ABFRL: From Conglomerate Fashion Play to India's Retail Giant

I. Introduction & Episode Roadmap

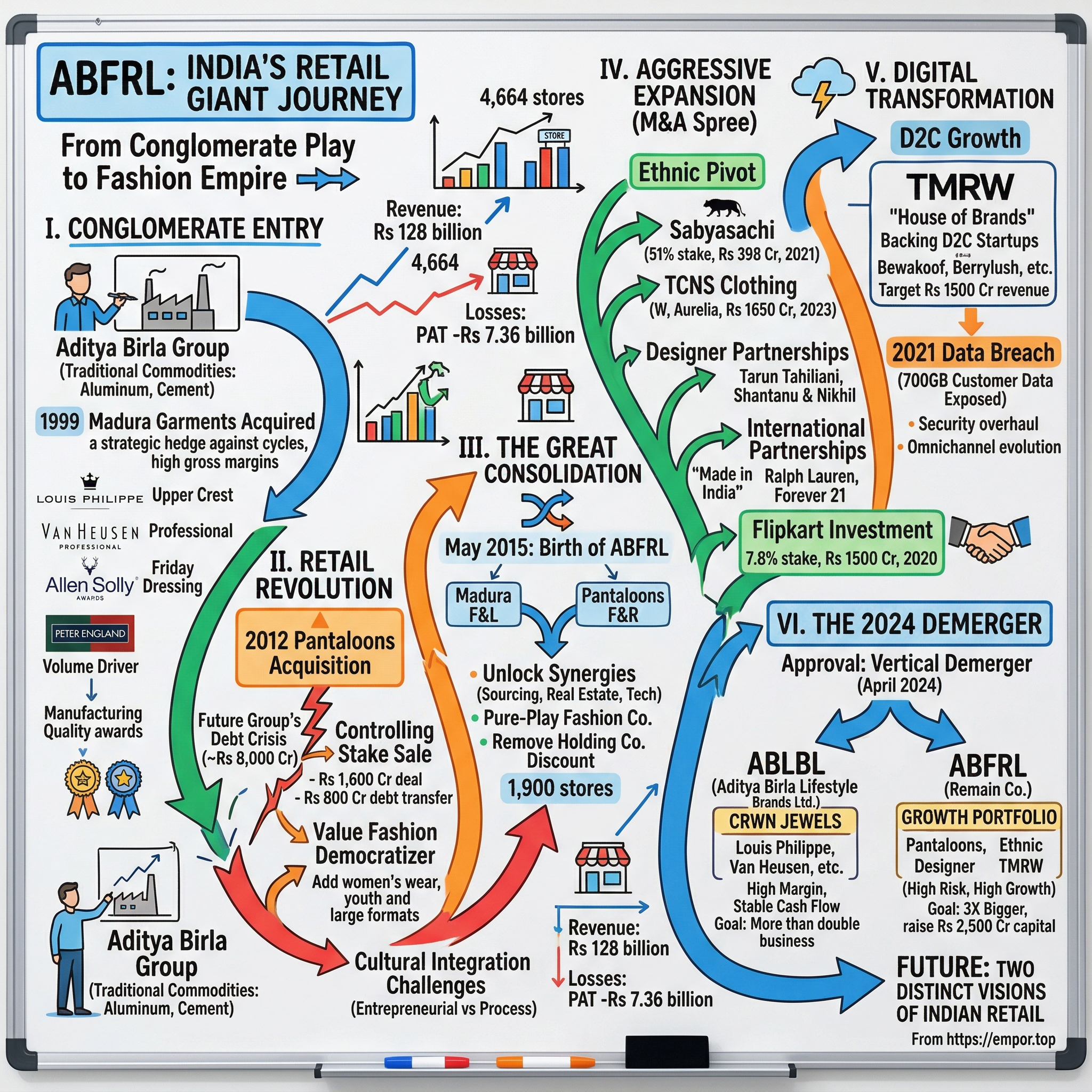

Picture this: It's 2024, and in a gleaming Mumbai boardroom, Kumar Mangalam Birla signs off on splitting his fashion empire in two—a dramatic demerger that would separate the crown jewels of Indian fashion retail. The company he's dividing, Aditya Birla Fashion and Retail Limited, runs 4,664 stores across India, generates ₹128 billion in annual revenue, and touches the wardrobes of millions of Indians daily. From the Louis Philippe suits worn in corporate boardrooms to the Pantaloons outfits filling middle-class closets, ABFRL has quietly become the fabric of modern India.

But here's the question that should intrigue any student of business: How did a traditional conglomerate—one built on aluminum, cement, and chemicals—transform itself into India's largest fashion retailer? The answer isn't just about money or market timing. It's about recognizing a fundamental shift in how a billion Indians would dress themselves as their country modernized.

The story we're about to unfold spans three decades, multiple economic cycles, and dozens of acquisitions. It's a tale of transformation that begins with a single textile acquisition in 1999 and evolves into a retail behemoth that would partner with everyone from Ralph Lauren to Sabyasachi. Along the way, we'll explore how ABFRL cracked the code on Indian formal wear, why they bought Kishore Biyani's crown jewel during his darkest hour, and how they're navigating the treacherous waters between traditional retail and digital disruption.

This isn't just a corporate history—it's a window into India's consumption story. As we trace ABFRL's journey from Madura's early days through the great 2024 demerger and beyond, we'll see how fashion became the unlikely battleground where old-economy conglomerates would compete with e-commerce giants, where international brands would clash with homegrown labels, and where the dreams of India's aspirational middle class would ultimately be won or lost.

II. Aditya Birla Group Context & Fashion Entry

To understand Kumar Mangalam Birla's decision to enter fashion retail in 1999, we need to step back into the sprawling headquarters of the Aditya Birla Group in Mumbai's Worli district. The year is 1995, and a 28-year-old chartered accountant has just inherited one of India's most storied conglomerates following his father's untimely death from prostate cancer. Kumar Mangalam Birla became chairman of the Aditya Birla Group in 1995, at the age of 28, following the death of his father.

The young chairman faced a daunting inheritance. His father, Aditya Vikram Birla, had been a visionary who was one of the first Indian industrialists to expand abroad, setting up plants in Southeast Asia, the Philippines and Egypt. The group he left behind was a commodities powerhouse—aluminum, cement, viscose staple fiber, carbon black—businesses where margins were thin, capital requirements enormous, and differentiation nearly impossible. Under his leadership, the group's annual turnover grew from $2 billion in 1995 to $60 billion in 2022.

But Kumar Mangalam saw something his predecessors hadn't fully grasped: India was changing. The liberalization reforms of 1991 had unleashed aspirational consumption among the middle class. International brands were flooding in. Shopping malls were sprouting in metros. And critically, Indian consumers were beginning to care about what they wore—not just for weddings and festivals, but for work, for weekends, for expressing identity.

The opportunity crystallized in 1999 when Madura Garments came up for sale. Madura Garments was established in 1988, acquired by the Aditya Birla Group in 1999. This wasn't just any apparel company—Madura had cracked a code that had eluded most Indian textile manufacturers. While others churned out unbranded fabric by the meter, Madura had built genuine brands: Louis Philippe for the C-suite executive, Van Heusen for the ambitious manager, Allen Solly for Friday dressing, Peter England for the value-conscious professional.

The strategic rationale was elegant in its simplicity. Fashion retail offered everything the group's traditional businesses didn't: high gross margins (40-50% versus 15-20% in commodities), consumer-facing brands that could command premiums, relatively low capital intensity compared to setting up aluminum smelters, and most importantly, a hedge against the cyclicality that plagued their industrial businesses. When aluminum prices crashed, people still needed to dress for work.

Kumar Mangalam Birla's key acquisitions included Madura Garments, marking what would become the first of over 60 acquisitions he would orchestrate. The price tag wasn't disclosed publicly, but industry insiders whispered numbers around ₹200-300 crore—a rounding error for a group with billions in revenue, yet a bet that would reshape their identity.

The cultural challenge was immense. The Birla Group DNA was B2B industrial manufacturing—long sales cycles, relationship-driven contracts, technical specifications. Fashion was its antithesis: fickle consumers, seasonal collections, store aesthetics, brand perception. Kumar Mangalam's managers in the aluminum division must have wondered what their chairman was thinking. But he understood something fundamental: The group has a presence in 42 countries and a combined annual revenue of US$70 billion, over 50% of which is derived from its overseas operations. To truly become a global conglomerate, they needed consumer businesses that could travel.

The Madura acquisition also represented a philosophical shift. The Birla family had built their fortune on the commanding heights of the economy—the industries that built nations. GD Birla had famously advised his grandson to "never utilize wealth only for fun and frolic" and to "spend the bare minimum on yourself". Fashion seemed almost frivolous by comparison. Yet Kumar Mangalam recognized that in the new India, aspiration itself had become an industry.

This wasn't just about diversification—it was about relevance. The group that had clothed India in viscose fiber would now dress its professionals in branded apparel. The transformation from commodity supplier to lifestyle enabler had begun, setting the stage for what would become a two-decade journey of acquisitions, integrations, and ultimately, the creation of India's largest fashion conglomerate.

III. The Madura Foundation: Building Premium Brands (1988–2012)

The conference room at Madura's Bangalore headquarters in 2000 must have felt like a collision of worlds. On one side sat the old guard from Coats Viyella—British-trained merchandisers who understood thread counts and color fastness. On the other, Kumar Mangalam Birla's team from Mumbai, versed in aluminum smelting and cement kilns. The agenda: figure out how to run India's most sophisticated apparel business within a commodities conglomerate.

Madura F&L was acquired by the Aditya Birla Group in 1999, growing to become a predominant favorite in the ready-made menswear industry in India. What Birla had actually purchased was a masterclass in brand architecture. The original Madura team, operating since 1988 under Coats Viyella, had done something remarkable—they'd convinced Indian men that a shirt wasn't just a shirt.

Consider the genius of their portfolio strategy. Louis Philippe, positioned at the top, wasn't competing with Arrow or Zodiac on price. It was selling an aspiration—the corner office, the business class upgrade, the Taj hotel stay. The brand's tagline, "The Upper Crest," wasn't subtle, but it didn't need to be. In status-conscious India, subtlety was overrated. Shirts priced at ₹2,000-3,000 when the average urban salary was ₹15,000 per month required confidence that bordered on audacity.

Van Heusen occupied the next rung—professional, international, accessible luxury. The brand pioneered wrinkle-free shirts in India, a technical innovation that became a lifestyle statement. The advertising featured men striding purposefully through airports and boardrooms, selling not just clothing but a vision of the globalized Indian professional. Since then, the company has spearheaded the branded apparel retail revolution in India and become a premium lifestyle player in the retail sector.

Allen Solly broke every rule Indian formal wear had established. Launched in 1993 with the tagline "My World, My Way," it introduced the radical concept of Friday dressing to a market where white shirts and dark trousers were almost uniforms. The brand's bright colors, unconventional fits, and casual-formal hybrid positioning created a category that didn't previously exist. Conservative corporate India initially resisted, but younger professionals embraced it as liberation from sartorial monotony.

Peter England, the volume driver, solved a different problem entirely. Positioned as "honest pricing," it gave middle-class Indians permission to buy branded apparel without guilt. At ₹500-800 per shirt, it wasn't dramatically more expensive than unbranded alternatives, but it carried the psychological security of a label, a warranty, consistent sizing—things that mattered when you were buying your first interview outfit.

The distribution strategy was equally sophisticated. While competitors relied on multi-brand outlets where their products fought for attention, Madura pioneered Exclusive Brand Outlets (EBOs). By 2005, they had 500+ stores where the entire environment—lighting, music, visual merchandising—reinforced brand positioning. A Louis Philippe store felt like a gentleman's club; a Peter England store was bright, accessible, family-friendly.

But the real innovation was in supply chain integration. Its manufacturing division was also the first apparel manufacturing unit to win India's prestigious Ramakrishna Bajaj National Quality Award. The company controlled everything from fabric sourcing to retail operations. Their Bangalore factory employed Toyota Production System principles—unusual for apparel manufacturing. Inventory turns, typically 2-3x in Indian apparel, reached 5-6x. This operational excellence meant they could maintain premium pricing while delivering superior margins.

The numbers told the story of transformation. When Aditya Birla acquired Madura in 1999, revenues were approximately ₹400 crore. By 2012, the business had grown to over ₹2,500 crore. More importantly, it had trained an entire generation of Indian consumers to pay premiums for branded apparel. The company that started by importing British sensibilities had created something uniquely Indian—a formal wear market that balanced global aesthetics with local preferences.

In 2000, the company became a division of Aditya Birla Nuvo Ltd, integrating more deeply into the conglomerate structure. This period also saw geographic expansion beyond metros. The insight was simple but powerful: a bank manager in Coimbatore had the same aspirations as one in Mumbai. By taking premium brands to Tier 2 cities through franchising, Madura unlocked markets competitors had ignored.

The cultural transformation within Aditya Birla Group was equally significant. Fashion required different muscles—trend forecasting, seasonal planning, marketing creativity. The group began hiring from NIFT and NID, not just IITs and IIMs. Marketing budgets, negligible in commodity businesses, expanded dramatically. Celebrity endorsements, fashion shows, magazine partnerships—the staid conglomerate was learning to be stylish.

Yet challenges persisted. E-commerce was emerging as a threat. International brands were entering through joint ventures. Fast fashion players like Zara were changing consumer expectations about variety and speed-to-market. The foundation Madura had built was solid, but the building above would need to be larger, more complex. The stage was set for the next act—one that would require not just organic growth but a transformative acquisition that would double the group's fashion footprint overnight.

IV. The Pantaloons Acquisition: Retail Revolution (2012–2015)

The Mumbai monsoon of 2012 was particularly brutal, but inside the Trident hotel's conference room, the rain hammering against floor-to-ceiling windows provided fitting ambiance for what was unfolding. Kishore Biyani, India's self-proclaimed "Retail King," sat across from Kumar Mangalam Birla's team, preparing to sign away his firstborn—Pantaloons, the company that had made him famous, the brand whose name he'd chosen to sound Italian while echoing the Urdu "patloon" for trousers.

In May 2012, Future Group announced a 50.1% stake sale of its fashion chain Pantaloons to Aditya Birla Group to reduce its debt of around ₹8,000 crore. The deal structure was Byzantine in its complexity—a controlling stake in Pantaloon Retail was acquired by Aditya Birla Nuovo Ltd in May 2012 in a complex deal involving a demerger of the business from the wider group. Biyani sold his majority stake in Pantaloons Retail to Aditya Birla Nuvo for Rs 1,600 crore, which included Rs 800 crore of debt transfer.

To understand why Biyani was willing to sell requires rewinding to his empire's peak. By 2009, there were over 100 Big Bazaar stores across the country, serving over two million customers each week, while Pantaloon Retail employed over 30,000 people and had over 12,000,000 square feet of retail space across 1000 stores in 71 cities. He'd built an empire on debt and audacity, expanding into everything from bookstores to salons. Pantaloons Retail had a debt-to-equity ratio of 3:1.

But debt is a cruel mistress in retail. Unlike other Indian retail chains, such as Shoppers Stop, that used a small amount of short-term borrowing and then financed growth through cash generated internally from sales, he had relied heavily on short-term borrowing for expansion. When the 2008 financial crisis hit, followed by India's high interest rate environment, Biyani's leveraged model began to crack. At that point in time, his group was laden with a debt of around Rs 5,000 crore.

For Kumar Mangalam Birla, this was opportunity dressed as distress. Pantaloons wasn't just another retail chain—it was India's answer to Gap or H&M, a democratizer of fashion that had taught middle-class Indians to shop in air-conditioned stores rather than crowded bazaars. The brand operated in a completely different segment from Madura's premium positioning, offering trendy, affordable fashion to younger consumers and families.

The strategic logic was compelling. While Madura dominated formal and premium casual wear for men, Pantaloons brought women's wear expertise, youth fashion credibility, and critically, a large-format retail footprint. In 2012, Aditya Birla Nuvo Ltd had entered into an agreement with the Future Group to infuse Rs 1,600 crore into Pantaloons and acquire a majority stake in the store chain. This wasn't just buying stores—it was acquiring customer relationships, retail locations in premium malls, and operational knowledge of value fashion retailing.

The integration challenges were monumental. Madura's culture was methodical, process-driven, almost academic in its approach to fashion. Pantaloons, birthed from Biyani's gut-instinct retail philosophy, was chaotic, entrepreneurial, reactive. Madura executives were horrified by Pantaloons' inventory management; Pantaloons managers couldn't understand why every decision needed a PowerPoint deck.

The numbers told a story of struggle and eventual stabilization. When acquired, Pantaloons was losing money—the debt servicing alone was crushing margins. But Aditya Birla Group had something Biyani didn't: patient capital and the ability to absorb losses while fixing operations. They invested in technology, streamlined the supply chain, and most importantly, gave the business breathing room.

In 2016, it was renamed as Aditya Birla Fashion and Retail Ltd—though the Pantaloons brand itself was retained for stores. This wasn't mere rebranding; it signaled the complete absorption of what had been Biyani's crown jewel into the Birla empire. The scrappy entrepreneur's creation had been institutionalized.

For Biyani, the sale was both tragedy and liberation. The former billionaire admitted that it was his impulsive decision to play on debt that cost him so much. From Big Bazaar's failure to handing Pantaloons to Aditya Birla Nuvo and selling a mall to pay off his debt, Kishore Biyani's tragic downfall has stunned the entire business world. Yet it allowed him to save the rest of Future Group, at least temporarily.

For Kumar Mangalam Birla, Pantaloons was transformative in a different way. It proved the group could execute large, complex acquisitions in consumer-facing businesses. It demonstrated that they could manage both premium and value segments without cannibalization. Most importantly, it provided the platform and confidence for what would come next—a consolidation that would create India's largest fashion retailer.

The cultural integration took years. Some Pantaloons executives left, unable to adapt to Birla's corporate style. Others thrived, bringing their entrepreneurial energy to a organization that valued it. Gradually, the two cultures merged into something new—structured but agile, process-oriented but customer-focused. The foundation was being laid for an even more ambitious transformation.

V. The Great Consolidation: Birth of ABFRL (2015)

The boardroom at Aditya Birla Nuvo's headquarters in May 2015 buzzed with an energy rarely seen in the typically staid conglomerate. Investment bankers from Standard Chartered shuffled papers while lawyers reviewed documentation one final time. Kumar Mangalam Birla stood to address the assembled directors: "Today, we create India's largest pure-play fashion company." The decision had been years in the making—a consolidation so complex it required three separate boards to approve, two independent valuers to certify, and would fundamentally reshape Indian fashion retail.

ABFRL emerged after the consolidation of the branded apparel businesses of Aditya Birla Nuvo Limited (ABNL), comprising ABNL's Madura Fashion division and ABNL's subsidiaries Pantaloons Fashion and Retail (PFRL) and Madura Fashion & Lifestyle (MFL), in May 2015. Post consolidation, PFRL was renamed Aditya Birla Fashion and Retail Ltd.

The strategic imperative was clear. The group's fashion assets were scattered across multiple entities—Madura Fashion sat within Aditya Birla Nuvo, Pantaloons operated as a separate listed subsidiary, and Madura Garments Lifestyle Retail Company functioned as yet another entity. This structure created inefficiencies, confused investors, and most critically, prevented the businesses from realizing synergies that seemed obvious on paper.

"Investors of ABNL had been asking for a demerger for a long time. This entity will create the largest pure-play fashion company in the country and remove the holding company discount of ABNL," Kumar Mangalam Birla said. The holding company discount was real—analysts estimated ABNL traded at 20-30% below its sum-of-parts value because investors struggled to value a company that combined fashion with financial services, telecom, and insulators.

The mechanics of the consolidation were Byzantine but elegant. Shareholders of ABNL would get 26 new equity shares of PFRL for every 5 equity shares held in ABNL, pursuant to the demerger of Madura Fashion. Similarly, shareholders of Madura Garments would get seven new equity shares of Pantaloons for every 500 Madura Garment equity shares held, pursuant to the demerger of Madura Lifestyle. The complexity reflected the challenge of fairly valuing businesses with different growth trajectories and margin profiles.

The numbers painted a picture of scale. The merged entity would be a Rs 5,290 crore company, operating 1,900 stores across India. The combined business would span the entire spectrum of Indian fashion—from Peter England's value proposition to Louis Philippe's premium positioning, from Pantaloons' family fashion to The Collective's luxury offerings.

But consolidation wasn't just about financial engineering. The consolidation would enable tapping of operational synergies on various fronts, such as sourcing, real estate and technology platforms. Consider the inefficiencies before: Madura and Pantaloons negotiated separately with the same mall developers, maintained duplicate warehouses in the same cities, ran parallel IT systems that couldn't talk to each other. Post-consolidation, a unified negotiating position with landlords alone could save tens of crores annually.

The cultural integration presented its own theater. Pranab Barua, appointed to lead the combined entity, faced the delicate task of merging organizations with distinct DNAs. Madura's premium brand managers, accustomed to focusing on brand equity and margins, suddenly had colleagues from Pantaloons who obsessed over footfalls and conversion rates. The first combined leadership meeting reportedly lasted twelve hours as executives debated everything from store design philosophy to inventory management metrics.

Fashion retailing was doing far better than the country's economy, with the combined entity's revenue growing by 40 per cent and EBITDA by 43 per cent, in the past two years. This performance vindicated the strategic bet—fashion was becoming a core business for the group, not just a diversification play.

The debt situation required careful management. The combined entity would have a debt of Rs 1,775 crore, after loans of about Rs 475 crore would be passed from Madura to Pantaloons. For a business generating strong cash flows, this was manageable, but it meant the newly consolidated entity would need to be disciplined about capital allocation.

Market reaction was initially mixed. Some investors worried about integration risks, others about whether premium and value brands could coexist without cannibalization. But Kumar Mangalam Birla had a broader vision. "This business generates strong cash flow and I believe that it can use its own internal accruals to fuel its own growth plan. It doesn't require any funding beyond that," Birla added.

The consolidation also marked a philosophical shift in how Indian conglomerates thought about consumer businesses. Rather than treating them as portfolio diversifications, the Birla Group was signaling that fashion deserved focused management, dedicated capital, and strategic priority. The creation of ABFRL wasn't just a corporate restructuring—it was a statement that Indian consumers had evolved beyond price-consciousness to brand-consciousness, and that serving them required scale, sophistication, and specialization.

ABFRL brings together the learnings and businesses of two renowned Indian fashion icons, Madura Fashion & Lifestyle and Pantaloons creating a synergistic core that will act as the nucleus of the future fashion businesses of Aditya Birla Group. This nucleus would soon attract an even more ambitious expansion—a shopping spree that would bring international brands, designer labels, and digital natives under one increasingly powerful umbrella.

VI. The M&A Spree: Building a Fashion Empire (2016–2024)

The conference room at ABFRL's headquarters in October 2020 felt different from usual board meetings. On one screen, Kalyan Krishnamurthy, CEO of Flipkart, joined via video link. On another, investment bankers presented valuation models. The agenda: Flipkart is acquiring a 7.8% stake in Aditya Birla Fashion for ₹1,500 crore—a validation from India's e-commerce giant that ABFRL had become too important to ignore.

This Flipkart investment marked the beginning of what would become ABFRL's most aggressive expansion phase. Between 2016 and 2024, the company would execute over a dozen major deals, transforming from a domestic apparel player into a comprehensive fashion powerhouse spanning luxury to value, western to ethnic, physical to digital.

The international brand partnerships came first, each carefully chosen to fill portfolio gaps. It has exclusive partnerships with brands such as Ralph Lauren, Hackett London, Ted Baker, Fred Perry, Forever 21, American Eagle, Reebok, Simon Carter and Galeries Lafayette. The strategy was surgical—Ralph Lauren for ultra-premium American style, Hackett for British luxury, Forever 21 for fast fashion, American Eagle for casual youth wear, Reebok for athleisure. Each brand brought not just products but knowledge—how to merchandise luxury, how to turn inventory faster, how to appeal to Gen Z.

But the real transformation came through the ethnic wear pivot. In January 2021, ABFRL stunned the market with its boldest move yet. Aditya Birla Fashion and Retail Ltd (ABFRL) has announced a strategic partnership with India's largest designer brand Sabyasachi by signing a definitive agreement for acquiring 51 per cent stake in Sabyasachi brand. Sabyasachi is India's largest and most influential luxury designer brand with strong Indian roots and global appeal. The price tag: ₹398 crore for 51% stake.

Sabyasachi Mukherjee wasn't just any designer—he was the architect of modern Indian luxury, the man who dressed Bollywood royalty and Silicon Valley billionaires' daughters for their weddings. The Sabyasachi brand, incorporated in 1990, had revenues of ₹274 crore in 2019-20, and is a leading player in designer apparel, jewellery and accessories for both men and women. For ABFRL, this wasn't just buying a brand; it was acquiring cultural capital that money typically couldn't buy.

The ethnic strategy accelerated. The company has strategic partnerships with Designers 'Shantanu & Nikhil', 'Tarun Tahiliani', 'Sabyasachi' and 'House of Masaba'. Each designer brought a different aesthetic—Tarun Tahiliani's fusion couture, Shantanu & Nikhil's military-inspired luxury, Masaba Gupta's quirky prints that resonated with millennials. The message was clear: ABFRL would own every price point and style sensibility in ethnic wear.

ABFRL Managing Director Ashish Dikshit said ethnic wear is going to be an increasingly important category as young and confident Indians rediscover their culture and heritage. "We see a 'Made in India' global brand like Sabyasachi occupying the pinnacle of our ethnic wear portfolio. Over the next few years, ABFRL intends to craft a portfolio that addresses the entire gamut of ethnic wear segments: value, premium and luxury," he said.

The masterstroke came in May 2023. ABFRL, India's leading fashion & apparel company, today announced that it has entered into definitive agreements to acquire TCNS Clothing, the owner of leading ethnic brands W, Aurelia, Wishful, Folksong and Elleven. The value of the promoter stake and open offer consideration for TCNS is ~ Rs. 1650 Cr. for 51% stake, making this one of the largest deals in the Indian fashion space.

TCNS wasn't a luxury play—it was volume ethnic wear, the everyday kurti that working women wore to office, the festive outfit for middle-class celebrations. TCNS had sales of Rs 896 crore during FY22. Combined with Sabyasachi at the top and these brands in the middle, ABFRL now owned the entire ethnic wear pyramid.

Speaking on the transaction, Mr. Kumar Mangalam Birla, Chairman, Aditya Birla Group, said, "This deal is yet another marker of the Aditya Birla Group's faith in the dynamism and buoyancy of the Indian consumer economy. As India stands on the cusp of a multi-decadal consumption boom, ABFRL is a forerunner in shaping the fashion landscape of our vibrant nation. For ABFRL, the TCNS deal is indeed a significant milestone as it complements our existing portfolio of exceptional brands across the entire spectrum of Indian fashion. By embracing TCNS's portfolio of loved women's ethnic brands, we are reinforcing our commitment to ethnic wear, the largest category in the apparel industry.

The numbers painted a picture of transformation. With this acquisition ABFRL's ethnic wear portfolio is expected to reach Rs.5000 Cr in the next 3 years. From zero presence in ethnic wear in 2015, ABFRL had built what would become a ₹5,000 crore business—larger than many standalone companies.

The deal-making wasn't without challenges. Integrating designer brands with corporate processes proved delicate. Sabyasachi Mukherjee, used to complete creative control, had to adapt to quarterly reviews and EBITDA discussions. Store managers trained in selling Peter England shirts had to learn the art of selling ₹3 lakh lehengas. The IT systems that tracked inventory for mass fashion struggled with made-to-order couture.

Market reception was mixed. Some investors worried about the prices being paid—51% of TCNS for ₹1,650 crore implied a valuation multiple that seemed aggressive for a company with modest profitability. Others questioned whether ABFRL could maintain the authenticity of designer brands while scaling them.

But Kumar Mangalam Birla saw something others missed. India wasn't just growing richer—it was growing prouder. The same consumers who wore western formals to work were rediscovering Indian wear for occasions. The pandemic had accelerated this trend, with virtual weddings requiring designer wear shipped globally. Commenting on the acquisition, Mr. Ashish Dikshit, Managing Director, ABFRL, said, "As young Indians identify a new-found confidence in their identities woven around Indian culture and heritage, the next set of leading consumer brands will be built in the Indian ethnic wear space. TCNS, through its brands W, Aurelia, Wishful, Folksong & Elleven, is catering to the Indian women's fashion needs across markets and price points. Each of these brands have been built over a long period of time and enjoy tremendous consumer love.

The Flipkart relationship added another dimension. Kalyan Krishnamurthy, CEO of Flipkart Group, said the two companies will work toward "making available a wide range of products for fashion-conscious consumers across different retail formats across the country. We look forward to working with ABFRL and its well-established and comprehensive fashion and retail infrastructure as we address the promising opportunity of the apparel industry in India." Flipkart already dominates in the online sales of apparels in India, thanks in part to Myntra, a fashion e-tailer it bought it in 2014.

By 2024, ABFRL's M&A spree had fundamentally transformed the company. As on 31 March 2024, ABFRL has a network of 4,664 stores, apart from being present in multi-brand outlets. It was no longer just a men's formal wear company that had acquired a value retailer. It was India's only fashion conglomerate with meaningful presence across every segment, style, and price point—a transformation that would soon lead to yet another dramatic restructuring.

VII. Digital Transformation & Omnichannel Evolution

The morning of December 21, 2021, started like any other at ABFRL's Mumbai headquarters until the cybersecurity team's monitors lit up with alerts. A hacker group called ShinyHunters had posted on dark web forums, claiming to have breached ABFRL's systems. The scale was staggering: A hacker group called ShinyHunters has allegedly made 700 GB of ABFRL's customer data public, including 5.4 Mn emails and phone numbers.

The breach was a brutal wake-up call for a company that had been aggressively building its digital capabilities. "We tried to get in touch with ABFRL. They sent a negotiator but he was just stalling (the offer was more than reasonable for a "US$ 45-Billion conglomerate"). So we decided to leak everything for you guys including their famous divisions such as Pantaloons.com or Jaypore.com," said the user in a forum post. Personal customer information such as names, phone numbers, dates of birth, addresses, order histories, credit card details, and passwords was also included in the public data. ABFRL employee information was also exposed in the data breach, including salary information as well as personal information ranging from religion to marital status.

The response was swift but revealed the challenges of digital transformation for traditional retailers. "ABFRL is investigating an information security issue involving illegal access to its e-commerce database," an Aditya Birla Group spokeswoman stated. "As a precaution, the company has reset all customer passwords and enabled OTP-based authentication, as well as taken further steps to secure access to customer and employee information."

But ABFRL's digital journey wasn't defined by this setback—it was accelerated by it. Six months later, in June 2022, the company launched TMRW, its most ambitious digital initiative yet. In the digital ventures sector, Aditya Birla Group made significant strides with the launch of TMRW. Housed under the fashion and retail flagship of the group, Aditya Birla Fashion and Retail (ABFRL), TMRW is building India's largest portfolio of disruptor brands in the fashion & lifestyle space and enabling the next phase of direct to consumer (D2C) growth in India. TMRW is on a path to create a leading technology-led digital-first 'House of Brands' business over the next several years.

TMRW represented a philosophical shift. Rather than trying to digitize legacy brands, ABFRL would acquire and nurture digital-native brands that understood the Instagram generation. The eight D2C brands that TMRW has backed are Berrylush, Bewakoof, Juneberry, Natilene, Nauti Nati, Nobero, Urbano and Veirdo. TMRW informed that after onboarding the mentioned eight D2C brands, it has attained a revenue run-rate o more than INR 700 Cr. It also aims to surpass an annualised revenue rate of over INR 1500 Cr in the coming 12 months.

The Bewakoof acquisition exemplified the strategy. Aditya Birla Fashion and Retail (ABFRL) is likely to acquire a controlling stake in a Mumbai-based start-up Bewkaoof by investing nearly Rs 100 crore. Both companies are supposed to be in the final stage of talks before the expected acquisition. Bewakoof wasn't just another apparel brand—it was a lifestyle built on quirky graphics, millennial humor, and Instagram virality. Their t-shirts with slogans like "Eat Sleep Repeat" and "Ghanta Engineer" had become cultural touchstones for young India.

"By tapping into ABFRL's fashion capabilities and category expertise, TMRW is on the path to replicate the success in the digital first space by building the next generation of memorable brands that will drive India's e-commerce growth," said, Ashish Dikshit, managing director of ABFRL. The strategy was clear: combine startup agility with corporate resources.

The omnichannel integration presented its own challenges. ABFRL's traditional brands had been built for physical retail—visual merchandising, store ambiance, personal selling. Digital required different muscles: performance marketing, influencer partnerships, real-time inventory management across channels. The company had to build capabilities from scratch or acquire them.

The technology stack transformation was massive. Legacy ERP systems designed for seasonal collections had to adapt to digital brands launching new products weekly. Point-of-sale systems had to integrate with e-commerce platforms. Inventory had to be unified across channels—a customer should be able to buy online and return in store, or check online if their size was available at the nearest outlet.

The data breach had forced a security overhaul, but it also accelerated digital investments. Two-factor authentication became mandatory. Customer data was encrypted and segregated. Regular security audits became routine. The breach cost wasn't just financial—it was reputational, forcing ABFRL to rebuild trust pixel by pixel.

By 2023, the digital transformation was showing results. In FY23, the company generated over ₹1,300 crore revenue from its online business. It has integrated around 2,000 brand stores and around 300 Pantaloon stores to its onmi-channel online platform. Online wasn't just another channel—it was becoming the channel, especially for younger brands.

According to the company, through the current portfolio, TMRW has marked a presence in various sub-segments of the apparel industry including casual, kids and western wear. TMRW plans to expand further in lifestyle categories including beauty and personal care space. It aims to partner with new-age founders by bringing in strategic, operational and technological capabilities.

The cultural transformation was perhaps the hardest. Store managers who'd spent careers focusing on visual merchandising had to learn about conversion funnels and cart abandonment. Designers trained in seasonal collections had to adapt to weekly drops. Marketing teams comfortable with billboards had to master programmatic advertising.

Yet the digital push wasn't meant to replace physical retail—it was meant to enhance it. Stores became experience centers where customers could touch and feel products before ordering online. Digital screens in trial rooms suggested matching accessories. Mobile apps notified customers when their favorite brand launched new collections.

The TMRW initiative also served another purpose: talent acquisition. "Both companies have signed a non-disclosure agreement and they have also finished due diligence. The team at Bewakoof is also moving to join Aditya Birla's new firm," a person aware of the development told The Economic Times. By acquiring digital-native brands, ABFRL was also acquiring digital-native talent—growth hackers, data scientists, content creators who understood the new consumer.

ShinyHunters' breach had been a crisis, but it catalyzed a transformation that might have taken years otherwise. From a company that sold clothes through stores, ABFRL was becoming a company that sold lifestyles through every conceivable channel. The foundation was being laid for what would soon become another dramatic transformation—the great demerger of 2024.

VIII. The 2024 Demerger: Two Paths, One Vision

The April 19, 2024 board meeting at ABFRL headquarters felt like déjà vu. Nine years after creating India's largest fashion conglomerate through consolidation, Kumar Mangalam Birla was about to split it apart. The Board of Directors of ABFRL, at its meeting on 19th April, has approved the proposal of vertical demerger of Madura Fashion & Lifestyle business (MFL Business) from ABFRL into a newly incorporated company named as Aditya Birla Lifestyle Brands Ltd. (ABLBL), which will be listed separately on completion of the demerger.

The logic was counterintuitive yet compelling. The company announced demerger on 1st April 2024. MFL contributes approximately 60% of ABFRL's consolidated revenue and 75% of its segment EBITDA, maintaining a margin of 15.6% in the first nine months of FY24. The remaining businesses of ABFRL, excluding MFL, generated around 40% of revenue with a 7.6% EBITDA margin. These numbers revealed the fundamental tension—Madura's premium brands were subsidizing the growth investments in ethnic wear, digital ventures, and value retail.

"The demerger is expected to unlock significant value for the shareholders of ABFRL as each of the listed entities will have their own distinct capital structures, independent growth trajectories & value creation opportunities," ABFRL said in its release. Translation: investors couldn't properly value a company that combined Louis Philippe's 20% EBITDA margins with loss-making digital ventures and capital-hungry ethnic acquisitions.

The structure was elegant in its simplicity. Upon completion of the demerger, as per the share entitlement ratio approved by the Board and recommended by the independent valuer, the shareholders of ABFRL will get one share of ABLBL for every one share in ABFRL, in addition to their existing shareholding in ABFRL. No cash changed hands, no shareholders were diluted—it was a pure split.

Post demerger, ABLBL will house Louis Phillippe, Van Heusen, Allen Solly, Peter England, American Eagle, Forever 21, Reebok and the innerwear business under Van Heusen brand. These were the crown jewels—established brands with predictable cash flows, loyal customers, and minimal capital requirements for growth. ABLBL wants to more than double its business and triple its cash profits by building on the strength of its popular and well-established brands.

ABFRL will house its value and masstige fashion retail play under Pantaloons and Style Up, its ethnic portfolio which also include its designer wear and the recently acquired portfolio of TCNS. It will also house a fast-growing bridge to the luxury and luxury platform of The Collective, Galleries Lafayette and select luxury brands and its portfolio of digital first fashion brands under TMRW. This was the growth portfolio—higher risk, higher capital needs, but potentially higher rewards. ABFRL aims to grow three times bigger by focusing on value fashion, ethnic wear, luxury brands, and online-first labels.

The debt allocation revealed priorities. The overall ABFRL borrowing, which is estimated to be aproximately Rs. 3000 crore as of 31st March 2024, will be split between the two companies. The estimated debt to be transferred to ABLBL will be approximately Rs. 1000 crore, and the balance will continue to stay with ABFRL. The message was clear: the stable Madura business could support some leverage, but the growth businesses needed a cleaner balance sheet.

The market reaction on May 22, 2025, was dramatic but expected. ABFRL share price plunges 66% as the much-anticipated demerger with Madura Fashion & Lifestyle (MFL) took effect. ABFRL shares saw a drop in price of fully 67% on the May 22, 2025 record date, making the closing price ₹88.80 on NSE. This wasn't value destruction—it was value reallocation. The Madura business that had been embedded in ABFRL was now trading separately as ABLBL.

The capital raise plans underscored the strategic divergence. Within 12 months after the completion of the demerger, ABFRL plans to raise approximately Rs. 2,500 crore equity capital to strengthen its balance sheet and fund the growth of the remaining businesses. The company's promoter group will fully support the proposed equity raise. This wasn't distress financing—it was growth capital for a company unburdened by the need to also fund dividend expectations from Madura's stable cash flows.

For employees, the demerger created clarity but also anxiety. Madura executives who'd built careers on brand management and operational excellence suddenly found themselves in a pure-play premium apparel company—no more subsidizing experimental ventures. ABFRL employees working on ethnic brands or digital initiatives no longer had to justify their investments against Madura's reliable returns.

The strategic implications were profound. A demerger allows each group to set its own plans for growth, update its capital arrangements and focus on what matters to it most. ABLBL could pursue international expansion for established brands without worrying about capital allocation to ethnic wear. ABFRL could make bold bets on digital brands without being penalized for diluting Madura's margins.

The timing wasn't accidental. Rising aspirations among middle and upper-class consumers are driving demand for ethnic wear and luxury fashion, making these categories more mainstream. The ethnic wear market was exploding, digital brands were reaching scale, but these opportunities required patient capital and tolerance for losses—something harder to justify when bundled with cash-generative premium brands.

The demerger also reflected a maturation in Indian capital markets. Investors were sophisticated enough to value different businesses appropriately rather than applying a blended multiple. The reason for demerging was to remove confusion in daily operations and create benefits for shareholders. Each entity could now attract its natural investor base—ABLBL for those seeking stable returns and dividends, ABFRL for growth investors willing to accept volatility for higher potential returns.

Kumar Mangalam Birla's decision to split what he'd spent a decade building wasn't an admission of failure—it was recognition that different businesses needed different strategies, capital structures, and even cultures. The conglomerate discount that had plagued ABFRL would be replaced by focused execution in two pure-play companies.

The demerger will be implemented through an NCLT scheme of arrangement and upon its completion, all shareholders of ABFRL will have identical shareholdings in both the companies. PWC LLP are the statutory auditors of the Company and AZB are the legal counsels for the transaction. Bansi S Mehta Valuers LLP were the independent valuers to the transaction. The machinery of corporate restructuring was in motion once again.

As shareholders received their ABLBL shares alongside their adjusted ABFRL holdings, they weren't just getting two companies instead of one. They were getting two distinct visions of Indian fashion's future—one built on the certainty of premium brands, the other on the possibility of ethnic resurgence and digital disruption. The great consolidation of 2015 had given way to the great demerger of 2024, each reflecting the market realities of its time.

IX. Financial Deep Dive & Unit Economics

The numbers tell a story of ambition colliding with market reality. Leading Indian conglomerate Aditya Birla Fashion and Retail (ABFRL) Ltd has reported a consolidated revenue of ₹139.96 billion (approximately $1.67 billion) for the year, marking a 13 per cent increase year-on-year (YoY). However, despite the revenue growth, the company recorded a loss with a profit after tax (PAT) of minus ₹7.36 billion. EBITDA stood at ₹17.03 billion, reflecting a 5 per cent YoY increase.

To understand ABFRL's financial DNA, you need to dissect it segment by segment, each with radically different unit economics. The lifestyle brands segment reported a 2 per cent YoY growth, achieving revenue of ₹15.64 billion. The EBITDA for this business rose by 36 per cent YoY to ₹3.05 billion, driven by improved gross margins and tighter cost controls, with an EBITDA margin of 19.5 per cent, up 480 basis points from last year. This was the cash engine—predictable, profitable, funding everything else.

But the growth segments painted a different picture. Excluding TCNS, the ethnic business saw a 51 per cent YoY growth in Q4, driven by higher same-store sales, network expansion, and category extensions. Notably, the Sabyasachi brand grew by 56 per cent YoY in Q4. The men's premium ethnic wear brand Tasva doubled its revenue over the last year in FY24. Hypergrowth, but at what cost?

The Pantaloons story exemplified the challenges of value retail. Pantaloons recorded quarterly sales of INR 895 crores, a growth of 10%. L2L for the quarter stood at 1%. EBITDA margin for the business grew by 270 basis points to reach 10.4%. For FY '24, revenue stood at INR 4,328 crores, a growth of 5% Y-o-Y. Like-for-like growth of just 1%—stores were cannibalizing each other, or worse, customers were trading down.

The store economics revealed structural challenges. As of March 2024, ABFRL has a network of 4,664 stores across approximately 37,205 multi-brand outlets with 9,563 point of sales in department stores across India. With 4,664 stores generating ₹140 billion in revenue, average revenue per store was approximately ₹3 crore annually—barely ₹8-9 lakh per month. After rent (typically 15-20% of sales), staff costs, and utilities, many stores were barely breaking even.

The capital allocation dilemma was stark. Lifestyle brands with 19.5% EBITDA margins required minimal capital—maybe a store refresh every 5-7 years. But ethnic brands needed constant investment in inventory (designer wear doesn't turn quickly), marketing (building luxury perception costs money), and stores (Sabyasachi boutiques couldn't look like Peter England outlets).

Both our Ethnic and D2C businesses, driven by a combination of organic growth and strategic acquisitions, more than doubled their revenue this quarter. The company achieved a consolidated EBITDA of INR 377 crores with margin expansion of 300 basis points to reach 11.1% versus 8% last year, powered by profitability, enhancement measures by our large established Lifestyle and Pantaloons businesses, our standalone business EBITDA grew by 59% Y-o-Y. The math was challenging—doubling revenue while EBITDA grew 59% meant margins were compressing in growth segments.

Working capital management added another layer of complexity. Premium brands like Louis Philippe could negotiate 60-90 day payment terms with suppliers, turning inventory 4-5 times annually. Designer brands carried inventory for 180+ days—wedding lehengas don't sell every day. Digital brands needed to maintain inventory across sizes and styles, killing working capital efficiency.

The debt situation reflected these tensions. To start with, this segment posted revenue of INR 6,518 crores with EBITDA of INR 460 crores in fiscal year FY '24. Margin for the segment stood at 7.1%, considering the inclusion of TCNS and investment in new businesses. With ₹3,000 crore in debt and EBITDA of ₹1,700 crore, the debt-to-EBITDA ratio of 1.8x wasn't alarming, but interest coverage was thin given the losses.

The international brand partnerships revealed another dynamic. The American Eagle brand continued its strong performance with a 27 per cent sales growth for the quarter. American Eagle grew 27%, Reebok 29%—but these were typically licensing deals where ABFRL paid 7-10% royalties on sales. Great for top-line growth, brutal for margins.

Post demerger, ABFRL will raise price capital of INR 2,500 crores to strengthen its balance sheet and support the growth needs of its constituent businesses. The ₹2,500 crore capital raise post-demerger wasn't desperation—it was recognition that fashion retail is capital-intensive during growth phases. Every new store required ₹50-80 lakh in fit-outs, ₹30-50 lakh in inventory, plus working capital.

The market's assessment was harsh but fair. Mkt Cap: 9,152 Crore (down -32.0% in 1 year). The company has delivered a poor sales growth of -3.50% over past five years. A market cap of ₹9,152 crore for a company with ₹14,000 crore revenue implied a price-to-sales ratio of 0.65x—the market was pricing in execution risk.

Aditya Birla Fashion and Retail Ltd (ABFRL) on Wednesday reported widening of consolidated net loss at ₹ 233.73 crore for June quarter FY26. The company had posted a loss of ₹ 214.92 crore during April-June quarter a year ago, according to a regulatory filing from ABFRL. Post-demerger losses were widening, but this reflected transition costs and growth investments rather than operational deterioration.

The unit economics varied wildly by format. A Louis Philippe store in a metro mall might generate ₹2 crore monthly revenue with 25% EBITDA margins. A Pantaloons store in the same mall did ₹1.5 crore at 10% margins. A Sabyasachi boutique might do ₹50 lakh but at 40% margins. The challenge was portfolio optimization—which format deserved capital?

The competitive dynamics added pressure. Zara and H&M were expanding aggressively, Reliance's Azorte was gaining share, and Tata's Westside was consistent. Online players like Myntra (ironically, a Flipkart subsidiary and ABFRL shareholder) were taking share. Every percentage point of market share lost meant ₹100+ crore in revenue.

And this is more a trend as we saw the demand side of the business coming down was on store expenses. You saw the rationalization network, so that reduces the fixed cost of less profitable stores or unprofitable stores. Store rationalization was acknowledgment that growth for growth's sake didn't work. Closing unprofitable stores improved margins but reduced network effects and supplier leverage.

For the financial year which ended on March 31, 2024, ABFRL net loss was at Rs 735.91 crore. It was at Rs 59.47 crore a year ago. Its revenue from operation in FY24 was Rs 13,995.86 crore. The deteriorating profitability—from ₹59 crore loss to ₹736 crore—reflected the cost of transformation. TCNS integration, digital investments, ethnic brand building—all necessary but expensive.

Looking forward, the financial trajectory depends on execution. If ethnic brands achieve scale while maintaining premium positioning, if digital brands reach profitability, if Pantaloons recovers like-for-like growth—the losses could turn to profits. But fashion retail is unforgiving. One bad season, one failed collection, one wrong trend call, and inventory piles up, margins evaporate.

The financial deep dive reveals a company in transition—profitable legacy businesses funding loss-making growth bets, stable cash flows supporting experimental ventures, proven formats subsidizing unproven concepts. Whether this transforms into sustainable profitability or perpetual losses depends on whether ABFRL can crack the code that has eluded most fashion retailers globally: scaling multiple brands across multiple segments profitably. The demerger was recognition that maybe, just maybe, trying to do everything under one roof was the problem, not the solution.

X. Playbook: Lessons in Conglomerate Fashion Retail

The ABFRL story offers a masterclass in the unique challenges of building fashion retail within a traditional conglomerate structure. The playbook that emerges isn't just about fashion—it's about how industrial giants can transform into consumer businesses, with all the cultural, operational, and financial gymnastics that entails.

Lesson 1: The Portfolio Approach to Brand Building

ABFRL's journey reveals a fundamental truth: in fashion, you can't be everything to everyone with one brand. Key segment growth included American Eagle at 27 per cent, Reebok at 29 per cent, and the ethnic business at 51 per cent. The portfolio strategy—owning multiple brands across price points—allowed ABFRL to capture value across the entire consumer pyramid without brand dilution.

The execution required different muscles for each segment. Louis Philippe needed brand custodians who understood premium positioning. Pantaloons required merchants who could spot trends quickly and negotiate aggressively. Sabyasachi demanded curators who respected creative integrity while driving commercial outcomes. Managing this complexity within one organization was like running multiple companies simultaneously.

Lesson 2: Managing Complexity Across Channels and Segments

The operational complexity of running 4,664 stores across formats, price points, and geographies would challenge any retailer. But doing it within a conglomerate accustomed to running aluminum smelters and cement plants required fundamental reimagination of management systems.

Traditional conglomerate metrics—capacity utilization, yield optimization, cost per ton—didn't translate to fashion. Instead, ABFRL had to master inventory turns, conversion rates, average transaction values, style success rates. The IT systems designed for commodity businesses had to evolve to handle SKU proliferation—a cement plant might have 5 products; a fashion retailer has 50,000.

Pantaloons business continued to make concerted efforts towards addressing market challenges and strengthening its business model for the future. As the year progressed, series of interventions around improving consumer proposition, enhancing product value equation and driving efficiencies in back-end operations led to improvement in sales and margins. Business intends to keep making progress on this path going forward as well. The constant optimization—improving value equation, driving efficiencies—showed that fashion retail is never "done." It requires continuous evolution.

Lesson 3: The India Playbook - Organized vs Unorganized Transition

ABFRL's growth coincided with—and capitalized on—India's transition from unorganized to organized retail. In 2000, 97% of apparel was sold through unorganized retail. By 2024, organized retail had captured 35-40% share. ABFRL rode this wave but also helped create it.

The strategy was multi-pronged: build trust through consistent quality (unlike variable unorganized retail), offer convenience through multiple payment options and returns policies, create aspiration through store ambiance and brand building. Every Pantaloons store that opened didn't just compete with other brands—it competed with the local tailor, the street vendor, the family textile shop.

Understanding Indian consumers' unique needs was crucial. Indians shop differently from Americans or Europeans—more family-oriented, more festival-driven, more price-quality conscious. ABFRL's brands reflected this: Peter England's "honest pricing," Pantaloons' family shopping experience, Sabyasachi's wedding focus.

Lesson 4: Capital Allocation in a Capital-Intensive Business

Fashion retail's capital intensity surprised many traditional investors. Every store required upfront investment, inventory needed funding, and brand building demanded marketing spend. Unlike a cement plant that, once built, generates cash for decades, fashion retail requires constant reinvestment.

This strategic demerger of ABFRL is paving the way for the creation of 2 separate growth engines, each with a clear capital allocation strategy and unique path for value creation. The demerger recognition that different businesses needed different capital structures was crucial. Premium brands could support debt; growth ventures needed equity.

The acquisition strategy also revealed capital allocation discipline. Paying ₹398 crore for 51% of Sabyasachi seemed expensive, but the brand's 56% growth validated the premium. The ₹1,650 crore for TCNS was a bigger bet, but it bought immediate scale in ethnic wear. Each acquisition was a capital allocation decision—build or buy?

Lesson 5: Why Fashion is Different from Other Conglomerate Businesses

Fashion's fundamental characteristics make it unlike any other business in the Aditya Birla portfolio. Fashion is emotional, not functional—people need cement, they want fashion. Fashion is fast-changing—aluminum's properties haven't changed in centuries; fashion changes every season. Fashion is creative—you can't engineer a successful design like you engineer a chemical process.

Our businesses demonstrated notable resilience amid the overall slowdown and added challenges of a shift in festive season and fewer wedding dates. Net profit for the quarter was affected by negative operating leverage resulting from subdued sales in a weak demand environment. The sensitivity to external factors—festive seasons, wedding dates, weather—made fashion unpredictable in ways industrial businesses aren't.

The talent requirement was also different. Fashion needs designers, merchandisers, visual artists—creative professionals who think differently from engineers and MBAs. Integrating these creative professionals into a traditional corporate structure, with its emphasis on process and predictability, created constant tension.

Lesson 6: The Technology Transformation Imperative

Fashion retail's digital transformation isn't optional—it's existential. ABFRL's journey from physical-only to omnichannel revealed how technology changes everything: customer acquisition (social media marketing vs. billboards), inventory management (real-time across channels vs. periodic stock takes), customer service (chatbots and virtual try-ons vs. store staff).

The TMRW initiative represented acknowledgment that digital-native brands require different capabilities. You can't run an Instagram-first brand with the same playbook as a mall-based store. The technology stack, marketing approach, inventory model, even the org structure needs to be different.

Lesson 7: Building vs Buying - The M&A Imperative

ABFRL's acquisition spree revealed a crucial insight: in fashion, time-to-market matters more than cost optimization. Building Sabyasachi from scratch would take decades; buying it provided instant credibility. Creating ethnic wear brands organically was possible but slow; acquiring TCNS provided immediate scale.

The integration challenges were real—different cultures, systems, processes. But the alternative—organic growth—was too slow in a rapidly consolidating market. Every year of delay meant competitors gained share, consumer preferences evolved, new channels emerged.

Lesson 8: The Patience Paradox

Perhaps the most important lesson is the patience paradox: fashion retail requires long-term thinking in a short-term industry. Building brands takes decades, but fashion cycles last weeks. Store investments have 7-10 year paybacks, but consumer preferences change annually.

In the face of persistent market headwinds, ABFRL has navigated another quarter, marked by subdued discretionary spending and a slow rural recovery affecting the value and masstige segments. Despite these market conditions, ABFRL remains steadfast in its commitment to its strategic vision. By doubling down on innovation with new product launches, enhancing customer interactions and experience, expanding our reach across channels and markets, and streamlining operations, we have laid the groundwork for future growth and resilience. This long-term commitment despite short-term pressures is what separates successful fashion retailers from failures.

The conglomerate backing provided this patience—capital during losses, support during transformation, ability to withstand market volatility. A standalone fashion retailer might have folded during COVID or the 2023 consumption slowdown. ABFRL could weather these storms because it had a parent with deep pockets and long-term vision.

The playbook that emerges is complex, nuanced, and still being written. It's about managing paradoxes—global aspiration with local relevance, premium positioning with democratic access, creative freedom with financial discipline, rapid growth with sustainable margins. Whether ABFRL has mastered this playbook or is still learning it remains the fundamental question for investors and observers alike.

XI. Bull vs Bear Case & Competitive Analysis

The investment case for ABFRL splits sharply between believers and skeptics, each armed with compelling data and narratives. The truth, as always in fashion retail, lies somewhere between the runway and the warehouse.

The Bull Case: Riding India's Consumption Wave

The bulls start with demographics. India adds 10 million people to its workforce annually. The middle class is expected to double from 300 million to 600 million by 2030. Per capita income crossed $2,500 in 2024—the inflection point where discretionary spending accelerates in emerging markets. Every statistic points to a consumption boom that will lift all boats, but especially fashion retailers.

Excluding TCNS, the ethnic business saw a 51 per cent YoY growth in Q4, driven by higher same-store sales, network expansion, and category extensions. Notably, the Sabyasachi brand grew by 56 per cent YoY in Q4. The men's premium ethnic wear brand Tasva doubled its revenue over the last year in FY24. The ethnic wear explosion validates the premiumization thesis. As Indians grow richer, they don't just buy more clothes—they buy better clothes, branded clothes, designer clothes.

The structural shift from unorganized to organized retail provides a multi-decade tailwind. Currently, 65% of apparel is still sold through unorganized retail. If organized retail captures just 2% share annually, it represents ₹5,000+ crore in incremental opportunity. ABFRL, with its multi-brand, multi-channel presence, is positioned to capture disproportionate share.

Post-demerger, both entities have cleaner investment narratives. ABLBL offers stable, profitable growth with strong cash generation—a dividend play in a growth market. ABFRL provides exposure to high-growth segments like ethnic wear and digital brands—a growth play with optionality. Investors can choose their risk-reward profile rather than accepting a blended compromise.

The Aditya Birla backing provides competitive advantages beyond capital. Supplier relationships built over decades translate to better payment terms. Real estate relationships help secure prime retail locations. Corporate governance standards attract international brand partners. The conglomerate DNA might be old-fashioned, but it provides stability in a volatile industry.

The portfolio approach creates a self-reinforcing ecosystem. A customer might start with Peter England in college, graduate to Allen Solly in their first job, upgrade to Van Heusen as they climb corporate ladders, and finally arrive at Louis Philippe in the C-suite. The ethnic portfolio provides similar progression. This lifetime value capture is powerful and defensible.

Post demerger, ABFRL will raise price capital of INR 2,500 crores to strengthen its balance sheet and support the growth needs of its constituent businesses. The ₹2,500 crore capital raise provides dry powder for growth. With a cleaned-up balance sheet, ABFRL can accelerate store expansion, fund marketing, and potentially make additional acquisitions. The promoter participation signals confidence.

The Bear Case: Structural Challenges in a Difficult Industry

The bears point to persistent losses despite a decade of growth. For the financial year which ended on March 31, 2024, ABFRL net loss was at Rs 735.91 crore. It was at Rs 59.47 crore a year ago. Losses widening from ₹59 crore to ₹736 crore isn't a trajectory that inspires confidence. When does the investment phase end and the harvest phase begin?

The company has delivered a poor sales growth of -3.50% over past five years. Negative five-year sales growth in a supposedly growing market raises fundamental questions. Is the market really growing? Is ABFRL losing share? Are the brands resonating with consumers?

Competition is intensifying from every direction. International fast fashion giants like Zara and H&M are expanding aggressively. Reliance Retail, with deeper pockets and better retail infrastructure, is attacking every segment. Direct-to-consumer brands are bypassing traditional retail entirely. E-commerce platforms are becoming brands themselves. Where does ABFRL's competitive advantage lie?

The ethnic wear bet, while promising, is expensive and uncertain. Designer brands are notoriously difficult to scale—creative talent doesn't follow corporate processes. The TCNS acquisition at ₹1,650 crore for 51% implies a valuation that requires perfect execution to justify. Can ABFRL maintain brand authenticity while driving corporate returns?

Digital disruption threatens the core business model. Why would consumers visit 4,664 stores when everything is available online? The massive retail footprint, once an asset, could become a liability—fixed costs in a variable revenue world. The store rationalization already underway suggests management recognizes this risk.

L2L for the quarter stood at 1%. Like-for-like growth of 1% is particularly concerning. It suggests new stores are cannibalizing existing ones, or worse, that the brands aren't resonating. In fashion retail, momentum matters—losing it is easier than regaining it.

The working capital intensity remains problematic. Fashion retail requires constant inventory investment, but fashion is perishable—unsold inventory becomes worthless. The balance between having enough stock to satisfy demand and not so much that markdowns destroy margins is delicate and easily disrupted.

Competitive Dynamics: A Crowded Field

The competitive landscape is brutal and getting worse. Reliance Retail, backed by India's richest man, is building a fashion empire through Azorte, Trends, and Centro. Their financial firepower, retail infrastructure, and ecosystem play (Jio customers becoming fashion customers) pose existential threats.

Tata's Westside has quietly built a profitable, differentiated position in the market. Their private label strategy, focused store footprint, and consistent execution contrast sharply with ABFRL's complexity. Sometimes, doing one thing well beats doing everything adequately.

Online players are rewriting rules. Myntra, despite being a Flipkart subsidiary and ABFRL shareholder, competes directly. Nykaa Fashion is leveraging its beauty customer base. Amazon Fashion brings global scale. These platforms have negative working capital cycles—customers pay before inventory is bought—a structural advantage ABFRL can't match.

The direct-to-consumer revolution bypasses traditional retail entirely. Brands like boAt (audio), Mamaearth (beauty), and Bewakoof (apparel) have shown that billion-dollar brands can be built without stores. Every D2C success story questions ABFRL's capital-intensive, store-heavy model.

International luxury brands are entering India directly rather than through partnerships. Gucci, Louis Vuitton, and Hermès are opening own stores. Uniqlo's entry with direct ownership rather than franchising suggests international brands see enough opportunity to go alone. This threatens ABFRL's international brand portfolio.

The Verdict: Execution Will Determine Destiny

The bull and bear cases are both compelling because they're both true. India's consumption story is real, but so is competitive intensity. The portfolio strategy makes sense, but complexity has costs. The ethnic opportunity is massive, but execution is difficult.

Our unwavering focus on these strategic cornerstones will ensure a strong resurgence as market conditions improve. Management's confidence in eventual resurgence reflects either deep conviction or necessary optimism. The truth will emerge over the next few years.

The investment case ultimately reduces to a bet on execution. Can ABFRL navigate the complexity it has created? Can it maintain brand relevance across segments? Can it achieve profitability while investing for growth? Can it adapt to digital disruption while leveraging physical assets?

For believers, current valuations offer an asymmetric opportunity—limited downside with significant upside if execution improves. For skeptics, the persistent losses and competitive pressures suggest more pain ahead. Both camps watch the same movie but see different endings.

The competitive analysis reveals an industry in flux, where traditional advantages (store networks, brand heritage, supplier relationships) matter less while new capabilities (digital marketing, data analytics, supply chain agility) matter more. ABFRL sits at this intersection—too traditional for new-age investors, too experimental for value investors.

Whether ABFRL emerges as India's fashion champion or another casualty in retail's graveyard depends on decisions being made today in boardrooms and stores, in design studios and warehouses, in spreadsheets and social media. The next chapter is being written in real-time, and its ending remains unscripted.

XII. Epilogue: The Future of Indian Fashion Retail

As the morning sun reflects off the glass façade of ABFRL's Mumbai headquarters in late 2024, Kumar Mangalam Birla stands where his journey began nearly three decades ago. The company he inherited as a commodities conglomerate has metamorphosed into something unrecognizable—and now split into two distinct entities, each charting its own course through Indian fashion's turbulent waters.

ABFRL also plans to raise Rs 2,500 crore in equity capital within 12 months post-demerger. The capital raise ahead signals not an end but a beginning. ABFRL aims to grow three times bigger by focusing on value fashion, ethnic wear, luxury brands, and online-first labels. On the other hand, ABLBL wants to more than double its business and triple its cash profits by building on the strength of its popular and well-established brands.

These aren't modest ambitions. Growing three-fold means ABFRL would reach ₹30,000+ crore in revenue—larger than most listed retailers in India. Tripling cash profits suggests ABLBL targeting ₹1,500+ crore in EBITDA—equivalent to a mid-sized FMCG company. The vision is clear: become India's undisputed fashion leader across every segment, channel, and price point.

The path forward requires navigating fundamental shifts reshaping fashion retail globally and in India specifically. Generation Z, born digital, shops differently—discovery on Instagram, research on YouTube, purchase on apps, returns without guilt. They value sustainability but demand fast fashion prices. They seek authenticity but follow influencers. Serving them requires capabilities ABFRL is still building.

The men's premium ethnic wear brand Tasva doubled its revenue over the last year in FY24. The ethnic wear renaissance represents more than a trend—it's a cultural reclamation. As India asserts itself globally, Indians are rediscovering their sartorial heritage. The wedding wear market alone, estimated at ₹50,000+ crore, offers massive headroom. But scaling ethnic requires different muscles than western wear—managing craftsmen not factories, selling occasions not products.

The sustainability imperative can't be ignored. Fashion is the world's second-largest polluter. Consumers increasingly demand transparency—where was it made, by whom, under what conditions? ABFRL's manufacturing heritage provides advantage here, but also responsibility. Can fast fashion and sustainability coexist, or must the business model fundamentally change?

Technology will reshape everything. AI-powered design can predict trends before they emerge. Virtual try-ons eliminate the fitting room. Social commerce collapses discovery and purchase into one click. Blockchain enables authentication of luxury goods. The retailer that masters technology won't just sell better—they'll sell differently.

A demerger allows each group to set its own plans for growth, update its capital arrangements and focus on what matters to it most. After the demerger, ABFRL plans to secure ₹2,500 crore through equity over the next 12 months to support its businesses and improve its balance sheet. The demerger provides clarity but also pressure. Each entity must prove its thesis. ABLBL must show that focus leads to margins. ABFRL must demonstrate that growth investments yield returns. There's nowhere to hide anymore.

The competitive landscape will only intensify. Amazon is investing billions in India. Reliance's retail ambitions are unlimited. International brands are entering directly. D2C brands are multiplying. Chinese ultra-fast fashion players like Shein lurk at the borders. The battlefield is crowded, and casualties are inevitable.

Yet opportunities abound for those who execute well. India's per capita apparel spending is $50 versus $500 in China and $2,000 in the US—the headroom is massive. Rural India, where 65% of the population lives, is largely unpenetrated. Men's ethnic wear, children's wear, athleisure, plus-size fashion—entire categories await organized retail.

The organizational challenge might be the greatest. Fashion retail requires a unique culture—creative yet commercial, global yet local, fast yet thoughtful. Building this culture within a traditional conglomerate framework has been ABFRL's greatest challenge and will determine its future success.

Kumar Mangalam Birla's vision extends beyond financial metrics. In interviews, he speaks of building Indian brands that compete globally, of creating employment for millions, of formalizing an industry that's largely informal. These aren't just corporate goals—they're nation-building aspirations.

The international opportunity beckons. Indian fashion, like Indian cuisine and cinema, has global potential. Sabyasachi lehengas are worn at American weddings. Ethnic kurtas are becoming mainstream in Middle Eastern markets. Could ABFRL become India's first global fashion powerhouse? The diaspora of 30 million Indians worldwide provides a beachhead.

But challenges loom large. Aditya Birla Fashion and Retail Ltd (ABFRL) on Wednesday reported widening of consolidated net loss at ₹ 233.73 crore for June quarter FY26. The company had posted a loss of ₹ 214.92 crore during April-June quarter a year ago, according to a regulatory filing from ABFRL. Post-demerger losses continue, testing investor patience. The promise of profitability has been made before—when will it materialize?

The macroeconomic environment adds uncertainty. Interest rates remain elevated. Urban consumption has slowed. Rural recovery is tepid. Input costs are rising. The external environment that provided tailwinds for two decades might become headwinds.

Yet betting against Indian consumption has historically been foolish. Every decade, prophets predict slowdown, and every decade, consumption surprises positively. The structural drivers—demographics, urbanization, formalization, aspiration—remain intact.

Focusing on what each entity does best and letting them grow separately with the demerger makes it easier for both companies to profit from changes in the Indian fashion business. Their markets and strategies will shift, so success will come from their adaptability, creativity and efficient strategy execution. The demerger wasn't just financial engineering—it was philosophical recognition that different dreams require different vehicles.

As 2025 unfolds, ABFRL and ABLBL embark on separate but interlinked journeys. They share heritage but not destiny, DNA but not direction. Whether they fulfill their ambitious visions or join the graveyard of retail failures will be determined by millions of small decisions—which designer to hire, which mall to enter, which trend to follow, which technology to adopt.

The story of ABFRL is far from over—if anything, it's just beginning. From a single acquisition in 1999 to a fashion conglomerate managing dozens of brands, thousands of stores, and millions of customers, the transformation has been remarkable. But in fashion, past success guarantees nothing. Every season is a new beginning, every collection a fresh bet, every store opening an act of faith.

Indian fashion retail stands at an inflection point. The next decade will determine winners and losers, leaders and laggards, survivors and casualties. ABFRL, now split but not diminished, has positioned itself at the center of this transformation. Whether it emerges as India's Inditex, LVMH, or something uniquely Indian remains unwritten.

The only certainty is change—in fashion, in retail, in India, in the world. Those who adapt will thrive. Those who don't will become case studies in business schools, cautionary tales of what could have been. For ABFRL and ABLBL, the future is a runway stretching to the horizon, and they've just begun their walk.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube