Apollo Tyres: The Indian Tyre Giant's Global Ambition

I. Introduction & Cold Open

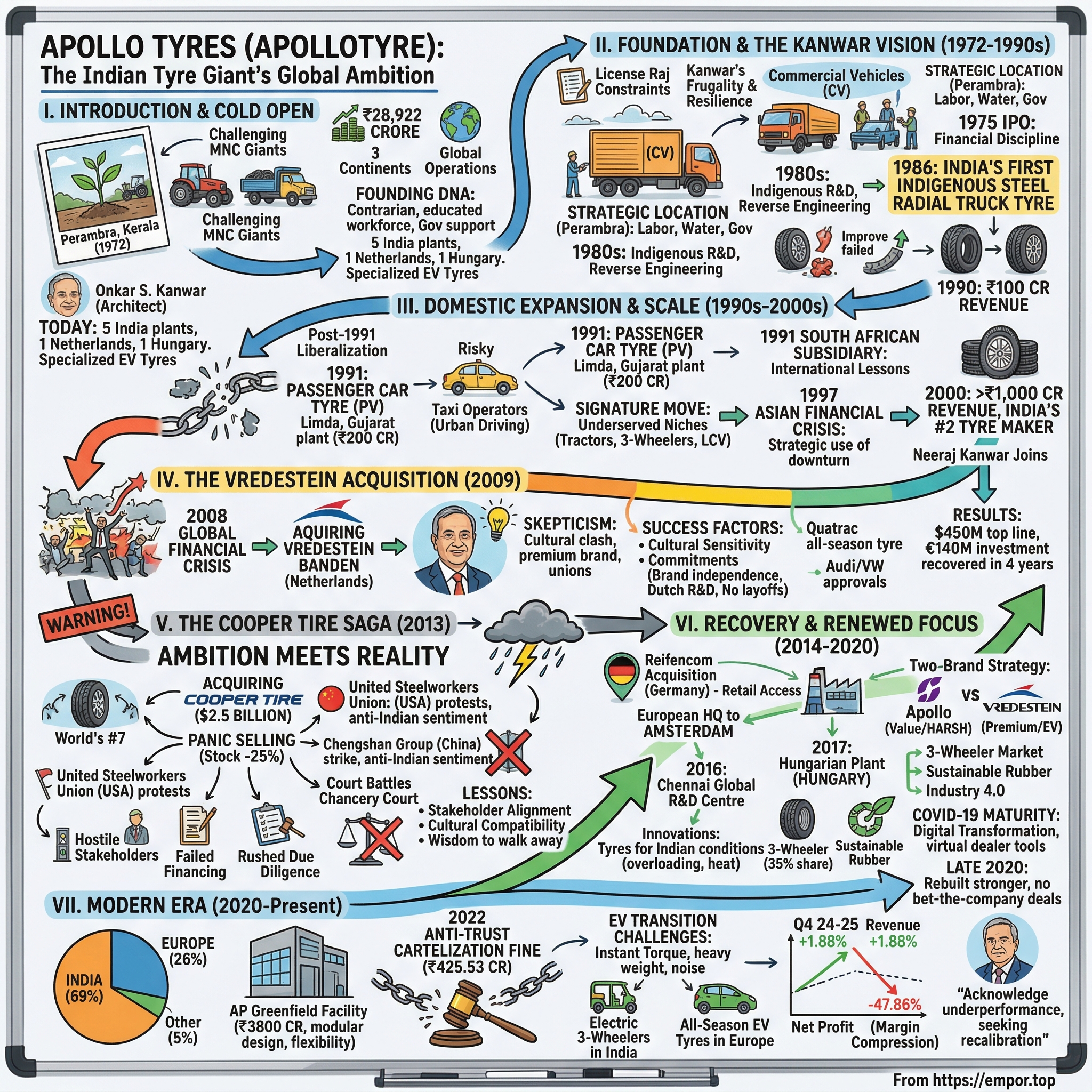

Picture this: September 28, 1972, in the lush, monsoon-soaked landscape of Kerala, far from India's industrial heartlands of Mumbai or Delhi. A group of entrepreneurs gather to incorporate a company that would dare to challenge multinational giants who'd dominated India's tyre market since the British Raj. The location seems improbable—Perambra, a small town better known for its cashew plantations than manufacturing prowess. Yet this is where Apollo Tyres would begin its journey from a single truck tyre plant to a global operation spanning three continents with a market capitalization of ₹28,922 crore.

The founding moment itself tells you everything about Apollo's DNA. While MNCs like Dunlop and Firestone operated from India's metros with their imported technology and foreign management, Apollo chose Kerala—a state with militant trade unions, heavy monsoons that disrupted logistics, but also an educated workforce and a government eager for industrial development. It was contrarian from day one.

The company's incorporation brought together an unusual coalition: Bharat Steel Tubes, Raunaq International, and individuals including Raunaq Singh, Mathew T. Marattukalam, and Jacob Thomas. But the real architect of Apollo's vision was Onkar S. Kanwar, who saw opportunity where others saw obstacles. In an era when "Made in India" often meant second-rate quality, Kanwar believed an Indian company could not just compete but eventually acquire European brands with century-old heritage.

Today, Apollo operates five manufacturing facilities in India, one in the Netherlands, and another in Hungary. Its tyres roll on everything from rural Indian tractors to European luxury sedans. The company that started making bias truck tyres now develops specialized EV tyres in European R&D centers. This transformation didn't happen through luck or timing alone—it's a story of calculated risks, spectacular failures, quiet recoveries, and the peculiar advantages of being an outsider.

Over the next several hours, we'll dissect how Apollo navigated India's License Raj, why the 2008 financial crisis became their European opportunity, how a $2.5 billion acquisition attempt nearly destroyed the company, and what their journey teaches us about building a global manufacturing champion from an emerging market. We'll explore three major inflection points that defined Apollo: the Vredestein acquisition that worked, the Cooper Tire deal that spectacularly didn't, and the current EV transition that might determine whether Apollo remains a regional champion or becomes a true global force.

II. Foundation & The Kanwar Vision (1972-1990s)

The India of 1972 was a different universe from today's economic powerhouse. The License Raj strangled entrepreneurship—you needed government permission to manufacture, expand capacity, even to import raw materials. Foreign exchange was so scarce that importing a machine required months of bureaucratic approvals. In this suffocating environment, starting a tyre company seemed almost masochistic. MNCs like Dunlop, Firestone, and Goodyear had sewn up the market, leveraging their global supply chains and technical expertise.

Yet Onkar S. Kanwar saw opportunity in these constraints. The son of a refugee who fled Pakistan during Partition with nothing, Kanwar understood frugality and resilience at a molecular level. His father had built a modest tubes and pipes business, but Kanwar dreamed bigger. He noticed that while passenger cars were luxury items in 1970s India, commercial vehicles were the economy's workhorses. Every sack of grain, every bale of cotton, every manufactured good moved on truck tyres. And these trucks, operated by cost-conscious fleet owners, needed affordable, durable tyres—not expensive imports.

The Perambra plant's location was strategic genius disguised as necessity. Kerala offered educated workers who could be trained in precision manufacturing, abundant water for cooling (critical in tyre production), and a state government desperate to industrialize. The trade unions that scared away other investors? Kanwar saw them differently—engage them as partners, share productivity gains, and you'd get a committed workforce that wouldn't job-hop to competitors.

Apollo's first public offering in 1975 raised modest capital, but more importantly, it forced financial discipline. Unlike family businesses that could hide inefficiencies, being publicly listed meant quarterly scrutiny. The company focused obsessively on one segment: bias truck tyres for the domestic market. While competitors chased prestige passenger car contracts, Apollo built relationships with fleet operators, understanding their routes, loads, and pain points.

The 1980s brought gradual expansion but Apollo remained disciplined. When competitors rushed to license foreign technology, paying hefty royalties, Apollo chose the harder path of indigenous development. They hired Indian engineers fresh from IITs, set up a modest R&D center, and reverse-engineered competitor products. The tyres weren't sophisticated, but they were robust and cheap—exactly what Indian truckers needed.

A defining moment came in 1986 when Apollo introduced India's first indigenously developed steel radial truck tyre. Radials were superior to bias tyres—better fuel efficiency, longer life, improved handling—but required different manufacturing technology. MNCs assumed Indian companies couldn't master this. Apollo proved them wrong, though initial quality issues nearly killed the product. Kanwar personally visited truckers, collected failed tyres, analyzed failure patterns. Within eighteen months, Apollo's radials matched imported quality at 70% of the price.

By 1990, Apollo had crossed ₹100 crore in revenues. Small by global standards, but they'd proven something important: an Indian company could innovate in manufacturing, not just assemble foreign designs. They'd built a distribution network reaching small towns where MNCs wouldn't venture. Most importantly, they'd developed an organizational capability that would become crucial later—the ability to learn from failure without losing nerve.

The transformation wasn't just about business metrics. Apollo was changing the narrative around Indian manufacturing. When government delegations visited the Perambra plant, they saw world-class housekeeping, workers who could explain statistical process control, and quality metrics matching global standards. This wasn't the stereotypical third-world factory. As India prepared to liberalize its economy in 1991, Apollo was ready to compete without protection.

III. Domestic Expansion & Building Scale (1990s-2000s)

The 1991 liberalization transformed India's business landscape overnight. Import duties crashed, foreign investment rules relaxed, and suddenly Apollo faced unrestricted competition from global giants. Many predicted domestic manufacturers would be steamrolled. The Bombay Club—a group of Indian industrialists—even petitioned for protection, arguing Indian companies needed time to adjust. Apollo took a different path: they accelerated expansion.

The decision to diversify into passenger car tyres in 1991 seemed suicidal. Passenger car buyers were brand-conscious, quality-obsessed, and had options. Why would someone choose Apollo over Michelin? But Kanwar understood something others missed: liberalization would eventually democratize car ownership. The Ambassador-driving bureaucrat would be replaced by millions of middle-class Maruti 800 owners who cared more about value than prestige.

Apollo's first passenger car tyre facility in Limda, Gujarat, represented a massive bet. The ₹200 crore investment was larger than the company's entire net worth. Banks were skeptical—one SBI executive reportedly asked Kanwar, "Why not just import and trade? Manufacturing is risky." But Apollo had learned something crucial from their truck tyre experience: controlling manufacturing meant controlling quality, costs, and destiny.

The real breakthrough came through an unlikely source: taxi drivers. While premium car owners wouldn't touch Apollo tyres, taxi operators—who drove 200 kilometers daily and changed tyres every few months—became eager early adopters. Apollo engineers spent months in Mumbai's taxi stands, measuring wear patterns, understanding failure modes. They developed a tyre specifically for high-mileage urban driving—harder compound for durability, simplified tread for easy rotation. Within two years, Apollo owned 40% of the taxi replacement market.

This bottom-up market entry strategy became Apollo's signature move. Rather than competing head-on with MNCs in premium segments, they identified underserved niches and dominated them. Rural tractors, three-wheelers, light commercial vehicles—segments too small for global giants but collectively massive. By 1995, Apollo had 5,000 dealers, most in Tier 2 and Tier 3 cities where MNC presence was minimal.

The 1991 South African subsidiary deserves special attention—it was Apollo's first international foray, remarkably ambitious for a company still finding its feet domestically. South Africa in the early 1990s was emerging from apartheid, its economy restructuring, creating opportunities for companies willing to take risks. Apollo didn't export from India; they set up local assembly, hired local workers, and positioned themselves as an African company of Indian origin. The venture barely broke even for years, but it taught Apollo invaluable lessons about operating in foreign markets—lessons that would prove crucial in the Vredestein acquisition years later.

Technology absorption accelerated through the 1990s. Apollo signed technical collaborations, but unlike earlier Indian companies that remained perpetual licensees, they insisted on knowledge transfer clauses. Young engineers were sent to partner facilities, not just to observe but to work on shop floors. They returned with more than technical knowledge—they understood quality culture, the rhythm of world-class manufacturing.

The 1997 Asian Financial Crisis briefly threatened expansion plans, but Apollo used the downturn strategically. While competitors froze investments, Apollo negotiated equipment purchases at distressed prices, locked in long-term rubber contracts, and hired talent from struggling competitors. When recovery came in 1999, Apollo had expanded capacity by 40% at a fraction of normal cost.

By 2000, Apollo's transformation was complete: revenues had crossed ₹1,000 crore, they manufactured the full spectrum from two-wheeler to truck tyres, and their brand had shed its budget image. The company that started in a Kerala backwater was now India's second-largest tyre manufacturer. But Kanwar, now joined by his son Neeraj, wasn't satisfied with domestic dominance. The real prize lay beyond India's borders.

The early 2000s saw methodical preparation for international expansion. Apollo upgraded manufacturing to global standards—ISO certifications, Six Sigma implementation, SAP integration. They hired MNC executives, not for their résumés but for their networks and knowledge of global markets. The domestic business generated steady cash flows, debt was manageable, and the organization had developed confidence. When the 2008 financial crisis created unprecedented M&A opportunities, Apollo was ready to pounce.

IV. The Vredestein Acquisition: European Ambitions (2009)

May 2009. The global financial system was in cardiac arrest. Lehman Brothers had collapsed eight months earlier, credit markets were frozen, and European banks were dumping assets at any price. In this chaos, Apollo Tyres announced it would acquire Vredestein Banden B.V. from the bankrupt Russian conglomerate Amtel-Vredestein N.V. The reaction in India was bewilderment—why was a Chennai-based company buying a Dutch brand no one could pronounce?

To understand why this deal mattered, you need to understand Vredestein's history. Founded in 1908, the company took its name from a farm in Loosduinen where its first factory stood. For over a century, Vredestein had been synonymous with Dutch precision engineering. Their tyres equipped the Dutch royal family's vehicles. During World War II, their factory was bombed by the Allies to prevent Nazi use. Post-war, they pioneered winter tyre technology for European conditions. This wasn't just a brand; it was European industrial heritage.

But heritage doesn't pay bills. By 2009, Vredestein was bleeding cash, trapped within Amtel's collapsed empire. The Enschede plant, despite 5.5 million tyre capacity and sophisticated technology, operated at 60% utilization. The workforce, 1,400 skilled Dutch workers with average tenure exceeding 15 years, feared the worst. Previous Russian owners had stripped assets, deferred maintenance, and destroyed morale.

Apollo's negotiation team, led by Neeraj Kanwar, faced skepticism from every direction. The Dutch government worried about an Indian company's commitment to local employment. The works council, powerful under Dutch law, could effectively veto the deal. European competitors whispered that Indians couldn't manage a premium brand. The asking price of €140 million seemed reasonable, but hidden liabilities lurked—pension obligations, environmental compliance, supplier contracts.

The breakthrough came through cultural sensitivity. Unlike typical M&A where acquirers impose their culture, Apollo approached Vredestein as students. Neeraj Kanwar spent weeks in Enschede, not in boardrooms but on the shop floor, learning about Dutch work culture, understanding the pride workers felt in their craft. When addressing the works council, he didn't present PowerPoints about synergies; he talked about preserving Vredestein's heritage while providing growth capital it desperately needed.

Apollo made three critical commitments that sealed the deal: maintaining Vredestein as an independent brand (not rebranding as Apollo Europe), keeping the Enschede facility as the group's European R&D center, and guaranteeing no involuntary redundancies for five years. Competitors mocked these as expensive concessions. Apollo saw them as investments in trust.

The integration challenges were immense. Dutch workers, accustomed to flat hierarchies and consensus decision-making, clashed with Indian managers' more hierarchical approach. The first winter was brutal—Indian executives, unprepared for Dutch weather and work-life balance expectations, struggled to adapt. One senior manager later recalled arriving for a 7 PM meeting to find the office empty—in the Netherlands, work ended at 5 PM, period.

But slowly, magic happened. Apollo's cost discipline combined with Vredestein's engineering excellence created unexpected synergies. Raw material procurement, leveraging Apollo's scale, reduced costs by 15%. Vredestein's winter tyre technology, applied to Apollo's Indian portfolio, created premium products for the Himalayan market. Most importantly, Vredestein engineers, given budgets for new product development after years of starvation, unleashed pent-up innovation.

The Quatrac series exemplified this renaissance. Vredestein developed Europe's first all-season tyre specifically for high-performance vehicles—a segment others ignored, assuming performance enthusiasts would always maintain summer/winter sets. But urbanization meant many European drivers had no space to store extra tyres. Quatrac filled this gap perfectly, winning awards and gaining OEM approvals from Audi and Volkswagen.

Financially, the acquisition exceeded all projections. Vredestein added $450 million to Apollo's top line immediately. More importantly, it provided entry to European replacement markets where margins exceeded 20%, compared to 8-10% in India. The Enschede plant, operating at full capacity by 2011, generated €50 million EBITDA annually. The €140 million investment was recovered within four years.

The real victory was reputational. Apollo had done what Indian companies rarely achieved—successfully acquired and integrated a European manufacturing business. When Harvard Business School wrote a case study on the acquisition, it highlighted Apollo's patient capital approach and cultural sensitivity. This wasn't the typical emerging market acquisition story of asset stripping or job exports. Apollo had preserved and enhanced a European institution.

The Vredestein success created organizational confidence that would influence Apollo's next move. If they could acquire and run a century-old Dutch company, why not try for something bigger? Why not become a truly global player? This thinking led directly to the Cooper Tire pursuit—a deal that would test Apollo's limits and nearly destroy everything they'd built.

V. The Cooper Tire Saga: Ambition Meets Reality (2013)

June 12, 2013. Neeraj Kanwar stood before assembled media at Mumbai's Taj Hotel, announcing Apollo's most audacious move yet: acquiring Cooper Tire & Rubber Company for $2.5 billion. At $35 per share, Apollo was paying a 40% premium for America's fourth-largest tyre maker. The combined entity would become the world's seventh-largest tyre company, with $6.6 billion in sales across four continents. Indian media hailed it as the "arrival" moment for India Inc. Within hours, Apollo's stock price told a different story—down 25% in panic selling.

The strategic rationale seemed impeccable on PowerPoint. Cooper brought three things Apollo desperately wanted: entry to the US replacement market (Cooper had 20% share in light truck tyres), manufacturing presence in China through joint ventures, and relationships with American OEMs including Ford and Chrysler. Apollo brought emerging market expertise, low-cost manufacturing, and ambitions to challenge the Michelins and Bridgestones of the world.

But PowerPoints don't capture organizational reality. Cooper was a 99-year-old company headquartered in Findlay, Ohio—a town where Cooper wasn't just an employer but the employer, supporting thousands of families across generations. The United Steelworkers union, representing 2,500 Cooper workers, saw Apollo as a threat to American jobs. Cooper's Chinese joint venture partner, Chengshan Group, viewed the deal as potential betrayal—they'd partnered with an American company, not an Indian one.

The first crack appeared in August, just two months after announcement. Workers at Cooper Chengshan Tire Company's Rongcheng plant—over 5,000 of them—went on strike. They painted "Indian slaves" on factory walls, blocked shipments, and demanded the deal be scrapped. The optics were devastating: Chinese workers protesting an Indian acquisition of an American company. Global media, sensing drama, descended on Rongcheng.

The strike's real instigator was Chengshan Group, Cooper's JV partner, who feared Apollo would favor its own Chinese operations over the joint venture. Under Chinese law, Chengshan had effective veto power over ownership changes. Cooper's management, eager to close the deal and collect their golden parachutes, had somehow forgotten to mention this detail during due diligence.

Meanwhile, in America, the United Steelworkers launched their own offensive. They filed arbitration claims alleging Cooper had violated collective bargaining agreements by not consulting them before the sale. They organized protests at Cooper facilities, contacted politicians, and painted Apollo as outsourcers who would shift production to India. One union leader memorably declared: "We didn't fight World War II and Korea to hand our jobs to Indians."

Apollo's response revealed their inexperience with hostile stakeholders. Accustomed to Indian labor relations where management held stronger cards, they underestimated American union power. Their attempts at reassurance—promising to maintain US employment—were dismissed as empty rhetoric. When Apollo executives visited Findlay for town halls, they faced hostile questions about everything from Hindu dietary restrictions to India's poverty levels.

The financial engineering also unraveled. Apollo had arranged a $2.1 billion bridge loan from Deutsche Bank and Goldman Sachs, contingent on closing by year-end. As problems mounted, the banks got nervous. Cooper's third-quarter results, released in October, showed declining sales and margins—partly due to the China strike but also reflecting deeper issues Apollo's due diligence had missed. The bonds Apollo issued to fund the deal were trading at distressed levels.

By November, both sides were in Delaware Chancery Court. Cooper sued to force Apollo to close, arguing they'd manufactured problems to renegotiate price. Apollo countersued, claiming Cooper had withheld material information about China operations and union agreements. The court proceedings revealed embarrassing details: rushed due diligence, over-optimistic projections, and fundamental misunderstandings about stakeholder management.

The December denouement was swift and brutal. Apollo informed Cooper they couldn't arrange financing in time, effectively killing the deal. Cooper terminated the merger agreement and demanded a $112.5 million breakup fee. The Delaware court, in a stinging rebuke, ruled neither party had acted in good faith—Cooper had hidden problems, Apollo had gotten cold feet. No breakup fee would be paid, but reputational damage was severe.

The failure's cost went beyond the $50 million in advisory fees and legal costs Apollo had burned. Their stock price remained depressed for months. International expansion plans were put on hold. Board members questioned management judgment. One independent director reportedly asked Neeraj Kanwar: "Did we learn nothing from Tata-Corus?"—referring to another problematic Indian overseas acquisition.

But the deepest impact was psychological. Apollo had always been the scrappy underdog that succeeded through grit and patience. The Cooper failure suggested they'd become overconfident, mistaking one successful European acquisition for global M&A expertise. The organization needed to relearn humility, rebuild credibility, and find a new path to growth that didn't depend on transformative acquisitions.

In private moments, Neeraj Kanwar would later admit the Cooper failure was necessary education. "We learned that money alone doesn't buy you a company," he said. "You need stakeholder alignment, cultural compatibility, and most importantly, the wisdom to walk away when fundamentals change." These lessons would shape Apollo's next phase—less glamorous than a mega-acquisition, but ultimately more sustainable.

VI. Recovery & Renewed Focus (2014-2020)

January 2014 found Apollo Tyres in an unfamiliar position: wounded, humbled, and facing skeptical investors who questioned whether management could be trusted with capital. The Cooper debacle had cost more than money—it had shattered the aura of competence Apollo had built through the Vredestein success. The easy path would have been retrenchment: focus on India, avoid foreign adventures, become a boring but profitable regional player. Apollo chose the harder path: systematic capability building without headlines.

The first move was almost therapeutic in its modesty. In 2015, Apollo acquired Reifencom, a German tyre distributor, for €45.6 million—pocket change compared to Cooper's billions. Reifencom wasn't sexy: 350 employees, 37 retail outlets, decidedly mid-market positioning. But it gave Apollo something precious: direct access to German consumers, Europe's largest replacement market, and intimate knowledge of retail dynamics. No strikes, no unions in revolt, just quiet integration of a business Apollo actually understood.

The European headquarters shift to Amsterdam in 2015 signaled strategic evolution. The Netherlands offered tax advantages, but more importantly, it positioned Apollo as a European company with Indian roots rather than an Indian company with European operations. Subtle but significant—European customers and regulators responded better to a company headquartered in Amsterdam than Chennai.

The real jewel of this period was the Global R&D Centre in Chennai, inaugurated in 2016. This wasn't just another corporate campus with glass facades and motivational posters. Apollo recruited 200 engineers from competitors, universities, and surprisingly, India's space and defense programs. The mandate was ambitious: develop tyres not for today's vehicles but tomorrow's—electric, autonomous, shared.

The R&D investment paid dividends through unexpected innovations. Apollo's engineers, analyzing warranty claims, noticed a pattern: tyres in India failed differently than elsewhere. Indian roads' unique combination of heat, overloading, and pothole impacts created stress patterns no global manufacturer had studied. Apollo developed compounds and construction techniques specifically for these conditions. The resulting tyres lasted 20% longer than competitors'. When tested on African roads with similar conditions, they performed brilliantly—opening new export markets.

2017 brought vindication through the Hungarian factory inauguration. Prime Minister Viktor Orban himself attended, praising Apollo for bringing high-tech manufacturing to Hungary. The symbolism mattered: a European head of government celebrating an Indian investment. The facility, built for €475 million, wasn't just about capacity—it was Apollo's statement that they belonged in Europe despite the Cooper failure.

The Hungarian plant showcased Apollo's evolved approach to international expansion. Unlike older facilities transplanting Indian practices, Hungary was designed collaboratively. Dutch engineers from Vredestein led product development, Indian managers handled supply chain, Hungarian workers contributed process improvements from their experience at other manufacturers. The resulting hybrid culture produced unexpected innovation: Europe's first dedicated all-season EV tyre, developed specifically for the emerging electric vehicle market.

The two-brand strategy crystallized during this period. Rather than forcing convergence between Apollo and Vredestein, management embraced differentiation. Apollo became the value warrior—reliable, affordable, optimized for harsh conditions. Vredestein pursued premium positioning—innovative, sustainable, designed for discerning consumers. Dealerships carried both, offering choice across price points. Critics called it brand confusion; Apollo called it portfolio optimization.

The 2018 entry into three-wheelers seems pedestrian but reveals strategic sophistication. Three-wheelers—autorickshaws, delivery vehicles, shared mobility solutions—were exploding across Asia, Africa, and Latin America. No global major took the segment seriously. Apollo developed specialized tyres handling three-wheelers' unique dynamics: asymmetric loading, constant turning, stop-start operation. Within eighteen months, they commanded 35% market share in India and were exporting to 15 countries.

Technology partnerships accelerated without fanfare. Apollo partnered with IIT Madras for material science research, with Dutch universities for sustainable rubber alternatives, with German firms for Industry 4.0 manufacturing. These weren't headline-grabbing alliances but systematic capability building. Each partnership addressed specific weaknesses identified during the Cooper post-mortem.

COVID-19 should have derailed everything. The March 2020 lockdown shut Indian plants completely. European facilities operated at minimal capacity. Demand collapsed as vehicles stayed parked. Yet Apollo's response demonstrated organizational maturity. Within weeks, they'd reconfigured supply chains, implemented safety protocols that became industry benchmarks, and pivoted production toward essential vehicle segments still operating.

The pandemic also accelerated digital transformation. Apollo launched virtual dealership tools, allowing customers to research, purchase, and schedule installation online. They developed predictive maintenance apps using smartphone sensors to assess tyre wear. These weren't revolutionary innovations, but they showed Apollo could adapt quickly—a capability that would prove crucial as the industry faced its next disruption: electrification.

By late 2020, Apollo had quietly rebuilt stronger than before. Revenue exceeded pre-Cooper levels. Margins improved through operational excellence rather than price increases. The organization had developed muscle memory for international operations without betting the company on single deals. Most importantly, they'd learned to execute without external validation—no magazine covers, no breathless media coverage, just consistent quarterly improvements.

VII. Modern Era: Scale, Challenges & Future Bets (2020-Present)

The year 2020 opened with Apollo Tyres at a crossroads. The pre-COVID business plan called for aggressive capacity expansion, digital transformation, and preparing for electric vehicle disruption. Within weeks, everything changed. The pandemic lockdowns didn't just disrupt operations—they revealed both vulnerabilities and strengths Apollo hadn't fully appreciated. What emerged from this crisis would define whether Apollo remained a solid regional player or evolved into something more ambitious.

The current footprint tells a story of methodical expansion: five manufacturing units across India (Perambra, Limda, Chennai, Kalamassery, and the new Andhra Pradesh facility), plus Enschede in the Netherlands and the Hungarian plant. The company now has five manufacturing units in India, one in the Netherlands and one in Hungary. The company generates 69% of its revenues from India, 26% from Europe and 5% from other countries. This geographic mix, heavily weighted toward India, reflects both opportunity and constraint—domestic dominance funding international ambitions.

The Andhra Pradesh facility, inaugurated in 2020, exemplifies Apollo's evolved approach to capacity expansion. On 9 January 2018, the Chief Minister of Andhra Pradesh, N Chandrababu Naidu laid the foundation stone for Apollo Tyres' ₹1,800-crore tyre factory in Andhra Pradesh. But the real investment ballooned further: The company will invest close to Rs 3800 crores in the Phase I of this greenfield facility. The plant, designed for an initial capacity of 55 lakh (5.5 million) tyres per year, wasn't just about adding capacity—it showcased Apollo's manufacturing philosophy evolution.

The facility employed modular design, allowing capacity replication without extensive re-engineering. Sustainability features included solar power generation and zero water discharge systems. More importantly, it was designed for flexibility—able to switch between passenger car and truck-bus radial production based on demand. By 2022, the plant targeted daily production of 15,000 passenger car tyres and 3,000 truck-bus radials, representing Apollo's bet on continued motorization in India.

But 2022 brought a different kind of challenge that tested Apollo's corporate governance. In April 2022, the Competition Commission of India raided the headquarters of Apollo Tyres along with other tyre companies like CEAT, MRF (Madras Rubber Factory) and Continental Tyre at multiple locations. Earlier in February the anti trust watch dog had released a statement about fining these tyre companies a total of ₹1,788 crores (of which Apollo Tyres fined ₹425.53 cr.) for sharing price sensitive information among themselves to manage their cartelization of tyre prices.

The cartelization case traced back to 2011-2012, when tyre manufacturers allegedly coordinated pricing through their industry association, ATMA. A penalty of Rs 425.53 crore was levied on Apollo Tyres alongside similar fines for competitors. The allegations centered on exchanging price-sensitive data and collectively deciding on tyre prices, particularly for commercial vehicle segments. While Apollo contested the charges, the episode highlighted the fine line between legitimate industry cooperation and anti-competitive behavior.

The financial impact went beyond the monetary penalty. Investor confidence wobbled, regulatory scrutiny intensified, and Apollo faced reputational damage in a market where trust matters. Management's response was telling—rather than prolonged legal battles, they provisioned for the penalty, strengthened compliance mechanisms, and refocused on operational excellence. The message was clear: Apollo would take its lumps and move forward.

The EV transition presents Apollo's most complex challenge yet. Electric vehicles stress tyres differently—instant torque creates different wear patterns, heavier battery weights require stronger construction, and the silence of electric motors makes tyre noise more noticeable. Apollo's response has been methodical rather than revolutionary. The Hungarian facility, working with Vredestein's Dutch engineers, developed Europe's first dedicated all-season EV tyre—not a modified conventional tyre but ground-up design for electric vehicles.

In India, Apollo faces a different EV challenge. The market is transitioning through two-wheelers and three-wheelers first, not passenger cars. Apollo's early entry into electric three-wheeler tyres, leveraging their 2018 market entry, positions them well. But the real test comes as Indian passenger car makers launch affordable EVs. Can Apollo develop cost-effective EV tyres for a price-sensitive market while maintaining margins?

Competition has intensified across all fronts. MRF remains the domestic leader with superior margins and brand power. CEAT has aggressively expanded in two-wheelers and passenger segments. International players like Bridgestone and Continental bring global scale and technology. Chinese manufacturers lurk at the edges, offering rock-bottom prices. Apollo's response has been to avoid direct confrontation—instead finding niches where their specific capabilities create advantage.

The recent financial performance reflects these crosscurrents. Apollo Tyres Ltd's revenue jumped 1.88% since last year same period to ₹6,451.42Cr in the Q4 2024-2025. Apollo Tyres Ltd's net profit fell -47.86% since last year same period to ₹184.62Cr in the Q4 2024-2025. The margin compression—profit declining despite revenue growth—tells a story of input cost pressures, competitive intensity, and investment requirements overwhelming pricing power.

Management acknowledged the challenges with unusual candor. Onkar Kanwar, Chairman, Apollo Tyres Ltd said "We acknowledge that our performance over the past few quarters has not met industry benchmarks and our own expectations. After a thorough internal review, we have identified the key challenges that contributed to this underperformance." This admission, rare for Indian companies, suggests Apollo recognizes the need for strategic recalibration rather than cosmetic fixes.

The dual-brand strategy continues evolving. Apollo brand focuses on value and durability—tyres for Indian trucks navigating potholed highways, African buses on dirt roads, Southeast Asian motorcycles in tropical heat. Vredestein pursues premium positioning in Europe—high-performance tyres for German autobahns, winter tyres for Scandinavian conditions, all-season tyres for urban European drivers. The challenge is maintaining this differentiation while achieving manufacturing synergies.

Technology investments have accelerated but remain measured. Apollo's Chennai R&D center, upgraded in 2016, employs 200 engineers but that's modest compared to global leaders' thousands. The focus is practical innovation—compounds for Indian conditions, construction techniques for overloaded vehicles, tread patterns for monsoon driving. Not breakthrough research but applied engineering that solves real problems.

Looking ahead, Apollo faces fundamental questions. Can they maintain domestic market share as Chinese players inevitably enter India more aggressively? Will the Vredestein brand achieve sufficient scale in Europe to justify continued investment? How quickly must they pivot to EV-specific products? Should they attempt another transformative acquisition or focus on organic growth? These aren't just strategic choices but existential questions about Apollo's identity—regional champion or global player, value competitor or technology leader, family business or professional corporation.

VIII. Business Model & Unit Economics

Understanding Apollo's business model requires grasping a fundamental tension: tyre manufacturing is simultaneously a commodity business (rubber goes in, round things come out) and a technology business (complex chemistry, precision engineering, brand differentiation). Apollo's unit economics reflect this duality—commodity-like input cost pressures combined with technology-driven pricing power in select segments.

Raw materials dominate the cost structure, typically accounting for 65-70% of revenues. Natural rubber leads the list, sourced primarily from Kerala and Tamil Nadu domestically, supplemented by imports from Thailand and Indonesia. The price volatility is staggering—rubber can swing 40% in a year based on weather, currency, and speculation. Apollo's procurement team operates like commodity traders, taking positions, hedging currencies, maintaining strategic inventory. A 10% rise in rubber prices can evaporate margins if not managed properly.

Carbon black, the second major input, comes from petroleum derivatives, linking Apollo's fortunes to oil prices. Steel wire for radial tyres adds another volatile element. The company maintains 60-90 days of raw material inventory—enough to smooth short-term spikes but not enough to avoid sustained input inflation. This working capital intensity means Apollo typically has ₹3,000-4,000 crore locked in inventory at any time.

The replacement versus OEM (Original Equipment Manufacturer) split shapes everything. Replacement markets—consumers buying tyres when old ones wear out—account for 70% of Apollo's Indian revenues. These sales carry 35-40% gross margins, as consumers pay retail prices and Apollo captures distribution margins. OEM sales to vehicle manufacturers generate volumes but at 20-25% gross margins, as automakers squeeze suppliers relentlessly.

The replacement market dynamics are fascinating. A truck operator in Gujarat doesn't buy Apollo tyres; he buys from Jayesh who runs the local tyre shop, who he's known for fifteen years, who extends 45-day credit during tough times. Jayesh stocks Apollo because the company's sales representative visits weekly, provides promotional materials, handles warranty claims efficiently. This human network, built over decades, is Apollo's real moat—impossible for new entrants to replicate quickly.

Distribution economics reveal the challenge. Apollo maintains relationships with 5,000+ dealers across India, but concentration is severe—the top 200 dealers generate 40% of sales. These large dealers demand higher margins, better credit terms, exclusive territories. Smaller dealers need hand-holding, inventory financing, sometimes even help with shop renovation. The cost of maintaining this network—sales force, logistics, credit management—consumes 8-10% of revenues.

The brand architecture strategy (Apollo for value, Vredestein for premium) creates distinct unit economics. Apollo-branded truck tyres in India might wholesale for ₹8,000, generating ₹2,400 gross profit, ₹800 EBITDA after allocating operating costs. A Vredestein high-performance tyre in Netherlands might retail for €200, with €80 gross profit, €30 EBITDA after higher European operating costs. The margin percentages look similar, but Vredestein's lower volumes mean fixed cost absorption challenges.

R&D investment economics deserve scrutiny. Apollo spends 1.5-2% of revenues on R&D—₹400-500 crore annually. This seems modest compared to Michelin's 3-4%, but the comparison is misleading. Apollo focuses on application engineering (adapting existing technology to local conditions) rather than fundamental research. Developing a new compound for Indian summer conditions might cost ₹10 crore; developing revolutionary airless tyres would cost billions. Apollo rationally chooses battles it can win.

Manufacturing economics have improved dramatically through operational excellence. The Chennai plant, Apollo's most modern, achieves 85% OEE (Overall Equipment Effectiveness), approaching global benchmarks. Automation has reduced direct labor to 8% of costs from 15% a decade ago. Energy costs, managed through captive power generation and efficiency improvements, have dropped to 4% of revenues from 6%. These incremental gains compound—a 1% improvement in manufacturing efficiency adds ₹250 crore to EBITDA.

Working capital management remains challenging. The business requires 90-100 days of working capital—inventory plus receivables minus payables. In a ₹25,000 crore revenue business, that's ₹7,000 crore of capital locked up. Apollo has gradually improved, reducing working capital days from 110 in 2015 to 95 currently, freeing up ₹1,000 crore for investment. But further improvement requires either squeezing suppliers (risky given raw material criticality) or dealers (dangerous given distribution importance).

Currency dynamics add complexity. Apollo earns 26% of revenues in euros but incurs most costs in rupees. A 10% rupee depreciation should theoretically boost profitability, but reality is messier. European revenues might increase in rupee terms, but imported raw materials also become expensive. The company maintains a natural hedge—European operations' local costs offset some currency risk—but volatility remains a constant companion.

The export strategy from India reveals interesting economics. Apollo exports 20% of domestic production, primarily to Africa, Middle East, and Southeast Asia. These markets pay 10-15% premiums over domestic prices for the same products—reflecting Apollo's brand strength in emerging markets versus India. But export logistics add cost, payment risks increase (especially in Africa), and currency volatility can erode margins. Still, exports provide valuable capacity utilization during domestic downturns.

Technology disruption threats loom over traditional economics. Retreading (replacing just the tread, not entire tyre) could reduce replacement demand by 30% if widely adopted. Tyre pressure monitoring systems, mandatory in new cars, extend tyre life by preventing under-inflation damage. Ride-sharing reduces per-capita vehicle usage. Electric vehicles' regenerative braking reduces tyre wear. Each innovation chips away at replacement demand—the industry's profit pool.

Capital allocation reveals management priorities. Apollo generates ₹2,500-3,000 crore operating cash flow annually. Maintenance capex consumes ₹800-1,000 crore. Growth investments (new capacity, technology) take another ₹1,000-1,500 crore. Debt service requires ₹400-500 crore. What remains—₹500-800 crore—goes to dividends, maintaining the family's 37% stake value while keeping public shareholders engaged. It's a delicate balance—invest enough to remain competitive but return enough to maintain market confidence.

The unit economics bottom line: Apollo operates a decent but not spectacular business model. Returns on capital employed hover around 12-15%, respectable but not exceptional. EBITDA margins of 13-17% trail global leaders' 20%+ but exceed most emerging market peers. The business generates cash reliably but requires constant reinvestment. It's a marathon, not a sprint—steady compounding rather than explosive growth.

IX. Playbook: Lessons from Apollo's Journey

Apollo's five-decade journey from a Kerala truck tyre maker to a global manufacturer offers rich lessons for emerging market companies harboring international ambitions. These aren't theoretical frameworks but battle-tested principles, learned through spectacular failures as much as quiet successes. Understanding Apollo's playbook means recognizing that building a global manufacturing champion from India requires different rules than those followed by Silicon Valley unicorns or Wall Street darlings.

Building in Emerging Markets: The India Advantage

Apollo's first lesson seems counterintuitive: starting in a difficult market creates strengths that easy markets never develop. Indian conditions—overloaded trucks, extreme temperatures, terrible roads, price-sensitive customers—forced Apollo to over-engineer products. A tyre surviving Mumbai-Kolkata highways handles European autobahns easily. This "stress-testing by default" created products that found ready markets across similar conditions in Africa, Southeast Asia, and Latin America.

The cost discipline enforced by Indian consumers became a global competitive advantage. When your home market haggles over ₹100 differences, you learn efficiency at a molecular level. Apollo's Indian operations achieve similar quality to European competitors at 60% of the cost structure. This isn't about cheap labor—automation has minimized that advantage. It's about frugal engineering, eliminating non-essential features, optimizing every process.

M&A Lessons: When to Push Through vs When to Walk

The Vredestein and Cooper experiences offer a masterclass in acquisition strategy. Vredestein succeeded because Apollo approached it with humility—preserving the brand, respecting the culture, investing in growth. They paid €140 million for a distressed asset and created €500 million in value through patient capital and operational improvement. The lesson: buy stressed assets with strong fundamentals, not dying businesses hoping for miracles.

Cooper failed because Apollo mistook size for strategy. The $2.5 billion price tag would have transformed Apollo overnight into a global player, but transformation isn't just about scale. The deal's complexity—multiple stakeholders, cultural chasms, hidden liabilities—exceeded Apollo's integration capabilities. Walking away, though painful and embarrassing, prevented a potentially fatal error. The lesson: know your limitations and respect them.

Managing a Dual-Brand Strategy

Apollo and Vredestein represent different promises to different customers, and maintaining this differentiation requires constant discipline. The temptation to leverage Vredestein's premium positioning to raise Apollo prices, or use Apollo's volumes to reduce Vredestein costs, must be resisted. Each brand needs its own identity, team, and economics. Shared infrastructure creates cost synergies, but shared branding creates confusion.

The geographic separation helps—Vredestein for Europe, Apollo for emerging markets—but isn't sufficient. The real differentiation comes through capability allocation. Vredestein gets first access to new technology, premium compounds, sophisticated designs. Apollo focuses on durability, value, practical innovation. It's not about superior versus inferior, but appropriate versus mismatched.

Family Ownership and Long-Term Thinking

The Kanwar family's 37% stake shapes everything. Unlike professional managers focused on quarterly earnings, family owners think in generations. This enabled Apollo to invest in the Andhra Pradesh plant during COVID, maintain R&D spending during downturns, and preserve employment during crises. The market sometimes punishes this long-term orientation through lower valuations, but it creates organizational stability that pure shareholder capitalism rarely achieves.

Family ownership also brings challenges—succession planning, professional management integration, governance standards. Apollo has navigated these by gradually professionalizing while maintaining family control. Independent directors provide oversight, professional CEOs run operations, but strategic decisions remain with the family. It's a delicate balance that many family businesses fail to achieve.

Competing with Global Giants as a Regional Champion

Apollo can't match Michelin's R&D budget or Bridgestone's global scale. Instead, they compete through focus and agility. While global giants optimize for developed markets, Apollo designs for emerging economy realities. While multinationals navigate complex matrix organizations, Apollo's decision-making remains relatively simple and fast. While global brands pursue premium positioning, Apollo owns the value-conscious majority.

The strategy isn't to beat global giants at their own game but to change the game's rules. In India, Apollo's distribution network and brand trust matter more than technological superiority. In Africa, ability to provide credit and local service trumps product sophistication. In Europe, Vredestein's heritage and focus create niches that global players ignore.

Manufacturing Excellence and Cost Leadership

Apollo's manufacturing philosophy emphasizes consistent improvement over breakthrough innovation. Each year, every plant must reduce costs by 3-5% through efficiency gains. This sounds modest, but compounded over decades, it's transformative. The Chennai plant today produces tyres at one-third the inflation-adjusted cost of the 1990s Perambra facility.

The approach is distinctly Indian: jugaad (frugal innovation) combined with Japanese-inspired quality systems. Workers are encouraged to suggest improvements, no matter how small. A shop-floor worker's idea to reorient storage racks saved ₹2 crore annually in material handling. Hundreds of such improvements, accumulated over years, create sustainable cost advantages that financial engineering never could.

The Value of Patience in International Expansion

Apollo's international journey spans three decades—from the 1991 South African subsidiary to today's European operations. Each step was measured, lessons absorbed before the next move. The South African venture taught currency risk management. Early exports revealed quality gaps. Vredestein provided European market understanding. Even the Cooper failure taught valuable lessons about stakeholder management.

This patience frustrates investors wanting dramatic growth, but it prevents dramatic failures. Apollo could have expanded internationally faster through aggressive acquisitions or greenfield investments. Instead, they built capabilities methodically, ensuring each international move was sustainable. The result: steady international growth without betting the company on any single expansion.

Innovation Through Constraints

Apollo's R&D philosophy embraces constraints rather than fighting them. Limited budgets force focus on practical problems. Indian market conditions demand robust, simple solutions. Price-sensitive customers prevent over-engineering. These constraints, initially seen as disadvantages, became innovation catalysts.

The best example is Apollo's truck radial development. Lacking resources for fundamental research, engineers focused on adapting existing technology to Indian conditions. The resulting tyres weren't technologically advanced but perfectly suited to market needs. This "appropriate innovation" philosophy now drives development across all markets—solving real problems rather than pursuing theoretical advances.

Stakeholder Capitalism Before It Was Fashionable

Long before ESG became corporate fashion, Apollo practiced stakeholder balance from necessity. In Kerala's militant union environment, worker partnership was survival. In small-town India, community support enabled operations. With 5,000 dealers dependent on Apollo's success, their interests couldn't be ignored. This forced multi-stakeholder orientation, initially seen as burden, became a strength.

When COVID hit, Apollo's stakeholder relationships paid dividends. Workers accepted temporary pay cuts knowing management would reciprocate when conditions improved. Dealers extended credit to struggling customers, knowing Apollo would support them. Communities around plants provided labor and logistics support during lockdowns. These relationships, built over decades, can't be bought during crises.

X. Bear vs Bull Case

Bear Case: The Structural Headwinds

The bear case against Apollo starts with Chinese competition—not potential but inevitable. Chinese tyre manufacturers have conquered global steel, solar, and electronics markets through a familiar playbook: massive scale, government support, and predatory pricing. They're now targeting tyres. Companies like Linglong and Sailun already export aggressively to Apollo's key markets in Africa and Southeast Asia. When they inevitably enter India seriously (perhaps through local manufacturing to avoid duties), Apollo's value positioning becomes vulnerable. How do you compete on price with companies that treat profit as optional?

Raw material volatility presents another structural challenge. Natural rubber, petroleum derivatives, and steel comprise 70% of costs, and Apollo controls none of these inputs. Climate change makes rubber supply increasingly unpredictable—Thailand's droughts, Kerala's floods, disease outbreaks. Oil price shocks transmit directly to carbon black costs. Steel tariffs and supply chain disruptions add further uncertainty. Operating margins can swing 500 basis points based on input costs alone, making earnings inherently unpredictable.

The EV transition threatens Apollo's core competencies. Electric vehicles stress tyres differently—instant torque, heavier weights, different wear patterns. But more fundamentally, EVs require fewer tyre replacements due to regenerative braking and sophisticated traction control. If replacement demand drops 20-30% as EVs proliferate, the entire industry's economics unravel. Apollo's limited R&D resources mean they're followers, not leaders, in EV tyre development.

Apollo's premium ambitions through Vredestein face structural impediments. European consumers, despite Vredestein's heritage, still perceive it as second-tier to Michelin or Continental. Breaking this perception requires massive marketing investment that Apollo cannot afford. Meanwhile, Vredestein's 5.5 million unit capacity subscale compared to competitors' tens of millions means higher unit costs. It's a Catch-22: need scale to compete but need success to achieve scale.

Regulatory challenges multiply across jurisdictions. The anti trust watch dog had released a statement about fining these tyre companies a total of ₹1,788 crores (of which Apollo Tyres fined ₹425.53 cr.) for alleged cartelization. Environmental regulations require expensive upgrades—European carbon taxes, Indian pollution controls, waste management requirements. Safety standards constantly evolve, requiring new testing, certification, and sometimes redesign. Each regulation adds cost without adding customer value.

The balance sheet, while manageable, constrains strategic flexibility. Net debt around ₹6,000 crore isn't alarming, but it limits Apollo's ability to make transformative investments. Interest coverage ratios of 4-5x provide cushion but not comfort. Any major acquisition or capacity expansion requires either equity dilution (which the family resists) or increased leverage (which rating agencies punish). Apollo is stuck in the middle—too leveraged for aggressive expansion, too subscale for global competition.

Bull Case: The Underappreciated Strengths

The bull case begins with India's unstoppable motorization. Despite recent slowdowns, India adds 20 million vehicles annually to its roads. The commercial vehicle segment, Apollo's stronghold, benefits from infrastructure development, GST-driven logistics efficiency, and e-commerce growth. Every kilometer of new highway, every Amazon warehouse, every Flipkart delivery creates tyre demand. With 28-29% market share in truck/bus segments, Apollo captures this growth disproportionately.

Infrastructure development multiplies tyre demand beyond simple vehicle growth. The government's ₹100 trillion infrastructure pipeline means more construction equipment, more material transport, more wear on existing tyres from rough construction-zone roads. The dedicated freight corridors will increase truck utilization rates. Port modernization drives container movement. Each infrastructure project cascades into replacement tyre demand where Apollo dominates.

Vredestein's European position, despite challenges, shows genuine promise. European Operations revenue also grew in single digits, but profitability improves as the brand gains traction. The all-season tyre segment, where Vredestein innovated early, grows 15% annually as urbanization makes seasonal tyre changes impractical. Electric vehicle adoption in Europe creates opportunities for specialized tyres where established players haven't yet dominated. Vredestein's ₹6,500 crore revenue might seem subscale, but it's a profitable, growing base for expansion.

Apollo's manufacturing cost advantages endure despite automation reducing labor's importance. Energy costs through captive generation, land costs from early investments, and engineering talent at Indian prices create structural advantages. The Chennai plant produces radial tyres at 60% of European costs with comparable quality. This cost gap won't close quickly—European environmental regulations and labor protections ensure that.

The distribution moat in India remains unassailable. Those 5,000 dealers, relationships built over decades, cannot be replicated quickly regardless of capital available. Chinese competitors entering India would need years to build similar networks. Meanwhile, Apollo leverages this distribution for adjacent products—batteries, lubricants, accessories—creating additional revenue streams with minimal incremental investment.

Brand loyalty in commercial segments is underappreciated by financial markets obsessed with passenger vehicles. A fleet operator who's used Apollo tyres for twenty years doesn't switch for 5% savings—reliability, service, warranty support matter more. This installed base creates recurring revenue streams far more predictable than passenger replacement markets. As Indian trucking consolidates into larger fleets, Apollo's B2B relationships become even more valuable.

The technology transition, while challenging, isn't existential. EVs need tyres, perhaps different ones, but tyres nonetheless. Apollo's practical innovation approach—solving real problems rather than pursuing breakthrough technology—positions them well for evolutionary change. They don't need to invent airless tyres; they need to adapt existing technology to new requirements. Their engineers have done this repeatedly—from bias to radial, from tube to tubeless.

Geographic diversification provides resilience. When Indian demand slowed during demonetization, Europe compensated. When European markets struggled during the sovereign debt crisis, India carried growth. Africa and Southeast Asia provide additional buffers. This diversification, painstakingly built over decades, smooths earnings volatility that purely domestic players face.

The Balanced View

Neither bears nor bulls have a monopoly on truth. Apollo faces real challenges—Chinese competition, raw material volatility, technology transitions—that could constrain growth and compress margins. But they also possess genuine strengths—market position, distribution networks, cost advantages—that provide defensive moats and growth opportunities.

The most likely scenario isn't dramatic success or failure but continued steady progress. Apollo will probably maintain 25-30% domestic market share, slowly grow European revenues, and generate 12-15% returns on capital. Not exciting enough for growth investors, too cyclical for value investors, but perfectly adequate for long-term holders who understand the business.

The key variables to watch aren't the obvious ones (quarterly earnings, raw material prices) but structural shifts: pace of EV adoption, Chinese manufacturing investment in India, success of Vredestein's premium positioning, and management's capital allocation choices. These determine whether Apollo remains a regional champion generating steady returns or transforms into something more ambitious.

XI. Epilogue: What Would We Do?

Standing in Apollo's boardroom today, facing the complexities of global tyre markets, technological disruption, and emerging competition, what strategic choices would maximize long-term value? This isn't armchair theorizing but practical decision-making with real constraints—limited capital, family ownership dynamics, organizational capabilities, and market realities.

The EV Tyre Opportunity

First priority: own the Indian EV tyre market before it properly exists. India's EV adoption will follow a different path than developed markets—two-wheelers and three-wheelers first, then small passenger cars, commercial vehicles last. Apollo should develop India-specific EV tyres now, not adapted global products but ground-up designs for Indian conditions, price points, and use cases.

Investment required: ₹500 crore over three years for R&D, testing facilities, and production line modifications. Partner with Indian EV manufacturers (Ola, Ather, Mahindra) for co-development, sharing costs and ensuring product-market fit. The goal isn't technological leadership but first-mover advantage in a market global players will ignore until it's too large to dismiss.

Geographic Expansion Priorities

Forget the US and China—too competitive, too expensive to enter meaningfully. Instead, double down on markets that mirror India's development trajectory: Indonesia, Vietnam, Nigeria, Egypt. These markets value Apollo's strengths (value pricing, durability, local service) over weaknesses (limited technology, brand perception).

Expansion model: local assembly rather than full manufacturing, using imported components from Indian plants. This minimizes capital investment while avoiding import duties. Partner with local distributors who provide market knowledge and working capital. Target $1 billion additional revenues from these markets within five years—achievable given their growth rates and Apollo's proven emerging market capabilities.

Premium vs Value Segment Focus

Accept reality: Apollo will never be a global premium brand. Vredestein can be a solid European regional premium player but won't challenge Michelin globally. Instead of fighting unwinnable battles, optimize current positioning. Vredestein focuses on specific European niches (all-season, electric, vintage cars) where heritage and specialization matter more than scale.

In India, create a new brand positioned between Apollo and Vredestein—call it "Apollo Select" or similar. Price 20% above regular Apollo, targeting India's growing affluent class who want better than budget but won't pay Michelin prices. Use Vredestein technology adapted for Indian conditions. This segment, currently underserved, could generate ₹2,000 crore annually with minimal cannibalization.

Technology Partnerships and Innovation Strategy

Stop trying to compete with global R&D budgets. Instead, become the world's best at adapting and implementing existing technology for emerging markets. Partner with universities and startups for specific innovations—IIT Madras for materials science, Dutch institutions for sustainability, Israeli companies for sensors and IoT.

Create an innovation fund of ₹100 crore annually for minority stakes in tyre-adjacent technologies—retreading equipment, tyre recycling, predictive maintenance software. These investments provide strategic insights and potential acquisition targets without massive R&D spending. Think venture capital approach rather than traditional corporate R&D.

Capital Allocation Between Growth and Dividends

The family's 37% stake needs dividend income, but growth requires investment. Solution: a formulaic approach that provides predictability. Commit to: 40% of normalized earnings as dividends (ensuring family liquidity), 40% for growth capex (maintaining competitiveness), 20% for debt reduction or opportunistic investments.

This formula, clearly communicated, would improve market valuation through predictability while maintaining strategic flexibility. Special dividends during windfall years, suspended dividends during crises, but always returning to the formula. Investors value predictability almost as much as growth.

The Next Big Acquisition Target?

Avoid transformational acquisitions—Cooper taught that lesson expensively. Instead, pursue bolt-on acquisitions that add specific capabilities or market access. Ideal targets: a Southeast Asian manufacturer for local presence ($200-300 million), a European retreading company for circular economy credentials ($50-100 million), or an Indian specialty tyre maker for adjacent segments ($100-200 million).

The key: never pay more than 1x revenue or 8x EBITDA, walk away if bidding escalates, and ensure cultural fit matters as much as strategic fit. Better to miss opportunities than overpay for illusions.

Organizational Transformation

Apollo needs different capabilities for future success. Hire talent from adjacent industries—automotive electronics for sensor integration, software for digital services, sustainability experts for circular economy initiatives. Create a separate digital division, physically and culturally distinct from traditional operations, tasked with developing new business models.

Implement reverse mentoring—young employees teaching senior management about digital trends, sustainability expectations, and changing consumer behavior. The organization's median age of 45 needs fresh thinking without discarding institutional knowledge.

The Sustainability Imperative

Environmental concerns will reshape the tyre industry. Get ahead by becoming India's first carbon-neutral tyre manufacturer by 2030. Sounds ambitious, but achievable through renewable energy (solar at Indian plants), sustainable materials (natural rubber from certified plantations), and circular economy initiatives (retreading, recycling).

Investment required: ₹1,000 crore over seven years. The return isn't just environmental credentials but cost savings (renewable energy cheaper long-term), regulatory compliance (avoiding future carbon taxes), and brand differentiation (especially in Europe). Sustainability isn't corporate charity but strategic positioning.

Managing the Cycle

Tyre demand is cyclical, but Apollo's response needn't be. Create a countercyclical investment fund, accumulating cash during good times for deployment during downturns. When competitors retreat during recessions, Apollo advances—acquiring distressed assets, hiring talent, gaining market share. This requires discipline to resist dividend pressures during accumulation phases.

The Ten-Year Vision

By 2035, Apollo should be: the undisputed leader in Indian commercial vehicle tyres (35% market share), a meaningful player in Indian passenger vehicles (25% share), the preferred tyre brand across emerging Asia and Africa ($2 billion revenues), and a sustainable manufacturer with circular economy leadership.

This isn't about becoming Michelin or Bridgestone—that ship has sailed. It's about owning specific positions where Apollo's capabilities create genuine competitive advantage. The aspiration isn't to be the biggest but the best at what they choose to do.

The Ultimate Question

Should the Kanwar family consider strategic alternatives—merger, sale, or transformational partnership? The honest answer: not yet. Apollo has unfinished business in India and emerging markets. Selling now would transfer value creation to acquirers. But in 5-7 years, if execution delivers, strategic options multiply. A merger of equals with another emerging market champion, a partnership with a Chinese giant for technology access, or even a sale to global major at premium valuations—all become possible.

The key is maintaining optionality while building value. Every decision should enhance strategic flexibility rather than constraining it. That's the ultimate lesson from Apollo's journey: in uncertain markets with technological disruption and emerging competition, adaptability matters more than any single strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube