Amara Raja Energy & Mobility: India's Battery Champion Takes on the Future

I. Introduction & Episode Roadmap

Picture this: It's 1985 in Chittoor district, deep in rural Andhra Pradesh. The roads are dusty, electricity is sporadic, and industrial development feels like a distant dream. A young entrepreneur named Dr. Ramachandra Naidu Galla has just returned from America with an audacious vision—to build world-class manufacturing facilities not in Bangalore or Mumbai, but right here in his ancestral village. His neighbors think he's lost his mind. Nearly four decades later, that "crazy" idea has grown into Amara Raja Energy & Mobility, a ₹17,400+ crore behemoth that powers millions of vehicles across India and exports to over 60 countries worldwide. Today, ARE&M commands a market capitalization of ₹17,468 crore with revenues of ₹12,405 crore, making it India's technology leader and one of the largest lead-acid battery manufacturers for industrial and automotive applications in India's storage battery industry. The company has successfully navigated multiple technological transitions, from pioneering valve-regulated lead-acid (VRLA) batteries to now betting big on lithium-ion cells with a massive gigafactory under construction. Its batteries are exported to over 50 countries across the globe, serving everyone from Maruti Suzuki to Indian Railways, from telecom towers to data centers.

But here's what makes this story truly remarkable: This isn't just another industrial success story. It's a tale of how a company built in India's hinterlands learned from the world's best (Johnson Controls), then had the courage to go it alone, and is now preparing for perhaps the biggest technological shift in automotive history—the transition to electric vehicles. It's about how you build a ₹17,000+ crore enterprise while maintaining the philosophy that business must serve society, not the other way around.

Over the next several hours, we'll unpack how Amara Raja built one of India's most formidable distribution networks, why they chose to end a 22-year partnership with the world's largest battery manufacturer, and how they're positioning themselves for the electric future while their core lead-acid business still generates 96% of revenues. We'll explore the strategic chess moves, the family dynamics, the technology bets, and the fundamental question every investor is asking: Can a lead-acid battery champion successfully transform into a lithium-ion powerhouse before the EV revolution makes their core business obsolete?

Buckle up. This is the story of how rural India took on the world—and what happens next might surprise you.

II. The Founder's Journey & Origins (1985)

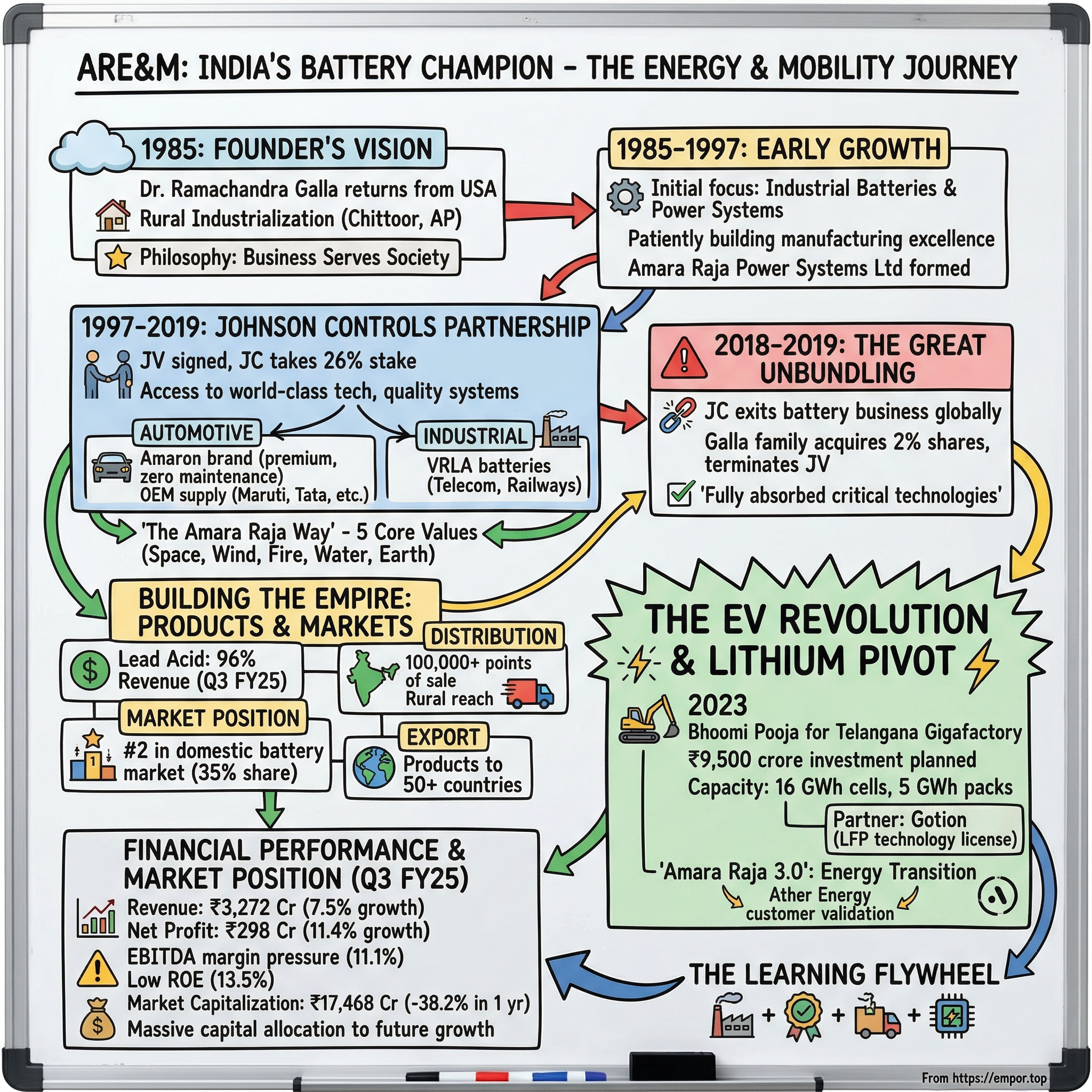

The year is 1985. Ronald Reagan is president of the United States, Rajiv Gandhi has just become India's youngest Prime Minister, and the Indian economy is still six years away from liberalization. In the dusty villages of Chittoor district in Andhra Pradesh, electricity arrives for maybe four hours a day if you're lucky. Industrial development? That's something that happens in Bombay or Madras, not here. Into this setting steps Dr. Ramachandra Naidu Galla—a man who grew up in Petamitta village fixing broken radios for neighbors, who walked seven miles each way to secondary school, who became the first person from his village to pursue higher education. Born on June 10, 1938, to Galla Gangulu Naidu and Galla Mangamma in the village of Petamitta in Chittoor District, he attended elementary school up until the fifth standard and later walked seven miles every day for secondary school. The boy who once understood electronics through dismantled radios would eventually earn not one but two master's degrees—one from IIT Roorkee and another from Michigan State University.

But here's where the story takes its first counterintuitive turn. In 1985, at age 47—an age when most successful engineers are thinking about early retirement—Dr. Galla left a comfortable career at Sargent & Lundy in Chicago, where he designed nuclear and fossil fuel power plants, to return to his dusty village. After working as an Electrical Engineer for Sargent & Lundy, he returned from the USA with the expressed purpose of making a difference by ushering development in his homeland at Chittoor District, Andhra Pradesh. His American colleagues thought he'd lost his mind. Why leave a six-figure salary to start from scratch in rural India?

The answer lay in a philosophy that would define everything Amara Raja would become. Born in a modest farmer family in a remote village of Andhra Pradesh, Dr. Galla experimented with establishing advanced manufacturing facilities in rural villages, creating non-migratory job opportunities. This wasn't charity—it was strategy. While everyone else was clustering in Bangalore and Mumbai, fighting for the same talent and infrastructure, Dr. Galla saw opportunity in India's hinterlands: lower costs, untapped labor pools, and most importantly, loyalty from communities starved of opportunity.

The naming of the company itself tells you everything about the man's values. The Amara Raja Group was founded by Dr Ramachandra N Galla who at the age of 50 made the bold decision to become an entrepreneur, supported by his wife Smt Aruna Kumari Galla and their children Dr Ramadevi Gourineni and Mr Jayadev Galla, the co-founders. The company wasn't named after himself but after Jaydev's grandparents—Amaravati and Rajagopal Naidu—a tribute to the family's agricultural roots and a reminder that success should honor those who came before.

The early years were brutal. Starting with Amara Raja Power Systems Ltd (which would later become Amara Raja Batteries), Dr. Galla had minimal funding and just a handful of employees. First, with little funding and few employees, Amara Raja Power Systems Ltd. ultimately became Amara Raja Batteries. The company initially focused on industrial batteries and power systems—unglamorous but essential products that kept telecom towers running and trains moving.

What made Dr. Galla different wasn't just his rural industrialization model—it was his patient, methodical approach to building capabilities. While other Indian entrepreneurs of the 1980s and 90s chased quick profits through trading or licensing deals, Dr. Galla was obsessed with technology absorption and manufacturing excellence. He wasn't interested in being a middleman; he wanted to build things.

This philosophy extended beyond business. Dr Galla established the Rajanna Trust that works towards education, skill development, rural development, health and management of water. The Trust strives to ensure fair and equitable participation of rural households in national development. By building better amenities for rural people, it promotes inclusive growth and inspires non-migratory living in the region. Roads were built, water tanks constructed, schools established—not as CSR checkboxes but as essential infrastructure for sustainable industrialization.

The Amara Raja Way, as it came to be known, wasn't just corporate jargon. The Amara Raja Way denotes five core values – Innovation, Excellence, Entrepreneurship, Experiences, and Responsibility. These are symbolically equated with the five natural elements – Space, Wind, Fire, Water and Earth – as embedded in the corporate logo. This wasn't some McKinsey consultant's framework but a genuine articulation of how a farmer's son thought about building a world-class company from a village.

By the mid-1990s, Amara Raja had established itself as a reliable manufacturer of industrial batteries. But Dr. Galla knew that to truly scale, the company needed something it couldn't build alone: world-class technology. The question was how to get it without becoming just another subsidiary of a multinational corporation.

The answer would come in 1997, in the form of a partnership that would transform Amara Raja from a regional player into a national powerhouse. But that partnership would also plant the seeds of a dramatic separation two decades later—a corporate divorce that would test whether rural India could truly compete on the global stage.

III. The Johnson Controls Partnership Era (1997–2019)

December 22, 1997. A conference room in Milwaukee, Wisconsin. Johnson Controls executives are looking at a map of India, trying to understand why a battery company from rural Andhra Pradesh wants to partner with the world's largest automotive battery manufacturer. The meeting almost didn't happen—Amara Raja was too small to even register on Johnson Controls' radar. But Dr. Galla had been persistent, leveraging every connection, making multiple trips to the United States, articulating a vision that went beyond just licensing technology.

Amara Raja Batteries of India signed a joint venture with Johnson Controls Inc. in December 1997, with the shareholders agreement dated December 22, 1997 signed between Johnson Controls Mauritius, Johnson Controls Battery Group and the Galla family. This wasn't just a technology transfer agreement—it was a comprehensive partnership where Johnson Controls would take a 26% equity stake in Amara Raja, providing not just technology but also management expertise, quality systems, and global best practices.

The timing was perfect. India's automotive market was exploding post-liberalization. Car ownership was transitioning from luxury to aspiration. But the battery market was dominated by Exide, which had been around since 1947. Breaking that monopoly would require something special—and Johnson Controls had it.

The automotive batteries business unit commenced operations in 2001 with a joint technology venture with Johnson Controls, the world's largest manufacturer of automotive batteries. It pioneered the introduction of zero maintenance technology in India's automotive battery segment. Think about what "zero maintenance" meant in 2001 India—no more checking water levels, no more garage visits every few months. For a country where car servicing was still a mystical art practiced by neighborhood mechanics, this was revolutionary.

The Amaron brand, launched under this partnership, wasn't just another battery—it was positioned as the premium, hassle-free alternative. The marketing was brilliant: "Amaron ki guarantee, Galli galli mein" (Amaron's guarantee, in every street). While Exide was the incumbent everyone knew, Amaron became the challenger everyone wanted to try.

But the real magic wasn't in the marketing—it was in the technology transfer. Amara Raja says that as part of the 1997 technical assistance agreement it has "fully absorbed all critical technologies" over the years. This absorption wasn't passive. Amara Raja engineers were sent to Johnson Controls facilities globally. They didn't just learn how to operate machines; they understood the chemistry, the metallurgy, the quality control philosophies.

The partnership structure itself was fascinating. Johnson Controls wasn't just a passive investor—they had board seats, veto rights on certain decisions, and strict quality audits. Every month, teams from Milwaukee would descend on the Tirupati facility, measuring everything from paste density to grid thickness. For a company that had started just 12 years earlier in a rural village, this level of scrutiny was both terrifying and transformative.

By 2008, the partnership had evolved. The global financial crisis was reshaping the automotive industry, and both companies saw opportunity in deeper collaboration. The shareholders agreement was amended on September 28, 2008, giving Amara Raja more operational freedom while maintaining Johnson Controls' technology pipeline.

The real test came in 2010. Amara Raja Batteries was named on Asia's 'Best Under A Billion' 2010 list of companies compiled by Forbes magazine. This wasn't just recognition—it was validation that a rural Indian company could compete globally. The company was now supplying batteries to virtually every major automotive OEM in India: Maruti Suzuki, Hyundai, Honda, Tata Motors, Mahindra.

What's remarkable is how Amara Raja used the Johnson Controls partnership to build capabilities beyond just automotive batteries. The technology for valve-regulated lead-acid (VRLA) batteries for industrial applications—telecom towers, railways, data centers—came from the same knowledge base but required significant local innovation. Indian telecom towers faced unique challenges: extreme heat, unreliable power grids, and maintenance access issues. Amara Raja's engineers, trained in Johnson Controls' methodologies, developed solutions that even their American partners hadn't thought of.

The relationship wasn't without tension. By 2015, Amara Raja was becoming increasingly confident in its capabilities. The company was exporting to over 50 countries, had built one of the most extensive distribution networks in India, and was generating innovations that Johnson Controls was interested in reverse-engineering for other markets. The student was becoming the teacher.

In October 2018, Amara Raja Batteries Ltd and Johnson Controls signed a technology collaboration agreement expanding their 20-year partnership to share and improve product design and manufacturing technologies. As part of this collaboration, Amara Raja licensed Johnson Controls' proprietary PowerFrame® grid technology. PowerFrame wasn't just an incremental improvement—it represented a fundamental advancement in battery durability and performance. This patented technology is up to 66 percent more durable and more corrosion-resistant than other grid designs.

But even as they were signing new technology agreements, both companies knew the partnership was approaching its end. In November 2018, Johnson Controls International announced its intention to sell its Power Solution business. For Johnson Controls, batteries were becoming non-core as they pivoted toward building technologies and HVAC systems. For Amara Raja, this presented both a crisis and an opportunity.

The negotiations that followed were delicate. Johnson Controls needed to exit cleanly as part of their global restructuring. Amara Raja needed to ensure business continuity—customers, technology, supplier relationships all hung in the balance. Consequently, JC and the Galla family reached an agreement, which would see the Galla family acquire 2 percent equity shares from JC and terminate the shareholders agreement with effect from April 1, 2019.

Twenty-two years of partnership had transformed Amara Raja from a small industrial battery manufacturer into India's second-largest battery company. The company had absorbed not just technology but an entire philosophy of manufacturing excellence. Johnson Controls had provided the ladder, but Amara Raja had done the climbing.

The irony? The partnership ended just as the automotive world was preparing for its biggest transformation in a century—the shift to electric vehicles. Johnson Controls was exiting batteries just as batteries were becoming the most important component in automobiles. Amara Raja would have to navigate this transition alone, but with capabilities that few Indian companies possessed.

IV. The Great Unbundling: Johnson Controls Exit (2019)

April 3, 2019. The news hits the wire at 9:15 AM, just as markets open. "Amara Raja Batteries terminates 22-year partnership with Johnson Controls." Within minutes, the stock is down 5%, trading at Rs 685 on the BSE—dangerously close to its 52-week low of Rs 671. Trading volumes surge more than three times normal as investors scramble to understand what this means. Is this independence or isolation?

The backstory to this divorce is crucial. In November 2018, Johnson Controls International announced its intention to sell its Power Solution business globally to Brookfield Business Partners. Johnson Controls was getting out of batteries entirely—a strategic decision that would later look prescient given the capital intensity of the lithium transition, or foolish given the EV boom, depending on your perspective.

For the Galla family, this presented an existential question: Should they find a new international partner (Brookfield was interested), maintain the status quo with a new owner, or go it alone? The negotiations that followed were a masterclass in strategic patience. The Galla family acquired just 2 percent equity shares from Johnson Controls, taking their stake from 26% to 28%—but that 2% was enough to terminate the shareholders agreement entirely with effect from April 1, 2019.

Think about the audacity of this move. With this, the Galla family has taken control of the company after 22 years of partnership. No more board vetoes, no more technology dependence, no more profit-sharing. But also no more safety net, no more automatic technology upgrades, no more global validation.

The market's initial reaction was brutal but predictable. Investors worried about technology gaps, about losing access to Johnson Controls' R&D pipeline, about competing against Chinese manufacturers without a global partner. But the Galla family had a different calculation. Amara Raja says that as part of the 1997 technical assistance agreement it has "fully absorbed all critical technologies" over the years. This wasn't bravado—it was fact. The company had spent two decades not just operating technology but understanding it, improving it, adapting it to Indian conditions.

The timing of the separation was particularly interesting. Just six months earlier, in October 2018, Amara Raja had signed a technology collaboration agreement with Johnson Controls to license PowerFrame® grid technology—ensuring they had access to the latest innovations even after the equity partnership ended. It was like getting the recipe book before leaving the restaurant.

What followed the announcement was even more dramatic. Reports emerged that Brookfield was re-evaluating its investment plans in the Indian batteries market due to "technological uncertainties." In August 2019, Amara Raja stock fell another 5% on these reports, trading near Rs 581. The market was essentially pricing in a scenario where Amara Raja would be technologically orphaned, unable to compete without a global partner.

But here's what the market missed: Independence wasn't weakness—it was preparation. The Galla family knew something that wouldn't become clear for another year: the future of batteries wasn't in lead-acid technology where Johnson Controls excelled, but in lithium-ion cells where the entire industry would need new partnerships anyway. Why remain tied to a partner whose core competency was becoming obsolete?

The financial implications were significant. No more technology license fees (which had been eating into margins), no more restrictions on entering new markets or partnering with Johnson Controls' competitors, and most importantly, complete strategic freedom to pivot toward electric vehicles and energy storage—markets that Johnson Controls had shown little interest in.

The human dynamics were equally fascinating. Harshavardhana Gourineni, Dr. Galla's grandson, had actually started his career in the Power Solutions division of Johnson Controls, working for 3 years across roles in manufacturing operations and demand planning before returning to India. The next generation had learned from the partner but wasn't beholden to it. They understood both the value and limitations of the Johnson Controls way.

The separation also revealed something about the robustness of Amara Raja's operations. Despite losing their technology partner, there was no disruption in manufacturing, no quality issues, no loss of OEM confidence. Maruti Suzuki, Hyundai, Honda—they all continued sourcing batteries. The distribution network of 30,000+ touchpoints didn't care who owned shares; they cared about product availability and margins.

In retrospect, the Johnson Controls exit was less a divorce and more a graduation. After 22 years, the student no longer needed the teacher. But the real test wasn't whether Amara Raja could maintain its lead-acid battery business without Johnson Controls—it was whether it could transform into an energy storage company for the electric age.

The irony is delicious. Johnson Controls exited the battery business just as batteries were becoming the most important component in the automotive industry. They sold their power solutions business for $13.2 billion to focus on building efficiency—missing the greatest battery boom in history. Meanwhile, Amara Raja, freed from the constraints of a partnership designed for the internal combustion age, was about to make its biggest bet yet.

V. Building the Battery Empire: Products & Markets

Walk into any mechanic shop in India—from the air-conditioned service centers of South Mumbai to the roadside garages of rural Bihar—and you'll see them: the distinctive red and black boxes of Amaron batteries, stacked like trophies of trust. This ubiquity didn't happen by accident. It's the result of one of the most sophisticated distribution plays in Indian corporate history.

Lead Acid Batteries represent 96% in Q3 FY25 of Amara Raja's revenues, but that simple statistic masks an empire of extraordinary complexity. The company operates across two major segments—automotive and industrial—each with distinct dynamics, customers, and competitive moats.

Let's start with automotive, where the magic happens. Amaron is the country's largest-selling aftermarket automotive battery brand, a position that took two decades to build. The brand strategy was counterintuitive: while competitors fought on price in the replacement market, Amara Raja positioned Amaron as premium. Amaron offered complete peace of mind with zero-maintenance and offered the longest warranty that the Indian market had ever seen.

The portfolio architecture is brilliant in its simplicity. Brands include Amaron, Powerzone, and Elito, each targeting different market segments. Amaron for the premium urban consumer who wants reliability above all. PowerZone, initiated to cater to the rural market that was dominated by the unorganized sector, became a market leader in less than 3 years. Elito for the price-conscious segment. Three brands, three price points, one manufacturing backbone.

But the real moat isn't the brands—it's the distribution. The company has a strong distribution network of 23 branches, 39 distribution points, 500+ Amaron franchisees, 100,000+ points of sale, 1,000+ power zone retail stores and 2000+ extensive service hubs in India. Think about what 100,000+ points of sale means. That's more touchpoints than McDonald's has globally. In India, where the unorganized sector still dominates battery replacement, this network is practically unassailable.

The OEM business tells a different story. It serves customers, including Maruti Suzuki, Tata Motors, Hyundai, Honda, Eicher, Mahindra, Ashok Leyland, and many more. These aren't just customers; they're validators. When Maruti Suzuki—which manufactures one out of every two cars sold in India—chooses your battery, you're not just a supplier. You're infrastructure.

The industrial battery business is where Amara Raja's technical prowess really shines. It is a pioneer in manufacturing Valve Regulated Lead Acid (VRLA) batteries in India, serving segments that most investors never think about but which keep the modern economy running. It is a market leader in the Telecom sector and the largest exporter of VRLA batteries.

Consider what powers a telecom tower in rural India. Grid electricity is unreliable, diesel generators are expensive, and downtime means lost revenue. VRLA batteries from Amara Raja provide the bridge—8 to 10 hours of backup power, maintenance-free, reliable in temperatures ranging from -10°C to 50°C. Amara Raja is the preferred supplier to major telecom service providers, telecom equipment manufacturers, the UPS sector (OEM & Replacement), Indian Railways, and the Power, Oil & Gas industry segments.

The product portfolio in industrial is equally strategic. Amara Raja's industrial battery brands comprise of PowerStack®, AmaronVolt® and Quanta®. PowerStack for data centers where even a millisecond of downtime can cost millions. Quanta for telecom towers where reliability is non-negotiable. AmaronVolt for smaller UPS applications. Each brand represents not just a product but a promise of uninterrupted power.

The export story adds another dimension. Amara Raja's Industrial and Automotive Batteries are exported to over 50 countries around the world. This isn't about dumping excess capacity in developing markets. Amara Raja batteries power vehicles in the Middle East's 50°C heat, telecommunications infrastructure in Southeast Asian humidity, and backup systems in African markets where power grids are still developing.

Manufacturing scale is crucial in the battery business—it's a game of chemistry, metallurgy, and massive fixed costs. The company has seven manufacturing plants with a capacity to produce 19 m 4-wheeler batteries, 30 m 2-wheeler batteries, and 2.3 bn ah of industrial batteries. These aren't just factories; they're fortresses of efficiency, running 24/7, where even a 1% improvement in yield can mean crores in additional profit.

The market share numbers tell the story of a successful challenger. Amara Raja Batteries has a market share of 35% in the domestic battery market compared to Exide Industries' 50%. Being number two isn't a weakness—it's a position of strength. You're large enough to have scale economies, but hungry enough to innovate. You can be aggressive on pricing when needed, but premium where you have advantages.

What's fascinating is how Amara Raja has used its lead-acid battery dominance as a platform for adjacencies. The company now manufactures automotive lubricants under the Amaron Hi-Life brand, leveraging the same distribution network, the same customer relationships, the same trust. It's classic platform economics—the marginal cost of adding new products to an existing channel approaches zero.

The financial architecture of this empire is worth understanding. Lead-acid batteries are often dismissed as a commodity business, but Amara Raja has consistently generated EBITDA margins in the mid-teens—remarkable for what is essentially a business of mixing lead, acid, and plastic. The secret? Operational excellence that would make Toyota jealous, combined with brand premiums that commodity players can only dream of.

But here's the existential question every investor must grapple with: What happens to this carefully constructed empire when electric vehicles don't need lead-acid batteries at all? When telecom towers switch to lithium-ion? When the entire substrate of the business shifts from lead to lithium?

The answer to that question is why Amara Raja is betting everything on what might be the most audacious transformation in Indian corporate history.

VI. The EV Revolution & Lithium Pivot

May 9, 2023. Divitipalli village, Mahbubnagar district, Telangana. The monsoon hasn't arrived yet, and the earth is cracked and dusty. K.T. Rama Rao, Telangana's IT Minister, stands next to 85-year-old Dr. Ramachandra Galla, watching as sacred water is poured on the ground. This Bhoomi Pooja isn't for another IT park or residential complex. It's for what will become one of India's largest gigafactory, manufacturing lithium-ion batteries, with a planned investment of Rs 9,500 crore over the next 10 years.

The symbolism is perfect: The man who started making batteries in rural India 38 years ago is now betting everything on the technology that will power India's electric future. But the scale of ambition here is breathtaking. The Amara Raja Giga Corridor aims to produce Lithium Cell and Battery Packs with an ultimate capacity of up to 16 GWh for lithium cells and 5 GWh for battery packs.

To understand what 16 GWh means: That's enough battery capacity to power approximately 320,000 electric cars annually (assuming 50 kWh per car) or millions of two-wheelers. It's more battery capacity than India's entire EV market currently consumes. It's a bet not on where the market is, but where it will be.

The technological leap required is staggering. Lead-acid batteries, which Amara Raja has mastered over four decades, are essentially 150-year-old technology—lead plates, sulfuric acid, basic chemistry. Lithium-ion cells are quantum physics by comparison—nanoscale coatings, complex lithium compounds, manufacturing environments cleaner than hospital operating rooms.

The initial facilities will also include advanced energy research and innovation center, which will be the first of its kind and it will be equipped with advanced laboratories and testing infrastructure for material research, prototyping, product life cycle analysis, and Proof of Concept demonstration. This isn't just a factory; it's an attempt to build an entire ecosystem.

But here's the challenge: India has zero lithium reserves. Every gram of lithium carbonate must be imported. The technology is dominated by Chinese, Korean, and Japanese companies who've spent decades perfecting it. The capital requirements are astronomical—Rs 9,500 crore is just the beginning. And the market? Well, EVs are still less than 2% of India's automotive sales.

This is where the story takes its most interesting turn. In June 2024, Amara Raja Advanced Cell Technologies signed a technical licensing agreement with GIB EnergyX Slovakia, a subsidiary of Gotion High-Tech Co Ltd, licensing Gotion's world class LFP technology for lithium-ion cells. Gotion isn't just any partner—it's one of China's battery giants, with 8 global R&D centers, 8,000 patented technologies covering the battery industry value chain, 20 major manufacturing locations around the world, and a capacity layout expected to reach 300 GWh by 2025.

Think about the geopolitical complexity here. At a time when India is trying to reduce dependence on China, when "Atmanirbhar Bharat" (self-reliant India) is government policy, Amara Raja is partnering with a Chinese company for its most critical technology. But this isn't naive capitulation—it's strategic pragmatism.

This comprehensive agreement enables Amara Raja to manufacture world class LFP cells in both cylindrical and prismatic form factors. The scope of licensing provides access to cell technology IP, support in establishing Gigafactory facilities conforming to latest generation process technologies, integration with Gotion's global supply chain network for critical battery materials, and customer technical support for solution deployment.

The LFP (Lithium Iron Phosphate) technology is particularly strategic. While less energy-dense than NMC (Nickel Manganese Cobalt) batteries, LFP cells are safer, cheaper, and don't require cobalt—a metal with serious supply chain and ethical concerns. For India's price-sensitive market and hot climate, LFP might be the perfect solution.

But Amara Raja isn't putting all its eggs in one basket. Amara Raja and Gotion are both shareholders and board members of InoBat, an emerging lithium battery technology company in Slovakia, tackling advanced applications such as electric aviation and developing a robust 'Cradle to Cradle' ecosystem of battery value chain. This gives them a window into next-generation technologies beyond just automotive applications.

The manufacturing timeline is aggressive. "The first phase will be completed in less than 24 months, which means our first giga factory will be operational before the end of next calendar year (2025)". The pack facility construction has been completed, and the first line is in the final stages of commissioning.

What's fascinating is how Amara Raja is approaching the talent challenge. They brought over a very lean team of supervisory staff from their pack facility located in Karakambadi, Andhra Pradesh and trained all local youth to run this plant. The same philosophy of rural employment that Dr. Galla started with in 1985 continues in the lithium age.

The customer validation is already coming. Amara Raja has signed agreements with Ather Energy, one of India's leading electric scooter manufacturers, for both NMC and LFP cells. This isn't just a supply agreement—it's a vote of confidence from a company that currently imports all its cells.

The financial equation is complex. This new facility in Telangana by Amara Raja plans to create employment opportunities for nearly 4,500 people and a similar number of indirect jobs. But the return on investment timeline for lithium-ion manufacturing is long—typically 7-10 years to break even. For a company that generated most of its profits from lead-acid batteries, this is a massive bet on an uncertain future.

The strategic positioning is clear from what Jayadev Galla calls "Amara Raja 3.0". Version 1.0 was industrial batteries. Version 2.0 was the automotive battery empire built with Johnson Controls. Version 3.0 is the transformation into an energy storage company for the electric age.

But here's the existential question: Can a company that perfected 19th-century technology successfully leap into 21st-century manufacturing? Can rural India compete with Shenzhen's gigafactories? Can patient, long-term thinking overcome the brutal economics of battery manufacturing where scale is everything and margins are razor-thin?

The answer might lie not in competing with China on scale, but in understanding India's unique needs. Two-wheelers, not cars, dominate Indian roads. The climate is hot, requiring different battery chemistry. Price sensitivity is extreme. Power supply is still unreliable in many areas. These aren't disadvantages—they're design parameters for a uniquely Indian solution.

As we'll see in the next section, this transformation isn't happening in isolation. It's part of a larger strategic repositioning that goes far beyond just making batteries.

VII. Financial Performance & Market Position

The numbers tell a story of steady growth masking fundamental tensions. In Q3 FY25, Amara Raja reported revenue from operations at ₹3,272.47 crore, up from ₹3,044.59 crore in Q3 FY24—a respectable 7.5% growth. Net profit after tax stood at ₹298.37 crore, up 11.38% year-over-year. On paper, these look like the results of a healthy, growing company. Dig deeper, and the picture becomes more complex.

The most telling metric is buried in the segment mix: Lead Acid Batteries represent 96% in Q3 FY25 versus 98% in FY23. That 2% shift might seem trivial, but it represents the beginning of a tectonic transition. The new energy business posted a 35% growth in revenue for the quarter, driven by energy storage systems and electric vehicle battery packs—but from a tiny base. It's like watching a speedboat race past an oil tanker; impressive acceleration, but the tanker still dominates the ocean.

The margin story is where the rubber meets the road. Company has a low return on equity of 13.5% over last 3 years—a number that would make Warren Buffett wince. The EBITDA margin dropped from 14.1% to 11.1% year-over-year in Q4 FY25, pressured by rising alloy prices and increased power costs, primarily driven by regulatory changes in solar power settlements and fuel surcharges. These aren't temporary headwinds; they're structural challenges in a commoditizing business.

The stock market's verdict has been brutal. Market Cap: ₹17,468 Crore (down -38.2% in 1 year). At its peak, Amara Raja traded at over ₹1,680 per share. Today, it hovers around ₹970, having lost nearly 40% of its value. The market is essentially saying: "We don't believe the lithium story compensates for the lead-acid decline."

But here's what the market might be missing. Revenue is forecast to grow 7.3% p.a. on average during the next 3 years, compared to a 21% growth forecast for the Electrical industry in India. At first glance, this looks terrible—Amara Raja growing at one-third the industry rate. But this comparison is misleading. The electrical industry includes pure-play EV companies growing from zero. Amara Raja is transitioning a ₹12,000+ crore business, not starting from scratch.

The competitive dynamics with Exide Industries are fascinating. Exide Industries has a market share of 50% in the domestic battery market compared to Amara Raja's 35%. But market share in a declining market is like being the tallest building in a sinking city. What matters is who's building the boats.

The capital allocation decisions reveal management's true beliefs. Despite margin pressures and a declining stock price, the company is plowing ₹9,500 crore into lithium-ion manufacturing. This isn't incremental investment; it's betting the farm. For context, that's nearly 8 years of current net profit being invested in an unproven technology where Amara Raja has no track record.

The working capital dynamics tell another story. The company's working capital requirements have reduced from 47.8 days to 33.6 days—impressive operational efficiency in a business where customer credit and inventory management are crucial. This improvement has freed up hundreds of crores that are being redeployed into new energy investments.

International expansion provides a bright spot. In the last FY, we strengthened our global presence by entering the North American and European markets, placing our products in over 50 countries. Export markets offer better margins and diversification from India's intense price competition. But they also expose Amara Raja to currency fluctuations and global supply chain disruptions.

The dividend policy reflects this transitional tension. The company has been maintaining a healthy dividend payout of 18.1%, trying to keep income investors happy while funding massive growth investments. It's a delicate balance—cut the dividend and risk further stock price decline; maintain it and potentially starve the growth initiatives of capital.

What's particularly interesting is the contrast between operational performance and market perception. The core business is executing well—revenue growing, market share stable, new products launching successfully. But the stock price reflects existential anxiety about the future. The market sees a melting ice cube (lead-acid batteries) and isn't convinced the company can build a new platform before the old one melts away.

The valuation metrics tell this story starkly. The P/E ratio is 18.15 times, a 60% discount to its peers' median range of 44.92 times. The P/B ratio is 2.32 times, a 71% discount to peers' median of 8.02 times. The market is essentially pricing Amara Raja as a value trap—a company whose assets will be worth less tomorrow than today.

But is this pessimism justified? The bear case is clear: EVs will kill lead-acid demand, Chinese competitors will dominate lithium-ion, and Amara Raja will be stuck in the middle with stranded assets and inadequate new technology. The bull case requires more imagination: India's automotive market will grow fast enough to offset EV substitution in the medium term, Amara Raja's distribution network provides a defensible moat even in commoditized batteries, and the lithium investments will pay off as India's EV market explodes.

The financial performance over the next two years will be crucial. Can Amara Raja maintain lead-acid profitability while the lithium investments are still burning cash? Can they achieve the promised operational efficiencies to offset commodity cost pressures? Can they convince the market that this isn't just another Indian industrial company fighting yesterday's war?

As we'll see next, the answer might lie not in the numbers but in the name itself.

VIII. The Name Change & Strategic Repositioning (2023)

September 2023. The company announces what seems like a cosmetic change: Amara Raja Batteries Limited becomes Amara Raja Energy & Mobility Limited. The stock market yawns. Analysts dismiss it as rebranding fluff. But for those paying attention, this wasn't just a name change—it was a declaration of war on the company's own legacy.

In the last FY, we made the big move of changing the company's name to "Amara Raja Energy & Mobility" to reflect our vision to be leading India's energy transition, especially in energy storage and mobility spaces. Jayadev Galla's words reveal the strategic intent: This isn't about batteries anymore. It's about energy and mobility—two of the most transformative sectors of the next decade.

The timing was deliberate. By September 2023, the gigafactory ground-breaking had happened, the Gotion partnership was in advanced negotiations, and the company had clarity on its technology roadmap. The name change was the public announcement of a transformation that had been years in the making.

But why "Energy & Mobility" and not, say, "Amara Raja Advanced Batteries" or "Amara Raja Power Solutions"? The answer reveals sophisticated strategic thinking. "Energy" encompasses not just batteries but entire energy storage systems, power electronics, charging infrastructure—the full stack of electron management. "Mobility" signals ambitions beyond just supplying components to building mobility solutions.

Amara Raja Energy & Mobility Limited (ARE&M) encompasses a diverse range of solutions and products, which includes energy storage solutions, Lithium-ion cell manufacturing, wide range of EV chargers, Li-ion battery pack assembly, automotive and industrial lubricants, and exploration of new chemistries, among others.

The organizational restructuring that accompanied the name change was equally significant. The company created distinct verticals: Traditional batteries under one leadership, New Energy Business under another. This wasn't just administrative reshuffling—it was acknowledgment that running a sunset business and a sunrise business simultaneously requires different muscles, metrics, and mindsets.

The market communication strategy was revealing. Instead of abandoning the battery heritage, ARE&M positioned itself as evolving from it. The message: We're not a battery company trying to learn energy storage; we're an energy storage company that happens to have 40 years of battery expertise. Subtle difference, massive implications.

The brand architecture evolved too. Amaron remained the flagship brand for traditional batteries, but new sub-brands emerged for different energy solutions. The company wasn't trying to stretch the Amaron brand to cover everything—a common mistake in corporate transitions. Instead, they built a house of brands under the ARE&M umbrella.

What's fascinating is how the name change influenced talent acquisition. Suddenly, ARE&M could attract software engineers, IoT specialists, and energy management experts who wouldn't have considered joining a "battery company." The name change was as much about internal transformation as external positioning.

The strategic adjacencies became clearer post-rebrand. EV charging infrastructure, energy management systems, grid storage solutions—all became legitimate territories for ARE&M to explore. Under the old "Batteries Limited" banner, these would have seemed like distractions. Under "Energy & Mobility," they're natural extensions.

The investor communication shifted notably. Quarterly presentations started featuring slides on total addressable market (TAM) for energy storage, EV adoption curves, and renewable energy integration. The company was training the market to value it not on current battery sales but on future energy opportunity.

But the name change also created new challenges. Customers who'd bought Amaron batteries for decades suddenly wondered if the company was still committed to their needs. Competitors seized the opportunity to position themselves as "focused battery specialists" versus ARE&M's "distracted conglomerate."

The international implications were significant. In export markets where "Amara Raja Batteries" had built credibility over decades, the new name required re-education. Some distributors worried that the company was abandoning batteries altogether—requiring extensive reassurance campaigns.

The internal cultural impact was profound. Employees who'd spent careers perfecting lead-acid technology suddenly found themselves in a company talking about software-defined vehicles and grid-scale storage. The resistance wasn't rebellion—it was existential anxiety about relevance.

The financial markets remained skeptical. The name change didn't stop the stock price decline. If anything, it accelerated concerns about capital allocation—would ARE&M spread itself too thin trying to be everything to everyone in the energy space?

The competitive positioning became more complex. ARE&M was no longer just competing with Exide in batteries. It was now theoretically competing with ABB in power electronics, with Tata Power in charging infrastructure, with global giants in energy storage. The pond got bigger, but so did the fish.

What the name change really represented was a generational transition. Dr. Galla built a battery company. Jayadev Galla and the next generation are building an energy company. The name change was the son's respectful but firm declaration that the future would be different from the past.

The regulatory implications were subtle but important. "Energy & Mobility" companies could access different government schemes, subsidies, and partnerships than "Battery" companies. The name change was partly about positioning for policy benefits in India's energy transition.

The ultimate test of the repositioning isn't whether the name sounds better—it's whether ARE&M can execute on the expanded vision. Can a company born in rural Andhra Pradesh making lead-acid batteries transform into a technology company competing in AI-driven energy management? Can patient, long-term thinking overcome the brutal pace of technology change?

IX. Playbook: Business & Investing Lessons

After spending hours deep in Amara Raja's story, several powerful lessons emerge—lessons that apply far beyond batteries and India. These aren't MBA-textbook insights but hard-won wisdom from four decades of building in emerging markets.

Lesson 1: Location as Strategy, Not Constraint

Dr. Galla's decision to build in rural Chittoor wasn't despite the location's disadvantages—it was because of them. Born in a modest farmer family in a remote village of Andhra Pradesh, Dr. Galla has experimented with a brave approach of establishing advanced manufacturing facilities in rural villages thus creating non-migratory job opportunities for local youth while improving the rural infrastructure.

The conventional wisdom says: Build where the infrastructure is. Amara Raja inverted this—build where the loyalty is. Rural workers, given opportunity, showed lower attrition, higher commitment, and deeper gratitude than their urban counterparts. The cost savings were secondary to the cultural advantages.

This principle extends beyond geography. The best opportunities often lie where others see only obstacles. Amara Raja's rural foundation became its moat—competitors couldn't replicate the community integration, government goodwill, and employee loyalty that came from being the primary employer in the region.

Lesson 2: Technology Absorption vs. Technology Dependence

The Johnson Controls partnership masterclass wasn't in having a foreign partner—it was in learning how to not need one. Amara Raja says that as part of the 1997 technical assistance agreement it has "fully absorbed all critical technologies" over the years.

Most Indian companies in the 1990s signed technology agreements that created permanent dependence. Amara Raja spent 22 years systematically absorbing, understanding, and improving upon Johnson Controls' technology. When the partnership ended, they weren't stranded—they were liberated.

The lesson: Every partnership should have an expiration date built into its DNA. Not because partnerships are bad, but because dependence is dangerous. The best partnerships make themselves obsolete by building capability in both parties.

Lesson 3: Distribution as Durable Competitive Advantage

In commoditized products, distribution is destiny. Amara Raja's 100,000+ retail touchpoints aren't just sales channels—they're information networks, brand ambassadors, and competitive barriers rolled into one.

The playbook: Build distribution for your first product, then use that distribution to launch adjacent products. The marginal cost of adding products to existing channels approaches zero, while the cost for competitors to replicate the network is prohibitive. This is why Amara Raja could successfully launch lubricants—the trucks were already going to the same destinations.

Lesson 4: Managing Transitions Through Organizational Structure

The creation of separate divisions for traditional and new energy businesses wasn't org-chart shuffling—it was survival strategy. You cannot ask the same team to maximize today's cash flows while cannibalizing them for tomorrow's growth. The incentives are incompatible, the skills are different, the timelines conflict.

The principle: When managing technological transitions, structural separation precedes strategic success. Different businesses need different metrics, different leaders, different cultures. Trying to transform within existing structures is like performing surgery on yourself—theoretically possible, technically difficult, usually fatal.

Lesson 5: Capital Allocation in Declining Markets

Company has a low return on equity of 13.5% over last 3 years. This number would typically scream "sell." But Amara Raja's capital allocation reveals sophisticated thinking: milk the declining business for cash flow, but invest every rupee of growth capital in the future business.

The framework: In transitional industries, ROE will necessarily decline as you invest ahead of returns. The question isn't whether ROE is falling—it's whether you're investing in businesses that will eventually generate higher returns than the declining business ever could. Judge management not on today's returns but on the optionality they're creating.

Lesson 6: Brand Permission and Extension Limits

Amaron became synonymous with car batteries in India. But ARE&M didn't try to stretch Amaron to cover lithium-ion cells or charging stations. They understood brand permission—what customers will believe from your brand—has limits.

The insight: Brand equity is like a rubber band. Stretch it too far and it snaps. Amara Raja created new brands for new categories while maintaining Amaron's position in traditional batteries. This prevented brand dilution while allowing category expansion.

Lesson 7: The Patience Premium in Impatient Markets

Indian public markets are notoriously short-term focused. Quarterly earnings calls dominate discourse. Yet Amara Raja is making 10-year bets on lithium-ion technology. The company said that it aims to invest Rs 9,500 crore in the region over the next 10 years.

The lesson: In impatient markets, patience becomes a competitive advantage. If you can withstand short-term stock price pressure, you can make investments your competitors cannot. The challenge is maintaining stakeholder confidence during the investment period—requiring exceptional communication and credible leadership.

Lesson 8: Ecosystem Development as Competitive Strategy

Amara Raja has chosen Telangana for its ambitious Amara Raja Giga Corridor, which will include a state-of-the-art energy research and innovation centre in Hyderabad, named Amara Raja E-hub. This isn't just about manufacturing—it's about creating an ecosystem where innovation, manufacturing, and talent development reinforce each other.

The playbook: Don't just build factories, build ecosystems. The research center attracts talent, talent attracts customers, customers provide feedback, feedback drives innovation, innovation attracts more talent. It's a virtuous cycle that compounds over time.

Lesson 9: Strategic Pragmatism Over Ideological Purity

Partnering with Chinese company Gotion while India pushes "Atmanirbhar Bharat" (self-reliance) seems contradictory. But Amara Raja chose technology access over ideological purity. They understood that catching up in lithium-ion technology without partnerships would take decades India doesn't have.

The principle: Strategy is about choices, not slogans. Sometimes the best path to eventual independence is temporary interdependence. Amara Raja is using Chinese technology to build Indian capability—strategic pragmatism at its finest.

Lesson 10: Family Business Governance in Public Markets

Promoter Holding: 32.9% The Galla family maintains control without majority ownership—a delicate balance requiring exceptional governance. They've professionalized management while maintaining family vision, attracted independent directors while retaining strategic control.

The lesson: Family businesses that survive generational transitions do three things well: They separate ownership from management, they bring in outside talent for specialized roles, and they maintain family involvement in vision and values while delegating operations. Amara Raja has managed this balance better than most.

The Meta-Lesson: Compound Learning

Perhaps the most powerful lesson from Amara Raja is about compound learning. Every capability they built—from manufacturing excellence to distribution networks to technology absorption—became the foundation for the next capability. Johnson Controls taught them world-class manufacturing. Manufacturing excellence enabled export competitiveness. Export exposure drove quality improvements. Quality improvements built brand premium. Brand premium funded R&D. R&D capabilities attracted technology partners.

It's a learning flywheel that's been spinning for four decades. The lithium-ion pivot isn't a departure from this pattern—it's the next revolution of the wheel.

For investors, the lesson is clear: In transitional industries, bet on learning velocity over current profitability. The companies that survive technological disruptions aren't necessarily the most profitable today—they're the fastest learners who can compound capabilities over time.

X. Bear vs. Bull Case Analysis

Every investment thesis is ultimately a bet on the future. With Amara Raja, that future is particularly binary: Either they successfully navigate the energy transition and emerge stronger, or they become a casualty of technological disruption. Let's examine both cases with the rigor they deserve.

The Bear Case: A Melting Ice Cube in the Desert

The bear thesis starts with a simple observation: Lead Acid Batteries (96% in Q3 FY25 vs 98% in FY23). Ninety-six percent of revenues come from a technology that's fundamentally threatened by electrification. This isn't disruption in the abstract—it's an existential threat hiding in plain sight.

Consider the timeline. Every major automotive OEM has announced EV transition plans. Maruti Suzuki, ARE&M's largest customer, plans to launch six EVs by 2030. Tata Motors aims for 50% EV sales by 2030. These aren't aspirations; they're board-approved strategies with capital allocated. When your biggest customers are actively planning to stop needing your main product, you have a problem.

The Chinese competition in lithium-ion is perhaps even more daunting. Gotion High-Tech has 8 global R&D centers, 8,000 patented technologies covering the battery industry value chain, 20 major manufacturing locations around the world, and a capacity layout expected to reach 300GWh by 2025. Amara Raja is planning 16 GWh. Gotion alone will have nearly 20 times that capacity. It's like bringing a knife to a gunfight where your opponent has an arsenal.

The economics of lithium-ion manufacturing are brutal. It's a scale game where the biggest players have insurmountable advantages in raw material procurement, R&D amortization, and manufacturing efficiency. CATL and BYD are producing at scales where their per-unit costs are below Amara Raja's raw material costs. How do you compete when your competitor's total cost is less than your bill of materials?

Company has a low return on equity of 13.5% over last 3 years. The EBITDA margin reduced to 11.1% from 14.1%. The financial deterioration is already visible. Returns are declining, margins are compressing, and this is before the real EV substitution has even begun. What happens when lead-acid volumes actually start declining 10-20% annually?

The capital allocation math is terrifying. ₹9,500 crore investment for uncertain returns in lithium-ion, while the cash-cow lead-acid business faces secular decline. The payback period for the gigafactory investment likely extends beyond the useful life of the lead-acid business. They're essentially betting the company on successfully building a new business before the old one dies.

Technology risk looms large. Lithium-ion itself might be transitional. Solid-state batteries, sodium-ion, aluminum-air—any of these could obsolete lithium-ion investments before they're fully depreciated. Amara Raja is investing billions to catch up to current technology that might itself be obsolete by the time they achieve scale.

The talent challenge is underappreciated. Building lithium-ion cells requires materials scientists, electrochemists, software engineers—talent pools where India has limited depth and global competition is fierce. Can a company headquartered in Tirupati attract and retain the caliber of talent needed to compete with firms in Shenzhen, Seoul, or Silicon Valley?

Market timing could be fatal. India's EV adoption might happen faster than expected (killing lead-acid demand) or slower than expected (making lithium investments uneconomical). There's a narrow window where the transition speed matches Amara Raja's transformation capabilities. Miss that window and you're dead.

The bear case bottom line: Amara Raja is a traditional manufacturing company trying to become a technology company while its core business faces obsolescence. The odds of successfully managing this transition, given the capital requirements, technological complexity, and competitive dynamics, are extremely low. The stock is a value trap—optically cheap but structurally challenged.

The Bull Case: The Energy Phoenix Rising

The bull thesis begins with India's unique market dynamics. India isn't Europe or China. Two-wheelers dominate, the climate is harsh, the power grid is unreliable, and price sensitivity is extreme. These aren't Western or Chinese markets—they require Indian solutions. Amara Raja understands these nuances better than any global player.

The new energy business posted a 35% growth in revenue for the quarter, driven by energy storage systems (ESS) and electric vehicle battery packs. The transformation is already underway. While lead-acid dominates today's revenue, the growth is entirely from new energy. This isn't a company talking about transformation—it's one executing it.

The lead-acid business has more life than bears assume. India's vehicle parc will grow from 300 million to 500 million vehicles by 2030. Even if EV penetration reaches 30% of new sales by 2030 (aggressive by any standard), the installed base of ICE vehicles requiring replacement batteries will continue growing for at least another decade. The cash cow has longer to live than pessimists believe.

Amara Raja Energy & Mobility (ARE&M) broke ground for its 16 GWh Li-ion cell factory in Mahbubnagar, Telangana. Phase 1 would consist of R&D centre, pack facility with 5 GWh capacity, commercial pilot plant, and 2 GWh of cell-making. The lithium execution is ahead of schedule. Pack assembly is already operational, cell production starts in 2025. They're not talking about someday—they're building now.

The Gotion partnership transforms the risk equation. The scope of licensing provides access to cell technology IP, support in establishing Gigafactory facilities conforming to latest generation process technologies, integration with Gotion's global supply chain network for critical battery materials. This isn't just technology transfer—it's full ecosystem access. Amara Raja gets to piggyback on Gotion's scale for procurement, dramatically improving their cost position.

Distribution remains a massive moat. Those 100,000+ retail touchpoints don't disappear because the product changes. Whether selling lead-acid batteries, lithium-ion packs, or charging stations, the relationship with mechanics, fleet operators, and retail customers remains ARE&M's sustainable advantage.

The financial position enables transformation. Unlike many disrupted companies, ARE&M has the balance sheet to fund its transition. Debt-free, cash-generative, with patient family ownership—they can withstand years of transition losses that would kill leveraged competitors.

Government support provides tailwind. India's PLI schemes, import barriers on Chinese cells, and push for local manufacturing all benefit ARE&M. The geopolitical desire to build non-Chinese supply chains creates opportunities for local champions. ARE&M is perfectly positioned as that champion.

The ecosystem play is undervalued. Amara Raja will collaborate with Ather to develop and supply NMC and LFP Lithium-Ion cells produced locally at their upcoming Gigafactory. Customer commitments are already in place. Ather isn't hoping ARE&M succeeds—they're betting on it with supply agreements.

Valuation provides margin of safety. The Amara Raja Energy EPS (TTM) is 51.61. Amara Raja Energy reported EPS of 9.10 for the latest quarter. Trading at 18x earnings for a company with dominant market position, even in a transitioning industry, provides downside protection. The market is pricing in disaster; any success could drive significant rerating.

The bull case bottom line: Amara Raja has the brand, distribution, balance sheet, and partnerships to successfully navigate the energy transition. The market is overly pessimistic about lead-acid's decline and underestimating ARE&M's execution capabilities in new energy. Patient investors could see multibagger returns as the transformation succeeds.

The Verdict: Calculated Risk vs. Reckless Gamble

Both cases have merit. The bear case rightly identifies the structural challenges—technological disruption is real, Chinese competition is formidable, and the capital requirements are massive. The bull case correctly points to ARE&M's unique advantages—distribution moat, local market knowledge, and early mover advantage in Indian lithium-ion production.

The investment decision ultimately comes down to three beliefs: 1. Can lead-acid cash flows sustain long enough to fund the lithium transition? 2. Will India's EV market develop in a way that favors local manufacturers? 3. Can ARE&M execute one of the most complex corporate transformations in Indian history?

If you believe the answer to all three is yes, ARE&M at current valuations could be the opportunity of a decade. If any one answer is no, it's a value trap that will destroy capital for years.

The truth likely lies somewhere in between—a moderately successful transformation that preserves capital but doesn't create spectacular returns. But in markets, moderate outcomes rarely occur. Companies either successfully transform or they don't. Amara Raja's next five years will determine which side of that binary outcome they land on.

XI. Recent Developments & Future Outlook

As we sit in August 2025, Amara Raja stands at the precipice of its most crucial phase. The decisions made in the next 18 months will determine whether this 40-year-old company thrives for another 40 years or becomes a cautionary tale of disruption.

The gigafactory progress is the immediate catalyst everyone's watching. "The first phase will be completed in less than 24 months, which means our first giga factory will be operational before the end of next calendar year (2025)" We're now in that critical window. The pack facility is commissioned, but the cell manufacturing—the real test—begins commercial production in Q4 2025.

The technology readiness is encouraging. Teams on both sides are already connected and working on transferring technical documentation, scheduling trainings on product design, and jointly designing the factories. We have a very tight schedule and aim to begin construction on the first LFP facility within the next quarter or so. From the start of construction, we are targeting to be running commercial production in 24 months.

But technical capability is just table stakes. The real question is market readiness. India's EV penetration in two-wheelers has reached 5%, in passenger vehicles barely 2%. These numbers need to hit 15-20% for ARE&M's lithium investments to generate acceptable returns. The trajectory is positive but the pace remains uncertain.

The competitive landscape is evolving rapidly. Ola Electric is building its own cell manufacturing. Reliance is partnering with global players. Tata is investing heavily in the entire EV value chain. ARE&M's first-mover advantage in Indian cell manufacturing is real but fragile. Six months' delay in execution could mean the difference between market leadership and also-ran status.

Customer validation continues building. Beyond Ather, discussions are underway with major two-wheeler OEMs, commercial vehicle manufacturers, and energy storage system integrators. But discussions aren't contracts, and contracts aren't revenue. The conversion of interest to orders will determine whether the gigafactory runs at capacity or becomes a white elephant.

The traditional business shows remarkable resilience. "Our traditional lead acid battery business continues to deliver strong results in both India and international markets." The aftermarket remains strong, OEM relationships are stable, and export growth continues. The cash cow isn't dying as fast as bears predicted, providing crucial breathing room for the transformation.

Raw material dynamics are shifting. Lithium prices have fallen 80% from their 2022 peaks, improving the economics of cell manufacturing. But this also reduces the cost advantage of local manufacturing versus imports. ARE&M needs to establish market position while the economics support local production—a window that might not stay open long.

The policy environment remains supportive but fluid. India's FAME subsidies are evolving, import duties are under review, and PLI schemes are being refined. Each policy change can dramatically alter competitive dynamics. ARE&M's government relations capabilities, built over decades, become a crucial competitive advantage in navigating this complexity.

Organizational capability building accelerates. The company is hiring aggressively for the new energy business—battery scientists from Korea, manufacturing experts from China, software engineers from Bangalore. The culture clash between rural manufacturing discipline and urban tech ambition is real but manageable. The key is maintaining the best of both worlds.

The financial trajectory for the next 24 months looks challenging but manageable. Lead-acid will generate ₹11,000-12,000 crore in revenue with declining but positive margins. The lithium business will burn ₹500-800 crore annually until scale is achieved. The math works if—and only if—lead-acid margins don't collapse and lithium ramp-up doesn't face major delays.

Strategic options are proliferating. ARE&M could accelerate through acquisitions, buying distressed lithium assets globally. They could pivot to becoming a technology licensor, leveraging their India expertise. They could focus on niches like stationary storage where Chinese competition is less intense. Optionality has value, but too many options can paralyze execution.

The next five years will see one of three scenarios:

Scenario 1: Successful Transformation (30% probability) The gigafactory ramps successfully, capturing 20-30% of India's cell market. Lead-acid business declines gradually, providing cash flow throughout the transition. Stock rerates to 35-40x earnings as market recognizes ARE&M as India's energy storage champion. Stock price: ₹2,500-3,000.

Scenario 2: Muddling Through (50% probability)

Lithium business achieves moderate success but faces intense competition. Lead-acid declines faster than expected, pressuring margins. Company survives but doesn't thrive, becoming a smaller player in a larger market. Stock price: ₹800-1,200.

Scenario 3: Disruption Casualty (20% probability) Gigafactory faces execution challenges, technology proves uncompetitive, or market develops slower than expected. Lithium investments don't generate returns while lead-acid cash flows evaporate. Company forced to restructure or sell assets. Stock price: ₹400-600.

The key monitorables for investors: - Gigafactory commissioning milestones (Q4 2025 critical) - Customer contract announcements (need 3-5 major OEMs) - Quarterly progression of new energy revenue (must exceed 10% by Q2 FY26) - Lead-acid margin trends (EBITDA must stay above 10%) - Working capital cycles in lithium business (critical for cash flow)

The intangibles matter as much as the numbers. Can management maintain employee morale during transformation? Will the Galla family stay committed through the valley of death? Does the company have the cultural flexibility to compete in fast-moving technology markets?

"We continue to make rapid progress in the Li-ion battery and chargers segment and are confident that we will be among the first companies to introduce an indigenously manufactured Li-ion cell in India." This confidence is either prescient or delusional. The next 18 months will tell us which.

The future of Amara Raja isn't just about one company. It's a test case for whether traditional Indian manufacturing can successfully transform for the new economy. Whether patient, long-term thinking can overcome the brutal pace of technological change. Whether building from rural India remains viable in an increasingly urban, digital world.

For investors, ARE&M represents a rare opportunity to bet on transformation at reasonable valuations. But it requires stomach for volatility, patience for multi-year execution, and faith that a company born in the lead-acid age can thrive in the lithium-ion era.

The story isn't close to over. In fact, the most interesting chapters are just beginning. Whether they're chapters of triumph or tragedy remains to be written. But one thing is certain: Amara Raja's journey from rural battery maker to energy solutions provider will be one of the defining corporate stories of India's economic transformation.

The question for investors isn't whether the transformation will be smooth—it won't be. The question is whether the destination justifies the journey. At current valuations, with current capabilities, facing current opportunities, that's a bet worth considering.

Just don't expect it to be easy. Transformations never are. But then again, neither was building a world-class battery company in rural Andhra Pradesh 40 years ago. And that worked out pretty well.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube