Alkyl Amines Chemicals: India's Specialty Chemical Champion

I. Introduction & Episode Roadmap

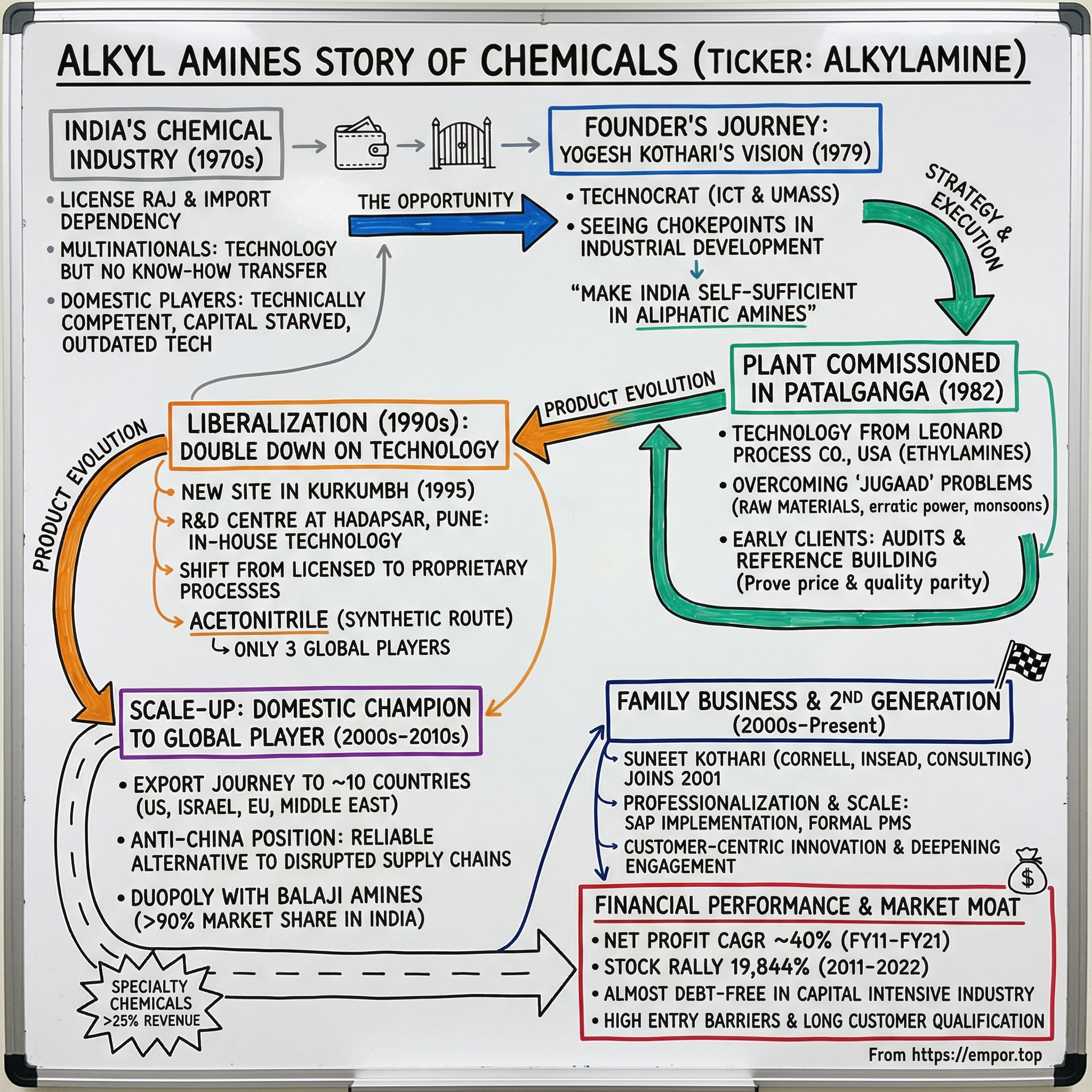

Picture this: In 1979, while India was still deep in the throes of the License Raj, a chemical engineer named Yogesh Kothari saw something others didn't—a glaring import dependency that was bleeding precious foreign exchange. Every kilogram of aliphatic amines that Indian pharmaceutical and agrochemical companies needed came from overseas, shipped in at premium prices with long lead times. Kothari didn't just see a problem; he saw India's next chemical champion waiting to be born.

The company was incorporated by Kothari in 1979 with the idea of making India self-sufficient in aliphatic amines. What started as an import substitution play in a Patalganga plant has transformed into something far more ambitious. Today, Alkyl Amines Chemicals Limited (AACL) is a global supplier and leader in aliphatic amine, amine derivative and specialty amines, commanding markets from pharmaceuticals to water treatment across continents.

The numbers tell a story of remarkable transformation: The company offers over 100 products and is a global leader in several products, including synthetic Acetonitrile, DMAHCL, Triethylamine, Diethylhydroxylamine, and is the sole global producer of many specialty amines. It exports its products to approximately 10 countries, including Philippines, United States of America, Israel, Norway, Spain, United Kingdom, Switzerland, Belgium, Malaysia, and Middle East countries.

This isn't just another chemical company story. It's about how a post-liberalization Indian firm cracked the code on competing globally in specialty chemicals—a space dominated by century-old Western giants and aggressive Chinese competitors. How did a company from Maharashtra become the sole global producer of certain specialty amines? Why are multinational pharmaceutical companies depending on a firm that didn't exist when most of them were already giants?

Our journey today takes us from the congested chemical clusters of 1970s India to the sophisticated R&D labs of modern Pune, from fighting for technology licenses to developing proprietary processes that even global leaders can't replicate. We'll explore how focus, technical expertise, and the often-underestimated power of niches can build a global champion. And yes, we'll tackle the paradox of how being debt-free in a capital-intensive industry became both a strength and perhaps a constraint.

II. The Pre-History: India's Chemical Industry Context

To understand Alkyl Amines' emergence, we need to first grasp the chemical landscape of 1970s India—a terrain shaped by socialist planning, chronic shortages, and the omnipresent hand of government control. The License Raj didn't just regulate industry; it suffocated it. Want to expand production? Get a license. Import raw materials? Another license. Even hiring beyond a certain number required government approval.

In this environment, India's chemical industry was a study in contrasts. On one side stood the multinationals—companies like ICI, Hoechst, and Bayer—who had entered during the British era or soon after independence. They brought technology but kept it close, manufacturing in India but rarely transferring real know-how. On the other side were domestic players, often family-owned, technically competent but capital-starved, making basic chemicals with outdated technology.

The amines situation was particularly acute. These nitrogen-containing organic compounds might sound esoteric, but they're the unsung heroes of modern chemistry. Being nitrogenous compounds, amines play a vital role in biological systems and form the building blocks in pharmaceutical, agrochemical, veterinary and nutritional industries. Notably in healthcare, amines are indispensable in the production of API's. Similarly, amines are critical in the production of agrochemicals.

Think of amines as molecular Lego blocks—simple structures that combine to create complex pharmaceuticals, pesticides, and industrial chemicals. Without them, you can't make anything from antihistamines to herbicides, from rubber chemicals to water treatment compounds. Yet in 1979, India imported virtually every kilogram, paying precious foreign exchange to suppliers in Europe, America, and Japan who controlled both the technology and the pricing.

The numbers were staggering. India's pharmaceutical industry was growing rapidly, but each new drug formulation meant more amine imports. The Green Revolution had created massive demand for agrochemicals, but the key intermediates came from abroad. Every industrial expansion—textiles, rubber, paints—increased the import bill. The government's own planning commission identified amines as a critical gap in the chemical value chain, but identifying a problem and solving it were vastly different challenges.

Enter Yogesh Kothari in 1979. Unlike many entrepreneurs of his generation who came from trading families, Kothari was a technocrat through and through. Mr. Yogesh M. Kothari, Chairman and Managing Director, is a Chemical Engineer from Institute of Chemical Technology, (erstwhile UDCT) Mumbai. He is also Master of Management Science and Master of Science-Chemical Engineering, from the University of Massachusetts, Lowell, U.S.A. This combination—ICT's legendary chemical engineering program plus American exposure to both technology and management—would prove crucial.

Kothari saw what others missed: amines weren't just another chemical to be imported. They were a chokepoint in India's industrial development. Control amines, and you influence the entire downstream chemical industry. Master their production, and you transform from a price-taker to a price-maker. But seeing the opportunity was one thing; executing it in License Raj India was entirely another.

III. The Founder's Journey: Yogesh Kothari's Vision (1979–1990s)

The year 1979 wasn't chosen randomly. India was at an inflection point—Janata Party's brief interlude was ending, Indira Gandhi would return to power, and economic liberalization was still a distant dream. In this environment, starting a chemical company required not just capital and technology, but almost superhuman persistence in navigating bureaucracy.

Kothari's vision was deceptively simple: make India self-sufficient in aliphatic amines. But simplicity in vision often masks complexity in execution. He has been conferred the title of Distinguished Alumni from ICT university—an honor that speaks to what he would achieve, but in 1979, he was just another entrepreneur with an idea and a problem: how to get technology that no one wanted to share.

The technology challenge was fundamental. Making amines involves reacting alcohols with ammonia under specific conditions of temperature and pressure, using catalysts that determine yield and purity. Sounds straightforward? It's not. The devil lurks in the details—catalyst composition, reactor design, separation techniques, recycling systems. Global leaders had spent decades perfecting these processes. They weren't about to hand them over to a potential competitor.

After months of negotiations, Kothari secured a breakthrough: The first plant was commissioned in 1982 at Patalganga to make ethylamines with technology from Leonard Process Company, USA. Leonard Process wasn't BASF or Dow—it was a smaller American firm, but it had solid technology. More importantly, it was willing to transfer it to India.

The Patalganga location itself tells a story. Located about 75 kilometers from Mumbai, it was close enough to access talent and infrastructure but far enough to find affordable land. The area would later become one of India's major chemical clusters, but in 1982, Alkyl Amines was among the pioneers, setting up shop in what was largely rural Maharashtra.

The early years were brutal. Technology transfer on paper is one thing; making it work is another. American technicians would fly in, set up equipment, train operators, and leave. Then reality would hit—Indian raw materials had different specifications, the power supply was erratic, monsoons created humidity problems the Americans hadn't anticipated. Each problem required innovation, adaptation, what Indians call 'jugaad' but with chemical engineering rigor.

The first plant was commissioned in 1982 at Patalganga to make ethylamine and cyclohexylamines with technology from Leonard Process Company, USA. The choice of products was strategic. Ethylamines were workhorses—used in pesticides, pharmaceuticals, rubber chemicals. Cyclohexylamines had more specialized applications, including artificial sweeteners. Start with volume, add value—a pattern that would define Alkyl's approach for decades.

Market development was perhaps even harder than production. Indian customers were used to importing from established suppliers. Why risk purchasing from a new Indian company? Quality concerns were real—pharmaceutical companies couldn't afford contaminated intermediates. Kothari's team had to prove not just price competitiveness but quality parity, batch-to-batch consistency, and supply reliability.

The solution was almost counterintuitive: start with the most demanding customers. If you could satisfy a multinational pharmaceutical company's specifications, others would follow. Early clients were skeptical, sending teams to audit facilities, demanding extensive documentation, running pilot batches. But each successful delivery built credibility. Each satisfied customer became a reference.

By the late 1980s, patterns were emerging. Subsequently, the capacity at the site was expanded to manufacture other amines with technical know-how of Acid Amines Technologies ,USA, and now hosts 2 multipurpose amines plants with a capacity exceeding 25000 MT/annum. The company wasn't just surviving; it was expanding. But expansion brought new challenges. More products meant more complexity. Larger scale meant bigger working capital requirements. And looming on the horizon was a change that would transform everything: economic liberalization.

IV. Product Evolution & Technology Development (1990s–2000s)

The 1990s began with a bang that reverberated through every Indian boardroom—economic liberalization. For Alkyl Amines, liberalization was both opportunity and threat. Suddenly, foreign companies could enter India more easily, import duties would fall, and the protective walls that sheltered domestic industry would crumble. Survive this, and you could thrive. Fail, and you'd become a footnote.

Kothari's response was to double down on technology and integration. The company had mastered basic amines, but that wasn't enough. The real value—and defensibility—lay in derivatives and specialty chemicals. It has two manufacturing sites with 9 production plants and related utilities at Patalganga and Kurkumbh in Maharashtra. The Kurkumbh facility, established in 1995, wasn't just an expansion; it was a statement of intent.

The company has an R&D centre at Hadapsar, Pune. This wasn't window dressing. While competitors relied on licensed technology, Alkyl began developing its own processes. The R&D center became a crucible for innovation, taking molecules from gram-scale to commercial production. Over the last decade, the company had added various new product processes which were developed in the R&D to expand its product range through inhouse technology.

The shift from licensed to proprietary technology is worth examining. When you license technology, you're always one step behind. The licensor has moved on to next-generation processes while you're implementing their last-generation tech. Developing your own technology is harder, riskier, and requires patient capital. But succeed, and you control your destiny.

Take acetonitrile, a solvent crucial for pharmaceutical HPLC analysis and DNA synthesis. Global production was dominated by a handful of players who made it as a byproduct of acrylonitrile manufacture. Alkyl developed a synthetic route—deliberate production rather than byproduct recovery. According to the management, acetonitrile is one such complex product with only three global players and was developed in-house. This wasn't just technical achievement; it was strategic positioning.

The 2000s brought new challenges and opportunities. China had emerged as the chemical factory of the world, flooding markets with low-cost products. But Alkyl had learned something crucial: in specialty chemicals, the race to the bottom is a race to bankruptcy. Instead of competing on price in commodities, focus on products where technology, quality, and reliability matter more than the last percentage point of cost.

Backward integration became the next frontier. Why buy raw materials when you could make them? Each step backward in the value chain meant better margins, more control, less dependence on suppliers. But it also meant more capital investment, more complexity. The decision to backward integrate wasn't taken lightly—it required careful analysis of make-versus-buy economics, technology availability, and market dynamics.

Alkyl Amines Chemicals Ltd. (AACL) is a global supplier of aliphatic amines, specialty amines and amine derivatives to the pharmaceutical, agrochemical, water treatment, rubber chemical and a variety of industries. We work closely with our customers to develop products for their requirements and cater to their specific needs on quality, specifications and supply chain. Our focus on technology, scale of manufacturing as well as our ethical approach to business sets us apart as the partner of choice for amine chemistry.

By 2010, the company had transformed from an import substituter to a global supplier. The product portfolio had expanded from basic amines to complex derivatives. The technology base had shifted from licensed to largely proprietary. But perhaps most importantly, the company had survived—and thrived through—India's economic opening, the Asian financial crisis, the dot-com bust, and the 2008 global financial crisis. Each crisis had been a test, and each test had made the company stronger.

V. The Scale-Up Story: Domestic Champion to Global Player (2000s–2010s)

The new millennium brought a different Alkyl Amines to the fore—confident, ambitious, and increasingly global in outlook. The domestic market had been conquered; import substitution was yesterday's battle. The new frontier lay beyond India's borders, in markets where "Made in India" still carried skepticism in specialty chemicals.

The export journey began modestly. At present, the company generates 85-90 per cent revenue from the domestic market—but that remaining 10-15% represented a crucial strategic shift. These weren't distress sales or surplus disposal; they were deliberate market entries, each requiring months of customer qualification, regulatory compliance, and trust-building.

It exports its products to approximately 10 countries, including Philippines, United States of America, Israel, Norway, Spain, United Kingdom, Switzerland, Belgium, Malaysia, and Middle East countries. Notice the diversity—not just developing markets where price might be paramount, but sophisticated markets like Switzerland and Norway where quality and reliability are non-negotiable.

The global financial crisis of 2008 proved to be an unexpected accelerator. As Western companies struggled with the downturn, they looked for cost optimization without quality compromise. Alkyl Amines, with its proven track record and competitive pricing, suddenly looked very attractive. Crisis became opportunity, but only because the groundwork had been laid over decades.

China's role in this period deserves special attention. By 2010, China dominated global chemical production, but cracks were appearing. Environmental regulations were tightening. The era of build-at-any-cost was ending. Customers who had shifted sourcing to China for cost were discovering hidden expenses—quality variability, supply disruptions, environmental concerns. Alkyl positioned itself as the reliable alternative, the "anti-China" in specialty amines.

The specialty chemicals pivot accelerated during this period. The third segment is specialty chemicals which contribute more than 25% to the revenue. Coming to the major product which Alkyl Amines focuses on is Acetonitrile. These weren't commodity products where price ruled supreme. They were complex molecules requiring sophisticated chemistry, where a few players globally could meet specifications.

It supplies amines and amine-based chemicals to the pharmaceutical, agrochemical, rubber, chemical, and water treatment industries. Each industry had different requirements, different regulatory frameworks, different competitive dynamics. Pharmaceutical customers cared about impurity profiles and regulatory documentation. Agrochemical companies focused on consistency and cost. Water treatment firms needed reliability above all. Managing this complexity required organizational capabilities far beyond simple manufacturing.

The financial performance during this period validated the strategy. The net profit of the company grew at a CAGR of nearly 40 per cent to Rs 295.34 crore in FY21 against Rs 10.37 crore in FY11. On the other hand, gross sales increased at a CAGR of 18.28 per cent to Rs 1,242.44 crore during the same period. These aren't just good numbers; they're exceptional for a chemical company, especially one that remained largely debt-free through this growth.

But it was the stock market that really took notice. The stock rallied 19,844 per cent to Rs 3,061.45 on February 15, 2022 from Rs 15.35 on February 15, 2011. On the other hand, the benchmark BSE Sensex gained 215 per cent to the 58,142-mark in the past 10 years. This wasn't irrational exuberance; it was recognition of a fundamental transformation—from domestic player to global force, from commodity to specialty, from follower to leader.

VI. Family Business & Second Generation (2000s–Present)

Every family business faces its moment of truth when the second generation enters. Will they be pale shadows of the founder, coast on inherited success, or bring fresh energy and perspectives? For Alkyl Amines, this transition began in 2001 when Suneet Kothari joined the company, and it's a masterclass in how to modernize while maintaining core values.

Mr. Suneet Y. Kothari, Executive Director, is a Chemical Engineer and Chemistry / Biochemistry Graduate from Cornell University, U.S.A. He has earned a MBA degree from INSEAD, France / Singapore. He was a management consultant with Diamond Technology Partners, U.S.A., after graduation. He has been with the Company since 2001.

The credentials matter less than what they represent. Cornell for technical depth—you can't lead a chemical company without understanding the chemistry. INSEAD for global business perspective—specialty chemicals is a global game. Diamond Technology Partners for analytical rigor—consulting teaches you to question everything, structure problems, and drive implementation. This wasn't nepotism; it was succession planning done right.

Suneet's entry coincided with a crucial period. The company had proven it could manufacture and compete. The question was: could it professionalize and scale? Family businesses often struggle here—informal processes that worked at smaller scale break down as complexity increases. The founder's intuitive decision-making, valuable in early stages, can become a bottleneck in larger organizations.

The professionalization wasn't dramatic—no McKinsey consultants parachuting in with transformation blueprints. Instead, it was gradual, systematic. SAP implementation for real-time visibility across operations. Formal performance management systems replacing informal assessments. Structured innovation processes supplementing entrepreneurial inspiration. The family touch remained, but it was augmented with professional discipline.

Promoter Holding: 72.0%. This number is crucial. The Kotharis maintained control—enough to drive long-term strategy without quarterly earnings pressure, but they also left room for institutional investors who brought not just capital but governance expectations. It's a delicate balance many family businesses fumble.

The generational transition also brought fresh perspectives on capital allocation. The elder Kothari's generation, scarred by the challenges of raising capital in closed-economy India, preferred to remain debt-free. The younger generation understood that in a globalized world, prudent leverage could accelerate growth. The company remained conservative—Company is almost debt free—but the conversation shifted from "no debt" to "optimal capital structure."

Cultural transformation accompanied organizational change. The paternalistic approach common in traditional Indian companies evolved into something more contemporary. Meritocracy gained prominence without abandoning loyalty. Performance metrics became explicit without losing the family feeling. International talent was welcomed without diluting the Indian core.

The R&D transformation under the second generation deserves special mention. All our products are developed by our dedicated research scientists and engineers at our technology center at Hadapsar, Pune, who interact with our customers to identify molecules of interest to scale up from gram to commercial. This customer-centric innovation wasn't just about responding to requests; it was about anticipating needs, co-creating solutions, becoming indispensable to customers' own innovation efforts.

What's remarkable is what didn't change. The focus on amines remained unwavering—no unrelated diversification into real estate or retail like many successful Indian companies. The commitment to manufacturing excellence persisted—no shift to trading or asset-light models. The ethical approach to business continued—no shortcuts, no compromises. The second generation brought evolution, not revolution.

VII. Financial Performance & Market Recognition (2010s–2020s)

Numbers tell stories, but in Alkyl Amines' case, they practically shout. The transformation from 2011 to 2021 reads like fiction, except auditors have verified every digit. The net profit of the company grew at a CAGR of nearly 40 per cent to Rs 295.34 crore in FY21 against Rs 10.37 crore in FY11. On the other hand, gross sales increased at a CAGR of 18.28 per cent to Rs 1,242.44 crore during the same period.

Let's pause here. A 40% profit CAGR over a decade in a chemical company? This isn't software with zero marginal costs. This is manufacturing—with raw materials, energy costs, environmental compliance, working capital cycles. Achieving this while remaining debt-free borders on alchemy, except the philosopher's stone here was operational excellence and product mix optimization.

The stock market response was even more dramatic. The stock rallied 19,844 per cent to Rs 3,061.45 on February 15, 2022 from Rs 15.35 on February 15, 2011. On the other hand, the benchmark BSE Sensex gained 215 per cent to the 58,142-mark in the past 10 years. A 200-fold increase while the index merely tripled. This wasn't momentum trading or meme stock mania—institutional investors were accumulating, understanding something the market initially missed.

Market Cap: 10,614 Crore as of recent data, placing it firmly in mid-cap territory but with large-cap ambitions. The valuation reflects not just current performance but future potential—the optionality embedded in their product portfolio, the operating leverage in their business model, the strategic value of their market positions.

The debt-free status deserves deeper analysis. Company is almost debt free. Company has been maintaining a healthy dividend payout of 28.1%. In capital-intensive chemicals, this is unusual. Competitors leverage balance sheets to accelerate growth. Alkyl chose a different path—fund growth through internal accruals, maintain financial flexibility, sleep well at night.

Is this financial conservatism optimal? Modern finance theory would say no—some leverage optimizes weighted average cost of capital. But theory assumes perfect markets, rational actors, predictable cash flows. Chemical markets are cyclical, raw material prices volatile, demand patterns can shift suddenly. In this context, financial strength becomes competitive advantage. When credit markets freeze, as in 2008, or when pandemic strikes, as in 2020, the debt-free company doesn't just survive—it can acquire distressed assets, gain market share, invest countercyclically.

The dividend policy reveals management philosophy. A 28% payout ratio balances shareholder returns with growth funding. It signals confidence—we generate enough cash to both reward shareholders and fund expansion. It also maintains discipline—can't waste money on vanity projects when you have dividend commitments.

Recent performance shows some moderation. The company has delivered a poor sales growth of 9.62% over past five years. This isn't necessarily negative. After explosive growth, consolidation is natural and perhaps necessary. It could reflect deliberate choices—focusing on margins over volumes, upgrading product mix over expanding tonnage, building capabilities over chasing revenues.

The latest quarterly results provide real-time validation. Net profit of Alkyl Amines Chemicals rose 74.23% to Rs 47.46 crore in the quarter ended September 2024 as against Rs 27.24 crore during the previous quarter ended September 2023. Sales rose 17.82% to Rs 414.89 crore in the quarter ended September 2024. The margin expansion—profits growing faster than sales—suggests pricing power, operational efficiency, or favorable product mix shifts.

Market recognition extends beyond stock price. Institutional ownership patterns, analyst coverage, inclusion in indices—all signal arrival in the big leagues. But perhaps the ultimate validation comes from customers. When global pharmaceutical companies depend on you for critical intermediates, when your supply disruption can halt their production, you've transcended vendor status to become a strategic partner.

VIII. Competitive Dynamics & Global Position

The global amines market is a fascinating study in industrial organization—part oligopoly, part fierce competition, with dynamics that vary dramatically by product and geography. Companies like Huntsman Corporation, BASF SE, Dow Chemicals, and AkzoNobel specialize in producing a wide range of amines such as ethanolamines, alkylamines, and specialty amines. These are the giants—century-old companies with integrated complexes, global reach, and R&D budgets exceeding Alkyl's entire revenue.

Yet David doesn't always lose to Goliath, especially when David picks his battles carefully. BASF SE, The Dow Chemical Company, Arkema, Huntsman Corporation, and Solvay S.A., among others, are the key manufacturers operating in the product market. These companies dominate ethanolamines and other large-volume amines where scale economies matter most. Alkyl deliberately chose different terrain—specialty aliphatic amines where technology and customer relationships matter more than sheer scale.

The domestic competitive landscape tells another story. Between the two, Alkyl Amines has a larger market cap of Rs 121.6 billion (bn), as against Balaji Amines, which has a market cap of Rs 81 bn. It is one of the largest manufacturers of aliphatic amines in India. The company is the largest manufacturer of aliphatic amines and their derivatives in India and the sole producer of a few specialty chemicals—referring to competitor Balaji Amines.

The India market structure is particularly interesting. Alkyl Amines and Balaji Amines are the only two companies that now account for >90% market share of aliphatic amines and amine-based derivatives in India. This duopoly didn't emerge by accident. The capital intensity, technical complexity, and long customer qualification periods create formidable entry barriers. Rashtriya Chemicals & Fertilizers, the third-largest player, is commanding only a single-digit market share.

China's role cannot be ignored. For two decades, Chinese producers devastated chemical markets globally with ultra-low pricing backed by state support, lax environmental standards, and massive scale. But the tide turned around 2015. The Chinese clampdown on polluting industries and shutting down of many smaller units have created demand supply mismatch. Suddenly, customers who had switched to Chinese suppliers for cost savings found themselves scrambling for alternatives as plants shut down overnight for environmental violations.

This created what investors call the "China Plus One" opportunity, but executing on it required capabilities Chinese competitors had eroded—consistent quality, reliable supply, environmental compliance, documentation standards. Alkyl had maintained these capabilities through the lean years when customers chased the last penny of savings. When the pendulum swung back, they were ready.

The Amines market was valued at USD 19,578.15 Million in 2022 and is expected to reach USD 26,794.05 Million by 2030, growing at a CAGR of 4% (2023-2030). In this context, Alkyl's growth trajectory looks even more impressive—significantly outpacing market growth through share gains and mix improvement.

The competitive moat deserves careful analysis. It's not one thing but a combination: technical expertise accumulated over decades, customer relationships spanning product development cycles, regulatory approvals that take years to obtain, and manufacturing flexibility that allows customization without sacrificing efficiency. The business is capital intensive in nature and takes long lead times in obtaining government environmental clearances. Customer product approvals also present formidable challenges for new entrants. Due to this, potential entrants have a disadvantage in comparison to established incumbents such as Alkyl Amines and Balaji Amines, who have been able to scale up and build strong customer relationships over the years.

The specialty chemicals positioning is crucial. In commodities, the lowest-cost producer wins. In specialties, value creation trumps cost minimization. When your product represents 0.1% of customer's cost but can shut down their production if unavailable or off-specification, price becomes secondary to reliability. This is where Alkyl plays—not in the brutal commodity trenches but in the profitable specialty niches.

IX. Challenges & Strategic Pivots

Every chemical company CEO loses sleep over raw material prices, and Alkyl is no exception. acetic acid, methanol, coal and ammonia were some of the raw materials that witnessed a substantial rise in prices. These aren't minor input costs—they're the fundamental building blocks, and their prices can swing 50% or more in a year, driven by everything from Middle East tensions to Chinese factory shutdowns.

The challenge isn't just price volatility—it's the asymmetry in passing costs through. When raw material prices spike, customers resist immediate price increases, citing contracts, competitive alternatives, relationship history. When raw material prices fall, customers demand immediate price reductions, armed with spot quotes and competitive bids. Heads you lose, tails you don't win.

Alkyl's response has been sophisticated hedging—not financial derivatives but operational hedging. Multiple suppliers across geographies, strategic inventory management, formula-based pricing contracts where possible, and most importantly, moving up the value chain where raw materials form a smaller percentage of final product value. You can't eliminate commodity exposure in chemicals, but you can minimize its impact.

Environmental regulations present another challenge, though perhaps "opportunity" is more accurate. We are committed to provide Quality Products and Services to our customers, with demonstrated concern towards Environment, Energy, Occupational Health and Safety. As regulations tighten globally—and they will only get stricter—companies with proven compliance track records gain competitive advantage. Every competitor shut down for violations is market share waiting to be captured.

The China factor remains complex. While environmental shutdowns created opportunities, Chinese producers aren't standing still. They're consolidating, upgrading technology, building plants in industrial parks with proper treatment facilities. The easy wins from China's environmental crackdown are history; future competition will be more sophisticated.

COVID-19 provided an unexpected stress test. Supply chains built over decades shattered in weeks. Demand patterns went haywire—pharmaceutical intermediates spiked while industrial chemicals crashed. Labor availability became uncertain. Yet the company navigated through, validating the resilience of its business model while exposing areas needing strengthening.

The company has delivered a poor sales growth of 9.62% over past five years. This isn't just about market conditions. It reflects strategic choices—or perhaps strategic drift. After decades of rapid growth, finding the next growth engine becomes harder. Do you enter adjacent chemistries where you lack expertise? Expand geographically where you lack presence? Or double down on existing strengths?

The strategic pivots underway suggest management is grappling thoughtfully with these questions. Recent capacity additions focus on specialty products rather than commodities. R&D investments are increasing, targeting next-generation molecules rather than me-too products. Customer engagement is deepening, moving from supplier to development partner. These aren't dramatic pivots but subtle shifts that could compound into transformation over time.

Raw material volatility isn't going away—if anything, geopolitical tensions and energy transition will amplify it. But companies that survive long enough develop antibodies. They learn to flex production based on input costs, develop alternative synthesis routes, build pricing power through differentiation. Alkyl has been developing these antibodies for four decades.

X. Playbook: Business & Investing Lessons

If Alkyl Amines were a business school case study, what would be the key takeaways? First, the power of focus in an era celebrating diversification. While Indian conglomerates built sprawling empires across unrelated industries, Alkyl stuck to amines. Not chemicals broadly, not specialty chemicals generally, but amines specifically. This laser focus created expertise competitors couldn't match, customer relationships they couldn't replicate, and economics they couldn't achieve.

The technical excellence story deserves emphasis. In commoditized industries, operational excellence means running plants efficiently. In specialty chemicals, it means solving problems customers didn't know they had, developing molecules they couldn't imagine, achieving specifications they thought impossible. Over the last decade, the company had added various new product processes which were developed in the R&D to expand its product range through inhouse technology. This isn't just R&D spending; it's building organizational capability that compounds over time.

The import substitution to global leadership journey offers broader lessons for emerging market companies. Start by replacing imports—you know there's demand, pricing is visible, customers exist. Build capabilities serving domestic market where mistakes are less costly and feedback loops shorter. Then gradually expand internationally, but not everywhere at once—pick markets carefully, build references systematically, earn trust gradually.

The debt-free philosophy challenges conventional financial wisdom but makes sense in context. Chemical markets are cyclical—peak-to-trough EBITDA swings of 50% aren't unusual. Raw material prices are volatile. Customer industries have their own cycles. In this environment, financial flexibility isn't just valuable—it's survival. The company that doesn't need to refinance in a credit crunch can think long-term when competitors are fighting for survival.

Family businesses that successfully professionalize offer unique lessons. The temptation to milk cash cows for family benefit is real. The tendency to place loyalty over competence is natural. The resistance to external perspectives is understandable. Alkyl navigated these challenges by maintaining family control while embracing professional management, preserving culture while evolving capabilities, respecting history while preparing for the future.

Building B2B brands in commodity-like markets seems oxymoronic—aren't B2B decisions rational, based on specifications and price? Yes and no. Trust matters enormously when your product can shut down customer's operations. Reliability matters when supply chains are stretched. Technical support matters when problems arise. Alkyl built a brand not through advertising but through decades of consistent delivery.

Long-term thinking in cyclical industries requires courage. When markets boom, everyone expands capacity. When markets crash, everyone cuts costs. Playing contrarian—investing in downturns, being cautious in upturns—requires conviction and capital. The debt-free balance sheet provides the capital; four decades of experience provides the conviction.

The lesson for investors is about looking beyond obvious metrics. P/E ratios and growth rates matter, but competitive position matters more. In specialty chemicals, market share in specific molecules can be more valuable than overall industry presence. Customer concentration that looks risky might actually reflect irreplaceability. Family ownership that seems outdated might provide stability and long-term orientation that public companies lack.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The optimist's view starts with structural tailwinds. India's pharmaceutical industry is globalizing, requiring international-quality intermediates. The agrochemical sector is innovating, developing new molecules needing specialized amines. Environmental regulations worldwide are tightening, favoring compliant producers. Asia-Pacific is expected to dominate the amines market owing to the rapidly growing FMCG industry in emerging economies such as India and China. Furthermore, growing government intervention in providing safe drinking water in economies such as India, China and Indonesia will further boost the market growth.

The competitive position looks increasingly attractive. The company is a leading manufacturer and global supplier of aliphatic amines, amine derivatives, and specialty chemicals. It offers over 100 products and is a global leader in several products, including synthetic Acetonitrile, DMAHCL, Triethylamine, Diethylhydroxylamine, and is the sole global producer of many specialty amines. Being sole global producer of anything in chemicals is remarkable; being so in multiple products suggests deep technical moats.

Financial strength amplifies opportunity. The debt-free balance sheet means growth isn't constrained by leverage covenants. Company is almost debt free. Company has been maintaining a healthy dividend payout of 28.1%. This combination—growth potential plus financial flexibility—creates optionality. They can acquire distressed assets, invest countercyclically, or return cash to shareholders as opportunities dictate.

The China Plus One theme has legs. The China plus one strategy and 'Make in India' initiatives are pushing the growth of the specialty chemicals industry. This isn't just about China's environmental issues; it's about supply chain resilience, geopolitical hedging, and risk management. Companies that shifted everything to China for cost are reconsidering. Alkyl offers an alternative that's cost-competitive but also reliable, compliant, and strategically located.

Technical capabilities keep improving. The R&D center isn't just maintaining products but developing new molecules, new processes, new applications. Each successful development strengthens customer relationships, adds to the product portfolio, and creates new growth avenues. In specialty chemicals, R&D ROI can be extraordinary—one successful molecule can transform a company.

Bear Case:

The skeptic's case starts with growth deceleration. The company has delivered a poor sales growth of 9.62% over past five years. After decades of rapid growth, is the company hitting natural limits? In focused strategies, growth eventually becomes challenging—you dominate your niche, then what? Adjacent markets require different capabilities; geographic expansion faces entrenched competitors.

Raw material volatility remains a perpetual risk. acetic acid, methanol, coal and ammonia were some of the raw materials that witnessed a substantial rise in prices. These aren't minor fluctuations but major swings that can devastate margins. Formula-based pricing helps but doesn't eliminate risk. A sustained period of input cost inflation without ability to pass through could seriously impact profitability.

Competition from Chinese players isn't disappearing. Yes, environmental regulations have leveled the playing field somewhat, but Chinese companies are adapting—building compliant facilities, developing technology, expanding internationally. The easy gains from China's disruption are behind us; future competition will be more sophisticated and aggressive.

Customer concentration could be problematic. While serving demanding customers validates capabilities, dependence on a few large buyers creates vulnerability. Pharmaceutical companies are consolidating; agrochemical giants are merging. Negotiating power is shifting toward buyers. Loss of a major customer could significantly impact revenues.

Limited pricing power in commodity products remains challenging. Despite the specialty focus, parts of the portfolio remain commoditized where price is paramount. In these products, the lowest-cost producer wins, and there's always someone willing to cut prices to gain share. The mix shift to specialties helps but doesn't eliminate this dynamic.

Environmental and regulatory risks are escalating globally. What's compliant today might not be tomorrow. Regulations are tightening, not just in India but globally. The cost of compliance keeps rising. One major incident—environmental release, safety accident, quality failure—could damage reputation built over decades.

The valuation question looms. After spectacular returns, is the easy money made? The stock has run up dramatically, pricing in significant future growth. The stock rallied 19,844 per cent to Rs 3,061.45 on February 15, 2022 from Rs 15.35 on February 15, 2011. Such returns are unlikely to repeat. Future returns will likely track business performance more closely, which while solid, may not justify premium valuations.

XII. Epilogue & "If We Were CEOs"

Standing at the crossroads of 2025, if we were sitting in the CEO's chair at Alkyl Amines, where would we focus? The electric vehicle revolution presents both threat and opportunity. EVs don't need traditional automotive chemicals, but battery manufacturing requires specialized chemicals. The company's expertise in specialty amines could translate into battery electrolyte additives, cathode processing chemicals, or separator treatments. This isn't core today, but could it be tomorrow?

Geographic expansion deserves fresh thinking. It exports its products to approximately 10 countries, including Philippines, United States of America, Israel, Norway, Spain, United Kingdom, Switzerland, Belgium, Malaysia, and Middle East countries. Ten countries is a start, but the real opportunity might be in the next fifty. Not everywhere—that's spreading too thin—but strategic markets where local presence, technical support, and rapid response provide competitive advantage.

The M&A opportunity seems underexploited. With a debt-free balance sheet and proven integration capabilities, why not acquire? Not random diversification, but strategic additions—complementary technologies, customer access, geographic presence. The global chemical industry is consolidating; being an acquirer rather than acquired requires scale and ambition.

Sustainability and green chemistry aren't just buzzwords—they're the future. Customers increasingly demand not just product performance but process sustainability. Bio-based routes to traditional molecules, green solvents, atom-efficient processes—these aren't CSR initiatives but competitive necessities. The company that masters green chemistry doesn't just comply with regulations; it defines them.

Building the next generation of technical talent becomes crucial as competition for chemical engineers intensifies globally. The Pune R&D center is good, but is it world-class? Partnering with universities, funding research, creating an innovation culture that attracts the best minds—these soft investments might matter more than hard assets.

The debt-free philosophy might need revisiting—not abandoning conservatism but optimizing capital structure. In a world of negative real rates, some leverage might make sense. Not for financial engineering but for accelerating growth, funding innovation, acquiring capabilities. The key is maintaining flexibility while optimizing returns.

Digital transformation in chemicals is still early innings. Beyond ERP systems, imagine AI-optimized production, predictive maintenance, digital twins of plants, blockchain-verified supply chains. These aren't futuristic concepts but emerging realities. The chemical company that masters digits alongside molecules gains insurmountable advantage.

Looking back at Alkyl Amines' journey from a single plant in Patalganga to a global specialty chemical player, the achievement is remarkable. Looking forward, the opportunity might be even greater. The building blocks are in place—technical expertise, customer relationships, financial strength, proven management. The question isn't whether they can grow but how fast and in which directions.

The story of Alkyl Amines is ultimately about transformation—of a company, certainly, but also of Indian manufacturing, of family businesses, of specialty chemicals globally. It demonstrates that focused execution beats diversified experimentation, that technical excellence creates sustainable moats, that patient capital compounds into extraordinary returns.

For investors, the lesson is about looking beyond the obvious—finding companies building monopolies in niches, accumulating capabilities that compound, serving customers in ways that create switching costs. For entrepreneurs, it's about the power of focus, the value of technical depth, the importance of culture. For India, it's proof that global champions can emerge from the most unlikely circumstances.

As we close this deep dive into Alkyl Amines, perhaps the most important insight is this: in a world obsessed with disruption and transformation, sometimes the biggest opportunities lie in doing traditional things extraordinarily well, in solving old problems with new methods, in building slowly but surely rather than moving fast and breaking things. Amines might not be artificial intelligence or electric vehicles, but they're the invisible ingredients that make modern life possible. And sometimes, the best businesses are hiding in plain sight, creating value molecule by molecule, customer by customer, decade by decade.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube