ACME Solar: From Telecom Towers to India's Renewable Energy Revolution

I. Introduction & Cold Open

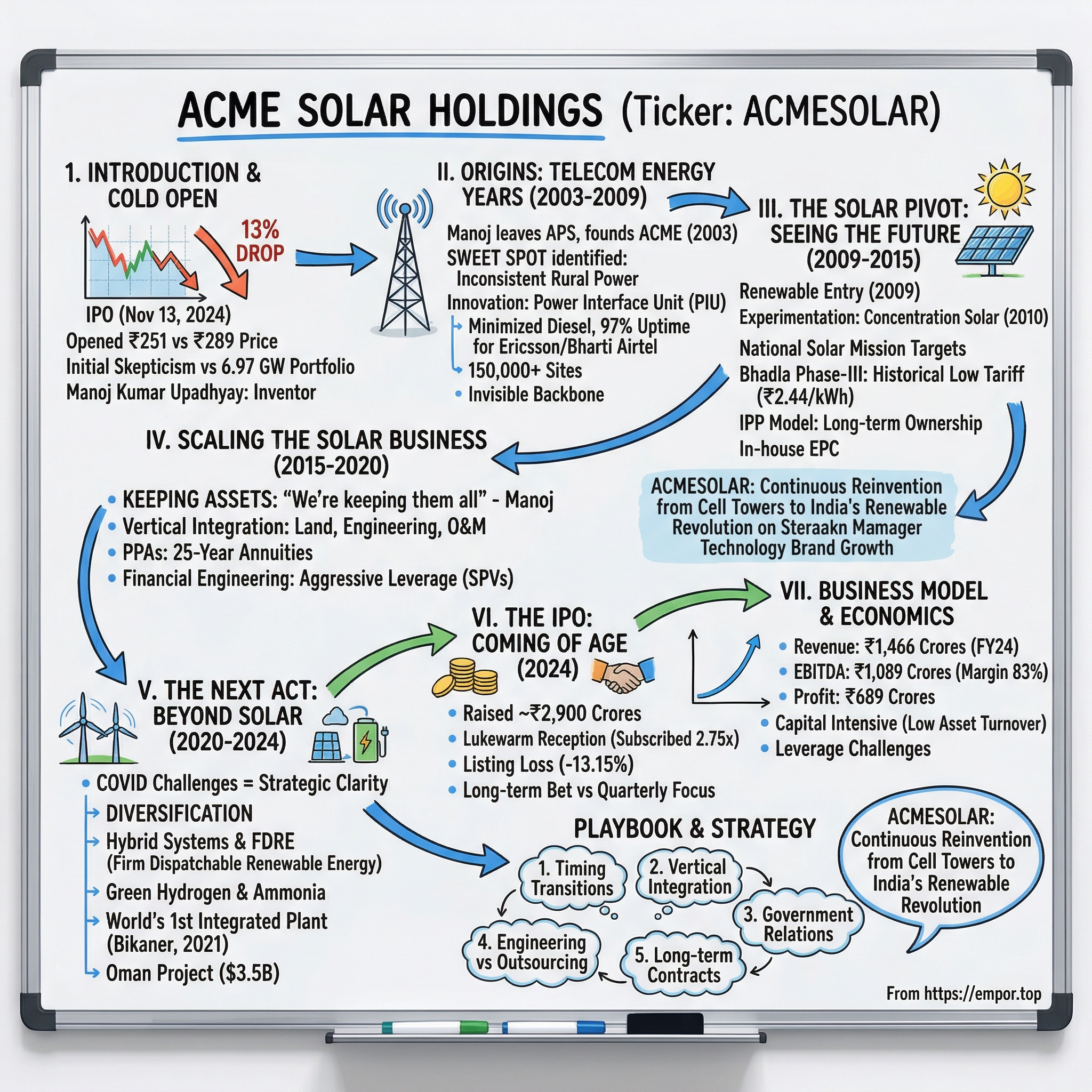

The Mumbai skyline glittered in the early morning haze of November 13, 2024, as trading screens across the financial district lit up with a new ticker symbol: ACMESOLAR. But instead of the typical first-day pop that accompanies major IPOs, something unusual happened. The stock, priced at ₹289 per share, opened at ₹251—a 13% drop that sent ripples through conference rooms from Nariman Point to Bengaluru's startup corridors.

This wasn't supposed to happen to one of India's renewable energy champions. Here was a company with 6.97 gigawatts of clean energy projects, backed by the legendary Manoj Kumar Upadhyay—the man who'd literally invented solutions that powered India's telecom revolution. The lukewarm reception seemed to defy logic in a country desperately racing toward 500 GW of renewable capacity by 2030.

But perhaps the market's initial skepticism tells us something deeper about ACME Solar's journey. This is, after all, a company that has reinvented itself completely—not once, but twice. From its origins as a scrappy telecom energy solutions provider in 2003 to becoming one of India's top 10 renewable energy players, ACME's story mirrors India's own infrastructure evolution.

Today, with a market capitalization hovering around ₹17,299 crores, ACME Solar stands as both a testament to entrepreneurial pivoting and a bellwether for India's energy transition. The company operates across solar, wind, hybrid systems, and something called FDRE—firm dispatchable renewable energy—a mouthful of a term that might just hold the key to solving renewable energy's biggest challenge: what happens when the sun doesn't shine and the wind doesn't blow?

Manoj Kumar Upadhyay didn't set out to build a renewable energy empire. In 2003, he was just an engineer with five patents to his name and a restless ambition that had already led him to walk away from a comfortable partnership. His decision to leave his stake in APS to his collaborators wasn't about money—it was about something more primal. "I wanted to shake up the world," he would later tell reporters, with the matter-of-fact tone of someone stating the weather.

What followed was a masterclass in reading market transitions, building engineering capabilities from scratch, and navigating the treacherous waters of Indian infrastructure development. It's a journey that took ACME from solving Ericsson's telecom tower problems in rural Bihar to competing head-to-head with the Adani Group in utility-scale solar farms.

The IPO's tepid reception—subscribed just 2.75 times compared to the frothy multiples typical of Indian offerings—raises fundamental questions. Is this a case of market myopia missing a transformational story? Or are investors right to be cautious about a capital-intensive business in a sector notorious for execution risks and policy uncertainties?

To understand ACME Solar today, we need to travel back two decades to when mobile phones were still a luxury and India's telecom infrastructure was expanding at a pace that would make Silicon Valley dizzy. Because sometimes, the best renewable energy stories begin not with solar panels or wind turbines, but with the unglamorous problem of keeping cell towers running in monsoon-soaked villages.

II. Origins: The Telecom Energy Years (2003-2009)

January 2003. The dotcom bust was still fresh in everyone's memory, India's GDP was barely crossing a trillion dollars, and Manoj Kumar Upadhyay was walking away from everything he'd built. His partners at APS must have thought he'd lost his mind. Here was a successful business, steady income, established relationships. But Manoj had that particular brand of restlessness that afflicts true entrepreneurs—the kind that makes comfortable success feel like slow suffocation.

"I was hugely ambitious and restless," he would later reflect, though "hugely" might be an understatement. Within weeks of leaving APS, he had incorporated ACME, named not after the cartoon company that supplied Wile E. Coyote, but as an acronym whose meaning he kept deliberately vague. What mattered wasn't the name but the mission: to solve real infrastructure problems that others ignored.

Three months. That's all it took for destiny to come knocking, though it arrived in the unglamorous form of a frustrated Ericsson engineer. The Swedish telecom giant was facing a crisis that threatened to derail India's mobile revolution. Their client, Bharti Airtel, was rapidly expanding into rural areas where the power grid was less reliable than monsoon predictions. Towers would go dark for hours, sometimes days. Diesel generators guzzled fuel and spewed smoke. Battery banks died premature deaths in the Indian heat.

The Ericsson engineer who approached Manoj had probably pitched this problem to a dozen companies. But something clicked when he explained it to the ACME founder. While others saw a technical challenge, Manoj saw a systemic issue that needed a fundamental rethink. Within weeks, he had sketched out what would become the Power Interface Unit—a deceptively simple device that would revolutionize how telecom towers managed energy. The genius of Manoj's innovation wasn't just technical—it was systemic. The Power Interface Unit minimized diesel usage, maximized utilization of mains power, and upped cell tower uptime from 80-90% to close to 97%. In an industry where every percentage point of uptime translated to millions in revenue, this was revolutionary.

"We did nearly 80% of Bharti Airtel's total roll-out from 2003-2009," Manoj would later recall, a statement that barely captures the frenetic pace of those years. Bharti grew from 12,000 sites in 2005 to 150,000 in just six years. The telecom industry was quite literally building a network the size of European countries every month, and ACME was at the heart of it.

But success bred more than just revenue—it bred patents. Manoj became the inventor of five patented product innovations and processes in telecom energy management. The Green Shelter, Phase Change Material, Free Cooling Units—each innovation tackled a specific pain point of running infrastructure in India's brutal climate. These weren't Silicon Valley-style software patents; they were hard-won solutions to physical problems that no one else had bothered to solve systematically.

S. Asokan, executive director of supply chain at Bharti Airtel, credits ACME for quickly identifying a "sweet spot," noting they "saw the opportunity and used it" by combining many power conditioning equipment available back then to create the PIU. This ability to see connections where others saw components would become ACME's defining trait.

The numbers were staggering. Within eight years, ACME's products were installed at more than 150,000 telecom sites across India, Sri Lanka, Bangladesh, and a clutch of African nations. The company had essentially become the invisible backbone of South Asia's mobile revolution, ensuring that calls connected even when the power grid didn't.

Yet even as revenues soared and installations multiplied, Manoj was already seeing the writing on the wall. The market was completely changing—there was little, if any new demand for telecom infrastructure in India. The boom couldn't last forever. By 2008, as the global financial crisis sent shockwaves through markets, Manoj was already plotting his next move.

The lesson from the telecom years wasn't just about riding a wave—it was about knowing when to paddle toward the next one. And in 2009, that next wave had a name: solar.

III. The Solar Pivot: Seeing the Future (2009-2015)

The year 2009 marked a curious inflection point in global energy markets. Solar panel prices were beginning their dramatic descent—a trajectory that would see costs fall by 90% over the next decade. India was grappling with chronic power deficits that left entire cities in darkness. And somewhere in an ACME boardroom, Manoj Kumar Upadhyay was drawing connections that seemed obvious only in hindsight.

ACME Solar entered the renewable energy sector in 2009, commissioning its first solar plant in 2012. But the real story begins earlier, with a characteristic Manoj move that confused competitors and thrilled engineers. In 2010, the company set up India's first concentrating solar power plant of 2.5 MW at Bikaner, Rajasthan—not photovoltaic panels like everyone else, but concentrated solar thermal technology. Why go thermal when everyone was racing toward photovoltaic? "You have to understand Manoj," a former executive would later explain. "He doesn't follow—he experiments. He wanted to understand every technology pathway before committing billions."

The timing of the formal consolidation in 2015—when ACME Solar Holdings was incorporated—wasn't random. It came after six years of patient experimentation, learning, and most importantly, watching costs plummet and government policies crystallize. The National Solar Mission had been launched in 2010 with an ambitious target of 20 GW by 2022. By 2015, Prime Minister Modi would revise that target to 100 GW, sending a clear signal that solar wasn't just policy priority—it was national strategy.

But the most dramatic moment came in May 2017, when ACME achieved something that made international headlines. At the 500 MW Bhadla Phase-III Solar Park auction, ACME quoted a tariff of Rs.2.44 (~$0.037)/kWh and won the bid to develop 200 MW solar—a historic low that shattered previous records and proved solar could compete head-to-head with coal on pure economics.

This wasn't just a number—it was a psychological barrier broken. Government officials pointed out this rate was lower than the average coal-based price and the grid parity price for solar to match with coal. The man who had once powered telecom towers in remote villages had just made renewable energy cheaper than fossil fuels in one of the world's most coal-dependent economies.

The strategic decisions during this period reveal a distinct philosophy. While competitors were content to be developers—build, flip, and move on—ACME chose the harder path of becoming an independent power producer (IPP). This meant owning and operating assets for their entire 25-year lifecycle, bearing both the risks and rewards of long-term ownership.

Building EPC capabilities in-house was another counterintuitive move. Most developers outsourced engineering, procurement, and construction to specialized firms. But Manoj remembered the telecom years—control your technology stack, and you control your destiny. By 2015, ACME had assembled teams that could handle everything from land acquisition to commissioning, creating a vertically integrated machine that would become crucial for rapid scaling.

The early wins validated the model. Projects in Gujarat, Rajasthan, and Andhra Pradesh came online with clockwork precision. Each success unlocked more financing, better terms, and bigger ambitions. Banks that had been skeptical of renewable energy started competing to fund ACME's projects.

Yet beneath the triumph, challenges lurked. Manoj identified two major challenges with the scale-up of solar power plants: "One is land acquisition because the data of most rural landholdings have not been updated in the revenue records for 80 years. The second is the availability of lenders."

These weren't problems you could solve with engineering prowess alone. They required patient navigation of India's labyrinthine bureaucracy, relationship building with hundreds of local officials, and creative financial structuring that could convince risk-averse banks to fund capital-intensive projects with 25-year payback periods.

By 2015, ACME had transformed from a telecom energy company dabbling in solar to a renewable energy powerhouse with a clear vision. The pivot was complete, but the real scaling was just beginning.

IV. Scaling the Solar Business (2015-2020)

The conference room at ACME's Gurugram headquarters hummed with tension in early 2016. Spread across the mahogany table were offers from international funds willing to pay premium valuations for ACME's operational solar assets. The sums were staggering—enough to make ACME's early investors wealthy beyond imagination. This was the moment most Indian renewable developers lived for: build, de-risk, flip to yield-hungry foreign capital, repeat.

Manoj killed the deal with four words: "We're keeping them all."

The decision to remain an asset owner rather than asset flipper would define ACME's trajectory for the next half-decade. While peers like ReNew Power and Azure Power were perfecting the art of recycling capital through asset sales, ACME was betting on something different—that owning and operating renewable assets through their entire lifecycle would create more value than any quick flip could generate.

The math was compelling if you had patience. A typical solar project with a 25-year Power Purchase Agreement (PPA) might generate internal rates of return (IRRs) of 14-16% for patient capital. But the first five years barely covered debt service. Years 6-15 generated decent cash flows. Years 16-25, with debt fully paid, were pure profit. By selling early, developers captured the construction premium but left the steady annuity income on the table.ACME's decision to maintain ownership meant finding creative ways to finance growth. The solution came through a sophisticated dance of project finance, corporate debt, and strategic partnerships. Each project was structured as a Special Purpose Vehicle (SPV), ring-fencing risks while allowing aggressive leverage at the project level—often 70-80% debt financing.

The geographic strategy was equally deliberate. Projects are distributed across 10 Indian states, chosen for their renewable energy potential. But this wasn't just about chasing the sun. Each state had different regulations, grid stability, land costs, and political dynamics. ACME built teams that could navigate Tamil Nadu's complex land acquisition as smoothly as Rajasthan's desert logistics.

Power Purchase Agreements became the bedrock of the business model. Long-term contracts, typically spanning 25 years, with government and private entities, ensure a stable cash flow and mitigate demand risk. These weren't just contracts—they were sovereign-backed annuities, as close to guaranteed revenue as you could get in infrastructure.

The integrated model that emerged by 2020 was formidable. ACME Solar manages all project phases in-house, from land acquisition, engineering, procurement and construction (EPC) to operations and maintenance (O&M). The company's in-house teams handle EPC and O&M functions, allowing them to control costs, monitor real-time performance, and minimize reliance on third-party contractors.

This vertical integration created a competitive moat. While competitors waited months for EPC contractors, ACME could mobilize teams within weeks. When module prices spiked, ACME's procurement relationships ensured supply. When grid issues arose, ACME's O&M teams were already on-site, not waiting for third-party service windows.

The financial engineering during this period was equally sophisticated. Between 2015 and 2020, ACME raised capital from development finance institutions, commercial banks, and bond markets. Each financing round came with better terms as the company's track record solidified. Interest rates dropped from double digits to high single digits. Tenure extended from 10 years to 18 years.

But the numbers tell only part of the story. The company has delivered a poor sales growth of -4.59% over past five years. Company has a low return on equity of 4.58% over last 3 years. These metrics, seemingly contradictory to a growth story, reveal the challenge of renewable energy economics—massive capital deployment for projects that take years to generate meaningful returns.

By 2020, ACME had built a machine—not just a collection of solar farms, but an integrated platform capable of developing, building, and operating renewable energy at scale. The foundation was set for the next transformation.

V. The Next Act: Beyond Solar (2020-2024)

The year 2020 brought unprecedented challenges. COVID-19 lockdowns halted construction sites. Supply chains from China—the source of 80% of solar modules—froze. Power demand collapsed as industries shut down. For a capital-intensive business with fixed costs and long-term contracts, this was the stress test from hell.

But crisis has a way of accelerating strategic clarity. As Manoj surveyed the landscape from lockdown, three trends became unmistakable: solar was becoming commoditized with wafer-thin margins, grid stability was emerging as the next bottleneck, and green hydrogen was transitioning from science fiction to policy priority.

The diversification strategy that emerged wasn't reactive—it was architectural. ACME Solar operates across multiple renewable technologies, such as solar, wind, and hybrid energy systems, along with FDRE, which provides firm, on-demand power through energy storage. Each technology addressed a specific market failure.

Wind projects, historically avoided by ACME, suddenly made sense when hybridized with solar. The complementarity was elegant—solar peaks during the day, wind often peaks at night. By co-locating both technologies and adding battery storage, ACME could offer something revolutionary: renewable energy that behaved like baseload power.

But the real innovation came with FDRE—Firm and Dispatchable Renewable Energy. The acronym sounds bureaucratic, but the implications were transformative. FDRE projects include storage components (battery or pumped hydro), allowing ACME to deliver power during peak demand periods, complementing intermittent energy sources.

Think about what this means. For decades, the knock against renewable energy was its intermittency—the sun doesn't always shine, the wind doesn't always blow. Grid operators had to maintain expensive gas turbines or coal plants as backup. FDRE changed the equation. By combining generation with storage, ACME could guarantee power delivery during specific hours, commanding premium tariffs that were 30-50% higher than vanilla solar. The green hydrogen ambitions represented ACME's boldest pivot yet. Expanding further, ACME is setting up a 1.2 GW solar PV module facility in Jaipur and leading Green Hydrogen and Green Ammonia initiatives. The company commissioned the world's first integrated green hydrogen and green ammonia plant in Bikaner, Rajasthan in 2021. The demonstration-sized facility is the first green hydrogen plant in India, powered by 5 MW of solar panels (with an expansion to 10 MW planned).

This wasn't just a pilot project—it was a statement of intent. Green ammonia, often dismissed as a niche chemical, suddenly emerged as the solution to one of energy's biggest challenges: how to transport and store hydrogen economically. Ammonia could be shipped globally using existing infrastructure, cracked back into hydrogen at the destination, or used directly as a fuel.

The Oman project took this vision to commercial scale. ACME Group signed a land agreement to set up a $3.5 billion green ammonia project at Special Economic Zone at the Port of Duqm in Oman. The long-term offtake agreement between Yara and Acme covers the supply of 100,000 tons per annum of renewable ammonia and possibly the world's first arm's length contract for renewable ammonia of this scale and tenure.

Backward integration became another strategic pillar. ACME Group is setting up a 1.2 GW solar PV module manufacturing facility under MKU Holdings Private Limited at Jaipur, Rajasthan, India. This wasn't just about capturing more value chain—it was about reducing dependence on Chinese suppliers who controlled 80% of global module production.

The financial turnaround during this period was dramatic. The company reported revenue of ₹1,466.27 crores in 2024 against ₹1,361.37 crore in 2023. The company reported profit of ₹689.26 crores in 2024 against loss of ₹3.17 crores in 2023. After years of heavy capital investment and negative returns, ACME was finally generating meaningful profits.

But perhaps the most significant development was the shift in investor perception. Renewable energy was no longer seen as subsidy-dependent charity but as a legitimate infrastructure asset class. Pension funds, sovereign wealth funds, and infrastructure investors began competing for renewable assets, driving down cost of capital and enabling even more aggressive expansion.

By 2024, ACME had transformed from a pure-play solar developer into an integrated renewable energy platform spanning generation, storage, manufacturing, and green molecules. The stage was set for the ultimate validation: public markets.

VI. The IPO: Coming of Age (2024)

The boardroom at ACME's Gurugram headquarters was unusually quiet on the morning of August 2024. After two decades of private ownership, the decision to go public wasn't just financial—it was existential. Manoj Kumar Upadhyay, now in his sixties, faced the classic founder's dilemma: maintain control and constrain growth, or dilute ownership to unleash the company's potential.

The numbers made the decision inevitable. The company to raise around ₹2,900 crores via IPO that comprises fresh issue of ₹2,395 crores and offer for sale up to 17,474,049 equity shares with face value of ₹2 each. With a pipeline of 6.97 GW requiring billions in capital, private funding sources were reaching their limits.

The use of proceeds revealed strategic priorities. Repayment/prepayment, in full or in part, of certain outstanding borrowings availed by its subsidiaries – INR 1,795 crore. This wasn't just debt reduction—it was balance sheet optimization, freeing up borrowing capacity for the next phase of growth.

But timing, as always in capital markets, proved tricky. The Indian IPO market in 2024 was experiencing fatigue. Retail investors, burned by recent listings, had become selective. Institutional investors questioned valuations across the renewable sector, worried about execution risks and policy uncertainty.

The roadshow revealed the challenge. In Mumbai, fund managers grilled the management on FDRE economics. In Singapore, sovereign funds questioned competition from Adani Green. In London, ESG investors wanted clarity on manufacturing plans. Each meeting exposed the complexity of explaining ACME's multi-faceted strategy to investors accustomed to simpler stories.

The pricing decision became contentious. Investment bankers pushed for ₹310-325 per share, arguing ACME deserved a premium for its integrated model and green hydrogen optionality. But Manoj, ever the pragmatist, insisted on ₹275-289, preferring a successful listing over maximum valuation.

ACME Solar Holdings IPO open date is November 6 and the IPO will close on November 8, 2024. The subscription data told a sobering story. The issue was overall subscribed merely 2.75 times - lukewarm reception. QIBs bid 2.42 times, retail 1.87 times—decent but not spectacular numbers that suggested careful evaluation rather than enthusiasm.

November 13, 2024, listing day, delivered a reality check. The IPO was offered at ₹289.00 per share and the ipo was listed at ₹251.00, showing initial market skepticism. It has delivered listing loss of -13.15%. The financial media had a field day—"ACME Solar Crashes on Debut," "Green Dreams Meet Market Reality."

Yet beneath the headlines, something interesting was happening. Post issue the promoter shareholding will come to 83.42 per cent, indicating possibility of further dilution. The Upadhyay family had retained overwhelming control, suggesting this IPO was just the first step in a longer journey.

The market dynamics revealed deeper concerns. Company has low interest coverage ratio. The company has delivered a poor sales growth of -4.59% over past five years. Company has a low return on equity of 4.58% over last 3 years. These metrics, while improving, highlighted the challenge of capital-intensive infrastructure businesses.

Broker recommendations were mixed but thoughtful. Bajaj Capital – Subscribe for long term, Jainam Broking – Subscribe for long term, SBI Securities – Subscribe for long term, Swastika Investmart – Subscribe for long term. The emphasis on "long term" was telling—this wasn't a quick flip opportunity but a bet on India's energy transition.

The most revealing moment came during the first earnings call post-IPO. An analyst asked about competition from Adani Green, which traded at 198x P/E versus ACME's 28x. Manoj's response was vintage: "We don't build for stock price. We build for 25-year PPAs. Let the market discover value over time."

This patient approach to value creation stood in stark contrast to the market's quarterly focus. But perhaps that was the point. ACME had survived the telecom bust, navigated the solar revolution, and was now positioning for the hydrogen economy. The IPO wasn't a destination but a milestone in a longer journey.

VII. Business Model & Unit Economics

Understanding ACME Solar's economics requires thinking like a infrastructure investor, not a tech analyst. Forget SaaS metrics or network effects—this is about IRRs, capacity factors, and levelized costs of energy.

The revenue model appears deceptively simple. Power Purchase Agreements (PPAs): Long-term contracts, typically spanning 25 years, with government and private entities, ensure a stable cash flow and mitigate demand risk. Most PPAs include fixed tariff rates, reducing revenue volatility. But beneath this simplicity lies sophisticated financial engineering.

Consider a typical 300 MW solar project. Capital expenditure: ₹1,200 crores. Debt-equity ratio: 75:25. Interest rate: 9%. PPA tariff: ₹2.50 per kWh. Capacity utilization factor: 24%. Annual generation: 630 million kWh. Annual revenue: ₹157.5 crores. Operating expenses: ₹15 crores. EBITDA: ₹142.5 crores. EBITDA margin: 90%.

Those margins would make software companies jealous, but there's a catch. Depreciation: ₹48 crores. Interest: ₹81 crores. Suddenly that ₹142.5 crore EBITDA becomes ₹13.5 crores in profit before tax. And this is year one—interest burden decreases over time while revenue remains constant, creating a J-curve profit profile.

Consolidated revenue from sale of electricity for Fiscal 2024 was INR 1,319 crore. EBITDA for FY2024 was INR 1,089 crore representing an EBITDA margin of 83%. After accounting for depreciation and interest, consolidated profit before tax (PBT) for the year 2024 was INR 161 crore.

The capital intensity is staggering. Total assets increasing from ₹10,887.62 crore in FY22 to ₹13,985.14 crore by June 2024, reflecting expansion in capacity and project investments. That's nearly ₹14,000 crores of assets generating ₹1,466 crores in revenue—an asset turnover ratio of just 0.10x. In comparison, manufacturing companies typically achieve 2-3x asset turnover.

But this is where the integrated model pays dividends. Total EPC operating profit was INR 288 Crore comprising EPC profit of INR 31 crore at ACME Solar standalone & INR 257 Crore at parent Acme Cleantech level. Historically, EPC work was done by both parent Acme Cleantech and the Company. However, going forward, entire EPC work and the corresponding EPC profit would be realized at Acme Solar Holdings Ltd as per internal restructuring.

The challenge of renewable energy economics in India goes beyond project-level returns. Grid integration costs, often ignored in headline tariffs, can add 20-30% to actual delivered cost. Transmission losses average 5-7%. Payment delays from state distribution companies average 180-300 days, creating massive working capital requirements.

Competition intensifies these challenges. Adani Green, with its 20 GW operational capacity and deep pockets, can bid aggressively for projects. ReNew Power's international listing provides access to cheaper capital. Azure Power's technology focus enables higher capacity factors. ACME must compete not just on price but on execution certainty.

The path to profitability requires scale, patience, and operational excellence. The diluted EPS has risen from ₹1.12 in March 2022 to ₹12.55 by March 2024, reflecting higher earnings per share for investors. The RoNW has increased from 3.25% to 26.95%, indicating an increase in the company's ability to generate returns on shareholder equity.

Operating leverage becomes meaningful only at scale. Fixed costs—corporate overhead, O&M teams, grid management—get spread across more megawatts. Financing costs decrease as track record improves. Procurement costs fall with volume. The first gigawatt loses money, the second breaks even, the third generates returns, and the fourth creates value.

The unit economics tell a story of transformation through scale and integration, but also highlight the fundamental challenge: generating acceptable returns in a capital-intensive, long-cycle business with sovereign counterparty risk. It's not for the faint-hearted or short-term focused.

VIII. Playbook: Lessons in Energy Transition

If ACME's journey offers a playbook, it's one written in sand rather than stone—constantly evolving with market conditions, technology curves, and policy shifts. But certain principles emerge with clarity.

Timing Market Transitions: The move from telecom to solar wasn't random—it captured the intersection of technology maturity, policy support, and market need. When ACME was just about three months old, someone from Ericsson approached him for help with the problem of irregular and fluctuating power supply to its towers. This pattern repeated with the shift to hybrid systems, FDRE, and now green hydrogen. Each transition began 2-3 years before the market recognized the opportunity, allowing ACME to build capabilities while competition was limited.

Vertical Integration as Competitive Advantage: The decision to build in-house EPC and O&M capabilities seemed capital-inefficient initially but proved crucial for rapid scaling. ACME Solar manages all project phases in-house, from land acquisition, engineering, procurement. The company's in-house teams handle EPC and O&M functions, allowing them to control costs, monitor real-time performance, and minimize reliance on third-party contractors. This integration enabled ACME to move from project conception to commissioning in 12-18 months versus the industry average of 24-30 months.

Managing Capital-Intensive Businesses in Emerging Markets: The playbook here involves sophisticated structuring—SPVs for risk isolation, non-recourse project finance to limit parent exposure, and strategic use of development finance institutions for cheaper, longer-tenure capital. But equally important is relationship capital—with banks, government officials, and local communities.

The Importance of Government Relations: In Indian infrastructure, policy is destiny. ACME's ability to navigate bureaucracy—from land acquisition in Rajasthan to environmental clearances in Tamil Nadu—became a core competency. This wasn't about corruption but about patient engagement, understanding regulatory intent, and aligning business models with policy objectives.

Building Engineering Capabilities vs Outsourcing: The telecom experience taught Manoj that controlling technology meant controlling destiny. He is the inventor of five patented product innovations and processes in this area. This philosophy extended to solar, where ACME developed proprietary mounting structures for high-wind areas, optimized module cleaning protocols for dusty environments, and created predictive maintenance algorithms that improved uptime by 2-3 percentage points.

Long-term Contracts vs Merchant Markets: While peers chased merchant power opportunities during price spikes, ACME stuck to long-term PPAs. This meant missing some upside but avoiding catastrophic downside. The 2020 power demand collapse vindicated this approach—ACME's revenues remained stable while merchant players saw 40-50% revenue drops.

The playbook reveals a deeper philosophy: infrastructure businesses win through patient execution, not brilliant strategy. Every competitor knows solar is growing, storage is important, and hydrogen represents the future. The difference lies in the unglamorous work of land acquisition, financing optimization, and operational excellence.

One executive summarized it perfectly: "Strategy meetings are monthly. Execution meetings are daily. That ratio tells you everything about how we think."

IX. Power & Strategy: The Renewable Energy Game

India's energy transition isn't just policy—it's thermodynamics meets geopolitics meets climate physics. The country's 500 GW renewable target by 2030 represents the largest infrastructure buildout in human history. To put this in perspective, it's equivalent to adding the entire U.S. power generation capacity in six years.

The math is staggering but necessary. India's per capita electricity consumption is one-third the global average. As 400 million people enter the middle class over the next decade, power demand will double. Meeting this demand with coal would make India the world's largest carbon emitter. Renewable energy isn't an option—it's an imperative.

But grid integration challenges threaten to derail this transition. Solar generation peaks at noon when demand is lowest. Wind is seasonal and unpredictable. The grid, designed for steady baseload power, struggles with intermittency. States like Karnataka and Tamil Nadu already curtail renewable generation 10-15% of the time because the grid can't absorb it.

FDRE projects include storage components (battery or pumped hydro), allowing ACME to deliver power during peak demand periods, complementing intermittent energy sources. This positions ACME perfectly for the next phase where storage-plus-generation becomes mandatory, not optional.

Competition from coal remains the elephant in the room. Despite global climate commitments, India added 6.7 GW of coal capacity in 2023. Coal plants provide 70% of electricity and employ 4 million people directly. The transition isn't just technical—it's political, social, and economic.

Technology curves favor renewables, but not uniformly. Solar costs have fallen 90% in a decade and may fall another 50% by 2030. Wind costs have declined 70% but are plateauing. Battery costs, the key to solving intermittency, have dropped 85% but need to fall another 70% to make storage truly competitive with gas peakers.

China's dominance in solar manufacturing creates strategic vulnerabilities. Chinese companies control 80% of polysilicon production, 95% of wafer production, and 75% of module assembly. India's production-linked incentive (PLI) scheme aims to build domestic capacity, but Chinese scale advantages are formidable. ACME's backward integration into manufacturing is as much about supply security as cost optimization.

The green hydrogen opportunity could reshape global energy trade. ACME is developing several green hydrogen and ammonia projects in India, Oman, and USA with an aim to have a cumulative portfolio of 10 mmtpa of green ammonia or equivalent hydrogen/derivatives by 2032. If renewable electricity is the new oil, green hydrogen is the new LNG—transportable, storable, and tradeable.

But execution challenges are immense. A typical green hydrogen project requires 3x the renewable capacity of the electrolyzer capacity. A 1 GW electrolyzer needs 3 GW of renewable generation, 5,000 acres of land, 50 million liters of water daily, and ₹25,000 crores of investment. The scale is unprecedented.

Policy navigation becomes crucial. The renewable energy sector depends on government support—through PPAs, transmission infrastructure, and payment guarantees. Policy changes can make or break projects. The 2024 reduction in customs duty on solar modules helped developers but hurt manufacturers. ACME, straddling both sides, must navigate carefully.

The strategic game is ultimately about positioning for multiple futures. If battery costs plummet, pure-play solar loses advantage—ACME's FDRE projects win. If green hydrogen takes off, early movers capture value—ACME's Bikaner plant provides learning curve advantages. If domestic manufacturing becomes mandatory, integrated players thrive—ACME's Jaipur facility becomes a moat.

X. Analysis & Investment Case

Bull Case:

India's renewable energy opportunity is generational. Power demand growing at 6-8% annually while renewable share must increase from 18% to 50% by 2030 creates a ₹10 trillion investment opportunity. ACME, with its 6.97 GW portfolio and proven execution, is positioned to capture disproportionate value.

The integrated capabilities create competitive advantages that compound over time. The company's in-house teams handle EPC and O&M functions, allowing them to control costs, monitor real-time performance, and minimize reliance on third-party contractors. Each project improves execution, reduces costs, and strengthens relationships—a virtuous cycle that's hard for new entrants to replicate.

FDRE and storage positioning addresses the grid's biggest pain point. As renewable penetration increases, grid stability services become more valuable than generation itself. ACME's early investment in storage and firm power positions it for premium tariffs and preferred dispatch.

Green hydrogen optionality provides massive upside. Acme built what is perhaps the world's first Green Ammonia plant in Bikaner, Rajasthan and in 2022 obtained the world's first certification for green ammonia from Oman project by TUV Rhineland. If green hydrogen achieves even 10% of optimistic projections, early movers will capture extraordinary value.

Promoter Holding: 83.4% demonstrates aligned interests. The Upadhyay family has skin in the game, thinking in decades not quarters. This patient capital approach enables long-term value creation over short-term optimization.

Valuation remains reasonable despite the sector's growth. Trading at 28x P/E versus Adani Green's 198x suggests significant rerating potential as execution delivers results.

Bear Case:

Company has low interest coverage ratio. In a rising rate environment, high leverage becomes a millstone. Each 100 basis point rate increase adds ₹100+ crores to interest costs, directly impacting profitability.

Execution risk on the large pipeline cannot be ignored. Converting 6.97 GW of portfolio into operational assets requires flawless execution across land acquisition, financing, construction, and commissioning. One major project failure could derail the entire growth story.

Policy and regulatory uncertainty remains existential. Changes in PPA terms, transmission charges, or renewable purchase obligations can destroy project economics overnight. The 2024 Andhra Pradesh government's attempt to renegotiate PPAs sent shockwaves through the sector.

Competition from well-funded players intensifies. Adani Green's 20 GW operational capacity and unlimited capital access, ReNew's international funding, and new entrants like JSW Energy create a race to the bottom on tariffs.

Technology risk and rapid cost deflation benefit future projects but hurt existing ones. A project commissioned at ₹4 crores/MW in 2020 competes with projects built at ₹2.5 crores/MW in 2024. This deflationary pressure compresses returns on older assets.

The company has delivered a poor sales growth of -4.59% over past five years. Company has a low return on equity of 4.58% over last 3 years. These backward-looking metrics raise questions about capital allocation and growth quality.

The investment case ultimately depends on time horizon and risk tolerance. For patient capital believing in India's energy transition, ACME offers leveraged exposure with execution capability. For those seeking near-term returns or concerned about leverage, the story requires more proof points.

XI. Recent News

ACME Solar has reported its third-quarter results for the financial year 2024-25 (Q3 FY 2024-25), ending on December 31, 2024. The company's profit after tax (PAT) rose by 152 per cent year-on-year, reaching Rs 1.12 billion, with a PAT margin of 28 per cent. The total revenue for the quarter stood at Rs 4.01 billion, reflecting a 9.9 per cent year-on-year increase and a 35.8 per cent quarter-on-quarter growth. The earnings before interest, tax, depreciation, and amortisation (EBITDA) grew by 15.7 per cent year-on-year to Rs 3.59 billion, achieving an EBITDA margin of 89.6 per cent.

Acme Solar Holdings Limited successfully completed the commissioning of four ISTS-connected projects in Jaisalmer, Rajasthan, totaling 1,023 MW / 1,483 MWp on December 18, 2024. This milestone makes it one of the largest single-location renewable energy projects in India this year. Once fully commissioned, the projects will deliver 1,200 MW / 1,752 MWp to the central grid, with the existing capacity of 1,023 MW already in operation. The remaining 177 MW is energized and under commissioning. With this, Acme Solar's total commissioned capacity will reach 2,540 MW / 3,578 MWp.

In terms of financing, ACME Solar has secured Rs 165 billion in debt for 1,700 MW of its under-construction portfolio. Additionally, refinancing efforts for the operational portfolio have resulted in Rs 55 billion in fresh debt at an average rate of 8.8 per cent per annum, reducing the cost of debt by 70 basis points and releasing Rs 6.5 billion in cash.

The Board of Directors declared an interim dividend of ₹0.20 per equity share for the period ended December 31, 2024. In April, ACME Solar Holdings secured a ₹2,491 crore long-term project finance facility with a tenure of 18–20 years to refinance existing debt and reduce financing costs for its 490 MW operational renewable energy projects across Andhra Pradesh, Rajasthan, and Punjab. The refinancing, sourced from SBI and REC at a reduced weighted average interest rate of 8.8%, has enhanced the company's credit profile and resulted in higher credit ratings for its Andhra Pradesh and Punjab entities under a co-obligor structure. This move supports the group's broader objective of achieving credit upgrades and lowering interest costs across all operational assets, which include projects with an operational track record of ~9 years in Andhra Pradesh (160 MW) and Punjab (30 MW), and ~3 years in Rajasthan (300 MW).

The stock performance post-IPO has been volatile. As of January 22, 2025, the stock is currently trading at ₹221.45, reflecting a 2.98% decrease from the previous closing price of ₹228.37. Following its Q3 FY25 earnings announcement, the company's stock hit a 10% upper circuit at ₹191.23 per share price on the National Stock Exchange (NSE).

Management changes continue as the company scales. ACME Solar appoints three VPs, COO and President of Renewable Energy resign effective August 2025.

XII. Links & Resources

Company Resources: - ACME Solar Holdings Official Website: www.acmesolar.in - ACME Group (Parent Company): www.acme.in - ACME Green Hydrogen & Chemicals: acme-ghc.in - Investor Relations and Press Releases: acmesolar.in/press-release

Regulatory Filings: - BSE Filings: BSE Limited (Stock Code: 544166) - NSE Filings: National Stock Exchange (Symbol: ACMESOLAR) - SEBI SCORES: scores.sebi.gov.in

Industry Reports: - India Brand Equity Foundation (IBEF) - Renewable Energy Reports - Central Electricity Authority (CEA) - Power Sector Reports - International Energy Agency (IEA) - India Energy Outlook - IRENA - India Renewable Energy Statistics

Key Competitors: - Adani Green Energy Limited - ReNew Power - Azure Power Global - Tata Power Renewable Energy - JSW Energy

Books on India's Energy Transition: - "The Climate Solution: India's Climate-Change Crisis and What We Can Do About It" by Mridula Ramesh - "Superpower: One Man's Quest to Transform American Energy" by Russell Gold - "The Grid: The Fraying Wires Between Americans and Our Energy Future" by Gretchen Bakke

Technical Resources: - Solar Power India Conference Proceedings - MNRE (Ministry of New and Renewable Energy) Policy Documents - SECI (Solar Energy Corporation of India) Tender Documents - Bridge to India Solar Reports

Financial Analysis: - Credit Rating Reports (CRISIL, ICRA) - Broker Research Reports (post-IPO coverage) - Industry Newsletters (Mercom India, PV Magazine India)

Green Hydrogen Resources: - Ammonia Energy Association: ammoniaenergy.org - International Hydrogen Council Reports - India Hydrogen Alliance Publications

Note: This analysis is based on publicly available information and does not constitute investment advice. Potential investors should conduct their own due diligence and consult with financial advisors before making investment decisions. The renewable energy sector carries significant execution, regulatory, and technology risks that should be carefully evaluated.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube