Authum Investment & Infrastructure Ltd: From NBFC Origins to Investment Powerhouse

I. Cold Open & Setting the Scene

Picture this: A company with a market cap of ₹48,864 crores, trading at ₹2,879 per share, that most investors have never heard of. Not because it's new—it's been around since 1982—but because for four decades, it operated in the shadows of India's financial system as just another non-banking financial company. Then, in a span of three years, it pulled off what industry veterans called impossible: acquiring two collapsed giants from Anil Ambani's empire for a combined ₹3,352 crores, resolving ₹20,000 crores in lender debt, and transforming itself into one of India's most aggressive investment machines.

The enigma of Authum Investment & Infrastructure Limited isn't just in its numbers—though a P/E ratio of 11.9 for a company delivering 209% profit CAGR over five years certainly raises eyebrows. It's in the audacity of its transformation. Here's a company that spent 40 years in the fund-based activities business—investing in shares, securities, mutual funds, and providing loans—then suddenly pivoted to become a specialist in acquiring and turning around distressed financial assets at a scale that made private equity firms nervous. The big question driving this narrative: What happens when you combine distressed asset acquisitions with strategic investments? The answer, as we'll discover, is a playbook that turned a sleepy NBFC into a financial engineering machine that even seasoned private equity firms now watch closely.

Recent moves show the company's continued aggression—in August 2024 alone, Authum increased its stake in Star Aerospace to 14.59% for approximately ₹112 crores, signaling its push into defense manufacturing. The company also formed a 99.99% owned sports subsidiary, Billion Dream Sports, showing diversification beyond financial services.

What we're about to unpack isn't just a corporate transformation story. It's a masterclass in timing, regulatory navigation, and the art of seeing value where others see only wreckage. As we dive into four decades of history, billion-dollar deals, and strategic pivots, we'll discover how a company most investors ignored until 2021 became one of the most intriguing stories in Indian finance.

II. Origins & The Pre-Transformation Era (1982-2020)

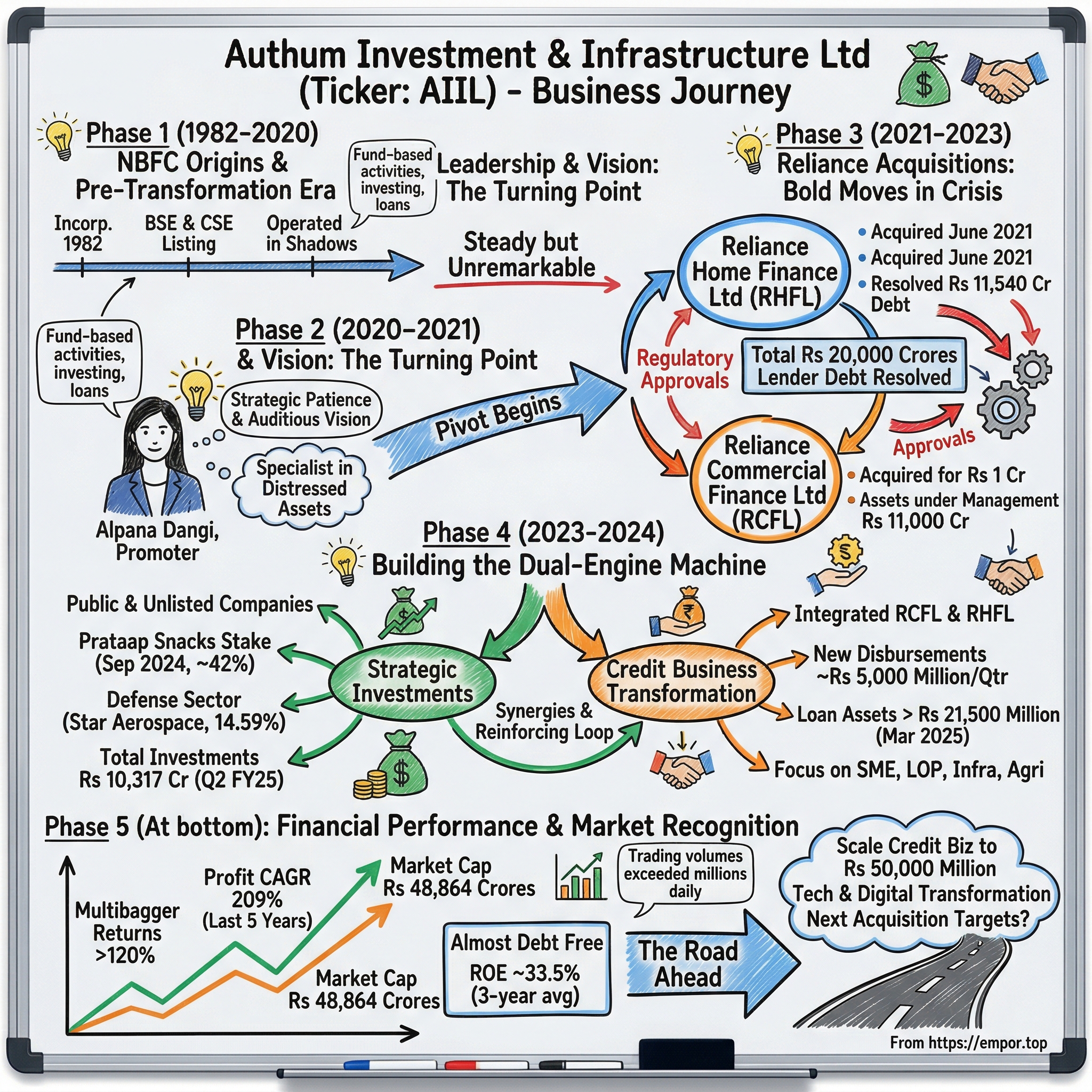

Incorporated on July 17, 1982, Authum Investment & Infrastructure Limited began its journey listed on the Bombay Stock Exchange and Calcutta Stock Exchange—back when India's financial markets were a fraction of their current size and sophistication. For context, this was the year SEBI didn't even exist yet; the stock market was still operating on physical share certificates, and the term "dematerialization" wouldn't enter the Indian financial lexicon for another decade and a half.

The company emerged during the tail end of the License Raj era, when starting any financial services business required navigating a labyrinth of permissions and regulations. It registered as a Non-Banking Financial Company (NBFC) with the Reserve Bank of India, positioning itself in what was then a niche corner of India's financial system. The NBFC sector in 1982 was vastly different from today—there were no prudential norms, no asset classification standards, and certainly no concept of systemically important NBFCs.

For nearly four decades, Authum operated in what can only be described as deliberate obscurity. The company carried on the business of investment in shares and securities and financing activities, but with a conservative approach that kept it far from the headlines. While peers like Bajaj Finance and Shriram Transport were building massive retail franchises and transforming into household names, Authum remained content with its traditional NBFC operations.

The India around Authum was transforming dramatically. The 1991 liberalization opened floodgates of foreign capital. The dot-com boom and bust came and went. The 2008 financial crisis shook global markets. Demonetization in 2016 reshaped India's financial landscape. Through all these seismic shifts, Authum maintained its steady, unremarkable course—investing in securities, providing loans, collecting interest, and distributing modest dividends to a small shareholder base that probably forgot they owned the stock.

What's striking about this period isn't what Authum did, but what it didn't do. It didn't chase the retail lending boom that made Bajaj Finance a multibagger. It didn't pursue the vehicle financing opportunity that built Shriram's empire. It didn't attempt to become a housing finance company when that sector was delivering astronomical returns. This wasn't necessarily poor judgment—it was simply a company content with its niche, operating without ambition to disrupt or be disrupted.

The company's classification as a non-deposit taking Systemically Important NBFC came much later, a regulatory designation that seems almost ironic given how unsystemic and unimportant it appeared to be for most of its existence. This designation, which applies to NBFCs with asset sizes above ₹500 crores, meant stricter regulatory oversight but also signaled a certain scale that would become crucial for what was to come.

By 2020, after 38 years of operations, Authum was the corporate equivalent of furniture—present but unnoticed. Its financials were unremarkable, its stock price moved in narrow bands, and analyst coverage was virtually non-existent. Trading volumes were thin, institutional ownership was minimal, and retail investors had likely never heard of it.

But beneath this facade of mediocrity, something was stirring. The company had been quietly building capital, maintaining clean books, and most importantly, keeping its regulatory record spotless—a detail that would prove invaluable when opportunity knocked. The four decades weren't wasted; they were preparation for a transformation that would shock everyone who thought they knew what Authum was about.

III. The Turning Point: Leadership & Vision (2020-2021)

The year 2020 brought more than just a pandemic to India's financial markets. It marked the beginning of one of the most audacious transformations in NBFC history, orchestrated by a figure who had been quietly repositioning pieces on the board: Mrs. Alpana Dangi, the company's promoter.

Alpana Dangi wasn't your typical NBFC promoter. While the financial press was obsessed with the likes of Uday Kotak and Ajay Piramal, Dangi operated with a different philosophy—one that valued strategic patience over public recognition. Her vision for Authum wasn't to compete in the crowded retail lending space but to become something entirely different: a specialist in complex financial restructuring and strategic investments.

The timing of this pivot was no accident. By 2020, India's financial sector was littered with the wreckage of over-leveraged companies. The IL&FS crisis of 2018 had triggered a liquidity crunch that exposed weak business models across the NBFC sector. The pandemic only accelerated this distress. While most saw crisis, Dangi and her team saw opportunity—specifically, the opportunity to acquire high-quality assets at distressed prices from sellers with no alternatives.

The strategic pivot began with a fundamental question: Why compete in commoditized lending when you can buy entire lending businesses at cents on the dollar? This wasn't just about being opportunistic; it required building capabilities that traditional NBFCs didn't have—legal expertise in complex restructuring, relationships with consortium lenders, understanding of bankruptcy law, and most importantly, the ability to move fast when opportunities emerged.

Internal transformation started with talent acquisition. Authum began recruiting professionals not from traditional NBFC backgrounds but from investment banks, private equity funds, and turnaround consulting firms. The company built teams specializing in due diligence, regulatory navigation, and post-acquisition integration. This wasn't publicized—Dangi understood that in distressed asset acquisition, the element of surprise is often the difference between winning and losing a deal.

Capital raising became the next priority. The company systematically strengthened its balance sheet, not through high-profile QIPs or preferential allotments that would attract attention, but through internal accruals and selective capital raises. The goal was to build a war chest large enough to pursue transformational acquisitions without being dependent on market conditions or external financing at the crucial moment.

The company also began studying potential targets with the intensity of a chess grandmaster analyzing opponents. The Anil Ambani group's financial services companies—Reliance Home Finance and Reliance Commercial Finance—were obvious candidates. Once jewels in the Reliance empire, they had become casualties of aggressive expansion, asset-liability mismatches, and the broader NBFC crisis. With combined debt exceeding ₹20,000 crores and operations virtually frozen, they were precisely the kind of complex, distressed situations that Authum was preparing to tackle.

What set Authum apart wasn't just the willingness to pursue these deals but the approach. While other bidders saw troubled NBFCs that would require massive capital infusion and years of restructuring, Authum saw embedded value in the form of lending licenses, existing customer relationships, and operational infrastructure that would cost billions to build from scratch. The calculation was elegant: pay a nominal amount for the equity, negotiate with lenders for debt resolution, and unlock value through operational turnaround.

By early 2021, the pieces were in place. The team was built, capital was ready, and targets were identified. What remained was execution—and that's where Authum would prove that four decades of quiet operation had been building toward something extraordinary. The company that nobody noticed was about to make moves that nobody would forget.

IV. The Reliance Acquisitions: Bold Moves in Crisis (2021-2023)

The conference rooms at Bank of Baroda's headquarters had seen many crisis meetings, but nothing quite like the summer of 2021. Authum was announced as the winning bidder for Reliance Home Finance Limited in June 2021, but the story of how they got there reads like a financial thriller.

The context was dramatic: RHFL's creditors, led by Bank of Baroda, were owed a total of Rs 11,540 crore. The company, once a crown jewel in Anil Ambani's empire, had collapsed under the weight of aggressive expansion and poor underwriting. Operations were virtually frozen, recoveries had plummeted, and traditional resolution mechanisms had failed. The Reserve Bank of India's June 7, 2019 framework for resolution of stressed assets had opened a path outside the bankruptcy courts, but nobody had successfully executed a deal of this magnitude. Authum's initial bid for RHFL proposed that lenders would receive Rs 2,887 crore along with the cash on RHFL's books—Rs 1,800 crore—with 90% paid upfront and the rest within a year. The audacity of the proposal wasn't just in the numbers but in the structure: Authum was essentially proposing to pay a fraction of the outstanding debt while convincing lenders this was their best option.

The negotiation drama that followed could fill a business school case study. The Securities and Exchange Board of India raised objections about the voting process, and the Shapoorji Pallonji Group filed a case that resulted in a stay on the distribution of funds. But the delay actually benefited lenders—loan recoveries in RHFL increased from Rs 1,600 crore to over Rs 3,000 crore during the waiting period.

Meanwhile, Authum was simultaneously pursuing Reliance Commercial Finance Limited with even more remarkable terms. On October 14, 2022, Authum acquired debt-ridden RCFL for just Rs 1 crore. Yes, you read that right—one crore rupees for an NBFC with assets under management of Rs 11,000 crore. The symbolism wasn't lost on anyone: this was less about the purchase price and more about the willingness to take on the complex task of resolution.

The regulatory hurdles were monumental. Both acquisitions required approvals from the Reserve Bank of India, SEBI, the Competition Commission of India, and ultimately, the Supreme Court of India. The Supreme Court allowed the resolution plan for RHFL to proceed, with dissenting debenture holders given the option to accept the terms or pursue other legal remedies. This wasn't just legal maneuvering—it was setting precedent for how distressed financial services companies could be resolved outside the bankruptcy courts.

The integration challenges were equally complex. A total of 30 banks led by Bank of Baroda, 40 institutional investors including mutual funds, and 20,000 retail investors were creditors of RHFL. Small investors with investments below Rs 5 lakh received 100% of their principal, while those above received 23%. This tiered approach to resolution showed Authum's understanding that protecting small investors was crucial for regulatory approval and public perception.

What made these deals truly transformational wasn't just their size but their implications. The two acquisitions were among the first successful resolutions of financial services entities outside the Insolvency & Bankruptcy Code process. The closure of these transactions resulted in resolution of approximately Rs 20,000 crore of consortium lender debt. For context, that's more debt resolution than most distressed asset funds achieve in a decade.

The operational turnaround began immediately. RCFL was rebranded as Reliance Money, retaining the brand equity while signaling new ownership. The company had helped create success stories for over 400,000 MSMEs and disbursed over Rs 88,000 crores to them. This wasn't a dead asset—it was a living, breathing business that just needed capital and management attention.

By March 2023, when the RHFL acquisition finally closed, Authum had pulled off what many thought impossible: acquiring two major NBFCs from the collapsed Anil Ambani empire for a combined Rs 3,352 crores, resolving Rs 20,000 crores in debt, and positioning itself as a major player in India's financial services sector. The quiet NBFC from 1982 had announced itself on the national stage with deals that would be studied in boardrooms and business schools for years to come.

V. Building the Investment Machine (2023-2024)

The dust had barely settled on the Reliance acquisitions when Authum revealed its true ambition: not just to be a turnaround specialist, but to build a dual-engine growth machine combining strategic investments with a revitalized credit business. This wasn't improvisation—it was the execution of a carefully crafted strategy that had been years in the making.

The investment philosophy that emerged was distinctive. While traditional NBFCs focused on lending and private equity firms chased high-growth startups, Authum positioned itself in the middle—a strategic investor with patient capital, operational expertise, and the ability to move quickly on complex opportunities. The company invests in publicly listed and unlisted companies, private equity investments, real estate investments, and debt instruments. It has also engaged in structured financing, fixed returns portfolios, secured lending, and equity investments in emerging companies. Total investments increased from Rs 3,186 Cr in FY22 to Rs 10,317 Cr as of Q2 FY25.The marquee deal that demonstrated this strategy was the acquisition of a 42.31 per cent stake in Prataap Snacks in September 2024. Working alongside investor Mahi Madhusudan Kela, Authum acquired 102.48 million shares of Prataap Snacks at Rs 746 per share, for a total consideration of approximately Rs 846.60 crore. The transaction triggered a mandatory open offer for an additional 26% of the company at Rs 864 per share.

What made this deal fascinating wasn't just the price—it was the strategic rationale. Prataap Snacks, with its Yellow Diamond brand and presence across 2.5 million touchpoints in India, represented a bet on consumption growth. But more importantly, it showed Authum's ability to partner with sophisticated investors like Kela and outbid traditional strategic buyers. The sellers—Peak XV Partners (formerly Sequoia India) and other PE investors—had been looking for an exit, and Authum provided the perfect combination of speed, certainty, and price.

The structured financing playbook that emerged was equally impressive. Authum wasn't just buying equity stakes; it was creating complex financial structures that provided steady returns while maintaining upside potential. The company engaged in secured lending to companies that traditional banks wouldn't touch, structured financing deals with embedded equity kickers, and fixed returns portfolios that provided stability to the overall investment mix.

Building these capabilities required more than just capital—it required institutional knowledge. The team that had successfully navigated the Reliance acquisitions now became the core of the investment machine. They understood how to evaluate distressed situations, how to structure deals that protected downside while capturing upside, and most importantly, how to move fast when opportunities emerged.

The portfolio diversification strategy was deliberate and methodical. While maintaining a core focus on financial services—where the company had deep expertise—Authum began exploring adjacent sectors. Real estate investments provided asset backing and steady yields. Private equity investments in emerging companies offered growth potential. Debt instruments provided predictable cash flows that could fund further acquisitions.

What set Authum apart from traditional investment companies was the synergy between its investment and credit businesses. The credit business provided steady cash flows and deep market intelligence about sectors and companies. The investment business provided capital appreciation and strategic optionality. Together, they created a flywheel effect—each business strengthening the other.

The numbers told the story of rapid scaling. Total investments increased from Rs 3,186 Cr in FY22 to Rs 10,317 Cr as of Q2 FY25—more than a threefold increase in just over two years. But this wasn't reckless growth; each investment was carefully evaluated, structured, and monitored. The company maintained strict investment criteria: focus on businesses with strong cash flows, look for situations where Authum's operational expertise could add value, and always maintain a margin of safety.

By the end of 2024, Authum had transformed from a company known for one or two big deals into a systematic acquirer with a proven playbook. The investment machine wasn't just running—it was accelerating, with each successful deal providing capital and credibility for the next one.

VI. The Credit Business Transformation

While the investment headlines grabbed attention, the transformation happening in Authum's credit business was equally remarkable—perhaps more so because it demonstrated the company's ability to not just acquire distressed assets but to turn them into growth engines.

As of March 31, 2025, the Credit Business had loans assets in excess of ₹21,500 million with a track record of fresh disbursements of at least ₹5,000 million per quarter. These weren't just legacy loans being collected; this was new business being written at a pace that would make established NBFCs take notice.

The foundation of this transformation was the successful integration of RCFL and RHFL's lending operations. Remember, these weren't just distressed portfolios—they were operational businesses with existing customer relationships, branch networks, and most importantly, lending licenses that would have taken years and significant capital to obtain organically.

RCFL, rebranded as Reliance Money, brought with it a robust SME lending franchise. The company had helped create success stories for over 400,000 MSMEs across the country and disbursed over Rs 88,000 crores to them. This wasn't a business that needed to be built from scratch—it needed to be revived, recapitalized, and redirected.

The product diversification strategy was comprehensive. The credit business now offered small and medium enterprise loans, loans against property, infrastructure financing, agriculture loans, and supply chain financing. Each product line was carefully evaluated for risk-return characteristics, and the company built specialized teams for underwriting and collection in each segment.

What distinguished Authum's approach was the focus on underserved segments where competition from banks and large NBFCs was limited. While everyone was chasing retail loans and housing finance, Authum focused on structured credit to mid-market companies, specialized financing for specific industries, and complex transactions that required deep understanding and quick decision-making.

The risk management framework evolution was perhaps the most critical aspect of the transformation. The failures at RHFL and RCFL had been primarily due to poor underwriting and inadequate risk controls. Authum implemented a completely new risk architecture: centralized credit approval for large exposures, sector-specific underwriting guidelines, early warning systems for asset quality deterioration, and perhaps most importantly, a culture that prioritized asset quality over growth.

The technology transformation was equally important. Authum invested heavily in digital infrastructure—not to compete with fintech startups in consumer lending, but to improve operational efficiency and risk management. Automated credit scoring for SME loans, digital collection platforms, and real-time portfolio monitoring systems were implemented across the business.

The results spoke for themselves. Fresh disbursements of Rs 5,000 million per quarter meant the company was originating Rs 20,000 million in new loans annually—a run rate that put it among the mid-sized NBFCs in India. More importantly, the asset quality metrics were strong, with NPAs kept well below industry averages through careful underwriting and proactive collection efforts.

The competitive positioning was unique. Unlike traditional NBFCs that competed on price or distribution, Authum competed on speed and flexibility. A mid-sized company looking for Rs 50 crores in structured financing could get a decision from Authum in days, not weeks. This speed, combined with the ability to structure complex transactions, created a defensible niche.

The synergies with the investment business were powerful. Information gathered from lending operations provided insights for investment decisions. Relationships built through lending opened doors for equity investments. And the steady cash flows from the credit business provided funding for opportunistic investments without dependence on external capital.

By 2025, the credit business had evolved from a distressed asset recovery operation to a thriving lending franchise. The transformation validated Authum's thesis that operational turnaround, not just financial engineering, could create value in distressed acquisitions. The credit business was no longer just a part of Authum's story—it was becoming the stable foundation on which more aggressive investment strategies could be built.

VII. Financial Performance & Market Recognition

The numbers tell a story that even skeptics find hard to ignore. In 2024, NSE:AIIL's revenue was 45.60 billion, an increase of 4.49%. Earnings were 42.41 billion. For a company that was virtually unknown three years ago, these figures represent not just growth but a complete metamorphosis.

The profit trajectory is even more remarkable. Company has delivered good profit growth of 209% CAGR over last 5 years—a growth rate that would be impressive for a startup, let alone a 40-year-old NBFC. This wasn't just financial engineering or one-time gains from acquisitions; this was sustained, operational performance improvement.

The quarterly results showed the consistency of execution. Q4 FY25 saw net profit rise 14.67% year-on-year to Rs 1,762.59 crore. Even in volatile quarters, the company maintained profitability and growth, demonstrating the resilience of its dual business model. When investment gains were lower, credit business filled the gap. When credit growth moderated, investment returns compensated.

Stock performance became the ultimate validation. The stock rose by more than 120% over the past year, recently reaching an all-time high near Rs 2,600. For context, the stock's lowest point was around Rs 730—representing a multibagger return for those who recognized the transformation early. Trading volumes, once negligible, now regularly exceeded millions of shares daily, indicating institutional interest.

The balance sheet transformation was equally impressive. Company is almost debt free—a remarkable achievement for a company that had just acquired two heavily indebted NBFCs. This wasn't just about paying down debt; it was about generating enough cash flow to fund growth while maintaining a fortress balance sheet.

Return metrics painted a picture of exceptional capital efficiency. The 3-year average ROE of 33.5% placed Authum among the most profitable financial services companies in India. For comparison, most NBFCs struggle to maintain ROE above 15%, and even the best rarely exceed 20% consistently. This wasn't just profitability—it was super-normal returns that suggested either exceptional execution or an unsustainable situation.

The market's evolving perception could be tracked through multiple metrics. Institutional ownership increased dramatically, with mutual funds and foreign investors taking significant positions. Analyst coverage went from zero to multiple brokerages initiating coverage with buy ratings. The P/E ratio of 11.9, despite the strong performance, suggested the market was still catching up to the transformation.

The dividend policy reflected management confidence. The company declared interim dividends regularly, signaling both strong cash generation and confidence in future prospects. This wasn't a company hoarding cash for unknown contingencies—it was returning capital to shareholders while still funding aggressive growth.

The sectoral comparison was telling. While traditional NBFCs traded at P/E ratios of 15-25x, Authum at 11.9x was still at a discount despite superior growth and returns. This valuation gap suggested either market skepticism about sustainability or an opportunity for further re-rating as the company proved its model.

Revenue mix evolution showed the strategic shift. Investment income now contributed nearly 90% of revenues in H1 FY25, up from virtually nothing three years ago. This wasn't just a lending company with some investments—it had become an investment company with a lending arm, a fundamental shift in business model that the market was still processing.

The geographic expansion, while not headline-grabbing, was steady. The company maintained operations across India through the acquired branch networks, but the real expansion was in the types of transactions and sectors it could now address. From real estate in Mumbai to manufacturing in Tamil Nadu, Authum had become a pan-India player in structured finance and strategic investments.

Market recognition came in various forms. Inclusion in additional indices, increased foreign institutional investor limits, and improved credit ratings all signaled growing institutional acceptance. The company that nobody knew in 2020 was becoming a must-watch name in Indian financial services by 2025.

VIII. Strategic Playbook & Investment Philosophy

Behind the headline-grabbing deals and impressive returns lies a strategic playbook that's both sophisticated and contrarian. Authum's approach to value creation isn't about following trends—it's about seeing opportunity where others see only risk.

The art of distressed asset acquisition, as practiced by Authum, goes beyond simply buying cheap. The company developed a systematic approach: First, identify situations where regulatory pressure or liquidity crisis forces sales. Second, evaluate the underlying business separate from the financial distress. Third, structure deals that align interests while protecting downside. Fourth, move with speed that larger competitors cannot match.

The RHFL and RCFL acquisitions exemplified this approach. While other bidders saw non-performing loan books and regulatory issues, Authum saw valuable NBFC licenses, established customer relationships, and operational infrastructure that would cost billions to build. The calculation was elegant: pay nominal amounts for equity, negotiate debt resolution, and unlock value through operational improvement.

Value creation through operational improvements became the second pillar of the strategy. This wasn't financial engineering—it was rolling up sleeves and fixing businesses. At RCFL, this meant rebuilding credit underwriting processes, upgrading technology systems, and re-engaging with customers who had been neglected during the distress period. The result: a business generating Rs 5,000 million in fresh disbursements quarterly.

The capital allocation framework revealed disciplined thinking. Every rupee could be deployed in multiple ways: new loans in the credit business, equity investments, structured debt, or returned to shareholders. The decision matrix was clear: prioritize opportunities with asymmetric risk-reward, maintain diversification across sectors and instruments, and always keep dry powder for exceptional opportunities.

The synergies between investment and lending businesses created a unique competitive advantage. Information from lending operations provided market intelligence for investments. Investment returns provided capital for lending growth. The combination created what strategists call a "reinforcing loop"—each business strengthening the other in a virtuous cycle.

Timing markets versus creating opportunities represented a philosophical choice. While most investors try to time market cycles, Authum focused on creating value regardless of market conditions. In bull markets, they could sell investments at premium valuations. In bear markets, they could acquire distressed assets cheaply. The dual business model provided flexibility to capitalize on any environment.

Risk management in high-stakes deals required institutional discipline. Every major acquisition went through multiple levels of due diligence: legal, financial, operational, and regulatory. The company built specialized teams for each aspect, often hiring external experts for specific transactions. The principle was simple: it's better to lose a deal than make a bad deal.

The structured financing playbook showed innovation within traditional frameworks. Instead of standard term loans, Authum created structures with equity kickers, revenue shares, or asset-backed features. These structures provided downside protection while maintaining upside participation—a combination that appealed to the company's risk-return framework.

Relationship capital proved as important as financial capital. The ability to get deals done in India's complex regulatory environment required relationships with regulators, banks, legal advisors, and industry players. Authum systematically built these relationships, understanding that in distressed situations, trust and speed matter more than price.

The portfolio construction philosophy balanced concentration with diversification. While the company made large, concentrated bets like Prataap Snacks, it also maintained a diversified portfolio of smaller investments. The approach: concentrate when conviction is high and edge is clear, diversify when seeking exposure to sectors or themes.

Speed as a competitive advantage became a defining characteristic. In the Prataap Snacks deal, Authum moved from initial discussions to signed agreements in weeks, not months. This speed wasn't recklessness—it was the result of having capital ready, decision-making authority clear, and due diligence capabilities in place.

The strategic playbook continued evolving with each transaction. Lessons from the Reliance acquisitions informed the Prataap Snacks deal. Experience in structured financing led to more complex transactions. Each success built capabilities and credibility for the next opportunity. The playbook wasn't static—it was a living document that adapted with experience and market conditions.

IX. Competition & Market Position

In India's financial services landscape, Authum occupies a unique position—neither a traditional NBFC nor a pure-play investment firm, but something more interesting: a hybrid that competes with both while resembling neither.

Traditional NBFCs like Bajaj Finance, Shriram Finance, and Muthoot Finance built their moats through distribution and specialization. Bajaj dominated consumer finance with millions of customers and thousands of touchpoints. Shriram owned commercial vehicle financing. Muthoot ruled gold loans. These companies competed on scale, efficiency, and deep domain expertise in specific lending verticals.

Authum's model deliberately avoided this competition. Instead of building distribution or specializing in one vertical, it focused on complex transactions that required structuring expertise and speed. When a mid-sized company needed Rs 100 crores in structured financing with equity kickers, they weren't calling Bajaj Finance—they were calling Authum.

The private equity competition was more relevant but equally distinct. Firms like KKR, Blackstone, and Carlyle had raised massive India funds and were looking for similar opportunities. But their fund structures created constraints that Authum didn't face. PE firms needed to deploy capital within fund life cycles, achieve specific IRR targets, and eventually exit. Authum, using permanent capital from its balance sheet, could be patient, flexible, and opportunistic.

The Prataap Snacks deal illustrated this advantage perfectly. While PE firms might have needed board control, specific exit timelines, and elaborate governance structures, Authum could structure a simpler deal that worked for all parties. The ability to be a strategic investor without the baggage of traditional strategic buyers—that was the sweet spot.

Competing with strategic buyers presented different dynamics. When Authum acquired distressed financial services companies, potential competitors included other NBFCs looking for inorganic growth, banks seeking NBFC subsidiaries, or international players entering India. But most strategic buyers moved slowly, needed elaborate internal approvals, and feared regulatory complexity. Authum's speed and risk appetite gave it an edge in competitive situations.

The moat that emerged wasn't traditional. It wasn't scale, brand, or distribution. Instead, it was a combination of capabilities that were individually replicable but collectively unique: permanent capital ready for deployment, expertise in complex financial restructuring, relationships with regulators and lenders, speed in decision-making and execution, and crucially, a track record that built credibility.

Regulatory advantages and challenges created an interesting dynamic. As a listed NBFC, Authum had regulatory clarity that private funds lacked. It could hold financial services assets directly, something that created complications for PE funds. The RBI knew how to regulate NBFCs; the framework was clear. This regulatory clarity became an advantage in deals involving regulated entities.

But regulation also created constraints. Capital adequacy requirements, exposure limits, and regulatory approvals for major transactions all added complexity. The company had to balance growth ambitions with regulatory compliance, a dance that required sophisticated understanding of both business and regulatory dynamics.

Future competitive dynamics suggested interesting possibilities. As Authum's success became visible, others would try to replicate the model. Large NBFCs might create special situations investing arms. PE funds might raise permanent capital vehicles. Strategic buyers might become more aggressive in distressed situations.

Yet replication would be difficult. The combination of patient capital, operational expertise, regulatory relationships, and risk appetite that Authum had built over years couldn't be easily replicated. More importantly, the company wasn't standing still—each successful deal enhanced capabilities and opened new opportunities.

The competitive positioning in different segments varied significantly. In distressed asset acquisition, Authum was becoming a dominant player. In structured credit to mid-market companies, it was one among several options. In strategic minority investments, it competed with both PE funds and strategic investors. This multi-front competition required different strategies and capabilities for each segment.

The international dimension added complexity. As global funds looked at India more seriously, competition for quality assets intensified. But Authum's local knowledge, regulatory relationships, and speed provided advantages that international players couldn't easily match. The ability to navigate India's complex business and regulatory environment remained a sustainable competitive advantage.

Market position metrics showed growing strength. While not the largest NBFC by assets or the biggest investor by deployments, Authum had carved out a distinct position as the go-to player for complex financial transactions. This positioning—specialist rather than generalist, opportunistic rather than systematic—created a defensible niche in India's vast financial services market.

X. Bull Case vs. Bear Case

Bull Case: The Compounding Machine

The optimists see Authum as early in a multi-decade compounding story. The proven execution on complex acquisitions—transforming two collapsed Reliance companies into profitable businesses—demonstrates capabilities that few Indian financial institutions possess. This isn't theoretical expertise; it's battle-tested operational excellence.

The 209% profit CAGR over the last 5 years provides the numerical foundation for bulls. Even if growth moderates to 20-25% annually—a significant deceleration—the compounding effects over a decade would be extraordinary. With ROE consistently above 30%, the company can fund growth internally while returning capital to shareholders.

Diversified revenue streams provide resilience that single-business models lack. When credit markets tighten, investment gains can compensate. When investment opportunities are scarce, the credit business provides steady returns. This isn't just diversification—it's intelligent portfolio construction where businesses have negative correlation during stress periods.

The strong capital position enables opportunistic moves. Being almost debt free with growing cash generation means Authum can act when others cannot. The next financial crisis, whenever it comes, won't be a threat—it will be an opportunity to acquire assets at distressed prices, just as they did with RHFL and RCFL.

Management's track record deserves premium valuation. The team that saw opportunity in Reliance's wreckage and executed flawlessly deserves benefit of doubt on future capital allocation. In a market where corporate governance concerns plague many companies, Authum's clean execution and transparent communication stand out.

The runway for growth appears vast. India's $4 trillion economy will need massive financial intermediation as it grows. Distressed assets from infrastructure to real estate provide acquisition opportunities. The credit business can scale multifold while maintaining quality. The investment portfolio can compound as holdings mature.

Bear Case: The Complexity Trap

Skeptics worry about concentration risk in the investment portfolio. Large positions in specific companies create mark-to-market volatility. If Prataap Snacks stumbles or market valuations compress, investment returns could evaporate quickly. Unlike diversified mutual funds, Authum's concentrated bets create binary outcomes.

Regulatory risks in the NBFC sector keep evolving. The RBI's increasing scrutiny, changing capital requirements, and potential restrictions on business models create uncertainty. One adverse regulatory change could impact profitability or force business model changes. The history of Indian financial services is littered with companies that couldn't adapt to regulatory shifts.

Market volatility impacts both businesses. In severe downturns, investment valuations decline while credit losses increase—a double whammy that could severely impact profitability. The 2008 crisis showed how correlations go to one during systemic stress. Authum hasn't been tested through a major crisis in its current form.

Integration risks from acquisitions remain. While RHFL and RCFL integration appears successful, the long-term sustainability is unproven. Credit losses could emerge from legacy portfolios. Operational challenges could surface as businesses scale. Integration success in two cases doesn't guarantee success in future acquisitions.

Key person dependency creates succession risk. The transformation has been driven by a small team led by Alpana Dangi. The specialized skills in deal-making, structuring, and execution aren't easily replaceable. Any disruption to key leadership could impact deal flow and execution quality.

Valuation multiples could compress as growth moderates. The current P/E of 11.9x might seem low, but it's based on exceptional recent performance. As the business matures and growth normalizes, multiples might compress further rather than expand. The market might be correctly skeptical about sustainability.

Competition will inevitably intensify. Success attracts competition. Larger NBFCs will enter special situations investing. PE funds will become more aggressive in distressed assets. The current advantaged position might erode as competitors build similar capabilities.

Quality of earnings questions persist. How much of recent profitability comes from one-time gains versus sustainable operations? Are investment valuations marked appropriately? Is the credit book adequately provisioned? These questions, while not suggesting problems, create valuation uncertainty.

The Balanced View

Reality likely lies between extreme optimism and pessimism. Authum has demonstrated exceptional execution and built valuable capabilities. The business model provides multiple growth drivers and resilience. Management has created significant value and deserves credibility.

Yet challenges exist. Complexity in the business model makes analysis difficult. Regulatory environment remains uncertain. Competition will intensify. And exceptional recent performance creates high expectations that might be difficult to meet.

For investors, the key question isn't whether Authum is good or bad—it's whether the current valuation adequately reflects both opportunities and risks. At 11.9x P/E with 30%+ ROE, the market seems to be pricing in skepticism. Whether that skepticism proves justified or excessive will determine future returns.

XI. The Road Ahead & Strategic Priorities

The pipeline of opportunities in distressed assets remains robust, perhaps even more so than when Authum began its transformation. India's banking system still carries stressed assets exceeding $100 billion. The Infrastructure sector has projects stalled for want of capital. Real estate developers face refinancing challenges. Each crisis creates opportunities for patient capital with operational expertise.

Authum's approach to this pipeline is becoming more sophisticated. Rather than waiting for distressed situations to emerge, the company now engages with potential targets early, offering structured solutions before crisis hits. This proactive approach allows better pricing and terms while helping companies avoid distress—a win-win that builds reputation and relationships.

Scaling the credit business represents the most predictable growth driver. With loan assets exceeding ₹21,500 million and quarterly disbursements of ₹5,000 million, the foundation is solid. The target appears to be reaching Rs 50,000 million in loan assets within three years—ambitious but achievable given the current run rate and market opportunity.

Technology and digital transformation, while not grabbing headlines, are crucial for long-term competitiveness. The company is investing in AI-based credit underwriting for SME loans, automated portfolio monitoring systems, and digital customer interfaces. This isn't about competing with fintech startups but about improving efficiency and risk management at scale.

Geographic expansion possibilities extend beyond India. While the company hasn't announced international plans, the expertise in distressed asset resolution and structured financing could travel. Southeast Asian markets, with their own NPL challenges and growing economies, present interesting opportunities. However, Authum seems focused on dominating India before looking abroad.

The next big acquisition targets are subject to speculation, but patterns are emerging. The company shows interest in financial services businesses with strong franchises but temporary distress, platform businesses that can be scaled with capital injection, and sectors where Authum's expertise in restructuring adds value. The recent establishment of Authum Asset Management Company suggests mutual funds or asset management could be next.

Strategic priorities are becoming clearer with each quarter: First, maintain the dual-engine model while ensuring neither business becomes too dominant. Second, build institutional capabilities to reduce key person dependency. Third, maintain balance sheet strength to enable opportunistic moves. Fourth, deepen sectoral expertise in chosen verticals. Fifth, build brand and reputation to become the preferred partner for complex transactions.

The medium-term vision appears to be becoming India's premier alternative asset manager—not in the traditional PE/VC sense, but as a permanent capital vehicle that can handle any complex financial situation. This positioning, unique in Indian financial services, could create significant value as the economy grows and financial markets deepen.

Capital allocation priorities will determine value creation. The company must balance growth investments in both businesses, opportunistic acquisitions when available, dividend payments to reward shareholders, and maintaining a war chest for special situations. Getting this balance right, especially as the business scales, will be crucial.

XII. Lessons & Takeaways

The Authum story offers profound lessons about value creation in financial services, timing in distressed investing, and the importance of building capabilities before opportunities arise.

Timing and patience in distressed investing cannot be overstated. Authum spent 38 years as an unremarkable NBFC before transforming itself. When the opportunity came—the collapse of Anil Ambani's empire coinciding with regulatory frameworks for resolution—the company was ready. This wasn't luck; it was patient preparation meeting opportunity.

Building capabilities before opportunities arise separated Authum from competitors. While others scrambled to understand complex resolution frameworks, Authum had already built teams, raised capital, and understood the regulatory landscape. The months spent preparing while others hesitated became the competitive advantage that won deals.

The importance of regulatory relationships proved decisive. In India's complex financial landscape, knowing how to navigate RBI, SEBI, and court systems matters as much as financial strength. Authum's clean regulatory record and professional approach to regulators opened doors that money alone couldn't.

Capital structure innovation enabled deals others couldn't execute. The ability to structure transactions with deferred payments, earn-outs, and contingent considerations allowed Authum to bridge valuation gaps and align interests. Financial engineering, often maligned, became a tool for value creation when used responsibly.

Creating value from complexity became the core competency. While most investors seek simple, clean situations, Authum specialized in the complex and messy. The Reliance acquisitions involved thousands of creditors, multiple regulatory approvals, and operational challenges. This complexity scared away competition and created opportunity for those willing to engage.

The power of permanent capital versus fund structures showed in execution. Unlike PE funds with defined holding periods and return targets, Authum could be patient, flexible, and opportunistic. This structural advantage, often underappreciated, enabled better deals and outcomes.

Operational excellence matters more than financial engineering. The success in turning around RCFL and RHFL came not from financial restructuring but from fixing operations—rebuilding credit processes, upgrading technology, and re-engaging customers. This operational focus distinguished Authum from purely financial investors.

Speed and decisiveness in execution created competitive advantage. In every major deal, Authum moved faster than competitors. This speed came from clear decision-making authority, prepared capital, and confidence in analysis. In distressed situations, speed often matters more than price.

The importance of aligned incentives throughout the organization ensured execution. From senior management to credit officers, incentives aligned with long-term value creation rather than short-term gains. This alignment, difficult to achieve in practice, drove operational improvements post-acquisition.

Building trust with stakeholders enabled complex transactions. Lenders trusted Authum to resolve NPLs fairly. Regulators trusted them to operate within frameworks. Sellers trusted them to close transactions. This trust, built through consistent execution, became a valuable asset.

For investors studying Authum, the lessons are equally valuable. Look for companies building capabilities before they're needed. Value permanent capital structures that enable flexibility. Recognize that complexity can create opportunity if managed well. Understand that operational improvements, not financial engineering, drive sustainable value creation.

The broader lesson for India's financial sector is that innovation doesn't always mean technology or new products. Sometimes innovation means applying old-fashioned operational excellence to complex situations others avoid. Authum proved that in India's vast financial market, there's room for specialists who do difficult things well.

XIII. Recent Developments and Market Updates

In August 2024, Authum formed a 99.99% owned sports subsidiary Billion Dream Sports Pvt Ltd with Rs.10 lakh capital, and increased its stake in Star Aerospace to 14.59% for approximately INR 112 crores, signaling diversification into defense manufacturing and sports sectors. These moves suggest the company's appetite for new sectors remains strong.

In July 2024, the promoter sold 3.41% stake for ₹1,290 Cr; with proceeds reinvested as low-cost debt for growth. This creative capital structure—where promoters provide low-cost funding rather than diluting at the company level—shows sophisticated thinking about capital efficiency.

The Q1 FY25 results showed continued momentum with net profit of Rs 1,762.59 crore, up 14.67% year-on-year. Revenue reached Rs 1,457.18 crore, demonstrating the sustainability of the business model beyond one-time gains. The company also declared an interim dividend, reflecting confidence in cash generation.

The Competition Commission of India's approval for the Prataap Snacks acquisition in January 2025 cleared the final regulatory hurdle, with the stock responding positively to the news. The integration of Prataap Snacks will be closely watched as a test of Authum's ability to create value in operating businesses outside financial services.

Note: This analysis is based on publicly available information and should not be considered investment advice. The financial services sector carries inherent risks, and past performance does not guarantee future results. Potential investors should conduct their own due diligence and consider their risk tolerance before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube