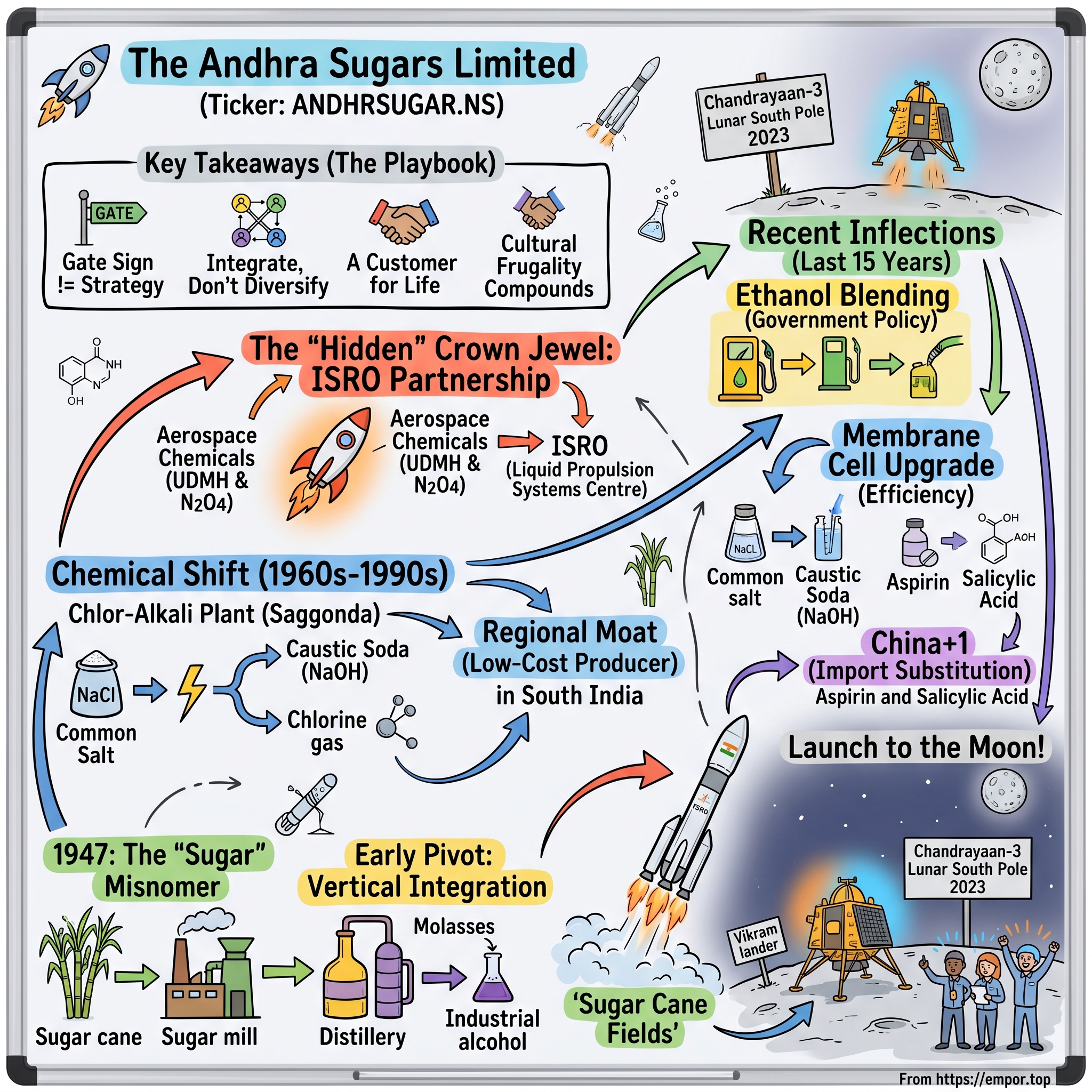

The Andhra Sugars: The Rocket Fuel of India

I. Introduction & The "Sugar" Misnomer

On the evening of August 23, 2023, a small four-legged Indian lander named Vikram (विक्रम) extended its struts over a patch of grey-black regolith near the Moon's south pole and quietly settled into the dust. India had become the fourth country in history to soft-land on the lunar surface, and the very first to do it near the south pole.1 Cameras cut to ISRO (भारतीय अंतरिक्ष अनुसंधान संगठन Indian Space Research Organisation) mission control in Bengaluru, where men in collared shirts hugged each other while women in saris wiped tears off their glasses. Cable news anchors lost their minds. Prime Minister Narendra Modi, video-conferencing from Johannesburg, called it "the dawn of a new India."

Nobody mentioned a sleepy delta town in coastal Andhra Pradesh called Tanuku (తాణుకు).

But you can be very sure that somewhere along the muddy bend of the Vasista Godavari river, in a chemical plant that smells faintly of chlorine and burnt molasses, the engineers of a company called The Andhra Sugars Limited (ఆంధ్ర షుగర్స్ లిమిటెడ్) cracked open a box of mithai. Because the storable, hypergolic, devil's-brew of propellants that pushed Chandrayaan-3 (చంద్రయాన్-3) through its trans-lunar burns, the same chemistry that has been climbing India out of Earth's gravity well for forty years, was almost entirely made by them.2

This is the story of how a sugar mill became a rocket fuel company. Or, more honestly, the story of how a "sugar" company stopped being a sugar company at all — and how the market has spent the better part of two decades trying to figure out what to call the thing that emerged.

The Andhra Sugars Limited (NSE: ANDHRSUGAR) is, on paper, a small-cap Indian listed company. Its consolidated revenue is in the band where a single bad monsoon or one government policy tweak can swing earnings double-digit percentage points. The name on the marquee says "Sugars." The Bombay Stock Exchange classifies it under the sector "Sugar." Screener.in lists it next to companies that make jaggery and confectionery.

And yet, look closely at the segment reporting, and you find a portfolio that has almost nothing in common with its industry classification.

Caustic soda. Chlorine. Aspirin. Salicylic acid. Industrial-grade sulphuric acid. Captive thermal and wind power. And — this is the part that makes it interesting — Unsymmetrical Dimethylhydrazine and Nitrogen Tetroxide, two of the most carefully handled molecules on the subcontinent, manufactured under contract for the Liquid Propulsion Systems Centre of ISRO.2

For a company that has spent decades hiding in plain sight under a commodity label, Andhra Sugars is a near-perfect case study in what Acquired.fm fans would recognise as a "hidden compounder" — a regional, family-run industrial that has quietly migrated its centre of gravity away from a cyclical, regulated base business and toward a small, defensible, almost monopolistic specialty franchise. The market still prices it roughly like a sugar mill. The cash flows tell a different story.

Over the next two hours, we are going to take that story apart. We will start in 1947, on the eve of Indian independence, with a young Telugu industrialist named Mullapudi Harischandra Prasad (మల్లపూడి హరిశ్చంద్ర ప్రసాద్) who decided that a free India needed its own sugar mills. We will trace how that one mill in Tanuku slowly bled outward into industrial alcohol, then into chlor-alkali, then — in one of the most consequential and least publicised pivots in Indian corporate history — into liquid rocket propellants. We will examine why a country that has launched 100-plus successful orbital missions trusts a single mid-cap chemical company in coastal Andhra to produce its hypergolic fuels. And we will walk through, candidly, what could go wrong.

So buckle in. We are going from sugar cane to the Moon, with a stop at a chlor-alkali cell along the way.

A note on framing before we begin. This is, in part, a story about the slow, unsexy work of building industrial capability inside a country that, for most of its post-independence history, was systematically excluded from global supply chains by sanctions, treaties, and the cost of imported technology. Almost nothing about the Andhra Sugars story makes sense outside that context. The company is, in many ways, a vehicle for understanding how India did the unglamorous work of industrialising itself one product line at a time — and how a small number of family-owned industrials, working in dialogue with state and central governments, ended up holding strategically critical positions that nobody outside their immediate ecosystem fully appreciated until decades later.

II. Founding & The Vision of Harischandra Prasad

In the summer of 1947, while Cyril Radcliffe was drawing borders across northern India with a fountain pen and Lord Mountbatten was haggling over the date of independence, a different sort of drawing was happening in a modest office in the Krishna-Godavari delta. A young industrialist named Mullapudi Harischandra Prasad — already part of a prominent zamindari and trading family in Tanuku — was sketching out the layout of what he wanted to be one of free India's first private-sector sugar mills. The drawings were rudimentary by modern standards, done in pencil on tracing paper, marked up in a mix of English engineering notation and Telugu marginalia. They were also, in a quiet way, an act of political optimism: betting that the new nation about to take its first breath at midnight on August 14 would honour the industrial ambitions of its private citizens.

To understand why this mattered, you have to understand what sugar meant to the late-colonial Indian economy. Sugar was not just a commodity. It was, alongside textiles and steel, one of the politically symbolic industries — the kind of business where Indian nationalists wanted to prove that a self-governing India could outproduce the British plantation system that had dominated tropical agriculture for two centuries. The Indian Sugar (Control) Order had been promulgated during the Second World War. Cane prices were already politicised. And the new Congress government, even before Independence Day, was making it clear that domestic industrialists who could deploy capital into agro-processing would have a friendly ear in Delhi.

Harischandra Prasad — known to his family simply as HP, and later eulogised in the regional press as the "Industrial Lion of Andhra" — had spent his early career helping run the family's commodity trading and rice-milling operations.[^3] He was, by every account, a relentless, hands-on industrialist with a near-religious obsession with the engineering details of his factories. The story told in Tanuku, and repeated by old plant hands well after his passing in 2011, is that during construction of the first sugar mill he insisted on personally inspecting the alignment of the cane carrier, climbed onto the structure in his dhoti, and would not come down until the calibration was right. He was the kind of founder who learned thermodynamics by reading textbooks at night and the kind of capital allocator who would walk past the air-conditioned office and sit in the boiler room to understand the steam balance.

The cultural context is worth pausing on, because it shaped the company that emerged. Mid-century Andhra, in particular the Godavari delta, was a region of relatively prosperous agrarian Brahmin and Kamma landlord families that had begun to migrate capital from land into industry and commerce in the early twentieth century. Tanuku itself sat at the centre of an unusually fertile cane and paddy belt, watered by the Godavari and connected by rail to both Chennai and Hyderabad. The town had old money, mercantile networks, and — equally important — political relationships with the early Congress establishment. Harischandra Prasad would later be associated, in various civic and trade-body capacities, with the broader project of building southern Indian private industry as a counterweight to the Marwari and Gujarati business houses that had dominated colonial-era commerce.

The Andhra Sugars Limited was formally incorporated in 1947 as a public limited company, with the first sugar factory at Tanuku. Within a few years, the company added a second facility at Taduvai and began experimenting with what would, in hindsight, become its most consequential decision: rather than treating molasses — the gooey, dark brown by-product of sugar refining — as a waste stream to be sold off cheaply, the company invested in a distillery to convert it into industrial alcohol.

This sounds prosaic. It was not. In the regulatory architecture of 1950s India, a license to manufacture industrial alcohol from molasses was a non-trivial moat. The "License Raj" — the system under which everything from output capacity to raw material allocation was approved by a central bureaucracy — meant that a private firm holding a distillation license effectively had a small, protected monopoly inside its catchment area. By the early 1960s, Andhra Sugars was not just a sugar mill. It was a sugar-and-alcohol complex, with cane growers feeding the front end and a downstream chemical chain pulling more value out of every tonne.

That move — turning a waste product into a feedstock — would become the organising philosophy of the company for the next seventy years. Every time the firm has decided to expand, the bias has been toward vertical integration: take whatever is sitting in the by-product tank at the end of one process and figure out whether it can become the input of a new one. Molasses fed industrial alcohol. Industrial alcohol fed downstream chemicals. Chlorine, when it eventually came online, fed a portfolio of derivatives. Even the heat from the boilers fed the captive power plant.

If this all sounds like the playbook of a German Mittelstand company crossed with a Gujarati family conglomerate, that is more or less the right intuition. The promoter group — primarily the Mullapudi clan, with allied marriages and shareholdings extending into a network of related industrial houses across coastal Andhra — ran the business with what one veteran Hyderabad-based fund manager described in conversation as "engineering-first, balance-sheet-second" instincts. Debt was kept low. Expansion was funded out of internal accruals. Dividends, even in the lean years, were not skipped. The corporate office, even today, sits not in Mumbai or Hyderabad but in Tanuku itself — a town of barely 80,000 people, two hours by road from the nearest jet airport.

There is a small but telling detail in the company's early documentation. Where most Indian industrial groups of the 1950s and 1960s used the language of "expansion" and "diversification" in their annual report chairman letters, Andhra Sugars persistently used a different word: "integration." The framing matters. Diversification, in business school terms, means owning unrelated businesses to spread risk. Integration means owning the steps adjacent to your existing operations, so that each step strengthens the others. From the very first decade, the company had picked a side: it was going to be an integrated industrial complex, not a holding company of unrelated industrial bets.

That cultural DNA — frugal, technical, regionally rooted, allergic to financial pyrotechnics — would later make Andhra Sugars an unusually credible counterparty for a customer with a very low tolerance for error. We will get to that customer in two sections. For now, the important thing is that by the late 1960s, the company had outgrown the label on the gate.

III. The Great Pivot: Sugar to Chemicals

There is a particular kind of trap that catches a lot of Indian agro-industrial businesses, and Andhra Sugars, by all rights, should have died inside it.

The trap is sugar itself.

Sugar in India is a regulated commodity in roughly the same way that the price of bread in 1970s Eastern Europe was a regulated commodity — which is to say, almost nothing about its economics is set by supply and demand. The central government dictates the minimum price the mill must pay the farmer for cane, known as the Fair and Remunerative Price. State governments, especially in Uttar Pradesh and Maharashtra, layer on a State Advised Price that can be even higher. The final price at which the mill can sell refined sugar is, for chunks of every cycle, capped by export and stock-holding restrictions. Until the early 2010s, mills were also required to surrender a portion of their output to the government at a discounted "levy" price, to be redistributed through the public distribution system.

You can imagine what this does to the economics.

In a good year, the gap between cane cost and sugar realisation is comfortable. In a bad year — when a bumper monsoon floods the cane belt and the central government simultaneously hikes the FRP to keep farmer voters happy — the entire industry loses money simultaneously. Sugar mills go through five-year boom-bust cycles with the metronomic predictability of a pendulum.

A purely sugar-focused company in this environment is, in capital allocation terms, almost unmanageable. You can be the most efficient cane crusher in your state and still lose money for two years out of every five. Sitting in Tanuku in the 1960s, watching the first of these cycles play out, the Mullapudi family made a decision that would define the next sixty years of the company's identity: they were going to use the cash from sugar to buy their way into a business that the central government couldn't price-control them out of.

That business was chlor-alkali.

The chemistry here is worth a brief detour, because it is so foundational that without it modern industrial life genuinely does not exist.

You take ordinary common salt — sodium chloride, NaCl — dissolve it in water, and run an electric current through the brine. The current rips apart the molecules. Out of one end of the cell you get caustic soda (sodium hydroxide, NaOH), a corrosive alkali that is used in everything from soap-making to aluminium refining to paper pulp bleaching. Out of the other end you get chlorine gas, which is the feedstock for PVC plastics, water disinfectants, pesticides, and a long tail of organic chemistry. As a free bonus, the process produces hydrogen, which can be burned for heat or used in further chemical synthesis.

A chlor-alkali plant, in other words, is a salt-and-electricity machine that turns one of the cheapest input bundles on earth into half a dozen industrial commodities that the modern economy cannot do without. The catch — and it is a real one — is that the process is extraordinarily electricity-intensive. Power can account for half or more of variable cost. The other catch is that the technology has come in waves: first mercury cells (now banned in most countries on environmental grounds), then diaphragm cells, then the modern membrane cell, which is dramatically more energy-efficient but requires a heavier upfront capex.

By setting up a chlor-alkali unit in Saggonda (సగ్గొంద), in the West Godavari district, Andhra Sugars solved several problems at once. It put itself near coastal salt supply. It positioned itself in a state with cheap thermal and, later, renewable power. It built engineering capability that was transferable, with modest adaptation, to a much wider chemical product slate. And — critically — it diversified the revenue mix away from a single regulated commodity into a portfolio of industrial chemicals where pricing was set by industrial supply and demand rather than by the food ministry.

The decision was also, in retrospect, a stroke of timing. The 1970s and 1980s were the years in which India's domestic chemical industry was being constructed essentially from scratch, in the slow-moving, license-rationed style of the planned-economy era. Capacity additions were approved one factory at a time. A company that managed to get a chlor-alkali license through the regulatory process in this period found itself, almost mechanically, holding a quasi-monopoly in its geographic catchment for years afterward, because new competing capacity simply could not be approved fast enough to challenge it. The same regulatory friction that throttled the broader Indian economy in those decades was, for incumbents who had already cleared the licensing hurdle, a moat. Andhra Sugars sat inside that moat in coastal South India for a decade and a half before liberalisation arrived.

The 1980s were spent expanding caustic soda capacity. The 1990s, especially after the 1991 liberalisation that finally dismantled the worst excesses of the License Raj, allowed the company to think about exports and downstream derivatives. By the late 1990s, Andhra Sugars' segment reporting was already showing chlor-alkali contributing a meaningful share of operating profit, even as sugar remained the larger top-line contributor. The mix had quietly inverted on the margin side first.

There is a wonderful, slightly mischievous detail buried in this story. The same molasses-to-alcohol playbook the company had run in its early years was now being repeated one level up the chemistry stack. Caustic soda and chlorine came out of the same cell. Hydrogen came out as a by-product. Sulphuric acid was made on-site to neutralise process streams. Every intermediate had a downstream use. The Tanuku-Saggonda complex was becoming, slowly, a fully integrated chemical campus that just happened to have a sugar mill bolted onto one end.

By the time the 21st century opened, the strategic question facing the next generation of management was no longer "should we be in chemicals or sugar?" The chemicals had won. The question was: what is the highest-margin, most defensible chemistry we can possibly do with this set of capabilities? And the answer to that question was sitting, almost literally, in the boil-off tank of a hydrazine pilot plant a few hundred kilometres south.

Before we get there, one detail about the 1991 liberalisation moment is worth noting because it speaks to the company's posture during periods of sweeping change. Many Indian industrials, when the License Raj began to dismantle, raced to capture share through aggressive capacity additions, joint ventures with foreign multinationals, and balance-sheet leverage. A meaningful number of those expansions ended badly in the slowdown of the late 1990s and the Asian Financial Crisis. Andhra Sugars did not race. The company added capacity steadily, kept leverage modest, did not enter foreign joint ventures it could not control, and preserved its option to invest counter-cyclically. The lesson, internalised early, was that booms end and the only thing that survives a downturn is a balance sheet you can sleep with at night.

IV. The "Hidden" Crown Jewel: The ISRO Partnership

To explain what happened next, we have to leave coastal Andhra for a moment and go to the headquarters of the Liquid Propulsion Systems Centre of ISRO, in Valiamala, Kerala.

It is the early 1980s. India has just demonstrated, with the SLV-3 mission of 1980, that it can put a satellite into orbit using indigenous solid-fuel rockets. The next-generation vehicle on the drawing board — what would eventually become the Polar Satellite Launch Vehicle, or PSLV — is going to need liquid propulsion stages.

The reason is straightforward physics.

Solid-fuel rockets are wonderfully simple, but they cannot be throttled or shut down mid-burn. For the precise orbital insertions that satellite operators need, you want a liquid stage that you can turn on, throttle, and turn off.

Liquid hydrogen and liquid oxygen are the most performant combination, but they are also cryogenic, meaning they have to be stored at temperatures so low that the entire vehicle architecture becomes more complex. For storable upper stages — the kind you can keep loaded in a rocket on the pad for hours or days — the propellant chemistry of choice in the 1980s, used by Europe's Ariane program and by India's emerging launcher family, was a pair of room-temperature liquids that ignite spontaneously on contact.

The fuel is Unsymmetrical Dimethylhydrazine, or UDMH.

The oxidiser is Nitrogen Tetroxide, or N2O4.

Mix them and they explode. There is no need for an ignition system, no spark plug, no electric igniter — the chemistry does it for you. This is what engineers call hypergolic propulsion, and it is the same family of chemistry that powered the Apollo lunar module's ascent stage and that flies on the Ariane upper stages.

Reliable. Storable. Lethal if mishandled.

The simplest analogy for a non-chemist is this: imagine two perfectly ordinary-looking liquids in two perfectly ordinary-looking tanks. They are at room temperature. They are happily inert when stored separately. The moment a valve opens and they meet inside a combustion chamber, they react with such violence and such consistency that you can design an entire rocket engine without ever having to worry about whether it will light. For a satellite that has been sitting in geostationary orbit for ten years and now needs to fire its station-keeping thrusters, this matters enormously: cryogenic propellants would have boiled off, electric ignition systems might have failed, but hypergolic chemistry just works. That reliability is the whole reason the propellant family has stayed in service across multiple generations of launchers and spacecraft, including India's own.

The catch — and this is the part that mattered for Andhra Sugars — was that UDMH and N2O4 are extraordinarily difficult to make at aerospace grade. The purity specifications are punishing. Hydrazine derivatives are toxic to the point of being treated as warfare-grade hazards in industrial regulation. Most countries that have rocket programs either make their hypergolic fuels in state-owned defence facilities or import them under tightly controlled bilateral agreements. India, in the post-1974 nuclear test isolation, did not have that option. The hydrazine had to be made indigenously.

The geopolitical dimension cannot be overstated. After Pokhran-I in 1974, India found itself under the kind of technology embargo that has shaped its industrial strategy ever since. The Missile Technology Control Regime, established in 1987, codified what was already happening informally: high-purity propellants, rocket-grade materials, and key precursors were not going to be available to India through normal commercial channels. The country had three options. It could give up on a serious space program. It could try to source materials through grey-market channels with all the attendant strategic risks. Or it could build its own indigenous supply base, slowly, painstakingly, with whatever domestic chemical companies it could persuade to take on the work. India chose option three, and Andhra Sugars became one of the small handful of private partners that made that choice viable.

In the early 1980s, ISRO began looking for an Indian private-sector partner that could be trusted to set up a hydrazine production unit under defence-grade quality and security protocols. The shortlist was small. The company needed an existing chemical manufacturing footprint, a track record with the central government, the engineering bench to absorb technology transfer, and — frankly — the patience to work on a contract whose volumes would be small but whose specifications would be impossibly tight. The plant would need to operate under personnel security clearances, with restricted access, with the kind of safety culture more commonly associated with nuclear facilities than with mid-cap chemical companies. Most private-sector competitors of the era either lacked the technical bench or — more often — looked at the project economics and concluded that the volumes were too small to justify the operational complexity.

Andhra Sugars, with its growing Saggonda complex and its decades-long relationship with the state and central governments, fit the bill. There is an interesting cultural dimension to why this worked. The Mullapudi family's posture toward government counterparties was neither adversarial nor obsequious — it was professionally cooperative in a way that earned trust over time. The company did not have a Mumbai or Delhi corporate affairs office aggressively lobbying for favours. It had a Tanuku-based set of engineers who showed up on time, delivered on spec, and treated the security and quality protocols with the seriousness the customer demanded. For an organisation like ISRO, which had been burned more than once by suppliers who underestimated the discipline required for aerospace work, this was the right cultural fit.

What followed was the establishment of the Aerospace Chemicals division at Saggonda — a dedicated propellant manufacturing facility for ISRO.2 The company also became a long-running supplier for several other specialty molecules ISRO uses. Over the subsequent four decades, this small, almost invisible division would grow into one of the most strategically important moats in the entire Andhra Sugars portfolio.

Think about what this contract actually is, from a business-strategy lens. Andhra Sugars is the qualified domestic source of storable liquid propellants for India's primary launch vehicles. The customer is, for practical purposes, captive — India's national space agency does not have a meaningful alternative domestic supplier. The product is non-substitutable inside ISRO's current launcher architecture; you can't decide one Friday that you'd like to use a different fuel without redesigning the engine. The certification process to even bid on this kind of business takes years and involves the Indian defence research establishment. And the volumes, while small in tonnage terms, carry margins that look nothing like a commodity chemical line item.

That, in Hamilton Helmer's framework, is a "Cornered Resource" power in close to its purest form. The resource is the qualification itself — the combination of regulatory clearance, technology transfer, and decades of zero-defect supply history. A new entrant cannot simply build a hydrazine plant in Gujarat next year and underbid. The barrier is not capital, it is trust.

Pause on that point, because it is the kind of moat that does not show up easily in financial statements but matters enormously in a strategic valuation. The aerospace propellants segment, on any given year's reported revenue, is a fraction of the consolidated top line. If you were a passive screener filtering for "specialty chemical exposure," this division would barely register. And yet, in the only meaningful counterfactual — what would it take for ISRO to qualify a new propellant supplier from scratch — the answer is "at least a decade and several billion rupees of investment by the central government in standing up a parallel capability." That is the definition of a structural barrier.

The most recent chapter in this story moved into an even higher-stakes domain. In 2022, the company announced that it had been awarded a contract by ISRO to set up a liquid hydrogen plant, supporting India's next-generation cryogenic upper stages and the Gaganyaan (గగన్యాన్) human spaceflight program.[^4] Liquid hydrogen is the high-energy fuel that lets you carry more payload to higher orbits — the same chemistry that flies on the upper stages of SpaceX's Falcon and on the Space Shuttle's main engines. For ISRO's pivot toward heavier launchers and crewed missions, securing a domestic liquid hydrogen supply was not optional, it was a sovereign capability question. The fact that the contract went to Andhra Sugars, rather than to a fresh defence PSU stood up specifically for the purpose, is the clearest possible signal of how deeply embedded the Tanuku company is in India's strategic supply chain.

Pause for one moment on the technology, because the engineering challenge here is meaningfully different from anything the company had done before. Hydrazine derivatives are storable at room temperature. Liquid hydrogen is not. It boils at minus 253 degrees Celsius — only twenty degrees above absolute zero — and at atmospheric pressure it boils away if you so much as look at the tank funny. Storing it, transporting it, and loading it into a rocket requires a level of cryogenic engineering that until recently existed in India only inside ISRO's own facilities and one or two state-owned gas companies. For a chemical company to step into this domain is, in technical complexity terms, a step-change from anything in the company's prior operating history. The fact that ISRO awarded the contract is a measure of confidence; the fact that the company accepted it is a measure of ambition.

It is also, almost certainly, the single most underappreciated optionality in the stock. Liquid hydrogen has a second life as the swing fuel of the global energy transition — green hydrogen, made from renewable electricity, is the most-discussed decarbonisation vector for heavy industry. A company that already operates a chlor-alkali plant (which produces hydrogen as a by-product) and is now building cryogenic liquefaction capability is positioned at a very interesting intersection.

We will see whether that optionality materialises. For now, the story is simpler: a sugar mill in Tanuku owns one of the most strategically protected niches in Indian industrial chemistry.

V. Recent Inflections: The Last 15 Years

Walk through the gates of the Saggonda complex on a humid March afternoon and the first thing that hits you is the scale.

The plant has expanded almost continuously since the mid-2000s, with the most aggressive bursts of capex landing between 2010 and 2018 as the company migrated its caustic soda capacity from older diaphragm and mercury cells to modern membrane cell technology. This is one of those decisions that looks boring from a press-release distance and turns out to be enormously consequential when you read the financials a decade later.

Membrane cell electrolysers are the current gold standard in chlor-alkali. They consume meaningfully less electricity per tonne of caustic soda produced than the older diaphragm cells they replaced, and they avoid the mercury contamination issues that have caused regulators across India, Europe, and East Asia to push the industry off mercury entirely. The trade-off is the upfront cost: a full membrane cell line is a serious capex commitment, and the payback comes through reduced power cost per tonne over many years of operation. In capital allocation terms, this is exactly the kind of investment that family-controlled industrials tend to make well and that quarterly-earnings-managed corporates tend to defer. The benefit is multi-year and operational; the cost is immediate and visible. A management team that owns its stock and plans in decades is structurally better positioned to make this call than one whose compensation depends on next year's EBITDA.

Andhra Sugars financed this transition largely out of internal accruals and modest term debt, sticking to the family's traditional aversion to over-leveraging the balance sheet. The result, by the late 2010s, was a chlor-alkali franchise that operated at lower variable cost per tonne of caustic soda than several of its larger, listed-on-the-Nifty competitors — including the Western Indian peers we will discuss in a moment. The strategic logic was straightforward: in a commoditised business, the only durable moat is being the lowest-cost producer in your regional catchment, and you only get to be the lowest-cost producer if you keep modernising the plant on a steady cadence rather than waiting for one big bang.

The second great inflection of the last fifteen years was on the sugar side, and it came not from anything the company did but from a policy shift in New Delhi.

In 2013, the Government of India began seriously expanding the Ethanol Blending Programme, under which oil marketing companies are mandated to blend ethanol with petrol at progressively higher percentages.3 What started as a 5% target crept upward over the following decade. By the early 2020s, the government had set an explicit roadmap toward 20% ethanol blending — a policy that fundamentally rewrote the economics of every sugar mill in India that owned a distillery.

The reason is almost too good for a sugar company.

Ethanol can be made from C-heavy molasses (the final by-product of sugar refining), from B-heavy molasses (an intermediate stream pulled out earlier in the process at the cost of some sugar yield), or directly from sugarcane juice. The government, in setting procurement prices, deliberately pegged the ethanol price high enough that mills had a meaningful incentive to divert sugar into ethanol.

For a company like Andhra Sugars, which had been making industrial alcohol from molasses since the 1950s and had the distillation infrastructure already on the ground, this was the policy equivalent of someone showing up at your door with a printing press for cash.

The result, across the Indian sugar industry, has been a structural margin uplift for distillery-equipped mills, partially insulating them from the worst of the cane-price cycle. For Andhra Sugars specifically, the ethanol opportunity has converted the sugar segment from a perpetual margin headache into a more balanced contributor.

The third recent inflection — quieter than the other two, but arguably the most interesting from a moat-building perspective — has been the company's steady expansion in salicylic acid and aspirin. Aspirin (acetylsalicylic acid) is one of the oldest synthetic pharmaceuticals on earth. Salicylic acid is its immediate precursor and also has standalone uses in dermatology and cosmetics. Both molecules have been dominated, on the global commodity supply side, by Chinese producers for the last two decades.

Andhra Sugars has been one of a small handful of Indian producers that has methodically expanded capacity in these intermediates, positioning itself as the domestic alternative to Chinese imports for India's large generic pharmaceutical industry.4 In the post-2020 environment, when the Indian government's "China+1" supply chain rhetoric translated into actual procurement preferences for domestic API intermediates, this division began to look less like a sleepy commodity line and more like a beneficiary of national industrial policy. The capacity additions in Aspirin manufacturing put the company into a position to materially address the import substitution opportunity for Indian formulators.

There is a second-order point here that is easy to miss. The salicylic acid and aspirin franchise sits inside the broader industrial chemicals umbrella at Tanuku, sharing utilities, engineering services, and quality infrastructure with the rest of the chemical complex. A standalone aspirin plant would carry its own fixed-cost overhead. An aspirin line bolted onto an integrated chemical site dilutes those overheads across multiple revenue streams. This is the same logic that makes the entire integrated complex more profitable than the sum of its parts, and it is one of the reasons a small, regionally concentrated player can compete on cost against much larger pure-play competitors in any single product line.

The thread tying these three inflections together is consistent: in each case, Andhra Sugars was already operating the underlying asset at the moment the policy or technology shift created the opportunity. The membrane cell upgrade landed during the global chlor-alkali commodity upcycle. The distillery footprint was decades old when the ethanol policy made it strategically valuable. The aspirin plant was already producing when "China+1" became a procurement preference. Strategy people call this "optionality on existing assets." Industrialists call it "luck favouring the prepared."

It is worth highlighting that this pattern — where pre-existing capability meets policy or market tailwind — is the single most reliable way that mid-cap Indian industrials have created compounding shareholder returns over the last twenty years. It is the opposite of the venture capital pattern, where you bet on a future technology and hope the market arrives. It is the slow-money pattern, where you operate a competent, integrated facility for decades and harvest the upside when the world finally needs what you already make. Andhra Sugars is the textbook example of the second pattern, and that pattern is increasingly rare in a market that prizes narrative growth above operational competence.

VI. Segment Analysis & "Hidden" Units

If you crack open the latest annual report and turn to the segment disclosures, the picture that emerges is, frankly, not the picture suggested by the gate sign or the BSE sector code.5

The company reports across four primary business segments, and the way revenue and profit distribute across them is the single most important fact for an investor trying to understand this stock.

The sugar and spirits segment is, in any given year, a non-trivial share of consolidated revenue. It carries volume but typically carries thinner margins. The cane crushing operation runs seasonally, the distillery runs nearly year-round, and the realisations are a function of central and state government policy more than any management decision. In a tough cane cycle this segment can earn very modest returns on capital; in a benign year with strong ethanol pricing it can earn a respectable contribution. But it almost never sets the company's earnings trajectory.

The chlor-alkali segment — caustic soda, chlorine, hydrochloric acid, and the related downstream chemicals — is the cash cow. It is the segment that pays for the capex of the other segments. Margins here are cyclical but structurally higher than sugar, and in the up-cycles of 2021–2022, caustic soda realisations across the Indian industry surged on the back of strong global demand for alumina (which uses caustic soda in the Bayer refining process) and the disruption of European supply during the energy crisis. Andhra Sugars participated in that up-cycle from a position of low-cost production, and the segment contribution to operating profit during those quarters was disproportionate.

The industrial chemicals and aerospace propellants segment is where the strategic moat lives. The propellant business itself is small in tonnage and cannot be disclosed in granular pricing detail because of the defence-sensitivity of the customer relationship, but the segment margins are visibly the highest in the portfolio. This is the line item that, in any given year, represents perhaps the most underappreciated optionality in the stock — both for its embedded strategic value and for its connection to the liquid hydrogen and Gaganyaan opportunities.

The power segment is the unsung supporting cast. The company operates captive thermal power capacity at the Saggonda complex and has been a long-running investor in wind energy in coastal Andhra Pradesh and Tamil Nadu. The strategic logic is straightforward: in an industry where electricity is half of variable cost, owning your own generation — and increasingly your own renewable generation — is not a side project, it is competitive infrastructure. The wind portfolio also gives the company a small but useful hedge against grid power price volatility and, increasingly, a marketable green energy story for ESG-sensitive customers.

The diagnostic that matters here, and the one Acquired listeners will recognise immediately, is the revenue-versus-profit divergence. The sugar segment dominates the casual narrative of the company. Even the name reinforces that narrative. But in a typical year, the majority of consolidated operating profit comes not from sugar but from the chemicals stack — caustic soda, industrial chemicals, and propellants combined. The segment that gives the company its public identity is, more often than not, the segment that contributes the smaller share of bottom-line earnings.

This is the crux of why the stock has historically traded at what you might call a "sector misclassification discount." Index funds and screeners that bucket the company alongside sugar mills price it on sugar-mill multiples. Investors who do the segment work see something more like a regional specialty chemicals company with embedded aerospace optionality and a sugar-flavoured cyclical hedge. Closing that valuation gap has been a slow process, and it remains incomplete.

The other under-appreciated unit in the portfolio is what the company describes simply as "Other Operating Income" — a catch-all for renewable energy certificates, carbon credits, by-product sales, and miscellaneous specialty chemicals. In any single year these are not large numbers. But they speak to a broader cultural posture: in an integrated industrial complex, almost nothing leaves the gate as pure waste. Heat is captured. By-products are sold. Slag from the boilers, gypsum from the sulphuric acid neutralisation, even the bagasse from sugar cane crushing — all of it has a downstream user. The plant is, in its quiet way, a circular industrial economy that long predates the marketing term.

A second-layer diligence point worth flagging here is on environmental and regulatory exposure. Caustic soda is a heavy-emissions industry by any measure, and hydrazine derivatives are subject to some of the most stringent hazardous-chemical handling regulations in Indian law. The company has so far navigated this regulatory environment without a public enforcement action of note, but the surface area of risk is real and worth monitoring. A material environmental incident at the Saggonda complex — particularly one involving the aerospace chemicals division — would be both an operational and a strategic event. Conversely, the company's progressive shift toward membrane cell technology, captive renewable power, and circular by-product use means that on a per-tonne basis, the carbon and environmental intensity of operations has been declining for over a decade. For ESG-mandated investors who look past the sector code, the picture is more nuanced than it first appears.

VII. Current Management & Capital Allocation

There is a particular type of Indian listed company where, if you sit through enough earnings calls, you start to recognise a kind of conversational fingerprint.

The management speaks slowly. They are conservative on guidance. They are reluctant to forecast more than one quarter out. When an analyst pushes for a specific number, the CFO will say "let us see how the monsoon develops" or "the cane availability picture is yet to crystallise." Outsiders sometimes find it frustrating. Long-term shareholders find it reassuring.

Andhra Sugars sits squarely in that tradition. The company has been run, for two generations, by the Mullapudi and Pendyala families, with allied promoter holdings spread across a network of related entities and trusts. Promoter holding has historically been well over 45%, a level that signals both alignment and absolute control.6 The current generation of leadership operates as a joint-managing-director structure, with the family branches sharing executive responsibility in a way that is unusual by the standards of Mumbai-listed corporates but very characteristic of southern Indian family businesses.

The current Joint Managing Director, Mr. Mullapudi Thimmaraja, represents the founding family in operational leadership.[^9] The collegial structure across the promoter group spreads decision-making responsibility — and, equally importantly, succession risk — across multiple branches of the controlling families. This is not the style of a Reliance-grade family corporate where one patriarch makes every call. It is the style of a quiet southern industrial dynasty where consensus is the operating culture and the next generation has been trained inside the company for decades.

If you have ever sat through a senior Indian family-business meeting where four or five family members each command operational respect and one of them is, almost imperceptibly, the first among equals — that is the texture of how decisions actually get made at Andhra Sugars. It is slower than a Mumbai-style top-down call. It is also more durable against single points of failure. The downside, of course, is that pivots are slower; the upside is that pivots, once made, are made with full institutional weight behind them.

The capital allocation philosophy that emerges from this culture has been remarkably consistent: prefer greenfield expansion to acquisitions; fund growth out of internal accruals and modest term debt; keep promoter pledges low or non-existent; pay a steady dividend rather than chase aggressive buybacks; and be willing to sit out periods of capital market exuberance if no genuinely productive use of capital is available.

You can see this philosophy in the negative space of the company's history. Andhra Sugars has not done a transformational acquisition in living memory. It has not chased the buyout-of-a-distressed-rival deals that periodically appear in the Indian chemical industry. It has not made an out-of-state move into a geography where it had no operational footprint. When competitors used the 2010s commodity cycle to leverage up balance sheets and chase scale through M&A, Andhra Sugars sat out and built membrane cell capacity at home.

To make this concrete, contrast the company's posture with that of its publicly listed chlor-alkali peers. Gujarat Alkalies and Chemicals Limited (GACL) is a state-promoted heavyweight with a much larger caustic soda footprint and the financial cushion of Gujarat state ownership. DCM Shriman is a diversified industrial conglomerate with chlor-alkali, sugar, and fertilisers across multiple states. Aditya Birla Chemicals (now part of Grasim Industries) is the scale leader in Indian chlor-alkali, with all the financial muscle of the Aditya Birla group behind it. Compared to those names, Andhra Sugars is a small, regionally concentrated, family-run operator.

But — and this is the part that often gets missed — being small and regionally concentrated has its own advantages in chlor-alkali. Caustic soda is heavy, corrosive, and expensive to transport. Owning the lowest-cost production capacity in your specific geographic catchment is more valuable than owning a larger but more distant footprint. Within the southern Indian market — Andhra, Tamil Nadu, Karnataka — Andhra Sugars is a deeply embedded incumbent with logistics economics that a Gujarat-based competitor cannot easily replicate.

Think about it from the perspective of a downstream customer in, say, Visakhapatnam or Chennai who needs reliable caustic soda for water treatment, paper pulp, or detergent manufacture. A truckload of caustic soda from Tanuku is a one-day delivery. A truckload from Bharuch or Vadodara is a multi-day haul across half the country, with the associated freight cost, breakage risk, and inventory holding penalty. The Gujarat producer can win the order only by accepting a meaningful price discount; the local producer, all else equal, captures the freight differential as margin. Multiply that across a few thousand customer relationships and you have a regional moat that pure scale at a distance cannot dissolve.

The same conservative posture extends to disclosure. The company's investor relations footprint is modest. There is no quarterly investor day in Mumbai. There is no glossy ESG report attempting to claim leadership on every UN Sustainable Development Goal. The annual report, available through the investor relations portal,5 is plainly written, technically detailed, and largely free of the marketing varnish that has crept into a lot of mid-cap Indian disclosures. For investors who like their information dry, this is a feature. For investors who like their managements to sell them a story, it is a friction.

Capital returns to shareholders have come primarily through dividends. The company has paid a dividend for an unbroken stretch of decades, which in an industry as cyclical as sugar and chlor-alkali is a non-trivial achievement. There has been no aggressive buyback program. There has been no flashy bonus issue. The compounding has happened in the operational metrics — capacity, margins, segment mix — rather than in financial engineering.

The fingerprint of this whole posture, captured in a phrase, is what one Hyderabad-based fund manager memorably called the "Tanuku style" — a culture of frugality, engineering rigour, and skepticism toward Mumbai corporate fashion. It is not a style that wins many points at industry conferences. It is a style that, over forty years of regulated commodity cycles and policy shifts, has kept a small-cap company on the public markets continuously, fully solvent, and increasingly valuable.

One concrete capital allocation question worth lingering on is what the company does with its operating cash flow when the chemicals up-cycle delivers a windfall quarter. The short answer is: very little that is dramatic. The company has not historically used cyclical peaks to fund out-of-character acquisitions, to launch a Mumbai office, or to pivot into adjacent industries where it has no engineering bench. Instead, the cash typically goes into a combination of debt repayment, modest dividend increases, and the next phase of capex at Saggonda. From a long-term shareholder's perspective, this is the right posture even if it lacks fireworks. Cyclical peaks are exactly the moments when management teams make the worst long-term decisions, because the temptation to extrapolate is strongest. Andhra Sugars has, with notable consistency, refused that temptation.

VIII. Strategy: Hamilton's 7 Powers & Porter's 5 Forces

Now let us put the company into a proper strategy framework, because the moat structure of Andhra Sugars is one of the most interesting puzzles in the Indian small-cap universe.

If you tried to fit a single label onto the business, you would fail. The sugar mill template is wrong. The pure-play chlor-alkali template is wrong. The specialty chemicals template gets closer but doesn't capture the regulated-commodity legacy. The defence supplier template captures the aerospace business but misses the rest of the operating portfolio. The honest answer is that this is a hybrid entity, and the way to value it correctly is to value each segment on its own terms and sum the parts — accepting that the market, for structural reasons, will probably continue to give the consolidated entity a discount to that sum-of-the-parts number.

Hamilton's 7 Powers

Start with Hamilton Helmer's 7 Powers. Of Helmer's seven categories — Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power — Andhra Sugars credibly possesses three, partially possesses a fourth, and has essentially none of the other three.

Cornered Resource (strong).

The strongest power, by a long distance, is Cornered Resource. The aerospace propellant business is the textbook case: a long-running, government-blessed, technology-transferred, security-cleared supply relationship with a sovereign customer whose alternative options for domestic supply are essentially zero. New entrants cannot bid their way in, because the "resource" is not the plant itself but the accumulated qualification — decades of zero-defect supply, security clearances at the personnel level, technology transfer arrangements with ISRO. This is precisely the kind of power that takes generations to build and cannot be replicated by a balance sheet.

Scale Economies (regional).

The second power is Scale Economies, but with an important geographic qualifier. Andhra Sugars is not the largest chlor-alkali producer in India — Aditya Birla's chemicals arm is much larger nationally. But in the southern Indian catchment, where transport economics matter and customer relationships are sticky, Andhra Sugars is a low-cost regional incumbent. The fixed-cost dilution that comes from operating an integrated Tanuku-Saggonda complex — sharing utilities, captive power, logistics, and engineering services across multiple chemistries — produces real unit-cost advantages that a single-product competitor at the same scale cannot easily match.

Process Power (partial).

The third, partially possessed power is Process Power. The company has spent decades operating hydrazine derivatives, caustic soda chemistries, and aspirin synthesis in close physical proximity. The institutional knowledge embedded in the engineering bench at Tanuku — the operational know-how to keep these very different chemistries running safely on a shared utility backbone — is itself a competitive asset. It is not, however, a Process Power in the same sense that, say, Toyota's production system is: it is more a function of cumulative operational experience than of a codified, reproducible methodology.

Powers absent.

The powers Andhra Sugars does not have are equally instructive. There is no meaningful branding power; nobody buys caustic soda because it has the Andhra Sugars label. There are no network effects. Switching costs in commodity chemicals are real but modest — a buyer can re-qualify a competing supplier in months. Counter-positioning, where an incumbent's existing business model prevents them from competing with you, is not really applicable in this industry structure.

Porter's 5 Forces

Now let us turn to Porter's 5 Forces — a different lens, more about industry structure than firm-specific moats.

The threat of new entrants is low to moderate, varying sharply by segment.

In sugar, the entry barrier is essentially government licensing — you cannot just start a sugar mill in a cane catchment that has not been allocated to you. In chlor-alkali, the entry barrier is capital intensity and environmental clearance; in modern India, getting an environmental clearance for a new chlor-alkali plant is a multi-year regulatory project. In aerospace propellants, the entry barrier is effectively absolute — only the Indian government can bless a new domestic supplier of hypergolic fuels.

Bargaining power of buyers is also segmented.

In sugar, the buyer is essentially the central and state government via levy mechanisms and procurement policy; buyer power is high. In caustic soda, buyers are large industrials with multiple supplier options and meaningful negotiating leverage. In aerospace propellants, the buyer is monopsonistic, but the dependency runs both ways — ISRO has no alternative, and as long as the relationship is healthy, buyer power is effectively neutralised.

Bargaining power of suppliers is dominated by two inputs: salt and power.

Salt is a low-margin commodity sourced from coastal salt pans; supplier power is low. Power is more interesting — Andhra Sugars has progressively reduced its exposure to grid power volatility by building captive thermal and renewable capacity, which is a deliberate strategy of supplier-power neutralisation.

The threat of substitutes is segment-specific.

There is no real substitute for caustic soda in most of its industrial applications. There is no substitute for storable hypergolic propellants in ISRO's existing launcher architecture, at least until the company designs entirely new engines. There are substitutes for cane sugar in some applications, but not enough to materially threaten the segment.

Industry rivalry is where the picture is most variable.

Sugar industry rivalry is intense and entirely price-based, exacerbated by government policy. Chlor-alkali rivalry is regional and shaped by transport economics, with periodic price wars in oversupply periods. Aerospace propellants have essentially no rivalry in the Indian market.

The integrated picture that emerges is of a company that has built genuine, durable competitive advantage in a small, strategically important niche (aerospace propellants), occupies a defensible regional position in a commoditised core business (chlor-alkali), and accepts a structurally tough, government-controlled commodity exposure in its legacy business (sugar). That is a portfolio with two strong moats and one structurally low-quality leg, which is, all in all, a more interesting risk-return profile than the sector classification would suggest.

There is one more frame worth applying here, which Acquired listeners will recognise from the show's discussion of conglomerates. Charlie Munger used to argue that the most durable businesses are the ones where multiple complementary advantages stack on top of each other in the same operating entity — a phenomenon he called "lollapalooza" effects. Andhra Sugars is, in a modest way, an example. The chlor-alkali plant produces hydrogen as a by-product, which feeds further synthesis. The captive power plant uses bagasse from sugar cane, closing one loop. The sulphuric acid produced for process use also has downstream sales. The Tanuku-Saggonda site shares engineering, safety, and quality infrastructure across propellants, chlor-alkali, sugar, and pharma. None of these is individually a game-changing moat. Stacked together inside a single integrated complex, they make it remarkably difficult for any single-product competitor to underprice the equivalent product from Andhra Sugars on a fully loaded basis.

IX. Bull Case, Bear Case, and Myth vs Reality

Let us steelman both sides, because a company this contradictory deserves both arguments at full strength.

This is the moment in any Acquired-style deep dive where we deliberately separate the question of "is this a good business" from the question of "is this a good investment at any given price." A great business at the wrong price can be a poor investment. A mediocre business at the right price can be an excellent one. The work we have done in the preceding sections establishes that Andhra Sugars is, by most reasonable strategic measures, a more interesting business than its sector classification implies. Whether that business is correctly priced is a separate exercise that depends on the entry multiple, the cycle position, and the time horizon of the holder.

The Bull Case

The bull case starts with the proposition that Andhra Sugars has, for two decades, been priced as a sugar mill but operated as a specialty chemical company with aerospace optionality.

As the ethanol blending policy continues to roll forward toward the 20% target, the sugar segment itself becomes structurally more profitable. As the membrane cell chlor-alkali capacity runs at full utilisation through an extended industrial up-cycle, the cash cow throws off cash faster than the company can deploy it. As ISRO ramps from a single-digit annual launch cadence toward a much higher cadence — driven by commercial satellite business, the Gaganyaan crewed program, and the lunar and Mars follow-up missions — the aerospace propellants and the new liquid hydrogen line become structurally more valuable. And as global pharmaceutical supply chains continue to de-risk away from Chinese sole-sourcing, the salicylic acid and aspirin franchise becomes a small but defensible beneficiary of "China+1."

Layer on top of that the conservative balance sheet, the high promoter holding, the consistent dividend track record, and the very real possibility that an extended re-rating from "sugar mill" to "specialty chemical company with embedded aerospace exposure" could meaningfully change the multiple the market is willing to pay. That is, in short, the long-term compounder thesis: an integrated, founder-family-controlled, low-debt, southern Indian industrial that has quietly accumulated three or four distinct margin engines and is paid to wait while the market figures it out.

The Bear Case

The bear case is equally well-developed.

Start with the most obvious risk: input price volatility. Chlor-alkali profitability is a direct function of power cost and salt price, and while the company has worked hard to insulate itself, it cannot fully escape these. Sugar profitability is, despite the ethanol upside, still fundamentally hostage to cane FRP increases and central government price interventions. A single tough monsoon or a single politically motivated FRP hike can compress segment-level economics meaningfully.

The second leg of the bear case is the conglomerate discount. The market does not, in general, pay full sum-of-the-parts multiples for diversified small-cap industrials. The very thing that makes Andhra Sugars interesting — the patchwork portfolio — is also what makes it hard for institutional investors to underwrite with conviction. The stock has, for long stretches, traded at multiples that imply the market is giving almost no credit to the aerospace business at all.

The third leg is succession and governance. A family-run company is only as durable as the alignment between its branches. Andhra Sugars has, by all visible evidence, managed this transition well across multiple generations. But succession risk is, by its nature, a tail risk that is invisible until the moment it isn't. The collegial joint-MD structure mitigates this, but does not eliminate it.

The fourth leg is the specific cyclicality of caustic soda. The 2021–2022 caustic soda up-cycle, which lifted segment margins across the industry, has been followed by softer realisations as European supply has come back online and global demand has cooled. Investors who underwrote Andhra Sugars at peak chlor-alkali margins will have to recalibrate expectations through the down-cycle. The mistake to avoid here is treating the peak as the baseline; the chlor-alkali industry has run in cycles for as long as it has existed, and there is no reason to believe this cycle is different.

There is also a fifth leg worth flagging, which sits in the category of regulatory tail risk. The aerospace propellants business depends, in the end, on a single sovereign customer and a single regulatory framework. Any meaningful change in ISRO's procurement model — say, a decision to in-source propellant manufacturing into a defence PSU, or to multi-source the contract across additional private players — would dilute the structural moat in this segment. The probability of such a shift is, on the available evidence, low. But it is non-zero, and a thoughtful long-term investor should at least be aware of where the foundation stone sits.

Myth vs Reality

Now, the myth vs reality section, because the consensus narrative on this company is wrong in a couple of specific ways.

Myth 1: It's a sugar company.

The first myth is that Andhra Sugars is "primarily a sugar company." This is the narrative the name and sector code reinforce. The reality, as we have established, is that the chemicals stack — chlor-alkali plus industrial chemicals plus aerospace propellants — typically delivers the majority of consolidated operating profit. Sugar is the historical anchor, not the present-day economic engine.

Myth 2: ISRO is a vanity line item.

The second myth is that the ISRO business is a "vanity" line item that does not move the needle. This too is wrong, in two ways. First, the propellant margins are meaningfully higher than commodity chemical margins, so even a modest revenue line punches above its weight at the operating profit level. Second, the optionality — the liquid hydrogen plant, the cryogenic capability, the potential green hydrogen tie-in — is the kind of small-but-strategic position that does not show up in this year's earnings but could matter quite a lot over a five-to-ten-year horizon.

Myth 3: It's a sleepy old-economy laggard.

The third myth, and this one is held by certain bear-side investors, is that Andhra Sugars is a "sleepy old-economy company that can't compete with modern speciality chemical firms." The plant-level evidence does not support this. The membrane cell migration was completed on schedule. The aspirin capacity additions came online with appropriate quality clearances. The liquid hydrogen capex is being executed against ISRO timelines. This is a company that does not advertise its operational execution, but it executes.

KPIs to Track

If you are looking for the one or two or three KPIs that matter most for tracking this company's ongoing performance, they are:

KPI 1: Caustic soda ECU realisation.

First, the chlor-alkali (caustic soda) ECU realisation — the "electrochemical unit" price that the industry uses as shorthand for combined caustic-and-chlorine economics. This is the single most important profit-driver in the portfolio at any given quarterly read.

KPI 2: Ethanol procurement price.

Second, the ethanol procurement price set by the central government for each supply year, in conjunction with the company's mix of B-heavy and direct cane-juice ethanol production. This is the swing factor that determines whether the sugar segment is a drag or a contributor.

KPI 3: Aerospace order book and capex milestones.

Third, the order book and capex execution timeline for the aerospace and industrial chemicals segment, particularly the liquid hydrogen plant ramp and any new ISRO contract announcements. This is the segment where small revenue moves translate into outsized strategic re-rating optionality.

Everything else — power costs, salt prices, working capital, dividend rate — is important, but if you have to triage attention, those three KPIs are where the action is.

One last note on competitive benchmarking before we close the section. Within the broader Indian chlor-alkali peer set, the most informative comparisons are with Gujarat Alkalies and Chemicals (GACL), DCM Shriram, and the chemicals arm of Grasim (incorporating the legacy Aditya Birla Chemicals). Each of these names has a meaningfully larger national footprint than Andhra Sugars. None of them carries an aerospace propellants franchise. None of them is family-controlled in the same Tanuku style. The right way to read Andhra Sugars against this peer set is not "smaller version of the same thing" but "different beast entirely, with overlapping product lines." On any given quarter the chlor-alkali metrics will move together for cycle reasons. On any multi-year horizon, the segment mix is what differentiates them, and that segment mix is what the market still has not fully digested.

X. Conclusion & Playbook Lessons

There is something deeply Indian about The Andhra Sugars Limited, and it has nothing to do with cane fields or chlor-alkali cells. It is the story of a family-run industrial company that started as a post-colonial-era ambition, survived four decades of the License Raj, navigated the 1991 liberalisation without losing its footing, and then quietly accumulated one of the most strategically protected niches in the entire Indian chemical sector — all without ever leaving the small delta town where it was founded.

To put this in proper context, consider the survivorship bias problem. Most Indian companies founded in the immediate post-independence period did not make it through to 2026. Some were nationalised in the wave of bank and industry nationalisations during the Indira Gandhi years. Some were destroyed by the License Raj's capricious capacity allocations. Some never adapted to the 1991 liberalisation. Some fell victim to family succession battles. The fact that Andhra Sugars not only survived but compounded operationally across all of these regime changes is, in itself, a kind of statement about the durability of the cultural model that runs the company.

The playbook lessons are worth pulling out cleanly, because they generalise far beyond this one stock.

Lesson One: The Gate Sign Is Not the Strategy

Do not let the name on the gate define the strategy of the company. The most consequential decision in Andhra Sugars' history was the decision, somewhere in the 1960s, to be a chemicals company that happened to own a sugar mill rather than a sugar company that dabbled in chemistry. Forty years later, the market is still pricing the gate sign.

Lesson Two: Integrate, Don't Diversify

Vertical integration, in a regulated commodity industry, is not a luxury — it is a survival mechanism. Every margin-thin business needs at least one downstream user for its by-products that escapes the price controls of the upstream business. Molasses into alcohol. Alcohol into chemicals. Chlorine into derivatives. Hydrogen into propulsion. The chain is not aesthetic, it is structural.

Lesson Three: A Customer for Life

A single, sovereign-grade customer relationship, built over decades, can be worth more than a diversified book of small accounts. The ISRO partnership is, in revenue terms, a small line item. In moat terms, it is the single most valuable thing the company owns. A customer for life is the rarest asset in business.

Lesson Four: Cultural Frugality Compounds

The "Tanuku style" — frugality, engineering excellence, allergy to corporate flash — is a perfectly viable cultural strategy for a small-cap industrial in a regulated economy. It does not generate magazine covers. It does generate compounding.

Lesson Five: Mind the Sector Code

And, finally, the lesson that matters most for investors. Sometimes the most interesting compounders are the ones the index funds cannot see properly, because the sector code is wrong. Andhra Sugars is filed under "Sugar." Its margins, its moats, and its future are not. The arbitrage between classification and reality, in a market as deep and as informationally efficient as Indian equities have become, does not last forever — but while it lasts, it is worth understanding.

From the cane fields of Tanuku, through the chlor-alkali cells of Saggonda, to the upper stages of a rocket arcing over the Bay of Bengal on its way to the Moon, the story of this small-cap company in coastal Andhra is a quiet, almost private reminder that India's industrial future is being built in places that do not appear on the front pages of the business press. And that some of the most interesting businesses on earth are the ones that no longer fit the name above their door.

Pull back one final time, and the broader picture is this.

India in 2026 is in the middle of an industrial reorientation that is bigger than any single company. Manufacturing share of GDP is being deliberately pushed higher through production-linked incentive schemes. The chemical industry is being re-architected around domestic substitution of Chinese imports. The space program is migrating from a state-monopoly model toward a more diversified ecosystem of public and private participation. The energy transition is creating entirely new demand stacks for hydrogen, ammonia, and battery-grade chemicals.

Each of these tailwinds, in isolation, is bullish for some subset of India's industrial corporates. Andhra Sugars is one of the small but unusual cases where multiple tailwinds intersect inside a single, decades-old integrated complex run by a family that has spent seventy years learning how not to break the operating engine.

Whether the market eventually re-prices the company to reflect the chemicals-and-aerospace reality, or whether the sugar gate sign continues to anchor sentiment for another decade, is a question that will be answered by quarterly earnings and by the consistency of the segment trajectory. What is no longer in serious dispute is the underlying portfolio. The Andhra Sugars Limited is not, in any meaningful operational sense, a sugar company. It is an integrated industrial chemicals platform with a strategically protected aerospace propellants franchise, a cane-and-ethanol cyclical hedge, and a regional chlor-alkali cash cow funding it all. The name on the gate is a historical accident. The cash flows tell a more interesting story. And somewhere over the lunar south pole, on a sliver of regolith that no human had ever touched, a small Indian lander whose upper stages were lifted by hypergolic propellants from Saggonda is the most poetic possible vindication of the company's seventy-year arc.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube