Anand Rathi Wealth: The Democratization of Wealth Management in India

I. Introduction & Episode Roadmap

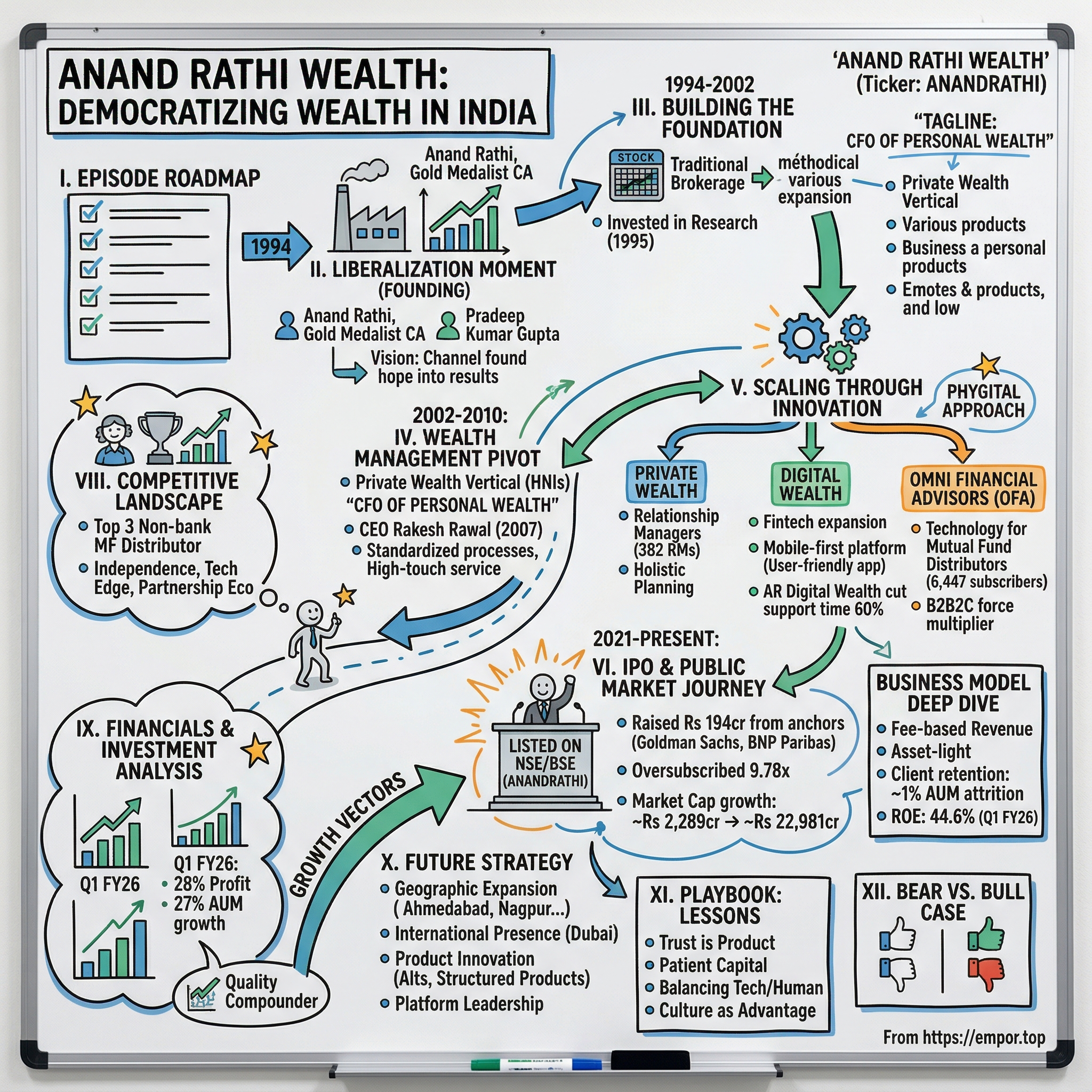

Picture this: It's 2021, and in the gleaming towers of Mumbai's financial district, a wealth management firm is preparing to go public. Not just any firm—Anand Rathi Wealth Limited, managing over ₹30,000 crores for 6,500+ families. The IPO would be oversubscribed 9.78 times, with anchor investors including Goldman Sachs and BNP Paribas clamoring for a piece. But this isn't a story that begins in boardrooms or with PowerPoint decks. It starts three decades earlier, in 1994, when India was awakening from its socialist slumber, and a gold medalist chartered accountant named Anand Rathi saw an opportunity that others missed: the democratization of wealth in a country where financial literacy was a privilege of the few. Today, Anand Rathi Wealth oversees assets under management (AUM) of over INR 87,797+ crores across 12,330+ families—a testament to how far this firm has come from its humble beginnings. But what makes this story particularly fascinating isn't just the numbers. It's how a traditional brokerage firm transformed itself into one of India's premier wealth management platforms, riding the waves of liberalization, technology disruption, and the creation of India's new wealthy class.

This is the story of how Anand Rathi Wealth became an NSE500-listed company that has been in the business of Private Wealth since 2002, catering to high-net-worth individuals, and how it built a business model that marries high-touch relationship management with cutting-edge technology—what they call the "phygital" approach. It's about navigating regulatory mazes, surviving market crashes, and most importantly, understanding that in India, wealth management isn't just about returns—it's about trust, relationships, and the delicate art of intergenerational wealth transfer.

As we unpack this journey, we'll explore the key inflection points: the post-liberalization gold rush of the 1990s, the strategic pivot to wealth management in 2002, the technology investments that set them apart, and the 2021 IPO that validated their model in public markets. We'll examine their three-pronged business model—Private Wealth, Digital Wealth, and the Omni Financial Advisors platform—and understand why their AUM reached Rs 87,797 crore with 27% year-over-year growth as of Q1 FY26.

But perhaps most importantly, we'll analyze what this means for investors, entrepreneurs, and anyone interested in understanding how financial services evolve in emerging markets. Because the Anand Rathi story isn't just about one company—it's a window into India's economic transformation and the democratization of wealth in the world's most populous nation.

II. The Liberalization Moment: Founding Context (1994)

The year was 1991, and India was on the brink of bankruptcy. Foreign exchange reserves had dwindled to barely three weeks of imports. The government, led by P.V. Narasimha Rao and Finance Minister Manmohan Singh, unleashed reforms that would fundamentally reshape India's economic landscape. License Raj was dismantled. Industries were delicensed. Capital markets were thrown open. For the first time since independence, India was open for business—real business. It was in this charged atmosphere that Anand Rathi, a Gold Medallist chartered accountant of 1966, saw an opportunity. At 50, when most professionals would be settling into comfortable corporate roles, Rathi was ready to take the entrepreneurial plunge. His credentials were impeccable: Before laying the foundation of the Anand Rathi Group, Mr Rathi had an illustrious and fruitful career with the Aditya Birla Group and DCM Ltd. He had worked alongside the legendary Aditya Birla himself for over 20 years, was the youngest president of Indian Rayon (now known as Aditya Birla Nuvo), and had been instrumental in shaping the group's cement business.

But what drove a man at the pinnacle of corporate success to start fresh? The answer lay in Rathi's vision for what India could become. He saw millions of Indians who would soon have disposable income but no access to professional financial advice. He saw a capital market that was about to explode but lacked the infrastructure to serve retail investors. Most importantly, he saw an opportunity to build something that didn't exist in India yet—a trusted, professional wealth management ecosystem. With an aim to channelise the new found hope and financial optimism into tangible results, Mr Anand Rathi and Mr Pradeep Kumar Gupta laid the foundation of the Anand Rathi Group in 1994. Pradeep Gupta wasn't just a co-founder—he was the operational genius who would complement Rathi's vision. Starting with a family-owned textile business, Mr. Gupta stepped into the financial world with Navratan Capital & Securities Pvt. Ltd. After scaling up the business, Mr. Gupta later joined hands with Mr. Anand Rathi to establish the Anand Rathi Group. Together, they represented the perfect marriage of strategic vision and execution capability.

The founding philosophy was radical for its time. The founding idea behind the Anand Rathi Group was to democratize the idea of financial wellbeing in India. It has been our mission from the first day to offer best-in-class financial services to our clients with utmost integrity and transparency. In a market where financial services were either the preserve of elite institutions or operated in grey markets, Anand Rathi wanted to build something different—professional, transparent, and accessible. The timing couldn't have been more perfect. In 1994, the National Stock Exchange (NSE) commenced operations on June 30 starting with the wholesale debt market segment and equities segment on November 3. It was the first exchange in India to introduce an electronic trading facility. The Securities and Exchange Board of India (SEBI) had just been given statutory powers in 1992 following the Harshad Mehta scam. Foreign institutional investors were allowed to invest for the first time. The Indian securities market was witnessing a flurry of Initial Public Offerings.

But while everyone was focused on the big-ticket IPOs and institutional deals, Anand Rathi saw something different. He saw millions of Indians who would need guidance navigating this new world of wealth creation. From setting up a research desk in 1995—one of the first independent research operations in India—the firm began building capabilities that would set it apart. This wasn't just about executing trades; it was about understanding markets, analyzing opportunities, and most importantly, educating clients.

What made Rathi's approach unique was his own credibility. Five years after founding the company, he would become president of BSE (Bombay Stock Exchange) during 1999-2001, spearheading the task of setting up and expansion of BSE Online Trading System (BOLT). During his tenure, major reforms like setting up of Central Depository Services (CDSL) and Trade Guarantee Fund were implemented. This wasn't just a businessman; this was someone who understood the plumbing of India's capital markets at the deepest level.

The vision was audacious yet simple: build a financial services firm that could serve everyone from the corner shop owner to the industrial magnate, with the same level of professionalism and integrity. In a country where financial advice often came from informal networks and trust was built on personal relationships, Anand Rathi would build trust through transparency, data, and consistent performance. The journey from this founding vision to becoming one of India's premier wealth management firms would take nearly three decades, but the seeds were planted in that transformative year of 1994.

III. Building the Foundation: From Brokerage to Wealth (1994–2002)

The early years were anything but glamorous. While the liberalization wave had opened doors, the Indian financial services market in the mid-1990s was still a wild west. Retail investors were scarred by frequent market manipulations, technology was primitive by today's standards, and the very concept of professional financial advisory was alien to most Indians. Into this chaos, Anand Rathi began building something systematic, something institutional.

The firm started as a traditional brokerage, focusing on equity trading—the bread and butter of any financial services firm in the 1990s. But even here, there was a difference. While competitors chased volumes through aggressive speculation and tips, Anand Rathi invested heavily in research. The dedicated research desk established in 1995 wasn't just a marketing gimmick; it represented a fundamental belief that informed investing, not speculation, would win in the long run. The expansion of services began methodically. The firm moved beyond pure equity brokerage into commodities, mutual funds, structured products, corporate deposits, and bonds. Each addition wasn't just about revenue diversification—it was about building a comprehensive financial solutions platform. By the late 1990s, Anand Rathi was distributing mutual funds, becoming one of the early independent distributors in a market dominated by banks and the Unit Trust of India.

What's fascinating about this period is how the firm navigated the trust deficit. In a market where financial advisors were often seen as stock tips providers or worse, commission-hungry salesmen, Anand Rathi took a different approach. They invested in education—both of their employees and their clients. Relationship managers weren't just trained in products; they were trained in financial planning, tax efficiency, and estate planning. This was revolutionary in an era when most brokers barely understood the products they were selling.

The credibility boost came when Anand Rathi himself became BSE President from 1999 to 2001. Here was the founder of a growing financial services firm helping architect the very infrastructure of India's capital markets. The expansion of BOLT (BSE Online Trading System), the establishment of the Trade Guarantee Fund, and the creation of Central Depository Services—these weren't just regulatory achievements. They were signals to the market that Anand Rathi understood the financial ecosystem at its most fundamental level.

But the real masterstroke was what came next. While competitors were fighting for market share in the crowded brokerage space, racing to the bottom on commissions, Anand Rathi was quietly preparing for a different game altogether. They saw that as India's economy grew, there would emerge a class of Indians with substantial wealth who needed more than just transaction execution. They needed advice, planning, and most importantly, a trusted partner to help them navigate the complexities of wealth.

By 2002, the firm had built the infrastructure, credibility, and client base needed for the next leap. They had 382 relationship managers—not just salespeople, but trained financial advisors. They had technology systems that could handle complex portfolio management. Most importantly, they had earned the trust of thousands of clients through eight years of consistent, ethical service. The stage was set for the transformation from a brokerage firm to a wealth management powerhouse.

IV. The Wealth Management Pivot (2002–2010)

Anand Rathi Wealth Limited has been in the business of Private Wealth since 2002, catering to high-net-worth individuals (HNIs). This wasn't just adding another vertical—it was a fundamental reimagination of what the company could be. The timing was prescient. India's GDP was about to enter a period of sustained high growth, creating wealth at an unprecedented pace. The number of dollar millionaires in India would grow from roughly 20,000 in 2000 to over 150,000 by 2010.

The Private Wealth vertical was designed differently from the ground up. Instead of the transactional approach of brokerage, this was about relationships. Instead of tips and recommendations, this was about financial planning. Instead of chasing the next hot stock, this was about building intergenerational wealth. The tagline they would later adopt—"CFO of personal wealth"—captured this philosophy perfectly.

Building this business required a different breed of professionals. The firm began recruiting not just from financial services but from private banks, consulting firms, and even family offices. These relationship managers were trained to think holistically about wealth—not just investments but taxes, estate planning, philanthropy, and succession. Each client would have a dedicated relationship manager who understood not just their portfolio but their family, their business, their dreams, and their fears.

The service model was high-touch and highly personalized. While the brokerage business might handle thousands of transactions a day, a Private Wealth relationship manager might spend weeks crafting a single financial plan. Where a broker might recommend a stock based on a research report, a wealth manager would recommend an asset allocation based on a client's entire financial picture. This wasn't scalable in the traditional sense, but that was precisely the point. The numbers validated the strategy. The number of high net worth individuals (HNIs or individuals with investable assets of $1 million or more) in India has grown for the second straight year by 2011. The wealth creation story of India from 2002 to 2010 was remarkable—GDP grew at an average of 7.5%, the stock market delivered spectacular returns, and real estate values soared. This created a perfect storm for wealth management services.

The technology investments during this period were crucial but understated. While competitors were still using spreadsheets and manual processes, Anand Rathi was building sophisticated portfolio management systems. They created tools for asset allocation, risk profiling, and performance tracking that were ahead of their time. This wasn't just about efficiency; it was about giving relationship managers the tools to have sophisticated conversations with clients about their wealth.

By 2007, a critical hire would shape the firm's future: Rakesh Rawal is one of the longest standing CEOs in the wealth management industry, serving as the CEO of Anand Rathi Wealth since 2007. Under Rawal's leadership, the Private Wealth business would transform from a promising vertical to the crown jewel of the Anand Rathi empire. His approach was systematic: standardize processes without losing personalization, scale operations without compromising quality, and most importantly, build a culture where relationship managers thought like fiduciaries, not salespeople.

The global financial crisis of 2008 became an unexpected validator of the model. While many wealth management firms saw massive client exits as markets crashed, Anand Rathi's focus on relationships over transactions paid off. Clients who had been educated about market cycles, who had diversified portfolios, and who trusted their advisors stayed put. More importantly, as competitors retreated, Anand Rathi continued to invest, hiring talent from distressed global firms and acquiring clients who had been abandoned by fair-weather advisors.

By 2010, the transformation was complete. What had started as a brokerage firm was now primarily a wealth management company. The Private Wealth vertical wasn't just contributing the majority of revenues; it was defining the company's identity. The stage was set for the next phase of growth—one that would embrace technology not as a threat to the high-touch model, but as an enabler of it.

V. Scaling Through Innovation: The Digital Revolution

The 2010s presented a paradox for wealth management firms globally. On one hand, robo-advisors and digital platforms threatened to commoditize financial advice. On the other, wealthy clients demanded more personalized service than ever. Anand Rathi's response was elegant: instead of choosing between human and digital, they chose both. The Digital Wealth vertical became their answer to this challenge—a fintech expansion of its offering, addressing the market's wealthy sector with a wealth solution given through a phygital channel, or a blend of human contact and technology.

This wasn't just digitizing existing processes. It was reimagining wealth management for a new generation of clients—entrepreneurs who had built digital businesses, professionals who were comfortable with technology, and younger inheritors who expected Amazon-like experiences from their financial advisors. The Digital Wealth platform allowed clients to view their portfolios in real-time, execute transactions instantly, and access research reports on-demand, all while maintaining access to their relationship manager for complex decisions.

But the real innovation came with the Omni Financial Advisors (OFA) vertical. Omni Financial Advisors (OFA) vertical is also an extension for capturing the wealth management landscape through which it provides a technology platform for mutual fund distributors (MFDs) to service their clients and grow their business. This was a B2B2C play that recognized a fundamental truth about India's wealth management market: there were thousands of independent financial advisors who had client relationships but lacked the technology and product access to serve them effectively. The OFA platform became a force multiplier. Technology platform subscriber base for Mutual Fund Distributors / Independent Financial Advisors (MFDs/IFAs) expanded to 6,447, creating a network effect that extended Anand Rathi's reach far beyond what its own relationship managers could achieve. These weren't competitors; they were partners who brought their own client relationships but relied on Anand Rathi for products, technology, and back-office support.

What made this digital transformation particularly impressive was its timing. While global wealth management firms were struggling with legacy systems and cultural resistance to change, Anand Rathi was building from a relatively clean slate. They could design systems for mobile-first experiences, real-time reporting, and seamless integration between human advisors and digital tools. Anand Rathi Digital Wealth (AR Digital Wealth) is a fintech company that leverages technology to significantly expand private wealth solutions. It offers digital solutions to High Net Worth Individuals (HNIs) through a mobile-first platform, overseeing clients with assets worth millions. AR Digital Wealth has adopted a digital-first approach, keeping pace with the increasing inclination of investors towards online platforms. Their user-friendly mobile app is designed to enable High Net Worth Individuals (HNIs) to access and manage their investments anytime, anywhere.

The investment in technology went beyond client-facing applications. Behind the scenes, the firm built sophisticated portfolio management systems, risk analytics engines, and compliance monitoring tools. This wasn't just about efficiency; it was about scale. The same relationship manager who might have managed 20 families in 2002 could now effectively serve 50 or more, with technology handling routine tasks while the human focused on what mattered—understanding client needs, providing emotional support during market volatility, and crafting personalized strategies.

By 2017, when the Digital Wealth Management initiative was formally launched, the transformation was complete. Anand Rathi wasn't just a wealth management firm that used technology; it was a technology-enabled wealth solutions provider. The positioning as "CFO of our client's personal wealth"—presenting structured, data-backed financial insights that help clients make informed decisions focusing on showcasing financial data and analytics related to wealth creation, risk assessment, tax provisions that enable efficiency, and intergenerational wealth planning—perfectly captured this evolution.

The numbers tell the story of success. AR Digital Wealth cut support turnaround time by 60% through accelerated issue resolution, demonstrating how technology could improve not just efficiency but client satisfaction. The firm was now managing not just wealth but data, not just portfolios but entire financial lives. And in doing so, they had positioned themselves perfectly for the next phase of their journey—accessing public markets to fuel even greater growth.

VI. The IPO Story & Public Market Journey (2021–Present)

December 2021 marked a watershed moment for Anand Rathi Wealth. After 27 years of building, scaling, and innovating, the company was ready for its public market debut. The timing seemed perfect—Indian capital markets were booming, retail participation was at all-time highs, and the wealth management sector was finally getting the recognition it deserved from institutional investors. The IPO details tell a story of confidence and validation. Anand Rathi Wealth raised Rs 194 crore from anchor investors, with participation from marquee names including BNP Paribas Arbitrage, Goldman Sachs Funds, SBI Mutual Fund, ICICI Prudential MF, HDFC MF, Axis MF, and Tata MF. The issue, priced at Rs 530-550 per share, was entirely an Offer for Sale (OFS) of 1.2 crore equity shares by promoters and existing shareholders, raising Rs 659.38 crores at the upper price band.

What's significant about this IPO structure is what it reveals about the company's maturity. This wasn't a growth capital raise—the company didn't need money. It was about providing liquidity to early investors and, more importantly, institutionalizing the business. Post-IPO, promoter stake would come down from 74.74% to 50.62%, bringing in public shareholders who would demand transparency, governance, and consistent performance.

The market reception was strong. The IPO was oversubscribed 9.78 times, with the retail portion seeing 2.58 times subscription, the non-institutional portion 3.70 times, and the qualified institutional buyer portion garnering an impressive 21.17 times subscription. On December 14, 2021, when the stock listed on BSE and NSE, it opened at a premium, validating the market's confidence in the wealth management story.

But the real test came after the listing. The post-IPO journey has been remarkable. The stock, which listed at around Rs 550, trades at significantly higher levels today, with market capitalization growing from approximately Rs 2,289 crores at IPO to Rs 22,981 crores—a staggering increase that reflects both operational performance and market re-rating of the wealth management sector. The stock's performance has been nothing short of spectacular. ANANDRATHI reached its all-time high on July 30, 2025 with the price of 2,730.00 INR, compared to its all-time low of 271.00 INR reached on February 24, 2022—a ten-fold increase from the lows. Market cap up 55.4% in just one year, with the stock trading at 34.1 times its book value—a valuation that would have been unthinkable for a financial services firm a decade ago.

What's driving this re-rating? The operational metrics tell the story. In Q1 FY26, Anand Rathi reports 28% profit growth, 27% AUM growth, record net mobilization Rs.3,825 Cr. The company's consolidated net profit jumped 33% to Rs 300.8 crore on 30% increase in total revenue to Rs 980.7 crore in FY25. These aren't just growth numbers; they're growth numbers with improving margins and returns. The annualized Return on Equity (ROE) stood at 44.6%—exceptional for any business, let alone one in financial services.

But perhaps more importantly, the public market journey has forced the company to become more transparent, more institutionalized, and more focused on sustainable growth rather than just AUM accumulation. The quarterly earnings calls, investor presentations, and regulatory disclosures have created a feedback loop that has made the company stronger. Promoter holding has decreased from 74.74% at IPO to 42.7% today, bringing in institutional investors who provide both capital and governance oversight.

The post-IPO period has also seen geographic expansion—The Company expanded its presence into 4 new cities: Ahmedabad, Vishakhapatnam, Coimbatore and Nagpur in 2022 and in 2024, has expanded its presence to Lucknow and Jabalpur. Each new location isn't just about physical presence; it's about tapping into the wealth creation happening across India's tier-2 and tier-3 cities, where entrepreneurship is flourishing and creating a new class of HNIs.

As we stand today, with the company valued at over Rs 22,000 crores, managing Rs 87,797 crores in AUM, and serving 12,330+ families, the IPO looks less like an exit and more like a beginning. The capital markets have given Anand Rathi Wealth the currency—both literal and figurative—to pursue its next phase of growth. And if the past is any indication, that growth will be both substantial and sustainable.

VII. Business Model Deep Dive

At its core, Anand Rathi Wealth's business model is deceptively simple: help wealthy individuals manage their money and take a fee for doing so. But the execution of this model reveals layers of sophistication that explain why the company commands premium valuations and delivers exceptional returns.

The revenue model is primarily fee-based, deriving income from multiple streams. Mutual fund distribution remains the largest contributor, with revenue from mutual fund distribution jumping 52% YoY to Rs 406 crore in Q4 FY25 alone. But this isn't just about selling mutual funds—it's about curating portfolios, providing asset allocation advice, and most importantly, hand-holding clients through market cycles. The share of equity mutual funds in AUM climbed to 53% as of March 2025, compared to 51% in March 2024, reflecting the firm's ability to guide clients toward long-term wealth creation through equities.

What makes the model particularly attractive is its asset-light nature. Unlike banks or NBFCs, Anand Rathi Wealth doesn't need significant capital to grow. They don't take balance sheet risk. They don't need branches in every neighborhood. What they need are relationships, trust, and technology—all of which scale beautifully. This explains the exceptional returns: ROE of 44.6% isn't an anomaly; it's the natural outcome of a business model with minimal capital requirements and high operating leverage.

The client acquisition strategy is equally sophisticated. Each of the 382 Relationship Managers operates like a mini-entrepreneur, responsible for acquiring and managing their client portfolio. But unlike traditional brokers who might chase anyone with money, Anand Rathi's RMs are trained to be selective. The average ticket size, the client profile, the long-term potential—everything is evaluated before onboarding. This selectivity shows in the numbers: 59% of clients have been associated for over 3 years, representing 79% of total private wealth's AUM.

Client retention is where the model truly shines. The company maintains a client attrition rate of approximately 1% in terms of AUM lost—extraordinary in an industry where client churn is endemic. How do they achieve this? Through what they call the "6-Way Support System"—a comprehensive approach that goes beyond investment advice to include estate planning, tax optimization, lending solutions, and even lifestyle services. When you become the "CFO of personal wealth," switching costs become prohibitive—not just financially but emotionally.

The partnership model adds another dimension. With 2500+ thriving business partners, Anand Rathi has created a distribution network that extends far beyond its own employees. These partners—often independent financial advisors, chartered accountants, or small wealth management firms—bring clients to Anand Rathi's platform while maintaining their own relationships. It's a win-win: partners get access to products, technology, and back-office support they couldn't afford independently, while Anand Rathi gets distribution without the associated costs.

Technology acts as the force multiplier across all these elements. The Digital Wealth platform isn't just a digital channel—it's a different way of serving clients who want the convenience of digital with the assurance of human support. The Omni Financial Advisors platform, serving 6,447 MFDs/IFAs, generates revenue not just from the platform fees but from the assets these advisors bring onto the platform. It's platform economics at its finest—build once, monetize infinitely.

The unit economics are compelling. While specific numbers aren't disclosed, industry analysis suggests that the cost of acquiring a client is recovered within 12-18 months, after which the client becomes highly profitable. Given that clients stay for years, often decades, and their AUM typically grows over time (both through market appreciation and additional investments), the lifetime value of a client far exceeds acquisition costs. Operating profit margins hovering around 45% validate this economic model.

But perhaps the most underappreciated aspect of the business model is its resilience. During market downturns, when transaction-based revenues might fall, the annuity-like trail commissions from mutual funds provide stability. During bull markets, increased investor interest drives both new client acquisition and higher investments from existing clients. The model works in all weather, which explains why the company has delivered consistent growth through multiple market cycles. This isn't just a business model; it's a compounding machine, where every new client, every new partner, and every new product adds to a flywheel that becomes harder to stop with each passing year.

VIII. Competitive Landscape & Market Position

In the rarefied world of Indian wealth management, Anand Rathi Wealth occupies a unique position—large enough to matter, nimble enough to innovate, and focused enough to excel. Ranking amongst the top three non-bank mutual fund distributors in India isn't just a statistic; it's a testament to how the firm has navigated one of the most competitive segments in financial services.

The competitive landscape is fragmented and fierce. At the top sit the private banks—HDFC Bank, ICICI Bank, Kotak Mahindra Bank—with their massive customer bases and ability to cross-sell wealth management to existing clients. Then there are the dedicated wealth managers—IIFL Wealth (now 360 ONE), Edelweiss Wealth, Motilal Oswal Private Wealth—each with their own strategies and strengths. Finally, there's the long tail of thousands of independent advisors, small firms, and family offices competing for the same pool of wealthy Indians.

What sets Anand Rathi apart in this crowded field? First, independence. Unlike bank-led wealth managers who might push proprietary products, Anand Rathi operates on an open architecture model, offering products from multiple manufacturers based on what's best for clients. This independence is particularly valued by sophisticated HNIs who understand the conflict of interest inherent in captive distribution.

Second, the technology edge. While traditional competitors relied on relationship managers and Excel sheets, Anand Rathi invested early and heavily in technology. Their platforms don't just digitize existing processes; they reimagine how wealth management can be delivered. Real-time portfolio tracking, automated rebalancing, tax optimization algorithms—capabilities that were once the preserve of institutional investors are now available to individual clients.

Third, the partnership ecosystem. Rather than seeing independent advisors as competition, Anand Rathi turned them into partners through the OFA platform. This co-opetition model—competing in some areas while collaborating in others—has created a network effect that's difficult for pure-play competitors to replicate. When 6,447 MFDs/IFAs are using your platform, you're not just a wealth manager; you're infrastructure for the industry.

The regulatory environment adds another layer of complexity and opportunity. SEBI's regulations on mutual fund commissions, the push for greater transparency, and the emphasis on investor protection have raised compliance costs for everyone. But for organized players like Anand Rathi, with robust compliance systems and processes, these regulations are a moat. Every new compliance requirement makes it harder for smaller players to compete and easier for established firms to consolidate market share.

The competitive dynamics are evolving rapidly. Global firms are entering India—whether through acquisitions or organic entry. Digital-only wealth managers are emerging, promising to democratize wealth management through technology. Robo-advisors are gaining traction among younger investors. Each represents both a threat and an opportunity.

Against this backdrop, Anand Rathi's strategy is clear: dominate the sweet spot between ultra-HNIs (who might prefer global private banks) and mass affluent (who might be served by robo-advisors). This segment—typically individuals with Rs 5-50 crores in investable assets—is large enough to be meaningful, sophisticated enough to value advice, and growing rapidly enough to sustain high growth rates.

Market share data, while not precisely available, suggests Anand Rathi controls approximately 2-3% of the organized wealth management market in India. That might seem small, but in a market estimated at over Rs 30 lakh crores and growing at 15-20% annually, even maintaining share means substantial absolute growth. More importantly, in specific segments—like mutual fund distribution to HNIs—their share is significantly higher.

The competitive moat is multi-layered. Brand and trust, built over three decades, can't be replicated quickly. The relationship manager network, with years of client relationships, creates switching costs. The technology platform, continuously enhanced, stays ahead of competitors trying to catch up. The partnership network creates distribution that would take years to build independently. Together, these create a competitive position that's not unassailable but certainly formidable.

Looking ahead, the competitive landscape will likely consolidate. Smaller players without scale will struggle with rising compliance costs and technology investments. Banks will continue to be formidable but will face their own challenges around conflicts of interest and organizational focus. New digital entrants will nibble at the edges but will find it hard to serve complex HNI needs. In this environment, Anand Rathi's position—scaled but agile, traditional but innovative, independent but connected—positions it well to not just survive but thrive. The question isn't whether they can compete; it's how much of the growing pie they can capture.

IX. Financials & Investment Analysis

The financial story of Anand Rathi Wealth reads like a textbook case of operational excellence in asset-light businesses. Revenue of Rs 976 Cr and Profit of Rs 321 Cr in recent quarters represent not just growth but quality growth—the kind that drops disproportionately to the bottom line and generates exceptional returns on capital.

The revenue trajectory tells a story of consistent execution. FY22 revenue of Rs 938 crores with 22% YoY increase was just the beginning. FY25 delivered total revenue growth of 30% YoY to Rs 981 crore, while Profit After Tax (PAT) rose by 33% to Rs 301 crore. What's remarkable isn't just the growth rate but its consistency—quarter after quarter, year after year, through market ups and downs.

Operating margins deserve special attention. With Operating Profit Margins consistently hovering around 45%, Anand Rathi Wealth demonstrates the beauty of the asset-light model. Every incremental rupee of revenue requires minimal additional cost—no new branches, no significant capital expenditure, just variable costs that scale linearly or better. This operating leverage means that revenue growth of 30% can translate to profit growth of 33% or higher.

The balance sheet is a study in efficiency. Unlike banks or NBFCs that need significant capital to grow, Anand Rathi Wealth's capital requirements are minimal. Working capital needs are negligible—clients pay upfront or assets are held in custody. Fixed assets are limited to office infrastructure and technology. The result? A business that generates Rs 301 crores in profit barely needs any capital reinvestment, creating a cash generation machine.

Return metrics validate the business quality. Return on Equity at 44.6% is exceptional by any standard—compare this to banks that struggle to maintain 15% ROE or even other financial services firms that celebrate 25% ROE. This isn't financial engineering; it's the natural outcome of a business model that uses minimal equity capital to generate substantial profits.

Valuation presents an interesting puzzle. Stock trading at 34.1 times book value would typically signal extreme overvaluation. But book value for an asset-light business is almost meaningless—the real assets walk out of the office every evening (the relationship managers) or exist in intangibles (brand, client relationships, technology platforms) that aren't captured on the balance sheet. Price-to-earnings might be more relevant, but even that needs context—a business growing at 30% with 45% ROE deserves a premium multiple.

The dividend policy reflects confidence and capital efficiency. Final dividend of Rs 7 per equity share for FY 2025 might seem modest, but it represents a balanced approach—returning excess capital to shareholders while retaining enough for growth investments. With minimal capital requirements for organic growth, most profits can theoretically be distributed, making this an attractive yield play for long-term investors.

Risk factors, however, can't be ignored. Market cycles directly impact both AUM (through mark-to-market) and revenue (through reduced investor activity). A 20% market correction could see AUM drop proportionally, affecting trail commissions. Regulatory changes, particularly around mutual fund commissions, pose ongoing risks—SEBI's periodic reviews of commission structures could impact margins. Competition, especially from digital platforms willing to operate at lower margins, could pressure pricing.

The capital allocation strategy going forward will be crucial. With limited organic capital needs, the company faces choices—aggressive expansion (new geographies, new products), acquisitions (consolidating smaller players), technology investments (building new platforms), or simply returning capital to shareholders. Each path has different implications for growth, returns, and valuation.

Currency and interest rate dynamics add another layer. Rising rates typically benefit the company through higher yields on float and treasury income. However, they can also dampen equity market enthusiasm, affecting AUM growth. The rupee's trajectory matters too—a depreciating rupee might encourage clients to diversify internationally, potentially affecting domestic AUM.

Looking at peer comparisons, Anand Rathi Wealth trades at a premium to some competitors but at a discount to others. 360 ONE (formerly IIFL Wealth), with its focus on ultra-HNIs, commands higher valuations. Traditional brokers with wealth management arms trade at discounts. The valuation seems fair for a company with Anand Rathi's growth profile, return metrics, and market position.

For investors, the financial analysis suggests a quality compounder—a business that can grow earnings at 20-25% annually with minimal capital needs, generating exceptional returns throughout. The key monitorables would be AUM growth (the leading indicator), revenue growth (showing pricing power), margin trends (indicating competitive intensity), and client metrics (revealing franchise strength). At current valuations, the market is pricing in continued excellence. Whether that's justified depends on one's view of India's wealth creation story and Anand Rathi's ability to capture a meaningful share of it.

X. Future Strategy & Growth Vectors

The next chapter of Anand Rathi Wealth's story is being written against the backdrop of India's unprecedented wealth creation. With India's HNI population expected to nearly double to 1.65 million by 2027 from the current 850,000, the tailwinds are strong. But capturing this opportunity requires more than just showing up—it requires strategic choices about where to play and how to win.

Geographic expansion represents the most obvious growth vector. While the firm has expanded into cities like Ahmedabad, Vishakhapatnam, Coimbatore, Nagpur, Lucknow, and Jabalpur, there's still vast untapped potential. India's wealth creation is increasingly happening outside the top metros—in cities where entrepreneurs are building businesses, professionals are earning substantial incomes, and family businesses are getting institutionalized. Each new city isn't just a new location; it's access to a new ecosystem of wealth.

International expansion, particularly the Dubai presence, opens another dimension. The Indian diaspora, particularly in the Gulf, represents substantial wealth that needs sophisticated management. Moreover, as Indian HNIs increasingly look to diversify globally, having international presence becomes crucial for serving their needs. Dubai, Singapore, London—each represents not just a market but a gateway to global investment opportunities.

Product innovation will be crucial for sustaining growth. While mutual funds remain the core, the firm is expanding into alternative investments, structured products, and portfolio management services (PMS). As clients become more sophisticated and wealthy, their needs evolve from simple mutual fund portfolios to complex structures involving multiple asset classes, tax optimization, and estate planning. The ability to offer comprehensive solutions rather than individual products becomes the differentiator.

The technology roadmap is perhaps the most exciting growth vector. The Digital Wealth platform is still in its early stages, with potential to serve a much larger client base than traditional relationship manager-led models. Imagine AI-powered advisors that can provide personalized advice at scale, blockchain-based platforms for seamless cross-border transactions, or machine learning algorithms that can predict client needs before they articulate them. Technology isn't just about efficiency; it's about reimagining what wealth management can be.

Segment expansion offers another avenue for growth. While the firm has traditionally focused on established HNIs, there's opportunity in adjacent segments. Young entrepreneurs creating wealth through startups, professionals earning substantial incomes but lacking financial sophistication, women inheriting and managing wealth independently—each represents a distinct segment with specific needs. The Digital Wealth platform particularly enables serving these segments profitably.

Strategic acquisitions could accelerate growth. The wealth management industry in India remains fragmented, with thousands of small players struggling with scale, technology, and regulatory compliance. Selective acquisitions could bring client relationships, geographic presence, or specialized capabilities. The public listing provides both the currency (stock) and credibility to pursue such opportunities.

The partnership strategy could evolve into platform leadership. With 6,447 MFDs/IFAs already on the OFA platform, there's potential to become the operating system for independent wealth advisors in India. This B2B2C model could scale far beyond what any direct-to-consumer model could achieve, creating network effects that become increasingly powerful over time.

ESG and sustainable investing represent both a growth opportunity and a strategic imperative. As awareness about environmental and social issues grows, wealthy Indians are increasingly interested in investing with impact. Building capabilities in ESG analysis, impact measurement, and sustainable investment products could differentiate the firm while capturing a growing market segment.

Family office services for ultra-HNIs present a natural evolution. As clients' wealth grows, their needs become more complex—from managing multiple entities to coordinating with various advisors to handling family governance issues. Offering comprehensive family office services could deepen relationships with the most valuable clients while significantly increasing revenue per client.

The education and content strategy could become a growth driver itself. Wealthy Indians are hungry for financial education—not just about products but about wealth psychology, family dynamics, and legacy planning. Building a content platform that positions Anand Rathi as a thought leader could attract clients while creating a moat competitors would find hard to replicate.

Succession planning within the firm itself will be crucial. Rakesh Rawal, CEO since 2007, has built an exceptional organization. But sustainable institutions need smooth leadership transitions. The recent elevation of Feroze Azeez to joint CEO signals thoughtful succession planning. Building the next generation of leaders—whether from within or through strategic hires—will determine whether the firm can sustain its growth trajectory.

The regulatory strategy needs careful consideration. As the firm grows larger and more visible, regulatory scrutiny will increase. Proactively engaging with regulators, contributing to policy discussions, and maintaining the highest standards of compliance isn't just about avoiding problems—it's about shaping the industry's future.

Looking ahead, the vision seems clear: become India's preeminent wealth solutions provider, serving multiple client segments through multiple channels with multiple products, all unified by technology and trust. The pieces are in place—brand, talent, technology, capital. The market opportunity is substantial and growing. The execution track record is strong. If the past is prologue, the future looks promising. The question isn't whether Anand Rathi Wealth will grow, but how fast and how profitably. And in that answer lies the investment thesis for those evaluating the stock.

XI. Playbook: Lessons for Founders & Investors

The Anand Rathi Wealth story offers a masterclass in building enduring financial services businesses in emerging markets. For founders attempting to build the next generation of financial institutions and investors evaluating such opportunities, the lessons are both tactical and philosophical.

Building Trust in Financial Services: Trust isn't built through advertising campaigns or celebrity endorsements. It's built through thousands of small actions over decades. Anand Rathi's approach—starting with the founder's credibility, maintaining transparency even when it hurt short-term profits, and most importantly, aligning with client interests—created a trust bank that became the firm's most valuable asset. For founders, the lesson is clear: in financial services, trust is your product. Everything else is just features.

The Power of Patient Capital: Anand Rathi Wealth took 27 years from founding to IPO. In an era of rapid unicorns and quick exits, this might seem anachronistic. But building a wealth management franchise requires patient capital—the kind that understands that client relationships take years to build, that brand recognition takes decades to establish, and that regulatory trust takes consistent compliance over long periods. Investors seeking quick returns should look elsewhere; this is a business for those who think in decades, not quarters.

Balancing Technology and Human Touch: The firm's "phygital" approach offers a template for navigating the technology transformation in financial services. Pure robo-advisors struggle to handle complex HNI needs. Pure human models can't scale efficiently. Anand Rathi's approach—technology for efficiency and scale, humans for empathy and complex decision-making—shows how traditional firms can embrace digital without losing their soul.

Creating Defensible Moats: In commodity businesses like mutual fund distribution, moats seem impossible. Yet Anand Rathi built multiple moats—brand trust that takes decades to build, relationship manager networks with deep client relationships, technology platforms with network effects, and regulatory compliance capabilities that create barriers to entry. The lesson: even in commoditized industries, thoughtful strategy can create differentiation.

Managing Cyclicality: Financial services is inherently cyclical. Markets boom and bust. Regulations tighten and loosen. Competition intensifies and retreats. Anand Rathi's approach—building a diversified revenue model, maintaining a strong balance sheet, investing through downturns—shows how to build anti-fragile businesses that get stronger through cycles rather than just surviving them.

The Value of Ecosystem Thinking: Rather than viewing the market as zero-sum competition, Anand Rathi built an ecosystem. Independent advisors became partners through the OFA platform. Competitors became co-distributors for certain products. Regulators became stakeholders through proactive engagement. This ecosystem thinking created value for all participants while strengthening Anand Rathi's position at the center.

Culture as Competitive Advantage: The remarkably low attrition rates—0.56% regret RM attrition—aren't accidents. They're the result of deliberate culture building where relationship managers are treated as entrepreneurs, where success is shared, and where long-term thinking is rewarded over short-term gains. For founders, the lesson is that in people businesses, culture isn't soft stuff—it's the hardest competitive advantage to replicate.

Timing Market Evolution: Anand Rathi didn't try to create the wealth management market in India; they waited for it to emerge and then positioned themselves to capture the opportunity. Starting as a brokerage when that's what the market needed, evolving to wealth management as HNIs emerged, embracing digital as technology became ready—this patient evolution shows the value of timing in strategy.

The Compound Effect of Reputation: Every client served well becomes a referral source. Every relationship manager trained properly becomes a brand ambassador. Every regulatory filing done correctly builds credibility. Over decades, these compound into a reputation that becomes the firm's greatest asset and highest barrier to entry. For investors, companies with compounding reputation are often undervalued because this asset doesn't appear on balance sheets.

Operational Excellence as Strategy: In financial services, operational excellence isn't just about efficiency—it's about trust. Every error erodes confidence. Every smooth transaction builds it. Anand Rathi's focus on operations—from technology systems to compliance processes—shows that in trust businesses, operational excellence is strategic, not just operational.

Building for Ownership Transition: The smooth transition from founder-led to professionally managed, from private to public, shows thoughtful institution building. Too many founder-led businesses struggle with succession. Anand Rathi's approach—bringing in professional management early, creating systems and processes that don't depend on individuals, and ultimately accessing public markets for governance and capital—provides a template for building businesses that outlast their founders.

The Power of Focus: While the Anand Rathi Group operates in multiple financial services segments, Anand Rathi Wealth maintained focus on wealth management. This focus allowed them to build deep expertise, strong brand recognition, and operational excellence in their chosen domain. For founders, the lesson is that in competitive markets, focus beats diversification.

Understanding Your True Business: Anand Rathi Wealth isn't really in the mutual fund distribution business or even the wealth management business. They're in the trust business, the relationship business, the peace-of-mind business. Understanding this deeper purpose informed every strategic decision, from hiring relationship managers to investing in technology. For investors, companies that understand their true business often have hidden competitive advantages.

These lessons collectively suggest a playbook for building enduring financial institutions: Start with trust, build with patience, scale with technology, differentiate through service, and always, always put the client first. It's a playbook that seems simple but proves incredibly difficult to execute. Those who can—whether founders building businesses or investors backing them—stand to create and capture tremendous value over time.

XII. Bear vs. Bull Case Analysis

Every investment thesis needs stress testing, and Anand Rathi Wealth is no exception. The bull case sees a multi-decade compounder riding India's wealth creation wave. The bear case sees risks that could derail the growth story. The truth, as always, lies somewhere in between.

The Bull Case: A Generational Wealth Creation Opportunity

India's wealth creation story is just beginning. With GDP expected to double by 2030, the number of millionaires nearly doubling to 1.65 million by 2027, and household savings increasingly moving from physical to financial assets, the tailwinds are hurricane-force. Anand Rathi Wealth, with its established brand, proven execution, and scalable platform, is perfectly positioned to capture this opportunity.

The business model dynamics are compelling. Every new client adds to a growing stream of recurring revenues. Technology investments have created operating leverage where marginal costs approach zero. The network effects from the OFA platform create a flywheel that accelerates with scale. ROE of 44.6% isn't peak—it's sustainable given the asset-light model. If the company can maintain 25% revenue growth with stable margins, the stock could deliver 30%+ annual returns.

Regulatory changes, rather than threats, are opportunities. Every new compliance requirement raises barriers to entry. The push for transparency benefits organized players. The emphasis on investor protection plays to Anand Rathi's strengths. As the industry consolidates, Anand Rathi could emerge as one of the few scaled winners.

The generational wealth transfer about to occur in India—estimated at $128 billion passing to the next generation—creates enormous opportunity for wealth managers who can navigate family dynamics and intergenerational planning. Anand Rathi's focus on comprehensive wealth solutions positions them perfectly for this transition.

International expansion could surprise on the upside. The Indian diaspora's wealth, the increasing globalization of Indian HNIs, and the potential for cross-border partnerships could open markets larger than India itself. If the firm can replicate even a fraction of its Indian success internationally, the growth runway extends dramatically.

The Bear Case: Multiple Risks Converging

Market dependency is the elephant in the room. A prolonged bear market wouldn't just reduce AUM through mark-to-market; it would dampen investor sentiment, reduce new client additions, and potentially trigger redemptions. A 30% market correction could see revenues drop 20% or more, and with high fixed costs (primarily people), margins would compress dramatically.

Regulatory risks are real and present. SEBI's periodic reviews of mutual fund commissions have consistently trended toward lower distributor margins. A significant cut in trail commissions or upfront fees could permanently impair the business model. The push toward direct plans, where investors bypass distributors entirely, poses an existential threat if it accelerates.

Competition is intensifying from every direction. Banks are getting serious about wealth management. Digital platforms are offering services at fraction of traditional costs. Global firms are entering India with deep pockets and proven models. The moat that seems wide today could narrow quickly if competitors successfully combine technology with lower costs.

Key person risks can't be ignored. While succession planning appears thoughtful, the loss of key relationship managers could see clients follow them. In a relationship business, people are the product, and people can leave. The 0.56% regret RM attrition is exceptional, but past performance doesn't guarantee future results.

Technology disruption could blindside traditional models. If AI-powered advisors become good enough for complex wealth management, if blockchain enables peer-to-peer financial services, if younger HNIs prefer purely digital models—the carefully constructed phygital approach could become a liability rather than an asset.

Fee compression seems inevitable. As the industry matures, as transparency increases, as competition intensifies, fees will face pressure. The 45% operating margins look unsustainably high in a competitive market. Even a 10% margin compression would significantly impact valuations.

The Balanced View: Navigating Between Extremes

The reality likely lies between these extremes. India's wealth creation story is real, but it won't be linear—there will be corrections, crises, and cycles. Anand Rathi Wealth will capture significant opportunity, but growth rates will moderate from current levels. Margins will face pressure but remain healthy given the business model advantages.

The key variables to monitor are AUM growth (the health indicator), margin trends (the competition indicator), client metrics (the franchise indicator), and regulatory changes (the disruption indicator). A base case might assume 20% AUM growth, stable margins, and 15-18% earnings growth—still attractive but not spectacular.

Valuation becomes crucial. At 34 times book value, the market is pricing in perfection. Any disappointment—a weak quarter, regulatory changes, key person exits—could trigger significant multiple compression. Conversely, successful execution could see multiples expand further as the quality of the franchise becomes more apparent.

For investors, the decision comes down to time horizon and risk tolerance. For long-term investors who believe in India's wealth creation story and Anand Rathi's ability to execute, current valuations might prove reasonable in hindsight. For those seeking near-term value or worried about market cycles, waiting for better entry points might be prudent.

The beauty and curse of quality companies is that they rarely offer obvious buying opportunities. By the time the concerns are resolved, the opportunity has passed. By the time the growth is proven, the valuation has expanded. Anand Rathi Wealth presents this classic dilemma—a wonderful business at a full price. Whether that's a buy, hold, or sell depends entirely on one's view of the future. And in that future lies both tremendous opportunity and considerable risk.

XIII. Epilogue & Reflections

As we conclude this deep dive into Anand Rathi Wealth, it's worth stepping back to consider what this story represents in the broader context of India's economic transformation and the future of wealth management globally.

The democratization of wealth management in India isn't just a business opportunity—it's a societal transformation. For generations, sophisticated financial advice was the preserve of the ultra-wealthy, often managed through informal networks and family connections. Companies like Anand Rathi are changing this, bringing institutional-quality wealth management to a broader audience. This isn't just about returns; it's about financial empowerment, intergenerational wealth preservation, and ultimately, social mobility.

The India that Anand Rathi was founded in—1994, just three years after liberalization—is almost unrecognizable today. From a closed economy with limited financial markets to one of the world's fastest-growing major economies with sophisticated capital markets, the transformation has been remarkable. Anand Rathi both benefited from and contributed to this transformation, helping channel savings into productive investments, enabling wealth creation, and building trust in financial markets.

Looking ahead, the future of wealth management in India will be shaped by several forces. Technology will continue to democratize access, but the need for human judgment in complex decisions will persist. Regulatory evolution will continue to shape industry structure, likely favoring organized, compliant players. Generational change will bring new expectations—younger clients expecting digital experiences, older clients requiring estate planning, and everyone demanding transparency and value.

The rise of India's wealth management industry also has global implications. As Indian wealth managers gain scale and sophistication, they could expand internationally, challenging established players in other markets. The innovations developed for the Indian market—serving clients across vast geography, managing complex family structures, navigating regulatory complexity—could prove valuable globally.

For Anand Rathi Wealth specifically, the next decade will be defining. Can they maintain growth rates as the base expands? Can they navigate technological disruption while preserving relationship advantages? Can they expand internationally while maintaining focus on India? Can they handle succession from founders to next generation leadership? These questions will determine whether Anand Rathi Wealth becomes a generational company or just another successful firm.

The lessons from this journey extend beyond financial services. Building trust in low-trust environments, scaling high-touch services through technology, creating ecosystems rather than zero-sum competition, building institutions that outlast founders—these lessons apply across industries and geographies. In a world increasingly divided between digital-first startups and traditional incumbents, Anand Rathi's hybrid approach offers a third way.

For investors, Anand Rathi Wealth represents a broader theme—the formalization and institutionalization of India's economy. As millions of Indians create wealth through entrepreneurship and professional success, they need sophisticated financial services. As family businesses professionalize, they need institutional-quality advice. As India integrates with global markets, its citizens need world-class wealth management. Companies serving these needs aren't just riding trends; they're building infrastructure for India's economic future.

The philosophical questions raised by this story are profound. What is the role of wealth managers in society? How do we balance technology efficiency with human empathy? What does democratization mean in inherently exclusive services? How do we create sustainable businesses in cyclical industries? These aren't just business questions; they're questions about the kind of economy and society we want to build.

As we watch Anand Rathi Wealth's next chapters unfold, we're not just watching a company—we're watching an industry mature, a economy transform, and a society evolve. The story that began with a chartered accountant's vision in 1994 has become part of India's larger narrative of growth, aspiration, and transformation.

The ultimate judgment of Anand Rathi Wealth's success won't be just in stock returns or AUM growth. It will be in the families whose wealth was preserved across generations, the entrepreneurs whose capital was deployed productively, the retirees whose futures were secured. In financial services, success is measured not in quarters but in generations. By that measure, the story of Anand Rathi Wealth is still being written.

For those of us observing from the outside—whether as investors, competitors, or simply interested observers—the Anand Rathi story offers both inspiration and instruction. It shows that in rapidly developing economies, patient capital combined with excellent execution can create tremendous value. It demonstrates that even in commoditized industries, differentiation is possible through focus and culture. Most importantly, it reminds us that behind every financial metric is a human story—of trust earned, relationships built, and futures secured.

As India continues its journey toward becoming a developed economy, the role of firms like Anand Rathi Wealth will only grow in importance. They are the bridges between savings and investment, between individual success and collective prosperity, between financial potential and realized wealth. In building their business, they're building India's future. And in that future, the story of Anand Rathi Wealth will be remembered not just as a business success, but as a participant in one of history's great economic transformations.

The question for all of us—investors, entrepreneurs, observers—is not just whether to bet on companies like Anand Rathi Wealth, but how to contribute to the larger project they represent: building financial systems that serve not just the wealthy but the aspiring, not just returns but relationships, not just today's needs but tomorrow's dreams. In that challenge lies the opportunity, and in that opportunity lies the future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube