Aether Industries: The Specialty Chemical Alchemists of India

I. Introduction & Episode Roadmap

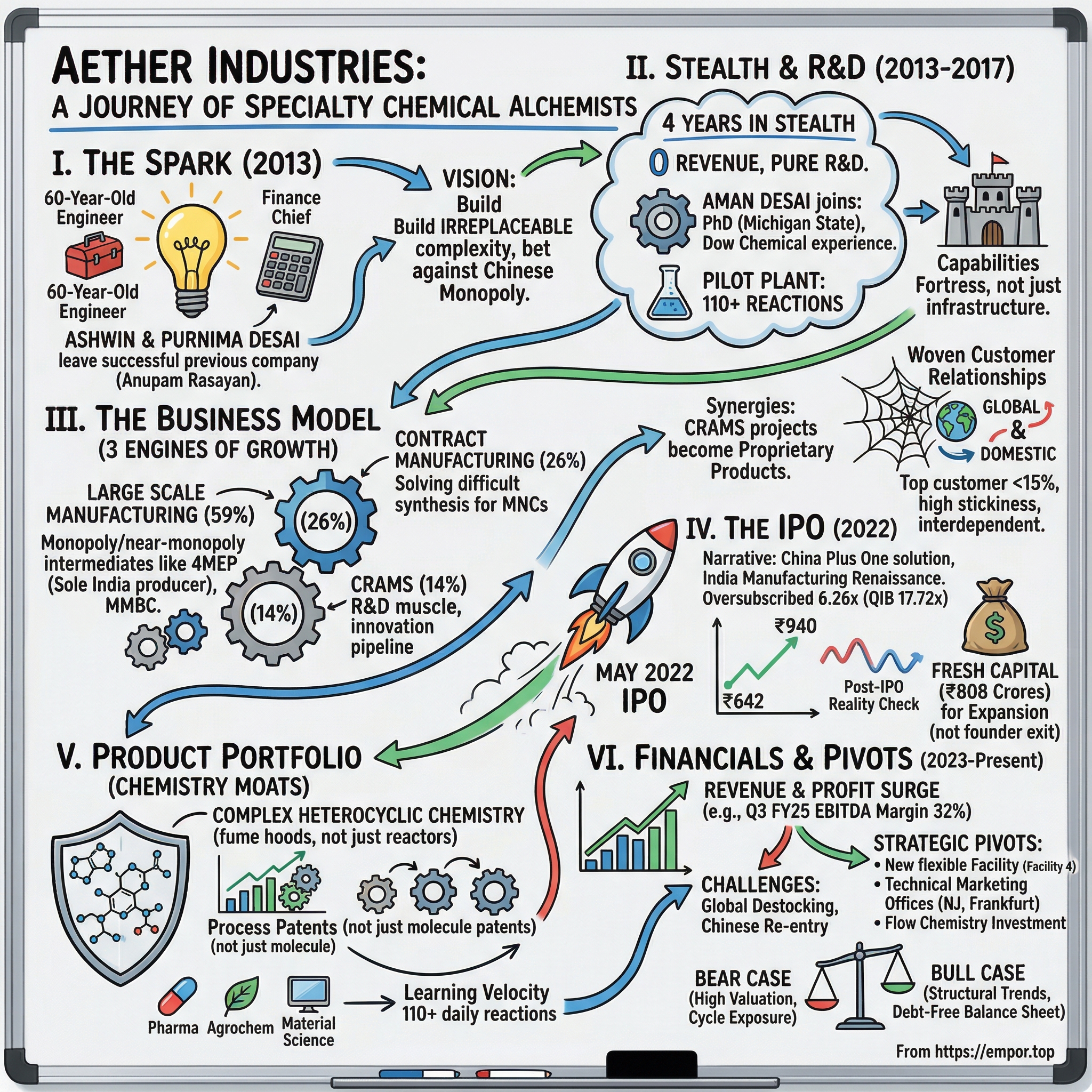

Picture this: A 60-year-old chemical engineer walks away from the successful company he built over four decades. His wife, the finance chief, joins him. Together, they start from scratch in 2013, spending four years in complete stealth mode—no revenue, no products, just pure R&D. By 2022, their new venture debuts on the Indian stock market valued at over $1 billion.

This is the story of Aether Industries—a specialty chemicals manufacturer that has quietly become the sole global producer of several critical chemical intermediates. While the world was obsessed with software unicorns and platform businesses, Ashwin and Purnima Desai were building something decidedly more tangible: a fortress of complex chemistry that even Chinese manufacturers couldn't replicate.

Aether isn't your typical chemical company churning out commodity products. They manufacture chemicals with names that sound like password suggestions—4-(2-Methoxyethyl) Phenol (4MEP), 3-Methoxy-2-Methylbenzoyl Chloride (MMBC), Thiophene-2-Ethanol (T2E). These tongue-twisters are the hidden ingredients in everything from advanced pharmaceuticals to high-performance photography materials. And here's the kicker: for many of these chemicals, Aether is the only manufacturer in India, and for some, one of the few globally.

The big question we're exploring today: How did a company founded in 2013 achieve a billion-dollar valuation in less than a decade, in an industry where Chinese dominance seemed insurmountable? The answer involves a unique blend of patient capital, second-generation expertise, and a contrarian bet that the world would eventually need an alternative to China's chemical manufacturing monopoly.

What you're about to discover is a masterclass in building irreplaceability. We'll explore how the Desais leveraged four decades of chemical industry experience to identify market gaps invisible to others, why they chose to operate in stealth for four years while burning cash, and how they structured a three-pronged business model that balances stability with explosive growth potential. We'll also dig into the post-IPO reality check—because not all that glitters in Dalal Street stays golden.

This isn't just a story about chemicals and valuations. It's about the evolution of Indian manufacturing, the power of deep technical expertise in an era obsessed with asset-light models, and what happens when a family business transforms into a public company. Buckle up for a journey through complex chemistry, family dynamics, and the art of building a moat molecule by molecule.

II. The Pre-History: From Anupam Rasayan to Aether

The year was 1976. India was in the throes of the Emergency, the economy was closed, and starting a chemical company meant navigating a labyrinth of licenses and permits. Yet in Surat—a city better known for diamonds and textiles—a young chemical engineer named Ashwin Desai decided to start Anupam Rasayan India Limited (ARIL).

Ashwin wasn't your typical entrepreneur. A 1974 graduate from the Institute of Chemical Technology in Mumbai (then UDCT), he possessed the rare combination of deep technical knowledge and commercial acumen. Over the next 37 years, he would transform ARIL from a small-scale operation into a Rs. 150 crore ($20 million) specialty chemicals company. But the real secret weapon wasn't just his chemical expertise—it was his partnership with his wife, Purnima.

While Ashwin handled the technical and strategic aspects, Purnima ran the financial engine of ARIL with military precision. She wasn't just keeping the books; she was instrumental in every critical decision, from capital allocation to customer negotiations. This wasn't a typical Indian family business where the wife played a ceremonial role—Purnima was a true co-architect of ARIL's success.

By 2013, ARIL was a well-oiled machine. They had established customers, steady cash flows, and a reputation for quality in the specialty chemicals space. Most 60-year-olds in their position would be thinking about succession planning or a comfortable retirement. The Desais had different plans.

The decision to leave ARIL wasn't born from failure or conflict—it was strategic foresight. Ashwin saw tectonic shifts happening in the global chemical industry. China's dominance was creating supply chain vulnerabilities. Environmental regulations were tightening. Pharmaceutical and agrochemical companies were desperately seeking alternative suppliers. But ARIL, with its existing commitments and structure, couldn't pivot fast enough to capture these opportunities.

"Sometimes, to build something truly transformative, you need to start with a clean slate," Ashwin would later tell investors. The Indian specialty chemicals landscape in 2013 was ripe for disruption. The industry was fragmented, with most players focused on commodity chemicals or simple intermediates. Complex chemistry—the kind that required sophisticated R&D and deep process knowledge—was still largely imported.

The Desais saw an opening that others missed. Their four decades in the industry had given them something invaluable: they knew which chemicals were critical yet undersupplied, which customers were desperate for alternatives to Chinese suppliers, and most importantly, which complex chemistries Indian manufacturers were avoiding because they were "too difficult."

Leaving behind a company you built over 37 years takes courage. Doing it at 60, when most of your peers are planning retirement, takes something more—vision mixed with audacity. The Desais weren't just starting another chemical company; they were architecting a new model for Indian specialty chemicals. And they were about to prove that in chemistry, as in life, sometimes the best reactions happen when you start with fresh reagents.

III. The Founding & Early R&D Phase (2013–2017)

Most companies measure their burn rate in months. Aether measured theirs in years. From 2013 to 2017, the company generated exactly zero revenue while pouring resources into R&D. In the startup world, this would be called a death march. In the Desais' playbook, it was called building a foundation.

The vision was audacious yet precise: create a niche in the global chemical industry through a creative approach to chemistry, technology, and systems. But unlike software startups that could iterate quickly, chemical R&D required patient capital and iron discipline. Every failed reaction was expensive. Every successful synthesis needed to be reproducible at scale. There were no shortcuts in chemistry.

The game-changer came when Aman Desai joined the venture. If Ashwin represented old-school chemical engineering wisdom, Aman embodied the new generation's scientific rigor. His credentials read like an academic's dream: a chemical technology degree from ICT Mumbai (following his father's footsteps), followed by a PhD in Organic Chemistry from Michigan State University. His doctoral research on novel synthetic methodologies had even been featured in Chemical & Engineering News—a rarity for graduate work.

But Aman wasn't just an academic. He'd spent years in the trenches at Dow Chemical's Process Development group, where he learned the art of scaling laboratory discoveries into industrial processes. At Dow, he'd seen how global chemical giants operated—their strengths, but more importantly, their blind spots. These blind spots would become Aether's opportunities.

The father-son dynamic could have been combustible. Chemical industry veterans often clash with PhD-wielding newcomers over "practical" versus "theoretical" approaches. Instead, it became synergistic. Ashwin brought market intelligence and customer relationships; Aman brought cutting-edge synthetic techniques and process optimization expertise. Purnima, meanwhile, managed the delicate cash flows required to sustain a company with no revenue.

During these four years, Aether built something remarkable: a pilot plant that could handle over 110 different reactions. This wasn't just infrastructure—it was a capability fortress. While competitors focused on scaling a few reactions, Aether was building the ability to tackle complex, multi-step syntheses that others wouldn't touch.

The company operated in complete stealth mode. No press releases, no industry conferences, no customer announcements. They were like chemists working in a sealed laboratory, carefully controlling every variable before revealing their results. The only visible sign of activity was the steady stream of patent applications and the growing team of PhD chemists joining from premier institutions.

By 2017, Aether had assembled a team of over 50 researchers and built capabilities spanning 25 different reaction types. They'd identified their target molecules—complex intermediates that were either monopolized by Chinese suppliers or simply not manufactured at scale anywhere. The R&D phase had validated their hypothesis: these molecules could be manufactured in India, profitably, and at quality levels exceeding Chinese alternatives.

The four-year "stealth mode" wasn't just about perfecting chemistry—it was about timing the market. By 2017, the global specialty chemicals industry was experiencing seismic shifts. Chinese environmental crackdowns were disrupting supply chains. Pharmaceutical companies were desperate for supply chain diversification. The stage was set for Aether's commercial debut.

Looking back, the 2013-2017 period seems almost quaint in its patience. In an era of "blitzscaling" and "move fast and break things," Aether chose to move deliberately and break nothing. Every molecule synthesized, every process optimized, every patent filed was a brick in an increasingly impregnable competitive moat. Revenue generation would begin in fiscal 2018, but the real value—the irreplaceable expertise and capabilities—had been building silently for four years.

IV. The Business Model Innovation: Three Engines of Growth

While most chemical companies pick a lane—either contract manufacturing or proprietary products—Aether built a three-cylinder engine that could fire on different strokes depending on market conditions. It's a model that sounds simple on paper but is devilishly complex to execute.

The first engine, Large Scale Manufacturing, accounts for 59% of revenue and represents Aether's crown jewels—advanced intermediates and specialty chemicals where they often hold monopoly or near-monopoly positions. These aren't commodity chemicals you can source from a dozen suppliers. We're talking about molecules like 4MEP, essential for advanced pharmaceuticals, where Aether is literally the only Indian manufacturer. When a global pharma giant needs this intermediate, they have perhaps two or three options worldwide. Aether is one of them.

The second engine, Contract Manufacturing (26% of revenue), leverages these same capabilities but puts them at the service of multinational corporations. This isn't typical toll manufacturing where you're just following someone else's recipe. Aether's contracts often involve taking a customer's problematic synthesis—maybe it's too hazardous, too complex, or too expensive in their current setup—and redesigning it using Aether's specialized capabilities. One executive described it as "chemical consulting with guaranteed outcomes."

The third engine, CRAMS (Contract Research and Manufacturing Services), contributes 14% of revenue but punches above its weight in strategic importance. This is where Aether flexes its R&D muscle, developing new synthetic routes, scaling up laboratory discoveries, and manufacturing high-value, low-volume products that might only need kilograms, not tons. It's also Aether's innovation pipeline—today's CRAMS project could become tomorrow's large-scale monopoly product.

Why is this three-pronged approach genius? Risk diversification is the obvious answer, but the real brilliance lies in the synergies. The same reactor that produces a proprietary intermediate on Monday can run a contract manufacturing batch on Wednesday and a CRAMS trial on Friday. The expertise gained from solving a complex CRAMS challenge can lead to a new proprietary product. Contract manufacturing relationships can evolve into joint development projects.

The "sole manufacturer" strategy deserves special attention. Becoming the only producer of a critical chemical isn't about being first—it's about being irreplaceable. Take MMBC, used in agrochemical synthesis. Aether didn't just figure out how to make it; they developed a process so efficient, so reliable, and so cost-effective that potential competitors looked at the market and decided it wasn't worth fighting for. When your total addressable market for a chemical is $50 million globally, there's often room for only one or two efficient producers.

This creates a beautiful dynamic: customers become dependent, but not resentful. They get reliable supply, consistent quality, and often better pricing than when multiple suppliers were racing to the bottom. Aether gets predictable demand, premium pricing power, and multi-year contracts. It's monopoly economics with a cooperative twist.

The customer diversification tells another story. As of March 2022, Aether's products reached over 34 global companies across 18 countries and more than 154 domestic companies. This isn't the typical Indian chemical company story of one anchor customer accounting for 40% of revenues. The largest customer represents less than 15% of sales. It's a portfolio approach to customer risk—lose one, and you don't lose the company.

But here's the masterstroke: many of these customer relationships are interwoven. A global agrochemical company might buy three different intermediates from Aether, have two products under contract manufacturing, and be jointly developing a new molecule through CRAMS. Switching away from Aether wouldn't just mean finding a new supplier—it would mean unwinding a complex web of interdependencies.

The model also provides exceptional capital efficiency. Unlike commodity chemicals where you need massive scale to compete on cost, specialty chemicals reward expertise over size. Aether's facilities are modest by chemical industry standards, but their output value per square meter rivals much larger operations. It's the difference between running a boutique that sells custom jewelry versus a warehouse that moves steel ingots.

As one industry analyst noted, "Aether has figured out something most chemical companies miss—in specialty chemicals, the specialty matters more than the chemicals." The three-engine model isn't just about diversification; it's about building a platform where technical expertise, customer relationships, and manufacturing capabilities reinforce each other in an ever-strengthening spiral.

V. The IPO Story: Perfect Timing or Lucky Break? (2022)

The drumbeat started in November 2021. Aether raised $13.5 million in a pre-IPO round, a relatively modest sum that suggested either extreme capital efficiency or exceptional confidence in public market reception. The smart money was betting on both.

By the time the IPO prospectus dropped in early 2022, the Indian capital markets were in a peculiar mood. The COVID pandemic had created a K-shaped recovery—tech stocks were soaring while traditional industries struggled. But beneath the surface, a different narrative was building. Supply chain disruptions had taught the world a harsh lesson about over-dependence on China. "China Plus One" wasn't just a strategy anymore; it was a survival imperative.

The IPO roadshow was a masterclass in narrative construction. The Desais didn't pitch Aether as just another chemical company. They positioned it as a solution to global supply chain anxiety, a play on India's manufacturing renaissance, and a bet on the irreplaceable value of deep technical expertise. The story resonated.

When the IPO bidding opened on May 24, 2022, the response was volcanic. The issue was oversubscribed 6.26 times, with the qualified institutional buyers' portion seeing 17.72 times subscription. The retail portion—usually the most conservative—was oversubscribed 1.14 times. For a specialty chemicals company that most retail investors couldn't even pronounce the products of, this was remarkable.

The pricing itself became a talking point. At ₹642 per share, Aether was asking investors to value the company at roughly ₹8,000 crores ($1.03 billion). For a company that had generated ₹590 crores in revenue in FY2021, this implied a price-to-sales ratio of about 13x—aggressive even by the frothy standards of 2022.

June 3, 2022, listing day, delivered the sugar rush investors craved. The stock opened at ₹708, a 10.3% premium to the issue price, and surged to ₹772 intraday—a 20% pop that had financial media channels running celebratory graphics. The market cap briefly touched ₹9,600 crores. Ashwin and Purnima Desai, who retained about 40% stake, were paper billionaires.

But even in the euphoria, shrewd observers noticed something interesting. Unlike typical IPOs where promoters cash out partially, the Desais didn't sell a single share. The entire IPO consisted of fresh capital raised for the company—₹808 crores that would fund expansion, not enrich founders. This wasn't an exit; it was a beginning.

The use of proceeds revealed the real strategy. About ₹400 crores was earmarked for a new manufacturing facility, ₹160 crores for working capital, and the rest for debt repayment and general corporate purposes. Aether wasn't raising capital to experiment—they had a clear roadmap for deployment.

Post-IPO performance, however, would provide a reality check. The stock peaked at ₹940 in September 2022, then began a slow, grinding descent. By March 2023, it was trading below the issue price. The global specialty chemicals sector was facing headwinds—inventory destocking, demand softness, and ironically, a resurgent Chinese chemical industry as COVID restrictions lifted.

The management's response was telling. Instead of panicking, they announced a Qualified Institutional Placement (QIP) in 2023, raising additional capital at a discount to the IPO price. The message was clear: short-term stock movements were noise; Aether was building for the long term.

Looking back, the IPO timing seems both perfect and problematic. Perfect because it caught the peak of market exuberance around manufacturing and China Plus One themes. Problematic because it set expectations that even exceptional execution would struggle to meet. The stock's journey from ₹642 to ₹940 to below ₹600 and back up again became a Rorschach test for investors—bulls saw buying opportunities, bears saw overvaluation correcting.

But perhaps the most important outcome of the IPO wasn't the capital raised or the valuation achieved. It was the transformation of Aether from a family enterprise to a public institution. Quarterly earnings calls replaced informal family meetings. Professional managers joined the founding family. The company that had operated in stealth for four years was now under the harsh glare of public scrutiny.

One fund manager who participated in the IPO reflected, "The IPO wasn't just about Aether going public. It was about Indian specialty chemicals announcing itself on the global stage." Whether that announcement was premature or prescient, only time would tell.

VI. The Product Portfolio: Chemistry as Competitive Advantage

Walk into Aether's R&D facility, and you'll find something unusual for an Indian chemical company: PhD chemists actually excited about their work. They're not just following standard procedures or optimizing known reactions. They're solving puzzles that have stumped the global chemical industry.

Take 4-(2-Methoxyethyl) Phenol, or 4MEP, Aether's flagship monopoly. This molecule is critical for synthesizing advanced pharmaceutical intermediates, particularly for cardiac and central nervous system drugs. The challenge isn't just making it—any competent chemist with the right equipment could manage that. The challenge is making it at 99.9% purity, in thousand-kilogram batches, consistently, while managing hazardous intermediates and meeting pharmaceutical-grade specifications.

Aether's process for 4MEP involves a seven-step synthesis with three isolation points. Each step has been optimized over thousands of iterations. The company holds process patents not for the molecule itself—that's been known for decades—but for their specific method of making it efficiently and safely. When a global pharma company evaluated alternative suppliers, they found that matching Aether's quality would require an investment of $15-20 million and at least two years of development. For a product with a global market of maybe $40 million, the math didn't work. Aether's monopoly was secure.

The portfolio spans an impressive range of chemistry. MMBC serves the agrochemical industry, particularly in manufacturing strobilurin fungicides—the same class that keeps the world's wheat and soybean crops disease-free. Thiophene-2-Ethanol (T2E) goes into advanced material science applications, including organic semiconductors that might power the next generation of flexible displays. OTBN is a key intermediate for specialty pigments that provide the deep blacks in automotive coatings.

But the real competitive advantage isn't any single molecule—it's Aether's ability to handle complexity that others avoid. Their specialty is heterocyclic chemistry, dealing with ring structures containing different elements. These reactions are notoriously finicky, sensitive to temperature, pressure, and trace impurities. One Aether chemist described it as "cooking a soufflé in an earthquake—possible, but you need to know exactly what you're doing."

The R&D fortress generates staggering productivity. Conducting over 110 reactions daily isn't just about volume—it's about learning velocity. Each reaction generates data: yields, impurity profiles, reaction kinetics. This data feeds into process optimization algorithms that can predict how changes in temperature, pressure, or catalyst loading will affect outcomes. It's big data meets chemistry, and it's happening in Surat, not Silicon Valley.

The company's patent strategy is equally sophisticated. Rather than patenting molecules (which competitors could work around), Aether patents processes, purification techniques, and analytical methods. They've created a thicket of intellectual property that makes competing not illegal, but economically irrational.

Consider their approach to Bifenthrin Alcohol, a key intermediate for pyrethroid insecticides. The molecule itself is off-patent, but Aether's process reduces solvent consumption by 60% and eliminates two hazardous intermediates compared to the standard route. Their production cost is 30% lower than Chinese competitors, but that's not why customers choose them. They choose Aether because the company can guarantee supply even when Chinese plants shut down for environmental inspections, Olympics, or political conferences.

The application diversity provides resilience. Pharmaceuticals account for about 40% of revenue, agrochemicals 30%, material science 15%, and the rest spread across coatings, photography, and oil and gas applications. When pharma demand softened in 2023 due to inventory corrections, agrochemical demand picked up the slack. It's portfolio theory applied to chemical manufacturing.

The R&D pipeline suggests the next phase of growth. Aether is developing intermediates for EV battery electrolytes, next-generation OLED materials, and biosimilar pharmaceuticals. These aren't incremental advances—they're bets on entirely new categories where early movers could establish the same kind of dominant positions Aether enjoys in its current portfolio.

One visiting analyst noted something telling: "Most chemical companies show you their reactors and talk about capacity. Aether shows you their fume hoods and talks about chemistry. That tells you everything about where their competitive advantage really lies."

The product portfolio isn't just a collection of molecules—it's a carefully curated demonstration of capabilities. Each product tells potential customers: "If we can make this incredibly complex molecule that no one else will touch, imagine what we could do for you." In specialty chemicals, that's the ultimate sales pitch.

VII. Financial Performance & Unit Economics

The numbers tell a story of explosive growth followed by reality's gravitational pull. Between fiscal 2018 (when revenue generation began) and fiscal 2021, Aether grew at a CAGR of nearly 60%—the kind of growth rate you expect from software companies, not chemical manufacturers dealing with physical molecules and regulatory approvals.

The trajectory was remarkable: from essentially zero revenue in FY2017 to ₹590 crores in FY2022, reaching ₹651 crores in FY2023. Net profit followed suit, climbing from ₹108.92 crores in FY2022 to ₹130.41 crores in FY2023. For a capital-intensive industry where many players struggle to maintain double-digit margins, Aether was printing EBITDA margins north of 25%.

But the real story lies in the unit economics. Unlike commodity chemicals where you win on scale, Aether's model rewards value over volume. A kilogram of their specialty intermediate might sell for ₹50,000, while the raw materials cost ₹15,000. The ₹35,000 gross margin has to cover energy, labor, depreciation, and R&D, but when you're the only manufacturer, you have pricing power that commodity players can only dream of.

The capital efficiency is striking. With a gross block of about ₹400 crores in FY2023, Aether generated ₹651 crores in revenue—an asset turnover ratio of 1.6x. Compare this to typical chemical companies that struggle to achieve 1x, and you understand why investors were initially enthusiastic. This isn't about sweating assets; it's about smart asset deployment.

Being almost debt-free amplifies returns. While competitors leverage up to build scale, Aether funded growth through internal accruals and equity. The interest coverage ratio is essentially infinite—there's barely any interest to cover. This might seem overly conservative, but in a cyclical industry where downturns can be brutal, a clean balance sheet is like wearing a life jacket while others swim naked.

The working capital cycle reveals operational excellence. Aether typically operates with a cash conversion cycle of 90-100 days—impressive for a B2B chemical company dealing with large corporations that love to stretch payables. The company manages this through a combination of advance payments for critical products (the benefit of being a monopoly supplier) and strict credit controls.

But FY2024 brought challenges. Global destocking in pharmaceuticals and agrochemicals hit demand. Chinese competitors, recovering from COVID restrictions, aggressively re-entered markets. Aether's revenue growth slowed, margins compressed, and the stock market's love affair cooled. The return on equity, which had peaked above 20%, settled to a more modest 8.42% over the last three years—respectable but not spectacular.

The Q3 FY2025 results, however, suggest a turnaround. Profit before tax jumped 112.26% year-on-year to ₹64.08 crores. EBITDA grew 109.12% to ₹75.7 crores, with margins expanding from 22% to 32%. The company attributed this to better product mix, operational efficiencies, and new customer additions. Critics wondered if this was sustainable or just inventory restocking.

The 2023 QIP raise added complexity to the financial picture. Raising capital at a discount to the IPO price was optically challenging, but it funded the fourth manufacturing facility without taking on debt. Management argued this was opportunistic—grabbing growth capital when available rather than when desperately needed. Shareholders saw dilution.

Breaking down the segment performance reveals interesting dynamics. Large Scale Manufacturing maintains the highest margins (around 35% EBITDA) but grows slowly. Contract Manufacturing offers lower margins (20-25%) but provides steady cash flows. CRAMS is marginally profitable but strategically crucial—today's development project is tomorrow's high-margin product.

The R&D spend deserves attention. At about 3-4% of revenue, it's higher than typical Indian chemical companies but lower than global innovators. This reflects Aether's positioning—not quite a pure R&D play, not quite a pure manufacturing play, but something in between. The company calls it "pragmatic innovation"—enough R&D to stay ahead, not so much that it kills current profitability.

Free cash flow generation remains robust. Even after capital expenditure for expansion, Aether generates positive free cash flow—the ultimate test of a business model's sustainability. This cash funds both growth and provides a buffer against industry volatility.

One metric that doesn't appear in standard financials but matters enormously: customer stickiness. Once a pharmaceutical or agrochemical company qualifies Aether as a supplier, switching costs are enormous—regulatory requalification, process revalidation, supply chain adjustment. This creates an annuity-like revenue stream that traditional financial metrics don't fully capture.

The financial performance story isn't one of unblemished success. It's a narrative of explosive early growth, market reality checks, and ongoing adaptation. The question for investors isn't whether Aether can maintain 60% growth—that's clearly unsustainable. It's whether the company can consistently deliver 15-20% growth with 25-30% EBITDA margins while maintaining its competitive moats. Early indications suggest yes, but the chemical industry has a way of humbling the overconfident.

VIII. Recent Developments & Strategic Pivots (2023–Present)

The December 2024 quarter results landed like a vindication letter to patient shareholders. Profit before tax surging 112% year-on-year wasn't just a number—it was Aether announcing that the post-IPO stumble was temporary, not terminal. EBITDA margins expanding from 22% to 32% told an even more important story: the company had successfully navigated the brutal destocking cycle that hammered chemical companies globally.

But the real strategic pivot wasn't in the numbers—it was in the ambition. The fourth manufacturing facility, funded by the 2023 QIP, represents more than capacity addition. It's Aether's bet on the next decade of chemistry. While existing facilities focus on current portfolio products, the new facility is designed for flexibility—able to handle everything from gram-scale development to ton-scale production, from -80°C cryogenic reactions to 300°C high-temperature processes.

The international expansion strategy has evolved from opportunistic exports to deliberate market development. Aether opened technical marketing offices in New Jersey and Frankfurt—not sales offices, but technical centers staffed with PhD chemists who can speak the language of Big Pharma's process development teams. The message is clear: Aether isn't just a low-cost Indian supplier; they're a technical partner who happens to have cost advantages.

New contract wins tell another story. In 2024, Aether signed multi-year agreements with two top-10 global agrochemical companies—names they can't disclose, but the stock market figured it out from the sudden capacity expansion announcements. These aren't typical supply agreements. They're "innovation partnerships" where Aether develops new routes to existing molecules, sharing the value created through cost reduction or environmental improvement.

The company's approach to the China challenge has been particularly clever. Rather than competing head-to-head on products where Chinese manufacturers have scale advantages, Aether is focusing on molecules that China is voluntarily exiting due to environmental concerns. When Jiangsu province shut down 40% of its chemical plants in 2023, Aether's order book swelled—not because they were cheaper, but because they were available.

Management changes have been subtle but significant. While the Desais remain firmly in control, professional managers now run key divisions. The head of R&D came from Dr. Reddy's, the supply chain chief from BASF, the sustainability officer from Dow. It's a careful balance—maintaining the entrepreneurial culture while adding corporate sophistication.

The sustainability push deserves special mention. Aether's new processes reduce solvent consumption by 40% and energy usage by 25% compared to industry standards. This isn't just greenwashing—it's a competitive advantage. When European customers face pressure to reduce Scope 3 emissions, Aether's processes help them meet targets. The company's "Green Chemistry Score"—a proprietary metric combining various environmental factors—has become a key selling point.

Stock performance has been a roller coaster. From the IPO price of ₹642, the stock surged to ₹940, crashed to ₹520, and has been climbing back since. Trading around ₹700-800 in recent months, it's been a test of investor conviction. The volatility reflects the market's struggle to value a company that's part commodity chemical producer, part innovation platform, part India manufacturing story.

The competitive landscape is shifting in Aether's favor. Chinese environmental regulations continue tightening. Indian competitors are struggling to match Aether's technical capabilities. Global customers are mandating supply chain diversification. It's a confluence of factors that management calls a "once-in-a-generation opportunity"—though they're careful to add that opportunities still require execution.

Recent capacity utilization data provides comfort. The existing three facilities are running at 75-80% utilization—high enough to generate strong returns, low enough to accommodate growth without immediate expansion needs. The fourth facility, coming online in 2025, isn't about meeting current demand—it's about being ready for the next wave.

The most intriguing development might be Aether's quiet move into flow chemistry—continuous manufacturing processes that could revolutionize how specialty chemicals are made. While competitors build bigger batch reactors, Aether is investing in modular flow systems that can produce the same output in 1/10th the space with 1/5th the energy. It's the kind of technological leap that could render traditional chemical manufacturing obsolete.

One analyst who recently visited the company noted a cultural shift: "Three years ago, they talked about being the best in India. Now they benchmark against Lonza and Albemarle. The ambition has scaled with the capability."

The strategic pivots of 2023-2024 reveal a company in transition—from fast-growing startup to sustainable market leader, from Indian supplier to global partner, from family business to professional enterprise. The growing pains are evident, but so is the potential. Whether Aether can execute on these ambitions while maintaining its competitive moats will determine if the stock's current valuation is a bargain or a trap.

IX. Playbook: Business & Investing Lessons

The "patient capital" approach Aether employed from 2013-2017 feels almost antiquated in today's hypergrowth startup ecosystem. Four years without revenue, funded entirely by the founders' previous success, burning cash on R&D with no guarantee of success—it's a playbook that would make venture capitalists nervous. Yet it worked precisely because chemistry doesn't follow software timeline rules.

Building irreplaceability through sole manufacturing positions is perhaps Aether's greatest strategic insight. It's not about being the biggest or cheapest—it's about being the only option for critical molecules. When you're the sole manufacturer of a pharmaceutical intermediate that goes into a $1 billion drug, your customer isn't negotiating price—they're ensuring supply. The lesson: in specialty markets, uniqueness trumps scale.

The family business dynamics offer a masterclass in succession planning. Rather than the typical Indian business story of second-generation children fighting for control or being handed sinecures, Aman Desai earned his position through a decade of education and experience at world-class institutions. He brought capabilities the founders couldn't have developed themselves—modern synthetic techniques, process analytical tools, global R&D best practices. The integration of old wisdom and new knowledge created something neither generation could have built alone.

The specialty chemicals opportunity in India versus China is often misunderstood. It's not about India being cheaper—Chinese manufacturing at scale is still often more cost-effective. It's about India offering something different: regulatory stability, intellectual property protection, English-language technical communication, and increasingly, sustainability credentials. Aether understood this distinction and positioned accordingly.

The timing of going public reveals another lesson: market readiness and business readiness rarely align perfectly. Aether went public when the market was euphoric about manufacturing and China Plus One themes, even though the business was just hitting its growth stride. They traded future flexibility for current capital, a decision that looks prescient given how quickly market windows can close.

The three-pronged business model—large scale manufacturing, contract manufacturing, and CRAMS—teaches portfolio theory applied to operations. Each segment hedges the others' weaknesses. When proprietary products face pricing pressure, contract manufacturing provides stable cash flows. When contract manufacturing margins compress, CRAMS projects offer innovation upside. It's diversification at the business model level, not just the product level.

Customer concentration risk management shows sophisticated thinking. By keeping even the largest customer below 15% of revenue and creating multiple touchpoints with each customer across different products and services, Aether built a web of relationships rather than dependent partnerships. Losing a customer hurts but doesn't cripple.

The R&D investment philosophy—enough to innovate, not so much as to destroy profitability—represents pragmatic innovation. Unlike pure R&D companies that burn cash hoping for breakthrough discoveries, or pure manufacturers that avoid innovation costs, Aether found a middle path. They invest in R&D that has clear commercial pathways, usually solving specific customer problems rather than pursuing blue-sky research.

The approach to intellectual property is instructive. Rather than relying solely on patents (which expire and can be challenged), Aether builds moats through process complexity, trade secrets, and customer relationships. Their competitive advantage is less about what they know and more about their ability to execute what they know reliably and at scale.

The capital allocation framework deserves study. Despite having access to cheap debt and generating strong cash flows, Aether chose to remain largely debt-free. This might seem overly conservative, but in a cyclical industry where downturns can be severe, a clean balance sheet provides options that leveraged competitors lack. When the 2023 downturn hit, Aether could invest in expansion while competitors struggled to service debt.

The international expansion strategy—technical centers before sales offices—flips the typical approach. Instead of trying to sell existing products into new markets, Aether first understands what those markets need, then develops solutions. It's customer-pull rather than product-push, and it's why their international revenue has grown despite intense competition.

For investors, Aether presents a fascinating case study in valuation complexity. How do you value a company that's part commodity chemical producer (deserving industrial multiples), part innovation platform (deserving higher multiples), and part India manufacturing story (deserving growth premiums)? The market's volatility in pricing Aether reflects this fundamental uncertainty.

The biggest lesson might be about building moats in supposedly commoditized industries. Chemicals are often viewed as undifferentiated commodities where only scale and cost matter. Aether proved that even in chemicals, specialization, technical expertise, and customer intimacy can create sustainable competitive advantages. They turned chemistry from a commodity into a capability.

The playbook isn't easily replicable—it requires patient capital, deep technical expertise, and fortuitous timing. But the principles—focus on irreplaceability, balance innovation with profitability, diversify strategically, and build capabilities before chasing revenue—apply far beyond chemicals. In any industry where technical complexity meets customer criticality, the Aether playbook offers a roadmap for building enduring value.

X. Analysis & Bear vs. Bull Case

The Bull Case: Chemistry Creating Asymmetric Upside

Bulls see Aether as a coiled spring, temporarily compressed by industry headwinds but ready to expand as structural trends align in its favor. The monopoly positions in critical chemicals aren't just market share statistics—they're licenses to print money when demand normalizes. When you're the sole manufacturer of an intermediate that goes into a blockbuster drug or a widely-used agrochemical, pricing power isn't theoretical—it's contractual.

The debt-free balance sheet isn't just conservative financial management—it's optionality in a volatile world. While leveraged competitors will struggle when the next downturn hits (and in chemicals, downturns are inevitable), Aether can play offense, acquiring distressed assets, hiring talent from struggling rivals, or investing in capacity when others are retrenching. The clean balance sheet is a call option on industry distress.

China Plus One isn't a temporary pandemic phenomenon—it's a structural shift in global supply chain thinking. Every supply chain audit, every business continuity plan, every regulatory compliance review now asks: "What's our China exposure?" Aether isn't just benefiting from this trend; they're one of the few Indian companies actually capable of absorbing the demand shift. When a global pharma company needs an alternative to their Chinese supplier, they don't want promises—they want proven capabilities. Aether has them.

The R&D capabilities and patent portfolio represent hidden value not reflected in current valuations. With over 20 patents and a pipeline of molecules in development, Aether is building tomorrow's monopolies today. The market values them like a chemical manufacturer, but they're increasingly resembling a specialty pharma company—developing molecules, owning intellectual property, capturing value through innovation.

Bulls point to the Q3 FY2025 results as validation. EBITDA margins expanding to 32% isn't just operational leverage—it's evidence that Aether's products command premium pricing when supply chains normalize. The 112% year-on-year profit growth suggests the company has pricing power that commodity chemical producers can only dream of.

The fourth manufacturing facility, coming online in 2025, isn't just capacity addition—it's a platform for the next phase of growth. Designed for flexibility and equipped for complex chemistry, it positions Aether to capture opportunities in emerging areas like EV battery chemicals and next-generation pharmaceutical intermediates.

The Bear Case: Gravity Reasserting Itself

Bears see a different story—a company priced for perfection in an imperfect industry. The low return on equity of 8.42% over the last three years isn't a temporary blip—it's evidence that the business model, while impressive, doesn't generate the returns that justify premium valuations. When you can get better returns from a fixed deposit than from equity in a "high-growth" chemical company, something's wrong.

Customer concentration, while managed, remains a fundamental risk. Yes, the largest customer is below 15% of revenue, but the top 10 customers likely account for over 50%. In specialty chemicals, customer relationships can change quickly—a procurement manager's cost-cutting mandate, a strategic shift to backward integration, a competitive Chinese offer that's too good to refuse. The web of relationships that bulls celebrate can unravel faster than it was woven.

The commodity cycle exposure is real and unavoidable. Specialty chemicals might command better margins than commodities, but they're not immune to cycles. When pharma companies destock, when agrochemical demand softens, when industrial production slows, specialty chemical suppliers feel the pain. Aether's FY2024 struggles weren't company-specific—they were industry-wide, and they'll happen again.

Valuation concerns are legitimate. Even after the correction from post-IPO highs, Aether trades at multiples that assume continued high growth and margin expansion. But chemistry has limits—reactions only go so fast, plants only run so many hours, markets only absorb so much product. The physical constraints of chemical manufacturing put a ceiling on growth that software companies don't face.

Chinese competition isn't disappearing—it's evolving. Yes, environmental regulations have shut down some Chinese capacity, but the survivors are stronger, more efficient, and increasingly sophisticated. Chinese chemical companies are moving up the value chain, investing in R&D, and building relationships with global customers. The window of opportunity from China's environmental challenges is closing.

The innovation pipeline, while impressive, faces a harsh reality: not every R&D project succeeds. For every successful new molecule, there are multiple failures—expensive failures that consume resources and deliver nothing. The market prices Aether as if every development project will succeed, but chemistry doesn't offer such certainties.

Bears also worry about execution risk as the company scales. Managing three facilities with 300 employees is different from managing four facilities with 500 employees. The family business culture that drove early success might not scale to institutional size. Professional managers might optimize operations but lose the entrepreneurial edge.

The Balanced View

The truth, as usual, lies somewhere in between. Aether has built something genuinely impressive—a specialty chemical company with real moats, strong capabilities, and favorable positioning for structural trends. But it operates in a cyclical, competitive industry where success attracts competition and today's monopoly can become tomorrow's commodity.

The company's ability to navigate the next few years will determine which narrative prevails. Can they successfully commercialize their R&D pipeline? Can they maintain margins as competition intensifies? Can they scale operations without losing their technical edge? These aren't predetermined outcomes—they're challenges requiring continued exceptional execution.

For investors, Aether represents a classic risk-reward calculation. The potential upside—becoming India's specialty chemical champion, expanding internationally, capturing value from innovation—is substantial. But the risks—cycle exposure, competition, execution challenges—are equally real. It's not a bet for the faint-hearted or the short-term oriented.

XI. Epilogue & "If We Were CEOs"

If we were sitting in Ashwin Desai's chair today, looking out at the next decade, the strategic choices would be both obvious and agonizing. The obvious part: continue investing in R&D, expand capacity, deepen customer relationships. The agonizing part: deciding where to place the big bets that will define Aether's next chapter.

The first move would be doubling down on the innovation engine, but with a twist. Instead of just building R&D capabilities, we'd create an "Aether Labs" in Boston or Basel—not to replace the Surat R&D center, but to tap into cutting-edge academic research and biotech innovation. The future of specialty chemicals isn't just in making existing molecules better—it's in designing entirely new molecules for emerging applications. Think custom molecules for mRNA vaccines, designer intermediates for gene therapies, or novel materials for quantum computing.

The second strategic shift would be vertical integration, but selectively. We wouldn't try to control the entire value chain—that's a capital allocation nightmare. Instead, we'd backward integrate into 2-3 critical raw materials where supply security matters more than cost optimization. Forward integration would be even more selective—perhaps acquiring a small custom synthesis company in Europe or the US that gives us direct access to innovator pharmaceutical companies.

The China strategy needs a rethink. Rather than viewing China as just competition, we'd explore partnership opportunities. A joint venture with a Chinese company for large-volume, lower-margin products could free up Aether's capacity for higher-value work while providing scale advantages. It's counterintuitive, but in chemicals, sometimes your competitor is your best partner.

Geographic expansion would follow customers, not markets. Instead of trying to build facilities in multiple countries, we'd create a network of partnerships—toll manufacturing agreements in key markets, technical collaboration centers near customer R&D hubs, strategic inventory positions to ensure rapid response. Physical assets matter less than responsive capabilities.

The talent strategy would be revolutionary for an Indian chemical company. We'd implement an "entrepreneur-in-residence" program, bringing in scientists with startup experience to lead new product development. Stock options would vest based on successful product commercialization, not just time served. The goal: create an ownership mindset at every level.

On the financial front, we'd consider a dual-listing in the US or Europe—not just for capital access, but for visibility among global customers and talent. The current NSE listing limits Aether's institutional investor base and analyst coverage. A NASDAQ or LSE listing would position Aether as a global specialty chemical company that happens to be based in India, not an Indian company trying to go global.

The biggest strategic question: Can Aether become India's BASF? The comparison might seem presumptuous—BASF has 150 years of history and €70 billion in revenue. But BASF started as a dye manufacturer in Mannheim, building chemistry capabilities that eventually spanned industries. Aether has the technical foundation, the entrepreneurial culture, and the market opportunity. What it needs is the ambition to think beyond being a successful specialty chemical company to becoming a chemical innovation platform.

The next decade will likely see consolidation in the Indian specialty chemical space. Aether could be an acquirer, rolling up smaller players with complementary capabilities. Or it could be acquired itself—global chemical giants are looking for Asian growth platforms, and Aether's capabilities would be attractive to companies like Clariant, Lonza, or even private equity players.

The EV revolution presents a particularly intriguing opportunity. Battery chemistry, thermal management materials, lightweight composites—all require specialty chemicals that don't exist at scale today. Aether's ability to develop and scale complex molecules positions it perfectly for this transition. We'd create a dedicated EV chemicals division, staffed with electrochemists and materials scientists, targeting the 2030 market when EV production really scales.

The sustainability angle can't be ignored. We'd set an ambitious target: become carbon neutral by 2035, not through offsets but through process innovation. Every new process would be evaluated not just on yield and cost, but on carbon intensity. This isn't just environmental responsibility—it's anticipating where customer demands and regulatory requirements are heading.

Looking back at the journey from 2013 to 2024, the biggest surprise isn't Aether's success—it's how quickly a focused, technically competent company can build moats in a supposedly commoditized industry. The Desais proved that in specialty chemicals, as in life, it's better to be irreplaceable than important.

The final reflection: Aether's story is still being written. Whether it becomes a case study in building enduring value or another example of early promise unfulfilled depends on decisions being made today in Surat boardrooms and R&D labs. For investors, customers, and competitors, Aether remains one of the most interesting experiments in Indian manufacturing—a test of whether technical excellence, patient capital, and entrepreneurial ambition can create a global champion from an unlikely origin.

The specialty chemical industry doesn't often produce dramatic narratives. It's a world of incremental improvements, patient development, and compound growth. But occasionally, a company like Aether emerges—turning chemistry into alchemy, transforming molecules into moats, building a billion-dollar business from beakers and reactors. That's a story worth following, whether you're an investor, an entrepreneur, or simply someone who believes that making things still matters in an increasingly digital world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube