Agarwal Toughened Glass: The SME Growth Machine and the Dual-Listed Playbook

I. Introduction & Episode Roadmap

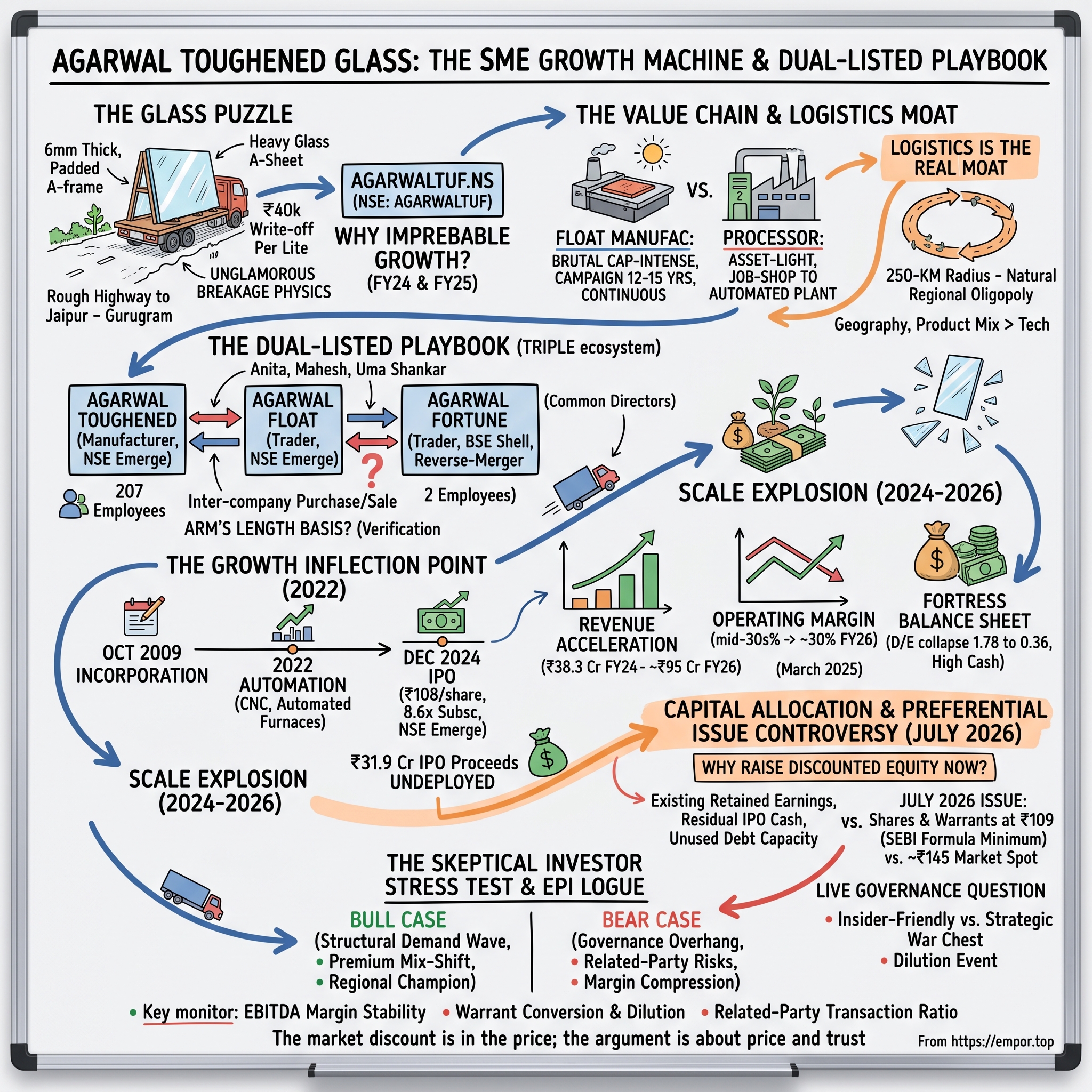

Picture a glass sheet the size of a garage door, six millimetres thick, riding upright in a padded steel A-frame on the back of a truck as it crawls the 260-odd kilometres of highway between Jaipur and Gurugram. Every pothole is a threat. Every hard brake is a potential ₹40,000 write-off. The driver knows that a single cracked lite means the whole panel is scrap — you cannot patch tempered glass, you cannot re-cut it, and you certainly cannot ship it back. This is the unglamorous, breakage-prone physics at the heart of one of the more improbable growth stories on India's SME exchange: a family-run safety-glass processor in Rajasthan that grew its top line from roughly ₹38 crore to nearly ₹95 crore in just two financial years while throwing off operating margins that would make a branded consumer-goods company blush.1[^2]

That company is Agarwal Toughened Glass India Ltd (NSE: AGARWALTUF), and the puzzle it presents is genuinely interesting. Glass is a lousy business on paper. It is heavy, it is fragile, it is expensive to move, and the barriers to buying a tempering furnace are embarrassingly low — you can order one from a catalogue. Upstream, the raw material is a pure commodity produced by continuous furnaces the size of aircraft hangars. And yet Agarwal Toughened, a downstream processor that buys those commodity sheets and cuts, tempers, and laminates them, reported an operating margin in the mid-30s percent range in FY24 and FY25 — richer than what many of the multi-billion-dollar global float giants earn on their core manufacturing.1 How?

The answer is not technology. It is geography, product mix, and a corporate structure that deserves careful scrutiny. Because the second thing that makes this story worth telling is not the growth rate — plenty of SME micro-caps post eye-watering growth for a year or two — but the architecture around it. The Agarwal family does not run one listed glass company. It runs an interlocking ecosystem of listed entities, related-party purchase-and-sale agreements, and, in July 2026, a preferential share-and-warrant issue priced conspicuously below where the stock was actually trading. This is where the narrative energy of a growth story collides with the skepticism a serious investor is obliged to bring.

Consider the sheer improbability of the margin profile for a moment, because it frames everything that follows. A branded fast-moving consumer goods company — the kind with decades of advertising, a household name, and shelf dominance — often earns operating margins in the high teens to low twenties. A commodity steel or cement producer might earn less. Agarwal Toughened, cutting and heating sheets of glass in an industrial estate outside Jaipur, was earning north of 35% at the operating line.1 When a business that sounds like a commodity processor earns margins that look like a premium brand, an analyst's first instinct should not be admiration — it should be suspicion. Either there is a genuine, non-obvious source of advantage, or there is something in the accounting, the accounting perimeter, or the sustainability of the numbers that will not survive contact with scale. Working out which of those it is — advantage or mirage — is the real project of this piece.

A few structural tailwinds are real and worth naming up front. India's luxury and commercial real-estate cycle has been unusually strong, green-building certifications increasingly demand double- and triple-glazed insulated units, and municipal safety codes have been steadily pushing builders away from ordinary annealed glass toward processed safety glass. Those are genuine demand drivers, not marketing. The question this article keeps returning to is whether Agarwal Toughened is a durable beneficiary of those trends or simply a well-timed rider on a construction boom, wrapped in a governance structure that a minority shareholder should price carefully.

There is also a temperamental reason this company is worth an hour of your attention even if you never buy a share. It is a near-perfect specimen of a species that has come to define a whole corner of the Indian equity market: the NSE Emerge / BSE SME micro-cap that IPOs on a wave of retail enthusiasm, posts blistering growth for a few years, and forces investors to reconcile two things that Western textbooks treat as opposites — extraordinary operating execution and promoter-first capital behaviour, coexisting in the same ticker. If you want to understand how to underwrite that entire asset class, Agarwal Toughened is a clean, self-contained lab experiment. Everything the class does well, and everything it does that should make you nervous, shows up here in miniature.

Here is the roadmap. First, the glass value chain — why the capital-intensive float manufacturers and the asset-light processors live in completely different economic universes, and why a 250-kilometre logistics radius matters more than any patent. Second, the "dual-listed playbook" — and why it is really a triple-listed family ecosystem, with related-party transactions running in both directions. Third, the birth and scaling of the business from a 2009 incorporation to a modern automated plant. Fourth, the late-2024 IPO and the financial explosion that followed. Fifth, the capital-allocation puzzle at the centre of the story: the July 2026 discounted equity raise, layered on top of IPO money that was still sitting largely unspent. Then the competitive framework, the bull-and-bear stress test, the durable lessons, and finally what a fundamental investor should actually watch from here. Let's start with the glass itself.

II. The Glass Value Chain: Float vs. Processed

To understand why a small Jaipur processor can out-earn a global giant on margins, you first have to understand that "glass company" describes two businesses that share a raw material and almost nothing else.

At the top of the chain sit the float glass manufacturers. The float process — molten glass floated across a bath of liquid tin to produce a perfectly flat, uniform ribbon — is one of the great industrial inventions of the twentieth century, patented by Pilkington in the late 1950s and still, seventy years on, essentially the only economical way to make flat glass at scale. Picture it: raw materials — silica sand, soda ash, dolomite, limestone — are melted together at around 1,500°C into a glowing orange liquid, which is then poured onto a long, shallow bath of molten tin. Because glass floats on tin the way oil floats on water, and because a liquid surface is naturally dead-flat, the glass spreads into a perfectly smooth ribbon as it cools and hardens, emerging metres later as a flawless flat sheet that no amount of grinding or polishing could improve. It is beautiful engineering. It is also brutally capital-intensive.

A float line costs hundreds of crores to build, and here is the punishing part: you cannot switch it off. A float furnace, once lit, runs continuously for twelve to fifteen years — a "campaign," in industry language — before it must be cold-repaired and relined at enormous cost. Shutting it down to match a soft quarter is not an option, because the molten glass would freeze solid inside and destroy the furnace. So float producers are structurally compelled to run flat-out, 24 hours a day, every day, and sell whatever tonnage the market will absorb. That single physical constraint dictates the entire economics: float glass is a textbook commodity with towering fixed costs, minimal differentiation, violently cyclical pricing, and margins that live and die by the industry's utilisation rate. When new capacity comes on and utilisation slips, prices crater and the whole industry bleeds; when construction booms and furnaces run tight, everyone prints money. In India this upstream layer is dominated by large players — the Saint-Gobain operations, Asahi India Glass, and a handful of others — plus a steady undercurrent of imports from China and the Middle East that periodically floods the domestic market and caps pricing power for everyone.[^2]

The key insight for our story is that this upstream layer, for all its scale and sophistication, is a worse business to own than the small processor downstream — because a furnace that can never turn off is a machine that can never say no to a price war. The processor, by contrast, can idle a tempering line on a slow week and lose almost nothing.

Now go one step downstream to the processors, where Agarwal Toughened lives. A processor buys those giant raw float sheets — typically in "jumbo" sizes of roughly 3.2 by 6 metres — and transforms them into finished architectural products cut to a specific building's exact specifications. According to the company's own disclosures, Agarwal Toughened processes multiple types of float glass into value-added products including laminated, frosted, and toughened safety glass.[^2]

The central transformation is tempering, and it is worth understanding physically because it explains the entire product's value. The glass is heated to roughly 620°C — just short of the point where it would slump — and then blasted with high-pressure jets of cold air. The outer surfaces cool and contract first, hardening while the core is still hot and soft; when the core finally cools and tries to shrink, the already-rigid skin will not let it. The result is a pane locked in permanent internal tension: the surface squeezed into compression, the middle pulled into tension, like a stone archway where every block is held in place by the pressure of its neighbours. Two things follow. First, the glass becomes four to five times stronger, because any crack must overcome that compressive skin before it can propagate. Second, and far more important commercially, its failure mode changes completely. Ordinary annealed glass breaks into long, sword-like shards — the reason falling glass has historically killed people. Tempered glass, once the skin is finally breached, releases all that stored energy at once and disintegrates into thousands of blunt, dice-like pebbles. It is the difference between a broken window and a weapon. That single property is why building codes mandate it, and why the product exists at all.

The crucial commercial consequence of tempering is that it is irreversible and unforgiving. Once a pane is toughened, you cannot cut it, drill it, or grind it — any attempt shatters the whole sheet instantly. Every hole, notch, and edge must be finished before the pane enters the furnace, to tolerances measured in millimetres, against an architect's drawing that may itself be revised mid-project. Get a measurement wrong and you do not have a repairable panel; you have a pile of pebbles and a re-order. This is the hidden reason processing is a real operating discipline rather than a button-press: the machinery is available off the shelf, but the precision, the measurement culture, and the scheduling competence are not. That said, none of it is proprietary — which is precisely why this is not a technology-moat business.

So where does the protection come from? The single most important word in this entire industry is logistics. Processed glass is finished to a specific size, it is fragile, and it ships upright in bulky steel A-frames that fill a truck by volume long before they fill it by weight — you are, in effect, paying to transport air and empty space around a fragile object. Move it too far and the combination of freight cost and breakage risk destroys the economics. Worse, the loss function is asymmetric and non-linear: a damaged bespoke panel cannot be sold to anyone else at a discount, because it was cut for exactly one window on exactly one building. It is worth its scrap value, which is approximately nothing. A distant supplier therefore carries not just higher freight but a higher probability of total loss on every unit — and must price that risk in.

The practical consequence — call it the roughly 250-kilometre rule — is that a processor's true addressable market is a regional radius around its plant, not a national one. This is why the global float giants, for all their scale, cannot simply parachute in and crush a local processor: they can flood the region with cheap raw glass, but the last-mile processing and fast, unbroken delivery to a construction site remains a stubbornly local game. Regional processors therefore operate inside naturally fragmented, semi-protected local oligopolies. It is a moat made of diesel, potholes, and breakage statistics — unglamorous, but genuinely load-bearing.

Layered on top of that logistics reality is a regulatory tailwind that is genuinely reshaping demand: Indian building codes and safety norms have been steadily mandating the shift from ordinary annealed glass to processed safety glass in facades, railings, skylights, and high-rise glazing. That is not a discretionary upgrade a builder can skip; it is increasingly a compliance requirement, which converts a "nice-to-have" premium product into structural, code-driven volume for certified processors. The upshot for an investor is that Agarwal Toughened's demand tailwind is real and partly non-cyclical — but its moat, such as it is, is a geographic and logistical accident, not a proprietary one. Any competitor willing to plant a furnace inside the same 250-kilometre radius competes on essentially equal technical footing. Which brings us to the far more distinctive part of this story: not the glass, but the family that structured the business around it.

III. The Agarwal Family and the Dual-Listed Playbook

Here is where the "top company story" gets genuinely unusual, and where an independent analyst has to slow down and read the fine print rather than the pitch.

The outline for this episode frames Agarwal as a "dual-listed" playbook — two sister companies, one that manufactures and one that trades. The reality, on the public record, is richer and a little more uncomfortable: the Agarwal family sits atop at least three related listed glass entities. There is Agarwal Toughened Glass India Ltd (AGARWALTUF), the manufacturer at the centre of this story, listed on the NSE Emerge SME platform in December 2024.[^2] There is Agarwal Float Glass India Ltd (AGARWALFT), a glass trading and distribution company listed earlier on NSE Emerge, whose stated business is "trading of glasses and other allied activities."3 And there is Agarwal Fortune India Ltd — formerly a shell called Devki Leasing and Finance Limited, renamed in September 2022 — now a BSE-listed entity that also trades raw and processed glasses of all kinds.4 The founding family's fingerprints are on all three.

Pause on that for a second, because the pattern is the point. Three separate listed vehicles. One family. All in glass. Two of them — Agarwal Float Glass and Agarwal Fortune India — describing their businesses in almost identical language as traders of raw and processed glass of all kinds, including laminated, safety, toughened, and fibre glass.34 Agarwal Fortune's route to the market is itself a small tell about how this corner of the market operates: rather than undertaking a fresh listing, the family took over a dormant listed finance shell, Devki Leasing and Finance Limited, and in September 2022 renamed and repurposed it into a glass-trading company based in Jaipur — a reverse-merger-flavoured path to a public ticker that is entirely legal and reasonably common, but which tends to arrive with a lighter operating history than a scrutinised IPO.4 Its scale is minimal: the entity reported a headcount of two.4 So of three listed family glass companies, one is a real factory with 207 employees, one is a shrinking trading book, and one is a repurposed shell with a two-person payroll. That is not an ecosystem built primarily for operating synergy. It looks more like an ecosystem built for optionality — and an investor should ask what kind.

The people at the top are worth introducing properly, because governance in an SME is ultimately about individuals, not org charts. Anita Agarwal serves as Chairman and Managing Director of Agarwal Toughened — a woman leading a Rajasthani industrial promoter family, which is itself notable in a sector and a region where that remains uncommon. Alongside her sit two brothers: Mahesh Kumar Agarwal, an Executive Director with more than fifteen years in the glass trade, and Uma Shankar Agarwal, a Non-Executive Director.[^2] These same two brothers are the named common directors bridging Agarwal Toughened and Agarwal Float Glass — the human wiring of the related-party relationship.[^2] Meanwhile, over at Agarwal Fortune India, the chairman-and-managing-director role and a non-executive directorship are held by individuals sharing the Agarwal family name, with the surrounding board seats filled largely by appointees installed at the time of the 2022 repurposing.4 The plant-level finance and compliance functions at Agarwal Toughened are held by professional key managerial personnel — a CFO and a company secretary — and the board carries the independent directors that listing rules require.[^2] But nobody should mistake formal compliance for genuine independence: control unambiguously rests with the family, across all three vehicles simultaneously.

It is worth being precise about why this matters, rather than gesturing vaguely at "governance." Independent directors and audit committees are the mechanism by which a minority shareholder's interests are supposed to be defended when a controlling family sits on both sides of a transaction. That mechanism is only as strong as the independence of the people staffing it and the quality of the information they receive. At Agarwal Toughened, the statutory audit is conducted by M/s Jethani and Associates, Chartered Accountants of Jaipur — a local firm, reappointed by shareholders for a further term.[^2] There is nothing improper about a Jaipur company using a Jaipur auditor; it is normal and cost-rational for a business of this size. But it is a fact worth holding: the entity checking the arm's-length pricing of transactions between three companies controlled by one family in one city is itself a small firm in that same city. That is not an accusation. It is a description of the concentration of trust that a minority investor is being asked to extend.

The stated commercial logic of the ecosystem is a synergy story, and it is a plausible one: the trading arm buys glass in bulk from primary float producers, captures volume discounts, and the manufacturing arm draws on that procurement muscle to source raw sheets cheaply before processing them into high-value products. But when you open Agarwal Toughened's FY25 related-party disclosures, the neat "trader-buys, manufacturer-processes" story gets complicated. In FY25 the manufacturer both sold goods to Agarwal Float Glass (roughly ₹5.0 crore, GST inclusive) and purchased goods from it (roughly ₹3.7 crore), with a further ~₹1.3 crore of purchases from Agarwal Fortune India.[^2] Goods, in other words, flow in both directions between the family companies. And the trading "engine" is not the powerhouse the synergy narrative implies: Agarwal Float Glass's revenue actually shrank — from about ₹79 crore in FY24 to ₹65 crore in FY26, with razor-thin net profit — even as the manufacturer's revenue rocketed past it.3 The tail, if it ever was one, is now smaller than the dog.

The trajectory of these related-party dealings is as revealing as their size. In FY24, transactions with the family's controlled entities were comparatively modest; by FY25, the aggregate of related-party dealings disclosed in the accounts had multiplied several times over, with the sale line to Agarwal Float Glass alone leaping from roughly ₹31 lakh to over ₹5 crore in a single year.[^2] Some of that is simply the mechanical consequence of a business that nearly doubled in size — bigger company, bigger inter-company flows. But it is growing considerably faster than the underlying business, which is a different thing and warrants an explanation that has not, to date, been offered in detail. The disclosures also reveal a wider web than the three listed vehicles alone: a proprietorship concern belonging to a relative of a director appears in the accounts with an interest-receivable balance, and directors and their relatives have taken and repaid unsecured loans from the company.[^2] None of this is unusual for an Indian family business of this vintage. All of it enlarges the surface area across which value can move.

This is the governance stress point, and it should be stated plainly rather than smoothed over. There is no public non-compete agreement between the sister entities, and the related-party transactions are material: management itself flagged that dealings with Agarwal Float Glass represented roughly 9.11% of turnover in the prior year and sought shareholder approval for transactions of up to ₹15 crore in FY26.[^2] The company's defence is the standard one — that all such transactions are "on an arm's length basis and in the ordinary course of business," reviewed by the Audit Committee.[^2] That may well be true. But "arm's length" between companies controlled by the same brothers, with no independent valuation report attached to the FY26 approval,[^2] is a claim a skeptical investor is entitled to treat as unproven rather than proven.

Consider what the absence of that valuation report actually means in practice. When Agarwal Toughened buys a truckload of raw float glass from Agarwal Float Glass, what price is paid? The only parties who know whether that price matches what an unrelated third-party trader would have charged are the same people who control both companies. The disclosure gives shareholders the aggregate value of the transactions but no independent benchmark against which to test the pricing. And pricing is where all the value sits. A few percentage points of margin on inter-company glass — invisible in an aggregate number, immaterial in any single invoice — is precisely the mechanism by which profit could be moved from a company where the family owns 64% to one where it owns rather more, or less, depending on which way the incentive runs. The structural risk is timeless: where the same family sits on both sides of a purchase order, margin, cost, and opportunity can in principle be shifted between entities to suit tax, valuation, or ownership incentives.

Let it be said clearly, because fairness demands it: nothing in the public record proves any of this is happening. The transactions are disclosed, they were put to shareholders, the audit committee approved them, and the statutory auditors issued an unmodified opinion on the FY26 accounts. Agarwal Toughened is, on the evidence, a real factory making real glass for real customers and earning real cash. The point is narrower and more durable: this structure means an investor cannot verify the arm's-length claim from outside, and must therefore either extend trust or demand a discount for the uncertainty. Sophisticated investors do the latter. Now, how did the manufacturing entity get big enough to matter?

IV. The Birth & Scaling of Agarwal Toughened Glass (2009–2024)

Every great Acquired story has an origin, and this one begins not with a garage but with a furnace in Rajasthan. Agarwal Toughened Glass India was incorporated in October 2009 in Jaipur, a family enterprise built by people who already understood the glass trade from the inside.[^2] For its first decade it was, functionally, a small regional job-shop: take raw float sheets, cut and temper them to order, and serve local builders and fabricators. It was a private limited company doing unglamorous, working-capital-heavy processing work — the kind of business that never makes headlines and rarely makes real money either.

The geography, though, was quietly excellent. Jaipur sits on the doorstep of India's National Capital Region — close enough to serve the Delhi-NCR construction machine, that relentless engine of commercial towers, corporate parks, and luxury high-rises, while enjoying Rajasthan's lower industrial land and operating costs. Within that logistics radius we discussed earlier, Jaipur is close to a very large, very glass-hungry market without paying Gurugram or Noida real-estate prices. Run the arithmetic that governs this industry: a processor sitting inside Delhi-NCR pays metropolitan land, labour, and power costs to serve the same customers; a processor sitting 600 kilometres away cannot serve them at all. Jaipur threads the needle — low-cost inputs, in-radius delivery. A processor's single most valuable strategic asset is the location of its plant, and the family, whether by foresight or the simple accident of being from Jaipur, planted theirs well. It is worth being honest that this may be luck rather than genius; the family was in the glass trade in Jaipur because the family was from Jaipur. But in a business where geography is the moat, being born in the right place is a legitimate competitive advantage, however it was acquired.

For the first decade, though, that advantage sat largely unmonetised. The gap between "we are well located" and "we can win a spec-heavy contract for a Gurugram office tower" is enormous, and it is measured in machinery, certifications, and consistency. A manual job-shop can cut and temper glass, but it cannot promise an architect that 4,000 panels will arrive over eleven months, each within a millimetre of specification, each certified, none late. That promise is the product. Everything else is a commodity.

The genuine inflection point came around 2022, when the company moved from being a manual job-shop to something closer to a modern automated plant. The registered manufacturing base sits in the RIICO Industrial Area at Ramchandrapura, Sitapura Extension, Jaipur,[^2] and the operational shift was from basic manual cutting toward computerised CNC glass-processing machinery and automated tempering furnaces. This is the difference between a workshop and a factory, and each element compounds. Automation cuts breakage, which in a business where a broken bespoke panel is a total loss falls straight to the bottom line. It tightens edge-polishing tolerances — which matters enormously for structural glazing, where a pane is held to a building by silicone and clamps rather than a frame, and where consultants specify processors on the precision of their edgework because a rough edge is a stress concentrator waiting to become a crack. It shortens turnaround, which is what a site manager staring at a delayed facade actually buys. And it makes the output consistent, which is the precondition for bidding institutional work at all.

By March 2025 the company employed 207 people[^2] — still small by any absolute measure, but no longer a family shed. That headcount is itself a useful reality check on the story: a business generating close to ₹95 crore of revenue with roughly two hundred employees is running meaningful revenue per head, which is what automation is supposed to deliver, and is a quiet corroboration that the plant modernisation was real rather than rhetorical.1[^2]

Just as important as the machinery was the product-mix pivot, because this is where the margin story actually lives. Basic toughened glass is a low-margin commodity where the processor is barely more than a subcontractor with a furnace. The value — and the pricing power — sits in the specialised products, and each deserves a moment because they are what the investment case rests on.

Laminated safety glass takes two lites and bonds them permanently with a plastic interlayer, typically PVB, under heat and pressure. The result behaves like a car windscreen: when it breaks, the fragments stay glued to the interlayer rather than falling. The pane fails without ever becoming a hazard below. That property is non-negotiable for overhead glazing, skylights, glass floors, balustrades, and any facade where a falling pane would land on a pedestrian — which is why it is written into codes rather than chosen on taste. It is also, usefully, a product where a cheap operator cannot easily compete: a bad lamination delaminates years later, clouding at the edges, and the reputational liability is severe.

Insulated glass units — double-glazed units, in common speech — seal two panes together around a spacer, trapping a dehydrated air or argon gap between them. The trapped gas is a poor conductor of heat, so the unit behaves like a thermal blanket for the building: think of the double wall of a vacuum flask. In a country where air-conditioning is the single largest driver of a commercial building's energy bill, an IGU directly reduces operating cost, which is precisely why green-building certification frameworks push developers toward them and why they have become near-mandatory in energy-efficient commercial construction. The economic significance is that the customer is no longer buying glass by the square foot; they are buying a measurable performance specification — a U-value — and performance specifications support pricing that commodities do not.

Then there are the specialty finishes: ceramic-fritted glass with ceramic ink fused into the surface during tempering for solar shading and pattern, acoustic glass that uses specialised interlayers to damp sound for buildings near highways and airports, and lacquered glass for interior applications. These carry meaningful price premiums over plain toughened product.

Management's entire strategic thesis, as laid out in its FY25 commentary, is to keep tilting the mix toward these higher-specification, customised products — energy-efficient double-glazed units, high-strength safety glass — where competition is thinner and the customer is buying certified performance rather than a cut sheet, while pursuing commercial real estate, upscale residential, and specialty installations like airports and malls.[^2] The logic is sound and the tailwinds are real. But note what an analyst cannot do from the outside: the company does not disclose a revenue breakdown by product category, so there is no public way to verify how much of the mix is genuinely premium IGU and laminated work versus plain toughened glass riding a construction boom. The mix-shift thesis is management's claim, and it is a plausible one — but the only evidence available to test it is the margin line itself. Which is exactly why what happened to margins in FY26 matters so much.

V. The Late-2024 IPO & The Modern Growth Explosion

By late 2024 the family decided it was time to convert operating momentum into public capital. The corporate machinery moved with the unglamorous precision these things require: the board authorised the issue by resolution on June 22, 2024, shareholders passed the enabling special resolution at an extraordinary general meeting three days later on June 25, and the NSE granted in-principle approval for listing on October 30, 2024.[^2] Then Agarwal Toughened Glass opened its initial public offering on the NSE Emerge SME platform, with the issue running from November 28 to December 2, 2024, at a price band of ₹105–₹108 per share.2 It was a fresh issue of 57,99,600 equity shares of ₹10 face value at the ₹108 top of the band, raising ₹62.64 crore,[^2] and the market's appetite was healthy — the book was subscribed roughly 8.6 times.2 The shares listed on December 5, 2024.2

Two details are worth extracting from that. First, it was a fresh issue — the entire ₹62.64 crore went into the company's balance sheet rather than into promoters' pockets via an offer-for-sale. That is the shareholder-friendly structure, and the family deserves credit for choosing it; a promoter group cashing out at IPO would have been a far worse signal. Second, the 8.6x subscription tells you something about the market environment more than about the company: late 2024 was a period of ferocious retail appetite for Indian SME IPOs, where oversubscription was closer to the norm than the exception. A well-received SME listing in that window is weak evidence of quality. For a small architectural-glass processor from Jaipur, though, walking onto a public exchange was still a genuine coming-of-age moment — and it came with obligations the family had not previously carried: quarterly disclosure, audit committees, related-party approvals put to a shareholder vote, and several thousand outside owners entitled to ask what happened to their money.

The more revealing question is where the money went — and here the primary documents tell a story that complicates the "growth machine needs capital" narrative. The prospectus earmarked the net proceeds across four buckets: purchasing machinery at the existing unit (about ₹9.67 crore), repaying certain borrowings (₹6.0 crore), funding incremental working capital (₹25 crore), and general corporate purposes.[^2] But the FY25 annual report reveals that as of March 31, 2025 — roughly four months after listing — the company had actually deployed only about ₹23.7 crore of the ₹55.6 crore allocated, leaving ₹31.9 crore still unutilised.[^2] Only ₹1.08 crore of the machinery budget had been spent, and only ₹10 crore of the ₹25 crore working-capital allocation.[^2] Hold that fact — more than half the IPO money still sitting on the balance sheet — because it becomes the crux of the capital-allocation controversy two sections from now.

Meanwhile, the operating results genuinely accelerated. Revenue from operations climbed from ₹38.3 crore in FY24 to ₹55.3 crore in FY25,[^2] and then surged again to roughly ₹95 crore of operating revenue (near ₹100 crore of total income) in FY26.1 Net profit followed the same arc — from about ₹8.6 crore in FY24 to ₹15 crore in FY25 and ₹21.6 crore in FY26 — with earnings per share reaching ₹12.22.1 The board approved the audited FY26 accounts in late May 2026, and the statutory auditors issued an unmodified opinion — meaning no qualifications, no emphasis-of-matter caveats on the numbers themselves.1 That matters and should be said: for all the governance questions this story raises, the reported financials come with a clean audit.

A near-doubling of revenue in the year after listing is exactly the kind of number that makes an SME stock a market darling. More usefully, it tells you the modernised plant's capacity was being filled with real orders rather than sitting idle — the single greatest risk of any capacity expansion is that you build it and the orders don't come, and that plainly did not happen here. The returns metrics corroborate the picture: a return on capital employed in the low-to-mid 20s percent and a three-year average return on equity in the mid-20s indicate the business is generating genuine economic returns well above any plausible cost of capital, not merely growing for growth's sake.1 Meanwhile the balance sheet was transformed by the listing: the debt-to-equity ratio collapsed from 1.78 at the end of FY24 to 0.36 a year later, while the current ratio jumped from 1.36 to 3.76.[^2] In plain terms, a company that had been running with meaningful leverage and tight liquidity suddenly had a fortress balance sheet and a large cash cushion. Remember that transformation — it is the reason the events of July 2026 are so hard to explain.

There is one more disclosure worth flagging, because it speaks to management's communication quality rather than its operations. The FY25 annual report's forward-looking commentary discussed the outlook by citing global growth forecasts of "around 3.1% in 2024 and rising slightly to 3.2% in 2025" — figures already stale by the time the report was published in September 2025.[^2] It is a small thing. But boilerplate macro commentary recycled past its shelf life is a mild signal about how much original thought goes into investor communication at this company, and it is consistent with a broader pattern: the disclosures satisfy the letter of the requirement without volunteering much that would help an outsider genuinely test the story. There is no analyst conference call to interrogate management, no quarterly investor Q&A of the kind a larger listed company would face. For an investor, that absence is itself material — it means the usual tools for assessing management credibility over time, like comparing what was promised on last year's call against what was delivered, simply are not available here.

But the podcast-worthy detail is in the margin line, because it is where the growth story shows its first strain. Operating margins that had held in the mid-30s percent range in FY24 and FY25 compressed toward roughly 30% in FY26.1 The mechanism is straightforward and, frankly, predictable: as a processor scales up to chase larger institutional and real-estate contracts, it trades price for volume — big buyers negotiate harder — even as the cost of raw float glass and energy inflates from the commodity layer upstream. Management has consistently flagged raw-float-glass and energy-cost volatility as its central margin risk,[^2] and FY26 is the year that risk started to bite. The honest read is that a processor with a low technical moat, selling into increasingly large and sophisticated buyers, should expect its margins to normalise downward as it grows — the question is where they settle. A drop from the mid-30s toward 30% is not alarming; a drift below the high-20s would begin to challenge the entire premium-mix thesis. That tension — spectacular growth, gently eroding margins, and a pile of undeployed cash — is the backdrop against which the company made its most controversial decision.

VI. Capital Allocation & The July 2026 Equity Controversy

This is the section where the growth story and the governance story finally collide, and it deserves to be told carefully because it is the single most important thing a prospective shareholder should understand about Agarwal Toughened Glass as of mid-2026.

Set the scene. It is the first half of 2026. The company is compounding beautifully. It is generating over ₹21 crore of annual profit, it carries only about ₹25 crore of total debt, and — as we just established — it is still sitting on tens of crores of IPO money that it has not yet spent.1[^2] A company in that position has three obvious ways to fund further expansion: use its own cash flow, deploy the IPO proceeds already in the bank, or borrow modestly against a lightly-geared balance sheet. Instead, the board chose a fourth path.

In May 2026, shareholders approved a preferential issue of up to 17.46 lakh equity shares and 46.80 lakh convertible warrants at ₹109 per unit — a raise of roughly ₹70 crore.6 On July 3, 2026, the company allotted 16.51 lakh equity shares and 45.90 lakh warrants at that ₹109 price, mobilising up to ₹68.04 crore.16

For the mechanically-minded reader, it is worth unpacking what a convertible warrant actually is, because the instrument choice is doing a lot of quiet work here. A warrant is a right — not an obligation — to subscribe to a share later at a price fixed today. Under SEBI's framework, the allottee pays 25% of the price upfront and the balance when they choose to convert, at any point within eighteen months. Now look at the asymmetry that creates. The allottee has, in effect, purchased a cheap eighteen-month call option on the company, paying roughly ₹27 per warrant today to lock in a ₹109 price. If the stock rises, they convert and capture the entire gain. If the stock falls below ₹109, they simply walk away and forfeit the 25% deposit. Heads they win big; tails they lose a quarter of their stake. That is a perfectly legal instrument, widely used, and it does have a legitimate rationale — it lets committed backers fund a capex programme in tranches as the money is actually needed, rather than dumping it all on the balance sheet at once.

But it is not a neutral instrument. It transfers optionality from the company to the allottee, and when the allottees include insiders, the company is writing its own insiders an eighteen-month option at a price the insiders' own board helped set. If all the warrants convert, the fully-diluted share count expands materially — on the order of a fifth larger than before — and every existing public shareholder's slice of the company, and of its future earnings, shrinks accordingly.

Now the part that raises eyebrows. The ₹109 execution price was set virtually flat with the December 2024 IPO price of ₹108 — as if eighteen months in which revenue nearly doubled and profit rose by roughly 40% had added almost nothing to the value of a share.1[^2]2 Yet through mid-2026 the stock was actually trading in the secondary market around ₹144–₹146.15 In other words, insiders and select non-promoter allottees were handed shares — and a locked-in right, via warrants, to buy more over the next year and a half — at roughly a 25% discount to where the investing public was transacting on the same days.

There is a legitimate technical defence, and it should be given its full weight. SEBI's pricing formula for preferential issues is based on a trailing volume-weighted average market price over defined look-back periods, not on the spot price. Companies must price at or above that regulatory floor. Because Agarwal Toughened's stock had appreciated over the look-back window, the trailing average sat well below the current market price, and ₹109 may well have been fully compliant with the formula. The discount is therefore not, on its face, improper, and no allegation of illegality is being made here.

But "permitted by the formula" and "aligned with minority interests" are very different standards, and conflating them is exactly the error the SME market invites. The pricing formula is a floor, not a mandate. Nothing prevented the board from pricing the issue closer to the prevailing market price — that was a choice, made by a board on which the family's executive directors sit, in favour of allottees who include insiders. And there is a subtler point that a careful reader should catch: the formula rewards issuing equity after a period when the stock has run up, precisely because the trailing average lags. The regulatory design creates a standing temptation, and the question for any investor is whether a given board resists it or exploits it.

Here is the analytical heart of it, and it is worth slowing right down. Why would a profitable, cash-rich, lightly-indebted company that had not even finished spending its last equity raise turn around and issue a large slug of new equity at a discount to market? Line up the alternatives it declined. It generated over ₹21 crore of annual profit it could have retained — indeed, it pays no dividend, so essentially all of that profit is available for reinvestment.1 It carried only about ₹25 crore of total debt against a business earning mid-20s returns on capital, meaning it had enormous unused borrowing capacity at interest rates far below its return on capital — the textbook definition of a company that should use debt, not equity, to fund expansion.1[^2] And it was still sitting on tens of crores of IPO proceeds it had not spent.[^2] A company with retained earnings, untapped debt capacity, and unspent prior equity chose, as its fourth option, to issue discounted shares and warrants. That ranking of preferences is the puzzle.

Two readings are possible, and an honest analyst should hold both without collapsing into either. The charitable reading: management foresees a genuinely large, lumpy capex cycle — new imported tempering and lamination lines, perhaps a second furnace, a capacity step-change to serve the Delhi-Mumbai Industrial Corridor — whose total cost dwarfs both the residual IPO cash and prudent incremental debt, and is raising a war chest ahead of it, with warrants letting committed strategic backers fund in tranches as milestones are hit. On this reading the discount is the price of securing patient capital, and the whole thing will look prescient in three years when a doubled plant is running full. The skeptical reading: with the stock cheap on a trailing-average basis relative to spot, this is an opportunistic, discounted equity lock-in that transfers value from minority public shareholders to insiders and favoured parties, dressed in the language of growth capital, and the "we need it for capex" rationale is retrofitted to a decision whose real driver is cheap insider accumulation.

The tell that keeps the skeptical reading firmly alive is the undeployed IPO cash. It is genuinely hard to construct an urgent, unmet ₹68 crore capital need while ₹30-odd crore of your previous raise sits uninvested and your borrowing capacity is barely touched.[^2] If the capex cycle were truly imminent and enormous, one would expect the residual IPO money to have been spent first — the ₹8.6 crore of unused machinery budget deployed, the working-capital allocation drawn down — before returning to shareholders for more. The sequence is backwards for the charitable story and exactly right for the skeptical one.

None of this can be adjudicated today, and it should not be pretended otherwise. The honest verdict is that the July 2026 raise is a live governance question, not a settled scandal. It will resolve, one way or the other, on evidence that has not yet arrived: whether the ₹68 crore is visibly and promptly deployed into disclosed, productive, revenue-generating capacity; whether the full list of warrant allottees, when disclosed, is dominated by insiders or includes genuine third-party strategic capital; and whether, when the warrants come up for conversion, the promoters convert at ₹109 into a stock trading far higher — capturing a gain the public was denied — or the deal quietly lapses. A fundamental investor's job is not to pre-judge the verdict but to watch those specific facts. That question is exactly what a competitive-forces analysis has to be weighed against, because a governance discount is only worth paying if there is a real business underneath it.

VII. Porter's 5 Forces & Hamilton Helmer's 7 Powers Analysis

Strip away the growth optics and ask the harder question a long-term investor must ask: does Agarwal Toughened Glass possess any durable competitive advantage, or is it simply a competent operator riding a good market? Two frameworks help war-game the answer.

Start with Hamilton Helmer's 7 Powers, which asks not "is this a good business today" but "what, if anything, stops a competitor from competing away its returns." On honest inspection, Agarwal clears the bar on only one power cleanly. Scale economies — but strictly regional. This is the real one. Because processed glass cannot travel far without freight and breakage costs eating the margin, a processor with a large, automated, well-located plant enjoys a genuine cost-and-service advantage inside its logistics radius that a distant competitor cannot match. That is a real power, but a bounded one — it protects Rajasthan and parts of Delhi-NCR, and evaporates the moment you cross into another processor's territory. Switching costs are low-to-moderate at best: a builder can change glass suppliers between projects with little friction, though the hyper-sensitivity of construction timetables to delivery delays and breakage gives an incumbent, reliable regional processor a soft stickiness — a site manager mid-project will not lightly gamble on an unproven supplier. Branding power exists only in the thin B2B sense: structural-glazing consultants specify processors on safety-compliance records and edge-polishing precision, which builds reputation, but this is professional trust, not consumer brand equity, and it does not command a true price premium the way a consumer brand would. The remaining powers — network economies, counter-positioning, cornered resources, process power — are essentially absent. This is not a company protected by a fortress; it is a company protected by a moat of transport costs and local reputation.

Before leaving Helmer, it is worth naming the power the company most conspicuously lacks, because its absence defines the ceiling on the business. There is no cornered resource — no exclusive supply contract, no patent, no scarce input that only Agarwal can access. In fact the opposite is true: its most important input is controlled by the very suppliers with the most power over it. And there is no counter-positioning — Agarwal is not doing something structurally that incumbents cannot copy without damaging their existing business; it is doing the same thing as every other processor, only inside a favourable postcode. A business with exactly one bounded power is a business whose returns are protected only at its geographic edges and are otherwise fully exposed to competition. That is not a criticism so much as a specification: it tells you the returns are real but capped, regional but not scalable into a national franchise, and defensible against distant entrants but not against a well-capitalised competitor who plants a furnace next door.

Now Porter's Five Forces, which maps the pressure on industry profitability from five directions at once. Bargaining power of suppliers is the critical threat, and it is high. The primary float manufacturers sit in a concentrated, oligopolistic upstream layer, and Agarwal is fundamentally a price-taker on its single largest input.[^2] Recall the physics from earlier: the float producer cannot turn its furnace off, which makes it desperate to sell tonnage — but it sells into a concentrated market of a few producers who do not need to undercut each other to move volume when construction is booming. The processor, buying that glass, has no comparable leverage; it needs the raw material far more than any single float giant needs one processor's order. When soda ash, silica, or gas costs push float prices up, the processor either absorbs the hit or tries to pass it on to price-sensitive builders — and FY26's margin compression is the visible fingerprint of exactly that squeeze arriving. This is the force that most directly threatens the investment case, because it operates continuously, not just in downturns.

Threat of new entrants is moderate, and the nuance is everything. The machinery is buyable off the shelf — a genuinely low barrier — but securing safety certifications, building the trust of developers and glazing consultants, and achieving the scale and consistency to bid credibly for institutional work takes years — a genuinely real barrier. So entry is easy at the low end and hard at the high end. Anyone can open a shop that toughens shower screens; almost no one can, from a standing start, win the glazing contract for an airport terminal. This asymmetry is precisely why Agarwal's strategic survival depends on climbing and staying at the high end. A processor that drifts back down into commodity toughening is a processor whose moat has evaporated, because at the low end the threat of entry is permanent and severe.

Competitive rivalry is fierce and comes from three directions at once. From below, a long tail of unorganised local toughening shops competes on price and undercuts on anything commoditised. Laterally, listed processing peers such as Sejal Glass fight for the same organised-sector institutional contracts. And from above, the downstream processing arms of integrated float giants like Asahi India Glass can process their own raw material — capturing the full chain's margin and, crucially, immune to the supplier-power problem that constrains a standalone processor. That last competitor is the most dangerous, because vertical integration is the one structural answer to Agarwal's single biggest vulnerability, and Agarwal does not have it.

Buyer power is meaningful and rising. Large real-estate developers and glazing contractors are exactly the sophisticated, volume-leveraged customers who negotiate hard, demand credit terms, and play processors against one another — and as Agarwal grows by chasing precisely these larger accounts, it is trading a fragmented, price-insensitive small-order book for a concentrated, price-sensitive large-order book. That is the mechanism behind the FY26 margin compression, and it is a structural feature of the growth strategy, not a one-off. Substitution, finally, is low: there is no material replacement for architectural safety glass in a modern glazed facade, and codes actively mandate it. This is the one force working unambiguously in the company's favour.

Netted out, the frameworks agree: this is a decent-but-not-fortified business. Its one real edge — regional logistics scale — is durable within a boundary but cannot be exported, its suppliers hold the whip hand on input costs, and its customers are getting stronger as the company chases bigger contracts. That is a perfectly investable profile, but only at a price that respects the ceiling on its structural returns. Which sets up the final reckoning between bull and bear.

VIII. Bull vs. Bear Case: The Skeptical Investor Stress Test

Every serious investment case is really an argument between two disciplined stories. Here is the strongest version of each, told without a thumb on the scale.

The bull case rests on a simple, powerful idea: Agarwal Toughened Glass is a well-run operator sitting in the sweet spot of a multi-year structural demand wave. India's luxury residential and commercial green-office construction cycle shows little sign of exhausting itself, and the regulatory push from annealed toward certified safety glass converts a chunk of that demand from discretionary to mandatory — a tailwind that keeps blowing even in a softer construction year. The company is not merely riding volume; it is actively tilting its mix toward the highest-margin products — double-glazed insulated units and laminated safety glass — where competition is thinnest and specification-driven buyers pay for certified performance.[^2] Its Jaipur base gives it a logistics-advantaged position to serve the enormous Delhi-NCR and Delhi-Mumbai Industrial Corridor markets. And the raw operating numbers back the story: revenue that more than doubled in two years, mid-20s percent ROCE and ROE, and net profit compounding at a rate few industrial small-caps can touch,1 all achieved on a modestly-geared balance sheet. A bull looks at that and sees an emerging regional champion in a fragmented, consolidating industry.

The bear case — the activist's stress test — does not dispute the growth. It disputes what the growth is worth to a minority shareholder, and it attacks on three fronts. First, related-party transfer risk: with the same family controlling the manufacturer and at least two glass-trading entities, and with goods flowing both ways across those companies at prices management self-certifies as arm's length but without independent valuation, profits and costs could be shifted between the family's private and public interests, and a public shareholder has limited ability to detect it.[^2] Second, insider-friendly capital allocation: the July 2026 discounted share-and-warrant issue, priced at ₹109 while the stock traded near ₹145, layered on top of still-unspent IPO cash, is precisely the kind of aggressive equity practice that erodes minority value and signals that promoter incentives may not be fully aligned with outside investors.1[^2] Third, structural fragility of the economics: a low-technical-barrier processor, dependent on an oligopolistic supplier for its key input and increasingly dependent on price-sensitive institutional buyers for its volume, is one soda-ash spike or one construction-cycle downturn away from the margin compression already visible in FY26 accelerating. The bear's summary verdict is not "this is a bad business" — it is "this is a good business wrapped in a governance structure that demands a discount."

There is a useful way to reconcile the two cases, drawn from how the market itself is pricing the stock. Through mid-2026 the shares traded around ₹145 on trailing earnings per share of roughly ₹12 — a price-to-earnings multiple of about twelve.1 Set that against the operating reality: a business compounding revenue at extraordinary rates, earning mid-20s returns on capital, in a structurally growing end-market. A clean, well-governed company with those operating metrics would not trade at twelve times earnings; it would command a multiple two or three times higher. So the market is already applying a large discount. The entire investment question collapses to a single judgement: is the discount the market demands for the governance and cyclicality risks larger or smaller than the discount those risks actually deserve? That is not a question this article can or should answer with a number — but framing it that way is more honest than either cheerleading the growth or dismissing the company for its governance. The growth is in the price at a discount; the argument is only about whether the discount is big enough.

It is also worth stress-testing the bear case against itself, because a disciplined skeptic must. The strongest counter to the bear is that the promoters chose a fresh-issue IPO rather than cashing out, retained every rupee of profit rather than paying themselves dividends, and built a genuine, audited, employment-generating factory rather than a paper business — none of which is what pure value-extractors typically do. A promoter group whose only aim was to enrich itself at minority expense had cleaner ways to do it than building a real plant that now employs hundreds and earns a clean audit opinion. The related-party flows and the discounted warrants are real yellow flags, but they coexist with real capital discipline elsewhere. The most probable truth is neither villainy nor sainthood: a capable operating family that runs its public company with a promoter-first instinct about capital and control, common in this market, requiring vigilance rather than alarm.

The synthesis a fundamental investor should carry away is that both cases are simultaneously true, and the debate is entirely about price and trust. The operating story is real; the governance overhang is also real; and unlike the operating story, the governance overhang is unlikely to resolve cleanly, because it is structural rather than temporary. This is the essence of what SME investing in India so often demands — and it points to a set of durable lessons that outlast this one company.

IX. Playbook & Durable Business Lessons

Step back from the ticker and Agarwal Toughened Glass becomes a compact case study in three transferable ideas.

Lesson one: for heavy, fragile goods, logistics is the moat that technology cannot be. The entire reason a small Jaipur processor can earn returns that a global float giant would envy is not that it knows something the giant doesn't — it buys the same off-the-shelf furnaces. It is that finished glass cannot travel, and so the market fragments into defensible regional territories. In industries where the product is expensive to move and easy to break — glass, ready-mix concrete, industrial gases, fresh food — local density and delivery reliability are more durable protections than any patent. The investor's takeaway is to look for the physical constraint that fragments the market, and then ask who owns the best position inside each fragment.

Lesson two: legal separation of trading and manufacturing is a double-edged sword. Splitting a high-volume, low-margin, working-capital-heavy trading operation from a lower-volume, high-margin, capex-heavy processing operation can genuinely protect the unit economics of the manufacturing entity — the public manufacturer isn't dragged down by the thin-margin trading book. But the same structure that isolates economics also creates the channel through which value can be moved between entities under common control. The separation that looks like financial hygiene from one angle looks like a related-party conduit from another. Both readings can be correct at once, which is exactly why the structure demands ongoing scrutiny rather than a one-time verdict.

Lesson three — the one most specific to this market — is the SME governance tax. On India's NSE Emerge and BSE SME platforms, exceptional operating growth is frequently accompanied by aggressive promoter equity practices: discounted preferential issues, warrant lock-ins to insiders, dense related-party dealing, and zero dividends despite consistent profits. Agarwal Toughened has, to date, paid no dividend despite years of rising earnings.1 None of this is necessarily fraudulent, and much of it is technically compliant. But it means the institutional and serious retail investor must apply a "governance discount" to the valuation — paying less per rupee of earnings than the same growth would command in a company with cleaner alignment. The mistake is not investing in SME growth stories; it is paying a large-cap governance premium for a small-cap governance reality. With those lessons in hand, what should an investor actually monitor from here?

X. Epilogue & What to Watch

As of mid-2026, Agarwal Toughened Glass India Ltd is a genuinely impressive operating asset carrying a genuinely unresolved governance question. It is a fast-growing, high-return, logistics-advantaged architectural-glass processor sitting in the fat middle of India's construction boom — and simultaneously a family-controlled SME whose capital-allocation choices and related-party architecture require a permanent skeptical eye. Neither half of that description cancels the other; both must be held together. The stock trades on a modest trailing earnings multiple,1 which is the market's own way of pricing the tension.

Rather than track everything, a disciplined investor should zero in on a very small number of signals that genuinely move the thesis. Three stand out.

First, EBITDA / operating-margin stability. The whole premium-processor thesis rests on the company defending margins in the low-30s percent range against relentless upstream input-cost inflation and increasingly powerful institutional buyers. FY26 already showed compression from the mid-30s toward roughly 30%.1 If the mix shift toward IGUs and laminated glass is real and durable, margins should stabilise around this level; if they keep sliding into the high-20s and below, the "we sell premium specification, not commodity glass" story is failing in practice, whatever management says on a call.

Second, warrant conversion and the resulting dilution. The roughly 45.9 lakh convertible warrants issued in July 2026 are a slow-motion dilution event with an eighteen-month runway.6 Watch not only whether they convert — signalling the allottees' own confidence — but at what pace, to whom precisely, and whether the ₹68 crore raised is visibly deployed into disclosed, productive capacity rather than parked. This is the single clearest future test of whether the July 2026 raise was a growth war chest or an insider lock-in.

Third, related-party transaction volume as a share of costs. The dealings between Agarwal Toughened and its sister trading entities — measured against cost of goods sold — are the most direct available proxy for the governance risk at the heart of the bear case.[^2] A stable or shrinking ratio, with independent pricing validation, would meaningfully de-risk the story over time. A rising ratio, especially if margins are simultaneously softening, would suggest the two risks are connected and demand a wider governance discount. In a business where the glass itself is a commodity and the moat is a truck route, it is ultimately the conduct of the people holding both sides of the purchase order that a long-term investor is really underwriting.

References

-

Agarwal Toughened Glass India Ltd — Company financials, ratios and shareholding — Screener.in ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Agarwal Toughened Glass India IPO — dates, price band, issue size, subscription and listing — Groww ↩↩↩↩

-

Agarwal Float Glass India Ltd — Company profile and financials (sister entity) — Screener.in ↩↩↩

-

Agarwal Fortune India Ltd (formerly Devki Leasing and Finance Ltd) — Company profile — Investing.com India ↩↩↩↩↩

-

Agarwal Toughened Glass India Ltd — Stock scorecard, price and valuation — Trendlyne ↩

-

Agarwal Toughened Glass India Ltd — Corporate filings and preferential allotment announcements — National Stock Exchange of India, 2026-07-03 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube