Aequs: The Ecosystems of Efficiency

I. Introduction: The "Toy Story" Meets "Top Gun"

Picture a flat-bed truck rolling out of a 250-acre walled compound on the dusty outskirts of ಬೆಳಗಾವಿ Belagavi, a Tier-2 city in northern Karnataka that most foreign investors would struggle to find on a map. On that truck sit two pallets. Pallet number one carries titanium and aluminium-alloy structural parts, each piece machined to a tolerance finer than a strand of human hair, destined for the wing of an Airbus A320 in Toulouse. Pallet number two carries injection-moulded polymer assemblies, also produced to obsessive specifications, but their destination is a Hasbro warehouse where they will be glued, painted, and packaged as the latest Transformers action figure for a Christmas shelf in Cincinnati.

Same compound. Same week. Same company. A 10-micron mindset feeding both the global aerospace duopoly and the global toy duopoly. Welcome to Aequs.[^1]

The question that should be running through every investor's head: how on earth does a single Indian company, listed on the National Stock Exchange under the ticker AEQUS.NS, end up supplying flight-critical hardware to Airbus, Boeing, Safran, and Collins Aerospace, while simultaneously turning out toys for Hasbro and Spin Master and stainless-steel cookware in partnership with Brazil's Tramontina?[^2]1 The boring answer is "contract manufacturing." The interesting answer — and the one we are going to spend the next two hours on — is that Aequs is not really a contract manufacturer at all. It is an ecosystem operator.

The thesis is deceptively simple. Most of the world's high-value physical goods, from a fan blade for a LEAP engine to the chassis of a remote-control car, share a common production grammar: forge, machine, surface-treat, assemble, certify, ship. In nearly every country, those steps are performed by separate companies in separate cities, with finished work-in-progress hauled hundreds of kilometres on creaking trucks between them. Aequs founder Aravind Melligeri's bet was that if you stuffed all of those steps into one fenced-in industrial cluster — what the company internally calls an "ecosystem of efficiency" — you could shave weeks off the cycle, points off the cost, and crucially, the freight subsidy that China has historically enjoyed.2

The market is taking that bet seriously. Following its 2025 listing, Aequs commanded a valuation in the low single-digit-billion-dollar range, putting it firmly in the conversation alongside its closest Indian peer Azad Engineering and ahead of most domestic aerospace ancillary suppliers.[^5] It is, in capital-markets shorthand, a billion-dollar pure-play on what global supply-chain consultants love to call "China Plus One" — the post-COVID, post-Trump, post-Ukraine scramble by Western OEMs to diversify production out of mainland China without sacrificing cost.

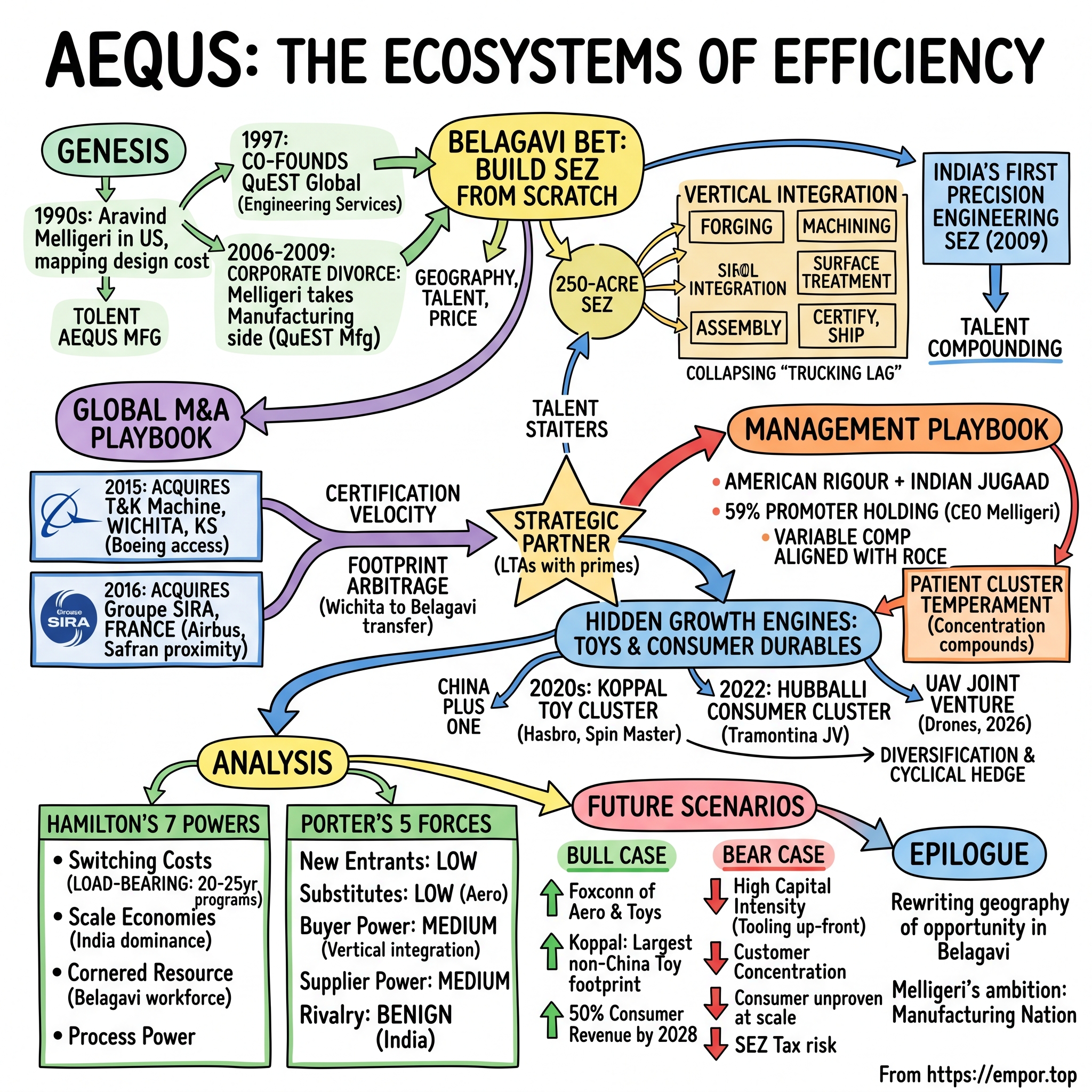

Over the next ten sections we will trace the arc: from Aravind Melligeri's first life as the co-founder of engineering services giant QuEST Global, through the audacious decision to plant India's first precision engineering SEZ in a town more famous for sugar mills than supersonic alloys, through a transatlantic acquisition spree, and into the strange but strategically luminous move into toys, cookware, and now drones. By the end you should understand not just what Aequs does, but why its particular architecture — clustered, vertically integrated, certification-protected — may be one of the more durable industrial moats being built in 2026. Let's start where every Aequs story actually starts: not with an airplane, but with an engineering services contract.

II. The Genesis: Engineering Services to Hard Assets

In the late 1990s, a young Karnataka-born engineer named ಅರವಿಂದ್ ಮೆಲ್ಲಿಗೇರಿ Aravind Melligeri found himself in the unglamorous Bethlehem of American engineering — Pratt & Whitney's facilities in Connecticut — staring at jet-engine blades and quietly mapping how every drawing in front of him could be redrawn in India for a third of the cost.2 He had arrived in the United States as a Penn State graduate student, trained in engineering, and discovered, like so many Indian technologists of his generation, that the global aerospace industry was effectively run on CAD files, finite element simulations, and stress analyses — work that could in principle be done anywhere there was a brain and a workstation.

In 1997, alongside Ajit Prabhu — another US-based Indian engineer who would become Aequs's intellectual sparring partner — Melligeri co-founded QuEST Global, a pure-play engineering services firm targeting the global aerospace, energy, and transportation primes. The timing was almost embarrassingly good. India's outsourcing wave was about to crash. ಇನ್ಫೋಸಿಸ್ Infosys, Wipro, and TCS had cracked open Western IT budgets. Now QuEST was opening the next door: high-end mechanical and aerospace engineering, the stuff that touched real metal and real lives. By the mid-2000s, QuEST was working with most of the global aerospace and gas-turbine OEMs, and it would eventually become one of the world's largest pure-play engineering services firms.2

But here is where the story takes its formative turn — the moment of disquiet that gives every great founder his second act. Sitting in QuEST review meetings, Melligeri kept noticing something. The Indian engineers were the ones doing the heavy intellectual lifting — the CFD modelling, the stress simulations, the design iteration. And yet, every time their drawings hit a foundry or a machining centre, the value capture vanished into the West. The engineering hours billed at $40. The forged titanium ring that came back, two months later, billed at $40,000. India had become very good at designing. The world was still printing money by building.

You can almost imagine the late-night whiteboard sessions: if engineering services is a 15% EBITDA business with a constant flight risk for talent, then precision manufacturing — properly capitalised, properly certified, properly clustered — is a 20%+ EBITDA business with a 20-year customer lock-in. The strategic prize was obvious. The execution path was terrifying. Building a precision-machining facility for aerospace is not a software project; it is a decade-long, capital-devouring, certification-gated industrial slog.

Between 2006 and 2009, Melligeri and Prabhu engineered what was effectively a corporate divorce by mutual respect. The manufacturing arm of QuEST — initially called QuEST Manufacturing — was carved out as a separate entity, with Aravind taking the manufacturing side and Ajit retaining the services business that remains QuEST Global today.2 Both companies would prosper. But the deeper insight was Aequs's alone: in a world where every Tier-1 aerospace supplier wanted to de-risk China, an integrated, certified, low-cost Indian hard-assets manufacturer would be playing a multi-decade game with structural tailwinds.

The Indian backdrop made the bet harder, not easier. The country in 2007-2009 had a software diaspora, not a hardware one. Power outages were routine. Land acquisition was a euphemism for litigation. The notion of a high-precision aerospace ecosystem inside India was, to put it mildly, contrarian. Which is exactly why a contrarian needed to do it. And the place he chose, against the advice of nearly everyone, was the town where his family had its roots.

III. The Belagavi Bet: Building an SEZ from Scratch

If you fly into ಬೆಳಗಾವಿ Belagavi today, you will land at a single-runway airport surrounded by sugarcane fields. The city sits roughly equidistant between Bengaluru and Mumbai — a half-day's drive from either, and almost exactly nowhere in particular. The dominant industries for most of the twentieth century were sugar processing, foundries, and the Indian Army's Maratha Light Infantry regimental headquarters. It is not a place anyone in 2008 was building a high-precision aerospace park. Which, of course, was the point.2

Aravind Melligeri's logic for choosing Belagavi was a triangle of geography, talent, and price. The town sat on the Karnataka-Maharashtra border, drawing engineering graduates from both states without paying Bengaluru salaries or fighting Bengaluru traffic. Land was a fraction of the cost of anything around the Devanahalli aerospace cluster outside Bengaluru. And critically, it was the founder's home turf — meaning he could navigate state politics, land acquisition, and local hiring through trust networks rather than RFPs. In India, that is not a soft factor. It is the difference between commissioning a plant in two years and being stuck in revenue court for ten.

In 2009, Aequs (then still operating as QuEST Manufacturing) commissioned what was officially notified by India's Ministry of Commerce as the country's first precision engineering Special Economic Zone — a 250-acre gated industrial estate dedicated to aerospace-grade manufacturing.[^6] To grasp why an SEZ designation mattered, think of it as a tax and customs holiday wrapped around an industrial park. Imports of raw materials and capital equipment flow in duty-free; exports flow out without the usual indirect-tax drag. For a sector like aerospace, where 80%+ of revenues are export, where input materials like titanium and Inconel are imported, and where margins are razor-thin, the SEZ structure converts an arithmetically marginal business into an arithmetically interesting one.

But the SEZ was just the wrapper. The real innovation — the one Aequs would later trademark as its "Ecosystems of Efficiency" doctrine — was what got placed inside it. Most aerospace supply chains around the world are horizontal: a forging vendor in one city, a machining vendor in another, a heat-treatment specialist in a third, a surface-finishing line in a fourth, a final assembly contractor in a fifth. A single component might travel 3,000 kilometres and pass through five tax jurisdictions before it reaches a final assembly bay. In India, where intercity logistics is notoriously slow and unpredictable, that horizontal model was a death sentence for margins.[^7]

Aequs's answer was to vertically stack the entire value chain inside one fence. Forging, precision machining, sheet metal work, surface treatment, special processes (anodising, painting, NDT inspection), and sub-assembly — all of it sitting within a kilometre of each other. The "trucking lag," as the company's internal lingo went, collapsed from weeks to hours. Inspection rounds that elsewhere required overnight courier shipments could happen in person, in the same building, in the same hour. Working capital, the silent killer of capital-intensive industries, dropped sharply.

The other strategic gift of the cluster was talent compounding. Once you trained a workforce of CNC machinists, inspection technicians, and AS9100 quality auditors inside one square kilometre, the marginal cost of training the next thousand was tiny. Belagavi, almost by accident, became one of the densest concentrations of certified aerospace-grade machinists in Asia — a labour pool that did not, and could not, exist anywhere else in India and would be expensive to replicate from scratch. We will come back to that "cornered resource" idea when we get to the Hamilton Helmer analysis, because it is one of the load-bearing pillars of the Aequs moat.

By 2013, the Belagavi cluster was operational at scale, exporting to Tier-1 customers in Europe and North America. The proof of concept was done. The next problem was no longer technical or even financial — it was credibility. Global OEMs do not buy from unknown Indian companies. They buy from people they have worked with for decades. Which meant Aequs needed to stop looking like an Indian start-up and start looking like a global manufacturer. Cue the rebrand and the acquisition playbook.

IV. Rebranding & The Global M&A Playbook

In 2014, the company quietly retired the QuEST Manufacturing nameplate and put up new signage: Aequs — Latin for "equal," chosen to signal parity with the global OEM supply base.2 The renaming was more than cosmetic. It was a declaration that the company was no longer an outpost of a larger Indian services firm; it was its own animal, with its own customers, its own balance sheet, and its own ambitions. The new logo went up in Belagavi the same year that two parallel conversations were happening inside the boardroom — one about scale, one about access — both pointing to the same conclusion: India alone would not get them where they needed to go.

The problem with selling precision aerospace components from India in 2014 was not capability. The problem was certification velocity. To become a qualified supplier to Airbus or Boeing on a new aircraft program is not a sales process; it is a three-to-five-year vetting ritual involving plant audits, first article inspections, AS9100 documentation, customer-specific quality protocols, and — most importantly — institutional trust accumulated over decades. Aequs was a teenager pitching for marriage to a centenarian. Even with flawless capability, the calendar alone meant they would miss an entire generation of aircraft programs while waiting in line.

The answer, executed with surgical clarity, was to buy the calendar. In late 2015, Aequs acquired T&K Machine Inc., a Wichita, Kansas-based aerospace machining specialist with an established customer footprint inside the Boeing and Spirit AeroSystems supply chains.2 Wichita is the heartland of American commercial aviation manufacturing — Boeing's spiritual home — and a US-based supplier address opens doors that an Indian-only supplier address simply cannot. Acquiring T&K did not just buy machines; it bought a 30-year supplier code in a Tier-1 ERP system. That is, in aerospace, priceless.

The pattern repeated, with French accent, the following year. In February 2016, Aequs announced the acquisition of Groupe SIRA, a French precision machining group with deep historical ties to Airbus, Safran, and Dassault.3 SIRA gave Aequs a Toulouse-adjacent presence — physical proximity to Europe's aerospace nervous system — at a moment when Airbus's supplier consolidation drive was creating both pressure and opportunity for medium-sized European machinists. The deal terms were not publicly disclosed in full, but the strategic logic was textbook: Aequs was paying for proximity and pedigree, not for cheap assets.

Here is where the "Acquired" lens matters. Compared to the typical aerospace M&A multiple of the era — generally cited at 6-8x EBITDA for tier-2 machining shops — Aequs paid at the higher end of the range, occasionally above it. The point was never to extract value from the acquired entity's existing book; the point was to use the acquired entity as a Trojan horse for the Belagavi cluster. Once T&K and SIRA were inside the Aequs perimeter, the company began the slow, deliberate work of transferring volume back to India: a program qualified through Wichita, but ultimately machined in Belagavi at one-third the labour cost. This is not asset-stripping. It is footprint arbitrage — and it is the move that converted Aequs from a vendor into what its customers list, in their own filings, as a strategic partner.[^11]

By 2018-2019, Aequs had transitioned into the second-tier supplier conversation with Safran, Collins Aerospace, Spirit AeroSystems, and Eaton. Multi-year, multi-program LTAs (long-term agreements) replaced one-off purchase orders. The company was no longer pitching for work; it was being asked to bid. That is the transition Western aerospace primes call going from "tactical" to "strategic." For a young company born in a sugar-mill town, it was the supplier equivalent of being invited inside the velvet rope. None of which would have been possible without the founder-led decision-making style that drove it. Which brings us to the man, and the leadership system, behind the operating philosophy.

V. Management & The Melligeri Playbook

Spend five minutes with Aravind Melligeri and you notice the absence of two things common in Indian industrial founders: bombast and bureaucracy. He does not pitch in superlatives. He does not surround himself with palace courtiers. He talks like an engineer who has spent twenty years in shop-floor reviews — because he has. His office in Belagavi is famously utilitarian; visitors who expect a corner-office tycoon are routinely surprised when he walks them onto the factory floor himself.2

Born and raised in Karnataka, Melligeri studied engineering in India before moving to Pennsylvania State University in the United States for graduate work. That biography matters because it explains the strange tonal mix the company runs on. There is the American engineering rigour — six-sigma documentation, AS9100 audit discipline, the obsessive culture of measurement and traceability. And there is the deeply Indian ಜುಗಾಡ jugaad (frugal innovation) — the willingness to substitute capital with creativity, to find a five-rupee solution where the textbook calls for a fifty-rupee one. Western aerospace executives who tour Belagavi report a quiet shock at how that combination produces output quality indistinguishable from a Toulouse machining bay at a fraction of the operating cost.2

Post-IPO, the promoter group retained roughly 59% of the equity, with Melligeri serving as Executive Chairman and CEO and continuing to lead the operational franchise.[^2] This level of insider ownership is, in Indian capital-markets terms, both reassuring and constraining. Reassuring because Melligeri is unambiguously aligned with public shareholders — every rupee of value he creates flows through to his own balance sheet. Constraining because liquidity is thin and the company is effectively a single-leader bet for the foreseeable future. Investors in Aequs are buying not just a business but a founder operating system.

The senior team around him reflects that operating system. The C-suite is technically dense — engineers, operations managers, supply-chain specialists — rather than finance-led. Compensation, according to the prospectus and FY25-26 disclosures, is structured with a meaningful variable component tied to capital efficiency (ROCE) and product mix shift toward higher-margin assemblies rather than to revenue alone.[^2] That detail is important. It means the management's incentive is not to chase top-line at any cost — a classic failure mode for capital-intensive manufacturers — but to compound the return on the asset base. In a business where a single CNC machining centre can cost $2-3 million, that incentive design is the difference between profitable growth and growth-fuelled bankruptcy.

A subtler element of the playbook is what one might call Melligeri's "patient cluster" temperament. Most Indian industrialists scale by adding factories. Melligeri scales by adding adjacencies inside existing clusters. The Belagavi SEZ has expanded its capability footprint without expanding its geographic footprint. The new Koppal and Hubballi sites repeat the cluster architecture verbatim. This is, in management terms, a deliberate refusal to chase the dispersal premium — the urge to plant a flag in every Indian state to please politicians. Aequs concentrates because concentration compounds. It is a style that requires personal authority to enforce: only a founder can say no, often, for years, to dilution of strategic focus.

A second-layer note for diligence-minded readers: key-person concentration is the obvious overhang. With Melligeri at the operational and strategic centre, succession planning is the single biggest qualitative risk the company carries. The board has so far disclosed limited public detail on a designated successor pipeline.[^2] This is not unusual for a founder-led, recently listed Indian manufacturer, but it is the item that should sit on any institutional checklist for as long as the founder remains the centre of gravity. With those caveats acknowledged, let us turn to the part of the business that, until recently, almost no one outside Karnataka was paying attention to.

VI. The Hidden Growth Engines: Toys & Consumer Durables

Drive two hours northeast of Belagavi, past sunflower fields and granite outcrops, and you arrive at ಕೊಪ್ಪಳ Koppal — a district more famous for iron ore and the ruins of Vijayanagara than for industrial precision. And yet, since the early 2020s, a 400-acre site outside Koppal has been quietly rising into what Aequs intends to be the largest integrated toy manufacturing cluster outside China.[^9] If the Belagavi story is about taking 10-micron precision and applying it to flight-critical aerospace, the Koppal story is about taking that same disciplined manufacturing DNA and applying it to mass-market consumer scale. Both ends of the spectrum, one company.

The strategic logic for toys is more elegant than it first appears. The global toy industry, dominated by Hasbro, Mattel, Spin Master, and a long tail of licensors, has spent the last decade desperately trying to diversify out of southern China. Rising Chinese labour costs, US-China tariff exposure, COVID-era supply shocks, and the specific Trump-era 25% tariffs on Chinese consumer goods all converged to push Western toy buyers to actively shop India and Vietnam. The problem until recently was that India simply did not have a toy manufacturing ecosystem of any scale. Polymer compounders, injection moulders, painting lines, packaging vendors — none of it existed in clustered form. Aequs's bet was that the same cluster-building muscle that worked in aerospace would work in toys.[^9]

By 2024, Aequs's Koppal cluster was running production runs for Hasbro and Spin Master, with publicly reported tie-ups expanding into additional licensors.[^11] Importantly, the unit economics of toys are nothing like aerospace. Toys are a high-volume, low-margin, fashion-cyclical business, dependent on injection moulding cycle times, polymer prices, and shipping schedules. But that is precisely why scale clustering matters: with Aequs handling tooling, moulding, decoration, assembly, and packaging inside one estate, the company captures more of the value chain than a single-step Chinese vendor, while paying Indian rather than Chinese wages.

The third leg of the consumer pivot sits in ಹುಬ್ಬಳ್ಳಿ Hubballi, the commercial twin of Belagavi, where Aequs operates a consumer durables cluster anchored by a joint venture with Brazilian cookware giant Tramontina. Signed in 2022, the JV established a stainless steel and non-stick cookware facility aimed at both the Indian domestic market and exports.[^10] The choice of Tramontina is itself telling. Tramontina is one of the world's largest privately held cookware manufacturers, with a reputation for precision metallurgy and process discipline. The JV is, in essence, another version of the foreign-acquisition playbook: import a global brand's process know-how, marry it to Indian cost and scale, and serve both inbound (Indian middle class) and outbound (export) demand simultaneously.

A fourth and newer category sits next to the cookware lines: consumer electronics and laptop manufacturing, tied to the Indian government's आत्मनिर्भर भारत Aatmanirbhar Bharat (self-reliant India) policy and its production-linked incentive (PLI) schemes for IT hardware.[^11] Whether laptops will become a meaningful contributor is too early to call. What is clear is that Melligeri's cluster framework lets him bolt new product categories onto existing physical infrastructure with marginal capex — a kind of platform leverage rarely seen in heavy manufacturing.

The headline revenue mix, as of the FY2025-26 disclosures, remained heavily aerospace-tilted — roughly 88% of revenue from aerospace and aerospace-adjacent customers — with the consumer and durables segments contributing the balance and growing at a materially faster pace.[^2] Management has guided that the consumer cluster is expected to account for closer to half of group revenue by 2028, though investors should treat that as a directional target rather than a near-term commitment. For a long-only fundamental investor, the more important point is that the consumer business exists and is being capitalised — meaning aerospace cyclicality is being structurally hedged within the same operating umbrella, an unusual and valuable construction.

VII. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

The standard mistake when analysing an Indian contract manufacturer is to apply a generic commodities lens — to look at the gross margin, decide it is "just" 30-something percent, and call the business unspecial. The Aequs lens is different because the moat is not arithmetic; it is architectural. Let us run the company through both Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces and see where the real edges sit.

Scale economies. The Belagavi SEZ is, by virtue of being India's first precision-engineering SEZ and the dominant aerospace cluster in the country, operating at a unit-cost level that no Indian peer can match without rebuilding from zero.[^6] Fixed costs — the SEZ infrastructure, the central inspection labs, the heat-treatment and surface-finishing lines — are spread across a higher and growing tonnage of output. Each incremental contract spreads the same overhead more thinly. Crucially, this scale advantage is local, not global: Aequs is not (yet) bigger than Spirit AeroSystems or Latécoère in absolute terms, but it is decisively bigger than any other Indian player in its specific niche.

Switching costs. This is the load-bearing power. Aerospace supplier qualification is a multi-year, multi-million-dollar, paperwork-drenched ritual. Once Aequs is qualified on a specific program — say, the LEAP engine fan case, or the A320neo wing pylon assembly — switching to another supplier mid-program is effectively impossible without re-certifying everything. Programs run for 20-25 years.2 What this means in practice is that revenue won today annuitises for a generation. Compare this to a typical industrial component supplier, where the customer can rebid the contract every two years, and the moat differential becomes obvious.

Cornered resource. The trained workforce of certified machinists, inspectors, and special-process technicians inside the Belagavi catchment area is, at this scale, unreplicable in India in any reasonable time frame. To duplicate it, a competitor would need to build an equivalent SEZ, attract an equivalent OEM customer base, run an equivalent decade-long training pipeline, and somehow do all this while Aequs's own moat continues to deepen. This is what Helmer calls a cornered resource — preferential access to a coveted asset that independently enhances value.

Process power. Often underrated. The accumulated tacit knowledge embedded in how Aequs runs a Belagavi production line — the inspection workflows, the supplier sequencing, the small thousand-line tweaks in shop-floor practice — is the kind of advantage that cannot be photocopied from a PDF. New entrants can buy the same machines, but they cannot buy the same shop-floor instinct.

Now the Porter overlay. Threat of new entrants: very low. Certification timeframes plus capital intensity (each major capex round runs into hundreds of crores of rupees) plus the SEZ tax regime that the government has not extended to greenfield aerospace plants since the early 2010s create a near-impenetrable barrier.[^6] Threat of substitutes: low for aerospace components (you cannot 3D-print a forged titanium ring at scale, yet); medium for toys and durables, where alternate Indian, Vietnamese, and Mexican vendors are emerging. Buyer power: this is the trickiest force. Airbus and Boeing are powerful counterparties, and their purchasing organisations are famously aggressive on pricing.[^11] However, the vertical integration of Aequs — meaning fewer middlemen between forge and finished part — gives the company more pricing pliability than a single-step machinist. Supplier power: medium. Critical inputs like titanium and Inconel are commodity-priced and globally sourced, with periodic spikes but no structural dependence on a single supplier. Industry rivalry: in India, fragmented and benign; globally, intense, but mediated entirely by the certification moat described above.

The summary is that Aequs has at least three Helmer-grade powers stacked on top of each other inside aerospace, with credible-but-unproven extensions into toys and durables. That is a stronger structural position than the average Indian industrial listing, and worth understanding in detail before getting to the playbook lessons.

VIII. Playbook: Business & Investing Lessons

If you strip Aequs down to its operating principles, four lessons emerge that generalise far beyond the company itself — and they are, frankly, the kind of moves more Indian industrials should be studying.

Lesson one: Vertical integration is the only winning posture in precision manufacturing. The naive view of contract manufacturing is that specialisation wins — that a machinist should machine, a forger should forge, a finisher should finish, and the customer should be the system integrator. That logic is correct in software, where integration cost is near zero. In physical goods, where every handoff costs working capital, logistics time, and quality risk, the math reverses. Aequs's success is partly a refutation of the "stick to your core competence" doctrine when "core competence" is defined too narrowly. Owning the full stack — from raw material to assembly — converts a series of low-margin steps into a single integrated value chain with a meaningfully higher return on capital.

Lesson two: China Plus One is not a discount story; it is an upgrade story. For the last decade, Western analysts have framed the diversification of manufacturing out of China as a hedging exercise — accept a slightly higher cost in exchange for geopolitical resilience. The Aequs case suggests something different: with the right cluster architecture, the second source can actually outperform the first source on quality, certification responsiveness, and engineering bandwidth, while staying competitive on cost. India's deep engineering services base — itself a legacy of Aequs's parent founder's earlier company — means Indian aerospace manufacturers can iterate on design changes faster than Chinese vendors operating at arms length from Western OEMs. This is the real investable thesis behind India's industrial moment, and Aequs is one of its purest expressions.[^11]

Lesson three: Run the factory like a software company. This sounds glib. What it means in practice is to treat shop-floor processes as compounding intellectual property — to instrument every machine, document every workflow, train every operator into a system that improves a few basis points each quarter. The cumulative result over a decade is a productivity gap with competitors that cannot be closed by buying new machinery. Aequs management talks publicly about ROCE as the primary internal scorecard rather than revenue growth, which is the manufacturing equivalent of a SaaS company tracking net revenue retention.[^2] In a sector where ego often drives capacity races, that discipline is rare and valuable.

Lesson four: De-risk a cyclical core by moving sideways, not by moving smaller. Most aerospace suppliers, faced with the inherent boom-bust cyclicality of the industry, react by either over-saving cash through downturns or by trying to diversify into adjacent aerospace sub-segments (defence, MRO, space). Aequs has done something more interesting. By moving sideways into structurally non-correlated end-markets — toys (consumer-led), cookware (replacement-cycle led), drones (defence and commercial mix) — the company has imported diversification into the same operating platform without having to learn entirely new manufacturing physics. This is a far more capital-efficient form of de-risking than building a separate defence division would be, and it directly addresses one of the loudest historical complaints about pure-play aerospace suppliers: the white-knuckle volatility of commercial aircraft demand cycles.

A bonus observation, less of a "lesson" and more of a pattern: founder-led, promoter-heavy Indian industrials with engineering DNA and Western customer bases have, as a category, outperformed promoter-light Indian conglomerates in the post-2020 capital markets. Aequs fits that pattern precisely. The Helmer powers above and the operating philosophy here are how that outperformance is manufactured — pun intended — rather than just observed. With the playbook in hand, the next question is what could go wrong, and what could go very right.

IX. Bear vs. Bull Case & The Future

A serious business analysis owes its audience an honest two-sided ledger. Aequs is neither a guaranteed compounder nor a structurally broken business; it is a recently listed industrial that lives or dies on execution against a credible thesis. Here is how that ledger reads in 2026.

The bull case. Aequs becomes, over the next decade, what one might call the Foxconn of aerospace and toys for the non-China world. The Belagavi cluster expands from its current footprint into adjacent acreage, capturing rising share of the Airbus and Boeing supplier consolidation drives. Koppal scales into the world's largest non-Chinese toy manufacturing footprint, with Hasbro, Spin Master, and additional licensors moving meaningful program volume in. Hubballi's Tramontina cookware JV expands into electrical appliances and small kitchen durables, capturing share from Chinese white-label vendors. The 2026 UAV joint venture with Vagus Technologies, announced in April of this year, plants a flag in the fast-emerging Indian drone manufacturing sector and gives Aequs a foothold in defence-adjacent revenues.[^12] In this scenario, the consumer cluster grows from a high-single-digit percentage of revenue today toward something in the 40-50% range by 2028, structurally re-rating the company from "aerospace ancillary" to "diversified precision manufacturer." The earnings power that emerges from full asset utilisation across three clusters, combined with the operating leverage inherent in cluster economics, would justify a meaningfully higher multiple than Indian industrial peers historically command.

The bear case. Capital intensity is the silent enemy. Each new program requires substantial up-front capex — tooling, machining centres, inspection equipment — with revenue recognition trailing capex by 18-24 months as qualification runs complete. If Aequs over-builds capacity ahead of program ramps that get delayed (as happens routinely in aerospace), the company carries idle assets and rising leverage simultaneously. The ₹2,856 crore Karnataka expansion MoU announced in March 2026 is exactly the kind of headline number that excites a stock and worries a credit analyst.[^7] Second, customer concentration is real. Airbus and Boeing, directly or through their Tier-1 supplier ecosystem, account for the lion's share of aerospace revenue. A 737 MAX-style demand shock, or a single program loss, can take a meaningful chunk out of the top line. Third, the consumer business is unproven at scale; Hasbro and Spin Master are large customers, but the toy industry is faddish, margin-thin, and historically a graveyard for non-Chinese contract manufacturers. Fourth, the SEZ tax regime that has historically enhanced Aequs's after-tax economics is subject to policy change; India's evolving corporate tax framework has already trimmed some SEZ benefits and could trim more.[^6]

The competitive comparison. Within India, the most-cited peer is Azad Engineering, which IPO'd in late 2023 and operates a higher-margin, narrower precision-engineering business focused on rotors and turbine blades. Azad trades at premium multiples to most industrials, reflecting its margin profile.[^5] Aequs, by contrast, is broader in scope (aerospace + toys + cookware + drones), more vertically integrated, and earlier in its multi-cluster build. The two are not direct substitutes; Azad is a sniper, Aequs is an ecosystem. Comparison to global peers is harder — Aequs's combination of aerospace and toys does not exist anywhere else of similar scale. The closest analogy is a vertically integrated regional manufacturer like Latécoère in France or a diversified industrial like Heico in the US, both of which trade at multiples that imply long runways for an Indian counterpart with a structural cost advantage.

Key performance indicators to watch. For a long-term fundamental investor following Aequs, three KPIs matter more than the rest. First, ROCE trajectory — the company's stated internal scorecard, and the cleanest gauge of whether incremental capex is generating returns or just inflating the balance sheet.[^2] Second, consumer-segment revenue share — the speed at which toys, cookware, and drones rise within the mix is the single best proxy for the de-risking thesis playing out. Third, aerospace program win count — not order book in rupees, which can fluctuate with raw material pricing, but the number of new programs Aequs is qualified into each year, because that is what determines revenue 24-36 months out. These three KPIs, tracked over time, will tell most of the story.

Myth vs reality. The consensus narrative on Aequs in 2026 frames the company as a "Make in India aerospace darling," which is half right and half misleading. The half that is right: Aequs has genuinely become India's most credible precision aerospace manufacturer at scale. The half that is misleading: the long-term equity story is not really about aerospace at all; it is about cluster architecture as an operating system, repurposable across industries. Investors who buy Aequs as a defence-and-aerospace play are buying the wrong story. The right story is industrial platform economics — and that is a more interesting, and more uncertain, bet.

X. Epilogue & Outro

Stand again outside the gates of the Belagavi SEZ at dusk, watching shift change. Hundreds of workers — mostly young, mostly local, mostly hired within the last decade — stream out of the cluster on motorbikes and into the surrounding town. Two decades ago, those same young people would have left Belagavi entirely, either for Bengaluru's IT parks or for the Gulf as expatriate labour. Today, the labour migration runs the other way. Engineers and technicians are moving to Belagavi because the work and the wages are now competitive with anywhere in India. This is what an industrial cluster does when it works: it rewrites the geography of opportunity.

That rewriting is the real legacy of the NSE listing. Listing a company is, in the most literal sense, a moment of price discovery — a number on a screen, a public market capitalisation, a set of analyst notes. But for a country like India, which has spent two generations exporting software and importing hardware, the listing of a credibly global precision manufacturer is also a moment of category discovery. It demonstrates, with prospectus numbers and audited financials, that a 250-acre patch of land in northern Karnataka can house a business worth fighting Toulouse and Wichita for. The category effect is bigger than the company effect. Other Indian manufacturers — in autocomponents, defence, semiconductors, medical devices — will reference the Aequs precedent for the next decade.

For Aravind Melligeri personally, the listing is also a closing of a 25-year arc that began in a Connecticut engine plant in the late 1990s. The young engineer who once watched titanium blades come off Western machines now runs the largest stack of aerospace machines on Indian soil and sends his own blades the other way across the Atlantic. The reversal is symbolic, but it is also concrete: thousands of jobs, tens of thousands of trained workers, billions of dollars of invested capital, and a vocabulary — "ecosystems of efficiency" — that has begun appearing in other industrial sectors' strategic decks.

Whether the public-market story ends with Aequs as the Foxconn of the non-China world or as a cautionary tale about capital intensity in a cyclical industry remains genuinely undetermined. But the underlying architectural innovation — clustered, vertically integrated, certification-protected, multi-end-market manufacturing — is now a fact in the world, and a fact that other founders will copy. In that sense, the company has already won the most important kind of bet a founder can win: the bet on whether their idea would have to exist after them, or could be allowed to disappear. The ecosystem in Belagavi, ಕೊಪ್ಪಳ Koppal, and ಹುಬ್ಬಳ್ಳಿ Hubballi exists now. The next decade is about how big it can get.

Melligeri's stated ambition, repeated in interviews and investor calls since the IPO, is a "manufacturing nation" — not a manufacturing company, a manufacturing nation.2 The phrase is grandiose. It is also, increasingly, defensible. India's industrial policy, capital availability, and labour cost structure have aligned in 2026 in a way they have not aligned in fifty years. Whether Aequs becomes the breakout name of that alignment is a question for the next several earnings cycles. But the architecture is built, the customers are signed, the founder is in his seat with a controlling stake, and the toy trucks and the titanium pallets keep rolling out the same gate on the same dusty road in northern Karnataka. The story is still being written. The setting, however, is no longer in doubt.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube