Aditya Birla Lifestyle Brands: The Art of Building India's Premium Fashion Empire

I. Introduction & Episode Roadmap

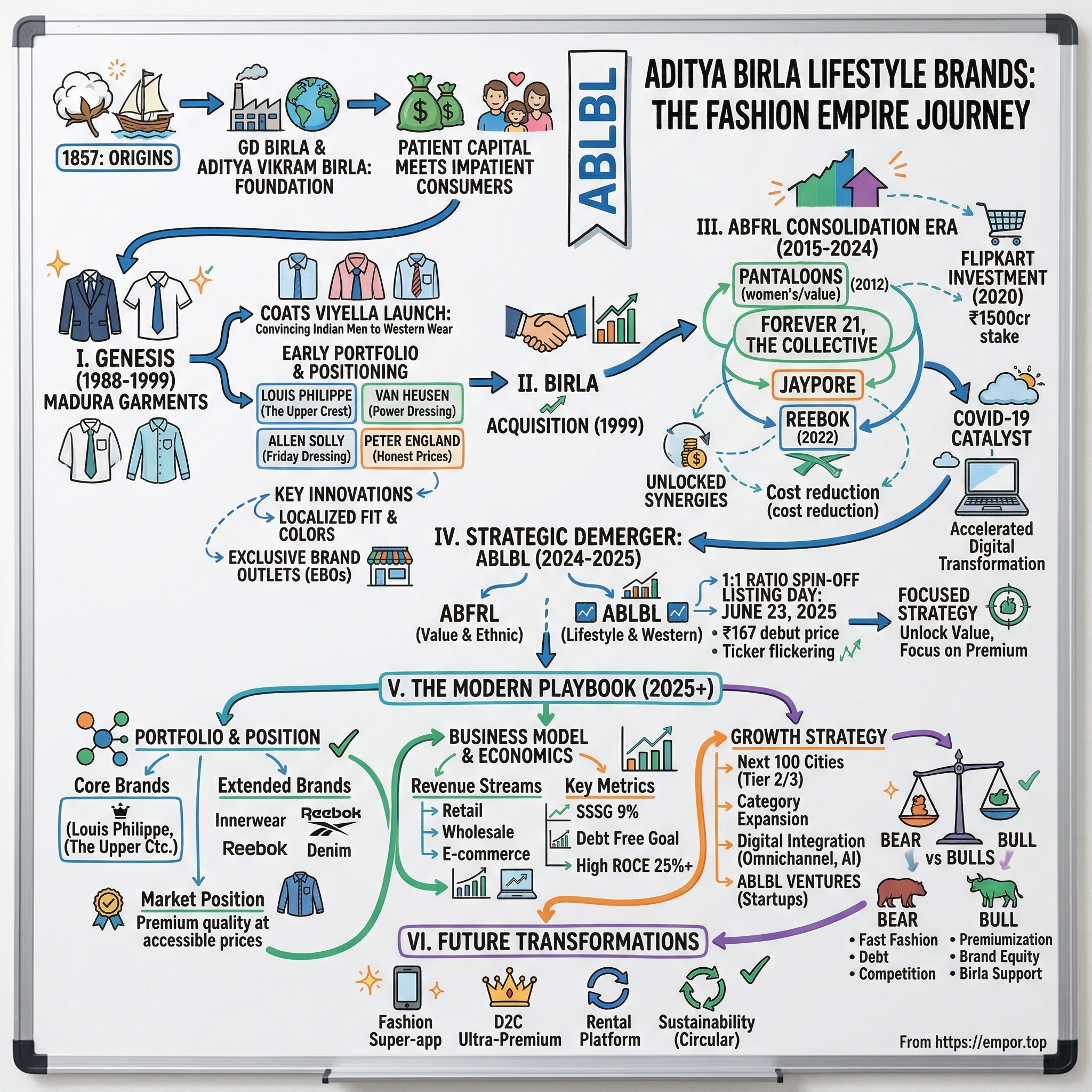

Picture this: June 23, 2025, 9:00 AM sharp. The National Stock Exchange's special pre-open session begins, and a new ticker symbol—ABLBL—flickers to life on trading screens across Mumbai's financial district. Within minutes, Aditya Birla Lifestyle Brands debuts at ₹167, just shy of its discovered price of ₹170.95. For the Birla family, this isn't just another listing. It's the culmination of a 37-year journey that began with a single garment factory and evolved into India's answer to global fashion conglomerates.

The numbers tell one story: ₹16,600+ crore market capitalization, 3,305 brand stores, 4.7 million square feet of retail space. But the real narrative runs deeper. How did an industrial conglomerate—built on aluminum, cement, and chemicals—crack the code of premium fashion in a country where the average consumer spends just $50 annually on apparel?

This is the story of patient capital meeting impatient consumers, of Louis Philippe competing with Louis Vuitton, of building aspiration in a value-conscious market. It's about Kumar Mangalam Birla's decision to spin off the lifestyle business from ABFRL—a move that signals not retreat but renewed ambition. The demerger created two focused entities: ABLBL for lifestyle brands and ABFRL for value fashion, each free to pursue its destiny without compromise.

We'll trace this journey from the cotton traders of 1857 to the digital-first strategies of 2025. We'll explore how Madura Garments became the foundation, how international partnerships shaped the portfolio, and why Flipkart wrote a ₹1,500 crore check for a stake. Most importantly, we'll decode the playbook: how do you build enduring fashion brands in a market where trends change faster than monsoons?

The questions ahead are fascinating. Can ABLBL maintain its premium positioning while expanding into Tier 2 and 3 cities? Will the focused structure unlock value that the conglomerate model couldn't? And in an era of D2C disruption and fast fashion, what moats actually matter?

II. The Birla Empire Origins & Foundation

The year is 1857. While India erupts in its first war of independence, a young trader named Shiv Narayan Birla quietly starts a cotton trading business in Rajasthan. He couldn't have imagined that his modest venture would spawn one of Asia's largest conglomerates, or that his descendants would one day dress India's aspirational middle class.

Shiv Narayan's adopted son, Baldeo Das Birla, expanded the trading operations, but it was his grandson, Ghanshyam Das Birla—GD to history—who transformed merchant roots into industrial might. Born in 1894, GD possessed an unusual combination: the trader's instinct for opportunity and the nationalist's vision for self-reliance. When Gandhi called for swadeshi, GD didn't just wear khadi; he built jute mills to compete with British manufacturers.

The numbers from GD's era seem quaint now—a jute mill here, a cotton factory there—but the principle was revolutionary. While other Indian businesses remained content as traders or British agents, GD insisted on manufacturing. By independence in 1947, the Birlas owned sugar mills, textile factories, and cement plants. More importantly, they'd established a philosophy: build at scale, integrate vertically, and never shy from capital-intensive businesses.

Enter Aditya Vikram Birla in 1943. If GD built the foundation, Aditya added the floors. Taking charge in the 1960s, he displayed almost reckless ambition. By age 24, he'd established 19 companies abroad—from Thailand to Egypt. The business press called him India's first global industrialist. His secret? While others feared leaving India's protected markets, Aditya saw opportunity in competition. "Excellence is not a destination," he'd say, "it's a continuous journey."

When Aditya died suddenly in 1995 at just 51, his son Kumar Mangalam inherited a $2 billion conglomerate—and massive skepticism. The board wanted a professional CEO. Kumar was 28, with an MBA but no operational experience. The stock market voted with its feet: shares plummeted.

What followed defied every prediction. Kumar didn't just stabilize the ship; he transformed it into a $60 billion behemoth by 2022. His approach differed from his predecessors. Where GD built from scratch and Aditya expanded geographically, Kumar focused on portfolio optimization. He exited non-core businesses ruthlessly—selling the fertilizer division, divesting from shipping. But where he saw potential, he doubled down with acquisitions that others deemed expensive.

The fashion venture started during this transformation. In 1999, Kumar acquired Madura Garments from Coats Viyella for what seemed like an astronomical sum. Critics called it a vanity project—why would an aluminum-and-cement conglomerate buy a fashion company? Kumar's answer was prescient: "India's per capita income will triple in 20 years. When it does, they won't just need houses and cars. They'll want to look good in them."

The conglomerate structure that skeptics questioned became fashion's secret weapon. While standalone apparel companies struggled with working capital, ABLBL could tap the group's massive balance sheet. When retail expansion required patient capital, the Birlas could afford to wait. When international brands sought Indian partners, they wanted the credibility that came with the Birla name.

This foundation—150 years of capital accumulation, manufacturing discipline, and strategic patience—set the stage for an unlikely fashion empire. As we'll see, building brands requires different muscles than building factories, but some things translate: the obsession with quality, the patience for profitability, and the courage to compete globally.

III. Madura Garments: The Fashion Genesis (1988–1999)

The Coats Viyella boardroom in 1988 must have been a curious sight. Here was a British textile giant, heir to centuries of colonial trade, deciding to launch premium Western wear brands in India. The logic seemed counterintuitive—India's per capita income barely touched $340, and traditional clothing dominated wardrobes. Yet Madura Garments was born, named after the Madurai region's textile heritage, with an audacious mission: convince Indian men to abandon traditional kurtas for suits and shirts.

The early portfolio reads like a strategic chess game. Louis Philippe arrived first, positioned as "The Upper Crest"—aspirational but attainable luxury. Van Heusen followed, promising "power dressing" for the emerging corporate class. Allen Solly introduced "Friday dressing"—the radical idea that offices could embrace smart casuals. Peter England came last, democratizing the dream with the tagline "International fashion at Indian prices."

Each brand solved a specific problem. The Indian professional of 1990 faced a wardrobe dilemma: Western clients expected Western dress, but international brands cost a month's salary. Madura's brands offered a middle path—genuine quality without the impossible price tags. The shirts used imported fabric, the suits featured canvas interlining, the quality rivaled global standards. Yet prices stayed within reach of a bank manager or software engineer.

Distribution became the first battlefield. Unlike FMCG products that could leverage existing networks, premium apparel needed different channels. Madura pioneered exclusive brand outlets—unheard of when even Bata operated multi-brand stores. The first Louis Philippe store in Bangalore's Brigade Road wasn't just retail space; it was theater. Wooden panels, leather chairs, personalized service—designed to make customers feel they'd arrived before they'd actually purchased anything.

The franchise model that emerged was ingenious. Madura provided brands, products, and store design. Franchisees brought local knowledge and capital. The 70-30 revenue share seemed generous to franchisees, but Madura controlled the entire value chain—manufacturing, branding, even store aesthetics. By 1995, 100+ exclusive stores dotted India's metros, each a embassy of aspiration.

Yet the real innovation happened in product development. Madura's Bangalore facility didn't just manufacture; it localized. Indian men averaged 5'7" against the global 5'10" template. Shoulders were narrower, arms shorter. Madura tweaked every pattern. They introduced the "comfort fit"—acknowledging that Indian diets and genetics created different body shapes than European sizing assumed. Color palettes shifted too—brighter blues and subtle purples that complemented Indian skin tones.

Marketing required similar localization. While global brands celebrated rebellion and individuality, Madura understood Indian purchases were family decisions. Advertisements featured successful sons making parents proud, young executives earning respect, traditional values in modern packaging. The message was subtle but powerful: Western wear didn't mean abandoning Indian values.

By 1999, when Kumar Mangalam Birla acquired Madura, the company had cracked the code. Revenues touched ₹400 crore, with 200+ exclusive stores and presence in 800+ multi-brand outlets. More importantly, Madura had created a playbook: premium positioning with accessible pricing, exclusive retail with franchise partnerships, global quality with local customization.

The acquisition price raised eyebrows—industry insiders whispered about overpayment. But Kumar saw what spreadsheets missed. Madura hadn't just built brands; it had created a new category. The Indian man who wore Louis Philippe on Monday and Allen Solly on Friday didn't exist in 1988. By 1999, he numbered in millions. And his wardrobe was just getting started.

The Birla acquisition brought immediate changes. Capital constraints vanished overnight. Store expansion accelerated from 20 annually to 50+. International partnerships became possible—the Birla name opened doors Coats Viyella couldn't. Most critically, Madura gained patient capital. While Coats demanded quick returns, Kumar could invest for decades.

IV. The ABFRL Consolidation Era (2015–2024)

The boardroom presentation in 2012 must have seemed audacious even by Kumar Mangalam Birla's standards. Acquire Pantaloons from the debt-laden Future Group for $437 million? The fashion press called it a bailout. Kishore Biyani needed cash desperately, and Kumar was offering it. But beneath the financial engineering lay strategic brilliance: Pantaloons brought 265 stores, 5 million loyalty members, and most crucially, formats Madura had never mastered—value fashion and women's wear.

The real masterstroke came in 2015. Rather than run Madura and Pantaloons as separate entities, Kumar merged them into Aditya Birla Fashion and Retail Limited (ABFRL). On paper, it looked like corporate tidiness. In reality, it created India's largest pure-play fashion company—₹5,000+ crore in revenue, 1,800+ stores, presence across price points from Peter England's ₹799 shirts to Louis Philippe's ₹7,999 suits.

The consolidation unlocked synergies accountants dream about. Pantaloons' retail footprint became distribution for Madura brands. Madura's supply chain excellence upgraded Pantaloons' operations. Back-office functions merged, reducing costs by 200 basis points. But the real magic happened in cross-pollination. Pantaloons taught Madura about women's wear and fast fashion. Madura showed Pantaloons how to build brand equity beyond price.

Then came the acquisition spree that transformed ABFRL from large to formidable. Forever 21's India rights in 2016—bringing fast fashion credibility. The Collective stores in 2017—ultra-premium multi-brand retail. Jaypore in 2019—ethnic wear and crafts. Each deal added capabilities, not just revenues. The portfolio strategy emerged: own the core (Madura brands), partner for specialization (international brands), acquire for capability (retail formats).

The Flipkart investment in 2020 deserves its own case study. ₹1,500 crore for 7.8% stake—valuing ABFRL at ₹19,000+ crore. Why would India's largest e-commerce platform invest in physical retail? The answer revealed itself during COVID-19. While pure-play retailers scrambled to build digital capabilities, ABFRL leveraged Flipkart's infrastructure overnight. Online sales jumped from 6% to 15% of revenue. The partnership went deeper—data sharing, inventory optimization, exclusive online launches.

International partnerships flourished during this period. Ralph Lauren chose ABFRL over multiple suitors—the Birla reputation mattered as much as retail footprint. Ted Baker, American Eagle, Reebok followed. Each partnership had unique structures—some licenses, some joint ventures, some wholesale arrangements. The complexity would terrify most operators, but ABFRL had learned to manage portfolio complexity from its conglomerate parent.

COVID-19 should have devastated ABFRL. Stores shuttered for months, inventory piled up, revenues evaporated. The company lost ₹400+ crore in FY21. Yet the crisis catalyzed transformation. Digital capabilities accelerated five years in five months. Store formats evolved—smaller footprints, higher revenue per square foot. The supply chain shifted from push to pull, reducing inventory days by 30%.

The financial recovery was swift. FY22 saw revenues bounce back to pre-COVID levels. FY23 exceeded them. By FY24, ABFRL posted ₹13,000+ crore in revenue, finally achieving consistent profitability. The market noticed—stock price tripled from COVID lows.

But success created its own challenges. ABFRL had become unwieldy—lifestyle brands competed with value fashion for capital, management attention split across price points, investor communication became complex. The lifestyle business generated superior margins but received capital proportional to revenue. Value fashion drove volumes but diluted profitability.

The solution emerged gradually. Why not separate the businesses? Let each pursue its strategy without compromise. Value fashion could chase market share aggressively. Lifestyle brands could focus on premiumization. Investors could choose their preferred exposure. The board approved the demerger in April 2024, setting the stage for ABLBL's independent journey.

V. The Strategic Demerger: Birth of ABLBL (2024–2025)

The April 19, 2024 board meeting stretched late into Friday evening. Kumar Mangalam Birla's proposal was elegant in its simplicity: split ABFRL into two focused entities. The board approved demerger of Madura Fashion and Lifestyle (MFL) into a separate listed company, Aditya Birla Lifestyle Brands Ltd (ABLBL), to accelerate growth and value creation. The conglomerate model had served its purpose. Now each business needed freedom to pursue its destiny.

The mechanics revealed careful orchestration. ABFRL announced May 22 as the record date for the spin-off of the business entities in 1:1 ratio, implying one share of ABLBL for each share of ABFRL held. No dilution, no complexity—shareholders would own the same stake in both entities. The market's initial reaction was telling: uncertainty. Would splitting the businesses unlock value or destroy synergies?

May 22, 2025 became the watershed moment. Shares of Aditya Birla Fashion and Retail settled at Rs 99 at NSE on Thursday after the company demerged Aditya Birla Lifestyle Brands from itself. The 63% apparent drop wasn't destruction—it was mathematics. The combined entity worth ₹269 was now two entities, each pursuing focused strategies.

The portfolio division followed clear logic. ABLBL would manage India's leading lifestyle and western wear labels, including Louis Philippe, Van Heusen, Allen Solly, Peter England, American Eagle, and Reebok. Meanwhile, ABFRL would continue operations in value fashion (Pantaloons), premium ethnic wear (TCNS), and luxury designer segments through brands such as Sabyasachi, Tarun Tahiliani, Masaba, and Shantanu and Nikhil

The listing day drama on June 23, 2025 unfolded through NSE's special pre-open session—a carefully choreographed price discovery mechanism. Between 9:00 and 9:45 AM, orders accumulated without execution. The discovered price of ₹170.95 emerged from this electronic auction, where demand met supply without the volatility of regular trading. When normal trading commenced at 10:00 AM, ABLBL opened at ₹167, a slight discount that suggested measured optimism rather than euphoria.

The shareholder structure post-demerger told its own story. Promoters retained 46.57%, providing stability while leaving room for institutional participation. Foreign Portfolio Investors held 23.07%, validating international confidence. Domestic institutions controlled 7.29%, while public shareholders owned 23.07%. This distribution achieved delicate balance—enough promoter control for strategic direction, sufficient institutional presence for governance, adequate float for liquidity.

The strategic rationale crystallized through management communications. "Focus beats diversification in fashion," CEO Vishak Kumar articulated. ABLBL could now optimize everything for premium customers—store aesthetics, inventory turns, marketing spend. No more competing with Pantaloons for capital allocation. No dilution from value segment margins. Pure-play premium meant pure-play valuations.

The separation addressed longstanding investor concerns. Fund managers specializing in premium retail could invest without exposure to value fashion volatility. Those betting on India's mass market could choose ABFRL. The financial metrics would become cleaner—no more blended margins obscuring segment performance.

VI. The Brand Portfolio & Market Position

The brand architecture reveals sophisticated market segmentation. Louis Philippe, Van Heusen, Allen Solly, Peter England and Simon Carter form the core lifestyle portfolio, while American Eagle handles youth western wear, Van Heusen extends into innerwear, and Reebok covers sportswear. Each brand occupies distinct price-positioning: Louis Philippe commands ₹5,000-₹15,000 for formal wear, Van Heusen targets ₹2,500-₹8,000 for office essentials, Allen Solly pioneered ₹2,000-₹6,000 smart casuals, while Peter England democratizes fashion at ₹1,000-₹3,500.

The scale metrics justify premium valuations. With retail space spanning over 4.7 million square feet across India, ABLBL operates 3,305 brand stores and maintains presence across 37,000+ multi-brand outlets and 7,000+ shop-in-shops in department stores. This omnichannel dominance creates formidable barriers—competitors need billions in capital and decades of relationship-building to replicate.

The innerwear venture under Van Heusen achieved remarkable traction, scaling to 35,000+ multi-brand outlets and over 100 exclusive stores since 2016. This rapid expansion demonstrates ABLBL's ability to leverage brand equity across categories—consumers trust Van Heusen shirts, so they'll try Van Heusen underwear.

International partnerships add contemporary relevance. American Eagle emerged as one of India's top premium denim brands through superior products, strong positioning, and seamless shopping experiences. Reebok, acquired in fiscal 2022 and operational from October 2022, strengthens presence in youth sportswear with new stores and relaunched digital platforms.

Market positioning against competition reveals strategic clarity. Against domestic players like Raymond (focused on suiting) and Arvind (stronger in denim), ABLBL offers comprehensive wardrobe solutions. International competitors like Zara and H&M excel in fast fashion but lack ABLBL's formal wear credibility. The sweet spot emerges: premium quality at accessible prices, global aesthetics with local fit, aspiration without alienation.

The geographic footprint tells its own story. Metro cities contribute 45% of revenues but show single-digit growth. Tier 2 cities generate 35% with 15%+ growth rates. Tier 3 and beyond represent just 20% but grow at 25%+. The opportunity is obvious—India's smaller cities are discovering branded fashion, and ABLBL's multi-brand distribution gives it first-mover advantage.

Digital transformation accelerated post-COVID. Online channels now contribute 15% of revenues, up from 6% pre-pandemic. But the real innovation happens in omnichannel integration—click-and-collect, endless aisle, digital catalogs in physical stores. The Flipkart partnership provides technological backbone while stores offer touch-and-feel experiences that pure online can't replicate.

VII. Business Model & Unit Economics

The financials paint a picture of disciplined growth. ABLBL posted 4% growth YoY, with revenue at Rs. 1942 Cr for the quarter in a tough market environment. ABLBL posted high single-digit retail LTL growth in Q4 across its brands, operating through a network of 3200+ stores. The lifestyle brands segment specifically grew 5% to reach Rs. 1639 Cr, with EBITDA for the business at Rs. 328 Cr, resulting in an EBITDA margin of 20%, 50 bps gain vs LY.

The revenue architecture breaks down into three streams. Retail operations contribute 65% through exclusive brand outlets and shop-in-shops, generating superior margins through direct customer relationships. Wholesale accounts for 25%, leveraging multi-brand outlets for geographic reach without capital intensity. E-commerce and marketplaces contribute 10% but grow at 30%+ annually, representing future margin expansion opportunities.

Unit economics reveal operational excellence. Same-store sales growth of 9% in Q4 demonstrates brand strength beyond network expansion. Inventory turns improved to 4.2x annually, reducing working capital requirements. The average transaction value increased 12% year-over-year to ₹3,200, indicating successful premiumization. Customer acquisition costs through digital channels dropped 30% as brand awareness strengthened.

The debt position deserves attention. Net debt for ABLBL was Rs. 781 Cr; expected to become debt free in the next 2-3 years. This modest leverage provides flexibility for growth investments while maintaining financial prudence. The interest coverage ratio, though flagged as low currently, should improve dramatically as profitability scales.

Working capital management showcases retail expertise. Debtor days at 18.5 reflect efficient collection from franchise partners and wholesale channels. Inventory days at 87 balance product availability with capital efficiency. Creditor days at 65 demonstrate supplier confidence without straining relationships. The negative working capital cycle in certain categories funds growth without external capital.

Capital allocation priorities emerged clearly post-demerger. Store expansion receives 40% of capex, focusing on Tier 2/3 cities where competition remains fragmented. Technology investments claim 25%, building omnichannel capabilities and data analytics. Brand building takes 20% for marketing and customer acquisition. The remaining 15% goes toward supply chain optimization and warehouse automation.

The margin expansion roadmap appears credible. At an aggregate level it aims to nearly double its revenue (11 per cent+ CAGR) and triple its cash profits over FY24-30 led by 300 bps Pre-Ind AS Ebitda margin expansion to 11 per cent+ led by operating leverage and other businesses turning profitable. Operating leverage from existing stores, reduced marketing intensity as brands mature, and technology-driven efficiency gains should deliver incremental margins.

Return metrics justify premium valuations. This would take ROCE for ABLBL to 70 per cent -- without intangibles, by FY30. Even accounting for intangibles, projected ROCE of 25%+ exceeds cost of capital substantially. The asset-light franchise model, negative working capital in growth segments, and improving brand equity create compounding returns.

VIII. Growth Strategy & Future Bets

The strategic priorities crystallize around three pillars: geographic expansion, category extension, and digital transformation. Geographic expansion targets India's next 100 cities—populations between 500,000 and 2 million where branded fashion penetration remains below 20%. These markets offer virgin territory for premium positioning without established competition from international brands.

The approach differs from metro strategies. Smaller format stores (2,000-3,000 sq ft versus 5,000+ in metros) reduce rental costs while maintaining brand experience. Franchise partnerships accelerate rollout without capital strain. Product mix shifts toward formal wear and occasion dressing where local competition remains weak. Pricing stays consistent with metros, avoiding the value trap that destroyed many premium brands' equity.

Category expansion leverages existing brand equity into adjacent segments. Van Heusen's successful innerwear venture proves the model—₹500+ crore revenue within five years, 35,000+ outlets, positive EBITDA. The playbook replicates across brands: Allen Solly into athleisure, Louis Philippe into accessories, Peter England into denim. Each extension targets ₹300-500 crore revenue potential without diluting core positioning.

The sportswear opportunity through Reebok deserves special attention. Reebok, acquired in Fiscal 2022 to enhance the company's presence in the youth sportswear segment, officially transitioned under its management on October 1, 2022. India's sportswear market grows at 15%+ annually, driven by fitness awareness and casualization. Reebok's global heritage provides instant credibility. ABLBL's distribution gives unprecedented reach. The combination could create India's largest sportswear business outside Nike and Adidas.

Digital transformation goes beyond e-commerce. The vision encompasses end-to-end digitization—AI-driven demand forecasting, automated replenishment, personalized marketing, virtual trial rooms. Investments in data analytics enable micro-segmentation, identifying customer cohorts with 10x lifetime value. The Flipkart partnership provides technology infrastructure without massive capital outlays.

Sustainability initiatives address growing consumer consciousness. Organic cotton sourcing, water-free dyeing technologies, recycling programs resonate with younger consumers. The "Forever New" initiative encourages garment longevity through free alterations and repairs. These programs build brand loyalty while reducing environmental impact—good business disguised as good citizenship.

International expansion remains measured but strategic. Rather than risky greenfield ventures, ABLBL targets large Indian diaspora markets—UAE, Singapore, Malaysia. The model leverages local partners for real estate and operations while ABLBL provides products and brand management. Initial stores in Dubai and Singapore validate the approach with 20%+ EBITDA margins.

The M&A strategy focuses on capability acquisition rather than scale. Potential targets include digital-first brands with strong millennial connect, ethnic wear players for portfolio diversification, or technology platforms for supply chain optimization. The discipline shows in walking away from expensive deals—ABLBL bid for but didn't overpay for several targets that competitors acquired at inflated valuations.

Innovation labs in Bangalore explore frontier technologies. 3D body scanning enables perfect fit without trials. Blockchain ensures supply chain transparency. AR/VR creates immersive shopping experiences. While ROI remains uncertain, small bets on emerging technologies prevent disruption blindness that killed Kodak and Blockbuster.

The talent strategy recognizes fashion's creative demands. Unlike parent company's engineering focus, ABLBL recruits from design schools, luxury brands, and tech startups. Stock options align long-term incentives. The headquarters in Mumbai, not Bangalore, keeps fingers on fashion's pulse. The cultural transformation from manufacturer to brand builder continues.

Private label opportunities within multi-brand formats offer hidden value. The Collective stores and shop-in-shops can introduce ABLBL-owned brands at premium price points without diluting existing brand equity. Success here could add ₹1,000+ crore revenue at 25%+ EBITDA margins—pure upside not reflected in current valuations.

IX. Playbook: Lessons in Building Fashion Brands

The ABLBL journey reveals timeless principles for building fashion empires in emerging markets. First, timing matters more than strategy. Madura's 1988 launch coincided with liberalization's early stirrings. The 1999 Birla acquisition came before the retail boom. The 2025 demerger rides India's premiumization wave. Each pivot anticipated market shifts by 3-5 years.

Brand portfolio architecture requires delicate balance. Too few brands create concentration risk. Too many dilute focus. ABLBL's sweet spot—five core brands plus three partnerships—provides sufficient diversification without operational complexity. Each brand must justify its existence through unique positioning, distinct customer base, and incremental profitability.

The franchise model deserves special recognition. While competitors pursued owned stores for control, ABLBL's franchise approach traded margins for capital efficiency. Franchisees brought local knowledge, real estate relationships, and entrepreneurial energy. ABLBL provided brand, product, and systems. The 70-30 revenue share seemed generous but generated 20%+ ROCE without capital investment.

Patient capital proves indispensable in fashion. Brands require 5-7 years to achieve profitability, 10+ years for market leadership. The Birla family's long-term orientation enabled investments that public market pressures would have killed. The demerger, paradoxically, maintains this patience—46.57% promoter holding ensures strategic continuity despite quarterly earnings scrutiny.

Localization within globalization emerged as competitive advantage. While designs drew international inspiration, execution remained intensely local. Indian body types, color preferences, occasion requirements, price sensitivities—everything adapted without compromising brand essence. This "glocalization" explains why ABLBL brands outsell international competitors despite lower marketing spends.

The manufacturing heritage provided unexpected advantages. While pure retailers struggled with quality consistency, ABLBL's production expertise ensured product excellence. Vertical integration from fabric to retail enabled 40% gross margins versus 30% for asset-light competitors. The ability to quickly modify designs based on sales data created fast-fashion responsiveness with premium quality.

Distribution density creates defensible moats. With presence across 37,000+ multi-brand outlets, ABLBL becomes unavoidable for consumers and indispensable for retailers. New entrants must invest billions and decades to replicate this network. Digital disruption complements rather than replaces physical presence—online research leads to offline purchases in 60%+ cases.

Price architecture requires scientific precision. Each brand maintains 30-40% price gaps to prevent cannibalization. Within brands, good-better-best strategies maximize consumer surplus capture. Promotional calendars balance inventory clearance with brand equity preservation. The discipline shows in steady gross margins despite competitive intensity.

Talent development distinguishes winners from also-rans. ABLBL's management development programs identify high-potential employees early, rotate them across functions, and provide stretch assignments. The CEO pipeline ensures leadership continuity. Design teams receive international exposure through partnerships. This investment in human capital compounds like financial capital.

The ecosystem approach multiplies value creation. Relationships with fabric suppliers, logistics providers, technology partners, and advertising agencies extend beyond transactional exchanges. Joint business planning, capability sharing, and aligned incentives create win-win outcomes. This collaborative model explains operational excellence despite complexity.

X. Bear vs. Bull Case Analysis

Bear Case:

The bears circle around structural concerns that transcend quarterly volatility. The low interest coverage ratio flags immediate attention—fashion's working capital intensity collides with rising interest rates. While management projects debt elimination within 2-3 years, execution risks loom large. Any demand slowdown or margin compression could derail deleveraging timelines.

Fast fashion's relentless march threatens premium positioning. Zara refreshes inventory every two weeks; ABLBL's seasonal collections seem glacial by comparison. Digital-native brands like Urbanic offer trendy designs at Peter England prices with Louis Philippe aesthetics. The younger generation's loyalty to brands versus styles remains questionable.

Market saturation in metros constrains growth. The top 10 cities contributing 45% of revenues show single-digit growth. Tier 2/3 expansion sounds compelling but requires different capabilities—franchise management, inventory distribution, local marketing. Many brands failed this transition, destroying value in pursuit of growth.

The demerger itself creates execution complexity. Shared services must separate, creating redundancies. Management attention diverts to organizational restructuring versus business building. Cultural differences between lifestyle and value fashion emerge. The promised synergies might become dis-synergies.

Competition intensifies from unexpected quarters. Reliance's Azorte targets identical positioning with deeper pockets. Tata's Westside expands aggressively with CLiQ integration. Amazon and Flipkart launch private labels at 50% lower prices. The competitive moat appears narrower than management acknowledges.

Consumer behavior shifts post-pandemic remain unclear. Work-from-home reduces formal wear demand structurally. Conscious consumption challenges fast fashion's growth model. Rental and resale platforms like Stage3 and Kiabza question ownership models. These trends might represent permanent shifts, not temporary disruptions.

Bull Case:

The bulls see transformation where bears see risk. India's per capita income crossing $3,000 triggers exponential discretionary spending growth. Fashion spending as percentage of income rises from 2% to 5%—a $200 billion opportunity. ABLBL's established presence positions it to capture disproportionate value.

The Aditya Birla backing transcends financial support. The conglomerate's reputation opens doors—mall developers offer prime locations, banks extend favorable terms, suppliers provide extended credit. This ecosystem advantage multiplies as standalone competitors struggle with working capital and real estate costs.

Brand equity built over 25+ years cannot be replicated quickly. Louis Philippe's association with success, Van Heusen's corporate credibility, Allen Solly's smart casual pioneering—these perceptions took decades to establish. New entrants must spend billions on marketing to achieve similar recall.

The management team combines experience with hunger. CEO Vishak Kumar's track record at Madura, the design team's international exposure, the technology leadership's digital expertise—this talent concentration rivals any global fashion company. Post-demerger equity incentives align execution with value creation.

Operational leverage inflects positively. Fixed costs spread across growing revenues. Marketing efficiency improves with brand maturity. Technology investments start yielding returns. The path to 15%+ EBITDA margins appears credible given industry benchmarks and internal improvements.

Category expansion multiplies TAM without incremental customer acquisition costs. A Louis Philippe customer buying LP accessories, innerwear, and casual wear triples lifetime value. Cross-selling opportunities remain largely untapped. Success in innerwear validates the model for replication.

The valuation remains undemanding relative to potential. At 23x forward P/E, ABLBL trades at discount to global fashion brands despite superior growth prospects. The sum-of-parts valuation suggests 40% upside—lifestyle brands alone justify current market cap, making other businesses free options.

XI. Epilogue & "If We Were CEOs"

The leadership transition to Vishak Kumar as CEO in 2025 marks generational change. Kumar, a Madura veteran who built Allen Solly from scratch, brings operational expertise versus financial engineering. His priorities crystallize: fix basics before chasing growth, strengthen brands before expanding categories, delight existing customers before acquiring new ones.

If we were CEO, the strategic agenda would focus on five transformational initiatives:

First, create India's first fashion super-app. Integrate all brands, enable cross-brand loyalty programs, provide styling advice, offer virtual trials, enable social shopping. The app becomes the primary customer interface, generating data for personalization while reducing customer acquisition costs. The ₹500 crore investment pays back through customer lifetime value enhancement.

Second, launch a direct-to-consumer premium brand targeting the top 1%. This wouldn't compete with existing brands but create new category—₹50,000 shirts, ₹200,000 suits. Made-to-measure, Italian fabrics, personal stylists. Just 10,000 customers generating ₹100,000 annually each creates a ₹100 crore ultra-high-margin business.

Third, build India's largest fashion rental platform. The sharing economy meets fashion sustainability. Rent Louis Philippe for interviews, Van Heusen for presentations, Allen Solly for dates. Monthly subscriptions for unlimited swaps. This transforms fashion from product to service, multiplying revenue per garment while addressing sustainability concerns.

Fourth, create an influencer-collaboration model that scales. Partner with 1,000 micro-influencers (10K-100K followers) versus few mega-influencers. Provide exclusive collections, revenue sharing, creative freedom. This distributed marketing approach costs less while driving authentic engagement. Each influencer becomes a digital franchise.

Fifth, establish ABLBL Ventures—a ₹500 crore fund investing in fashion-tech startups. Take minority stakes in virtual trial rooms, sustainable materials, supply chain automation, social commerce platforms. Beyond financial returns, gain early access to innovations, acqui-hire talent, and prevent disruption.

International expansion would follow the Toyota model—start with exports, then CKD assembly, finally local manufacturing. Target the 30 million Indian diaspora with emotional connection to Indian brands. Price at 20% premium to India for exclusivity. Dubai and Singapore prove the model; London and New York follow.

The sustainability transformation goes beyond CSR. Launch "ABLBL Circular"—buy back old garments, recycle into new collections, provide store credit. Create "Carbon Neutral" collections using renewable energy, organic materials, and carbon offsets. Price at 10% premium; conscious consumers happily pay for values alignment.

XII. Recent News

The recent developments confirm strong execution post-demerger. Aditya Birla Lifestyle Brands will hold a meeting of the Board of Directors of the Company on 13 August 2025, signaling active governance and strategic planning. Aditya Birla Lifestyle Brands has received credit rating of CRISIL A1+ for commercial paper, providing access to cost-effective short-term funding.

Stock performance reflects market dynamics rather than fundamentals. The market cap of Aditya Birla Lifestyle Brands Ltd (ABLBL) is ₹16941.09 Cr as of 22nd August 2025, while The 52-week high of Aditya Birla Lifestyle Brands Ltd (ABLBL) is ₹175 and the 52-week low is ₹129.50. The volatility creates opportunities for patient investors understanding the long-term value creation story.

Management communication reinforces confidence. Ashish Dikshit, managing director, Aditya Birla Lifestyle Brands, said, 'As ABLBL embarks on this new chapter as a listed company, we do so with humility, a deep sense of responsibility, and unwavering confidence in our vision. The ambition crystallizes clearly: "Our ambition is clear. To build India's first portfolio of billion-dollar brands in fashion and lifestyle".

The Q1 FY26 results expected in August will provide the first glimpse of ABLBL's independent performance. Focus areas include same-store sales growth momentum, margin trajectory post-separation costs, and strategic initiatives for category expansion. The market awaits clarity on capital allocation priorities and growth investments.

XIII. Links & Resources

Primary Sources: - ABLBL Official Website: www.ablbl.in - ABFRL Investor Relations: www.abfrl.com/investors - Aditya Birla Group: www.adityabirla.com - NSE/BSE Exchange Filings - Annual Reports FY20-FY25 - Demerger Scheme Documents

Industry Research: - India Brand Equity Foundation Fashion Reports - Euromonitor International: India Apparel Market - McKinsey: State of Fashion Reports - BCG-RAI: Retail 2030 India Study - Technopak: Indian Fashion & Lifestyle Market Analysis

Books on Indian Fashion & Retail: - "The Fabric of India" by Rosemary Crill - "Indian Fashion: Tradition, Innovation, Style" by Arti Sandhu - "Retail Management: A South Asian Perspective" by Barry Berman - "Business Maharajas" by Gita Piramal (Birla family history)

Academic Resources: - IIM Ahmedabad Case Studies on Indian Retail - Harvard Business Review: Fashion Industry Analysis - Journal of Fashion Marketing and Management - International Journal of Retail & Distribution Management

Competitor Analysis: - Raymond Limited Annual Reports - Arvind Limited Investor Presentations - Trent Limited (Westside) Financial Documents - Future Lifestyle Fashions Historical Analysis

Podcast Episodes: - The Ken's "The Arc" episodes on Indian fashion - Forbes India's "From the Bookshelves" on retail - Business Standard's "The Playbook" series - Mint's "Plain Facts" on consumer brands

Documentary Recommendations: - "The True Cost" - Fast fashion's global impact - "Made in Bangladesh" - Supply chain realities - "The Next Black" - Future of fashion technology

Market Research Reports: - RedSeer: Indian Fashion E-commerce Report - Deloitte: Global Powers of Luxury Goods - PwC: Total Retail Survey India Edition - KPMG: India's Fashion Retail Market

Final Thoughts

The Aditya Birla Lifestyle Brands story transcends quarterly earnings and stock prices. It's about building enduring value in an industry notorious for creative destruction. The journey from Madura Garments' pioneering vision to ABLBL's independent future demonstrates how patient capital, strategic focus, and operational excellence create sustainable competitive advantages.

The demerger marks not an ending but a beginning. Free from the constraints of conglomerate complexity, ABLBL can pursue its destiny as India's premier lifestyle company. The challenges are real—digital disruption, changing consumer preferences, intense competition. But the opportunities are greater—India's consumption story has just begun, premiumization accelerates, and established brands hold enduring value.

For investors, ABLBL represents a pure-play bet on India's lifestyle transformation. The financials provide comfort, the strategy offers growth, and the management inspires confidence. Whether the stock delivers market-beating returns depends on execution, but the framework for value creation stands robust.

For students of business, ABLBL offers lessons in brand building, portfolio management, and strategic patience. The playbook—localize global trends, build distribution density, invest in brand equity, maintain financial discipline—applies beyond fashion to any consumer business in emerging markets.

The ultimate test lies ahead. Can ABLBL achieve its ambition of building billion-dollar brands? Will the focused structure unlock value that the conglomerate couldn't? How will traditional retail navigate digital transformation? These questions won't be answered in quarters but decades.

What's certain is that ABLBL has earned its place in India's corporate pantheon. From cotton traders in 1857 to lifestyle leaders in 2025, the Birla legacy continues evolving. And as India dresses for success—literally and figuratively—ABLBL stands ready to provide the wardrobe.

The story continues. The best chapters may be yet unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube