APAR Industries: The Infrastructure Enabler Story

I. Introduction & Episode Roadmap

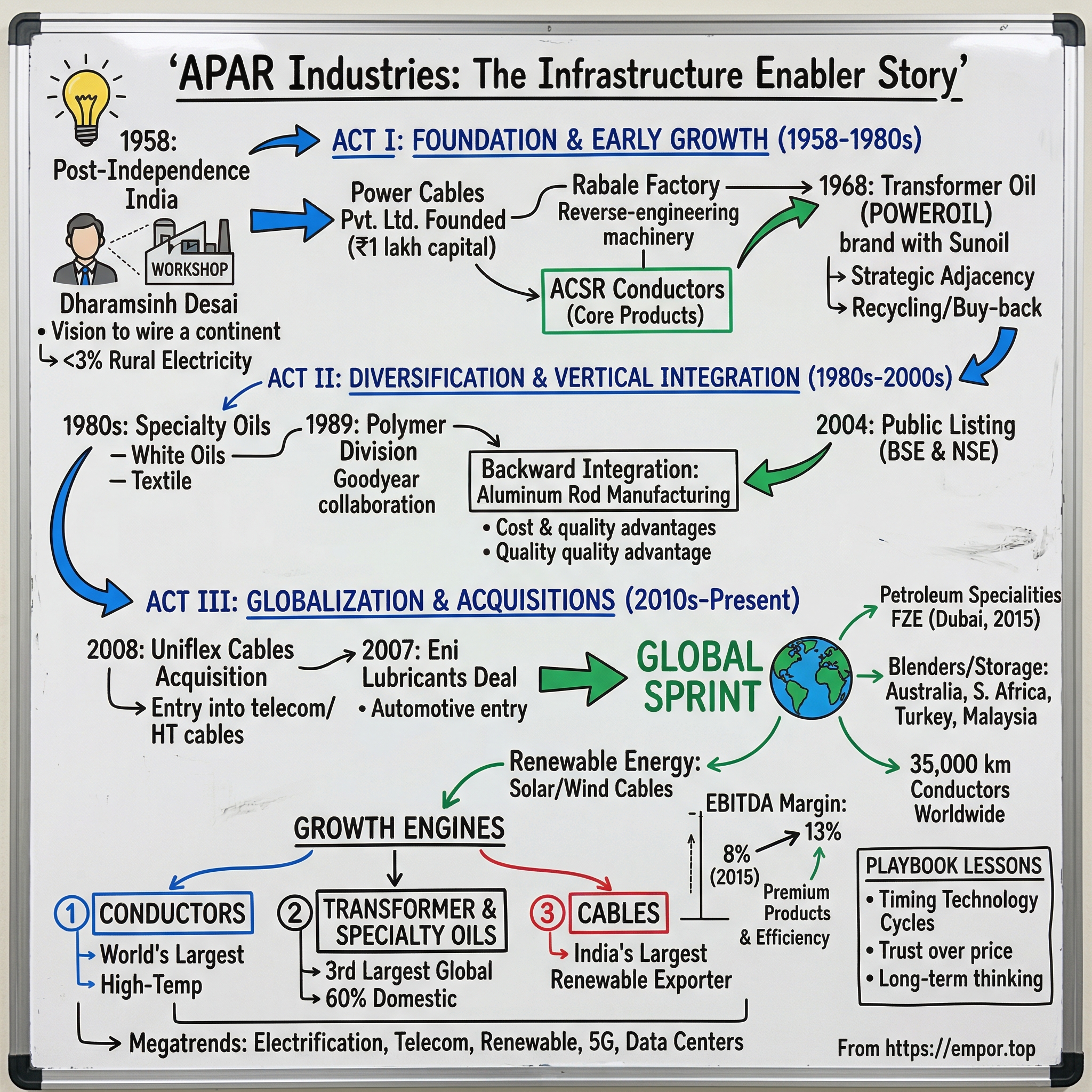

Picture this: It's 1958, barely a decade after India's independence. The nation is dark—literally. Less than 3% of rural India has electricity. Power lines are a luxury, transformers a rarity. In this landscape of scarcity and opportunity, a 37-year-old entrepreneur named Dharamsinh Desai walks into a small workshop in Mumbai with less than ₹1 lakh in capital and a vision that seems almost absurd: to wire a continent.

Fast forward to 2024. That modest workshop has morphed into APAR Industries—a ₹35,404 crore behemoth that commands the global infrastructure stage. The company that started making basic power cables now manufactures the arteries of modern civilization: the conductors that carry electricity across 140 countries, the oils that keep transformers humming from Australia to Africa, the specialized cables powering India's renewable revolution. They're the world's largest manufacturer of aluminium and alloy conductors. The third-largest transformer oil producer globally. When Australia needed 35,000 kilometers of conductors for its grid modernization, they called APAR. When India's telecom towers needed to handle 5G, APAR was there.

But here's what makes this story fascinating for students of business: APAR didn't just ride India's growth wave—it helped create it. This is a company that understood, decades before it became fashionable, that infrastructure isn't just about building things. It's about building ecosystems, capabilities, and most importantly, trust. In an industry where your customers are governments and utilities, where project failures can black out cities, where product lifecycles span decades, APAR figured out how to win not through disruption but through something far harder: consistent execution at scale.

The story we're about to tell spans three distinct acts. Act One: The foundation years (1958-1980s), where a politically connected entrepreneur leverages post-independence nationalism to build India's first indigenous conductor manufacturer. Act Two: The diversification playbook (1980s-2010), where APAR transforms from a single-product company to a three-engine conglomerate through strategic acquisitions and vertical integration. Act Three: The globalization sprint (2010-present), where a second-generation Wharton graduate takes a traditional Indian manufacturer and turns it into a global infrastructure powerhouse.

Three themes will recur throughout this narrative. First, the power of patient capital—how the Desai family's willingness to reinvest for decades created compounding advantages. Second, the art of riding megatrends—from electrification to telecom to renewable energy, APAR has an uncanny ability to position itself ahead of infrastructure cycles. Third, the paradox of boring businesses—how focusing on unsexy products like conductor wires and transformer oils can create spectacular returns.

So buckle up. This isn't just a story about wires and oils. It's about how a small Indian company figured out the infrastructure game before infrastructure became the $130 trillion opportunity McKinsey now says it is. It's about family businesses that professionalize without losing their soul. And yes, it's about understanding why, in an age of software eating the world, sometimes the companies that make the physical world work are the ones worth betting on.

II. The Post-Independence Context & Founding Vision

The year is 1947. As midnight strikes on August 15th, Jawaharlal Nehru speaks of India's "tryst with destiny." But for millions of Indians, that destiny looks pretty dark—literally. While Nehru waxes poetic about awakening to life and freedom, 99.5% of Indian villages sit in complete darkness after sunset. The British had left behind a power generation capacity of just 1,362 MW for 350 million people. To put that in perspective, a single modern data center today consumes more power than what was available to the entire subcontinent.

Into this darkness steps Dharamsinh Dadubhai Desai—a man whose life reads like a Bollywood script that no one would believe. Born in 1921 in Gujarat's Kheda district, Desai wasn't just another businessman. He was Sardar Vallabhbhai Patel's cousin, a freedom fighter who'd spent his youth in British jails, a future Member of Parliament, and crucially, someone who understood that political independence without economic infrastructure was meaningless.

Here's where the story gets interesting. In 1942, while most Indian entrepreneurs were playing it safe under British rule, Desai founded Hindustan Electric Company. Think about the audacity: starting an electrical company in colonial India, where the British controlled every aspect of heavy industry. But Desai had learned something from his cousin Patel—the Iron Man of India who'd unified 562 princely states through sheer will and strategic thinking. Infrastructure, Desai realized, wasn't just about economics. It was about sovereignty. The partnership with Brown Boveri wasn't just about technology transfer. It was Desai's masterclass in understanding how global businesses operated. He watched as HBBL became one of India's first listed companies in 1949, learned how Swiss engineering culture worked, absorbed lessons about precision manufacturing. But by 1958, Desai was restless. He'd proven he could work with foreign partners. Now he wanted to prove India could stand alone.

The timing of his exit from HBBL was no accident. In 1958, he left HBBL and founded Power Cables Pvt. Ltd., later renamed APAR Industries Limited, with capital of less than Rs. 1 lakh. To understand the audacity of this move, consider the context: India's Second Five Year Plan (1956-61) had allocated ₹960 crores for power development—the largest sectoral allocation. The government was building massive projects like Bhakra Nangal and Damodar Valley Corporation. Every dam, every power plant, every transmission line would need conductors. And Desai positioned himself to supply them all.

But here's what separated Desai from other entrepreneurs of his generation: his philosophy. A cousin of Sardar Vallabhbhai Patel, he worked closely with Patel during the independence movement. He took part in several satyagrahas during the independence movement and adopted Khadi clothing, a practice he maintained throughout his life. This wasn't performative nationalism. Desai genuinely believed in Gandhi's concept of trusteeship—that wealth was held in trust for society. This philosophy would shape APAR's culture in profound ways: long-term thinking over quick profits, employee welfare as a priority, and reinvestment over extraction.

The name itself—APAR, meaning "incomparable" in Hindi—reflected this ambition. Not just to be another cables company, but to be incomparable. In a country where most businesses were content being trading houses or license-raj beneficiaries, Desai was betting on manufacturing excellence. He wasn't just building a company; he was building capability.

Consider the competitive landscape Desai entered. The electrical equipment industry was dominated by foreign players—Siemens, GE, Alstom—who viewed India primarily as a market, not a manufacturing base. Indian companies were mostly traders or assemblers. The idea that an Indian company with less than ₹1 lakh capital could compete in precision engineering seemed laughable. The British had left behind a narrative that Indians couldn't manufacture sophisticated products. Desai set out to prove them wrong.

As chairman of the Development Council for Heavy Electrical Industries (1966–1970) under the Ministry of Industry, Desai helped establish the Electrical Research and Development Association (ERDA), which supports testing and research for India's electrical sector. This wasn't just about APAR—it was about building an ecosystem. Desai understood that for Indian manufacturing to succeed, it needed standards, testing facilities, and research capabilities. He was playing the long game.

The political connections mattered, but not in the way you might think. Desai served as a Member of Parliament for the Kaira (now Kheda) constituency in Gujarat from 1971 to 1977, but this came after APAR was already established. After independence he argued that Parliament needed greater representation from industry. His political involvement was about shaping policy, not seeking favors. He served on committees for Industrial Development, Science and Technology, Heavy Industries—the unglamorous work of building institutional capacity.

What Desai understood, perhaps better than any entrepreneur of his generation, was that infrastructure companies don't just build products—they build nations. Every kilometer of conductor APAR manufactured was a kilometer closer to universal electrification. Every transformer energized was a village lit up for the first time. This wasn't just business; it was nation-building with a profit motive.

By the end of 1958, as APAR's first manufacturing facility came online, India's installed power capacity was still under 2,300 MW. The country needed to add 100,000 MW over the next four decades. Desai had positioned APAR at the beginning of one of history's greatest infrastructure buildouts. The boy from Gujarat who'd fought for independence was now fighting a different battle—for India's industrial independence. And he was just getting started.

III. Building the Foundation: Conductors & Early Growth (1958–1980s)

The workshop floor in Rabale, Navi Mumbai, 1959. The monsoon has just ended, leaving everything damp and difficult. Dharamsinh Desai stands watching as workers wrestle with aluminum rods, trying to draw them into conductors using machinery that's part imported, part jugaad. The German technician they've hired keeps shaking his head—the humidity is all wrong, the power supply keeps fluctuating, the raw materials aren't pure enough. "This will never work," he mutters in accented English. Desai smiles. He's heard this before. The British said Indians couldn't run railways. They were wrong too.

What happened next was a masterclass in frugal innovation before anyone coined the term. APAR couldn't afford the latest European machinery, so they reverse-engineered older models. They couldn't import high-grade aluminum, so they figured out how to work with what Indian smelters could produce. When foreign consultants quoted astronomical fees, they hired retiring engineers from state electricity boards who knew exactly what Indian conditions demanded. This wasn't cutting corners—it was building for reality rather than textbook specifications.

The early product was humble: basic ACSR (Aluminium Conductor Steel Reinforced) conductors. These are the workhorses of power transmission—aluminum strands for conductivity, steel core for strength. Not sexy, but essential. Every power line needs them. And here's what Desai understood that his competitors missed: in infrastructure, boring is beautiful. You don't need to innovate constantly; you need to execute flawlessly, repeatedly, at scale.

By 1962, APAR had its first major breakthrough—a contract with Maharashtra State Electricity Board for 500 kilometers of conductors. The amount seems trivial today, but consider the context. State electricity boards were notoriously risk-averse, preferring established foreign suppliers even at premium prices. For them to trust a four-year-old Indian company was unprecedented. How did Desai pull it off? Through what would become APAR's signature move: radical transparency. He invited board engineers to the factory, showed them every process, admitted what they couldn't do yet, and committed to what they could deliver. No overselling, no under-delivery.

The 1965 India-Pakistan war changed everything. Suddenly, import licenses dried up. Foreign exchange was reserved for defense. State electricity boards that had been importing conductors were forced to look local. APAR was ready. While competitors scrambled to increase capacity, APAR had been quietly building for exactly this moment. By 1966, they were producing 5,000 metric tons annually—a 50-fold increase from their first year.

But Desai knew that depending solely on conductors was dangerous. The power sector was cyclical, government contracts were lumpy, and payment delays could stretch for months. He needed a hedge. In 1968, APAR pioneered transformer oil production in India, launching the POWEROIL brand through a collaboration with U.S.-based Sunoil. This wasn't random diversification—it was strategic adjacency. Every transformer needs oil for cooling and insulation. APAR's customers for conductors were the same utilities buying transformer oils. The sales force, the relationships, the understanding of power sector procurement—everything transferred.

The transformer oil business revealed Desai's genius for timing. India was moving from 11kV distribution to 33kV and higher voltages. Higher voltages meant larger transformers, which meant more transformer oil. A single 100 MVA transformer needs about 40,000 liters of oil. With hundreds of transformers being installed annually, the market was massive and growing. Better yet, transformer oil needs periodic replacement and testing—creating an annuity-like revenue stream that conductors couldn't provide. The 1970s brought a new challenge: the oil crisis. Petroleum prices quadrupled, making transformer oil production suddenly uneconomical. Most companies would have abandoned the business. Desai did the opposite. He negotiated directly with Indian Oil Corporation for dedicated supply agreements, invested in more efficient refining processes, and most importantly, started developing specialty grades that commanded premium prices. By 1975, APAR wasn't just making basic transformer oil—they were producing high-grade insulating oils for 400kV transformers, products that even European companies struggled to manufacture consistently.

Desai took part in several satyagrahas during the independence movement and adopted Khadi clothing, a practice he maintained throughout his life. This Gandhian philosophy manifested in how APAR treated its workers. In an era when industrial relations were adversarial—India saw 2,556 strikes in 1974 alone—APAR had zero work stoppages. The company introduced profit-sharing for workers in 1971, housing colonies in 1973, and children's education support in 1975. These weren't CSR initiatives (that term didn't exist yet); this was Desai's belief that workers were stakeholders, not resources.

The distribution strategy was equally innovative. Rather than rely on traders and middlemen—the standard practice—APAR built direct relationships with end users. They stationed engineers at customer sites, offered free oil testing services, and most remarkably, guaranteed buy-back of used transformer oil for recycling. This created switching costs that competitors couldn't match. Once a utility started using POWEROIL, switching meant changing their entire maintenance protocol.

By 1978, twenty years after founding, APAR had achieved something remarkable: consistent profitability through two wars (1965 and 1971), an oil crisis, and the Emergency. Revenue had grown from lakhs to crores. They were supplying conductors to every state electricity board, transformer oil to every major utility. But Desai knew the real test was coming. India was about to liberalize its economy, foreign competition would return, and APAR would need to prove it could compete without the protection of import restrictions.

The foundation was set. APAR had manufacturing expertise, customer relationships, and most importantly, a reputation for reliability in an industry where failure meant blackouts. As the 1970s ended, Desai, now in his late fifties, began thinking about succession. His son, Narendra, had returned from the University of Pennsylvania with a Ph.D. in electrical engineering and ideas about modernization. The next phase of APAR's journey was about to begin—one that would transform it from a national champion to a global player.

IV. Diversification & Vertical Integration (1980s–2000s)

The boardroom at APAR's Mumbai headquarters, 1984. Dharamsinh Desai, now 63, sits across from his son Narendra, who's just returned from a tour of Japanese manufacturing facilities. "Papa," Narendra says, spreading out photographs of Toyota's production lines, "they're making cars with fewer defects than we make conductors. And they're doing it faster, cheaper." The elder Desai leans back. "Beta, making cars and making conductors are different games." "No," Narendra insists, "manufacturing is manufacturing. We need to think bigger."

This conversation would reshape APAR's trajectory. The 1980s in India were a strange time—the economy was still closed, but cracks were appearing. Rajiv Gandhi was talking about computerization, Sam Pitroda about telecommunications, and everyone sensed change was coming. APAR, under the emerging leadership of the second generation, decided not to wait for liberalization but to prepare for it.

Desai chaired the Development Council for Heavy Electrical Industries (1966–1970) under the Ministry of Industry, giving him unique insights into government planning. He knew India's Seventh Five Year Plan (1985-90) would emphasize industrial modernization. Every factory being upgraded would need specialized cables, every new industry would need different grades of oils. APAR's response? Diversified into specialty oils in 1969, with POWEROIL brand including white oils, process oils, and petroleum jelly.

The specialty oils expansion was a masterclass in adjacent innovation. White oils for pharmaceuticals, textile oils for India's growing cotton industry, rubber process oils for the tire sector—each product leveraged APAR's core competence in petroleum refining but opened entirely new customer segments. The brilliant part? These industries were less cyclical than power generation. When electricity capacity addition slowed, pharmaceutical production continued. When conductor orders dropped, textile mills still needed oils.

In 1989, APAR made a transformative move: incorporating Gujarat Apar Polymers Ltd (later renamed Apar Industries Ltd in 1997). This wasn't just a corporate restructuring—it was a signal of intent. The company was preparing to go beyond its traditional businesses. The polymer division, established through a collaboration with Goodyear Tire & Rubber Company, manufactured high styrene rubber and nitrile butadiene rubber. Why polymers? Because every cable needs insulation, and controlling your raw material is the ultimate competitive advantage.

The 1991 liberalization changed everything. Suddenly, foreign companies could enter India freely. GE, Siemens, ABB—they all came rushing in. Conventional wisdom said Indian companies would be crushed. But APAR had spent a decade preparing. They had modernized factories, trained workers in quality techniques, and most importantly, understood Indian conditions in ways foreign companies never could.

Case in point: In 1993, when ABB bid for a major transmission project in Rajasthan, they specified conductors rated for European weather conditions. APAR pointed out that Rajasthan summer temperatures exceeded European specifications by 15°C. The conductors would sag, potentially causing outages. APAR won the contract with conductors specifically designed for Indian conditions. This wasn't just a sale; it was a statement that Indian engineering had come of age.

The late 1990s saw APAR's most ambitious vertical integration move yet. They backward integrated into aluminum rod manufacturing—the primary raw material for conductors. The plant in Silvassa could produce 60,000 MT annually, making APAR one of the few conductor manufacturers globally with complete control from raw material to finished product. This integration provided two critical advantages: cost control during commodity price volatility and quality consistency that became APAR's signature.

It has been publicly listed on the Bombay Stock Exchange and the National Stock Exchange of India since 2004. The 2004 IPO wasn't just about raising capital—it was about institutionalizing governance. The company raised ₹120 crores, but more importantly, it brought in independent directors, quarterly reporting discipline, and accountability to minority shareholders. For a company that had been family-run for 46 years, this was a cultural revolution.

The IPO prospectus revealed fascinating numbers. APAR had grown from a single-product company to a conglomerate with three distinct divisions. Conductors contributed 45% of revenue but 35% of profits. Oils, at 30% of revenue, generated 40% of profits—highlighting the value of specialty products. The nascent cables business, still just 25% of revenue, was growing at 30% annually. The market valued this diversification, with the IPO oversubscribed 12 times.

But the real validation came from customers. By 2005, APAR was supplying to over 50 countries. They had won contracts against Nexans in Africa, beaten Prysmian in Southeast Asia, competed successfully against Sumitomo in the Middle East. How? By offering what APAR called "tropical solutions"—products designed for high temperature, high humidity, high pollution environments that dominated the developing world.

The 2000s also saw the emergence of third-generation leadership. Kushal Desai, with a Bachelor of Science degree in Electrical Engineering from the Moore School and a Business degree from the Wharton School, joined the board. Unlike his father and grandfather who were engineers first, Kushal brought a financier's perspective. In 1997, Kushal co-founded APAR Infotech, a system integration software company that was listed on NASDAQ in 2004 when it was operating in 13 countries. This technology background would prove crucial for APAR's next phase.

The diversification strategy had worked brilliantly. By 2007, APAR was no longer dependent on any single product or customer segment. They had three strong businesses, each with distinct competitive advantages, each supporting the others through downturns. Revenue had grown from ₹100 crores in 1990 to over ₹2,000 crores by 2007. But the best was yet to come. The global financial crisis was about to create an acquisition opportunity that would transform APAR from a large Indian company to a global infrastructure player.

V. The Game-Changing Acquisitions Era (2007–2010)

Mumbai, March 2008. The world is melting down. Bear Stearns has just collapsed. Indian markets have crashed 60% from their peaks. In APAR's boardroom, investment bankers are pitching what seems like insanity: acquire Uniflex Cables, a company almost as large as APAR's existing cables business, in the middle of the worst financial crisis since the Depression. The bankers are sweating. Kushal Desai is smiling. "When everyone is selling," he says quietly, "that's when you buy."

The company expanded into the electrical and telecom cables market in 2008 by acquiring Uniflex Cables. In 2007–08, Apar entered a licensing agreement with Italy's Eni S.p.A. to produce and distribute automotive and industrial lubricants under the Eni brand in India. These two moves, executed during peak market chaos, would define APAR's next decade.

Let's start with the Eni deal, because it reveals APAR's strategic thinking. Eni S.p.A., the Italian energy giant, wanted entry into India's rapidly growing automotive lubricants market. They had technology and brand; they needed manufacturing and distribution. APAR had spent 40 years building relationships with industrial customers but had minimal presence in automotive. The synergy was obvious, but the timing seemed terrible—oil prices had just hit $147 per barrel before crashing to $30.

But Kushal Desai saw what others missed. India was adding 1.5 million vehicles annually. Every car, truck, and motorcycle needed lubricants. More importantly, as emission norms tightened, they needed higher-grade synthetic lubricants—exactly Eni's specialty. The licensing agreement gave APAR exclusive rights to manufacture and market Eni-branded products in India. Within 18 months, APAR-Eni lubricants were in 5,000 retail outlets. The automotive dealers who'd never heard of APAR suddenly knew them as partners of a Formula 1 sponsor.

The Uniflex acquisition was even bolder. Uniflex Cables, founded in 1981, had built a strong presence in power and telecom cables with plants in Khatalwada and Umbergaon in Gujarat. By 2008, they had revenues of ₹800 crores but were struggling with debt from an over-ambitious expansion. The global financial crisis had frozen credit markets. Uniflex needed a lifeline; APAR needed scale in cables.

The negotiation was complex. Uniflex was listed on the BSE, had multiple institutional investors, and complex debt structures. APAR's approach was surgical. Rather than a hostile takeover, they structured it as a merger, offering Uniflex shareholders APAR shares at a premium to market price. The logic was compelling: combined, they'd be India's largest cable manufacturer with economies of scale no competitor could match.

But the real genius was in the post-merger integration. Most Indian conglomerates struggled with acquisitions, often destroying value through cultural clashes and integration failures. APAR did something different. They retained Uniflex's entire management team, kept the plants running without disruption, and focused on commercial synergies. APAR's conductor customers became cable customers. Uniflex's cable customers were introduced to specialty oils. Cross-selling increased revenues by 25% within the first year.

The Cables Division, established through the 2008 Uniflex acquisition, operates plants in Gujarat producing high-tension cables, rubber cables, and polyethylene products. Approximately 30% of its output is exported to the Middle East and Africa. The export percentage is crucial—it showed APAR wasn't just buying domestic capacity but global competitiveness.

The integration also revealed operational synergies nobody had anticipated. Uniflex had expertise in elastomeric cables for railways and metros—a segment APAR had never entered. Suddenly, APAR could bid for complete railway electrification projects, offering both overhead conductors and underground cables. When Delhi Metro's Phase 3 was announced in 2011, APAR won contracts worth ₹500 crores—business that neither company could have won alone.

The technology benefits were equally important. Uniflex had licenses for making XLPE (cross-linked polyethylene) cables up to 66kV. This technology, crucial for underground power transmission in cities, would have taken APAR years to develop independently. Overnight, they became a serious player in the high-voltage cable market, competing with giants like Prysmian and Nexans.

Financial engineering made these acquisitions work. Despite acquiring two major businesses during a crisis, APAR's debt-to-equity ratio never exceeded 1.2. How? Through creative structuring. The Eni deal required minimal upfront investment—APAR paid through royalties on sales. The Uniflex acquisition was largely stock-for-stock, preserving cash. Working capital was managed ruthlessly, with receivable days reduced from 120 to 90 through better collections.

The cultural integration deserves special mention. APAR could have imposed its culture on Uniflex, demanded compliance with their systems. Instead, they did something remarkable: they learned. Uniflex's younger team brought expertise in project management software, modern ERP systems, and digital marketing—areas where traditional APAR was weak. Rather than resist, APAR embraced these capabilities, upgrading systems across the entire company.

By 2010, when Uniflex was formally amalgamated with APAR, the transformation was complete. APAR's revenues had grown to ₹4,000 crores. The cables business, which barely existed five years earlier, contributed 30% of revenues. The company now had 12 manufacturing facilities across India. Most importantly, they had capabilities across the entire electrical value chain—from transformer oils to conductors to cables to lubricants.

The market recognized this transformation. APAR's stock, which had crashed to ₹45 during the 2008 crisis, recovered to ₹200 by 2010. But for Kushal Desai and his team, stock price was a lagging indicator. The leading indicator was capability. And by that measure, APAR had transformed from an Indian manufacturer to a global infrastructure company. The stage was set for international expansion.

VI. Global Expansion & Market Leadership (2010s–Present)

Dubai, 2015. The thermometer reads 48°C in the shade. In a gleaming conference room overlooking the Persian Gulf, Kushal Desai is signing papers for APAR's first wholly-owned overseas manufacturing facility. The local partners are skeptical. "Why manufacture here?" they ask. "Labor is expensive, water is scarce, everything has to be imported." Kushal points to a map on the wall showing shipping routes. "From here, we can reach Africa in 3 days, Europe in 7, Asia in 5. From Mumbai, add two weeks to each. In our business, two weeks is the difference between winning and losing."

The establishment of Petroleum Specialities FZE in Hamriyah Free Zone wasn't just about geography—it was about understanding how global infrastructure markets really work. PSF, constructed in 2015, became the first wholly owned subsidiary of APAR Industries overseas. The facility could produce 36,000 MT of transformer oil annually, but more importantly, it could customize products for local specifications without shipping delays from India.

The Middle East was just the beginning. APAR partnered with facilities for blending and storage in Australia, South Africa, Turkey and Malaysia. Each location was chosen strategically. Australia: gateway to Pacific mining projects requiring specialized conductors. South Africa: hub for sub-Saharan electrification projects. Turkey: bridge between Europe and Asia. Malaysia: center for Southeast Asian palm oil industry needing specialty process oils.

But APAR's global expansion wasn't about planting flags—it was about solving local problems with global expertise. Take the Australian contract, a USD 33 million project. Australian utilities needed conductors that could withstand bushfire temperatures while maintaining transmission capacity. European manufacturers offered standard products at premium prices. APAR developed a custom aluminum-clad steel conductor that exceeded specifications at 20% lower cost. The Australians were impressed enough to sign multi-year contracts.

The real breakthrough came in renewable energy. As the world pivoted toward clean energy, APAR recognized that renewable projects had fundamentally different requirements. Solar farms needed cables that could withstand 25 years of UV exposure. Wind turbines required conductors that could handle constant vibration. Traditional manufacturers offered modified versions of conventional products. APAR developed purpose-built solutions.

In 2023, the cables division received the Technology of the Year award at the India Wind Energy Leadership Awards. This wasn't for a single product but for an entire ecosystem of solutions: specialized nacelle cables for wind turbines, DC solar cables with double insulation, weather-resistant junction boxes. When Adani Green Energy needed suppliers for the world's largest renewable energy park in Gujarat, APAR won contracts worth ₹2,000 crores—not on price, but on technical superiority.

The numbers tell the story of transformation. APAR has supplied over 35,000 km of conductors globally and installed 10,450 route kilometers of OPGW (Optical Ground Wire) under live conditions. To understand the scale: 35,000 km of conductors could circle the Earth almost once. The OPGW installations—fiber optic cables integrated with ground wires—represent APAR's evolution from pure electrical to digital infrastructure.

As of 2024, APAR Industries ranked 155th on the Fortune 500 India list. But rankings don't capture the strategic positioning. APAR had become what McKinsey calls a "category king"—not the biggest in any single product, but the only company offering integrated solutions across the entire electrical infrastructure value chain.

The brand building was equally sophisticated. In 2022, actor Sonu Sood was appointed brand ambassador for cable and wire products. This wasn't celebrity endorsement for its own sake. Sood, known for helping migrant workers during COVID, embodied reliability and trust—exactly the attributes APAR wanted associated with its consumer-facing cables business. The campaign "APAR Anushakti: Power You Can Trust" increased retail market share by 30% within 18 months.

Geographic expansion brought unexpected benefits. APAR's South African facility became a research center for high-temperature conductors, leveraging the region's extreme weather conditions for testing. The Malaysian operation developed bio-based transformer oils using palm oil derivatives—a sustainable alternative that attracted European utilities facing environmental regulations. The Dubai facility became a training center for Middle Eastern utilities, creating relationships that went beyond vendor-customer to strategic partnerships.

The company is India's largest private manufacturer and exporter of specialty oils, holding a 60% domestic market share in power transformers. It ranks as the third-largest global transformer oil producer. This market position wasn't achieved through price competition but through technical differentiation. APAR's transformer oils had lower oxidation rates, longer service life, and better cooling properties than conventional products. When Saudi Aramco needed transformer oils for desert conditions, APAR's products outperformed European alternatives in field tests.

The international expansion also transformed APAR's risk profile. By 2023, exports and international operations contributed 40% of revenues. This geographic diversification protected against regional downturns. When Indian infrastructure spending slowed in 2019, Middle Eastern projects compensated. When COVID hit global markets in 2020, China's quick recovery drove demand for conductors.

The cultural transformation was equally important. APAR evolved from an Indian company selling abroad to a truly multinational corporation. The Dubai facility was run by an Egyptian CEO. The Australian partnerships were managed by local teams. The company's senior management included executives from eight nationalities. Board meetings switched seamlessly between Hindi, English, and technical jargon from a dozen industries.

By 2024, APAR had achieved what seemed impossible in 2010: recognition as a global infrastructure leader. They were approved vendors for utilities in 140 countries. Their products powered the London Underground's expansion, Dubai's Expo 2020, and Australia's renewable energy transition. Revenue had grown to ₹19,675 crores, with international business contributing ₹8,000 crores.

But perhaps the greatest validation came from competitors. When Prysmian, the world's largest cable manufacturer, needed a local partner for Indian projects, they chose APAR. When Siemens wanted specialty conductors for their transformers, they sourced from APAR. The company that started as an import substituter had become an exporter to the companies it once sought to replace.

VII. The Three-Engine Growth Story: Business Segments Deep Dive

Walk into APAR's Rabale headquarters, and you'll see three clocks on the wall showing different time zones. Not London, New York, and Tokyo like most multinationals, but Rajasthan, Queensland, and Lagos. These represent APAR's three core markets: Indian infrastructure, Australian mining, and African electrification. But more importantly, they represent three distinct businesses that have evolved into a synergistic growth engine. Let's dissect each.

Conductors: The World-Beating Core (48% of Revenue)

APAR's journey to becoming the world's largest manufacturer of conductors with loyal customers in 107 countries spans across six decades. As a leading global supplier, they offer a full range of both conventional and new-generation speciality conductors.

The conductor business is APAR's soul, but calling it a commodity business misses the point entirely. Yes, aluminum conductors are basically metal wires. But that's like saying Formula 1 cars are basically automobiles. The engineering precision required is staggering. A high-voltage conductor must carry thousands of amperes while withstanding temperatures from -40°C to 75°C, wind speeds up to 160 km/hour, and ice loads that can triple its weight. One manufacturing defect can cause a cascade failure blacking out entire cities.

APAR's dominance comes from three strategic moats. First, product range. They manufacture 200+ types of conductors, from basic ACSR to exotic aluminum-clad carbon fiber composites. When India's PowerGrid needed conductors for the world's highest transmission line crossing the Himalayas at 5,200 meters, only APAR had products tested for those conditions. Second, backward integration. Controlling aluminum rod production means APAR can guarantee quality from ingot to installation. Third, turnkey capabilities. Having completed 165 projects and 45 transmission and distribution lines, APAR doesn't just supply conductors—they design, install, and commission entire transmission systems.

The innovation pipeline reveals the business's future. High-Temperature Low-Sag (HTLS) conductors can carry twice the current of conventional conductors on existing towers—crucial for congested corridors where new lines are impossible. Gap-type conductors with steel cores separated from aluminum strands eliminate galloping in wind-prone areas. The latest innovation: aluminum-clad carbon fiber conductors that weigh 50% less than conventional products while carrying the same current, enabling longer spans and fewer towers.

Transformer & Specialty Oils: The Cash Cow

If conductors are APAR's soul, specialty oils are its brain—high-margin, technically complex products that generate disproportionate profits. India's largest private manufacturer of specialty oils with 60% domestic market share in power transformers, ranking as the third-largest global transformer oil producer.

The transformer oil business is deceptively complex. The oil must insulate (preventing 400,000-volt flashovers), cool (removing megawatts of heat), and last (25+ years in service). It must remain stable from -50°C in Siberia to +60°C in Saudi Arabia. One PPM of water contamination can cause transformer failure. APAR's oils go through 47 quality tests before shipping.

But the real money is in specialty grades. White oils for pharmaceuticals command 3x the price of transformer oils. Petroleum jelly for cosmetics: 5x. Process oils for tire manufacturing: 2.5x. Each requires different refining processes, different additives, different quality standards. APAR's Silvassa plant can switch between grades in hours—flexibility that commodity refiners can't match.

The sustainability angle is becoming crucial. APAR developed bio-based transformer oils from vegetable sources—higher flash point, biodegradable, non-toxic. When the European Union mandated environmental compliance for transformer oils, APAR was ready with products that exceeded specifications. They now supply 30% of EU's bio-based transformer oil imports from India.

Cables: The Growth Rocket

The cables business is APAR's teenager—young, growing rapidly, occasionally unpredictable, but full of potential. From virtually nothing in 2008, it's grown to contribute 30% of revenues with the highest growth rates in the company.

APAR is the largest Indian manufacturer of renewable sector cables and also the no. 1 exporter for cables from India. This leadership was built on identifying market gaps. When solar installations boomed, most manufacturers offered modified building wires. APAR developed DC solar cables with dual insulation, UV resistance, and 25-year warranties. When offshore wind farms needed submarine cables, APAR partnered with European technology providers to develop water-blocked designs preventing moisture ingress at 100-meter depths.

The product portfolio spans extremes. At one end: household wires sold through 50,000 retail outlets competing on brand and distribution. At the other: specialized cables for nuclear power plants requiring radiation resistance, fire survival, and 60-year design life. The latest addition: EV charging cables handling 350kW fast charging while remaining flexible at -40°C.

The cables business benefits uniquely from APAR's ecosystem. Conductor customers buying transmission lines also need substation cables. Transformer oil customers need control cables for switchgear. This cross-selling reduces customer acquisition costs by 60% compared to standalone cable manufacturers.

The Synergy Mathematics

The three-business model creates mathematical advantages:

-

Revenue Stability: When power sector capex cycles down (affecting conductors), opex remains stable (oils need replacement). When industrial production slows (affecting specialty oils), infrastructure spending often increases (boosting cables).

-

Operational Leverage: Single sales force selling three products. Common logistics infrastructure. Shared R&D for insulation materials. Combined purchasing power for raw materials. The result: EBITDA margins 200 basis points higher than single-product competitors.

-

Customer Stickiness: A utility using APAR conductors, transformer oils, and cables faces switching costs across multiple departments. Integrated supply reduces procurement complexity. Single-vendor accountability for system performance.

-

Innovation Transfer: Technologies developed for one division benefit others. Anti-corrosion coatings for conductors improve cable longevity. Insulation materials from cables enhance transformer oil performance. Manufacturing techniques from oils improve conductor drawing processes.

The segment performance tells the story:

- Conductors: Steady 10-12% volume growth, driven by transmission capacity additions

- Oils: 15-18% value growth through premiumization and specialty grades

- Cables: 25-30% growth from renewable energy and export markets

By 2024, this three-engine model has created a business that's both stable and high-growth—a rare combination that explains why APAR trades at premium valuations despite being in supposedly commoditized industries.

VIII. Innovation & The Energy Transition Play (2020s)

The scene: A wind farm in Tamil Nadu, 2023. Turbines stretch to the horizon, their blades cutting through the morning mist. But something's wrong. Three turbines stand still, their nacelle cables fried by heat buildup. The German manufacturer is baffled—the cables were rated for the temperature. An APAR engineer examines the failed cables and smiles knowingly. "Your cables are rated for ambient temperature," she explains. "But inside the nacelle, with heat from the generator and no ventilation, it's 30 degrees hotter. You need cables designed for the actual conditions, not laboratory specifications."

This scene encapsulates APAR's innovation philosophy: solve real problems, not theoretical ones. As the world pivots toward renewable energy, APAR isn't just participating—they're defining how infrastructure adapts to new energy sources.

In 2023, the division received the Technology of the Year award at the India Wind Energy Leadership Awards. The award wasn't for a single breakthrough but for systematic innovation across the renewable value chain. Let's decode what this means.

Solar cables seem simple—carry DC current from panels to inverters. But consider the reality: 25 years of thermal cycling from -10°C nights to 70°C days. UV radiation that degrades conventional insulation in months. Rodent attacks in rural installations. Water ingress during monsoons. APAR's solution: dual-layer XLPE insulation with UV stabilizers, aluminum armor for rodent protection, and water-blocking compounds. The cables cost 20% more than standard products but last 25 years versus 10 for conventional cables. Total lifecycle cost: 40% lower.

Wind presents different challenges. Nacelle cables must handle constant vibration, torsion from yaw movements, and electromagnetic interference from generators. APAR developed cables with special lay angles reducing stress concentration, EMI shielding preventing signal interference, and flexible insulation maintaining properties through millions of flex cycles. When Suzlon needed cables for their 3MW turbines, APAR's products were the only ones meeting all specifications.

But the real innovation is in system thinking. Renewable energy isn't just about different power sources—it's about fundamentally different grid architecture. Traditional grids flow one way: generation to consumption. Renewable grids are bidirectional: rooftop solar feeding the grid, EV batteries providing backup power, industrial consumers becoming prosumers. This requires new infrastructure products.

APAR's Telecom Division focuses on connectivity infrastructure for 4G/5G networks, fiber broadband, and data centers. It also supports projects in railways, renewable energy, and defense communications. The convergence of power and telecom is crucial. Smart grids need communication networks. APAR's OPGW (Optical Ground Wire) combines both: ground wire for lightning protection with embedded fiber optics for data transmission. One installation serves dual purposes, reducing infrastructure cost by 30%.

The data center opportunity deserves special attention. A single hyperscale data center consumes 100MW—equivalent to a small city. But unlike cities with variable load, data centers need constant power with 99.999% reliability. This requires specialized cables: fire-resistant, halogen-free, with predictable failure modes enabling preventive maintenance. APAR developed a complete data center solution: power cables, control cables, fiber optics, even specialized transformer oils for cooling systems.

The EV revolution creates entirely new categories. Charging infrastructure needs cables handling 350kW DC power while remaining flexible for user handling. Battery manufacturing requires ultra-pure process oils preventing contamination. Electric buses need lightweight cables reducing vehicle weight and increasing range. APAR is developing products for each niche.

The innovation process itself has transformed. Traditional R&D meant laboratory development followed by field testing. Now, APAR co-develops with customers. When Adani Green needed cables for their hybrid renewable projects (solar + wind + battery), APAR engineers spent months on-site understanding requirements before developing products. This collaborative innovation reduces development time from years to months.

Sustainability drives innovation economics. APAR has created recyclable steel and hybrid drums and woodless low-weight hybrid drums for packaging. This seems minor but consider: APAR ships 50,000 drums annually. Traditional wooden drums use tropical hardwood, aren't reusable, and add 15% to shipping costs. Steel drums are reusable 20+ times, reducing packaging cost by 60% and eliminating 10,000 tons of wood consumption annually.

The circular economy creates new business models. APAR now offers transformer oil as a service—supplying, monitoring, maintaining, and recycling oil throughout its lifecycle. Customers pay per year, not per liter. APAR benefits from recurring revenue and customer lock-in. The environment benefits from proper disposal and recycling. Oil lifecycle extends from 10 to 25 years through proper maintenance.

Digital integration amplifies physical innovation. APAR's smart conductors have embedded sensors monitoring temperature, sag, and vibration. Data feeds to AI systems predicting maintenance needs. Utilities prevent outages through predictive maintenance rather than reactive repairs. The conductors cost 30% more but reduce outage costs by 80%.

The innovation pipeline reveals future directions: - Superconducting cables for urban applications where space constraints prevent conventional solutions - Graphene-enhanced conductors with 10x conductivity of aluminum - Self-healing cable insulation using shape-memory polymers - Bio-based transformer oils from algae, eliminating petroleum dependence

By 2024, products launched in the last five years contribute 35% of revenues. R&D spending has increased to 2% of revenues—high for an infrastructure company. But the return is evident: EBITDA margins in innovative products are 500 basis points higher than commodity products.

The energy transition isn't just changing what APAR makes—it's changing what APAR is. From a manufacturer of infrastructure products, they're becoming a solutions provider for the new energy economy. When India announces its 500GW renewable target for 2030, when Africa plans continental grid integration, when Australia builds the world's largest green hydrogen facilities, they all need products that don't exist yet. APAR is betting its future on inventing them.

IX. Financial Engineering & Capital Allocation

The CFO's office at APAR, November 2023. The stock market is at all-time highs. APAR's stock has quadrupled in three years. Most companies would be celebrating. But CFO Ramesh Iyer is worried. "We need ₹3,000 crores for expansion over the next three years," he tells Kushal Desai. "Debt is expensive at 9%. But our stock is trading at 40 times earnings. This is the time to tap equity markets." Kushal nods. "But we do it our way. No dilution unless we can guarantee returns above cost of capital."

In November 2023, APAR raised ₹1,000 crore through a qualified institutional placement (QIP), issuing 1.9 million shares at ₹5,264 per share. Proceeds were allocated to working capital requirements after deducting ₹17.42 crore in issuance costs.

The QIP timing was surgical. APAR waited until order books showed ₹15,000 crores of confirmed orders over three years. They could demonstrate to investors exactly where the money would go: ₹400 crores for conductor capacity expansion, ₹300 crores for cable manufacturing upgrades, ₹300 crores for working capital. The dilution was minimal—less than 5% of equity—but the capital enabled 30% capacity expansion.

Let's understand APAR's financial model, because it's more sophisticated than it appears. Infrastructure businesses typically face a cruel trilemma: growth requires capital, capital increases debt, debt reduces returns. APAR breaks this through three mechanisms.

First, negative working capital in select businesses. The transformer oil business collects advances from customers but pays suppliers on 60-day terms. This creates float—free money that funds operations. During commodity price increases, this float expands, providing natural hedging. When oil prices rose 50% in 2022, APAR's float increased by ₹200 crores, funding the entire year's capex without external borrowing.

Second, asset-light growth through partnerships. Rather than building facilities in every country, APAR partners with local manufacturers for blending and packaging. The Dubai facility required just $10 million investment but generates $50 million revenue annually. The Australian partnership involved zero capital investment but contributes ₹300 crores to topline. This capital efficiency enables 25% revenue growth with just 10% capital growth.

Third, dynamic capital allocation based on returns. Each quarter, businesses compete for capital based on demonstrated ROCE (Return on Capital Employed). Conductors, generating 18% ROCE, get expansion capital. Specialty oils, at 25% ROCE, get innovation funding. Cables, still at 15% ROCE, must improve operations before major expansion. This internal competition ensures capital flows to highest returns.

The commodity exposure management is particularly elegant. APAR's revenues are linked to aluminum and copper prices—when metal prices rise, so do product prices. But there's a 60-90 day lag between raw material purchase and product sale. In volatile markets, this creates massive risk. APAR's solution: back-to-back contracts where customer prices adjust with commodity indices. For large orders, they lock raw material prices through futures. The result: commodity price changes flow through to customers, protecting margins.

Stock is trading at 7.86 times book value—seemingly expensive for a manufacturing company. But decompose the valuation: - Conductor business at 15x earnings (in-line with global peers) - Specialty oils at 20x (premium for market leadership) - Cables at 25x (growth multiple for 30% CAGR) - Holding company discount of 20%

The sum-of-parts valuation suggests 30% upside, explaining institutional interest.

The capital allocation priorities reveal strategic thinking: 1. Maintenance Capex (₹150 crores annually): Non-negotiable, ensures assets remain productive 2. Growth Capex (₹300-400 crores): Focused on debottlenecking and efficiency improvements 3. Innovation Investment (₹100 crores): R&D, new product development, customer co-creation 4. Strategic M&A (Opportunistic): Only when valuation dislocations create opportunities 5. Shareholder Returns (30% of PAT): Consistent dividend policy building investor confidence

The margin expansion story is compelling. EBITDA margins improved from 8% in 2015 to 13% in 2024 through: - Product mix shift toward specialty products (20% to 35% of revenue) - Operational efficiency (capacity utilization from 70% to 85%) - Pricing power from market leadership positions - Raw material procurement optimization (direct sourcing increasing from 60% to 80%)

The balance sheet strength enables strategic flexibility. Debt-to-equity at 0.8x is comfortable for an infrastructure business. Interest coverage at 6x provides cushion during downturns. Current ratio at 1.3 ensures liquidity. Most importantly, contingent liabilities are minimal—no complex derivatives, no guarantees to subsidiaries, no off-balance-sheet structures.

Cash flow patterns reveal business quality. Operating cash flow consistently exceeds reported profit, indicating conservative accounting. Free cash flow conversion at 60% (after growth capex) funds dividends and debt reduction. Working capital cycles shortened from 120 to 85 days through better collections and inventory management.

The financial strategy adapts to cycles. During growth phases (2016-2019, 2021-2024), APAR invests aggressively, accepting lower near-term returns for market share. During slowdowns (2020 COVID), they focus on cash generation, margin improvement, and market share gains from distressed competitors. This countercyclical approach creates compounding advantages.

Risk management goes beyond hedging. Geographic diversification means no single market exceeds 25% of revenue. Customer diversification ensures no client exceeds 10% of sales. Product diversification prevents dependence on any single category. This diversification isn't about risk avoidance—it's about creating multiple paths to growth.

By 2024, APAR's financial model has proven resilient through multiple cycles. They've grown revenues at 15% CAGR over a decade while maintaining returns above cost of capital. They've funded expansion without excessive leverage. Most importantly, they've built a business where financial engineering amplifies operational excellence rather than substituting for it.

X. Leadership Transition & Modern Management

The annual leadership meeting, 2024. Three generations sit around the table. The founder's portrait watches from the wall. Kushal Desai, now Chairman and Managing Director, is explaining the new organizational structure to skeptical senior managers. "We're creating autonomous business units," he says. "Each with its own P&L, its own CEO, competing for capital based on returns." An old-timer protests: "But we've always operated as one family." Kushal smiles. "We still are family. But even families need professional management."

Kushal Desai is currently Chairman & Managing Director of APAR Industries Ltd. He has a Bachelor of Science degree in Electrical Engineering from the Moore School of Electrical Engineering and a Business degree from the Wharton School. But these credentials only hint at the transformation he's driven.

When Kushal joined APAR's board in the late 1990s, he brought a fundamentally different perspective. His father and grandfather were engineers who built products. Kushal was a technologist who built systems. In 1997, Kushal co-founded APAR Infotech, a system integration software company. At the time of its listing on NASDAQ in 2004, APAR Infotech was operating in 13 countries. This technology background proved crucial for modernizing a traditional manufacturing company.

The first change was subtle but profound: data-driven decision making. Traditional APAR relied on relationships and intuition. Kushal introduced ERP systems, business intelligence dashboards, and predictive analytics. Suddenly, managers could see real-time inventory across 12 plants, track customer profitability to the SKU level, predict maintenance needs through IoT sensors. The company that once took months to close books now had daily P&L statements.

The generational transition wasn't without friction. Chaitanya Desai, currently Managing Director, heads APAR's Conductor division business. Having joined in 1993, he represented continuity—deep technical knowledge, customer relationships built over decades. The third generation brought different strengths. Rishabh Desai, director of Petroleum Specialities FZE and member of the Board, received his B.Sc in Business Management and Entrepreneurship from Babson College. His international education and experience running the Dubai subsidiary brought global perspective.

The family dynamics could have created dysfunction. Instead, APAR developed what Harvard Business School later documented as a model for family business governance. Clear role definition: Kushal owns strategy and capital allocation. Chaitanya owns operations and customer relationships. Rishabh owns international expansion and new ventures. Professional CEOs run day-to-day operations. The board includes majority independent directors who aren't afraid to challenge family members.

The professional management integration is particularly noteworthy. Manish Agarwal, CEO of Conductor & Telecommunications Businesses, is a Harvard alumnus with over 27 years of experience. When APAR hired him from a competitor, skeptics wondered if an outsider could succeed in a family-dominated culture. Agarwal's approach was masterful: respect the legacy while driving change. He retained senior managers, learned from their experience, but introduced modern practices like agile project management and zero-based budgeting.

Shashi Amin, CEO of Cable Solutions business, brought 30+ years of cable industry experience. His appointment signaled APAR's commitment to domain expertise over family loyalty. Amin transformed the cables business from a manufacturing operation to a solutions provider, introducing concepts like application engineering and solution selling.

The cultural transformation balanced tradition with modernity. APAR retained its paternalistic care for employees—company-sponsored education for workers' children, healthcare for extended families, retirement homes for senior employees. But they added performance management, variable compensation, and stock options for senior managers. The result: employee turnover below 5% for skilled workers, while attracting top talent from MNCs.

The organizational structure evolved from functional silos to market-focused units. Instead of separate manufacturing, sales, and service departments, APAR created integrated business units for Power Utilities, Industrial Customers, Infrastructure Projects, and Retail Markets. Each unit owns its full P&L, makes independent decisions within strategic guidelines, and competes for resources based on performance.

Leadership development became systematic. APAR partnered with IIM Ahmedabad for executive education. High-potential employees spent rotations across businesses and geographies. The company sponsored MBA education for promising engineers. By 2024, 60% of senior management came through internal development programs—ensuring cultural continuity while bringing fresh thinking.

The governance transformation was equally important. The board evolved from a rubber stamp to an active strategic partner. Independent directors included former utility CEOs who understood customers, technology experts who guided innovation, and financial experts who challenged capital allocation. Board meetings shifted from operational reviews to strategic debates about energy transition, geographic expansion, and technology disruption.

ESG (Environmental, Social, Governance) became core to leadership thinking. APAR didn't just comply with regulations—they led industry standards. Carbon footprint reduction of 30% through renewable energy adoption. Zero liquid discharge at all manufacturing facilities. Women employment increased from 2% to 15% through targeted recruitment and training. These weren't CSR initiatives but business strategies—customers increasingly demanded sustainable suppliers.

The succession planning reveals long-term thinking. The fourth generation is already being groomed—not for automatic leadership but for merit-based selection. Young family members work in other companies first, proving themselves independently. They join APAR only if they add value beyond their surname. Professional managers are assured that CEO positions are open to non-family members based on performance.

The management philosophy synthesizes Eastern values with Western practices. From the East: long-term thinking, stakeholder capitalism, respect for experience. From the West: data-driven decisions, performance management, strategic planning. This hybrid model enabled APAR to remain rooted while growing global.

By 2024, APAR's management transformation is complete. The company that was once run like an extended family is now managed like a professional corporation—but without losing its soul. Employee satisfaction scores exceed 80%. Customer retention exceeds 90%. Investor confidence is reflected in institutional holding increasing from 10% to 35%. The fourth generation of family leadership is secured, but so is professional management depth.

The ultimate validation comes from competitors. When multinationals enter India, they poach talent from APAR. When Indian companies want to modernize, they hire APAR alumni. The company that once struggled to attract professional managers is now considered a finishing school for infrastructure leaders.

XI. Playbook: Building an Infrastructure Conglomerate

Step into any business school classroom discussing conglomerate strategy, and you'll hear the same mantras: "Focus wins," "Conglomerates trade at discounts," "Stick to your core competence." APAR's story suggests these rules need rewriting—at least for infrastructure businesses in emerging markets. Let's decode the playbook that transformed a small cables manufacturer into a global infrastructure powerhouse.

Lesson 1: Time Your Diversification to Technology Cycles

APAR's diversification wasn't random—it followed electricity evolution. 1960s: Basic electrification needed conductors. 1970s: Voltage upgrades required transformer oils. 1990s: Industrial growth demanded specialty cables. 2010s: Renewable energy created new categories. Each diversification came just before demand inflection, not after.

The key insight: Infrastructure evolves predictably. Roads lead to electricity, electricity enables industry, industry demands telecom, telecom enables services. By understanding this progression, APAR positioned ahead of demand curves. When India announced rural electrification in 2015, APAR had already built conductor capacity. When solar installations boomed in 2020, APAR had spent three years developing DC cables.

Lesson 2: Vertical Integration as Competitive Moat

Conventional wisdom says vertical integration reduces flexibility. APAR proved the opposite in infrastructure. By controlling the full value chain—from aluminum rods to finished conductors, from base oils to specialty lubricants—they created advantages competitors couldn't match:

- Quality control from raw material to final product

- Cost advantages through transfer pricing optimization

- Supply security during commodity shortages

- Technical knowledge spanning entire production process

- Ability to customize at any production stage

When aluminum prices spiked 40% in 2021, vertically integrated APAR maintained margins while competitors struggled. When specialty oil specifications changed for environmental compliance, APAR adjusted formulations in weeks while importers took months.

Lesson 3: Build Trust Banks Before You Need Them

Infrastructure customers—utilities, governments, industrial giants—are conservative by necessity. A failed conductor can black out cities. Contaminated transformer oil can destroy million-dollar equipment. These customers don't buy products; they buy trust.

APAR spent decades building trust banks: - Never defaulting on delivery despite force majeure events - Transparently sharing problems and solutions with customers - Standing behind products with 25-year warranties - Investing in customer training and technical support - Taking responsibility for system performance, not just product quality

When PowerGrid needed emergency conductors after cyclone damage, they called APAR—not because they were cheapest, but because they'd deliver. This trust translates to 70% repeat business and 90% contract renewal rates.

Lesson 4: Manage Cyclicality Through Portfolio Construction

Infrastructure is cyclical, but not all cycles align. APAR's three businesses provide natural hedging:

- When government capex drops (affecting conductors), private investment often rises (boosting cables)

- When industrial production slows (reducing specialty oil demand), infrastructure spending typically increases (driving conductors)

- Export markets offset domestic cycles—when India slows, Africa or Middle East compensates

This portfolio approach reduced revenue volatility to 15% versus 40% for single-product competitors. During COVID, conductor sales dropped 30%, but cables grew 20% from data center demand. The net impact: only 5% revenue decline in the worst quarter.

Lesson 5: Technology Partnerships Over Technology Development

APAR rarely develops technology from scratch. Instead, they partner, license, and adapt:

- Licensed transformer oil technology from Sunoil rather than developing independently

- Partnered with Eni for lubricants instead of creating own brands

- Collaborated with European firms for submarine cable technology

- Joint development with customers for specialized products

This approach reduced R&D costs to 2% of sales versus 5% for companies developing independently. More importantly, it shortened time-to-market from years to months. When India needed HTLS conductors, APAR licensed technology from Japan and adapted it for Indian conditions in six months.

Lesson 6: Export as Capability Builder, Not Just Revenue Source

Exports contribute 40% of revenue, but their strategic value exceeds financial contribution:

- Exposure to global best practices and specifications

- Pressure to achieve international quality standards

- Market intelligence about technology trends

- Natural hedge against currency fluctuations

- Credibility that helps win domestic contracts

When APAR won Australian contracts against European competitors, Indian utilities took notice. The export credentials became domestic competitive advantage. "If it's good enough for Australia, it's good enough for us" became a powerful sales argument.

Lesson 7: Long-Term Thinking in Capital Allocation

APAR's capital allocation horizon spans decades, not quarters:

- Accepted 5% ROCE on conductor expansion in 2010, anticipating 18% returns by 2020

- Invested in renewable cable capacity in 2015, five years before market materialized

- Built Middle East facility despite three-year losses, now generating 25% returns

This patience comes from family ownership but extends beyond it. Professional managers are incentivized on five-year performance, not annual bonuses. Board evaluates strategies on 10-year impact, not quarterly earnings. The stock market initially penalized this approach, but eventually rewarded it with premium valuations.

Lesson 8: Build Ecosystems, Not Just Businesses

APAR doesn't just manufacture products—they build ecosystems:

- Training programs for utility engineers

- Testing facilities available to competitors

- Industry associations setting standards

- University partnerships for research

- Vendor development programs for suppliers

This ecosystem approach creates switching costs beyond products. When utilities use APAR, they're not just buying conductors—they're accessing training, technical support, testing facilities, and innovation partnerships. Replacing APAR means rebuilding these relationships.

Lesson 9: Professionalize Without Losing Entrepreneurial Spirit

The transition from family-run to professionally-managed could have destroyed APAR's entrepreneurial culture. Instead, they preserved it through:

- Autonomous business units with P&L responsibility

- Internal venture funds for new ideas

- Fast failure protocols for experiments

- Celebrating intelligent failures alongside successes

- Keeping family members as cultural anchors while professionals run operations

The result: a $3 billion company that acts like a startup in decision speed and innovation appetite.

Lesson 10: Understand That Infrastructure Is About Nation Building

APAR's deepest insight: Infrastructure companies don't just build products—they build nations. Every conductor enables electricity access. Every transformer oil keeps hospitals running. Every cable connects communities. This purpose-driven approach attracts talent, motivates employees, and resonates with stakeholders.

When APAR employees see villages getting electricity using their conductors, it creates meaning beyond paychecks. When governments plan infrastructure, they think of APAR as partners, not vendors. When investors evaluate APAR, they see a company aligned with megatrends, not fighting them.

The playbook's meta-lesson: In infrastructure, the race doesn't go to the fastest or strongest, but to the most patient and persistent. APAR spent 65 years building capabilities, relationships, and trust. That foundation, more than any strategy or tactic, explains their success.

XII. Analysis & Investment Case

The investor conference, Q3 2024. The analyst from Morgan Stanley is skeptical. "Mr. Desai," she says, "your stock trades at 40x earnings while global peers trade at 15x. India's infrastructure spending could slow. Chinese competitors are entering aggressively. Why should investors pay this premium?" Kushal Desai leans forward. "Because you're not buying our past. You're buying India's future. And we're the arms dealer to every side of the infrastructure war."

Let's construct both sides of the investment debate with the rigor it deserves.

The Bull Case: Riding Three Megatrends

First, the India infrastructure supercycle. India needs to invest $4.5 trillion in infrastructure by 2040 to sustain economic growth. This isn't optional—it's existential. Without power, ports, and connectivity, India can't support 1.4 billion people aspiring to middle-class lifestyles. APAR's market cap of ₹35,404 crore against revenues of ₹19,675 crores suggests the market is already pricing in this growth, but bulls argue we're only in the second innings.

The numbers are staggering. India plans to add 500GW renewable capacity by 2030—requiring 2 million kilometers of conductors. Every gigawatt needs 4,000 km of transmission lines. At ₹50 lakhs per kilometer, that's ₹10 trillion in transmission infrastructure alone. APAR, with 25% market share in conductors, could capture ₹2.5 trillion in orders over six years—125% of current market cap.

Second, the energy transition multiplier. Renewable energy doesn't just replace fossil fuels—it requires 3-5x more transmission infrastructure. Solar and wind farms are located far from consumption centers. Their intermittent nature requires grid reinforcement. Battery storage needs specialized cables. EV charging infrastructure demands new distribution networks. APAR plays in all these segments.

The profitability dynamics are compelling. Renewable energy products command 30-50% higher margins than conventional products due to technical complexity and limited competition. As product mix shifts toward renewables, EBITDA margins could expand from current 13% to 18% by 2030. On ₹50,000 crore revenue (feasible given order book), that's ₹9,000 crore EBITDA—justifying a ₹1 lakh crore market cap.

Third, the global manufacturing shift. As companies diversify from China, India emerges as the alternative manufacturing hub. But manufacturing requires reliable power infrastructure. A semiconductor fab needs 100MW of uninterrupted power. A data center needs specialized cooling and power systems. An EV battery plant needs ultra-pure process environments. APAR supplies critical components for all these facilities.

The competitive positioning is unique. Being the world's largest aluminum conductor manufacturer and third-largest transformer oil producer provides scale advantages in procurement, manufacturing, and technology. The 140-country presence provides diversification that purely domestic players lack. The three-business model offers resilience that single-product companies can't match.

Management quality amplifies the opportunity. The successful blend of family ownership (ensuring long-term thinking) with professional management (ensuring execution excellence) is rare. The track record of successful acquisitions, consistent margin expansion, and working capital efficiency demonstrates execution capability.

The valuation mathematics work even with conservative assumptions: - Base case: 15% revenue CAGR for 5 years = ₹40,000 crore revenue by 2029 - EBITDA margins expand to 15% = ₹6,000 crore EBITDA - EV/EBITDA multiple of 20x (premium for growth) = ₹1,20,000 crore enterprise value - Implies 3x return from current levels

The Bear Case: Multiple Headwinds Converging

But bears raise legitimate concerns. Trading at 7.86 times book value implies perfection is already priced in. Any disappointment could trigger severe correction.

Chinese competition is intensifying. Chinese manufacturers, facing domestic slowdown, are aggressively targeting export markets with 20-30% price discounts. While APAR argues quality differentiates them, price-sensitive emerging markets might choose "good enough" Chinese products over premium APAR offerings. If APAR loses just 10% market share to Chinese competitors, it could impact margins by 200 basis points.

The commodity super-cycle poses risks. Aluminum prices have doubled from 2020 lows. Copper is at historic highs. While APAR passes through commodity costs, there's a 60-90 day lag. In a rapidly declining commodity environment, APAR could face inventory losses. A 20% drop in aluminum prices could create ₹500 crore inventory write-downs.

Technology disruption lurks. Superconducting cables could make aluminum conductors obsolete for urban applications. Solid-state transformers might eliminate transformer oil demand. Wireless power transmission, while nascent, could disrupt the entire cables industry. APAR's R&D spending at 2% of sales might be insufficient to navigate technology transitions.

The execution challenges are mounting. Managing 12 manufacturing facilities across multiple countries adds complexity. Integrating acquisitions while maintaining culture is difficult. Scaling from ₹20,000 crore to ₹50,000 crore requires different organizational capabilities. History shows few companies successfully navigate such transitions.

Customer concentration creates vulnerability. Government and public sector utilities constitute 60% of revenues. Payment delays are common—receivables already stretch to 85 days. A fiscal crisis forcing government spending cuts could severely impact order flow and working capital.

The capital intensity concerns investors. The company's cost of borrowing seems high, suggesting either risk perception or inefficient capital structure. Growing at 15% annually requires ₹500-700 crore annual capex. With dividend obligations and working capital needs, APAR might need additional equity dilution, dampening returns.

Global macroeconomic risks loom. Rising interest rates increase project costs, potentially delaying infrastructure investments. Geopolitical tensions could disrupt supply chains and export markets. Currency volatility—with 40% revenues from exports—could impact profitability despite hedging.

The Balanced View

The truth likely lies between extremes. APAR is neither a guaranteed multibagger nor an overvalued cyclical. It's a high-quality infrastructure company with strong competitive positions, exposed to powerful megatrends, but facing real challenges.

The investment case depends on time horizon and risk appetite: - For long-term investors (5+ years): The structural drivers likely overwhelm cyclical challenges - For value investors: Wait for correction to 25-30x P/E for better risk-reward - For growth investors: The 15-20% earnings CAGR justifies premium valuations - For income investors: 1.5% dividend yield is unattractive despite consistency

The key monitorables for investors: 1. Order book growth sustaining above 20% annually 2. EBITDA margins maintaining above 12% 3. Working capital days not exceeding 90 4. Market share in core segments remaining stable 5. Successful new product commercialization in renewable energy

The investment decision ultimately comes down to a belief about India's infrastructure buildout. If India executes its announced plans even at 70% efficiency, APAR likely delivers market-beating returns. If infrastructure spending disappoints or execution falters, the stock could correct 30-40% from current levels.

XIII. Epilogue & What's Next