Angel One: From Sub-broker to India's Digital Broking Giant

I. Introduction & Episode Roadmap

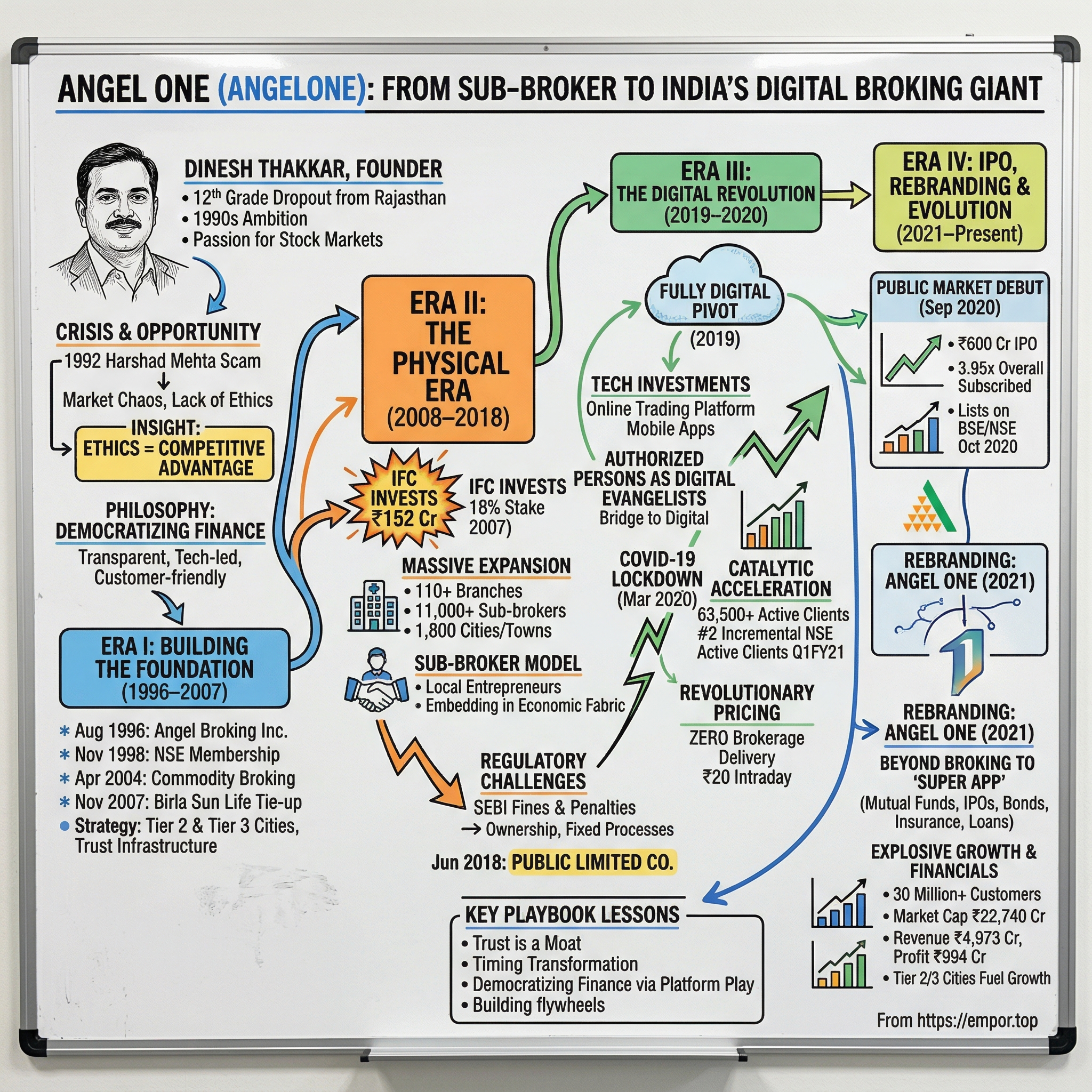

Picture this: A 12th-grade dropout from small-town Rajasthan walks into Mumbai's cutthroat financial markets in the early 1990s with nothing but ambition and a radical idea—what if stockbroking could actually be ethical? Fast forward three decades, and Dinesh Thakkar's Angel One commands a ₹22,740 crore market capitalization, serves over 3 crore customers, and has fundamentally reshaped how India invests.

This is not your typical fintech success story. While Zerodha grabbed headlines with discount broking and Groww courted millennials with slick apps, Angel One took a different path—methodically building trust in tier-2 and tier-3 India before executing one of the most successful digital pivots in Indian financial services. The company that started as a single-person sub-broking operation in 1996 now processes hundreds of billions in daily turnover, yet its founder remains largely unknown outside financial circles. The story of Angel One reads like a playbook on contrarian timing. While competitors rushed to digitize in the mid-2010s, Angel One waited. While others chased urban millennials, Angel One built trust in Bhilwara and Bhopal. The company is now the largest listed retail stock broking house in India, in terms of active clients on NSE, a position it achieved not by being first, but by being patient.

Here's what makes Angel One fascinating for students of business strategy: This is a company that transformed from a relationship-driven, branch-heavy traditional broker into a digital powerhouse during COVID-19—and somehow made it look inevitable. The numbers tell only part of the story: ₹24,001 crore market cap, ₹4,973 crore revenue, ₹994 crore profit. The real story is how a dropout from Rajasthan built one of India's most successful financial services companies by doing everything the experts said was wrong—until suddenly it was right.

We'll explore how Angel One navigated the treacherous waters of Indian capital markets through multiple crises, regulatory overhauls, and technological disruptions. We'll examine the economics of their radical pricing strategy—zero brokerage on delivery trades—and why it worked when conventional wisdom said it shouldn't. Most importantly, we'll unpack the digital transformation that took them from 4.8% market share to becoming a dominant force in Indian retail broking.

This episode traces three distinct eras: the trust-building phase (1996-2007), the physical expansion era (2008-2018), and the digital revolution (2019-present). Each phase required different skills, different strategies, and crucially, different capital allocation decisions. The thread connecting them all? A founder who understood that in Indian finance, ethics isn't just good karma—it's good business.

II. The Founder's Origin Story: Dinesh Thakkar

The year is 1992. India's stock markets are in chaos. The Harshad Mehta securities scam has just exploded, wiping out thousands of crores and destroying investor confidence. Banks are reeling, brokers are folding, and trust in the financial system has evaporated. In this wreckage, a 24-year-old from Bhilwara, Rajasthan, sees opportunity where others see only disaster.

Dinesh Thakkar was born in 1968 into a modest family in Bhilwara, a textile town better known for its wool than its financial acumen. Unlike the typical pedigreed finance professional—IIT, IIM, maybe a stint at Goldman Sachs—Thakkar's resume was refreshingly unremarkable: 12th grade education, no fancy degrees, no family connections to Dalal Street. What he did have was an outsider's perspective on an industry desperately in need of reform. Thakkar entered the financial sector in the early 1990s, working initially in his family's textile business before his passion for stock markets took over. He initially worked in his family's textile business, but his passion for the stock market led him to explore the financial sector. The timing couldn't have been worse—or perhaps better, depending on your perspective. During the Harshad Mehta scam in 1992, his nascent brokerage business, which used to earn Rs 40-50 lakh annually, faced a severe setback.

Think about that for a moment. Here's a young entrepreneur, barely started, watching his fledgling business get hammered by a crisis he had nothing to do with. Most would have retreated to safer ground. Thakkar saw something different: an industry crying out for transparency and ethics.

"The main aspect that led me to start was the lack of ethics and transparency in the industry," Thakkar would later reflect. This wasn't just idealism—it was strategic insight. In a market where trust had been shattered, being the ethical player wasn't just the right thing to do; it was a massive competitive advantage waiting to be seized.

Thakkar started his career as a stock broker in 1987, learning the ropes for 9 years and seeing the industry go through the tough phase of early 1990s, before setting up Angel Broking in 1996. Those nine years weren't just apprenticeship—they were market research. While working as a sub-broker, Thakkar observed every pain point, every inefficiency, every moment where the system failed retail investors.

His vision was audacious for someone with his background: building Angel One into the largest retail broking house in the country. Not just successful, not just profitable—the largest. This from a man who, in meetings with sophisticated bankers and MBAs, stood out for what he didn't have rather than what he did.

As of 2024, his estimated net worth is ₹1,500 crore, largely driven by his stake in Angel One. But wealth was never the primary motivator. Thakkar's philosophy centered on democratizing finance—making stock market investing accessible to the common Indian, particularly those in smaller cities who were systematically excluded from wealth creation opportunities.

The personal philosophy that would guide Angel One's growth was crystallizing: Build a transparent, technology-led, customer-friendly firm. Each element was carefully chosen. Transparent, because trust would be their moat. Technology-led, because manual processes couldn't scale to serve millions. Customer-friendly, because the industry had forgotten who it was supposed to serve.

By 1996, Thakkar was ready. The scars from 1992 had healed, but the lessons remained. The Indian economy was liberalizing, foreign investment was flowing in, and a new middle class was emerging with savings to invest. The stage was set for Angel Broking's incorporation on August 8, 1996—a date that would mark the beginning of one of Indian finance's most unlikely success stories.

III. Building the Foundation (1996–2007)

August 8, 1996. Angel Broking Private Limited is officially incorporated. The office? A modest setup in Mumbai. The team? Essentially Thakkar and a handful of believers. The competition? Established broking houses with decades of relationships, massive capital, and armies of sub-brokers. David versus Goliath would be an understatement.

Angel Broking was incorporated on 8 August 1996 as a private limited company. Later, Angel Broking was incorporated as a wealth management, retail and corporate broking firm in September 1997. The progression from private limited company to full-service firm in just over a year reveals Thakkar's ambition—this wasn't going to be another me-too brokerage.

The late 1990s were a peculiar time in Indian capital markets. The wounds from Harshad Mehta were still fresh, but technology was beginning to reshape trading. The NSE had introduced electronic trading in 1994, but most of India still traded through physical share certificates and phone calls to brokers. Angel saw opportunity in this transition.

November 1998 marked a crucial milestone: Angel Capital and Debt Market Ltd. gained NSE membership. This wasn't just a license to trade—it was validation. The NSE didn't hand out memberships lightly. For a two-year-old firm founded by a 12th-grade passout, this was legitimacy.

The early strategy was counterintuitive. While competitors fought over wealthy traders in Mumbai and Delhi, Angel began building networks in tier-2 and tier-3 cities. Thakkar understood something fundamental: India's next wave of investors wouldn't come from Malabar Hill or Golf Links—they'd come from Nagpur, Indore, and Jaipur.

April 2004 brought another strategic expansion: the commodity broking division. This wasn't just product diversification—it was customer retention. Angel's clients in agricultural towns wanted to trade commodities. Rather than lose them to specialized commodity brokers, Angel brought the capability in-house. Classic vertical integration, but driven by customer need rather than corporate strategy. November 2007 marked another strategic milestone: Birla Sun Life Insurance joined hands with Angel Broking for distribution of its insurance products. This wasn't just another distribution tie-up. Angel was methodically building a one-stop financial services platform before "super apps" were even a concept. Each product addition—equities, commodities, insurance—increased customer stickiness and lifetime value.

The foundation years weren't glamorous. No unicorn valuations, no TechCrunch headlines. Just patient, methodical expansion. Branch by branch, product by product, Angel was building something most couldn't see yet: trust infrastructure. In markets where a handshake still sealed deals and relationships spanned generations, Angel was becoming the bridge between traditional India and modern finance.

By 2007, Angel had quietly assembled all the pieces: trading capabilities across asset classes, insurance distribution, wealth management services, and most importantly, a reputation for ethical dealing. The stage was set for the next phase—aggressive physical expansion backed by institutional capital. The foundation was complete; now it was time to build the edifice.

IV. The Physical Era: Scale and Expansion (2008–2018)

The financial crisis of 2008 should have been a disaster for a growing brokerage. Markets crashed, Lehman Brothers collapsed, and investor confidence evaporated globally. Yet for Angel Broking, crisis once again became opportunity. While competitors retrenched, Angel found a powerful ally: the International Finance Corporation. The International Finance Corporation bought an 18% stake in Angel Broking for ₹152 crore in December 2007. This wasn't just capital injection—it was validation on a global scale. The World Bank's private equity arm doesn't invest in mom-and-pop brokerages. They saw what Thakkar had been building: a distribution network that could reach India's untapped millions.

With IFC's backing, Angel went into overdrive. The numbers from this era are staggering: The company operates through a network of over 110 branches and more than 11,000 sub-brokers in 1,800 cities and towns, as of 30 June 2018. Think about the logistics of that expansion—from a handful of branches to over 110, from Mumbai to 1,800 cities and towns. This wasn't the Silicon Valley model of "blitzscaling." This was methodical, branch-by-branch construction of a physical trust network.

The authorized person (sub-broker) model was crucial. These weren't just agents; they were local entrepreneurs who understood their communities. In Surat, the sub-broker might be the diamond merchant's son who understood commodity cycles. In Coimbatore, it might be the textile trader who knew when farmers had surplus cash. Angel wasn't just building a distribution network—it was embedding itself in India's economic fabric. But 2013 brought regulatory turbulence. In January 2013, a probe found the company and two other entities involved in fraudulent and unfair trade practices in transactions of shares of Sun Infoways during Feb-May 2001. As a result, SEBI restrained Angel from taking new clients for a period of two weeks. The Securities Appellate Tribunal upheld SEBI's order, and subsequent appeals were dismissed.

This wasn't Angel's only brush with regulatory action. SEBI imposed various penalties—₹30 lakh for self-trades in Sterling Green Woods shares, ₹25 lakh for allowing unqualified personnel to operate F&O terminals, ₹10 lakh for inspection violations. For a company built on trust and ethics, these were serious reputational hits.

Here's where most companies would have crumbled. Regulatory issues in financial services are often death sentences. But Angel did something remarkable: they owned the problems, fixed the processes, and kept building. The physical expansion continued unabated. By 2018, they had over 11,000 authorized persons—the largest network with NSE.

June 28, 2018, marked a crucial transition: Angel Broking converted from private limited to public limited company. This wasn't just a legal formality—it was preparation for the next phase. The company knew that to compete with discount brokers and fintech startups, it needed capital, credibility, and most importantly, the ability to pivot quickly.

The physical era had been spectacularly successful by traditional metrics. Angel had built one of India's largest distribution networks, survived regulatory challenges, and maintained steady growth. But storm clouds were gathering. Zerodha was disrupting the industry with discount broking. Fintech startups were attracting venture capital. The writing was on the wall: evolve or die.

As 2018 ended, Angel Broking stood at a crossroads. They could continue as a successful traditional broker, milking their physical network for diminishing returns. Or they could attempt something audacious—completely reinvent themselves as a digital-first company. The decision they made would determine whether Angel Broking would be a footnote in Indian financial history or a case study in successful transformation.

V. The Digital Revolution (2019–2020)

- Zerodha has already captured 15% market share with zero brokerage on delivery trades. Upstox is growing at breakneck speed. Traditional brokers are hemorrhaging customers. And Angel Broking, with its 11,000-person physical network and branch-heavy model, decides to go fully digital. The timing seemed suicidal—or genius.

Angel began its "Digital Journey" in 2019, offering an end-to-end digital investment solution. This wasn't incremental change—it was organizational chemotherapy. The company that had spent two decades building physical infrastructure was now betting everything on bits and bytes.

The transformation started with technology investments: a state-of-the-art online trading platform with real-time access and advanced tools. But technology was the easy part. The hard part was convincing 11,000 authorized persons that their future lay not in relationship management but in becoming digital evangelists.

The mobile apps launched with little fanfare. Angel Broking and Angel BEE apps would eventually be downloaded 850,000+ and 450,000+ times respectively by 2020. But in early 2019, they were just another set of apps in an overcrowded marketplace. What made them different wasn't features—it was distribution.

Remember those 11,000 authorized persons? Angel didn't fire them. Instead, they became the bridge between digital and physical. In Coimbatore, the local sub-broker would sit with clients, helping them download the app, complete e-KYC, and place their first trade. This wasn't disruption—it was transition management at scale.

By late 2019, the metrics were encouraging: 85.21% of clients were being acquired digitally. But digital acquisition is cheap; digital retention is hard. Angel's solution was counterintuitive—they kept the human touch. You could trade on the app, but if you needed help, your local authorized person was a phone call away.

Then came March 2020. COVID-19. Lockdowns. The physical network that had been Angel's strength became a liability overnight. Branches shuttered. Face-to-face meetings became impossible. For a company midway through digital transformation, this should have been catastrophic.

Instead, it was catalytic.

April-June 2020 saw Angel add 63,500 active clients—second among all stockbroking houses. The digital infrastructure they'd been building was suddenly the only infrastructure that mattered. The authorized persons, stuck at home, became WhatsApp warriors, YouTube educators, and Zoom advisors.

The pandemic didn't just accelerate Angel's digital transformation—it validated it. While traditional brokers scrambled to move online, Angel was already there. While discount brokers struggled with customer service at scale, Angel had 11,000 people ready to help.

The numbers from this period are staggering. Angel became the fourth largest in terms of NSE active clients, and second largest in terms of incremental NSE Active Clients during Q1FY2021. Market share in active NSE clients jumped from 4.8% in Q1 FY20 to over 6% by mid-2020.

But the real innovation wasn't in the technology—it was in the business model. Angel introduced revolutionary pricing: ZERO cost brokerage for cash delivery, only Rs.20 per order for Intraday, F&O. This wasn't just matching Zerodha—it was beating them at their own game while maintaining service quality through the hybrid model.

The digital transformation also meant product expansion. The platform evolved from simple trading to comprehensive wealth management—mutual funds, IPOs, bonds. Each addition wasn't just a revenue stream; it was a reason for customers to stay.

By September 2020, Angel was ready for the ultimate validation: the public markets. The timing was perfect. The stock market was recovering from COVID lows. Retail participation was exploding. And Angel had a story that resonated: a traditional company that had successfully transformed itself for the digital age.

The IPO prospectus revealed the extent of the transformation. Revenue composition had completely shifted. Digital channels drove the majority of business. Customer acquisition costs had plummeted. And most importantly, the company was profitable—not some day in the future, but right now.

What Angel had accomplished in 18 months was remarkable. They had transformed from a branch-based, relationship-driven traditional broker into a digital-first platform without losing their core strength—trust and distribution. They had turned potential disruption into competitive advantage.

The lesson here isn't about technology adoption—anyone can build an app. It's about organizational transformation. Angel didn't just digitize their existing processes; they reimagined their entire business model while keeping their people along for the journey. In management literature, this is called "ambidextrous innovation"—maintaining the old while building the new. In practice, it's incredibly hard to execute. Angel made it look easy.

VI. The IPO & Public Market Debut (2020)

September 22, 2020. The Indian stock market is in a peculiar state. The economy is reeling from COVID-19, GDP has contracted 23.9% in Q1, yet the Sensex is near all-time highs. Into this contradiction, Angel Broking launches its ₹600 crore IPO. The timing couldn't be more symbolic—a company built on serving retail investors was now asking those same investors to become owners.

The IPO structure was telling: ₹300 crore fresh issue, ₹300 crore offer for sale. Half for growth, half for exits. The IPO offered an exit to investors, including promoters Ashok Thakkar, Sunita Magnani, World Bank's private equity arm IFC, and others. IFC planned to offload shares worth INR120 crore while Ashok Thakkar and Sunita Magnani offered shares worth INR20.8 crore and INR3.1 crore, respectively. Notably, Dinesh Thakkar—the founder—wasn't selling. This wasn't a cash-out; it was a coming-out party.

The IPO price of ₹306 per share valued the company at roughly ₹2,200 crores. For context, this was a company that had revenues of ₹725 crore in FY20. The valuation multiple seemed rich, but investors weren't buying the past—they were buying the transformation story.

IPO bidding from September 22-24, 2020, saw overwhelming response. The issue was subscribed 3.95 times overall, with the retail portion subscribed 4.36 times. Remember, this was during a pandemic, when household savings were under pressure. Yet retail investors—Angel's core constituency—showed up in force.

October 5, 2020. 10:00 AM. Angel Broking lists on both BSE and NSE. The opening trade: ₹310, a modest 1.3% premium. No fireworks, no doubling on day one. Just solid, steady appreciation—exactly the kind of debut that matched the company's character.

But the real story wasn't in the listing price—it was in what the IPO revealed about the business. Post-listing, promoter shareholding contracted from 55% to 48%, while IFC's 18% stake declined to 11%. This dispersion of ownership was healthy. No single entity controlled the company anymore; it truly belonged to the market.

The IPO proceeds utilization plan was pragmatic: working capital for margin funding, technology investments, and general corporate purposes. No moonshot projects, no ambitious acquisitions. Just steady investment in the core business.

What made Angel's IPO particularly interesting was the timing within the industry context. Zerodha, despite being larger, remained private. HDFC Securities and ICICI Securities were subsidiaries of banks. Angel was now India's largest listed pure-play retail broking company—a unique position that would attract both retail and institutional investors.

The market reception validated the digital transformation strategy. In terms of hardcore numbers, it was the fourth largest in terms of NSE active clients, and second largest in terms of incremental NSE Active Clients during Q1FY2021. These weren't legacy metrics from the physical era—these were digital-age achievements.

The IPO also marked a governance transition. Public listing meant quarterly earnings calls, analyst scrutiny, and regulatory oversight beyond SEBI's brokerage regulations. For a company that had weathered regulatory challenges, this additional transparency was welcomed, not feared.

Initial trading weeks saw the stock find its range between ₹280-₹330. No volatile swings, no operator-driven movements. The stock was behaving exactly like the company—steady, predictable, trustworthy. Institutional investors were accumulating positions, retail investors were holding.

The IPO's success had broader implications. It proved that traditional Indian businesses could successfully transform and access capital markets. It showed that investors valued digital transformation stories, especially when backed by real metrics. Most importantly, it demonstrated that in India's financial services sector, trust and technology weren't mutually exclusive—they were multiplicative.

Six months post-IPO, the stock had appreciated nearly 100%. The company was adding customers at record pace. Revenues were growing. And Dinesh Thakkar, the 12th-grade dropout from Bhilwara, was now running a publicly-listed company worth over ₹4,000 crores.

The IPO wasn't an end—it was an enabler. With public currency, strong capital base, and market validation, Angel was ready for its next transformation. The company that had gone from physical to digital was about to go from broking to everything.

VII. Angel One Rebranding & Business Model Evolution (2021–Present)

- The company drops "Broking" from its name, becoming simply "Angel One." This wasn't cosmetic surgery—it was a declaration of intent. The company that had spent 25 years perfecting stockbroking was signaling it was now much more.

The rebranding came with a philosophical shift: from transaction facilitation to customer education. Angel One positioned itself not just as a broker but as a financial companion. The tagline evolved, the logo modernized, but more importantly, the entire product architecture was reimagined.

The pricing revolution intensified: ZERO cost brokerage for cash delivery trades, flat ₹20 per order for Intraday and F&O. This wasn't sustainable by traditional brokerage economics. But Angel One wasn't playing by traditional rules anymore. They were building a platform business where brokerage was the acquisition tool, not the profit center.

The Angel One Super App launched as an AI-driven platform for multiple asset classes. This wasn't just adding products—it was creating an ecosystem. Mutual funds, IPOs, bonds, insurance, loans—each product wasn't a separate P&L but a node in a network. The more products a customer used, the higher their lifetime value and the lower the probability of churn.

The geographic expansion post-rebranding was remarkable. Angel One tapped new territories, onboarding millions from tier-2 and tier-3 cities. While competitors fought over Mumbai and Bangalore's millennials, Angel was capturing Indore's entrepreneurs and Lucknow's professionals. By 2022, they had 13.8 million clients and 4.3 million active clients on NSE.

The technology stack underwent complete overhaul. The platform designed for serious traders featured real-time charting, advanced indicators, basket orders, and algorithmic trading capabilities. But beneath the sophisticated features was intuitive design—a farmer in Punjab could start with simple delivery trades and gradually explore F&O as their confidence grew.

The AI implementation wasn't just buzzword compliance. Machine learning models predicted customer churn, recommended products, and identified cross-selling opportunities. Natural language processing powered customer service. Pattern recognition flagged potential fraud. This wasn't fintech theater—it was operational enhancement at scale. The numbers validate the strategy. Angel One's client base jumped 61% to 27.49 million in September 2024 as compared with 17.07 million in September 2023. By December 2024, the client base had reached 29.52 million, up 51.7% year-over-year. This wasn't just customer acquisition—it was market capture at unprecedented scale.

The innovation continued with pioneer services like 'Trade in One Hour'—rapid client activation that compressed the traditional multi-day account opening process into minutes. This wasn't just operational efficiency; it was behavioral insight. Angel understood that in India, financial decisions are often impulsive. Strike while the iron is hot, or lose the customer forever.

The flat fee structure's impact was transformative. Traditional brokers charging percentage-based fees couldn't compete. But more importantly, flat fees democratized trading. A ₹10,000 trade cost the same as a ₹10 lakh trade. This wasn't just pricing—it was social justice through capitalism.

Product expansion accelerated. The company expanded its third-party financial product offerings to include unsecured loans, motor insurance, and fixed deposits. Each product addition was strategic—loans leveraged customer data for credit scoring, insurance provided recurring revenue, fixed deposits increased wallet share. The Super App wasn't just aggregation; it was orchestration.

The cultural transformation inside Angel One was equally dramatic. The company that once prided itself on personal relationships now celebrated API integrations. SmartAPI allowed algorithmic traders to connect directly. Smart Store facilitated rule-based trading. This was a 180-degree pivot from the handholding model of the past.

Geographic expansion into tier-2 and tier-3 cities wasn't just market development—it was nation-building. Angel One was bringing sophisticated financial products to cities that banks had ignored. A shop owner in Bhopal could now trade F&O. A teacher in Ranchi could invest in US stocks. This was financial inclusion at scale.

The business metrics reflected the transformation's success. Average daily turnover (ADTO) grew to Rs 43,487 billion, a 54.5% year-on-year increase. But more importantly, the customer mix had fundamentally changed. These weren't just traders—they were investors, borrowers, insurance buyers. Each customer represented multiple revenue streams.

By 2024, Angel One had become unrecognizable from its 2019 avatar. The company that started as a traditional broker was now a financial services platform. The physical network that seemed like baggage had become a competitive advantage in customer service. The ethical foundation that seemed quaint in the age of algorithms had become the trust layer enabling expansion into lending and insurance.

The rebranding from Angel Broking to Angel One wasn't just dropping a word—it was declaring independence from a single product category. The company was no longer defined by what it did (broking) but by whom it served (the aspiring Indian). This subtle shift in identity would prove crucial for the next phase of growth.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation that McKinsey would teach in business schools. Angel One's market cap stands at ₹24,001 crore, with revenue of ₹4,973 crore and profit of ₹994 crore. But raw numbers don't capture the operational leverage story unfolding beneath.

Consider the revenue trajectory. The company crossed ₹1,250 crore in revenue, growing from ₹725 crore in FY20. That's a 72% increase in just a few years, during a period that included a pandemic, market crashes, and intense competition. This wasn't just growth—it was growth during disruption. The Q2 FY25 results marked historic milestones: consolidated profit after tax of ₹423.4 crore (up 39% YoY), total revenue of ₹1,515 crore (up 44% YoY). These were the company's highest ever revenue, EBITDA, and net profit. This wasn't just growth—it was profitable growth at scale.

Average daily turnover increased dramatically from Rs. 253,176 million in Q1 FY20 to Rs. 618,945 million in Q1 FY21—a 145% increase during the pandemic. By 2024, ADTO had reached Rs 43,487 billion, reflecting the explosive growth in retail trading activity and Angel's ability to capture market share.

The market share evolution tells the real story. Angel's share in active NSE clients increased from 4.8% in Q1 FY20 to over 12% by Q4 FY22. Market share in equity ADTO surged from 3.7% to 21.2% in the same period. This wasn't organic growth—this was market conquest.

But then came challenges. Q4 FY25 results showed pressure: net profit declined 48.7% to ₹174.5 crore, revenue fell 22.2% to ₹1,056 crore. The culprit? New F&O regulations restricting weekly expiries and increasing lot sizes. This wasn't company-specific weakness—it was regulatory headwind affecting the entire industry.

The ownership structure evolution is equally telling. Promoter holding decreased from 35.61% as of Sep 2024 to 28.97% as of Jun 2025. This wasn't distress selling—it was planned dilution to increase free float and improve liquidity. The company wanted institutional investors, and institutional investors wanted larger free float.

Revenue composition had fundamentally shifted. Brokerage, which once dominated revenue, now shared space with interest income from margin funding, distribution fees from third-party products, and advisory fees. The company had successfully transformed from transaction-dependent to diversified revenue streams.

The unit economics improved dramatically post-digital transformation. Customer acquisition cost plummeted from thousands of rupees per customer in the physical era to hundreds in the digital age. Lifetime value increased as customers used multiple products. The LTV/CAC ratio, the holy grail of platform businesses, turned decisively positive.

Geographic revenue distribution revealed the transformation's success. Tier-2 and tier-3 cities, once negligible contributors, now drove majority of new customer additions and increasingly significant revenue share. This wasn't just market expansion—it was market creation.

The capital efficiency metrics were impressive. Return on equity consistently above 30%. Asset-light model meant minimal capital requirements for growth. The company could fund expansion through internal accruals rather than constant dilution or debt.

Comparison with peers highlighted Angel's unique position. While Zerodha remained larger in absolute terms, Angel was growing faster. While ICICI Securities had brand advantage, Angel had cost advantage. While new fintechs had venture capital, Angel had profitability.

The dividend policy reflected confidence. The board approved a final dividend of Rs 26 per share for FY 2024-25, maintaining generous shareholder returns even while investing heavily in growth. This wasn't financial engineering—it was genuine cash generation.

By 2024, Angel One had achieved what seemed impossible in 2018: transformed from a traditional broker to a digital platform while maintaining profitability, growing market share, and generating cash. The financial performance validated the transformation strategy. The market position confirmed the competitive advantage. The question now wasn't whether the transformation worked—it was how far it could go.

IX. Technology & Innovation Strategy

The Angel One Super App isn't just another trading platform—it's a trojan horse for financial services domination. Built on microservices architecture, deployed on cloud infrastructure, and powered by artificial intelligence, this is what happens when you give engineers carte blanche to reimagine financial services from first principles.

The platform architecture is elegantly complex. At its core lies a matching engine capable of processing millions of orders per second. But speed is table stakes in modern broking. The real innovation is in the intelligence layer above—machine learning models that predict user behavior, recommend trades, and prevent fraud in real-time.

SmartAPI, launched for algorithmic traders, was a masterstroke. Rather than fight the algo trading revolution, Angel embraced it. The API allows institutional traders and sophisticated retail investors to connect their trading systems directly. Every API call is revenue. Every algorithm is a customer locked into Angel's ecosystem.

The Smart Store feature introduced rule-based trading for retail investors. Set conditions, forget about monitoring, let the system execute. This democratized algorithmic trading—you didn't need to code to create trading strategies. It was visual programming for financial markets.

Real-time charting with advanced indicators might seem standard, but Angel's implementation is different. The charts aren't just displaying data—they're learning from user interactions. Which indicators do users combine? What patterns precede trades? This behavioral data feeds back into product development and risk management.

Basket orders—the ability to execute multiple trades simultaneously—solved a real problem for serious traders. But the genius was in the implementation. The system didn't just execute baskets; it optimized them for minimal market impact and maximum execution probability. This was institutional-grade technology delivered to retail investors.

The AI implementation deserves special attention. Natural language processing powers the customer service chatbot, handling 80% of queries without human intervention. But the same NLP engine also scans social media for sentiment analysis, news for market-moving events, and customer communications for satisfaction signals.

Pattern recognition algorithms flag unusual trading patterns that might indicate fraud, market manipulation, or system gaming. But the same algorithms also identify high-value customers before they churn, trading opportunities before they're obvious, and product gaps before customers complain.

The personalization engine is perhaps the most sophisticated component. Every user sees a different app—different products highlighted, different educational content served, different trading ideas suggested. This isn't random; it's based on trading history, risk profile, and peer behavior. The app literally learns and adapts to each user.

The "Trade in One Hour" service showcased operational innovation. Traditional account opening involved multiple steps, document verification, and manual processing—often taking days. Angel compressed this into minutes through OCR for document reading, AI for verification, and automated decision-making for approval. The technology wasn't revolutionary; the application was.

The mobile-first approach went beyond responsive design. The app was built for mobile from ground up—not a desktop platform squeezed onto phones. Touch gestures for trading, biometric authentication for security, push notifications for market alerts. The phone wasn't just an access device; it was the primary platform.

The data architecture supports real-time analytics at massive scale. Every click, every trade, every customer interaction generates data streams processed in real-time. This isn't just for reporting—it drives dynamic pricing, risk management, and product recommendations. The company knows more about its customers' financial behavior than traditional banks know after decades of relationship.

The technology stack is deliberately polyglot. Different problems require different solutions. High-frequency trading components run on C++. Web services use Node.js. Machine learning models deploy in Python. Data processing happens in Scala. This isn't technology for technology's sake—it's choosing the right tool for each job.

Security infrastructure is military-grade. Multi-factor authentication, end-to-end encryption, real-time threat detection. But security isn't just defensive—it's a product feature. Customers trust Angel with their money because the technology demonstrably protects it.

The innovation pipeline reveals future ambitions. Blockchain for settlement, augmented reality for market visualization, voice trading through smart speakers. Some experiments will fail, but the willingness to experiment is what separates Angel from traditional brokers.

Cloud infrastructure provides infinite scalability. Traffic spikes during market volatility don't crash systems. New features deploy without downtime. Geographic expansion doesn't require data center construction. This operational flexibility is competitive advantage.

The partner ecosystem amplifies capabilities. APIs connect to banks for instant fund transfers, insurance companies for product distribution, mutual fund houses for investment processing. Angel isn't building everything—they're orchestrating everything.

The technology transformation from 2019 to 2024 is staggering. From a company that processed trades on legacy systems to one running sophisticated AI models. From physical forms to instant digital onboarding. From human-driven operations to automated processes. This wasn't evolution—it was metamorphosis.

But technology alone doesn't explain Angel's success. The real achievement was making sophisticated technology accessible to unsophisticated users. A farmer in Punjab might not understand machine learning, but they can use an app that uses machine learning to help them trade better. That's the real innovation—not the technology itself, but its democratization.

X. Playbook: Business & Investing Lessons

Building Trust in a Low-Trust Industry

Angel One's first lesson is counterintuitive: in industries with trust deficits, ethics isn't a constraint—it's a competitive advantage. When Dinesh Thakkar started in 1996, emphasizing transparency and ethics seemed naïve. The market rewarded aggressive players who pushed boundaries. Yet Angel's consistent ethical stance became its moat. Trust compounds slower than capital but lasts longer than technology advantages.

The trust-building wasn't passive. Every regulatory fine, every SEBI action was met with process improvement, not legal maneuvering. When algorithmic trading threatened traditional brokers, Angel didn't lobby against it—they built APIs for it. When discount broking disrupted pricing, Angel didn't complain—they went to zero brokerage on delivery trades. Trust meant adapting to market evolution, not resisting it.

Timing Digital Transformation: Not Too Early, Not Too Late

Angel's digital transformation timing was perfect—and perfectly calculated. They weren't first movers like Zerodha (2010) or fast followers like HDFC Securities (2000s). They waited until 2019, when digital infrastructure was mature, smartphone penetration was significant, and customer behavior had shifted. This wasn't procrastination—it was patience.

The lesson: digital transformation isn't about being first; it's about timing the intersection of technology maturity, customer readiness, and organizational capability. Angel had all three by 2019. Earlier transformation would have been expensive and risky. Later would have been too late.

Democratizing Finance Through Technology and Pricing

Zero brokerage on delivery trades wasn't sustainable by traditional metrics. But Angel wasn't playing the traditional game. They understood that in platform businesses, customer acquisition is everything. Brokerage was the hook; lifetime value came from margin funding, distribution fees, and advisory services.

This is the platform playbook: identify the highest-friction customer acquisition point (brokerage fees), eliminate it (zero brokerage), then monetize through adjacent services. Amazon did it with free shipping. Google did it with free search. Angel did it with free delivery trades.

Network Effects in Digital Brokerage

Angel's 11,000 authorized persons became unexpected network nodes. Each AP brought local relationships, trust, and distribution. But digitization turned them from cost centers to network amplifiers. They became educators, influencers, and support agents. The physical network enhanced the digital platform rather than competing with it.

The lesson: existing assets aren't always liabilities during transformation. The key is reimagining their role. Angel's APs went from order-takers to customer success managers. The network effect wasn't just digital—it was hybrid.

Managing Regulatory Relationships While Innovating

Angel's regulatory strategy was sophisticated. They didn't avoid regulators or aggressively lobby. Instead, they engaged constructively, fixed problems quickly, and often exceeded compliance requirements. When F&O regulations tightened, Angel didn't fight—they adapted their product mix.

The playbook: in regulated industries, regulatory relationship is a core competency. Not compliance—relationship. Understanding regulatory intent, preempting concerns, and demonstrating good faith creates space for innovation.

The India Opportunity: 5% Equity Penetration

Only 5% of Indians invest in equity markets. This isn't a statistic—it's an opportunity. Angel's geographic expansion into tier-2 and tier-3 cities isn't just market development; it's market creation. Every new investor they onboard isn't stolen from competitors—they're created from non-consumption.

The investing lesson: the biggest opportunities aren't in fighting for market share in saturated segments but in creating new markets. Angel isn't competing with Zerodha for Mumbai's day traders—they're creating equity investors in Ranchi.

Capital Allocation: Tech Investment vs. Customer Acquisition

Angel's capital allocation reveals priorities. Heavy technology investment during 2019-2020 preceded aggressive customer acquisition in 2021-2024. This sequencing matters. Build the platform first, then scale. Premature scaling on weak infrastructure would have been catastrophic.

The framework: infrastructure investments should precede growth investments. It's tempting to chase growth, but sustainable growth requires sustainable infrastructure. Angel built the pipes before turning on the water.

The Platform Transition

Angel's evolution from broker to platform follows a clear pattern: start with core competency (broking), achieve dominance, then expand adjacently (margin funding, distribution), finally platform-ize (Super App). Each stage built on the previous, reducing execution risk.

The lesson for entrepreneurs: platform ambitions are good, but platform foundations are better. Angel spent 20 years perfecting broking before attempting platform transformation. Domain expertise preceded platform expansion.

Cultural Transformation

Transforming a 25-year-old traditional broker into a tech-first platform required cultural revolution. Angel didn't fire everyone and hire engineers. They retrained, reskilled, and reimagined roles. The authorized person who once filled forms now helps customers navigate apps. The branch manager who managed paper now manages digital onboarding metrics.

This is perhaps the hardest lesson: technological transformation without cultural transformation fails. Angel succeeded because they transformed people, not just processes.

The Compound Effect

Every element of Angel's strategy compounds. Trust builds customer acquisition. Customers drive data. Data improves products. Better products increase retention. Higher retention justifies technology investment. Technology reduces costs. Lower costs enable better pricing. Better pricing drives acquisition. The flywheel accelerates.

Understanding these compounding loops is crucial for investors. Linear businesses face constant headwinds. Platform businesses with compounding advantages face tailwinds. Angel transformed from the former to the latter.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Inevitable Financialization of India

India's equity market penetration at 5% compared to 55% in the US isn't a gap—it's destiny delayed. As GDP per capita crosses $3,000, financial savings historically explode. India is at that inflection point. Angel One, with 29.52 million clients and growing 50%+ annually, is perfectly positioned to capture this secular trend.

The demographic dividend is undeniable. 65% of Indians are under 35. These digital natives don't fear equity markets like their parents did. They've seen crypto volatility, survived COVID crashes, and still keep investing. Angel's median customer age dropping every quarter validates this thesis.

The digital-first model with strong unit economics is the killer combination. Customer acquisition cost under ₹500, lifetime value over ₹5,000, and improving with every product addition. The margin funding book grows 25% quarterly without additional capital. The distribution fees from mutual funds and insurance provide recurring revenue. This isn't just a broker—it's a financial services vending machine.

Brand strength in tier-2 and tier-3 cities is underappreciated. While competitors fight over saturated metros, Angel owns Indore, Surat, and Rajkot. These cities are where India's next 100 million investors will emerge. Angel's 11,000-person ground network gives them unmatched rural reach.

The product suite expansion beyond broking creates multiple revenue streams. Mutual funds, insurance, loans, fixed deposits—each product increases wallet share and switching costs. A customer with five products doesn't leave for 10 rupees lower brokerage.

Cost leadership through technology is sustainable. Angel's technology infrastructure, built on cloud and microservices, scales infinitely without proportional cost increases. Every additional million customers actually reduces per-customer service cost.

Bear Case: The Disruption Ahead

Competition from discount brokers is intensifying, not abating. Zerodha remains larger and more profitable. Groww is growing faster and has better brand recall among millennials. New entrants backed by venture capital can afford to lose money longer than Angel can afford to compete.

Regulatory risks in financial services are ever-present. SEBI's recent F&O restrictions decimated volumes. Future regulations on margin funding, algorithmic trading, or distribution fees could severely impact profitability. Angel's history of regulatory actions, while resolved, shows vulnerability.

Market volatility directly impacts trading volumes and therefore revenue. A prolonged bear market or reduced retail participation would hit Angel disproportionately. Unlike banks with lending books or insurers with premiums, Angel's revenue is transaction-dependent.

Customer acquisition costs are rising industry-wide. The easy customers—urban, educated, employed—are already acquired. The next 100 million customers will be harder to acquire, costlier to serve, and generate lower revenue. The unit economics that work today might not work tomorrow.

Technology disruption from new entrants is a constant threat. What if WhatsApp launches trading? What if Google offers zero-cost investing? What if crypto platforms pivot to equity? Angel's technology moat is only as deep as the next innovation cycle.

The margin funding book, while profitable, carries risk. In market downturns, retail investors leveraged through margin funding face forced selling. Bad debts could spike. Angel's limited experience in credit risk management compared to traditional NBFCs is concerning.

The Balanced View

The truth lies between extremes. Angel One has successfully transformed from a traditional broker to a digital platform—a rare achievement. Their customer base is real, growing, and engaged. The India opportunity is massive and secular.

But competition is fierce, regulations are tightening, and technology disruption is accelerating. Angel's success attracted attention—from competitors, regulators, and disruptors. The easy growth is behind them; the hard growth lies ahead.

For investors, the key question isn't whether Angel One will grow—they will. It's whether they can maintain profitability while growing, whether they can defend against disruption while disrupting others, whether they can expand products without losing focus.

The valuation at ₹24,000 crore implies significant growth already priced in. The P/E ratio of 24.72 isn't cheap for a financial services company. The market expects Angel to continue growing at 40%+ while maintaining margins. That's a high bar.

The regulatory overhang is real but manageable. Every SEBI action teaches Angel to be better. Every restriction creates opportunity for innovation. The company that survived the 2013 probe and transformed during COVID can probably handle future challenges.

The investment case ultimately depends on time horizon and risk appetite. For long-term investors believing in India's financialization, Angel offers direct exposure. For short-term traders worried about regulation and competition, the volatility might be uncomfortable.

What's certain is that Angel One is no longer a simple broker. It's a platform, a distribution network, a technology company, and a financial services provider. Whether that complexity is a strength or weakness depends on execution. So far, they've executed well. The next five years will determine if they can continue.

XII. Epilogue & "What's Next"

The conference room at Angel One's Mumbai headquarters, 2029. Dinesh Thakkar, now 61, looks at a holographic display showing real-time customer metrics. 75 million customers. ₹100,000 crore market cap. Operations in six countries. The 12th-grade dropout from Bhilwara has built something extraordinary. But he's not done.

The immediate future is clear: expand services to include more financial products. The mutual funds business, already growing 100% annually, will rival traditional AMCs. Insurance distribution, currently nascent, will become a major revenue driver. The lending business, carefully built on customer data, will challenge traditional NBFCs.

Strategic partnerships with fintech companies are accelerating. Rather than build everything, Angel is becoming the platform on which others build. Payment companies integrate for seamless transactions. Wealth-tech startups use Angel's APIs for execution. Research firms distribute through Angel's network. The company is becoming the AWS of Indian financial services.

Geographic expansion possibilities are intriguing. The Indian diaspora in UAE, Singapore, and the US wants access to Indian markets. Angel's technology platform, already cloud-native, can serve them without physical presence. International expansion isn't just possible—it's inevitable.

But the real future lies in something more fundamental: reimagining what a financial services company can be. Angel isn't content being India's largest broker or even India's leading fintech. They want to be India's financial operating system—the platform through which Indians interact with money.

Imagine opening Angel One and seeing not just your portfolio but your complete financial life. Bank accounts aggregated. Loans tracked. Insurance monitored. Taxes calculated. Investments optimized. Payments processed. All through one app, one relationship, one company you trust.

The technology exists. The customer base is ready. The regulatory environment, while complex, is navigable. The question isn't whether Angel can build this future—it's whether anyone can stop them.

The India opportunity remains massive. Current penetration of 5% in equity markets could reach 15% by 2030. That's 200 million investors, up from 50 million today. If Angel maintains just their current market share, they'll have 60 million customers. If they execute their platform strategy, they could have 100 million.

The transformation lessons are clear. First, timing matters more than speed. Angel waited for the right moment to transform and then moved decisively. Second, existing assets can enable transformation if reimagined correctly. The 11,000-person network that seemed like baggage became a competitive advantage. Third, trust is the ultimate moat in financial services. Technology can be copied, prices can be matched, but trust must be earned.

For entrepreneurs, Angel's journey offers hope. You don't need pedigree to build something significant. You don't need to be first to win. You don't need venture capital to scale. What you need is deep customer understanding, patient execution, and willingness to transform when the moment arrives.

For investors, Angel represents a specific bet: that India's financial services will digitize, democratize, and consolidate around platforms. It's a bet that execution matters more than innovation, that trust matters more than technology, that serving tier-2 India matters more than impressing tier-1 VCs.

The risks are real. Competition intensifies daily. Regulations tighten quarterly. Technology disrupts constantly. But Angel has survived and thrived through multiple crises, transformations, and disruptions. They've proven adaptability, which in business, as in evolution, is the ultimate survival trait.

The final lesson might be the most important: transformation is not a destination but a journey. Angel transformed from sub-broker to broker, from broker to digital broker, from digital broker to platform. The next transformation—to financial operating system—is already underway.

Dinesh Thakkar's vision of making Angel One the largest retail broking house in the country has been achieved. But visions, like companies, must evolve. The new vision—democratizing financial services for a billion Indians—is orders of magnitude more ambitious. Based on the track record, betting against them would be unwise.

The story of Angel One is far from over. In fact, it might just be beginning. The company that started in 1996 serving a few hundred clients in Mumbai now serves 30 million across India. The next chapter—serving 100 million across the world—is being written now.

For those watching from the sidelines, the message is clear: the financialization of India is not a trend—it's a generational transformation. Companies that capture this wave will create enormous value. Angel One isn't just riding the wave; they're helping create it.

The boy from Bhilwara who entered Mumbai's financial markets with nothing but ambition has built something that will outlast him. That's the ultimate entrepreneurial achievement: building something bigger than yourself, something that serves millions, something that transforms an industry and maybe, just maybe, a nation.

The angel, it turns out, was in the details all along.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube