Acutaas Chemicals: From Surat's Lab to India's Pharma Intermediate Powerhouse

I. Introduction & Episode Roadmap

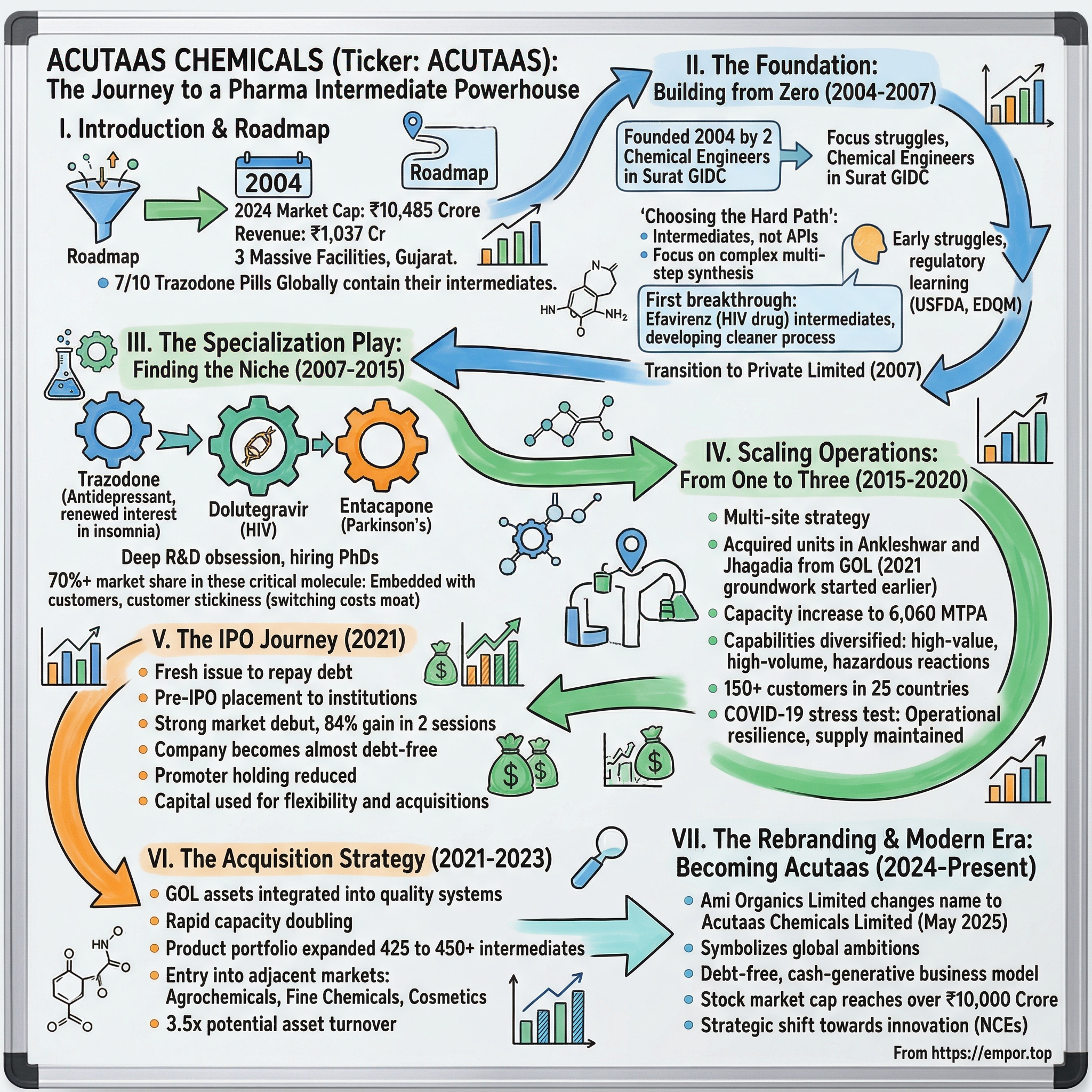

Picture this: In a nondescript industrial estate in Surat, 2004, two chemical engineers are standing in an empty plot, visualizing not just a factory but a future where their molecules would fight cancer, HIV, and Parkinson's disease across the globe. They had no idea that twenty years later, their company would command a ₹10,485 crore market capitalization, or that seven out of ten Trazodone antidepressant pills manufactured worldwide would contain their intermediates.

This is the story of Acutaas Chemicals—formerly Ami Organics—a company that most investors have never heard of, yet whose molecules are probably in your medicine cabinet right now. With ₹1,037 crore in revenue and operations spanning three massive facilities across Gujarat, Acutaas has quietly become one of India's most important pharmaceutical intermediate manufacturers. The central question we're exploring today: How did a small company from Surat, founded with modest capital in an industrial estate, transform into a critical supplier whose molecules are embedded in the global pharmaceutical supply chain? This isn't just another chemical company story—it's about finding the exact intersection where complex chemistry meets desperate medical need, where Indian manufacturing prowess meets global regulatory standards, and where a 70% market share in critical drug intermediates becomes possible.

Here's what we'll uncover: the founding vision that started in 2004, the strategic bets on specific therapeutic areas, the timing of their public market debut, and their recent transformation into Acutaas Chemicals in 2025. We'll examine how they built a portfolio of 520+ products across 23 therapeutic areas, why they chose to be the arms dealer rather than the warrior in the pharma wars, and what their debt-free balance sheet means for the future. The company manufactures different types of Advanced Pharmaceutical Intermediates and materials for agrochemicals and fine chemicals, having developed and commercialized over 450 pharma intermediates for APIs and NCEs across 17 therapeutic areas.

Let's dive in.

II. The Foundation Story: Building from Zero (2004-2007)

The year is 2004. The Gujarat Industrial Development Corporation (GIDC) estate in Sachin, Surat, is a maze of chemical plants, warehouses, and the unmistakable acrid smell of industrial chemistry. Two men—Nareshkumar Ramjibhai Patel and Chetankumar Chhaganlal Vaghasia—are walking through an empty plot, not seeing barren land but visualizing reactors, distillation columns, and a future where their molecules would save lives.

The company was founded in 2004 and is based in Surat, India. But what the official records don't tell you is the audacity of their vision. While everyone else in Surat was chasing the textile boom or jumping into diamond processing, Patel and Vaghasia chose the hardest path: pharmaceutical intermediates. Not the glamorous finished drugs that patients recognize, but the critical building blocks—the unsung heroes of modern medicine.

The Gujarat chemical cluster wasn't chosen by accident. This was India's chemical heartland, where pipelines carrying industrial gases crisscrossed overhead, where effluent treatment plants were shared infrastructure, where chemical engineers fresh from MS University Baroda could be hired without relocating families. The ecosystem mattered as much as the economics. In Sachin GIDC, you could source hydrochloric acid at 2 AM, find a fabricator to fix a reactor at midnight, and have access to a testing lab within a 10-kilometer radius.

Ami Organics, initially founded as a partnership firm in Surat, India in 2004, converted to a private limited company in 2007. This transformation from partnership to private limited wasn't just paperwork—it signaled ambition. The founders were building for scale, not survival.

The early struggles were brutal. Picture this: You're a nobody from Surat calling Cipla or Dr. Reddy's, trying to convince them to source critical intermediates from you instead of established suppliers. Every pharmaceutical company's quality team wants to audit your facility, your processes, your documentation. One failed batch, one delayed delivery, one quality deviation—and you're out. Forever.

The founders made a crucial early decision that would define everything: focus on intermediates, not APIs (Active Pharmaceutical Ingredients). Why? APIs meant competing with Chinese giants who had scale, with established Indian players who had regulatory approvals, with multinational corporations who had unlimited capital. But intermediates—especially complex ones requiring 10-15 step syntheses, handling hazardous reactions, managing controlled substances—that was where a small, nimble, technically excellent company could win.

They started with anti-retroviral intermediates. The timing was perfect. The global AIDS crisis had created massive demand for affordable HIV medications. The Indian government's decision to ignore product patents (while respecting process patents) until 2005 meant Indian companies could reverse-engineer these molecules. And someone needed to supply the intermediates.

Their first major breakthrough came with Efavirenz intermediates—a crucial HIV drug. They developed a process that was not just cheaper but cleaner, with fewer hazardous waste products. The pharma intermediates have application in certain high-growth therapeutic areas, including anti-retroviral, anti-inflammatory, anti-psychotic, anti-cancer, anti-Parkinson, anti-depressant and anti-coagulant. This wasn't just business; it was purpose. Every kilogram of intermediate they produced would eventually help HIV patients in Africa, Asia, and Latin America access life-saving medicines.

The regulatory learning curve was steep. FDA Form 483 observations, European EDQM requirements, Japanese PMDA standards—each market had its own quality expectations, documentation requirements, audit processes. The founders spent more time in conference rooms explaining deviations than in the plant making products. But each audit, each observation, each corrective action made them stronger.

By 2007, they had survived the crucial first three years—the period when 90% of chemical startups fail. They had paying customers, repeat orders, and most importantly, a reputation for reliability. The partnership structure had served its purpose, but to grow further, they needed more capital, better governance, and the ability to attract institutional funding. The transformation to a private limited company wasn't just about legal structure—it was about ambition.

III. The Specialization Play: Finding the Niche (2007-2015)

The conference room at their Sachin facility in 2008 witnessed a debate that would define Acutaas's future. On the whiteboard: a list of 50 potential molecules. The question: Which battles to fight? The temptation was to chase every opportunity—after all, when you're small and hungry, every order looks appetizing. But Patel and Vaghasia made a counterintuitive decision: go deep, not wide.

They identified three molecules where they could dominate: Trazodone (antidepressant), Dolutegravir (HIV), and Entacapone (Parkinson's). Not random choices—each represented a different challenge in synthetic chemistry, each served a growing therapeutic area, and most importantly, each had specific technical barriers that would keep competitors out.

The company manufactures pharma intermediates for certain APIs, including dolutegravir, trazodone, entacapone, nintedanib and rivaroxaban. Take Trazodone—an antidepressant that was seeing renewed interest for off-label use in insomnia. The key intermediate required a tricky chlorination reaction that most manufacturers struggled to control. Too much heat and you get unwanted isomers. Too little and the reaction doesn't complete. Ami Organics spent eighteen months perfecting the process, installing specialized equipment for temperature control, developing in-house analytical methods to detect impurities at parts-per-million levels.

The result? By 2012, seven out of every ten Trazodone pills manufactured globally contained their intermediate. This wasn't market share—it was market dominance.

The R&D obsession during this period was remarkable. While competitors were content with "good enough" processes, Ami Organics kept pushing. They hired PhD chemists from NCL Pune, collaborated with professors at ICT Mumbai, sent their staff for training at European equipment manufacturers. The company has developed and commercialized over 450 pharma intermediates for APIs and NCEs across 17 therapeutic areas.

The development process for each molecule followed a pattern that became their playbook: First, reverse-engineer the synthetic route from patents and literature. Second, identify the pain points—which step has the lowest yield, which intermediate is hardest to purify, which reaction is most hazardous. Third, develop alternative routes that address these pain points. Fourth, file process patents for the improvements. Fifth, scale up gradually—gram scale to kilogram to pilot plant to commercial.

But the real innovation wasn't just in chemistry—it was in customer engagement. They embedded their technical teams with customers' R&D departments. When Mylan was developing a generic version of a blockbuster drug, Ami Organics's chemists were in Mylan's labs, understanding their requirements, their constraints, their timeline. This wasn't vendor management—it was partnership.

The regulatory dance intensified during this period. Each customer audit brought new requirements. Divi's Laboratories wanted them to implement a particular quality system. A European customer required them to register under REACH regulations. An American innovator company needed them to file a Drug Master File with the FDA. Each requirement meant investments—in people, systems, infrastructure. But each compliance certificate was also a moat.

By 2013, they had a problem every business dreams of: too much demand. The Sachin facility was running three shifts, reactors were booked months in advance, and they were turning away orders. The decision to expand wasn't easy—chemical plants are capital intensive, take 18-24 months to commission, and require upfront investment with uncertain returns.

The customer stickiness model was proving its worth. Ami Organics manufactures specialty chemicals with varied end usage, focused on development and manufacturing of advanced pharmaceutical intermediates for regulated and generic APIs and New Chemical Entities (NCE). Once a customer validated their intermediate in a drug formulation, filed it with regulators, and got approval, switching to another supplier meant repeating the entire regulatory process. The switching costs weren't just financial—they were regulatory, time-based, and risk-based. By 2015, Ami Organics had become a case study in specialized manufacturing excellence. They commanded 70%+ market share in Trazodone, Dolutegravir, and Entacapone intermediates—a dominance rarely seen in the fragmented chemical industry.

IV. Scaling Operations: From One Plant to Three (2015-2020)

The boardroom discussion in late 2015 was heated. The Sachin facility was bursting at the seams—running at over 90% capacity, with customers on waiting lists. The decision before them: incremental expansion at the existing site or a bold multi-location strategy. They chose bold.

The numbers were daunting. Chemical plants aren't like software companies where you can scale with servers. A new facility meant ₹100+ crores in capital expenditure, 18-24 months of construction, environmental clearances, safety audits, and the risk that customer demand might shift by the time the plant was operational.

But what sealed the decision was a visit from a major European pharmaceutical company. The procurement head was blunt: "We love your quality, your pricing is competitive, but you're a single-point failure in our supply chain. One fire, one accident, one regulatory issue at Sachin, and our entire production stops." Supply chain resilience wasn't just nice to have—it was mandatory for big contracts.

The expansion strategy was surgical. Instead of building greenfield facilities, they looked for distressed assets. The global pharmaceutical industry was consolidating, and many small chemical manufacturers were struggling with tighter environmental regulations and rising compliance costs. This created opportunities.

It acquired two units namely, the Ankleshwar and Jhagadia units from Gujarat Organics Limited (GOL) in 2021. But the groundwork for these acquisitions started years earlier. The company had been evaluating multiple facilities, understanding their equipment, assessing their compliance status, and most importantly, determining how quickly they could be integrated into Ami Organics's quality systems.

The expansion from 2,460 MT to 6,060 MTPA capacity wasn't just about volume—it was about capability diversification. Each facility was designed with specific chemistry in mind. Sachin focused on high-value, low-volume intermediates requiring precise temperature control. Ankleshwar handled larger volume products with simpler chemistry. Jhagadia was equipped for hazardous reactions that required special containment.

This period also saw the China+1 phenomenon accelerate. The world was slowly waking up to its over-dependence on Chinese chemical manufacturers. Environmental crackdowns in China were causing sudden supply disruptions. Geopolitical tensions were rising. And then came 2020—COVID-19 turned supply chain diversification from a nice-to-have strategy to an existential necessity.

The Company supplies its products to more than 150 customers directly in India and to approximately 25 countries overseas. But behind this number was a carefully orchestrated customer acquisition and retention strategy. The company maintained dedicated technical service teams for key accounts. When a customer faced a quality issue, Ami Organics's chemists would fly out within 24 hours. When a customer needed to accelerate a product launch, Ami Organics would run special campaigns, working round the clock.

The customer stickiness numbers tell the story: 50 customers had been with them for over 5 years, 13 for over 10 years. In an industry where switching suppliers is common, this retention was extraordinary. The secret? Once Ami Organics's intermediate was validated in a customer's drug formulation and filed with regulators, changing suppliers meant months of revalidation, new regulatory filings, and risk of production delays.

Manufacturing excellence during this period went beyond just capacity. Ami Organics Ltd. is a diligently managed pharmaceutical company built with flexible cGMP compliant production space and R&D laboratories that are fully licensed as per Indian Factory Act. They implemented Toyota Production System principles—unusual for a chemical company. Batch cycle times were reduced by 30%. Solvent recovery systems were installed, reducing raw material costs and environmental impact. Digital batch records replaced paper, enabling real-time tracking and faster investigations of deviations.

The pandemic year of 2020 was their stress test. While competitors struggled with lockdowns and labor shortages, Ami Organics's three-facility strategy proved its worth. They could shift production between sites, maintain social distancing by spreading operations, and ensure continuous supply to customers manufacturing critical COVID-19 treatments. Revenue grew even as the world shut down—validation of their operational resilience.

V. The IPO Journey & Public Market Debut (2021)

September 1, 2021. The equity capital markets were frothy, specialty chemical stocks were trading at astronomical valuations, and every broker had the same thesis: "China+1 will drive a multi-decade boom for Indian chemical companies." Into this environment, Ami Organics launched its IPO.

The ₹570 crore IPO consisted of ₹370 crore OFS by 19 individuals (worth ₹327 crore) and by promoter (₹43 crore), with a ₹200 crore fresh issue to repay ₹140 crore debt (making them debt free post IPO) and ₹90 crore for working capital. The structure was telling—this wasn't about raising growth capital but about providing exits to early investors and cleaning up the balance sheet.

₹100 crore had already been raised in pre-IPO in August at ₹603 per share. The pre-IPO placement to institutional investors was strategic—it provided price discovery and created anchor demand for the public issue. The investors included mutual funds and alternative investment funds who had done deep due diligence, providing confidence to retail investors.

The company had issued shares at ₹610 apiece after a strong response to its IPO. The pricing wasn't aggressive by 2021 standards—at 26x trailing earnings, it was reasonable compared to peers trading at 40-50x. But the real story was in the details.

The use of proceeds revealed management's thinking. Seventy percent of the fresh issue was earmarked for debt repayment. In an era when most companies were leveraging up to fund growth, Ami Organics was going the opposite direction. Why? Because debt in the chemical industry is dangerous—one accident, one environmental violation, one major customer loss, and suddenly debt service becomes impossible. A clean balance sheet meant flexibility to pursue acquisitions, ability to bid for large contracts without balance sheet constraints, and most importantly, peace of mind during downturns.

Shares of Ami Organics were up 20 per cent at Rs 1,121 on the BSE in intra-day trade after making a strong market debut, gaining a solid 84 per cent in just two trading sessions from its issue price of Rs 610 per share. The market's enthusiasm wasn't just about the company—it was about the sector, the theme, the narrative. Every chemical company IPO in 2021 was getting similar response.

Promoter holding reduced from 47% to 41% post IPO. This was significant—the promoters were diluting but maintaining control, signaling confidence in the long-term story while also recognizing the need for institutional participation.

The post-IPO performance validated the market's faith. Within months, the company was using its new financial strength to pursue strategic opportunities, culminating in the Gujarat Organics acquisition that would transform their capacity and capabilities.

VI. The Acquisition Strategy: Gujarat Organics & Expansion (2021-2023)

March 2021—six months before the IPO—Ami Organics made a move that would double their capacity overnight. Ami Organics Limited agreed to acquire Specialty Chemicals Business Unit in Ankleshwar of Gujarat Organics Ltd. for INR 230 million on March 4, 2021, completing the acquisition on March 31, 2021. This was just the beginning.

Ami Organics agreed to acquire Specialty Chemicals Business Unit in Jhagadia of Gujarat Organics Ltd. for approximately INR 700 million on March 13, 2021, completing the acquisition on March 31, 2021. Combined, these acquisitions added 3,600 MT of capacity for less than ₹100 crore—a fraction of what greenfield facilities would cost.

But the real value wasn't in the assets—it was in the timing and integration. Gujarat Organics was a distressed seller, struggling with working capital issues and unable to invest in compliance upgrades. For them, the facilities were liabilities. For Ami Organics, with its strong balance sheet and operational expertise, they were opportunities.

On 31.3.21, company acquired 3,360 MT specialty chemicals capacity for just Rs. 93 cr, increasing its installed capacity to 6,060 MT from FY22 onwards. With a 3.5x potential asset turnover ratio, FY22 revenue could more than double YoY.

The integration was methodical. First, implement Ami Organics's quality systems—no production until cGMP compliance was achieved. Second, evaluate the existing product portfolio—keep products that fit the strategy, discontinue commoditized ones. Third, cross-sell to existing customers—suddenly, Ami Organics could offer not just pharmaceutical intermediates but also specialty chemicals for cosmetics, polymers, and agrochemicals.

Owing to the acquisition, the company has further diversified and strengthened its chemical speciality portfolio. The product portfolio expanded from 425 to 450+ intermediates, but more importantly, they now had entry into adjacent markets without losing focus on their core pharmaceutical business.

The acquisition also brought unexpected benefits. Gujarat Organics had relationships with agrochemical companies that Ami Organics had never accessed. Some equipment was specialized for chemistries that Ami Organics had avoided due to capital constraints. The Jhagadia facility had 15,830 square meters of additional land—room for future expansion without new environmental clearances.

The financial engineering was elegant. The acquisition was partly funded via Rs. 65 cr debt (balance Rs. 28 cr internal accruals), which was aimed to be repaid from fresh issue proceeds. By using bridge financing before the IPO and repaying immediately after, they avoided dilution while securing the assets before competition arose.

Revenue mix post-acquisition told the integration story: 88.4% from pharma intermediates (the core business protected), 4.8% from agrochemicals (new market entry), and 6.7% from other specialty chemicals (optionality for future). This wasn't diversification for its own sake—it was calculated expansion into adjacent markets where the same capabilities could create value.

VII. The Rebranding & Modern Era: Becoming Acutaas (2024-Present)

April 16, 2025, the Board of Directors approved the change in the name of the company from Ami Organics Limited to Acutaas Chemicals Limited. To outsiders, it might seem like corporate vanity—another rebranding exercise. But for insiders, it represented something deeper: the transformation from a Surat-based intermediate manufacturer to a global specialty chemicals player.

The name "Acutaas" itself was carefully chosen—suggesting accuracy, acuity, and excellence. It was easier to pronounce globally, didn't carry regional associations, and signaled a fresh chapter. Ami Organics Limited was formerly known as Ami Organics Limited and changed its name to Acutaas Chemicals Limited in May 2025. The company was founded in 2004 and is based in Surat, India.

The timing wasn't coincidental. The stock's market cap had reached ₹10,485 crore (up 98.4% in 1 year). The company had achieved what few chemical companies manage—transitioning from debt-heavy manufacturing to a debt-free, cash-generative business model. Company is almost debt free.

The rebranding coincided with strategic shifts. The company was no longer content being an intermediate supplier—they were moving closer to the innovation end of the pharmaceutical value chain. Collaborations with innovator companies on New Chemical Entities (NCEs) meant they were now involved in drug development, not just manufacturing.

The portfolio expansion into cosmetics, polymers, and personal care wasn't random diversification—it was following their customers. Many pharmaceutical companies also had consumer health divisions. The same quality standards, regulatory rigor, and technical capabilities that made Ami Organics successful in pharma intermediates were directly applicable to these adjacent markets.

Current performance metrics validated the strategy. Sales rose 37.13% to Rs 308.48 crore in the quarter ended March 2025 as against Rs 224.96 crore during the previous quarter ended March 2024. For the full year, net profit rose 271.08% to Rs 158.71 crore in the year ended March 2025 as against Rs 42.77 crore during the previous year ended March 2024. Sales rose 40.34% to Rs 1006.88 crore in the year ended March 2025 as against Rs 717.47 crore during the previous year ended March 2024.

But the real transformation was in margins and return metrics. Net margins had expanded from 9.77% to 15.85%—exceptional in an industry where 10% is considered good. This wasn't just operating leverage; it was the result of product mix optimization, operational excellence, and the bargaining power that comes with market dominance in key molecules.

The debt-free status opened new strategic options. While competitors were constrained by leverage, Acutaas could pursue acquisitions, invest in R&D, or return capital to shareholders—all without asking anyone's permission. In the chemical industry, where opportunities and crises arrive without warning, this flexibility was invaluable.

VIII. Business Model Deep Dive & Unit Economics

To understand Acutaas, you need to understand the specialty chemicals value chain—and why their position in it is so valuable. Picture drug manufacturing as a pyramid. At the top are the finished formulations—the pills patients take. Below that are the Active Pharmaceutical Ingredients (APIs)—the actual drug molecules. And at the foundation are intermediates—the building blocks used to construct APIs.

Most investors focus on the top of the pyramid—branded pharmaceuticals with 80% gross margins. But that's also where the risk lies: patent cliffs, regulatory failures, competitive dynamics. Acutaas chose the foundation—less glamorous but more stable, less margin but more predictable.

Why intermediates over APIs? Consider the economics: An API manufacturer needs to maintain finished product inventory, manage formulation complexity, and navigate end-market regulations. An intermediate manufacturer sells to the API manufacturer—one step removed from the complexity. When an API goes off-patent and prices crash, the API manufacturer suffers. The intermediate manufacturer simply supplies the new generic manufacturers entering the market.

The unit economics are compelling. A typical pharmaceutical intermediate might sell for ₹500-5,000 per kilogram, with gross margins of 40-50%. But the real money isn't in the margin—it's in the volume predictability. Once validated in a customer's process, an intermediate generates revenue for 7-10 years, the typical lifecycle of a drug. Compare that to specialty chemicals for electronics or textiles, where products become obsolete in 2-3 years.

EBITDA stood at Rs 85 crore, registering growth of 96.8% compared with Rs 43.2 crore in Q4 FY24. EBITDA margin was at 27.5% in Q4 FY25 as against 19.2% in Q4 FY24. This margin expansion tells a story. As volumes increase, fixed costs get absorbed. But more importantly, as customer relationships deepen, pricing power increases. When you're supplying 70% of global requirements for a critical intermediate, customers don't negotiate on price—they negotiate on supply security.

The R&D investment thesis is often misunderstood. Acutaas isn't trying to discover new drugs—they're trying to discover better ways to make existing molecules. A 10% yield improvement in a critical reaction can mean millions in additional profit. A new synthetic route that avoids a controlled substance can open up new markets. This isn't moonshot R&D—it's incremental innovation with immediate commercial application.

The working capital dynamics are favorable compared to peers. Raw materials are typically commodity chemicals—readily available, multiple suppliers, standard payment terms. Finished products are specialty intermediates—limited suppliers, customer dependency, favorable payment terms. This creates a natural working capital advantage.

Customer concentration, often seen as a risk, is actually a moat. The Company supplies its products to more than 150 customers directly in India and to approximately 25 countries overseas. But dig deeper—the top 10 customers likely account for 60-70% of revenue. This concentration creates deep relationships, dedicated service, and switching costs that protect the business.

Export versus domestic dynamics add another layer. In Q4 FY25, export stood at 74% and domestic business was at 26%. Exports mean dealing with developed market regulations, higher quality requirements, but also better pricing and payment terms. Domestic sales provide volume stability and relationships that can be leveraged for new products.

IX. Playbook: Lessons in Chemical Entrepreneurship

The Acutaas story offers a masterclass in building a specialty chemical business. Here are the key lessons:

Finding and Dominating Niches: Don't try to be everything to everyone. Acutaas chose specific molecules—Trazodone, Dolutegravir, Entacapone—and became the best in the world at making their intermediates. Market share above 50% creates pricing power, customer dependency, and competitive moats that are nearly impossible to breach.

Building Trust in a Trust-Deficit Industry: The chemical industry has a reputation problem—environmental disasters, quality scandals, unreliable supply. Acutaas built trust through consistency. Never miss a delivery. Never compromise on quality. When problems arise (and they always do), communicate immediately and fix them transparently.

The Power of Customer Stickiness: In B2B chemicals, switching costs are your best friend. Once your intermediate is validated, specified, and filed with regulators, you're embedded in your customer's supply chain for years. Focus on increasing these switching costs through technical service, regulatory support, and supply chain integration.

Timing Market Shifts: Acutaas rode three waves perfectly—the generic pharmaceutical boom (2004-2010), the quality upgrade cycle (2010-2015), and the China+1 diversification (2015-present). They didn't create these waves, but they positioned themselves to benefit from each.

Capital Allocation in Capital-Intensive Manufacturing: The temptation in chemicals is to keep building capacity. Acutaas showed discipline—expand only when utilization exceeds 70%, acquire distressed assets rather than building greenfield, and maintain a strong balance sheet for opportunistic moves.

Managing Regulatory Complexity as Competitive Advantage: Every regulatory requirement—FDA audits, EU REACH registration, environmental compliance—is a barrier to entry. Acutaas turned compliance from a cost center to a moat. Smaller competitors couldn't afford the investment; larger competitors didn't have the focus.

The Acquisition Playbook: Buy distressed assets, not successful companies. The Gujarat Organics facilities were struggling—that's why they were affordable. With operational excellence and financial strength, Acutaas could turn these liabilities into assets. This is financial engineering meets operational excellence.

X. Bear vs. Bull Case & Competitive Analysis

The Bull Case:

The structural drivers for Acutaas are compelling. The global pharmaceutical intermediate market is growing at 6-7% annually, driven by aging populations and increasing healthcare access. But the real opportunity is market share shift. Chinese manufacturers, who historically dominated, are facing environmental restrictions, rising costs, and geopolitical headwinds. This isn't a temporary phenomenon—it's a structural shift that could play out over a decade.

With the company trading at 8.01 times book value and generating strong cash flows, the valuation remains reasonable compared to peers trading at 10-15x book. The company is operating at only 63% capacity utilization—meaning revenue can grow 50% without major capital investment.

Customer relationships are deepening, not just broadening. The 50+ customers who've been with them for five years aren't just buying products—they're embedded partners. High switching costs mean these relationships are essentially annuities, generating predictable cash flows for years.

The debt-free balance sheet is a weapon in a capital-intensive industry. While competitors struggle with leverage, Acutaas can pursue acquisitions at attractive valuations, invest in new technologies, or simply return capital to shareholders. In a downturn, they're buyers, not sellers.

Recent performance validates the strategy. Looking ahead to FY26, we anticipate robust growth across all business segments, driving our confidence in achieving 25% revenue growth. This isn't hope—it's based on contracted orders, capacity expansion, and new product launches.

The Bear Case:

Promoter holding has decreased over last quarter by 3.30%—never a positive signal. While some dilution is natural post-IPO, continued selling suggests insiders might be less optimistic about future prospects.

Product concentration remains a critical risk. With 70% market share in key molecules, Acutaas is vulnerable to technological disruption. If someone develops a new synthetic route for Trazodone or if the drug itself becomes obsolete, significant revenue could evaporate quickly.

Chinese competition isn't disappearing—it's evolving. Chinese manufacturers are moving up the value chain, improving quality, and finding ways around environmental restrictions. The China+1 tailwind could reverse if geopolitical tensions ease or if Chinese manufacturers successfully upgrade.

Regulatory risks lurk everywhere. A single FDA warning letter, an environmental violation, or a quality failure could shut down a facility for months. In an industry where customers have zero tolerance for supply disruption, one mistake could lead to permanent customer loss.

Commodity chemical price volatility can squeeze margins. While Acutaas has pricing power in finished products, they're price takers in raw materials. A spike in solvent prices or key raw materials could compress margins before price increases can be passed through.

Competitive Positioning:

Against peers like Divi's Laboratories (market cap: ₹89,000 crore), Laurus Labs (₹29,000 crore), and Neuland Laboratories (₹17,000 crore), Acutaas is a mid-sized player. But size isn't everything in specialty chemicals.

Divi's has scale but also complexity—they're in APIs, intermediates, and custom synthesis. This breadth creates opportunities but also diffuses focus. Laurus is transitioning from ARV APIs to oncology and custom synthesis—a risky strategic shift. Neuland is focused on APIs, putting them closer to market risk.

Acutaas's focused intermediate strategy, dominant market shares in specific molecules, and debt-free balance sheet give them advantages that offset their smaller size. They're not trying to win everywhere—just in the specific battles they've chosen.

XI. Future Outlook & Strategic Options

The biosimilar intermediate opportunity is massive and largely untapped. As biological drugs worth $100+ billion lose patent protection over the next decade, biosimilar manufacturers will need specialized intermediates. Acutaas's expertise in complex chemistry positions them well, but they'll need to invest in new capabilities—fermentation, purification, and analytical technologies specific to biologics.

CDMO (Contract Development and Manufacturing Organization) expansion is the natural evolution. Currently, Acutaas primarily manufactures established intermediates. But their R&D capabilities and regulatory expertise could support custom synthesis for innovator companies. This would mean higher margins, deeper customer relationships, but also higher risk and longer development cycles.

Forward integration into APIs remains tempting but dangerous. The margin structure is attractive, but it would mean competing with customers—a strategic minefield. The smarter move might be selective integration, choosing one or two APIs where they have overwhelming intermediate dominance.

Geographic expansion, particularly in the US, could accelerate growth. While they export to America, local manufacturing would provide faster response times, eliminate shipping costs, and qualify them for certain government contracts. But US manufacturing means higher costs, different regulatory requirements, and cultural challenges.

Green chemistry initiatives aren't just about compliance—they're about competitive advantage. Customers increasingly demand sustainable supply chains. Acutaas's solvent recovery systems and waste reduction programs are a start, but there's opportunity to become the sustainability leader in pharmaceutical intermediates.

AI and machine learning applications in process optimization could transform the business. Predicting yield improvements, optimizing reaction conditions, and accelerating development timelines—these aren't futuristic concepts but near-term opportunities. The company that figures out how to apply AI to chemical process development will have a massive advantage.

XII. Recent News & Developments

The latest quarterly results tell a story of momentum. Net profit of Acutaas Chemicals rose 217.49% to Rs 44.29 crore in the quarter ended June 2025 as against Rs 13.95 crore during the previous quarter ended June 2024. Sales rose 17.30% to Rs 207.24 crore in the quarter ended June 2025 as against Rs 176.67 crore during the previous quarter ended June 2024.

The stock market has recognized this performance. Over the past year, it has increased by 82.93%, significantly surpassing the Sensex's growth. The company is attending investor conferences in Mumbai in August 2025, signaling increased institutional engagement post-rebranding.

A significant development is the subsidiary restructuring. Intimation Of Change Of Name Of Wholly Owned Subsidiary Company From Ami Organics Electrolytes Private Limited To Acutaas Chemicals Electrolytes Private Limited. This suggests expansion into battery chemicals—a strategic adjacency that leverages their chemical expertise while tapping into the electric vehicle megatrend.

Management commentary remains bullish. The company has raised revenue guidance, expecting 25% growth in FY26 based on visibility from contracted orders and new product launches. With promoter holding at 32.66%, down from higher levels but still significant, insiders maintain meaningful skin in the game.

XIII. Links & Resources

For investors seeking deeper understanding of Acutaas Chemicals and the specialty chemicals sector, several resources provide valuable context:

Company Resources: - Annual Reports and Investor Presentations (available on BSE/NSE websites) - Quarterly Earnings Call Transcripts - DRHP (Draft Red Herring Prospectus) from the 2021 IPO

Industry Analysis: - CRISIL Reports on Indian Specialty Chemicals Sector - India Chemical Council Annual Reports - McKinsey's "India Chemical Industry: Unleashing the Next Wave of Growth"

Regulatory Frameworks: - FDA Drug Master File Guidelines - EU REACH Compliance Documentation - Indian Factory Act and Environmental Regulations

Books on Chemical Industry & Pharmaceutical Manufacturing: - "The Alchemy of Air" by Thomas Hager (understanding industrial chemistry) - "Pharma: A History of the Pharmaceutical Industry" by Gerald Posner - "The $800 Million Pill" by Merrill Goozner (drug development economics)

Academic Papers: - "Supply Chain Resilience in the Pharmaceutical Industry" - Harvard Business Review - "China+1 Strategy: Implications for Indian Chemical Sector" - IIM Ahmedabad

Peer Company Analysis: - Divi's Laboratories Annual Reports - Laurus Labs Investor Presentations - Global specialty chemical comparisons (BASF, Clariant, Huntsman)

The Acutaas Chemicals story is far from over. From a partnership firm in Surat to a ₹10,000+ crore market cap specialty chemicals leader, the journey demonstrates that in the complex world of pharmaceutical manufacturing, sometimes the most valuable position isn't at the top of the pyramid but at its foundation. As global pharmaceutical supply chains continue evolving, as new diseases require new medicines, and as India solidifies its position as the pharmacy of the world, companies like Acutaas that combine technical excellence, operational discipline, and strategic focus will continue creating value—one molecule at a time.

The transformation from Ami Organics to Acutaas Chemicals isn't just a name change—it's a declaration of ambition. The next chapter will test whether they can maintain their dominance while expanding scope, whether they can stay focused while exploring adjacencies, and whether they can preserve their entrepreneurial culture while becoming an institution. For investors, customers, and competitors alike, Acutaas Chemicals remains a company worth watching closely.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube