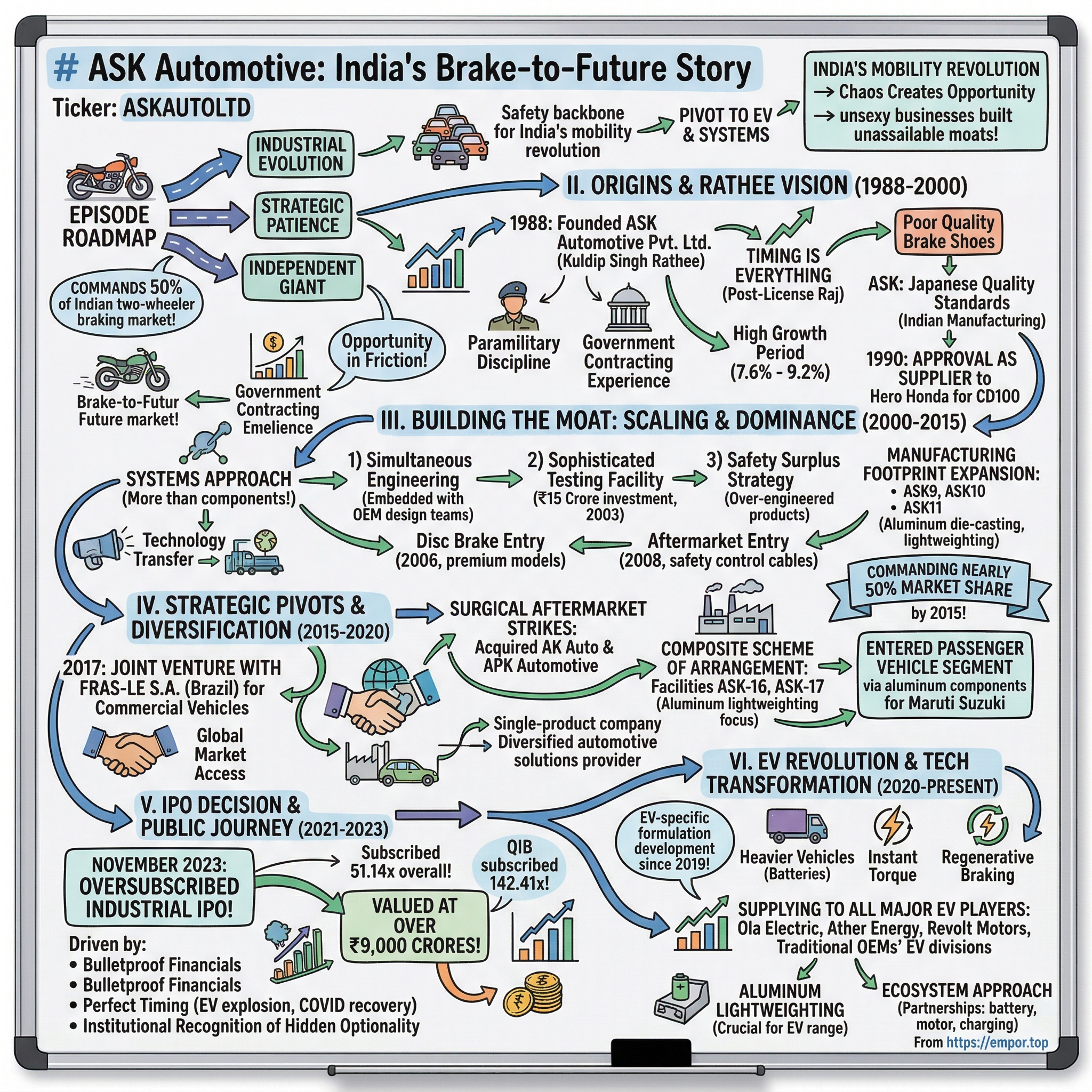

ASK Automotive: India's Brake-to-Future Story

I. Introduction & Episode Roadmap

Picture this: Every second motorcycle rolling off an Indian assembly line—whether it's a Hero Splendor navigating Delhi's chaotic streets or a Royal Enfield thundering through Ladakh's mountain passes—stops because of brakes made by one company. That company is ASK Automotive, and if you've never heard of them, you're not alone. They're the invisible giant of Indian roads, commanding 50% of the two-wheeler braking market while remaining virtually unknown outside automotive circles.

Here's the staggering reality: In a country where 16.25 million two-wheelers were sold in 2023 alone—representing 76% of all vehicles by volume—ASK Automotive has quietly become the safety backbone of India's mobility revolution. Every time millions of Indians twist their brake levers in Mumbai's monsoon traffic or Bangalore's IT corridors, there's a good chance they're trusting their lives to ASK's engineering.

But how does a company founded in 1988, during the dying days of India's License Raj, transform from a single-product brake shoe manufacturer into a sophisticated systems provider that's now pivoting to serve both combustion engines and electric vehicles? How do you build a moat so deep that global giants can't cross it, even in a market as price-sensitive as India?

This is the story of ASK Automotive—a masterclass in industrial evolution, strategic patience, and the art of becoming indispensable. We'll journey from Kuldip Singh Rathee's founding vision through the company's methodical conquest of India's OEM landscape, its bold international partnerships, and its November 2023 IPO that valued the company at over ₹9,000 crores. Along the way, we'll decode how a brake manufacturer became a bellwether for India's entire automotive transformation.

What makes ASK particularly fascinating isn't just their market dominance—it's their timing. As India stands at the precipice of an EV revolution, with the government targeting 30% electric two-wheeler penetration by 2030, ASK finds itself uniquely positioned. They're not just riding the wave; they're helping to engineer it, having already secured partnerships with next-generation EV makers like Ola Electric and Ather Energy.

So buckle up. This isn't just a story about brake shoes and safety cables—it's about how unsexy businesses build unassailable moats, how component suppliers can dictate terms to OEMs, and why the companies that stop vehicles might be more valuable than those that make them go. Most importantly, it's about recognizing that in the great Indian mobility transformation, the real power might not lie with the brands on the showroom floor, but with the suppliers whose names you'll never see.

II. Origins & The Rathee Vision (1988–2000)

The streets of Faridabad in 1988 told two different stories. In the gleaming showrooms, Japanese motorcycles—Yamaha RX100s and Suzuki Samurais—promised speed and modernity to India's emerging middle class. But in the grimy service stations where these machines inevitably ended up, mechanics wrestled with a persistent problem: brake shoes that wore out too quickly, compromising safety and frustrating riders who'd paid premium prices for reliability.

Kuldip Singh Rathee saw opportunity in this friction—literally. A first-generation entrepreneur with an economics degree from St. Stephen's College, Delhi, he founded ASK Automotive Private Limited on January 18, 1988. What made Rathee different wasn't just his vision—it was his background. He had previously served in the Central Reserve Police Force, directly recruited as deputy superintendent of police from 1974 to 1978, and later worked as a Class I contractor with the Central Public Works Department. This unique combination of paramilitary discipline and government contracting experience would prove invaluable in navigating India's Byzantine industrial landscape.

The timing was everything. India in 1988 stood at an inflection point—the License Raj still gripped the economy, but cracks were showing. The economy was experiencing high growth of 7.6 percent during 1988-1991, with industrial growth pushing a hefty 9.2 percent. Two-wheeler sales had exploded from 46,633 vehicles in 1980 to over 200,000 by 1989. Yet this boom exposed a critical weakness: India's component suppliers couldn't keep pace with either the volume or quality demands of the new Indo-Japanese joint ventures transforming the industry.

Consider the absurdity of the brake shoe market in 1988. Despite two-wheelers representing the overwhelming majority of vehicles on Indian roads, most brake components were either imported at crushing duties or manufactured by small-scale units using outdated technology. The big OEMs—Hero Honda (formed in 1984), TVS-Suzuki, Bajaj-Kawasaki—were desperate for reliable local suppliers who could meet Japanese quality standards while navigating Indian bureaucracy.

Rathee's genius lay in recognizing that brake shoes weren't just components—they were trust products. Unlike cosmetic parts or even engine components where failure might strand you, brake failure could kill you. This created an enormous moat for anyone who could build credibility. But credibility in 1988 India meant something very specific: you needed government licenses, OEM certifications, and most importantly, the ability to scale production without compromising quality.

The early days were brutal. ASK started with a single product—brake shoes for two-wheelers—in a modest facility. While competitors chased variety, Rathee obsessed over this one component. Every brake shoe was a referendum on the company's future. A single batch failure could destroy relationships that took years to build. In an era before ISO certifications became commonplace, ASK developed its own rigorous testing protocols, sometimes destroying thousands of units to perfect the friction material composition.

The License Raj system, which had been in place since the 1950s and would persist for four decades, paradoxically helped ASK in those early years. Businesses were required to obtain licenses from the government to operate, and these licenses were often difficult to obtain. But once you had them, they became competitive moats. Rathee's government connections and understanding of bureaucratic processes—honed during his police and contracting days—helped ASK navigate the labyrinthine approval processes that defeated many competitors.

The company's early manufacturing philosophy was distinctly Indian yet surprisingly sophisticated. Unable to afford expensive imported machinery, ASK's engineers reverse-engineered production processes, often improving upon them. They developed proprietary friction material formulations using locally available raw materials, achieving performance metrics that matched international standards at a fraction of the cost. This wasn't jugaad—it was systematic innovation born of constraint.

By 1990, ASK had achieved what seemed impossible just two years earlier: approval as a supplier to Hero Honda for their CD100 model. This wasn't just a commercial victory; it was a validation of Rathee's thesis that an Indian company could meet Japanese quality standards. The Hero Honda engineers, initially skeptical, were won over by ASK's fanatical attention to consistency—every brake shoe performed identically, a rarity in Indian component manufacturing.

As the government loosened restrictions on business creation and import controls while promoting the growth of the automobile industry, ASK positioned itself perfectly for the liberalization wave about to hit India. While others saw the end of License Raj as threatening competition, Rathee saw it as liberation—finally, ASK could expand without spending months navigating permit applications.

The 1990s beckoned with promise. The true influx of modernization and globalization was coming to India as finance minister Manmohan Singh initiated economic liberalization in 1991. For ASK, which had spent three years building capabilities under the old system, this was like training at high altitude and then competing at sea level. They were ready for the explosion in demand that liberalization would bring.

What's remarkable about ASK's origin story isn't the technology or even the market opportunity—it's the patience. In an era when software companies were promising overnight riches, Rathee was content to perfect brake shoes. This wasn't sexy. It wasn't revolutionary. But it was essential. And in the unglamorous world of automotive components, essential meant profitable.

The foundation was set. ASK had proven it could manufacture critical safety components to international standards. It had secured blue-chip customers. Most importantly, it had developed something money couldn't buy: trust. As India entered the 1990s and the two-wheeler market prepared to explode from hundreds of thousands to millions of units annually, ASK was perfectly positioned to capture this growth. But first, it needed to transform from a single-product manufacturer to something much more ambitious—a systems provider that could anticipate and meet the evolving needs of India's mobility revolution.

III. Building the Moat: Scaling & Market Dominance (2000–2015)

The conference room at Hero MotoCorp's Gurgaon headquarters in 2001 was tense. The world's largest two-wheeler manufacturer had just launched the CBZ—India's first indigenous 150cc motorcycle—and brake failure reports were trickling in from dealers. The problem wasn't catastrophic, but for a safety-critical component, even minor inconsistencies were unacceptable. Hero's procurement head turned to ASK's team: "Fix this, or we'll have to look at imports."

Kuldip Singh Rathee's response would define ASK's next decade: "Give us your entire brake system. Not just shoes—everything." It was audacious. ASK was proposing to evolve from component supplier to systems integrator overnight. But Rathee understood something fundamental about the Indian auto industry post-liberalization: OEMs desperately wanted to reduce supplier complexity. Managing dozens of vendors for different brake components was a nightmare. One accountable partner for the entire system? That was valuable.

This systems approach became ASK's weapon of choice in building an insurmountable moat. By 2002, they weren't just supplying brake shoes—they were providing complete brake panel assemblies, integrating shoes, springs, cams, and levers into tested, ready-to-install units. This seemingly simple shift had profound implications. OEMs could now single-source their entire brake system, reducing procurement complexity, inventory costs, and quality variables.

The expansion required capital and courage. Between 2000 and 2005, ASK methodically built manufacturing capabilities across India, but always with strategic intent. They didn't just build factories; they built ecosystems. Each facility was located near major OEM plants, reducing logistics costs and enabling just-in-time delivery—critical in an industry where inventory carrying costs could destroy margins.

The numbers tell only part of the story. By 2005, ASK was supplying brake systems to virtually every major two-wheeler OEM in India: Hero, Honda, Bajaj, TVS, Yamaha, and Suzuki. But the real achievement was market share—approaching 35% and climbing. In a fragmented industry with hundreds of component suppliers, this was unprecedented consolidation.

What enabled this dominance? Three interlocking strategies that competitors couldn't replicate:

First, ASK mastered the art of simultaneous engineering. While competitors waited for OEM specifications before starting development, ASK's engineers were embedded with OEM design teams from day one. When Honda developed the Shine—which would become India's highest-selling 125cc motorcycle—ASK's team was designing the brake system in parallel, not sequentially. This cut development time by months and created switching costs that made replacement virtually impossible.

Second, they built India's most sophisticated brake testing facility in 2003, including dynamometers that could simulate everything from Himalayan descents to tropical humidity. This ₹15 crore investment seemed excessive for a component supplier, but it transformed ASK's relationship with OEMs. Now, instead of sending samples to Japan or Italy for validation, OEMs could test at ASK's facility. The psychological impact was enormous—ASK wasn't just meeting international standards; they were setting them.

Third, and most cleverly, ASK created what they called the "safety surplus strategy." While competitors optimized for minimum acceptable performance to win on price, ASK deliberately over-engineered their products by 20-30%. This meant their brake shoes lasted longer, performed more consistently, and most importantly, created a safety buffer that OEMs valued enormously. In a market where a single accident could trigger massive recalls and destroy brand value, this safety surplus was insurance worth paying for.

The mid-2000s brought an unexpected challenge that would ultimately strengthen ASK's position: the rise of disc brakes in premium motorcycles. Industry observers predicted this would devastate drum brake manufacturers like ASK. Instead, Rathee saw opportunity. In 2006, ASK acquired disc brake pad manufacturing technology and within eighteen months was supplying to the same OEMs for their premium models. The message was clear: ASK wasn't a brake shoe company; it was a braking solutions company.

The masterstroke came in 2008 when ASK entered the aftermarket with safety control cables—clutch cables, brake cables, throttle cables, and speedometer cables. This wasn't diversification for its own sake. Cables and brakes shared customers, distribution channels, and most importantly, the same value proposition: safety-critical components where quality literally meant life or death. By bundling these products, ASK could offer distributors better margins while gaining deeper market intelligence about replacement cycles and failure patterns.

The aftermarket entry also solved a strategic vulnerability. OEM business, while lucrative, was inherently cyclical and concentrated. The aftermarket provided steady, high-margin revenue that could cushion downturns. More importantly, it created a feedback loop—aftermarket data revealed real-world performance issues that helped improve OEM products.

By 2010, ASK had achieved something remarkable: they had become irreplaceable. When Bajaj developed the Pulsar 200NS with its revolutionary perimeter frame, ASK was the only supplier Bajaj considered for the brake system. When Honda introduced the CB Unicorn with its emphasis on refined performance, ASK's brakes were non-negotiable. This wasn't vendor lock-in through contracts—it was lock-in through capability.

The manufacturing footprint expansion accelerated. ASK9 opened in Manesar in 2014, followed by ASK10 in IMT Manesar and ASK11 in Ahmedabad in 2015. Each facility represented not just capacity addition but capability enhancement. ASK11 in Ahmedabad, for instance, was specifically designed for aluminum die-casting—a prescient bet on lightweighting that would pay dividends as fuel efficiency regulations tightened.

The international dimension deserves mention. While ASK remained India-focused, they began exporting to Southeast Asia and Africa—markets with similar price sensitivity and operating conditions. These weren't large revenues, but they provided crucial learnings about different regulatory requirements and performance expectations that would inform product development.

Competition during this period was fierce but ineffective. Multinational suppliers like Bosch and Brembo had superior technology but couldn't match ASK's price points. Local competitors could compete on price but not on quality or scale. Chinese suppliers tried entering the market with aggressive pricing but failed to meet OEM quality requirements. ASK occupied a sweet spot—good enough quality at Indian prices with Japanese-level reliability.

The human capital story was equally important. ASK built India's largest team of brake system engineers—over 200 by 2015. But more than numbers, it was the culture. Engineers were rotated between OEM projects, aftermarket products, and R&D, creating cross-pollination of ideas. The company sponsored master's degrees at IITs for promising engineers, creating loyalty and capability simultaneously.

Financial discipline underpinned everything. Despite rapid expansion, ASK maintained ROCE above 20% throughout this period. They achieved this through obsessive focus on working capital—negotiating 60-day payment terms with OEMs while paying suppliers in 30 days, essentially using vendor financing for growth. Capital expenditure was always counter-cyclical, expanding capacity during downturns when equipment was cheaper and contractors hungry for work.

By 2015, ASK's moat was complete. They commanded nearly 50% market share in two-wheeler braking systems. They were sole suppliers for critical platforms across every major OEM. They had expanded from one product to complete systems. Most importantly, they had transformed from vendor to partner—involved in product development from conception to end-of-life.

But Rathee knew moats need constant reinforcement. The two-wheeler market was evolving—electric vehicles were emerging, emission norms were tightening, and customer expectations were rising. ASK needed to evolve too. The answer would come through strategic partnerships and acquisitions that would transform ASK from an Indian champion to a company with global ambitions. The foundation was built; now it was time to construct the superstructure.

IV. Strategic Pivots & Diversification (2015–2020)

The boardroom at ASK's Gurgaon headquarters in December 2016 was electric with possibility. Kuldip Singh Rathee had just returned from Brazil, where he'd met with executives from Fras-Le S.A., one of the world's five largest friction material manufacturers. The proposal on the table was audacious: create a joint venture that would catapult ASK from two-wheeler dominance into the commercial vehicle segment—trucks, buses, and trailers that represented an entirely different engineering challenge and market opportunity.

This wasn't diversification for diversification's sake. Rathee understood that ASK's two-wheeler moat, while formidable, had a ceiling. India's commercial vehicle market was exploding—freight movement was growing at 10% annually, and stricter safety regulations were driving demand for advanced braking systems. But more strategically, commercial vehicle brakes operated on different replacement cycles, had different margin structures, and most importantly, provided a natural hedge against two-wheeler market volatility.

The deal, signed on December 5, 2017, in Caxias do Sul, Brazil, established ASK Fras-Le Friction Private Limited with plans to invest more than ₹100 crores over three years and generate employment for more than 900 people. Fras-Le would hold 51% controlling interest while ASK retained 49%. For ASK, giving up control was unprecedented, but the technology transfer and global market access Fras-Le brought were worth the compromise.

The timing was perfect. "The market for commercial vehicles in India is very large and shows excellent prospects for future development," noted Sérgio de Carvalho, CEO of Fras-Le, referring to India's economic stability. What he didn't say publicly was that Fras-Le needed ASK as much as ASK needed them—Indian manufacturing costs with Brazilian technology could compete globally against European suppliers.

The joint venture represented a masterclass in strategic complementarity. ASK was the world leader in two-wheeler friction while Fras-Le was among the world leaders in the commercial vehicle friction segment. ASK brought deep understanding of Indian OEMs, established manufacturing infrastructure, and relationships with component distributors. Fras-Le brought 60 years of commercial vehicle expertise, access to over 100 export markets, and most crucially, friction formulations that could handle the extreme heat and load conditions of Indian commercial vehicles.

But the Fras-Le deal was just the opening move in ASK's transformation strategy. In 2018, the company executed two critical acquisitions that would reshape its aftermarket presence. Through business purchase agreements dated March 26, 2018, ASK acquired the entire independent aftermarket business of AK Auto Industries (including the ASK14 facility) from Aman Rathee and APK Automotive (including the ASK15 facility) from Prashant Rathee.

These weren't random acquisitions—they were surgical strikes on the aftermarket. AK Auto and APK had built strong distribution networks in tier-2 and tier-3 cities where ASK's OEM-focused approach had limited penetration. By acquiring these businesses from family members (Aman and Prashant Rathee were Kuldip's sons), ASK ensured seamless integration while eliminating potential conflicts of interest as the company prepared for public listing.

The masterstroke came in 2019 with the composite scheme of arrangement involving A.A. Autotech Private Limited. Through this scheme, manufacturing facilities ASK-16 and ASK-17, both situated in IMT Manesar, were transferred to ASK from A.A. Autotech Private Limited. This wasn't just about adding capacity—these facilities were specifically equipped for aluminum die-casting and precision machining, capabilities that would prove crucial as ASK expanded beyond friction materials.

The aluminum lightweighting story deserves special attention. As emission norms tightened globally, every gram of weight reduction mattered. ASK recognized that their expertise in precision manufacturing could extend beyond brakes to other safety-critical aluminum components—engine parts, transmission housings, suspension components. The ASK16 and ASK17 facilities gave them the capability to offer integrated lightweighting solutions to OEMs struggling to meet BS-VI emission norms.

What made these acquisitions brilliant wasn't just what ASK bought, but how they integrated them. Instead of maintaining separate operations, ASK created what they called "capability clusters"—each facility specialized in specific technologies but shared knowledge, customers, and supply chains. ASK14 became the hub for aftermarket packaging and distribution. ASK15 focused on rapid prototyping for new products. ASK16 and ASK17 handled aluminum die-casting and precision machining.

The financial engineering was equally sophisticated. The acquisitions were structured as slump sales, allowing ASK to acquire assets without inheriting liabilities. The consideration was primarily through inter-company adjustments and deferred payments, preserving cash for operational expansion. Most cleverly, the timing coincided with the government's production-linked incentive schemes for automotive components, allowing ASK to claim benefits on the expanded capacity.

By 2019, ASK had also identified a crucial gap in their portfolio: they were supplying safety-critical components to virtually every vehicle segment except passenger cars. The four-wheeler market in India was fundamentally different—dominated by Maruti Suzuki with over 50% share, with global suppliers like Bosch and Continental deeply entrenched. Direct competition was suicidal. Instead, ASK chose collaboration.

The company began developing specialized aluminum components for passenger vehicles—not brakes, but lightweighting solutions for engines and transmissions. This wasn't competing with their core business; it was leveraging their precision manufacturing capabilities in adjacent spaces. By 2020, ASK was supplying aluminum die-cast components to Maruti Suzuki, effectively entering the passenger vehicle segment through the side door.

The international expansion strategy during this period was deliberately modest but strategic. While the Fras-Le venture provided access to global markets, ASK focused on countries with similar operating conditions to India—Bangladesh, Sri Lanka, Nepal, and select African markets. The new company's products would be supplied to India, Bangladesh, Nepal and Sri Lanka and would also be exported to other countries through Fras-Le's global network.

The cultural transformation within ASK during these years was profound. From a family-run business focused on one product category, it evolved into a professionally managed conglomerate with multiple business verticals. The second generation—Aman and Prashant Rathee—brought international exposure and professional management practices. Aman, with his Master's Degree in Business Administration from Purdue University and certification in mergers and acquisitions from Harvard Business School, led the M&A strategy and international partnerships.

Risk management became increasingly sophisticated. With exposure to commercial vehicles, passenger cars, and international markets, ASK couldn't rely on intuition anymore. They implemented enterprise resource planning systems, established dedicated risk committees, and most importantly, created firewalls between different business segments to prevent contagion during downturns.

The results spoke for themselves. Revenue grew from ₹1,567.77 crores in March 2021 to ₹2,566.28 crores in March 2023—a 64% increase in just two years. But more importantly, ASK had transformed from a single-product company to a diversified automotive solutions provider. They weren't just surviving the industry transformation; they were shaping it.

By 2020, ASK stood at another inflection point. The company had successfully diversified across products, segments, and geographies. The operational foundation for a public listing was in place. But the biggest transformation was yet to come—the electric vehicle revolution that would challenge everything ASK knew about mobility. The question wasn't whether ASK could adapt to EVs; it was whether they could lead the transformation.

V. The IPO Decision & Public Journey (2021–2023)

The war room at JM Financial's Mumbai headquarters on November 6, 2023, was buzzing with nervous energy. The anchor book for ASK Automotive's IPO had just opened, and within hours, orders were flooding in from institutional investors who'd never shown interest in auto component companies before. Goldman Sachs, Neuberger Berman, Morgan Stanley—names that typically chased tech unicorns were suddenly fascinated by a brake manufacturer from Gurgaon. By day's end, ASK had raised ₹250.17 crore from anchor investors, setting the stage for what would become one of the most oversubscribed industrial IPOs of 2023.

The decision to go public wasn't born of necessity—it was strategic positioning. ASK's revenue had increased by 26.78% and profit after tax had grown by 48.75% between FY2022 and FY2023. The company didn't need capital; what it needed was currency—stock that could be used for acquisitions, talent retention, and most importantly, validation as India's automotive sector underwent its most significant transformation since liberalization.

The journey to the IPO began with ASK's conversion from a private limited company to a public limited company on January 6, 2023. This wasn't just paperwork—it represented a fundamental shift in how the Rathee family viewed their creation. For 35 years, ASK had been run like an extended family business, with decisions made over chai in Kuldip Singh Rathee's office. Now, it would face quarterly earnings calls, analyst scrutiny, and the relentless pressure of public markets.

The IPO structure itself was revealing: it was entirely an offer for sale of 2.96 crore shares, with no fresh capital raise. Kuldip Singh Rathee was selling 20,699,973 equity shares aggregating to ₹583.74 crores, while Vijay Rathee was selling 8,871,417 shares aggregating to ₹250.17 crores. This wasn't about funding growth—ASK had sufficient cash flows for organic expansion. Instead, it was about liquidity for promoters who'd built their wealth over decades, and creating a public market for ASK shares that would enable future M&A using stock as currency.

The pricing strategy was conservative yet confident. The price band was set at ₹282 per share, valuing the company at approximately ₹5,500 crores pre-money. This represented roughly 21 times FY2023 earnings—not cheap for an auto component company, but justified by ASK's market position and growth trajectory. The lot size of 53 shares requiring a minimum investment of ₹14,946 was deliberately kept accessible to retail investors, signaling confidence that demand would come from all investor categories.

The three-day bidding window from November 7-9, 2023, became a masterclass in demand generation. The roadshow presentations weren't selling past performance—they were selling the future. ASK positioned itself not as a brake manufacturer but as a safety technology company at the intersection of India's two megatrends: the continued growth of two-wheeler penetration and the EV revolution.

The subscription numbers told the story. The IPO was subscribed 51.14 times overall, with the QIB portion subscribed 142.41 times and NII category 35.47 times. Even the traditionally cautious retail segment subscribed 5.09 times. For context, most industrial IPOs in 2023 struggled to achieve full subscription. ASK's oversubscription wasn't just strong—it was a statement that investors understood the moat.

What drove this enthusiasm? Three factors converged perfectly:

First, ASK's financials were bulletproof. The company had demonstrated consistent growth through multiple cycles, maintained ROCE above 20%, and most importantly, generated strong free cash flows. Unlike many IPOs that came with promises of future profitability, ASK was already printing money.

Second, the timing was impeccable. India's two-wheeler market was recovering from COVID-19 disruptions, electric two-wheeler sales were exploding with government subsidies, and global supply chain realignments were favoring established domestic suppliers. ASK wasn't just riding these trends—they were positioned to benefit from all of them simultaneously.

Third, and perhaps most importantly, institutional investors recognized ASK's hidden optionality. While the company was valued as a traditional auto component supplier, its EV partnerships, aluminum lightweighting capabilities, and potential for international expansion created multiple avenues for valuation re-rating.

The grey market provided another signal of investor appetite. The grey market premium jumped to ₹50-55 per share after strong institutional interest, up from ₹40 before bidding began, suggesting potential listing gains of 18-20%.

But the real validation came from the quality of institutional investors. The anchor book wasn't filled with momentum traders or hedge funds looking for a quick flip. These were long-term investors who understood manufacturing, appreciated moats, and most importantly, believed in India's consumption story. Their participation sent a message to the broader market: ASK wasn't just another IPO; it was an infrastructure play on India's mobility transformation.

The lead managers—JM Financial, Axis Capital, IIFL Securities, and ICICI Securities—had deliberately targeted this investor base. The roadshow emphasized ASK's role in "Making in India" for global markets, its contribution to road safety, and its alignment with government priorities around localization and import substitution.

On November 15, 2023, ASK Automotive's shares opened for trading at ₹304.90 on BSE and ₹303.30 on NSE, representing an 8% premium to the issue price. While some had expected a larger pop given the subscription numbers, the modest premium actually worked in ASK's favor. It suggested institutional support at these levels and reduced the likelihood of immediate profit-taking.

The post-listing performance revealed something interesting about market perception. Unlike typical IPOs that see volatile trading in early days, ASK's stock price remained remarkably stable, trading in a narrow range with healthy volumes. This wasn't the behavior of a momentum stock—it was the trading pattern of a company that institutions were accumulating for long-term portfolios.

The financial metrics post-IPO were impressive. With a market capitalization of ₹9,214 crores, revenue of ₹3,630 crores, and profit of ₹257 crores, ASK was trading at reasonable multiples compared to global auto component peers. More importantly, the company maintained its operational momentum, with order books remaining strong and new customer acquisitions continuing.

For the Rathee family, the IPO represented both an end and a beginning. They retained 79% ownership, ensuring continued control while achieving liquidity. But more than financial gains, the IPO validated their four-decade journey from a single-product manufacturer to India's brake hegemon.

The strategic implications were profound. As a listed company, ASK could now use stock for acquisitions, attract global talent with ESOPs, and most importantly, had the credibility to partner with international OEMs looking for Indian suppliers. The public listing wasn't just about raising capital—it was about raising ambition.

Industry observers noted that ASK's successful IPO could trigger a wave of listings from other profitable, family-owned auto component companies. If a brake manufacturer could command such valuations and investor interest, what about companies making critical EV components or semiconductor-adjacent products?

The IPO also marked a generational transition. While Kuldip Singh Rathee remained chairman, the increased visibility and governance requirements of a public company accelerated the professionalization that his sons Aman and Prashant had been driving. Quarterly earnings calls, investor meets, and analyst coverage meant ASK could no longer operate in the shadows—they were now in the spotlight.

As 2023 drew to a close, ASK's IPO stood as a testament to patient capital and strategic timing. They hadn't rushed to list during the 2021 bubble when valuations were frothy but fundamentals weak. Instead, they waited until the business was truly ready, the market was receptive, and the story was compelling. The result wasn't just a successful IPO—it was a blueprint for how traditional manufacturing companies could access capital markets while maintaining operational excellence.

VI. The EV Revolution & Technology Transformation (2020–Present)

The Ather Energy test facility in Whitefield, Bangalore, March 2021. A prototype electric scooter, its body panels removed to expose the aluminum frame and battery pack, sits on a dynamometer running a simulated hill climb. The engineers watching the screens aren't from Ather—they're from ASK Automotive, and they're about to make a decision that will reshape their company's future. The brake pads on the scooter are glowing cherry red, but they're still gripping. After 45 minutes of continuous testing that would destroy conventional brake materials, ASK's new EV-specific formulation is still performing within spec.

This moment crystallized a transformation that had been building since 2020. ASK had identified the EV sector as an opportunity and diversified in FY 2021, but the decision wasn't reactive—it was prescient. While competitors dismissed electric two-wheelers as a niche segment that would take decades to mature, ASK's engineers had been studying the fundamental differences in braking requirements between internal combustion engine (ICE) and electric vehicles since 2019.

The physics were counterintuitive. Electric vehicles were heavier due to battery packs, generated instant torque that stressed brakes differently, and most critically, used regenerative braking that fundamentally altered heat cycles in friction materials. Traditional brake formulations that worked perfectly for ICE vehicles would glaze or fade in EVs. ASK needed to reinvent their core product from first principles.

The R&D investment was massive. ASK developed new test protocols specifically for EV applications, including regenerative braking simulation, battery weight compensation algorithms, and thermal cycling patterns unique to electric powertrains. By June 30, 2023, the company had developed a portfolio of 52 proprietary formulations, with seven specifically optimized for electric vehicles. These weren't incremental improvements—they represented fundamental breakthroughs in friction material science.

The market timing was perfect. Ola Electric, founded in 2017, received 500,000 bookings for scooters in the first month of availability and started delivering its S1 and S1 Pro models in December 2021. Ather Energy, founded by Tarun Mehta and Swapnil Jain in 2013, had become India's fourth-largest electric two-wheeler manufacturer. These weren't just new customers—they were new categories of customers with different quality expectations and performance requirements.

ASK's approach to the EV market was characteristically strategic. Instead of waiting for EV manufacturers to approach them, ASK's engineers embedded themselves in EV development teams from the concept stage. When Ola was designing the S1, ASK was already testing brake formulations optimized for its specific weight distribution and regenerative braking profile. When Ather was developing the 450X, ASK had pre-validated braking solutions ready for integration.

The partnerships weren't just commercial—they were technological collaborations. ASK shared real-time field data with EV manufacturers, helping them optimize regenerative braking algorithms to work in harmony with friction brakes. This systems-level thinking created switching costs that went beyond simple supplier relationships. ASK wasn't just providing parts; they were co-creating braking systems.

The technical challenges were formidable. EV brakes needed to handle different duty cycles—long periods of minimal use due to regenerative braking, followed by sudden high-load events during emergency stops. The friction materials needed to resist glazing during light use while maintaining bite during panic braking. ASK's solution involved multi-layer pad construction with different compounds optimized for different temperature ranges—a technology previously reserved for racing applications.

Manufacturing for EVs also required different approaches. EV manufacturers operated on different timelines than traditional OEMs—product cycles were shorter, iteration was faster, and customization was expected. ASK created dedicated EV production lines with flexible tooling that could switch between different formulations within hours, not days. This agility became a competitive advantage as EV manufacturers rapidly iterated their designs.

The aftermarket opportunity in EVs was particularly interesting. Unlike ICE vehicles where brake replacement was predictable, EV brake wear patterns were highly variable depending on driving style and regenerative braking usage. ASK developed predictive maintenance algorithms that could estimate brake life based on vehicle telematics data—turning a commodity product into a smart component.

By 2022, ASK was supplying braking systems to virtually every major EV manufacturer in India, including new-age players like Ola Electric, Ather Energy, and Revolt Motors, as well as traditional OEMs' EV divisions. The company's EV revenue, while still small in absolute terms, was growing at over 100% annually and commanded higher margins than traditional products.

The aluminum lightweighting story paralleled the EV transformation. As battery weight became a critical constraint, every gram saved elsewhere extended range. ASK's aluminum die-casting capabilities, initially developed for engine components, found new applications in EV chassis, motor housings, and battery enclosures. The same precision engineering that made ASK a trusted brake supplier made them invaluable for lightweight structural components.

The technology development wasn't happening in isolation. ASK established partnerships with battery manufacturers to understand thermal management requirements, with motor suppliers to optimize regenerative braking integration, and with charging infrastructure providers to understand duty cycles. This ecosystem approach positioned ASK not just as a component supplier but as a systems integrator for EV mobility.

The investment in EV wasn't without risks. The industry faced challenges, including fire incidents in March 2022 that led Ola to recall 1,441 scooters. Each incident triggered industry-wide reviews of safety standards, with braking systems under particular scrutiny. ASK's response was to over-engineer safety margins even further, conducting failure mode analysis that went beyond regulatory requirements.

The intellectual property development was crucial. ASK filed patents not just for friction materials but for complete braking systems optimized for electric vehicles. These included innovations in brake-by-wire systems, regenerative braking integration, and predictive maintenance algorithms. The patent portfolio became a strategic asset, creating barriers for competitors trying to enter the EV braking market.

Human capital transformation accompanied the technological shift. ASK hired software engineers to develop brake control algorithms, data scientists to analyze field performance, and material scientists specializing in advanced composites. The company's engineering team expanded from 200 in 2015 to over 400 by 2023, with half focused on EV and advanced applications.

The financial model for EV business differed significantly from traditional automotive. Development costs were front-loaded, with longer payback periods but higher lifetime value. ASK adapted by creating separate P&L structures for EV projects, with different ROI expectations and timeline horizons. This financial flexibility allowed them to invest aggressively while maintaining overall profitability.

The global dimension was increasingly important. As Indian EV manufacturers looked to export, they needed suppliers who could meet international safety standards. ASK's certifications from European and American testing bodies became a competitive advantage, enabling their EV customers to access global markets with confidence.

By 2023, ASK's transformation was complete. From a brake shoe manufacturer serving ICE vehicles, they had evolved into a mobility solutions provider for the electric age. The company wasn't just adapting to the EV revolution—they were helping to engineer it. The same discipline, quality focus, and customer intimacy that built their ICE business were now creating an equally dominant position in electric mobility.

The challenge ahead was scaling. With 1.14 million electric two-wheelers sold in India in 2024, the market was still nascent compared to the 16 million ICE two-wheelers sold annually. But the trajectory was clear. Government mandates, improving battery technology, and changing consumer preferences all pointed toward rapid electrification. ASK was ready—not just with products but with an entire ecosystem of capabilities that would be essential for the electric future.

VII. Market Position & Competitive Dynamics

India's two-wheeler market achieved domestic sales of 16.25 million units in 2023, with ASK Automotive holding approximately 50% market share in terms of production volume for OEMs and the branded independent aftermarket. This dominance wasn't accidental—it was architected through three decades of strategic positioning that created multiple reinforcing moats.

Understanding ASK's market position requires appreciating the unique structure of India's two-wheeler industry. Unlike developed markets where four-wheelers dominate, two-wheelers represent 76% of India's total automotive market by volume. This isn't just about economics—it's about infrastructure. Indian roads, particularly in tier-2 and tier-3 cities, are designed for two-wheelers. Parking spaces, traffic patterns, even social customs are built around motorcycles and scooters.

Within this massive market, the brake component segment has peculiar dynamics. While tires, batteries, and even engines can be differentiated through marketing, brakes are invisible until they fail. This invisibility creates a paradox: customers don't think about brakes when buying a vehicle, but OEMs obsess over them because brake failure can destroy a brand overnight. This dynamic favors established suppliers with proven track records over newcomers with potentially superior technology.

ASK's customer concentration both demonstrates their strength and represents their primary risk. The company is dependent on its top three customers for more than half of its revenue, meaning that if the company loses any of these customers or if their business declines, it could have a significant negative impact on overall revenue. These customers—likely Hero MotoCorp, Honda, and Bajaj—aren't just buyers; they're strategic partners whose fortunes are intertwined with ASK's.

This concentration isn't necessarily weakness—it's a reflection of market structure. The Indian two-wheeler market is dominated by five players who collectively control over 85% market share. Supplying all of them, as ASK does, essentially means controlling the market. The switching costs for these OEMs are enormous—not just in terms of validation and tooling, but in risking their vehicles' safety on unproven suppliers.

The competitive landscape reveals why ASK's moat is so resilient. Global giants like Bosch and Continental have superior technology and deeper pockets, but they've failed to crack the Indian two-wheeler brake market. Why? Because ASK's advantage isn't technological—it's systemic. They understand Indian roads, Indian driving conditions, and most importantly, Indian price points. A Bosch brake system might perform better in laboratory conditions, but ASK's performs better at Indian price-performance expectations.

Local competition is fragmented and subscale. Hundreds of small manufacturers produce brake shoes, but they operate in the replacement market's bottom tier, competing purely on price. They lack the quality certifications, testing capabilities, and most critically, the trust required to supply OEMs. ASK occupies a sweet spot—local enough to understand the market, large enough to meet OEM requirements.

Chinese competition, which has disrupted many Indian manufacturing sectors, has notably failed in safety-critical components like brakes. Indian OEMs, burned by quality issues in other components, are extremely reluctant to source brakes from China. The reputational risk of a brake failure traced to a Chinese supplier far outweighs any cost savings. This creates a natural protection for domestic suppliers like ASK.

The aftermarket dynamics are equally favorable. ASK's "ASK" brand has become synonymous with quality in independent repair shops. Mechanics, who influence replacement decisions, prefer ASK because they reduce comeback rates—customers returning with complaints. This word-of-mouth marketing is incredibly powerful in India's relationship-driven business environment.

Market growth projections provide tailwind for ASK's dominance. The auto component market is expected to grow at 12-14% CAGR through 2028, with advanced braking systems growing at 8.9% CAGR. But these aggregate numbers hide more interesting dynamics. The premium segment, where ASK has been gaining share, is growing faster than the mass market. Electric vehicles, where ASK has first-mover advantage, are growing exponentially from a small base.

The export opportunity remains largely untapped. While ASK exports to twelve countries, international sales remain under 10% of revenue. This isn't weakness—it's optionality. As Indian two-wheeler manufacturers like Hero and Bajaj expand globally, they prefer taking trusted suppliers with them. ASK's international growth will likely follow their customers' international expansion, reducing market development risk.

Entry barriers in the brake manufacturing industry are deceptively high. While the basic technology is well-understood, the practice requires massive capital investment in testing equipment, years of OEM validation, and most importantly, trust built over decades. A new entrant would need to invest hundreds of crores just to match ASK's infrastructure, then wait years to get validated by OEMs, all while competing against an incumbent with 50% market share and economies of scale.

The regulatory environment increasingly favors established players. Stricter safety norms, emission regulations driving weight reduction, and upcoming mandates for anti-lock braking systems all require sophisticated R&D capabilities that smaller players lack. Each new regulation essentially raises the bar for competition while playing to ASK's strengths in engineering and testing.

ASK's pricing power is subtle but real. While they can't dramatically raise prices without OEM pushback, they've consistently maintained margins above 20% while raw material costs fluctuated. This pricing discipline comes from value engineering—constantly finding ways to deliver the same performance at lower cost, then sharing some savings with customers while retaining the rest as margin.

The platform nature of ASK's business creates additional competitive advantages. Once an OEM validates ASK for one vehicle platform, extending to other platforms becomes easier. This creates a multiplier effect—each new customer relationship leads to multiple product opportunities. Competitors must win platform by platform, while ASK can leverage existing relationships for new business.

Technology transitions represent opportunity rather than threat for ASK. The shift to disc brakes from drum brakes, which many predicted would hurt ASK, actually strengthened their position as they quickly developed disc brake capabilities. The move to ABS (Anti-lock Braking Systems) will require sophisticated brake components that only advanced suppliers can provide. Each technology transition raises the bar and culls weaker competitors.

The sustainability angle is becoming increasingly important. ASK's investment in asbestos-free formulations, recyclable materials, and reduced environmental impact resonates with global OEMs facing ESG pressure. While not yet a major factor in India, this positions ASK well for future regulatory changes and export opportunities to environmentally conscious markets.

Network effects, unusual in manufacturing, are emerging in ASK's business. As they gather more field data from more vehicles, their ability to optimize formulations improves. This data advantage compounds over time—new entrants not only start behind in manufacturing but also in understanding real-world performance patterns.

The key strategic question isn't whether ASK's dominance is sustainable—multiple reinforcing factors suggest it is. The question is whether the market itself will remain attractive. If two-wheeler sales plateau or shift dramatically to shared mobility, ASK's moat becomes less valuable. But given India's demographic trajectory, infrastructure constraints, and cultural preferences, the two-wheeler market seems secure for at least another decade.

Competitive threats are more likely to come from business model innovation than direct competition. Battery-as-a-service models, vehicle subscription services, or integrated mobility platforms could change how braking systems are procured and valued. ASK's response has been to embed themselves deeper into OEM operations, making themselves indispensable regardless of business model changes.

The ultimate test of ASK's market position is pricing resilience during downturns. During COVID-19, when two-wheeler sales collapsed, ASK maintained margins while competitors struggled. This resilience comes from their diversified customer base, aftermarket presence, and operational efficiency—a combination competitors find difficult to replicate.

VIII. Playbook: Business & Operating Lessons

The conference room in ASK's Manesar facility has a peculiar feature: a wall displaying brake shoes that failed. Not competitors' failures—ASK's own. Each failed component has a plaque describing what went wrong, when, and most importantly, what was learned. This "failure museum" embodies ASK's operating philosophy: excellence comes not from avoiding mistakes but from learning faster than competitors.

Lesson 1: Trust is the Ultimate Moat in Safety-Critical Components

ASK's foundational insight was that in safety-critical components, trust trumps technology. While competitors focused on technical specifications, ASK invested in relationship building. They didn't just meet OEM engineers; they invited them to family weddings. They didn't just submit test reports; they conducted tests in front of customers. This high-touch approach seems inefficient but creates switching costs that no specification sheet can overcome.

The trust-building extended to crisis management. When a batch of brake shoes showed premature wear in 2003, ASK didn't wait for customer complaints. They proactively recalled the entire batch, absorbed the cost, and implemented corrective measures before most customers noticed the issue. This response, which cost ₹3 crores, earned them Hero Honda's exclusive supplier status worth hundreds of crores over the next decade.

Lesson 2: The Art of OEM Relationships in India

Indian OEM relationships operate on different principles than Western markets. Contracts matter less than personal relationships. Price matters less than reliability. ASK mastered this by embedding themselves in OEM operations. Their engineers spent months at OEM facilities, understanding not just technical requirements but organizational dynamics. They learned who influenced decisions, what metrics mattered internally, and how to position their solutions accordingly.

The key was becoming indispensable beyond the product. ASK engineers helped OEMs with problems unrelated to brakes—supply chain optimization, quality systems, even recruiting. This value-added approach transformed ASK from vendor to partner. When OEMs faced production issues, ASK engineers were often the first called, regardless of whether brakes were involved.

Lesson 3: Manufacturing Excellence Through Constraint

ASK's manufacturing philosophy was shaped by capital constraints. Unable to afford cutting-edge German equipment, they bought used Japanese machinery and modified it. This forced innovation—their engineers became experts at extracting performance from modest equipment. The constraint became an advantage: ASK could achieve 90% of global best practice at 50% of the cost.

The localization went beyond equipment. ASK developed local supplier networks for raw materials, reducing import dependence and cost. They trained local toolmakers to maintain equipment, avoiding expensive foreign technicians. This localization created resilience—during COVID-19 when global supply chains collapsed, ASK maintained production using entirely local resources.

Lesson 4: Balancing Innovation with Reliability

ASK's innovation philosophy was conservative by Silicon Valley standards but perfect for their market. They followed a "fast follower" strategy—letting others prove new technologies, then implementing improved versions. This reduced R&D risk while maintaining technological relevance. When disc brakes emerged, ASK wasn't first, but their implementation was most reliable.

Innovation happened in increments rather than breakthroughs. Each year, ASK improved friction formulations by 2-3%—imperceptible to users but compound over decades. This continuous improvement culture, borrowed from Japanese manufacturing, created sustained advantage without risky bets on unproven technologies.

Lesson 5: Capital Allocation in Capital-Intensive Manufacturing

ASK's capital allocation was countercyclical and strategic. They expanded capacity during downturns when equipment was cheap and contractors hungry for work. The 2008 financial crisis, which devastated competitors, saw ASK's largest capacity expansion. By the time demand recovered, ASK had capacity while competitors scrambled to expand.

Working capital management was obsessive. ASK negotiated 60-day payment terms from OEMs but paid suppliers in 30 days, essentially using vendor financing for growth. Inventory was managed through sophisticated demand forecasting that balanced carrying costs with service levels. This capital efficiency allowed ASK to maintain ROCE above 20% despite being in capital-intensive manufacturing.

Lesson 6: Managing Technology Transitions

ASK's approach to technology transitions was pragmatic. They maintained profitable legacy products while investing in future technologies. When disc brakes emerged, ASK continued dominating drum brakes while building disc brake capabilities. This dual strategy provided cash flow for innovation while avoiding disruption risk.

The key was timing. ASK didn't chase every technology trend but waited for clear market signals. They entered disc brakes when OEM adoption reached 20%, EVs when sales crossed 100,000 units annually. This timing strategy reduced market risk while maintaining technology leadership where it mattered.

Lesson 7: Supply Chain Resilience Strategies

ASK's supply chain strategy emphasized resilience over efficiency. They maintained multiple suppliers for critical materials, even at higher costs. They kept strategic inventory buffers, accepting carrying costs as insurance. They developed alternative formulations that could use different raw materials if supplies disrupted.

Supplier relationships were cultivated carefully. ASK paid on time, even during cash crunches. They shared productivity gains with suppliers rather than squeezing margins. This approach created loyalty—during raw material shortages, suppliers prioritized ASK over larger customers who paid less reliably.

Lesson 8: The Importance of Aftermarket Presence

ASK's aftermarket strategy provided multiple benefits beyond revenue. It generated cash flow independent of OEM cycles. It provided market intelligence about product performance and failure modes. Most importantly, it created brand pull—consumers asking for ASK brakes influenced OEM sourcing decisions.

The aftermarket approach was sophisticated. ASK created different product tiers for different market segments—premium for brand-conscious consumers, value for price-sensitive segments. They invested in anti-counterfeiting measures—holograms, unique packaging, SMS verification—protecting brand value and margins.

Lesson 9: Building Learning Organizations

ASK's learning culture was systematic. Every product failure triggered root cause analysis. Every customer complaint generated process improvements. Every competitor move prompted strategic review. This learning was documented and shared—creating institutional memory that survived personnel changes.

Training investment was substantial. Engineers attended international conferences, workers received continuous skill upgrades, even administrative staff learned quality principles. This investment in human capital created capabilities that equipment alone couldn't provide. ASK's workers could achieve precision that automated systems struggled with, giving flexibility that pure automation lacked.

Lesson 10: Strategic Patience and Long-term Thinking

Perhaps ASK's greatest lesson is the power of strategic patience. They spent five years perfecting brake shoes before expanding products. They accepted lower margins to build market share, knowing margins would expand with scale. They invested in capabilities years before markets emerged, positioning for opportunities others couldn't see.

This patience extended to stakeholder management. The Rathee family retained control through multiple funding rounds, accepting dilution slowly. They resisted IPO pressures until the business was truly ready. They prioritized sustainable growth over quick wins, building a company for generations rather than quarterly earnings.

IX. Bear vs. Bull Case & Financial Analysis

Standing in ASK's boardroom today, you can see two futures. On one wall, charts showing India's unstoppable mobility growth, ASK's dominant market position, and expanding margins. On the opposite wall, equally compelling charts showing customer concentration risks, technology disruption threats, and margin pressure from commoditization. Which future will materialize depends on factors both within and beyond ASK's control.

The Bull Case: Structural Tailwinds and Competitive Moats

The optimistic view starts with ASK's commanding 50% market share in India's two-wheeler braking systems market serving 16.25 million units annually. This isn't just market share—it's market control. When half of all two-wheelers in India stop because of your products, you've achieved something beyond normal competitive advantage.

The market growth trajectory provides powerful tailwinds. India's two-wheeler penetration at roughly 130 vehicles per 1,000 people remains far below developed market levels of 500+. Even reaching Southeast Asian levels of 300 would more than double the market. With GDP per capita rising and financing becoming accessible, this growth seems inevitable rather than aspirational.

The EV transition multiplies this opportunity. With 1.14 million electric two-wheelers sold in India in 2024 and growing exponentially, ASK's early positioning in EV-specific formulations creates first-mover advantages. Higher ASP for EV braking systems, combined with rapid volume growth, could double ASK's addressable market by 2030.

ASK's manufacturing and R&D capabilities represent irreplaceable assets. Their portfolio of 52 proprietary formulations represents decades of accumulated knowledge. The testing infrastructure, OEM relationships, and field performance data create compounding advantages that strengthen over time.

Financially, the bull case is compelling. With revenue of ₹3,630 crores and profit of ₹257 crores, ASK generates substantial cash flow for reinvestment. ROCE consistently above 20% demonstrates efficient capital allocation. The asset-light aftermarket business provides margin expansion opportunity as it scales.

International expansion remains largely untapped. As Indian OEMs expand globally, they'll likely take trusted suppliers with them. ASK could replicate their Indian dominance in similar markets—Bangladesh, Africa, Southeast Asia—where conditions and price points align with their capabilities.

The regulatory environment increasingly favors established players like ASK. Upcoming ABS mandates, stricter emission norms driving lightweighting, and safety regulations all require sophisticated capabilities that smaller competitors lack. Each regulation essentially raises entry barriers while playing to ASK's strengths.

The Bear Case: Concentration Risks and Disruption Threats

The pessimistic view starts with customer concentration. Dependence on top three customers for more than half of revenue means losing any of these customers or business decline could significantly impact overall revenue. This concentration creates negotiating leverage for OEMs who know ASK can't afford to lose them.

Technology disruption poses existential questions. If autonomous vehicles eliminate private ownership, if shared mobility reduces vehicle sales, if new materials make friction braking obsolete—ASK's entire business model becomes questionable. While these scenarios seem distant, technology transitions can happen faster than expected.

The company depends on third party suppliers for raw material requirements including aluminum. Raw material costs, particularly for specialty chemicals and metals, are volatile and often beyond ASK's control. Sustained input cost inflation without corresponding price increases could squeeze margins significantly.

Competition from global players remains a threat. While they've failed so far, companies like Bosch or Continental could decide India's market is strategic enough to accept lower margins. Their technology advantages and global scale could eventually overcome ASK's local advantages.

The ICE to EV transition, while an opportunity, also poses risks. If transition happens faster than expected, ASK's ICE-focused infrastructure becomes stranded assets. If it happens slower, heavy EV investments generate subpar returns. Threading this transition requires perfect timing—difficult in uncertain markets.

Market maturity in two-wheelers could arrive sooner than expected. Urban congestion, improving public transport, and environmental concerns could reduce two-wheeler demand in major cities where ASK generates disproportionate revenue. Rural markets, while large, have different price points and service requirements.

Financial Analysis: Valuation Perspectives

At a market capitalization of ₹9,214 crores, ASK trades at approximately 36x P/E based on current earnings. This seems expensive for a manufacturing company but potentially reasonable for a market leader with strong growth prospects.

Peer comparison provides context. Global automotive component companies trade at 15-25x P/E, suggesting ASK commands a premium. This premium could be justified by higher growth rates, market dominance, and EV exposure. However, it also suggests limited upside unless growth accelerates beyond current expectations.

The EV/EBITDA multiple around 20x aligns with high-quality industrial companies but leaves little room for disappointment. Any miss on growth or margins could trigger multiple compression, creating downside risk even if business fundamentals remain strong.

Free cash flow generation remains robust, with FCF/Sales around 5-6%. This cash generation supports both growth investments and potential dividends, providing downside protection. The ability to self-fund growth reduces dilution risk and maintains family control.

Balance sheet strength with modest debt provides flexibility. ASK could leverage up for acquisitions or capacity expansion without stressing coverage ratios. This financial flexibility becomes valuable during industry consolidation or technology transitions.

Scenario Analysis: Multiple Futures

The base case assumes steady market growth, maintaining market share, and gradual EV transition. This generates 15-20% revenue CAGR and 20-25% profit CAGR over five years, justifying current valuations with modest upside.

The optimistic scenario sees accelerated EV adoption, successful international expansion, and margin expansion from premiumization. Revenue could compound at 25-30%, profits at 30-35%, potentially doubling the stock price over three years.

The pessimistic scenario involves losing a major customer, delayed EV transition, and margin pressure from competition. Revenue growth slows to single digits, margins compress, and multiple contracts—potentially halving the stock price.

The probability-weighted expected return suggests modest upside with meaningful downside risk. This asymmetry argues for waiting for better entry points unless you have strong conviction in the bull case.

Key Monitorables for Investors

Customer concentration metrics matter most. Any change in top three customer shares, new customer additions, or customer losses would significantly impact the investment thesis. Quarterly order books and customer guidance provide early indicators.

EV sales trajectory and ASK's share within EV OEMs indicate future growth potential. Monthly vehicle registration data, available publicly, provides real-time market feedback.

Margin trends reveal competitive dynamics and pricing power. Gross margin expansion indicates value addition and pricing discipline. EBITDA margin trends show operating leverage and efficiency gains.

Capital allocation decisions signal management confidence and strategic direction. Large capex announcements suggest growth confidence. Acquisitions indicate strategic pivots. Dividend policy reveals cash generation confidence.

The Verdict: Quality at a Price

ASK Automotive represents a high-quality business with substantial moats trading at premium valuations. For long-term investors believing in India's mobility story and ASK's ability to navigate technology transitions, current levels might prove reasonable. For value investors seeking margin of safety, patience might be rewarded with better entry points during market volatility.

The investment decision ultimately depends on time horizon and risk tolerance. ASK isn't a value play or momentum trade—it's a quality compounder requiring patience and conviction. The business quality is undeniable; whether the stock offers attractive returns depends on entry price and execution over the next decade.

X. Epilogue: The Road Ahead

The view from ASK Automotive's headquarters in Gurgaon tells two stories simultaneously. Looking north, you see the congested streets of old Delhi, where millions of two-wheelers navigate chaos daily—ASK's current empire. Looking south toward Gurgaon's Cyber City, you glimpse the future: electric vehicles gliding silently past glass towers, autonomous pods ferrying executives, the mobility revolution that will reshape everything ASK knows.

This duality—mastery of the present, uncertainty about the future—defines ASK's strategic moment. They've won the last war decisively, controlling half of India's two-wheeler braking market. But the next war will be fought with different weapons, on different terrain, against different enemies. The question isn't whether ASK can compete—it's whether they can transform fast enough to lead.

India's mobility transformation over the next decade will be unlike anything the world has seen. No country has attempted to electrify transportation at this scale, with this population density, at this income level. The government's target of 30% EV penetration by 2030 means adding millions of electric vehicles annually to infrastructure designed for the 19th century. This chaos creates opportunity for companies that can navigate uncertainty while maintaining operational excellence—exactly ASK's sweet spot.

The autonomous vehicle revolution, while seemingly distant, poses fundamental questions. If vehicles can communicate and coordinate, avoiding accidents through AI rather than friction, what happens to brake manufacturers? ASK's response has been pragmatic: autonomous vehicles will still need emergency braking systems, perhaps even more sophisticated ones given the liability implications of AI failure. They're already developing fail-safe systems that activate when sensors fail—betting that redundancy will matter more, not less, in an autonomous world.

International expansion represents the clearest growth path. India's two-wheeler manufacturers are globalizing, with Hero MotoCorp targeting Africa, Bajaj dominating multiple emerging markets, and TVS expanding across Southeast Asia. These companies prefer taking proven suppliers with them rather than qualifying new ones in each market. ASK's opportunity is to become the embedded supplier for Indian OEMs' global ambitions—a strategy that minimizes market development risk while maximizing growth potential.

The technology roadmap extends beyond traditional braking. ASK is exploring brake-by-wire systems that eliminate mechanical linkages, regenerative braking optimization that maximizes energy recovery, and predictive maintenance systems that alert riders before failures occur. These aren't incremental improvements—they're fundamental reimaginations of what braking systems can be.

If we were CEO of ASK today, three priorities would dominate:

First, accelerate the EV transition while maintaining ICE profitability. This means running two businesses in parallel—optimizing the cash-generating ICE business while investing aggressively in EV capabilities. The challenge is resource allocation: too much focus on ICE risks missing the EV wave; too much on EV risks destroying current profitability.

Second, reduce customer concentration through geographic expansion. Every new market entered, every new customer acquired reduces dependency on top Indian OEMs. The target should be no single customer exceeding 15% of revenue within five years—achievable through international expansion and aftermarket growth.

Third, build software capabilities that transform ASK from hardware supplier to systems integrator. The future of automotive lies in software-defined vehicles where mechanical components are controlled by code. ASK needs to own the software layer for braking systems, creating switching costs beyond physical components.

The organizational transformation required is profound. ASK needs to attract software engineers to a brake manufacturing company, create innovation culture within manufacturing discipline, and maintain family control while professionalizing management. This cultural evolution might prove harder than any technology transition.

Why Component Manufacturers Matter in the EV Revolution

The conventional wisdom suggests EV disruption will destroy traditional automotive suppliers. The reality is more nuanced. EVs are simpler mechanically but more complex systematically. They require fewer parts but more sophisticated ones. They eliminate some components while creating entirely new categories.

Component manufacturers like ASK that can navigate this transition become more valuable, not less. They bring manufacturing expertise that software-focused EV startups lack. They understand supply chains, quality systems, and scale production—capabilities that take decades to build. Most importantly, they understand reliability at scale, something EV makers are still learning.

The Indian context amplifies these advantages. EV manufacturers in India can't rely on Chinese suppliers due to geopolitical tensions and quality concerns. They can't afford Western suppliers due to cost constraints. They need local partners who can deliver global quality at Indian prices—exactly ASK's proposition.

Key Takeaways for Founders and Investors

ASK's journey offers several lessons for founders building in traditional industries:

Patience Pays: ASK spent 35 years building market dominance. In an era celebrating overnight unicorns, their methodical approach seems anachronistic. Yet their moats are deeper, their margins more sustainable, and their market position more defensible than most unicorns.

Timing Matters More Than Speed: ASK wasn't first in any technology but timed entries perfectly. They entered disc brakes when adoption hit 20%, EVs when volumes justified investment. This "fast follower" strategy reduced risk while maintaining competitiveness.

Trust Scales Better Than Technology: In safety-critical industries, trust becomes the ultimate moat. ASK invested in relationships, reliability, and reputation—intangibles that technology alone can't displace.

Local Champions Can Win Against Global Giants: ASK defeated Bosch and Continental not through superior technology but through deeper market understanding. In industries where local conditions matter, geographic focus beats global scale.

For investors, ASK demonstrates that unsexy businesses in traditional industries can generate exceptional returns. The key is identifying companies with:

- Dominant market positions in growing markets

- High switching costs creating customer stickiness

- Management capable of navigating technology transitions

- Financial discipline maintaining returns through cycles

- Strategic patience to compound advantages over time

The Road Ahead

ASK Automotive stands at an inflection point. They've conquered the Indian two-wheeler braking market, built formidable moats, and positioned for the EV transition. The foundation for the next phase of growth is solid. But the road ahead is far from certain.

Success will require balancing contradictions: maintaining manufacturing excellence while building software capabilities, serving ICE customers while preparing for EVs, expanding globally while strengthening local positions, professionalizing management while maintaining entrepreneurial culture.

The ultimate test will be whether ASK can transform from a component supplier to a mobility solutions provider. This isn't just about making better brakes—it's about reimagining what safety means in an autonomous, electric, connected world. It's about evolving from stopping vehicles to enabling safe mobility.

The stakes extend beyond ASK. As India attempts to leapfrog into electric mobility while serving the transportation needs of 1.4 billion people, companies like ASK become critical infrastructure. Their success or failure impacts not just shareholders but millions depending on safe, affordable transportation.

Looking back at ASK's 36-year journey from a single-product manufacturer to market dominator, the path seems inevitable. Looking forward, nothing is certain except change. But if history is any guide, ASK's combination of engineering excellence, strategic patience, and operational discipline positions them well for whatever comes next.

The story of ASK Automotive isn't finished—in many ways, it's just beginning. They've proven they can dominate traditional markets. Now they must prove they can shape emerging ones. They've shown they can stop vehicles safely. Now they must show they can help India's mobility revolution move forward safely.

For a company that built its fortune on friction, the future ironically depends on reducing friction—in transportation, in technology adoption, in the transition to sustainable mobility. The company that masters stopping might ultimately enable India to accelerate into the future.

That's the paradox and promise of ASK Automotive: a brake manufacturer that could help India accelerate, a traditional company enabling transformation, a hidden champion emerging into the spotlight just as the stage is set for the next act of India's mobility story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube