Alok Industries: From Textile Giant to Bankruptcy to Reliance Rescue

I. Cold Open & The Unthinkable Deal

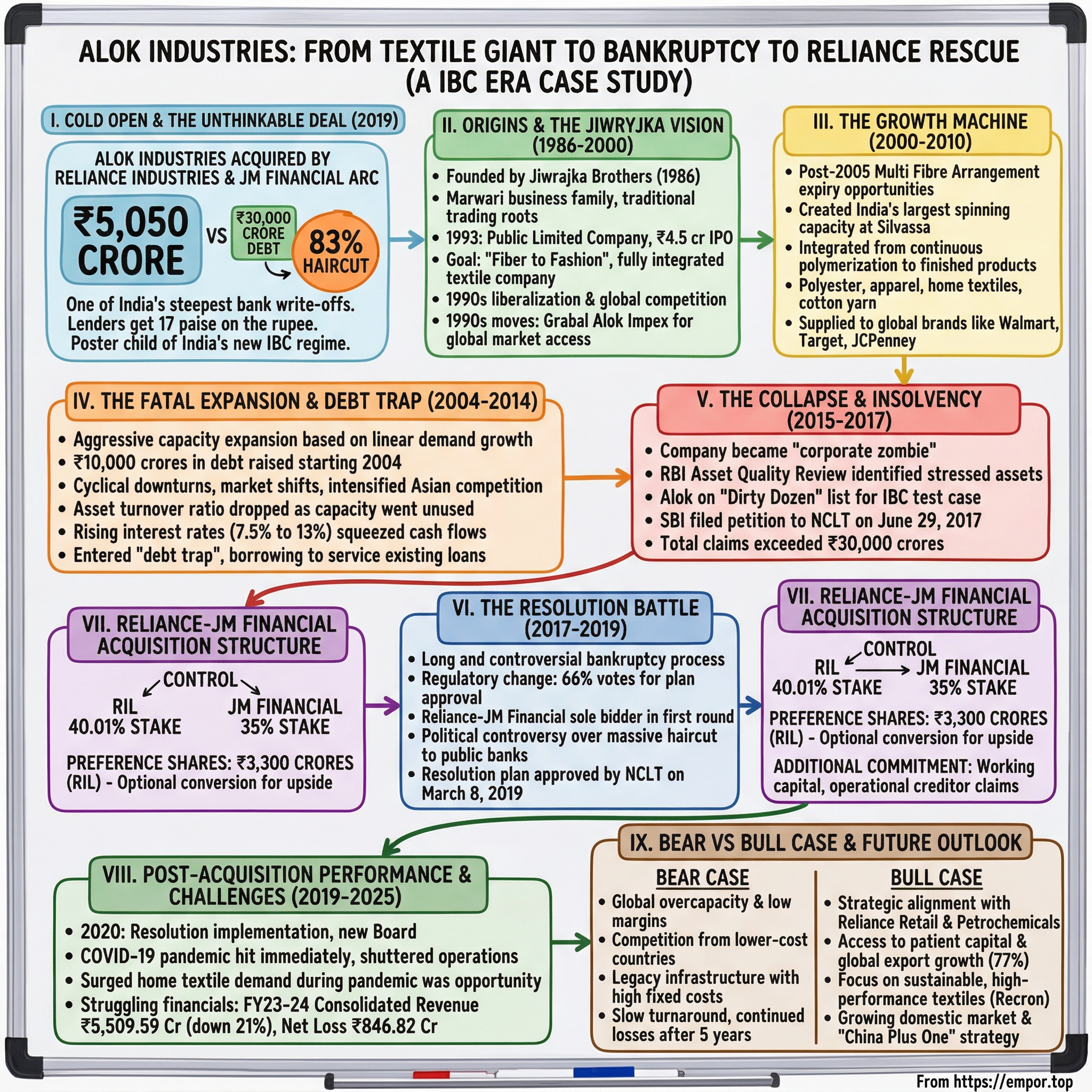

The Ahmedabad bench of the National Company Law Tribunal had seen many corporate battles, but March 8, 2019, was different. The judges approved what would become one of India's most controversial bankruptcy resolutions—Reliance Industries and JM Financial Asset Reconstruction Company would acquire Alok Industries for just ₹5,050 crore. The shock wasn't the acquisition itself, but the arithmetic: Alok owed nearly ₹30,000 crore to banks and operational creditors. The lenders were accepting an 83% haircut—one of the steepest write-offs in Indian corporate history.

Picture the scene in banking boardrooms across Mumbai that day. Senior executives who had extended billions in loans to what was once India's largest integrated textile company were now signing off on recovering just 17 paise on every rupee lent. How does a company that employed 26,000 people, operated world-class manufacturing facilities, and supplied fabric to global fashion houses collapse so spectacularly?

The answer lies in a decade-long saga of ambition, miscalculation, and the brutal economics of global textile manufacturing. Alok Industries wasn't just another corporate failure—it became the poster child for India's new bankruptcy regime, a test case for whether the Insolvency and Bankruptcy Code could handle complex corporate restructurings. What happened to Alok reveals uncomfortable truths about leverage, cyclical industries, and the price of trying to build a global champion from India.

For Reliance Industries, led by Mukesh Ambani, the acquisition represented something else entirely: a calculated bet on distressed assets at rock-bottom prices. While creditors mourned their losses, Reliance saw opportunity—vertical integration possibilities, export potential, and assets worth multiples of the purchase price. The deal would test whether financial engineering could resurrect what operational excellence couldn't sustain.

The story of Alok Industries is really three stories intertwined: the rise of an ambitious textile empire, the spectacular unraveling when debt met reality, and the ongoing experiment of whether deep-pocketed acquirers can extract value from corporate wreckage. Each chapter teaches different lessons about Indian capitalism, global competition, and the thin line between vision and delusion in business.

II. Origins & The Jiwrajka Vision (1986-2000)

In 1986, when Surendra Bhagirathmal Jiwrajka and his brother Bhagirathmal founded Alok Industries in Mumbai, India's textile industry was at an inflection point. The country was slowly emerging from decades of socialist policies, and entrepreneurs could finally dream beyond the "Hindu rate of growth." The Jiwrajka brothers didn't just want to make textiles—they wanted to revolutionize how India produced them.

The brothers came from a traditional Marwari business family with roots in trading, but they saw manufacturing as the future. Their timing was impeccable. India's textile industry in the late 1980s was fragmented, with thousands of small powerlooms and outdated spinning mills. Most Indian textile companies operated in silos—spinners sold to weavers, weavers to processors, processors to garment makers. Each handoff added cost and complexity. The Jiwrajkas envisioned something radically different: complete vertical integration under one roof.

When Alok went public in 1989, just three years after incorporation, it was still a modest operation. But the IPO prospectus revealed ambitious plans. The company would integrate "from fiber to fashion," controlling every step of textile production. This wasn't just operational efficiency—it was about capturing value at every stage of the supply chain. Where competitors saw discrete businesses, the Jiwrajkas saw an ecosystem.

The 1990s brought liberalization, and with it, exposure to global markets and competition. Suddenly, Indian textile companies weren't just competing with each other but with efficient producers from China, Bangladesh, and Vietnam. Many Indian players retreated or focused on protected domestic markets. Alok did the opposite—it decided to compete globally by building scale and integration that even international competitors would struggle to match. By the mid-1990s, the company had established its first major facility in Silvassa, strategically located near Mumbai but benefiting from tax incentives. In 1993, the fate of Alok Industries changed and it became a public limited company with an IPO of Rs. 4.5 crore. The Jiwrajkas weren't content with just spinning cotton—they wanted to control every stage from fiber to finished product. This obsession with integration would define both Alok's rise and eventual fall.

The late 1990s saw Alok make its first international moves. Through technical and financial collaboration with Grabal, Grabher Group GmbH of Austria, Alok entered the global embroidery market through Grabal Alok Impex Limited. This wasn't just about acquiring technology—it was about learning how European manufacturers operated, understanding quality standards that Indian companies rarely met, and building relationships with international buyers who had never considered India as a serious supplier.

By 2000, Alok had transformed from a startup into a serious player. The company was generating hundreds of crores in revenue, employed thousands of workers, and had begun exporting to developed markets. But this was just the foundation. The real ambition—and the seeds of destruction—would come in the next decade.

III. The Growth Machine (2000-2010)

The new millennium brought a fundamental shift in global textile trade. The Multi Fibre Arrangement, which had governed textile quotas since 1974, was set to expire in 2005. For countries like India, this meant unprecedented access to global markets. For the Jiwrajka brothers, it meant the opportunity to build something unprecedented—a fully integrated textile conglomerate that could compete with anyone, anywhere.

Alok's integration strategy was breathtaking in scope. In the polyester segment, the company was fully integrated starting from the continuous polymerization plant to the production of chips, POY, FDY, DTY, and PSF. Its apparel fabric division included woven fabric, knitted fabric, garments, and safety textiles. The home textiles business sold bedding and terry towels, while the cotton yarn division produced cotton and cotton blended fabrics in various counts on a wide range of finishes.

The polyester integration was particularly sophisticated. Starting with PTA (purified terephthalic acid) and MEG (monoethylene glycol), Alok could produce polyester chips, then convert them into various yarn types—partially oriented yarn (POY), fully drawn yarn (FDY), drawn texturized yarn (DTY), and polyester staple fiber (PSF). Each product served different market segments, from technical textiles to fashion fabrics. This wasn't just manufacturing—it was industrial choreography.

From an initial capacity of 50,000 spindles in 2007, Alok created India's largest spinning capacity at one location (Silvassa) with 411,840 spindles and 5,680 rotors to produce about 80,000 tons of cotton yarn per annum. Almost 95 percent of this yarn was consumed in-house for fabric production, making it the strongest vertical integration of textiles in India.

The numbers tell only part of the story. Walking through Alok's Silvassa facility in 2008 was like touring a small city. The complex sprawled across hundreds of acres, with different units for spinning, weaving, processing, and garmenting. Workers arrived in buses from surrounding villages, three shifts keeping the machinery running 24/7. The canteen served thousands of meals daily. The company had its own power plants, water treatment facilities, and even housing colonies.

Global brands began taking notice. Walmart, Target, JCPenney—retailers who had traditionally sourced from China or Bangladesh—started placing orders with Alok. The company's ability to control the entire supply chain meant faster turnaround times and consistent quality. If a buyer wanted a specific fabric construction with particular dyeing and finishing, Alok could deliver it all under one roof.

Looking to expand texturising capacity and save on raw material costs, Alok increased the total production capacity of POY from 54,000 tpa to 200,000 tpa through the continuous polymerization (CP) route in March 2009. Under the CP route, POY is manufactured from PTA and MEG. Alok Industries expected growth in global demand for polyester yarn and was setting up another CP plant with a capacity of 300,000 tonnes, taking the total capacity to 500,000 tonnes. Of this, 100,000 tpa commenced operation in March 2011.

The ambition was staggering. While competitors focused on niches—some did only spinning, others only home textiles—Alok wanted to do everything. The company wasn't just building factories; it was creating an ecosystem. Suppliers of chemicals and dyes set up facilities nearby. Logistics companies established dedicated routes. Banks opened branches to serve the thousands of employees.

But beneath the impressive growth lay a dangerous assumption: that global demand for textiles would keep growing indefinitely, that being the lowest-cost producer with the most integration would guarantee success. The Jiwrajkas were betting everything on scale, taking on massive debt to finance expansion. In boardrooms, they spoke of becoming a $5 billion company, of rivaling Asian textile giants, of making Alok a global household name.

By 2010, Alok Industries had completed 25 years of their corporate journey, with a turnover of more than Rs. 6,300 crores and received the IMC (RBNBQ) Award which accorded it with the status of 'Recognised Star Trading House.' The company seemed unstoppable, a testament to Indian entrepreneurship and ambition. Few could see the storm clouds gathering.

IV. The Fatal Expansion & Debt Trap (2004-2014)

The period from 2004 to 2014 would prove to be Alok's Icarus moment—flying too close to the sun on wings made of debt. What began as aggressive expansion turned into a cautionary tale about the perils of overleveraging in a cyclical industry.

Starting in 2004, Alok embarked on what can only be described as a borrowing binge. The company raised approximately ₹10,000 crores in debt, convinced that scale would provide an insurmountable competitive advantage. The logic seemed sound: textile manufacturing is a volume game where the lowest-cost producer wins. By building massive integrated facilities, Alok could theoretically produce at costs that smaller competitors couldn't match.

But the Jiwrajkas fundamentally misread the market. They built capacity assuming linear growth in global textile demand, ignoring the cyclical nature of the industry. Textile consumption doesn't grow steadily—it surges during economic booms and crashes during recessions. Fashion trends shift, consumer preferences change, and new competitors emerge from unexpected places. While Alok was building mega-factories, nimble producers in Bangladesh and Vietnam were capturing market share with smaller, more flexible operations.

The company's asset turnover ratio—a key measure of how efficiently a company uses its assets to generate sales—tells the story of this strategic miscalculation. From 2004 to 2014, this ratio fell drastically. Alok had built enormous capacity, but the sales weren't materializing to justify the investment. Factories designed to run at 90% capacity were operating at 60% or less. Fixed costs—interest payments, maintenance, salaries—kept mounting regardless of production levels.

The global financial crisis of 2008 should have been a warning. Textile demand plummeted as Western consumers cut spending. Orders from major retailers dried up. But instead of retrenching, Alok doubled down. The company continued its expansion, believing the downturn was temporary. Management spoke of being ready when demand returned, of gaining market share while competitors struggled.

Competition from other Asian nations intensified. Bangladesh, with its duty-free access to European markets and lower labor costs, became a formidable rival. Vietnam, benefiting from trade agreements and foreign investment, emerged as a preferred sourcing destination. China, despite rising costs, maintained its dominance through superior infrastructure and supply chain efficiency. Alok found itself in a brutal price war, with margins shrinking even as volumes grew.

The interest rate environment delivered the final blow. When Alok had borrowed in the mid-2000s, interest rates were around 7.5%. By 2013, the company was paying nearly 13% on its loans. This near-doubling of borrowing costs devastated cash flows. Every percentage point increase meant hundreds of crores in additional interest payments—money that should have gone to modernization, working capital, or debt reduction.

Consider the mathematics of destruction: ₹10,000 crores borrowed at 13% meant annual interest payments of ₹1,300 crores. Even in good years, Alok's EBITDA rarely exceeded ₹1,500 crores. After interest payments, there was barely enough left for maintenance capital expenditure, let alone growth investments or debt repayment. The company had entered what bankers euphemistically call a "debt trap"—borrowing more just to service existing loans.

The human cost was equally devastating. As financial pressure mounted, Alok began delaying salary payments. Vendors went unpaid for months. The company that once prided itself on being a premier employer became known for its financial distress. Talented managers left for competitors. Morale plummeted. The factories that once hummed with activity began showing signs of neglect—broken windows unreplaced, machinery maintenance deferred, safety standards compromised.

By 2014, the situation was irreversible. Alok owed money to everyone—banks, suppliers, employees, even statutory authorities. The company's working capital had evaporated. Orders required advance payments that Alok couldn't make. Banks refused to extend new credit. The spiral accelerated: less working capital meant fewer orders, which meant lower revenues, which meant even less ability to service debt.

V. The Collapse & Insolvency Proceedings (2015-2017)

The endgame began in 2015, though the company fought desperately to avoid the inevitable. Alok Industries had become a corporate zombie—technically alive but functionally dead. With ₹30,000 crores in debt against annual revenues that had collapsed to a fraction of their peak, the company was beyond conventional rescue.

The Reserve Bank of India had been watching. In 2015, the central bank initiated its Asset Quality Review, forcing banks to recognize stressed assets they had been hiding through restructuring schemes. Alok Industries couldn't hide anymore. It was the only textile company placed on the list of the 12 stressed units identified with the amendment of IBC—the so-called "Dirty Dozen" that would become test cases for India's new bankruptcy regime.

Inside Alok's Mumbai headquarters, the atmosphere was funereal. Senior executives spent more time in meetings with lawyers and bankers than running operations. The Jiwrajka family, once titans of industry, were reduced to pleading for one more restructuring, one more lifeline. They proposed asset sales, fresh equity infusions, operational improvements—anything to avoid losing control of their life's work.

But it was too late. On June 29, 2017, State Bank of India filed a petition before the National Company Law Tribunal for initiation of Corporate Insolvency Resolution Process against Alok Industries under the provisions of the Insolvency and Bankruptcy Code, 2016. The NCLT admitted the petition on July 18, 2017.

The admission to insolvency was a watershed moment. For the first time, one of India's largest companies would go through a court-supervised bankruptcy process. The resolution professional took control, displacing the Jiwrajka family from management. Employees worried about their futures. Suppliers wondered if they would ever be paid. The factories that had once symbolized India's manufacturing ambitions became symbols of corporate excess.

The insolvency process revealed the true extent of Alok's financial disaster. Claims poured in from creditors—not just banks but operational creditors who had supplied raw materials, provided services, or were owed statutory dues. The total claims exceeded ₹30,000 crores, making it one of the largest corporate insolvencies in Indian history.

The operational impact was immediate and severe. Production lines shut down as working capital disappeared. Export orders were cancelled. Thousands of workers were laid off or put on indefinite leave. The integrated manufacturing complex that had taken decades to build began deteriorating. Machinery gathered dust. Skilled workers dispersed to other companies or industries.

The social consequences rippled through communities. In Silvassa and Vapi, where Alok was a major employer, the economic impact was devastating. Small businesses that depended on Alok's workers—tea stalls, grocery stores, transport operators—saw their customer base evaporate. Banks that had given home loans to Alok employees faced rising defaults. The company's collapse wasn't just a corporate failure; it was a social catastrophe.

VI. The Bankruptcy Drama & Resolution Battle (2017-2019)

The insolvency proceedings that began in July 2017 would become a landmark case in Indian corporate history, testing the newly minted Insolvency and Bankruptcy Code and setting precedents for future resolutions. The drama that unfolded over the next 20 months had all the elements of a corporate thriller—bidding wars, regulatory changes, political controversy, and ultimately, a resolution that shocked the banking sector.

Initially, several parties expressed interest in acquiring Alok. The company's assets, despite the financial distress, were attractive—modern manufacturing facilities, established customer relationships, experienced workforce. But as potential bidders conducted due diligence, many backed away. The complexity of Alok's operations, the massive debt burden, and the deteriorating condition of assets scared off all but the most determined acquirers.

A crucial regulatory change altered the game. An ordinance to the Insolvency and Bankruptcy Code lowered the minimum votes needed for passing a resolution plan from 75% to 66%. This seemingly technical change had profound implications—it meant a resolution plan could be approved even if a significant minority of creditors objected. For Alok's resolution, this would prove decisive.

Reliance Industries and JM Financial ARC emerged as the sole bidder for Alok Industries in the first round. The Reliance-JM combine offered ₹5,050 crores for a company that owed nearly ₹30,000 crores—an 83% haircut that sent shockwaves through the banking sector. For Reliance, led by Mukesh Ambani, this wasn't just about acquiring distressed assets cheaply. It was about vertical integration for their retail ambitions and a strategic entry into textiles at a fraction of replacement cost.

The proposed haircut triggered political controversy. Opposition parties questioned how banks could accept such massive losses on public money. Parliamentary debates raged about crony capitalism and sweetheart deals. Bank unions protested, arguing that while promoters who had destroyed value walked away, public sector banks bore the losses. The media extensively covered every twist, making Alok a household name for all the wrong reasons.

Behind closed doors, the negotiations were intense. The Committee of Creditors, representing 27 banks, had to decide between accepting massive losses or potentially getting even less in liquidation. Financial models showed that liquidation would yield perhaps 10-15% recovery at best. The Reliance offer, while painful, was still better than the alternative. Banks also considered Reliance's track record and deep pockets, believing they could revive operations and preserve some jobs.

The resolution plan wasn't just about the headline number. It included intricate provisions for different classes of creditors, treatment of employees, and operational continuity. Reliance committed to infusing additional working capital, honoring certain operational creditor claims, and maintaining employment for a specified period. These commitments, while adding to the effective acquisition cost, were crucial for getting creditor approval.

On March 8, 2019, the Ahmedabad bench of the National Company Law Tribunal approved the resolution plan. The judgment was comprehensive, addressing various objections and establishing important precedents. The tribunal noted that while the haircut was substantial, the resolution was better than liquidation and achieved the IBC's objectives of maximizing asset value and balancing stakeholder interests.

The approval marked the end of the Jiwrajka family's control over Alok Industries. From founding the company in 1986 to losing it in 2019, their journey encapsulated the possibilities and perils of Indian entrepreneurship. They had built something remarkable but had been undone by excessive leverage and strategic miscalculation. The family's attempts to challenge the resolution through various legal avenues would continue, but their industrial empire was gone.

VII. The Reliance-JM Financial Acquisition Structure

The acquisition structure crafted by Reliance Industries and JM Financial was a masterclass in financial engineering, designed to minimize upfront cash outlay while maintaining control. Understanding this structure reveals how sophisticated buyers extract value from distressed situations and why the headline acquisition price often understates the true economic impact.

Reliance Industries holds 40.01% stake while JM Financial (acting as PAC with RIL) through its subsidiary holds 35% stake in it. Reliance Industries also has 9% optionally convertible preference shares and non-convertible redeemable preference shares worth 3,300 crores, making it a subsidiary of Reliance.

The equity structure was carefully calibrated. Reliance's 40.01% stake gave them effective control while keeping their direct exposure limited. JM Financial's 35% wasn't just passive investment—they acted as a Partner Acting in Concert (PAC) with Reliance, meaning their combined 75% gave them absolute control over all major decisions. This structure allowed Reliance to leverage JM Financial's expertise in distressed assets while sharing the risk.

The preference shares component added another layer of sophistication. The ₹3,300 crores in preference shares provided additional capital without diluting equity control. These instruments typically carry fixed dividends and conversion options, giving Reliance flexibility in how they eventually realize value. If Alok recovers strongly, they can convert to equity and capture the upside. If not, they maintain priority in capital structure.

Beyond the headline ₹5,050 crore acquisition price, Reliance committed substantial additional resources. Working capital infusion was critical—textile operations require significant funding for raw materials, and banks were reluctant to lend to a company just emerging from bankruptcy. Reliance's balance sheet strength and banking relationships were essential for restarting operations.

Why would Reliance, primarily known for petrochemicals and telecommunications, want a textile company? The strategic rationale was multifaceted. First, Reliance Retail was expanding aggressively, and vertical integration into textile manufacturing could provide cost advantages and supply chain control. Second, Alok's polyester operations complemented Reliance's petrochemical business—they could supply raw materials internally, capturing additional margin.

Third, and perhaps most importantly, Reliance got world-class manufacturing assets at a fraction of replacement cost. Building Alok's integrated facilities from scratch would cost tens of thousands of crores and take years. By acquiring through bankruptcy, Reliance paid perhaps 20% of replacement value. Even accounting for rehabilitation costs and working capital, the economics were compelling.

The timing was also strategic. In 2019, the textile industry was at a cyclical low, with global trade tensions and economic uncertainty depressing demand. Reliance was betting on eventual recovery, positioning themselves to benefit when the cycle turned. Their patient capital approach—ability to sustain losses while rebuilding operations—contrasted sharply with the financial stress that had doomed Alok under its previous owners.

For JM Financial, the investment represented their evolution from pure asset reconstruction to operational turnarounds. They brought expertise in navigating the IBC process, managing creditor relationships, and financial restructuring. Their partnership with Reliance combined financial engineering skills with operational capabilities—a powerful combination for distressed asset investing.

The acquisition also sent a broader signal to the market. Reliance's entry into textiles through bankruptcy acquisition showed that even the largest Indian conglomerates saw value in the IBC process. It legitimized distressed asset investing, previously seen as the domain of vulture funds. Other large corporates would subsequently follow Reliance's playbook, acquiring assets through the IBC at attractive valuations.

VIII. Post-Acquisition Performance & Challenges (2019-2025)

The resolution plan of Reliance Industries and JM Financial ARC was approved by the National Company Law Tribunal, Ahmedabad Bench in its order dated 8 March 2019 and the implementation of the Approved Resolution Plan was concluded in 2020 with the re-constitution of the Board of Directors on 14th September, 2020. But just as Reliance was preparing to revive Alok's operations, the world changed dramatically.

The COVID-19 pandemic struck just months after Reliance took control. Global textile demand collapsed as retailers cancelled orders and consumers stopped shopping for apparel. The factories that Reliance had planned to restart remained shuttered during lockdowns. Workers who had hoped for stability faced continued uncertainty. The revival plan, carefully crafted over months, had to be completely reimagined.

Yet the pandemic also revealed unexpected opportunities. Home textile demand surged as people spent more time indoors. The work-from-home revolution drove demand for comfortable, casual clothing. Supply chain disruptions in competing countries created opportunities for Indian manufacturers. Reliance's deep pockets allowed Alok to weather the storm and position for recovery while competitors struggled. The financial performance tells a sobering story. Operating income during the year fell 21.2% on a year-on-year basis in FY23-24. The Company achieved a consolidated revenue of ₹5,509.59 crore lower by 21.26% as compared to consolidated revenue of ₹6,989.20 crore in the previous year. The reported consolidated Loss After Tax for the year was ₹846.82 crore as compared to Loss After Tax of ₹880.46 crore in the previous year.

Despite the losses, there are signs of operational improvement. Operating EBITDA was ₹71.91 crore as compared to negative EBITDA of ₹12.82 crore in the previous year. This shift from negative to positive EBITDA, while modest, suggests that at an operational level, the business is stabilizing. The challenge remains the massive debt burden inherited from the bankruptcy—even with the haircut, servicing the remaining obligations consumes most operational cash flow.

Export sales increased by 77.55% to Rs. 1,699.54 crore from Rs. 957.20 crore in previous year. This export growth is particularly significant given the challenging global environment. It suggests that under Reliance's management, Alok is regaining credibility with international buyers who had abandoned the company during its financial distress.

The management changes reflect Reliance's hands-on approach. Mr. Harsh Bapna was appointed as Chief Executive Officer and Key Managerial Personnel of the Company with effect from 01st April, 2024. The company has also brought in textile veterans like Biji Chacko as Group Chief Operating Officer, signaling serious intent to revive operations rather than simply harvesting assets.

Now part of Reliance Industries, India's largest conglomerate, Alok Industries is set to strengthen its position in the global textile market. The integration with Reliance's broader ecosystem is beginning to show results. Alok Industries incorporates innovative technologies from Reliance, including, Recron GreenGold, Recron EcoGold, Recron Kooltex, and Ecotherm for sustainable and high-performance textiles.

The most recent quarterly results paint a mixed picture. The revenue of Alok Industries Ltd for the Dec '24 is ₹870.63 crore as compare to the Sep '24 revenue of ₹898.78 crore. The EBITDA of Alok Industries Ltd for the Dec '24 is ₹-35.11 crore as compare to the Sep '24 EBITDA of ₹-32.59 crore. The net profit of Alok Industries Ltd for the Dec '24 is ₹-272 crore as compare to the Sep '24 net profit of ₹-262 crore.

The continued losses, even five years after acquisition, raise questions about the turnaround timeline. Reliance's patient capital approach means they can sustain these losses, but investors wonder when—or if—profitability will return. The company faces structural challenges: global overcapacity in textiles, competition from lower-cost producers, and the massive fixed costs of maintaining integrated operations.

IX. Business Model Analysis & Competitive Dynamics

Understanding Alok's business model requires appreciating the complexity of integrated textile manufacturing. The company operates through four main divisions, each representing different stages of the textile value chain and serving distinct market segments.

The polyester division (61% of business) is fully integrated starting from the continuous polymerization plant to the production of chips, POY, FDY, DTY, and PSF. The apparel fabric division (18%) includes woven fabric, knitted fabric, garments, and safety textiles. Home textiles (12%) sells bedding and terry towels. Cotton yarn (9%) produces cotton and cotton blended fabrics in various counts on a wide range of finishes.

The polyester integration is particularly strategic. Starting with basic petrochemical inputs, Alok can produce various yarn types that serve different end-markets. POY (partially oriented yarn) goes to texturizers, FDY (fully drawn yarn) directly to weavers, DTY (drawn textured yarn) for knitting, and PSF (polyester staple fiber) for blending with cotton. This diversity provides resilience—when one segment weakens, others might compensate.

The competitive positioning is challenging. In polyester, Alok competes with massive Chinese producers who benefit from scale and government support. In cotton, Bangladesh and Vietnam have emerged as formidable competitors, offering similar quality at lower costs due to preferential trade agreements and lower wages. India's infrastructure challenges—power costs, logistics inefficiencies, regulatory complexity—add to the competitive disadvantage.

Yet Alok has certain advantages. The integrated model allows for quick response to customer needs. A buyer wanting a specific fabric with particular specifications can get everything done under one roof—spinning, weaving, dyeing, finishing. This speed and flexibility matter in fashion, where trends change rapidly and time-to-market is critical.

The home textiles segment shows particular promise. As global consumers increasingly shop online, demand for bedding and bath products has grown. Alok's ability to offer complete solutions—from yarn to finished products—appeals to large retailers looking to simplify their supply chains. The company's recent focus on sustainable and innovative fabrics aligns with changing consumer preferences.

Raw material cost pressures remain a perpetual challenge. Cotton prices fluctuate based on weather, global demand, and government policies. Polyester inputs track crude oil prices, adding another layer of volatility. Managing these input costs while maintaining competitive pricing requires sophisticated hedging strategies and operational flexibility.

The global textile industry is undergoing structural shifts that affect Alok's prospects. The "China Plus One" strategy adopted by many brands—diversifying sourcing beyond China—should benefit Indian manufacturers. Sustainability concerns are driving demand for traceable, environmentally friendly production. Automation is reducing the labor cost advantage of traditional textile exporters.

Alok's response has been to focus on value-added products rather than commodity textiles. Technical textiles for industrial applications, performance fabrics for sportswear, sustainable materials using recycled inputs—these segments offer better margins than basic fabrics. The challenge is that these markets require continuous innovation and customer engagement, capabilities that atrophied during Alok's financial distress.

The domestic market presents both opportunity and challenge. India's growing middle class drives apparel demand, but the market is highly fragmented with numerous small players. E-commerce growth benefits organized players like Alok who can ensure consistent quality and reliable supply. The integration with Reliance Retail provides a captive customer, though transfer pricing and arm's length considerations limit how much this relationship can be leveraged.

X. Playbook: Lessons from India's IBC Era

Alok Industries has become the definitive case study for India's Insolvency and Bankruptcy Code era, offering crucial lessons about corporate restructuring, distressed investing, and the real cost of excessive leverage. The playbook that emerges from this saga applies far beyond textiles.

The IBC, enacted in 2016, fundamentally changed how India handles corporate bankruptcy. Before IBC, the process was chaotic—multiple forums, endless litigation, asset stripping by promoters. Companies could remain in limbo for decades while value evaporated. The IBC introduced time-bound resolution, creditor committees with real power, and crucially, the ability to replace management. Alok was among the first major tests of this new regime.

The acceptance of 83% haircuts marked a psychological shift in Indian banking. For decades, banks had pretended that bad loans would eventually be repaid, engaging in elaborate restructuring schemes that merely postponed recognition of losses. The Alok resolution forced reality—sometimes recovering 17% is better than chasing 100% forever. This acceptance, painful as it was, began clearing the banking system's clogged arteries.

For distressed asset investors, Alok established a template. Patient capital with operational expertise could acquire world-class assets at fractional values. The key was having the staying power to weather initial losses while rebuilding operations. Reliance's approach—bringing in professional management, investing in working capital, leveraging group synergies—showed how financial engineering alone wasn't enough. Operational turnaround was essential.

The role of patient capital cannot be overstated. Reliance knew that reviving Alok would take years, possibly decades. They had the balance sheet to sustain losses while rebuilding. This contrasts sharply with private equity buyers who typically need returns within 5-7 years. In distressed situations, the ability to take a 10-15 year view can be the difference between success and failure.

Capital allocation lessons emerge starkly. The Jiwrajkas' error wasn't building an integrated textile business—that strategy had merit. The fatal flaw was financing it entirely with debt, leaving no buffer for industry downturns. They violated the fundamental rule of matching assets and liabilities: long-term assets require long-term capital, preferably equity. Using short-term debt for long-term capacity expansion is a recipe for disaster.

The operational turnaround versus financial engineering debate finds resolution in Alok's story. Financial restructuring—the debt haircut—was necessary but not sufficient. Without operational improvements, new investment, and customer confidence restoration, even the reduced debt would eventually become unsustainable. Successful turnarounds require both financial and operational expertise.

The IBC process also revealed the importance of stakeholder management. Creditors, employees, vendors, customers, regulators—each group had different interests and concerns. The resolution plan had to balance these competing claims while maintaining business viability. The political scrutiny added another dimension, making the process as much about perception management as financial restructuring.

For banks, Alok highlighted the perils of herd behavior in lending. During the boom years, every bank wanted exposure to Alok, competing to offer loans. Due diligence was superficial, relying on the assumption that such a large company couldn't fail. When troubles emerged, the same herd behavior operated in reverse—everyone wanted out simultaneously, accelerating the collapse.

XI. Bear vs Bull Case & Future Outlook

The investment case for Alok Industries today presents a fascinating study in contrasts, with compelling arguments on both sides that reflect broader questions about India's manufacturing future and the economics of turnaround investing.

The bear case starts with brutal industry realities. Global textile manufacturing suffers from chronic overcapacity, with new production constantly coming online in lower-cost countries. Margins are wafer-thin, and differentiation is difficult. Technology disruption—from synthetic biology creating new materials to automation reducing labor advantages—threatens traditional producers. Alok, with its legacy infrastructure and high fixed costs, seems poorly positioned for this evolution.

The financial performance reinforces skepticism. Five years after acquisition, the company continues posting losses. Quarterly results show revenue declining and losses persisting. The debt burden, while reduced from pre-bankruptcy levels, still constrains investment capacity. Interest coverage remains negative. At current burn rates, even Reliance's patience might eventually wear thin.

Structural challenges within India compound the difficulties. Power costs remain high compared to competitors. Labor productivity lags despite lower wages. Port infrastructure and logistics add time and cost. Regulatory compliance creates friction. These factors aren't company-specific but affect Alok's competitiveness nonetheless.

The bull case, however, sees hidden value and turnaround potential. With a market cap of ₹8,823 crore, Alok trades at a fraction of replacement cost. Building similar integrated facilities today would cost ₹30,000-40,000 crore. Even in distress, the assets have substantial value. If operations stabilize and generate even modest profits, the equity could multiply.

The Reliance backing provides crucial advantages. Access to working capital, customer relationships through Reliance Retail, raw material synergies with petrochemical operations—these create competitive advantages independent operators lack. Reliance's digital initiatives could eventually revolutionize supply chain management and customer engagement.

Export growth demonstrates operational recovery momentum. International customers returning to Alok signals restored confidence. As global brands diversify supply chains away from China, India stands to benefit. Alok's integrated capabilities and Reliance backing position it to capture this shift.

The sustainability trend favors integrated producers who can ensure supply chain transparency and environmental compliance. Alok's investments in sustainable technologies and renewable energy address these concerns. As regulations tighten globally, compliant producers will command premiums.

India's domestic consumption story remains compelling. With per capita textile consumption still low compared to developed markets, growth potential is substantial. The formalization of retail, e-commerce expansion, and rising disposable incomes all benefit organized players like Alok.

Can Alok return to profitability? The path exists but requires multiple factors aligning. Global textile demand must grow faster than capacity additions. India needs to improve its manufacturing competitiveness through infrastructure investment and regulatory reform. Alok must complete its operational turnaround, achieving efficiency levels that justify its integrated model.

The timeline matters as much as the destination. If profitability takes another 5-10 years, the equity returns might still disappoint even if the turnaround succeeds. The opportunity cost of capital locked in a perpetual turnaround could exceed eventual gains. For investors, the question isn't just whether Alok will recover, but whether the wait justifies the risk.

XII. Epilogue & Reflections

The Alok Industries saga transcends a simple corporate failure and rescue story. It serves as a mirror reflecting the ambitions, excesses, and evolution of Indian capitalism over three decades. From entrepreneurial vision to reckless expansion, spectacular collapse to controversial rescue, each chapter teaches enduring lessons about business, finance, and human nature.

What this case teaches about leverage and growth is sobering. The Jiwrajkas weren't fraudsters or incompetents—they were experienced industrialists who built something remarkable. But they confused growth with progress, scale with strength. They believed that being bigger would make them invincible, that integration would provide unassailable competitive advantage. Instead, size became a liability when markets turned, and integration meant nowhere to hide when demand collapsed.

The leverage that enabled rapid expansion became the noose that strangled the company. Every downturn required more borrowing to survive, creating a vicious cycle. Interest payments consumed cash flow that should have funded innovation and efficiency improvements. The company was running harder just to stand still, then running harder still just to move backward more slowly.

India's corporate debt resolution journey found its poster child in Alok. The IBC process, for all its imperfections, worked. A company that would have languished in limbo for decades under the old regime was resolved in two years. Creditors took losses but recovered something. New owners brought fresh capital and expertise. Jobs were preserved, at least partially. The system proved it could handle complex corporate restructurings.

Yet uncomfortable questions linger. Should banks have extended such massive loans to a single borrower? Did regulatory forbearance allow problems to metastasize? Could earlier intervention have preserved more value? The 83% haircut represents not just financial losses but misallocated social resources—capital that could have funded education, healthcare, or infrastructure instead disappeared into unproductive assets.

The price of ambition in cyclical industries emerges as a central theme. Textiles, like most commodities, experiences regular boom-bust cycles. Building a business assuming perpetual boom is hubris. The survivors are those who prepare for downturns during upturns, who maintain financial flexibility when others leverage up, who remember that cycles are called cycles because they come back around.

For investors, Alok offers a meditation on value creation versus value destruction. The same assets that destroyed tens of thousands of crores under one ownership might create value under another. The difference lies not in the physical assets but in how they're financed, managed, and positioned. Value is contingent, not inherent—dependent on strategy, execution, and timing.

The human dimension deserves acknowledgment. Behind the financial statistics were real people—workers who lost jobs, vendors who went unpaid, investors who lost savings. The Jiwrajka family lost not just wealth but legacy, their name forever associated with one of India's largest corporate failures. These human costs, unmeasurable in spreadsheets, represent the true price of corporate excess.

Looking forward, Alok Industries remains a work in progress, its final chapter unwritten. Will Reliance succeed in turning around what the Jiwrajkas couldn't sustain? Will integrated textile manufacturing prove viable in India? Will the assets acquired for ₹5,000 crore eventually justify multiples of that valuation?

These questions matter beyond Alok's specific fate. They probe whether India can build globally competitive manufacturing, whether the IBC can consistently resolve corporate distress, whether patient capital can resurrect failed businesses. Alok Industries, even in its diminished state, remains a test case for Indian capitalism's maturation.

The story's ultimate lesson might be about humility. In business, as in life, success is temporary, failure is educational, and resurrection is possible but never guaranteed. The Alok Industries saga—from textile giant to bankruptcy to Reliance rescue—reminds us that in capitalism's creative destruction, today's giants can become tomorrow's casualties, and today's wreckage might become tomorrow's foundation for renewal.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube