Albert David Limited: The 86-Year-Old Pharma That Almost Disappeared

I. Introduction & Episode Roadmap

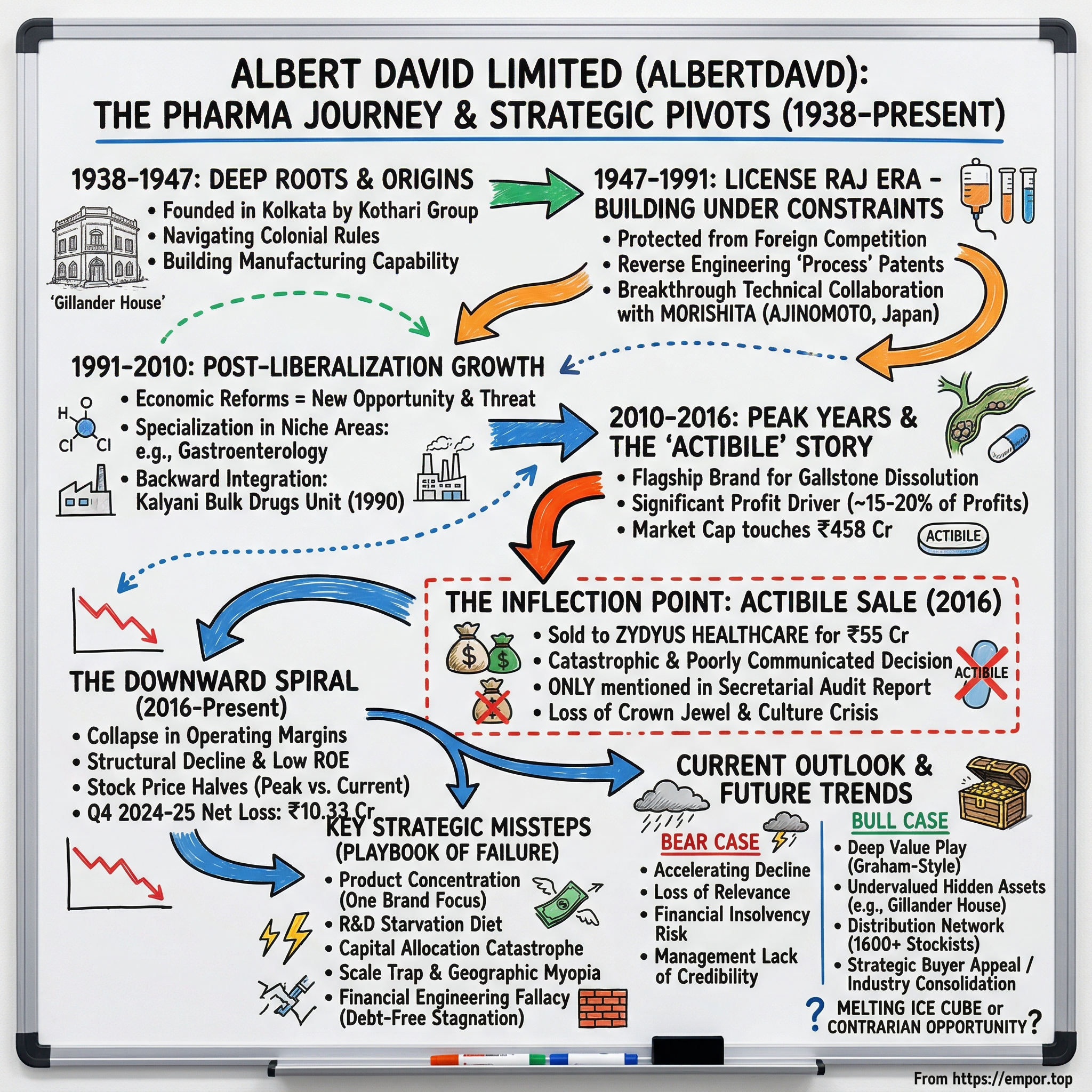

Picture this scene: In the narrow lanes of Kolkata's Netaji Subhas Road, inside the art-deco Gillander House, an 86-year-old pharmaceutical company fights for survival. Albert David Limited (ADL), incorporated in 1938 at Calcutta, belongs to a renowned industrial house of Kolkata, the Kothari Group. Once a proud pioneer of India's pharmaceutical independence, the company now battles negative profitability and a collapsing stock price that has shed nearly half its value in just twelve months.

How does a company that survived the trauma of partition, navigated the License Raj with aplomb, and built a reputation as a large IV fluid manufacturer, both in glass and polyethylene containers, find itself on the brink of irrelevance? The answer lies in a single, catastrophic decision made in March 2016—a decision so poorly communicated that the director's report, as well as the management discussion & analysis sections, were completely silent on this development, with the only mention in the FY2016 annual report appearing in the secretarial audit report.

This is not just another story of corporate decline. It's a cautionary tale about what happens when a heritage pharmaceutical company sells its crown jewels, fails to replace its innovation pipeline, and watches helplessly as nimbler competitors eat its lunch. From a market capitalization that once touched Rs 458 crore to a net profit that fell -180.02% year-over-year to negative ₹10.33 Cr in Q4 2024-2025, Albert David's journey reads like a Shakespearean tragedy set in the cutthroat world of Indian pharmaceuticals.

The questions we'll explore cut to the heart of corporate strategy: Why would management sell their most valuable asset without proper disclosure? How did a company with such deep roots in India's pharmaceutical heritage lose its way so completely? And perhaps most intriguingly—is there any path back from the abyss?

II. Pre-Independence Origins & Kothari Group Context

The year was 1938. While Europe teetered on the brink of World War II and India simmered under the final decade of British colonial rule, a group of Marwari businessmen in Calcutta made a bold bet on pharmaceuticals. Prior to independence, the role of indigenous firms was limited. In 1901, Acharya P. C. Ray set up the Bengal Chemicals and Pharmaceutical Works (BCPW); followed by Alembic Chemical Works (1907) and Bengal Immunity (1919). Over the next few decades, various small-scale and large-scale domestic production units were established like Indo Pharma, Unichem, Chem Pharma, Chemical Industries and Pharmaceutical Industries (CIPLA), Calcutta Chemicals, Zandu Pharmaceutical Works.

Into this nascent ecosystem stepped the Kothari Group, establishing Albert David Limited in the commercial heart of Calcutta. The timing was both audacious and prescient. At the time of independence in 1947, the value of the Indian pharmaceutical sector was around Rs. 10 Crore. The Indian pharma market was dominated by Western MNCs that controlled between 80 and 90 percent of the market primarily through importation.

The Kothari Group itself represented a particular breed of Indian entrepreneurship—the kind that emerged from the trading communities of Rajasthan to build industrial empires in Bengal. Founded by Chandula Mothilal Kothari in 1917, the group had already established itself in various sectors before venturing into pharmaceuticals. Their decision to enter this space wasn't merely opportunistic; it was strategic. They understood that healthcare would be fundamental to an independent India's development.

Operating from what would later become their iconic address—the four-storied commercial building known as "Gillander House" at Netaji Subhas Road, Kolkata - 700001—Albert David began its journey manufacturing basic pharmaceutical formulations. The British colonial administration's approach to healthcare had created a peculiar market dynamic. The British rule in India led to the introduction of allopathic medicine and the establishment of several medical colleges and institutions. The first pharmacy course was introduced in 1863 at Calcutta Medical College.

What made Albert David different from other indigenous attempts? The company didn't just aspire to copy Western formulations—it aimed to build comprehensive manufacturing capabilities. While competitors focused on simple preparations, Albert David invested in understanding complex pharmaceutical processes. This foundation would prove crucial when India gained independence and needed domestic capacity to serve its vast population.

The pre-independence pharmaceutical landscape was brutal for Indian companies. Patent laws favored British manufacturers, import duties were structured to benefit colonial interests, and access to technical knowledge was severely restricted. Yet Albert David persevered, learning by observation, hiring whatever local talent existed, and slowly building competencies that would bloom after 1947.

By the time midnight struck on August 15, 1947, and India awoke to freedom, Albert David had survived nine years of colonial pharmaceutical manufacturing—a feat that positioned it uniquely for the nation-building era that followed.

III. The License Raj Era: Building Under Constraints (1947–1991)

The newly independent India that Albert David woke up to in 1947 was a nation desperate for self-sufficiency. Prime Minister Nehru's vision of a socialist pattern of society meant pharmaceutical companies would operate under an intricate web of licenses, quotas, and price controls. For Albert David, this era would paradoxically become its golden foundation period.

The License Raj—that much-maligned system of permits and permissions—actually protected companies like Albert David from foreign competition. The Indian government ended India's recognition of Western-style "product" patent protection for pharmaceuticals, agricultural products, and atomic energy. Product-specific patents were disregarded in favor of manufacturing "process" patents that allowed Indian companies to reverse engineer or copy foreign patented drugs without paying a licensing fee.

By the 1970s, Albert David had evolved from a simple formulation unit to a diversified pharmaceutical manufacturer. The company's product portfolio expanded dramatically: manufacturing and trading of Pharmaceutical Formulations, Infusion Solutions, Herbal Dosage Forms and Bulk Drugs by way of domestic sale or export. Apart from these, it manufactures disposable syringes and needles and a wide range of bulk drugs.

The real breakthrough came through international collaboration. In a masterstroke of technology transfer, ADL entered into a technical collaboration with Morishita Pharmaceuticals, Japan, a subsidiary of Ajinomoto -- the world leader in amino acids -- to manufacture amino acid infusions. This wasn't just any partnership. Ajinomoto's expertise in amino acids represented cutting-edge biotechnology, and their willingness to collaborate with an Indian company signaled Albert David's growing technical credibility.

The amino acid story deserves special attention. Japan was the first country in the world to make a medical infusion containing high-quality amino acids. This was done in 1956, and was designed to address nutritional deficiencies before and after surgery. By securing this technology, Albert David positioned itself at the forefront of parenteral nutrition in India—a market that would explode as India's hospital infrastructure expanded.

The 1980s brought another dimension to Albert David's growth. The company recognized that IV fluids would become critical to India's healthcare infrastructure. Unlike tablets or capsules that could be manufactured by hundreds of small players, IV fluids required sophisticated manufacturing capabilities, stringent quality control, and significant capital investment. Albert David made that bet, emerging as one of India's prominent IV fluid manufacturers.

But the crown jewel of the License Raj era was the establishment of the Kalyani bulk drugs unit. A new unit in Kalyani, West Bengal, to manufacture bulk drugs, which went on stream in 1990. This backward integration move came just as India stood on the cusp of economic liberalization, positioning Albert David with both formulation and API capabilities.

The numbers tell a story of steady, if unspectacular, growth. While companies like Ranbaxy and Cipla were making headlines with their aggressive expansion, Albert David built quietly, focusing on complex products that required real manufacturing expertise rather than mere copying skills. The strategy seemed sound: build technical capabilities, establish manufacturing excellence, and wait for the market to recognize quality.

As 1991 approached and India prepared to open its economy, Albert David looked well-positioned. It had manufacturing capabilities across the pharmaceutical value chain, international technical partnerships, and a reputation for quality in critical care products. What could possibly go wrong?

IV. Post-Liberalization: Partnerships & Growth (1991–2010)

July 24, 1991. Finance Minister Manmohan Singh stood in Parliament and announced the dismantling of the License Raj. For Albert David, nestled in its Kolkata headquarters, this moment represented both tremendous opportunity and existential threat. The protective walls that had nurtured Indian pharmaceutical companies for four decades were coming down.

The company's initial response was textbook strategic positioning: double down on partnerships and technical excellence. While competitors rushed to set up marketing offices in Mumbai and Delhi, Albert David stayed true to its Kolkata roots, believing that manufacturing excellence would trump aggressive marketing. This decision—noble in intent—would later prove to be a critical miscalculation.

The partnership strategy, however, showed real vision. Building on the successful Morishita collaboration, Albert David expanded its international relationships. The company didn't just license products; it absorbed manufacturing technologies, particularly in specialized delivery systems. The focus remained on products that required genuine technical expertise—amino acid infusions, specialized IV fluids, and later, complex oral formulations.

The late 1990s brought an interesting pivot. Albert David began developing capabilities in niche therapeutic areas, particularly gastroenterology. This wasn't random. The company's leadership recognized that lifestyle diseases were emerging as India's next health crisis. Urban India was getting richer, eating differently, and developing medical conditions that rural India had never seen at scale. Gallstones, once considered a rich person's ailment, were becoming increasingly common.

It was during this period that Albert David began developing what would become its most valuable asset—though nobody knew it yet. The company's R&D team, modest by industry standards but competent in formulation development, began working on ursodeoxycholic acid (UDCA) formulations for gallstone dissolution. The product that emerged from this effort would be branded Actibile.

The 2000s saw Albert David attempting to straddle two worlds. On one hand, it maintained its traditional business of IV fluids and hospital products, competing on quality in institutional sales. On the other, it began building a presence in chronic therapy areas through its field force. ADL is a part of the Kolkata-based Kothari Group, a prominent drug house manufacturing Pharmaceutical Formulations, Infusion Solutions, Herbal Dosage Forms, Bulk Drugs. Company is in strategic liaison with academic institutes like the Indian Institute of Chemical Biology (CSIR) & Department of Biotechnology, Calcutta University for outsourcing research.

Yet, warning signs were already visible. The company's revenue growth lagged industry averages. While the Indian pharmaceutical market grew at 15-20% annually through the 2000s, Albert David trudged along at single digits. The competitive landscape was changing dramatically. Sun Pharma was rolling up smaller companies through acquisitions. Dr. Reddy's and Ranbaxy were making waves in the US generic market. Cipla was becoming a global name through its AIDS drugs activism.

Albert David's response? Stay the course. Management believed in their strategy of technical excellence and niche focus. They pointed to their debt-free balance sheet as proof of prudent management. They highlighted their consistent, if modest, profitability. In a market increasingly driven by hype and financial engineering, Albert David prided itself on being boring but reliable.

The 2008 financial crisis provided an unexpected validation. While leveraged competitors struggled with debt servicing, Albert David's conservative approach allowed it to weather the storm without drama. Management felt vindicated. The tortoise, they believed, would eventually overtake the hares.

But in pharmaceuticals, as in evolution, it's not the strongest or the fastest who survive—it's the most adaptable. And Albert David's definition of adaptation was about to be severely tested. The company had built impressive capabilities, established valuable partnerships, and created some genuinely good products. What it hadn't built was the scale and marketing muscle needed to compete in modern Indian pharma.

As the decade closed, Albert David remained profitable, debt-free, and technically competent. It also remained stubbornly sub-scale, increasingly invisible to both investors and doctors, and dangerously dependent on a handful of products. The stage was set for both its greatest triumph and most catastrophic mistake.

V. Peak Years & The Actibile Story (2010–2016)

Sometimes a single product can define a company's destiny. For Pfizer, it was Viagra. For Ranbaxy, it was Ciprofloxacin. For Albert David, that product was Actibile—a drug that would lift the company to its modern zenith before becoming the instrument of its downfall.

Actibile wasn't just another me-too product in Albert David's portfolio. It represented something far more significant: the company's ability to identify and dominate a niche therapeutic area. Ursodeoxycholic acid (UDCA), the active ingredient, had been known since the early 1900s, originally extracted from bear bile. But Albert David's formulation and positioning of Actibile for the Indian market showed genuine pharmaceutical marketing acumen.

The brilliance lay not in the molecule but in the market understanding. As India's middle class expanded and dietary habits westernized, gallbladder stones emerged as an epidemic hiding in plain sight. Traditional treatment meant surgery—expensive, scary, and requiring significant recovery time. Actibile offered a medical alternative: dissolve the stones with a pill. For middle-class Indians terrified of going under the knife, this was revolutionary.

By 2012, Actibile had become Albert David's star performer. Albert David Ltd sold the brand Actibile in FY2016 for ₹55 cr. to Zydus Healthcare in March 2016—a valuation that speaks to the brand's value. Working backwards from typical pharma valuations of 2-3x annual sales, Actibile was likely generating Rs 18-25 crore in annual revenues, or roughly 5-7% of Albert David's total sales, with significantly higher contribution to profits given the premium pricing power in this niche.

The Actibile success had a transformative effect on Albert David's market perception. The stock market, always hungry for growth stories, began paying attention. The company's market capitalization climbed steadily, reaching Rs 458 crore—not spectacular by pharma standards, but respectable for a traditional Kolkata-based manufacturer.

Inside Gillander House, confidence was high. Management presentations began featuring Actibile prominently. The sales force, long used to pushing commodity products like IV fluids, suddenly had a genuine brand to detail to doctors. Gastroenterologists knew Albert David not as another generic company, but as the Actibile company.

The product's success also validated Albert David's strategy of focusing on niche therapeutic areas rather than competing in crowded markets like antibiotics or pain management. Plans were drawn up to build a broader gastroenterology franchise. The company began evaluating in-licensing opportunities for complementary products. There was talk of establishing a dedicated gastro sales division.

Yet beneath this success lay a fundamental weakness. Actibile's very success highlighted Albert David's broader failures. If the company could build such a successful brand, why was it only one? Where was the next Actibile? The product pipeline, never robust to begin with, showed no obvious successors. R&D spending remained minimal—a fraction of what competitors invested.

The market dynamics were also shifting. Larger companies had noticed the lucrative gallstone dissolution market. Zydus, Sun, and others were launching their own UDCA brands with aggressive pricing and promotion. Albert David's first-mover advantage was eroding. The company faced a classic innovator's dilemma: invest heavily to defend Actibile's position or diversify resources to build new brands.

Financial performance during this period reflected this underlying tension. During FY2009-15, the operating profit margin (OPM) of Albert David Ltd was consistent within the range of 10-13%. However, in recent years, the OPM declined sharply from 12% in FY2015 to 6% in FY2018. While Actibile drove top-line growth, overall margins were under pressure from competition in commodity products and rising marketing costs.

The Kothari Group's approach to Albert David during these peak years deserves scrutiny. Unlike activist promoters who might have pushed for aggressive expansion or strategic sales, the Kotharis maintained their traditionally conservative stance. No major capital raises were attempted. No transformative acquisitions were pursued. The company remained debt-free, but also ambition-free.

By late 2015, storm clouds were gathering. Demonetization was about to hit India's cash-dependent pharmaceutical distribution system. GST implementation loomed on the horizon, threatening to disrupt traditional supply chains. Competition in the UDCA market was intensifying. Albert David needed to make bold moves to protect its franchise and fund future growth.

Instead, it made the decision that would define its next decade—for all the wrong reasons. The approach from Zydus Healthcare for Actibile must have seemed like manna from heaven: Rs 55 crores for a single brand. Cash upfront. Clean exit. In the boardroom at Gillander House, it probably looked like brilliant financial engineering. In reality, it was corporate seppuku in slow motion.

VI. The Inflection Point: Actibile Sale to Zydus (2016)

March 28, 2016. A Monday that would live in infamy in Albert David's corporate history, though you'd never know it from reading the company's official communications. On this day, Cadila Healthcare's wholly owned subsidiary Zydus Healthcare Limited entered into a definitive agreement to acquire 'Actibile' from Albert David Limited. The brand falls in the gastroenterology segment and is used for dissolving gall bladder stones.

The deal structure itself was revealing: Rs. 55.00 crores for territories including (i) the Union of India; (ii) Nepal, (iii) South America (excluding Peru and Colombia), (iv) The United States of America; (v) Japan, (vi) South Africa; (vii) the European Union; and (viii) East Europe. This wasn't just selling a brand in India—it was surrendering global rights to what could have been Albert David's international expansion vehicle.

But the real scandal wasn't the sale itself—it was the silence that followed. In an act of corporate communication malfeasance that defies explanation, management discussion & analysis sections were completely silent on this development. Any investor would expect that she would get the message about such important development in the director's report or the management discussion & analysis.

The only official mention came buried in the secretarial audit report, like a confession hidden in footnotes: "We further report that during the period under audit, the Company has sold its brand 'Actibile' to M/s. Zydus Healthcare Limited, Ahmedabad for a lump sum consideration of Rs.55 crores".

Even more bizarrely, the proceeds of Rs 41 crore on net proceeds from Actibile brand sale were shown in cash flow from operations rather than investing activities in fiscal 2016. This accounting treatment, while perhaps technically defensible, obscured the one-time nature of this windfall and painted a falsely rosy picture of operational cash generation.

Why would management sell its crown jewel? The immediate financial pressures weren't obvious—Albert David remained debt-free with reasonable cash reserves. Several theories emerge from analyzing the context:

The Defensive Theory: Facing intensifying competition in the UDCA market, management may have decided to "sell at the top" rather than invest heavily in defending market share. If they believed Actibile's best days were behind it, Rs 55 crores might have seemed like good value.

The Capital Allocation Theory: Perhaps management had identified other opportunities requiring capital—new product development, capacity expansion, or acquisitions. Selling Actibile would provide war chest for transformation. (Spoiler: No such transformation materialized.)

The Promoter Theory: The Kothari Group, with promoter holding increasing from 62.13% to 62.24%, may have needed liquidity for other group ventures or personal requirements. Selling Actibile provided cash without diluting stake.

The Incompetence Theory: Management simply didn't understand what they had. They saw Actibile as one product among many, not recognizing it as the cornerstone of Albert David's brand transformation.

Zydus's perspective was crystal clear. Pankaj R Patel, chairman and managing director of Zydus Group, said, "The gastrointestinal segment has been one of our core focus segments. This acquisition will strengthen our portfolio of brands and leverage our equity in this key segment". Zydus understood what Albert David's management apparently didn't: strong brands in niche therapeutic areas are incredibly valuable.

The immediate market reaction was muted, partly because of the communication failure. Many investors likely didn't even realize the sale had happened until months later. CRISIL had expected a decline in operating margin consequent to sale of high margin Actibile brand, however the decline was higher.

Inside Albert David, the Actibile sale created a cultural crisis. The sales force, proud of representing a branded product, suddenly found themselves back to pushing commodities. Gastroenterologists who had associated Albert David with innovation began forgetting the company existed. The R&D team, already under-resourced, lost whatever motivation remained to develop the next breakthrough product.

The financial impact was swift and brutal. While FY2016 numbers were cushioned by the one-time gain, the underlying operational deterioration was evident to anyone who looked closely. The company reported the commencement in the decline in OPM in FY2016, the year in which it sold Actibile to Zydus. However, the company sold Actibile in the month of March 2016, which is the last month of the financial year.

Looking back, the Actibile sale represents everything wrong with Albert David's management: short-term thinking, poor communication, and fundamental misunderstanding of value creation in pharmaceuticals. They sold their future for a one-time gain of Rs 55 crores—a Faustian bargain that would haunt them for years to come.

VII. The Downward Spiral (2016–Present)

The unraveling of Albert David post-Actibile has been both swift and brutal, a corporate catastrophe playing out in slow motion across quarterly results and steadily declining stock charts. What began as strategic misstep has morphed into existential crisis.

The numbers tell a story of accelerating decline. The company has delivered a poor sales growth of 1.52% over past five years. Company has a low return on equity of 12.5% over last 3 years. But these aggregate figures actually mask the severity of recent deterioration. Net loss of Albert David reported to Rs 10.33 crore in the quarter ended March 2025 as against net profit of Rs 12.91 crore during the previous quarter ended March 2024. Sales declined 15.91% to Rs 74.89 crore in the quarter ended March 2025 as against Rs 89.06 crore.

The full-year picture is even more damning: Net profit declined 77.19% to Rs 17.20 crore in the year ended March 2025 as against Rs 75.42 crore during the previous year ended March 2024. Sales declined 4.60% to Rs 345.77 crore in the year ended March 2025 as against Rs 362.46 crore.

What makes these numbers particularly alarming is their trajectory. This isn't a company facing temporary headwinds—it's one in structural decline. Operating margins have collapsed from the 10-13% range during the "good years" to negative territory. The Q3 2024-25 results were especially shocking: Net profit fell -150.16% since last year same period to ₹-9.39Cr. The company generated -151.96% fall in its net profits since last 3-months. Net profit margin fell -171.2% since last year same period to -12.68%.

Beyond the financials, Albert David faces a crisis of relevance. The company's product portfolio, never particularly innovative to begin with, now looks positively antiquated. IV fluids, basic injectables, and commodity oral solids—these are products any contract manufacturer can produce. Without Actibile, Albert David has no answer to the question: "Why should anyone buy from you?"

The market has rendered its verdict emphatically. The stock price has collapsed from its 52-week high of Rs 1,537 to current levels around Rs 800, destroying nearly half of shareholder value. Market capitalization has shrunk to Rs 459 crore—less than what the company might have been worth if it had kept and properly nurtured Actibile.

Management changes have added to the turmoil. In view of the resignation of T. S. Parmar from the post of Managing Director & CEO, the company appointed Umesh Kunte as Chief Executive Officer with effect from February 6, 2023. While Kunte brings experience—aged 54 years, a pharma industry veteran with over three decades of experience in domestic as well as international markets, having worked with Ajanta Pharma, Besins Healthcare, Merck, Piramal Healthcare, Ranbaxy, and USV Ltd—he faces an almost impossible task.

The external environment hasn't helped. Demonetization in late 2016 disrupted the cash-dependent pharmaceutical distribution network. GST implementation in 2017 created additional chaos. The company was hit by twin reforms of demonetization and introduction of GST. In addition, the company faced increasingly intense competition from the unorganized sector. The impact of competition is so severe that the company could not maintain the profitability.

But blaming external factors is too easy. Plenty of pharmaceutical companies navigated these same challenges successfully. The real problem is internal: a fundamental lack of competitive advantage. Without unique products, superior manufacturing, innovative marketing, or cost leadership, Albert David offers nothing that hundred other companies don't provide better or cheaper.

The company's attempts at stabilization have been feeble. The 2021 co-marketing agreement with Corona Remedies—The company has recently signed a co-marketing agreement with the Kolkata based company Albert David Ltd. in 2021—represents tactical maneuvering rather than strategic transformation. Co-marketing agreements are typically stop-gap measures, ways to utilize idle field force capacity without investing in innovation.

Employee morale, never quantified in annual reports but visible in field feedback, has cratered. The sales force, once 400-plus strong, has shrunk. Good performers have left for better opportunities. Those who remain often do so from lack of alternatives rather than commitment.

Even the one supposed strength—the debt-free balance sheet—has become a weakness. Company is almost debt free, but this reflects not financial prudence but lack of growth ambition. In an industry where successful companies leverage balance sheets to fund expansion, Albert David's zero-debt status signals stagnation, not strength.

The tragedy is that this decline was entirely preventable. Had management retained Actibile, invested the Rs 55 crores in developing follow-on products, and built on their gastroenterology franchise, Albert David might today be a thriving mid-sized pharma company. Instead, it's a cautionary tale—a zombie company walking dead through India's pharmaceutical landscape.

VIII. Strategic Partnerships & Survival Mode (2021–Present)

Desperation makes for strange bedfellows. As Albert David's financial performance cratered post-2020, management scrambled for lifelines—any partnership, any deal, any arrangement that might arrest the decline. What emerged was less a strategy than a series of tactical retreats, each one acknowledging the company's diminishing relevance.

The Corona Remedies co-marketing agreement of 2021 exemplified this approach. Corona, a rapidly growing Ahmedabad-based company, represented everything Albert David wasn't: aggressive, ambitious, and ascending. CORONA is the second fastest growing company, amongst the top 30 companies in IPM, in terms of domestic sales MAT DEC '24. CORONA registered a CAGR of 20%, displaying a growth of more than 2.25 times of IPM growth.

For Corona, the Albert David partnership provided access to established distribution in Eastern India and manufacturing capacity for certain products. For Albert David, it meant field force utilization and some revenue guarantee. But co-marketing agreements are essentially admissions of defeat—acknowledgments that you can't compete independently.

The arrangement's structure revealed Albert David's weakness. Rather than licensing products to Corona (which would imply valuable intellectual property), or acquiring products from them (which would require capital), Albert David essentially became a contract manufacturer and regional distributor. The company that once partnered with Japan's Ajinomoto as equals now served as a junior partner to a domestic player a third its age.

Under new CEO Umesh Kunte, attempts at revitalization followed predictable patterns. Cost-cutting initiatives targeted the easiest expenses—travel, marketing spending, R&D (what little remained). The field force was "rationalized," corporate speak for firing people. Manufacturing was "optimized," meaning capacity utilization declined as volumes shrunk.

The impact of competition is so severe that the company could not maintain the profitability of its syringe & needle manufacturing unit. Therefore, ultimately, it had to shut this unit down. This closure symbolized Albert David's retreat from manufacturing excellence to mere survival.

Kunte's background—experience in turnaround situations as well as growth acceleration, strategic and business management, leadership, finance with M&A—suggested potential for dramatic restructuring. But turnarounds require resources, and Albert David's cupboard was increasingly bare. The Actibile sale proceeds had long been consumed by operational losses. The debt-free balance sheet, once a strength, now simply meant no financial flexibility.

The promoter response during this crisis period has been telling. The Kothari Group increased their stake marginally—from 62.13% to 62.24%—enough to signal continued support but not enough to suggest real commitment. No capital infusion materialized. No strategic vision emerged from the promoters. The sense is of a family holding that has become more burden than asset, maintained from inertia rather than conviction.

Product development, the lifeblood of pharmaceutical companies, essentially ceased. The company's "pipeline" consisted of line extensions and me-too generics—the pharmaceutical equivalent of rearranging deck chairs on the Titanic. Without investment in R&D, without capability to in-license innovative products, and without capital for acquisitions, Albert David had no path to product-led recovery.

Marketing efforts became increasingly desperate. The company participated in medical conferences it couldn't afford, sponsored events that brought no return, and maintained a field force that doctors increasingly ignored. The Albert David brand, never strong to begin with, became synonymous with mediocrity in medical circles.

The financial results for fiscal 2024-25 confirmed the failure of these survival tactics. Quarterly losses mounted. Revenue declined not just from competition but from actual loss of customers. An annual revenue de-growth of -11% needs improvement, Pre-tax margin of 7% is okay, ROE of 4% is fair but needs improvement. These antiseptic assessments understated the severity—this wasn't underperformance but corporate death spiral.

Even the one remaining asset—manufacturing infrastructure—faced obsolescence. Pharmaceutical manufacturing requires constant investment in upgrading equipment, maintaining compliance, and meeting evolving regulatory standards. Albert David's facilities, once pride of the company, increasingly looked dated. The Kalyani bulk drug facility, commissioned with fanfare in 1990, now represented stranded asset rather than strategic advantage.

The partnership strategy, such as it was, reflected tactical desperation rather than strategic vision. Each quarter brought speculation about new tie-ups, potential investors, or strategic alternatives. None materialized into anything transformative. The company had become un-partnerable—too weak to attract serious players, too proud to accept subordinate role, too poor to invest in transformation.

By mid-2024, Albert David existed in a twilight zone—not quite dead but far from alive. The quarterly earnings calls, when they happened, became exercises in managing decline rather than building future. Analysts stopped covering the stock. Investors wrote off their holdings. Employees updated resumes. And in Gillander House, the lights stayed on, but nobody was really home.

IX. Playbook: What Went Wrong

Every corporate failure is unique in its details but familiar in its patterns. Albert David's descent from respected pharmaceutical manufacturer to penny stock cautionary tale offers a masterclass in strategic missteps. Let's dissect the playbook of failure.

The Product Concentration Curse: Albert David's fatal flaw was building a one-product success story without succession planning. Actibile represented roughly 5-7% of revenues but likely 15-20% of profits given its premium pricing. When companies become dependent on single products, selling them isn't strategic flexibility—it's corporate suicide. The playbook lesson: diversification isn't just about risk management; it's about survival.

The R&D Starvation Diet: In pharmaceuticals, R&D isn't expense—it's investment. Albert David treated it as cost to be minimized. While industry leaders invest 8-15% of revenues in R&D, Albert David spent fractions of that. Company is in strategic liaison with academic institutes like the Indian Institute of Chemical Biology (CSIR) & Department of Biotechnology, Calcutta University for outsourcing research—this sounds impressive until you realize "strategic liaison" meant occasional consultations, not serious collaboration. Without R&D, pharmaceutical companies are just contract manufacturers with marketing departments.

The Capital Allocation Catastrophe: The Actibile sale proceeds—Rs 55 crores—represented a once-in-a-generation opportunity for transformation. Management could have: acquired complementary brands, invested in biosimilar development, built a specialty pharmaceutical platform, or even returned cash to shareholders. Instead, the money disappeared into operational losses, consumed by the very inefficiencies it could have fixed. This is capital allocation malpractice of the highest order.

The Communication Breakdown: The silence around Actibile's sale wasn't just poor disclosure—it was symptomatic of management's disconnect from stakeholder reality. By burying the announcement in secretarial audit reports, management showed either breathtaking incompetence or deliberate obfuscation. Neither interpretation inspires confidence. In capital markets, communication isn't just about compliance; it's about credibility.

The Scale Trap: In modern pharmaceuticals, scale matters more than ever. Distribution costs are largely fixed. Regulatory compliance costs are rising. Marketing expenses require critical mass for impact. Albert David existed in the worst possible zone—too large to be nimble, too small to compete with giants. The company needed to either grow dramatically or find a niche where size didn't matter. It did neither.

The Geographic Myopia: Remaining anchored in Kolkata while India's pharmaceutical industry shifted to Hyderabad, Ahmedabad, and Mumbai wasn't just physical isolation—it was cultural isolation. Albert David missed the industry's evolution toward innovation, international markets, and institutional investment. Geography isn't destiny, but in pharmaceuticals, ecosystem matters.

The Promoter Paradox: The Kothari Group's approach embodied the worst of both worlds—neither fully committed nor willing to exit. Maintaining 62% stake prevented strategic investors but didn't translate into strategic vision. Family-owned businesses can thrive (see Sun Pharma) or exit gracefully (see Ranbaxy to Daiichi Sankyo). Albert David did neither, trapped in governance purgatory.

The Partnership Pretense: Technical collaborations with Morishita in the 1980s made sense when India needed technology transfer. But by 2010s, successful Indian companies were innovating independently or acquiring foreign companies. Albert David's late-stage partnership with Corona Remedies wasn't strategic alliance—it was outsourcing relevance.

The Financial Engineering Fallacy: Being debt-free became Albert David's defining characteristic, mentioned prominently in every investor presentation. But in an industry requiring constant investment, zero debt signals zero ambition. Financial prudence became excuse for operational mediocrity. The playbook lesson: balance sheet strength means nothing without business model strength.

The Competitive Blindness: While Albert David focused on maintaining margins in commodity products, the industry transformed around it. Biosimilars emerged. Digital marketing revolutionized doctor engagement. Specialty pharmaceuticals created new profit pools. Albert David missed every trend, fighting yesterday's war with outdated weapons.

The ultimate lesson from Albert David's playbook isn't about any single mistake—it's about compound failure. Each strategic error made the next one more likely, creating a vicious cycle of decline. The Actibile sale wasn't the cause of Albert David's problems; it was the symptom of deeper dysfunction. Companies don't fail because of one bad decision. They fail because of systematic inability to adapt, innovate, and execute.

For investors, the playbook offers clear warnings: beware companies with single-product dependencies, scrutinize capital allocation decisions, demand transparent communication, and recognize that in pharmaceuticals, standing still means falling behind. For managers, it's even simpler: in pharmaceuticals, you innovate or you die. Albert David chose death by a thousand cuts.

X. Bear vs. Bull Case & Future Outlook

Even dying companies trade on hope. As Albert David's stock bounces along multi-year lows, brave souls and deep-value hunters scan the wreckage for signs of life. Could this be the ultimate contrarian play, or is it simply a value trap heading toward inevitable delisting?

The Bear Case: Death Spiral Confirmed

The bearish argument writes itself with brutal clarity. Net profit declined 77.19% to Rs 17.20 crore in the year ended March 2025 as against Rs 75.42 crore during the previous year. Sales declined 4.60% to Rs 345.77 crore. This isn't cyclical downturn—it's structural collapse.

Revenue decline accelerates each quarter. When pharmaceutical markets grow at 10-12% annually, Albert David's shrinking top line means market share evaporation. Every lost customer becomes nearly impossible to win back. Doctors forget the company exists. Distributors allocate shelf space to growing brands. The death spiral becomes self-fulfilling.

Operational leverage works both ways. As revenues decline, fixed costs become crushing burden. Manufacturing facilities designed for Rs 500 crore revenue can't be profitable at Rs 300 crore. The Kalyani bulk drug facility becomes stranded asset, consuming maintenance capital while generating losses.

Competition intensifies rather than moderates. In commodity generics, new entrants appear constantly, driven by low entry barriers and overcapacity. In specialty products where Albert David might differentiate, the company lacks resources to compete. It's trapped in the worst segment with the weakest position.

Management credibility is shot. The Actibile debacle destroyed trust. Current leadership under Kunte hasn't articulated convincing turnaround strategy. The promoter group seems checked out, maintaining stake from inertia rather than conviction. Who would bet on this team engineering recovery?

The financials point toward insolvency. Current cash generation can't support operations indefinitely. While the company remains debt-free, that simply means slower death rather than quick bankruptcy. Eventually, accumulated losses will erode net worth, triggering regulatory issues and potential delisting.

The Bull Case: Deep Value with Hidden Assets

Yet contrarians might spot opportunity in maximum pessimism. Trading at Rs 800 against book value of Rs 1,200, the stock offers Benjamin Graham-style asset play. The market capitalization of Rs 459 crore might undervalue hidden assets.

The Gillander House property alone could be worth significant sum. Prime Kolkata commercial real estate in the heart of the business district doesn't appear at fair value on 1938-established company's books. The manufacturing facilities, while underutilized, represent replacement value far exceeding market cap.

The debt-free status provides flexibility. Unlike leveraged competitors facing bankruptcy, Albert David can survive extended downturn. Patient capital could wait for cycle to turn, competition to rationalize, or strategic buyer to emerge.

The distribution network, while weakened, still exists. Relationships with 1,600+ stockists and presence across Eastern India took decades to build. For right product portfolio, this infrastructure could be reactivated quickly. Corona Remedies partnership validates this distribution value.

Regulatory approvals and manufacturing licenses have option value. In increasingly regulated pharmaceutical industry, established players with clean compliance records become acquisition targets. Someone might pay premium for ready-made platform.

The promoter stake at 62.24% provides stability and potential catalyst. If Kothari Group decides to exit, strategic buyer would need to make open offer at premium. Alternatively, if promoters inject capital or merge Albert David with other group companies, value could be unlocked.

Industry consolidation is inevitable. India has 10,000+ pharmaceutical companies, clearly unsustainable. As industry matures, subscale players will be absorbed. Albert David's 86-year history, established brands (however weak), and manufacturing infrastructure might attract acquirer.

The Verdict: Melting Ice Cube

The bull case, while intellectually interesting, requires leap of faith unsupported by evidence. Asset value means nothing if business burns cash. Distribution networks atrophy without products to sell. Manufacturing facilities become liabilities without volumes.

More importantly, pharmaceutical industry doesn't reward patience—it punishes inaction. Every quarter Albert David delays transformation, competitors grow stronger. The melting ice cube metaphor fits perfectly: value evaporates daily, imperceptibly but inevitably.

The most likely scenario is continued gradual decline punctuated by occasional false dawns. Management will announce new partnerships that disappoint. Quarterly results will show "improvement" from low bases. The stock might rally 20-30% on short covering, then resume downtrend.

Eventually—perhaps in 2-3 years—something will force resolution. Accumulated losses might trigger net worth erosion. Key manufacturing licenses might be surrendered. The promoters might accept reality and seek buyer. Or perhaps Albert David simply fades away, another footnote in Indian pharmaceutical history.

For investors, the lesson is clear: cheap stocks can get cheaper, especially in industries requiring constant innovation. Albert David isn't contrarian opportunity—it's value trap with 86-year pedigree. The company that helped build India's pharmaceutical independence now serves as cautionary tale about what happens when you stop evolving.

The market has spoken: at Rs 459 crore market cap for Rs 350 crore revenue company generating losses, even pessimists might be too optimistic.

XI. Epilogue: Lessons & Reflections

Every business failure is a teaching moment wrapped in tragedy. As we close the book on Albert David's long descent from pharmaceutical pioneer to penny stock, what lessons emerge from the wreckage?

The Danger of Selling Crown Jewels: The Actibile sale will be studied in business schools as textbook value destruction. When companies sell their best assets, they rarely invest proceeds wisely. Management always believes they can replace what they're selling, but execution rarely matches intention. The lesson is stark: in distress, companies instinctively sell what others want to buy—precisely what they should keep.

Why Some Thrived While Others Withered: India's post-liberalization pharmaceutical landscape created dramatic winners and losers. Sun Pharma grew from nothing to global giant through acquisitions. Cipla became worldwide name through AIDS activism and respiratory franchise. Dr. Reddy's pioneered reverse engineering and paragraph IV challenges. What did they have that Albert David lacked? Vision, ambition, and willingness to take calculated risks. Albert David confused conservatism with prudence, stability with stagnation.

The Scale Imperative: Modern pharmaceuticals is a scale game. R&D costs are rising. Regulatory requirements are increasing. Marketing expenses require critical mass. Companies must either achieve scale or find niches where scale doesn't matter. Albert David did neither, trapped in no-man's land between small specialists and large generics players. The middle ground, comfortable in License Raj era, became killing field in competitive markets.

Management Transparency Matters: The Actibile sale disclosure failure wasn't administrative oversight—it was character revelation. Management that hides bad news, buries material information, and avoids hard conversations can't be trusted with capital. In modern markets, communication is strategy. Companies that can't explain their actions coherently probably don't understand them either.

Heritage Is Not Strategy: Albert David's 86-year history, frequently mentioned in company documents, became burden rather than asset. Heritage creates entitlement mentality, resistance to change, and false sense of permanence. In pharmaceuticals, what matters isn't how long you've existed but how well you innovate. Kodak was 131 years old when digital photography killed it. Age is not advantage.

The Family Business Paradox: Indian pharmaceutical's greatest successes (Sun, Cipla, Lupin) and failures (Ranbaxy, Albert David) were family-controlled. The difference? Successful families professionalized management, invested in innovation, and weren't afraid to dilute stakes for growth. Failed ones treated companies as personal property, avoided hard decisions, and confused longevity with success.

Can Heritage Companies Reinvent?: The honest answer is rarely. Organizational antibodies resist change. Culture calcifies around past success. Leadership lacks urgency until crisis becomes terminal. Albert David had multiple opportunities for reinvention—post-liberalization, during Actibile's success, after the sale. Each time, inertia won.

Yet occasionally, heritage companies do transform. IBM shifted from hardware to services. Microsoft embraced cloud after missing mobile. But these transformations required brutal honesty, massive investment, and leadership willing to destroy old business models. Albert David demonstrated none of these qualities.

The Broader Message: Albert David's story resonates beyond pharmaceuticals. In every industry, former champions struggle with disruption. Success creates complacency. Complacency breeds decline. Decline accelerates into irrelevance. The cycle is predictable yet seemingly unavoidable.

For investors, Albert David offers cautionary tale about value traps, the importance of management quality, and dangers of averaging down on declining businesses. Cheap can always get cheaper when business model is broken.

For managers, the lessons are existential. In dynamic industries, standing still means falling behind. Past success guarantees nothing. Every strategic decision compounds—good ones create opportunities, bad ones close doors. And when you're lucky enough to build something valuable like Actibile, for heaven's sake, don't sell it for quick cash.

For India's pharmaceutical industry, Albert David represents path not taken. While dynamic companies built global franchises, created innovative products, and generated tremendous wealth, Albert David clung to old ways until no ways remained.

Perhaps the saddest aspect is the waste. Albert David had everything needed for success: early-mover advantage, technical partnerships, manufacturing capabilities, established brands, and debt-free balance sheet. It lacked only leadership with vision and courage to change.

In the end, Albert David's epitaph might read: "Here lies a company that confused survival with success, prudence with paralysis, and heritage with strategy. It lived for 86 years but stopped growing after 60. May its failures teach what its successes could not."

The lights still burn in Gillander House, but Albert David's story is essentially over. What remains is merely corporate afterlife—financial statements without purpose, employees without mission, assets without strategy. The company that began in colonial Calcutta with dreams of pharmaceutical independence ends in modern Kolkata as testament to what happens when dreams die.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube