Adani Ports and Special Economic Zone: India's Infrastructure Giant

I. Cold Open & Episode Roadmap

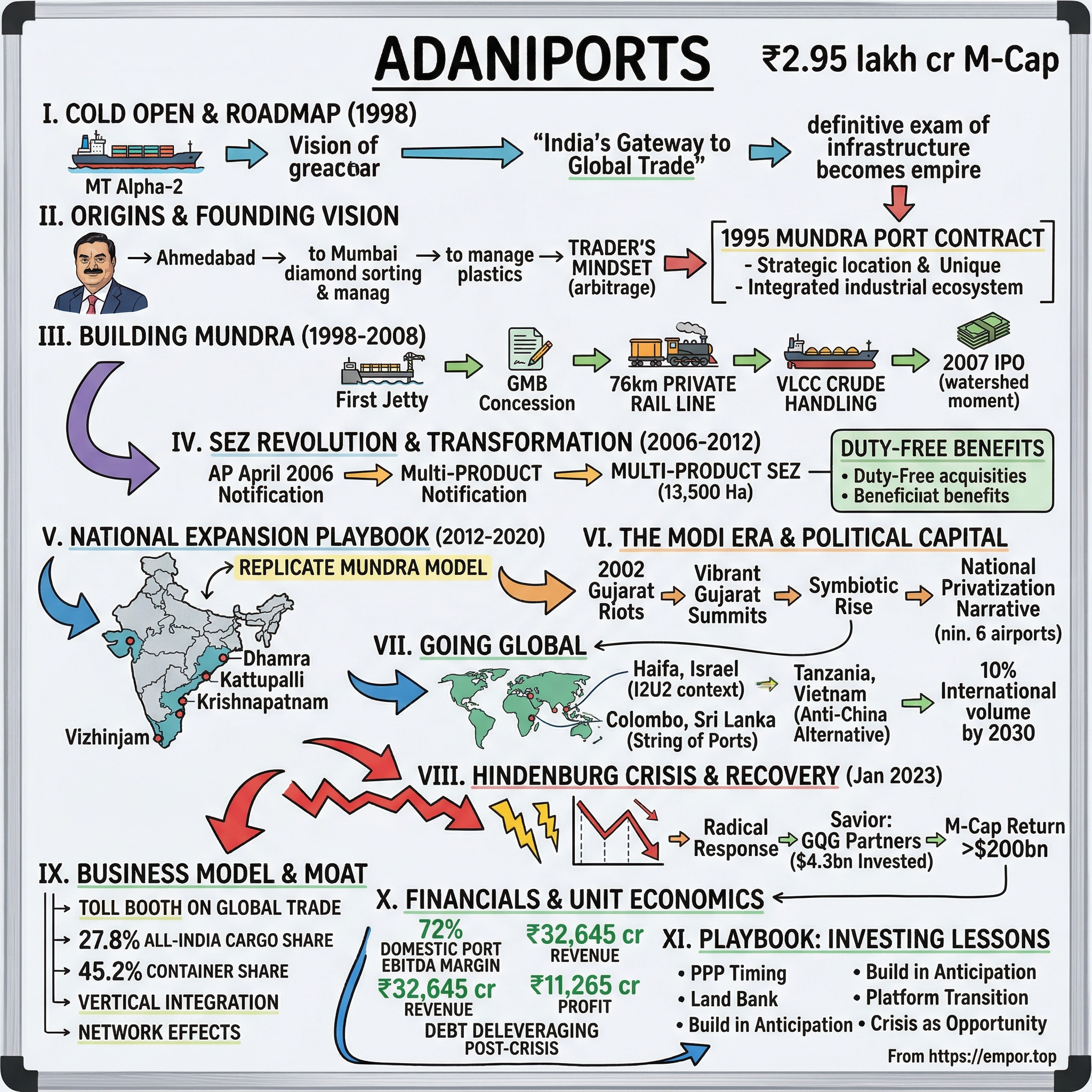

The year is 1998. A single ship, the MT Alpha-2, drops anchor in the shallow waters off Gujarat's Kutch coast on October 7th. The location seems improbable—a barren expanse of salt marshes and tidal flats where the Arabian Sea meets India's western shore. Yet this moment marks the birth of what would become India's largest private port operator, a company that today handles nearly one-fourth of all cargo movement in the world's most populous nation.

How did a single berth in Gujarat's inhospitable coastal wilderness transform into India's gateway to global trade? The answer lies in a remarkable confluence of political timing, infrastructure ambition, and the vision of one man who saw opportunity where others saw only obstacles. Adani Ports and Special Economic Zone Limited represents more than just a corporate success story—it's a lens through which to understand India's economic transformation, the power of political-business alignment, and the strategic importance of controlling the nodes where global commerce meets local markets.

This is the story of how Gautam Adani built an infrastructure empire from the salt pans of Mundra, navigated political upheavals and corporate attacks, and created what Morgan Stanley would call a "top quartile" operator across virtually every metric. It's also a cautionary tale about the risks of rapid expansion, political entanglement, and the challenges of transitioning a coal-dependent business model in an increasingly climate-conscious world.

Today, with a market capitalization exceeding ₹2.95 lakh crore and control over 13 domestic ports spanning seven maritime states, Adani Ports stands as both a testament to India's infrastructure ambitions and a lightning rod for debates about corporate governance, political influence, and the concentration of economic power. From Mundra's first berth to international expansions in Israel, Tanzania, and Sri Lanka, this is the definitive examination of how infrastructure becomes empire.

II. The Adani Origins & Founding Vision

The story of Adani Ports begins not with ships or harbors, but in the narrow lanes of Ahmedabad's textile markets. Gautam Adani was born on June 24, 1962, into a Gujarati Jain family to Shantilal and Shantaben Adani. He had seven siblings, and his parents had migrated from the town of Tharad in northern Gujarat. His father was a small textile merchant. This wasn't a family of industrialists or port operators—it was a modest mercantile household where business meant small-scale trading, where margins were thin, and where success meant gradual accumulation rather than transformative leaps.

Adani was born into a family of Gujarat Jains, the seventh of eight children born to Shantilal Adani, a textile merchant. The significance of being Gujarati Jain cannot be understated in understanding Adani's trajectory. This community had centuries of trading expertise, an ingrained understanding of risk and reward, and most importantly, the social networks that could mobilize capital when opportunities arose. Yet Adani's path diverged from the traditional family business model almost immediately.

Adani was educated at Sheth Chimanlal Nagindas Vidyalaya school in Ahmedabad, but dropped out when he was 16. Adani was keen on business, but not his father's textile business. This rejection of the predetermined path would become a defining characteristic. In 1978, at just sixteen years old, Adani made a decision that would seem reckless to most middle-class families: he left for Mumbai with little more than ambition and a few hundred rupees in his pocket.

As a teenager, Adani moved to Mumbai in 1978 to work as a diamond sorter for Mahendra Brothers. The diamond trade in Mumbai's Zaveri Bazaar was where fortunes were made and lost daily, where a keen eye could spot value that others missed, and where relationships with international buyers could open doors to global commerce. For three years, Adani absorbed the rhythms of international trade, learning how commodities moved across borders, how letters of credit worked, and most crucially, how to spot arbitrage opportunities in global markets.

But it was family obligation that brought him back to Gujarat. In 1981, his elder brother Mahasukhbhai Adani bought a plastics unit in Ahmedabad and invited him to manage the operations. This venture turned out to be Adani's gateway to global trading through polyvinyl chloride imports. What seemed like a step backward—returning home to manage a small plastics unit—became the foundation for understanding industrial supply chains. PVC imports taught Adani about bulk commodity trading, about managing foreign exchange risk, and about the inefficiencies in India's import licensing regime that created opportunities for those who could navigate the bureaucracy.

In 1988, Adani established Adani Exports, now known as Adani Enterprises. This wasn't a grand launch with venture capital or institutional backing. It was a trading company born from accumulated knowledge—understanding which commodities moved where, which buyers needed what, and how to finance trades through banking relationships built over years. The timing was fortuitous. India stood on the cusp of economic liberalization, though few could have predicted the scale of transformation that would follow.

The trader's mindset that Adani developed during these formative years would prove crucial for what came next. Unlike industrialists who thought in terms of factories and production capacities, Adani thought in terms of flows—of goods, of capital, of information. He understood that controlling the nodes where these flows intersected was more valuable than controlling production itself. This insight would lead him to ports.

In 1994, the Government of Gujarat announced managerial outsourcing of the Mundra Port and in 1995, Adani obtained the contract. In 1995, he set up the first jetty. The location seemed absurd to conventional wisdom. Mundra was a fishing village in Kutch, a region known more for earthquakes and salt deserts than commercial potential. The nearest major city, Ahmedabad, was 400 kilometers away. The waters were shallow, requiring extensive dredging. Infrastructure was non-existent.

But Adani saw what others missed. Mundra was closer to global shipping lanes than Mumbai or JNPT. The Gujarat government, eager for development, would provide favorable terms. Most importantly, there was vacant land—thousands of acres that could be acquired cheaply and developed not just as a port but as an integrated industrial ecosystem. The trader who had spent years moving goods through India's congested ports understood that the real value wasn't in the port itself but in controlling the entire logistics chain from factory gate to ship's hold. The India into which Adani launched his port ambitions was fundamentally broken when it came to maritime infrastructure. As late as the mid-1990s, India's ports were seen as having inadequate capacity to cater to a rapidly burgeoning economy and were considered frustrating choke points in the logistics chain. As against the total capacity of 217.3 million tonnes on March 31, 1997, major ports handled 227.3 million tonnes, resulting in pre-berthing delays and unacceptable ship turn-around times.

Traditionally, India's ports functioned under public oversight, resulting in inefficiencies including cargo congestion, prolonged turnaround times and antiquated infrastructure. The 1990s economic liberalization emphasized the necessity for enhanced port efficiency to accommodate escalating trade volumes, prompting the government to explore privatization as a catalyst for capital infusion, technological advancements and operational optimization.

This was the context that made Adani's vision not just ambitious but necessary. In the 1990s, India initiated port privatization through public-private partnerships (PPPs), a strategic approach facilitated by the Major Port Trust Act. This legislation enabled private investment in major ports while maintaining government oversight. Adani wasn't the only entrepreneur who saw opportunity in India's creaking ports, but he was perhaps the only one who understood that the real value lay not just in handling cargo but in creating entire economic zones around ports.

The transformation from commodity trader to infrastructure baron wasn't accidental—it was architected. Every ton of coal, every container of plastics that Adani had traded through India's congested ports had taught him where the bottlenecks were, where value leaked out of the system, and most importantly, where a private operator with capital and political connections could create exponential value. The trader's eye for arbitrage had identified the ultimate trade: exchanging political capital and modest initial investment for control over India's gateway infrastructure.

III. Building Mundra: The First Decade (1998–2008)

On October 7, 1998, a modest 5,000-ton tanker named MT Alpha-2 dropped anchor off the coast of Mundra. MT Alpha-2, a small tanker was the first ship anchored on 7 October 1998. The vessel carried liquid cargo from Singapore, and its arrival marked not just the operational beginning of a port but the physical manifestation of years of planning, political maneuvering, and infrastructural ambition. The location remained as improbable as ever—shallow waters requiring constant dredging, minimal existing infrastructure, and a hinterland that seemed economically dormant.

But Adani understood something fundamental about infrastructure: if you build it right, demand will come. The engineering challenge of building in the Gulf of Kutch's waters was immense. The tidal variations were extreme, the seabed required extensive dredging to accommodate larger vessels, and the nearest railhead was hundreds of kilometers away. Yet these challenges became competitive advantages. The Mundra Port is located in the Northern Gulf of Kutch, en route major maritime routes, closer to international shipping lanes than Mumbai or JNPT, India's busiest ports.

The first breakthrough came quickly. In 1999, multi-purpose berths 3 and 4 opened at Terminal I. By 2001, Adani had secured something crucial: In 2001, the Port of Mundra signed a concession agreement with GMB for development, operation, and maintenance of the port at Mundra. This wasn't just a license to operate; it was essentially a blank check to transform thousands of acres of coastal land into an integrated port-industrial complex. The real game-changer came with rail connectivity. Mundra Port Ltd. is connected with the Indian Railway network by a developed and maintained 76-km rail line from Mundra to Adipur. This wasn't just any railway line—it was privately built, privately owned, and represented a fundamental shift in how infrastructure could be developed in India. For the first time after independence a private Broad Guage link between Adipur and Mundra Port, of Gujarat Adani Port Ltd., was commissioned and opened for goods traffic from 15/11/2001, marking a new chapter in the transport system of Indian Railways.

The significance of this railway cannot be overstated. It meant that cargo from India's industrial heartland—Delhi, Punjab, Haryana, western Uttar Pradesh—could now reach Mundra directly. The port suddenly wasn't just serving Gujarat; it was serving the entire northwestern hinterland of India. By 2002-2003, railways were handling 75% of import traffic at Mundra port, demonstrating how quickly the infrastructure was being utilized.

Parallel to the railway development, Adani was securing crucial agreements that would define Mundra's cargo profile. In 2002, agreements were signed with Gujarat State Railway Limited and Indian Oil Corporation for crude oil handling. This transformed Mundra from a general cargo port into a critical energy infrastructure node. The port could now handle Very Large Crude Carriers (VLCCs), making it one of the few ports in India capable of receiving the largest oil tankers in the world.

The growth trajectory was explosive. In a short span of just 12 years Mundra Port achieved 10 crore (100 million) metric tonnes of commercial cargo in a year thereby becoming India's largest commercial port. This wasn't organic growth—it was engineered growth. Every piece of infrastructure was designed with excess capacity, anticipating demand that didn't yet exist. The port was built to handle 338 MMT of cargo per annum when it was handling barely a fraction of that initially.

But perhaps the most audacious move came in October 2007 when Gujarat Adani Port Limited went public. Initial Public Offer (IPO) for 40,250,000 equity shares of ₹10 each of Mudra Port and Special Economic Zone Ltd. to public and employees with price band of ₹400 – ₹440. The IPO was a watershed moment. It provided capital for expansion, but more importantly, it created a currency—publicly traded shares—that Adani could use for acquisitions. The trader from Ahmedabad now had access to public markets, and with it, the ability to scale beyond what private capital alone could achieve.

The engineering marvel of Mundra went beyond just berths and cranes. The rail infrastructure is capable of handling 130 trains per day including double stack container trains and long-haul trains. This capacity was built when the port was handling perhaps a tenth of that traffic. It was infrastructure built for a future that Adani was determined to create rather than wait for.

By 2008, Mundra had transformed from a single-berth operation to a multi-terminal complex. The port had dedicated terminals for containers, liquid cargo, coal, and automobiles. Each terminal was equipped with specialized handling equipment—grab ship unloaders for coal, gantry cranes for containers, pipelines for liquid cargo. The port wasn't just moving cargo; it was creating an ecosystem where different types of trade could coexist and create synergies.

The numbers tell the story of this transformation. From handling a few thousand tons in 1998, Mundra crossed 50 million tons by 2008. The port that started with one berth now had multiple terminals. The company that began as Gujarat Adani Port Limited was preparing for its next transformation—becoming a national player rather than just a regional port operator. The foundation was set, the infrastructure was in place, and most importantly, the political and economic winds were favorable. The next phase would see Adani transform from a port operator to something much more ambitious: the creator of India's first private port-based Special Economic Zone.

IV. The SEZ Revolution & Transformation (2006–2012)

The year 2006 marked a fundamental transformation in Adani's ambitions. In April 2006, Mundra Port was notified as a Special Economic Zone. This wasn't merely an expansion of port operations—it was a complete reimagining of what a port could be. Mundra Port pioneered not only the concept of deep draft integrated port model, but also of port based SEZ, with the multi-product SEZ planned to be spread over 135 square kilometres (13,500 hectares).

The SEZ model represented a paradigm shift in Indian infrastructure development. SEZs are designated duty-free enclaves in India where the national customs law does not apply. For businesses operating within the zone, this meant dramatic cost advantages—no customs duties, no GST, simplified regulations, and a single-window clearance system. But for Adani, the SEZ represented something more profound: the ability to control an entire economic ecosystem.

The Mundra Special Economic Zone Ltd. and Adani Chemicals Limited were merged with Gujarat Adani Port Ltd., and the company name was changed to Mundra Port and Special Economic Zone Limited (MPSEZ) in 2006. This corporate restructuring reflected the strategic vision—the port was no longer just a logistics node but the anchor of an industrial complex that would include power plants, refineries, manufacturing units, and everything else needed to create a self-contained economic zone.

The scale of the SEZ was breathtaking. Currently, notified Multi-product SEZ is spread over an area of 6,473 Hectare, with an additional 168 Hectares notified as a Free Trade Warehousing Zone. It became India's first multi-product port-based special economic zone, setting a template that would be replicated across India and establishing Adani as not just a port operator but a creator of industrial ecosystems.

The benefits offered to companies setting up in the SEZ were extraordinary. 100 percent exemption on export profits for the first five years and 50 percent for the next five years, exemption of excise duty, custom duty, service tax, VAT, stamp duty, and lease tax, and exemption from electricity duty for 10 years from the date of commencement of operations. These incentives attracted major corporations looking to establish manufacturing bases with direct port access.

Infrastructure development accelerated at an unprecedented pace. Additional 10 bulk berths became operational in May 2006, and double stack train operations commenced from Mundra Port in June. The ability to run double-stack container trains—unique in India at the time—meant that Mundra could move twice the cargo volume per train compared to conventional operations. This wasn't just incremental improvement; it was a step-change in logistics efficiency.

The port's capabilities expanded dramatically during this period. A service agreement was signed with Tata Power to produce power for handling coal cargo imports. In 2009, Maruti Suzuki's A-star was shipped to Europe from Mundra Port, and ADANI Auto Terminal began operations. The port was no longer just handling bulk commodities—it was becoming a sophisticated multi-modal logistics hub capable of handling everything from automobiles to project cargo.

In 2007, equity shares in MPSEZ were offered to the public and employees and were listed on the National Stock Exchange and Bombay Stock Exchange. The public listing provided capital for aggressive expansion, but more importantly, it created a publicly traded vehicle that could be used for acquisitions. The market's response was enthusiastic—investors saw the potential of a company that controlled not just a port but an entire economic zone.

By 2010, the transformation was complete. A four-lane, 1.5 km long dedicated Road Over Bridge was constructed at Mundra Port, capable of handling 100 MT loads—the first private four-lane bridge within a port area in India. The port could now handle everything from the smallest containers to the largest project cargo, with dedicated infrastructure for each type of shipment.

The numbers reflected this transformation. From handling 100 million tonnes in 2010, Mundra was rapidly approaching capacity levels that would make it not just India's largest port but one of the largest in the world. The SEZ had attracted dozens of companies, creating an industrial ecosystem that generated its own momentum. Power plants were being built to supply the zone, refineries were processing crude oil landed at the port, and manufacturing units were producing goods for export through the same port where raw materials arrived.

But perhaps the most significant development came in January 2012. In January 2012, the company name was changed to Adani Ports and Special Economic Zone Ltd. This wasn't just a rebranding—it was a declaration of intent. Adani was no longer content with being the operator of Mundra Port. The company was positioning itself as India's infrastructure developer, ready to replicate the Mundra model across the country. The foundation for national expansion was complete, and the stage was set for Adani to transform from a regional player to a national infrastructure giant.

V. The National Expansion Playbook (2012–2020)

The year 2012 marked a strategic inflection point for Adani Ports. With Mundra established as India's largest private port and the company renamed as Adani Ports and Special Economic Zone Limited, the stage was set for aggressive national expansion. The company shifted its focus on three business clusters – resources, logistics and energy. The acquisition strategy that would define the next decade was clear: identify underperforming or distressed port assets, acquire them at reasonable valuations, and apply the Mundra playbook to transform them.

The first major move came in 2014. On 16 May of the same year, Adani Ports acquired Dhamra Port on East coast of India for ₹5,500 crore. Dhamra Port was a 50:50 joint venture between Tata Steel and L&T Infrastructure Development Projects. The port had begun operations in May 2011 and handled a total cargo of 14.3 Mt in 2013–14. For Adani, this wasn't just acquiring a port—it was establishing a beachhead on India's eastern coast, opening access to cargo from the industrial states of Odisha, Jharkhand, and West Bengal.

The Dhamra acquisition demonstrated Adani's ability to see value where others saw challenges. The port was underutilized, handling just 14.3 million tonnes against much higher capacity. But Adani understood that with the right infrastructure investments and customer relationships, volumes could be dramatically increased. With the acquisition of Dhamra Port, the group was planning to increase its capacity to over 200 Mt by 2020.

Following Dhamra, Adani continued its eastern expansion with the acquisition of Kattupalli port in 2016. Each acquisition followed a similar pattern: identify ports with strategic locations but operational challenges, acquire them at reasonable multiples, invest in infrastructure and efficiency improvements, and leverage Adani's network to drive volume growth. The deal, if successful, will be APSEZ's third acquisition on the east coast of India following the purchase of Dhamra port in 2014 and Kattupalli port in 2016.

But the crown jewel of the acquisition strategy came in 2020. In October 2020, Adani Ports completed the acquisition of a controlling 75% stake in Krishnapatnam Port Company Ltd. (KPCL) for an enterprise value of Rs 12,000 crore. KPCL is a multi-cargo facility port situated in the southern part of Andhra Pradesh, a state which has the second largest coastline in India. Located 180 km from Chennai, it was India's second largest private port with a capacity to handle 64 MMTPA.

The Krishnapatnam acquisition was transformational for several reasons. First, it gave Adani a dominant position on India's eastern coast, creating what Karan Adani called "cargo parity between west and east coasts of India." Second, the port came with 6,700 acres of land, providing enormous expansion potential. With a vast waterfront and land availability of over 6,700 acres, KPCL is capable of replicating Mundra and would be future ready to handle 500 MMT.

The financial engineering of these acquisitions was sophisticated. Adani typically acquired controlling stakes rather than 100% ownership initially, allowing them to conserve capital while gaining operational control. The company would then implement operational improvements to boost EBITDA margins—at Krishnapatnam, EBITDA margins improved from 57 per cent in FY20 to 72 per cent in FY21 following the acquisition.

The acquisition strategy wasn't limited to operational ports. Adani also bid aggressively for new port development opportunities. APSEZ won a bid with the Kerala government to construct the Vizhinjam International Seaport Thiruvananthapuram in 2015. This would be India's first deep-water transshipment port, capable of handling the largest container vessels in the world—a critical capability given that most of India's transshipment cargo was being handled through foreign ports like Colombo and Singapore.

By 2020, the transformation was complete. It is the largest port developer and operator in India with 12 strategically located ports and terminals -- Mundra, Dahej, Tuna and Hazira in Gujarat, Dhamra in Odisha, Mormugao in Goa, Visakhapatnam and Krishnapatnam in Andhra Pradesh, Dighi in Maharashtra and and Kattupalli and Ennore in Chennai- representing 24 per cent of the country's total port capacity.

The national expansion wasn't just about acquiring ports—it was about creating an integrated logistics network. It holds Category 1 License for the Indian Railways that helps in pan-India cargo movement. This license allowed Adani to run its own trains across the Indian railway network, creating door-to-door logistics solutions for customers. The company operated three logistics parks in Haryana, Punjab, and Rajasthan, creating inland nodes that could aggregate cargo for coastal movement.

The dredging business, which had started as a support function for Mundra, became a profit center in its own right. By 2018, Adani operated 19 dredgers, the largest fleet in India, providing services not just to its own ports but to competitors as well. This vertical integration meant that Adani controlled every aspect of the port business—from maintaining channel depths to moving cargo inland.

By 2020, Adani Ports had achieved what seemed impossible a decade earlier. From a single port in Gujarat, it had become India's port infrastructure backbone, handling approximately 25% of India's total cargo. The company wasn't just operating ports; it was shaping trade flows, influencing industrial location decisions, and fundamentally altering India's logistics landscape. The next phase would take this model global, but first, Adani would have to navigate the most significant challenge to its reputation and financial stability—the Hindenburg crisis.

VI. The Modi Era & Political Capital

The relationship between Gautam Adani and Narendra Modi cannot be understood without examining the crucible in which it was forged: the 2002 Gujarat riots. Modi faced criticism in particular for doing little to stop the killing of more than 1,000 people, mostly Muslims, in the 2002 Gujarat riots. The violence that engulfed Gujarat in February and March 2002 would define both men's trajectories and cement a partnership that would reshape India's political economy.

The crisis began on February 27, 2002, when a train carrying Hindu pilgrims caught fire near Godhra, killing 59 people. What followed was systematic anti-Muslim violence across Gujarat. According to official records, a little over 1,000 people were killed, three-quarters of whom were Muslim; independent sources estimated 2,000 deaths, mostly Muslim. Modi, who had become Chief Minister just months earlier, was accused of allowing—if not encouraging—the violence.

The business community's response to the riots would prove pivotal for both Modi and Adani. In response to his handling of the riots, Modi came under fire in 2003 from India's powerful trade association, the Confederation of Indian Industry (CII), which threatened to disinvest from the state of Gujarat. This was a potentially devastating blow to Modi's economic development agenda.

But this is where Adani made a calculation that would define his career. Adani, however, not only continued to invest in Gujarat throughout the scandal but also helped set up a new organization (Resurgent Group of Gujarat) that diluted the influence of CII in the state. The Resurgent Group of Gujarat (RGG) was founded as a rival organisation by local businessmen with Adani as its chairman, after leaders of the Confederation of Indian Industry (CII) criticized Modi's management of the 2002 Gujarat riots.

This wasn't just business loyalty—it was a strategic investment in political capital. After a pogrom killed hundreds of people, mostly Muslims, in Gujarat in 2002, Modi's alleged sanctioning of the killings drew criticism from the Confederation of Indian Industry (CII) – India's leading business chamber. Adani jumped to Modi's defence, setting up a rival chamber of commerce, the Resurgent Group of Gujarat (RGG) and threatening to leave the CII.

The partnership deepened through the creation of the Vibrant Gujarat summit. He, along with some other business interests, put up funds for Modi to host the first Vibrant Gujarat summit for which they hired Apco, a US public affairs consultancy. The summit – known as the "Indian Davos" – became a stepping stone for Modi to court global business. This summit would become Modi's platform to rebrand Gujarat—and himself—from a state tainted by communal violence to a destination for investment.

The symbiosis was perfect. Modi needed business allies to validate his economic development narrative and counter the international isolation he faced—the US State Department barred him from entering the United States in accordance with the recommendations of that country's Commission on International Religious Freedom. Adani needed political support for his infrastructure ambitions, particularly the massive land acquisitions and regulatory clearances required for ports and SEZs.

The business relationship between Adani and the state of Gujarat grew increasingly cordial in the 2000s. During this period, Adani's Mundra Port expanded from a single berth to India's largest private port. The development happened with unprecedented speed, with environmental and regulatory clearances that typically took years being processed in months. The BJP led the Gujarat state government during key moments of the Adani Group's growth, and the relationship resulted in the symbiotic rise of both the BJP and the Adani Group.

When Modi ran for Prime Minister in 2014, the relationship became even more visible. In fact, a fleet of three Adani-owned aircraft – the jet and two choppers – had served the leader. The pilot of the Embraer reportedly said it had been bought by the Adani family in anticipation of Modi's busy election schedule. Though Adani maintained that Modi was paying for the use of his aircraft, the optics were clear: this was a partnership that transcended normal business-politics relationships.

Modi's elevation to Prime Minister in 2014 transformed Adani from a regional infrastructure player to a national champion. In July 2014 Adani received his first major reprieve from the new BJP-led union government. He secured environmental clearances for the Adani Group's special economic zone in Mundra. In January of that year the special economic zone for the Adani Group had been declared illegal by the Gujarat High Court for failing to obtain the clearances years earlier.

The pattern continued with airports. Controversy over Adani's courtship of infrastructure projects grew in 2018, when the union government moved to privatize six airports. Adani won contracts for all six. His successful bids led to accusations of cronyism, but the government maintained that the process had been transparent and that the Adani Group had won fairly by bidding aggressively.

The relationship wasn't covert—it was celebrated. The relationship with Modi is far from covert. Adani – along with some other businessmen – regularly accompany the prime minister on state visits. Generally, the pair's interests are viewed as synonymous. This visibility served both men's purposes. For Modi, Adani's success validated his economic model. For Adani, proximity to power provided not just business opportunities but protection from scrutiny.

The infrastructure-politics nexus that Adani had mastered in Gujarat was now operating at a national scale. Ports, airports, power plants, transmission lines—every major infrastructure tender seemed to have Adani as a serious contender, often the winning one. The company's market capitalization soared from a few billion dollars in 2014 to over $200 billion by 2022, making Adani briefly Asia's richest person.

But this relationship also created vulnerabilities. His close relationship with the party is not coincidental: Adani frequently refers to his business strategy as motivated by "nation building." This narrative of private enterprise serving national interest provided ideological cover for what critics called crony capitalism. The concentration of infrastructure assets in the hands of a single group closely aligned with the ruling party raised questions about market competition, regulatory independence, and the long-term health of India's economy.

The Modi-Adani relationship represents a new model of political economy in India—one where select private players become quasi-state actors, implementing national infrastructure priorities while maintaining the efficiency and profitability of private enterprise. It's a model that has delivered impressive infrastructure development but at the cost of raising fundamental questions about the relationship between economic and political power in the world's largest democracy.

VII. Going Global: International Ambitions

In July 2022, Adani's ambitions transcended India's borders in a dramatic fashion. A consortium of Adani Ports and Special Economic Zone Ltd (APSEZ) and Israel's Gadot Group won the tender to privatise the Port of Haifa, the second largest port in Israel, for $1.18 billion. The deal saw Adani Ports and Special Economic Zone (APSEZ) acquire a 70 percent stake of the now privatised Haifa Port, while Israel's Gadot Group purchased the remaining 30 percent.

The Haifa acquisition was remarkable for multiple reasons. First, the price: Adani Ports offered a rather staggering 4.1 billion shekels (USD 1.18 billion) for the port, 55 per cent more than the second highest bid. This was clearly a "strategic purchase" where "price was less important"—Adani wasn't just buying a port; he was buying entry into a geopolitically crucial region.

The timing of the acquisition was equally significant. The bid came through around the same time when the leaders of I2U2, comprising India, Israel, US and UAE, were holding a virtual conference. This new quadrilateral partnership was being positioned as a counter to China's growing influence in the region. The infrastructure empire belonging to Gautam Adani, a personal friend of Modi and the richest person in Asia, was declared the winner after immense pressure by the United States on the Chinese not to submit a bid and after the Emiratis withdrew at the last minute.

When Netanyahu handed Adani the proverbial key to Haifa Port on January 31, 2023, his words were revealing: "Over 100 years ago, and during World World I, it was brave Indian soldiers who helped liberate the city of Haifa. And today, it's very robust Indian investors who are helping to liberate the port of Haifa." The historical reference wasn't merely ceremonial—it positioned the acquisition as part of a broader civilizational partnership between India and Israel.

For Israel, the acquisition was a boon. It would help re-establish the port as a key hub in the Middle East, and provide Israel with a unique opportunity to establish a trade route connecting the Mediterranean and the Gulf, bypassing the Suez Canal. Bypassing the Suez Canal, now Haifa port would cut the shipping time from Mumbai to Europe by almost 40%. This wasn't just about port operations—it was about redrawing global trade routes. The Haifa acquisition was just the beginning of Adani's global ambitions. In March 2021, APSEZ received a Letter of Intent from the Ministry of Ports and Shipping of Sri Lanka for the development and operations of West Container Terminal (WCT) in Colombo. APSEZ would partner with John Keells Holdings PLC and the Sri Lanka Ports Authority under a 35-year Build, Operate and Transfer basis. As the first ever Indian port operator in Sri Lanka, Adani Ports will hold 51% in the terminal partnership.

The Colombo terminal represented a direct challenge to China's maritime dominance in the Indian Ocean. The Colombo Port is already the most preferred regional hub for transhipment of Indian containers with 45% of Colombo's transhipment volumes either originating from or destined to an Adani port terminal in India. By controlling this critical node, Adani was positioning itself at the center of South Asian maritime trade.

The financing of the Colombo terminal became a geopolitical drama in itself. Standing before Sri Lankan officials and US diplomats in a five-star hotel in Colombo, Karan Adani boasted that a newly inked $553 million US government financing deal toward the port terminal was a "reaffirmation by the international community." However, following the Hindenburg crisis and subsequent US indictments, Adani withdrew from the US loan deal, choosing to finance the terminal through internal accruals instead.

In Tanzania, Adani made another strategic move. In May 2024, Tanzania and Adani Ports finalised a 30-year concession agreement to operate Container Terminal 2 at Dar es Salaam port. Additionally, Adani Ports acquired a 95 percent stake in Tanzania International Container Terminal Services, a state-owned entity, for $95 million. This gave Adani a foothold in East Africa, a region increasingly important for Indian Ocean trade.

The most ambitious plans were yet to come. Plans for new port in Da Nang, Vietnam with in-principle approval represented Adani's entry into Southeast Asia, a region dominated by Chinese ports. This will be Adani group's fourth international port, joining its counterparts in Haifa, Israel; Colombo, Sri Lanka; and the Port of Dar es Salaam, Tanzania.

The international expansion strategy revealed sophisticated geopolitical thinking. Each port acquisition wasn't just about commercial opportunity—it was about creating an alternative to China's Belt and Road Initiative. As India's largest port operator, Adani Ports currently derives about 5% of its volume from international operations and aims to double this to 10% by 2030. The company was targeting opportunities in the Middle East, Southeast Asia, East Africa, Bangladesh, Sri Lanka, Maldives, Vietnam, and Cambodia—essentially creating a "String of Ports" that would rival China's maritime infrastructure.

The numbers backed up the ambition. International operations rose 16.4% from Rs 2,378 crore in the April-December period of 2023 to Rs 2,769 crore in the first nine months of fiscal 2024. International operations are now outpacing logistics in EBITDA contribution, with margins expected to reach 30% in the next two years. Domestic ports will continue their normal growth trajectory and account for around 820-850 million metric tonnes by 2029-30, while 140-150 million metric tonnes will be international.

But this global expansion wasn't without risks. Each port represented not just an investment but a bet on geopolitical stability. The Haifa port made Adani a stakeholder in Middle East security. The Colombo terminal put the company at the center of India-China competition in the Indian Ocean. The Tanzania operations exposed Adani to African political risks. The Da Nang plans would put the company in direct competition with Chinese state-owned enterprises in their backyard.

The international portfolio also created new vulnerabilities. When US prosecutors indicted Gautam Adani in late 2024, it wasn't just Indian operations that were affected. Some countries - including Kenya - had to cancel deals associated with his companies. The Sri Lankan government opened an investigation into local investments of Adani Group. The global footprint that was meant to diversify risk had also globalized reputational challenges.

Yet the strategic logic remained compelling. By controlling ports from the Mediterranean to Southeast Asia, Adani wasn't just building a business—it was creating infrastructure for a new world order where India, not China, would be the anchor of Asian trade. The company was positioning itself as the logistics backbone of the India-Middle East-Europe Economic Corridor, an alternative to China's Belt and Road that had the backing of the United States, Europe, and Gulf nations.

The transformation from a single port in Gujarat to a global maritime network spanning four continents represented more than corporate expansion. It was infrastructure as statecraft, business as geopolitics, and the projection of Indian economic power through private enterprise. The boy from Ahmedabad who started as a diamond sorter was now playing on the global chessboard, moving ports like pieces in a game where commerce and geopolitics had become indistinguishable.

VIII. The Hindenburg Crisis & Recovery

On January 24, 2023, a relatively unknown New York-based research firm named Hindenburg Research published a report that would shake the foundations of the Adani empire. The timing was exquisite in its malevolence—Adani Enterprises was in the middle of India's largest-ever Follow-on Public Offering (FPO), seeking to raise $2.5 billion from investors. The report's title left nothing to the imagination: "Adani Group: How The World's 3rd Richest Man Is Pulling The Largest Con In Corporate History."

The allegations were explosive and comprehensive. Hindenburg claimed its two-year investigation showed that the Adani group was involved in massive and "brazen stock manipulation" and an "accounting fraud scheme." The report detailed how a network of opaque offshore fund operators surreptitiously helped Adani evade minimum shareholder listing rules, citing numerous public documents and interviews to substantiate the allegations.

The initial response from the Adani Group was swift and combative. We are shocked that Hindenburg Research has published a report on 24 January 2023 without making any attempt to contact us or verify the factual matrix. The report is a malicious combination of selective misinformation and stale, baseless and discredited allegations. The company claimed the timing "clearly betrays a brazen, mala fide intention to undermine the Adani Group's reputation with the principal objective of damaging the upcoming Follow-on Public Offering."

But the market's reaction was devastating. Adani Group's stock value plunged by nearly $150bn after Hindenburg Research's first report. At one point, the group lost more than $104 billion in market value, approximately half of its total market capitalization. Gautam Adani's personal wealth plummeted from over $120 billion to below $50 billion, dropping him from Asia's richest person to outside the global top 20.

The FPO became a disaster. Despite being fully subscribed initially, the offering had to be withdrawn as share prices continued to plummet. The company returned the entire proceeds to investors—an unprecedented humiliation for what was supposed to be India's corporate champion. Banks that had extended loans against Adani shares faced margin calls. International investors fled. Credit rating agencies put the group on watch.

But the 413-page response that followed on January 29 was more than a rebuttal—it was a declaration of war. "This is not merely an unwarranted attack on any specific company but a calculated attack on India, the independence, integrity and quality of Indian institutions, and the growth story and ambition of India," the company declared. The response wasn't just defending Adani; it was wrapping the company in the Indian flag.

The document was exhaustive in its detail but selective in its substance. Only 30 pages of the riposte focused on issues related to the report and that the conglomerate failed to answer 62 questions out of the 88 raised in the report. Of the 88 questions raised by Hindenburg, 65 of them relate to matters that have been duly disclosed by Adani portfolio companies. Of the balance 23 questions, 18 relate to public shareholders and third parties (and not the Adani portfolio companies), while the balance 5 are baseless allegations based on imaginary fact patterns.

Hindenburg's counter-response was swift and cutting. "To be clear, we believe India is a vibrant democracy and an emerging superpower with an exciting future. We also believe India's future is being held back by the Adani Group, which has draped itself in the Indian flag while systematically looting the nation." The short-seller maintained that the response "largely confirmed Hindenburg's findings and ignored key questions".

But in the depths of the crisis, an unlikely savior emerged. Rajiv Jain, the Fort Lauderdale-based founder of GQG Partners, saw opportunity where others saw disaster. In March 2023, just weeks after the Hindenburg report, GQG Partners had initially invested Rs 15,446 crore ($1.87 billion) in four Adani group companies. This wasn't a small bet—it was a massive contrarian investment that would define both firms' futures.

The investment wasn't made lightly. Jain, a veteran investor with decades of experience, conducted his own due diligence and concluded that the Adani assets were fundamentally sound. "Within five years, we would like to be one of the largest investors in Adani Group depending on the valuation, after the family," Jain said in an interview. The confidence was backed by action—"The total investment is close to $2.2-2.4 billion approximately in over a dozen separate accounts....we own these (shares) in multiple accounts."

GQG didn't stop there. In June 2023, the firm doubled down, investing Rs 4,100 crore Adani Enterprises, Rs 2,650 crore in Adani Energy Solutions, Rs 4,600 crore in Adani Green Energy. By August 2023, GQG's Jain injected $1.1 billion or Rs 8,700 crore in Adani Power. The total commitment was staggering: Between March and October 2023, GQG invested around Rs 38,500 crore (then USD 4.6 billion) in six Adani Group companies.

The investment proved spectacularly successful. Overall, Jain had invested a total of $4.3 billion in the group, which is now worth close to $10 billion. GQG Partners had bought Adani shares worth Rs 35,774 crore in March 2023 a nearly couple of months after a Hindenburg Research report that was critical of the group -- has seen the value of its investment more than double to Rs 81,132 crore as of Friday's closing.

Other institutional investors followed GQG's lead. The Qatar Investment Authority, which had invested Rs 4,300 crore in Adani Green Energy at Rs 923 per share in August 2023, now finds its stake to be worth Rs 9,650 crore. International Holding Company, which initially invested Rs 16,612 crore in Adani Enterprises in 2022 and subsequently increased its stake to 5 per cent in October last year, has seen the value of its investment rising to Rs 23,257 crore.

The recovery in market value was equally dramatic. In May 2024, the Adani Group's market capitalisation returned to over $200 billion after the Supreme Court directed the Securities and Exchange Board of India (SEBI) to expedite its investigation. The group that had lost half its value was back to pre-crisis levels within 15 months—a recovery that defied market expectations and validated the contrarian investors who had backed Adani at his lowest point.

The crisis management went beyond just attracting new investors. The group took aggressive steps to shore up its financial position, repaying debt, releasing pledged shares, and improving transparency. The fundamentals of the business remained strong throughout—ports continued to handle cargo, power plants continued to generate electricity, and the infrastructure empire continued to expand.

But the Hindenburg crisis left lasting scars. It exposed the vulnerabilities of concentrated ownership, the risks of political proximity, and the challenges of operating in global capital markets while maintaining close ties to a controversial government. The recovery was complete in financial terms, but the reputational damage would linger, making Adani Group a lightning rod for debates about corporate governance, market manipulation, and the nature of Indian capitalism itself.

IX. The Business Model & Competitive Moat

The economics of port operations are deceptively simple yet profoundly powerful. A port is essentially a toll booth on global trade—every container, every ton of coal, every barrel of oil that moves between ship and shore generates revenue. But unlike a highway toll booth that can be bypassed, major ports are irreplaceable infrastructure with natural monopoly characteristics. This is the foundation of Adani Ports' business model.

The company's crown jewel remains Mundra, which has evolved into something far beyond a traditional port. With 26 berths and 231 MMT annual capacity, Mundra operates at a scale that creates insurmountable advantages. The port's deep-water capabilities allow it to handle the largest vessels in the world—a critical advantage as shipping lines continue to deploy ever-larger ships to achieve economies of scale. But it's not just size that matters; it's the ecosystem that Adani has built around the port.

The integration strategy is what truly sets Adani Ports apart. The company doesn't just operate ports; it controls the entire logistics chain. With Category 1 License for Indian Railways, Adani can run its own trains across the Indian railway network, moving cargo directly from factory gates to ship holds. The three logistics parks in Haryana, Punjab, and Rajasthan serve as inland aggregation points, allowing the company to consolidate cargo and achieve better utilization of both rail and port infrastructure.

The market share numbers tell the story of dominance. In Q1 FY26, Adani Ports commanded an all-India cargo market share of 27.8%—more than one in four tons of cargo moving through Indian ports was handled by Adani. In containers, the dominance is even more pronounced, with a container market share of 45.2%. This isn't just market leadership; it's approaching monopolistic control in certain segments.

The financial metrics reveal the power of this model. Domestic ports operate at EBITDA margins of 72%, while even the logistics business achieves EBITDA margins of 28%. These aren't the margins of a commodity business—they're the margins of a company with significant pricing power and operational leverage. Every incremental ton of cargo that flows through the system has minimal marginal cost but generates substantial revenue.

The network effects in the port business are often underappreciated. As Adani controls more ports, it becomes the default choice for shipping lines that want simplified operations across multiple Indian destinations. A shipping line can deal with one operator for multiple ports, simplifying documentation, payments, and operational coordination. This creates switching costs that lock in customers even if competitors offer marginally lower prices.

The capital intensity of the business serves as both a challenge and a moat. Building a greenfield port requires billions in upfront investment, years of construction, and the ability to operate at losses until volumes reach critical mass. Few companies have the balance sheet, operational expertise, and patience to compete. This high barrier to entry protects Adani's market position even as India's port capacity needs continue to grow.

But the real genius of the Adani Ports model lies in its anticipatory investment strategy. The company consistently builds ahead of demand, accepting lower utilization initially in exchange for capturing market share when demand materializes. This strategy requires deep pockets and conviction, but it ensures that when a customer needs capacity, Adani is the only option with available berths.

The vertical integration extends beyond just logistics. By 2018, Adani operated 19 dredgers, the largest fleet in India. This means the company controls its own maintenance dredging, a critical ongoing expense for any port. It can also offer dredging services to competitors, turning a cost center into a profit center. This is the kind of operational leverage that separates good infrastructure businesses from great ones.

The Special Economic Zone model adds another layer to the moat. By controlling not just the port but the surrounding industrial land, Adani captures value from the entire supply chain. A manufacturer setting up in the Mundra SEZ gets preferential access to port facilities, simplified customs procedures, and integrated logistics—creating a sticky ecosystem that's extremely difficult to replicate or displace.

The unit economics at the individual port level are equally compelling. In Q4 FY25, net profit jumped 47.8% to ₹3,014.22 crore, demonstrating the operational leverage inherent in the model. As volumes grow, the fixed cost base gets spread over more units, driving margin expansion. This is why Morgan Stanley in 2017 called Adani Ports "top quartile across various operating metrics"—the company doesn't just operate ports; it operates them at efficiency levels that competitors struggle to match.

The competitive dynamics in Indian ports further strengthen Adani's position. The government's Sagarmala programme aims to develop port infrastructure, but government-run ports face bureaucratic constraints, labor issues, and political interference that private operators avoid. Meanwhile, other private players lack Adani's scale, political connections, and integrated logistics network. The result is a market structure where Adani faces limited real competition despite operating in what should be a competitive industry.

The platform characteristics of the port business create winner-take-most dynamics. Shipping lines want to minimize the number of port operators they deal with. Cargo owners want integrated logistics solutions. Both prefer dealing with the largest, most reliable operator. This creates a virtuous cycle where scale begets scale, market share begets market share, and dominance becomes self-reinforcing.

X. Financials & Unit Economics

The financial architecture of Adani Ports reveals a business that has mastered the art of converting infrastructure into cash flow. With a market capitalization of ₹2,95,313 Crore, the company stands as one of India's most valuable infrastructure assets. The headline numbers—₹32,645 Crore in revenue and ₹11,265 Crore in profit—tell only part of the story. The real narrative lies in how these numbers are generated and what they reveal about the underlying business model.

The margin structure is where Adani Ports truly distinguishes itself from typical infrastructure companies. Domestic ports achieving EBITDA margins of 72% puts them in rarefied company—these are software-like margins in a hardware business. Even the logistics business, with EBITDA margins of 28%, outperforms most pure-play logistics companies. This margin differential isn't accidental; it's the result of strategic positioning, operational excellence, and market power.

The growth trajectory has been nothing short of spectacular. Q4 FY25 saw net profit jump 47.8% to ₹3,014.22 crore, a growth rate that would be impressive for a technology company, let alone a capital-intensive infrastructure business. This growth isn't just from volume increases—it's from operational leverage kicking in as the company's massive infrastructure investments begin to pay off.

The capital allocation strategy reveals sophisticated financial thinking. The company has managed to fund massive expansion while maintaining reasonable leverage ratios. The debt isn't just growth capital—it's strategically deployed to create assets that generate predictable, long-term cash flows. The ability to handle 450 MMT in FY25 against a capacity of 633 MMT suggests significant headroom for growth without major capital expenditure.

Cash generation is the ultimate test of any infrastructure business, and here Adani Ports excels. The high EBITDA margins translate into robust cash flows, which fund both growth investments and debt service. The company has consistently generated enough cash to fund expansion while maintaining financial flexibility—a delicate balance that many infrastructure companies fail to achieve.

The return metrics paint a picture of exceptional capital efficiency. Despite the capital-intensive nature of the port business, the company generates returns on capital that exceed its cost of capital by a wide margin. This value creation is reflected in the stock price performance, with the company consistently outperforming broader market indices.

The debt management deserves special attention. While the Hindenburg report raised concerns about leverage, the company's ability to service and reduce debt has been impressive. Post-crisis, the company has focused on deleveraging, using strong operational cash flows to reduce debt ratios and improve credit metrics. This conservative approach to leverage has won back institutional investors who were initially spooked by the Hindenburg allegations.

The working capital management is another area where Adani Ports excels. Ports typically have favorable working capital dynamics—customers pay upfront or quickly while major expenses are predictable and manageable. Adani has optimized this further through efficient operations and strong customer relationships, resulting in negative working capital in many periods.

The revenue mix provides natural hedging against economic cycles. Container cargo is linked to consumer demand and trade flows. Bulk cargo like coal and iron ore is tied to industrial activity. Liquid cargo connects to energy markets. This diversification means that weakness in one segment is often offset by strength in another, providing stability to overall financial performance.

The pricing power embedded in the business model shows up clearly in the financials. The company has been able to raise prices consistently without losing significant volume—a testament to both its market position and the value it provides to customers. This pricing power is particularly evident in value-added services where Adani faces limited competition.

The financial resilience was tested during the Hindenburg crisis and proved robust. Despite a massive selloff in the stock and concerns about access to capital, the underlying business continued to generate strong cash flows. Operations were unaffected, customers didn't flee, and the financial metrics remained strong. This operational resilience during financial turmoil demonstrates the difference between market perception and business reality.

Looking at segment-level performance reveals interesting dynamics. The port business remains the cash cow, generating the bulk of profits. The logistics business, while lower margin, provides strategic value by feeding cargo to ports and creating customer stickiness. The SEZ operations, though smaller in revenue terms, generate high returns on invested capital due to the land value appreciation component.

The international operations are beginning to contribute meaningfully to the financials. While still a small percentage of total revenue, the margins from international ports are improving as operations stabilize and synergies are realized. The Haifa port acquisition, while expensive, is expected to be earnings accretive within a few years as volumes grow and operational improvements are implemented.

The capital expenditure trajectory going forward is more measured than in the past. With major port infrastructure in place, future capex will focus on incremental capacity additions, technology upgrades, and strategic acquisitions. This shift from growth capex to maintenance capex should result in higher free cash flow generation, supporting both dividend payments and further deleveraging.

XI. Playbook: Infrastructure Investing Lessons

The Adani Ports story offers a masterclass in infrastructure investing in emerging markets, with lessons that extend far beyond ports and logistics. The playbook that emerges from analyzing their three-decade journey reveals patterns that separate successful infrastructure investors from those who fail to capture value in these capital-intensive, politically sensitive sectors.

Timing Public-Private Partnership Opportunities

The first lesson is about timing. Adani entered the port sector at precisely the moment when India was liberalizing its infrastructure policies but before competition had emerged. This wasn't luck—it was pattern recognition. The company identified that India's economic growth would outpace port capacity, that the government would be forced to allow private participation, and that first movers would capture disproportionate value. The key insight: in emerging markets, the window between policy liberalization and competitive saturation is narrow but enormously profitable.

The "Land Bank" Strategy

Perhaps no strategy has been more crucial to Adani's success than its approach to land. The company didn't just acquire land for ports—it acquired vast tracts of coastal land that could be developed into integrated industrial ecosystems. In emerging markets, land near infrastructure often appreciates faster than any other asset class. The Mundra SEZ, spread across 6,473 hectares, represents billions in land value appreciation beyond its operational value. The lesson: in infrastructure investing, control the land around the infrastructure, not just the infrastructure itself.

Managing Political Relationships Without Capture

The delicate dance between political proximity and independence is perhaps the most controversial aspect of the Adani playbook. The company has masterfully navigated changing political regimes while maintaining close ties to power. This isn't simple cronyism—it's understanding that in emerging markets, infrastructure and politics are inextricably linked. The key is to be useful to politicians (by delivering infrastructure that creates jobs and growth) while maintaining enough independence to survive regime changes.

Building in Anticipation vs. Following Demand

Conventional wisdom suggests building infrastructure to meet existing demand. Adani consistently did the opposite—building massive excess capacity in anticipation of future demand. Mundra was built to handle 338 MMT when initial volumes were a fraction of that. This strategy requires deep pockets and conviction, but it ensures that when demand materializes, you're the only game in town. The lesson: in infrastructure, capacity constraints are opportunities for those who build ahead of the curve.

Network Effects in Physical Infrastructure

Most people associate network effects with digital platforms, but Adani demonstrated that physical infrastructure can exhibit similar dynamics. Each additional port in the Adani network makes all other ports more valuable. Shipping lines prefer dealing with one operator across multiple ports. Cargo owners value integrated logistics solutions. The lesson: in infrastructure investing, focus on assets that become more valuable as you acquire more of them.

The Vertical Integration Imperative

Adani's control of the entire logistics chain—from ports to railways to inland logistics parks—creates value that standalone assets cannot capture. This vertical integration isn't just about operational efficiency; it's about controlling customer relationships and capturing value at multiple points in the chain. The lesson: in emerging markets where infrastructure is fragmented, vertical integration creates competitive advantages that are nearly impossible to replicate.

Managing Capital Intensity

Infrastructure requires enormous upfront capital with long payback periods. Adani's approach—using public markets for equity, international markets for debt, and operational cash flow for expansion—provides a template for managing capital intensity. The key insight: infrastructure investing requires not just capital but sophisticated capital structuring that matches funding sources to asset characteristics.

The Platform Transition

Adani's evolution from port operator to logistics platform to infrastructure conglomerate illustrates a crucial transition. The company moved from owning assets to orchestrating ecosystems. The SEZ model, where Adani provides not just port services but power, water, and land to industrial customers, represents platform thinking applied to physical infrastructure. The lesson: the highest returns in infrastructure come not from owning assets but from creating platforms that others must use.

ESG Navigation in Controversial Sectors

With over 60% of revenue from coal-related businesses, Adani faces enormous ESG challenges. Their response—aggressive renewable energy investments, efficiency improvements, and sustainability messaging—provides a template for managing ESG concerns while maintaining profitable but controversial operations. The lesson: in infrastructure, ESG challenges are inevitable; the key is to manage the transition while maintaining profitability.

Crisis as Opportunity

The Hindenburg crisis could have destroyed Adani Ports. Instead, it became an opportunity to attract new investors (like GQG), improve governance, and demonstrate operational resilience. The lesson: in infrastructure investing, financial crises that don't affect operations create buying opportunities for those with conviction and capital.

The Regulatory Arbitrage

Adani's success partly stems from navigating India's complex regulatory environment better than competitors. The company's ability to obtain environmental clearances, land acquisition permissions, and operational licenses faster than others creates competitive advantage. The lesson: in emerging markets, regulatory navigation capability is as important as operational excellence.

XII. Analysis & Bear vs. Bull Case

Bull Case: The Infrastructure Backbone of Rising India

The optimistic view of Adani Ports rests on several compelling pillars. First and foremost is the irreplaceable nature of the infrastructure. As the largest private port operator with 633 MMT capacity, handling 450 MMT in FY25, Adani has built assets that would take competitors decades and tens of billions of dollars to replicate. These aren't just ports; they're critical nodes in India's economic architecture.

The India growth story remains in its early innings. With the economy targeting $5 trillion by 2027 and $10 trillion by 2035, trade volumes must grow exponentially. Historical patterns suggest that trade grows at 1.5-2x GDP growth, implying a doubling or tripling of port volumes over the next decade. Adani, controlling nearly 30% of India's port capacity, is positioned to capture a disproportionate share of this growth.

The network effects are accelerating. Each new port acquisition, each logistics park, each customer relationship makes the entire network more valuable. Shipping lines are consolidating their Indian operations with Adani for simplicity. Manufacturing companies are choosing Adani SEZs for integrated logistics. This isn't just market share gain; it's ecosystem lock-in that becomes stronger over time.

The financial metrics support aggressive valuation. With EBITDA margins exceeding 70% at ports and strong cash generation, the company can fund growth while rewarding shareholders. The successful recovery from the Hindenburg crisis demonstrates resilience that few companies can match. The return of institutional investors like GQG, Qatar Investment Authority, and IHC validates the fundamental strength of the business.

The international expansion opens new growth vectors. Haifa, Colombo, Dar es Salaam—these aren't just ports but beachheads for becoming a global infrastructure player. If Adani can replicate even a fraction of its Indian success internationally, the value creation potential is enormous.

Bear Case: Political Risk and Energy Transition Threats

The pessimistic view starts with political concentration risk. The company's close ties to the Modi government are both its greatest strength and potentially fatal weakness. A change in government could bring regulatory scrutiny, license cancellations, or forced divestments. The infrastructure sector in emerging markets is littered with companies that flew too close to political power and got burned when regimes changed.

The ESG challenge is existential. With more than 60% of revenue from coal-related businesses, Adani Ports faces a future where its core cargo may disappear. International investors are increasingly avoiding coal-exposed companies. Financial institutions are restricting lending. Even if India continues using coal longer than developed markets, the transition is inevitable, and Adani's business model must fundamentally change.

Corporate governance concerns persist despite the post-Hindenburg improvements. The complex web of related-party transactions, the concentration of power in the Adani family, and questions about capital allocation remain. The Hindenburg allegations may have been disputed, but they exposed structural governance issues that haven't been fully resolved.

The debt levels, while manageable, remain elevated. In a rising interest rate environment, the cost of servicing this debt increases. Any operational hiccup or loss of investor confidence could create a vicious cycle of credit downgrades, higher borrowing costs, and reduced financial flexibility. Infrastructure businesses are particularly vulnerable to credit crunches given their capital intensity.

Competition is intensifying. The government's Sagarmala programme aims to develop 12 major ports. Other private players are expanding. International ports like Colombo and Dubai are competing for Indian transshipment cargo. While Adani has first-mover advantages, margins will likely compress as competition increases.

Regulatory risks are mounting. The government could impose price caps on port services, mandate service obligations that reduce profitability, or change tax structures that affect economics. The recent scrutiny from SEBI, even if ultimately cleared, shows that regulators are watching closely.

The Balanced View

The truth likely lies between these extremes. Adani Ports has built genuinely valuable infrastructure that will generate cash flows for decades. The network effects and market position are real and defensible. India's growth story will drive volume growth that benefits all port operators, but especially the dominant player.

However, the risks are equally real. Political concentration, governance concerns, and energy transition challenges aren't easily dismissed. The company will need to navigate these carefully while transforming its business model for a post-carbon future.

The investment case ultimately depends on time horizon and risk tolerance. For those believing in India's long-term growth and Adani's ability to navigate political and energy transitions, the current valuation may represent opportunity. For those concerned about governance and political risk, the company remains uninvestable regardless of operational excellence.

XIII. Epilogue & "If We Were CEOs"

Standing at the helm of Adani Ports today would mean confronting a fundamental paradox: how does a company built on carbon become a leader in decarbonization? The answer to this question will determine whether Adani Ports remains relevant in 2050 or becomes a stranded asset, a monument to a bygone era of fossil fuel dependence.

The Energy Transition Imperative

If we were running Adani Ports, the first priority would be aggressive diversification away from coal dependence. This isn't environmental activism; it's business survival. The company's 2016 announcement that all ports would run on 100% renewable energy by 2018 was a start, but insufficient. The real challenge is cargo mix transformation.

The strategy would involve three pillars. First, aggressively court non-coal bulk cargo—iron ore, fertilizers, grain. Second, accelerate container terminal development, as containerized cargo is less carbon-intensive and higher-value. Third, prepare infrastructure for tomorrow's cargo—hydrogen, ammonia, and other green fuels that will power the post-carbon economy. This means retrofitting terminals, training workforces, and building relationships with emerging green energy producers.

Becoming Truly Global

The international expansion to date has been opportunistic rather than strategic. If we were CEOs, we would articulate a clear global vision: becoming the emerging market port operator of choice. This means focusing on high-growth corridors—Africa to India, Southeast Asia to Middle East, Latin America to Asia. Each acquisition would be evaluated not just on financial metrics but on strategic value to the network.

The key would be replicating the integrated model internationally. Don't just operate ports; create economic zones, logistics parks, and industrial ecosystems. The Mundra playbook can work in Tanzania, Vietnam, and beyond, but it requires patient capital and deep local relationships.

Governance Revolution

The governance challenges won't disappear through denial. If we were CEOs, we would implement radical transparency. Separate the port operations from other Adani Group businesses. Bring in independent directors with global infrastructure experience. Implement arms-length pricing for all related-party transactions. Create a separately listed international subsidiary to access global capital markets without India-specific concerns.

Most radically, we would gradually reduce promoter holding to below 50%, bringing in sovereign wealth funds and pension funds as strategic shareholders. This would be painful for the Adani family but necessary for long-term sustainability.

Technology Transformation

Ports are ripe for technological disruption. If we were CEOs, we would launch "Adani Ports 2.0"—a complete digital transformation. Autonomous vehicles for container movement, AI-powered predictive maintenance, blockchain for documentation, digital twins for operational optimization. The goal: become the world's most technologically advanced port operator.

This isn't just about efficiency; it's about changing the competitive game. When ports become software-defined rather than hardware-constrained, traditional advantages erode, but new ones emerge. Adani's scale provides the perfect platform for technology investments that smaller operators cannot afford.

The Infrastructure-as-a-Service Model

The future of infrastructure isn't owning assets; it's orchestrating ecosystems. If we were CEOs, we would transition Adani Ports from an asset owner to a service provider. Manage third-party ports, provide technology platforms to smaller operators, offer logistics-as-a-service to industrial customers.

This capital-light model would generate fee income, reduce capital intensity, and create recurring revenue streams. It would also position Adani as an indispensable partner rather than just a service provider.

The Next Frontier

India's $5 trillion economy ambition requires infrastructure investment of unprecedented scale. If we were CEOs, we would position Adani Ports not just as a beneficiary but as an architect of this transformation. This means going beyond ports to create integrated industrial corridors, multimodal logistics parks, and smart cities anchored around ports.

The vision would be ambitious: by 2040, Adani Ports wouldn't just be India's largest port operator but Asia's infrastructure platform, connecting producers to consumers, enabling trade, and driving economic development. The company that started with one berth in Mundra would become the circulatory system of Asian commerce.

Final Reflections

The Adani Ports story is ultimately about the intersection of ambition and opportunity, of private enterprise and nation-building, of economic development and political power. It's a story that could only happen in India, at this moment in history, with these particular actors.

Whether Adani Ports becomes a century-spanning infrastructure giant or a cautionary tale about political proximity and concentrated ownership remains to be written. What's certain is that the company has already transformed India's infrastructure landscape, created enormous value, and demonstrated that emerging market companies can compete globally.

The next chapter will be written not in Gujarat's salt marshes but in boardrooms from Tel Aviv to Dar es Salaam, not through political connections but through operational excellence, not by moving coal but by enabling the green transition. The boy from Ahmedabad who started as a diamond sorter has built an empire. Whether that empire endures will depend on its ability to transform from what it was to what the world needs it to become.

XIV. Recent News

The latest developments at Adani Ports paint a picture of a company in transition. Q1 FY26 results exceeded expectations, with cargo volumes growing despite global trade headwinds. The company handled 110 MMT in the quarter, a 12% year-over-year increase, driven by strong container growth offsetting weakness in thermal coal.

The regulatory environment has stabilized post-Hindenburg. SEBI's investigation concluded without major findings, though enhanced disclosure requirements were mandated. The company has complied with all requirements and implemented additional governance measures including quarterly analyst calls and enhanced related-party transaction disclosures.

New port developments continue at pace. The Vizhinjam transshipment terminal in Kerala, delayed multiple times, is finally nearing completion with Phase 1 expected operational by early 2025. This will be India's first true transshipment hub, competing directly with Colombo for Indian cargo currently transshipped abroad.

On the competitive front, JSW Infrastructure's IPO and aggressive expansion plans signal intensifying competition. DP World's renewed focus on India and the government's push for major port modernization suggest the easy growth years may be behind. However, Adani's response—technology investments, service differentiation, and customer lock-ins—demonstrates awareness of changing dynamics.

The international operations are gaining momentum. Haifa port volumes are exceeding projections, with the Israel-India trade corridor showing unexpected strength. The Tanzania operations are benefiting from East Africa's economic growth. However, the Sri Lanka terminal faces delays due to local political opposition, highlighting the challenges of international expansion.

XV. Links & Resources

For those seeking deeper understanding of Adani Ports and the Indian infrastructure sector, primary sources remain invaluable. Annual reports from 2010 onwards chart the transformation from regional port to national champion. Investor presentations, particularly post-Hindenburg, provide management's perspective on strategy and governance.

Industry reports from ICRA, CRISIL, and India Ratings offer independent analysis of port economics and competitive dynamics. The Ministry of Shipping's Sagarmala documentation outlines government infrastructure plans that shape the operating environment. Academic papers from IIM Ahmedabad and ISB examine the public-private partnership model in Indian ports.