A. K. Capital Services Limited: The Kingmaker of Indian Debt

I. Introduction & Episode Roadmap

Picture a trading floor that has no ticker crawl, no bell, no CNBC camera crew jostling for the closing shot. Picture instead a conference room in Mumbai's financial district where a handful of bankers are working the phones — not to a hedge fund in London or a sovereign wealth desk in Singapore, but to the treasurer of a district cooperative bank in Maharashtra, the investment committee of a state electricity board provident fund, and the trustee of a temple endowment somewhere in Tamil Nadu. On the table is a bond issue for a large public-sector borrower. The job is not to make it exciting. The job is to make it disappear — quietly, fully subscribed, at the right yield, before the market moves. This is the world A. K. Capital Services Limited has lived in for more than three decades, and it is the reason most Indian equity investors have never heard of a company that has arranged some of the largest debt placements in the country.

A. K. Capital Services (AKCAPIT.BO, listed on the Bombay Stock Exchange under scrip code 530499) is a boutique merchant bank that made a bet almost nobody else in 1993 wanted to make: that the boring, illiquid, unglamorous business of arranging corporate and government bonds would one day matter enormously.1 Its official home is akgroup.co.in, and the group brands itself, with a straight face, as "the bond house of India."7

The core paradox of this story is a David-and-Goliath problem. How does a firm with a market capitalization of roughly ₹1,100–1,200 crore compete in debt capital markets against balance-sheet leviathans like Axis Bank, HDFC Bank, and ICICI Bank — institutions that can underwrite an entire issue with the deposit float of a single branch network? The answer, as we will see, is that A. K. Capital chose never to fight on the giants' terms at all. It chose to become indispensable in the plumbing rather than dominant on the balance sheet.

Here is the roadmap for this episode. We will trace four intertwined threads. First, the strategic migration from a generalist post-liberalization merchant bank into a pure-play debt capital markets (DCM) specialist. Second, the hybrid engine that defines the company today — a fee-based syndication business bolted onto a capital-heavy Non-Banking Financial Company (NBFC) that increasingly drives the profits. Third, the regulatory realities: the 2018 shadow-banking crisis that froze the market, and the SEBI settlement of October 2025 that exposed uncomfortable questions about how bond books get built. And fourth, the digital horizon — the retail bond revolution and the awkward, revealing role of IndiaBonds.com, a platform built not inside the listed company but beside it, in the hands of the promoter family.

That last thread is where the neutral investor lens earns its keep. A. K. Capital is a genuinely interesting business with a real, defensible niche. It is also a company where the most exciting growth option sits outside the shares you can actually buy. Both things are true, and the job of this story is to hold them together without flinching. Let us start where every good bond desk starts: with the origin of the relationships.

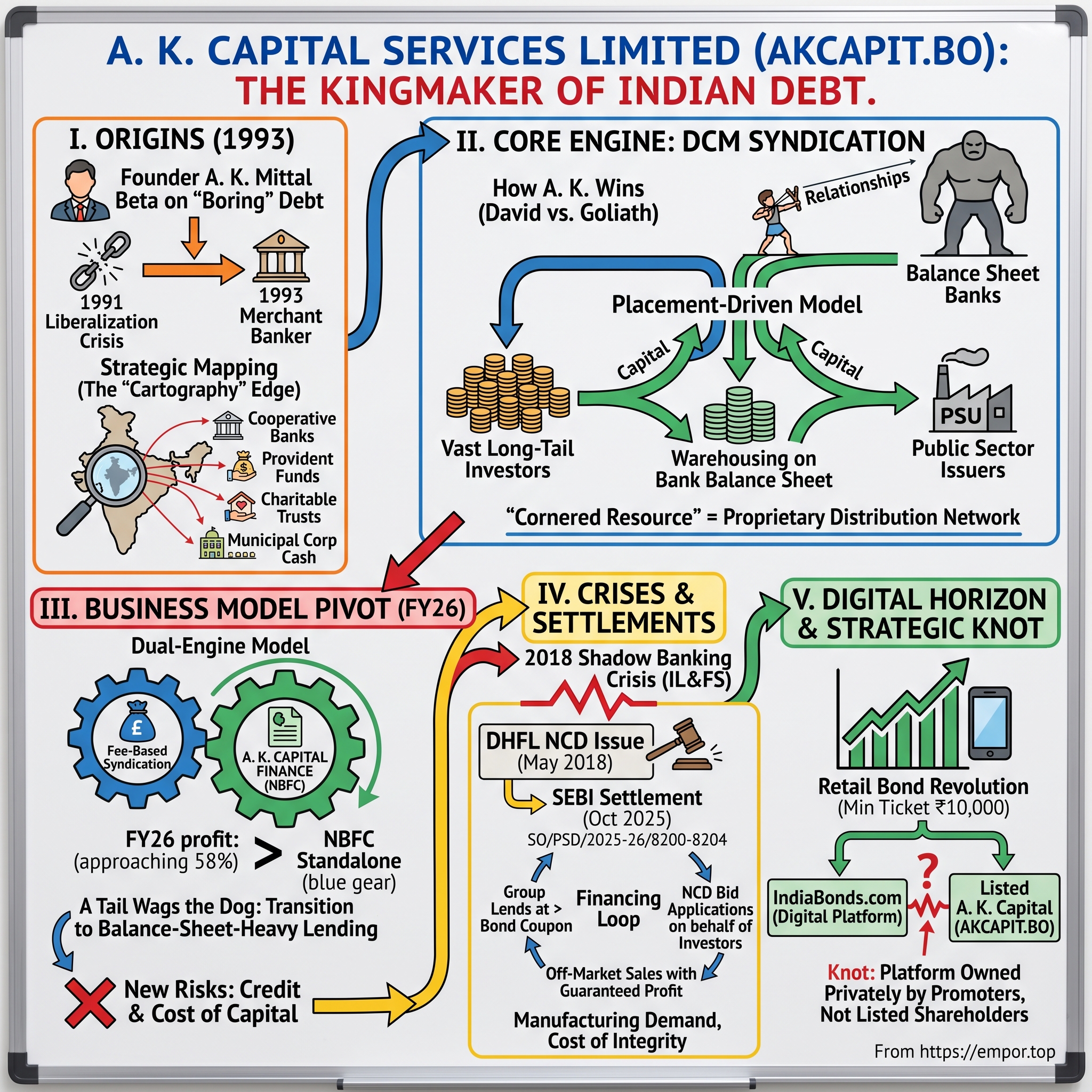

II. The Origins & Founding Context (1993–2007)

In October 1993, the Indian economy was two years into the most consequential policy rupture in its post-independence history. The 1991 balance-of-payments crisis had forced open a command economy, license-raj controls were falling, and a generation of financiers suddenly found themselves in a market that was being invented in real time.1 Most of them ran toward equity. The Bombay Stock Exchange was booming, initial public offerings were the talk of every drawing room, and the fastest way to be somebody in Indian finance was to take a company public.

A. K. Mittal walked the other way. When he founded A. K. Capital Services in that first flush of liberalization, he registered it as a Category I Merchant Banker and pointed it at the least fashionable corner of the market: corporate bonds.16 It was, on paper, a strange choice. India's corporate bond market in the early 1990s was barely a market at all. It was illiquid, fragmented, opaque, and utterly dominated by public sector undertakings that issued paper to a captive audience of state-owned insurers and banks. There was no vibrant secondary trading, no deep institutional bid, no glamour. What there was, Mittal reasoned, was a structural gap — and structural gaps, unlike hot IPO cycles, do not close in a single boom.

The strategy that emerged in those early years was less about financial engineering than about cartography. A. K. Capital set out to map the demand side of Indian debt with a granularity nobody else bothered with. While the big houses courted the handful of large institutional funds, A. K. Capital went looking for the long tail: municipal corporations sitting on idle cash, regional retirement and provident funds hunting for yield, charitable trust portfolios, and — crucially — the thousands of semi-urban and cooperative banks scattered across the country that needed safe, rated, high-coupon paper but had no relationship with a Delhi or Mumbai investment bank. Each of these buyers was tiny. Collectively, they were an ocean. And an issuer who wanted a bond fully placed did not care whether the money came from one giant or a thousand minnows, so long as it came.

This is the seed of what would later be dressed up in strategy-framework language as a "cornered resource" — a proprietary distribution network of relationships that took years of patient, unglamorous phone calls to build and that a competitor could not simply buy. It is worth pausing on what kind of person builds a business this way. Mittal was not chasing the deal that would make the front page; he was chasing the deal that would make the next hundred deals easier. That is a temperament, not just a strategy.

By the mid-2000s, the patience was paying off. By 2005, the firm had climbed into the top ranks of domestic bond arrangers, taking on marquee assignments including work on Government of India-backed instruments such as Food Corporation of India (FCI) Special Bonds and a growing roster of PSU issuances.6 The company reached the public markets itself and, over this period, established the template it still runs on: win the mandate on relationships and placement power, not on the size of its own balance sheet.

The lesson embedded in this founding decade is the one that runs through the entire A. K. Capital story. The firm's edge was never capital. It was knowing exactly who, across a sprawling and under-banked country, would buy a given bond at a given yield on a given afternoon. That knowledge is the asset. Everything the company has become — the league-table rankings, the NBFC, even the governance controversies — flows from the decision to own that knowledge rather than the balance sheet. To understand how valuable that is, we have to understand the strange architecture of the market it operates in.

III. Decoding the Core: The DCM Ecosystem & How A.K. Wins

To an outsider, "arranging a bond" sounds like a single job. It is not. It is a relay race, and understanding the handoffs is the key to understanding why a small firm can beat a big bank at part of it while never threatening the bank at another part.

Start with the borrower — say, a state-owned power utility that needs ₹5,000 crore for a decade. It has two broad paths. It can walk into a large commercial bank and ask the bank to lend from its own balance sheet, funded by the cheap deposits sitting in millions of savings accounts. Or it can issue bonds — securities sold to a crowd of investors — and hire an arranger to design the instrument, price it, and find the buyers. The Indian debt capital market is split, roughly, between these two models: the balance-sheet arrangers (the big banks, who can both advise and fund) and the placement-driven boutique houses (A. K. Capital, the Trust Group, Darashaw, Tipsons and a handful of others) who bring no meaningful deposit base but bring distribution.6

Here is the crucial asymmetry. A bank like Axis or HDFC wins debt mandates partly by offering to swallow the issue whole — to warehouse it on a balance sheet measured in lakhs of crores. That is a weapon a ₹1,200-crore boutique can never match. But most large bond issues are not meant to sit on any single balance sheet. They are meant to be distributed — spread across insurers, pension funds, mutual funds, banks' treasury books, and that vast long tail of cooperative and provident-fund buyers. And distribution is a game of relationships and reach, not of capital. This is the seam A. K. Capital lives in: it does not out-muscle the giants, it out-distributes them.

The company has historically been described as holding roughly a mid-single-digit share of domestic debt issuances and routinely ranking among the top handful of arrangers in the league tables that the market watches.6 Investors should treat any precise, self-reported market-share figure with appropriate caution — league-table positions shift issue by issue, and definitions vary by compiler — but the directional claim is well supported by the firm's three-decade presence at the top of PSU and corporate bond mandates. The point is not the decimal. The point is that a firm this small keeps showing up on deals many multiples its size, which only makes sense if it is being hired for something the giants cannot replicate.

That something is the placement machine. When A. K. Capital takes a mandate, its edge is the ability to ring around a fragmented universe of yield-seeking institutions and clear the paper efficiently — the proprietary database of corporate clients, central and state PSUs, and the thousands of cooperative banks and provident funds that have learned, over decades, that A. K. Capital sources compliant, rated, high-coupon debt and does not waste their time. In the language of Hamilton Helmer's 7 Powers, this is the "cornered resource": an asset the company controls that rivals cannot easily obtain and that produces differential returns. We will stress-test how durable that power really is later, because a relationship network is only a moat until the counterparties can be reached one tap away on a phone — a threat that, ironically, the promoter family itself has been busy building.

For now, the investor takeaway is this: A. K. Capital's competitive position rests on distribution reach, not financial firepower, and that is both its genius and its ceiling. It explains why the firm can earn attractive fees on deals it could never fund — and why, to grow beyond the fee pool, it eventually had to do the one thing its founding thesis avoided. It had to build a balance sheet.

IV. The Dual-Engine Business Model: Merchant Banking + NBFC

Every asset-light advisory business eventually meets the same tempting, dangerous fork in the road, and A. K. Capital's arrival at it is the pivot of the modern story. On one side sits the pure fee business: elegant, high-return, capital-free, and utterly at the mercy of the cycle. On the other sits the balance sheet: heavier, riskier, hungrier for capital — but able to underwrite, to hold, to earn a spread, and to smooth the lumpy income of a syndication shop. A. K. Capital, like nearly every merchant bank before it, walked toward the balance sheet.

The company today runs two engines. The first is standalone merchant banking — the classic advisory and syndication business that arranges and places debt for a fee. It is beautifully capital-light: when it works, it throws off high returns on equity because it consumes almost no equity. But it is violently cyclical. When interest rates spike or a credit scare freezes issuance, the fee pool can evaporate in a quarter, and there is nothing on the balance sheet to earn through the drought. In FY26, the standalone entity reported a profit of roughly ₹61.6 crore on total income of about ₹188 crore — a reminder that the "original" business, while smaller than the group, remains a serious cash generator.3

The second engine is the NBFC: A. K. Capital Finance Limited (AKCFL). This is the capital-heavy machine, and its role is best understood as the balance-sheet muscle that the parent's founding thesis deliberately lacked. AKCFL can underwrite an issue, hold bonds on its own book, and "park" paper when a placement needs balance-sheet support to get over the line — turning the group from a pure agent into a principal that can put its own money at risk to win and clear deals. It also runs a broader treasury and lending operation, earning a spread between its cost of funds and the yield on its book.

Here is the quietly radical part: the balance-sheet engine has become the bigger profit driver. On a consolidated basis, A. K. Capital reported net profit of ₹114.04 crore (₹11,404.48 lakh) for the financial year ended March 31, 2026, up about 31% from ₹87.13 crore the prior year, on total income of roughly ₹573 crore (up from ₹484 crore).3 Within that, company disclosures indicate the NBFC contributed on the order of ₹50 crore of net profit over the nine months to December 2025 — approaching 58% of group earnings.6 Read that again. A company whose entire identity was built on arranging other people's debt without a balance sheet now earns the majority of its money from a balance sheet. The advisory tail has, in profit terms, started to wag the dog.

What does that migration actually buy, and what does it cost? On the benefit side, the NBFC smooths the cycle and lets the group capture spread income and underwriting economics it once left on the table. On the cost side, it imports the two risks every lender carries: credit risk and cost-of-capital risk. On asset quality, the group has reported sound metrics — nil gross non-performing assets at the NBFC as of FY25 — which suggests disciplined underwriting so far, though "so far" is doing real work in a book that has grown through a benign credit environment.6 The more visible pressure is on margins. Core net interest margin at the NBFC moderated to around 3.7% in the first nine months of FY26, down from roughly 4.6% in FY25, as the rising cost of funds outran the yield on assets.6 That compression is the mechanical signature of a balance-sheet business in a higher-rate world, and it is precisely the risk the asset-light founders never had to think about.

The capital-allocation direction of travel confirms where management's conviction lies. In early 2026, the listed parent infused ₹75 crore into AKCFL via non-cumulative compulsorily convertible preference shares (CCPS) — a deliberate decision to feed the balance-sheet engine rather than return the cash or double down on the fee business.6 For investors, this is the single most important structural fact about the company today: A. K. Capital is no longer best understood as a merchant bank with a lending sideline. It is increasingly a bond-focused NBFC with an elite distribution franchise attached. That reframing changes which numbers matter, which risks bite, and how the whole thing should be valued. And it means the company's fate is now tied to the credit cycle in a way it never was in its first two decades — a lesson the market taught the entire sector, brutally, in 2018.

V. Inflection Points: The Shadow Banking Crisis & The DHFL Scandal

In the autumn of 2018, the plumbing of Indian finance sprang a leak that nearly flooded the whole house. In September, Infrastructure Leasing & Financial Services (IL&FS) — a sprawling, systemically important infrastructure financier that everyone had assumed was as safe as the government behind many of its projects — began defaulting on its obligations. The shock was less about the size of any single default than about what it revealed: a shadow-banking sector that had funded long-dated assets with short-dated money, rolling over commercial paper on the assumption that the music would never stop. When confidence cracked, the roll-over market froze, and NBFCs across the country suddenly could not refinance.

For a firm like A. K. Capital, the crisis did not arrive as a headline. It arrived as a phone that stopped ringing. Corporate bond issuance seized up as investors fled anything that smelled of credit risk and yields gapped wider. A syndication business lives on issuance volume; when volume vanishes, so does the fee pool. The strategic response across the boutique DCM world — and A. K. Capital's included — was a defensive crouch: pivot from aggressive syndication toward capital preservation and treasury safety, protect the balance sheet, and wait for the freeze to thaw.1 It was the first real demonstration that the newly built NBFC engine was a double-edged asset — a source of resilience in that it could earn through, but also a source of exactly the refinancing and credit exposure that had just detonated across the sector.

The crisis also cast a long, retrospective shadow over one specific deal — one that would return to haunt the company seven years later. In May 2018, just months before IL&FS blew up, Dewan Housing Finance Corporation Limited (DHFL) launched a large public issue of non-convertible debentures (NCDs), aiming to raise up to ₹12,000 crore, with coupons stretching up to around 9.10%.10 A. K. Capital Services was one of a syndicate of lead managers on the issue, alongside names like Edelweiss, Axis Bank, ICICI, SBI Capital Markets, and the Trust Group — it was one arranger among many, not the sole architect.10

DHFL, of course, went on to become one of the most notorious collapses in Indian financial history, ultimately felled by fraud allegations and dragged through insolvency. But the part of the DHFL story that matters for A. K. Capital is not the borrower's fraud — it is the mechanics of how the bond book was built. A public NCD issue has to look successful. A book that is visibly under-subscribed spooks investors and can fail outright, and in the jittery months of 2018, the pressure on arrangers to show fully subscribed public debt issues was intense. How, exactly, does a placement machine guarantee that a book fills up when genuine demand is uncertain? That question sat quietly for seven years — and when SEBI finally answered it, the answer would cost A. K. Capital's group both money and a chunk of its reputation for the boring, dependable competence on which its entire franchise was built.

VI. The SEBI Settlement & Governance Stress Test (October 2025)

On October 16, 2025, the Securities and Exchange Board of India issued a settlement order — reference SO/PSD/2025-26/8200-8204 — that pulled back the curtain on precisely how at least one bond book got built, and it was not a flattering view.112 The order resolved an investigation into the A. K. Capital group's conduct around the May 2018 DHFL NCD issue, and the specifics are worth walking through slowly, because they go to the heart of the "placement machine" the whole franchise is built on.

According to the regulator's findings, five group entities were involved: A. K. Capital Services (the listed parent), A. K. Capital Finance (the NBFC), A. K. Stockmart, E-Ally Securities (India), and Ridhi Sidhi Distributors.1 SEBI alleged that the group used powers of attorney to submit bid applications for roughly 1.41 million NCDs on behalf of 911 investors — in effect, driving a large block of "retail" demand through instruments it controlled.1 More damning was the financing loop: AKCFL extended loans to these investors to fund their bond purchases at interest rates higher than the bonds' own coupons.1 Pause on the economics of that. An investor who borrows at, say, 10.5–11% to buy a bond yielding around 9% is guaranteed to lose money on a hold-to-maturity basis. Nobody does that voluntarily — which is the tell. The arrangement only makes sense if the investor was never meant to hold the bond at all.

And, per SEBI, they were not. After allotment, the group allegedly facilitated off-market sales of the NCDs — arranging guaranteed, profitable exits for these investors so that the negative carry on the loan was more than offset by a pre-baked resale gain.1 Stitch it together and you get a mechanism for manufacturing the appearance of broad retail demand: control the bids, fund the bids, and guarantee the exit. The book looks full. The issue looks successful. The market sees a fully subscribed public issue and takes comfort. That is the alleged playbook, and it is exactly the kind of thing that erodes the one asset a bond house cannot afford to lose — trust in the integrity of the demand it reports.

The group settled without admitting or denying the findings, which is the standard architecture of a SEBI consent order and should not be read as either confession or exoneration. The financial cost totaled about ₹4.33 crore across the five entities, including disgorgement of roughly ₹72 lakh of gains plus 12% annual interest.2 The three main entities — the listed parent, the NBFC, and A. K. Stockmart — each paid about ₹1.33 crore, with the two smaller distributors paying a few tens of lakhs apiece.2 The settlement terms had been recommended by SEBI's high-powered advisory committee and cleared by its panel of whole-time members on September 5, 2025, with payment completed by October 3, 2025; on settlement, SEBI agreed not to pursue enforcement for the identified violations.2

The analytically honest reading is twofold. On one hand, ₹4.33 crore is financially trivial for a group earning over ₹100 crore a year — this was not a solvency event or even a material earnings dent. On the other hand, the reputational and governance signal is disproportionate to the rupees. The episode reveals a structural temptation embedded in the syndication model itself: when your value proposition is "we can always fill the book," the incentive to fill it by any means available is permanent, and it intensifies exactly when the market is most fragile. Investors evaluating management credibility should file this not as a one-off legal expense but as evidence about how the franchise behaves under commercial pressure. It is also a reminder that the same distribution machinery that is the company's greatest asset can, pointed slightly wrong, become its greatest liability. Which makes the next chapter — the attempt to move that machinery online, and who owns it — all the more consequential.

VII. The Digital Frontier: IndiaBonds.com & Retail Democratization

For thirty years, A. K. Capital's distribution edge lived in a place no competitor could copy: the heads and phone contacts of its bankers, and the trust of a few thousand institutional buyers. Then the ground shifted. SEBI, on a multi-year mission to broaden the corporate bond market, steadily lowered the barriers to retail participation — culminating in a reduction of the minimum ticket size for many listed corporate bond issues to as little as ₹10,000, down from the ₹10 lakh face values that had long walled retail investors out.7 Suddenly, "a bond in every hand" was not a slogan but a plausible market. The addressable universe of buyers exploded from a few thousand institutions to, potentially, tens of millions of savers.

Whoever built the rails for that flow — the digital platform where an ordinary investor could browse, compare, and buy a corporate bond as easily as a mutual fund — stood to own a piece of the next chapter of Indian fixed income. And the A. K. Capital ecosystem did build exactly that. In 2021, IndiaBonds was launched as one of India's early Online Bond Platform Providers (OBPP), a SEBI-recognized category of licensed digital bond marketplaces.7 Its co-founders were Aditi Mittal — a two-decade fixed-income veteran who is a Whole-time Director of A. K. Capital Services and an executive at the NBFC subsidiary — and Vishal Goenka, a former Deutsche Bank Singapore managing director and Merrill Lynch London credit trader who came on as CEO and co-founder.78 The platform later raised external capital, including a maiden funding round of about ₹32.5 crore, to build out technology and reach.13

Here is where the story develops a knot that a neutral analyst cannot smooth over. IndiaBonds is strategically central to the A. K. Capital story — it is the digital front door to the retail bond market, a natural distribution channel, and a source of referral and business flow that plausibly benefits the listed company. But its equity value is not held by the listed company. It sits privately, under the promoter-controlled India Bond Private Limited, in the hands of the promoter family and outside investors.7 The growth option and the public shareholders are, structurally, in different rooms.

This is the related-party friction, and it deserves to be stated plainly rather than waved away. When a listed company's most exciting adjacent growth asset is owned by its promoters rather than by the company itself, minority shareholders face a familiar tension: they may bear costs, lend brand, and provide business flow that helps the private asset compound, while the equity upside of that asset accrues to the promoter family. Contrast this with how peers have handled analogous opportunities. Firms like JM Financial and Nuvama have generally built or acquired their wealth-tech and digital distribution platforms inside their listed entities, so that public shareholders participate in the value created. A. K. Capital kept its primary digital growth option next door.

None of this is illegal, and there are benign readings — a fast-moving fintech may genuinely need the freedom, risk appetite, and outside venture capital that a conservative listed NBFC balance sheet cannot easily provide. But "benign reading available" is not the same as "no issue." The governance question is real: is the listed entity capturing fair value for whatever it contributes to IndiaBonds, and is the flow of business and money between the public company and the private platform disclosed, arm's-length, and fairly priced? For a long-term investor, the honest posture is watchfulness. The digital frontier is where A. K. Capital's decades-old distribution moat either scales into the retail era or quietly migrates off the public balance sheet — and which of those happens depends on structures that are still being written.

VIII. Strategic Frameworks: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Strip away the narrative and war-game the business cold, and a clarifying picture emerges. Let us run A. K. Capital through two lenses — Michael Porter's Five Forces for the shape of the industry, and Hamilton Helmer's 7 Powers for the durability of the firm's edge — because together they explain both why the company has survived and why its position is more fragile than three decades of continuity might suggest.

Begin with Porter. The threat of new entrants is low-to-medium. The relationship network and regulatory licensing that a pure-play debt arranger needs cannot be assembled overnight, and the boring, low-margin nature of the business deters glamour-seeking capital. But that same barrier is being lowered by digitization, which threatens to turn relationship reach into a software feature. The bargaining power of issuers is high: large corporates and PSUs run competitive processes and squeeze syndication fees, which is precisely why fee margins in DCM are thin and why balance-sheet giants can dangle "we'll fund it ourselves" as a fee-crushing weapon. The threat of substitutes is high and structural: an issuer who does not like the bond market can take a direct bank loan, tap external commercial borrowing offshore, or — for equity-eligible names — simply raise equity. Bonds compete against every other form of financing. And rivalry is intense, pitting a small boutique against banking groups that fund corporate debt with the cheapest liability base in the country: retail deposits. On four of five forces, the structural picture is genuinely tough. This is not a comfortable industry; it is a demanding one where a specialist survives only by being better at one specific thing than anyone else bothers to be.

Which is exactly what the 7 Powers lens is for. The clearest power A. K. Capital holds is the cornered resource — the proprietary, decades-deep relationship database of cooperative banks, regional trusts, provident funds, and PSU treasuries that lets it place paper others cannot. This is the source of its differential fee income, and it is real. The second is counter-positioning: by choosing to be a pure-play debt specialist while peers chased equity, A. K. Capital occupied a niche the giants found too small and unglamorous to contest head-on, and it built expertise there that a diversified bank cannot easily match without cannibalizing its own lending economics. A third, more contestable, claim is scale economies within its niche — high transaction volumes across many small buyers create an operational efficiency in placement that lets the firm compete on price during competitive PSU bidding.

But here is the stress test the frameworks force. A cornered resource built on relationships is only a moat until the relationships can be disintermediated. The rise of online bond platforms — including one built by the promoter family itself — is a slow-motion assault on the very asset that makes A. K. Capital special. When a cooperative bank treasurer or a retail saver can see and buy bonds on a screen, the value of knowing that treasurer personally erodes. The company's edge is real today; whether it is durable depends on whether A. K. Capital can convert an analog relationship moat into a digital one before the moat drains — and, awkwardly, the most promising digital vehicle for doing so is currently owned next door. That tension is the crux of the entire investment question.

IX. Playbook: Business and Investing Lessons

Step back from the specifics, and A. K. Capital offers three portable lessons that apply far beyond one mid-cap bond house — the kind of pattern-recognition that makes a single company's story useful to an investor looking at dozens of others.

The first lesson is about the gravitational pull from asset-light to asset-heavy. A. K. Capital was born as a pure advisory business, the most capital-efficient model in finance: earn fees, consume no balance sheet, compound returns on a tiny equity base. And yet, three decades on, the majority of its profit comes from a lending balance sheet. This is not a failure of discipline; it is the near-inevitable trajectory of service-driven financial firms. Advisory income is cyclical and cannot be warehoused, competitors with balance sheets can undercut on integrated deals, and the temptation to earn spread on the flow you already source is overwhelming. The lesson for investors is to watch this migration wherever it appears — in brokers, advisers, and boutique banks — because the firm you bought for its capital-light returns quietly becomes a firm that must be underwritten for credit risk and cost of capital. The valuation multiple appropriate to a fee machine is not the one appropriate to an NBFC, and the market does not always re-rate on the day the mix shifts.

The second lesson is about niche domination versus scale. A. K. Capital is a case study in how a micro-cap can defend a genuine franchise against institutions a thousand times its size — not by matching their firepower, but by owning a distribution network so fragmented and so painstakingly built that the giants find it uneconomic to replicate. The playbook is to find the seam in the market that the big players consider too small, too boring, or too operationally annoying to bother with, and then to own it completely. The risk in the playbook, as we have seen, is that seams can be closed by technology faster than by competitors.

The third lesson is the sharpest, and it is about governance and where the optionality lives. When you analyze a public company, do not just study the assets on its balance sheet; study the valuable assets adjacent to it that are owned by the people who control it. A. K. Capital's highest-optionality asset — its digital retail platform — is a promoter-held related party, not a public subsidiary. The lesson is not "avoid such companies"; it is "price the structure honestly." Ask whether minority shareholders participate in the upside they help create, or merely subsidize it. That single question, applied rigorously, separates investors who understand what they own from those who only understand what the company reports. With those lessons in hand, we can finally weigh the whole case — bull against bear.

X. Bear vs. Bull: KPIs, Risks, Valuation, and the Future

By the middle of 2026, the market's verdict on A. K. Capital looked, at a glance, euphoric. The stock had climbed from around ₹1,450 in late 2025 toward record territory, with exchange data pointing to highs in the vicinity of ₹1,850 in June 2026, on the back of strong double-digit growth in both revenue and profit.11 The bull and bear cases both start from the same set of facts and reach opposite conclusions — which is exactly why this is an interesting business rather than an obvious one.

The bull case rests on a genuine secular tailwind. India is in the early innings of a decades-long financialization of household savings, and the corporate bond market — still small relative to the economy and to bank credit — is precisely the market policymakers are trying hardest to deepen. Every reform that broadens bond issuance and retail participation expands A. K. Capital's pond. The recent numbers give the tailwind teeth: consolidated net profit of ₹114.04 crore in FY26, up roughly 31%, on income of about ₹573 crore, with a strong Q3 that saw consolidated profit rise more than 50% year-on-year and the board declare a ₹22 dividend.345 Layer on robust promoter alignment — the promoter group holds about 72.15%, led by the family's investment vehicle and A. K. Mittal's direct 17.62%, with Aditi Mittal at 3.31% — and buying more in the open market through 2025 and 2026, and you have management with real skin in the game.9 A skeptic should note that concentrated promoter ownership cuts both ways, but on the bull reading it signals conviction.

The bear case is the mirror image of every strength. The migration to a balance-sheet model means the company now carries a rising-rate problem it never used to have: higher funding costs compress the NBFC's net interest margin (already down to about 3.7% from 4.6%) and, worse, a rate spike or credit scare can throttle issuance volumes and fee income at the same time — a double hit that 2018 demonstrated is not theoretical.6 There is credit risk on the lending book; nil gross NPAs are reassuring but were earned in a benign cycle, and the real test of underwriting comes when the cycle turns. And there is the governance overhang, now with a documented data point: the October 2025 SEBI settlement over the DHFL book-building, the related-party structure of IndiaBonds, and a series of promoter reclassifications moving relatives such as Abhinav Kumar Mittal, Sanjiv Kumar, and Kavita Garg into the public category — the kind of promoter-group housekeeping that a skeptical investor watches closely for what it does to control and float.17

The activist stress test writes itself. A skeptical long/short investor would ask: why does the group's crown-jewel digital option sit outside the listed entity, and what is the true value leakage? How arm's-length are the transactions between the public company and India Bond Private Limited, and are they growing? Is the reported nil-NPA book a sign of underwriting skill or of a cycle that has not yet tested it? And does the SEBI settlement reflect an isolated lapse or a structural willingness to bend the book-building process under pressure? None of these has a settled answer, which is the point — they are the questions that determine whether the recent share-price strength is a re-rating of a durable franchise or the top of a credit-cycle-fueled sentiment wave.

Which brings us to the KPIs that actually matter. Ignore the noise and track three things. First, the net interest margin of the NBFC subsidiary — this is now the swing factor in group profitability and the cleanest read on whether rising funding costs are eating the balance-sheet engine. Second, market share and league-table position in domestic debt issuance — the direct measure of whether the core distribution franchise is holding, gaining, or quietly ceding ground to banks and platforms. Third, the volume and terms of related-party transactions with India Bond Private Limited — the single best window into whether value is being fairly shared with, or slowly siphoned from, public shareholders. Watch those three, and you are watching the real business rather than the stock price.

XI. Epilogue & Outro

A. K. Capital Services began as a contrarian bet that the dullest corner of Indian finance would one day be its most important, and on that bet A. K. Mittal has been vindicated. The firm turned patient relationship-building into a genuine cornered resource, survived the shadow-banking crisis that killed flashier peers, and rode the deepening of India's bond market to record profits and a record share price by mid-2026.

But the company that emerges from this story is more complicated than the "quiet titan of debt" framing suggests. It is a business quietly transforming itself from a capital-light fee machine into a credit-cycle-geared NBFC, importing the exact risks its founding thesis was built to avoid. It is a franchise whose defining asset — a network of relationships — faces slow disintermediation by the very digital platform its promoters are building beside, rather than inside, the listed company. And it is a management team whose alignment is high but whose recent record includes a regulatory settlement that exposed the darker mechanics of the placement model.

For the long-term investor, the case is neither a clean bull nor an easy dismissal. A. K. Capital is a leveraged play on the expansion of Indian fixed income, run by an aligned and experienced promoter family, trading on strong recent momentum — and simultaneously a business where credit risk, margin compression, and related-party governance sit as live, unresolved questions rather than settled ones. The tailwind is real. So are the frictions. Which force compounds faster over the next decade is the whole game, and it will be decided not in the league tables but in the credit cycle and the fine print of who owns the future.

References

-

A.K. Capital Group Settles SEBI Probe Over DHFL NCD Issue Irregularities — Business Standard, 2025-10-17 ↩↩↩↩↩↩↩↩↩↩

-

AK Capital Group Pays Rs 1.33 Crore Each To Settle DHFL NCD Case with SEBI — Moneylife, 2025-10-17 ↩↩↩

-

A.K. Capital FY26 Net Profit Rises 31% to ₹11,404 Lakh — ScanX, 2026 ↩↩↩

-

A.K. Capital Services Q3 FY26 Result Analysis — MarketsMojo, 2026 ↩

-

A.K. Capital Services Surges on Strong Q3, Declares ₹22 Dividend — Whalesbook, 2026 ↩

-

A. K. Capital Services Limited — Annual Report 2024-25 ↩↩↩↩↩↩↩↩↩

-

Fintech Bond Investment Platform IndiaBonds gets CEO & Co-Founder Vishal Goenka — PR Newswire, 2023-01-19 ↩

-

A.K. Capital Services Promoter Group Increases Shareholding to 72.14% Through Open Market Acquisitions — IndiaIPO ↩

-

IndiaBonds Raises ₹32.5 Crore in Maiden Funding Round — MarcaMoney ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube