Adani Energy Solutions: The Grid that Powers the New India

I. Introduction: The "Boring" Utility with Tech-Level Growth

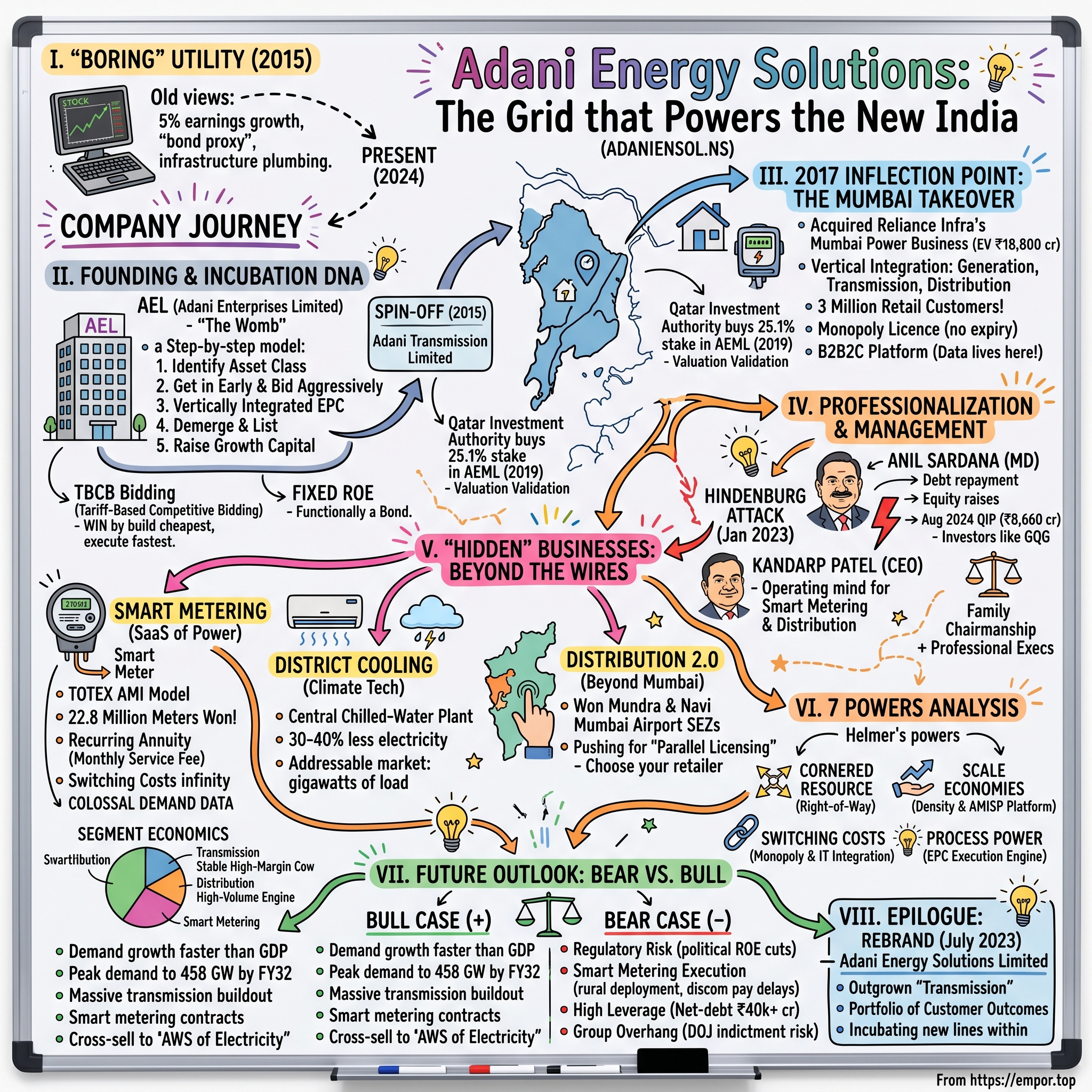

Picture a trading desk in Mumbai on a humid afternoon in 2015. A junior analyst pulls up a freshly listed ticker on his Bloomberg terminal — Adani Transmission Limited. He stares at the screen, then at his senior. "What do we do with this thing?" The senior shrugs. "It's a utility. Park it in the boring bucket. Maybe 5% earnings growth. A bond proxy." They close the tab and move on to the cement stocks.

That was the dominant view of Indian transmission utilities a decade ago — sleepy regulated entities that earned a fixed return on equity, paid out modest dividends, and were largely ignored by the growth-chasing crowd that lived for Infosys, HDFC Bank, and the next consumer story. Power transmission was infrastructure plumbing. Necessary, profitable, but unsexy.

That analyst, if he is still on a desk somewhere, has had a strange decade. The "boring" utility he ignored — now branded अदाणी ऊर्जा समाधान Adani Energy Solutions — grew its asset base roughly five-fold between FY16 and FY24, layered on a Mumbai distribution monopoly, became India's largest private smart-metering player, and rebranded itself from "Adani Transmission" to "Adani Energy Solutions" in July 2023 to signal an even more ambitious identity[^1]. Through one of the most violent short-seller attacks ever directed at an Indian conglomerate — the Hindenburg report of January 2023 — the company kept commissioning lines, kept winning bids, and kept raising capital from the world's most sophisticated infrastructure investors1.

So how did this happen? How does a company that did not exist as a standalone entity until 2015 end up as the toll booth for India's energy transition, a smart-meter behemoth, and a future "energy-as-a-service" platform — all inside a single decade?

The answer is buried in the अदाणी समूह Adani Group's distinct organisational DNA: the "infrastructure incubation" model. The mothership, Adani Enterprises, builds and tests new infrastructure verticals on its own balance sheet, then carves them out as listed pure-plays the moment they reach scale. Ports went first. Power generation followed. Then transmission. Then green energy. Then gas. Each spinoff inherits relationships, balance-sheet muscle, and — crucially — a promoter who is willing to under-bid the field for thirty-year concessions because his cost of capital and execution speed are simply better than anybody else's.

To understand Adani Energy Solutions is to understand that this is not really a utility. It is a high-growth infrastructure platform wearing a utility's clothes. The same family that built Mundra Port from a salt flat into India's largest private port has now turned its operating cadence on the wires, transformers, and smart meters that carry electrons from solar parks in Rajasthan to flats in Bandra. And the story of how they did it — the audacious Mumbai takeover, the talent coup from Tata Power, the smart-metering pivot, the post-Hindenburg recapitalisation — is one of the most interesting case studies in modern Indian capitalism.

This is the deep dive.

II. Founding & The "Incubation" DNA

Walk through the lobby of Adani House in Ahmedabad and you will notice something that the marketing brochures don't quite advertise: every business that has ever made the Adani Group money started life as a division inside Adani Enterprises Limited (AEL) — the holding-company-meets-incubator that गौतम अदाणी Gautam Adani founded in 1988 to trade commodities. AEL is the womb. Everything else is a child.

The pattern, repeated with almost industrial discipline, goes like this. Step one: identify a long-duration, capital-intensive infrastructure asset class where the government is the ultimate counterparty. Step two: get in early, before the field is crowded, and bid aggressively for the first set of concessions. Step three: build with a vertically integrated EPC (engineering-procurement-construction) capability so that you control timelines and costs. Step four: once the vertical has enough operating assets to stand alone, demerger and list it. Step five: use the listing to raise growth capital at lower cost, and then redeploy that into more bidding rounds.

Adani Ports was the first major demerger, in 2007. Adani Power followed in 2009. And then, on the night of June 25, 2015, the transmission vertical — assets that had been sitting inside Adani Enterprises, mostly built to evacuate power from group-owned Mundra and Tiroda thermal stations — was spun out as Adani Transmission Limited and listed on the NSE and BSE through a scheme of arrangement2. There was no IPO. Shareholders of Adani Enterprises simply received Adani Transmission shares in proportion to their holdings.

It is worth pausing on why that mattered. In the Indian power transmission sector, projects are awarded through one of two routes. The first, older route is "Regulated Tariff Mechanism" (RTM), where the central regulator — the Central Electricity Regulatory Commission, or CERC — awards a project to a chosen developer (historically the state-owned Power Grid Corporation of India) and then sets a tariff that allows the developer to recover its capital plus a fixed regulated return on equity, typically around 15.5%[^4]. It is a cost-plus model. Comfortable, but slow.

The second route, introduced in 2011 and made dominant by the Ministry of Power thereafter, is Tariff-Based Competitive Bidding (TBCB). Under TBCB, the project is awarded to the developer who quotes the lowest levelised tariff over the typical 35-year concession life of the asset. Whoever can build cheapest, finance cheapest, and execute fastest — wins. Whoever overbids, eats the loss.

This was the regulatory shift that Adani recognised before the rest of the private sector did. The state-owned incumbents were structurally slow. Tata Power and Sterlite (now part of the GR Infra and KKR-backed IndiGrid universe) were competitive, but neither had the bid-then-build ferocity that the Adani Group brought from its ports business. Adani had spent twenty years bidding for and building infrastructure on time and on budget; transmission lines, in the end, are just steel towers and aluminium conductors strung across a right-of-way. Build them faster, finance them cheaper, and the IRR math works.

The "Fixed ROE" framing is the part outsiders often miss. Indian transmission, unlike merchant generation, has almost no demand risk. Once a line is commissioned and the regulator notifies its "availability tariff," the asset gets paid based on whether it is available to carry electrons — not on whether electrons actually flow. The grid operator pays the line owner a monthly fixed charge so long as the line stays up. Availability targets in India sit above 99% for well-run lines. That makes a commissioned transmission asset functionally a bond — a 35-year, inflation-linked, government-backed cash flow stream — but built with equity that earns regulated double-digit returns.

The trick, then, is not the operating phase. It is the construction phase. If a developer can build a transmission line for ₹100 when the regulator assumed ₹120 of capex, the developer pockets a 20% capex saving as additional return on the equity portion. Capital efficiency in construction is what separates a 12% IRR from an 18% IRR. And Adani, with its in-house EPC arm and group purchasing power on steel and conductor, was structurally advantaged on exactly that dimension.

By the time Adani Transmission was demerged, the company already operated 5,050 ckm (circuit kilometres) of transmission lines, all built originally to connect group thermal plants to the central grid2. From that base, the playbook was clear: aggressively bid for TBCB projects across India, especially those evacuating power from the renewable-rich states of Rajasthan and Gujarat, and compound the asset base. The starting gun had been fired.

III. The 2017 Inflection Point: The Mumbai Takeover

If the 2015 demerger was the starting gun, the December 2017 announcement was the moment Adani Transmission stopped being a transmission company.

Anil Ambani's अनिल अंबानी Reliance Infrastructure had spent the better part of a decade trying to make its integrated Mumbai power business work. The asset was a jewel — a vertically integrated generation, transmission, and distribution licence covering the suburbs of Mumbai, serving roughly three million retail consumers across some of the most affluent postcodes in India. The catch was that Reliance Infrastructure had been running heavy losses across the group, ADAG was bleeding cash, and the parent needed a deleveraging event. So the Mumbai jewel was put on the block.

On December 21, 2017, Adani Transmission announced that it would acquire the Mumbai integrated power business of Reliance Infrastructure for an enterprise value of ₹18,800 crore — roughly $2.9 billion at the prevailing exchange rate[^5]. The transaction was structured as a slump sale of the generation, transmission, and distribution undertakings into a new Adani-controlled entity that would later be christened Adani Electricity Mumbai Limited (AEML).

The market reaction was, to put it charitably, mixed. Sell-side analysts looked at the multiple — roughly 11–12x trailing EV/EBITDA — and compared it to listed peers like Tata Power and Torrent Power, which were then trading closer to 8–9x. By that lens, Adani had paid a clear premium. The bear thesis wrote itself: aggressive promoter, overpriced asset, integration risk on a unionised workforce, regulatory exposure to the Maharashtra Electricity Regulatory Commission (MERC). Several brokerages downgraded the stock in the months following the announcement.

But the bear thesis missed what was actually being bought. Adani Transmission, as a transmission company, was selling capacity on wires. Margins were high but the customer count was zero — the counterparty was always a state-owned discom or central trading entity. AEML, by contrast, came with three million retail customers in India's wealthiest, most cash-rich metropolitan area, a regulated distribution monopoly licence that does not expire (subject to performance), and an existing 500 MW captive generation plant at Dahanu. Overnight, Adani went from a wires-only B2B utility to a B2B2C platform with direct billing relationships in Mumbai.

Why does that distinction matter? Because retail distribution is where data lives. Every meter is a customer touchpoint. Every billing cycle is a recurring revenue event. The unit economics of distribution — once the network is built — look much more like a subscription business than an infrastructure asset. Customer acquisition cost is effectively zero (you are the only legal supplier in your area). Churn is effectively zero. Pricing is regulated but inflation-protected. And the asset base on which you earn your regulated return keeps compounding because urban Mumbai keeps adding load.

The Adani team understood this. The deal also gave them something less tangible but equally valuable: balance-sheet credibility with global infrastructure investors. A wires-only company in Andhra Pradesh is a hard sell to a Canadian pension fund or a Gulf sovereign wealth fund. A Mumbai distribution monopoly is not. Two years after the deal closed, in December 2019, the قطر للاستثمار Qatar Investment Authority (QIA) bought a 25.1% stake in AEML for $452 million, validating the asset's standalone value and giving Adani a high-quality minority partner at the operating subsidiary level3. The acquisition that the street had called overpriced was, two years on, being marked up by sovereign capital.

There was also a quiet operational story that played out over the next several years. Aggregate Technical and Commercial losses — the industry term for power that is generated, sent down the network, but never billed or collected — sat at industry-average levels when Adani took over the Mumbai distribution business. Under the new ownership, AT&C losses in the Mumbai licence area trended well below national averages, settling in single digits — among the best-in-class for any distribution utility in the country, public or private4. The unsexy work of upgrading meters, repairing networks, and tightening collections paid off in cash.

In hindsight, Mumbai was not an acquisition. It was a category change. Adani Transmission walked in as a builder of wires and walked out as a manager of customers. And once you manage customers, every other energy-adjacent product — smart meters, district cooling, rooftop solar, EV charging — becomes a cross-sell, not a cold sale. That realisation would, eventually, force a name change.

But before we get to the name change, we need to talk about the people who made the operating side actually work.

IV. Current Management & The Professionalization of Adani

For most of the अदाणी समूह Adani Group's history, the joke in corporate India was that the org chart was a family tree. Gautam Adani as Chairman. Rajesh Adani राजेश अदाणी, his younger brother, as Managing Director of Adani Enterprises. Karan Adani करण अदाणी, his elder son, running Adani Ports. Pranav Adani प्रणव अदाणी, his nephew, handling agri and FMCG. Family-led, family-controlled, family-run. The professional CFO was a hired hand; everyone else who mattered shared a surname.

That model has limits. As the group's businesses crossed into the multi-tens-of-billions of enterprise value, and as global capital started underwriting larger and larger debt and equity tranches, the demand for "professional management" — with the regulatory comfort and operational depth that institutional investors expect — became impossible to ignore. Adani Energy Solutions has been, perhaps more than any other group company, the laboratory for that shift.

The signature move came in 2018, when Anil Sardana अनिल सरदाना joined the group. Sardana was not just any executive. He was the former Managing Director and CEO of Tata Power, where he had run India's largest private integrated power utility for nearly seven years. Before that, he had spent decades inside Tata Group entities, including a stint running Tata Teleservices. In the close-knit, almost monastic world of Indian power-sector leadership, Sardana was Tata royalty. The Tata Group culture — process-driven, audit-heavy, deliberately conservative — was widely viewed as the antithesis of the Adani culture, which prized speed and bias-to-action.

When Sardana joined Adani as the head of the transmission and distribution business, the message to the market was unmistakable: this is not a family shop anymore. He brought with him an entire operating template — capex governance committees, asset-commissioning checklists, safety protocols modelled on Tata standards — and grafted it onto the Adani execution engine. The result was a hybrid: Tata's institutional discipline marrying Adani's promoter-grade speed. Sardana now serves as the Managing Director of Adani Energy Solutions5.

Below him sits Kandarp Patel कंदर्प पटेल, the CEO. Patel is the operating mind behind the smart-metering and distribution expansion playbook. While Sardana sets the institutional cadence, Patel runs the day-to-day battle of winning advanced-metering-infrastructure (AMI) tenders, integrating IT and OT (operational technology) systems, and managing the deployment logistics of putting tens of millions of physical devices into Indian homes and small businesses. Smart-metering, as we will see, is the single most operationally complex business inside AESL, and it is Patel's portfolio.

At the top sits Gautam Adani as Chairman, still the ultimate capital allocator and the man who signs off on bid prices. But notice the structure: a family chairman with strategic and capital-allocation authority, paired with a non-family MD and CEO who own operational execution. This is, almost exactly, the structure that the better-governed Indian conglomerates — the Tatas, the Bajajs, the L&Ts of an earlier generation — converged on once they crossed a certain scale.

The incentive design tells the same story. Promoter holding in Adani Energy Solutions has hovered above 70% for most of its listed life, which gives the family enormous skin in the game6. But internal KPIs for the executive team are reportedly weighted heavily toward EBITDA growth, asset commissioning timelines, and AT&C loss reduction — operating metrics, not just top-line revenue. The compensation philosophy avoids the trap that has hurt other Indian promoter groups, where revenue-linked bonuses encouraged unprofitable growth.

A word, too, on the Hindenburg episode. On January 24, 2023, the U.S.-based short seller Hindenburg Research published a report alleging stock manipulation, accounting irregularities, and undisclosed related-party transactions across the Adani Group, wiping out roughly $150 billion of group market capitalisation at the trough1. Adani Energy Solutions was caught in the downdraft. What followed was not a retreat but a doubling down: the group accelerated debt repayment, pulled forward equity raises, and brought in additional institutional investors. AESL specifically completed a Qualified Institutional Placement (QIP) of ₹8,660 crore in August 2024 — one of the largest QIPs by an Indian utility — with allocations to GQG Partners (the U.S. boutique manager that famously took a contrarian long position post-Hindenburg) and several other global long-only funds7.

That a utility could raise that much equity, on those terms, less than two years after a short-seller attack, told you a lot about how institutional capital had come to view the asset. It also told you something about Sardana and Patel: they had professionalised the company sufficiently that global investors were willing to underwrite the operating story even while the wider promoter-level controversy still rumbled.

The transition from family shop to institutional platform is not complete. But Adani Energy Solutions is meaningfully further down that path than most of its sister companies. And that, more than any single transmission line or smart meter, is what underwrites the next decade of growth.

V. "Hidden" Businesses: Beyond the Wires

If you read only the cover of an Adani Energy Solutions investor presentation, you would assume the company is a transmission utility. The cover photo is invariably a sweeping shot of a 765 kV line marching across a desert landscape. The pitch deck talks about circuit kilometres and substation MVA capacity. Boring grid stuff.

Then you turn the page.

Sitting inside AESL is a portfolio of "hidden" businesses that, in aggregate, may end up worth more than the legacy transmission asset base within this decade. Investors who have done the work know this. The casual observer does not. Let us unpack each.

Smart Metering: The "SaaS" of Indian Power

The single most important business inside AESL today is smart metering — a vertical that did not even exist as a meaningful line item three years ago. Here is the setup. India has roughly 250 million electricity consumers, the vast majority served by financially stressed state-owned distribution companies (discoms). These discoms lose, on average, around 20% of the power they purchase to a combination of technical losses (line resistance, transformer inefficiencies) and commercial losses (theft, under-billing, collection failures). Those losses are why most Indian discoms have been technically bankrupt for two decades. Every state government bailout — and there have been many — eventually gets undone by losses creeping back up.

The Ministry of Power's answer, codified in 2021, was the Revamped Distribution Sector Scheme (RDSS), a ₹3 lakh crore programme that, among other things, committed central funding to roll out 250 million smart prepaid meters across India by FY26. The procurement model chosen — and this is the critical innovation — was the TOTEX (total expenditure) AMI Service Provider model. Under TOTEX, the discom does not buy the meters. Instead, a private operator (the AMISP) finances, installs, commissions, and operates the meter network for a typical 8–10 year concession, and gets paid a per-meter monthly service fee. The discom pays nothing upfront; the AMISP earns a steady recurring annuity[^11].

This is where the SaaS comparison comes in. A smart-meter AMISP looks a lot like a SaaS business. High upfront installation cost (analogous to customer acquisition cost). Long-tenor recurring revenue (analogous to ARR). Negligible variable cost once deployed (the meter sits on a wall and pings the cloud). Switching costs that approach infinity (rip-and-replace of installed meters is a regulatory and operational nightmare).

By March 2024, Adani Energy Solutions had won smart-meter contracts covering over 22.8 million meters — making it by a wide margin the largest private AMISP in India[^12]. Geographically, the wins were spread across Bihar, Andhra Pradesh, Assam, and Maharashtra. The cumulative order book translates to a multi-decade annuity stream once the meters are deployed and the per-meter service fees start flowing.

The numbers behind the smart-meter unit economics are genuinely interesting. A single meter costs in the range of ₹6,000-7,500 to procure and install. The monthly service fee paid by the discom, depending on the bid, ranges from ₹70-90 per meter per month. Over a 10-year concession life, each meter generates roughly ₹8,400-10,800 of revenue against ₹6,000-7,500 of upfront capex, plus modest operating expense. That is not the highest IRR business in the world, but the bid-then-build economics scale gloriously: every additional meter is incremental margin against a fixed central IT and ops backbone. Build a national platform once; deploy it twenty-million times.

The other thing that nobody talks about, but matters enormously, is the data. A smart meter pings consumption data every 15 to 30 minutes. Across 20 million meters, that is a colossal demand-side dataset that, in time, becomes the underlying intelligence for grid optimisation, dynamic tariff design, demand-response programmes, and EV-charging load management. Adani is not buying meters. It is building the data infrastructure for India's electricity demand-side.

District Cooling: The Climate-Tech Side Bet

Less developed, but strategically interesting, is the district cooling initiative. The concept: instead of every flat in a high-rise running its own split AC, a central chilled-water plant produces cooling for an entire commercial district or large mixed-use development, and pipes the cold water out to individual building units. Energy efficiency improves dramatically — district cooling typically uses 30–40% less electricity than equivalent decentralised cooling — and the carbon footprint shrinks correspondingly.

For a country where cooling demand is the single fastest-growing component of electricity consumption, this is meaningful. AESL began exploring district cooling concessions in collaboration with greenfield smart-city and special economic zone developers, including group-owned developments at GIFT City and Dholera. The economics rely on long-tenor anchor offtake agreements with commercial occupants. It is a small line today, but the optionality matters: if district cooling penetrates even modestly in Indian commercial real estate, the addressable market is several gigawatts of equivalent thermal load.

Distribution 2.0: Beyond Mumbai

The Mumbai win, as discussed, gave AESL a regulated distribution monopoly serving roughly three million retail consumers. The next chapter is geographic expansion. AESL won a distribution licence for the Mundra Special Economic Zone, where the group's own port and industrial cluster sits, giving it captive industrial offtake. It then won the distribution franchise for Navi Mumbai's airport SEZ and a handful of other niche industrial circles.

More ambitiously, AESL has been one of the most vocal advocates of "parallel licensing" — the regulatory concept that any consumer in India should be able to choose between competing distribution licensees, much like consumers in the U.K. can choose their energy retailer. The legal framework exists; political execution lags. If parallel licensing arrives in earnest in major Indian metros, AESL is structurally positioned to take share from the financially weaker state discoms.

The Segment Economics

Putting it together, the three businesses contribute differently to the P&L. Transmission is the steady, high-margin cash cow, with EBITDA margins consistently north of 90% on a stable base. Distribution is the high-volume engine, lower margin on a percentage basis but enormous in absolute rupees because of the gigawatt-hours flowing through the Mumbai network. Smart metering is the growth vector — currently a smaller share of EBITDA but ramping fast as deployed meter counts compound, and accretive to the long-term valuation because of its annuity nature.

The investor pitch, in plain English: a regulated utility floor plus a SaaS-shaped growth top. That is a combination Indian capital markets have not had to value before.

VI. Playbook: The Hamilton 7 Powers Analysis

Hamilton Helmer's "7 Powers" framework — the rubric most thoughtful investors borrow from his 2016 book — asks one question of any business: where does sustainable, durable advantage come from? Helmer's seven sources are Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power. A boring utility is not supposed to score on any of them. A great utility scores on three or four. AESL, by our reading, scores on at least four — which is why it has been able to compound at growth-stock rates inside a regulated wrapper.

Cornered Resource: The "Right of Way"

The single most underappreciated moat in Indian transmission is right-of-way (RoW). Stringing a 765 kV double-circuit line across 400 kilometres of rural India requires obtaining easements across thousands of individual landholdings, coordinating with state forestry departments, navigating tribal-area protections under the Fifth Schedule, and clearing wildlife-corridor environmental approvals. The acquisition of RoW for a major inter-state line can take three to five years and absorb hundreds of crores of administrative cost. Once acquired, it is functionally irreplaceable. No competitor can build a parallel line through the same corridor.

That makes commissioned transmission lines a textbook Cornered Resource in Helmer's framework — a privileged access to a critical input (in this case, geography itself) that competitors cannot replicate at any reasonable cost. The same asset, in a country with cheaper land and faster permitting, would not have the same moat. India's land-acquisition pain is precisely what makes the commissioned asset valuable.

Scale Economies: The Density Play in Mumbai

In the Mumbai distribution business, the marginal cost of servicing the next 100,000 customers, on a network that already exists, is meaningfully lower than the average cost of the existing customer base. This is classic Scale Economies. Fixed costs — the distribution network, the customer service organisation, the IT and billing infrastructure — are spread over a denser customer base every year as Mumbai's load grows. Operating leverage compounds quietly inside the regulated framework.

Smart metering offers a different flavour of scale. The central technology stack — the head-end system that ingests meter pings, the meter data management system, the analytics layer — is largely fixed-cost. Whether the platform manages five million meters or fifty million, the marginal cost of an additional meter on the platform is small. The first AMISP to cross 50 million meters in India will have a cost-per-meter that no late entrant can match.

Switching Costs: The Stickiness of Installed Infrastructure

Switching Costs in this business operate at three layers. At the consumer layer, retail distribution is a regulated monopoly — by definition, the consumer cannot switch. At the discom layer, once an AMISP has installed and integrated 10 million meters into the discom's billing system, switching to a competitor would mean ripping out the meters and rebuilding the IT integration, a multi-hundred-crore exercise no discom CFO would willingly authorise. At the regulatory layer, the 35-year transmission concessions are themselves immovable — the licence is the asset, and the asset stays.

Process Power: The Adani Execution Engine

The fourth Helmer power that AESL arguably has is Process Power — embedded, hard-to-copy operating capabilities. The group's EPC arm has built more high-voltage substations in India over the last decade than any other private contractor. The procurement engine sources steel, conductor, and transformers at scale-pricing that smaller competitors cannot match. The financing engine — the relationships with State Bank of India, ICICI, JICA, the Asian Development Bank, and the recent wave of international bond markets — gets capital faster and cheaper. None of these capabilities is a single trick; collectively, they form a process moat that has taken twenty years to build.

Porter's Five Forces, Briefly

Sitting alongside Helmer is the older Porter framework, which is also useful here. Threat of new entry: very low. The capital intensity (billions of dollars), regulatory licensing burden, and right-of-way acquisition timeline make greenfield entry impractical for any but the most credible operators. Threat of substitutes: effectively zero. There is no substitute for an electric grid in a modern economy; rooftop solar plus batteries reduces grid dependence at the margin but does not replace it. Buyer power: moderate, because end consumers are tariff-takers but state regulators set rates and can squeeze ROEs. Supplier power: moderate, with steel and aluminium pricing exposure offset by scale procurement. Competitive rivalry: moderate in the bidding round, low in operations.

The framework story is clean: AESL operates a business with multiple, layered, durable moats, in an industry where Porter would have predicted exactly that outcome. The question is no longer whether the business has a moat. The question is whether the moat can be widened — through smart metering, through data, through district cooling, through cross-sell — into adjacencies that the regulator has not yet learned to cap.

VII. Bear vs. Bull Case & Future Outlook

Every infrastructure platform's investment debate eventually compresses down to a single question: is this a regulated asset (price-capped, predictable, dull) or a platform (compounding, optionality-laden, valuable)? The bull and bear cases for Adani Energy Solutions hang on which side of that line investors place it.

The Bull Case

Start with the demand picture. India's electricity demand, after decades of growing roughly in line with GDP, is now growing faster than GDP — a structural inflection driven by air-conditioning penetration, EV adoption, data-centre buildout, and industrial electrification8. The Central Electricity Authority's projection for India's peak demand sits around 458 GW by FY32, nearly double the FY24 peak. To carry those electrons from the renewable-rich states (Rajasthan, Gujarat, Tamil Nadu) to the load-heavy states (Maharashtra, Karnataka, Delhi), India needs to build, by the CEA's own estimate, hundreds of thousands of additional circuit kilometres of high-voltage transmission. AESL, as the largest private operator in the space, is positioned to win a disproportionate share of that buildout.

Stack on top of that the smart-metering opportunity. If even half of India's 250 million electricity consumers get smart meters under TOTEX contracts, the addressable market is in the range of ₹1.5–2 lakh crore of cumulative revenue across the AMISP industry. AESL today controls a low-to-mid-double-digit share of awarded contracts. If they hold or grow that share, the smart-meter business alone becomes a multi-tens-of-thousand-crore revenue line by FY30.

Then layer on the cross-sell optionality. A company that owns the distribution network in Mumbai, the smart-meter platform across multiple states, and (through group subsidiaries) the rooftop-solar EPC capability and EV-charging concessions has, in principle, every primitive needed to be the "AWS of Indian electricity" — a platform on top of which retail energy products are bundled, billed, and serviced. None of that optionality is in current consensus numbers.

The capital story has also stabilised. The August 2024 QIP brought in ₹8,660 crore from quality long-only institutional investors7. Net-debt-to-EBITDA, while elevated as is normal for an infrastructure business, has come off its peaks. Credit ratings — both domestic (CRISIL AA+/Stable on the long-term debt) and international (investment-grade equivalents from S&P and Fitch on key SPV bonds) — have held through the Hindenburg cycle[^14]. Capital recycling, including the QIA partnership at AEML and selective stake sales at the SPV level, allows growth without diluting the listed parent's equity excessively.

The Bear Case

The bear case is not subtle. Start with regulatory risk. Indian transmission and distribution ROEs are set by a regulator that is, ultimately, a political body. The 15.5% regulated return on equity that defines the sector's IRR math is not a constitutional guarantee. It is a decision made every five-year tariff cycle by CERC and the state ERCs. If a future government decides that 15.5% is too generous and cuts it to 13%, billions of dollars of equity value evaporate overnight across the listed names. This is the single biggest tail risk that no operating excellence can hedge against.

Second is execution risk on smart metering. Deploying 20 million physical devices across rural and semi-urban India, integrating each with a discom's legacy billing system, and collecting per-meter fees from a customer (the discom) that may itself be in financial distress, is a genuinely hard operating challenge. Delays in deployment translate directly into deferred revenue. Discom payment delays translate into receivables build-up. AESL's smart-meter receivables, while currently well-managed, are a line item to watch.

Third is leverage. Infrastructure businesses are inherently capital-intensive, and the Adani Group has historically operated with debt loads at the higher end of comfortable. Net debt on AESL's balance sheet sat in the range of ₹40,000+ crore at recent reporting dates[^15]. Servicing that debt requires the regulated tariff machinery to keep producing cash on schedule. Any combination of payment delays from state discoms, regulatory tariff cuts, or interest-rate shocks puts pressure on coverage ratios.

Fourth is the group overhang. Even after the post-Hindenburg recapitalisation, the Adani Group remains under scrutiny from regulators including SEBI, and from international ESG-focused investors who avoid the group on governance grounds. Indictment of group executives in any foreign jurisdiction — and the U.S. Department of Justice's November 2024 indictment of Gautam Adani and other executives over alleged bribery related to the renewable energy business is the most prominent example — creates headline risk and could complicate access to specific pools of international capital, even if the specific subsidiary (AESL) is not directly implicated9.

Comparative Lens

How does AESL stack up against the listed alternatives? टाटा पावर Tata Power is the most comparable Indian peer — also integrated across generation, transmission, and distribution, also building out renewables and EV charging, but with a less aggressive bid-then-build cadence and a larger legacy generation exposure. टोरेंट पावर Torrent Power is a smaller integrated utility with strong distribution in Gujarat. पावर ग्रिड Power Grid Corporation of India, the state-owned giant, is the dominant transmission player but is structurally slower and politically constrained. इंडीग्रिड IndiGrid, the listed transmission InvIT, offers pure regulated transmission exposure with high payout ratios but limited growth.

Within that competitive set, AESL is the highest-growth, highest-optionality, highest-leverage name. It is also the most controversial. Reasonable investors will weight those tradeoffs differently.

KPIs That Matter

For investors tracking the company over time, three numbers carry most of the signal. First, net asset commissioning per year — measured in circuit kilometres for transmission and in deployed meters for the smart-meter business. This is the growth pipeline turning into cash-flowing assets. Second, AT&C losses in the Mumbai distribution licence area — the operating-quality indicator for the distribution business, where every percentage point of loss reduction compounds into bottom-line cash. Third, net-debt-to-EBITDA — the leverage health check, which determines how much further the platform can scale before it has to slow down or recycle capital.

Three numbers. Track those, and the story largely tells itself.

Myth vs. Reality

A few consensus narratives deserve fact-checking. Myth one: AESL is just a transmission company. Reality: by FY24, the integrated business mix — transmission, distribution, smart metering, and emerging cooling/services lines — meant that "transmission-only" was already a partial description of revenue, and a smaller part of forward growth. Myth two: the Hindenburg report broke the operating story. Reality: stock-price impact was severe and lasting, but underlying operating metrics — line commissioning, meter deployment, AT&C losses — continued to trend in the right direction through 2023 and 2024. Myth three: the smart-meter business is just a low-margin manufacturing play. Reality: under the TOTEX AMISP model, this is a long-tenor recurring services business, not a hardware sale.

VIII. Epilogue: The Energy Solution Rebrand

On July 14, 2023, in a routine BSE filing that most market participants barely noticed, Adani Transmission Limited became Adani Energy Solutions Limited[^1]. A change of name is, on the surface, a cosmetic act. Investor relations decks get reprinted, stationery gets refreshed, the ticker symbol updates. But corporate rebrands at this scale almost always carry a strategic message. This one carried two.

The first message was about identity. "Transmission" describes a single product — wires that move electrons. "Energy Solutions" describes a portfolio of customer outcomes — reliable supply, efficient consumption, lower emissions, smarter demand management. The rebrand was a public acknowledgement, by management, that the company had outgrown the transmission-only label. The Mumbai distribution acquisition had happened six years earlier. The smart-metering business had ramped. The district-cooling effort was in early commercial development. The narrative had finally caught up with the balance sheet.

The second message was about future ambition. Calling yourself "Adani Energy Solutions" gives you permission to sell, eventually, almost any energy-adjacent product line — rooftop solar, battery storage, EV charging, electricity retail, demand-side management — without further rebranding. It is a strategic option-pricing exercise: a name as a wide-mouthed funnel rather than a narrow product label. Compare and contrast with global utilities that have made similar transitions. National Grid's "Energy Solutions" arm. Iberdrola's diversified Iberdrola Solutions retail platform. Enel's X division. The pattern, across geographies, is consistent: incumbent regulated utilities, sensing that the energy transition is reshaping the customer relationship, rebrand around solutions and use the rebrand to enter adjacencies.

What is genuinely interesting is how this connects back to the founding "incubation" thesis. The Adani Group is, in many ways, replaying its own playbook at a sub-company level. Just as Adani Enterprises incubated transmission for a decade before spinning it out, Adani Energy Solutions is now incubating smart metering, district cooling, and parallel distribution within its own legal entity. In ten or fifteen years, it would not be surprising if AESL's smart-metering arm became a standalone listed entity — a "Snowflake of Indian power" — while the transmission core continued to compound as a regulated utility.

The deeper question, for any long-term investor, is whether the energy transition rewards platform companies or asset companies. The case for asset companies — pure-play transmission, pure-play solar generation, pure-play storage — is that focus produces operational excellence and the lowest cost of capital for each silo. The case for platform companies is that the customer relationship, the data, and the cross-sell opportunities accrue to whoever sits across multiple energy verticals. Adani Energy Solutions is making the second bet.

The original analyst who closed the Adani Transmission tab in 2015 was not wrong about utilities being boring. He was wrong about which company was a utility. The wires, the substations, the Mumbai distribution circle, the smart meters — they are all the same physical category, but the operating model and growth profile are a different species entirely. What the अदाणी समूह Adani Group has built, quietly and at enormous scale, is an infrastructure platform with a SaaS layer on top, sitting on the cornered resource of Indian rights-of-way, run by professional managers, financed by global institutional capital, and rebranded for a decade of energy-transition demand growth.

Whether that platform compounds in the way the bulls hope, or gets capped by the regulator the way the bears fear, will define one of the most interesting chapters of Indian capitalism over the coming years. Either way, it is no longer a story you can ignore by clicking "close tab."

References

References

-

Adani Group: How The World's 3rd Richest Man Is Pulling The Largest Con In Corporate History — Hindenburg Research, 2023-01-24 ↩↩

-

Qatar Investment Authority to buy 25% stake in Adani Electricity Mumbai — Reuters, 2019-12-11 ↩

-

Profile of Anil Sardana, MD of AESL — Bloomberg Executive Profile ↩

-

Adani Energy Solutions completes Rs 8,660 crore QIP — Business Standard, 2024-08-01 ↩↩

-

Quarterly Earnings Transcripts — Adani Energy Solutions Investor Relations ↩

-

U.S. Indictment of Gautam Adani and Executives — Reuters, 2024-11-20 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube