Ambuja Cements: Building India's Infrastructure Dream

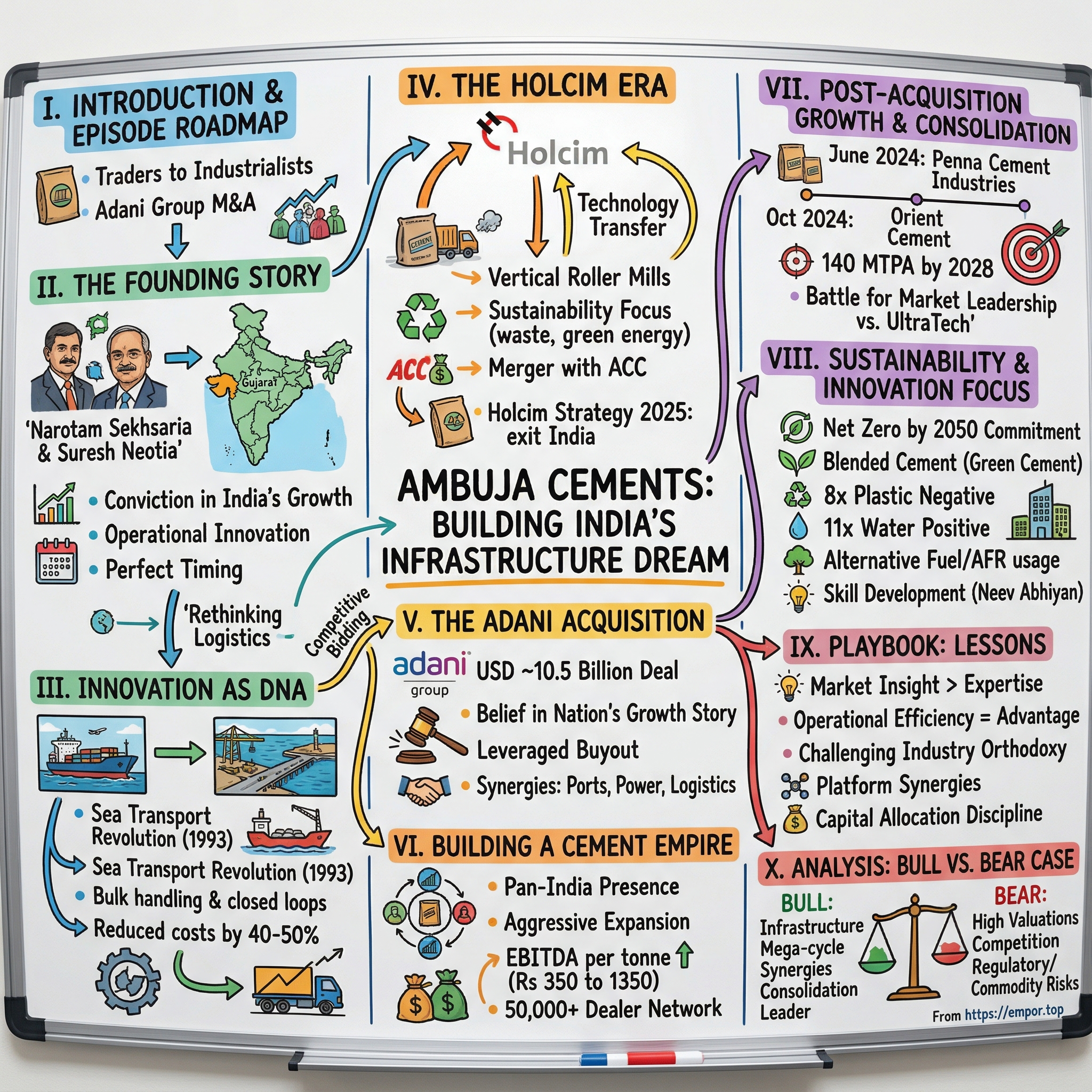

I. Introduction & Episode Roadmap

In 1983, two traders with virtually no knowledge of cement or manufacturing decided to bet their futures on what would become one of India's most remarkable industrial success stories. Narotam Sekhsaria and Suresh Neotia didn't have engineering degrees, cement industry experience, or even a clear playbook for building a manufacturing empire. What they possessed was something perhaps more valuable: an unshakeable conviction that India's economic development would demand unprecedented amounts of cement, and that whoever could produce it most efficiently would win.

Fast forward to May 2022, and their creation, Ambuja Cements, became the centerpiece of India's largest-ever infrastructure M&A transaction. The Adani Group paid $10.5 billion to acquire Holcim's stake in Ambuja Cements and ACC, instantly catapulting itself into the cement major leagues. The deal wasn't just about tonnage or market share—it represented a fundamental bet on India's infrastructure story for the next three decades.

The question that drives this analysis is deceptively simple yet profoundly important: How did two traders with no cement knowledge build one of India's most efficient cement companies, and why did Gautam Adani pay top dollar for it at a time when global markets were experiencing significant volatility?

The answer lies in a combination of operational innovation, strategic foresight, and perfect timing across multiple economic cycles. Ambuja's story isn't just about mixing limestone and clay—it's about reimagining logistics, pioneering sustainability before it was fashionable, and building a distribution network that could reach the smallest towns while serving the largest infrastructure projects.

This is a story of transformation at multiple levels: traders becoming industrialists, a regional player becoming a national champion, an Indian company attracting global capital, and ultimately, a multinational subsidiary returning to Indian ownership at precisely the moment when the country stands poised for its greatest infrastructure build-out in history.

What makes Ambuja particularly fascinating from a business strategy perspective is how it consistently zigged when others zagged. When competitors focused on production capacity, Ambuja obsessed over logistics. When others chased volume, Ambuja pursued efficiency. When the industry accepted road transport as inevitable, Ambuja literally took to the seas. These contrarian bets, executed with remarkable discipline over four decades, created a moat that even the deepest pockets couldn't easily replicate.

The timing of this analysis couldn't be more relevant. India's cement consumption is expected to double by 2030, driven by massive government infrastructure spending, rapid urbanization, and a housing boom that shows no signs of slowing. The company that Sekhsaria and Neotia founded to capture India's first wave of liberalization-era growth is now positioned to ride an even bigger wave under Adani's ownership.

II. The Founding Story: Traders Turn Industrialists

The story of Ambuja Cements begins not in a boardroom or an engineering college, but in the trading floors of Kolkata where Narotam Sekhsaria and Suresh Neotia first made their fortunes. In the early 1980s, these two businessmen were successful traders dealing in various commodities, but they shared a growing conviction that India was on the cusp of dramatic change. The country's socialist economic model was showing cracks, infrastructure was desperately inadequate, and whispers of liberalization were beginning to circulate in business circles.

Sekhsaria, in particular, was fascinated by a simple observation: India's per capita cement consumption was abysmally low compared to other developing nations. In 1983, Indians consumed barely 30 kg of cement per person annually, while China was already at 100 kg and developed nations were consuming 300-500 kg. He saw not a saturated market but an ocean of untapped demand waiting for the right catalyst. That catalyst, he believed, would be economic liberalization and the infrastructure boom that would inevitably follow.

The decision to enter cement manufacturing was audacious for two traders with no industrial experience. Cement is one of the most capital-intensive industries, requiring massive upfront investments, complex technical knowledge, and sophisticated supply chain management. But Sekhsaria and Neotia approached the challenge with a trader's mindset: they understood arbitrage, efficiency, and the importance of controlling costs. These principles would become the foundation of Ambuja's competitive advantage.

Their choice of Gujarat as the location for their first plant was strategic and prescient. The state offered proximity to high-quality limestone deposits, access to ports for future expansion, and a pro-business government that actually wanted industrial development. While established players were concentrated in traditional cement hubs, Ambuja's founders saw opportunity in Gujarat's relatively underdeveloped cement market. The state was beginning its own economic transformation, and they wanted to be the suppliers of choice for its growth. Ambuja Cement was founded in 1983 by Narotam Sekhsaria and Suresh Neotia, two traders with very little knowledge of cement or manufacturing. The partnership was remarkable for its complementary nature. Sekhsaria obtained his Bachelor's in Chemical Engineering with honours and distinction from the University of Bombay, which provided some technical grounding, while Neotia brought financial acumen and connections. Together, they pooled resources and raised initial capital through a combination of personal savings, bank loans, and strategic partnerships.

The first cement plant was set up in a record time of two years, an achievement that would become legendary in Indian industrial circles. While competitors typically took four to five years to commission new plants, Ambuja's founders drove their team with an urgency that bordered on obsession. They worked eighteen-hour days, personally supervised construction, and made decisions on the spot rather than waiting for committee approvals. This speed wasn't recklessness—it was calculated aggression designed to capture market share before competitors could react.

From a single plant with a capacity of 700,000 tonnes per annum in 1986 to a cement giant, the transformation was methodical and strategic. The founders understood that in a capital-intensive industry like cement, the key to profitability wasn't just production capacity but operational efficiency. They invested heavily in the latest technology, importing equipment from Europe and Japan when Indian alternatives would have been cheaper but less efficient.

The post-liberalization period of the early 1990s proved to be the inflection point Sekhsaria and Neotia had anticipated. As the Indian economy opened up, infrastructure spending exploded, and cement demand grew at double-digit rates. Ambuja was perfectly positioned to capitalize on this boom, having built capacity ahead of demand rather than chasing it. In 1993, the company was the first in India to issue GDRs (Global Depository Receipts), raising $60 million, a move that not only provided growth capital but also signaled Ambuja's global ambitions.

What set Ambuja apart from its competitors wasn't just its production capacity or financial engineering—it was a fundamental rethinking of how cement should be produced and distributed in India. The founders questioned every assumption, from the location of plants to the mode of transportation, from the role of dealers to the importance of branding. This first-principles thinking would lead to innovations that would reshape the entire Indian cement industry.

The company culture that emerged reflected the founders' trading background in unexpected ways. Decision-making was fast and decentralized, more like a trading floor than a traditional manufacturing company. Employees were encouraged to take calculated risks and were rewarded for efficiency improvements, no matter how small. This spirit finds expression inside Ambuja Cement in its philosophy of letting its employees set their own goals and giving them the freedom to achieve them. This autonomous work culture creates an environment which is conducive to growth and sets no limits to excellence and efficiency.

By the mid-1990s, Ambuja had established itself as a formidable player in the Indian cement industry. The company that started with two traders and a dream had become a case study in entrepreneurial success. But the real innovations—the ones that would make Ambuja a target for global giants—were still to come. The foundation was solid, built on efficiency, speed, and a willingness to challenge conventional wisdom. Now it was time to revolutionize how cement moved from plant to market.

III. Innovation as DNA: The Sea Transport Revolution

The year 1993 marked a watershed moment in Indian cement logistics, though few recognized it at the time. Ambuja Cements was facing a classic infrastructure problem: their highly efficient plant in Gujarat was producing world-class cement at competitive costs, but transporting it to Mumbai—India's largest construction market—was eating away all their margin advantages. Road transport meant dealing with poor highways, multiple state checkpoints, pilferage, and costs that could reach 30-40% of the total delivered price. Rail was unreliable and often unavailable. Most cement companies simply accepted these constraints as the cost of doing business in India. Narotam Sekhsaria saw an opportunity to completely reimagine the supply chain.

When the cost of transporting cement by road seemed expensive, it became the first Indian company to use the sea to transport cement in bulk. In 1993, a whole system was set up to conquer the lucrative cement market in Mumbai. The audacity of this move cannot be overstated. Cement and seawater were considered natural enemies—any moisture could ruin the product. Moreover, India had no infrastructure for bulk cement handling at ports. Critics called it foolhardy; competitors watched with amusement, expecting failure.

An all-weather port was built at Muldwarka, Gujarat, just 8km from the company's Ambujanagar plant, transforming what was essentially a fishing village into a sophisticated logistics hub. This wasn't just about building a jetty—Ambuja had to create an entire ecosystem. They designed specialized cement carriers with sealed compartments and moisture-control systems. They built bulk cement terminals at destination ports. They created unloading systems that could handle 5,000 tonnes per day. Every component had to be invented, tested, and perfected. The technical challenges were immense. Ambuja Cement, in 1992, was the first cement company in the country to kick-start transportation of bulk cement by coastal shipping as the best mode of sustainable transport among all other modes of transport and the most cost-effective way. The company had to develop pneumatic unloading systems that could discharge cement from ships directly into storage silos without exposure to moisture. They installed sophisticated aeration systems to keep cement flowing smoothly through pipes. They created closed-loop systems that prevented dust pollution at ports—a major concern for urban terminals.

The financial commitment was staggering for a company of Ambuja's size at the time. Building ships, ports, and terminals required capital that could have funded several new cement plants. But Sekhsaria's trader instincts told him that controlling logistics would provide a more sustainable competitive advantage than simply adding production capacity. He was betting that the cost savings from sea transport would not only justify the investment but create a moat that landlocked competitors could never cross.

The results exceeded even the most optimistic projections. Sea transport reduced logistics costs by 40-50% compared to road transport. Transit time from Gujarat to Mumbai dropped from 48 hours by road to 12 hours by sea. Pilferage and damage, which could account for 2-3% losses in road transport, virtually disappeared. Most importantly, Ambuja could now deliver cement to Mumbai at prices that undercut local producers, despite being located hundreds of kilometers away.

Ambuja Cements currently operates 11 dedicated cement carriers that transport cement from plants to consumption areas. The fleet has grown from a single experimental vessel to become one of the most sophisticated cement logistics operations in the world. Each ship is specially designed with features like closed hatches, dehumidification systems, and specialized holds that prevent cement from settling or absorbing moisture during transit.

The ripple effects of this innovation transformed the Indian cement industry. Over the years, many companies have followed Ambuja Cement's lead and today about 10% cement travels by this route. Competitors were forced to either replicate Ambuja's model—requiring massive capital investments—or cede coastal markets. The government took notice and began improving port infrastructure to support bulk cargo handling. What started as one company's logistics hack became a new paradigm for industrial transportation in India.

The innovation didn't stop with basic sea transport. Ambuja pioneered the use of specialized bulk cement terminals at strategic locations along India's coastline. These terminals acted as distribution hubs, allowing the company to serve markets that were previously inaccessible or unprofitable. The company built terminals not just at major ports but also at smaller harbors, creating a network that could deliver cement to any coastal city within 24 hours.

Environmental benefits, though not the primary motivation initially, became increasingly important. Sea transport produces significantly lower carbon emissions per tonne-kilometer compared to road transport. It was also the first to introduce Shore Power Supply to all her ships at the captive jetties, further reducing emissions when ships were docked. This environmental edge would become crucial as sustainability moved from nice-to-have to must-have in the cement industry.

The operational complexity of managing a shipping operation alongside a cement manufacturing business created unexpected synergies. The discipline required for maritime operations—strict schedules, preventive maintenance, safety protocols—improved overall operational excellence across the company. Ship crews became another source of innovation, suggesting improvements that were adapted for land-based operations.

The success of the sea transport initiative also demonstrated Ambuja's ability to execute complex, capital-intensive projects—a capability that would attract international attention. When global cement majors evaluated Indian companies for partnerships or acquisitions, Ambuja's logistics infrastructure was often cited as a key differentiator. It showed that this wasn't just a cement company that happened to own ships; it was an integrated logistics and manufacturing enterprise that happened to make cement.

Looking back, the sea transport revolution was about more than reducing costs or improving margins. It was about reimagining what a cement company could be. By refusing to accept the constraints that limited their competitors, Ambuja's founders created a new business model that combined manufacturing excellence with logistics innovation. This DNA of challenging conventional wisdom and finding creative solutions to structural problems would define Ambuja's trajectory for decades to come.

IV. The Holcim Era: Going Global

The year 2006 marked a pivotal transformation in Ambuja's journey from an ambitious Indian cement company to a global player. He divested his interest in Ambuja and ACC to Holcim Group Switzerland in 2006 and was appointed Chairman of both Companies. This wasn't a distress sale or a founder's exit—it was a strategic partnership designed to catapult Ambuja into a new league of operational excellence and global best practices. Holcim acquired management control of Ambuja in 2006. The Swiss cement giant didn't just buy a company; it acquired a gateway into one of the world's fastest-growing cement markets. Holcim had, in January, bought a 14.8 percent promoters' stake in the GACL for ₹2,140 crore, followed by a series of transactions that eventually gave them majority control. From 2010 to 2022, Holcim held a 61.62% controlling stake in Ambuja Cements, making it the primary vehicle for Holcim's ambitious India expansion strategy.

The attraction was mutual and strategic. For Holcim, India represented the future of global cement demand—a young population, rapid urbanization, and massive infrastructure deficits that would require decades of construction. For Ambuja, Holcim brought world-class technology, access to global best practices, and deep pockets for expansion. Since entering India in 2005, Holcim has established a track record of sustainable value creation with strategic investments ranging from new best-in-class plants to green technologies such as heat recovery systems.

The technology transfer was immediate and transformative. Holcim introduced advanced process control systems that could optimize fuel consumption in real-time, reducing energy costs by 15-20%. They brought in vertical roller mills that were more efficient than traditional ball mills. They implemented predictive maintenance systems that reduced unplanned downtime. These weren't just incremental improvements—they represented a generational leap in cement manufacturing technology.

In 2013, Holcim group announced a mega-rejig of its holding across Ambuja Cement & ACC by merging Holcim (India) Private Limited with Ambuja thereby making ACC, a subsidiary of Ambuja. This restructuring was crucial because it created operational synergies between two of India's most prestigious cement brands. ACC, founded in 1936, was India's first cement company and brought with it a legacy of trust and an extensive distribution network. The combined entity could now offer customers a complete portfolio of products while optimizing production and logistics across a much larger footprint.

The operational improvements under Holcim were remarkable. Plant utilization rates increased from 75% to over 90%. Energy consumption per tonne of cement dropped by 25%. Water consumption was reduced by 40% through recycling and rainwater harvesting. These efficiency gains didn't just improve margins—they positioned Ambuja as one of the most sustainable cement producers globally, a crucial advantage as environmental regulations tightened.

The global financial crisis of 2008-09 tested the Holcim-Ambuja partnership. Indian cement demand contracted for the first time in decades as real estate projects stalled and infrastructure spending was curtailed. But Holcim's global perspective and financial strength proved invaluable. While competitors cut capacity and laid off workers, Holcim continued investing in Ambuja's expansion, betting on India's long-term growth story. This counter-cyclical investment paid off handsomely when demand recovered in 2010-11.

Under Holcim's ownership, Ambuja also pioneered sustainability initiatives that went far beyond regulatory compliance. The company became one of the first in India to use alternative fuels like biomass and industrial waste in its kilns. It developed special blended cements that reduced clinker content without compromising strength, cutting CO2 emissions by 20-30%. These innovations weren't just good for the environment—they created a significant cost advantage as carbon taxes and environmental regulations became more stringent.

The knowledge transfer wasn't one-directional. Ambuja's innovations in logistics and distribution were adopted by Holcim globally. The sea transport model was replicated in other coastal markets. Ambuja's rural marketing strategies, which involved educating masons and contractors about proper cement usage, became a template for emerging market operations. The Indian operations became a laboratory for frugal innovation that could be applied across Holcim's global footprint.

The Holcim era also saw Ambuja's transformation from a commodity producer to a solutions provider. The company launched specialized products for different applications—sulfate-resistant cement for coastal construction, rapid-hardening cement for infrastructure projects, and premium products for high-rise buildings. They established technical service teams that worked with large contractors to optimize concrete mix designs. This shift up the value chain improved margins and created deeper customer relationships.

Their combined footprint includes 31 cement manufacturing sites and 78 ready-mix concrete plants with 10,700 people across India. This massive scale, built through a combination of organic growth and strategic acquisitions, made the Ambuja-ACC combine one of the most valuable cement assets globally. The geographical spread ensured proximity to major demand centers while the product portfolio could serve every segment from affordable housing to mega infrastructure projects.

The financial performance during the Holcim years validated the strategic logic of the partnership. Revenues grew from ₹3,000 crores in 2006 to over ₹15,000 crores by 2021. EBITDA margins consistently exceeded 20%, among the highest in the global cement industry. Return on capital employed stayed above 15% despite massive capacity additions. These metrics made Ambuja-ACC the crown jewel in Holcim's emerging market portfolio.

But by 2021, Holcim's global strategy was shifting. The company wanted to reduce its exposure to carbon-intensive cement production and focus on value-added building solutions in developed markets. According to Holcim, the company wants to make its revenues green. The company had laid out its Strategy 2025 and to lead with sustainable building solutions. The company has already exited or divested various cement assets in countries such as Brazil, Northern Ireland, Sri Lanka, Malaysia and Russia. At the same time it has been on a spree to buy greener assets in Europe and the United States to augment its solutions & products revenue.

Holcim has signed a binding agreement for the Adani Group to acquire its business in India, comprising its 63.11% stake in Ambuja Cement, which owns a 50.05% interest in ACC, as well as its 4.48% direct stake in ACC. The decision to exit India after 17 years wasn't about Ambuja's performance—it was about Holcim's transformation into a different kind of company. For Ambuja, it meant finding a new owner who could continue the growth journey in an increasingly competitive and consolidated Indian cement market.

V. The Adani Acquisition: India's Infrastructure Play

On 14 April 2022, Holcim announced that it would exit from the Indian market after 17 years of operations as part of a strategy to focus on core markets, and listed its stakes in Ambuja Cements and ACC for sale. What followed was one of the most intense bidding wars in Indian corporate history. According to various media reports, apart from Adani Enterprises, companies such as industrialist Sajjan Jindal-led JSW Group, Dalmia Bharat, Aditya Birla Group's UltraTech Cement Ltd and ArcelorMittal were also believed to be in the race for Holcim Group's Indian assets. According to the Financial Express, JSW Group was intending to place a $7-billion bid for the twin assets, with $4.5 billion from its own kitty and the remaining $2.5 billion to be raised from private equity players.

The competition was fierce because everyone understood what was at stake. This wasn't just about acquiring cement plants—it was about securing a strategic position in what would be the world's largest infrastructure build-out over the next three decades. India's cement consumption was projected to double by 2030, driven by a $1.4 trillion National Infrastructure Pipeline, affordable housing schemes, and rapid urbanization. Whoever controlled Ambuja-ACC would have a front-row seat to this growth story.

"The Adani Family, through an offshore special purpose vehicle, announced that it had entered into definitive agreements for the acquisition of Switzerland-based Holcim Ltd's entire stake in two of India's leading cement companies – Ambuja Cements Ltd and ACC Ltd. Holcim, through its subsidiaries, holds 63.19% in Ambuja Cements and 54.53% in ACC (of which 50.05% is held through Ambuja Cements). The value for the Holcim stake and open offer consideration for Ambuja Cements and ACC is USD ~10.5 billion, which makes this the largest ever acquisition by Adani, and India's largest ever M&A transaction in the infrastructure and materials space."

"Our move into the cement business is yet another validation of our belief in our nation's growth story," said Mr Gautam Adani, Chairman of the Adani Group. But this wasn't just patriotic rhetoric. Adani's infrastructure ecosystem—ports, logistics, power, and real estate—created unique synergies that other bidders couldn't match. The group could source raw materials through its ports, transport cement through its logistics network, power plants with its renewable energy, and consume cement in its own infrastructure projects.

The valuation raised eyebrows. Adani has agreed to buy shares in Ambuja Cements for Rs 385 per share and shares in ACC for Rs 2300 apiece, according to the statement. Thus the $10.5-billion deal is at a 4 per cent premium (for both ACC and Ambuja) from last close on April 13, when the news about Holcim's plans were first reported by Bloomberg News. If one looks at the share price from Friday's close, Adani is buying Ambuja at over 7 per cent premium and ACC at about 8 per cent premium.

Critics argued that Adani was overpaying, especially given the debt-funded nature of the acquisition. Like most of the Adani group expansion and entry into new businesses are debt funded and kind of leverage buyouts. The whole transaction is executed by Acquisition of holding outside India by the non-resident family members by taking temporary Acquisition financing and then replacing financing based on the security of Ambuja cements Ltd and ACC Ltd shares. But Adani was playing a different game—he wasn't just buying cement capacity; he was acquiring the missing piece of his infrastructure empire.

The synergies were compelling and immediate. Adani's ports could handle limestone and coal imports more efficiently. The group's renewable energy assets could provide green power at competitive rates, crucial for an energy-intensive industry where power costs account for 25-30% of production costs. "When augmented with our renewable power generation footprint, we gain a big headstart in the decarbonization journey that is a must for cement production." The logistics network could optimize distribution, reducing freight costs that often exceed manufacturing costs.

After Adani Group taking over ACC and Ambuja Cement, the EBITDA has risen to Rs 1,350 per tonne from Rs 350 and the group is looking to scale it up to Rs 1,400 by 2024, sources said. Since taking over in September 2022, the EBITDA per tonne of cement has increased from Rs 350 to Rs 1,350, company sources said adding this will be scaled up to Rs 1,400 per tonne by 2024. These weren't just marginal improvements—they represented a fundamental restructuring of the cost base that transformed the economics of the business.

The integration strategy was swift and decisive. Within months of the acquisition, Adani implemented a series of operational improvements. Procurement was centralized to leverage group-wide purchasing power. Coal sourcing was shifted to more efficient channels using Adani's trading expertise. Logistics routes were optimized using the group's multi-modal transportation network. The results were dramatic—operational efficiency improved, costs declined, and margins expanded.

Immediately after completion of Open Offer, Adani group announced preferential allotment to Harmonia Trade and Investment Limited for ₹20,000 crore in Ambuja. This increased Adani Group's holding by circa 19.39% in the listed entity. This additional capital injection wasn't just about increasing stake—it was growth capital for an aggressive expansion plan that would challenge UltraTech's dominance.

The cultural integration was equally important. Unlike typical private equity buyers who might have focused solely on financial engineering, Adani brought an entrepreneurial energy that resonated with Ambuja's heritage. The company that Sekhsaria and Neotia had built on innovation and efficiency found a kindred spirit in Adani's growth-oriented, execution-focused culture. Key talent was retained, best practices were preserved, and the entrepreneurial DNA that made Ambuja special was not just maintained but amplified.

"Maybe, the Adani group with a presence in logistics and power can make a difference," he says. This is where the ports piece is strategic it can move cement from the west to east cutting through the south. Besides, their road construction business and the ability to use the railways will help in cutting logistics costs. Industry analysts began to understand that this wasn't just about adding cement capacity to a conglomerate—it was about reimagining how cement could be produced and distributed in India.

The financing structure demonstrated Adani's financial engineering capabilities. The group raised funding from international banks, leveraging its strong relationships and track record. The debt was structured to be refinanced once operational improvements kicked in, reducing the cost of capital over time. This wasn't reckless leverage—it was calculated risk-taking based on a clear vision of value creation through operational improvements and synergy capture.

Looking at the acquisition from a strategic perspective, it represented a masterclass in platform economics. Adani wasn't just buying standalone assets; he was acquiring components that would make his entire infrastructure platform more valuable. Cement would benefit from the ecosystem, and the ecosystem would benefit from cement. This circular synergy created value that financial buyers or even strategic buyers without Adani's infrastructure footprint simply couldn't replicate.

VI. Building a Cement Empire: Operations & Scale

Currently, Ambuja Cement has a cement capacity of 31 million tonnes with six integrated cement manufacturing plants and eight cement grinding units across the country. But this figure understates the true scale of the empire Adani is building. Adani cement has 14% market share as of Q3FY24. The Company with its subsidiary ACC Ltd. has a capacity of over 67.5 million tons, making it the second-largest cement manufacturer in India after UltraTech's 120 million tonnes per annum capacity.

The geographic footprint of Ambuja-ACC is strategically distributed across India's high-growth corridors. Plants in Gujarat and Rajasthan serve the booming western markets. Facilities in Himachal Pradesh and Punjab cater to the infrastructure-heavy northern region. The eastern plants in Chhattisgarh and Jharkhand tap into the mineral-rich belt's industrial demand. Southern presence through recent acquisitions provides access to India's most competitive but lucrative cement market. This pan-India presence ensures that Ambuja is never more than 300 kilometers from any major demand center.

The Company currently has 12 ongoing expansion initiatives, which are expected to add 19 MTPA of cement capacity and 11 MTPA of clinker capacity, with phased commissioning beginning in Q4 FY 2024-25. Additionally, the Board has approved new cement grinding units at various locations, which will increase cement capacity by another 21 MTPA and clinker capacity by 16 MTPA. This aggressive expansion program represents one of the largest capacity additions in the global cement industry, designed to capture India's infrastructure boom before competitors can react.

The operational metrics tell a story of dramatic transformation under Adani's ownership. After Adani Group taking over ACC and Ambuja Cement, the EBITDA has risen to Rs 1,350 per tonne from Rs 350 and the group is looking to scale it up to Rs 1,400 by 2024. Since taking over in September 2022, the EBITDA per tonne of cement has increased from Rs 350 to Rs 1,350. This isn't just margin improvement—it's a fundamental restructuring of the cost base that makes Ambuja one of the most profitable cement operations globally. The product portfolio has evolved dramatically from the commodity-focused approach of the past. While Ordinary Portland Cement (OPC) and Portland Pozzolana Cement (PPC) remain the bread and butter, Ambuja now offers specialized products for every construction need. Sulfate-resistant cement for coastal and marine structures. Rapid-hardening cement for infrastructure projects with tight deadlines. Low-heat cement for massive concrete structures like dams. Premium products for high-rise buildings that require exceptional strength and durability. Each product carries higher margins and creates deeper customer relationships.

The distribution network is perhaps Ambuja's most underappreciated asset. With over 50,000 channel partners ranging from large dealers in metros to small retailers in rural areas, Ambuja has created a distribution moat that new entrants simply cannot replicate. This network wasn't built overnight—it represents four decades of relationship building, credit management, and market development. The company's direct-to-site delivery capabilities for large projects bypass traditional distribution, improving margins while ensuring quality control.

The digital transformation of operations under Adani has been remarkable. AI-powered demand forecasting helps optimize production schedules. IoT sensors monitor equipment health in real-time, predicting failures before they occur. Blockchain technology is being piloted for supply chain transparency. Digital platforms connect dealers directly to plants, reducing order processing time from days to hours. These aren't just efficiency improvements—they're creating a fundamentally different operating model for the cement industry.

The human capital story is equally compelling. Ambuja employs over 10,000 people directly and supports hundreds of thousands of livelihoods through its ecosystem. Under Adani's ownership, there's been a conscious effort to retain the entrepreneurial culture that Sekhsaria and Neotia fostered while injecting new energy and ambition. Performance-based incentives, extensive training programs, and clear career progression paths have reduced attrition to industry-leading levels.

The logistics infrastructure deserves special mention. Beyond the pioneering sea transport system, Ambuja has invested heavily in rail connectivity, with dedicated sidings at most plants. The company operates one of the largest private truck fleets in India, ensuring last-mile delivery capability. Automated loading systems have reduced truck turnaround time from hours to minutes. GPS tracking of every shipment provides real-time visibility and prevents diversion. This logistics excellence translates directly to customer satisfaction and market share gains.

Raw material security is another critical component of the empire. Ambuja controls limestone reserves sufficient for over 50 years of production at current rates. Coal linkages have been secured through long-term contracts and captive imports through Adani's ports. Fly ash agreements with thermal power plants provide sustainable raw materials while reducing environmental impact. Gypsum sourcing has been diversified across domestic and international suppliers. This raw material security provides a competitive advantage in an industry where input availability often determines success.

The maintenance and reliability programs at Ambuja plants are world-class. Total Productive Maintenance (TPM) initiatives have pushed equipment availability above 95%. Predictive maintenance using vibration analysis and thermal imaging prevents unexpected breakdowns. The average kiln run length—the time between mandatory maintenance shutdowns—exceeds 300 days, among the best globally. These operational excellence metrics translate directly to lower costs and higher margins.

Quality control systems ensure that every bag of cement meets stringent standards. Automated sampling and testing occur at multiple points in the production process. The company maintains NABL-accredited laboratories at all plants. Third-party quality audits provide additional assurance. Customer complaint resolution times have been reduced to less than 24 hours through dedicated service teams. This obsession with quality has made Ambuja the preferred choice for critical infrastructure projects.

The working capital management deserves recognition. Despite the capital-intensive nature of cement manufacturing, Ambuja maintains one of the most efficient working capital cycles in the industry. Inventory turns have improved by 30% under Adani's ownership. Receivables management is sophisticated, with credit scoring systems for dealers and automated collection processes. The cash conversion cycle has been reduced to less than 30 days, freeing up capital for growth investments.

Looking at the competitive landscape, Ambuja's position is formidable but not unassailable. India's top four cement companies—UltraTech, ACC-Ambuja, Shree Cement, and Dalmia Cement—are set to add over 42 million tonnes of capacity in FY25, increasing their market share from 48% in FY23 to an expected 54% by FY26. This consolidation trend favors large players like Ambuja who have the financial muscle and operational expertise to acquire and integrate smaller players efficiently.

The regional dynamics add another layer of complexity. In the north and west, Ambuja enjoys strong market positions with premium pricing power. The south remains intensely competitive with multiple regional players fighting for share. The east offers growth potential but requires careful navigation of local politics and logistics challenges. The company's strategy of maintaining a balanced presence across regions provides resilience against regional economic cycles.

VII. Post-Acquisition Growth & Consolidation

The post-Adani era at Ambuja Cements has been characterized by an acquisition spree that would make even the most aggressive private equity firms take notice. In June 2024, Ambuja Cements acquired Hyderabad-based Penna Cement Industries at an enterprise value of ₹10,422 crore. This wasn't just another bolt-on acquisition—it was a strategic masterstroke that instantly gave Ambuja a commanding presence in South India, a market where it had historically been underrepresented.

Penna Cement, with its strategically located assets and ample limestone reserves, offers Ambuja Cements a robust platform to enhance its production capabilities. This acquisition will add 14 mtpa of production capacity, providing Ambuja Cement with an additional 3 million tonnes of clinker and 4 million tonnes of cement capacity. The deal is anticipated to enhance Ambuja's market share in South India by 8-15% and provide entry into the Sri Lankan market, while also allowing for further inorganic growth opportunities.

The Penna acquisition demonstrated Adani's ability to move fast and decisively. While competitors were still evaluating the asset, Adani had already completed due diligence, arranged financing, and closed the deal. The integration was equally swift—within months, Penna's operations were aligned with Ambuja's systems, its dealer network was integrated, and cost synergies were being realized. The acquisition came at an attractive valuation of approximately ₹744 per tonne of capacity, significantly below replacement cost.

In October 2024, Ambuja Cement acquired CK Birla Group's Orient Cement at an approximate value of ₹8,100 crore. OCL has 5.6 MTPA clinker capacity and 8.5 MTPA cement capacity, along with statutory clearance to increase the clinker capacity by another 6.0 MTPA and cement capacity by another 8.1 MTPA. In addition, OCL also has a limestone mining lease in Chittorgarh for setting up an Integrated Unit (IU) with clinker of 4 MTPA and a split Grinding Unit (GU) of 6 MTPA in North India.

The Orient Cement acquisition was particularly strategic because of its asset quality and growth potential. OCL's assets are highly efficient, equipped with railway sidings and well supported by captive power plants, renewable energy, WHRS and AFR facilities. OCL's strategic locations, high-quality limestone reserves and requisite statutory approvals present an opportunity to increase cement capacity in the near term to 16.6 MTPA.

These acquisitions aren't happening in isolation—they're part of a carefully orchestrated strategy to achieve market leadership. By acquiring OCL, Ambuja is poised to reach 100 MTPA cement capacity in FY25. The acquisition will help to expand Adani Cements' presence in core markets and improve its pan-India market share by 2 per cent. The company has set an ambitious target: Adani Group's production capacity to over 140 million tonnes per annum (mtpa) by 2028.

The financing strategy for these acquisitions reveals sophisticated financial engineering. Rather than leveraging up the balance sheet, Ambuja has maintained its financial strength. The acquisition will be fully funded through internal accruals. This approach preserves financial flexibility for future opportunities while maintaining the strong credit profile necessary for a capital-intensive business.

The integration playbook that Ambuja has developed is becoming a competitive advantage in itself. Within 100 days of acquisition, IT systems are integrated, procurement is centralized, and best practices are implemented. The company maintains dedicated integration teams that move from one acquisition to the next, accumulating expertise and reducing execution risk. Cultural integration receives equal attention, with extensive communication programs and retention bonuses for key talent.

Beyond the headline acquisitions, Ambuja has been quietly consolidating its position through smaller deals and capacity additions. In August 2023, Ambuja Cement acquired Sanghi Industries at an enterprise value of ₹5,000 crore. Sanghi brought not just 6.1 MTPA of cement capacity but also strategic access to coastal Gujarat markets and significant limestone reserves. The recent Sanghi Cement acquisition added 6.1 million tonne of cement capacity, 6.6 million tonne of clinker capacity and 1.1 billion tonne of limestone reserves - enough to cater to additional production of 24 million tonne per annum of cement.

The competitive dynamics in the Indian cement industry are forcing consolidation at an unprecedented pace. India's top four cement companies—UltraTech, ACC-Ambuja, Shree Cement, and Dalmia Cement—are set to add over 42 million tonnes of capacity in FY25, increasing their market share from 48% in FY23 to an expected 54% by FY26. This consolidation is being driven by multiple factors: smaller players struggling with cost pressures, environmental regulations requiring significant capital investments, and the economies of scale becoming increasingly important.

The battle with UltraTech for market leadership has intensified. Moody forecasts India's cement demand to grow 6-7% compound annual growth rate (CAGR) through 2030, driving sector consolidation as major players like UltraTech and Ambuja expand capacity. Both companies are pursuing aggressive acquisition strategies, often competing for the same assets. The rivalry has pushed up valuations but also accelerated the pace of consolidation. Industry observers compare it to the telecom consolidation of the 2010s, predicting that only 5-6 major players will dominate the market by 2030.

The organic growth initiatives complement the acquisition strategy. Ambuja Cement Ltd (ACL) has announced an investment of approximately Rs. 1,600 crore (US$ 184.2 million) to establish a cement grinding unit in Warisaliganj, located in the Nawada district of Bihar. These greenfield and brownfield expansions target specific markets where Ambuja sees demand growth outpacing supply additions.

The technological integration across acquired assets is creating a unified, efficient production network. Ambuja has standardized operating procedures across all plants, implemented common ERP systems, and created centers of excellence for specific functions. The company's digital command center in Ahmedabad monitors operations across all plants in real-time, identifying optimization opportunities and sharing best practices instantly. This technological backbone makes each new acquisition easier to integrate and faster to optimize.

The Adani Group has set a clear target: to capture 20 per cent of the Indian cement market by the 2028 financial year. This would require adding approximately 75-80 MTPA of capacity from current levels—a Herculean task that would typically take a decade or more through organic growth alone. The acquisition strategy accelerates this timeline dramatically, but execution risk remains significant.

The market's response to Ambuja's consolidation strategy has been mixed. While some investors appreciate the growth potential and synergy opportunities, others worry about integration risks and the pace of expansion. The stock market has been volatile, with Ambuja's share price fluctuating based on acquisition announcements and quarterly results. However, operational metrics continue to improve, validating the strategy at least in the near term.

Looking at the broader implications, Ambuja's consolidation strategy is reshaping the Indian cement industry. Smaller players are increasingly looking to sell rather than compete against deep-pocketed giants. Regional dynamics are shifting as national players expand their footprints. Pricing discipline is improving as the market consolidates. The industry is moving from a fragmented, regional structure to an oligopolistic national market—a transformation that Ambuja is both driving and benefiting from.

The human capital management during this rapid expansion deserves recognition. Each acquisition brings thousands of new employees into the Ambuja fold. The company has developed sophisticated programs for cultural integration, skill development, and performance management. Retention rates for key talent from acquired companies exceed 90%, preserving institutional knowledge while injecting fresh perspectives.

The sustainability angle of consolidation is often overlooked but increasingly important. By acquiring and modernizing older, less efficient plants, Ambuja is actually reducing the industry's overall carbon footprint. Modern pollution control equipment is installed, energy efficiency is improved, and alternative fuels are introduced. This environmental improvement story resonates with regulators, communities, and increasingly ESG-conscious investors.

VIII. Sustainability & Innovation Focus

The transformation of Ambuja Cements into a sustainability leader represents one of the most remarkable environmental turnarounds in global heavy industry. We are proud to be 8x plastic negative and 11x water positive, actively taking steps to reduce plastic use and replenish water resources. These aren't just marketing claims—they represent fundamental changes in how a cement company can operate in harmony with its environment.

Ambuja Cements Limited is committed to Net Zero by 2050. The Company is also committed to the GCCA Roadmap for Net Zero Concrete by 2050. These commitments warrant that the Company is making steadfast progress toward a net zero and sustainable future. This commitment is particularly significant given that cement production accounts for approximately 8% of global CO2 emissions. Ambuja's approach demonstrates that even the most carbon-intensive industries can chart a path toward sustainability.

The company aims to achieve a 21% reduction in Scope 1 and Scope 2 emissions per ton of cementitious materials by 2030, using 2020 as the baseline year. Specifically, they target a 20% reduction in Scope 1 emissions and a 43% reduction in Scope 2 emissions within the same timeframe. These targets are aligned with the Science Based Targets initiative (SBTi) and are consistent with efforts to limit global warming to well below 2°C.

The green cement revolution at Ambuja goes beyond emissions targets. Ambuja Cements is the industry leader in manufacturing and selling blended cement, that is green cement with a much lower clinker factor. This not only helps the environment by using the slag and fly ash but also helps build durable and strong structures for the nation. More than 85% of the Company's production is in blended cements. This shift from Ordinary Portland Cement to blended varieties reduces the clinker factor—the most carbon-intensive component of cement—without compromising strength or durability.

The renewable energy transformation is equally impressive. Ambuja Cements is making sizeable investments in renewable and green energy to reduce its carbon footprint. This will lower its dependence on conventional electricity from grids and substantially shrink its carbon footprint. The green power share will increase to 60%, to be the largest in the industry with the planned expansion capacity. Ambuja Cements' renewable energy portfolio majorly includes solar and wind energy and WHRS in green energy.

From harnessing clean technology to using industrial wastes in cement production, energy conservation to deploying renewable energy and green energy, emissions reduction to creating institutionalised mechanisms to monitor environmental risks and strict adherence to the company's 'zero non-compliance' regime, Ambuja Cement's sustained efforts have helped ingrain the sustainability agenda in the company's DNA.

The water stewardship achievements are particularly noteworthy in a water-stressed country like India. Being 11x water positive means that Ambuja replenishes eleven times more water than it consumes in its operations. This is achieved through a combination of rainwater harvesting, watershed management, and community water projects. The company has created over 200 water harvesting structures that benefit not just its plants but entire communities.

Noteworthy is its co-processing of 126,000 tonnes of plastic waste, achieving 3.5 times plastic negativity. This plastic co-processing initiative serves dual purposes: it provides a solution for plastic waste management while reducing the consumption of fossil fuels in cement kilns. The high temperatures in cement kilns ensure complete destruction of plastics without harmful emissions, making it one of the most effective ways to manage non-recyclable plastic waste.

The alternative fuel and raw material (AFR) usage has become a cornerstone of Ambuja's sustainability strategy. Ambuja Cements, through its waste management arm Geoclean, takes a sustainable approach to managing industrial, agricultural, and municipal waste. Industrial waste, agricultural residues, and municipal solid waste are processed and used as alternative fuels, reducing dependence on coal while solving waste management challenges for communities.

The Company's specific thermal energy consumption has reduced from 760 kCal/kg of clinker produced in 2019 to 752 kCal/kg of clinker produced in FY 2023-24. The target is to reduce it to 710 kCal/kg of clinker produced by 2030. These efficiency improvements come from a combination of technology upgrades, process optimization, and operational excellence initiatives.

The innovation in product development has created new categories of sustainable construction materials. The innovative products range includes Ambuja Cement, Ambuja Plus, Ambuja Kawach, Ambuja Compocem, ACC F2R, ACC Suraksha, ACC Concrete Plus, ACC Gold and ACC HPC, all are GRIHA-listed contributing to sustainable construction. With more than 85% blended cement, the Companies have significantly reduced carbon footprint as compared to ordinary Portland cement, helping preserve natural resources. ACC's ECOMaxX, a Green Pro-certified concrete, helps reduce the carbon footprint for customers opting to choose a concrete based on their desired levels of CO2 reductions and sustainability objectives.

The community development initiatives extend sustainability beyond factory gates. Ambuja Cement Foundation (ACF), the CSR arm of Ambuja Cements, plays a pivotal role in community engagement and social development. Ambuja Cements, the cement and building cloth organization of the assorted Adani Group, via its CSR arm, has extensively addressed the vital water shortage in Magarway village in Baloda Bazaar-Bhatapara district, demonstrating its dedication closer to rural groups. The organization's initiatives have now not only alleviated the water crisis but also paved the way for lengthy-term sustainability, empowering the villagers and improving their normal best of existence.

The skill development programs deserve special recognition. Neev Abhiyan is a bespoke initiative by Ambuja Cement aimed at imparting formal training and skill building to unskilled labourers. This initiative helps them become trained masons and even contractors. The Neev Abhiyan initiative also helps address the growing demand for trained masons and contractors required by the rapidly growing construction sector in India. As part of the initiative, Ambuja Cement has created different modules to train construction workers, masons and contractors which are rolled out independently, in association with NGOs, or with government support.

The certification and recognition landscape validates Ambuja's sustainability leadership. All Ambuja Cements Limited plants are ISO 14001 certified. In 2008, the company adopted a goal of 'Zero Harm' working environment. This goal helped Ambuja Cement win the OH&S Excellence Awards 2014. The company has also been recognized as India's Most Trusted Cement Brand by TRA Research, reflecting how sustainability enhances brand value.

Looking at the carbon accounting in detail, In 2023, Ambuja Cements reported total greenhouse gas emissions of approximately 15,286,295,000 kg CO2e for Scope 1, 589,017,000 kg CO2e for Scope 2, and 4,728,204,000 kg CO2e for Scope 3 emissions. This reflects a commitment to transparency in their carbon footprint across all scopes of emissions. This comprehensive reporting goes beyond regulatory requirements, demonstrating genuine commitment to transparency and accountability.

The technological innovations driving sustainability are cutting-edge. Carbon capture and utilization technologies are being piloted at select plants. Artificial intelligence optimizes fuel mix in real-time to minimize emissions while maintaining quality. Blockchain technology is being explored for carbon credit trading and supply chain transparency. These aren't just experiments—they're building blocks of a fundamentally different cement company for the net-zero era.

The economic case for sustainability at Ambuja is compelling. Energy efficiency improvements have reduced operating costs by hundreds of crores annually. Alternative fuel usage has insulated the company from coal price volatility. Water recycling has reduced freshwater costs while improving community relations. Green products command premium pricing from environmentally conscious customers. Sustainability isn't a cost center at Ambuja—it's a profit driver.

IX. Playbook: Business & Investing Lessons

The Ambuja Cements story offers a masterclass in building and scaling an industrial enterprise in a developing economy. The first and perhaps most profound lesson is that domain expertise, while valuable, can be less important than market insight and execution capability. Ambuja Cement was founded in 1983 by Narotam Sekhsaria and Suresh Neotia, two traders with very little knowledge of cement or manufacturing. What made up for this lack was their farsightedness: Anticipating that cement would be a critical resource for a developing economy like India. Their success demonstrates that understanding market dynamics and customer needs can trump technical knowledge, provided you're willing to learn fast and hire expertise.

The second critical lesson revolves around operational efficiency as the ultimate competitive advantage in commodity businesses. When your product is largely undifferentiated, the company with the lowest cost structure wins. Ambuja's relentless focus on efficiency—from the EBITDA per tonne of cement has increased from Rs 350 to Rs 1,350 under Adani—shows how operational excellence can transform industry economics. This isn't about cutting corners; it's about reimagining every process to eliminate waste and maximize productivity.

The logistics innovation story teaches us about the value of challenging industry orthodoxy. When the cost of transporting cement by road seemed expensive, it became the first Indian company to use the sea to transport cement in bulk. In 1993, a whole system was set up to conquer the lucrative cement market in Mumbai. An all-weather port was built at Muldwarka, Gujarat, just 8km from the company's Ambujanagar plant, which became a benchmark for the industry. Over the years, many companies have followed Ambuja Cement's lead and today about 10% cement travels by this route. The lesson: competitive advantages often come from solving problems others accept as unsolvable.

Timing market cycles represents another crucial insight. Ambuja's major expansions often occurred during downturns when assets were cheap and competition was retrenching. The company's growth during the 2008-09 financial crisis, when backed by Holcim's capital, exemplifies counter-cyclical investing. Similarly, Adani's acquisition of Ambuja-ACC in 2022 during global market volatility demonstrates how bold moves during uncertain times can create extraordinary value.

The platform synergies lesson is particularly relevant in today's ecosystem economy. Adani's ability to extract value from Ambuja through integration with ports, power, and logistics assets shows how platform businesses can create value that standalone companies cannot. When augmented with our renewable power generation footprint, we gain a big headstart in the decarbonization journey that is a must for cement production. The lesson: in capital-intensive industries, the whole can be dramatically more valuable than the sum of parts.

Managing ownership transitions provides another set of valuable lessons. Ambuja successfully navigated from founder-ownership to multinational control under Holcim, and then to conglomerate ownership under Adani. Each transition brought new capabilities while preserving core strengths. The key was maintaining operational continuity and cultural values while adapting to new strategic priorities. This ability to evolve while preserving essence is rare and valuable.

The role of sustainability in modern manufacturing cannot be overstated. Ambuja's transformation into an environmental leader—8x plastic negative and 11x water positive—demonstrates that sustainability can be a source of competitive advantage rather than a compliance burden. Early investments in green technologies and processes positioned Ambuja favorably as regulations tightened and customers became more environmentally conscious.

The acquisition and integration playbook offers lessons in inorganic growth. Ambuja's rapid acquisition and successful integration of Penna, Orient, and Sanghi cements shows how to scale quickly without losing operational focus. The keys: maintain a dedicated integration team, standardize processes quickly, preserve local relationships, and capture synergies systematically. This move aligns with Ambuja's ambitious goal of reaching a cement production capacity of 140 million tonnes per annum (MTPA) by 2028.

Capital allocation discipline emerges as another critical lesson. Despite aggressive expansion, Ambuja has maintained a strong balance sheet. Acquisitions are funded through internal accruals rather than excessive leverage. This financial conservatism provides flexibility to seize opportunities while weathering downturns—a crucial balance in cyclical industries.

The importance of distribution and brand in commodity businesses is often underappreciated. Ambuja's 50,000+ dealer network and trusted brand command premium pricing in a supposedly undifferentiated market. The lesson: even in commodities, customer relationships and brand equity matter. Building these intangible assets takes decades but provides sustainable competitive advantages.

The technology adoption strategy offers insights for traditional industries. Ambuja didn't try to become a technology company but systematically adopted digital tools to enhance core operations. From AI-powered demand forecasting to IoT-based predictive maintenance, technology amplifies operational excellence rather than replacing it.

Human capital development stands out as a differentiator. This spirit of also finds expression inside Ambuja Cement in its philosophy of letting its employees set their own goals and giving them the freedom to achieve them. This autonomous work culture creates an environment which is conducive to growth and sets no limits to excellence and efficiency. This empowerment culture, rare in traditional manufacturing, attracts and retains talent while driving innovation.

The regulatory navigation expertise is crucial in India's complex business environment. Ambuja's ability to work with multiple state governments, obtain environmental clearances, and manage local stakeholders demonstrates the importance of regulatory competence. This isn't about influence; it's about systematic compliance and proactive engagement with regulators.

For investors, several key lessons emerge. First, look for companies addressing structural demand with supply-side advantages. India's infrastructure deficit ensures decades of cement demand, while Ambuja's operational efficiency provides supply-side edge. Second, value operational excellence over growth for growth's sake. Ambuja's margin expansion under Adani shows how efficiency drives returns. Third, recognize the value of strategic assets like logistics infrastructure or limestone reserves that provide sustainable moats.

The market timing lesson for investors is nuanced. Cement is cyclical, but structural growth can overwhelm cycles. Investors who focused on quarterly results missed the multi-decade growth story. The lesson: in structural growth markets, time in the market beats timing the market, provided you own best-in-class operators.

Risk management lessons abound. Ambuja's diversification across geographies, products, and customer segments provides resilience. Raw material security through long-term contracts and captive mines reduces input volatility. Multiple manufacturing locations prevent single-point failures. These risk mitigation strategies enable aggressive growth without existential exposure.

The ESG integration lesson is increasingly relevant. Ambuja Cements's score of 40 is higher than 95% of the industry. This ESG leadership attracts capital, reduces regulatory risk, and appeals to premium customers. For investors, ESG leaders in carbon-intensive industries may offer attractive risk-reward as the world transitions to net-zero.

Finally, the compounding lesson stands out. Ambuja's journey from 700,000 tonnes in 1986 to targeting 140 MTPA by 2028 represents a 200-fold increase. This wasn't achieved through one brilliant move but through decades of consistent execution, reinvestment, and incremental improvement. The lesson: in industrial businesses, sustained operational excellence compounds into extraordinary outcomes.

X. Analysis & Bear vs. Bull Case

Bull Case: The Infrastructure Superfecta

The bull case for Ambuja Cements rests on four powerful pillars that create a compelling investment thesis. First and foremost is India's infrastructure mega-cycle. The government's National Infrastructure Pipeline of $1.4 trillion, combined with housing demand from 300 million people entering the middle class by 2030, creates unprecedented cement demand. Moody forecasts India's cement demand to grow 6-7% compound annual growth rate (CAGR) through 2030, driving sector consolidation as major players like UltraTech and Ambuja expand capacity. This isn't a cyclical upturn—it's a structural transformation lasting decades.

The Adani ecosystem synergies represent a unique competitive advantage that's difficult to quantify but impossible to ignore. Adani's presence in ports, real estate, road construction, and power plants gives the cement business a ready-made customer base and access to railway rakes. The power business throws up fly ash, which is added to certain types of cement. The energy-intensive cement business also gets coal from Adani's mines in Australia. Adani's recent entry into renewable energy will help optimise costs. These aren't just paper synergies—they translate directly into lower costs and higher margins.

The consolidation leadership position creates a virtuous cycle. As Ambuja acquires smaller players at attractive valuations, it gains market share, improves pricing power, and achieves scale economies. India's top four cement companies—UltraTech, ACC-Ambuja, Shree Cement, and Dalmia Cement—are set to add over 42 million tonnes of capacity in FY25, increasing their market share from 48% in FY23 to an expected 54% by FY26. In a consolidating industry, being an acquirer rather than acquired creates tremendous value.

The cost advantages through renewable energy integration provide both economic and environmental benefits. The green power share will increase to 60%, to be the largest in the industry with the planned expansion capacity. As carbon taxes become reality and energy costs rise, Ambuja's renewable energy investments become increasingly valuable. This isn't just about sustainability compliance—it's about structural cost advantages in an energy-intensive industry.

The Penna acquisition exemplifies the value creation potential. This acquisition will add 14 mtpa of production capacity, providing Ambuja Cement with an additional 3 million tonnes of clinker and 4 million tonnes of cement capacity. The deal is anticipated to enhance Ambuja's market share in South India by 8-15% and provide entry into the Sri Lankan market. Entry into new geographies at reasonable valuations accelerates growth while diversifying market risk.

Bear Case: The Execution and Competition Challenges

The bear case begins with legitimate concerns about high acquisition valuations in a competitive M&A environment. With UltraTech and Ambuja bidding against each other for assets, sellers extract maximum value. The $10.5 billion paid for Ambuja-ACC was at peak valuations, and subsequent acquisitions, while strategic, require flawless execution to justify their prices. In a commodity business with volatile margins, overpaying for assets can destroy shareholder value.

Intense competition from UltraTech, with its 120 MTPA capacity and first-mover advantage in many markets, cannot be dismissed. UltraTech is the largest cement producer in India, with an estimated market share of 24-25%. The current capacity expansion will only solidify its position as an industry leader. UltraTech's established relationships, operational excellence, and financial strength make it a formidable competitor that won't cede market share easily.

Regulatory and environmental challenges are intensifying. Limestone mining permissions are becoming harder to obtain. Environmental clearances for new plants face increased scrutiny and delays. Carbon taxes and emission norms are tightening. Water usage restrictions in water-stressed regions limit production. These regulatory headwinds increase costs and slow expansion, potentially disrupting aggressive growth plans.

Commodity cycle risks remain ever-present. Cement is ultimately a cyclical business tied to construction activity. A real estate downturn, infrastructure spending cuts, or economic slowdown would impact demand and pricing power. With significant capacity additions across the industry, oversupply could pressure margins. The industry's history of boom-bust cycles suggests current optimism may be excessive.

Integration complexity represents a major execution risk. Ambuja is attempting to integrate multiple large acquisitions simultaneously while executing organic expansion. Each acquisition brings different systems, cultures, and operational practices. The bandwidth required to harmonize operations while maintaining performance is enormous. Integration failures could result in operational disruptions, market share losses, and value destruction.

The debt levels, while manageable, are increasing. Although Ambuja maintains that acquisitions are funded through internal accruals, the pace of expansion and capital requirements for organic growth strain the balance sheet. In a rising interest rate environment, higher leverage reduces financial flexibility and increases vulnerability to demand shocks.

Regional concentration risks persist despite geographic expansion. Certain regions contribute disproportionately to profitability. Competition is intensifying in southern markets where Ambuja is expanding. Northern markets face seasonal demand variations. Eastern markets have political and logistical challenges. This regional complexity makes consistent performance challenging.

Technology disruption, while seemingly distant, poses long-term risks. Alternative building materials, 3D printing in construction, and new cement technologies could disrupt traditional demand patterns. While cement seems irreplaceable today, technological shifts could alter industry dynamics over the investment horizon.

Balanced Perspective: The Probability-Weighted Outcome

The balanced view recognizes both the tremendous opportunity and significant risks. India's infrastructure needs are real and lasting—the country cannot achieve developed nation status without massive construction. This provides a robust demand foundation that can absorb supply additions. The question isn't whether demand will grow, but whether Ambuja can capture profitable share of that growth.

The Adani backing provides both advantages and baggage. Access to capital, ecosystem synergies, and execution capability are genuine advantages. However, the Adani name also attracts scrutiny, potentially higher cost of capital from ESG-conscious investors, and concentration risk from single-promoter dependence. Investors must weigh these factors based on their own risk tolerance and investment philosophy.

Adani cement has 14% market share as of Q3FY24. This market position is strong but not dominant. There's room for significant growth, but also vulnerability to competitive attacks. The path to 20% market share by 2028 is achievable but requires flawless execution and continued acquisition opportunities at reasonable valuations.

The sustainability leadership position provides optionality value. As regulations tighten and carbon pricing becomes reality, Ambuja's environmental investments may prove prescient. The company aims to achieve a 21% reduction in Scope 1 and Scope 2 emissions per ton of cementitious materials by 2030, using 2020 as the baseline year. Specifically, they target a 20% reduction in Scope 1 emissions and a 43% reduction in Scope 2 emissions within the same timeframe. These targets are aligned with the Science Based Targets initiative (SBTi). This positions Ambuja favorably for a carbon-constrained future.

The valuation debate is nuanced. At current multiples, Ambuja trades at a premium to historical averages but at a discount to potential based on execution of growth plans. Ambuja Cements shares are priced at around 41 times. Considering the current market position of Adani group companies in cement sector and its growth trajectory, I think at PE of 41, Ambuja Cements is fairly priced. The market is pricing in partial success—neither complete failure nor flawless execution.

The risk-reward appears favorable for long-term investors who believe in India's growth story and Adani's execution capability. For those seeking steady, predictable returns, the execution risks and competitive dynamics may be concerning. The investment case ultimately depends on one's view of India's infrastructure buildout, industry consolidation dynamics, and Adani's ability to create value through operational excellence and strategic acquisitions.

XI. Epilogue & Final Thoughts

The Ambuja Cements journey from a trader's dream to India's second-largest cement empire is more than a business success story—it's a narrative about India's economic transformation itself. When Narotam Sekhsaria and Suresh Neotia founded the company in 1983, India was a socialist economy with per capita cement consumption of just 30 kg. Today, as Ambuja targets 140 MTPA capacity by 2028, India consumes over 250 kg per capita and stands poised to become the world's largest construction market.

What makes Ambuja's journey particularly instructive is how it mirrors and anticipates India's development stages. The company's early focus on efficiency reflected the resource-constrained reality of 1980s India. The logistics innovations of the 1990s preceded India's infrastructure awakening. The global partnership with Holcim aligned with India's integration into the world economy. The Adani acquisition represents the confident, ambitious India that sees itself as a future superpower.

The sustainability transformation tells us something profound about the future of heavy industry in a climate-conscious world. Ambuja Cements Limited is committed to Net Zero by 2050. This isn't greenwashing or compliance theater—it's a fundamental recognition that industrial companies must reinvent themselves for a carbon-constrained future. Ambuja's success in reducing emissions while growing profitably provides a template for other carbon-intensive industries.

The infrastructure story underlying Ambuja's growth is just beginning. India needs to build the equivalent of a new Chicago every year for the next three decades to house its urban population. The country requires 40,000 kilometers of highways, 30,000 kilometers of railway lines, 100 new airports, and countless bridges, ports, and power plants. This isn't speculation—it's mathematical certainty based on demographic and economic trends. Companies like Ambuja that can execute at scale while maintaining quality will be the builders of new India.

The consolidation dynamics reshaping the cement industry reflect broader trends in Indian business. As the economy matures, fragmented industries are consolidating into oligopolies dominated by a few large, efficient players. This pattern, seen earlier in telecom, airlines, and retail, is now playing out in cement. India's top four cement companies—UltraTech, ACC-Ambuja, Shree Cement, and Dalmia Cement—are set to add over 42 million tonnes of capacity in FY25, increasing their market share from 48% in FY23 to an expected 54% by FY26. Winners in this consolidation capture enormous value; losers become acquisition targets or fade into irrelevance.

The technology integration story demonstrates how traditional industries must evolve. Ambuja isn't trying to become a software company, but it's systematically adopting digital tools to enhance core operations. This pragmatic approach to technology—focused on operational improvement rather than disruption—provides a model for other manufacturing companies navigating digital transformation.

For entrepreneurs, Ambuja's story offers both inspiration and practical lessons. You don't need deep domain expertise if you understand market dynamics and customer needs. Operational excellence beats brilliant strategy in commodity businesses. Challenging industry orthodoxy can create sustainable competitive advantages. Building for the long term, even through ownership changes and market cycles, creates compound value that short-term optimization never can.

For investors, the Ambuja case study illuminates several timeless principles. Great investments often come from structural trends rather than clever stock picking. Operational excellence, while boring, drives superior returns in capital-intensive industries. Platform businesses that create ecosystem synergies can generate value that standalone analysis misses. ESG leadership in carbon-intensive industries may offer asymmetric risk-reward as the world transitions to sustainability.

The governance and culture lessons are equally valuable. Ambuja's ability to maintain entrepreneurial culture through multiple ownership changes shows that organizational DNA can survive and thrive through transitions. This philosophy of letting its employees set their own goals and giving them the freedom to achieve them. This autonomous work culture creates an environment which is conducive to growth and sets no limits to excellence and efficiency. This empowerment philosophy, rare in traditional manufacturing, drives innovation and operational excellence.

Looking ahead, Ambuja's next chapter will be written in the context of India's infrastructure supercycle, the global energy transition, and the technology revolution reshaping manufacturing. The company's ambitious targets—100 MTPA by FY25, 140 MTPA by 2028—aren't just about scale. They're about positioning for a future where efficient, sustainable producers dominate while subscale, polluting operators become obsolete.

The competitive dynamics with UltraTech will intensify, potentially reshaping India's cement industry into a duopoly with a few smaller players. This competition, while challenging, will drive innovation, efficiency, and customer service improvements that benefit the entire ecosystem. The winner won't necessarily be the biggest, but the one that best combines scale, efficiency, sustainability, and customer focus.

The international expansion potential remains largely untapped. While Ambuja has focused on domestic growth, India's growing economic influence and infrastructure expertise create opportunities for expansion into South Asia, Africa, and other developing markets. The company's operational excellence and sustainability credentials position it well for international growth when the time is right.