Aimtron Electronics: The Cross-Border ESDM Challenger

I. Introduction & Episode Roadmap

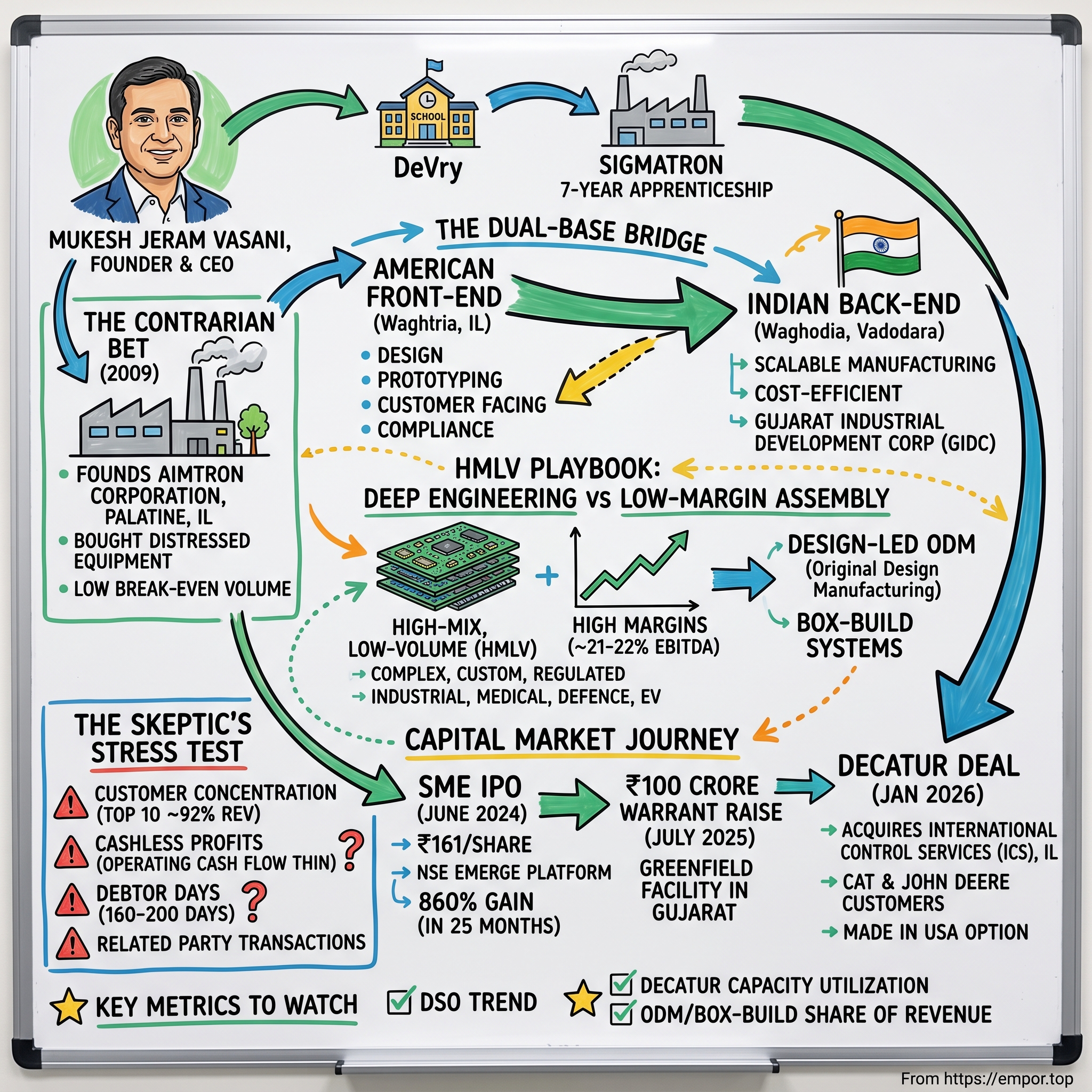

Start with a number that sounds like a typo. A share of Aimtron Electronics that a retail investor bought in the initial public offering in June 2024 for ₹161 traded, two years later, at roughly ₹1,389 — and touched an intraday peak of about ₹1,480 the day before this article was written.12 That is an 860% gain in twenty-five months, on a company most professional fund managers in Mumbai had never heard of before its listing, operating on the junior "SME Emerge" platform of the National Stock Exchange where the average daily volume can be a rounding error.

Now hold that number next to the man at the center of the story. Mukesh Jeram Vasani was, by the company's own telling, born in 1964 into a farming family in Gujarat, trained as a civil engineer, and did not arrive in the United States until his late thirties. He worked Chicago construction, then went back to school — at DeVry, a for-profit technical institute better known for late-night television advertisements than for minting industrialists — to study electronics.3 In 2009, at the very bottom of the Global Financial Crisis, when American contract manufacturers were being liquidated for parts, he founded a small electronics assembly shop in Palatine, Illinois, and bought distressed, high-precision equipment at cents on the dollar.3 Seventeen years later that shop is one leg of a company the Indian public market values at roughly ₹2,864 crore.2

This is a genuinely improbable story, and it sits inside a genuinely large one. The macro backdrop is the structural re-wiring of the global electronics supply chain — the industry the Indian government calls Electronics System Design and Manufacturing, or ESDM. Two forces are pushing work toward India at once: New Delhi's "Make in India" subsidy architecture, and the quieter corporate scramble that Western manufacturers call "China+1" — the desire to hold at least one supply source outside China after the tariff and pandemic shocks of the last several years. Aimtron is a very small boat riding a very large wave, and the interesting question is whether it is riding the wave or merely being carried by it.

It is worth being concrete about how large that wave is, because it explains why a company this small can command the attention it does. For two decades India talked about becoming an electronics manufacturing power and mostly imported its electronics from China instead. Then three things shifted at once. New Delhi threw real money at the problem — production-linked incentive schemes that pay manufacturers to make components and finished electronics on Indian soil, turning "Make in India" from a slogan into a subsidy line. The pandemic and the subsequent tariff wars taught every Western procurement officer a lesson their spreadsheets had ignored: a supply chain concentrated in a single country is a single point of failure, and "China+1" went from prudent to mandatory. And India's own electronics consumption climbed, giving domestic manufacturers a home market to scale against. The result is one of the genuine structural growth stories in global manufacturing — and a flood of capital hunting for any listed vehicle with a credible claim on it. That flood is part of why an obscure SME-platform stock could be repriced eight-fold; the tide lifted the whole harbour, and the analyst's job is to work out how much of Aimtron's ascent is the boat and how much is the tide.

Because Aimtron is not the wave. It is a niche player, and deliberately so. It does not stamp out millions of identical circuit boards for mobile phones the way the ESDM giants do. It has bet the company on the opposite strategy: High-Mix, Low-to-Medium Volume manufacturing — complex, custom, regulated electronics for industrial machines, medical devices, defence systems and electric vehicles, made in small batches at high margins. Whether that niche is a fortress or a trap is the debate this article will stage.

Here is the roadmap. First, the promoter's journey from a Gujarati village to a DeVry classroom to a distressed-asset auction in Illinois. Second, the "dual-base" architecture that bridges American design with Indian production. Third, the economics of the high-mix niche and why it prints margins that would embarrass a phone assembler. Fourth, the SME IPO and the ₹100 crore warrant raise that funded expansion. Fifth, the audacious January 2026 outbound acquisition of an American manufacturer serving Caterpillar and John Deere. Sixth — and this is where the neutrality earns its keep — the skeptic's stress test: customer concentration, receivables that take half a year to collect, and a web of related-party transactions with the founder's own American company. Then the competitive powers, the bull-versus-bear debate, and the handful of numbers that will actually tell you whether the story is working. We begin, as origin stories should, with the founder and a crisis.

II. The Promoter's Journey: From Gujarat Fields to DeVry and Chicago

Every founder myth has a moment of reinvention, and Vasani's arrived improbably late in life — in a classroom, surrounded by students half his age. Picture a man already into his late thirties, an immigrant with a civil engineering background and a construction job in the Chicago suburbs, deciding that the career he had crossed an ocean to build was the wrong one. According to the company's account, he trained originally as a civil engineer in Gujarat and moved to the United States around 2002–2003, drawn by the entrepreneurial gravity of America rather than by any particular plan.3 The plan, when it came, was a bet: that the future belonged to electrons, not concrete.

So he enrolled at DeVry in Illinois to earn an electronics education, and — this is the part that matters — he did not treat it as a credential to frame on a wall.3 He went to work inside the industry he was studying. Public records of his career show stints at Chicago-area electronics firms, including a period at contract manufacturer SigmaTron International, where a person learns the unglamorous physics of the trade: how solder paste flows, how a Surface Mount Technology line places thousands of microscopic components per hour, how a single misaligned resistor can fail a board six months into a customer's product cycle.3 Vasani has said in interviews that he spent roughly seven years learning the commercial and technical realities of electronics assembly before striking out on his own.3 That apprenticeship is easy to skip past in a highlight reel, but it is the whole foundation of the business. Contract electronics is a discipline where reputation is earned one qualified board at a time, and Vasani spent the better part of a decade earning the right to be trusted with someone else's product.

What the trade actually involves

It is worth pausing here to explain what that trade actually involves, because the whole investment case turns on why it is hard. A printed circuit board — the green sliver you would find inside any electronic device — is the nervous system of a product: a slab of insulating material laced with copper pathways onto which dozens or hundreds of tiny components are mounted. Surface Mount Technology is the automated process of placing those components — some of them smaller than a grain of sand — onto the board with micron-level precision, then baking the assembly in a reflow oven so the solder melts and sets in exactly the right places. Get it slightly wrong and the board might still power on, pass a cursory test, and then fail in the field months later when a bad solder joint cracks under vibration or heat. That gap between "looks fine" and "is reliable" is the entire value proposition of a serious contract manufacturer. Anyone can buy the machines. Knowing how to run them so that a board survives a decade inside a tractor or an operating theatre is the craft, and it is not written down in a manual — it is accumulated, expensively, through years of scrap and failure analysis. Vasani spent his forties acquiring exactly that tacit knowledge.

There is a second, quieter part of the apprenticeship that mattered as much as the technical one: he learned the commercial physics of a brutal business. Contract electronics manufacturing is structurally unforgiving. You buy expensive components up front, you carry them as inventory, you assemble them, you ship, and then you wait — often for months — to be paid, all while your customer holds the leverage of a relationship you cannot afford to lose. Margins are thin unless you climb into complexity. Vasani watched, from the inside, how the firms that survived were the ones that either achieved enormous scale or retreated into difficult, defensible niches where price was not the only variable. He would build his own company on the second strategy, and the choice was not a hunch — it was the considered conclusion of a man who had already seen the alternative up close.

The contrarian bet of 2009

Then came the contrarian move that the company treats as its founding legend. In 2009 — the year the Western financial system was still smoldering, when order books were collapsing and electronics shops across the American Midwest were shutting down — Vasani founded Aimtron Corporation in Palatine, Illinois.3 The timing looks reckless until you understand the logic. A recession is a terrible time to sell electronics and a wonderful time to buy the machines that make them. High-end SMT lines that cost hundreds of thousands of dollars new were being auctioned out of bankrupt competitors for a fraction of that. Vasani, with limited capital, bought precision equipment from distressed liquidation sales — acquiring a capital base at prices that would have been unthinkable eighteen months earlier or later.

What did that buy him, strategically? A cost structure. When you acquire your core assets at a deep discount, your depreciation and your break-even volume are permanently lower than a rival who bought at the top of the cycle. Every unit that comes off a machine you bought for a tenth of its list price carries a fraction of the fixed-cost burden that weighs on a competitor still paying down equipment financed at the peak. It let a tiny start-up credibly serve demanding customers. And crucially, it let Aimtron plant itself in a specific, defensible corner of the market from day one: low-volume, high-compliance manufacturing for local American industrial and medical companies that needed high-reliability printed circuit board assemblies — PCBAs — made close to home rather than shipped from Shenzhen.3 That is not a glamorous niche. It is a sticky one. A medical-device maker that has qualified a supplier through months of testing does not re-shop the contract to save three cents a board.

The choice of niche also reflected a reading of American manufacturing anxiety that would only deepen over the following decade. Even in 2009, a category of US customer existed that was uneasy about offshoring its most sensitive electronics — the defence contractor barred by regulation, the medical firm terrified of a supply chain it could not audit, the industrial company that had been burned once by a quality escape from a distant supplier and swore never again. For those buyers, "local and reliable" beat "cheap and far away." Aimtron positioned itself precisely in that psychological gap: near enough to visit, small enough to care, disciplined enough to pass the audits. It was a modest business — a job shop with good machines — but it was pointed at exactly the customers who would prove least willing to leave. In hindsight, the geopolitical winds of the 2020s, with their tariffs and their supply-chain nationalism, would blow directly into those sails. But that was luck layered on top of a sound instinct, and it is worth keeping the two separate.

The lesson Vasani would later repeat — and that we will test against his actual capital-allocation record in the sections that follow — is that crises are when contrarians buy. It is a genuinely useful principle. It is also, worth noting up front, the kind of principle that is far easier to celebrate in a founder's origin story than to execute repeatedly with other people's money. Having built a beachhead in Illinois, Vasani's next move was the one that turned a local job-shop into something structurally more interesting: he went home to Gujarat.

III. Building the Dual-Base Bridge: Vadodara Meets Palatine

In 2011, two years after the Palatine shop opened its doors, Vasani incorporated Aimtron Electronics Private Limited in Waghodia, an industrial belt on the outskirts of Vadodara in Gujarat.[^4] On paper it was a second factory. In strategy terms it was the whole thesis. The move created what the company calls its "dual-base" model, and it is worth slowing down to explain, because everything Aimtron claims about its margins and its moat ultimately rests on this one architectural choice.

The idea is a division of labor across two continents, each doing what it is structurally best at. The American entities — Aimtron Corporation and, later, Aimtron Electronics LLC — sit where the customers are. They function as the customer-facing front end: design consultation, rapid prototyping, regulatory and compliance work, and the hand-holding that industrial and medical clients demand when they are entrusting a partner with a mission-critical board. The Indian facilities — Waghodia and Vadodara, and later a design and engineering presence in Bengaluru — provide the scalable, cost-efficient manufacturing muscle.[^4] The slogan the company uses for this, and slogans are worth quoting precisely because they reveal what management wants you to believe, is "American quality with Indian cost structures and talent."

Think of it as a relay race. The baton — a customer's product idea — is picked up in Illinois, where the language, the time zone, the engineering conversation and the compliance regime all match the client's world. It is handed off across the ocean to Gujarat, where the same board can be built at a labor and overhead cost a fraction of the American equivalent. For a certain kind of customer — a mid-sized US industrial firm that wants the reassurance of a domestic partner but the economics of an offshore one — this is a genuinely attractive proposition. It is also the structural reason Aimtron can plausibly claim margins well above a pure Indian contract assembler: it captures the front-end value in dollars while paying the back-end cost in rupees.

Why Gujarat specifically, and why Vadodara? The choice was not sentiment, though sentiment surely played a part for a founder returning to his home state. Gujarat has spent two decades cultivating itself as India's most industry-friendly state — organized industrial estates, reliable power, a business culture and political apparatus oriented around manufacturing, and a diaspora that funnels both capital and orders back home. Waghodia, where Aimtron built, sits inside the Gujarat Industrial Development Corporation belt outside Vadodara, a mid-sized industrial city with an engineering-college pipeline feeding a steady supply of technicians at wages a small fraction of the American equivalent. The dual-base model, in other words, was not just "America plus a cheap country." It was America plus a specific, deliberately chosen manufacturing ecosystem where a mid-sized firm could get power, people and permits without the frictions that plague industry elsewhere in India. The geography is part of the strategy.

There is a subtlety in the dual-base model that a careful reader should not miss, because it is where the beauty and the danger both live. The two "bases" are not arm's-length strangers transacting in a market; they are entities under common family control, moving product and value back and forth across a border and a tax regime. When the American front end books an order and the Indian back end fulfils it, the revenue, the margin and the receivable have to be split between two related companies — and the way that split is drawn determines how much profit lands in the listed Indian vehicle that public shareholders own, versus the private American ones that the promoter owns outright. Done cleanly and at genuine arm's-length prices, the model is a legitimate engine of cross-border advantage. Done less cleanly, it is a mechanism through which value could, in principle, be steered. We will return to this in the stress test; for now, note only that the same structure that generates the margin also generates the governance question.

The 2016–2017 design pivot

But a factory that only builds to someone else's blueprint is a commodity, and commodities compete on price until the margin bleeds out. The most important strategic decision in Aimtron's history was the recognition of exactly this danger. Around 2016–2017, management began pushing the company up the value chain — away from "build-to-print" contract assembly, where the client hands over a finished design and you simply solder it together, and toward "design-led" original design manufacturing, or ODM.[^4] The company established an Aimtron design studio in Illinois and began doing the genuinely hard, sticky work: designing the circuits themselves, writing custom firmware, and engineering complete "box-build" systems — not just the bare board, but the entire finished electronic product inside its enclosure.

Why does this matter so much? Because design is where switching costs are born. When a customer merely rents your assembly line, they can leave whenever a cheaper line appears. When your engineers have designed the customer's product — know its firmware, own the test jigs, hold the tribal knowledge of why version three failed and version four didn't — leaving becomes expensive, slow and risky. The move from assembler to designer is the move from vendor to partner, and it is the single most important thing to watch in judging whether Aimtron has a real business or a rented one. It also, not coincidentally, lifts the margin. The question of exactly how much, and how durable that margin is, takes us into the economics of the niche itself.

IV. The HMLV Playbook: Deep Engineering vs. Low-Margin Assembly

To understand why Aimtron chose the road it did, you have to understand the fork in the road — and to do that, meet the giant it deliberately refused to become. Dixon Technologies is the poster child of Indian electronics manufacturing: a company that assembles millions upon millions of mobile phones, televisions and washing machines. It is a magnificent volume machine. It is also, by the brutal logic of its own business, a low-margin one — high-volume, low-mix assembly typically runs at operating margins in the low-single-digit range, because when you are making millions of identical units for brand-name customers, those customers have the leverage, the product is commoditized, and every rupee of cost is negotiated to the bone.

Aimtron went the other way, into the arena the industry calls High-Mix, Low-to-Medium Volume — HMLV. Instead of a million identical boards, picture a few hundred of one design, then a changeover, then a few hundred of another: complex, custom electronics for industrial automation, agricultural technology, medical devices, electric vehicles and defence.4 Every one of those end-markets shares a defining trait — the customer cannot afford failure. A ventilator, a tractor's engine controller, a missile subsystem: these are products where a field failure is a catastrophe, not an inconvenience. That fear is Aimtron's business model.

Here is the economic magic of HMLV, and why the margins look so different. First, engineering complexity — you are paid for difficulty, and difficulty resists price competition. Second, frequent line changeovers — the constant re-tooling that makes high-mix work operationally painful is exactly what keeps the commodity giants out, because their entire cost advantage depends on never stopping the line. Third, and most powerfully, regulatory qualification. To make boards for aerospace and defence you need certifications like AS9100; for medical devices you need ISO 13485; and the process of getting a specific product qualified with a specific customer can take twelve to twenty-four months of testing. That long qualification cycle is a moat with a drawbridge that takes two years to lower. The result: Aimtron has reported EBITDA margins in the low-twenties percent range — a different universe from the low-single-digits of the volume assemblers.5

Two factories

A useful way to feel the difference is to compare two imaginary factories. Factory A makes ten million identical phone chargers a year for a single global brand. Its lines never stop, its component costs are negotiated in bulk, its yield is optimized to the fourth decimal place — and its customer, who could move the contract with a phone call, keeps the price pinned a whisker above cost. Factory A survives on volume and operational perfection, and one lost contract can hollow it out. Factory B makes four hundred controllers for a mining-equipment maker, then re-tools and makes two hundred boards for a ventilator company, then re-tools again for a defence radio. Every changeover costs time; every product carries its own certification burden; nothing benefits from economies of scale. And yet Factory B earns five or six times Factory A's margin, because each of its customers is locked in by qualification, and none of them can find a dozen alternative suppliers willing to do work this fiddly. Aimtron chose to be Factory B. The bet is that in a world obsessed with scale, the profitable ground is the ground scale cannot reach.

But — and independent analysis has to keep saying "but" — the HMLV model carries its own curse, and it is not the one the sales deck emphasizes. Precisely because there are no economies of scale, growth does not get cheaper as you get bigger. Doubling revenue means roughly doubling the working capital tied up in components and half-built boards, and it means winning and qualifying a fresh cohort of customers rather than simply running the existing lines harder. The volume assembler's nightmare is losing a contract; the HMLV specialist's nightmare is choking on the cash needs of its own success. Hold that thought. It is the hinge on which the entire second half of this story swings.

Now, the honest caveat, because this is where independent analysis has to push back on the sales pitch. Aimtron did not invent this playbook, and it is not the only one running it. On the main board of the Indian exchanges sit a cluster of far larger HMLV specialists — Kaynes Technology, Syrma SGS, Avalon Technologies, Centum Electronics — all chasing the same high-reliability, high-margin verticals, all with more capital, longer track records and deeper customer rosters. Aimtron's roughly ₹300 crore of FY26 revenue is a fraction of what those companies turn over. The niche is real; Aimtron's ownership of it is not exclusive.

The comparison is worth dwelling on, because it reframes what Aimtron actually is. Kaynes and Syrma are multi-thousand-crore revenue companies with diversified plants, marquee customer lists and the balance-sheet heft to fund years of working-capital-intensive growth from a position of strength. Avalon brings a similar US-plus-India design-led footprint to Aimtron's own, and Centum has decades in defence and aerospace electronics. Against that field, Aimtron is not a category leader; it is an ambitious minnow that has picked the same fishing ground as several sharks. Its differentiators — the founder's genuine American operating history, the cross-border cultural fluency, the willingness to buy an American plant outright — are real and unusual for its size. But "real and unusual for its size" is a very different claim from "structurally advantaged against larger rivals." An investor paying more than sixty times earnings is implicitly betting that the minnow grows into the pod, and that is a bet about execution and capital, not about an unassailable moat. The rest of this article is, in a sense, an examination of whether that bet is reasonable.

The internal mix reveals where the company is trying to go. By its own account, the bulk of revenue still comes from PCBA — the core board-assembly work — with the higher-value box-build business (integrating a full electronic system) growing as a share, and front-end design and engineering a small but strategically outsized sliver.4 Notably, at the time of the IPO prospectus, PCBA accounted for the overwhelming majority of sales — around 88% in the 2023 period — so the "shift to box build and design" is a direction of travel management is steering toward, not a destination it has reached.6 By end-market, industrial automation is the anchor, with automotive and EV components the second pillar, and the remainder spread across power, medical, gaming and defence.4 The strategic push toward box-build is the whole game: it locks customers in deeper and it lifts the blended margin. Whether Aimtron can execute that shift faster than four better-capitalized rivals is an open question — and answering it costs money, which is where the capital markets enter the story.

V. The SME Listing & Raising the ₹100 Crore War Chest

On June 6, 2024, Aimtron Electronics listed on the NSE's SME Emerge platform, and the market's reaction told you something about the moment as much as the company. The IPO had been priced at ₹161 per share, a book-built issue of roughly ₹87 crore that the company earmarked for the unglamorous trinity of Indian growth-company finance: repaying debt, buying plant and machinery, and feeding the working-capital furnace.16 The shares opened for trading at ₹241 — a listing-day pop of nearly 50% before the business had proven anything at all as a public company.[^8]

That opening pop is a window into a peculiar corner of the Indian market. The SME platforms — junior boards designed to let small companies raise public capital with lighter listing requirements — became, over 2023 and 2024, an arena of extraordinary retail and high-net-worth frenzy. Issues were subscribed dozens or hundreds of times over; a decent business with a China+1 or defence or electronics story attached could be re-rated to multiples that would make a main-board analyst wince. Some of this reflected genuine hunger for exposure to India's manufacturing renaissance. Some of it was the ordinary mania of a bull market finding its most speculative expression in its least liquid, least scrutinized corner. Aimtron listed into that weather. It is important to separate the quality of the business from the temperature of the market that repriced it, because the second can reverse far faster than the first.

A word on what the SME Emerge platform actually is, because it materially shapes the risk. It was created to give genuinely small companies a lighter-touch route to public capital than the main board's exacting requirements — smaller minimum ticket sizes, less onerous continuous-disclosure obligations, and a shallower pool of institutional scrutiny. The trade-off for investors is thinner liquidity, lighter analyst coverage, and a shareholder base tilted toward retail and high-net-worth punters rather than long-horizon institutions. In a rising market that structure can be intoxicating: a small float plus a good story plus limited supply of stock equals violent upward re-ratings. In a falling market the same mechanics work in reverse, and a thinly traded SME stock can gap down with brutal speed when the crowd tries to leave through a narrow door. The regulator, the Securities and Exchange Board of India, spent 2024 and 2025 visibly tightening the screws on SME listings after a run of froth and a handful of governance scandals, adding scrutiny to fundraises and migrations. None of this is specific to Aimtron. All of it is part of the weather any SME-platform shareholder is standing in.

There is a genuinely interesting strategic tell in how Aimtron chose to finance its next leg of growth, and it rewards close reading. Most companies at this stage would either wait to migrate to the main board — where valuations are richer and capital is deeper — or launch a conventional follow-on offering open to all shareholders. Aimtron did neither.

And reprice it the market did. Over the twenty-five months following the listing, the stock climbed from ₹161 to roughly ₹1,389, peaking near ₹1,480 in mid-July 2026 — an 8.6-fold move.2 That ascent lifted the market capitalization to around ₹2,864 crore against a company that reported ₹301 crore of revenue, placing it at a trailing price-to-earnings multiple north of 60 times.2 Those are not the valuation coordinates of a sleepy job-shop. They are the coordinates of a stock in which the market has priced years of flawless execution in advance — a point that will matter enormously when we weigh the bear case.

The warrant issue

The more revealing capital-markets decision came in July 2025, and it says something about how management thinks. Rather than wait to migrate to the main board or tap a conventional follow-on, the board approved raising about ₹100 crore through preferential convertible warrants — up to 14.79 lakh warrants priced at ₹666 each, convertible into equity.7 Two features stand out. First, the promoter group — Mukesh Vasani and Nirmal Vasani among them — subscribed directly, putting their own capital in alongside outside investors.7 That is skin in the game, and it aligns incentives; the promoter group held roughly 70.9% of the company as of early 2026, with Vasani himself the dominant holder, and no pledged shares.4 Second, warrants are a specific instrument: the subscriber pays a fraction up front and the balance on conversion within eighteen months, which gives the company staged capital and the promoter optionality. It is a founder-friendly structure, and minority holders should understand it as such.

Where did the ₹100 crore go? Into bricks and SMT lines. The company announced a greenfield facility on a three-acre plot adjacent to its existing Waghodia unit, to be fitted with additional high-end SMT lines and end-to-end assembly capacity, aimed squarely at scaling the box-build business the strategy depends on.7 Placing the new plant next door to the existing one is a small but telling operational choice — it lets Aimtron share utilities, management and skilled labour across the two sites rather than starting cold in a new location, and it concentrates the company's manufacturing brain in one industrial cluster. The stated purpose is capacity for larger box-build programmes: energy-storage systems, EV chargers, robotic assemblies — precisely the bulkier, higher-value system-level work that a bare PCBA line cannot handle.[^4] In other words, the greenfield spend is not just "more of the same"; it is capital pointed at the mix-shift the entire margin thesis depends on.

Doubling capacity is a rational move for a company whose order book was growing faster than it could build. But raising equity-linked capital to fund working capital and capacity, only a year after an IPO that did the same, also foreshadows the balance-sheet tension at the heart of the bear case — a company adding SMT lines it cannot yet self-finance, on the promise that the resulting orders will one day convert to cash. First, though, management did something far more ambitious with its new war chest than pour a factory floor. It went shopping in America.

VI. The Decatur Deal: A $17 Million High-Stakes Outbound Acquisition

The announcement, in late January 2026, had the flavor of a role reversal that would have seemed absurd a generation ago: a Gujarat-based small-cap, barely eighteen months public, buying an American factory that supplies Caterpillar and John Deere.8 Through its US subsidiary Aimtron Electronics LLC, the company agreed to acquire International Control Services, Inc. — ICS — of Decatur, Illinois, an ESDM and ODM operation running a 58,000-square-foot plant on roughly 3.9 acres.8[^11] For a company that reported FY25 revenue of about ₹159 crore, planting a flag on a Midwestern factory floor was a statement of intent bordering on audacity.

What was actually paid

The financials of the deal deserve careful, neutral handling, because the public numbers are not fully consistent and an honest analyst should say so. What is clear is that ICS was a business generating roughly US$16.9–17 million in annual revenue at the time of purchase.89 The headline figure widely attached to the transaction is "$17 million," but that number describes ICS's revenue, and at least one account reported the actual cash consideration as materially lower — under ₹75 crore, or roughly US$8 million — with a US$4.3 million debt component in the financing.9 Management framed the funding as a blend of the July 2025 warrant proceeds, internal accruals, and that debt.[^11]9 The precise purchase price and the multiple paid are, in the disclosures available, not stated with the clarity a minority investor would want — and that ambiguity is itself worth filing away, because the difference between paying $8 million and $17 million for the same business is the difference between a bargain and a full price.

What the deal buys strategically is easier to assess. First, an instant customer roster in North American agrotech and heavy engineering — active accounts with Tier-1 original equipment manufacturers including Caterpillar and John Deere, the kind of relationships that take years to build from scratch.8 Second, a ruggedized-electronics capability and an American manufacturing footprint that, in an era of tariff anxiety, gives Aimtron's customers a domestic "Made in USA" option to sit alongside its Indian cost base. Third, and most quantifiable, a stated integration plan: management said ICS was running at roughly 54% capacity utilization and set a target of about 90% over three years, aiming to lift the acquired revenue toward a US$25–30 million annual run-rate.8[^11]9 On the deal call, founder Vasani put it in terms of "clear three-year visibility," while chief operating officer Nirmal Vasani described the acquisition as a cornerstone of a "Glocal" strategy and a step toward becoming "a ₹1,000 crore global ESDM powerhouse."9

Take that Caterpillar-and-John-Deere point seriously, because it is the most valuable thing on the truck. Landing a Tier-1 account with a company like Caterpillar is not a sales achievement; it is a multi-year qualification ordeal, and a supplier that already holds those approvals owns something a competitor cannot simply outbid for. That is the genuine prize of buying an incumbent rather than building greenfield — you inherit the certifications, the tribal knowledge, the reference calls and the sheer institutional trust that took ICS years to accumulate. It also slots neatly into the tariff logic: a heavy-equipment OEM nervous about the cost and optics of imported electronics now has an Aimtron-owned option that stamps "Decatur, Illinois" on the box while drawing on Indian engineering and, potentially, Indian sub-assembly. If the dual-base model was about designing in America and building in India, the ICS deal adds a third node — building in America too, when the customer's politics demand it. On paper, that is a more complete cross-border machine than most companies ten times Aimtron's size can offer.

The "Glocal" and "₹1,000 crore powerhouse" language is worth flagging for what it is: aspiration, delivered in the register of a founder selling a vision. Against roughly ₹300 crore of FY26 revenue, a ₹1,000 crore ambition implies more than tripling the business, and the honest analytical move is neither to mock it nor to bank it, but to file it as a target against which management can later be measured. Founders who state numbers publicly are, at least, giving the market a yardstick. Whether the yardstick gets hit is the only thing that will matter, and the disciplined investor writes the target down and waits.

There is also a risk-radar dimension to Decatur that cuts in Aimtron's favour and deserves acknowledgment. Tariff policy has become one of the least predictable inputs in global manufacturing, and a company whose entire value proposition is "we build your electronics in India" carries an obvious exposure if Washington decides to tax that arrangement. Owning an American plant is a hedge against precisely that political risk — it gives Aimtron a domestic answer to a customer who wakes up to a new tariff schedule, and it converts a vulnerability into an option. That is genuinely thoughtful positioning, and it is more than most companies of this size bother to build. The cost of the hedge, of course, is that American manufacturing is expensive manufacturing: the Decatur plant does not enjoy the rupee cost base that makes the Indian operation profitable, which is exactly why its margins depend so completely on filling that idle 46% of capacity.

Here is where a skeptic sharpens the pencil. The bull case for the deal is a multiple arbitrage that sounds almost too good: buy a profitable American manufacturer at a single-digit EBITDA multiple, fold its earnings into an Indian listed vehicle trading at more than 40 times EBITDA, and the same dollar of profit is instantly revalued many times over simply by changing which stock exchange it reports to. That arithmetic is real, and it is exactly why cross-border roll-ups can create value on paper. But it only works if two things hold: the acquired earnings are durable, and the promised utilization gains actually materialize. If ICS's 54% utilization does not climb — if the Caterpillar and John Deere volumes are cyclical rather than growing, or if integrating an American workforce and cost base proves harder than a slide deck implies — then Aimtron will have spent a meaningful chunk of its post-IPO capital on a low-return asset dressed up in a high-multiple stock. The re-rating logic cuts both ways: it magnifies good execution and it magnifies mistakes. Which brings us, unavoidably, to the parts of the story management would prefer to spend less time on.

VII. The Skeptical Investor's Stress Test: Customer Concentration & Cashless Profits

Every compelling growth story deserves a hostile cross-examination, and Aimtron's has three exhibits that a short-seller would put on the screen before saying a word. Take them in order, because together they describe a single underlying tension: this is a company whose income statement is far healthier than its balance sheet.

Exhibit one: concentration. According to the IPO prospectus, for the period ended September 30, 2023, Aimtron's top ten customers accounted for 92.46% of revenue from operations — and in prior years the figure was higher still, 96% in FY23 and 93% in FY22.10 Read that number slowly. Roughly nine in every ten rupees of revenue depended on ten relationships. That is the shadow side of the HMLV model: the same deep, sticky, hard-won engagements that create switching costs also create devastating fragility. If a single major client re-sources, hits financial trouble, or simply de-stocks in a downturn, Aimtron's growth does not slow — it can lurch. Switching costs protect you right up until the moment a customer decides to switch anyway, and concentration turns any single such decision into a corporate event. The company would argue the roster is diversifying as it scales; that is plausible and is precisely the sort of claim to verify against future disclosures rather than accept on faith.

Exhibit two, and the most important number in this entire article: the company earns profits it cannot yet turn into cash. The reported growth is genuinely spectacular — FY26 revenue rose about 89% to ₹301.2 crore and profit after tax climbed roughly 79% to about ₹46 crore, with the order book swelling around 176% to ₹521 crore.5 But look underneath the accrual accounting. Aimtron's debtor days — the average time it takes to collect cash after booking a sale — have run in the range of roughly 160 to 200 days; the prospectus-era figure was around 164 days.10 In plain English: the company waits more than half a year, on average, to be paid. Combine long receivables with the heavy up-front inventory and raw-component procurement that HMLV growth demands, and you get a working-capital cycle that swallows cash. Operating cash flow has historically been thin, negative, or barely positive even as reported profits soared — the classic signature of a business "growing out of money," where the faster you grow, the more cash you must feed into the machine before customers pay you back.

This is the real reason the equity raises keep coming. The IPO, then the ₹100 crore warrant issue, then debt to help fund the American deal — each is, in part, a way of financing a working-capital gap that rapid growth keeps widening. There is nothing inherently fraudulent or even unusual about this; it is the central financial challenge of nearly every fast-growing manufacturer. But it means the quality of Aimtron's profits is inseparable from the quality of its collections, and a minority shareholder is effectively betting that management can bring the cash-conversion cycle under control before dilution or leverage erodes the returns that all that growth is generating.

To see why this is the crux, run the mechanics slowly. Suppose Aimtron books a ₹100 sale in April. The profit lands in the April income statement, and the newspapers report a company growing 89%. But the ₹100 does not arrive in the bank until roughly October, and in the meantime Aimtron has already had to spend cash buying the components for the next order, which it hopes to collect the following spring. The faster it grows, the more of these overlapping six-month gaps it is carrying at once, and the larger the pile of cash it must source from somewhere other than customer payments. That "somewhere" is investors and lenders. This is why a business can be simultaneously highly profitable and chronically short of cash — and why, for a company like this, the single most revealing figure is not revenue growth or even margin, but the trend in the cash-conversion cycle. A skeptic would put it bluntly: until proven otherwise, treat the reported profit as an accounting event and watch the bank balance for the truth.

Exhibit three: the family on both sides of the table. Aimtron Corporation, the US entity Vasani founded in 2009, is not merely an affiliate — it has been a significant customer of the Indian listed company and is under common promoter control, making it a related party.6 When a founder's privately held American company buys product from the publicly held Indian one he controls, minority investors have to ask the uncomfortable questions: Are the transfer prices genuinely arm's-length? Are receivables from the related party collected on the same terms as from arm's-length customers, or are they a place where cash can quietly get stuck? These are not accusations; they are the standard diligence any concentrated, family-controlled, cross-border structure invites, and they are harder to answer from the outside precisely because so much of the value chain sits inside entities the public cannot see.

A second-layer diligence reader would add a few quieter flags to the file, none decisive but all worth a footnote in the mind. The reported growth has been accompanied by repeated recourse to equity-linked and debt financing, which is the balance-sheet tell of a business that cannot yet self-fund. The disclosure around the ICS purchase price was less than crisp, with the widely quoted "$17 million" describing revenue rather than consideration — the kind of ambiguity that is individually forgivable but collectively worth noticing in a company asking the market for a premium multiple. And the governance architecture is about as concentrated as it gets: a founder-chairman who is also the controlling shareholder, a family occupying the key executive seats, and a private overseas entity bearing the same name transacting with the listed one. Again, concentration is not wrongdoing. But it removes the friction that independent boards and dispersed ownership provide, and it places an unusually heavy weight on trusting the founder — which is exactly why his behaviour over time, not his slogans, is the thing to track.

So how should one weigh management's credibility? Fairly — which means holding the positives and the concerns in the same hand. On the positive side: the promoter owns roughly 70.9% with zero pledged shares, keeps standalone debt conservative, and has executed the stated HMLV-to-box-build roadmap with visible commercial traction.45 On the concerning side: a pattern of raising capital and pivoting aggressively — into a US acquisition — barely a year after listing, receivables that management has repeatedly signaled it will improve, and a governance structure concentrated almost entirely within one family. None of this is disqualifying. All of it is material. The honest verdict is that the numbers on the income statement have, so far, outrun the questions on the balance sheet — and the investment case rests on whether that stays true. To judge that, it helps to step back and ask what, if anything, actually protects this company.

VIII. Strategic Moats: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the growth rates and the founder story, and the question an investor is really trying to answer is durability: when a competitor with more money decides to take Aimtron's customers, what stops them? Two analytical frameworks help war-game the answer — Hamilton Helmer's 7 Powers and Michael Porter's five competitive forces — and applied honestly, they yield a mixed verdict rather than a flattering one.

Start with the power Aimtron possesses most convincingly: switching costs. This is the genuine article. In high-reliability HMLV, a customer's board is not a purchase; it is a marriage. Qualifying a supplier for a defence or medical or heavy-industrial product means twelve to twenty-four months of testing, the development of bespoke test jigs, and formal regulatory certification under regimes like AS9100 or ISO 13485. Once Aimtron's design-led box-build is embedded inside an industrial machine or a ventilator, ripping it out to save a few percent on unit cost means re-qualifying, re-testing, re-certifying — months of risk and expense for a trivial saving. That is a real moat, and it is the single strongest pillar under the stock. The catch, already noted, is that the same mechanism produces the customer concentration that is the company's biggest vulnerability. The moat and the risk are the same wall.

The second claimed power is what Helmer would call a cornered resource, and here the assessment has to be more skeptical. Management's implicit argument is that the Vasani family itself is the scarce asset — a genuinely bicultural bridge, rooted in suburban Illinois while maintaining manufacturing and local relationships in Gujarat, an operating model rare among mid-sized firms. There is something to this; cross-border trust and dual-jurisdiction fluency are not easily hired. But a "cornered resource" that is really just the founder's personal network is also a key-man risk wearing a nicer suit. It does not obviously survive succession, and it is not defensible in the way a patent or an exclusive supply contract would be. Call it an advantage, not a fortress.

The third is counter-positioning — Aimtron's bet that the volume giants structurally cannot follow it into low-volume custom work without wrecking their own economics. This is largely correct as against a Dixon or a Foxconn, whose entire cost advantage depends on long unbroken production runs; they would poison their own model by chasing high-mix crumbs. A giant optimized for making a million identical units cannot suddenly become nimble at making four hundred bespoke ones without dismantling the very discipline that makes it a giant — and its shareholders would revolt at the margin drag. That asymmetry is genuine. But counter-positioning offers no protection at all against the peers who are already in the same niche — Kaynes, Syrma SGS, Avalon, Centum — and who are better capitalized. So the moat holds against the giants above and offers nothing against the rivals alongside. The powers Aimtron most conspicuously lacks are also worth naming, because their absence defines the ceiling: there is no economy of scale (the whole point of HMLV is that scale doesn't compound), no network effect, no brand power in any consumer sense, and no process power that a well-run competitor could not replicate. What remains is one strong wall — switching costs — and a founder's cross-border hustle. That is enough to build a good business. It is not obviously enough to defend a sixty-times multiple.

Porter's five forces sharpen the same picture into something closer to a warning. Bargaining power of buyers is very high — a direct consequence of that 92% concentration; a handful of large customers can and do dictate 180-day payment terms, which is the balance-sheet problem restated as a competitive fact. Bargaining power of suppliers is high — the active semiconductor components Aimtron buys are controlled by a small number of global chipmakers and distributors, over whom a ₹300-crore company has essentially no pricing leverage, as the shortages of recent years painfully demonstrated. Competitive rivalry is high — the same four listed peers, all expanding capacity into the same China+1 tailwind. The forces that are muted — the threat of new entrants is dampened by those qualification barriers, and there is no real substitute for a qualified PCBA — are the ones that align with the switching-cost moat. The overall reading: Aimtron sits in an attractive industry with one strong, narrow moat, squeezed between powerful customers and powerful suppliers, and running hard against well-funded peers. That is a defensible position, not a dominant one — and the distinction is exactly what the bull and bear cases fight over.

IX. The Bull vs. Bear Debate: Rerating vs. Working Capital Traps

Put two sophisticated investors in a room over this stock and they will not disagree about the facts — they will disagree about which facts matter. Here is the argument, made as strongly as the evidence allows on each side.

The bull case rests on momentum that is genuinely hard to dismiss. FY26 revenue grew about 89% to ₹301.2 crore, and — more telling than any single year's revenue — the order book jumped roughly 176% to ₹521 crore, about 1.7 times the year's sales, with management citing wins in defence, exports, IoT and AI-adjacent industrial platforms.5 An order book growing faster than revenue is the closest thing manufacturing offers to a leading indicator, and it suggests the demand is real, not manufactured. Layer on the structural margin story: the shift toward design-led box-build has supported EBITDA margins around 21–22%, the kind of profitability that justifies a premium if it holds.5 Add the US acquisition, which — if the utilization plan works — brings blue-chip Western OEMs and a tariff-hedged American footprint. And hold in reserve the optionality of a migration from the SME platform to the NSE main board, an event that would open the stock to institutional investors currently barred from the junior board and could, on its own, drive a re-rating regardless of fundamentals. That is a legitimately exciting package.

There is a governance-and-disclosure overlay to the bull case that deserves its due as well, because it is not all rhetoric. The promoter group's roughly 70.9% stake with zero pledged shares is a genuine positive: a founder who has not borrowed against his own equity is not one wall of a margin call away from a forced sale, and heavy insider ownership aligns his fortunes with minority holders'.4 The direct promoter participation in the warrant issue points the same way. And the order-book disclosure, quarter after quarter, has given investors a forward metric to hold management to — a discipline many small-caps avoid. These are the behaviours of a management team that, so far, has done roughly what it said it would.

The bear case rests on the one thing the bull case cannot conjure away: cash. The chasm between reported profit and operating cash flow is the whole argument. If debtor days do not fall from their 160–200 range, the company must keep feeding the working-capital machine from external sources — meaning more dilution or more debt — and every such raise chips at the per-share value the growth is supposedly creating. Concentration is the second blade: with the top ten customers at ~92% of revenue, the loss of even one or two marquee accounts would not dent the model, it would deform it. Third is integration risk in Decatur — if utilization stalls below the 90% target, the American bet curdles from a multiple-arbitrage triumph into an overpriced, low-return distraction; cross-border acquisitions by first-time acquirers have a long and unhappy history, and a company that has never before absorbed a foreign workforce is attempting exactly that. And fourth is valuation itself: a trailing P/E north of 60 on an SME-platform micro-cap prices in years of perfection, which means any stumble — a soft quarter, a receivables scare, an RPT question that lingers — could trigger a de-rating far more violent than anything the fundamentals alone would justify.2 Premium multiples are unforgiving landlords.

A short-seller or activist would press one more point, and it is the sharpest: the pattern of behaviour. A company lists on a junior board, raises money for working capital and machines, then within a year raises ₹100 crore more via a promoter-friendly warrant structure, then within months of that deploys capital and debt into an outbound US acquisition whose headline value is not cleanly disclosed — all while receivables sit at half a year and a related party sits inside the customer base. None of these facts alone is damning. Stacked together, they describe a management team moving fast, raising often, and expanding aggressively at exactly the moment it was promising discipline on collections. The activist's question is not "is this fraud?" — there is no evidence of that — but "is the capital being allocated with the care that a sixty-times valuation assumes?" That is a fair question, and the only honest answer today is that it is unproven in either direction.

The three numbers that settle it

Notice that the bull and bear are not really arguing about whether Aimtron is a good business. They are arguing about the gap between accounting reality and cash reality, and about whether a tiny company can institutionalize the disciplines — collections, integration, governance — that its founder-driven growth has so far outrun. That is why the whole debate collapses, usefully, into a very short list of things to watch. Three numbers will tell you which case is winning long before the headlines do.

The first is consolidated days sales outstanding — the cash-collection metric. If DSO trends down from the historical ~160–200 days, the bear's central thesis is weakening and the profits are becoming real cash; if it stays elevated or rises, no amount of order-book growth will matter. The second is capacity utilization at the Decatur plant — the single cleanest gauge of whether the American acquisition is being integrated or merely owned; the march (or stall) from 54% toward 90% is the referee of that bet. The third is the box-build and ODM share of revenue — the structural mix-shift from commodity assembly toward system integration and design, which is what the entire margin and switching-cost thesis is built on; if that share climbs, the moat is deepening, and if it flatlines near its historical PCBA-heavy mix, the premium is unearned. Everything else is noise around those three signals.

X. Epilogue & Playbook Lessons

Step back from the ticker and Aimtron reads less like a stock and more like a set of lessons about how mid-sized companies can — and cannot — punch above their weight.

The first lesson is the one Vasani has built his identity around: crises are capital-allocation opportunities. Buying distressed SMT lines in 2009 at cents on the dollar was not luck; it was a deliberate exploitation of a down-cycle to acquire a permanently lower cost base, and it is the reason a first-generation immigrant with limited capital could credibly serve demanding customers from day one. The durable insight is that the best time to buy productive assets is precisely when everyone else is forced to sell them. The caution, visible in the years since, is that the same contrarian confidence that builds a company from a liquidation auction can, at scale and with public shareholders' money, tip into a habit of aggressive expansion that the balance sheet struggles to fund.

The second lesson is the dual-presence arbitrage — the recognition that a company can win globally by disaggregating its value chain across geographies, placing the high-value, high-touch front end (design, compliance, customer intimacy) where the customers are, and the cost-sensitive back end (manufacturing) where the economics are. It is an elegant model, and the ICS acquisition is its logical culmination: Aimtron now designs in America, manufactures in India, and — increasingly — manufactures in America too when a customer's supply-chain politics require it. Whether that elegance survives the friction of integrating an American workforce and the scrutiny of related-party plumbing is the test the next three years will administer.

The third lesson is the hardest and the most universal: growth and working capital are a trade-off, not a free lunch. A company can report soaring revenue and rising profit and still be quietly starved of cash, because on paper a sale is booked the day it ships, while in reality the money arrives — if the model works — six months later. High margins on a spreadsheet are not the same as cash in the bank, and a fast-growing manufacturer that ignores the quality of its collections can grow itself straight into a liquidity crisis. Aimtron's entire investment case, stripped to its essence, is a wager that management can close the distance between its income statement and its bank balance faster than its own growth widens it.

There is a final lesson buried in the valuation, and it belongs to the buyer rather than the company: a great business bought at a great price and a great business bought at a punishing one are not the same investment. Nothing in Aimtron's operating story requires the stock to trade at more than sixty times earnings; that multiple was conferred by a particular market mood in a particular corner of the exchange, and it can be withdrawn as quickly as it was granted. The company's job is to keep collecting cash, integrating Decatur, and shifting its mix toward design — the operational work. The multiple is the market's mood about that work, and moods on thinly traded junior boards are famously fickle. Separating the quality of the enterprise from the price of the ticket is the whole discipline here, and the two have rarely been as far apart as the last two years made them.

So does the cross-border challenger scale into the ranks of India's elite main-board ESDM names, or does the working-capital gap and the concentration risk catch up with the multiple first? This article does not pretend to know. What it can say is that Aimtron is neither the effortless compounder its share-price chart implies nor the accounting mirage a reflexive skeptic might assume. It is a real business with a real, narrow moat, a real founder with a real track record, and a real balance-sheet vulnerability sitting underneath a very demanding valuation. Watch the three numbers — the days it takes to collect cash, the utilization of the American plant, and the share of revenue coming from design-led system integration. They will tell the story long before the story tells itself.

References

-

Aimtron Electronics IPO Date, Price, GMP, Review, Details — Chittorgarh ↩↩

-

Aimtron Electronics Ltd share price, About Aimtron, Key Insights — Screener.in ↩↩↩↩↩

-

Mukesh Vasani — Founder & CEO, Aimtron Corporation (career and DeVry background) — Crunchbase ↩↩↩↩↩↩↩↩

-

Aimtron Electronics promoters confirm no encumbrance on shares in FY26 — ScanX ↩↩↩↩↩↩

-

Aimtron Electronics Reports Strong FY26 Performance with Revenue Nearly Doubling Year-on-Year — ScanX ↩↩↩↩↩

-

Aimtron Electronics Limited — SME Issue Prospectus, June 2024 — SEBI ↩↩↩

-

Aimtron Electronics raises Rs 100 crore via warrant issue to set up greenfield facility in Gujarat — The Week, 2025-07-15 ↩↩↩

-

Aimtron Electronics Acquires US-Based ICS Company to Strengthen Global ESDM Capabilities — Autocar Professional, 2026-01 ↩↩↩↩↩

-

Aimtron Electronics Eyes $25-30 Mn Additional Biz from ICS Acquisition — Outlook Business, 2026-01 ↩↩↩↩↩

-

Aimtron Electronics IPO — customer concentration and debtor days (prospectus data) — Groww ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube