Asahi India Glass: The Invisible Giant Behind India's Glass Revolution

I. Introduction & Episode Thesis

Picture this: Every time you step into a Maruti Suzuki, roll down the windows of a Hyundai, or gaze through the floor-to-ceiling glass panels of a modern office tower in Gurugram, you're touching the work of a company that most Indians have never heard of. Asahi India Glass—AIS to insiders—commands a staggering 77% market share in passenger car glass in India, yet remains virtually unknown outside boardrooms and factory floors.

Here's the central paradox we're exploring today: How did a joint venture between a century-old Japanese glass maker, an Indian business family, and India's largest car manufacturer evolve from a single-customer supplier into a ₹20,000 crore invisible infrastructure giant? This isn't just a story about glass—it's about the hidden champions that build the physical world around us, the companies that become so essential they disappear into the background of modern life.

The numbers tell one story: dominant market share, integrated manufacturing from sand to solutions, relationships with every major automaker in India. But the real story—the one we'll unpack over the next several hours—is how AIS navigated the treacherous journey from captive supplier to market maker, from technology importer to innovation driver, from commodity producer to value-added solutions provider.

What makes this particularly fascinating for investors is the tension at the heart of AIS's business model. On one hand, you have extraordinary market dominance and deep customer relationships built over four decades. On the other, you have the brutal realities of capital-intensive manufacturing, cyclical end markets, and the perpetual threat of commoditization. It's a case study in building moats in businesses where moats shouldn't exist.

As we trace AIS's evolution from its 1984 founding to today's market leader, we'll examine critical inflection points: the decision to break free from single-customer dependency, the bold backward integration into float glass, the diversification into architectural segments, and the current navigation of the EV transition. Each phase reveals lessons about industrial strategy, patient capital, and the unique dynamics of building manufacturing excellence in emerging markets.

The timing of this analysis couldn't be more relevant. With India's infrastructure boom accelerating, EVs demanding new glass technologies, and global supply chains reconfiguring post-pandemic, AIS sits at multiple crossroads. The question isn't whether glass will remain essential—it's whether AIS can capture the value creation ahead or become another mature industrial caught in the margin squeeze between innovation and commoditization.

II. The Perfect Storm: Origins & Founding Context (1984-1987)

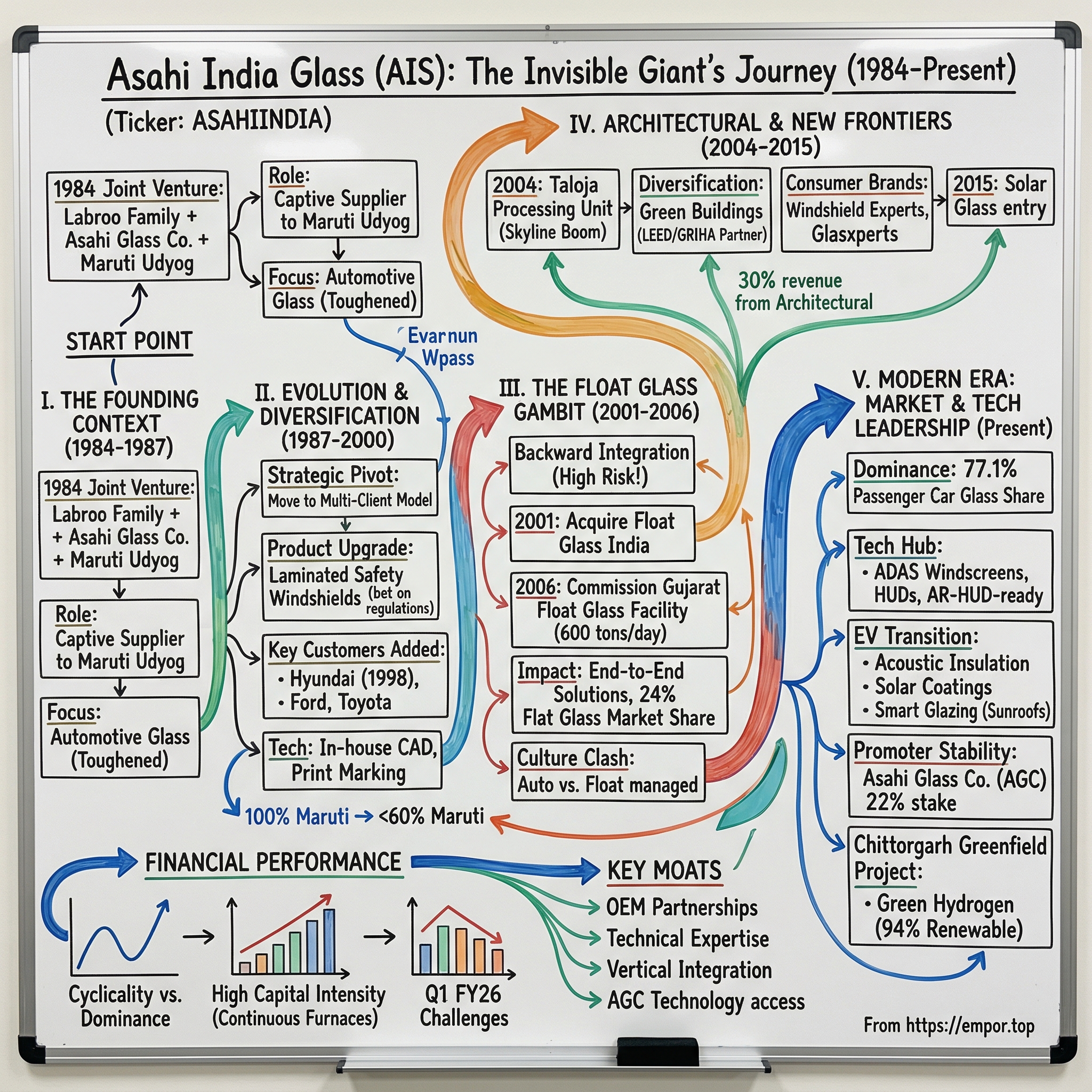

The year was 1984. While George Orwell's dystopia captured Western imagination, in India, a different transformation was brewing. In a nondescript industrial plot in Haryana, three unlikely partners were about to shake hands on a venture that would reshape Indian manufacturing: the Labroo family's entrepreneurial ambition, Asahi Glass Company's century of Japanese glassmaking expertise, and Maruti Udyog's revolutionary mission to motorize middle-class India.

To understand why this partnership made perfect sense, you need to understand Asahi Glass Company of Japan. Founded in 1907 by Toshiya Iwasaki—the second son of the Mitsubishi zaibatsu president—Asahi Glass wasn't just Japan's first sheet glass producer. It embodied the Meiji-era obsession with catching up to the West through technical excellence. By the 1980s, AGC had evolved into a global glass technology powerhouse, but it faced a classic Japanese conglomerate problem: saturated home markets and the need for new frontiers.

Enter B.M. Labroo, whose family business philosophy was quintessentially Indian: relationships first, technology second, patience always. The Labroos weren't industrialists in the traditional sense—they were deal-makers who understood that in pre-liberalization India, success came from bridging foreign technology with local execution. They saw in Maruti Udyog's ambitious plans not just a customer, but an entire ecosystem waiting to be built.B.M. Labroo belonged to that special generation—India's "Midnight's Children"—who came of age with independence, imbued with the spirit of change and destiny. When his son Sanjay, a Wharton graduate, chose to return to India in the mid-1980s instead of pursuing a lucrative Wall Street career, the elder Labroo saw not just filial duty but entrepreneurial destiny.

Maruti Udyog, meanwhile, represented India's most audacious industrial experiment. The brainchild of Sanjay Gandhi's failed attempt at indigenous car manufacturing had been resurrected as a joint venture with Suzuki Motor Corporation. By 1983, Maruti had begun rolling out the iconic 800, but they faced a critical bottleneck: automotive glass. India's existing glass manufacturers couldn't meet the quality standards or volumes required for mass motorization. Every windshield, every side window had to be imported—an unsustainable model for a company targeting lakhs of vehicles annually.

The convergence was elegant in its logic. AIS was established as a Joint Venture between the Labroo family, Asahi Glass Co. Ltd. (AGC), and Maruti Suzuki, becoming Maruti Udyog's first joint venture. Each partner brought irreplaceable assets to the table. AGC provided the technical know-how—the precise chemistry of tempered glass, the engineering specifications for automotive safety standards, the production processes refined over decades. The Labroos brought local navigation skills—understanding of Indian bureaucracy, relationships with suppliers, the ability to manage labor in a pre-liberalization environment. Maruti provided the most precious asset of all: guaranteed demand.

But here's what made this origin story particularly prescient. While most Indian industrialists in 1984 were still thinking in terms of import substitution and license raj economics, the AIS founders were already playing a different game. They understood that being a captive supplier was both a blessing and a curse—it provided initial stability but could become a growth trap. From day one, the articles of association included provisions for expanding beyond Maruti, though nobody could have predicted just how critical that foresight would prove.

The initial operations were deliberately modest—a single production line manufacturing toughened glass for Maruti's rear and side windows. No laminated windshields yet, no architectural ambitions, certainly no dreams of backward integration into float glass. Just the relentless focus on meeting Maruti's exacting standards while learning the intricate dance of Japanese quality control systems meeting Indian manufacturing realities.

What emerged from those early years wasn't just a glass company—it was a template for how international technology transfer could work in emerging markets. The Japanese didn't just send machines; they sent engineers who lived in Haryana for months, teaching everything from furnace temperature calibration to visual inspection techniques. The Indians didn't just provide labor; they adapted Japanese processes to local conditions, finding creative solutions when imported components broke down or monsoons disrupted production schedules.

By 1987, AIS had achieved something remarkable: consistent quality at volumes that matched Maruti's explosive growth. But success bred its own challenges. Being Maruti's sole supplier meant riding the roller coaster of automotive demand cycles. More critically, it meant that AIS's destiny was entirely tied to decisions made in boardrooms in New Delhi and Hamamatsu. The company's founders knew they needed to evolve—but first, they had to master the art of keeping their most important customer happy while secretly planning their escape from single-customer dependency.

III. Single Customer to Multi-Client Evolution (1987-2000)

The year 1991 changed everything. While economists celebrate it as India's liberalization moment, for AIS it represented an existential crossroads. The protected markets that had made the Maruti monopoly possible were opening up. Global automakers were eyeing India. And AIS's leadership faced a delicate high-wire act: how do you court Maruti's future competitors while remaining their trusted sole supplier?

The answer began in the engineering labs of Bawal, where AIS engineers were perfecting a technology that would transform their strategic position: laminated windshields. By 1992, AIS ventured into manufacturing laminated safety windshields. This wasn't just a product upgrade—it was a deliberate move up the value chain. Laminated glass required precision engineering that simple toughened glass didn't demand. Two sheets of glass sandwiching a polyvinyl butyral (PVB) interlayer, heated and pressed to create a safety barrier that would crack but not shatter. The technology existed globally, but adapting it to Indian conditions—extreme heat, monsoon humidity, cost constraints—required innovation. The strategic importance of the 1996 capacity expansion to 750,000 laminated windshields cannot be overstated. AIS anticipated mandatory requirements for laminated windshields, betting that Indian safety regulations would eventually catch up to global standards. This wasn't just capacity addition—it was a chess move that would lock in customer relationships before competitors could react.

The real breakthrough in breaking single-customer dependency came through an unlikely door: the Asian financial crisis of 1997. As Korean chaebols reeled from the crisis, Hyundai needed to localize rapidly to survive in India. In 1998, when Hyundai Motor India commenced operations near Chennai, AIS was ready. The company had deliberately built excess capacity, trained engineers in Korean specifications, and—crucially—convinced Maruti that supplying competitors would actually strengthen the entire ecosystem.

By 1989, after increasing tempered glass production capacity by installing a new furnace, AIS began manufacturing toughened glass for other automobile manufacturers. But the real acceleration came in the late 1990s. By 1999, AIS had added not just Hyundai but Ford, Toyota, and Hindustan Motors to its client roster. Each new customer required a delicate dance—convincing them that a Maruti supplier could maintain confidentiality, demonstrating that Japanese quality systems could adapt to American or Korean specifications, proving that an Indian company could meet global standards.

The technology evolution during this period reveals AIS's strategic sophistication. With the turn of the millennium, AIS increased its technology capabilities including laminated bending furnace for producing complex laminated windshields, CAD station and in-house designing, and print marking on glass for brand visibility. These weren't random upgrades—each investment targeted a specific customer pain point. Complex laminated windshields? That's for the curved, aerodynamic designs emerging from global R&D centers. In-house CAD capabilities? That meant AIS could collaborate on new model development rather than just execute specifications.

Consider the organizational gymnastics required here. AIS had to build Chinese walls between teams serving competing automakers. The Maruti team couldn't know what innovations were being developed for Hyundai. The Ford engineers couldn't access Toyota's proprietary specifications. Yet all these teams had to share the same furnaces, the same quality systems, the same management structure. It's like running multiple restaurants out of the same kitchen without the recipes mixing.

The numbers tell the success story: from 100% revenue concentration with Maruti in 1987 to less than 60% by 2000. But numbers don't capture the cultural transformation. AIS evolved from a vendor mindset—where you wait for specifications—to a partner mentality where you anticipate needs. When Tata Motors was developing the Indica, India's first indigenously designed car, AIS engineers were embedded in the design team, suggesting glass specifications that would optimize both cost and performance.

What's particularly instructive for investors is how AIS managed margin pressure during this expansion. Every new customer demanded price concessions—"Why should we pay Maruti prices when we're giving you volumes?" But AIS understood that in automotive supply chains, the real currency isn't price—it's reliability. Zero defects matter more than 5% cost savings when a single bad windshield can stop an entire assembly line.

The period also saw AIS master the art of technical differentiation in a seemingly commoditized product. The company introduced black ceramic printing and heat-lite printing for production of automotive glasses for the first time in India. These weren't just aesthetic improvements—they were functional innovations that reduced cabin temperature, improved privacy, and enhanced the premium feel of vehicles. Each innovation created switching costs that made it harder for customers to shift suppliers.

By 2000, AIS had achieved something remarkable: it had become simultaneously indispensable to competitors. Maruti needed AIS because only AIS had the scale to meet their volumes efficiently. Hyundai needed AIS because only AIS had the local manufacturing depth to meet localization requirements. Ford and Toyota needed AIS because only AIS had the technical capabilities to meet global quality standards while maintaining Indian cost structures.

The lesson here isn't just about customer diversification—it's about the sequencing of strategic moves. AIS didn't try to escape Maruti dependency through confrontation. Instead, it used its Maruti relationship as a learning laboratory, a cash generator, and a credibility builder. By the time it approached Maruti's competitors, AIS could point to a thirteen-year track record of zero defects, on-time delivery, and continuous innovation. As we'll see in the next phase of AIS's evolution, this foundation of trust and technical excellence would enable an even bolder strategic gambit: backward integration into the heart of glass manufacturing itself.

IV. The Float Glass Gambit: Backward Integration (2001-2006)

In the boardrooms of Mumbai's Nariman Point, investment bankers called it financial engineering. In the furnace rooms of Gujarat, engineers called it the mother of all technical challenges. But for AIS's leadership, the acquisition and integration of Float Glass India in 2001 was something else entirely: a declaration of independence.

To understand why this move was so audacious, you need to understand the economics of float glass. The technology, invented by Britain's Pilkington in 1959, involves floating molten glass on a bed of molten tin to create perfectly flat sheets. It requires furnaces that run 24/7 for fifteen years straight—you literally cannot turn them off without destroying the entire installation. The capital investment is staggering: hundreds of crores for a single line. The technical expertise is rarified: only a handful of companies globally had mastered the process. And the risk? If you get the chemistry wrong, you're producing expensive scrap at the rate of 600 tons per day.

In 2001, AIS acquired a stake in Asahi Glass Co., Japan's subsidiary Float Glass India. In 2003, the amalgamation was approved with 79.6% equity in FGI held by AIS. This wasn't just M&A—it was AIS swallowing a company that, on paper, was its technological superior. Float Glass India had been established by AGC Japan as their Indian beachhead for architectural glass. But it was hemorrhaging money, trapped between high capital costs and India's fragmented construction market.

The integration challenges were immense. Float glass culture and automotive glass culture are as different as steel mills and Swiss watches. Float glass is about continuous process optimization—tiny improvements in yield, energy efficiency, defect rates. Automotive glass is about customer responsiveness—quick changeovers, just-in-time delivery, zero-defect quality. AIS had to merge these cultures without breaking either.

But here's where the strategic genius emerged. AIS didn't just want to make float glass—it wanted to revolutionize the entire value chain. The traditional model had float glass manufacturers selling to processors who sold to fabricators who sold to installers. Each step added margins, complexity, and quality risk. AIS's vision: control everything from sand to installation, capturing value at every step while ensuring quality throughout.

The 2006 commissioning of the state-of-the-art float glass facility in Gujarat marked the culmination of this strategy. With 600 tons per day capacity, this wasn't just another glass plant—it was a statement of technological arrival. The facility incorporated the latest AGC technology: online coating systems that could deposit metal oxide layers measured in nanometers, automated inspection systems that could detect defects invisible to the human eye, energy recovery systems that turned waste heat into process steam. The economic rationale for backward integration was compelling but risky. AIS provides end to end solutions in the entire glass value chain - from the manufacturing of float glass, processing, fabrication to installation services. By controlling float glass production, AIS could ensure quality consistency, reduce dependency on imports, and capture manufacturing margins that previously went to suppliers. But the capital requirements were staggering—a modern float line required investments approaching ₹1,000 crore when including working capital and ramp-up costs.

What made AIS's approach unique was the simultaneous development of multiple value-addition capabilities. While the float furnaces were being commissioned, AIS was also building coating lines, cutting-edge processing facilities, and even developing proprietary glass formulations. The company understood that making commodity float glass was a ticket to play, not a winning strategy. The real value lay in what you did with that glass afterward.

The technical challenges of running a float glass operation in India added layers of complexity. When the company started construction of its plant at Roorkee, then it had estimated the commencement of commercial production of the float glass unit in December 2006 and it could start commercial production in January 2007. For automotive glass units at Roorkee, the estimated completion date was August 2007, which it could complete by October 2007. These weren't just construction delays—they reflected the difficulty of achieving the precise conditions required for float glass production. Temperature variations of even a few degrees could create optical distortions. Contamination measured in parts per billion could create defects. The tin bath alone required months of conditioning before producing saleable glass.

But here's where AIS's integrated strategy paid dividends. Unlike standalone float glass producers who had to find markets for their output, AIS had captive consumption through its automotive business. This provided a cushion during the learning curve, when yields were sub-optimal and quality was still stabilizing. Every square meter of glass that didn't meet automotive standards could be diverted to less demanding architectural applications.

The market impact was immediate and profound. One of India's largest manufacturer of Float Glass, AIS currently enjoys a total market share of 24% in the Indian Flat Glass Industry. By 2006, AIS wasn't just participating in the value chain—it was reshaping it. Competitors who had previously competed on processing capabilities now had to worry about raw material access. International suppliers who had counted on Indian import demand suddenly faced a sophisticated local producer backed by Japanese technology.

The strategic implications extended beyond economics. Vertical integration gave AIS unprecedented flexibility in product development. When automotive customers wanted specialized coatings or architectural clients demanded energy-efficient glass, AIS could tweak formulations at the float stage rather than relying on post-production treatments. This speed of innovation became a competitive weapon, allowing AIS to move from customer request to commercial production in months rather than years.

For investors analyzing this phase, the key insight is timing. AIS didn't integrate backward when float glass was commoditized and margins were thin. They moved when India's construction boom was accelerating, when automotive production was scaling, and when technology transfer from AGC could provide a genuine competitive advantage. The company understood that in capital-intensive businesses, when you move matters as much as whether you move.

The integration also revealed AIS's financial discipline. Despite the massive capital requirements, the company maintained a balanced approach to funding, using a combination of internal accruals, strategic debt, and technology partnerships rather than diluting equity excessively. This preserved value for shareholders while building industrial capabilities that would prove invaluable in the next phase of growth.

As 2006 drew to a close, AIS had transformed from a converter of glass to a creator of glass. But the real test lay ahead: Could the company leverage this integrated platform to capture the explosive growth in India's architectural segment while maintaining its automotive dominance? The answer would reshape not just AIS but India's entire built environment.

V. Architectural Glass & Diversification Strategy (2004-2015)

The Mumbai skyline of 2004 told two different stories. Looking up, you saw the future: gleaming towers of glass and steel, each facade a testament to India's global ambitions. Looking closely, you saw the problem: almost every square meter of that architectural glass was imported, shipped from China, Europe, or Southeast Asia. For AIS's leadership, staring at those towers from their Nariman Point offices, this wasn't just a market opportunity—it was a provocation.

Commercial production at the company's Architectural Processing Unit in Taloja commenced in 2004. But this modest announcement masked a profound strategic pivot. AIS was attempting something that had defeated numerous competitors: building an architectural glass business from scratch in a market dominated by established importers, fragmented distribution channels, and customers who bought on price, not brand.

The timing seemed counterintuitive. India's real estate sector in 2004 was notorious for its opacity, payment delays, and boom-bust cycles. Builders treated glass as a commodity, squeezing suppliers for every rupee. Architects, trained abroad, specified international brands by default. And the technology requirements for architectural glass—solar control coatings, acoustic insulation, safety treatments—were completely different from automotive applications.

But AIS saw what others missed: India's architectural glass market wasn't one market but dozens of micro-markets, each with distinct needs. The Bangalore IT campus needed solar control to reduce air-conditioning loads. The Delhi luxury hotel wanted acoustic glass to block traffic noise. The Mumbai residential tower required safety glass to meet new building codes. Each application demanded not just product innovation but solution design, technical support, and after-sales service that importers couldn't provide.

The company's approach was methodical, almost academic in its rigor. AIS Glass Solutions Ltd. was set up in 2005 to further expand in the architectural glass value chain. The year 2006 saw establishment of two more architectural processing facilities in Rewari and Chennai along with further capacity expansion across existing plants. These weren't just production facilities—they were capability centers, each designed to serve regional markets with localized products and services.

The product innovation during this period was relentless. AIS didn't just copy global products; it created India-specific solutions. Take the Ecosense range—glass designed for India's extreme climate variations, from Rajasthan's 50°C summers to Kashmir's sub-zero winters. Or the Opal series, which balanced light transmission with heat reflection in ratios optimized for Indian latitudes. Each product required months of R&D, testing in Indian conditions, and education of architects who had never considered glass as anything more than a transparent barrier.

But the real breakthrough came through a strategic insight: in India, the customer for architectural glass wasn't really the builder or architect—it was the end user who would live or work behind that glass for decades. This led to the creation of consumer-facing brands that seemed almost absurd for a B2B glass company. Glasxperts wasn't just a processing service—it was positioned as a lifestyle solution for discerning homeowners. The marketing spoke not of U-values and SHGC ratings but of comfort, aesthetics, and energy savings that middle-class Indians could understand.

The 2008 financial crisis, which devastated real estate globally, became an unexpected catalyst for AIS's architectural ambitions. As international suppliers pulled back from India, local sourcing became not just economical but essential. AIS aggressively filled the vacuum, offering payment terms that foreign suppliers couldn't match, technical support that resided in India rather than a phone call away, and the ability to customize products for Indian conditions.

The transformation of AIS's architectural business accelerated with India's green building movement. As LEED and GRIHA certifications became marketing tools for premium developments, high-performance glass evolved from luxury to necessity. AIS positioned itself as the sustainability partner, educating developers about how the right glass could earn certification points while reducing operational costs. The company's technical teams became de facto consultants, sitting with architects during design phases, running energy simulations, and specifying glass solutions that optimized entire building envelopes.

In 2015, AIS made another strategic leap: venturing into solar glass. This wasn't just product extension—it was a bet on India's renewable energy future. Solar glass required different optical properties, durability standards, and supply chain dynamics than architectural or automotive glass. But AIS understood that as India pushed toward ambitious solar targets, local manufacturing of solar glass would become a strategic imperative.

The consumer glass initiatives—Glasxperts and Windshield Experts—deserve special attention. These weren't side projects but strategic platforms for market education and brand building. It also provides consumer glass offerings in the form of Glasxperts and Windshield Experts. By creating direct-to-consumer touchpoints, AIS could influence specification decisions at the grassroots level. The homeowner who had a positive experience with Glasxperts for their residence became an advocate when their office needed glass solutions.

The financial performance validated the strategy. By 2015, architectural glass had grown from virtually zero to nearly 30% of AIS's revenues. More importantly, it provided diversification from automotive cycles, access to new customer segments, and platforms for value-added innovation that commodity automotive glass couldn't support. The architectural segment's gross margins, while volatile with real estate cycles, peaked higher than automotive during boom periods.

The challenges were equally instructive. Payment cycles in construction stretched to 180 days or more, stressing working capital. Competition from cheap Chinese imports required constant innovation to maintain price premiums. The need to maintain inventory across hundreds of SKUs—different sizes, thicknesses, coatings, colors—complicated operations and increased carrying costs.

Yet AIS persisted, understanding that architectural glass wasn't just another revenue stream—it was the future of glass itself. As India urbanized, as buildings became more sophisticated, as energy efficiency became mandatory rather than optional, architectural glass would transition from building material to building technology. The company that controlled this transition would shape India's built environment for generations.

For investors, the architectural diversification revealed AIS's ability to execute complex strategic pivots while maintaining operational excellence in its core business. The company didn't abandon automotive for architectural—it used automotive as a platform to build architectural. This portfolio approach, balancing stable automotive revenues with high-growth architectural opportunities, would prove crucial as AIS entered its next phase: the era of smart glass, digital integration, and the fundamental transformation of what glass could be.

VI. Modern Era: Market Dominance & Technology Leadership (2015-Present)

The test track at Maruti's Manesar facility, 2019. A prototype of the new S-Presso subcompact SUV screams around corners, its oddly tall stance pushing the limits of physics. Inside the vehicle, AIS engineers aren't watching the road—they're monitoring sensors embedded in the windshield, measuring optical distortion under stress, checking heads-up display clarity, validating that the rain sensors maintain calibration through Indian puddles that are more like temporary lakes. This isn't your grandfather's windshield—it's a transparent computer, and AIS is writing the operating system.

In the Indian passenger car glass segment, AIS has 77.1% market share as of 2017. AIS also holds 20% market share in India's architectural glass segment as of 2017. These numbers tell a story of dominance, but they don't capture the technological transformation that underpins it. The modern AIS isn't just making glass—it's creating transparent intelligence platforms for the connected vehicle era.

The client portfolio reads like a who's who of global automotive: Maruti Udyog, Tata Motors, Hyundai Motors, Mahindra & Mahindra, General Motors, Ford India, Fiat India, Honda, Eicher, Volvo, Hindustan Motors, Skoda Auto, Volkswagen India, Toyota Kirloskar, and Piaggio. But what's remarkable isn't the breadth—it's the depth. AIS isn't just a supplier to these companies; it's embedded in their product development cycles, their technology roadmaps, their fundamental conception of what a vehicle can be. The manufacturing footprint tells a story of strategic positioning rather than random expansion. AIS Auto Glass has four production facilities at Bawal (Haryana), Roorkee (Uttarakhand), Chennai (Tamil Nadu), and Taloja (Maharashtra). They also have five automotive glass manufacturing plants in India. Each location was chosen not just for proximity to customers but for specific technological capabilities. Bawal serves the northern automotive cluster, Chennai anchors the southern export hub, Roorkee provides access to technical talent, and Taloja bridges automotive and architectural markets.

The technology capabilities represent a quantum leap from the toughened glass of the 1980s. AIS design of ADAS Windscreens offers seamless integration of the ADAS sensors, cameras, ultrasonic transmitters and steering angle sensors mounted on windscreens with great precision. These sensors see through the windscreens in a compatible environment and ensure quick response essential for assisting the driver for additional safety. This isn't just about making glass—it's about creating optical platforms for artificial intelligence.

Consider what goes into a modern ADAS-enabled windshield. AIS is also leading in display-enabled glazing by developing laminated windshields for head-up displays (HUDs) and AR HUDs, which project key vehicle information onto the glass. It's the first in India to localise this solution using press-bend technology, meeting rising demand from automakers. The glass must maintain perfect optical clarity while incorporating heating elements for defrosting, antennas for connectivity, rain sensors for automatic wipers, and a specialized wedge angle for HUD projection—all while meeting safety standards that require it to withstand impact without shattering.

The rise of ADAS has given AIS a new role beyond making glass. It now supplies tightly engineered brackets that hold ADAS sensors like rain, light, and lane-departure detectors. Making both the glass and these critical parts positions AIS as a full system supplier. This evolution from component supplier to system integrator changes the entire competitive dynamic. Competitors can't just match AIS's glass quality—they need to replicate an entire ecosystem of capabilities.

The promoter structure provides stability in this technology transition. Promoter Asahi Glass Company Ltd (AGC), is the largest shareholder holding a 22% stake in the company as of June 2024, AGC is one of the leading manufacturers of glass globally, with a 12% global market share in the float glass segment and 30% in auto glass share. This isn't passive ownership—it's active technology partnership. AGC's global R&D feeds directly into AIS's Indian operations, while AIS's frugal innovation and emerging market expertise flow back to AGC's global operations.

The EV transition, rather than threatening AIS's automotive business, is creating new opportunities. Electric vehicles require different glass specifications—better acoustic insulation to compensate for the absence of engine noise, specialized coatings to reduce cabin heat load and preserve battery range, and integration points for the sensors that enable autonomous driving features. Recently, the company introduced smart glazing solutions such as illuminated laminated sunroofs, laminated side-lites, and AR-HUD-ready windscreens. A laminated sunroof and windscreen featuring PDLC switching glazing is also in the works, offering adjustable transparency. These innovations create customer delight besides offering better comfort to the end customer.

What sets AIS apart is its in-house strength in designing and developing new products, along with the ability to make the process equipment, tools, and fixtures required for manufacturing. These capabilities not only support AIS's own operations but also benefit its global associate companies. This is crucial—AIS isn't just assembling technology developed elsewhere but creating intellectual property that has global applications.

The export story is gaining momentum. AIS is quietly but steadily growing its global footprint. Its products now find its way into export vehicles made by top OEMs like Hyundai, Kia, and Volkswagen through both direct and indirect channels, including CKD (completely knocked down) programmes. AIS is also seeing increasing interest from global customers keen to diversify their supply chains beyond China. Products like the dynamic illuminated sunroof and AR HUD windscreens are helping the company emerge as a serious alternative for advanced glazing solutions.

What sets AIS apart is how it has transformed over the years. From simply following customer blueprints, it now co-develops glass solutions—offering design, prototyping, and full system integration. As vehicles become more digital, electric, and connected, AIS is getting ready to work more closely with software teams and systems experts, not just glass engineers. This transformation from vendor to partner, from manufacturer to innovator, represents the next phase of AIS's evolution.

The market dominance statistics—77% in automotive, growing share in architectural—mask a more fundamental achievement. AIS has become what economists call a "platform company" in manufacturing. Just as digital platforms like Amazon or Google become more valuable as they add users and services, AIS becomes more entrenched as it adds capabilities and relationships. Every new technology it masters, every new customer it serves, every new application it develops increases the switching costs for existing customers and barriers for new competitors.

Yet challenges loom. The latest quarterly results show pressure: Q1 FY26 saw a 27.98% decline in net profit to ₹56.17 crore despite an 8.48% increase in net sales to ₹1,228.74 crore. Margin compression in a capital-intensive business with high fixed costs creates operational leverage that cuts both ways. When volumes grow, profits soar. When demand softens, the bottom line gets hammered.

VII. Financial Performance & Unit Economics

The numbers tell a story of scale, but also of struggle. ₹4,691 crore in revenue, ₹345 crore in profit—on paper, AIS looks like a profitable market leader. But dive deeper into the unit economics and financial architecture, and you discover a more complex narrative: a capital-intensive manufacturer navigating the treacherous waters between growth investment and margin preservation, between market dominance and financial performance. The Q1 FY26 results provide a window into current challenges. Asahi India Glass Limited reported a 27.98% decline in net profit to ₹56.17 crore for June 2025, despite an 8.48% increase in net sales to ₹1,228.74 crore. This divergence between revenue growth and profit decline reveals the fundamental tension in AIS's business model: volume growth doesn't automatically translate to profit growth when input costs spike or product mix shifts toward lower-margin segments.

Let's dissect the unit economics. In the automotive segment, AIS produces roughly 10 million pieces of automotive glass annually. With automotive revenues of approximately ₹3,000 crore, that translates to roughly ₹3,000 per piece—but this masks enormous variation. A simple door glass might generate ₹500, while an ADAS-enabled windshield could command ₹15,000. The product mix, therefore, becomes as important as volume in determining profitability.

The capital intensity is staggering. A modern float glass line requires ₹800-1,000 crore in investment and must run continuously for 15 years. With depreciation alone consuming ₹60-70 crore annually per line, the break-even utilization is typically above 70%. Below that threshold, the fixed cost burden crushes margins. Above it, incremental production flows almost directly to the bottom line. This operational leverage explains why AIS's profits can swing wildly with relatively small changes in demand.

The working capital dynamics add another layer of complexity. Automotive OEMs typically pay on 60-90 day terms, while AIS must maintain raw material inventory for 30-45 days and finished goods for another 15-30 days. This creates a cash conversion cycle exceeding 120 days, requiring roughly ₹1,500 crore in working capital to support current revenue levels. Every 1% increase in interest rates costs AIS approximately ₹15 crore annually—material in a business where net profits are ₹345 crore.

Stock is trading at 7.47 times book value, which seems expensive for a manufacturing company. But this metric misses crucial nuances. Much of AIS's book value reflects historical cost of assets that would be far more expensive to replicate today. A float glass plant built for ₹600 crore in 2006 might cost ₹1,500 crore to construct today. The replacement value of AIS's assets likely exceeds book value by 50-100%, suggesting the price-to-book ratio understates the company's asset efficiency.

The company has delivered a poor sales growth of 11.7% over past five years. This seemingly disappointing growth rate, however, occurred during one of the most challenging periods for Indian automotive and construction sectors—demonetization, GST implementation, NBFC crisis, and COVID-19. That AIS maintained double-digit growth through these headwinds speaks to resilience rather than weakness.

The margin structure reveals strategic choices. Gross margins in the 35-40% range seem healthy, but EBITDA margins of 15-17% and net margins of 7-8% show the impact of high depreciation and interest costs. This is the price of vertical integration—you capture more value but carry more fixed costs. During good times, this structure generates superior returns. During downturns, it becomes a millstone.

The segment-wise performance tells different stories. Automotive glass, despite market dominance, faces margin pressure from OEM cost-reduction demands and rising input costs. Architectural glass offers higher gross margins but greater volatility tied to real estate cycles. Float glass provides the lowest margins but strategic control over raw material. The optimal mix constantly shifts with market conditions, requiring dynamic capital allocation.

The cash flow profile deserves attention. While reported profits are ₹345 crore, operating cash flow often exceeds ₹500 crore due to high depreciation charges. This cash generation funds both growth capex and dividends, though the balance varies with investment cycles. During expansion phases, free cash flow turns negative as capex exceeds operating cash flow. During consolidation phases, the company generates substantial free cash.

The debt position frames the financial risk. With debt-to-equity around 0.8x and interest coverage above 4x, AIS maintains a conservative balance sheet by manufacturing standards. But with massive expansion plans requiring ₹1,700-1,900 crore over 2022-2025, leverage will increase. The key question: Can AIS time its capacity additions to coincide with demand upturns rather than downturns?

The return metrics paint a mixed picture. Return on equity of 15-17% seems adequate but not exceptional. Return on capital employed of 12-14% falls below the cost of capital during tough periods. These metrics improve dramatically at high utilization but deteriorate quickly when demand softens. The cyclicality isn't just in revenues—it's amplified in returns.

For investors, the financial analysis reveals a company caught between two worlds. The stability of market dominance battles the volatility of capital-intensive manufacturing. The promise of technology-driven margin expansion confronts the reality of commodity input costs. The opportunity of India's growth collides with the challenge of funding that growth profitably.

The valuation question becomes: Are you buying a stable market leader trading at reasonable multiples, or a cyclical manufacturer at peak margins? The answer determines whether AIS represents value or a value trap. As we'll explore in the competitive dynamics, the sustainability of AIS's financial performance depends not just on market growth but on maintaining competitive advantages in an industry where advantages erode quickly.

VIII. Competitive Moats & Strategic Advantages

In Warren Buffett's castle metaphor, moats protect businesses from competitive assault. But what happens when your castle is made of glass—transparent, fragile, seemingly commoditized? AIS has spent four decades building moats that shouldn't exist in a commodity business, creating competitive advantages through intangible assets in an industry obsessed with tangible production.

Promoter holding: 54.1%—this number represents more than ownership; it's a statement of commitment. In an era when promoter stakes are diluted for growth capital, the Labroo family and AGC have maintained majority control. This isn't sentimentality—it's strategic. The promoter structure enables long-term thinking in an industry where quarterly earnings volatility can panic public shareholders into value-destroying decisions.

The OEM relationships constitute AIS's most powerful moat. It provides glass to automobile manufacturers including Maruti Udyog, Tata Motors, Hyundai Motors, Mahindra & Mahindra, General Motors, Ford India, Fiat India, Honda, Eicher, Volvo, Hindustan Motors, Skoda Auto, Volkswagen India, Toyota Kirloskar, and Piaggio. But these aren't vendor relationships—they're technical partnerships embedded in product development cycles that span 3-5 years.

Consider the switching costs from an OEM's perspective. Changing glass suppliers isn't like changing steel vendors. Every piece of glass must be validated for optical properties, safety standards, fit tolerances, and integration with sensors and electronics. The validation process alone takes 12-18 months and costs millions. A single quality issue—a windshield that doesn't properly support ADAS sensors, for instance—can halt an entire assembly line, costing lakhs per hour. These switching costs create relationship stickiness that transcends price competition.

The technical expertise moat runs deeper than most investors appreciate. Glass-making might seem straightforward—melt sand, form sheets, cut to size. But automotive glass requires mastery of dozens of technologies: chemical tempering for strength, acoustic dampening for noise reduction, coating deposition for solar control, optical engineering for HUD compatibility, sensor integration for ADAS functionality. Each technology requires years to master and continuous innovation to maintain leadership. AIS's technical teams don't just make glass—they solve complex materials science problems.

The Japanese technology partnership with AGC provides continuous capability renewal. AGC is one of the leading manufacturers of glass globally, with a 12% global market share in the float glass segment and 30% in auto glass share. This isn't a licensing arrangement where technology transfers once—it's ongoing collaboration where innovations flow bidirectionally. AGC's global R&D benefits from AIS's frugal engineering, while AIS accesses cutting-edge technology without bearing full development costs.

The integrated manufacturing moat creates competitive advantages at multiple levels. Competitors who buy float glass face supply uncertainty and quality variability. Those who only process glass can't optimize formulations for specific applications. Those who only serve automotive can't leverage architectural volumes for scale. AIS's end-to-end presence—from sand to installation—provides cost advantages, quality control, supply security, and innovation capabilities that focused players can't match.

Distribution and service networks form an underappreciated moat. It also provides consumer glass offerings in the form of Glasxperts and Windshield Experts. With 100+ Windshield Experts centers and growing Glasxperts presence, AIS has direct customer touchpoints that pure B2B players lack. These networks don't just generate revenue—they create brand awareness, gather market intelligence, and influence specification decisions at multiple levels.

The data and design capabilities increasingly matter. AIS doesn't just respond to specifications—it helps create them. When an OEM designs a new vehicle, AIS engineers collaborate from concept stage, suggesting glass solutions that optimize aerodynamics, reduce weight, improve safety, and enable new features. This design collaboration creates intellectual property jointly owned with customers, further increasing switching costs.

Manufacturing flexibility provides competitive advantage in a market with extreme demand variability. AIS's plants can switch between products—automotive to architectural, clear to coated, standard to specialized—based on market conditions. This flexibility requires sophisticated planning systems, multi-skilled workforces, and equipment designed for quick changeovers. Competitors with dedicated lines lack this adaptability.

The sustainability credentials increasingly matter for global OEMs with ESG commitments. AIS is setting up the greenfield project in Chittorgarh for manufacturing high-quality float glass to be used for automotive and architectural purposes with technology collaboration from its partners—AGC Europe. The arrangement with INOX Air Products to establish a Green Hydrogen plant aligns with AIS's comprehensive sustainability strategy. These aren't CSR initiatives—they're strategic differentiators in a world where supply chain emissions affect customer choices.

Geographic positioning creates local advantages. AIS's plants near automotive clusters reduce logistics costs and enable just-in-time delivery. The ability to respond quickly to OEM requirements—design changes, volume fluctuations, quality issues—provides competitive advantage over imports or distant domestic competitors. In automotive supply chains, proximity is power.

But moats aren't permanent, and AIS's show signs of erosion. Chinese competitors offer 20-30% lower prices, forcing AIS to compete on value rather than cost. New technologies like polycarbonate could substitute glass in some applications. Electric vehicles reduce content per vehicle as simpler designs require fewer glass pieces. Global OEMs increasingly source globally, reducing the advantage of local presence.

The competitive threat matrix reveals vulnerabilities. Saint-Gobain brings global scale and technology depth. Fuyao Glass offers Chinese cost structures and aggressive pricing. Local processors provide flexibility and lower overhead. New entrants with modern plants have lower depreciation burdens. Each competitor attacks different parts of AIS's value proposition.

Yet AIS's response reveals strategic sophistication. Rather than competing on price, it competes on total cost of ownership—factoring in quality, delivery, service, and innovation. Rather than protecting existing products, it cannibalizes itself with new technologies. Rather than defending market share at any cost, it focuses on profitable segments. This strategic discipline preserves moats even as competitive pressures intensify.

The network effects, though subtle, amplify competitive advantages. Every OEM relationship provides learning that improves service to other OEMs. Every architectural project builds capabilities applicable to automotive. Every innovation in one segment creates possibilities in others. These network effects create a virtuous cycle where success breeds success.

For investors, the moat analysis suggests AIS possesses durable but not impregnable competitive advantages. The combination of customer relationships, technical capabilities, integrated manufacturing, and strategic partnerships creates barriers that would take competitors years and billions to replicate. But these advantages require continuous investment to maintain. The moment AIS stops innovating, stops investing, stops deepening customer relationships, the moats begin to drain. As we'll see in examining future challenges, maintaining these competitive advantages while navigating industry disruption will determine whether AIS remains a castle or becomes a ruin.

IX. Challenges & Future Battlegrounds

The Chittorgarh facility under construction in Rajasthan tells you everything about AIS's future challenges. This isn't just another float glass plant—it's a ₹1,400 crore bet on green manufacturing, powered by solar energy and green hydrogen, targeting 94% renewable energy usage. But here's the paradox: AIS is investing unprecedented capital to manufacture a commodity product in an era when every business trend points toward asset-light models. This tension between industrial ambition and financial reality defines the battlegrounds ahead.

The EV transition presents both existential opportunity and threat. Electric vehicles require 30% less glass by count—no engine bay means no complex windshield angles, simpler designs mean fewer parts. But they demand 200% more technology per piece—acoustic glass to compensate for missing engine noise, solar control to preserve battery range, heads-up displays for minimalist interiors. The question isn't whether AIS can make EV glass—it's whether EV glass will be as profitable as ICE vehicle glass.

Chinese competition has evolved from price disruption to technology leadership. Fuyao Glass isn't just cheaper—it's increasingly innovative, with smart glass capabilities and global scale that even AGC respects. The Chinese cost advantage isn't just labor—it's scale (10x AIS's production), government support (subsidized energy and capital), and ecosystem effects (complete supply chain localization). AIS can't win on cost, so it must win on something else—but what? The recent anti-dumping duties on solar glass imports reveal both opportunity and vulnerability. India's Ministry of Finance has imposed an antidumping duty on solar glass imports from China in the range of $673 to $677 per metric ton and for imports from Vietnam at $565 per metric ton. In its investigation, DGTR noted the solar glass imports from China and Vietnam (totaling 779,017 MT) constituted almost the entirety of the imports into India, with a share of 98% during the period of investigation. Imports from China grew from 29,324 MT in 2020-21 to 659,732 MT during the period of investigation. While these duties protect domestic manufacturers like AIS, they also highlight India's dependence on imports and the massive scale advantage Chinese producers possess.

Raw material inflation presents an accelerating challenge. Soda ash prices have doubled in three years. Natural gas costs fluctuate wildly with geopolitical tensions. Silica sand quality varies with mining regulations. Each 10% increase in raw material costs erodes EBITDA margins by 2-3 percentage points. Unlike automotive OEMs who can pass costs to consumers, glass manufacturers face rigid contract prices and intense competition.

Technology disruption looms from unexpected directions. Smart glass that can change opacity electronically threatens traditional architectural applications. Gorilla Glass and similar technologies from Corning challenge automotive applications. 3D-printed glass could revolutionize custom applications. Polycarbonate continues improving in optical clarity and cost. Each alternative technology nibbles at glass's traditional advantages.

The ESG requirements aren't just about compliance—they're reshaping competitive dynamics. As a leading and conscientious glass enterprise, AIS is deeply committed to sustainability. It fills us with immense pride that AIS's Soniyana Float Glass facility will be the first in India's Float Glass industry to be powered by Green Hydrogen. Our new plant at Soniyana aims to fulfill 94% of its energy needs through environmentally friendly and sustainable sources. But these green investments require capital that could otherwise fund capacity expansion or technology development. The question becomes: Can AIS afford to be sustainable? Can it afford not to be?

Real estate cycles create architectural segment volatility. India's property market oscillates between irrational exuberance and deep depression, often triggered by regulatory changes (RERA), financial crises (NBFC liquidity), or black swan events (COVID). AIS's architectural business, now 30% of revenues, amplifies this cyclicality. The company must maintain capacity for boom periods while surviving bust phases—a challenging balance.

The talent challenge intensifies as glass manufacturing evolves from industrial process to technology integration. AIS needs chemical engineers who understand software, data scientists who appreciate manufacturing, and sales teams who can sell solutions not products. But India's best engineering talent gravitates toward IT and finance, not manufacturing. Building technical capabilities while competing for talent against tech giants presents an ongoing challenge.

Geopolitical risks multiply. The India-China border tensions affect technology transfer from Chinese equipment suppliers. The Russia-Ukraine conflict disrupts European glass technology partnerships. US-China tensions complicate global supply chains. Middle East instability affects energy costs. Each geopolitical shock ripples through AIS's operations, requiring constant adaptation.

The consolidation pressure builds as global glass giants seek growth through acquisition. Saint-Gobain, Guardian, and Fuyao all have acquisition war chests exceeding AIS's market cap. The question isn't whether consolidation will come to Indian glass but when and how. Will AIS be acquirer or acquired? Can it maintain independence while achieving global scale?

Digital transformation requirements extend beyond products to processes. Industry 4.0 demands connected factories, predictive maintenance, and AI-driven quality control. But retrofitting 40-year-old plants with digital infrastructure requires massive investment with uncertain returns. The risk of being left behind technologically battles the risk of over-investing in unproven technologies.

The regulatory landscape keeps shifting. Automotive safety standards evolve toward global harmonization, potentially eliminating local advantages. Building codes increasingly mandate energy efficiency, creating opportunities but also compliance costs. Environmental regulations tighten, requiring continuous investment in pollution control. Each regulatory change requires adaptation, investment, and sometimes fundamental business model shifts.

Customer concentration risk, despite diversification, remains material. While AIS serves multiple OEMs, the top five customers still account for over 60% of automotive revenues. The loss of a single major customer—through insourcing, competitor win, or market exit—would significantly impact profitability. Maintaining customer relationships while avoiding dependency requires constant balance.

The innovation imperative accelerates. Product life cycles shorten from decades to years. Customer requirements evolve from specifications to co-creation. Competition shifts from product features to system solutions. AIS must innovate not just in glass but in business models, customer engagement, and value creation. The challenge: innovation requires patient capital in an industry demanding quarterly performance.

For investors, these challenges frame the essential question: Is AIS a mature company managing decline or a platform company navigating transformation? The answer depends on execution—whether AIS can navigate these multiple challenges simultaneously while maintaining operational excellence and financial discipline. The next few years will determine whether AIS emerges stronger from these battlegrounds or becomes another industrial casualty of technological disruption.

X. Investment Analysis & Valuation Framework

Sitting in a Mumbai broker's office, staring at AIS's stock chart, you might see a volatile industrial stock trapped in a range. But step back, and you see something else: a 40-year experiment in whether manufacturing excellence can create shareholder value in a world increasingly enamored with asset-light models. At ₹20,002 crore market cap, the market is essentially asking: What's the right price for India's glass monopoly in an age of disruption?

The bull case starts with market position and proceeds through structural tailwinds. Mkt Cap: 20,002 Crore (up 28.8% in 1 year) Despite recent operational challenges, the stock has delivered reasonable returns, suggesting the market sees through temporary headwinds to structural value. With 77% automotive market share and growing architectural presence, AIS has pricing power that commodity manufacturers typically lack. India's vehicle penetration at 30 per 1,000 people versus 800 in developed markets suggests decades of growth ahead. The EV transition, rather than reducing content, increases value per vehicle through technology-rich glass. Infrastructure spending, urbanization, and green building mandates drive architectural demand. The promoter commitment, technology access, and integrated manufacturing create barriers that protect returns.

The bear case focuses on financial performance and competitive threats. The company has delivered a poor sales growth of 11.7% over past five years. This isn't temporary—it reflects structural challenges in core markets. Margin pressure from raw material inflation appears permanent, not transitory. Chinese competition intensifies despite trade barriers. Technology substitution accelerates across applications. The capital intensity requires continuous investment just to maintain position, destroying free cash flow. Real estate cyclicality makes 30% of revenues unpredictable. Customer concentration, despite diversification, remains concerning.

Stock is trading at 7.47 times book value—expensive by manufacturing standards but perhaps justified by irreplaceable assets and market position. The replacement cost of AIS's manufacturing footprint likely exceeds ₹30,000 crore, suggesting book value understates economic value. But high price-to-book also implies the market expects superior returns that recent performance hasn't delivered.

Let's build a valuation framework from first principles. Start with normalized earnings power. Remove one-time charges, adjust for cycle position, and assume mid-cycle margins of 16% EBITDA. On ₹5,000 crore normalized revenue, that's ₹800 crore EBITDA. Subtract ₹200 crore maintenance capex (not growth), ₹100 crore interest, and ₹150 crore taxes. Normalized free cash flow to equity: ₹350 crore. At 20x FCF (reasonable for a dominant franchise), fair value: ₹7,000 crore. Current market cap of ₹20,000 crore implies either massive growth ahead or significant overvaluation.

But this static analysis misses optionality. The green hydrogen initiative at Chittorgarh could pioneer sustainable manufacturing that commands premium valuations. The ADAS and smart glass capabilities could capture disproportionate value in automotive evolution. The architectural segment could inflect with India's construction boom. Export opportunities could materialize as global supply chains reconfigure. Each option has value not captured in current earnings.

Comparison with global peers provides context. Fuyao Glass trades at 15x earnings despite faster growth. Saint-Gobain trades at 12x but with lower returns on capital. Guardian Industries went private at 8x EBITDA. By these metrics, AIS at approximately 25x P/E seems expensive. But India trades at a premium to global peers across sectors, reflecting growth potential and scarcity value.

The capital allocation track record reveals management priorities. Over the past decade, AIS has reinvested most cash flows into capacity expansion rather than returning cash to shareholders. This makes sense if returns exceed cost of capital, but recent ROCE of 12-14% suggests value destruction at the margin. The massive ₹1,700-1,900 crore expansion plan raises questions: Will this investment generate returns above cost of capital, or is it empire building?

The sum-of-parts valuation tells a nuanced story. Value automotive at 15x earnings (₹250 crore × 15 = ₹3,750 crore). Value architectural at 20x given higher growth (₹80 crore × 20 = ₹1,600 crore). Value float glass at book value given commodity nature (₹2,000 crore). Add cash, subtract debt. Total value: ₹7,000-8,000 crore. Current market cap of ₹20,000 crore implies the market sees something the numbers don't—either hidden assets, massive growth, or speculation.

The ESG angle increasingly matters for valuation. Global investors allocate capital based on sustainability metrics. AIS's green hydrogen initiative, renewable energy adoption, and circular economy efforts could attract ESG funds. But these same initiatives require capital that could otherwise boost near-term returns. The valuation question becomes: Does sustainability create or destroy shareholder value?

Risk-adjusted returns framework suggests caution. With beta around 1.2, AIS amplifies market movements. Add company-specific risks—customer concentration, technology disruption, regulatory changes—and the required return approaches 15%. Current valuations imply growth rates that seem optimistic given historical performance and industry dynamics.

The private equity perspective reveals strategic value. A PE buyer could merge AIS with regional players, creating a pan-Asian glass giant. Technology transfer from global partners could accelerate innovation. Operational improvements could expand margins by 200-300 basis points. Financial engineering could optimize capital structure. This strategic value—perhaps ₹25,000-30,000 crore—sets a ceiling on valuations.

For different investor archetypes, AIS presents differently. Growth investors see EV transformation and infrastructure boom. Value investors see expensive multiples and cyclical risks. Quality investors appreciate market dominance but question capital allocation. Income investors note modest dividends and reinvestment priorities. Each perspective is valid, explaining the stock's volatility as different investors dominate at different times.

The key variables for monitoring include: automotive production volumes (leading indicator for revenues), raw material costs (impact on margins), capacity utilization (operational leverage), architectural order book (forward visibility), technology adoption in new models (value per vehicle), and competitive intensity (market share trends).

What would make this a great investment? Evidence of sustained margin expansion through technology. Successful export scale-up reducing India dependence. Architectural segment achieving automotive-like market share. New technologies creating switching costs. Capital allocation shifting toward shareholder returns. These catalysts could justify premium valuations.

What would confirm it's a value trap? Continued margin pressure despite volume growth. Market share losses to imports or new entrants. Technology substitution accelerating. Overcapacity from aggressive expansion. EV transition reducing content value. These risks could trigger significant derating.

The verdict? AIS represents a complex investment proposition—neither obvious buy nor clear sell. It's a bet on India's physical infrastructure growth, manufacturing excellence in a services world, and technology adoption in traditional industry. At current valuations, the market prices in significant success. Whether that optimism proves justified depends on execution in an increasingly challenging environment.

XI. Lessons & Playbook

The conference room at IIM Ahmedabad, where MBA students dissect business cases, might seem worlds away from the furnace floors of Bawal where molten glass flows at 1,500°C. But AIS's journey from single-customer supplier to market dominator offers lessons that transcend industry boundaries—a playbook for building industrial champions in emerging markets.

Lesson 1: Joint Ventures as Capability Accelerators The AIS model demonstrates that successful JVs require three elements: complementary capabilities (Japanese technology + Indian market access), aligned incentives (all partners benefited from growth), and patience (it took 15 years to achieve true independence). The critical insight: JVs work when they're structured as capability-building platforms, not just market-entry vehicles. Too many JVs fail because partners view them as transactions rather than transformations.

Lesson 2: The Sequencing of Strategic Moves AIS didn't try to do everything at once. First, master single-product manufacturing (1984-1992). Then, diversify customers while maintaining quality (1992-2000). Next, integrate backward for control (2001-2006). Finally, expand into adjacent markets (2006-present). Each phase built on the previous, creating cumulative advantage. The lesson: in capital-intensive businesses, strategic sequencing matters more than strategic brilliance.

Lesson 3: Managing Customer Concentration Risk AIS's evolution from 100% Maruti dependence to a diversified portfolio offers a masterclass in relationship management. The key wasn't abandoning the anchor customer but using that relationship as a learning laboratory and credibility builder. By becoming indispensable to Maruti, AIS became attractive to Maruti's competitors. The paradox: the best way to reduce customer concentration is to serve your concentrated customers exceptionally well.

Lesson 4: Vertical Integration Timing AIS waited 17 years before integrating into float glass—not because it couldn't do so earlier, but because the economics weren't right. The company waited until it had sufficient scale, technical capability, and market position to justify the massive capital investment. Premature vertical integration destroys value; properly timed integration creates competitive advantage. The lesson: in manufacturing, when you integrate matters as much as whether you integrate.

Lesson 5: Building Moats in Commodity Businesses Glass is ultimately silicon dioxide—a commodity. Yet AIS built defensible positions through intangibles: customer relationships, technical capabilities, integrated operations, and service networks. The playbook: accept that your product is a commodity, then make everything around the product non-commoditized. This requires thinking beyond manufacturing to the entire customer experience.

Lesson 6: Technology Partnership vs. Independence AIS's relationship with AGC demonstrates sustained technology partnership benefits. Rather than viewing technology transfer as a one-time transaction, AIS structured ongoing collaboration where both parties benefited from innovation. This avoided the trap of technological obsolescence that befalls many emerging market manufacturers who either go alone or rely on static technology transfer.

Lesson 7: The Discipline of Capital Allocation AIS's capital allocation reveals both successes and failures. The successful backward integration into float glass created value. But aggressive capacity expansion during downturns destroyed value. The lesson: in capital-intensive businesses, capital allocation is strategy. Every rupee invested in fixed assets is a rupee that can't be redeployed quickly. This requires exceptional discipline and timing.

Lesson 8: Cultural Integration in Manufacturing Merging Japanese quality obsession with Indian jugaad innovation created a unique culture. Japanese processes provided discipline and consistency. Indian creativity solved problems when imported equipment broke or specifications changed. This cultural synthesis—structured flexibility—became a competitive advantage. The lesson: don't choose between global best practices and local innovation; synthesize them.

Lesson 9: The Portfolio Approach to Risk AIS's multi-segment strategy—automotive, architectural, float—provides resilience through diversification. When automotive slumps, architectural might boom. When both struggle, float glass provides base-load revenues. This portfolio approach requires accepting lower returns in each segment for higher stability overall. For industrial companies, this trade-off often makes sense given high fixed costs.

Lesson 10: Building Brands in B2B AIS's investment in consumer brands like Windshield Experts seems illogical for a B2B company. But these initiatives create brand awareness that influences specification decisions, provide market intelligence, and build direct customer relationships. The lesson: even B2B companies benefit from B2C thinking, especially when end-users influence purchase decisions.

Lesson 11: Sustainability as Strategy, Not CSR AIS's green hydrogen initiative isn't corporate responsibility—it's strategic positioning for a carbon-constrained future. By moving early on sustainability, AIS aims to create competitive advantage through lower emissions, customer preference, and potential carbon credits. The lesson: in manufacturing, sustainability is becoming a source of competitive advantage, not just compliance cost.

Lesson 12: Managing Cyclicality AIS has survived multiple cycles—the 1991 liberalization shock, 1997 Asian crisis, 2008 financial crisis, 2020 pandemic. The playbook: maintain financial flexibility during upturns (don't leverage fully), invest counter-cyclically during downturns (when assets are cheap), and focus on operational excellence always (costs you can control). This requires resisting both irrational exuberance and excessive pessimism.

Lesson 13: The Innovation Imperative AIS's evolution from simple toughened glass to ADAS-enabled smart glass demonstrates continuous innovation. But innovation in manufacturing differs from software—it requires patient capital, physical infrastructure, and tolerance for failure. The lesson: manufacturing innovation is incremental and cumulative rather than disruptive and discontinuous. Small improvements compound into competitive advantage.

Lesson 14: Emerging Market Advantages AIS leveraged unique emerging market advantages: low-cost engineering talent, proximity to high-growth markets, ability to develop frugal innovations, and relationships in relationship-driven markets. These advantages offset developed market disadvantages in technology and capital access. The lesson: don't try to compete with developed market companies on their terms; change the terms of competition.

Lesson 15: The Long Game AIS took 40 years to build its current position—four decades of patient capital, continuous investment, and strategic evolution. In an era of quarterly capitalism, this long-term orientation provides competitive advantage. The lesson: industrial leadership isn't built in IPO cycles but in generational cycles. This requires ownership structures and governance that enable long-term thinking.

The Meta-Lesson: Complexity as Competitive Advantage AIS's business is complex—multiple technologies, customer segments, and value chains. This complexity creates headaches but also barriers. Competitors can't easily replicate 40 years of accumulated capabilities. Customers can't easily switch from integrated suppliers. The lesson: in industrial businesses, managed complexity creates competitive advantage. The challenge is managing complexity without becoming complicated.

For other industrial companies, the AIS playbook suggests a path: Start with a focused niche and anchor customer. Build technical capabilities through partnerships. Expand gradually into adjacent segments. Integrate vertically when economics justify. Create intangible advantages around commodity products. Maintain financial discipline through cycles. Invest in sustainability before it's mandatory. Think in decades, not quarters.

The limitations are equally instructive. This playbook works for industries with high capital requirements, technical complexity, and local advantages. It's less relevant for pure technology businesses, service industries, or winner-take-all markets. The AIS model requires patient capital, stable governance, and tolerance for cyclicality—conditions not always available.

XII. Epilogue: The Future of Glass

Standing at the edge of AIS's newest facility in Chittorgarh, watching robotic arms handle sheets of glass that will become the windows through which India sees its future, you realize this isn't really a story about glass at all. It's about the physical infrastructure of human progress—the transparent barriers that protect us while connecting us to the world outside.

The future of glass is being written in code as much as chemistry. Smart glass that can switch from transparent to opaque with an electrical current, windows that generate electricity through embedded photovoltaics, surfaces that can display information while maintaining transparency—these aren't science fiction but commercial products AIS is developing today. The company introduced smart glazing solutions such as illuminated laminated sunroofs, laminated side-lites, and AR-HUD-ready windscreens. A laminated sunroof and windscreen featuring PDLC switching glazing is also in the works, offering adjustable transparency.

The IoT revolution transforms glass from passive barrier to active interface. Imagine office windows that automatically tint based on sun position and internal temperature, optimizing energy consumption without human intervention. Or automotive glass that doesn't just display information but communicates with infrastructure, other vehicles, and the cloud, making the windshield the primary interface for autonomous vehicles. AIS is positioning for this future, but success isn't guaranteed—it requires capabilities in software, sensors, and systems integration that go far beyond traditional glass manufacturing.

India's infrastructure boom presents unprecedented opportunity. The country needs to build the equivalent of a new Chicago every year for the next two decades to accommodate urbanization. Each building needs glass—not just any glass, but high-performance glass that manages heat, light, sound, and safety. The government's push for green buildings and energy efficiency makes advanced glass mandatory, not optional. AIS could ride this wave, but only if it can scale manufacturing, maintain quality, and fund growth without destroying returns.

The circular economy challenges traditional business models. Glass is infinitely recyclable without quality loss—a perfect circular material. But this requires rethinking the entire value chain from linear (make, use, dispose) to circular (make, use, recycle, remake). AIS is investing in recycling infrastructure, but the economics remain challenging. The question: Can circular economy principles create competitive advantage, or will they remain a cost center?

Climate change reshapes demand patterns. Extreme weather requires glass that can withstand higher wind loads, larger temperature variations, and more frequent storms. Rising temperatures drive demand for solar control glass. Sustainability mandates push for lower embodied carbon. Each climate impact creates market opportunity, but also requires innovation investment. AIS's green hydrogen initiative positions it for a low-carbon future, but at significant capital cost.

The geopolitics of supply chains accelerates localization. The pandemic exposed the fragility of global supply chains. Rising tensions between major powers make dependence on imports risky. India's push for self-reliance ("Atmanirbhar Bharat") creates policy support for domestic manufacturing. AIS benefits from these trends, but must also compete without the crutch of protection as India integrates into global value chains.

Biotechnology might revolutionize glass production. Researchers are developing biological processes to produce glass at room temperature, mimicking how marine organisms create glass structures. Others are embedding living materials in glass to create self-healing or self-cleaning surfaces. These technologies remain experimental, but they could fundamentally disrupt traditional manufacturing. AIS must monitor and potentially invest in these disruptions or risk obsolescence.