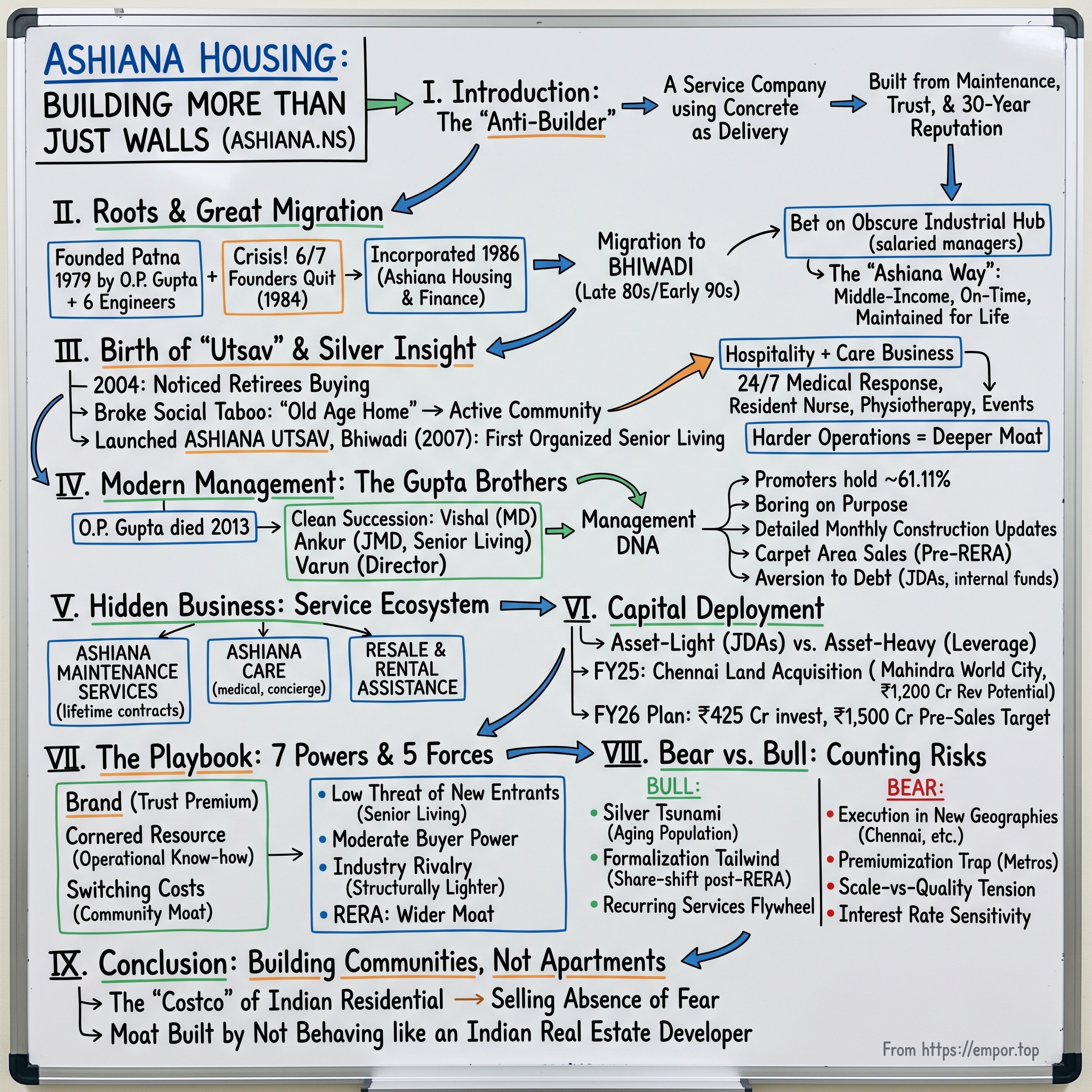

Ashiana Housing: Building More Than Just Walls

I. Introduction: The "Anti-Builder" of India

Walk into the sales lounge of almost any Indian real estate developer and you encounter the same theatre. A glossy brochure with computer-generated infinity pools. A salesperson promising possession "by next Diwali, sir." A floor plan that conspicuously omits the carpet-versus-super-built-up area calculation. And, in the back of the buyer's mind, the nagging suspicion — drilled in by a decade of headlines about Amrapali, Unitech, Jaypee, and a dozen unfinished towers around Noida — that the keys might never actually arrive.

Now picture the opposite. A 240-acre community in भिवाड़ी Bhiwadi, a dusty industrial town on the Rajasthan-Haryana border, where retirees in their seventies play Tambola in a clubhouse. The same developer who sold them the flat in 2008 is still mowing the lawn in 2026. The unit they bought has been independently measured down to the square inch. The monthly construction update for the next phase was emailed to them, on time, every month. Their daughter in San Francisco can log in to a portal and see exactly where the project stands.

That second picture is आशियाना हाउसिंग Ashiana Housing Limited, and it is one of the strangest companies in Indian real estate — strange because it is, by Indian developer standards, almost embarrassingly normal. No off-balance-sheet entities. No flamboyant promoter Instagram. No suing of homebuyers. Just a small family-run firm from Patna that quietly invented an entire product category in India — organized senior living — and built the most boring, most trusted brand in a sector defined by its untrustworthiness.

The thesis of this episode is that आशियाना Ashiana is not really a builder at all. It is a service company that uses concrete as a delivery mechanism. The mortar holds the bricks together, but the moat is built out of maintenance contracts, doctor's-on-call rosters, resale assistance, and a thirty-year reputation for handing over what was promised, when it was promised. In an industry where the customer's biggest fear is the developer disappearing, आशियाना Ashiana made the radical choice to never leave.

This is the story of how a partnership of seven engineers in Bihar — six of whom would soon walk out the door — became the category creator for वरिष्ठ नागरिक आवास senior citizen housing in India, a market that the consulting firm जोन्स लांग लासाल JLL has projected to grow into a multi-billion-dollar opportunity by the end of the decade.1 It is the story of a debt-averse, JDA-loving capital allocator that watched the rest of the industry blow itself up on land banks. And it is, ultimately, the story of why the average age of a homebuyer at a आशियाना Ashiana Utsav community is closer to seventy than thirty-five — and why that demographic accident may turn out to be the most defensible business model in Indian real estate.

We start where every good Indian business story starts: with a family, a small partnership, and an argument.

II. Roots & The Great Migration: From Patna to Bhiwadi

Patna in 1979 was not a city anyone associated with sophisticated real estate. The state of Bihar was on the verge of decades of political turmoil. The roads were unreliable, the power supply was a rumour, and the local construction business was dominated by small-time contractors who built one floor at a time, plot by plot, with cash deals settled in the back rooms of property brokers. Into this milieu walked an engineer named ओम प्रकाश गुप्ता Om Prakash Gupta, a man who would die in 2013 having built a publicly listed company that practically nobody in Patna at the time could have imagined.2

Gupta did not start alone. He pooled together with six fellow engineers, each contributing ₹70,000 — a meaningful sum at the time, though hardly venture capital by any modern standard — and founded the partnership as आशियाना इंजीनियर्स Ashiana Engineers.3 The name आशियाना ashiana is Urdu/Hindi for "nest" or "abode," and the early projects in Patna lived up to the metaphor: middle-income flats with the previously unheard-of luxuries of community amenities and post-sale maintenance. In Bihar in the early 1980s, this was not a value proposition. It was an alien concept.

The first crisis was a textbook partnership blow-up. By 1984, six of the seven engineers had quit — disputes over decision-making, the usual debris when too many strong opinions chase the same corner office.3 Gupta was left holding the company. Most founders, faced with that kind of attrition, fold or sell. Gupta restructured. On June 25, 1986, the company was formally incorporated as आशियाना हाउसिंग एंड फाइनेंस Ashiana Housing & Finance (India) Limited, registered with the Registrar of Companies in West Bengal.2 The Bihar roots stayed, but the legal home moved east, and the strategic gaze began drifting west.

That westward drift turned into the company's defining migration. Through the late 1980s and early 1990s, Gupta made the unfashionable decision to abandon his home market entirely and bet the company on an obscure industrial cluster on the Delhi-Jaipur highway: भिवाड़ी Bhiwadi, in Rajasthan's Alwar district.4 At the time, Bhiwadi was a place that none of the listed Indian developers would have touched with a balance sheet. It had no IT industry, no metro, no glamour — just a slowly accreting belt of small-and-medium manufacturing units producing auto parts, ceramics, and chemicals for the factories of Gurgaon and Manesar.

This is the part of the story that gets glossed over in the official corporate timelines, but it is the most important strategic move the company ever made. Gupta did not pick Bhiwadi because it was cheap, although it was. He picked it because of who lived there: a managerial and supervisory class with steady industrial salaries, who needed quality housing for their families and had nowhere organized to buy it. The buyers were engineers from माहिंद्रा Mahindra, होंडा Honda, and सेंट गोबैन Saint-Gobain plants — the people who, in Mumbai or Bangalore, would have been the natural customers for a गोदरेज Godrej Properties or an ओबेरॉय Oberoi Realty. In Bhiwadi, they had आशियाना Ashiana and very little else.

What Gupta then did with this captive market was, by Indian standards of the time, almost philosophical. He decided that the company would not just build the homes and walk away. It would stay. It would run the swimming pool. It would clean the corridors. It would maintain the diesel generators. This was a near-heretical idea in an Indian builder ecosystem that had perfected the art of pocketing the sale proceeds and vanishing into the next project. Out of this came what insiders eventually called the "Ashiana Way" — middle-income housing, delivered on time, maintained for life. It was an ethos forged not in a strategy offsite, but on the dusty plots of Bhiwadi, where there was no one else to do the maintenance and where the brand reputation lived or died on whether the lift worked in July.

By the time the company's name was finally simplified to आशियाना हाउसिंग लिमिटेड Ashiana Housing Limited in 2007 — dropping the "Finance" hangover from its NBFC-era ambitions — Bhiwadi was the spine of the business.5 It was also the petri dish where Gupta and his sons would, almost by accident, stumble onto the second great strategic insight of the company's life: that the people moving into Bhiwadi flats were not just young engineers. They were also, increasingly, their parents.

III. The Birth of "Utsav" and the Silver Insight

In 2004, the conversation inside आशियाना Ashiana shifted from "what should we build next" to "who is buying what we already built." A pattern had been emerging in the Bhiwadi sales office. A surprising number of buyers were not the engineers themselves, but their fathers and mothers — Delhi-based retirees who had read about Bhiwadi, seen the prices, and decided that they could not justify renting in दिल्ली Delhi for another two decades. They wanted gated, low-maintenance, single-floor living, away from the chaos of the capital but close enough to it. They wanted, although nobody yet had a vocabulary for it in the Indian market, a retirement community.

The cultural problem was that nobody in India was supposed to admit they wanted one.

To understand the audacity of what आशियाना Ashiana did next, one has to understand the social emotional charge around the concept of a "home" for older Indians. In the Western imagination, an active retirement community in फ्लोरिडा Florida is aspirational. In India, until well into the 2000s, the very phrase "old age home" was synonymous with shame — the place where parents were dumped by children who had failed in their dharma. The संयुक्त परिवार joint family ideology, where three generations cohabit under one roof, was the cultural default and a moral identifier. To move into a senior-only community was to advertise familial failure.

What आशियाना Ashiana saw — and what most Indian developers either missed or refused to touch — was that the underlying social structure had already collapsed. Liberalization in 1991 had sent an entire generation of children to बेंगलुरु Bengaluru, गुड़गांव Gurgaon, मुंबई Mumbai, and increasingly to सिलिकॉन वैली Silicon Valley. The joint family was now a long-distance Zoom call. The parents were, in fact, lonely. The shame was a fiction; the demand was real. Somebody just had to be willing to be the brand that named it.

आशियाना Ashiana was that brand. After roughly three years of internal study and product design, the company launched आशियाना उत्सव Ashiana Utsav in भिवाड़ी Bhiwadi in 2007 — the first organized, large-scale senior living community in India.6 The branding was a masterstroke. "Utsav," the Sanskrit word for "festival" or "celebration," carried none of the institutional dread of "old age home." It was framed not as a retreat from family, but as a destination of choice. Brochures featured grandparents who had moved closer to their grandchildren, not further away — a Bhiwadi flat being a two-hour drive from a Gurgaon IT campus where the adult kids worked.

The product itself was where the real strategic moat began to form. A traditional Indian builder builds, sells, and exits. आशियाना Ashiana looked at Utsav and realized it was selling, in effect, a hospital-adjacent hospitality business. The community needed twenty-four-hour medical response, a resident nurse, ambulance tie-ups, physiotherapy, geriatric-friendly grab bars and ramps, hobby classes, cultural events, festival celebrations.7 This was not construction. This was running a small assisted-living operation that happened to have apartments attached to it.

That distinction matters more than any single financial metric in the आशियाना Ashiana story. A construction business has a cost structure dominated by cement, steel, and labour. A hospitality-and-care business has a cost structure dominated by people and processes. The two require completely different management muscles, and the second is enormously harder to replicate from scratch. By 2026, two decades into the experiment, the company runs senior living projects in भिवाड़ी Bhiwadi, लवासा Lavasa near Pune, जयपुर Jaipur, and चेन्नई Chennai, and hosts an annual residents' carnival called "Jashn" that pulls more than 500 seniors across geographies.7 Try replicating the institutional knowledge — what to feed a diabetic resident with kidney complications, how to handle a 3 a.m. cardiac event in a community of 800 — from a builder's playbook. You cannot.

That, in essence, was the silver insight: the harder the operations, the deeper the moat. And in a country whose over-60 population was on track to roughly double over the next two decades, the silver tsunami was just beginning to lap at the shore.

IV. Modern Management: The Gupta Brothers

ओम प्रकाश गुप्ता O.P. Gupta died in 2013 at the age of sixty-six, a year and change after the company had handed over the first phase of आशियाना उत्सव Ashiana Utsav in लवासा Lavasa.28 He left behind something rarer in Indian family business than capital or land: a fully constructed succession.

The succession came in the form of three brothers — विशाल गुप्ता Vishal Gupta, अंकुर गुप्ता Ankur Gupta, and वरुण गुप्ता Varun Gupta. By the time the founder passed, all three had been working in the business for years. There was no Murthy-style return-of-the-founder drama, no Ambani-style fraternal split. The transition was, by the unglamorous standards of Indian corporate governance, almost startlingly clean.

विशाल Vishal, the eldest, became Managing Director — by FY2024-25, he had spent twenty-eight years inside the company, running finance, project execution, and general administration.9 He is the one who signs off on capital allocation, who decides whether to chase a Pune land parcel or wait six months. अंकुर Ankur, with more than twenty-two years in the company, took the role of Joint Managing Director and became the public face of the senior living business; he had personally led much of the research that informed the Utsav product design.9 वरुण Varun, the third brother, came in as Whole-time Director with responsibility for the on-ground project businesses outside senior living.

The financial structure of the family says a lot about how they think. As of the most recent shareholding pattern, the promoter group — which is essentially the brothers and family — held approximately 61.11% of आशियाना Ashiana.10 Within that promoter group, वरुण Varun was the single largest individual holder at roughly 19.8%, a deliberate distribution that keeps no one brother dominant.10 Foreign institutions held about 7.9%, domestic institutions about 8.0%, and the public the remaining 23%.10 In an Indian family-run real estate company, those institutional numbers are remarkable — they imply that professional money has looked at the books, looked at the governance, and decided that it can sit on the cap table.

The cultural DNA of the management is "boring on purpose." Two specific behaviours stand out. First, आशियाना Ashiana is one of the very few Indian developers to publish detailed monthly construction updates for every project — photographs, milestones, percentage of slab work complete, the whole apparatus that, in most Indian builders, is hidden behind sales-team-only WhatsApp groups. Second, the company sells flats on "carpet area" — the actual usable square footage inside the walls — long before रेरा RERA, the Real Estate (Regulation and Development) Act of 2016, made that mandatory across India. To understand why this matters, consider that the rest of the industry historically inflated headline areas using the "super built-up" definition, which lumped in lobbies, lift wells, and notional common-area shares to make per-square-foot prices look lower. आशियाना Ashiana's carpet-area transparency was, in effect, a self-imposed price hike — and the buyers, weirdly, loved them for it.

The second philosophical commitment of the brothers is the aversion to debt. Where most Indian developers historically grew by stockpiling land — pledging it, borrowing against it, paying high-double-digit interest costs, and praying the cycle didn't turn — आशियाना Ashiana decided to grow through संयुक्त विकास समझौता joint development agreements (JDAs) and incremental land purchases funded largely by internal accruals. This was an unsexy choice in 2007. It looked positively prophetic by 2013, when the cycle did turn, when डीएलएफ DLF was struggling with debt and when यूनिटेक Unitech and आम्रपाली Amrapali would later become regulatory case studies. The discipline showed up in small, recent ways too: in May 2026, the company prepaid roughly ₹34.28 crore to आईसीआईसीआई प्रूडेंशियल ICICI Prudential funds against secured non-convertible debentures, a routine debt servicing event that nonetheless tells you exactly how this management likes to die — owing very little.11

Boring, as a strategy, is wildly underrated. And the boring expression of that strategy is what the next section is about: the hidden services empire bolted onto the housing business.

V. Hidden Businesses: The Service Ecosystem

If you asked the average analyst what आशियाना Ashiana does, the answer would be "they build flats." That answer is, charitably, half-right. To see the other half, you have to look at a part of the income statement that most builders treat as a rounding error: the line variously labelled as "Other Operating Income" or "Maintenance and Hospitality."

Most Indian developers, the moment a project is "handed over," wash their hands. They convene the residents into a रेजिडेंट्स वेलफेयर एसोसिएशन Residents' Welfare Association (RWA), hand them the keys to the diesel generator, and decamp to the next plot. The economics, on paper, look better — the developer offloads a low-margin, high-headache business. In practice, the moment the developer leaves, the brand experience degrades: lifts break, security guards drift away, the swimming pool turns green. The next prospective buyer of a flat in the area then googles the developer's name and discovers a Facebook group full of furious owners.

आशियाना Ashiana looked at this conventional wisdom and chose the opposite. From its earliest Bhiwadi communities onward, the company structured its operations so that आशियाना मेंटेनेंस सर्विसेज Ashiana Maintenance Services (and its sister entities) retained the maintenance contract for the lifetime of the community, in many cases without an option for the residents to switch providers. The framing inside the company was that maintenance was not a cost centre; it was the manufacturing equipment for the brand.

The economics of this are subtle but powerful. A maintenance contract is, in finance terms, an annuity. The flat is a one-time payment; the maintenance is a recurring payment, indexed loosely to inflation. Across a 25-year life of a community, the recurring stream begins to rival the original sale revenue on a present-value basis. And because the operating costs are largely passed through, the margin is structurally low but the predictability is structurally high — the precise opposite of the lumpy, project-driven revenue that defines the development business.

Bolted onto maintenance is a second hidden engine that the company brands loosely as आशियाना केयर Ashiana Care. This is the hospitality and concierge service that runs inside the senior living projects — the doctor on call, the on-site nurse, the housekeeping for residents who pay for it as an add-on, the meal plans, the medication reminders, the ambulance tie-ups with nearby hospitals.7 These services are sold as monthly subscriptions. They look small in absolute revenue terms today. They are absolutely critical in resale terms tomorrow.

That is the third hidden lever: resale and rental assistance. आशियाना Ashiana runs an internal desk that helps existing owners sell or rent out their units to new buyers, especially in the senior living communities where many flats turn over due to bereavement or relocation back to children.12 Why does the developer care? Because a fragmented, distressed secondary market drags down headline prices in the project, which in turn drags down the developer's pricing power on new launches in the same micromarket. Controlling the secondary market is, effectively, controlling the brand floor.

The newest experiment is at the other end of the demographic spectrum. The company has been quietly building out किड्स सेंट्रिक होम्स kid-centric homes — communities designed around the needs of families with young children. The architectural cues are different (more playgrounds, more crèche space, more visibility from the kitchen to the play area), but the underlying business logic is identical to Utsav. It is not a building. It is a community service wrapped around a building. If senior living is the company's silver-economy bet, kid-centric is the millennial-parent bet. Both are demographic tailwinds that pure-play construction firms cannot easily pursue, because the operating expertise sits in the service layer.

Put all of this together and what emerges is less a real estate developer than a vertically integrated lifestyle operator that uses physical real estate as its anchor product. The cement-and-steel business gets the headlines. The services flywheel underneath it gets the customer for life.

VI. Capital Deployment: Asset-Light vs. Asset-Heavy

Real estate, fundamentally, is a capital allocation business in fancy clothes. Every developer in the world is doing some version of the same trade: acquiring land, building on it, and selling the finished product. Where they differ — and where most of them die — is in how they finance the land.

The high-leverage approach is the one made famous, and infamous, by the marquee Indian developers of the 2005-2012 cycle. Buy land outright, in cash. Pledge it against bank loans and non-convertible debentures. Use the borrowings to buy more land. Plan to ride the next residential boom and refinance everything at lower rates. When the cycle turns — and Indian real estate cycles turn brutally — the cost of capital eats the developer alive. डीएलएफ DLF, यूनिटेक Unitech, and a host of others learned this in slow, public motion through the 2010s.

The asset-light alternative is the संयुक्त विकास समझौता Joint Development Agreement (JDA) model. Under a JDA, the landowner contributes the land and retains ownership through construction; the developer brings the construction expertise, capital, and sales engine; and the two parties split the finished saleable units or the sale proceeds in an agreed ratio. The landowner gets a slice of upside without selling outright. The developer gets a project without funding the land purchase. The capital intensity of the business drops dramatically.

आशियाना Ashiana has been one of the most consistent practitioners of this model in India, particularly outside its core भिवाड़ी Bhiwadi heartland. The peer it is most often compared with is गोदरेज प्रॉपर्टीज Godrej Properties, which built its entire national footprint on JDA-style asset-light expansion. Where गोदरेज Godrej used JDAs as a pure growth weapon — a way to put the family brand on as many projects as quickly as possible — आशियाना Ashiana used them as a discipline. The JDA acts as a built-in approval test: if a landowner believes in the project, they will sign a JDA; if no landowner is willing, the project probably should not be done.

This discipline is visible in the company's current footprint. As of mid-2025, आशियाना Ashiana had nine ongoing projects: three in भिवाड़ी Bhiwadi, three in चेन्नई Chennai, and one each in जयपुर Jaipur, पुणे Pune, and लवासा Lavasa.13 The geographic concentration is intentional. The company has been deliberate that it will not chase land in markets where it does not yet understand the buyer.

The biggest single recent move was in Chennai. In FY2024-25, आशियाना Ashiana acquired roughly 22.71 acres of land within माहिंद्रा वर्ल्ड सिटी Mahindra World City near Chennai for a large-scale senior living project. Management has guided that the project carries an estimated revenue potential of around ₹1,200 crore against roughly 15 lakh saleable square feet.14 The choice of an integrated township as the host environment is itself a strategic signal: senior living requires not just the apartments, but a surrounding ecosystem of healthcare, daily services, and infrastructure. Plugging into a Mahindra-built township is faster than building one from scratch.

The company's broader capital plan for FY26 was to invest about ₹425 crore in senior living development alone — earmarked for landowner payouts, construction, and related project expenses.14 Management has set a target of pre-sales of ₹1,500 crore and signalled that senior living would rise to roughly 25% of pre-sales value, with planned expansion into मुंबई Mumbai and बेंगलुरु Bengaluru.15

Of course, the JDA model is not without its own risks, and आशियाना Ashiana has been bitten too. In May 2026, the company terminated a 20-acre land lease with माहिंद्रा वर्ल्ड सिटी जयपुर Mahindra World City Jaipur, citing non-visibility on approvals required from the counterparty.16 In an outright purchase, the developer controls the timeline; in a JDA or lease, the developer is exposed to whatever delays the landowner runs into. Capital-light is not capital-free.

The other often-cited "what about Lavasa?" question — the integrated hill-city development outside Pune that became a long-running case study in Indian real estate of regulatory and approval risk — is also instructive. आशियाना Ashiana was a participant in the broader Lavasa story through its own आशियाना उत्सव Ashiana Utsav Lavasa project, with the first phase handed over to residents in 2013 and Phase 4 receiving its completion certificate as recently as July 4, 2024.8 The project was not a financial blow-up for the company, but the experience reinforced an internal preference for established industrial hubs and Tier-1 satellite markets over speculative greenfield masterplans.

When real estate cycles turn — and India's will — the developers that survive are the ones with low fixed debt, no land speculation, and a long string of patient JDA partners. आशियाना Ashiana has, deliberately, built itself to look exactly like that.

VII. The Playbook: 7 Powers and 5 Forces

The temptation, with a company like आशियाना Ashiana, is to call it "well managed" and leave it at that. That kind of vague praise is exactly the kind of analysis that gets investors killed in cyclical industries. The more useful question is: what specific structural advantages does the company have, and how do they map onto the strategy frameworks that survive a downturn?

Hamilton Helmer's 7 Powers framework is a good starting lens. Three of the seven powers apply in unusually clean ways here.

The first is Brand. Brand power, in Helmer's definition, is the ability to charge a higher price for an objectively identical product, purely because of the name attached. In Indian real estate, the brand premium is not five percent. It is the difference between a project that gets sold out and a project that gets stuck. आशियाना Ashiana has spent four decades building a "trust premium" in a trust-deficit industry — and the proof point is the buyer behaviour pattern of the senior living business, where elderly customers, who are by definition more risk-averse than first-time twenty-five-year-old buyers, gravitate toward the most boring, most reliable name on the menu.

The second is Cornered Resource. In आशियाना Ashiana's case, the cornered resource is not a license, a patent, or a plot of land. It is two decades of accumulated operational know-how in geriatric community management. The hundreds of small, unwritten decisions that go into running a senior living community — what kind of railings, how to space the doctor visits, how to manage end-of-life care without traumatizing the rest of the community — are not in any consulting deck. They are baked into the institutional memory of the staff and management. A pure construction firm that decides tomorrow to enter senior living is at least seven to ten years away from catching up.

The third is Switching Costs, dressed here in an unusual form: the "community moat." Once an elderly resident has moved into an Utsav community, made friends, learned the geography, established their daily routine of the morning walk and the evening Tambola game, the personal cost of switching to a different community is enormous. It is not financial; it is emotional and social. This locks in not just the resident but, indirectly, the brand reputation in their family — the daughter who saw her mother thriving at Utsav is the same daughter who will recommend Utsav to her in-laws.

Now flip the lens to Porter's Five Forces, and the picture sharpens further.

The threat of new entrants in residential real estate generally is, in principle, high — land is more or less available, capital can be raised, and India has thousands of small builders. But specifically in senior living, the threat is low. New entrants face the cornered-resource problem above, and they face a brand-trust problem that a 35-year-old retiree's family is not going to take a chance on with an untested player.

Buyer power in senior living is moderate. Elderly buyers are price-conscious, and they have alternative options like staying in their existing home with hired help. But the lack of comparable organized players in senior living means that, in practice, आशियाना Ashiana is competing against the status quo, not against another developer. That is a much more pleasant competitive structure.

Supplier power in real estate is essentially the construction supply chain — cement, steel, glass, labour contractors — and is broadly fragmented in India. This is a force आशियाना Ashiana neither uniquely benefits from nor suffers from; it is industry-neutral.

The threat of substitutes is interesting. The substitute for organized senior living is informal senior living: keeping the parent at home, hiring a घरेलू सहायक domestic helper, hoping the children stay nearby. This substitute is enormous and free, and it is also slowly losing ground every year as urbanization and emigration continue to eat into the joint family structure. The long arc is favourable.

Industry rivalry in residential is intense, with developers slashing prices and offering freebies. But in senior living, rivalry is structurally lighter because there are simply fewer players willing to commit to the operating complexity. This is what makes the segment so attractive as a growth driver — it is one of the few residential sub-segments in India where price competition has not yet eaten margins.

There is also a regulatory tailwind worth naming explicitly: रेरा RERA, enacted in 2016, has been a forced cleanup of the Indian residential sector. The mandatory escrow of 70% of project receipts, the registration of every project, the standardization of carpet-area pricing, all of these have raised the cost of being a sloppy builder. They have, in effect, pushed industry economics toward the way आशियाना Ashiana was already doing things voluntarily. RERA does not give the company a new moat; it widens the moat that was already there.

Strong frameworks should produce strong investment debate. So now we have to talk about the bear case.

VIII. Bear vs. Bull: Counting the Risks

The bull case for आशियाना Ashiana has been hinted at throughout this story, but it deserves to be assembled in one place. It rests on three demographic and structural pillars.

First, the silver tsunami. The Indian population over the age of 60 — वरिष्ठ नागरिक senior citizens in the regulatory vocabulary — was, per consulting estimates, approximately 150 million people in 2025 and was projected to grow to roughly double that within fifteen years.1 India had not yet hit its demographic peak, but the over-60 cohort was already growing faster than any other age band, and a small fraction of that cohort represented the entire addressable market for organized senior housing. The penetration rate for organized senior living in India was, depending on which consultant did the math, in the low single digits, compared with the high double digits in mature markets like the US and Australia. The gap was not a gap. It was a chasm. And आशियाना Ashiana was, by a wide margin, the best-known organized provider sitting at the edge of that chasm.

Second, the formalization tailwind in Indian real estate broadly. The post-RERA, post-जीएसटी GST, post-आईबीसी IBC (Insolvency and Bankruptcy Code) Indian residential sector is structurally different from the wild-west sector of the 2000s. Unorganized developers, who once held the majority of share, have been losing ground to listed, RERA-compliant, financially disciplined players. Even without the senior living story, आशियाना Ashiana's mid-income core business is positioned to take share from collapsing local builders. The five-year revenue CAGR of approximately 37% reported in FY25 reflects that share-shift more than any cyclical recovery.9

Third, the recurring services flywheel. As more communities mature, the proportion of stable, annuity-like maintenance and आशियाना केयर Ashiana Care revenue rises, smoothing the lumpy nature of project sales and reducing the equity-risk discount that the market traditionally applies to pure construction firms.

The bear case, however, is not trivial.

The most serious risk is execution in new geographies. The company's playbook works exquisitely well in भिवाड़ी Bhiwadi, where it has thirty years of buyer relationships, supply chain depth, and community goodwill. Replicating that in चेन्नई Chennai, with its very different climate, language, and buyer culture, is a real test. Senior buyers in Chennai have different food expectations, different religious calendars, and different healthcare integration needs than buyers in NCR. The ₹1,200-crore Chennai project is, in many ways, a referendum on whether the operating model scales geographically.14

The second risk is the "premiumization trap." As आशियाना Ashiana moves into Mumbai and Bengaluru — which it has signalled as the next expansion frontiers — the land cost structure changes dramatically.15 In भिवाड़ी Bhiwadi, a senior living unit could be priced for a middle-class retiree. In मुंबई Mumbai, only the affluent can afford anything close to comparable square footage. The company has to decide whether to remain a mass-market operator (in which case it gives up the metros) or move upmarket (in which case it becomes a different kind of business). This is the kind of strategic fork that has tripped up many otherwise well-run Indian consumer companies.

The third risk is the scale-vs-quality tension. The company is, by Indian developer standards, small. Where listed peers turn over multiple millions of square feet annually, आशियाना Ashiana has historically delivered in a smaller range, with deliberate caps on how many projects it runs concurrently. Management has guided to ₹1,500 crore in pre-sales for FY26, with senior living climbing to roughly a quarter of that mix.15 Doubling that volume over the next five years without losing the family-run quality control is a real organizational challenge — the kind that has historically broken Indian family businesses as they transition from owner-managed to professionally managed.

The fourth risk is more macro: interest rate sensitivity and the housing cycle. Indian residential demand is rate-sensitive, and आशियाना Ashiana's mid-income buyer is more sensitive than the luxury buyer. A sustained period of high rates, weak income growth, or general macro stress could throttle new bookings even as the senior living segment continues to grow.

A second-layer risk worth flagging is the company's counterparty exposure on JDAs and land leases. The May 2026 termination of the Mahindra World City Jaipur land lease, while clean and mutually agreed, is a reminder that asset-light models depend on counterparty execution.16 Approval delays, ownership disputes, or partner restructuring can ripple through.

Finally — and this is more of a question than a risk — the question of whether the next generation of the Gupta family will inherit the temperament. Family businesses in India are littered with founders' grandchildren who decided they wanted to be venture capitalists, or worse, expand into "platforms." The brothers have been disciplined. Whether their children will be remains untested.

Investors looking for the right KPIs to track the company would do well to focus on three numbers, in this order: total pre-sales value (which captures whether the brand is selling), the senior living share of pre-sales (which captures whether the strategic story is playing out), and free cash flow from maintenance and hospitality (which captures whether the services flywheel is becoming the annuity it promises to be).

IX. Conclusion: Building Communities, Not Apartments

There is a useful Acquired-style comparison floating around when you describe आशियाना Ashiana to people who have never heard of it: it is the कॉस्टको Costco of Indian residential real estate. The analogy is imperfect, but it is directionally right. Like Costco, आशियाना Ashiana charges a recurring fee (maintenance, services) in addition to the transaction it is most associated with. Like Costco, it has cultivated a customer base that is wildly loyal and somewhat self-selecting. Like Costco, it has kept overhead low and pricing transparent. Like Costco, it has refused, almost stubbornly, to pursue the maximum short-term margin in favor of a longer-term franchise.

What आशियाना Ashiana actually sells, when you strip away the floor plans and the brochures, is the absence of fear. The fear that the developer will vanish. The fear that the building will not be finished. The fear that the lift will not work. The fear, in the case of senior living, that no one will come if a parent collapses at 3 a.m. The product is peace of mind, delivered through concrete.

For most of Indian corporate history, this was not considered a real product. It was assumed that homebuyers had no choice, that they would tolerate whatever the developer dished out. आशियाना Ashiana ran a forty-year experiment to see whether the assumption was true. The answer, by 2026, looks unambiguous: the buyers who can choose, increasingly do. And the most demanding buyers — elderly retirees with their children's hard-earned dollars in escrow — choose first.

The legacy of ओम प्रकाश गुप्ता O.P. Gupta was not that he built buildings. It was that he built a company whose unit of output was not a flat but a community. The legacy of his sons, still unfolding, will be whether they can scale that idea from भिवाड़ी Bhiwadi's industrial outskirts to the metro markets of मुंबई Mumbai and बेंगलुरु Bengaluru without breaking it. The math is on their side; the operational complexity is the variable.

In a sector where most of the headlines have been about the developers that died, the more interesting story is the small, debt-averse, service-obsessed family firm in भिवाड़ी Bhiwadi that quietly built the most defensible niche in Indian real estate by refusing to behave like an Indian real estate developer. The walls were always the easy part. What आशियाना Ashiana built was everything inside them.

References

References

-

Senior Living in India — Jones Lang LaSalle (JLL) Research ↩↩

-

How this mid-income housing company grew to Rs 650 Cr revenue after six co-founders quit — YourStory ↩↩

-

The Ongoing Story of Ashiana Senior Living in India (2004-2026) — Jeevin Senior Care ↩

-

Senior Citizen Homes in Bhiwadi / Ashiana Utsav — Ashiana Housing ↩↩↩

-

Ashiana Housing — Press Releases (Lavasa Phase 4 CC, 2024) ↩↩

-

Ashiana Housing — NCD Debt Servicing Disclosure, May 2026 — ScanX ↩

-

Ashiana Utsav Bhiwadi Resale and Rental Property For Seniors — Ashiana Housing ↩

-

Ashiana Housing to invest Rs 425 crore in FY26 on senior living projects — Devdiscourse ↩

-

Ashiana Housing acquires 23-acre Chennai land for senior living project, eyes ₹1,200 crore revenue — Storyboard18 ↩↩↩

-

Ashiana Housing Targets ₹1500 Cr Pre-Sales; Eyes Mumbai, Bangalore Expansion — Whalesbook ↩↩↩

-

Ashiana Housing terminates land lease agreement for group housing project in Jaipur — Business Standard, May 2026 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube