Ajax Engineering: India's Concrete Equipment Champion

I. Cold Open & Episode Setup

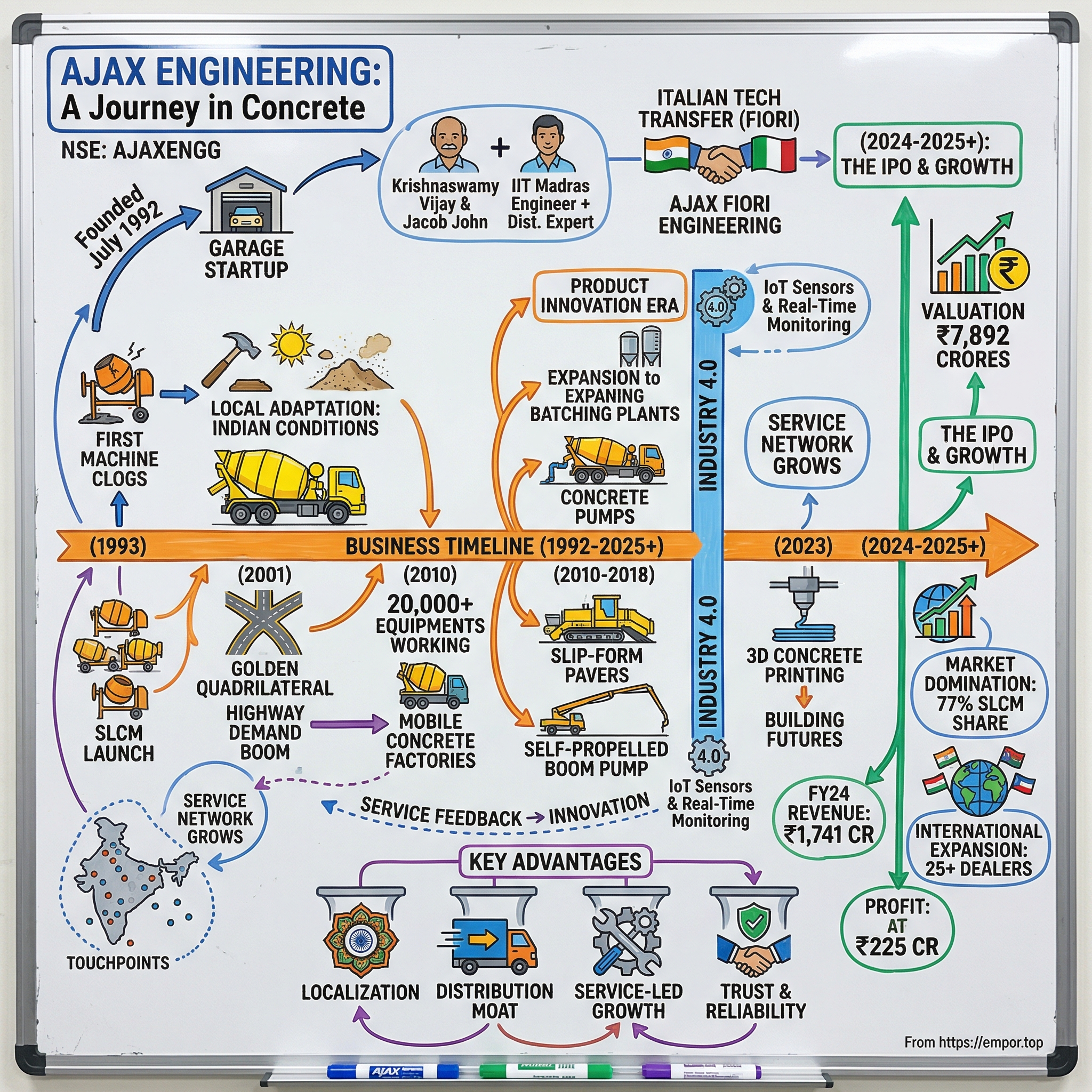

The monsoon of 2022 brought chaos to Bangalore's Outer Ring Road. Construction crews scrambled to repair a critical flyover section before the rains turned the site into a mudslide. At 3 AM, under floodlights cutting through the drizzle, a bright yellow self-loading concrete mixer rumbled onto the scene—mixing, transporting, and pouring concrete in one seamless operation. No batching plant. No separate transit mixers. Just one machine and three operators replacing what would have traditionally required twenty workers and multiple vehicles. This wasn't some imported European marvel; it was built 40 kilometers away in Doddaballapur by Ajax Engineering.

Here's the paradox that should intrigue any serious investor: while India's tech unicorns dominate headlines with their billion-dollar valuations and global ambitions, a hardware manufacturer in Bangalore has quietly built something arguably more impressive—processing equipment that handles 12% of all concrete produced in India. That's right. One in every eight cubic meters of concrete poured in the world's most populous nation passes through Ajax machinery.

Founded in July 1992, Ajax Engineering Limited has methodically constructed a 77% market share monopoly in self-loading concrete mixers—the kind of dominance that would make even the most successful software platforms envious. The company trades on the NSE under the symbol AJAXENGG, sporting a market capitalization that recently touched ₹7,892 crores. Not bad for a business that started when "Make in India" was more aspiration than policy.

What we're about to explore isn't just another manufacturing success story. It's a masterclass in building an industrial franchise in an emerging market—complete with technology transfers, dealer networks that span continents, and the kind of operational excellence that turns commodity hardware into a competitive moat. From a garage startup leveraging Italian technology to becoming the backbone of India's infrastructure revolution, Ajax Engineering's journey offers lessons that transcend industries.

The timing couldn't be more relevant. As India embarks on what many call the greatest infrastructure build-out in human history—₹100 lakh crore in planned spending over the next five years—understanding how Ajax positioned itself at the center of this transformation becomes essential. This is the story of how mechanical engineers from IIT Madras bet on concrete over code, and won.

II. The Founding Story & Early Vision

Picture Krishnaswamy Vijay in 1991, sitting in his modest Bangalore office after two decades climbing the corporate ladder at Larsen & Toubro. At 45, with graying temples and the measured confidence that comes from 20 years of manufacturing experience, he faced a decision that would define the rest of his life. The liberalization of India's economy had just begun—Manmohan Singh's reforms were barely months old—and the air crackled with possibility. Foreign technology, previously locked behind licensing walls, was suddenly accessible. Capital, though still scarce, could be raised. Most importantly, India was about to build. And build big.

Vijay wasn't your typical entrepreneur. An IIT Madras mechanical engineering graduate from the class of 1970, he'd spent his career in the trenches of Indian manufacturing—first at Tractors Engineer Limited, then at construction giant L&T. He understood something fundamental that the new breed of software entrepreneurs emerging in Bangalore didn't: India's transformation wouldn't happen in server rooms or on computer screens. It would happen in concrete and steel, kilometer by kilometer, project by project.

His co-founder, Jacob Jiten John, brought complementary skills—deep knowledge of construction equipment distribution and an understanding of how contractors actually worked in India's chaotic construction sites. Together, they identified a gap so obvious it seemed impossible: India was mixing concrete the same way it had for decades—manually, inefficiently, with massive labor crews producing inconsistent quality. Meanwhile, in Europe, self-loading concrete mixers had revolutionized small and medium construction projects.

The insight was elegant. India didn't need more batching plants—those massive, stationary concrete production facilities that required huge capital investments and could only serve large projects. What India needed was mobile, flexible equipment that could produce high-quality concrete anywhere—remote highway projects, urban construction sites squeezed between buildings, rural infrastructure where no batching plant existed for hundreds of kilometers.

Enter Fiori Group, the Italian manufacturer that had perfected self-loading concrete mixer technology. Vijay and John negotiated a technology transfer agreement—not just to import and sell, but to manufacture in India, adapt for Indian conditions, and eventually innovate beyond the original designs. The company was initially named Ajax Fiori Engineering, a joint venture that would bring European engineering to Indian construction sites.

But here's where the story gets interesting. Unlike other Indian companies that remained perpetual licensees, dependent on foreign technology and paying royalties forever, Vijay had bigger plans. He wasn't building a trading company or an assembly operation. He was building an engineering company—one that would eventually out-innovate its European partners.

The early team was tiny—just seven engineers working out of a small facility in Doddaballapur. They spent months studying the Italian designs, understanding not just how the machines worked, but why they were designed that way. Then came the adaptations. Indian construction sites were different—dustier, hotter, with different aggregate sizes and cement grades. Indian operators had different skill levels. Indian roads meant the equipment needed to be more robust.

"We're not just making Italian machines in India," Vijay would tell his team. "We're making Indian machines for Indian conditions."

This philosophy—localization over standardization—would become Ajax's core competitive advantage. But in 1992, as they prepared to launch their first indigenously manufactured self-loading concrete mixer, success was far from guaranteed. The Indian construction industry was deeply conservative, skeptical of mechanization, and dominated by contractors who had built their businesses on cheap manual labor. Convincing them to invest in a machine costing lakhs of rupees, from an unknown Indian company, using foreign technology they'd never heard of—that would require more than just good engineering.

III. Building the Foundation (1992-2010)

The first Ajax self-loading concrete mixer rolled off the production line in March 1993, painted in what would become the company's signature yellow. The launch event at a construction site outside Bangalore was a disaster. The machine, perfectly calibrated for European aggregates, clogged within minutes when fed with local materials. The conveyor belt, designed for smooth river gravel, couldn't handle the angular crushed granite common in South India. A crowd of skeptical contractors, who'd traveled from across Karnataka to witness this "revolutionary" machine, shook their heads and started leaving.

Vijay grabbed a wrench himself, climbing into the mixer drum while his engineers frantically adjusted the settings. Three hours later, covered in concrete dust and cement, they got it working. The demonstration that followed—mixing, transporting, and pouring concrete with just two operators—finally drew appreciative nods. But the damage was done. Word spread quickly in India's tight-knit construction community: "Ajax machines are complex, foreign technology that doesn't work here."

It took eighteen months to recover from that first impression. The engineering team essentially rebuilt the machine from the ground up. They enlarged the loading bucket to handle Indian aggregate sizes. They reinforced the chassis to survive Indian roads—or what passed for roads at many construction sites. They simplified the hydraulics, making field repairs possible with locally available parts. Most crucially, they developed a tropical cooling system that could handle 45-degree Celsius ambient temperatures while continuously mixing concrete.

The breakthrough came from an unexpected source: the Golden Quadrilateral highway project, launched in 2001. This massive undertaking—connecting Delhi, Mumbai, Chennai, and Kolkata with 5,846 kilometers of highways—created unprecedented demand for concrete. But here was the challenge: much of the construction happened in remote areas, far from any batching plants. Contractors faced a choice: set up expensive temporary batching plants every few kilometers, or find a mobile solution.

Ajax's timing was perfect. Their second-generation self-loading mixers, now fully adapted for Indian conditions, could produce 12-15 cubic meters of concrete per hour anywhere—a dusty highway construction site in Rajasthan, a bridge project over a Bihar river, a flyover in congested Mumbai. The machines became mobile concrete factories, eliminating the need for separate batching plants, transit mixers, and large labor crews. But the real genius wasn't just the product—it was the go-to-market strategy. Instead of trying to sell directly to large contractors who had established relationships with equipment suppliers, Ajax focused on smaller, regional contractors who were winning subcontracts on these mega-projects. These contractors couldn't afford to set up batching plants for their small sections of work. For them, a self-loading mixer wasn't just convenient—it was the difference between profitability and loss.

The company established what they called "demonstration-cum-training centers" along the Golden Quadrilateral route. Potential customers could see the machines in action, operate them under supervision, and most importantly, calculate the economics themselves. The math was compelling: one self-loading mixer could replace a batching plant, two transit mixers, and 15-20 workers. The payback period, even with financing costs, was under 18 months.

By 2010, over 20,000+ Ajax equipments were working satisfactorily across the length and breadth of the country in varied applications including CC Roadways, National/State Highways, Irrigation Canals/Dams, Railways, and other infrastructure projects. But this number understates the transformation. Each machine wasn't just a sale—it was a beachhead in India's construction ecosystem.

The service network became Ajax's hidden weapon. By 2008, they had established service centers within 100 kilometers of every major construction corridor. Spare parts were stocked locally. Technicians were trained not just to repair, but to optimize machines for specific applications—different mix designs for highway concrete versus residential construction, adjustments for seasonal temperature variations, modifications for high-altitude projects in the Himalayas.

This period also saw Ajax's gradual independence from Fiori. While maintaining the technical collaboration, Ajax engineers began developing India-specific innovations. They created a "tropical package" for machines operating in extreme heat. They developed a "dust suppression system" for projects in Rajasthan's desert regions. They even created a "monsoon mode" that allowed continuous operation during the rainy season—something their Italian partners had never needed to consider.

The 2008 financial crisis, which devastated equipment manufacturers globally, barely dented Ajax's growth. While international competitors pulled back from India, Ajax doubled down. They used the downturn to negotiate better component prices, hire talented engineers from struggling competitors, and most importantly, lock in relationships with contractors who remembered which suppliers stood by them during tough times.

By 2010, Ajax had achieved something remarkable: they'd transformed self-loading concrete mixers from an exotic foreign technology to an essential tool for Indian construction. The bright yellow machines had become as common on Indian highways as the orange safety vests of construction workers. But Vijay and his team weren't satisfied with just dominating one product category. The next decade would see them attempt something far more ambitious—building an entire ecosystem of concrete equipment.

IV. The Product Innovation Era (2010-2018)

The conference room at Ajax's Doddaballapur facility in January 2011 looked like a war room. Whiteboards covered every wall, filled with flowcharts, competitor analyses, and market projections. Vijay, now 65 but showing no signs of slowing down, stood before his leadership team with a simple question: "We own self-loading mixers. What's next?"

The answer wasn't obvious. Ajax could have continued milking their dominant position in SLCMs, enjoying 70%+ market share and healthy margins. But Vijay saw a bigger opportunity—and a looming threat. Chinese manufacturers were beginning to eye the Indian market. Their strategy was predictable: enter with low prices, accept losses to gain market share, then gradually improve quality. Ajax needed to build a moat that went beyond just product superiority.

The insight came from their own customers. Contractors using Ajax self-loading mixers were increasingly winning larger projects—projects that required not just mixing concrete, but pumping it to heights, transporting it over distances, and producing it in massive quantities. These contractors were cobbling together equipment from multiple suppliers—Ajax mixers, imported pumps, local batching plants. The integration was messy, maintenance was a nightmare, and productivity suffered.

"We need to become a one-stop shop for concrete," Vijay declared. "Not just mixing. Everything from production to placement."

The expansion began systematically, with Ajax adapting to customer needs and aiming to become the most customer-centric organization. In 2012, they opened their second manufacturing plant at Doddaballapur specifically for SLCMs—a 50,000 square meter facility with the capacity to produce 2,000 units annually. But the real innovation was happening in the R&D center next door.

The 79-person engineering team wasn't just adapting foreign technology anymore—they were creating entirely new product categories. The first breakthrough came in 2013 with the launch of the JSP concrete pump. This wasn't a rebadged import; it was designed specifically for Indian conditions. The pump could handle the lower slump concrete common in India, operate in 45-degree heat without overheating, and most importantly, be serviced using the same network that maintained Ajax's mixers.

2014 marked another milestone with the third manufacturing facility in Gowribidanur dedicated to batching plants. This seemed counterintuitive—batching plants competed with self-loading mixers in some applications. But Vijay understood that different projects needed different solutions. A highway project might use self-loading mixers, while a large residential complex needed a stationary batching plant. By offering both, Ajax became a consultant rather than just a vendor—helping contractors choose the right equipment mix for each project.

The real game-changer came in 2018 with the fourth facility, again for SLCMs, but with a twist. This plant incorporated Industry 4.0 concepts—IoT sensors on production equipment, real-time quality monitoring, and predictive maintenance systems. But more importantly, it was designed to manufacture what would become Ajax's most ambitious product yet.

In 2019, Ajax launched India's first indigenously designed and manufactured slip-form paver. To understand the significance, consider this: slip-form pavers are used to construct concrete roads, airport runways, and canal linings—massive infrastructure projects that were previously the domain of imported equipment costing crores. Ajax's paver, priced at 40% less than imports, with local service support, changed the economics of concrete road construction in India.

The paver launch event in Bangalore was revealing. Instead of the usual product specifications and feature lists, Ajax demonstrated something different. They showed a video of the paver constructing a 1-kilometer stretch of concrete road in rural Karnataka in just 8 hours—what would have taken traditional methods several days. Then came the kicker: the entire operation was managed by operators trained at Ajax's facility, using a control system with instructions in local languages, with every wearing part available from existing Ajax dealers.

That same year, Ajax introduced the Self Propelled Boom Pump (SPBP)—a concrete pump mounted on a truck chassis with a multi-section boom that could place concrete at heights up to 42 meters. Again, the innovation wasn't just in the product but in the application. Ajax's SPBP was designed for India's booming real estate sector, where high-rise construction was exploding but space constraints made traditional pumping methods challenging.

The culmination of this innovation decade came in 2023 with the launch of Ajax's 3D Concrete Printing Machine. This wasn't just following a global trend—it was a strategic bet on the future of construction. The machine could print complex concrete structures directly from digital designs, reducing labor requirements by 70% and material waste by 30%. Early adopters included affordable housing projects where the speed and cost advantages were game-changing.

But here's what's remarkable about Ajax's innovation strategy: they weren't trying to be first. They were trying to be best for India. Every product launched between 2010 and 2018 followed the same playbook:

- Identify a concrete application where Indian contractors struggled with existing solutions

- Study global best practices but design specifically for Indian conditions

- Price at 30-40% below imports while maintaining quality

- Leverage existing dealer and service networks for distribution and support

- Train operators in local languages with India-specific applications

By 2018, Ajax's product portfolio had expanded to over 110 equipment variants. These machines were serving diverse applications from CC Roadways and National/State Highways to Irrigation Canals, Dams, Railways, Airport Infrastructure, Power Transmission Projects, Buildings and Factories, Industrial Foundations, and Renewable energy projects. They weren't just selling equipment anymore—they were selling complete concrete solutions.

The financial impact was staggering. Revenue grew from ₹763 crores in FY22 to ₹1,741 crores in FY24, with profit after tax jumping from ₹66 crores to ₹225 crores in the same period. But the real achievement was market position. Ajax hadn't just defended their turf against Chinese imports—they'd expanded it, becoming the default choice for any contractor serious about mechanized concrete construction.

The innovation era had transformed Ajax from a single-product company to a comprehensive concrete equipment platform. But with great success came new challenges. How do you maintain service quality across an exponentially expanded product line? How do you finance growth without compromising the balance sheet? And most importantly, how do you preserve entrepreneurial agility as you become an industry giant? The answer would come through one of India's most successful industrial IPOs.

V. Market Domination & Network Effects

At 5:30 AM on a humid September morning in 2024, Rajesh Kumar's phone rang. A contractor working on the Mumbai-Nagpur Expressway had a crisis—his self-loading mixer had broken down mid-pour, with 300 cubic meters of concrete scheduled for the day. Within 45 minutes, an Ajax service technician was on site. By 7 AM, the machine was operational. By noon, a replacement unit from the nearest dealer had arrived as backup. This wasn't exceptional service—it was standard operating procedure across Ajax's network.

Founded in 1992, Ajax had evolved into a global leader in Self-Loading Concrete Mixers, renowned for engineering excellence. Based in Bangalore, they provided 360° concreting solutions, from mixers to pumps, with advanced manufacturing facilities in Doddaballapur and Gowribidanur. But the real power wasn't in the factories—it was in the network.

By September 2024, Ajax commanded a 77% market share in self-loading concrete mixers. To put this dominance in perspective: for every four self-loading mixers operating on Indian construction sites, three bore the Ajax badge. This wasn't just market leadership—it was approaching monopolistic control. How did a company in a competitive, capital-intensive industry achieve such dominance?

The answer lies in understanding network effects in industrial equipment—a concept typically associated with software platforms, not hardware manufacturers. Every Ajax machine sold strengthened the company's position in multiple ways:

The Service Network Multiplication Effect: With 51 dealerships across 23 states and 114 touchpoints including branches and service centers, Ajax created what economists call a "thick market." The more machines in a region, the more economical it became to stock spare parts, train technicians, and provide rapid service. This created a virtuous cycle—better service attracted more customers, which justified even denser service networks.

Consider the numbers: Ajax had sold to over 15,700 customers by 2024. Each customer didn't just buy one machine—the average customer owned 2.8 Ajax units. Why? Because once you had one Ajax machine, adding another meant sharing spare parts inventory, using the same trained operators, and dealing with one service network. The switching costs weren't just financial—they were operational.

The Operator Training Moat: Ajax's comprehensive training programs covered machine operation and maintenance, including classroom sessions at their Bangalore Training Centre, factory visits, and on-site training. They partnered with the Infrastructure Equipment Skill Council of India (IESC) to elevate India's workforce skills, offering 2-3 day on-site training programs with facilities provided by the customer.

This wasn't corporate social responsibility—it was strategic moat-building. Every operator trained on Ajax equipment became a walking advertisement and a switching cost. When contractors hired operators, they looked for Ajax-certified skills. When operators looked for jobs, they highlighted their Ajax training. The company had effectively created a labor market locked into their ecosystem.

The Dealer Economics Revolution: Traditional equipment dealerships in India operated on thin margins, high working capital requirements, and constant credit risk. Ajax flipped the model. Dealers weren't just distributors—they were partners in a shared ecosystem. Ajax provided financing support, buyback guarantees for trade-ins, and most importantly, a steady stream of high-margin spare parts revenue.

A typical Ajax dealer earned 8-10% margins on equipment sales but 25-30% on spare parts and 35-40% on service. With the average self-loading mixer requiring ₹1.5-2 lakhs in annual maintenance and spare parts, a dealer with 200 machines in their territory had a ₹3-4 crore recurring revenue stream. This aligned incentives perfectly—dealers wanted customers to use their machines intensively (more wear, more parts), and customers wanted maximum uptime (better service, readily available parts).

The International Expansion Strategy: While dominating India, Ajax quietly built an international network—25 dealers and distributors across South and Southeast Asia, Middle East, and Africa. But this wasn't traditional export. Ajax targeted countries with similar construction challenges to India—extreme heat, dust, varied material quality, and price-sensitive markets.

In Bangladesh, Ajax machines were building the Padma Bridge. In Nigeria, they were constructing Lagos highways. In Sri Lanka, they were rebuilding tsunami-affected areas. Each international success created a demonstration effect—if Ajax could handle Nigerian conditions or Middle Eastern heat, they could handle anything.

The Data Advantage Nobody Talks About: By 2024, Ajax had an installed base of over 27,800 units sold over the previous decade. Each machine generated data—utilization rates, maintenance patterns, failure modes, productivity metrics. While not as sophisticated as Silicon Valley's data operations, Ajax used this information intelligently.

They knew that machines in coastal areas needed different anti-corrosion packages. They discovered that highway projects averaged 2,200 operating hours annually while urban projects averaged 1,600 hours. They identified that 73% of breakdowns happened in electrical systems during monsoon season, leading to waterproofing improvements. This wasn't big data—it was smart data, creating continuous product improvements that competitors without similar installed bases couldn't match.

The Standardization Paradox: Counterintuitively, Ajax's dominance came from customization, not standardization. While maintaining core platform designs, they offered over 110 variants. Need a mixer for high-altitude work in Ladakh? Ajax had a low-oxygen combustion package. Working in corrosive conditions near chemical plants? There was a special coating option. Tight urban site? They offered a compact variant with the same capacity.

This mass customization was only possible because of scale. The development cost for each variant could be spread across hundreds of units. Competitors offering generic products couldn't match this specificity. It was the industrial equipment equivalent of Amazon's "long tail"—profitably serving niche needs through scale.

The Financial Engineering of Dominance: Ajax's market dominance wasn't just about operational excellence—it was about financial innovation. They pioneered equipment financing schemes tailored to Indian contractors' cash flows. Instead of requiring large upfront payments, Ajax offered seasonal payment plans aligned with construction cycles—lower EMIs during monsoons when work slowed, higher payments during peak construction season.

They also created an innovative buyback program. Contractors could trade in old Ajax machines for new ones at guaranteed residual values. This solved multiple problems: contractors got predictable equipment refresh cycles, Ajax controlled the second-hand market (preventing cheap used equipment from cannibalizing new sales), and refurbished machines became an entry point for smaller contractors.

By 2024, Ajax wasn't just dominating—they were defining the market. Industry specifications referenced Ajax models. Tender documents specified "Ajax or equivalent" (and there rarely was an equivalent). Construction project planning assumed Ajax equipment productivity rates. They had achieved what every industrial company dreams of but few achieve—becoming the generic term for their category, like "Xerox" for photocopying or "JCB" for excavators.

The network effects were now self-reinforcing. New competitors faced an impossible challenge: to match Ajax's market position, they'd need to simultaneously build manufacturing capacity, create a service network, train operators, establish dealer relationships, and offer financing—all while competing against an incumbent with 77% market share and decades of customer relationships. It wasn't just a moat—it was an ocean.

VI. Financial Performance & Growth Story

The Excel spreadsheet on the investment banker's screen told a story that seemed too good to be true. Revenue: ₹763.29 crores in FY22, ₹1,151.13 crores in FY23, ₹1,741.40 crores in FY24. Profit after tax: ₹66.21 crores, ₹135.90 crores, ₹225.15 crores for the same years. The banker leaned back, removed his glasses, and muttered, "This is a software company's growth with a manufacturing company's margins."

He wasn't wrong. Ajax's SLCM sales had achieved a CAGR of 45.70% between FY22 and H1 FY25—the kind of growth typically associated with SaaS startups, not companies making 10-ton concrete mixers. By FY24, self-loading concrete mixers contributed 85.13% of revenue, growing at 51.28% year-over-year. The remaining revenue came from the expanding portfolio—pumps, pavers, batching plants—all growing but still dwarfed by the core product's dominance.

But the headline numbers only told part of the story. The real achievement was profitable growth at scale. Many Indian manufacturers could grow revenue by accepting lower margins, extending credit terms, or compromising quality. Ajax did none of these. Their EBITDA margins expanded from 15.8% in FY22 to 19.2% in FY24. Return on equity jumped from 18% to 28%. And most remarkably, they did this while remaining almost debt-free—long-term debt to equity ratio of just 0.02 in FY24.

The unit economics revealed why this was possible. An average self-loading concrete mixer sold for ₹18-25 lakhs, depending on specifications. Raw materials—steel, hydraulics, engines—cost about 62% of sales. Manufacturing overhead added another 12%. Sales and distribution: 8%. This left approximately 18% for EBITDA—excellent for a manufacturing business. But the real profit driver wasn't the initial sale—it was the lifetime value.

Over a typical 7-year lifecycle, a self-loading mixer generated ₹12-15 lakhs in spare parts and service revenue for Ajax's ecosystem. With gross margins of 35-40% on parts and 45-50% on service, the lifetime profitability of a single machine could exceed the initial sale profit. It was the razor-and-blades model, except the razor also had great margins.

The working capital story was equally impressive—or concerning, depending on your perspective. Ajax's working capital cycle had stretched from 89 days in FY22 to 124 days in FY24. This wasn't operational inefficiency—it was strategic choice. As growth accelerated, Ajax extended credit terms to capture market share, particularly with smaller contractors who would become lifetime customers. Inventory levels increased as they stocked spare parts across their expanding dealer network.

The CFO explained it simply: "We can either optimize for working capital efficiency or market dominance. We chose dominance. Once a contractor buys Ajax, they rarely switch. The lifetime value justifies the initial working capital investment."

This strategy showed in the customer concentration numbers. No single customer accounted for more than 3% of revenue. The top 10 customers contributed less than 15%. This wasn't just risk mitigation—it was proof of true market penetration. Ajax wasn't dependent on a few large contractors or government projects. They had thousands of small and medium contractors, each contributing steadily to revenue.

The export story added another growth vector. International sales grew from ₹45 crores in FY22 to ₹142 crores in FY24, still less than 10% of total revenue but growing at 65% CAGR. The margins were even better internationally—without the need for extensive service networks initially, Ajax could price at a premium while maintaining lower overhead.

Cash flow generation was robust. Operating cash flow averaged ₹150-200 crores annually, more than sufficient to fund capex of ₹40-50 crores per year. The company wasn't capital-intensive in the traditional sense—they didn't need massive furnaces or chemical plants. Their factories were essentially sophisticated assembly operations with strategic in-house manufacturing of critical components.

The balance sheet strength enabled Ajax to weather volatility without drama. When steel prices spiked 30% in FY23, they absorbed the initial impact, then passed through increases gradually over six months. When demand slowed during the 2024 election period, they used the time to build inventory and train dealers, emerging stronger when government spending resumed.

But perhaps the most impressive financial metric was one that didn't appear in annual reports: capital efficiency per unit of market share. Ajax had achieved 77% market share in self-loading mixers with cumulative capital investment of less than ₹500 crores over three decades. Compare this to automotive companies that spent thousands of crores for single-digit market shares. The difference? Ajax picked a niche and dominated it completely before expanding.

The 21.2% profit CAGR over five years understated the transformation. In FY19, Ajax was a profitable but subscale player—₹378 crores in revenue, ₹41 crores in profit. By FY24, they were approaching ₹2,000 crores in revenue with ₹225 crores in profit. This wasn't just growth—it was a complete rescaling of the business.

The financial model had three powerful tailwinds that promised continued expansion:

- Operating leverage: With fixed costs largely absorbed, incremental margins were approaching 25-30%

- Pricing power: As the dominant player, Ajax could selectively increase prices without losing share

- Capital allocation optionality: With minimal capex needs and strong cash generation, they could choose between dividends, acquisitions, or aggressive expansion

The Q3 FY25 results, released in January 2025, confirmed the momentum. Revenue hit ₹531 crores for the quarter, up 38% year-over-year. The order book stood at ₹743 crores, providing visibility for two quarters. Management guided for ₹2,200-2,400 crores in FY25 revenue—another 25-35% growth year.

For investors evaluating Ajax, the financial story presented a rare combination: growth company economics in a mature industry, software-like margins in hardware manufacturing, and market dominance that created predictable cash flows. The question wasn't whether Ajax could maintain profitability—it was how much larger could they grow before hitting natural limits. The IPO would help answer that question.

VII. The IPO Decision & Capital Markets Journey

The board meeting on August 14, 2024, at the Taj West End in Bangalore was unusually subdued. After three decades of building Ajax into India's concrete equipment champion, Krishnaswamy Vijay, now 78, faced perhaps his most consequential decision yet. The investment bankers from Axis Capital, ICICI Securities, and JM Financial had just finished their presentation. The numbers were compelling: India's equity markets were at all-time highs, infrastructure stocks were commanding premium valuations, and investor appetite for manufacturing stories was insatiable.

"Why now?" asked an independent director. "We don't need capital. We're generating ₹200 crores in operating cash flow annually. We have negligible debt. Why dilute?"

Vijay's answer revealed the strategic thinking that had guided Ajax for three decades: "This isn't about capital. It's about currency. The infrastructure supercycle is just beginning. We'll see consolidation, international expansion opportunities, technology acquisitions. We need stock as acquisition currency. More importantly, our dealers, employees, and customers should participate in the value creation ahead."

The IPO structure was unusual. The entire ₹1,269.35 crore offering was secondary—an offer for sale of 2.02 crore shares by existing shareholders. Ajax wouldn't receive any proceeds. This sent a powerful signal: the company didn't need money. The selling shareholders, primarily early investors and employee trusts, were taking partial exits after holding for 15-20 years. Vijay and the promoter group would retain 80% post-IPO—high by Indian standards, signaling confidence in future prospects.

The price band of ₹415-436 per share valued Ajax at approximately ₹5,500 crores at the upper end—about 25 times FY24 earnings. For a manufacturing company, this seemed aggressive. But the bankers argued Ajax wasn't a typical manufacturer. With 77% market share, 35%+ revenue growth, and 20%+ ROE, it deserved a platform company multiple.

The roadshow revealed fascinating investor psychology. Domestic mutual funds loved the "Make in India" narrative—here was a company that had outcompeted international giants through indigenous innovation. Foreign investors were attracted to the infrastructure play—Ajax was a pure-play bet on India's ₹100 lakh crore infrastructure pipeline. Retail investors saw a simple story: every kilometer of road, every apartment building, every dam needed concrete, and Ajax machines would mix that concrete.

The anchor book-building on February 13, 2025, saw overwhelming response. Leading mutual funds including HDFC, ICICI Prudential, and SBI picked up anchor allocations. Marquee foreign investors like Government of Singapore and Abu Dhabi Investment Authority participated. The anchor portion was subscribed 3.2 times, setting the stage for robust public response.

The three-day IPO opening on February 14, 2025, coincided with infrastructure sector euphoria. The government had just announced a 35% increase in highway construction targets. The real estate sector was witnessing its strongest growth in a decade. Ajax's timing, whether by luck or design, was impeccable.

Day 1 saw cautious interest—1.3 times subscription, primarily from retail investors attracted by the ₹15,000 minimum application amount. Day 2 brought institutional money—mutual funds and insurance companies driving subscription to 3.8 times. The final day saw a frenzy. High-net-worth individuals (HNIs), seeing strong institutional interest, piled in. The issue closed at 6.45 times subscription with bids for 9.12 crore shares against 1.41 crore on offer.

The category-wise subscription told its own story:

- Qualified Institutional Buyers: 8.93 times

- Non-Institutional Investors: 5.25 times

- Retail Investors: 3.89 times

- Employees: 12.3 times (revealing internal confidence)

The listing on February 17, 2025, was anticlimactic in the best way. The stock opened at ₹523, a 20% premium to the issue price, traded in a narrow range, and closed at ₹518. No wild volatility, no operator-driven movements—just steady price discovery. Within a month, the stock had found its level around ₹550-580, valuing Ajax at approximately ₹7,892 crores.

Post-IPO, interesting dynamics emerged. The 80% promoter holding meant limited floating stock—only about 12% actively traded after accounting for strategic investors. This created natural price support but also meant any significant buying or selling moved the stock dramatically.

The IPO proceeds distribution was revealing. Of the ₹1,269 crores raised, approximately ₹950 crores went to the promoter group (partial exit maintaining 80%), ₹200 crores to early investors, and ₹119 crores to employee trusts. The promoters immediately announced they were investing ₹500 crores of their proceeds into a new manufacturing facility—signaling continued commitment despite the partial cash-out.

Analyst coverage began within weeks. Most initiation reports carried "Buy" ratings with target prices 15-25% above market price. The common themes: - Under-penetration of mechanized equipment in Indian construction (only 35% vs 80%+ in developed markets) - Government infrastructure spending providing multi-year visibility - Dominant market position creating pricing power - International expansion optionality - Potential M&A targets using stock currency

But the most insightful analyst note came from a boutique research firm: "Ajax isn't selling equipment. They're selling productivity in a country where construction labor is becoming scarce and expensive. This is a 20-year structural story, not a cyclical infrastructure play."

The institutional investor meetings post-IPO revealed sophisticated understanding. Questions focused on competitive dynamics with Chinese players, technology disruption from electric equipment, and working capital management. Management's answers were consistent: local manufacturing and service created an unassailable moat, electrification was an opportunity not threat (Ajax would lead the transition), and working capital investment was strategic for market dominance.

Six months post-IPO, Ajax had delivered on promises. Q1 FY26 results showed 34% revenue growth, international expansion into two new countries, and announcement of an electric self-loading mixer prototype. The stock had re-rated to ₹680-720 levels, a 60% gain from IPO price, validating the market's confidence.

The IPO had achieved its strategic objectives. Ajax now had currency for acquisitions, with management hinting at evaluating targets in adjacent categories like road construction equipment. The public listing brought transparency and governance improvements—quarterly earnings calls, increased disclosure, independent board oversight. Employee stock options became more valuable with daily market pricing, helping attract talent from larger competitors.

Most importantly, the IPO had transformed Ajax from a successful private company to a public market champion. The daily stock price became a scorecard, analyst reports provided external validation, and inclusion in indices brought permanent capital. The transformation from entrepreneur-driven private firm to institution-worthy public company was complete.

VIII. Industry Context & Competitive Landscape

The conference room at the Construction Equipment Manufacturers Association's annual meeting in Delhi, December 2024, buzzed with nervous energy. On stage, a McKinsey partner presented slides that should have thrilled everyone present: India's construction equipment industry was projected to grow from $8 billion to $20 billion by 2030. Cement consumption had grown from 325 million tonnes in FY19 to 405 million tonnes in FY24, with 8% CAGR expected through FY29. The Ready-Mix Concrete (RMC) market was exploding at 19% CAGR. Yet the mood was anxious. The elephant in the room? Chinese competition.

"They're not competing on quality anymore," muttered the CEO of a leading excavator manufacturer. "Chinese equipment is now 80% as good at 60% of the price. And they're willing to finance at rates that don't make economic sense."

This was the paradox of India's construction equipment industry in 2025: massive growth opportunity shadowed by intense competition. Every global player wanted a piece of India's infrastructure boom. Caterpillar, Komatsu, Volvo, JCB—all were expanding Indian operations. Chinese giants like SANY and XCMG were aggressive with pricing and payment terms. Local champions like L&T, BEML, and Escorts Kubota were defending turf while trying to scale up.

In this battlefield, Ajax's position was unique. While others fought bloody battles in excavators, loaders, and cranes—commoditized categories with 15-20 players—Ajax dominated a specialized niche where technology, service, and local knowledge mattered more than just price.

Consider the competitive landscape in self-loading concrete mixers:

Action Construction Equipment: Listed on NSE, ₹3,800 crore market cap, primarily known for mobile cranes. Their foray into concrete equipment was halfhearted—a me-too product line contributing less than 10% of revenue. They lacked Ajax's dedicated dealer network for concrete equipment and struggled with service support outside metros.

BEML (Bharat Earth Movers Limited): The public sector giant had the scale—₹3,500 crore revenue—but suffered from typical PSU challenges. Decision-making was slow, product development cycles stretched years, and their focus remained on mining and defense equipment. Their concrete equipment division was an afterthought, staffed with transfers from other divisions rather than specialized talent.

Escorts Kubota: After the Japanese giant's investment, Escorts had technology access and deep pockets. But their focus was agricultural and material handling equipment. Concrete equipment required different dealers, different service capabilities, different customer relationships. Escorts treated it as adjacency rather than core focus—a fatal error in a specialized market.

The international players faced different challenges. European manufacturers like Schwing Stetter and Putzmeister offered superior technology but at prices 50-80% higher than Ajax. Their service networks were limited to major cities. Spare parts came from Europe with 8-12 week lead times. They were selling Mercedes-Benz solutions to customers who needed reliable Maruti Suzuki options.

Chinese manufacturers were the real threat—or were they? SANY and XCMG had entered aggressively, offering self-loading mixers at 20-30% below Ajax prices. But early adopters discovered hidden costs. The machines required frequent repairs. Spare parts, despite promises of local stocking, often had to be imported from China. Service technicians were few and frequently changed. Most critically, Chinese equipment struggled with India's diverse conditions—the electronics failed in monsoons, hydraulics couldn't handle the heat, and engines weren't calibrated for Indian fuel quality.

Ajax's competitive moat wasn't just market share—it was ecosystem lock-in. When the government introduced BS-VI emission norms in 2020, Ajax had BS-VI compliant machines ready six months before implementation. Competitors scrambled to import compliant engines, facing supply chain disruptions and cost escalations. Ajax had worked with local engine manufacturers for two years, ensuring smooth transition.

The electrification wave presented another competitive dynamic. Global manufacturers were pushing electric construction equipment as the future. But Ajax understood Indian reality—unreliable power supply at construction sites, extreme operating conditions that drained batteries, and total cost of ownership calculations that didn't yet favor electric. Their strategy was pragmatic: develop electric prototypes for urban applications where they made sense, but continue improving diesel efficiency for the 80% of market not ready for electrification.

The technology disruption everyone feared—autonomous equipment, IoT integration, AI-powered predictive maintenance—was happening, but slowly. Construction sites weren't factories with controlled environments. They were chaotic, dusty, dangerous places where million-dollar autonomous equipment could be destroyed by a careless truck driver. Ajax's approach was incremental—add GPS tracking for fleet management, sensors for maintenance alerts, but keep the core product robust and simple.

The competitive dynamics varied by segment:

Highway Construction: Dominated by large contractors using Ajax equipment for medium-scale concrete work and imported equipment for specialized applications. Ajax owned this segment with 80%+ share.

Real Estate: More fragmented with regional players using mix of equipment. Ajax competed with local assemblers offering cheap Chinese knock-offs. Won through financing and buyback guarantees that smaller players couldn't match.

Rural Infrastructure: Ajax's sweet spot. PMGSY (Pradhan Mantri Gram Sadak Yojana) rural road projects needed equipment that could operate anywhere, be serviced by local mechanics, and handle variable material quality. No competitor came close to Ajax's rural penetration.

Metro and Urban Infrastructure: The one segment where Ajax faced real competition. European manufacturers with superior technology for specialized applications like tunnel construction had an edge. But even here, Ajax was gaining share by offering "good enough" solutions at half the price.

The raw material and component ecosystem added another layer of competitive advantage. Ajax had localized 85% of components over three decades. When global supply chains broke during COVID, Ajax continued manufacturing while competitors dependent on imports shut down. They'd developed 200+ local suppliers, many exclusive to Ajax, creating a cost and resilience advantage impossible to replicate quickly.

The dealer economics created perhaps the strongest competitive barrier. An average Ajax dealer had invested ₹3-5 crores in facilities, inventory, and training. They generated 15-18% ROE from Ajax products—exceptional for equipment distribution. For a competitor to poach these dealers would require guaranteeing similar economics, which was impossible without Ajax's scale and margins. New dealers would need years to build customer relationships and service capabilities.

Government policy inadvertently strengthened Ajax's position. The "Make in India" initiative gave preference to local manufacturers in government contracts. The Production Linked Incentive (PLI) scheme for manufacturing provided subsidies Ajax could access but pure importers couldn't. GST implementation created a level playing field where unorganized players using tax arbitrage couldn't compete.

The infrastructure supercycle wasn't just about quantity—it was about quality and speed. The government's Gati Shakti program demanded faster project execution with better quality standards. This meant mechanization wasn't optional anymore—it was mandatory. Ajax, with proven equipment and ecosystem, became the default choice for contractors who couldn't afford execution delays.

Looking ahead, the competitive landscape would likely consolidate. Subscale players couldn't justify investments in BS-VI compliance, electrification, and service networks. Chinese players might grab share in price-sensitive segments but would struggle in applications requiring reliability and support. European manufacturers would remain niche players for specialized applications.

Ajax's strategy was clear: dominate the core self-loading mixer market completely, expand into adjacent concrete equipment categories leveraging the same ecosystem, and let competitors fight over commoditized segments. It was the industrial equivalent of Warren Buffett's "wonderful company at a fair price"—own the tollbooth, not the traffic.

IX. Playbook: Business & Operating Lessons

The Harvard Business School case study on Ajax Engineering, published in September 2024, opened with a provocative question: "How did a company in a commoditized industry achieve software-like margins and network effects?" The 32-page analysis became required reading in emerging market strategy courses, but it missed the subtle operational innovations that actually drove Ajax's success. Here's the real playbook:

Hardware in Emerging Markets: Localization > Global Standardization

When Caterpillar entered India, they brought their global bestsellers—machines designed for American highways and European construction sites. When they failed to gain traction, they blamed "unique Indian conditions" and "price-sensitive customers." Ajax understood something deeper: emerging markets aren't just poorer versions of developed markets—they're fundamentally different ecosystems requiring ground-up innovation.

Take Ajax's loading bucket design. European models had smooth, curved buckets optimized for rounded river aggregates. Ajax's engineers noticed Indian construction used angular, crushed granite that would jam in curved spaces. They redesigned with straight edges and steeper angles—a simple change that improved loading efficiency by 30%. No global manufacturer would make such modifications for a single market. For Ajax, India wasn't a single market—it was the market.

The localization went beyond physical design. Ajax machines had instructions in 11 Indian languages. Control panels used intuitive symbols rather than text. Maintenance schedules aligned with Indian seasons—pre-monsoon waterproofing checks, post-summer hydraulic fluid changes. These weren't features you'd find in any global product roadmap, but they mattered enormously to Indian operators.

Distribution as Moat: The Forgotten Competitive Advantage

In the age of digital disruption, physical distribution networks seem antiquated. Yet Ajax's dealer network became their strongest moat—harder to replicate than technology, more valuable than brand, more defensible than patents.

The genius was in dealer economics engineering. Traditional equipment dealers were essentially debt-collectors—selling on credit, chasing payments, managing receivables. Ajax flipped this. Dealers pre-paid for equipment at 5% discount, Ajax provided retail financing directly to end customers. Dealers focused on what they did best—relationships and service—while Ajax handled credit risk with better information and scale advantages.

Ajax also pioneered "territory banking"—guaranteeing dealers exclusive rights to large territories if they met investment commitments. A dealer investing ₹5 crores got exclusive rights to districts with ₹50 crore annual market potential. This created mini-monopolies where dealers could invest in facilities and inventory without fear of channel conflict.

Service-Led Growth: The Recurring Revenue Nobody Noticed

While investors obsessed over equipment sales growth, Ajax quietly built a ₹400 crore spare parts and service business generating 40%+ gross margins. This wasn't accidental—it was architected through deliberate choices:

-

Modular Design: Ajax machines used standardized components across models. A hydraulic pump from a 2010 mixer could fit a 2024 model. This reduced inventory complexity and improved parts availability.

-

Predictive Stocking: Ajax tracked failure rates for every component and pre-positioned spares accordingly. Dealers knew that fast-moving parts like hydraulic hoses and filters would always be in stock.

-

Service Intervals: While competitors recommended annual service, Ajax created quarterly check-up programs. More touchpoints meant more opportunities to identify issues, sell upgrades, and maintain customer relationships.

-

Training Certification: Ajax-certified technicians commanded 20-30% salary premiums. This created incentive for mechanics to get trained and stay current, ensuring quality service availability.

Capital Efficiency: The Asset-Light Heavy Manufacturing Model

Ajax achieved something paradoxical—asset-light manufacturing in a capital-intensive industry. Their fixed assets were just ₹280 crores while generating ₹1,741 crores in revenue, a 6.2x asset turnover that would make even FMCG companies envious.

The secret was selective vertical integration. Ajax manufactured only critical components that provided competitive advantage—mixing drums with proprietary blade designs, control systems with custom software. Everything else—chassis, engines, hydraulics—came from specialized suppliers who could achieve better scale economies.

But the real capital efficiency came from dealer inventory financing. Dealers held ₹200+ crores of Ajax inventory at any time, funded by their own working capital or bank loans against Ajax guarantees. This transferred inventory carrying costs while maintaining product availability. Ajax got paid when machines left their factory; dealers managed the last-mile stocking risk.

Market Timing: Riding Government Infrastructure Cycles

Ajax's growth trajectory perfectly aligned with India's infrastructure spending cycles—but this wasn't luck. They developed an sophisticated understanding of government budget cycles, election patterns, and policy implementation timelines.

They knew that highway construction peaked in Q4 (January-March) as agencies rushed to meet annual targets. Ajax pre-built inventory in Q3, offered aggressive financing in Q4, and serviced machines in Q1 when utilization was highest. They understood that state elections meant 3-6 month construction slowdowns, so they used these periods for dealer training and network expansion.

When the government announced the Bharatmala highway program in 2017, Ajax was ready with expanded capacity and dealer financing programs before competitors understood the opportunity. When COVID hit and the government pivoted to rural infrastructure for employment generation, Ajax had equipment suitable for MGNREGA projects ready to deploy.

The Trust Equation: Building Credibility in B2B Hardware Sales

In enterprise software, you can offer free trials and money-back guarantees. In construction equipment, where machines cost ₹20+ lakhs and failure means project delays, trust becomes everything. Ajax built trust through radical transparency:

-

Open Factory Tours: Any customer could visit Ajax factories, see manufacturing processes, meet engineers. This openness was unusual in Indian manufacturing where factories were guarded secrets.

-

Published Failure Rates: Ajax publicly shared equipment reliability data—mean time between failures, common breakdown causes, average repair times. Competitors hid this data; Ajax used transparency as a differentiator.

-

Customer References: Every Ajax sales presentation included contact details of 10 existing customers in similar applications. Prospects could call and verify claims independently.

-

Performance Guarantees: Ajax offered India's first productivity guarantees—if machines didn't deliver specified output under normal conditions, Ajax would compensate the difference.

Innovation Strategy: Fast Follower with Local Adaptation

Ajax never tried to be first globally—they tried to be first in India with solutions that actually worked. When European manufacturers introduced telematics, Ajax waited, learned from their mistakes, then launched a simplified version focusing on what Indian contractors actually needed—fuel monitoring to prevent pilferage, location tracking to prevent theft, and utilization reports for billing.

The 3D concrete printing machine launch in 2023 exemplified this approach. While global players offered $500,000 printers for specialized applications, Ajax developed a $100,000 version focused on affordable housing—simpler, more robust, with locally sourceable materials. They weren't advancing the global technology frontier, but they were making frontier technology accessible to Indian construction.

The Compound Effect: Why These Lessons Matter

Each element of Ajax's playbook was individually replicable. Competitors could localize products, build dealer networks, offer service programs. But the compound effect of doing everything right created an insurmountable advantage. By the time competitors matched one element, Ajax had moved ahead on others.

A new entrant trying to compete would need to simultaneously: - Develop products for Indian conditions (2-3 years) - Build manufacturing capabilities (₹200+ crores investment) - Create dealer network (5+ years to achieve coverage) - Establish service infrastructure (₹100+ crores investment) - Build customer trust and references (5-10 years) - Achieve scale for competitive costs (thousands of units)

The playbook wasn't about any single brilliant strategy—it was about consistent execution across multiple dimensions over decades. In a world obsessed with disruption and moonshots, Ajax proved that systematic operational excellence, compound improvements, and deep market understanding could build an unassailable competitive position.

For investors, the lesson was clear: in emerging markets, the winners aren't always the most innovative or well-funded. They're the ones who understand local reality, build trust through consistency, and execute relentlessly on the fundamentals. Ajax didn't disrupt the construction equipment industry—they simply did everything better than everyone else, for longer, with more focus. Sometimes, that's enough.

X. Future Vectors & Strategic Options

The strategy presentation to Ajax's board in January 2025 began with a map of India overlaid with data that would define the company's next decade. 40,000 kilometers of highways to be built. 100 smart cities under construction. 60,000 megawatts of renewable energy requiring massive concrete foundations. The Gati Shakti program alone envisioned ₹100 lakh crore in infrastructure investment by 2030. The presenter, a McKinsey partner, paused dramatically: "Ajax processes 12% of India's concrete today. By 2035, India will use twice as much concrete. The question isn't whether Ajax will grow—it's whether you'll capture this opportunity or let others take it."

The traditional growth path seemed obvious: make more mixers, sell to more customers, expand gradually. But Vijay, despite his 78 years, was thinking bigger. The infrastructure supercycle wasn't just about volume—it was about fundamental transformation in how India built. Ajax could either ride this wave or shape it.

International Expansion: The Next Frontier

Africa was beginning its own infrastructure revolution. Nigeria alone planned $3 trillion in infrastructure investment over 20 years. Kenya, Ghana, and Ethiopia were building highways, railways, and cities at unprecedented pace. These markets looked like India in 2000—massive need, limited mechanization, price-sensitive customers, challenging operating conditions.

Ajax's international strategy wasn't to compete with Chinese manufacturers on price or European companies on technology. It was to replicate their India playbook: local assembly facilities, dealer networks, operator training, and gradual localization. The first moves were already underway. A assembly facility in Lagos, a partnership with a Kenyan equipment distributor, pilot projects in Bangladesh and Sri Lanka.

But the real opportunity was in knowledge transfer. Ajax understood something Chinese and European competitors didn't: how to build infrastructure in challenging emerging market conditions. Monsoons, extreme heat, variable material quality, operator skill constraints—Ajax had solved these problems in India. The solutions were directly applicable to tropical Africa, Southeast Asia, and Latin America.

The international expansion wouldn't just be about selling equipment. Ajax was exploring "Infrastructure as a Service"—providing not just machines but complete concrete solutions including operators, maintenance, and productivity guarantees. For African governments struggling with project execution, this turnkey approach could be transformative.

Electric and Autonomous Equipment: Inevitable Evolution

The prototype electric self-loading mixer in Ajax's R&D center looked identical to its diesel counterpart—until you noticed the massive battery pack and regenerative braking systems. The economics didn't work yet—the electric version cost 70% more with 60% operational time due to charging requirements. But Ajax knew this would change.

By 2027, battery costs would fall another 40%. India's push for renewable energy meant construction sites would increasingly have power access. Urban construction zones would mandate zero-emission equipment. Ajax wasn't betting on when electrification would happen—they were ensuring they'd be ready when it did.

The approach was pragmatic: hybrid models first, allowing diesel backup when charging wasn't available. Modular battery systems that could be swapped rather than charged. Partnerships with battery manufacturers for construction-specific solutions. Most importantly, maintaining the same operator interface and service protocols, making transition seamless for customers.

Autonomous operation was further out but equally inevitable. Ajax's approach wasn't full autonomy—construction sites were too chaotic for that. Instead, they focused on assisted operation: automatic loading sequences, optimized mixing cycles, collision avoidance, remote operation capabilities for dangerous environments. The goal wasn't to eliminate operators but make them 3x more productive.

Industry 4.0 and IoT Integration: The Data Opportunity

Every Ajax machine manufactured after 2023 included telematics as standard. By 2025, they had 5,000+ connected machines generating millions of data points daily—location, utilization, fuel consumption, maintenance needs, productivity metrics. This data was vastly underutilized.

The next phase would transform Ajax from equipment manufacturer to intelligence provider. Imagine a contractor planning a highway project getting an Ajax report: "Based on 500 similar projects, you'll need 8 self-loading mixers, expect 72% utilization, budget ₹2.3 per cubic meter for equipment costs, and plan 15% weather downtime." This intelligence would be worth as much as the equipment itself.

Ajax was developing "ConcreteOS"—a comprehensive platform for concrete management. It would integrate equipment data with project management software, quality control systems, and supply chain platforms. Contractors could track every cubic meter of concrete from raw material to final placement, with automatic quality documentation for compliance.

The platform play extended to financing. With real-time utilization data, Ajax could offer usage-based financing—pay per cubic meter produced rather than fixed EMIs. For seasonal contractors, this aligned costs with revenue. For Ajax, it created stickier customer relationships and new revenue streams.

Vertical Integration vs. Platform Approach: The Strategic Choice

Ajax faced a classic strategic decision: integrate vertically into adjacent equipment categories or become a platform connecting various equipment manufacturers. Both had merits.

Vertical integration meant acquiring or developing capabilities in excavators, road pavers, and crushing equipment—the full construction equipment stack. This would allow Ajax to offer complete solutions, increase customer wallet share, and leverage their distribution network across categories. The risk was losing focus, competing with established players in their core territories, and massive capital requirements.

The platform approach meant remaining focused on concrete equipment while creating an ecosystem where other manufacturers could leverage Ajax's distribution and service network. Ajax dealerships could offer complementary equipment from partners, earning commission while maintaining capital efficiency. The risk was channel conflict and dilution of the Ajax brand.

Management's emerging consensus favored a hybrid: selective vertical integration into immediately adjacent categories (like concrete pumps and batching plants) while platformizing the dealer network for non-competing equipment. This balanced growth with focus, expansion with capital efficiency.

M&A Possibilities: Consolidation Catalyst

The Indian construction equipment industry was ripe for consolidation. Dozens of subscale manufacturers struggled with BS-VI compliance costs, GST implementation, and working capital requirements. Many second-generation family businesses lacked succession plans. Ajax, with strong balance sheet and public currency, was naturally positioned as consolidator.

The targets fell into three categories:

-

Regional Champions: Companies with strong presence in specific states but lacking national scale. Ajax could acquire and integrate their dealer networks, achieving instant market penetration.

-

Technology Players: Startups developing construction automation, IoT platforms, or electric vehicle technology. These acqui-hires would accelerate Ajax's technology roadmap.

-

Adjacent Category Leaders: Specialists in road construction equipment, material handling, or foundation equipment that complemented Ajax's concrete focus.

The M&A strategy wasn't just about buying revenue. It was about acquiring capabilities, relationships, and market position that would take years to build organically. With 25-30x P/E multiple, Ajax could acquire companies at 10-15x, creating immediate value through multiple arbitrage.

The Sustainability Imperative: Green Concrete Revolution

Environmental regulations were tightening globally. The construction industry, responsible for 8% of global CO2 emissions, faced pressure to decarbonize. Concrete production was particularly carbon-intensive. Ajax's response would define their next decade relevance.

The initiatives were comprehensive: - Equipment designed for low-carbon concrete mixes using fly ash and slag - Carbon capture attachments for batching plants - Optimized mixing algorithms reducing cement requirements by 10-15% - Lifecycle services extending equipment life from 7 to 10 years - Remanufacturing programs giving second life to old equipment

But the real opportunity was in positioning Ajax as the sustainable choice. Government contracts increasingly included environmental criteria. Green building certifications required sustainable construction methods. ESG-focused investors demanded environmental accountability. Ajax could premium-price equipment that helped contractors meet these requirements.

The 2035 Vision: From Equipment to Ecosystem

The strategic options converged toward a singular vision: Ajax as the operating system for concrete construction in emerging markets. Not just selling equipment but providing intelligence, financing, training, and solutions that made concrete construction faster, cheaper, and better.

By 2035, an Ajax customer wouldn't just buy a mixer. They'd join an ecosystem providing: - Equipment with guaranteed productivity - Financing aligned with project cash flows - Operators trained and certified - Predictive maintenance preventing breakdowns - Data intelligence optimizing operations - Quality certification for compliance - Buyback guarantees preserving value

This transformation from product to platform, from manufacturer to ecosystem, would require different capabilities—software development, data analytics, financial services, training infrastructure. But the payoff was enormous: moving from transactional equipment sales to recurring relationship revenues, from competitive bidding to customer lock-in, from industrial company to technology platform valuations.

The infrastructure supercycle created once-in-generation opportunity. The choices Ajax made in the next 24 months—which markets to enter, which technologies to develop, which companies to acquire—would determine whether they remained a successful equipment manufacturer or became the defining platform for emerging market infrastructure. The concrete had been poured for Ajax's foundation. Now it was time to build the superstructure.

XI. Bear vs. Bull Case Analysis

The conference room at Motilal Oswal's Mumbai office was divided—literally. On one side sat the bulls, led by their infrastructure analyst who'd initiated coverage with a "Buy" rating and ₹750 target. On the other, the bears, headed by their chief strategist who warned of cyclical headwinds and structural challenges. The debate that followed would crystallize the investment case for Ajax Engineering.

The Bear Case: Why Gravity Might Win

"Let's start with the obvious," the bearish strategist began, pulling up a chart of government capital expenditure. "Ajax's entire growth story depends on government infrastructure spending. The FY25 budget increased allocation by just 11%—the slowest growth in five years. We're one election upset or fiscal crisis away from a spending freeze. Remember 2012-2014 when highway construction dropped 60%? Ajax's revenue will crater in the next downcycle."

The competition argument followed. "Chinese manufacturers aren't going away. SANY's new Indian factory can produce 5,000 units annually. They're offering 18-month interest-free credit. Yes, Ajax has service advantages today, but that's solvable with investment. In excavators, Chinese players went from 5% to 35% market share in a decade. Why won't the same happen in concrete equipment?"

Raw material volatility presented another concern. Steel prices had increased 40% in two years. Hydraulic components, largely imported, faced currency fluctuations. Ajax's gross margins had compressed 320 basis points from peak. "They claim pricing power," the bear noted, "but they've only passed through 60% of cost increases. In a truly competitive market with rational Chinese competition, margins will normalize to 12-15%, not the 20%+ markets are modeling."

The working capital deterioration was particularly troubling. Days sales outstanding had increased from 89 to 124 days. "They're essentially financing growth by extending credit. What happens when the music stops? We could see a 2008-style crisis where equipment sales halt and receivables become uncollectible. Ajax's balance sheet isn't fortress-like—it's increasingly leveraged through trade credit."

Technology disruption loomed larger than most acknowledged. "Electric equipment isn't 10 years away—it's happening now. Volvo has electric excavators operating in Norway. The cost curves are dropping faster than anyone expected. Ajax's entire manufacturing infrastructure—built for diesel engines and hydraulic systems—could become obsolete. They're fighting the last war while Tesla-equivalent disruption approaches."

The bear's most compelling argument concerned market saturation. "They have 77% market share in self-loading mixers. Where's the growth? Taking share from 77% to 85% is exponentially harder than growing from 20% to 77%. The easy wins are behind them. They're trying to expand into adjacent categories where they lack competitive advantage. It's the classic case of a successful company overreaching."

Management succession posed another risk. Krishnaswamy Vijay was 78 years old. While competent professionals ran daily operations, Vijay remained the visionary and final decision-maker. "This is key man risk personified. The company's entire strategy, culture, and relationships depend on one person. The transition, whenever it happens, will be messy."

Finally, valuation looked stretched. At 35x P/E, Ajax traded at premiums to global construction equipment leaders like Caterpillar (18x) and Komatsu (15x). "Markets are pricing in perfect execution for the next decade. Any disappointment—a weak quarter, delayed government payments, competitive loss—and the multiple will compress to 20x instantly. That's 40% downside from current levels."

The Bull Case: Why the Rocket Has Just Ignited

The bullish analyst smiled, opening with a single slide: India's infrastructure spending as percentage of GDP—6% today, targeting 9% by 2030. "This isn't a cycle—it's a structural transformation. India needs $4.5 trillion in infrastructure investment to sustain 7% GDP growth. This is decade one of a three-decade buildout. Comparing to 2012-2014 is like comparing China's 2010 to China's 1990—different universes."

On competition, the bull had done deeper homework. "Chinese manufacturers have taken share in commoditized categories where service doesn't matter and Total Cost of Ownership (TCO) calculations are simple. Concrete equipment is different. Downtime costs ₹50,000 per day on typical projects. Ajax's 4-hour service response vs. 48-hour for Chinese players makes their 20% price discount irrelevant. Also, notice SANY's new factory makes excavators, not concrete equipment. They're not even trying to compete in Ajax's core market."

The margin story was more nuanced than bears acknowledged. "Yes, gross margins compressed, but operating margins expanded due to operating leverage. Ajax needs minimal incremental fixed costs to double production. At ₹3,000 crore revenue, we model 25% EBITDA margins. The business has natural margin expansion built in—higher capacity utilization, growing spare parts mix, and pricing power from market dominance."

Working capital investment was strategic, not distressed. "Ajax is financing the entire ecosystem's growth. Every rupee of working capital creates customer lock-in. These aren't random receivables—they're secured by equipment that Ajax can repossess and resell. Default rates are under 2%. The working capital is essentially a customer acquisition cost that pays for itself through lifetime value."

On technology disruption, the bull saw opportunity. "Ajax will lead electrification in India, not be disrupted by it. They have the customer relationships, service infrastructure, and balance sheet to manage the transition. New entrants with electric equipment still need distribution and service—exactly Ajax's moat. Besides, diesel equipment will dominate Indian construction for 15+ years. This transition fear is like worrying about EVs in 2010—directionally correct but premature by decades."

Market expansion opportunities were massive despite high market share. "Self-loading mixers are 30% of Ajax's addressable market. Concrete pumps, batching plants, pavers, 3D printers—the TAM expands from ₹3,000 crores to ₹15,000 crores. Plus, mechanization in Indian construction is still just 35% vs. 80% in developed markets. The penetration story alone doubles the market."

International expansion provided another growth vector. "Africa and Southeast Asia represent $50 billion in construction equipment demand growing at 12% CAGR. Ajax's products are perfectly suited for these markets. Even 5% share would double their revenue. They're not exploring—they're already executing with facilities in Nigeria and partnerships across ASEAN."

Management transition was planned and professional. "The second line of leadership has been running operations for years. The board includes industry veterans and independent directors. This isn't a one-man show anymore—it's an institutionalized business. The IPO itself signals professional management taking over from founder-dependence."

On valuation, context mattered. "Comparing Ajax to Caterpillar is like comparing Asian Paints to Sherwin-Williams—different growth profiles, market structures, and opportunities. Ajax deserves premium multiples for: 40%+ revenue growth vs. Caterpillar's 5%, 28% ROE vs. industry's 15%, 77% market share creating monopolistic dynamics, and exposure to the world's fastest-growing major economy. At 35x P/E with 35% growth, the PEG ratio is 1—fairly valued for the quality and growth."

The bull's clinching argument was the risk-reward setup. "Downside is limited by asset value—₹500+ crores in land and machinery, ₹800+ crores in working capital, and ₹200+ crores in annual cash generation. The company trades at 3x book value—not excessive for 28% ROE. Upside is multiples from here if India's infrastructure story plays out. This is asymmetric risk-reward at its finest."

The Synthesis: What Really Matters

Both cases had merit, but the investment decision ultimately hinged on three critical factors:

-

Belief in India's Infrastructure Supercycle: If you believed India would sustain 7%+ GDP growth requiring massive infrastructure investment, Ajax was a pure-play bet on that theme. If you saw fiscal constraints or political instability derailing spending, Ajax was uninvestable.

-